GlobalFoundries: From AMD Spinoff to Specialty Semiconductor Powerhouse

I. Introduction & Episode Roadmap

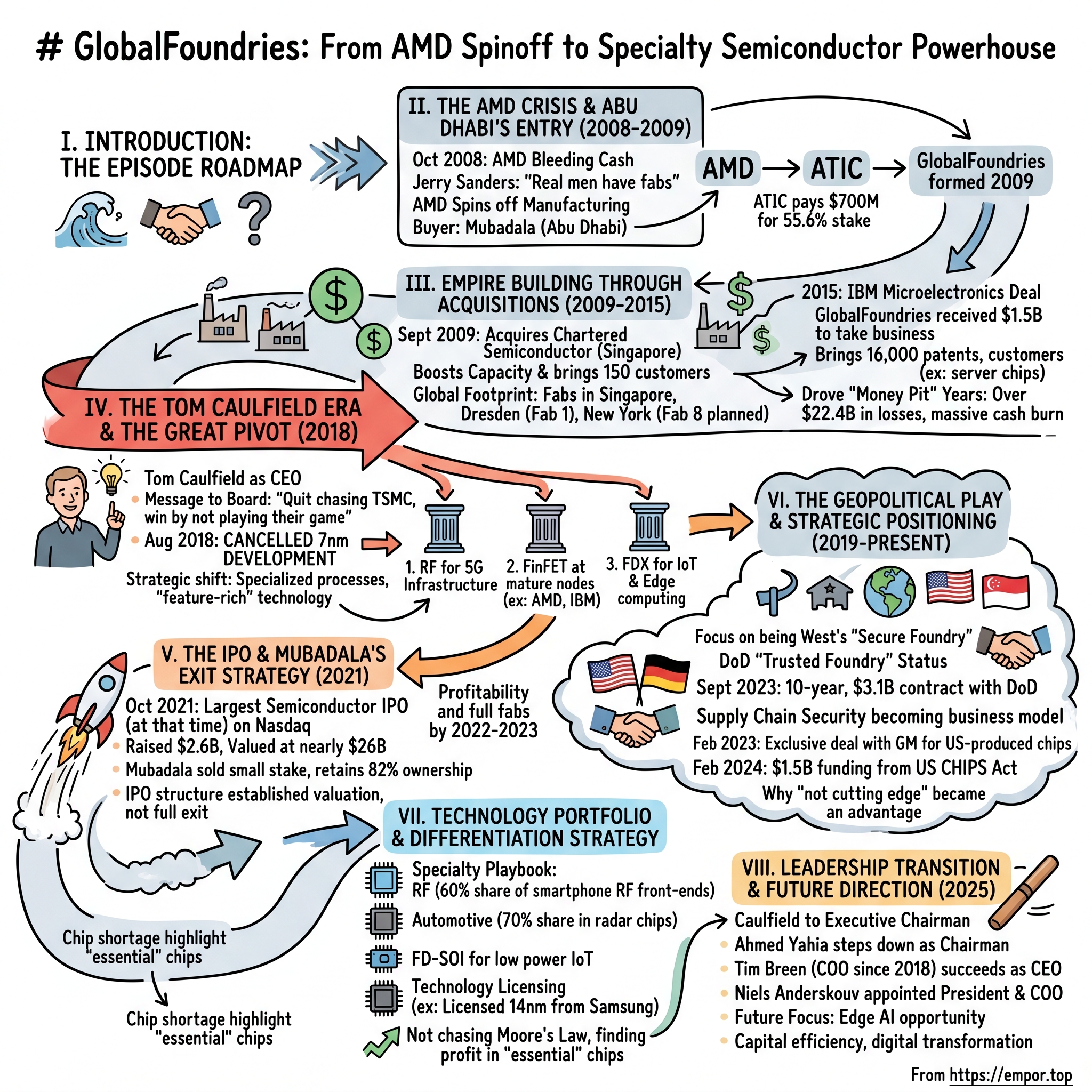

Picture this: October 2008. Lehman Brothers has just collapsed. The global financial system is in freefall. And in Dresden, Germany, AMD's CEO Dirk Meyer is about to announce something that would have been unthinkable just years earlier—the company is abandoning Jerry Sanders' sacred mantra that "real men have fabs." AMD, bleeding cash and unable to keep pace with Intel's manufacturing prowess, is spinning off its entire manufacturing operation. The buyer? An Abu Dhabi sovereign wealth fund that had never run a semiconductor company.

What happened next defied every prediction. That spinoff—GlobalFoundries—would lose $22.4 billion over the next decade, abandon the cutting-edge technology race entirely, and somehow emerge as one of the most strategically important semiconductor companies in the world. Today, it's the third-largest foundry by revenue, trailing only TSMC and Samsung. Its chips power everything from your iPhone's cellular connection to classified defense systems. And in 2021, it pulled off what was then the largest semiconductor IPO in history.

The paradox at the heart of this story: GlobalFoundries succeeded not by competing with TSMC on leading-edge nodes, but by deliberately choosing to stay behind. While TSMC pushes toward 2nm processes that cost $30 billion per fab, GlobalFoundries makes its billions on technology nodes that others consider obsolete. It's a masterclass in strategic positioning—finding profit where others see only commodities.

This is the story of how a Middle Eastern investment fund built a semiconductor empire from the remnants of AMD's manufacturing operations, why quitting the technology race was the smartest move they ever made, and what GlobalFoundries teaches us about finding competitive advantage in the most capital-intensive industry on Earth. We'll explore the three major pivots that saved the company, the geopolitical chess game that turned a liability into an asset, and why being "strategically uninteresting" might be the ultimate moat in semiconductors.

II. The AMD Crisis & Abu Dhabi's Entry (2008–2009)

The conference room at AMD's Sunnyvale headquarters felt like a funeral parlor in late 2007. CFO Bob Rivet had just presented the numbers to the board, and they were catastrophic. Intel's new 45nm process was crushing AMD's 65nm chips in both performance and power efficiency. To catch up, AMD needed to spend $3-4 billion on next-generation fab equipment—money it simply didn't have. The company's debt-to-equity ratio was approaching dangerous levels. Without immediate capital injection, AMD would either go bankrupt or become irrelevant.

CEO Hector Ruiz had been quietly exploring options for months. Private equity showed little interest—semiconductor manufacturing was too capital-intensive, too risky. Asian foundries like TSMC weren't interested in buying AMD's fabs; they had their own expansion plans. Then, through investment bankers at Lehman Brothers (yes, that Lehman Brothers), came an unexpected suitor: Mubadala, the Abu Dhabi sovereign wealth fund. Why Abu Dhabi? The story begins not in Silicon Valley but in the gleaming towers of Abu Dhabi, where Khaldoon Al Mubarak, CEO of Mubadala, was orchestrating one of the most ambitious economic diversification strategies in the Middle East. Mubadala Development Company followed in 2002 to further diversify the economy, and by 2007, they had begun investing in technology companies worldwide. Their initial AMD investment wasn't random—it was calculated. They saw an undervalued asset in AMD's manufacturing capabilities and believed they could build something transformative.

On 7 October 2008 Advanced Micro Devices (AMD) announced it planned to go fabless and spin off their semiconductor manufacturing business into a new company temporarily called The Foundry Company. Mubadala announced their subsidiary Advanced Technology Investment Company (ATIC) agreed to pay $700 million to increase their stake in AMD's semiconductor manufacturing business to 55.6 percent (up from 8.1 percent). Mubadala would invest $314 million for 58 million new shares, increasing their stake in AMD to 19.3 percent, and $1.2 billion of AMD's debt would be transferred to The Foundry Company.

The deal structure was ingenious. AMD got immediate cash infusion and debt relief while retaining guaranteed wafer supply. Mubadala got state-of-the-art fabs in Dresden and planned facilities in New York, plus AMD's technology roadmap through 32nm. But more importantly, they got Doug Grose, AMD's manufacturing chief who knew every detail of those fabs, and access to IBM's technology alliance—the secret sauce that would keep them competitive.

Jerry Sanders' famous mantra that "real men have fabs" had finally been broken. The man who founded AMD on the principle that controlling your own manufacturing was essential to competing with Intel was no longer alive to see his philosophy abandoned (he had retired in 2002), but his successors faced a brutal reality: the capital requirements for leading-edge semiconductor manufacturing had become unsustainable for all but the largest companies.

Waleed Al Mokarrab, Chairman of ATIC, stated: "Despite the current economic climate, this is an industry with tremendous opportunities for longterm growth and innovation. Through its global footprint, world-class technology know-how and access to state-of-the-art research and development, we believe GLOBALFOUNDRIES is well-positioned to challenge for market leadership in this competitive industry".

The ambition was breathtaking. This wasn't just about saving AMD—it was about creating a TSMC competitor from scratch, backed by sovereign wealth that could afford to play the long game. On 4 March 2009 GlobalFoundries was officially announced, marking the birth of what would become the semiconductor industry's most unlikely success story.

III. Empire Building Through Acquisitions (2009–2015)

Six months after GlobalFoundries opened for business, Doug Grose received a call that would transform the company's trajectory. Temasek, Singapore's sovereign wealth fund, wanted out of Chartered Semiconductor. The Singaporean foundry was bleeding cash, its technology was generations behind TSMC, and the 2008 crisis had crushed demand. But Grose saw what others missed: Chartered had something GlobalFoundries desperately needed—200 customers and the operational DNA of a real foundry.

On 7 September 2009 ATIC announced it would acquire Chartered Semiconductor, based in Singapore, for S$2.5 billion (US$1.8 billion) and integrate Chartered Semiconductor into GlobalFoundries. The price tag raised eyebrows—Chartered was losing money and its most advanced process was 65nm, while GlobalFoundries was already producing 45nm chips. But the acquisition wasn't about technology; it was about transformation. The Chartered deal helps GlobalFoundries by boosting its manufacturing capacity and brings in 150 customers. Overnight, GlobalFoundries went from being AMD's captive manufacturer to a real foundry serving Qualcomm, STMicro, and Broadcom. The acquisition gave GF several 200 and 300mm fabs in Singapore, and roughly 200 customers. The acquisition began a transformation of the new foundry, creating a process of dealing with many dozens of customers rather than just one.

Meanwhile, in upstate New York, bulldozers were clearing ground for what would become Fab 8 in Malta—GlobalFoundries' greenfield bet on American manufacturing. The location wasn't accidental. New York State offered $1.4 billion in incentives, and the site was just 20 miles from IBM's semiconductor research center in Albany. This proximity would prove crucial when IBM came calling with an extraordinary proposal in 2014.The IBM Microelectronics deal in 2015 turned the industry on its head: GlobalFoundries received US$1.5 billion from IBM to accept taking over IBM Microelectronics, including a 200 mm fab (now Fab 9) in Essex Junction, Vermont, and a 300 mm fab (now Fab 10) in East Fishkill, New York. Think about that—IBM paid someone else to take its semiconductor business. It was the ultimate admission that the economics of chip manufacturing had become untenable for all but the largest players.

The deal brought GlobalFoundries 16,000 patents, thousands of experienced engineers, and IBM's ASIC business serving enterprise customers. But more importantly, it completed GlobalFoundries' geographic footprint: Fab 1 is in Dresden, Germany. Fabs 2 through 7 are in Singapore. Fabs 8 through 10 are in the northeast United States. This global distribution would later become a strategic advantage when geopolitical tensions made supply chain resilience a boardroom priority.

By 2015, Mubadala had assembled a semiconductor empire through sheer financial force. Mubadala has spent over $22.4B on GlobalFoundries, through paid in capital and a loan which will be converted to paid in capital. Through the years, many missteps, bad investments, and business failures have caused them to lose over $22.4B—a staggering sum even for a sovereign wealth fund. The money pit years had begun, and there seemed no end in sight. GlobalFoundries was burning cash trying to keep pace with TSMC and Samsung on leading-edge nodes while simultaneously trying to serve hundreds of customers with varying needs. Something had to give.

IV. The Tom Caulfield Era & The Great Pivot (2018)

Tom Caulfield walked into the GlobalFoundries boardroom in March 2018 with a reputation as a turnaround artist. The former executive at Samsung's semiconductor division had seen the brutal economics of the leading-edge race up close. His message to Mubadala was blunt: "We can keep losing billions chasing TSMC, or we can win by not playing their game."

The company was at a crossroads. The 7nm process development was consuming $2-3 billion annually, with no guarantee of success. Even if they succeeded technically, they'd need another $15-20 billion to build a 7nm fab at scale. Meanwhile, TSMC was already moving to 5nm. The math simply didn't work—GlobalFoundries would need to match TSMC's $15 billion annual capex just to stay competitive, all while having one-tenth the customer base. Caulfield became President and CEO of GF in 2018. During his tenure he repositioned the technology portfolio to focus on differentiated, essential chips and steered the company to sustainable profitability. The decision came on August 27, 2018, when GlobalFoundries announced it had cancelled their 7LP process due to a strategy shift to focus on specialized processes instead of leading edge performance. The industry was stunned. AMD, their largest customer, immediately began transitioning their next-generation CPUs to TSMC. Wall Street analysts called it capitulation.

But Caulfield saw it differently. "The vast majority of today's fabless customers are looking to get more value out of each technology generation," he explained. While TSMC was pouring billions into 7nm and 5nm nodes that only a handful of companies could afford, GlobalFoundries refocused on what he called "feature-rich" technologies: RF for 5G infrastructure, silicon-on-insulator for automotive, specialized processes for defense applications.

The strategy had three pillars. First: RF– radio frequency, the analog portion combined with a digital modem for 4G and 5G. GlobalFoundries already had strong RF technology from the Chartered acquisition, and 5G deployment was about to explode globally. Second: FinFET– for today's higher performance applications in support of companies like AMD and IBM, but at mature nodes where the economics made sense. Third: FDX– low power platform using fully-depleted silicon-on-insulator technology, perfect for IoT and edge computing applications.

The operational transformation was equally dramatic. Caulfield implemented what he called "intelligent manufacturing"—using AI and machine learning to optimize fab operations. Utilization rates jumped from 84% to fully booked for 2022 and 2023. Cycle times dropped by 30%. Defect rates fell to industry-leading levels. The company that had been hemorrhaging cash for a decade suddenly became profitable.

Why was this brilliant rather than retreat? Because Caulfield understood something the industry had missed: not every chip needs to be on the leading edge. Your car's radar system doesn't need 5nm transistors. The 5G base station connecting your phone doesn't benefit from 3nm processes. The secure chip in your passport runs perfectly on 45nm technology. By focusing on these "essential" chips rather than chasing Moore's Law, GlobalFoundries found profitability where others saw only commodities.

V. The IPO & Mubadala's Exit Strategy (2021)

The roadshow presentations in October 2021 felt surreal to anyone who had followed GlobalFoundries' troubled history. Here was a company that had lost $22.4 billion over twelve years, quit the technology race three years earlier, and was now pitching itself as the future of semiconductors. The timing, however, was perfect. The chip shortage of 2020-2021 had CEOs of Fortune 500 companies calling semiconductor executives directly, begging for allocation. Suddenly, having geographic diversity and focusing on "essential" chips looked prescient rather than second-rate.

On October 28, 2021, the company sold shares in an IPO on the Nasdaq stock exchange at US$47 each, at the higher end of its targeted price range, and raised about US$2.6 billion. It was the largest semiconductor IPO in history at that time, but also the largest semiconductor IPO across all of Nasdaq that year. The market valued GlobalFoundries at nearly $26 billion—more than AMD's market cap when it spun off its manufacturing division thirteen years earlier.

The IPO structure revealed Mubadala's sophisticated approach to exits. Rather than flooding the market, they sold only a small stake while retaining 82% ownership. Mubadala knows they cannot dump the entire company on the open market, so they will only IPO a small portion of the shares outstanding. The filing makes it very clear that Mubadala will continue to be the majority owner of GlobalFoundries. This wasn't just about liquidity—it was about establishing a public market valuation while maintaining control.

The investor presentation told a compelling story: GlobalFoundries served over 200 customers, had locked in long-term agreements worth $17 billion, and operated the only foundry with facilities in the US, Europe, and Asia. The geopolitical angle was particularly powerful. With US-China tensions escalating and semiconductor supply chains under scrutiny, GlobalFoundries positioned itself as the "secure" alternative to Asian foundries. The financial press couldn't decide if they were witnessing genius or madness. GlobalData's analyst Lil Read called it "essentially GlobalFoundries crying to Wall Street for help," noting the company had lost nearly half a billion dollars in the first half of 2021 despite the chip shortage. But institutional investors saw something different. BlackRock, Fidelity, and Silver Lake had already indicated strong interest before the roadshow even began.

The numbers told both stories. Yes, GlobalFoundries was unprofitable—it had lost $1.35 billion in 2020. But revenues were growing again after the strategic pivot, jumping 13% year-over-year in 2021's first half to $3.04 billion. More importantly, the company's gross margins were improving as utilization rates climbed. Caufield's message to investors was clear: "We're only in the third year of our strategic transformation. We're only just getting started."

The geopolitical premium was real. With US-China tensions escalating and the CHIPS Act on the horizon, having a Western foundry with global reach commanded a valuation multiple that would have been unthinkable five years earlier. GlobalFoundries wasn't just selling wafer capacity; it was selling supply chain insurance to companies that had learned the hard way what happens when all your chips come from Taiwan.

For Mubadala, the IPO marked a crucial milestone but not an exit. By maintaining 82% ownership, they signaled confidence in the long-term story while establishing a liquid market for future sales. The sovereign wealth fund that had pumped $22.4 billion into a money-losing venture could finally point to a public market valuation that justified—or at least explained—their patience.

VI. The Geopolitical Play & Strategic Positioning (2019–Present)

The Pentagon official's visit to Fab 8 in Malta, New York, in 2019 wasn't publicized, but it marked a turning point in GlobalFoundries' transformation from commercial foundry to strategic asset. The Department of Defense had a problem: virtually all advanced semiconductors were manufactured in Asia, creating an existential vulnerability for American defense systems. GlobalFoundries had a solution: become the West's secure foundry. GlobalFoundries is a "Trusted Foundry" for the U.S. federal government and has similar designations in Singapore and Germany, including certified international Common Criteria standard (ISO 15408, CC Version 3.1). This designation requires extraordinary security measures—background checks on all employees, restricted access to certain fab areas, and chain-of-custody protocols that ensure chips can't be tampered with or counterfeited.

On September 21, 2023, the U.S. Department of Defense (DoD) awarded GlobalFoundries a 10-year contract for the supply of securely manufactured semiconductors for critical aerospace and defense applications. With an initial award of $17.3 million and an overall 10-year spending ceiling of $3.1 billion, this represented the third consecutive 10-year contract between DoD and GlobalFoundries' Trusted Foundry team.

The strategic importance went beyond defense contracts. In February 2023 GlobalFoundries signed a deal to become the exclusive provider of US-produced semiconductor chips for General Motors amid an ongoing shift to electric vehicles in what was referred to as an "industry-first" deal. This wasn't just about supply—it was about supply chain security. GM had learned during the 2020-2021 chip shortage that relying entirely on Asian suppliers created existential risks. The CHIPS Act windfall crystallized GlobalFoundries' transformation into a national strategic asset. In February 2024, the U.S. Department of Commerce announced a $1.5 billion planned investment in GF as part of the CHIPS and Science Act, making GF the recipient of the first major award from the funding initiative. This wasn't charity—it was recognition that GlobalFoundries had become essential to American economic and military security.

The strategic positioning went beyond just taking government money. GlobalFoundries had spent years cultivating relationships that made it indispensable. When Ford needed a secure chip supply for its electric vehicles, GlobalFoundries was the only viable domestic option. When the Pentagon needed chips that couldn't be compromised by foreign adversaries, GlobalFoundries' Trusted Foundry status made it the default choice.

Why being "not cutting edge" became an advantage is perhaps the most counterintuitive part of the GlobalFoundries story. The chips that actually run the world—the ones in your car's braking system, your phone's cellular modem, the radar systems at airports—don't need 3nm transistors. They need reliability, security, and consistent supply. By focusing on these "boring" chips while everyone else chased Moore's Law, GlobalFoundries found itself in the perfect position when supply chains became a boardroom priority.

The geopolitical tailwinds are only strengthening. With Taiwan under constant threat from China and Intel struggling with its foundry ambitions, GlobalFoundries' geographic diversification and specialty focus look prescient. Supply chain resilience has become a business model, and GlobalFoundries is selling insurance to a world that suddenly realizes how vulnerable it is.

VII. Technology Portfolio & Differentiation Strategy

Walk through GlobalFoundries' Fab 8 in Malta and you won't see the extreme ultraviolet (EUV) lithography machines that define TSMC's most advanced fabs. Those $200 million behemoths are absent by design. Instead, you'll find row after row of equipment optimized for what the industry calls "feature-rich" processes—technologies that add specific capabilities rather than just shrinking transistors.

The specialty foundry playbook that Caulfield implemented has three core pillars, each targeting markets where mature nodes are actually preferred. First, RF dominance for 5G infrastructure. GlobalFoundries inherited strong RF-SOI (radio frequency silicon-on-insulator) technology from the Chartered acquisition, and they've invested heavily in enhancing it. Today, they manufacture over 60% of the world's smartphone RF front-end modules. Every iPhone contains GlobalFoundries chips handling cellular communications.

Second, the automotive semiconductor boom. Cars are becoming computers on wheels, but they need chips that can operate reliably for 15+ years in temperature extremes. GlobalFoundries' 22nm FD-SOI technology offers the perfect balance of performance, power efficiency, and reliability for automotive radar, infotainment, and powertrain applications. The company claims over 70% market share in automotive radar chips.

Third, FD-SOI technology for low-power applications. While the industry focused on FinFET for high-performance computing, GlobalFoundries quietly became the leader in fully-depleted silicon-on-insulator technology. FD-SOI offers unique advantages for battery-powered devices: adaptive body biasing allows dynamic power optimization, and the technology scales well for analog/RF integration.

The technology licensing strategy reveals how GlobalFoundries maximizes value from mature nodes. In 2016 GlobalFoundries licensed the 14 nm 14LPP FinFET process from Samsung Electronics. In 2018 GlobalFoundries developed the 12 nm 12LP node based on Samsung's 14 nm 14LPP process. Rather than developing everything in-house, they license proven technologies and optimize them for specific applications.

Why mature nodes matter more than you think becomes clear when you examine the economics. A 28nm chip might cost 70% less to manufacture than a 7nm equivalent, while providing 90% of the performance for most applications. For a radar chip or IoT sensor that needs to hit a $2 price point, using 7nm would be economic suicide. GlobalFoundries has turned this reality into a business model.

Customer concentration presents both benefits and risks. AMD remains a major customer, though less dominant than in the past. Qualcomm, Broadcom, NXP, and MediaTek have all increased their reliance on GlobalFoundries for specialty chips. The company's top 10 customers represent about 73% of revenue—high concentration, but diversified across industries and geographies. The risk is obvious: losing any major customer would hurt. The benefit: deep partnerships that create switching costs and enable collaborative development.

VIII. Leadership Transition & Future Direction (2025)

The announcement on February 5, 2025, caught nobody by surprise who understood GlobalFoundries' methodical approach to succession planning. Caulfield succeeds Ahmed Yahia who will step down from the Board and his role as Chairman after more than a decade in the position. Breen, who has been with GF since 2018, and is currently Chief Operating Officer (COO), succeeds Caulfield. In addition, Niels Anderskouv, currently GF's Chief Business Officer, has been appointed GF's President and COO.Tim Breen represents continuity with evolution. Having joined GlobalFoundries in 2018 alongside Caulfield, he's been the operational architect behind many of the company's efficiency gains. As COO since 2023, Breen has overseen the company's global operations, including manufacturing, quality, supply chain, and IT teams. His background at Mubadala Investment Company, where he led projects across energy and industrials, brings a different perspective—one focused on capital efficiency and sustainable returns rather than technology for technology's sake.

"As the AI wave moves from cloud to edge, GF is uniquely positioned to accelerate growth," Caulfield noted in the transition announcement. This hints at GlobalFoundries' next strategic focus: AI edge computing opportunity. While TSMC and Nvidia dominate cloud AI training chips, edge AI inference—running AI models on devices rather than in data centers—requires exactly the kind of power-efficient, cost-optimized chips that GlobalFoundries specializes in.

The geographic expansion versus concentration debate continues under new leadership. GlobalFoundries has facilities across three continents, but the question is whether to double down on existing sites or expand further. The CHIPS Act funding enables significant expansion in the US, but Europe and Asia remain critical markets. The company must balance customer demands for geographic diversity with the operational efficiency of concentration.

Intel speculation and industry consolidation rumors have swirled around the transition. Some observers note that Caulfield's move to Executive Chairman leaves him available for other opportunities, potentially including Intel's vacant CEO position. Meanwhile, GlobalFoundries itself could become an acquisition target as the industry consolidates. However, with Mubadala still holding 82% and the company's strategic importance to US national security, any major transaction seems unlikely in the near term.

What changes under Breen? Expect more focus on operational excellence, digital transformation of manufacturing, and careful capital allocation. What stays the same? The commitment to specialty foundry positioning, geographic diversity, and serving as the West's secure chip supplier. The strategy Caulfield put in place has proven successful; Breen's job is to execute it at scale while preparing for the next technology transition.

IX. Playbook: Business & Investing Lessons

The GlobalFoundries story offers a masterclass in strategic pivots, demonstrating when to abandon the technology race—and when not to. The conventional wisdom in semiconductors has always been that you must stay at the leading edge or die. Intel's struggles today stem partly from this belief. But GlobalFoundries proved there's another path: find the sweet spot where mature technology meets essential applications.

The key insight: not every market needs cutting-edge technology. Your car's radar chip doesn't benefit from 3nm transistors—it needs reliability, cost-effectiveness, and specific features like high-voltage tolerance. By focusing on these "boring" applications while others chased Moore's Law, GlobalFoundries found profitability in what others considered commodity markets.

The sovereign wealth fund playbook in tech reveals both the power and limitations of patient capital. Mubadala's $22.4 billion investment in GlobalFoundries looks irrational through a venture capital lens—the returns will never justify the risk. But through a sovereign wealth lens, it makes perfect sense. Abu Dhabi bought technology transfer, human capital development, and economic diversification. The financial returns are secondary to the strategic value.

This model is being replicated globally. Saudi Arabia's Public Investment Fund is following a similar playbook with Lucid Motors and other tech investments. Singapore's Temasek has long pursued this strategy. The lesson: when your investment horizon is measured in decades rather than quarters, you can make bets that others can't afford.

Operational excellence in a commodity business becomes the differentiator when technology isn't. GlobalFoundries' transformation from 84% utilization to fully booked isn't about breakthrough innovation—it's about relentless focus on cycle time reduction, defect elimination, and customer service. In mature technology nodes, the winner isn't who has the best technology but who can deliver it most reliably and cost-effectively.

How to pivot a $20B+ company successfully requires three elements GlobalFoundries got right. First, clarity of vision—Caulfield didn't hedge or equivocate about abandoning 7nm. Second, stakeholder alignment—Mubadala had to accept writing off billions in sunk costs. Third, execution discipline—the entire organization had to reorient from technology leadership to operational excellence. Most large company pivots fail because they lack one of these elements.

The value of being "strategically uninteresting" might be GlobalFoundries' most counterintuitive lesson. While TSMC faces constant geopolitical pressure over Taiwan risk and Intel struggles with its dual role as competitor and foundry, GlobalFoundries flies under the radar. It's important enough to matter but not dominant enough to threaten. This positioning allows it to work with competitors, serve government clients, and operate across geopolitical divides.

Managing government relationships as competitive advantage has become essential in semiconductors. GlobalFoundries' success in securing CHIPS Act funding, DoD contracts, and trusted foundry status across multiple countries shows the importance of regulatory strategy. The company that once seemed like a technological also-ran has become indispensable to multiple governments' strategic plans.

Why specialization beats generalization in semiconductors contradicts the conventional wisdom of diversification. TSMC succeeds by doing one thing—contract manufacturing—exceptionally well. Intel struggles trying to be both a product company and a foundry. GlobalFoundries found its niche in specialty processes and stuck to it. In semiconductors, focus creates the scale and expertise needed to compete.

X. Analysis & Bear vs. Bull Case

The Bull Case: GlobalFoundries sits at the intersection of multiple powerful trends. Geopolitical tailwinds are only strengthening as US-China tensions escalate and Europe seeks semiconductor sovereignty. The company's unique position as the only Western foundry with global reach becomes more valuable each year. The CHIPS Act funding and DoD contracts provide both capital and guaranteed demand.

Specialty dominance in RF, automotive, and IoT markets creates defensive moats. These markets are growing rapidly—5G infrastructure deployment, vehicle electrification, and edge AI computing all require GlobalFoundries' specialized chips. The company's 70% market share in automotive radar and 60% share in smartphone RF front-ends would take competitors years to replicate.

Fully utilized fabs with rising prices drive margin expansion. As one of only four scaled foundries outside China capable of serving these markets, GlobalFoundries has pricing power. The company's gross margins have expanded from 7% in 2018 to over 25% today, with room for further improvement as utilization remains at peak levels.

Government support provides a funding advantage competitors can't match. Between CHIPS Act grants, investment tax credits, and state incentives, GlobalFoundries effectively receives a 30-40% subsidy on US expansion. This allows it to invest aggressively while maintaining returns that satisfy Mubadala.

The Bear Case: Customer concentration risk remains significant despite diversification efforts. The top 10 customers still represent 73% of revenue. Losing a major customer like AMD or Qualcomm would materially impact results. As these customers develop their own supply chain strategies, they may seek to diversify away from any single foundry.

Mature node commoditization threatens long-term margins. While GlobalFoundries currently enjoys pricing power due to shortages, supply and demand will eventually balance. Chinese foundries like SMIC are aggressively expanding capacity in mature nodes. Once supply normalizes, pricing pressure could compress margins back toward historical levels.

The Mubadala overhang creates uncertainty about long-term ownership. With 82% ownership and $22.4 billion invested, Mubadala will eventually need to monetize its stake. Any significant sale would pressure the stock price. Moreover, potential acquirers might be deterred by Mubadala's control, limiting strategic options.

Competitive positioning versus TSMC, UMC, and SMIC shows GlobalFoundries as a strong number three but distant from number one. TSMC generates 10x GlobalFoundries' revenue with superior margins. UMC competes directly in mature nodes with lower costs. SMIC, despite US sanctions, continues expanding capacity with Chinese government support. GlobalFoundries must constantly defend market share against larger and smaller competitors.

Financial metrics tell a story of transformation but questions remain. The path to profitability has been achieved—GlobalFoundries reported its first full-year profit in 2022. Margins are expanding, with gross margins reaching 27% in recent quarters. Capital efficiency has improved dramatically, with capex/revenue ratios falling from 40% to 20%. But the question remains: is this sustainable profitability or shortage-driven anomaly?

The $22.4 billion loss question—was it worth it?—depends on your perspective. From a pure financial return standpoint, Mubadala will never recoup its investment. Even at today's $30 billion market cap, they're underwater on a cash basis. But from a strategic standpoint, Abu Dhabi now owns critical technology infrastructure, has developed human capital in advanced manufacturing, and positioned itself as essential to global supply chains. For a sovereign wealth fund thinking in 50-year horizons, that might be worth $22 billion.

XI. Epilogue & Reflections

The GlobalFoundries story rewrites the conventional narrative of success in semiconductors. Here is a company that failed at its original mission—becoming a TSMC competitor—lost $22.4 billion over a decade, and quit the technology race that defines the industry. By any traditional measure, it should be a cautionary tale of hubris and waste.

Instead, GlobalFoundries emerged as the unexpected winner of the semiconductor wars. Not by leading in technology, but by recognizing that leadership isn't always about being first. While competitors chase 2nm processes that cost $30 billion per fab, GlobalFoundries profitably manufactures chips on 28nm processes in fully depreciated fabs. It's the tortoise in a race where everyone else is trying to be the hare.

What GlobalFoundries teaches us about strategic pivots extends beyond semiconductors. The company's transformation shows that admitting failure and changing course can be more valuable than stubborn persistence. Caulfield's decision to abandon 7nm wasn't giving up—it was recognizing reality and finding opportunity in that recognition. Too many companies fail because they can't admit when their strategy isn't working.

The future of specialty foundries looks increasingly bright. As chips proliferate into every device and system, the demand for specialized rather than general-purpose semiconductors grows. The winner in automotive radar doesn't need 3nm transistors; they need RF expertise and automotive qualification. GlobalFoundries bet that specialization would beat generalization, and that bet is paying off.

Perhaps the most important lesson is about patience, capital, and timing. Mubadala's willingness to absorb massive losses for over a decade enabled GlobalFoundries to survive long enough to find its strategy. The 2020-2021 chip shortage created the market conditions for profitability. The geopolitical tensions of 2022-2025 made supply chain resilience valuable. Sometimes success isn't about being smart—it's about surviving long enough for the world to realize you were right.

The GlobalFoundries story isn't finished. The company faces real challenges: customer concentration, competition from China, the eventual normalization of supply and demand. But it has also proven remarkably adaptable, transforming from AMD's castoff manufacturing division into an essential player in global technology infrastructure. In an industry obsessed with moving forward, GlobalFoundries found success by strategically standing still.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube