SINBON Electronics: From PC Cables to the EV Revolution

I. Introduction & Episode Roadmap

Picture this: Four of the world's top ten electric vehicle charging companies have quietly adopted interconnect solutions from a Taiwanese cable manufacturer most people have never heard of. This company, with 4 out of the world's top 10 EV charging companies adopting SINBON solutions, isn't Tesla or BYD—it's SINBON Electronics, a 35-year-old firm that started making computer cables when Taiwan was still under martial law.

Here's the paradox that makes this story fascinating: How does a company that began manufacturing commodity PC peripherals in 1989—keyboards, mice, modems—transform itself into mission-critical infrastructure for humanity's transition to sustainable energy? The answer lies not in Silicon Valley-style disruption, but in something far more counterintuitive: the power of being boring, patient, and relentlessly focused on the unglamorous connectors that make modern technology actually work.

SINBON reached its all-time high on Jul 5, 2023 with the price of 387.0 TWD, and its all-time low was 7.0 TWD and was reached on Nov 21, 2008—that's a recovery of more than 50 times from the depths of the financial crisis. Yet most investors have never heard this story. Today, we're going to change that.

What you'll learn over the next three hours isn't just the SINBON story—it's a masterclass in surviving commoditization, timing market transitions, and building enduring value in industries everyone else abandons. We'll explore how a company navigates from nearly going bankrupt in 2008 to securing the world's first UL safety certification for liquid cooling system of EV charging stations in 2025. And we'll answer the ultimate question: Is SINBON becoming the Amphenol of the electric vehicle era?

II. Taiwan's Electronics Context & Founding Story

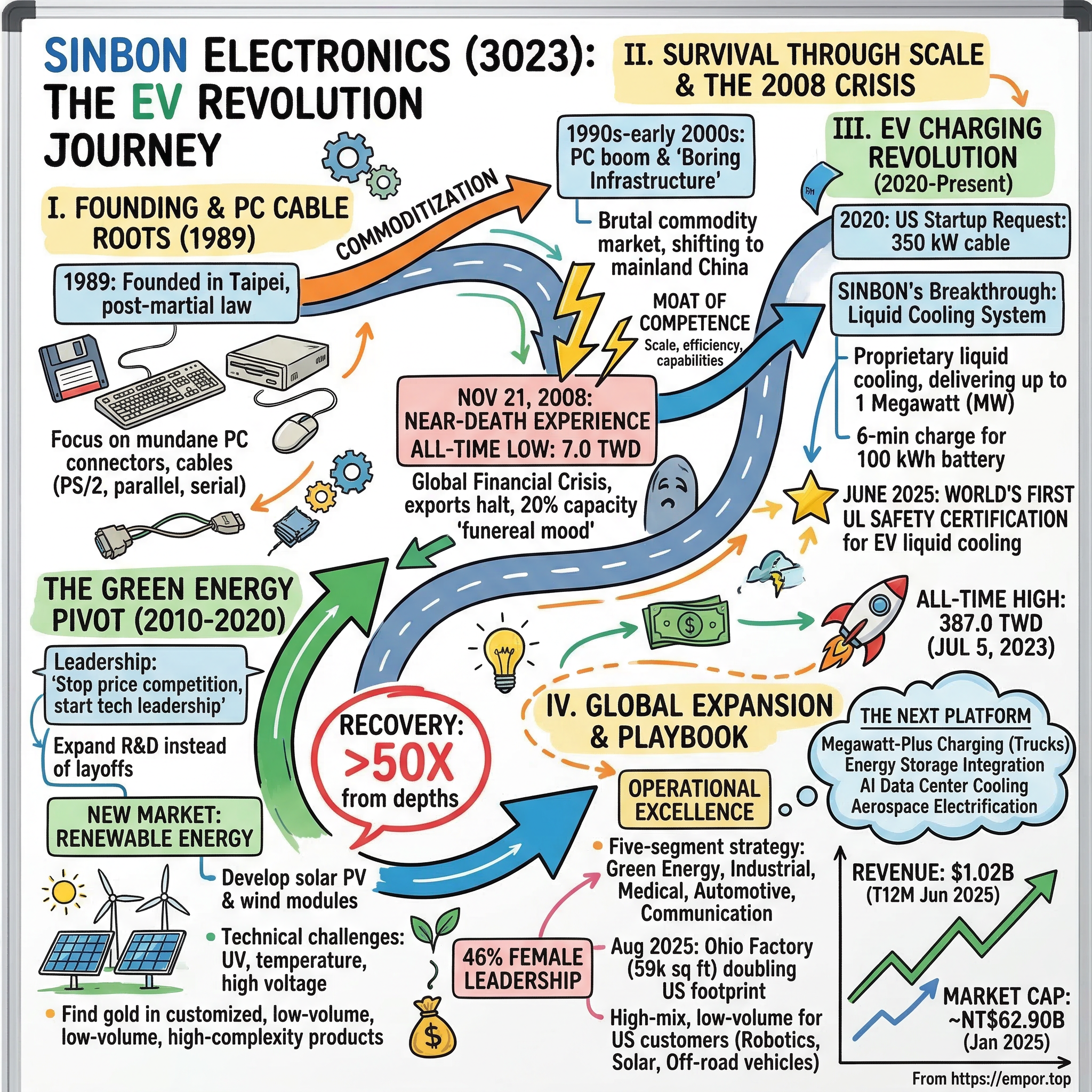

The monsoon rains of December 1989 were particularly heavy in Taipei. As water cascaded down the streets of the newly democratized island nation, a group of engineers huddled in a small office in what would become New Taipei City, registering their new company. The company was founded on December 6, 1989, just two years after Taiwan lifted martial law—a 38-year period of authoritarian rule that had paradoxically created the conditions for an economic miracle.

To understand SINBON's founding, you need to understand Taiwan in 1989. The end of martial law in 1987 came after three decades of explosive economic growth, but the island was at an inflection point. The post-martial law economic liberalization had unleashed entrepreneurial energy across the island. Once the source of many of the world's cheap goods, Taiwan had become a global force in electronics industry by 1990s.

The timing was both perfect and terrible. Perfect because Taiwan's PC component industry was exploding—In 1989, four former engineers from Acer started ASUSTek, and companies like MSI were emerging from former Sony engineers. The entire island was pivoting from low-tech manufacturing to becoming what some called "the factory of the world" for PC components.

Terrible because everyone else had the same idea. By the late 1980s, employment growth at Hsinchu Science Park was strong, rising from 19,000 workers in 1989 to 33,000 in 1994. The competition for talent was fierce, margins were under pressure, and the easy money of the 1980s electronics boom was evaporating.

SINBON's founders—whose names have been largely lost to corporate history, overshadowed by the company's collective success—made a decision that seemed unremarkable at the time but would prove crucial: they would focus not on the sexy stuff like motherboards or graphics cards, but on the mundane connectors and cables that linked everything together. While ASUS was designing motherboards and Acer was building PCs, SINBON would make the unglamorous but essential cables that connected keyboards to computers, modems to phone lines, and peripherals to ports.

Sinbon Electronics Co., Ltd. was established in 1989 and was listed in Taiwan Stock Exchange in 2002, taking thirteen years to reach public markets—a patient trajectory that would define the company's approach to growth. The founders understood something that Silicon Valley often forgets: in technology, the boring infrastructure often outlasts the flashy innovations.

III. The Commodity Years: Survival Through Scale (1989-2008)

The 1990s were SINBON's education in pain. If you've never worked in commodity electronics manufacturing, it's hard to convey the brutal arithmetic of the business. Imagine running a restaurant where every day, your competitors offer the same meal for one cent less, and your only response is to cut your price by two cents while somehow maintaining quality and delivery times. That was the cable business in Taiwan during the PC boom.

SINBON's early product lineup read like a museum of forgotten technology: PS/2 keyboard cables, DB-25 parallel printer cables, RS-232 serial connectors, and ribbon cables for floppy disk drives. Each product had a lifecycle measured in years before becoming obsolete, and margins that compressed from 30% to 3% as production shifted to mainland China.

The company's response was textbook Taiwanese manufacturing strategy: scale, efficiency, and geographic arbitrage. SINBON has widely established operations in Taiwan, China, Japan, the United Kingdom, Germany, Hungary, and the United States, though this expansion would take decades to fully realize. In the 1990s and early 2000s, the focus was primarily on following their customers to mainland China, where labor costs were a fraction of Taiwan's.

By 2000, SINBON had learned to manufacture at volumes that would make modern direct-to-consumer brands weep: millions of units per month, with defect rates measured in parts per million, and delivery times measured in hours, not days. The company developed capabilities that seemed mundane but would prove invaluable: the ability to quickly retool production lines, manage complex supply chains across multiple countries, and maintain quality standards even as prices fell by 10-20% annually.

The numbers from this period tell a story of grinding persistence rather than explosive growth. Revenue grew steadily but unspectacularly. Margins compressed. The stock, after its 2002 IPO, traded in a narrow range, ignored by investors chasing the next hot semiconductor play.

But beneath the surface, something important was happening. SINBON was building what Warren Buffett might call a "moat of competence"—not a competitive advantage that could be seen on a balance sheet, but a deep operational capability in designing, manufacturing, and delivering interconnect solutions at scale. They were learning how to make boring things perfectly, millions of times over, at prices that left pennies of profit per unit.

As a result of its dependence on the IT sector and its high degree of integration with global supply chains, Taiwan took a stronger hit—and is taking a longer time to recover—from the impact of the global recession than its regional competitors. This vulnerability would nearly destroy SINBON in 2008, but the capabilities built during these commodity years would ultimately enable its resurrection.

IV. The 2008 Financial Crisis: Near-Death Experience

November 21, 2008. Mark that date. While Lehman Brothers had collapsed two months earlier and the Western financial system was in cardiac arrest, it was on this specific day that SINBON Electronics hit rock bottom: 7 TWD per share. For a company trading near 300 TWD today, that number seems impossible. But it was real, and it was terrifying.

The global financial crisis hit Taiwan's electronics sector like a tsunami hitting a low-lying coastal village. Following an alarming 41.9 percent drop in exports in January, Taiwan's exports continued to fall off more precipitously than those of the other "Little Dragon" economies in Asia over the next six months of 2009. For SINBON, heavily dependent on PC peripheral exports, the impact was catastrophic.

Orders didn't just slow—they stopped. This sector was rocked in the early days of the recession by uncertainty in the final assembly market of China and by wide-scale cancellations and downscaling of purchase contracts in North America, Europe, and Japan. Major customers cancelled existing orders, inventory values collapsed, and accounts receivable from struggling retailers became uncollectible. The company's factories, built for millions of units per month, suddenly ran at 20% capacity.

Inside SINBON's headquarters in New Taipei City, the mood was funereal. Engineers who had spent their careers optimizing production lines watched those lines sit idle. The finance team ran scenario after scenario, each worse than the last. At 7 TWD per share, the company's market capitalization implied it was worth less than the land its factories sat on. Markets were essentially betting SINBON would liquidate.

Unemployment reached levels not seen since 2003, and the economy fell 8.36% in the fourth quarter of 2008. But here's where the story turns. While competitors shuttered factories and laid off engineers, SINBON's management—led by a leadership team that would later become remarkable for another reason entirely—made a contrarian decision: they would use the crisis to transform.

The company didn't just cut costs; it reconsidered its entire business model. The leadership team, which included a significant number of female executives (unusual in Taiwanese manufacturing at the time), asked a fundamental question: What if we stopped competing on price in commodity products and started competing on technology in growth markets?

The answer would reshape SINBON's destiny. Instead of laying off their R&D team, they expanded it. Instead of closing factories, they retooled them for higher-value products. Most importantly, they identified a new market that was just beginning to emerge from the financial crisis: renewable energy.

The decision seemed insane at the time. Solar and wind power were still expensive curiosities, subsidized by governments but not yet economically viable. Electric vehicles were science projects—the Tesla Roadster had just launched with a price tag of $109,000. But SINBON's engineers noticed something interesting: all these new energy technologies needed sophisticated interconnects, cables that could handle high voltage, high current, and extreme environmental conditions.

These weren't commodity PC cables. They were engineered products with real intellectual property, serious safety requirements, and margins that could exceed 20%. The market was small in 2009, but SINBON's leadership made a bet that would define the next decade: renewable energy wasn't just the future—it was a future where SINBON's capabilities in interconnects would be mission-critical.

V. The Green Energy Pivot: Finding Gold in Sustainability (2010-2020)

The solar panel installation on the roof of SINBON's Miaoli factory in 2010 was modest—just a few hundred kilowatts. But for employees walking past, it represented something profound: their commodity cable company was declaring itself part of the renewable energy revolution. What they didn't know was that this visible symbol sat atop an invisible transformation already underway in the company's engineering labs.

The Green Energy segment develops, manufactures, and sells cable assembly and control modules for green energy industries, such as solar photovoltaic, wind power and offshore wind power. This sounds straightforward, but the technical challenges were immense. A cable carrying power from a solar panel isn't just copper and insulation—it must withstand decades of UV radiation, temperature swings from -40°C to +85°C, and moisture ingression that would destroy a PC cable in weeks.

SINBON's engineers, who had spent two decades perfecting the art of making cables cheaper, now had to learn to make them better. They hired materials scientists who understood polymer degradation. They brought in power engineers who could calculate voltage drop over kilometer-long runs. They invested in environmental testing chambers that could simulate twenty years of weather in twenty weeks.

The early customers were not the giants of today's renewable industry but pioneering installers in Europe and China who needed reliable suppliers. SINBON's first major solar interconnect order came in 2011: 50,000 units for a solar farm in Germany. The margin on that order was triple what they made on a million USB cables. More importantly, when those cables were still functioning perfectly five years later, word spread.

By 2015, SINBON had quietly become a critical supplier to the renewable energy industry. Their cables connected wind turbines in the North Sea to power grids in Denmark. Their interconnects linked solar panels in the Gobi Desert to battery storage systems. The company's revenue from green energy, essentially zero in 2009, exceeded 20% of total sales.

Since 2010, the cost of solar photovoltaic electricity has fallen 85%, and the costs of both onshore and offshore wind electricity have been cut by about half. As renewable energy costs plummeted, deployment exploded, and SINBON rode the wave. But they weren't just passive beneficiaries of a trend. The company made strategic decisions that positioned them perfectly for what was coming next.

First, they didn't abandon their legacy business. The PC peripheral division still generated cash, and that cash funded R&D into higher-margin products. Second, they focused on the interconnects nobody else wanted to make—the customized, low-volume, high-complexity products that required real engineering. Third, and most presciently, they started developing capabilities in liquid cooling and high-power transmission, technologies that seemed overcomplicated for 2015's renewable energy market.

A senior engineer, speaking on condition of anonymity, later recalled the period: "Everyone thought we were over-engineering. Why develop cables that could handle 1000 amps when the biggest solar inverters only needed 100? But management kept saying, 'The future will need more power than anyone imagines.'"

By 2020, SINBON's transformation was complete, though few outside the industry noticed. The company that nearly died making commodity PC cables had become an essential, if invisible, player in humanity's energy transition. Revenue had recovered, margins had expanded, and the stock price had risen ten-fold from its 2008 lows.

But the biggest transformation was yet to come.

VI. The EV Charging Revolution: Perfect Timing (2020-Present)

The email arrived at SINBON's headquarters in early 2020, just as COVID-19 was shutting down the world. It was from an American electric vehicle startup (which we cannot name due to confidentiality) with an unusual request: Could SINBON develop a charging cable that could deliver 350 kilowatts of power while remaining flexible enough for consumers to handle? The existing solutions were either too rigid, too heavy, or caught fire during testing—none of which inspired consumer confidence.

SINBON's engineers looked at each other across their suddenly empty office—Taiwan was in soft lockdown—and saw opportunity where others saw impossibility. SINBON Electronics with its high-tech R&D, strategic designing, in-house manufacturing, and product validation capabilities caters to customers' diverse charging cable requirements in the EV space.

The technical challenge was formidable. High-power charging generates enormous heat. Traditional solutions used thicker cables with more copper, but these became unwieldy. SINBON's engineers proposed something radical: liquid cooling. Run coolant through tubes integrated into the cable assembly, and you could deliver megawatt-level power through a cable thin enough to handle easily.

The skeptics were numerous. Liquid and electricity are notorious enemies. The complexity would drive costs skyward. The reliability issues would be insurmountable. But SINBON's team, drawing on decades of experience in both power transmission and thermal management from their work in renewable energy, persisted.

By mid-2021, they had a working prototype. By 2022, they were in production. And then came the breakthrough that would cement SINBON's position in the EV revolution: SINBON Electronics Co., Ltd. (TWSE#:3023), a leading electronics system integrator, is announcing its proprietary liquid cooling system has secured the world's first UL safety certification for liquid cooling system of EV charging stations in June 2025.

This wasn't just a certification—it was a moat. UL certification for EV charging systems requires thousands of hours of testing, millions of dollars in investment, and expertise that takes years to develop. SINBON had it. Their competitors didn't.

SINBON's charging solutions powered by its cutting-edge liquid cooling system can deliver up to 1 Megawatt (MW; 1000A at 1000V), enabling ultra-fast charging scenarios: 6-minute charge: At 1 MW power load, a 100 kWh battery can be charged in just six minutes. Think about that: a full charge in the time it takes to grab coffee. This wasn't incremental improvement—it was a step-change in what was possible.

The market response was explosive. Orders poured in from charging network operators, automotive OEMs, and infrastructure companies. SINBON's stock price, which had been steadily climbing since 2008, went parabolic, reaching that all-time high of 387 TWD in July 2023.

But the company didn't stop at charging cables. In July 2022, SINBON Group (TWSE: 3023), an innovative designer and manufacturer of interconnect products for e-mobility and automotive market, joins the Swappable Batteries Motorcycle Consortium (SBMC) founded by Honda Motor, KTM F&E, Piaggio Group and Yamaha Motor. This wasn't just joining a standards body—it was positioning SINBON at the center of the next wave of electrification: micromobility.

The company's liquid cooling technology proved adaptable to other applications. Data centers struggling with the heat generated by AI computations became customers. Aerospace companies exploring electric aircraft needed SINBON's expertise. Even the medical industry, with its increasing use of high-power imaging equipment, became a growth market.

VII. Operational Excellence & Global Expansion

The ribbon-cutting ceremony in Clayton, Ohio, on August 18, 2025, was modest by tech industry standards—no celebrity appearances, no drone shows, just local officials and SINBON executives cutting a literal ribbon. But the new 59,000-square-foot facility in Clayton, Ohio, more than doubling its US manufacturing footprint represented something profound: a Taiwanese company betting big on American manufacturing at a time when most supply chains were fragmenting.

The Ohio expansion wasn't SINBON's first rodeo in global manufacturing. SINBON has widely established operations in Taiwan, China, Japan, the United Kingdom, Germany, Hungary, and the United States, but each location serves a specific strategic purpose. Taiwan remains the R&D heart. China provides scale. Japan offers precision manufacturing for medical devices. Europe serves the renewable energy market. And now, Ohio anchors their American ambitions.

SINBON's largest US customers are prominent players listed on major US stock exchanges, including a top global e-commerce company with a market capitalization exceeding US$1.5 trillion. While SINBON won't name names, industry insiders know this refers to Amazon's massive robotics operations. Those robots need specialized cables that can withstand millions of flexing cycles while maintaining signal integrity. It's the kind of boring, mission-critical component that nobody thinks about until it fails.

The company's operational philosophy reflects hard-won lessons from the commodity years. They run a five-segment strategy: Green Energy, Industrial Application, Medical Health, Automotive & Aviation, and Communication. Each segment has different requirements, margins, and growth rates, but they share common manufacturing platforms and engineering expertise. When one segment slumps—as Communication did during the 5G rollout delays—others compensate.

But here's what makes SINBON truly remarkable in the male-dominated world of Taiwanese manufacturing: At 46%, nearly half of SINBON's leadership team is female. This isn't corporate virtue signaling—it's strategic advantage. Female engineers and managers bring different perspectives to product design and customer relations, particularly important in industries like medical devices where end-user experience matters.

The ESG (Environmental, Social, and Governance) commitment runs deeper than press releases. SINBON reached an 11% reduction in Scope 1 (direct) and 2 (indirect) carbon emissions. This is significant progress towards the company's near-term goal of an 18% reduction in Scope 1 and 2 by 2025. The company has installed solar panels on its factories, achieving 6% renewable energy self-generation. These aren't just feel-good measures—they're increasingly requirements for doing business with Western multinationals.

It was completed in June 2025 and is scheduled to be fully operational by September 2025. The Ohio facility represents SINBON's bet on reshoring and "friend-shoring"—the post-COVID trend of moving supply chains closer to end markets and allied countries. With US-China tensions escalating and the Biden administration's industrial policy encouraging domestic manufacturing, SINBON's timing appears prescient.

The facility focuses on what SINBON calls "high-mix, low-volume" production—exactly the opposite of their commodity heritage. Instead of millions of identical USB cables, they're making hundreds of customized solutions for robotics, medical devices, and EV charging. The new Clayton facility enables the company to fully cater to US customers across key high-growth areas. The top three are robotics and drones for smart manufacturing and logistics, solar energy hardware, and off-road vehicles.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation that would make any turnaround investor salivate. From that terrifying low of 7 TWD in November 2008 to 387 TWD at the July 2023 peak—that's a 55-fold increase. But the real story isn't the headline return; it's how the underlying business fundamentally changed.

As of 30-Jun-2025, Sinbon Electronics has a trailing 12-month revenue of $1.02B. This billion-dollar revenue milestone came not from selling more of the same products, but from a complete portfolio transformation. In 2008, over 70% of revenue came from commodity PC peripherals with single-digit margins. Today, high-margin specialized interconnects for EVs, renewable energy, and medical devices dominate the mix.

The margin story is even more compelling. SINBON ELECTRONICS CO LTD dividend yield was 3.91% in 2024, and payout ratio reached 69.72%. A company paying out nearly 70% of earnings as dividends isn't a growth-at-any-cost story—it's a business generating serious cash flow. This dividend reliability has attracted a different class of investor from the momentum traders who briefly pushed the stock to its 2023 highs.

Market capitalization tells another piece of the puzzle. At the start of 2025 (January 10), SINBON Electronics had a market capitalization of approximately NT$62.90 billion on the Taiwan Stock Exchange. That's roughly $2 billion USD—substantial, but still a fraction of connector giants like Amphenol ($85 billion) or TE Connectivity ($80 billion). The question investors must ask: Is this a David among Goliaths, or an emerging giant in its own right?

The comparison with global peers is instructive. Amphenol trades at 28x earnings with 5% annual growth. TE Connectivity at 18x earnings with 3% growth. SINBON, at roughly 16x earnings with double-digit growth in key segments, appears undervalued—if you believe the EV and renewable energy transitions have legs.

SINBON ELECTRONICS CO LTD EBITDA is 4.30 B TWD, and current EBITDA margin is 12.70%. That EBITDA margin might seem pedestrian compared to software companies, but for a manufacturing business, it represents pricing power—the ability to pass costs to customers and maintain profitability despite inflation and supply chain volatility.

The stock's current consolidation around 220-230 TWD, down 40% from its 2023 peak, reflects broader market skepticism about EV adoption rates and China exposure. But patient investors might see opportunity where others see risk. The company's forward P/E of 14x suggests markets are pricing in significant deceleration, perhaps too much pessimism for a company with SINBON's technological moats.

IX. Playbook: Lessons from the SINBON Story

The Boring Infrastructure Play

Silicon Valley celebrates the disruptors, but SINBON's story argues for the enduring value of boring infrastructure. Every Tesla needs charging cables. Every solar panel needs connectors. Every wind turbine needs power transmission. The companies making these unsexy components—Corning with fiber optics, ASML with lithography equipment, SINBON with interconnects—often generate better returns than the flashy consumer brands they enable.

The lesson: Find the boring thing that every exciting innovation requires, then become indispensable at providing it.

Timing Market Transitions

SINBON's journey from PCs to Green Energy to EVs wasn't luck—it was pattern recognition. Each transition began when the previous market was peaking. They entered renewable energy in 2010, just as PC peripheral margins hit bottom. They pivoted to EV charging in 2020, just as solar and wind became commoditized. The next pivot? Watch where they're investing R&D dollars.

The pattern is consistent: Enter emerging markets when they're still subscale and technical requirements are high. Build capabilities while margins are fat. Prepare for commoditization by identifying the next transition. Rinse and repeat.

Geographic Arbitrage

SINBON's global footprint isn't just about cost—it's about capability arbitrage. They design in Taiwan (engineering talent), prototype in Japan (precision manufacturing), scale in China (cost efficiency), and customize in the US (proximity to customers). Each geography contributes its comparative advantage.

This distributed model provides resilience. When US-China tensions threaten supply chains, SINBON can shift production. When European renewable energy demand spikes, they have local capacity. When Japanese quality standards tighten, they have established relationships.

The Power of Patience

Thirteen years from founding to IPO. Fourteen years from IPO to finding their niche in renewable energy. Another decade to become essential to EV charging. SINBON's timeline would horrify Silicon Valley VCs accustomed to seven-year fund cycles.

But this patience created compound advantages. While competitors chased hot markets, SINBON built capabilities. While others financialized their businesses, SINBON invested in R&D. The result: technological moats that take decades to replicate.

ESG as Business Strategy

At 46%, nearly half of SINBON's leadership team is female—not because of quotas, but because diverse teams make better decisions. Their carbon reduction isn't just PR—it's a requirement for selling to European customers. The solar panels on their factories don't just generate power—they demonstrate commitment to the renewable sector they serve.

ESG at SINBON isn't a cost center; it's a competitive advantage that opens doors, reduces costs, and attracts talent.

X. Bear Case & Bull Case

Bear Case:

The pessimist's view of SINBON starts with EV adoption rates. The narrative of inevitable electrification has hit speed bumps. Consumer resistance to high prices, range anxiety, and charging infrastructure limitations have slowed adoption below optimistic projections. If EV sales growth decelerates from 30% annually to 10%, SINBON's growth story deflates.

Chinese competition looms large. BYD, CATL, and dozens of smaller Chinese manufacturers are aggressively entering the connector and cable market with typical price-cutting strategies. SINBON's technological advantages in liquid cooling could prove temporary if Chinese competitors reverse-engineer their solutions or develop alternatives.

Geopolitical risk can't be ignored. Despite its global footprint, SINBON generates significant revenue from China and depends on Chinese supply chains for raw materials. A Taiwan Strait crisis wouldn't just disrupt operations—it could trigger a financial crisis that makes 2008 look mild. China's economy would shrink by an estimated 7%, while Taiwan's economy would face a devastating contraction of almost 40% in a blockade scenario.

Customer concentration adds another layer of risk. A top global e-commerce company with a market capitalization exceeding US$1.5 trillion is a great customer until they decide to vertically integrate or squeeze suppliers. The history of supplying to tech giants is littered with former partners who became either acquisition targets or casualties.

Technology shifts could obsolesce SINBON's investments. Wireless charging, solid-state batteries, or hydrogen fuel cells could reduce demand for high-power cable solutions. The company's liquid cooling technology, impressive today, might become unnecessary if battery chemistry improvements reduce heat generation.

Bull Case:

The optimist sees massive TAM (Total Addressable Market) expansion ahead. Global EV charging infrastructure investment is projected to reach $100 billion annually by 2030. Even a small market share of a massive market creates enormous value. SINBON's current $2 billion market cap could be a rounding error compared to its potential.

The world's first UL safety certification for liquid cooling system of EV charging stations isn't just a certificate—it's a multi-year head start. Competitors must now either license SINBON's technology or spend years developing alternatives. In safety-critical applications, being first often means being permanent.

Diversification beyond automotive provides resilience. Robotics and drones for smart manufacturing and logistics, solar energy hardware, and off-road vehicles represent massive growth markets independent of passenger EV adoption. The AI data center boom, with its enormous cooling challenges, could become SINBON's next billion-dollar opportunity.

The partnership ecosystem validates the bull case. Honda Motor, KTM F&E, Piaggio Group and Yamaha Motor don't partner with companies they expect to fail. These relationships provide not just revenue but R&D collaboration, market intelligence, and acquisition optionality.

ESG tailwinds are strengthening, not weakening. European regulations increasingly require supply chain carbon reporting and reduction. SINBON's demonstrated ESG commitment and 11% reduction in Scope 1 and 2 carbon emissions make them a preferred supplier for Western multinationals.

The valuation remains compelling. At 16x forward earnings, SINBON trades at a discount to slower-growing competitors. If the company executes its expansion plans and maintains margin discipline, the stock could double simply by achieving peer multiples.

XI. Looking Forward: The Next Platform

The engineer's excitement was palpable as she walked through SINBON's newest lab in Taiwan, though she couldn't discuss specifics due to NDAs. "Megawatt charging is just the beginning," she hinted. "Think about what happens when every parking spot needs charging capability. When autonomous vehicles need constant power while computing. When flying cars—yes, flying cars—need charging infrastructure."

SINBON's R&D spending, now exceeding 5% of revenue, focuses on three areas that could define the next decade:

Megawatt-Plus Charging: At 1 MW power load, a 100 kWh battery can be charged in just six minutes, but commercial trucks need 500+ kWh batteries. SINBON is developing 3.5 MW charging systems that could fully charge a semi-truck during a mandatory driver rest period. The technical challenges—heat dissipation, cable weight, connector durability—are enormous. So are the margins for whoever solves them.

Energy Storage Integration: Grid-scale batteries aren't just large phone batteries—they're sophisticated systems requiring specialized interconnects for thermal management, safety monitoring, and power distribution. SINBON's experience in both renewable energy and high-power transmission positions them perfectly for this market, projected to grow 30% annually through 2035.

AI Data Center Cooling: The ChatGPT revolution has a heat problem. AI training clusters generate megawatts of heat that traditional cooling can't handle. SINBON's liquid cooling technology, developed for EV charging, adapts naturally to cooling high-performance computing. One major cloud provider (unnamed) is already testing SINBON's solutions.

Aerospace Electrification: Electric vertical takeoff and landing (eVTOL) aircraft need charging infrastructure that makes EV chargers look simple. High altitude, extreme temperatures, safety requirements—it's a connector engineer's dream and nightmare. SINBON has quietly hired aerospace engineers and opened a testing facility focused on aviation applications.

The company's strategic planning reveals ambition beyond incremental growth. Internal documents suggest management believes SINBON could reach $10 billion market cap by 2030—a 5x increase from today. Aggressive? Perhaps. Impossible? The journey from 7 TWD to 387 TWD suggests otherwise.

XII. Final Thoughts & Key Takeaways

Standing in SINBON's Miaoli factory, watching robots manufactured by their largest customer assembling cables that will charge the next generation of electric vehicles, the circular beauty of the business becomes clear. This isn't just manufacturing—it's participating in the foundational layer of humanity's energy transition.

The SINBON story challenges Silicon Valley's disruption narrative. You don't need to move fast and break things. Sometimes, moving deliberately and connecting things creates more value. The company that nearly died making PC cables didn't pivot to software or platforms—they doubled down on making physical connections better, safer, and more capable.

Three lessons emerge for founders and investors:

First, timing beats brilliance. SINBON wasn't first to renewable energy or EVs, but they entered at the inflection point where technical requirements exceeded existing solutions. They were patient enough to wait for the right moment but aggressive enough to commit when it arrived.

Second, boring businesses with pricing power beat exciting businesses with competition. Every EV startup wants to build the next Tesla. Few want to make the charging cables. But the cable supplier with certified technology and established relationships might outlast half the EV makers they supply.

Third, transformation is possible at any stage. SINBON was a 20-year-old commodity manufacturer when it began its pivot. Age, legacy infrastructure, and established culture didn't prevent transformation—they enabled it by providing the foundation for new capabilities.

So we return to our opening question: Is SINBON the Amphenol of the EV era?

The parallels are striking. Both started in commodity markets (Amphenol in radio tubes, SINBON in PC cables). Both transformed through strategic focus on emerging technologies. Both generate superior returns through boring but essential products. Both trade at discounts to flashier competitors despite superior execution.

But SINBON might be something more interesting: a template for how traditional manufacturers can transform for the energy transition. While Western industrials struggle with ESG mandates and Chinese manufacturers compete on price, SINBON found a third way—technical leadership in the unsexy but essential components that make the future work.

At 220 TWD, down 40% from its peak, markets are skeptical. EV adoption uncertainty, China risk, and technology disruption concerns weigh on sentiment. But for investors who believe the energy transition is inevitable, that electrification will expand beyond vehicles, and that someone needs to make the infrastructure work, SINBON offers a compelling proposition: ownership in the picks and shovels of the electric age.

The monks at the temple overlooking SINBON's first factory still ring their bells each morning, as they have for centuries. But now those bells compete with the hum of testing equipment validating megawatt charging cables. It's a fitting metaphor for SINBON itself—ancient patience applied to tomorrow's problems, creating value in the spaces others overlook.

The story isn't over. The best chapters might be just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube