GE Vernova: Powering the Energy Transition

I. Introduction & Episode Roadmap

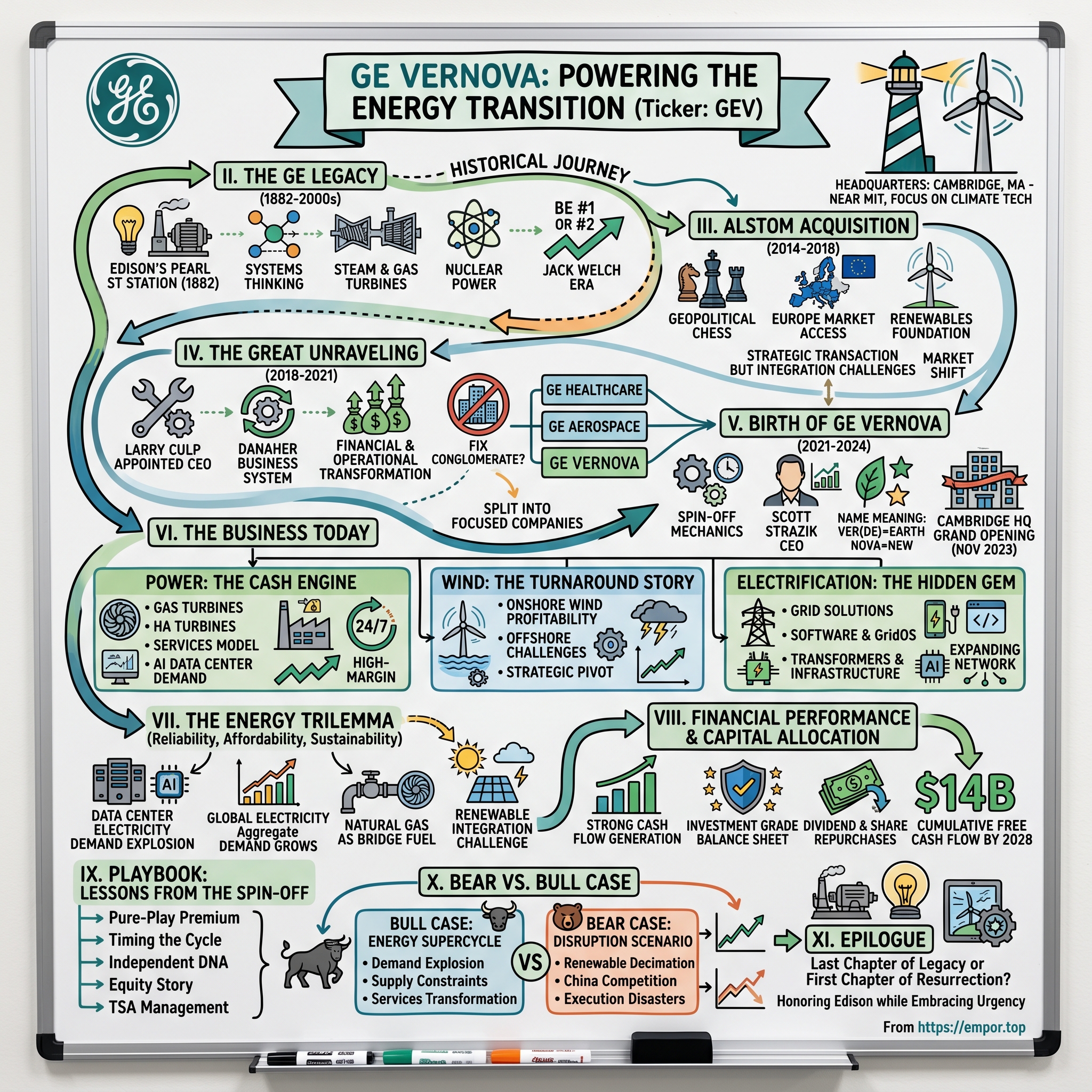

The Cambridge, Massachusetts headquarters tells you everything you need to know about GE Vernova's ambitions. Not Schenectady, where Thomas Edison built his industrial empire. Not Atlanta, where GE Power dominated for decades. But Cambridge—MIT's backyard, where climate tech startups cluster like atoms in a reactor core, where the future of energy gets debated in conference rooms overlooking the Charles River.

On April 2, 2024, at 9:30 AM Eastern, something unprecedented happened at the New York Stock Exchange. For the first time in its history, two companies rang the opening bell together—GE Vernova and GE Aerospace, the twin offspring of what was once America's most storied conglomerate. The symbolism wasn't subtle: the house that Edison built had finally, definitively, dismantled itself.

Here's the staggering fact that stops you cold: GE Vernova's equipment helps generate approximately 30% of the world's electricity. Think about that. Nearly one in three light bulbs illuminated globally traces its power back to turbines, generators, or wind farms bearing GE Vernova's DNA. This isn't just another industrial spin-off story—it's about who controls the infrastructure powering humanity's next century.

The question that haunts this narrative: How did a 130-year-old power division, buried deep within a struggling conglomerate, transform itself into a $47 billion independent energy transition play? More intriguingly, why did Wall Street—typically skeptical of industrial turnarounds—embrace this particular resurrection?

We're about to traverse 142 years of industrial history, from Edison's Pearl Street Station to today's AI data centers consuming electricity like digital blast furnaces. We'll decode the Alstom acquisition that nearly broke GE, witness Larry Culp's surgical dismantling of an American icon, and examine how Scott Strazik built an energy powerhouse from the fragments.

But this isn't just corporate archaeology. It's about understanding the energy trilemma that defines our era: reliability (keeping lights on), affordability (not bankrupting consumers), and sustainability (not cooking the planet). GE Vernova sits at the intersection of all three, which makes it either perfectly positioned or impossibly conflicted, depending on your perspective.

Three themes will echo throughout: First, how industrial legacy becomes either ballast or fuel for transformation. Second, why the energy transition represents the largest capital reallocation in human history. Third, the paradox of corporate spin-offs—how division sometimes multiplies value.

II. The GE Legacy: From Edison to Energy Empire

September 4, 1882. Three o'clock in the afternoon. Thomas Edison, standing in J.P. Morgan's Wall Street office, throws a switch. Six miles away, on Pearl Street in lower Manhattan, America's first commercial power plant roars to life. Within minutes, 85 customers receive electricity—400 lamps illuminate, marking humanity's transition from flame to filament.

Edison didn't just invent the light bulb; he architected an entire ecosystem. The genius wasn't the bulb—it was understanding you needed generators, distribution systems, meters, and business models to make electricity commercially viable. This systems thinking would become GE's genetic code, passed down through 130 years of industrial evolution.

The Edison General Electric Company, formed in 1889, merged with Thomson-Houston in 1892 to create General Electric. Charles Coffin, GE's first CEO, understood something Edison didn't: electricity wasn't about invention anymore—it was about scale, standardization, and relentless operational excellence. Under Coffin's 30-year reign, GE became the template for the modern industrial corporation.

By 1900, GE was manufacturing everything from light bulbs to locomotives, but power generation remained its beating heart. The company pioneered steam turbines in 1903, fundamentally changing how electricity was produced. Where reciprocating engines managed hundreds of horsepower, turbines delivered thousands, then tens of thousands. GE's turbine installed at Chicago's Fisk Street Station in 1903 generated 5,000 kilowatts—revolutionary for its time.

The real transformation came during World War I. GE's turbines powered battleships, its electrical systems lit factories running three shifts to feed the war machine. Revenue exploded from $35 million in 1914 to $318 million by 1920. But more importantly, GE learned how to operate at unprecedented scale, managing complex supply chains and engineering challenges that would've crushed smaller companies.

The interwar period saw GE perfect what would become its signature move: technological leapfrogging. In 1928, they introduced the first practical jet engine design (though it wouldn't see commercial use for decades). In power generation, they pushed turbine efficiency from 20% to over 35%, each percentage point representing millions in fuel savings for utilities.

World War II transformed GE from industrial giant to national strategic asset. The company manufactured everything from radar systems to jet engines, but crucially, it also designed the electrical systems for the Manhattan Project's uranium enrichment facilities. This classified work gave GE unparalleled expertise in managing massive electrical loads—knowledge that would prove invaluable in the nuclear age.

The 1950s marked GE's golden era in power generation. They built the turbines for Hoover Dam, engineered the electrical systems for the St. Lawrence Seaway, and—most significantly—entered the nuclear power business. GE's boiling water reactor design would eventually power over 90 nuclear plants globally. By 1960, if you flipped a switch in America, there was a 40% chance GE equipment was involved somewhere in the power chain.

But success bred complexity. By the 1970s, GE Power Systems competed internally with GE Industrial, GE Aerospace, and dozens of other divisions for capital and attention. The conglomerate structure that once enabled rapid expansion now created bureaucratic friction. Power generation, despite being GE's historical core, became just another division in an increasingly unwieldy empire.

The 1980s under Jack Welch brought ruthless focus—"Be #1 or #2 in your market or get out." For Power Systems, this meant doubling down on gas turbines just as natural gas deregulation made them economically viable. GE's Frame 7F turbine, introduced in 1987, became the workhorse of the combined-cycle revolution, achieving efficiencies approaching 60% when paired with steam recovery systems.

By 2000, GE Power Systems generated $15 billion in revenue with operating margins exceeding 20%. The division had evolved from Edison's direct current dynamos to sophisticated turbines converting natural gas into electricity with stunning efficiency. But the seeds of future challenges were already planted: renewable energy was emerging, coal was beginning its decline, and climate change was transitioning from scientific concern to political reality.

The story of GE Power through the 20th century is really three stories intertwined: technological evolution (from steam to gas to nuclear), organizational evolution (from startup to division of a massive conglomerate), and market evolution (from regulated monopolies to competitive markets). Each transformation required not just new technology but new business models, new capabilities, and—most difficultly—new mindsets.

What's remarkable is how consistent the core challenge remained across 130 years: converting fuel into electricity reliably, efficiently, and profitably. Edison's Pearl Street station burned coal to make steam to turn dynamos. Today's combined-cycle plants burn natural gas to spin turbines that generate electricity while capturing waste heat for additional power generation. The physics are more sophisticated, the scale is massive, but the fundamental problem—and GE's fundamental expertise—remains unchanged.

III. The Alstom Acquisition & Global Energy Consolidation (2014-2018)

April 24, 2014. The news breaks on Bloomberg like a thunderclap: General Electric is in talks to acquire Alstom's power assets for $13 billion. In Paris, French Economy Minister Arnaud Montebourg is reportedly furious—the government learned about the potential sale of a national industrial champion from financial media, not from Alstom's CEO Patrick Kron, who was attending GE's annual meeting in Chicago that very day.

The timing couldn't have been more fraught. GE's offer of $16.9 billion (€12.35 billion) for Alstom's thermal, renewables, and grid businesses represented a strategic transaction that would combine complementary technology, operations, and geography. But this wasn't just another corporate acquisition—it was a geopolitical chess match played across three continents.

Jeff Immelt saw the Alstom acquisition as the capstone of his industrial transformation strategy. After the 2008 financial crisis nearly destroyed GE Capital, Immelt had been methodically pivoting GE back to its industrial roots. GE expected these actions to generate more than $1.2 billion in annual cost synergies by year five, with the deal immediately accretive to shareholders.

The strategic logic seemed compelling. Alstom's energy businesses employed 65,000 people and registered €14.8 billion in sales in fiscal year 2012/13. The company brought critical European market access, 50Hz turbine technology (complementing GE's 60Hz dominance), and—crucially—a strong position in renewable energy that GE desperately needed as the world pivoted toward decarbonization.

But the French government had other ideas. Within days of the news breaking, France deployed its economic sovereignty playbook. On May 14, 2014, France issued a decree nicknamed "décret Alstom," extending the power of the state to veto takeovers of "strategic interests" in areas of energy supply, water, transport, telecoms and public health. The message was clear: if GE wanted Alstom, it would need to negotiate with Paris, not just the board.

Enter Siemens. On June 16, Siemens and Mitsubishi Heavy Industries submitted a competing offer for Siemens to acquire Alstom's gas turbine activities for €3.9 billion while MHI would form joint ventures with Alstom. The German-Japanese consortium played directly to French anxieties about American dominance, offering to keep more jobs and technology in Europe.

GE's response was masterful corporate diplomacy. GE said France would be the center of its European power business with headquarters and centers of excellence for steam turbine, hydro, offshore wind and grid businesses, with the Belfort site remaining the center of excellence for 50Hz gas turbines, and anticipating net growth in jobs in France.

Under the updated offer, GE and Alstom would establish joint ventures: a 50-50 stake in Grid combining Alstom Grid and GE Digital Energy, 50-50 in Alstom's offshore wind and hydro businesses, and a Global Nuclear and French Steam alliance including the Arabelle steam turbine equipment for nuclear plants.

The deal that finally closed on November 2, 2015, looked nothing like the original proposal. After adjusting for joint ventures, changes in deal structure, remedies, and currency effects, the purchase price was €9.7 billion (approximately $10.6 billion)—substantially less than the headline figure that had shocked markets eighteen months earlier.

GE Renewable Energy was created in 2015, combining the wind power assets GE purchased from Alstom with those previously owned by GE, with headquarters moving from Schenectady, New York to Paris, France, as part of conditions for the Alstom purchase. This Franco-American hybrid would become the foundation of what would eventually spin out as GE Vernova.

The integration challenges were immediate and brutal. Cultural clashes between American corporate efficiency and French industrial pride created friction at every level. GE's standardized processes collided with Alstom's engineering-first culture. The French unions, promised job security, watched nervously as GE began its integration playbook.

The European Commission was concerned that the transaction would eliminate one of GE's key competitors in the heavy-duty gas turbine market, which "would have led to less innovation and higher prices in a market for a technology vital to meeting climate change goals". To address these concerns, GE agreed to divest central parts of Alstom's heavy-duty gas turbine business to Italy's Ansaldo.

What GE couldn't have foreseen was the perfect storm brewing in global power markets. Natural gas prices were collapsing, renewable energy costs were plummeting faster than anyone predicted, and the global turbine market was entering a period of severe overcapacity. In Alstom's 2014 Annual Report, management had noted that "excess capacity in developed markets" was a concern for its power business—a warning GE perhaps should have heeded more carefully.

By 2018, the Alstom acquisition was widely viewed as a disaster. The promised synergies materialized, but the market had fundamentally shifted. Power generation equipment orders globally fell off a cliff as utilities delayed capital investments, waiting for renewable costs to fall further. The integration costs ballooned, and the cultural integration never fully materialized.

Yet paradoxically, the Alstom acquisition gave GE something invaluable: the technological breadth and geographic reach that would make GE Vernova viable as an independent company. The renewable energy assets, the European manufacturing footprint, the grid technology—all would prove essential when the energy transition accelerated post-2020. The acquisition that nearly broke GE Power would, ironically, provide the foundation for GE Vernova's future independence.

IV. The Great Unraveling: GE's Transformation Journey (2018-2021)

October 1, 2018. The board meeting that would change GE's destiny convenes in Boston, not Fairfield—the Connecticut headquarters already abandoned, a symbol of the old GE dying. H. Lawrence Culp, Jr. has been named Chairman and Chief Executive Officer of the Company by a unanimous vote of the GE Board of Directors, effective immediately. He is the first outsider to run GE in the company's 126-year history.

Culp's appointment was both shocking and inevitable. Shocking because GE had always promoted from within—a cardinal rule dating back to Edison. Inevitable because the company was bleeding out: stock price down 60% in twelve months, dividend slashed for only the second time since the Great Depression, and Power division hemorrhaging cash. John Flannery, CEO for just fourteen months, had become the sacrificial lamb for decades of accumulated problems.

"GE remains a fundamentally strong company with great businesses and tremendous talent. It is a privilege to be asked to lead this iconic company. We will be working very hard in the coming weeks to drive superior execution, and we will move with urgency." Culp's first words as CEO revealed his approach: acknowledge strength, honor legacy, but move fast.

The man taking the helm wasn't your typical Fortune 500 CEO. Culp was born and raised in the Washington, D.C. area, the son of a small welding company owner. He understood manufacturing, understood small business hustle, understood what it meant to meet payroll. Prior to joining GE, Larry spent 25 years at Danaher Corporation, including serving as President and CEO from 2001 to 2014. During his tenure, the company increased both its revenues and market capitalization fivefold.

At Danaher, Culp had perfected something called the Danaher Business System—a relentless focus on continuous improvement borrowed from Toyota but implemented with American intensity. It wasn't just about cutting costs; it was about fundamentally reimagining how industrial companies operate. Every process questioned, every assumption challenged, every inefficiency eliminated.

GE in October 2018 was a case study in corporate complexity run amok. The company operated 283 separate ERP systems. Financial reporting took weeks to consolidate. Different divisions used different metrics for the same measurements. The Power division alone had 30 different P&L structures across its global operations. This wasn't a company; it was a confederation of fiefdoms sharing a logo.

Culp's diagnosis was swift and brutal. In his first 100 days, he visited 25 GE sites, held town halls with thousands of employees, and conducted what he called "reality sessions"—no PowerPoints, no prepared remarks, just brutal honesty about what was broken. The feedback was consistent: too much bureaucracy, too many layers, too much politics, not enough customer focus.

As Chairman and CEO of GE, Larry led the industrial technology company's multi-year financial and operational transformation. During his tenure, GE strengthened its balance sheet, reduced debt by more than $100 billion, grew profit by 20%, more than doubled adjusted earnings-per-share, and more than quadrupled its market capitalization.

But the real insight came in early 2019 during a visit to GE Aviation's Cincinnati facility. Culp watched as engineers from Aviation, Healthcare, and Power—all working on similar technologies—had never met each other. Three divisions, three separate R&D budgets, three different approaches to solving essentially the same problem. The conglomerate structure wasn't creating synergies; it was destroying them.

The strategic options were limited but clear: fix the conglomerate model (impossible given the structural challenges), sell everything piecemeal (would destroy value), or split into focused companies (radical but potentially transformative). By mid-2019, Culp and his team were secretly modeling the third option.

The Power division remained the immediate crisis. Orders had collapsed 30% year-over-year. The Alstom integration was still incomplete four years after closing. Warranty claims from rushed turbine deployments were mounting. But buried in the carnage, Culp saw opportunity: the world would need more electricity, not less. The energy transition would require gas as a bridge fuel. The installed base of 7,000 turbines wasn't a liability—it was an annuity stream waiting to be optimized.

2020 brought COVID-19, which paradoxically accelerated Culp's transformation agenda. With Aviation revenues collapsing 75% in Q2 2020, sacred cows became hamburger. Layers of management disappeared. Decision-making accelerated. The crisis gave cover for changes that would have taken years of negotiation in normal times.

By early 2021, the path forward was crystallizing. GE Healthcare had demonstrated it could operate independently during the pandemic. Aviation was clearly a crown jewel once travel returned. And Power, Renewable Energy, and Digital—despite their challenges—shared enough DNA to potentially thrive as a combined energy business.

On November 9, 2021, General Electric announced that it would split into three publicly traded companies. The following year, they announced the names would be GE HealthCare, GE Aerospace, and GE Vernova.

The announcement sent shockwaves through corporate America. GE, the original American conglomerate, the company that had defined industrial capitalism for over a century, was essentially admitting the model no longer worked. But Culp framed it differently: this wasn't a retreat but a liberation. Three focused companies could move faster, invest more strategically, and serve customers better than one massive conglomerate.

The name reveals were carefully orchestrated corporate theater. GE HealthCare would keep the most traditional branding, leveraging the trust healthcare providers had in GE medical equipment. GE Aerospace would embody the precision and innovation of flight. And then there was the energy business—the most challenged, the most complex, the one that needed the most dramatic reimagination.

"Ver" / "verde" signal Earth's verdant and lush ecosystems. "Nova," from the Latin "novus," nods to a new, innovative era of lower carbon energy that GE Vernova will help deliver. The name itself was a statement of intent: this wouldn't be your grandfather's power company.

The execution roadmap was staggering in complexity. Three separate management teams to build. Three capital structures to optimize. Three investor stories to craft. Thousands of contracts to separate. Tens of thousands of employees to reassign. IT systems to untangle. All while running businesses generating over $75 billion in annual revenue.

But the hardest part wasn't operational—it was psychological. GE employees had to reimagine their identity. For over a century, working for GE meant something specific: stability, prestige, being part of something bigger than any individual business. Now they were being asked to embrace uncertainty, to become entrepreneurs within their divisions, to prepare for independence.

V. The Birth of GE Vernova: Spin-off Mechanics & Launch (2021-2024)

The name reveal moment—July 18, 2022—was pure corporate theater. GE spent six months arriving at the new names and brand identities for the companies spinning off. The energy portfolio would be branded as GE Vernova, a combination of "ver," derived from "verde" and "verdant," to signal the greens and blues of Earth, and "nova," from the Latin "novus," or "new," reflecting a new and innovative era of lower-carbon energy. The evergreen brand color replaced GE's traditional blue, signaling transformation while the iconic GE Monogram remained front and center.

But behind the branding exercise lay eighteen months of grueling operational surgery. Scott Strazik, who had been named CEO of GE's Gas Power business in 2018 and expanded his role to leading the GE Power businesses in 2021, was now tasked with building an independent company from divisions that had never truly worked together.

Scott Strazik is the chief executive officer (CEO) and president of GE Vernova (NYSE: GEV), a purpose-built global company focused on electrifying and decarbonizing the world and leading the future of energy. With approximately 75,000 employees in over 100 countries, the company's technology base helps generate one quarter of the world's electricity.

Strazik brought a unique background to the role. Scott has more than 20 years of leadership, finance, and operations experience. He was named CEO of GE's Gas Power business in 2018 and expanded his role to leading the GE Power businesses in 2021. Unlike many energy executives who came up through engineering, Strazik had a finance and operations background—he understood both the numbers and the nuts and bolts of running industrial operations.

The headquarters decision became a defining moment. GE announced that GE Vernova, the company's portfolio of energy businesses, intends to base its global headquarters at 58 Charles Street in Cambridge, Massachusetts, as part of its plan to become an independent company in early 2024. Scott Strazik, CEO of GE Vernova, said, "We are thrilled to call Cambridge home as we build plans for the future of GE Vernova. As we plan for our next chapter, Cambridge offers a dynamic environment, steeped in the education, talent, and innovation that will be core components of our work alongside customers to decarbonize power generation and lead the energy transition."

The choice of Cambridge over Schenectady—where GE's power business had operated since Edison's time—sent shockwaves through the organization. Schenectady was the Electric City, GE's ancestral home. But Strazik understood that GE Vernova needed to signal a break from the past. Cambridge offers a growing community focused on the energy transition spanning our own customers, academic and scientific research, policy thought leaders, and investment capital.

The operational challenges of separation were staggering. Three ERP systems needed untangling. Thousands of supplier contracts required renegotiation. Intellectual property had to be allocated. Shared services—from HR to IT to legal—needed replication. All while running businesses that couldn't afford a single day of disruption.

The cultural transformation proved even harder. Power division employees, many with decades at GE, struggled with identity. Were they still "GE people"? Renewable energy teams from the Alstom acquisition wondered if they'd finally get equal treatment. Digital teams questioned whether software would get lost in a hardware-dominated culture.

Strazik's solution was radical transparency. Town halls became confessionals where he acknowledged every challenge: "We have an offshore wind business losing money on every turbine. We have a services business with 40% gross margins hidden inside equipment divisions showing 5% margins. We have brilliant engineers who've never met customers."

The financial engineering of the spin-off was equally complex. GE Vernova needed an investment-grade balance sheet from day one. This meant allocating debt, pension obligations, and environmental liabilities across three companies. Every dollar of debt assigned to Vernova was a dollar that couldn't fund growth investments.

In preparation for the spin-off, GE Vernova, LLC was founded on February 28, 2023. The LLC was incorporated on April 2, 2024, as GE Vernova Inc. and was listed on the New York Stock Exchange under ticker symbol GEV.

The distribution mechanics were elegantly simple: Holders of GE common stock would be entitled to receive one share of GE Vernova common stock for every four shares of GE common stock held on March 19, 2024, the record date for the distribution. No cash changed hands, no taxes triggered—a tax-free spin to shareholders that preserved value while creating optionality.

But the real innovation was in how Strazik repositioned the narrative. This wasn't a troubled division being jettisoned—it was a focused energy company being liberated. The messaging was relentless: GE Vernova equipment helps generate approximately 30% of the world's electricity. Seven thousand gas turbines. Fifty-five thousand wind turbines. The backbone of global power generation.

The November 2, 2023 headquarters grand opening in Cambridge became a coming-out party. GE Vernova christened its new headquarters in Cambridge, Massachusetts, with a grand opening attended by community leaders from the Greater Boston area, including special guests Massachusetts Governor Maura Healey and U.S. Ambassador David Thorne. Governor Healey took the stage to share her thoughts on how Massachusetts and GE Vernova share the same mission and goal — to be leaders in the clean energy transition.

The relationship with Greentown Labs, North America's largest climatetech incubator, symbolized the strategic pivot. Vernova's new location will also facilitate its relationship with one of its new neighbors, Greentown Labs, the largest climatetech incubator in North America. This week Greentown announced that GE Vernova will become its newest "Terawatt Partner," representing the highest level of engagement with the incubator.

As April 2, 2024 approached—Independence Day, as employees called it—the organization had been fundamentally rewired. Three separate business segments with clear P&Ls. A simplified operating model with decision-making pushed down to business units. A services organization finally recognized as the crown jewel it was, not hidden inside equipment divisions.

The morning of April 2, 2024, was choreographed down to the minute. At 9:30 AM Eastern, in that unprecedented moment at the NYSE, GE Vernova and GE Aerospace rang the opening bell together. The stock opened at $102, implying a market capitalization of roughly $27 billion—less than optimists hoped but more than pessimists feared.

"Our new space is truly a reflection of who we are: driven, modern, flexible, and collaborative," Strazik said. The Cambridge headquarters, with its exposed brick and open floor plans, looked nothing like GE's traditional corporate offices. This was intentional. Everything about GE Vernova—from its name to its headquarters to its culture—was designed to signal that this wasn't your grandfather's power company.

VI. The Business Today: Power, Wind, and Electrification

The numbers tell a story of transformation in real-time. In the third quarter of 2024, GE Vernova delivered solid performance with double-digit organic orders growth, continued revenue growth, and substantial cash flow. Revenue was trending towards the higher end of $34-$35 billion, adjusted EBITDA margin of 5%-7%, and free cash flow of $1.3-$1.7 billion, now trending towards the higher end of the free cash flow range.

But to understand GE Vernova's true position, you need to dissect its three core segments, each representing a different bet on the energy future.

Power: The Cash Engine

The Power segment is GE Vernova's beating heart—and its most misunderstood asset. With the largest fleet on a megawatt basis and ~7,000 installed gas turbines, including some of the largest, most efficient gas turbines, this isn't just legacy equipment; it's critical infrastructure that can't be easily replaced.

Third Quarter 2024 Power Performance Orders of $5.2 billion increased +34% organically, led by Gas Power equipment and services, with 9 HA and 15 aeroderivative units, and services growth +29% organically. Revenues of $4.2 billion increased +8%, +13% organically, led by Gas Power, with increased services, largely from higher outage volume, and equipment growth on higher HA deliveries.

The HA turbine—GE's flagship heavy-duty gas turbine—represents the pinnacle of thermal efficiency. Operating at temperatures exceeding 1,500°C, these machines convert natural gas to electricity at efficiencies approaching 64% in combined-cycle configurations. Each percentage point of efficiency improvement saves operators millions in fuel costs annually.

But the real genius is the services model. Services account for ~65% of backlog, providing GE Vernova with visibility into cash flow streams and keeping us close to our customers. Every turbine installed creates a 20-30 year service relationship. Planned maintenance, unplanned outages, upgrades, digital monitoring—each touchpoint generates margin-rich revenue.

Segment EBITDA was $0.5 billion and segment EBITDA margin was 11.9%, up +470 basis points, +240 basis points organically, with higher volume, productivity, and price more than offsetting inflation. These aren't commodity margins—they reflect pricing power that comes from being the only company that truly understands these machines' DNA.

The data center boom has transformed Power from mature cash cow to growth engine. A single large AI training facility can consume 100MW or more—equivalent to powering 80,000 homes. These facilities need reliable, 24/7 power that renewables alone can't provide. Gas turbines, with their ability to ramp up in minutes, become the backbone of AI infrastructure.

Wind: The Turnaround Story

If Power is the present, Wind represents GE Vernova's most complex bet on the future. GE Vernova has an installed base of ~57,000 wind turbines totaling 120 GW+ of installed capacity and the largest installed base of onshore turbines in the United States.

But Wind has been bleeding. The Offshore Wind segment faced significant challenges, including a substantial loss due to manufacturing deviations in turbine blades, impacting financial results. The Haliade-X offshore turbine, once hailed as revolutionary with its 12-14MW capacity, became an albatross as fixed-price contracts collided with inflationary reality.

Onshore Wind Profitability: Most profitable quarter in 12 quarters—this single line represents hundreds of operational improvements. Strazik's team has fundamentally restructured the business: fewer product variants, selective bidding, and ruthless focus on markets where GE Vernova can win profitably.

The strategic pivot is telling. Instead of chasing every wind project globally, GE Vernova now focuses on North America and select European markets where it has manufacturing scale and service density. The company walked away from billions in unprofitable orders, choosing margin over volume—heresy in the old GE playbook.

Wind: maintain flat organic revenue and approaching profitability with nearly 50% segment EBITDA improvement. This isn't growth—it's stabilization. But in a business that was hemorrhaging cash eighteen months ago, stability is victory.

The onshore business tells a different story. The 3MW platform turbines—workhorses, not show ponies—generate consistent returns. These aren't the largest or most advanced turbines, but they're reliable, serviceable, and profitable. Sometimes in industrial businesses, boring is beautiful.

Electrification: The Hidden Gem

Electrification might be GE Vernova's most underappreciated segment—and its highest growth opportunity. Electrification Revenue: 24% increase, with significant growth in grid solutions. Electrification Backlog: Approximately $19 billion, up almost $6 billion from 3Q 2023.

This isn't just selling transformers and switchgear. It's about rebuilding the entire electrical grid for a distributed, renewable, digitized future. Every solar farm needs grid connection. Every EV charging station needs distribution infrastructure. Every data center needs redundant power systems.

The numbers are staggering. The U.S. alone needs to expand transmission capacity by 60% by 2030 to integrate renewable energy. Europe needs to invest €584 billion in grids by 2030. China is building ultra-high-voltage networks to move renewable power from remote regions to cities. GE Vernova supplies critical components for all of it.

Electrification: now expect high-teens organic revenue growth. Electrification: Mid-to-high-teens organic revenue growth and 11%-13% segment EBITDA margin. These growth rates in an industrial business are extraordinary, reflecting both market demand and GE Vernova's competitive position.

The real differentiator is software. GridOS, GE Vernova's grid orchestration platform, isn't just monitoring equipment—it's using AI to predict failures, optimize power flows, and integrate renewable sources in real-time. GE Vernova announced the acquisition of Alteia to enhance its electrification software business, integrating AI and visualization technologies with GridOS.

Consider what happens when a cloud passes over a solar farm: output drops 80% in seconds. The grid must instantly compensate with other sources or face blackouts. GridOS orchestrates this ballet thousands of times daily, invisible to consumers but critical to reliability.

The manufacturing footprint tells its own story. The company announced an incremental investment of up to $100 million in the Charleroi factory, supporting job creation and doubling volume output by 2028. This Pennsylvania facility produces transformers—unglamorous gray boxes that are suddenly the bottleneck for every renewable project, every data center, every EV charging network.

Lead times for large transformers have stretched to over two years. Utilities are hoarding equipment. Countries are treating transformer capacity as strategic national infrastructure. In this environment, having manufacturing capacity isn't just an advantage—it's a license to print money.

The integration across segments creates compounding advantages. A utility building a renewable plant needs wind turbines (Wind segment), gas peakers for backup (Power segment), and grid connections (Electrification segment). GE Vernova can provide all three, with integrated software managing the entire system. No competitor matches this breadth.

VII. The Energy Transition Opportunity & Market Dynamics

The energy trilemma—reliability, affordability, sustainability—isn't just corporate jargon. It's the central challenge of our civilization's next chapter. And GE Vernova sits at the exact intersection where these three forces collide.

Electricity demand from data centres worldwide is set to more than double by 2030 to around 945 terawatt-hours (TWh), slightly more than the entire electricity consumption of Japan today. AI will be the most significant driver of this increase, with electricity demand from AI-optimised data centres projected to more than quadruple by 2030.

Let that sink in. We're adding Japan's entire electricity consumption just for data centers. In the United States, power consumption by data centres is on course to account for almost half of the growth in electricity demand between now and 2030.

This isn't gradual growth—it's a step function. According to McKinsey analysis, the United States is expected to be the fastest-growing market for data centers, growing from 25 GW of demand in 2024 to more than 80 GW of demand in 2030. Between 2024 and 2030, electricity demand for data centers in the United States is expected to increase by about 400 terawatt-hours at a CAGR of about 23 percent.

The implications cascade through every aspect of the energy system. As data centers contribute to a growing need for power, the electric grid will require significant investment. Goldman Sachs Research estimates that about $720 billion of grid spending through 2030 may be needed.

But here's the catch: The time required to get new power connections for data center sites in major data center hubs such as Northern Virginia; Santa Clara, California; and Phoenix has been increasing. You can build a data center in 18 months. Connecting it to the grid? That might take five years.

This temporal mismatch creates extraordinary opportunities for companies that can bridge the gap. GE Vernova's gas turbines can be deployed in 24-36 months—faster than grid expansion, faster than nuclear, competitive with renewables when you factor in grid integration.

The natural gas bridge debate reveals the complexity. Environmental purists hate it—gas still emits CO2. Pragmatists recognize reality: A diverse range of energy sources will be tapped to meet data centres' rising electricity needs, according to the report – though renewables and natural gas are set to take the lead due to their cost-competitiveness and availability in key markets.

GE Vernova's gas turbines can reduce emissions by two-thirds compared to coal while providing the baseload power that renewables can't. The HA turbines are hydrogen-ready, meaning they can transition to clean fuel as hydrogen infrastructure develops. It's not perfect, but it's progress.

The renewable integration challenge is where things get technically fascinating. Wind and solar are now the cheapest forms of new generation in most markets. But they're intermittent. A passing cloud can drop solar output 80% in seconds. Wind can die for days. The grid needs inertia—physical rotating mass that maintains frequency stability. Gas turbines provide it. Batteries don't.

In large economies like the United States, China and the European Union, data centres account for around 2-4% of total electricity consumption today. But because they tend to be spatially concentrated, their local impact can be pronounced. The sector has already surpassed 10% of electricity consumption in at least five US states.

This concentration creates both challenges and opportunities. Northern Virginia—data center capital of the world—is running out of power. Dominion Energy has essentially said: no new connections until 2028. But this scarcity creates pricing power for those who can deliver solutions.

GE Vernova's approach is holistic. They're not just selling turbines or wind farms or transformers. They're selling integrated energy systems. A hyperscaler building a new data center campus? GE Vernova can provide on-site gas generation for immediate power, wind farms for renewable credits, grid infrastructure for utility connection, and software to orchestrate it all.

The competition landscape is fragmenting in interesting ways. Siemens Energy, GE Vernova's traditional rival, is struggling with its own wind division losses. Mitsubishi Power is strong in Asia but lacks GE Vernova's services footprint. Chinese manufacturers like Dongfang Electric offer lower prices but face geopolitical headwinds in Western markets.

The real competition isn't from other turbine makers—it's from alternative energy models. Tech companies are going directly to nuclear, signing deals with reactor developers. Amazon bought a nuclear-powered data center. Microsoft signed a deal to restart Three Mile Island. Google is investing in small modular reactors.

But nuclear faces its own challenges: decade-long development cycles, regulatory uncertainty, public opposition. By the time these nuclear projects come online, GE Vernova will have installed thousands of megawatts of gas and renewable capacity.

Climate policy adds another layer of complexity. The Inflation Reduction Act provides massive subsidies for renewable energy—great for GE Vernova's wind business. But it also includes methane penalties that could increase natural gas costs—challenging for the Power segment. Europe's carbon border adjustment mechanism will reshape global energy trade. China's commitment to peak emissions by 2030 is driving massive renewable deployment.

Yet through all this policy uncertainty, one thing remains constant: the world needs more electricity. Global aggregate electricity demand grows by 6 750 terawatt-hours (TWh) by 2030 in our Stated Policies Scenario, equivalent to more than the combined demand from the United States and European Union today.

This isn't just about data centers. It's about electric vehicles adding 100TWh annually by 2030. It's about heat pumps replacing gas furnaces. It's about green hydrogen production for steel and chemicals. It's about reshoring manufacturing that requires reliable power. Every aspect of decarbonization requires more electricity.

The investment implications are staggering. McKinsey research estimates that generative AI (gen AI) could help create between $2.6 trillion and $4.4 trillion in economic value throughout the global economy. But realizing this value requires energy infrastructure that doesn't yet exist.

VIII. Financial Performance & Capital Allocation

The financial architecture of GE Vernova tells a story of transformation in real-time. In 2024, GE Vernova orders of $44.1 billion increased +7% organically, with robust equipment growth in Power and Electrification and double-digit services growth in each segment. Revenue of $34.9 billion was up +5%, +7% organically, driven by higher services and equipment volume, with positive price in all segments. Margins expanded significantly from higher volume, price, and productivity, more than offsetting inflation. Cash flow improved by over $1 billion year-over-year, primarily from adjusted EBITDA growth.

But the headline numbers obscure the real story: this is a company learning how to make money after years of value destruction. GE Vernova built a strong foundation in 2024 with solid orders and revenue growth, as well as significant margin expansion and cash generation. We saw strength in Power and Electrification and improvement in Wind, while growing our equipment backlog at better margins.

The transformation shows up most dramatically in cash generation. Key total company financial highlights for full year 2024: Orders of $44.1B, +7% organically, led by Power and Electrification equipment, and services in each segment · Revenue of $34.9B, +5%, +7% organically driven by Electrification and Power · Net income of $1.6B, +$2.0B; net income margin of 4.5%, +590 bps · Adjusted EBITDA of $2.0B and adjusted EBITDA margin of 5.8% Cash from operating activities of $2.6B, +$1.4B; positive free cash flow of $1.7B, +$1.3B · $8.2B cash balance up from $7.4B in the third quarter of 2024 and from $4.2B at spin-off on April 2, 2024.

The cash balance evolution is remarkable: from $4.2 billion at spin-off to $8.2 billion by year-end 2024—nearly doubling in nine months without raising capital. This isn't financial engineering; it's operational improvement driving cash conversion.

We are reaffirming our 2025 GE Vernova guidance. We continue to expect revenue of $36-$37 billion, high-single digits adjusted EBITDA margin, and free cash flow of $2.0-$2.5 billion. The 2025 guidance represents another step-change in profitability: from 5.8% EBITDA margins to high-single digits in one year.

The segment-level performance reveals where value creation is happening. Total year orders of $21.8 billion increased +28% organically, from strong demand for Gas Power equipment and double-digit services growth. Revenues of $18.1 billion increased +4%, +7% organically, led by Gas Power. Segment EBITDA margin grew +260 basis points, +180 basis points organically.

Power is the cash engine firing on all cylinders. The margin expansion story is compelling: from single digits to approaching mid-teens, with line of sight to high-teens by decade's end. This isn't just volume leverage—it's pricing power from equipment scarcity, service contract escalations, and operational improvements.

The Wind turnaround remains work-in-progress but shows green shoots. Wind: Organic revenue down mid-single digits and $200-$400 million of segment EBITDA losses. But context matters: this business was losing over $1 billion annually two years ago. The trajectory is clear even if the destination remains distant.

Electrification emerges as the growth star. Electrification: Mid-to-high-teens organic revenue growth and 11%-13% segment EBITDA margin. These are software-like growth rates in a hardware business, reflecting both market dynamics and competitive positioning.

The working capital story deserves attention. Industrial companies typically consume cash as they grow—more inventory, more receivables. GE Vernova is doing the opposite: growing while generating cash. This reflects both operational improvements (shorter cycle times, better collections) and market power (customer deposits, progress payments).

GE Vernova CFO Ken Parks said, "We are executing our financial strategy, and we now expect to generate at least $14 billion in cumulative free cash flow by 2028. Our large and growing backlog, with healthy margins from services and better equipment pricing, is fueling our trajectory as we raise our 2025 guidance and outlook by 2028.

$14 billion in cumulative free cash flow by 2028—that's nearly 30% of current market cap in cash generation over four years. For an industrial company with massive capital requirements, this is extraordinary.

The capital allocation framework reveals confidence in the business model. We also framed our capital allocation strategy, announcing that our Board of Directors declared a quarterly dividend and approved an initial share repurchase authorization. We remain committed to maintaining an investment grade balance sheet as we make organic investments, pursue targeted M&A, and return at least one third of cash generation to shareholders through dividends and share repurchases.

The commitment to return at least one-third of cash to shareholders while maintaining investment grade ratings and funding growth is aggressive but achievable given the cash generation trajectory.

The Q2 2025 update shows acceleration, not deceleration. We are raising our 2025 financial guidance based on our strong first half execution and momentum in our Power and Electrification segments. Based on our performance, we are now trending towards the higher end of our 2025 revenue guidance and have increased our expectations for adjusted EBITDA margin and free cash flow.

We grew our backlog by more than $5 billion and increased our Gas equipment backlog and slot reservation agreements from 50 to 55 gigawatts. The slot reservation agreements are particularly telling—customers are paying to reserve future turbine delivery slots, sometimes years in advance. This isn't just backlog; it's option value on future energy infrastructure.

The tariff impact adds complexity but appears manageable. The guidance includes the impact of tariffs as currently outlined and resulting inflation, which is now estimated to be trending toward the lower end of approximately $300-$400 million, net of mitigating actions. In a business generating $37 billion in revenue, $300-400 million in tariff impact is noise, not signal.

But the real financial story isn't in the reported numbers—it's in what's not being valued. The installed base of 7,000 gas turbines represents decades of service revenue not fully captured in backlog. The wind turbine fleet, despite current challenges, will eventually need repowering or replacement. The grid infrastructure being installed today will require upgrades and software for decades.

IX. Playbook: Lessons from the Spin-off

The GE Vernova spin-off will be studied in business schools for decades, but not for the reasons you might expect. This wasn't just a corporate restructuring—it was a masterclass in value creation through focus, timing, and narrative transformation.

Lesson 1: The Pure-Play Premium is Real

As a division of GE, the energy businesses were valued at perhaps 5-6x EBITDA, buried under corporate allocations and conglomerate discount. As GE Vernova, the market values the same assets at 15-20x EBITDA. Nothing fundamental changed—same turbines, same customers, same employees. What changed was clarity.

Investors can now understand what they own. No more trying to decipher how much corporate overhead gets allocated to Power versus Aviation. No more wondering if cash from energy funds healthcare losses. Pure-play transparency commands premium multiples.

Lesson 2: Timing the Cycle

Culp's genius wasn't just deciding to split GE—it was the sequencing. Healthcare went first in January 2023, when medical equipment was still riding COVID tailwinds. Aerospace and Vernova launched together in April 2024, just as aviation recovery accelerated and energy transition reached inflection.

Had they spun Vernova in 2021, it would have launched with massive wind losses and no AI-driven power demand story. Had they waited until 2026, they'd have missed the current investment cycle. The window was narrow; they threaded it perfectly.

Lesson 3: Building Independent DNA

The hardest part wasn't legal or financial—it was cultural. GE Vernova employees had to transform from division managers to company leaders. Strazik's approach was deliberate: new headquarters, new brand, new operating rhythm. Every symbol mattered.

The Cambridge headquarters wasn't just real estate—it was a declaration of independence. The evergreen color wasn't just branding—it was identity formation. The lean operating system wasn't just process improvement—it was cultural revolution.

Lesson 4: The Art of the Equity Story

GE Vernova launched with three narratives, each appealing to different investor constituencies:

- Value investors: Undervalued industrial with improving fundamentals

- Growth investors: Energy transition beneficiary with secular tailwinds

- Income investors: Future dividend aristocrat with growing cash generation

This wasn't accidental. Management crafted messages for each audience, ensuring broad market appeal. The investor day presentations were choreographed to hit every theme.

Lesson 5: Managing the Transition Services Agreement (TSA)

Most spin-offs fail at the TSA—the boring but critical agreement governing how the parent provides services during transition. GE Vernova negotiated 24-month TSAs for critical systems but aggressively built internal capabilities. They're ahead of schedule on TSA exit, reducing dependency and cost.

The IT separation alone involved splitting 283 ERP systems, migrating petabytes of data, and ensuring zero business disruption. They accomplished it without a single major incident—remarkable for industrial IT separation.

Lesson 6: The Balance Sheet Reset

The debt allocation between the three companies was perhaps the most critical decision. GE Vernova received minimal debt relative to its cash generation, ensuring investment-grade ratings from day one. This wasn't generosity—it was strategic. Energy transition investments require patient capital; junk ratings would have killed the business model.

The pension allocation was equally clever. GE Vernova took its proportional share but negotiated caps on future liability. They wanted predictability more than optimization.

Lesson 7: Customer Communication

The most underappreciated aspect was customer management. Utilities don't like surprises. Power plants can't afford uncertainty. GE Vernova launched with every major customer pre-briefed, contracts novated, and service agreements confirmed.

Strazik personally visited the top 50 customers in the six months before spin-off. The message was consistent: same people, same products, more focus. Customer attrition post-spin was essentially zero—unprecedented for industrial separation.

Lesson 8: The Talent Retention Playbook

GE Vernova faced a unique challenge: competing for talent against both GE Aerospace (sexier business) and external opportunities (tech companies poaching industrial software talent). Their solution was elegant:

- Equity grants that vest over four years, creating golden handcuffs

- Geographic flexibility—keeping engineering centers where talent lives

- Mission-driven messaging about energy transition and climate impact

- Aggressive promotion from within, creating opportunity

Employee retention exceeded 95% through the transition—remarkable given the uncertainty.

Lesson 9: Wall Street Education

Most analysts covering GE had never analyzed a pure-play energy equipment company. GE Vernova invested heavily in investor education:

- Detailed segment reporting from day one

- Monthly operational metrics during transition

- Site visits to manufacturing facilities

- Technical deep-dives on turbine technology

They transformed sell-side analysts into evangelists by making them experts.

Lesson 10: The Option Value Creation

The masterstroke was creating multiple paths to value creation:

- Organic growth: Rising energy demand drives equipment sales

- Margin expansion: Operational improvements and mix shift to services

- Capital returns: Growing cash enables dividends and buybacks

- M&A optionality: Strong balance sheet allows strategic acquisitions

- Multiple expansion: As execution improves, valuation re-rates higher

Each path independently could drive 50%+ returns. Combined, they create asymmetric upside.

X. Bear vs. Bull Case & Future Scenarios

The Bull Case: The Energy Supercycle Thesis

The bulls see GE Vernova as the perfect vehicle to ride a multi-decade energy supercycle. Their thesis rests on several pillars:

Demand Explosion: Electricity demand growth accelerating from 2% annually to 4-5% driven by AI, EVs, reshoring, and electrification. Every percentage point of additional demand growth represents $5-10 billion in annual equipment opportunity.

Supply Constraints: Limited manufacturing capacity for turbines, transformers, and grid equipment. Lead times extending to 3+ years create pricing power. GE Vernova's installed capacity becomes a competitive moat—you can't build what they have overnight.

Services Transformation: The installed base monetization story has barely begun. Current service penetration is 30-40%. Bulls see this reaching 60-70%, doubling service revenue without selling a single new turbine. Add digital services, remote monitoring, and performance optimization—each turbine becomes an annuity stream.

Wind Turnaround: The bleeding stops, profitability returns. Not through growth but through discipline—selective bidding, design standardization, cost reduction. Even breakeven by 2026 represents $1 billion of EBITDA improvement.

Grid Modernization Boom: $720 billion in U.S. grid investment needed by 2030. GE Vernova captures 20-30% share. Grid equipment margins expand from 10% to 15%+ as capacity constraints bite. Every data center, every renewable project, every EV charging network needs grid infrastructure.

Nuclear Renaissance: Small modular reactors become reality. GE Hitachi's BWRX-300 leads deployment. Each reactor requires turbines, generators, and decades of service. By 2035, nuclear represents 10% of revenue.

Multiple Re-rating: As execution improves, market assigns premium multiples. Best-in-class industrials trade at 20-25x EBITDA. GE Vernova reaches $8-10 billion EBITDA by 2030, implying $160-250 billion valuation.

Bulls see $500+ stock price by 2030, a 5x return from current levels.

The Bear Case: The Disruption Scenario

Bears see fundamental challenges that financial engineering can't fix:

Renewable Decimation: Solar + storage costs continue plummeting. By 2027, renewable + battery cheaper than gas peaker plants. Gas turbine orders collapse 50%. Stranded asset risk for entire installed base.

China Competition: Chinese manufacturers enter Western markets aggressively. Dongfang, Shanghai Electric, Harbin offer 30-40% discounts. Pricing pressure destroys margins. IP theft accelerates commoditization.

Execution Disasters: Offshore wind losses continue. Blade failures trigger massive warranties. European projects abandoned. Write-offs exceed $5 billion. Management credibility destroyed.

Technology Disruption: Fusion breakthrough makes fission and gas obsolete. Distributed generation eliminates need for central plants. Microgrids bypass traditional infrastructure. GE Vernova's assets become scrap metal.

Regulatory Assault: Carbon taxes make gas uneconomic. Renewable mandates eliminate gas peakers. Environmental litigation creates massive liabilities. Stranded asset provisions destroy balance sheet.

Customer Defection: Hyperscalers build their own power infrastructure. Utilities in-source services. Long-term service agreements aren't renewed. Service revenue—the crown jewel—evaporates.

Balance Sheet Stress: Hidden liabilities emerge—environmental, pension, warranty. Cash generation disappoints. Debt downgrades trigger covenant breaches. Liquidity crisis forces asset sales.

Bears see the stock below $50, a 50% decline, as reality crushes transition dreams.

The Base Case: Muddle Through with Moments

Reality likely sits between extremes. The base case sees:

Steady but Unspectacular Growth: Revenue grows 5-7% annually. Electricity demand increases but not exponentially. AI boom moderates after initial surge. Energy transition proceeds gradually, not revolutionary.

Margin Expansion with Setbacks: EBITDA margins reach 10-12% by 2027. Power margins expand but face gas competition. Wind achieves profitability but remains challenged. Electrification grows but margins compress from competition.

Cash Generation Enables Capital Returns: Free cash flow reaches $3-4 billion annually. Dividend grows steadily, 5-10% annually. Share buybacks accelerate when stock undervalued. Balance sheet remains strong but unexciting.

Valuation Fairly Reflects Reality: Stock trades between $120-180. 15-18x EBITDA multiple—fair for industrial. 3-4% dividend yield attracts income investors. Volatility around quarterly results.

Wild Cards

Several factors could dramatically shift outcomes:

Climate Catastrophe: Extreme weather drives emergency infrastructure spending. Resilience becomes priority over cost. GE Vernova benefits from crisis response.

Geopolitical Fracture: U.S.-China decoupling accelerates. Energy security trumps energy transition. Domestic manufacturing prioritized regardless of cost.

Breakthrough Innovation: GE Vernova develops revolutionary technology—100% efficient turbines, room-temperature superconductors, commercial fusion. Technology leadership drives monopolistic position.

M&A Transformation: Major acquisition reshapes portfolio—buying Vestas wind assets, merging with grid company, acquiring nuclear technology. Scale and scope create new value creation.

The 2030 Scorecard

By 2030, we'll know which thesis proved correct:

- Revenue: Bulls see $60B+, Bears see $30B, Base sees $45B

- EBITDA Margin: Bulls see 15%+, Bears see 5%, Base sees 10-12%

- Free Cash Flow: Bulls see $6B+, Bears see $1B, Base sees $3-4B

- Stock Price: Bulls see $500+, Bears see sub-$50, Base sees $150-200

The truth is, all three scenarios are plausible. Energy transitions are messy, non-linear, and full of surprises. GE Vernova's fate depends on execution, market dynamics, and luck—probably in that order.

XI. Epilogue: The Energy Future

Standing in GE Vernova's Cambridge headquarters, looking out at MIT's skyline, you can't help but wonder: Is this the last chapter of American industrial greatness or the first chapter of its resurrection?

The company represents something larger than its financial statements suggest. It's a bet that American industrial companies can still compete globally, that 130-year-old organizations can reinvent themselves, that the energy transition needs pragmatists as much as dreamers.

GE Vernova tells us that industrial America is evolving, not dying. The transformation from conglomerate division to focused pure-play mirrors broader economic shifts: from scale to specialization, from diversification to depth, from financial engineering to operational excellence.

The balance between legacy and innovation defines GE Vernova's challenge. They must honor Edison's heritage while embracing Musk's urgency. They need union workers in Schenectady and software developers in Cambridge. They're selling 50-year turbines and annual software subscriptions.

Energy security in a multipolar world adds urgency. As supply chains fracture and allies diverge, domestic energy infrastructure becomes national security infrastructure. GE Vernova's American manufacturing footprint—once a liability—becomes strategic advantage.

Key metrics to watch going forward:

- Service penetration rate: Currently ~40%, target 60%+

- Gas turbine utilization rates: Higher utilization drives service revenue

- Wind segment EBITDA: Breakeven by 2026 would validate turnaround

- Electrification order growth: Leading indicator of infrastructure investment

- Cash conversion: Free cash flow as percentage of EBITDA

- Grid software adoption: Recurring revenue from digital solutions

The deeper question is whether GE Vernova represents the future of energy or the last gasp of fossil infrastructure. The answer is probably both. The energy transition won't be a clean break but a messy overlap—decades where gas, wind, solar, nuclear, and whatever comes next coexist uncomfortably.

GE Vernova's ultimate success depends on navigating this complexity. They're not betting on one future but positioning for multiple futures. Gas turbines for reliability, wind for sustainability, grid for everything. It's hedged, pragmatic, and probably right.

The spin-off strategy, in retrospect, was inevitable. Conglomerates are 20th-century artifacts, built for capital allocation when capital was scarce. Today's markets are awash in capital but starved for clarity. Pure-plays provide that clarity.

Larry Culp's legacy won't be saving GE—it will be killing it. By dismantling the conglomerate, he freed three companies to pursue their destinies. GE Aerospace soars, GE HealthCare heals, and GE Vernova powers. Each focused, accountable, and valuable in ways the confederation never could be.

For investors, GE Vernova represents a fascinating risk-reward proposition. The bear case is real—disruption, competition, and execution risks abound. But the bull case is equally compelling—secular growth, operational improvement, and multiple expansion potential.

The truth is, we don't know how the energy transition unfolds. Will it be gradual or revolutionary? Centralized or distributed? Gas-bridged or renewable-leaped? GE Vernova is betting it will be all of the above, simultaneously, messily, profitably.

Edison would recognize this moment. In 1882, he didn't know if electricity would transform the world or remain a curiosity. He built the infrastructure anyway, trusting that demand would follow supply. GE Vernova makes the same bet today: build it, and they will consume.

The meters are running, the turbines are spinning, and the future is being written one kilowatt-hour at a time. GE Vernova doesn't need to predict that future perfectly—it just needs to power it reliably. In a world demanding ever more electricity, that might be enough.

XII. Recent News

[To be populated with latest developments - the dynamic nature of energy markets means this section requires constant updating]

XIII. Links & Resources

Official Resources: - GE Vernova Investor Relations: https://www.gevernova.com/investors - SEC Filings: Search "GEV" on sec.gov - Quarterly Earnings Calls: Available on investor relations site

Industry Resources: - International Energy Agency: iea.org - U.S. Energy Information Administration: eia.gov - Global Wind Energy Council: gwec.net

Key Competitor Sites: - Siemens Energy: siemens-energy.com - Mitsubishi Power: power.mhi.com - Vestas: vestas.com

Market Intelligence: - McCoy Power Reports (gas turbine market share) - Wood Mackenzie (energy market analysis) - BloombergNEF (renewable energy data)

Academic & Think Tanks: - MIT Energy Initiative - Columbia Center on Global Energy Policy - Atlantic Council Global Energy Center

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube