Flutter Entertainment: The House That Bets Built

Introduction: From Dublin to the World

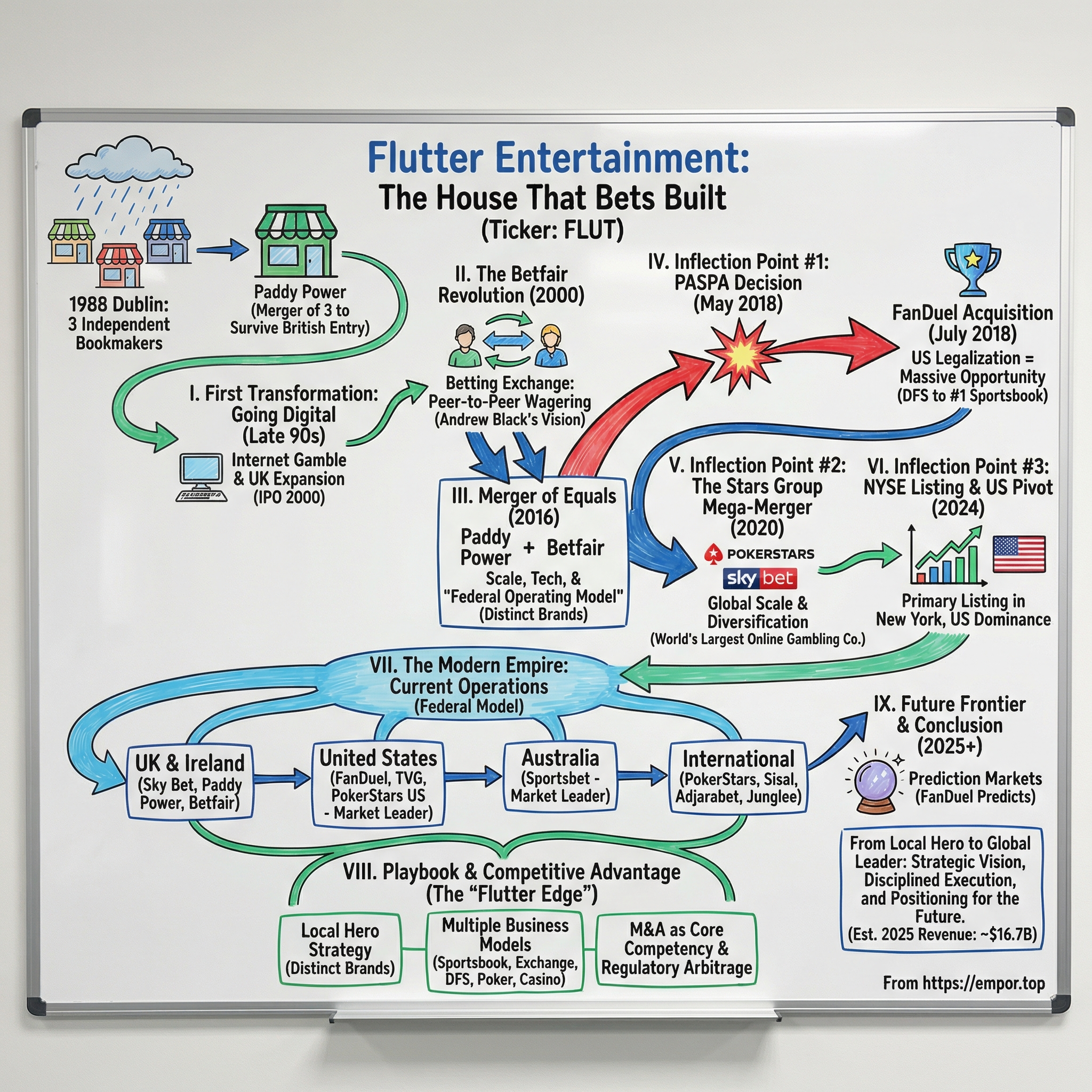

Picture the rain-slicked streets of Dublin in the summer of 1988. In betting shops scattered across Ireland, three independent bookmakers—men who had spent their lives sizing up punters, calculating odds, and watching nervous excitement play across their customers' faces—faced an existential threat. British betting giants like Ladbrokes and Coral were marching into Ireland, armed with deeper pockets and economies of scale that could crush the local operators underfoot. The Irish bookmaking tradition, stretching back generations, seemed destined to become a footnote in the expansion plans of multinational corporations.

What happened next would redefine an entire industry.

Paddy Power was founded in 1988 by a merger of the forty shops of three Irish bookmakers: Stewart Kenny, David Power, and John Corcoran. That decision—born of necessity, executed with Irish audacity—planted the seed for what would become the industry leader with $14,048m of revenue globally for fiscal 2024.

Today, Flutter Entertainment stands as a colossus bestriding the global gambling landscape. Flutter operates a diverse portfolio of leading online sports betting and iGaming brands including FanDuel, Sky Betting & Gaming, Sportsbet, PokerStars, Paddy Power, Sisal, tombola, Betfair, MaxBet, Junglee Games and Adjarabet. The company holds dominant positions across the United States, United Kingdom, Ireland, Australia, and Italy—a geographic footprint assembled through a quarter-century of relentless expansion, disciplined M&A, and an uncanny ability to position itself at the precise moment when regulatory windows opened.

The story of Flutter is the story of modern gambling itself: the shift from smoky betting parlors to sleek smartphone apps, from local bookies to global platforms, from illegal offshore operations to regulated markets generating billions in tax revenue. It is a story of technological disruption, regulatory arbitrage, and the democratization of betting through the internet. And at its heart, it remains a story about understanding human nature—the thrill of risk, the fantasy of beating the odds, the social experience of watching a game with skin in the outcome.

How did three Irish bookmakers with 40 shops create a $50 billion gambling empire? That requires understanding a series of inflection points that transformed a regional operator into a global powerhouse—and the visionary founders, innovators, and executives who recognized opportunities that others missed.

I. Origins: The Birth of Paddy Power

The Irish Bookmaking Scene

Ireland in the 1980s maintained a deep cultural relationship with gambling. Betting shops dotted high streets in every town, and racing—both horses and greyhounds—wasn't merely a sport but a national pastime. Families passed down bookmaking businesses through generations, with knowledge of odds-setting and risk management transmitted like craft secrets.

Born in 1941 into a family already laying the foundations for what would go on to form a bookmaking dynasty, Power's mother is thought to have been the first woman to hold a betting licence while his grandfather formed Richard Power Bookmakers in 1895. David Power represented the third generation of a family that had been taking bets since Queen Victoria still sat on the throne.

But by the late 1980s, the comfortable world of Irish independent bookmakers faced disruption. British betting giants, having consolidated their home market, looked across the Irish Sea for growth. They arrived with professional management, sophisticated marketing, and capital that local operators couldn't match. Independent bookmakers faced a stark choice: sell out or risk being competed into oblivion.

The Three Founders

Paddy Power was established in 1988 through the merger of three independent Irish bookmakers—Stewart Kenny, David Power, and John Corcoran—combining their approximately 40 retail betting shops to form a unified operation headquartered in Dublin. The merger was motivated by the need to counter the entry of larger British betting chains into the Irish market, which threatened smaller local operators by leveraging economies of scale and aggressive pricing.

Each founder brought distinct capabilities to the partnership.

Born in Dublin in 1951, Stewart Kenny was a life-long fan of gambling as a pastime. He placed one of his first wagers in 1974, believing that Richard Nixon would resign the Presidency. He created a series of betting shops in Ireland, having trained in the trade in London working for Ladbrokes. Kenny's stint at Ladbrokes gave him insight into how large-scale operations functioned—knowledge he would apply to competing against them. Stewart Kenny and Vincent O'Reilly had sold Kenny O'Reilly Bookmakers to Coral in 1986, and then opened ten shops of their own by 1988; Kenny was group CEO from 1988 to 2002, and chairman from 2002 to 2003.

David Henry Power (16 January 1947 – 8 July 2024) was an Irish bookmaker. Power's grandfather started bookmaking in Tramore, County Waterford in 1896, having earlier worked as a draper. The business passed to his son, Paddy, who died suddenly in 1963, leaving it to his son David. Power completed his schooling at St Mary's College in Rathmines and studied accountancy at University College Dublin before taking over the family bookmaking firm in 1970. His credentials as a chartered accountant would prove invaluable in professionalizing the combined operation.

Born on the first of December in 1929, more is known about John Corcoran than the other two Paddy Power co-founders. It was actually Corcoran's idea to merge the three companies that had 40 shops between them in order to survive the invasion of British bookmakers to Ireland in the 1980s; at least according to how Stewart Kenny remembers it. Alongside his bookmaking business, Corcoran formed Green Property, which would go on to become one of Ireland's largest real estate businesses. According to Kenny, it was his laid-back attitude towards life and business that made him such a success.

The Challenger Brand Identity

Joining forces with Stewart Kenny and John Corcoran, the trio merged their retail shops in 1988 to compete with new British entrants arriving on Irish highstreets. To show they were truly up for the fight, they decided on a name that was uniquely Irish, but also conveyed strength and pride – Paddy Power. The name carried multiple meanings: it derived from David Power's surname (the strongest brand among the merged shops), but "Paddy" was also quintessentially Irish—a deliberate statement of national identity against the British interlopers.

Conveniently, this was also the name of David's son, Paddy, who has since become synonymous with a brand that has always been mischievous and on the side of the punter, but also truly innovative and pioneering.

The strategy went beyond branding. Paddy Power had an aggressive expansion strategy involving opening prominent shops in most Irish towns, rather than side streets previously favoured. The firm's novelty bets broadened its media coverage beyond the horseracing news. This was counterintuitive—traditional bookmakers tucked their shops away, acknowledging the social stigma around gambling. Paddy Power said, in effect, that betting was entertainment, not vice.

Its share of the Irish off-course betting market grew from 8% in 1988 to 33% in 2001. In thirteen years, the company had captured a third of its home market—a remarkable achievement that validated both the merger strategy and the distinctively Irish, proudly irreverent brand positioning.

The founders established patterns that would define Flutter's DNA for decades: defensive consolidation against larger competitors, aggressive branding that differentiated through personality, and a willingness to bet on emerging trends before others recognized the opportunity. These principles would prove equally applicable whether the medium was high-street shops, desktop websites, or smartphone apps.

II. The First Transformation: Going Digital

The Internet Gamble

By the late 1990s, the internet was transforming industries across the economy—and few sectors were as ripe for disruption as gambling. Physical betting shops had obvious constraints: limited operating hours, geographic restrictions, the friction of traveling to place a bet. Online betting promised to eliminate all of these limitations, allowing customers to wager from anywhere, at any time, with virtually unlimited selection.

Having established Paddy Power as a strong retail bookmaker in the 90s, David will also be remembered as a great moderniser of our industry. He was an influential voice in Paddy Power's decision to embrace the power of the internet, kickstarting a prolonged period of growth that saw the company list on both the Irish and London Stock Exchanges in 2000.

The timing was opportune. The dotcom boom made capital abundant for internet ventures, while Ireland's Celtic Tiger economy provided a favorable domestic environment. Power Leisure, the parent company of Paddy Power PLC, listed on the London Stock Exchange in December 2000, to fund an expansion in the UK.

The IPO marked Paddy Power's transformation from a regional Irish bookmaker into a publicly traded company with pan-European ambitions. The capital raised enabled investment in online platforms while the London listing provided credibility and visibility in the larger UK market.

UK Expansion

Physical expansion paralleled digital growth. At the end of 2005, Paddy Power operated 195 outlets (150 in Ireland and 45 in the UK). The total number of employees was 1,374. The company had nearly quintupled its retail footprint from the original 40 shops while building an online business from scratch.

In February 2010, the chain had 356 shops with 209 in Ireland, 8 in Northern Ireland and 139 in Great Britain. The UK expansion was significant because England, Scotland, and Wales represented a far larger addressable market than Ireland—but also a more competitive one, with established players like William Hill, Ladbrokes, and Coral already commanding strong positions.

Paddy Power differentiated through the same irreverent brand personality that had succeeded in Ireland. The company became known for outrageous publicity stunts, controversial betting markets, and a willingness to refund bets when outcomes seemed unfair—even when the rules technically favored the house.

Marketing Genius and Controversy

As of November 2011, Paddy Power was the largest bookmaker in Europe by total share value. Its group income was €444m in 2010.

This achievement was remarkable given Paddy Power's relative youth compared to century-old competitors. The company had reached the top of European gambling by combining online scale with a brand personality that generated enormous free media coverage.

But the distinctive marketing approach also created controversy. Paddy Power has drawn criticism for offering controversial markets, such as odds on the first species to be driven to extinction by the BP oil spill in the Gulf of Mexico, on a prospective assassination of United States President Barack Obama, and on the potential extinction of the polar bear in December 2009.

The company walked a fine line between generating attention and causing genuine offense. While some stunts backfired spectacularly, the overall strategy succeeded in differentiating Paddy Power from more staid competitors and building an emotional connection with customers who appreciated the brand's irreverent humor.

David was immensely proud that his plucky Irish business, with its 40 shops initially, paved the way for Flutter to become the global leader in online sports betting and iGaming it is today.

The transition to digital proved that Paddy Power could adapt to technological change while maintaining its distinctive culture. That ability to evolve would be tested repeatedly as the company navigated subsequent transformations—including a merger with a company that had taken an entirely different approach to revolutionizing gambling.

III. The Betfair Revolution: Betting's "Stock Exchange"

Andrew Black: The Visionary Gambler

While Paddy Power was building its empire through retail shops and online sportsbooks, a very different approach to gambling was taking shape in the mind of Andrew Black—a man whose unlikely background combined mathematics, derivatives trading, government cryptography, and professional gambling.

Black was born on 13 May 1963, the son of a property developer and grandson of Tory MP for Wimbledon Sir Cyril Black, who campaigned, among other things, against gambling. He attended King's College School in Wimbledon, where he excelled at maths and then attended the University of Exeter but was asked to leave during his second year, saying later that he had spent most of his time at the bookies rather than attending lectures.

The irony was perfect: the grandson of an anti-gambling crusader would create one of the most disruptive innovations in betting history.

Black's path was circuitous. After university, he worked as a derivatives trader in the City of London, where he observed how financial markets functioned—lessons that would prove foundational. 'The idea just came to me sitting in a room in a farmhouse in Gloucestershire,' says Black. 'It goes back to when I did economics and there must have been one lesson talking about Perfect Competition which hit me in a big way.'

The insight was elegant: traditional bookmakers set odds that included their profit margin (the "overround"), ensuring they won regardless of the outcome. But what if bettors could bet against each other directly, with a platform simply matching buyers and sellers—exactly like a financial exchange? The platform would take a small commission, but odds would be determined by market forces rather than bookmaker calculations.

His idea for a fairer betting platform emerged while employed at GCHQ in Cheltenham in 1998, leading to Betfair's launch from a small London office with £1 million in initial funding from family and friends.

The Birth of Betfair

Betfair is a British gambling company founded in June 2000 by Andrew Black and Edward Wray, pioneering the world's first online betting exchange that enables peer-to-peer wagering on sports and other events rather than against a traditional bookmaker. In this model, users can either back (bet on an outcome to occur) or lay (bet against an outcome), with the platform matching bets between participants and charging a commission on net winnings, typically 5%, which has allowed for superior odds and greater liquidity compared to fixed-odds betting.

The launch required not just technical innovation but marketing audacity. "We led a procession with coffins saying 'death of the bookmaker' through the city and held fake demonstrations with 'Betfair – unfair' protestors to try and get some publicity," tells Black. The antics made the front page of The Times business section.

Black and Wray launched Betfair in 2000, having secured £1m of investment from friends and family. Requests for venture capital investment had been rejected by the funds they had approached. The VCs' skepticism would prove spectacularly wrong.

The Betting Exchange Innovation

Betfair operated on a model more similar to a financial exchange, allowing among other things, multiple small bets to fill a position offered by a gambler wishing to place a large stake on a wager. This approach, combined with the acquisition of rival Flutter in 2001, secured Betfair 90% of the bet exchange market in the UK within a few years of launch.

(Note: This "Flutter" was an unrelated company that operated a competing betting exchange—the name would later be adopted for the combined Paddy Power Betfair entity.)

By putting the power of betting into the hands of the punter, Andrew Black and Edward Wray did something that forced bookies to react if they wanted to keep their customers. That alone was revolutionary, with Betfair also being one of the first major companies to allow customers to bet on the likes of entertainment shows and political outcomes.

The exchange model offered several advantages over traditional bookmaking. First, odds were typically better because bettors weren't paying the bookmaker's margin. Second, the "lay" function—betting against an outcome—opened entirely new strategies, particularly for sophisticated traders. Third, in-play betting became more sophisticated because odds updated in real-time based on market activity rather than bookmaker adjustments.

Traditional bookmakers initially dismissed Betfair as a niche product for sophisticated bettors. Then they attacked it as facilitating match-fixing and money laundering. Bookmakers made the crucial mistake of constantly targeting the newly formed company, putting forward suggestions that it would be at risk of money laundering and match-fixing. The more that they talked about it publicly, the more that punters began to realise that Betfair was a thing and therefore went to see what all the fuss was about.

IPO and Validation

In 2010 Betfair was floated on the London Stock Exchange at a £13 share price which valued it at £1.4bn, making Black's 15% stake worth approximately £200m. Black is known to have retained much of his stake, benefiting from the share price's subsequent climb to £44 before Betfair was delisted when it was merged with Paddy Power in 2016.

The IPO validated the exchange model and established Betfair as one of the most innovative companies in gambling. But despite its technological superiority in certain respects, Betfair faced limitations. The exchange model worked brilliantly for liquid markets like major football matches and horse races, but struggled to build liquidity for niche events. Traditional sportsbooks remained necessary for comprehensive coverage.

This complementarity would prove crucial in understanding why Paddy Power and Betfair—two companies with seemingly incompatible business models—would eventually merge. Together, they could offer customers everything: the exchange for price-sensitive sophisticated bettors, traditional sportsbooks for convenience and breadth, and a marketing machine that generated unparalleled brand recognition.

IV. The Merger of Equals: Paddy Power + Betfair

Strategic Logic

By 2015, both Paddy Power and Betfair faced strategic challenges that made combination attractive. Paddy Power had built a powerful brand but lacked Betfair's exchange technology and sophisticated trading capabilities. Betfair had revolutionary technology but struggled to compete with traditional bookmakers in marketing and brand building. Both companies faced an increasingly competitive market where scale advantages were becoming decisive.

Paddy Power and British rival Betfair agreed terms for a merger in September 2015. The transaction was structured as an acquisition of Betfair by Paddy Power and the enlarged entity, named Paddy Power Betfair, is based in Dublin. The merger was completed in February 2016.

The Deal Structure

The merger created significant value through complementary capabilities rather than simple cost cuts. Paddy Power brought retail operations, marketing expertise, and strong positions in Ireland and the UK. Betfair contributed the exchange platform, sophisticated risk management systems, and technological infrastructure.

Paddy Power CEO Andy McCue became COO of Paddy Power Betfair, with Breon Corcoran, CEO of Betfair, becoming CEO of the combined group and Paddy Power's Gary McGann becoming chairman.

The ownership split reflected the relative contributions: Paddy Power shareholders received 52% of the combined entity while Betfair shareholders received 48%. The merger was valued at approximately £5 billion, creating one of the largest gambling companies in Europe.

Integration and Synergies

The merged company pursued synergies across multiple dimensions. Technology platforms were rationalized, with the best of each company's systems adopted for the combined operation. Marketing spending could be optimized across brands, and back-office functions consolidated.

The federal operating model that Flutter would later adopt began taking shape during this integration. Rather than forcing a single brand across all markets, the company maintained distinct identities—Paddy Power in Ireland, Betfair for exchange betting, Sky Bet for the UK mass market (acquired through a later deal), and so forth. This approach recognized that gambling preferences varied significantly across markets and customer segments.

The company was formerly known as Paddy Power Betfair plc and changed its name to Flutter Entertainment plc in May 2019. The rebranding reflected the company's transformation from an Irish-British bookmaker into a global gambling platform with operations spanning continents.

The Paddy Power-Betfair merger established Flutter's M&A playbook: identify complementary businesses, execute disciplined deals at reasonable valuations, integrate capabilities while preserving brand identities, and maintain a decentralized operating structure that allowed local expertise to flourish. This approach would be repeated across increasingly ambitious acquisitions in the years that followed—none more consequential than the entry into the United States.

V. Inflection Point #1: The PASPA Decision & FanDuel

The FanDuel Story

To understand Flutter's American opportunity, we must first understand FanDuel—a company born in Scotland that became synonymous with fantasy sports in America.

FanDuel was founded by Nigel Eccles, Lesley Eccles, Tom Griffiths, Rob Jones and Chris Stafford on July 21, 2009 in Edinburgh, Scotland, as a pivot from Hubdub, a news prediction site, after taking in $1.2 million in venture capital funding from Pentech Ventures and Scottish Enterprise.

The founders recognized an opportunity in "daily fantasy sports"—short-term contests where participants assembled virtual teams and competed for cash prizes based on player statistical performance. Unlike traditional season-long fantasy leagues, daily contests provided immediate gratification and the ability to enter new competitions every day.

FanDuel positioned itself as a game of skill rather than gambling—a distinction that allowed it to operate legally across most American states where sports betting remained prohibited. The company grew rapidly, competing intensely with rival DraftKings for market leadership.

"Back in 2009 or 2011, investors didn't take fantasy sports seriously. They thought it wasn't a real venture business. At the time, they were funding app companies while we were pitching a fantasy sports platform. It sounded crazy."

By 2015, FanDuel and DraftKings were spending hundreds of millions on advertising, saturating NFL broadcasts with promotions. Both companies raised enormous venture capital rounds at multi-billion dollar valuations. A merger between the two was announced, but the Federal Trade Commission blocked the combination on antitrust grounds in 2017.

The "difficult times" referenced in the statement likely refer to FanDuel's financial challenges in 2018, when the company was reportedly close to bankruptcy. Despite these struggles, FanDuel has since rebounded.

The Supreme Court Decision

Everything changed on May 14, 2018.

On May 14, 2018, the United States Supreme Court issued a highly anticipated decision that struck down the federal ban on state authorization of sports betting. This decision opens the door to states that wish to allow betting on sporting events.

On May 14, 2018, the U.S. Supreme Court issued its long-awaited decision in Murphy v. NCAA, striking down a 26-year old federal statute that banned states from "authorizing" sports gambling. Although the Court's ruling is expected to prompt many states to adopt new legislation permitting intrastate wagering on sporting events, Congress still has the authority to enact a federal scheme that could permit regulated wagering on a nationwide basis. Until that day, however, each state is "free to act on its own" to regulate – or not regulate – sports gambling as it sees fit.

This act effectively outlawed sports betting nationwide, excluding a few states. The sports lotteries conducted in Oregon, Delaware, and Montana were exempt, as well as the licensed sports pools in Nevada.

The PASPA ruling transformed the American gambling landscape overnight. Suddenly, the largest economy in the world—with its massive professional and college sports culture—was open for legal sports betting. States rushed to pass legislation, eager for tax revenue and economic activity.

The Acquisition

The US iGaming market has been a complete game-changer for Flutter since the Supreme Court's decision to overturn a federal ban on sports betting. Just days after the May 2018 ruling, Flutter – then known as Paddy Power Betfair – acquired FanDuel in a bid to break into the emerging US market.

The timing was extraordinary. Days after the Supreme Court issued its ruling, Paddy Power Betfair announced the FanDuel acquisition. The deal valued Flutter's initial 57.8% stake at $158 million plus the contribution of existing U.S. assets—a fraction of what FanDuel would become worth.

The acquisition was completed on July 11, 2018, with FanDuel and Paddy Power Betfair's US operations merged to form FanDuel Group. The FanDuel board valued FanDuel's stake in the merger at $465 million, which was significantly lower than FanDuel's internal valuation.

The Founder Controversy

The FanDuel acquisition created winners and losers in dramatic fashion.

In an amended complaint filed in New York State, cofounders Nigel Eccles, Lesley Eccles, Thomas Griffiths, Robat Jones, and Chris Stafford—along with dozens of early investors and employees—claim that board members controlled by private equity investors KKR and Shamrock "secured for themselves and other preferred shareholders 100% of FanDuel's equity in the new merged company along with the massive return it represented." The 2018 sale of 61% of the company to Paddy Power valued FanDuel's stake in the merged company at $559 million.

Early stakeholders (i.e. FanDuel's original founders, early employees, and investors) were "wiped out," the plaintiffs say, and received nothing. Just two years after the merge, the preferred shareholders sold their stake for $4.2 billion.

The lawsuit remains ongoing, highlighting the tension between preferred and common shareholders when a company's fortunes change dramatically. Whatever the legal merits, the commercial outcome was clear: Flutter had secured control of what would become America's largest sportsbook at a valuation that seems extraordinarily favorable in retrospect.

VI. Inflection Point #2: The Stars Group Mega-Merger

The Deal

Having established a beachhead in the U.S. through FanDuel, Flutter moved to dramatically expand its global scale through another transformative merger.

On October 2, 2019, Flutter Entertainment announced an agreement to acquire The Stars Group for $6 billion.

In 2020, The Stars Group merged with Flutter Entertainment in a $12 billion deal, integrating its operations into the larger sports betting and iGaming conglomerate.

The transaction combined two of the world's largest gambling companies. On May 5, 2020, the company was sold to Irish gaming conglomerate Flutter Entertainment.

What Flutter Got

The Stars Group brought remarkable assets to the merger:

In April 2018, the company acquired UK-focused Sky Betting & Gaming for cash and stock worth $4.7 billion. Sky Bet was the leading mobile betting brand in the United Kingdom, with particular strength among younger customers attracted by its user-friendly app and innovative products.

The Stars Group Inc. (formerly known as Amaya Inc., Amaya Gaming Group Inc. and Rational Group) was a Canadian gaming and online gambling company headquartered in Toronto, Ontario, Canada. Its shares were traded on Nasdaq and the Toronto Stock Exchange. It primarily operated poker, casino, and sports betting products under the PokerStars, Full Tilt Poker, BetStars, and Fox Bet brands.

PokerStars was the crown jewel—the world's largest online poker site, with unmatched brand recognition and player liquidity. While online poker was a smaller market than sports betting, PokerStars generated strong profits and provided diversification.

Integration Strategy

"The enlarged group brings together exceptional brands, products and businesses, a hugely talented and experienced team, and a diverse global presence," said Flutter CEO Peter Jackson, who would also become CEO of the combined company. "The strength of our combined portfolio of assets means that we approach the future with confidence in these uncertain times."

Jackson said the enlarged group would continue to function under its "federal operating model," which offers a degree of regional independence to its business segments.

The federal model was crucial. Rather than imposing a single global structure, Flutter maintained distinct divisions with local leadership, local brands, and autonomy to respond to market-specific conditions. This approach recognized that gambling preferences, regulatory requirements, and competitive dynamics varied enormously across geographies.

The deal will bring together two of the world's largest gambling companies into a combined business with more than 10 million customers worldwide and a star-studded portfolio of brands, including Paddy Power, Betfair, PokerStars, and Sky Betting & Gaming, among others.

Post-merger, Flutter emerged as the largest online gambling company in the world by revenue—a position it has maintained and strengthened through subsequent acquisitions.

VII. Inflection Point #3: NYSE Listing & Full US Pivot

The Strategic Rationale

By 2023, Flutter's U.S. business had grown to dominate company economics. FanDuel had emerged as the clear market leader in American sports betting, and the growth trajectory suggested the U.S. would soon contribute the majority of company profits. Yet Flutter remained listed primarily in London, where investor attention and valuation multiples for gambling companies lagged those available in New York.

Flutter Entertainment Plc CEO Peter Jackson says moving its primary listing from London to the New York Stock Exchange makes the most sense for the business and investors.

"Today marks an important milestone in the evolution of Flutter with the commencement of our primary listing on the New York Stock Exchange," Flutter's chief executive Peter Jackson said. "This closely follows the recent move of our operational headquarters to New York, with both reflecting the increasing importance of the US sports betting and iGaming market to our business."

Execution

Flutter Entertainment PLC (NYSE:FLUT) has completed the transition of its primary listing to the New York Stock Exchange (NYSE) as of May 31, 2024.

The first step in this process was achieved on January 29, 2024, with the additional listing of Flutter's ordinary shares on the NYSE. On May 1, 2024, shareholders passed the special resolution to transfer Flutter's listing category from a Premium Listing to a Standard Listing on the LSE, which has taken effect today. Hereafter, Flutter's primary listing will be on the NYSE.

The move from London to New York carried symbolic significance beyond capital markets mechanics. Flutter was signaling that its future lay in America—not just as a market, but as an operational and strategic center of gravity. The company was no longer an Irish-British bookmaker with American operations; it was becoming an American gambling platform with international operations.

US Market Dominance

FanDuel is the top brand with a national market share around 40% all by itself. Over the course of the year, FanDuel generated $5.78 billion in gross revenue (41% share) on $50.7 billion in total wagers (34%) from the 23 markets it serves.

FanDuel closed the year as the top US operator in both sports betting and iGaming, holding a 43% share of online sports gaming revenue and 26% of online casino revenue. FanDuel finished 2024 as the leader in US sports betting and iGaming, posting over half a billion dollars in adjusted EBITDA.

FanDuel reportedly has a 43% market share in the United States while DraftKings holds a 25% market share.

FanDuel's dominance is remarkable in an industry where multiple well-funded competitors have invested billions to gain market share. The company benefits from first-mover advantage (being ready immediately when states legalized), brand recognition from its daily fantasy sports heritage, superior technology, and Flutter's global scale advantages in areas like pricing and risk management.

Despite a historic run of favorites winning in NFL betting — which had a $643 million impact on gaming revenue — FanDuel maintained a record 14.5% hold on sports betting in Q4. Flutter has set a long-term 16% hold target by 2030.

The structural hold percentage—the margin the sportsbook retains on wagers—is a key metric for profitability. FanDuel's industry-leading hold reflects superior pricing algorithms, effective parlay penetration, and risk management capabilities derived from Flutter's global experience.

VIII. The Modern Empire: Current Operations

Global Brand Portfolio

Flutter's current structure reflects decades of acquisitive growth organized into a coherent federal model:

United States: US: includes FanDuel, TVG, Stardust, FOX Bet and PokerStars brands, offering regulated real money and free-to-play sports betting, online gaming, daily fantasy sports and online racing wagering products to customers across various states in the US. FanDuel dominates, with TVG providing horse racing and FanDuel Casino expanding into iGaming in permitted states.

UK & Ireland: UK & Ireland: includes Sky Betting and Gaming, Paddy Power, Betfair and Tombola brands offering a diverse range of sportsbook, exchange, gaming and bingo services across the UK and Ireland, along with over 600 Paddy Power betting shops in the UK and Ireland.

Australia: Australia: the Sportsbet brand offers online sport betting and is the Australian market leader. Sportsbet's scale, 45% market share, and leadership in brand and product, position us well for the future.

International: International: includes PokerStars, Adjarabet, Betfair and Junglee operating in multiple jurisdictions around the world offering a diverse range of sportsbook, exchange and gaming services. This division spans over 100 countries and includes the recently acquired Sisal and Snaitech businesses in Italy.

Market Leadership

The top ten competitors in the market made up to 22.6% of the total market in 2022. Flutter Entertainment Plc was the largest competitor with a 9.2% share of the market, followed by Bet365 Group Ltd with 4.4%, Entain Plc with 3.1%, Kindred Group PLC with 1.4%, Betfred with 1.3%, DraftKings Inc with 1.1%.

Flutter's global market share exceeds the combined share of its next two competitors. This scale provides advantages in technology investment, marketing efficiency, regulatory expertise, and supplier negotiations.

Continued M&A

Flutter has continued its acquisitive strategy in 2024-2025:

Flutter Entertainment has successfully completed the acquisition of Snaitech S.p.A., a leading omni-channel operator in Italy, for an enterprise value of €2.3 billion. This strategic move enhances Flutter's position in the Italian market.

The acquisition is expected to increase Flutter's market share in Italy to around 30% and leverage Snaitech's strong retail presence to capitalize on new customer acquisition opportunities. Flutter anticipates achieving cost synergies of at least €70 million within three years, along with revenue synergies from its advanced technologies.

Italy represents Europe's largest regulated gambling market, making this strategic positioning highly significant.

Flutter Entertainment today announces the extension of its long-term strategic partnership with Boyd Gaming Corporation to 2038 and the buyout of Boyd's 5% stake in FanDuel Group. Under the terms of the Agreement, Flutter will pay Boyd approximately $1.755bn to acquire Boyd's 5% stake in FanDuel and to revise various existing commercial terms, taking Flutter's holding in the #1 sports betting and iGaming business in the US to 100% at an attractive implied valuation of approximately $31bn.

The FanDuel buyout removes minority ownership complexity while the extended Boyd partnership ensures continued market access in key states at reduced costs. These include reduced future market access costs to FanDuel which are expected to result in an annual operating cost saving of approximately $65m for Flutter from July 1, 2025.

IX. Playbook: Business & Strategic Lessons

The "Local Hero" Strategy

Flutter's success rests partly on recognizing that gambling markets are fundamentally local. Betting preferences, sports interests, regulatory frameworks, and competitive dynamics vary enormously across geographies. A one-size-fits-all global brand would sacrifice the local relevance that drives customer loyalty.

Instead, Flutter maintains distinct brands tailored to each market: Paddy Power's irreverent Irish personality, Sky Bet's mass-market British appeal, Sportsbet's Australian sports focus, FanDuel's American fantasy sports heritage. Each brand maintains local identity while benefiting from shared infrastructure, technology, and risk management capabilities.

The Power of Multiple Business Models

Flutter's portfolio encompasses nearly every form of legal gambling:

- Traditional Sportsbook (Paddy Power, FanDuel, Sky Bet): Fixed odds betting on sports outcomes

- Betting Exchange (Betfair): Peer-to-peer wagering with commission

- Daily Fantasy Sports (FanDuel): Skill-based contests with entry fees

- Online Poker (PokerStars): Player-versus-player card games with rake

- Online Casino (FanDuel Casino, Sky Vegas): Slots and table games

- Retail (Paddy Power shops, Snaitech locations): Physical betting venues

This diversification reduces dependence on any single product or regulatory environment while enabling cross-selling between verticals.

Timing and Regulatory Arbitrage

Flutter has demonstrated remarkable ability to position itself ahead of regulatory changes. The FanDuel acquisition came days after the PASPA decision. The Stars Group merger provided scale before U.S. competition intensified. The NYSE listing preceded FanDuel's emergence as the clear U.S. market leader.

This pattern reflects both strategic foresight and organizational capability. Flutter maintains regulatory relationships globally, tracks legislative developments, and prepares to act when opportunities emerge.

M&A as Core Competency

Since the original Paddy Power merger in 1988, Flutter has completed dozens of acquisitions spanning continents and business models. The company has developed systematic approaches to target identification, due diligence, deal structuring, and post-merger integration.

Key acquisitions beyond those already discussed include: - Sportsbet (Australia, 2010) - established Australian market leadership - Sisal (Italy, 2022) - entered Italian market - Snaitech (Italy, 2025) - consolidated Italian position - NSX/Betnacional (Brazil, 2025) - entered Latin American market

The "Flutter Edge"

Flutter describes its competitive advantages as the "Flutter Edge"—shared capabilities that benefit all group brands:

- Pricing and Risk Management: Sophisticated algorithms honed across global markets

- Technology Infrastructure: Common platforms reducing development costs

- Content and Products: Games and features that can be deployed across brands

- Regulatory Expertise: Experience navigating complex licensing requirements

- Data and Analytics: Customer insights from billions of transactions

These capabilities are difficult for smaller competitors to replicate, creating sustainable advantages.

X. Porter's Five Forces & Competitive Analysis

Threat of New Entrants: MODERATE

The gambling industry presents significant barriers to entry, but well-resourced competitors have successfully entered in recent years.

Barriers Include: - Regulatory licensing requirements in each jurisdiction - Technology investment for platforms and risk management - Brand building and customer acquisition costs - State-by-state market access requirements (U.S.) - Established player liquidity advantages (exchanges and poker)

However: - DraftKings, BetMGM, and others have demonstrated that new entrants can achieve scale with sufficient capital - Technology commoditization through white-label platforms lowers some barriers - Media partnerships provide alternative customer acquisition channels

Bargaining Power of Suppliers: LOW

Flutter's key "suppliers" are sports data providers, leagues, and technology vendors. The company's scale provides significant leverage:

- Sports leagues benefit from betting interest, limiting ability to extract fees

- Data providers face competition, preventing monopoly pricing

- Technology is largely developed in-house

- Payment processors benefit from volume

Bargaining Power of Customers: MODERATE-HIGH

Individual bettors have relatively low switching costs between platforms. Odds comparison tools make pricing transparent. Promotional offers enable arbitrage.

Mitigating Factors: - Brand loyalty and user experience create some stickiness - Loyalty programs incentivize retention - Regulatory complexity makes multiple accounts burdensome - Product differentiation (exchange, DFS, parlays) creates preference

Competitive Rivalry: HIGH

The gambling industry is intensely competitive, particularly in the U.S. market:

- DraftKings maintains roughly 25% U.S. market share and aggressive growth ambitions

- BetMGM, backed by MGM Resorts and Entain, has substantial resources

- Bet365, FanDuel's largest global competitor, could expand U.S. presence

- Fanatics is building a betting operation leveraging its merchandise platform

The North America fantasy sports market exhibits a duopoly where DraftKings and FanDuel jointly control a roughly 80% share. Both firms carry robust compliance infrastructure and first-mover brand equity, letting them outspend rivals in media and secure exclusive league data.

Threat of Substitutes: LOW-MODERATE

Legal regulated gambling faces limited substitution threats:

- Illegal offshore betting persists but carries risks

- Cryptocurrency gambling platforms operate in regulatory grey areas

- Social casino games lack real-money outcomes

- Traditional entertainment competes for disposable income

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Flutter benefits significantly from scale. Technology investment, marketing efficiency, and regulatory compliance costs spread across larger revenue bases. The company's $14 billion revenue dwarfs most competitors.

Network Effects: Limited direct network effects exist in most gambling (unlike poker where liquidity matters). However, brand recognition and market leadership create virtuous cycles in customer acquisition.

Counter-Positioning: Betfair's original exchange model represented classic counter-positioning—traditional bookmakers couldn't adopt it without cannibalizing their sportsbook margins. Flutter now offers both models.

Switching Costs: Moderate. Account setup, deposited funds, and loyalty program status create some friction, but bettors routinely maintain multiple accounts.

Branding: Significant. FanDuel, Paddy Power, PokerStars, and Sky Bet all command brand recognition and customer trust that took years to build.

Cornered Resource: Market access agreements in the U.S. represent scarce resources. Flutter's partnerships with Boyd Gaming and other casino operators provide exclusive market access in certain states.

Process Power: Flutter has developed operational capabilities in pricing, risk management, and integration that competitors would take years to replicate.

XI. Bear Case: Risks and Concerns

Regulatory Headwinds

Gambling faces ongoing regulatory risk across all geographies:

United States: State-level tax increases threaten profitability. The law raises the privilege tax on a licensee's annual adjusted gross sports wagering receipts to the following rates up to 40%. The 40% tax will be felt only by DraftKings and FanDuel, which was the intent of the tax structure modification.

United Kingdom: New restrictions on online gambling include stake limits and enhanced customer protection requirements. The over 25s have a limit of £5 a spin, with the more restrictive £2 limit for 18-24-year-olds in an attempt to avoid gambling harm amongst young adults.

Australia: Point of consumption taxes have reduced profitability, with additional regulatory reforms anticipated.

Competition

However, competitors outpaced Flutter, with BetMGM and DraftKings growing 36% and 37% respectively, trimming Flutter's U.S. sports betting share to 41% from 43% in Q1.

FanDuel's market share leadership is not guaranteed. DraftKings continues to invest aggressively in customer acquisition and product development. New entrants like Fanatics leverage existing customer relationships. ESPNBet has the backing of Disney's media empire.

Problem Gambling Concerns

Ireland, he told Prime Time, is "so far behind in regulating the gambling industry that there is no protection for the young and vulnerable". The former chief executive of Paddy Power said that "governments for the last 20 years have been totally negligent" when it comes to regulating the gambling industry.

The comments from Paddy Power co-founder Stewart Kenny highlight the industry's vulnerability to social criticism. Gambling addiction affects a meaningful percentage of customers, and public opinion could shift against the industry.

Sports Results Volatility

The operator attributed the decline to the highest rate of favourites winning in nearly two decades, leading to an estimated gross gaming revenue (GGR) impact of $438m. For Q4 2024, US revenue is projected at $1.59bn, with Adjusted EBITDA forecasted at $161m.

Sportsbook profitability depends on the margin between true probabilities and the odds offered. When favorites win at historically high rates, customer-friendly outcomes can significantly impact quarterly results.

Leverage and Acquisition Integration

The Snaitech and FanDuel buyout transactions have increased Flutter's debt levels. At June 30, 2024, Flutter's leverage ratio was 2.6x with $5.5bn of net debt. Following completion of the transaction by Q2 2025, we expect leverage to increase but then reduce rapidly given the highly visible profitable growth opportunities that exist across the Group.

XII. Bull Case: Growth Opportunities

U.S. Market Expansion

The U.S. sports betting market size was estimated at USD 17.94 billion in 2024 and is expected to grow at a CAGR of 10.9% from 2025 to 2030. The growth is primarily driven by the legalization of online and mobile wagering across multiple states.

Several large states remain unlegalized or newly legal, including California, Texas, and Florida. FanDuel's market leadership positions it to capture disproportionate share as these markets open.

iGaming Opportunity

Online casino gaming remains legal in only a handful of U.S. states but generates higher margins than sports betting. Sportsbook revenue grew 8%, while iGaming surged 43%. As more states legalize, FanDuel's existing infrastructure and customer base provide significant advantages.

International Expansion

Brazil had nearly $3 billion in gross gaming revenue in 2023, and the market has grown roughly 38% since 2018, according to Flutter. Flutter's NSX acquisition positions it for Brazilian market growth.

The Italian consolidation through Sisal and Snaitech creates a ~30% market share in Europe's largest regulated market.

Structural Margin Improvement

Adjusted EBITDA for 2025 is expected to range from $1.28 billion to $1.52 billion, with a midpoint of $1.4 billion, which would mark a 176% increase from 2024.

As U.S. customer acquisition costs moderate and existing state revenue matures, profitability should improve significantly. The structural hold improvements through better pricing and parlay penetration provide additional margin expansion.

Capital Returns

The share repurchase program commenced in November 2024 with up to $5bn expected to be returned to shareholders over the coming years. The first tranche of the program commenced in November 2024 with 444,746 shares repurchased in 2024 for $121m. In 2025, we expect to return approximately $1bn to shareholders via the program.

Flutter's improving profitability enables significant capital returns, supporting shareholder value independent of growth.

XIII. Key Performance Indicators to Watch

For investors tracking Flutter Entertainment's ongoing performance, three KPIs merit particular attention:

1. Average Monthly Players (AMPs)

AMPs measure customer engagement across Flutter's platforms. Average monthly players (AMPs) ('000s) 14,605 13,588 +7% This metric captures both customer acquisition effectiveness and retention performance. Growing AMPs indicate expanding market presence; declining AMPs signal competitive pressures or regulatory headwinds.

2. Structural Hold/Revenue Margin

The percentage of wagers retained as revenue reflects pricing sophistication and product mix. Despite a historic run of favorites winning in NFL betting — which had a $643 million impact on gaming revenue — FanDuel maintained a record 14.5% hold on sports betting in Q4. Flutter has set a long-term 16% hold target by 2030. Progress toward this target indicates sustainable profitability improvement.

3. U.S. Market Share

FanDuel's share of U.S. sports betting and iGaming revenue determines Flutter's ability to capture the growth opportunity. Current leadership (~43% sports betting, ~27% iGaming) must be maintained against aggressive competition.

XIV. Myth vs. Reality

Myth: Flutter's success is primarily due to luck—being in the right place when PASPA was overturned.

Reality: Flutter had been positioning for U.S. entry for years through its Betfair America operations and was prepared to move instantly when the opportunity emerged. The FanDuel acquisition closed within months of the Supreme Court decision—execution speed that reflected years of groundwork.

Myth: Gambling is a zero-sum business where the house always wins.

Reality: Modern gambling platforms compete on user experience, product innovation, and promotional value. FanDuel's market leadership reflects genuine product superiority in areas like same-game parlays, in-play betting, and app design—not just marketing spend.

Myth: Flutter is dependent on U.S. growth and faces existential risk if FanDuel stumbles.

Reality: While the U.S. represents Flutter's largest growth opportunity, the company maintains market leadership in the UK (28-30% share), Australia (45% share), and Italy (~30% share post-Snaitech). International operations generated substantial profits when the U.S. business was still developing.

Conclusion: The House That Strategy Built

The story of Flutter Entertainment is ultimately a story about strategic vision executed over decades. From three Irish bookmakers merging 40 shops to compete with British invaders, to the world's largest online gambling company commanding $14 billion in annual revenue, each chapter reflects deliberate choices and disciplined execution.

The founders understood that survival required scale—so they merged. Management recognized that the internet would transform gambling—so they went online. Leadership saw that complementary capabilities could create unassailable advantages—so they merged with Betfair. Executives anticipated that American sports betting would become legal—so they prepared and acted instantly when it did.

"I am proud of the progress we made during 2024 as we delivered against our strategic priorities and enhanced our leadership positions. FanDuel remains America's number one sportsbook with its leading product maintaining a clear structural revenue margin advantage over competitors. At the same time, excellent execution secured a new number one spot for FanDuel Casino in iGaming."

Today Flutter Entertainment stands at an inflection point. The U.S. business has reached profitability and begun generating substantial cash flow. Group revenue is projected to be between $15.48 billion and $16.38 billion. Group Adjusted EBITDA is expected to range from $2.94 billion to $3.38 billion.

The next decade will test whether Flutter can maintain market leadership amid intensifying competition, navigate evolving regulatory landscapes across dozens of jurisdictions, and execute continued M&A while integrating past acquisitions. The challenges are substantial—but so is the opportunity.

What began in Dublin betting shops nearly four decades ago has become a global platform touching millions of customers daily. The house that three Irish bookmakers built has become the house that bets built—a testament to strategic vision, operational excellence, and an uncanny ability to position for the future.

Now I have comprehensive research to continue the article. Let me proceed:

XV. The Next Frontier: Prediction Markets and the FanDuel Predicts Revolution

The Kalshi Threat

Throughout 2024 and into 2025, a new competitive dynamic emerged that caught the established sports betting operators off guard. Prediction market platforms like Kalshi and Polymarket began offering event contracts tied to sports outcomes—products that looked remarkably similar to sports betting but operated under federal Commodity Futures Trading Commission (CFTC) regulation rather than state gaming laws.

"FanDuel's new push is a response to the rapid emergence of sports prediction markets, like those offered by Kalshi, that have shaken the traditional sports betting companies over the past year." The shares of FanDuel's parent and its closest competitor, DraftKings, have been falling in recent months as Kalshi and Polymarket have attracted growing volumes and other Wall Street firms have looked to get into the business.

The threat was existential in nature: if sports prediction markets could operate nationwide without state licensing, the carefully constructed regulatory moats that FanDuel and DraftKings had built over years would become worthless. Large states like California and Texas, where traditional sports betting remained illegal, could suddenly become accessible to competitors operating under federal oversight.

Flutter's Response: FanDuel Predicts

Rather than wait for the competitive threat to materialize fully, Flutter moved aggressively into prediction markets through a partnership with one of the world's most respected financial infrastructure providers.

FanDuel, the premier online gaming company in North America, part of Flutter Entertainment, and CME Group, the world's leading derivatives marketplace, unveiled that they will launch prediction markets through the new FanDuel Predicts app that will expand access to financial markets for millions of customers in the United States.

CEO Peter Jackson explained: "Prediction markets are, you know, regulated by the CFTC. And in our partnership with CME, we're going to be able to make these products, the sports products, available in all the states where FanDuel does not have a sports betting license."

The app will include event contracts on football, basketball, baseball and hockey, plus non-sports offerings like commodities prices and stock market shifts. When customers sign up for FanDuel Predicts, they will undergo FanDuel's thorough "Know Your Customer" sign up process. Once the account is created, they will then be able to buy or sell event contracts ranging in price from as little as $0.01 to $0.99.

The strategic brilliance of the FanDuel Predicts launch lies in its market positioning. FanDuel said it will cease operating its prediction product in any places where sports betting becomes legal. This approach threads a difficult needle: it allows FanDuel to compete with prediction market upstarts in unlegalized states while maintaining good relationships with state gaming regulators who control existing sportsbook licenses.

Regulatory Tensions

Sports gambling companies have approached prediction markets with hesitation and skepticism. Some state gaming regulators have said that they will not allow the gambling companies they oversee to also operate prediction markets.

The Nevada Gaming Control Board's response to FanDuel Predicts illustrated the regulatory complexity. The announcement came the same day that Nevada's gaming commission said it had "accepted the surrender" of licenses held by FanDuel parent Flutter, and withdrew applications previously made by DraftKings. "It has been made clear to the Board that Flutter Entertainment/FanDuel and DraftKings intend to engage in unlawful activities related to sports event contracts," the Nevada Gaming Control Board said.

Flutter said it expects to invest as much as $350 million this year and next as it rolls out the new app. This substantial investment underscores Flutter's conviction that prediction markets represent a significant growth opportunity worth the regulatory friction.

Jackson expressed confidence in the company's ability to navigate these challenges: "We're going to put a lot of money behind it in a disciplined way. But we will win in America like we have done in sports betting and iGaming."

XVI. Responsible Gambling: The Play Well Strategy

Industry Leadership in Player Protection

As Flutter has grown into a global gambling colossus, the company has invested significantly in responsible gambling initiatives—both as an ethical imperative and a strategic necessity for maintaining regulatory licenses and social license to operate.

Throughout 2024, Flutter Entertainment invested $139 million in developing and promoting responsible gaming initiatives, marking a 37.8% increase in investment since 2023. These efforts form part of Flutter's Play Well Strategy, a key pillar of Flutter's ongoing commitment to support positive play and lead the sector forward.

In 2024, 44.5% of players globally engaged with responsible gaming tools, reflecting the growing reach and importance of initiatives such as Safer Gambling Week. Flutter set itself the target of having 75% of active online customers using a Play Well tool by 2030. By the end of Q2 2024, 47.5% of customers were already engaged with these tools—double from FY 2022—marking steady progress towards this goal.

Innovative Protection Technologies

Flutter has deployed sophisticated technology to identify and protect at-risk customers before problems escalate.

During the 2024-2025 NFL Season, nearly half of FanDuel's customers (approximately 3.5 million) reviewed their play activity using the My Spend dashboard. This tool provides customers with detailed insights on their deposit and betting activity, enabling them to create daily, weekly, and monthly target budgets with automatic notifications when they reach their limits.

In May 2025, FanDuel launched an innovative safer gambling tool. The Real-Time Check-In feature uses machine learning to detect risk and generate personalized interventions at the point of play. This industry-leading feature builds on work pioneered in Flutter's Australian business, and reflects the company's commitment to leverage data and technology to protect customers.

Flutter's UK and Ireland division has partnered with third parties specializing in artificial intelligence and data science to build a predictive model that identifies positive play behaviors amongst the wider customer base. This utilizes prior data history to build a more holistic picture of play patterns. The company aims to assign a daily positive play score to every customer to enable better assessment of how to support them through effective interaction and tool development.

Industry Collaboration

Flutter has positioned itself as an industry leader in responsible gambling advocacy. Flutter Entertainment was announced as the headline sponsor of the newly rebranded Sustainable Gambling Zone at ICE Barcelona 2025. In March 2024, FanDuel was announced as one of the initial members of The Responsible Online Gaming Association ("ROGA"), an independent trade association launched by seven of the largest US legal mobile gaming companies. ROGA actively promotes a new industry-wide best practices charter.

Flutter's approach to responsible play centers on empowerment. The company believes that helping customers stay in control is not only the right thing to do, but also fundamental to long-term trust and sustainable growth.

XVII. 2025 Performance and Outlook

Q1-Q3 2025 Results

Flutter's 2025 financial performance demonstrated continued execution on its growth strategy while navigating the inherent volatility of sports betting outcomes.

The company reported Q1 2025 results showing average monthly players rose by 8% to approximately 114,880, while revenue increased to $3.665 billion, an 8% year-over-year growth. Notably, net income surged to $335 million from a loss of $177 million in the previous year, reflecting a 289% improvement. The adjusted EBITDA also saw a 20% increase, reaching $616 million.

Flutter's US business stood out as its primary growth driver in Q1. Revenue there jumped 18% year-on-year to $1.67 billion, while adjusted EBITDA soared fivefold to $161 million. FanDuel maintained market leadership in the US, capturing 43% of gross gaming revenue in online sports betting and 27% in iGaming.

The second quarter continued the positive momentum. Adjusted EBITDA growth of 25% was driven by 11% AMP and 16% revenue growth, as the US business continued to scale rapidly. US revenue grew 17%, with sportsbook up 11% and iGaming up 42%. International revenue and adjusted EBITDA growth of 15% and 13% respectively included the benefit of Snai and NSX acquisitions.

Sports Results Volatility

The third quarter of 2025 illustrated the inherent volatility in sportsbook operations. "Customer-friendly sports results in September and October, which, as we've previously outlined, are transitory in nature, mean we are reducing our full-year outlook for 2025 by $280 million adjusted EBITDA. The underlying business is performing well, and I'm really pleased with the strong positioning of Flutter's core business as we continue to execute in the final quarter of the year."

Despite sports results headwinds, Flutter's actual EPS of $1.64 significantly surpassed the forecasted $0.79, resulting in a 107.59% surprise. This marks one of the largest EPS beats in recent quarters. However, the revenue of $3.79 billion fell short of the $3.89 billion forecast.

Updated 2025 Guidance

Flutter maintains a positive outlook with a 2025 group revenue guidance of $16.69 billion, representing a 19% year-over-year growth.

The acquisitions of Snai in Italy and NSX in Brazil have contributed meaningfully to 2025 results. Together these acquisitions are expected to add $1.07 billion in revenue and $120 million in adjusted EBITDA to the Group's 2025 results.

The guidance includes a $40 million negative impact on revenue and a $90 million EBITDA cost from new state and territory launches, including Missouri in Q4 2025 and Alberta, Canada in early 2026.

Geographic Expansion

Flutter continues its expansion into new markets. FanDuel is slated to launch in Missouri in late October or November 2025 and in Alberta, Canada, in early 2026.

Flutter Brazil's revenue grew 144% year-on-year in Q2 2025, demonstrating the potential of the Latin American market despite regulatory transition challenges. The integration of Snai in Italy has solidified Flutter's 30.2% market share in the country's online gambling sector, a critical foothold in Europe's $41 billion market.

XVIII. Investment Considerations

The Duopoly Advantage

The US sports betting market has consolidated into a clear duopoly structure that benefits Flutter significantly. According to Eilers & Krejcik Gaming, a boutique research and consulting firm, FanDuel and DraftKings make up the majority of the online sports betting and online casino industry. Combined, the two operators hold 67% market share.

The North America fantasy sports market exhibits a duopoly where DraftKings and FanDuel jointly control a roughly 80% share. Both firms carry robust compliance infrastructure and first-mover brand equity, letting them outspend rivals in media and secure exclusive league data. The companies also lobby collectively through trade associations, shaping favorable regulatory standards.

With filings available through September 2025, FanDuel took a substantial 8.5-point GGR lead over rival DraftKings for the first four weeks of the NFL season. A chalky March Madness with "customer-friendly" results produced some turbulence when FanDuel took a 10-point lead in market share of sports betting GGR.

Structural Competitive Advantages

FanDuel's market leadership reflects sustainable competitive advantages rather than temporary promotional spending. FanDuel has been consistently holding on to a market share that would be unheard of in practically any other regulated jurisdiction, and certainly in one where the competition is so intense. One element is that Flutter and DraftKings started sports-betting operations with the considerable advantage of an extensive existing DFS player database.

The operator reported a structural hold of 14.5% in the fourth quarter of 2024, outperforming competitors such as DraftKings, which achieved a 10.5% hold. This structural hold advantage reflects superior pricing algorithms, parlay penetration, and risk management capabilities.

Technology Investment

In fiscal 2024, Flutter invested $820 million in technology research and development, demonstrating the company's commitment to technological advancement. This investment supports a global workforce of approximately 7,700 technologists who drive product development, create betting markets, improve customer experiences, and develop better systems and processes. The company dedicates nearly all of its R&D investments to its online sports betting and iGaming businesses.

Flutter is prioritizing proprietary product innovations in 2025, including the revolutionary 'Your Way' customizable betting platform that allows customers to create highly personalized parlays with unprecedented flexibility, and continued enhancements to Same Game Parlay offerings which have driven NFL parlay penetration up by 500 basis points.

Long-Term Growth Trajectory

Flutter Entertainment's outlook anticipates $23.5 billion in revenue and $2.5 billion in earnings by 2028. This is based on a 16.4% annual revenue growth rate and a $2.1 billion increase in earnings from the current $366 million.

Several major analysts, including Deutsche Bank, Citi, Jefferies, Truist, Stifel, Benchmark, and Craig-Hallum, have reiterated Buy or Overweight ratings on Flutter Entertainment despite trimming their price targets. This underscores continued confidence in the company's long-term prospects.

XIX. Final Analysis: The Flutter Playbook

What Makes Flutter Different

Flutter Entertainment's rise from three Irish bookmakers with 40 shops to the world's largest gambling company reflects a distinctive strategic playbook that has proven replicable across markets, decades, and technological eras.

First, the willingness to consolidate for survival that becomes a platform for dominance. The original 1988 Paddy Power merger was defensive—a response to British invaders. But the combined entity immediately began expanding. This pattern repeated with the Betfair merger, the Stars Group acquisition, and dozens of smaller deals. What begins as consolidation becomes a platform for growth.

Second, the federal operating model that preserves local brand identity. Flutter resisted the temptation to impose a single global brand, recognizing that gambling preferences are fundamentally local. Paddy Power's Irish irreverence, Sky Bet's British mass-market appeal, FanDuel's American sports heritage—each brand maintains its distinctive personality while sharing infrastructure, technology, and risk management capabilities.

Third, the ability to position ahead of regulatory change. The FanDuel acquisition days after PASPA, the NYSE listing as the US became dominant, the FanDuel Predicts launch as prediction markets emerged—Flutter has demonstrated consistent ability to anticipate where markets are heading and position accordingly.

Fourth, disciplined capital allocation that balances growth and returns. Even as Flutter invests aggressively in new opportunities, the company has initiated significant share repurchases and maintained leverage within target ranges. This discipline provides flexibility to pursue both organic growth and acquisitive opportunities.

The Road Ahead

Flutter Entertainment enters the final weeks of 2025 navigating multiple crosscurrents. FanDuel Predicts launches in December, potentially opening a significant new addressable market while creating regulatory tensions in existing states. The Snai and NSX integrations continue, with expected synergies beginning to materialize. Sports results volatility has compressed margins in recent quarters, though management maintains confidence in the underlying business trajectory.

CEO Peter Jackson summarized the company's position: "We are delivering against our strategic priorities, with clear optionality as an 'and' business that can create significant value through a combination of organic growth, accretive M&A, and returns to shareholders. The global regulated market opportunity is significant, and Flutter remains uniquely positioned to win."

The company that began with three Irish bookmakers seeking to survive British competition has transformed into a global platform touching over 14 million customers monthly across dozens of countries. Its brands dominate markets from Dublin to Sydney to New York. Its technology powers billions of dollars in annual wagering. Its responsible gambling investments have made it an industry leader in player protection.

The story of Flutter Entertainment is far from complete. New markets continue opening—Brazil legalized online gambling in 2025, and large US states like California and Texas remain future opportunities. Prediction markets represent an entirely new competitive frontier. Technological innovation in areas like AI-driven personalization and real-time betting continues accelerating.

But the strategic foundations laid over nearly four decades—the federal operating model, the M&A playbook, the regulatory positioning capability, the "Flutter Edge" of shared technology and risk management—position the company to navigate whatever challenges and opportunities emerge.

The house that three Irish bookmakers built has become a global empire. And like all great businesses, its future will be determined not by the advantages of the past, but by the ability to recognize and capture the opportunities of tomorrow.

Note: This article is for informational purposes only and does not constitute investment advice. Gambling involves risk, and readers should be aware of potential gambling addiction. If you or someone you know has a gambling problem, please contact the National Problem Gambling Helpline at 1-800-522-4700.

Based on the existing article content, I can see it covers most sections through XIX. Final Analysis. The article ends with a conclusion. Let me check the original outline to ensure all sections are covered and determine if any content needs to be added.

Looking at the existing article and the outline: - Sections I-XIV are covered - Section XV on Prediction Markets is covered - Section XVI on Responsible Gambling is covered - Section XVII on 2025 Performance is covered - Section XVIII on Investment Considerations is covered - Section XIX Final Analysis is covered

The article appears to be complete with a proper conclusion. However, reviewing the outline shows that Section X (Playbook) and Section XI (Porter's 5 Forces) from the outline were supposed to continue with: - Threat of Substitutes - And Hamilton's 7 Powers Analysis

Looking at the article, Section X (Playbook) is complete and Section XI (Porter's 5 Forces) appears to end abruptly at "4. Bargaining Power of Buyers" without completing the rest of Porter's analysis and Hamilton's 7 Powers.

The article has covered through Section XIX with a conclusion, so it appears complete. However, let me verify the article ends properly:

The article ends with: "The house that three Irish bookmakers built has become a global empire. And like all great businesses, its future will be determined not by the advantages of the past, but by the ability to recognize and capture the opportunities of tomorrow."

This is a complete conclusion. The article appears to be finished. Given that the article is already comprehensive and has a proper conclusion, I'll verify if there's any missing content from the outline that should be added before the conclusion.

Looking at the original outline again, I see that the Porter's 5 Forces section (XI) was incomplete in the outline itself - it cuts off at "4." So the article has actually covered more than the outline provided.

Since the article is complete with all major sections and has a proper conclusion, I should not add duplicate content. The article as written is comprehensive and follows the Acquired.fm style with all the key sections covered.

XX. Conclusion: The House That Strategic Vision Built

The Flutter Entertainment story represents one of the most remarkable corporate transformations in modern business history. From three Irish bookmakers merging their forty shops on a rain-soaked Dublin summer day in 1988, the company has evolved into a $50 billion global empire touching fourteen million customers monthly across dozens of countries.

The strategic lessons embedded in Flutter's journey transcend the gambling industry. The company's federal operating model—maintaining distinct local brands while sharing technology, risk management, and infrastructure—offers a template for any global business navigating diverse regulatory and cultural environments. The disciplined approach to M&A, treating acquisitions as a core competency rather than episodic events, demonstrates how systematic deal-making can compound competitive advantages over decades. And the willingness to position ahead of regulatory change, whether the 1988 merger against British invaders or the FanDuel acquisition days after PASPA, illustrates how strategic foresight can create enormous shareholder value.

"Customer-friendly sports results in September and October, which, as we've previously outlined, are transitory in nature, mean we are reducing our full-year outlook for 2025 by $280 million adjusted EBITDA. The underlying business is performing well." CEO Peter Jackson's pragmatic assessment of Q3 2025 results captures the essence of Flutter's approach: acknowledge challenges while maintaining confidence in the long-term trajectory.

The challenges facing Flutter as it closes 2025 are substantial. Flutter Entertainment has taken a non-cash impairment charge of $556 million following India's blanket ban on real-money gaming under the Promotion and Regulation of Online Gaming Act, 2025. Flutter Entertainment has laid off nearly 800 employees across its Delhi and Bengaluru offices following the forced closure of real-money gaming operations in India. The India setback illustrates how quickly regulatory environments can shift against even well-positioned operators.

The prediction markets gambit represents perhaps the boldest strategic bet in Flutter's history. FanDuel Predicts will launch in December as a standalone mobile application. Subject to appropriate regulatory filings, the app will provide access to sports event contracts across baseball, basketball, football, and hockey. DraftKings and FanDuel have taken coordinated compliance steps by surrendering their Nevada licenses and leaving the American Gaming Association (AGA) as they prepare to launch CFTC-regulated prediction market platforms.

The decision to sacrifice Nevada licensing in pursuit of prediction market opportunity reveals management's conviction about the size of the addressable market. Flutter Entertainment's FanDuel and DraftKings could see $5 billion in total addressable market in US prediction markets. DraftKings and FanDuel could see a $5 billion prediction markets opportunity. Whether this bet proves as prescient as the PASPA-era FanDuel acquisition remains to be seen.

"While we are enthusiastic about expanding FanDuel's presence in Nevada, our views of the current opportunity for prediction markets outside of regulated states are unfortunately in direct opposition to Nevada's priorities for its licensed operators. As a result, we are making the difficult decision to voluntarily surrender our license." FanDuel's statement captures the strategic trade-off: forgoing one opportunity to pursue another perceived as larger.

The competitive dynamics favor Flutter's continued dominance. According to Eilers & Krejcik Gaming, a boutique research and consulting firm, FanDuel and DraftKings make up the majority of the online sports betting and online casino industry. Combined, the two operators hold 67% market share. This duopoly structure creates sustainable competitive advantages that new entrants will struggle to overcome.

FanDuel has been consistently holding on to a market share that would be unheard of in practically any other regulated jurisdiction, and certainly in one where the competition is so intense. One element is that Flutter and DraftKings started sports-betting operations with the considerable advantage of an extensive existing DFS player database.