Millicom (TIGO): The Emerging Markets Telecom Pioneer That Built Latin America's Digital Highways

Introduction: A Swedish-American Heritage, A French Future

On a February morning in 2025, Millicom's CEO Marcelo Benitez stood before investors to deliver news that encapsulated three decades of transformation. "In 2024, we successfully completed our restructuring program, and strengthened the company's financial position so we can continue to focus on our purpose: building digital highways, connecting people, and developing our communities." Behind those words lay one of the most remarkable stories in global telecommunications—a company that helped birth Orange UK, abandoned three continents, and is now being reshaped by one of Europe's most aggressive telecom dealmakers.

Millicom's full-year 2024 performance showed revenue of $5.80 billion, up 2.5% year-on-year, with operating profit increasing 62.5% to $1.34 billion. Net income reached $253 million, while EBITDA grew 16.9% to $2.47 billion. These numbers, while impressive, only tell part of the story. The central question that draws us to Millicom isn't about the financials—it's about how a Swedish-American joint venture that helped create one of Europe's most iconic telecom brands became the dominant player across Central America's telecom landscape, and what French billionaire Xavier Niel sees in it that others missed.

Millicom International Cellular SA is a Luxembourgish fixed line and mobile telecommunications services provider operating in Latin America under the Tigo brand. Its main shareholder is Xavier Niel, a French billionaire who owns 40% of the company. As of March 31, 2025, Millicom operating subsidiaries and joint ventures employed more than 14,000 people and provided mobile services to approximately 46 million customers, with a cable footprint of more than 14 million homes passed.

This is the story of strategic pivots executed across decades—from a global footprint spanning 21 countries to a focused Latin American powerhouse. It's a tale of founders who saw mobile telephony's potential when 92% of humanity had no phone service, of corporate battles between Swedish industrial dynasties, and of a French disruptor who may finally bring Millicom into the next phase of its evolution.

Origins: The Unlikely Pioneers of Mobile Telephony (1979–1990)

Two Threads That Would Become One

The story of Millicom begins not in one place, but in two—a Swedish industrial empire searching for reinvention and an American startup betting on a technology most considered science fiction.

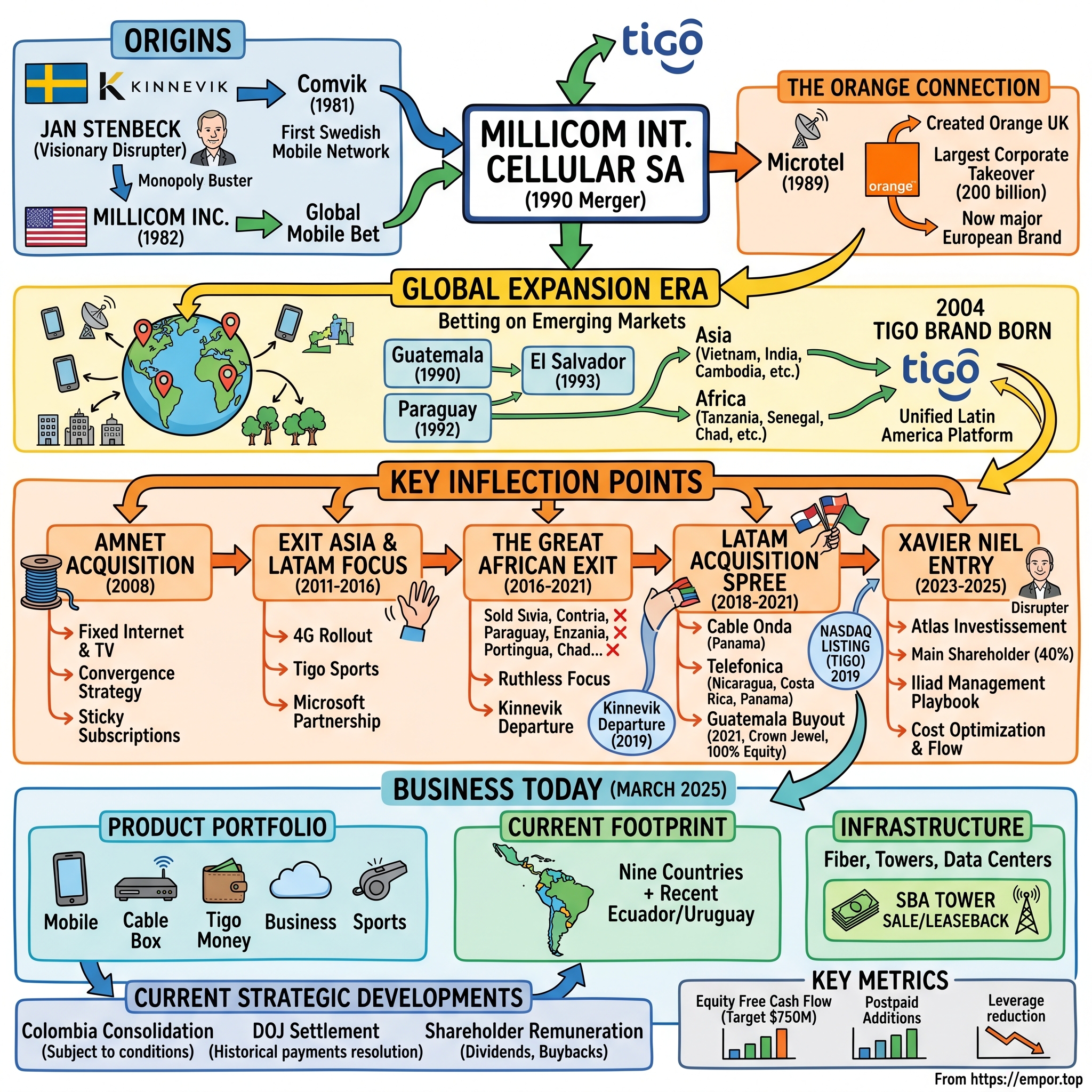

In 1979, Sweden's industrial landscape was dominated by century-old companies mining iron, cutting timber, and rolling steel. After his father Hugo Stenbeck Sr. died, Jan Stenbeck returned to Sweden and gained control over Investment AB Kinnevik after a bitter feud with his siblings. He came to change the focus of the investment company away from traditional Swedish industries, such as pulp and paper industry and steel manufacturing, towards media and telecommunication.

Jan Stenbeck was no ordinary Swedish industrialist. Born on 14 November 1942 in Stockholm, the youngest son of business lawyer Hugo Stenbeck and his wife Märtha, he passed the studentexamen at Östra Real in Stockholm and received a Candidate of Law degree from Uppsala University and a Master of Business Administration degree from Harvard Business School in 1970. His time at Morgan Stanley in New York had exposed him to American entrepreneurial culture—a world away from Sweden's consensus-driven corporate establishment.

Jan Hugo Robert Arne Stenbeck was a Swedish financier, media proprietor, and business disruptor who inherited and expanded the family-controlled Kinnevik conglomerate from traditional industries like forestry and steel into a telecommunications and broadcasting powerhouse. Assuming control of Kinnevik in 1976 following his father's death, Stenbeck aggressively pursued diversification.

In 1981, Stenbeck made his first audacious move. In 1981, Comvik, originally established to challenge the state-sanctioned telecommunications monopoly held by Televerket, marked a pivotal moment in Swedish telecommunication history. The visionary Jan Stenbeck, through Investment AB Kinnevik, initiated a strategy to disrupt existing monopolies. Comvik successfully launched Sweden's first automatic analogue mobile telephony network in 1981, three months ahead of Televerket's NMT network.

This wasn't just business innovation—it was regulatory warfare. Comvik launched Sweden's second cellular telephone network on December 1, 1981, circumventing Televerket's fixed-line monopoly by leveraging radio-based mobile technology, which incurred substantial losses throughout the decade but was sustained by Stenbeck's family capital and strategic investments. By employing political lobbying, media campaigns framing the effort as a "David versus Goliath" battle, and enlisting legal and technical experts, Stenbeck pressured policymakers.

The American Thread

Across the Atlantic, another pioneering effort was underway. After two years of planning, the company began operations when the founders completed a $131,000 share purchase in May 1982. The firm took over paging company Meta Systems in October 1982 and then raised $9 million in its first round of financing, managed by chief executive officer Orhan Sadik-Khan and Kevin Kimberlin. Since 92% of the world population had no phone service at the time, Millicom promoted mobile technology on a global basis.

The American Millicom Incorporated operated with a different thesis: while Western markets had established telecommunications infrastructure, emerging markets had nothing. Mobile technology could leapfrog decades of fixed-line development. To do this, Millicom created joint-ventures with local and strategic partners. On 13 December 1982, a joint-venture with Racal Electronics was awarded a cellular license for the United Kingdom.

The Merger and the Orange Connection

The convergence of these two threads created something remarkable. Millicom International Cellular SA was established on 14 December 1990, by Shelby Bryan, Jan Stenbeck, Telma Sosa, and Olvin Galdamez, combining the cellular telephone properties owned by Industriförvaltnings AB Kinnevik and Millicom Incorporated.

But before this merger, the American Millicom had already planted seeds that would grow into one of Europe's largest telecom companies. The inception of the Orange brand occurred in 1990 in the United Kingdom with the formation of Microtel Communications, a consortium initially formed by Pactel Corporation (American), British Aerospace, Millicom and Matra (French).

In December 1989, Millicom set up Microtel Communications Ltd. by teaming up with Pacific Telesis and British Aerospace. Microtel was awarded a personal communication network (PCN) license to compete with Vodafone in the United Kingdom, a service launched on 28 April 1994 under its brand name, Orange. This venture was acquired in October 1999, at which time Orange and its new parent, Mannesmann, were in turn both taken over by Vodafone. At a value of $202 billion, the takeover of Mannesmann by Vodafone was the largest transaction in corporate history.

This is a remarkable piece of telecom history that few remember: Millicom's founders helped create what became Orange—one of Europe's largest telecom companies. Orange (formerly Microtel) was then sold to France Telecom, which subsequently changed its corporate name to Orange. The brand that Millicom helped birth in the UK now operates across dozens of countries with hundreds of millions of customers.

For investors studying Millicom today, this origin story reveals something fundamental about the company's DNA: these were pioneers who understood that telecommunications infrastructure creates value over decades, not quarters. They saw opportunity in markets others ignored. That strategic vision would define Millicom's trajectory through the next three decades.

The Global Expansion Era: Betting on Emerging Markets (1990–2004)

The Strategy: Go Where Others Won't

By 1990, Millicom International Cellular SA existed as a distinct entity, and its founders faced a pivotal choice. The developed world's mobile markets were becoming crowded and capital-intensive. The emerging world remained largely untouched.

They chose the frontier.

In 2000, Millicom started investing in three continents: Asia, Africa, and Latin America. The logic was elegant: in developed markets, mobile was replacing fixed-line infrastructure. In emerging markets, mobile could be the first and only telecommunications infrastructure millions of people would ever use. The economics were radically different—lower customer acquisition costs, simpler networks, and populations hungry for connectivity.

The strategy worked. By 2001, Millicom had assembled a global empire. The company's operational footprint peaked that year when it boasted a presence in 21 different countries across three continents. This was frontier capitalism at its most ambitious.

Building the Portfolio

The Latin American foundation was laid early and deep. Millicom has operated in Guatemala since 1990. It owns a 100% equity interest in the operation after acquiring the remaining 45% stake from its local joint venture partner in a $2.2 billion deal in November 2021. Guatemala would eventually become the crown jewel of the entire Millicom operation.

Millicom provides mobile and cable and other fixed services in El Salvador through Telemovil, which is wholly owned by Millicom. Tigo El Salvador has operated in the country since 1993. Paraguay operations began in 1992, creating a footprint that stretched across Central and South America.

The company's geographic diversity was extraordinary. Millicom completed the sale of its Asian business segment in 2011 with the sale of Laos. It previously operated in Cambodia, India, Indonesia, Pakistan, Philippines, Sri Lanka, and Vietnam. In Africa, operations spanned from Ghana to Rwanda, from Senegal to Tanzania.

This was classic emerging market telecommunications strategy: establish early positions in fast-growing markets, build infrastructure when costs are low, and capture decades of growth as populations urbanize and digitize. The approach required patience and tolerance for political risk, currency volatility, and regulatory uncertainty—characteristics that would eventually lead Millicom to make some of the most consequential strategic pivots in telecom history.

The Birth of the Tigo Brand

By 2004, Millicom's scattered operations needed cohesion. In 2004, Millicom conceptualized the TIGO brand. The rebranding effort was more than cosmetic. The Tigo brand launched in 2004, replacing former national brands COMCEL and Amigo de COMCEL.

The Tigo name—simple, memorable, easily pronounced across languages—would become one of the most recognized telecommunications brands in Latin America. The standardized branding enabled marketing efficiencies, cross-border operational synergies, and a unified customer experience that proved particularly valuable in Central America's interconnected economies.

For investors, the 2004 Tigo launch signals an important maturation point. The company had moved beyond opportunistic market entry toward building an integrated, brand-driven telecommunications platform. This transition from asset collection to brand building would define the next phase of Millicom's evolution.

INFLECTION POINT #1: The Cable Bet—AMNET Acquisition (2008)

The Strategic Pivot from Mobile-Only

In boardrooms across the telecom industry during 2007-2008, a fierce debate raged: was the future mobile-only, or would convergence—combining mobile, fixed-line, broadband, and video—prove essential? Millicom placed its bet.

In 2008, Millicom acquired AMNET for fixed Internet and TV services, leading to the company's formal cable business entrance. The acquisition, valued at approximately $510 million, transformed Millicom's strategic profile.

AMNET operated across Central America as a broadband, cable TV, and fixed telephony provider. In El Salvador and Honduras, it provided all three services. In Costa Rica, the company delivered broadband and cable TV. In Nicaragua and Guatemala, it focused on corporate data services.

Why This Mattered

The AMNET acquisition represented Millicom's recognition of a fundamental truth about telecommunications economics: mobile services generate revenue but suffer from intense price competition and customer churn. Fixed-line services—particularly broadband and pay-TV—create sticky subscription relationships with predictable recurring revenue.

This was the foundation for Millicom's "convergence" strategy—combining mobile and fixed services to create bundled offerings that would reduce churn, increase average revenue per user, and create infrastructure-based competitive moats. A customer with mobile, broadband, and TV services from Tigo is far less likely to switch than a customer with just prepaid mobile.

The deal also addressed a fundamental challenge in emerging markets: while mobile voice and SMS drove early growth, the smartphone revolution was approaching. Customers would increasingly want data—and lots of it. Fixed broadband infrastructure would prove essential for backhaul and for serving enterprise customers.

Technology Investments

Millicom didn't just acquire infrastructure—it invested aggressively in network modernization. Millicom launched 3G service in August 2008 in Bolivia and in September 2008 in Guatemala, Honduras, Paraguay, and El Salvador. These upgrades positioned the company to capture the coming mobile data explosion.

The AMNET acquisition established a playbook that Millicom would repeat across Latin America: acquire fixed infrastructure assets, integrate them with mobile operations, and create convergent offerings that competitors couldn't match. This strategy would prove essential as Millicom evolved from a mobile operator into a comprehensive telecommunications provider.

INFLECTION POINT #2: Exit Asia, Double Down on Latam & Africa (2011–2016)

The Strategic Focus Decision

By 2011, Millicom faced a critical strategic question. The company operated across three continents in markets with vastly different characteristics, regulatory environments, and growth trajectories. Was geographic diversification an asset or a distraction?

Millicom completed the sale of its Asian business segment in 2011 with the sale of Laos. With the sale of its last remaining Asian operation, Millicom shifted its focus to Latin America and Africa.

The Asian exit reflected hard-won lessons. In markets like India and the Philippines, Millicom faced entrenched competitors with deep pockets and local market knowledge. The capital required to compete effectively exceeded the returns available. Management concluded that their competitive advantage was strongest in Latin America and Africa—markets where their early presence, brand recognition, and local relationships created sustainable advantages.

Modernization and 4G Rollout

The capital freed from Asian operations funded aggressive network investments. Millicom launched its first 4G high-speed internet services in Colombia in 2014, followed by Bolivia later in the year, and the remaining markets soon after. In 2014, Millicom launched the TIGO Sports Television channel in Paraguay and Bolivia.

The Tigo Sports launch exemplified Millicom's evolving strategy. Local content—particularly football—drives customer engagement and reduces churn in ways that generic telecommunications services cannot. By investing in exclusive sports content, Millicom created differentiation that pure infrastructure competitors couldn't replicate.

Strategic Partnerships

Millicom also pursued partnerships that enhanced its capabilities without requiring massive capital outlays. In 2012, Millicom partnered with UNICEF to protect children's rights—a partnership that demonstrated corporate responsibility while building brand equity in markets where trust matters enormously.

In 2016, Millicom partnered with Microsoft to provide cloud services to its Tigo Business customers in eight markets in Latin America. This partnership positioned Millicom to capture enterprise demand as Latin American businesses digitized their operations.

The 2011-2016 period represents Millicom's maturation from opportunistic emerging markets investor to focused Latin American telecommunications leader. The exits from Asia weren't retreats—they were strategic concentrations that enabled deeper investments in core markets. This focus would prove essential as the next, more dramatic strategic pivot approached.

INFLECTION POINT #3: The Great African Exit (2016–2021)

The Rationale for Leaving Africa

The decision to leave Africa represents one of the most consequential strategic moves in Millicom's history. African operations had been part of the company since its earliest days. But by 2016, management concluded that focus—ruthless, complete focus—was worth more than diversification.

The mathematics were unambiguous. According to Millicom's 2017 financial reports, consolidated African operations represented less than 10% of annual group revenues and EBITDA. Yet these operations consumed management attention disproportionate to their contribution. Currency volatility, political instability, and competitive pressure in African markets created earnings variability that complicated capital allocation and investor communication.

More fundamentally, Millicom had identified where it could win. In Latin America—particularly Central America—the company had market-leading positions, strong brands, integrated infrastructure, and proven operational excellence. In Africa, Millicom often faced better-capitalized competitors with deeper local connections.

The Exit Timeline

The African exit proceeded methodically over half a decade:

Millicom (TIGO) completed the sale of Sierra Leone in 2009. Millicom (TIGO) completed the sale of Mauritius in 2014. Millicom (TIGO) completed the sale of Democratic Republic of the Congo in 2016.

Millicom (TIGO) and Bharti Airtel merged in Ghana to complete AirtelTigo in 2017. Millicom (TIGO) completed the sale of Rwanda in 2017. Millicom (TIGO) completed the sale of Chad in 2019. Millicom (TIGO) completed the sale of Senegal in 2019 to Axian Telecom.

In April 2021, Millicom announced the sale of its operations in Tanzania and for its stake in the AirtelTigo joint venture in Ghana, completing its multi-year plan to divest its African operations and focus on its Latin American markets.

The Kinnevik Separation

The African exit coincided with another seismic change in Millicom's ownership structure. In 2019 Kinnevik distributed its remaining shareholding in Millicom to its shareholders.

This was profound. Kinnevik—Jan Stenbeck's vehicle, the company that had co-founded Millicom and shepherded it through three decades—was exiting. The distribution removed a key historical shareholder and set up the ownership transition that would follow. Kinnevik's departure reflected its own strategic pivot toward digital consumer businesses and away from traditional telecommunications.

For Millicom, Kinnevik's exit created both opportunity and vulnerability. The company's shares became more accessible to new investors—but also to potential acquirers who might have different visions for the company's future.

INFLECTION POINT #4: The Acquisition Spree—Consolidating Latin America (2018–2021)

Cable Onda Acquisition (2018)

With Africa receding in the rearview mirror, Millicom turned its attention to aggressive consolidation in Latin America. The first major move came in Panama.

On October 8, 2018, Millicom announced it was acquiring a controlling 80% stake in Cable Onda, the largest cable and fixed telecommunications services provider in Panama. The price tag: $1.46 billion.

The strategic logic was compelling. Cable Onda's fixed-line infrastructure complemented Millicom's mobile operations, creating opportunities for bundled offerings. More importantly, the acquisition gave Millicom contiguous country operations from Guatemala to Colombia—a geographic corridor that enabled B2B capabilities and operational efficiencies impossible with scattered market positions.

Telefónica Central America Acquisitions (2019)

The Cable Onda deal whetted management's appetite for transformation. In February 2019, Tigo announced the purchase of Telefónica's Panamanian, Costa Rican, and Nicaraguan operations for $650 million, $570 million, and $430 million respectively, totaling $1.65 billion. The transaction closed in August of that year.

These weren't just asset purchases—they were market consolidations. By absorbing Telefónica's Central American operations, Millicom eliminated a competitor and gained scale advantages that improved negotiating power with equipment vendors, content providers, and regulators.

In 2019, Millicom common shares started trading on the Nasdaq Stock Market in the United States under the symbol TIGO. The U.S. listing expanded Millicom's investor base and improved liquidity, supporting the aggressive M&A strategy with enhanced access to capital markets.

The Guatemala Buyout—The Crown Jewel (2021)

The most significant transaction of this era—arguably in Millicom's entire history—came in November 2021.

Millicom has operated in Guatemala since 1990. It owns a 100% equity interest in the operation after acquiring the remaining 45% stake from its local joint venture partner in a $2.2 billion deal in November 2021.

The significance of this deal cannot be overstated. Tigo Guatemala is the most profitable business within the Millicom Group, with EBITDA margins exceeding 51%. In 2020, Tigo Guatemala revenue grew 4.8% to $1.5 billion, EBITDA rose 4.0% to $778 million. Based on its robust financial and operating performance in the first nine months of 2021, Tigo Guatemala's financial targets for full year 2021 were: Revenue of about $1.6 billion, up 6% year-over-year; EBITDA of $850 million, implying an EBITDA margin of 53%.

The acquisition brought massive infrastructure assets under Millicom's complete control: approximately 4,400 towers, two tier-3 data centers, and more than 21,000 kilometers of fiber. These weren't just revenue streams—they were strategic assets that create barriers to entry and enable decades of profitable operation.

Tigo Guatemala is the country's largest mobile operator with more than nine million customers and market share of 53.4 percent. Market leadership at this scale creates virtuous cycles: better network quality attracts more customers, more customers generate revenue for network investments, better networks attract more customers.

For investors, the Guatemala buyout crystallized what Millicom had become: not a collection of emerging market telecom assets, but an integrated Latin American telecommunications platform with a crown jewel operation generating world-class margins.

INFLECTION POINT #5: Xavier Niel's Entry & The Battle for Control (2023–2025)

The Activist Investor Arrives

The ownership vacuum created by Kinnevik's departure would eventually be filled—by one of Europe's most aggressive telecommunications investors.

In 2023, Apollo Global Management and Marcelo Claure held discussions with Millicom regarding a potential acquisition of all outstanding shares of the company. The discussions were terminated on June 16, 2023. At the same time, French billionaire Xavier Niel built a 25.02% stake in Millicom through his company Atlas Investissement, making him the company's main shareholder.

Xavier Niel is no ordinary investor. Xavier Niel is a French billionaire businessman. He is involved in the telecommunications and technology industry and is the founder and majority shareholder of the French Internet service provider and mobile operator Iliad trading under the Free brand. He is also co-owner of the newspaper Le Monde, co-owner of the rights of the song "My Way" and owner of Monaco Telecom, Salt Mobile and Eir. He is chairman and chief strategy officer for Iliad, and also a board member of KKR, Unibail-Rodamco-Westfield, and ByteDance.

As of July 2025, his net worth is estimated at US$13 billion.

Niel built his reputation—and his fortune—by disrupting established telecommunications markets. French billionaire Xavier Niel rose to prominence in the telecom world for his ownership of domestic telco Iliad. He went on to capture the industry's attention when Iliad sparked a price war in the mobile sector when the telco's Free Mobile unit launched in January 2012. Niel employed a similar price-war tactic when Iliad Italia launched in May 2018.

His stake-building in Millicom began quietly. Niel first acquired a 7% stake in Millicom in November 2022. Atlas Investissement said it identified Millicom as an "attractive investment opportunity thanks to its strong position as a regional market leader in Latin America, high-quality assets, and strong brand."

The Tender Offer Battle (2024)

By summer 2024, Niel had accumulated approximately 29% of Millicom and launched a formal tender offer.

Xavier Niel confirmed his intention to buy out other shareholders of Millicom International Cellular in a deal worth about $4.1 billion. Investment firm Atlas Luxco offered $24 per share to other Millicom shareholders.

Millicom's board rejected the offer as insufficient. Atlas Luxco raised its offer to acquire Latin America-focused operator group Millicom to US$4.4 billion. Atlas Luxco detailed that it increased its offer from US$24 per share by 7.3% to US$25.75.

The businessman worked to steadily increase his shareholding over the next two years, culminating with a controversial August 2024 buyout of shares from investors holding a combined 11.25% stake. Despite an independent committee of board members arguing that the offer price would "significantly undervalue Millicom and not be in the best interests of Millicom's shareholders," Niel's approach succeeded.

The New Management Era

Niel's influence brought immediate operational changes. Following the acquisition of significant stakes, three new directors appointed by Atlas Investissement joined the company's board in May 2023: Michaël Golan, former CEO of Iliad, Nicolas Jaeger, CFO of Iliad, and Thomas Reynaud, CEO of Iliad.

Maxime Lombardini was appointed Chair of Millicom's Board of Directors on May 21, 2025, following his designation as Interim Chair from September 19, 2024. Previously, he was President and Chief Operating Officer for Millicom, leading all operational and financial responsibilities with a focus on driving profitable growth.

He joined the Iliad Group, one of the major players in the European telecoms sector, in 2007, as Chief Executive Officer and continued his tenure through 2018. In May of 2018, he assumed the role of Chairman of Iliad's Board of Directors until March 2020.

The appointment introduced a new management style: significant headcount reductions, lower capital expenditure, standardization of network and frequency usage charges. This approach—aggressive cost optimization followed by market share gains—had worked spectacularly for Iliad in France, Italy, and Poland. Whether it can translate to Latin American markets remains the central question of Millicom's next chapter.

French billionaire Xavier Niel, through Atlas Investissement, became the main shareholder of Millicom by March 2025, holding a substantial 40% stake.

Why This Matters

Xavier Niel owns the Iliad Group with operations in France, Italy, Poland, Sweden and the Baltics, while NJJ has invested in telecom assets in Switzerland, Ireland, Monaco, Cyprus, Malta, Sweden and the Baltics.

This represents the first significant investment by a major French telecom group in the Latin American telecommunications sector. Niel's involvement brings operational expertise from markets where cost efficiency and network quality enabled dramatic market share gains against established incumbents.

The transformation is already evident in financial results. Millicom International Cellular SA achieved a record equity free cash flow of $728 million for full year 2024, excluding tower sales. The company successfully reduced its leverage to below 2.5x, meeting one of its key financial targets. Millicom resumed shareholder remuneration, including dividends and a $150 million share buyback program.

The Business Today: Products, Markets & Operations

Current Footprint

As of March 2021, Millicom maintains operations across nine Latin American countries: Bolivia, Colombia, Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, Panama and Paraguay.

But the footprint is expanding. Millicom announced the successful completion of its USD 380 million acquisition of Telefónica's telecommunications operations in Ecuador on October 30, 2025. This transaction represents another major step in Millicom's strategy to deepen its presence in South America, following the company's recent acquisition of Telefónica Uruguay.

On October 7, 2025, Millicom completed the acquisition of 100% of Telefonica Moviles del Uruguay S.A. (Movistar) following final regulatory approval for an enterprise value of $440 million.

With operations now spanning eleven countries, Millicom reinforces its position as one of Latin America's leading telecommunications groups. The company continues to advance digital inclusion and innovation, investing in next-generation networks.

Product Portfolio

Millicom's revenue streams span multiple categories:

Mobile Services: The core business includes postpaid and prepaid mobile voice, data, and SMS services. Mobile remains approximately 50% of total revenue, with strong momentum in postpaid conversions.

Fixed Broadband and Cable: The AMNET legacy and subsequent acquisitions created an integrated fixed-line business serving residential and business customers with high-speed internet and pay-TV services.

Tigo Money: Since its launch over a decade ago, Tigo Money has become the leading mobile wallet in the markets served, with almost 6 million active users. Many Latin American citizens are gaining first-time access to financial systems through the Tigo Money app. Millicom is leveraging these strengths in a push to make Tigo Money the premier fintech player in these markets.

Enterprise Services (Tigo Business): Cloud services, cybersecurity, and managed services for business customers represent a growing revenue stream with higher margins than consumer services.

Content: Tigo Sports and Tigo ONEtv provide local entertainment content that drives engagement and reduces churn.

Infrastructure Transformation

A significant recent development has been the tower sale-leaseback transaction with SBA Communications. US tower company SBA Communications agreed to acquire 7,000 telecom towers from Millicom International Cellular for $975 million. The sale-leaseback deal covers towers in Guatemala, Honduras, Panama, El Salvador, and Nicaragua.

As is common practice with these deals, Millicom and SBA agreed a 15-year leaseback deal for these towers, plus a build-to-suit agreement that covers up to an additional 2,500 new sites. For SBA, the agreement bolsters its position in Guatemala, Panama, El Salvador and Nicaragua, and adds a new market in Honduras.

As of June 13, 2025, Millicom International Cellular announced the partial closing of the transaction with SBA Communications through the sale of LATI International. Millicom generated approximately $600 million in proceeds from partial closing. Millicom's Board of Directors intended to approve the distribution of a special interim cash dividend of $2.50 per share, representing approximately 45% of net proceeds.

This transaction exemplifies Millicom's evolving capital allocation strategy: monetize infrastructure assets at favorable valuations, return capital to shareholders, and focus operational resources on customer-facing services where the company can add unique value.

Recent Strategic Developments

Colombia Consolidation

Millicom's Colombian strategy represents perhaps its most ambitious current initiative. Millicom and Telefonica entered into a definitive agreement for the acquisition by Millicom of Telefonica's controlling 67.5% equity stake in Coltel, subject to closing conditions including regulatory approvals. Millicom has also agreed to offer to purchase the remaining 32.5% of Coltel equity owned by La Nación and other investors at the same purchase price per share offered to Telefonica. The purchase price of $400 million is subject to customary adjustments.

The deal presents regulatory challenges. The combined entity would merge Colombia's second and third-largest mobile operators, potentially reducing competition. Currently, Claro, owned by America Movil, holds 45% of the market, while Telefonica and Millicom have 25% and 18%, respectively.

Colombia's competition regulator approved the merger of Movistar and Tigo with conditions and possible penalties in the event of non-compliance, in order to facilitate the sale of Telefónica Colombia's shares to Millicom. Following this operation, the sale of the Colombian government's shares to Millicom and EPM's shares to Tigo remains pending.

DOJ Settlement

A significant legal overhang was resolved in November 2025. Millicom announced that its subsidiary, Comunicaciones Celulares S.A. ("Comcel"), reached an agreement with the U.S. Department of Justice ("DOJ") to resolve an investigation concerning historical improper payments made to Guatemalan government officials. At the time of the conduct, Comcel operated as a joint venture over which Millicom lacked operational control.

The investigation is being resolved through a deferred prosecution agreement (DPA). In recognition of the 2015 self-report and Comcel's and Millicom's extensive cooperation and remediation efforts, the agreement will remain in place for two years, rather than a standard three-year term, and DOJ will not require a corporate monitor. Under the terms of the agreement, Comcel will pay a $60 million fine and forfeit $58.2 million in approximate benefits derived from the improper payments.

Comunicaciones Celulares S.A. entered into a deferred prosecution agreement with the Department of Justice to resolve a criminal investigation related to conduct by employees and executives of TIGO Guatemala. As part of the resolution, TIGO admitted its participation in a widespread and systematic bribery scheme including cash payments to Guatemalan legislators in return for their support of legislation benefiting TIGO. This is the first criminal Foreign Corrupt Practices Act corporate resolution reached since the FCPA "pause" was lifted.

While the settlement removes a significant legal uncertainty, the underlying conduct—which occurred when Millicom lacked operational control of the Guatemala joint venture—illustrates the governance challenges inherent in joint venture structures common in emerging markets.

Bull and Bear Case Analysis

Bull Case

1. Structural Market Position: Millicom holds market-leading or strong second positions across its core Central American markets. Tigo Guatemala is the country's largest mobile operator with market share of 53.4 percent. These positions were built over three decades and are protected by significant infrastructure investments, brand equity, and regulatory relationships.

2. Cash Flow Generation: Millicom achieved a record equity free cash flow of $728 million for full year 2024, excluding tower sales. The company's target of approximately $750 million in EFCF for 2025 suggests sustainable cash generation that supports debt reduction, dividends, and strategic investments.

3. Iliad Management Expertise: Niel and his team have demonstrated an ability to extract operational efficiencies in telecommunications markets across Europe. If similar cost discipline can be applied to Millicom's operations while maintaining service quality, margin expansion could be substantial.

4. Consolidation Opportunities: Telefónica's continued exit from Latin America creates acquisition opportunities. The Spanish carrier has been looking to consolidate its operations in Latin America since 2019 as it looks to cut overall debt and reduce exposure to currency swings. Millicom acquired Telefónica's Panamanian, Costa Rican, and Nicaraguan mobile units in 2019 for a combined $1.6 billion. The Uruguay and Ecuador acquisitions extend this trend.

5. Tigo Money Upside: Millicom's goal is to further increase financial inclusion among Latin American citizens while tapping into a lucrative "blue ocean opportunity" in a geography where Tigo already leads. In pursuing this opportunity, Millicom is amassing a deep bench of tech talent, building key infrastructure and seeking equity investors with complementary fintech expertise.

Bear Case

1. Currency Risk: The company faces potential negative impacts on equity free cash flow in 2025 due to FX risks in Bolivia, Colombia, and Paraguay. Bolivia's currency devaluation and the adoption of an estimated spot rate for financial reporting are expected to negatively impact service revenue and EBITDA.

2. Regulatory and Political Risk: Operating in Central and South America exposes Millicom to political instability, regulatory changes, and corruption risk. The DOJ settlement highlights historical issues that may resurface.

3. Competition Intensification: The competitive landscape in Colombia remains challenging, with aggressive market behavior impacting fixed broadband growth. América Móvil's Claro brand remains a formidable competitor with deep pockets.

4. Concentrated Ownership Risk: Xavier Niel's 40% stake gives him effective control over corporate decisions. His interests may not always align with minority shareholders—particularly if he pursues a take-private transaction at valuations minority holders consider inadequate.

5. Market Size Limitations: The Latin America telecommunication market was valued at USD 149.84 billion in 2024. Millicom operates primarily in Central America and the Andean region—not the larger Brazilian or Mexican markets where growth potential is greater but where Millicom has no presence.

Porter's Five Forces Analysis

Threat of New Entrants: LOW. Telecommunications requires massive capital investment, spectrum licenses, and years of infrastructure build-out. Regulatory barriers are high. New entrants are unlikely in Millicom's core markets.

Bargaining Power of Suppliers: MODERATE. Equipment vendors (Ericsson, Nokia, Huawei) are concentrated, but Millicom's scale provides negotiating leverage. Network equipment is increasingly commoditized.

Bargaining Power of Buyers: MODERATE TO HIGH. Consumer switching costs have declined as number portability became universal. Price sensitivity is high in prepaid segments. However, bundled services create stickiness.

Threat of Substitutes: MODERATE. OTT services (WhatsApp, Zoom) substitute for voice and messaging. However, these services require connectivity that Millicom provides. The company captures value through data rather than voice.

Competitive Rivalry: HIGH. América Móvil (Claro) is a well-capitalized competitor present across Millicom's markets. Price competition is intense in mobile services. Convergent offerings (bundles) provide differentiation.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Millicom benefits from scale in procurement, network operations, and marketing. However, scale advantages are regional rather than global—Millicom is sub-scale compared to América Móvil.

Network Effects: Limited direct network effects in telecommunications. However, Tigo Money could develop network effects as more merchants and users join the platform.

Counter-Positioning: Millicom has counter-positioned against global operators by focusing exclusively on Latin America while competitors like Telefónica spread resources globally. This focus enables deeper market knowledge and operational excellence.

Switching Costs: Bundled services (mobile + broadband + TV + Tigo Money) create meaningful switching costs. Postpaid contracts with device subsidies also create lock-in.

Branding: The Tigo brand has significant equity in Central America. Brand recognition and trust are valuable in markets where corporate reputation varies widely.

Cornered Resource: Spectrum licenses are cornered resources—once awarded, they cannot be replicated. Millicom's fiber and tower infrastructure (even leased) represents physical assets competitors cannot easily duplicate.

Process Power: Not evident. Telecommunications operations are increasingly standardized and equipment vendor-dependent.

Key Metrics and Investment Considerations

Critical KPIs to Monitor

1. Equity Free Cash Flow (EFCF): This is the single most important metric for Millicom investors. EFCF measures cash available for debt reduction, dividends, and strategic investments after capital expenditures and lease payments. Management targets approximately $750 million for 2025.

2. Postpaid Mobile Net Additions: In Guatemala, the postpaid customer base expanded 20% year over year. As mentioned, one of the levers is migration of prepaid to postpaid, which is particularly relevant in Guatemala. Postpaid conversion drives ARPU improvement and reduces churn—it's the clearest indicator of competitive positioning and revenue quality.

3. EBITDA Margin by Country: Guatemala reported a record adjusted EBITDA margin of 56.6%, up 147 basis points compared to the same period last year. Country-level margins reveal operational efficiency and competitive dynamics. Guatemala's exceptional margins should be monitored for sustainability while Colombia's margins should be tracked for improvement.

Valuation Considerations

At current levels, Millicom trades at a discount to Latin American telecom peers on most conventional metrics. However, several factors complicate valuation:

- Controlling Shareholder: Niel's 40% stake means the stock's liquidity and governance differ from widely-held peers

- Currency Dynamics: USD-reported financials mask local currency operational performance

- Legal Settlements: The $118 million DOJ settlement impacts near-term cash flow

Regulatory and Legal Considerations

FCPA Settlement: Under the terms of the agreement, Comcel will pay a $60 million fine and forfeit $58.2 million in approximate benefits derived from improper payments. The fine amount represents a 50 percent discount off the bottom end of the applicable penalty range under the U.S. Sentencing Guidelines—the highest penalty discount available under applicable DOJ policy. While the settlement removes uncertainty, investors should monitor for any additional regulatory or legal proceedings.

Colombia Regulatory Approval: The Telefónica Colombia merger remains subject to final closing conditions. Regulatory conditions imposed could affect deal economics.

Spectrum Renewals: Telecommunications licenses typically require periodic renewal. Millicom's spectrum holdings across markets represent valuable but time-limited assets.

Conclusion: The Next Chapter

Millicom's journey from Swedish-American startup to Latin American telecommunications leader encompasses nearly every theme that defines the emerging markets telecommunications industry: regulatory battles, currency crises, strategic pivots, and ownership transitions.

The company that helped birth Orange UK has become something entirely different—a focused Latin American operator with market-leading positions in Central America and expanding presence in South America. Under Xavier Niel's influence, Millicom is pursuing aggressive efficiency improvements while maintaining its acquisition strategy.

The central questions for investors are straightforward but difficult: Can Iliad's European playbook translate to Latin American markets? Will Niel ultimately take the company private, and if so, at what valuation? Can Millicom maintain its competitive positions as América Móvil and regional competitors invest heavily in network modernization?

What isn't in question is Millicom's strategic position. Through its TIGO® and Tigo Business® brands, Millicom provides a wide range of digital services and products, including TIGO Money for mobile financial services, TIGO Sports for local entertainment, TIGO ONEtv for pay TV, high-speed data, voice, and business-to-business solutions. As of December 31, 2024, Millicom employed approximately 14,000 people and provided mobile and fiber-cable services through its digital highways to more than 46 million customers, with a fiber-cable footprint over 14 million homes passed.

From Jan Stenbeck's battles against Swedish telecommunications monopolies to Xavier Niel's cost optimization playbook, Millicom has always been shaped by visionary—and sometimes controversial—leaders willing to challenge conventional wisdom. That tradition continues as the company enters its fourth decade, building the digital highways that connect Latin America's people, businesses, and communities to the global digital economy.

The story of Millicom isn't over. If anything, under Niel's stewardship, the most transformative chapters may be just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube