First Citizens BancShares: The Family Bank That Ate Silicon Valley

I. Introduction & Cold Open

Picture this: It's Saturday, March 25, 2023. While most Americans sleep, a handful of executives at First Citizens BancShares are huddled in conference rooms, poring over spreadsheets that would make most bankers dizzy. The numbers are staggering—$167 billion in assets, $119 billion in deposits, a tech-focused loan book that just weeks earlier had been the crown jewel of Silicon Valley Bank. By Monday morning, they'll have pulled off one of the most audacious bank acquisitions in American history.

The headlines that followed were almost surreal. A 125-year-old family-controlled bank from Raleigh, North Carolina—known more for its methodical expansion through small-town America than Silicon Valley swagger—had just swooped in to rescue the heart of tech banking from FDIC receivership. In a single weekend, First Citizens transformed from a regional player into a top-20 U.S. financial institution commanding over $200 billion in assets.

How does a bank that started in a tobacco warehouse in Smithfield, North Carolina, end up owning the banking relationships of half of America's venture-backed startups? How does a company so conservative that it survived the Great Depression without taking government aid become the go-to buyer for the FDIC's most complex failed bank resolutions?

The answer lies in a paradox that defines First Citizens: It's simultaneously one of America's most conservative banks and one of its most aggressive acquirers. This duality—patient underwriting meets opportunistic deal-making—has been encoded in the bank's DNA by three generations of the Holding family, who maintain iron-clad control through a dual-class share structure that would make even Mark Zuckerberg envious.

What we're about to explore isn't just a banking story. It's a masterclass in how family control, regulatory relationships, and contrarian thinking can create extraordinary value in moments of crisis. It's about how a bank nobody in Silicon Valley had heard of became their unlikely savior. And it's about how the Holding family built a financial empire by zigging when others zagged, buying when others couldn't, and maintaining a multi-generational perspective in an industry obsessed with quarterly earnings.

The threads we'll pull include the original sin of American branch banking restrictions, the peculiar governance structure that enabled rapid crisis response, and the decades-long cultivation of trust with the FDIC that made First Citizens their speed-dial partner when banks fail. We'll see how each generation of Holdings added their own chapter to this story—from Robert Powell Holding's Depression-era prudence to Frank Holding Jr.'s 21st-century deal spree.

But perhaps most importantly, we'll examine what this means for American capitalism. In an era of activist investors and quarterly capitalism, First Citizens represents something almost anachronistic: a Fortune 500 company run like a family office, where decisions are measured in decades rather than quarters, and where having "skin in the game" means your great-grandfather's name is literally on the building.

II. The Holding Dynasty: Three Generations of Banking (1898-1957)

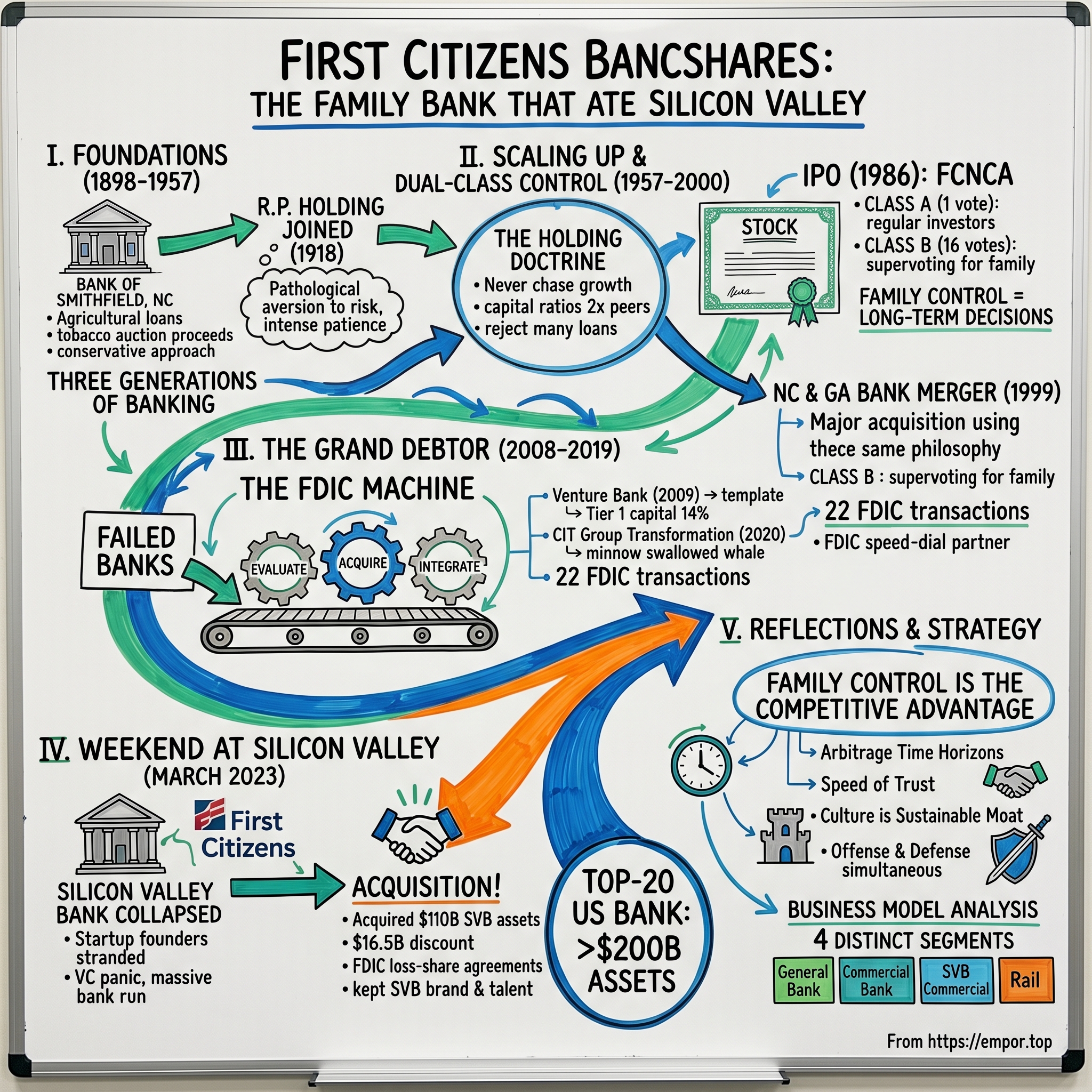

The story begins not with the Holdings, but with a group of tobacco farmers in Smithfield, North Carolina, who on March 1, 1898, pooled their money to open the Bank of Smithfield. The initial capital was modest—just $10,000—and the location even more so: a small agricultural town whose main claim to fame was ham, not high finance. These farmers weren't trying to build an empire; they simply needed a place to deposit tobacco auction proceeds and finance next season's crops.

For its first two decades, the bank operated exactly as you'd expect—making agricultural loans, holding deposits, and occasionally foreclosing on farms when tobacco prices crashed. It was competent but unremarkable, one of thousands of small banks dotting the American landscape before the Federal Reserve even existed.

Everything changed in 1918 when a young man named Robert Powell Holding joined the bank. Holding wasn't from money—his father was a minister—but he possessed two qualities that would define the family's banking philosophy for the next century: an almost pathological aversion to risk and an equally intense patience for opportunity. Colleagues described him as someone who could "watch paint dry if it meant avoiding a bad loan."

By 1935, Holding had worked his way up to president, just in time to navigate the bank through the tail end of the Great Depression. While larger banks were failing or merging desperately, Holding's conservative approach—he famously required three forms of collateral for any loan over $100—kept the Bank of Smithfield solvent. He didn't grow the bank much during these years, but he didn't shrink it either. Survival was victory.

The real acceleration began in 1928, before Holding's presidency but with his influence growing, when W. Horace Carter and his brother-in-law Lewis R. Holding (Robert Powell's cousin) acquired control of the bank. This wasn't a hostile takeover or a distressed sale—it was more like a careful changing of the guard, with local owners selling to other locals who had slightly bigger ambitions.

The Carter-Holding partnership saw something others missed: North Carolina was industrializing. Textile mills were sprouting across the Piedmont, furniture factories in High Point, and tobacco processing was becoming mechanized. Each factory needed banking services, and the big Charlotte banks weren't particularly interested in Goldston or Garner or Gibson. This created a vacuum that a smart regional bank could fill.

They renamed the institution First Citizens Bank & Trust Company in 1929—terrible timing given what happened in October, but the name stuck. The word "Citizens" was deliberate, positioning the bank as belonging to the community rather than distant shareholders. This wasn't just marketing; it reflected a genuine philosophy that deposits were a sacred trust and lending was about relationships, not just ratios.

What made the Holdings different from hundreds of other family banks across America was their approach to expansion. Rather than opening new branches from scratch—expensive and slow—they became early practitioners of what would later be called "roll-up" strategy. Throughout the 1930s and 1940s, they acquired small, often struggling banks in neighboring towns. The playbook was consistent: buy cheap, usually from a retiring owner or a family that had lost interest in banking; keep the local management but instill First Citizens' conservative underwriting; use the acquired bank's deposits to fund careful expansion.

By 1957, when Robert Powell Holding passed away, First Citizens had grown from a single Smithfield office to a network spanning eastern North Carolina. The asset base had expanded from that initial $10,000 to over $50 million—impressive growth, but still small enough that the Holding family maintained absolute control.

The governance structure they established during these years would prove crucial decades later. The Holdings created two classes of stock: Class A shares for regular investors and Class B shares with supervoting rights for the family. This wasn't unusual for the era—many family businesses used similar structures—but the Holdings were particularly clever about it. They made sure the Class B shares couldn't be sold to outsiders without converting to Class A, essentially creating a poison pill against hostile takeovers.

Robert Powell Holding's three sons—Frank, Robert Jr., and Lewis—had all joined the bank by the 1950s, each groomed in different aspects of the business. Frank focused on commercial lending, Robert on operations, and Lewis on investments. This division of labor would become a template for future generations: spread the family across the organization to maintain control and knowledge of every division.

The 1950s also saw First Citizens develop what insiders called the "Holding Doctrine": never chase growth for growth's sake, never make a loan you wouldn't make with your own money, and always keep enough capital to survive two simultaneous crises. This might sound like standard conservative banking, but the Holdings took it to an extreme. They maintained capital ratios nearly double their peers and turned down more loans than they approved, even in boom times.

This conservatism had a fascinating side effect: it made First Citizens incredibly attractive to regulators. While other banks were constantly pushing boundaries, getting into trouble, and requiring regulatory intervention, First Citizens was the student who never caused problems. This would prove invaluable when the family wanted to make acquisitions—regulators tend to approve deals for banks they trust.

As the 1950s drew to a close, First Citizens stood at a crossroads. The Holding brothers faced pressure to either go public for growth capital or remain a sleepy regional bank. The solution they crafted—going public while maintaining family control—would set the stage for everything that followed.

III. Going Public While Staying Private: The IPO and Control Structure (1957-2000)

The death of Robert Powell Holding in 1957 triggered a succession crisis that would define First Citizens' future. Not because the brothers fought—quite the opposite. They were so aligned in their vision that they created something unique in American banking: a public company that operated like a private one.

Frank Holding took the helm as CEO, but this wasn't a monarchy. The three brothers developed what employees called the "triumvirate system"—major decisions required consensus among all three, minor decisions could be made by any two. They met every morning at 7 AM in Frank's office, no agenda, just coffee and conversation about the bank. These informal sessions became legendary within First Citizens as the place where real decisions were made, long before they reached the official board.

The 1960s brought the Interstate Banking Act restrictions, which paradoxically helped First Citizens. While money-center banks were blocked from expanding across state lines, First Citizens could vacuum up every small bank in North Carolina without competition from the big boys. Between 1960 and 1970, they acquired twelve banks, each following the same pattern: identify a town with growing industry but tired bank ownership, negotiate privately with the owners (often over dinner at the Holding farm), pay cash at a fair but not generous price, and integrate slowly to avoid culture shock.

But the real innovation came in 1986 when First Citizens went public on NASDAQ under the ticker FCNCA. The IPO was structured brilliantly—or deviously, depending on your perspective. The family sold just enough Class A shares to raise $50 million in growth capital while retaining all Class B shares. The math was elegant: Class B shares carried 16 votes each versus one vote for Class A, meaning the Holdings could maintain majority voting control while owning just 20% of the economic interest.

Wall Street initially balked at this structure. One analyst famously called it "feudalism masquerading as capitalism." But the Holdings didn't care about Wall Street opinion; they cared about patient capital. The investors who did buy in were a peculiar bunch—mostly North Carolina institutions, family offices who understood the model, and value investors attracted to the bank's rock-solid balance sheet.

The 1990s tested this structure when activist investor Carl Icahn accumulated a 4.9% stake and pushed for board seats. The Holdings' response was masterful in its simplicity: they did nothing. With voting control locked up, Icahn could make noise but couldn't force change. After eighteen months of frustration, he sold his stake, reportedly calling First Citizens "uninvestable but unassailable."

A pivotal moment came in 1999 with the merger with First Citizens Bancorporation of Georgia. This wasn't just another acquisition—it was a $400 million all-stock deal that nearly doubled the bank's size. The Georgia operation, despite the similar name, was unrelated to the North Carolina bank but had been built on remarkably similar principles: conservative lending, family ownership (the Ottley family), and a focus on small-town banking.

The merger negotiations, conducted primarily between Frank Holding Jr. (who had succeeded his father as CEO) and George Ottley, took just six weeks from first contact to signed agreement. Both men later said the speed was possible because they "spoke the same language"—not Southern politeness, but the language of multi-generational thinking. The deal structure preserved both families' influence: the Ottleys received Class B shares, making them the only non-Holdings to ever own supervoting stock.

This period also saw First Citizens develop its signature approach to regulatory relationships. While other banks hired armies of lobbyists and fought regulations tooth-and-nail, First Citizens took a different tack. They invited regulators to their annual planning sessions, implemented suggested changes before they became mandatory, and never—not once in forty years—received a formal enforcement action. One FDIC examiner was quoted saying, "First Citizens is boring in the best possible way."

The technology investments of the late 1990s revealed another paradox of family control. While publicly-traded peers were spending fortunes on flashy digital initiatives to impress quarterly earnings calls, First Citizens invested steadily but conservatively in back-office systems. They were late to online banking but early to automated underwriting. They skipped the ATM wars but built sophisticated risk management systems. The approach was purely pragmatic: spend money on what helps make better lending decisions, not on what looks good in presentations.

By 2000, First Citizens had $15 billion in assets, operated 340 branches across North Carolina, South Carolina, and Virginia, and had completed thirty-seven acquisitions without a single material loss. The family's stake had been diluted to about 20% economic ownership, but voting control remained absolute at 52%. The stock had delivered a 15% annual return since the IPO, beating the S&P 500 without a single year of losses.

The new millennium brought new challenges—interstate banking was fully deregulated, creating massive national competitors; the internet was disrupting traditional branch banking; and the Holdings were aging, with succession questions looming. But the family had built something remarkable: a structure that allowed them to act quickly and decisively while public market investors came along for the ride. This would prove invaluable when the financial crisis created the opportunity of a lifetime.

IV. The Third Generation Takes Charge: Frank Holding Jr. Era (2008-2019)

Frank Holding Jr. officially took the chairman's seat in 2009, with his sister Hope Holding Bryant as vice chairwoman, marking the third generation of family leadership. But the transition really began on September 15, 2008—the day Lehman Brothers collapsed. While Wall Street burned and Congress debated bailouts, Holding Jr. convened an emergency session with an unusual agenda: "How do we profit from this chaos?"

The room was stunned. Banks were failing daily, credit markets were frozen, and even Goldman Sachs was converting to a bank holding company for Federal Reserve protection. Yet Holding Jr. saw opportunity where others saw apocalypse. "Every crisis," he told his executives, "creates a new pecking order. We're going to move up that order."

His thesis was simple but contrarian: the FDIC would need buyers for failed banks, lots of them, and quickly. Banks with clean balance sheets, excess capital, and—crucially—experience integrating acquisitions would become the FDIC's preferred partners. First Citizens checked all three boxes. While competitors were nursing wounds from subprime mortgages and leveraged loans, First Citizens' boring, traditional banking model had kept them largely unscathed. Their Tier 1 capital ratio was 14%, nearly double the regulatory requirement.

The first test came in January 2009 when the FDIC called about Venture Bank, a small Washington state institution with $970 million in assets. Most buyers passed—too far away, too complicated, wrong time. Holding Jr. flew out personally, spent twelve hours reviewing loans, and submitted a bid that evening. First Citizens won, acquiring $640 million in assets with FDIC loss-sharing on $530 million of them. The actual cash outlay? Just $12 million.

This deal established the template First Citizens would perfect over the next decade. The FDIC loss-sharing agreements were financial engineering at its finest: the government would absorb 80% of losses on covered assets for the first three years, stepping down to 95% coverage thereafter. First Citizens essentially got free optionality—upside if the loans performed, limited downside if they didn't.

Between 2009 and 2019, First Citizens completed twenty-two FDIC-assisted transactions, absorbing $15 billion in assets while paying virtually nothing upfront. Each Friday, when the FDIC announced that week's bank failures, First Citizens had a team ready to evaluate and bid. They became so proficient that FDIC staff started calling them first, knowing they could close deals in seventy-two hours that would take others weeks.

The 2014 merger with First Citizens Bancshares of South Carolina revealed another dimension of the Holding strategy. This wasn't an FDIC deal but a family reunion of sorts. In 1964, three of the original Holding brothers had acquired control of a South Carolina bank, essentially creating a cousin institution. Fifty years later, Frank Jr. engineered a $360 million all-stock merger that brought 156 branches and $3.8 billion in assets back into the fold.

The negotiation was unlike anything investment bankers typically see. Instead of conference rooms and lawyers, key discussions happened at the Holding family farm outside Raleigh. The South Carolina cousins weren't just selling a business; they were deciding whether to reunite a family enterprise. The deal terms reflected this: the cousins received Class B shares, maintaining their governance influence, and several joined the combined company's board.

Cultural integration, always the achilles heel of bank mergers, was remarkably smooth. Both institutions shared the same DNA—conservative underwriting, relationship focus, multi-generational thinking. Employees joke that the only real difference was barbecue preferences (vinegar-based in North Carolina, mustard-based in South Carolina).

But Holding Jr.'s masterstroke during this period was building what he called "the machine"—a standardized process for evaluating, acquiring, and integrating failed banks. First Citizens developed proprietary models that could value a loan portfolio in hours, not weeks. They created integration playbooks that covered everything from IT system migration to employee communications. They even maintained a bench of experienced executives who could parachute into acquired banks as interim management.

The numbers tell the story: First Citizens' assets grew from $16 billion in 2008 to $37 billion by 2019, while maintaining return on equity above 10% throughout. The stock price increased five-fold during Holding Jr.'s first decade as chairman, dramatically outperforming both the KBW Bank Index and the S&P 500.

Yet the family never lost its conservative DNA. Despite all the acquisitions, First Citizens maintained the highest capital ratios among its peers. They never participated in the leveraged loan boom, avoided cryptocurrency speculation, and kept their investment portfolio in boring government bonds. One analyst described them as "aggressive acquirers but paranoid lenders"—a paradox that would serve them well in the next chapter.

The decade also saw subtle but important governance evolution. Hope Holding Bryant's role as vice chairwoman wasn't ceremonial—she led the bank's risk committee and had veto power over any acquisition exceeding $1 billion. The fourth generation began appearing in management ranks, with Frank Holding III joining the commercial banking division and learning the business from the ground up.

As 2019 drew to a close, First Citizens looked like a tremendous success story but not a transformational one. They were the 64th largest bank in America, successful but not significant on the national stage. Nobody could have predicted that within four years, they would engineer two deals that would catapult them into the top twenty—and make them the unlikely savior of Silicon Valley's banking system.

V. The CIT Group Transformation: Doubling Down (2020-2022)

The October 13, 2020 announcement landed like a thunderbolt: First Citizens would acquire CIT Group in an all-stock transaction valued at $2.2 billion, creating the 19th largest bank in America. The audacity was breathtaking—CIT had $61.7 billion in assets compared to First Citizens' $47.9 billion. The minnow was swallowing the whale.

Ellen Alemany, CIT's chairwoman and CEO, had been shopping the company for months. CIT's century-long history read like a cautionary tale of Wall Street excess: from financing America's industrial growth in the 1920s to a disastrous subprime mortgage spree that led to bankruptcy in 2009. Post-bankruptcy CIT had rebuilt as a commercial lender, but without cheap deposits, their funding costs made profitability elusive. They needed a deposit-rich partner; First Citizens needed national commercial lending capabilities.

The initial investor reaction was brutal. First Citizens stock dropped 12% on announcement day. Analysts questioned everything: How could a regional bank integrate a complex commercial lender? Why take on CIT's railcar leasing business? Could the Holdings maintain control with such massive stock issuance?

Behind closed doors, Frank Holding Jr. was serene. The family had war-gamed this exact scenario for years—how to make a transformational acquisition while preserving family control. The solution was elegant: issue Class A shares to CIT shareholders while the family retained all Class B shares. Even with dilution, the Holdings would maintain 38% voting control, enough to block any hostile actions.

The integration planning revealed First Citizens' hidden strength—they'd done this so many times that transformation was routine. They deployed their "machine," but scaled up dramatically. Instead of integrating a few dozen branches, they were absorbing thousands of commercial relationships. Instead of simple community bank IT systems, they were merging complex international platforms.

The regulatory approval process became a eighteen-month marathon. The Federal Reserve, which normally rubber-stamped First Citizens deals, scrutinized everything. Could a family-controlled bank safely manage $110 billion in assets? Were the governance structures appropriate for a systemically important institution? The Holdings made strategic concessions—adding more independent directors, enhancing risk committees—without surrendering voting control.

During this limbo period, something remarkable happened: both banks thrived independently. CIT's commercial lending boomed as the economy recovered from COVID. First Citizens continued its FDIC acquisition spree, adding three more failed banks. By the time the merger closed in January 2022, the combined entity would have $115 billion in assets, not the projected $110 billion.

The January 3, 2022 merger closing was anticlimactic—no champagne toasts or bell-ringing ceremonies. Holding Jr. spent the day visiting CIT's New York offices, holding town halls with anxious employees. His message was consistent: "We bought CIT for what you know, not to change what you do." This wasn't corporate speak—First Citizens retained 95% of CIT's commercial lending staff and kept their underwriting processes largely intact.

The first year results vindicated the strategy spectacularly. The combined bank generated $2.1 billion in net income for 2022, with return on equity hitting 15%. The feared culture clash never materialized. CIT's sophisticated New York bankers found the Holdings' straightforward style refreshing after years of private equity ownership. First Citizens' community bankers gained access to CIT's national platform and expertise.

Two decisions during integration proved particularly shrewd. First, rather than consolidate operations in Raleigh, First Citizens maintained CIT's New York and California offices as "centers of excellence" for commercial lending. This prevented talent flight and preserved customer relationships. Second, they kept CIT's rail leasing business—a $6 billion portfolio of railcars that analysts had assumed would be sold. The Holdings recognized it as a stable, cash-generating asset perfect for a patient owner.

The technology integration, typically a nightmare in bank mergers, went remarkably smoothly. First Citizens had quietly spent the previous decade building modular systems that could absorb new platforms. Instead of forcing everything onto one system, they created interfaces that let different businesses run on their optimal platforms while sharing data seamlessly.

By late 2022, First Citizens had achieved something remarkable: they'd doubled in size while actually improving operational metrics. Efficiency ratio dropped from 68% to 61%. Net interest margin expanded by 30 basis points. Credit losses remained below 0.5% of loans. The stock price reached $850, up 50% from pre-announcement levels.

But the real prize wasn't visible in financial statements. First Citizens now had relationships with most of America's middle-market companies through CIT's commercial platform. They had expertise in equipment financing, factoring, and asset-based lending that few regional banks possessed. Most importantly, they'd proven they could execute a transformational merger while maintaining their conservative culture.

The fourth quarter 2022 earnings call featured an unusual moment. An analyst asked Holding Jr. about acquisition appetite going forward. His response was cryptic: "We're always prepared to act when opportunities present themselves, especially when others can't or won't." Nobody knew he was already in discussions with the FDIC about a failing California bank that would make the CIT deal look quaint by comparison.

VI. Weekend at Silicon Valley: The SVB Acquisition (March 2023)

March 9, 2023, 11:42 AM Pacific Time: California regulators shut down Silicon Valley Bank and appointed the FDIC as receiver. The preceding forty-eight hours had witnessed the fastest bank run in history—$42 billion in deposits fled in a single day, a quarter of the bank's total. Tech executives were texting frantically, venture capitalists were calling emergency meetings, and startup founders were wondering if they could make payroll.

Inside First Citizens' Raleigh headquarters, a different energy prevailed. Frank Holding Jr. assembled his crisis team—the same group that had executed twenty-plus FDIC deals—with a simple directive: "This is why we've been preparing for fifteen years."

The SVB collapse was a perfect storm of risk management failures. The bank had gorged on deposits during the 2020-2021 tech boom, growing from $60 billion to $210 billion in just two years. They invested these deposits in long-term securities at historic low rates. When the Fed hiked rates and tech funding dried up, SVB faced a lethal combination: securities losses that wiped out their capital and depositors who needed their money back immediately.

What made SVB unique—and attractive to First Citizens—was the quality of its client base. This wasn't a subprime lender or a commercial real estate gambler. SVB banked half of all U.S. venture-backed companies, maintained relationships with 90% of Silicon Valley VCs, and had spent forty years building expertise that couldn't be replicated. The bank had failed not because of bad loans but because of bad asset-liability management.

The FDIC initially tried to sell SVB whole over the weekend of March 11-12. Multiple bidders emerged—JPMorgan, PNC, Citizens Financial—but all balked at the concentration risk and integration complexity. The FDIC then created a bridge bank, Silicon Valley Bridge Bank, to operate while they sought a buyer. For two weeks, uncertainty reigned. Would SVB be broken up? Would deposits be fully protected? Would the venture ecosystem survive?

Behind the scenes, First Citizens was executing their playbook at warp speed. They deployed fifty analysts to evaluate SVB's loan book, using their CIT commercial lending expertise to understand venture debt and warrants. They modeled dozens of scenarios for deposit retention. Most brilliantly, they structured a bid that gave the FDIC what it desperately needed: certainty and speed.

The March 27, 2023 announcement revealed the deal's elegant structure. First Citizens would acquire $110 billion of SVB's assets at a $16.5 billion discount. The FDIC would provide loss-share agreements on both commercial loans and securities, essentially capping First Citizens' downside. The FDIC retained $90 billion of securities that would be liquidated over time. First Citizens would pay nothing upfront—in fact, they received $35 billion in cash from the FDIC to balance the books.

Wall Street's reaction was extraordinary. First Citizens stock opened at $896, up 54% from Friday's close. By day's end, it hit $1,003. The market capitalization increased by $9 billion in a single day—four times the stated purchase price. The message was clear: First Citizens had pulled off the deal of the century.

But the real story was what happened inside Silicon Valley Bridge Bank that weekend. First Citizens executives, led by CIT veterans who understood complex commercial lending, met with SVB's top hundred clients. The message was carefully crafted: "We're not here to change Silicon Valley banking. We're here to ensure it survives and thrives." They committed to maintaining SVB's specialized venture debt products, keeping the experienced bankers, and even preserving the SVB brand for the commercial division.

The numbers were staggering. First Citizens' assets jumped from $115 billion to $219 billion overnight. They gained 37 private bank offices serving high-net-worth individuals, expertise in venture capital and private equity, and relationships with companies that would define the next decade of American innovation. The deposit base, even after the run, exceeded $130 billion.

The execution over following months proved First Citizens wasn't just lucky—they were prepared. Deposit retention exceeded 80%, far above the 50% many predicted. They honored all SVB's existing loan commitments, crucial for maintaining trust. They integrated SVB's technology platform with CIT's commercial systems in just six months, a process initially estimated at two years.

One decision proved particularly inspired: maintaining SVB as a distinct division with its own brand and culture. While other acquirers might have forced integration, First Citizens recognized that SVB's value lay in its uniqueness. The venture debt team kept their offices in Menlo Park, continued their Monday partner meetings, and maintained their quirky tradition of ringing a ship's bell for successful exits.

The regulatory response was fascinating. Rather than concern about First Citizens' rapid growth, regulators seemed relieved. Here was a stable, conservatively-run institution absorbing the chaos. The Fed and FDIC fast-tracked approvals that normally take months. One examiner privately told First Citizens executives: "You're the solution, not the problem."

By year-end 2023, First Citizens stock reached $1,420, a 250% gain from pre-SVB levels. The family's stake, while diluted in percentage terms, had increased in value by $4 billion. Fourth-generation family members, initially skeptical of such dramatic expansion, were converts. As Frank Holding III reportedly said at a family gathering: "Great-grandfather would be shocked by the size but proud of the execution."

The SVB acquisition transformed First Citizens from a successful regional bank into a national powerhouse. They now touched every corner of American innovation—from Austin startups to Boston biotech, from Los Angeles media companies to New York fintechs. The conservative bank from North Carolina had become the unlikely guardian of Silicon Valley's financial infrastructure.

VII. Power: Family Control as Competitive Advantage

The morning after the SVB acquisition announcement, a Fortune reporter asked Frank Holding Jr. how First Citizens moved so quickly on such a complex deal. His answer was revealing: "When you don't have to convince a thousand stakeholders, you can act at the speed of trust."

This speed advantage manifests in ways both obvious and subtle. During the SVB weekend, while potential acquirers were scheduling board calls and preparing investor presentations, Holding Jr. made the decision to bid in a two-hour family discussion. Hope Holding Bryant had full authority to approve risk parameters. Frank Holding III was on-site in California evaluating operations. The family didn't need to debate whether to act—they'd been preparing for this moment for years.

The dual-class structure that enables this speed is both simple and sophisticated. Class B shares, held exclusively by family members and trusts, carry sixteen votes versus one vote for publicly-traded Class A shares. With roughly 20% economic ownership, the Holdings control 52% of voting power. But the real power isn't in the math—it's in the alignment this creates.

Consider the counterfactual: If First Citizens had conventional governance, would they have bid on SVB? The stock market initially punished banks that showed interest. Analysts were universally skeptical. Any normal board would have faced enormous pressure to pass. But the Holdings could ignore short-term market sentiment because they measure success in decades, not quarters.

This dynamic extends beyond crisis acquisitions. First Citizens maintains higher capital ratios than peers—"inefficient" by Wall Street standards but crucial for opportunistic deals. They've kept the railcar leasing business that generates steady cash but confuses analysts. They invest in relationship banking in an era of digital disruption. Each decision seems suboptimal in isolation but creates competitive advantage in combination.

The family control structure also enables unusual stakeholder management. Employees know the Holdings aren't selling to the highest bidder next quarter, creating genuine career paths. Regulators trust that commitments made today will be honored tomorrow. Communities understand that First Citizens won't abandon branches the moment they become marginally unprofitable. This stakeholder trust becomes a moat that compounds over time.

Yet the Holdings have been clever about preventing the typical pathologies of family control. They've consistently promoted non-family executives to key roles—the current president and CFO have no family connection. They maintain majority-independent boards at all subsidiaries. They submit to full regulatory examination despite exemptions available to smaller institutions. The message is clear: family control doesn't mean amateur management.

The succession planning is particularly sophisticated. Fourth-generation family members don't automatically get senior roles—they start in entry-level positions and must prove competence. Several Holdings have worked at other banks to gain outside perspective. The family holds annual "education sessions" where younger members learn about banking, governance, and their fiduciary duties. This isn't nepotism; it's apprenticeship.

Compensation provides another fascinating window into family control benefits. Frank Holding Jr.'s 2023 compensation was $8.5 million—substantial but modest compared to peers running similar-sized banks. Jamie Dimon made $36 million running JPMorgan. But the Holdings don't need massive cash compensation because their wealth is tied to equity value. The $4 billion increase in their stake value from the SVB deal dwarfs any annual paycheck.

This alignment cascades through the organization. First Citizens grants more employee stock options than similar banks, creating thousands of mini-owners. The ESOP owns 3% of shares. Long-term incentive plans vest over seven years, not the typical three. The message permeates: think like owners, not employees.

The family's influence extends beyond formal governance into cultural DNA. The "Holding Doctrine" isn't written in any manual but every employee knows it: conservative underwriting, patient capital, community focus. Stories of Robert Powell Holding checking loan applications during the Depression still circulate. Frank Sr.'s morning coffee meetings have evolved into regular "family forums" where strategy gets debated.

There are real costs to this structure. First Citizens trades at a persistent discount to peers—typically 10-15% lower price-to-book ratio. Index funds often exclude them due to limited float. Activist investors won't touch them. Some talented executives leave, frustrated by the family ceiling. These aren't bugs; they're features that filter for stakeholders who share the long-term vision.

The ultimate test of family control came during 2023's regional banking crisis. While Silicon Valley Bank, Signature Bank, and First Republic collapsed partly due to flighty deposits and short-term thinking, First Citizens stood ready to acquire. The difference wasn't luck or skill alone—it was ownership structure. The Holdings could remain calm because they controlled their destiny.

As one veteran board member explained: "Public company governance is about preventing disasters. Family governance is about enabling opportunities." This distinction explains why First Citizens could build a national banking franchise while maintaining small-town values. The family doesn't just own the bank; they embody its strategy.

VIII. Business Model & Strategy Analysis

Strip away the dramatic acquisitions and family drama, and First Citizens' business model is surprisingly straightforward: gather stable, low-cost deposits through traditional branch banking, deploy them into conservative commercial loans, and use excess capital for opportunistic acquisitions. It's banking as it existed before derivatives, trading desks, and investment banking complications.

The bank operates through four distinct segments that each tell part of the story. The General Bank segment—the original First Citizens—runs 550 branches across 23 states, gathering $145 billion in deposits at an average cost of just 1.2%. This is the stable foundation that enables everything else. These branches sit in suburbs and small towns from California to Florida, serving customers who still value personal relationships and local decision-making.

The Commercial Bank segment, largely inherited from CIT, operates nationally with offices in major metropolitan areas. This division handles middle-market lending, equipment financing, and specialized verticals like healthcare and technology. With $47 billion in loans, it generates higher yields than traditional banking but requires sophisticated underwriting expertise that took decades to build.

The SVB Commercial segment, maintaining its distinct identity, focuses on venture capital, private equity, and innovation economy banking. Despite the dramatic failure that led to its acquisition, this division's core franchise remains invaluable—relationships with 40% of U.S. venture-backed companies and expertise in exotic instruments like venture debt and warrant structures. The unit generated $1.8 billion in revenue in its first year under First Citizens ownership.

The Rail segment, the $6 billion railcar leasing operation that puzzles analysts, exemplifies the Holdings' contrarian thinking. While not traditional banking, it generates steady cash flow, requires patient capital, and benefits from scale. In an era of supply chain complexity, owning hard assets that move America's goods provides both diversification and inflation protection.

Geographically, First Citizens has achieved something remarkable: true national presence without losing local touch. They're the number-one deposit holder in North Carolina, top-five in South Carolina, but also maintain meaningful presence in California (#8), Florida (#12), and Texas (#15). This isn't the hub-and-spoke model of money-center banks but rather a collection of strong regional franchises united by common ownership and culture.

The deposit franchise deserves special attention. In an era where deposits have become commoditized and rate-sensitive, First Citizens maintains a 65% ratio of non-interest-bearing deposits—extraordinary for a bank without a major investment banking operation. This partly reflects the SVB commercial relationships, where companies keep operating accounts despite low rates. But it also reflects decades of relationship building in communities where First Citizens is often the only bank that never left.

The lending philosophy remains stubbornly traditional despite the bank's dramatic growth. Commercial loans comprise 68% of the portfolio, but with average loan-to-value ratios of just 55% and debt service coverage ratios exceeding 1.5x. They've largely avoided commercial real estate speculation, keeping exposure below 20% of loans compared to 30-40% at peer banks. The consumer book is even more conservative—primarily prime mortgages and auto loans to existing customers.

What makes First Citizens special isn't any single brilliant strategy but rather the patient accumulation of competitive advantages. Their cost of funds is 50 basis points below peers. Their efficiency ratio of 58% beats the 65% industry average. Their net interest margin of 3.4% exceeds most regional banks. None of these advantages alone is insurmountable, but together they create a fortress.

The technology strategy embodies this incremental advantage philosophy. While neobanks burn billions on customer acquisition and megabanks build proprietary trading platforms, First Citizens invests in mundane but crucial capabilities: automated underwriting that reduces decision time from days to hours; APIs that integrate with clients' accounting systems; risk management systems that aggregate exposure across all four segments in real-time.

The acquisition integration capability might be First Citizens' most underappreciated asset. They've developed playbooks, technologies, and teams that can absorb new banks in months, not years. This isn't just about cost synergies—though they consistently achieve 130% of targeted savings. It's about maintaining business momentum during integration, keeping employees engaged, and preserving customer relationships. The fact that SVB's deposit retention exceeded 80% despite the traumatic failure speaks to this capability.

Capital allocation remains disciplined despite abundant opportunities. The bank maintains a 12.5% Tier 1 capital ratio, well above the 10% regulatory requirement for their size. They've authorized $3.5 billion in share buybacks but execute opportunistically rather than mechanically. Dividends yield just 2% but have grown for forty-seven consecutive years. The message is consistent: preserve capital for opportunities, return excess to shareholders, never stretch for growth.

The risk management framework, overseen by Hope Holding Bryant, deserves particular credit. While SVB failed due to interest rate risk, First Citizens maintains one of the industry's most conservative securities portfolios—primarily short-duration governments and agencies. They hedge extensively but simply, using basic swaps rather than complex derivatives. Credit underwriting remains centralized for large loans, preventing the delegation drift that doomed many competitors.

Looking forward, First Citizens faces the classic challenge of all successful acquirers: organic growth. The bank's normalized organic loan growth is just 4-5% annually, below the 7-8% peer average. This isn't concerning yet—they have plenty of integration work ahead—but eventually, they'll need to prove they can grow without buying. The early signs are encouraging: the SVB division is winning new mandates, CIT's middle-market lending is expanding, and the traditional bank continues its steady march through the Southeast.

IX. Bear & Bull Cases

The Bull Case: A Generational Opportunity Perfectly Executed

The optimistic view starts with valuation. Despite the 250% stock price gain, First Citizens trades at just 1.3x tangible book value compared to 1.6x for peers. Apply a peer multiple and the stock has 20% upside from current levels. But that assumes First Citizens is just another regional bank, which fundamentally misunderstands what they've built.

The SVB acquisition alone could drive years of outperformance. First Citizens paid effectively nothing for a franchise that generated $3 billion in annual revenue before its collapse. Even assuming 30% revenue degradation, the acquisition math is extraordinary. More importantly, they gained capabilities that would take decades to build organically—venture debt expertise, Silicon Valley relationships, and innovation economy exposure that positions them for America's economic future.

The family control structure, often viewed as a governance negative, is actually the ultimate competitive advantage. While public company CEOs optimize for quarterly earnings and their own tenure, the Holdings can make decade-long bets. This patient capital advantage only grows more valuable as markets become more short-term oriented. The next banking crisis—and there's always a next crisis—will find First Citizens ready to acquire while others are struggling to survive.

The integration track record suggests execution risk is minimal. Twenty-five successful acquisitions create pattern recognition and muscle memory. The same team that integrated tiny North Carolina thrifts successfully absorbed CIT's complex commercial operations and SVB's exotic venture banking. This isn't luck; it's competence compounding over decades.

Regulatory relationships represent an underappreciated moat. First Citizens has become the FDIC's preferred buyer for complex resolutions. This isn't just about reputation—it's about proven capability to execute under pressure. As banking continues consolidating, this relationship becomes increasingly valuable. The FDIC literally cannot afford to lose First Citizens as a willing acquirer.

The geographic and business diversity created through acquisitions provides multiple growth vectors. The Southeast population boom benefits the traditional banking franchise. The innovation economy recovery drives SVB commercial banking. Rising interest rates help the securities portfolio. Economic normalization aids CIT's middle-market lending. It's hard to envision a scenario where all cylinders aren't firing.

The Bear Case: Icarus Flying Too Close to the Sun

The pessimistic view begins with integration risk. First Citizens has never absorbed anything approaching SVB's complexity—exotic products, entitled employees, and a culture that couldn't be more different from North Carolina banking. The 80% deposit retention might not hold as venture capitalists recover from their crisis gratitude. Key bankers could leave once retention bonuses expire, taking crucial relationships with them.

The family control structure that enabled rapid growth could become an albatross. Fourth-generation Holdings might lack the competence or commitment of their predecessors. Succession disputes could paralyze decision-making. The dual-class structure prevents market discipline, potentially enabling value-destructive empire building. Corporate governance advocates increasingly oppose such structures, potentially leading to regulatory pressure or index exclusion.

Concentration risk has expanded dramatically. First Citizens now has massive exposure to venture capital and private equity, sectors known for boom-bust cycles. The next tech downturn could reveal that SVB's problems weren't just duration mismatch but fundamental business model flaws. The bank's conservative DNA might reject the risk-taking necessary for innovation economy banking.

The regulatory compact could shift unfavorably. First Citizens is approaching the $250 billion asset threshold that triggers enhanced supervision. Stress testing, resolution planning, and heightened capital requirements could constrain the opportunistic acquisition strategy. Regulators who welcomed First Citizens as a crisis solution might view them differently as a systemic risk.

Cultural dilution poses a subtle but serious threat. Each acquisition brings employees with different values and practices. The conservative underwriting culture that protected First Citizens through multiple crises could erode as they absorb more aggressive lenders. The family's influence diminishes as the organization grows beyond their ability to personally shape culture.

Market structure evolution could undermine the entire strategy. Branch banking continues declining as digital natives avoid physical locations. Venture debt might get disrupted by private credit funds with more flexibility. Middle-market lending faces competition from direct lenders and fintechs. First Citizens could find itself perfectly positioned for yesterday's banking industry.

The valuation discount might persist or widen. ESG-focused investors increasingly exclude dual-class companies. Index funds can't buy shares proportional to market cap due to limited float. The family's controlling stake creates acquisition overhang—nobody will bid for First Citizens without Holding approval. These technical factors could permanently constrain multiple expansion.

The Balanced View

Reality likely lies between these extremes. First Citizens will probably successfully integrate SVB and continue generating above-average returns, but unlikely to maintain the spectacular growth of recent years. The family control structure will remain both advantage and limitation. The bank will prosper in the next crisis but face tougher competition in normal times.

The key question isn't whether First Citizens succeeded—they clearly have—but whether that success is sustainable. Banking history is littered with regional champions who expanded too fast, lost their culture, and ultimately failed or were absorbed. First Citizens has defied this pattern so far, but the true test comes over the next decade as they digest their massive acquisitions and prove they can thrive without crisis-driven opportunities.

X. Playbook: Lessons for Founders & Investors

The First Citizens story offers profound lessons that extend far beyond banking. Whether you're building a startup, managing a portfolio, or thinking about corporate governance, the Holdings' century-long journey provides a masterclass in patient capital, opportunistic execution, and the power of aligned incentives.

Lesson 1: Build Trust Before You Need It

First Citizens spent decades becoming the FDIC's preferred acquirer. They took small deals nobody wanted, executed flawlessly, and never renegotiated after winning. This wasn't about any single transaction—it was about becoming the automatic phone call when complex problems arose. When SVB collapsed, the FDIC knew First Citizens could execute because they'd done it twenty times before.

For founders, this means cultivating relationships with potential acquirers, partners, and investors years before you need them. For investors, it means maintaining reputation for fair dealing even when you could extract more value. Trust compounds faster than capital, but only if you never break it.

Lesson 2: Concentration and Diversification Aren't Opposites

First Citizens appears paradoxical—concentrated family ownership but diversified business lines, focused on traditional banking but opportunistic in acquisitions, conservative in underwriting but aggressive in expansion. The lesson: concentrate decision-making power while diversifying operational risk. The Holdings could make bold bets precisely because their core business was so stable.

This principle applies broadly. Venture capitalists concentrate capital in few deals but diversify across vintages. Successful founders maintain controlling stakes but hire diverse expertise. The key is distinguishing between decisions that require consistency (strategy, culture) and those that benefit from variety (tactics, execution).

Lesson 3: Arbitrage Time Horizons

The Holdings' greatest advantage wasn't intelligence or capital but time horizon. While public markets obsessed over quarterly earnings, they planned in decades. This temporal arbitrage enabled them to maintain excess capital for opportunities, invest in relationships with unclear payoffs, and survive periods of underperformance that would end other CEOs' careers.

For investors, this suggests focusing on companies with structural advantages in long-term thinking—family control, dual-class shares, or founder leadership. For operators, it means creating structures that enable patience. The quarterly earnings call is the enemy of strategic thinking.

Lesson 4: Speed Comes from Preparation, Not Haste

First Citizens completed the SVB acquisition in a weekend, but they'd been preparing for fifteen years. They had models ready, teams assembled, and playbooks written. When opportunity arose, they didn't need to think—just execute. Speed wasn't about moving fast but about having already done the thinking.

This preparation principle scales. Successful acquirers maintain standing diligence teams. Great investors have frameworks for rapid decision-making. Winning founders pre-negotiate term sheets before fundraising. The moment of decision is too late to start preparing.

Lesson 5: Culture Is the Only Sustainable Moat

First Citizens' true competitive advantage isn't their deposit franchise or regulatory relationships but their culture of conservative underwriting and patient capital. This culture survived three generations, dozens of acquisitions, and multiple crises. It's the only thing competitors cannot replicate.

Building durable culture requires deliberate action. The Holdings achieved this through stories (retelling founder legends), structures (dual-class shares enforcing values), and selection (promoting only those who embody principles). Culture isn't what you say but what you reward and punish over decades.

Lesson 6: Governance Innovation Is Strategic Innovation

The dual-class structure that enables Holding family control isn't a historical accident but deliberate strategy. By separating economic ownership from voting control, they created a system that encourages long-term thinking while accessing public markets. This governance innovation was as important as any product innovation.

Modern founders should think similarly about governance as strategy. Supervoting shares, controlled company provisions, and staggered boards aren't just defenses but tools for executing long-term visions. The key is using these tools to create value, not just preserve control.

Lesson 7: Roll-Ups Work When Operations Matter More Than Synergies

First Citizens succeeded where many roll-ups fail because they focused on operational excellence rather than cost synergies. Each acquired bank was improved through better underwriting, technology, and capital allocation—not just cost-cutting. The synergies were real but secondary to operational improvements.

This challenges conventional M&A wisdom that prioritizes immediate cost savings. Sustainable value creation comes from making acquired assets perform better, not just cheaper. This requires operational expertise, not just financial engineering.

Lesson 8: Crisis Creates Opportunity for the Prepared

Every major First Citizens expansion coincided with crisis—the Great Depression, S&L crisis, 2008 financial crisis, COVID pandemic, and 2023 regional bank failures. While others retreated, First Citizens advanced. But this wasn't blind contrarianism—they had the balance sheet, expertise, and relationships to act when others couldn't.

The lesson extends beyond banking. Economic disruptions create discontinuities that prepared operators can exploit. But preparation requires maintaining capacity (capital, talent, relationships) during good times when it seems wasteful. The price of opportunism is patience.

Lesson 9: Family Businesses Can Scale

Conventional wisdom suggests family businesses cannot scale beyond certain size or complexity. First Citizens disproves this, growing from a single branch to a $220 billion institution while maintaining family control. The key was professionalizing management while preserving family governance—separating ownership from operation.

This model could inspire a new generation of scaled family enterprises. Technology makes coordination easier. Capital markets increasingly accept dual-class structures. The advantages of aligned, patient capital only grow as markets become more short-term focused.

Lesson 10: Success Requires Both Offense and Defense

First Citizens mastered the paradox of simultaneous conservatism and aggression. Conservative underwriting provided the capital for aggressive acquisitions. Patient deposit gathering funded opportunistic lending. Strong defense enabled overwhelming offense when opportunities arose.

Most businesses fail by overemphasizing one dimension. Aggressive companies flame out in downturns. Conservative companies miss transformational opportunities. First Citizens shows that with proper structure and culture, you can excel at both—but only if you accept lower returns during normal times as the price of extraordinary returns during disruptions.

These lessons coalesce into a unified philosophy: build institutions, not just businesses. The Holdings didn't optimize for their own wealth but for multi-generational durability. They sacrificed short-term returns for long-term dominance. They chose control over liquidity. These trade-offs seem irrational to quarterly capitalism but obvious to anyone thinking in centuries.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube