East West Bancorp: Building the Financial Bridge Between Two Worlds

I. Introduction: A Bank Born of Exclusion, Built for Connection

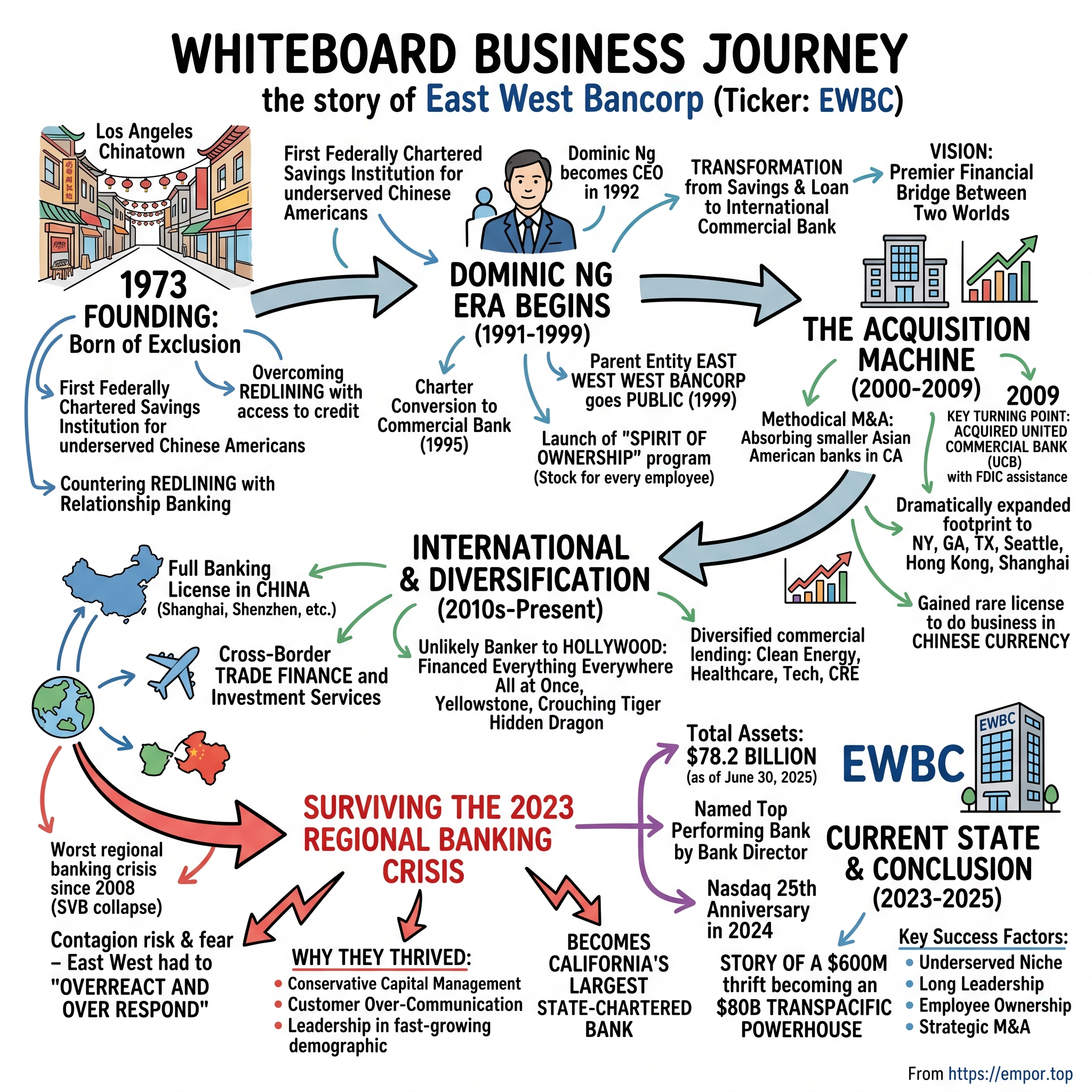

Picture the streets of Los Angeles' Chinatown in early 1973—narrow lanes bustling with immigrant families, small grocers arranging wares, and community elders gathering in tea houses to discuss life in this new land. Among them, eight visionaries—F. Chow Chan, Betty Tom Chu, Richard K. Quan, Gilbert L. Leong, Philip Chow, John A. Nuccio, Christopher L. Pocino, and John M. Lee—were about to challenge an unspoken rule of American banking: that Chinese immigrants didn't deserve access to credit.

East West Bank was founded in 1973 in Los Angeles' Chinatown neighborhood to primarily serve the needs of Chinese Americans who faced significant barriers in accessing financial services from mainstream banks. This initiative of its eight co-founders made it the first federally chartered savings institution focused on this underserved population.

The problem wasn't just bureaucratic inconvenience. Founded amid widespread discrimination against Asian immigrants, the bank opened its first branch in Chinatown to provide essential loan and deposit services, including home mortgages and auto financing, to individuals overlooked by mainstream financial institutions. The bank focused on building trust within the immigrant population by offering accessible banking options in an era when redlining and bias limited credit availability in minority neighborhoods.

Fast forward fifty-two years, and the arithmetic is staggering. East West Bancorp, Inc. is a public company with total assets of $78.2 billion as of June 30, 2025. The Company's wholly-owned subsidiary, East West Bank, is the largest independent bank headquartered in Southern California, and operates over 110 locations in the United States and Asia.

The central question of this story is compelling: How did a tiny savings & loan, started in LA's Chinatown to serve families shut out of the mainstream banking system, become the premier financial bridge between the world's two largest economies?

The answers lie in visionary leadership, opportunistic M&A, niche specialization as a competitive moat, and a culture of survival that turned the 2023 regional banking crisis from existential threat into market opportunity. Dominic Ng has been the CEO of Los Angeles-based East West Bank since 1992, and chairman and CEO since 1998, transforming it from a savings and loan association into an international commercial bank.

"Looking back on 2024, East West marked another year of record revenue, net income and EPS, generating a 17% return on average tangible common equity for shareholders," said Dominic Ng. "We grew deposits by over $7 billion, reflecting the strength of our customer relationships."

What follows is the full story of how a $600 million community thrift became an $80 billion transpacific powerhouse—and what it means for investors watching the next chapter unfold.

II. Founding & Early Years: Serving the Underserved (1973-1990)

The Origin Story: When the System Says No

In 1973, the American Dream came with fine print. For Chinese immigrants arriving in Los Angeles, the largest Chinatown in the United States was a vibrant hub of culture and commerce—but also a reminder of their outsider status. Mainstream banks didn't just neglect these communities; they actively excluded them through redlining, language barriers, and cultural indifference.

When mainstream banks fall short of serving minority communities or immigrants, these groups often face prolonged struggles, waiting for more inclusive solutions or settling for the bare minimum. But in 1973, a group of Asian Americans decided to challenge the status quo. They sought to address these unmet financial needs and took a decisive stand to change this reality.

The path to founding a bank proved almost as difficult as the discrimination the founders sought to overcome. Building a bank from the ground up was a formidable challenge for this minority group. To overcome obstacles, they sought support from friends and allies within the Italian American community to become part of the founding organization, as the government policies at the time did not acknowledge Asian Americans as bank founders.

On January 2, 1973, East West Federal Savings Bank officially opened its doors. The bank was specifically established to address the financial needs of the underserved Chinese American community. At the time, many Chinese immigrants faced significant discrimination and barriers to traditional banking services, including limited access to loans and deposits, prompting a group of community leaders to create an institution tailored to their requirements.

Countering Redlining with Relationship Banking

The founding mission was deceptively simple: help families buy homes, finance cars, and build small businesses. But in practice, this meant building an entirely new model of community banking.

The bank recognized the cultural and linguistic challenges Chinese Americans had faced at the time. Because many community members were more comfortable speaking Mandarin or Cantonese, the bank employed bilingual staff who could communicate in these languages, making it easier for them to navigate banking processes and understand financial products.

This wasn't just good social policy—it was good business. By focusing on the specific needs of the Chinese American community, East West Bank aimed to build a strong foundation of trust. The bank also played a role in promoting financial literacy, providing educational resources and guidance on topics such as budgeting, saving, investing and credit management.

Steady Early Growth

The first two decades were marked by patient expansion within Southern California's growing Asian American communities. From 1979, East West Bank began expanding into surrounding neighborhoods such as Montebello, Silver Lake, Artesia, South Pasadena and other San Gabriel Valley cities. This expansion continued through the 1980s, driven by the growing Chinese American community. In 1984, the headquarters were relocated from Los Angeles' Chinatown to San Marino, California, to better serve suburban communities.

During its early years through the 1980s, East West Bank expanded modestly within Southern California, reaching approximately 10 branches by 1990. By 1991, its assets had grown to approximately $600 million.

Six hundred million dollars. Ten branches. A respectable community thrift serving a loyal niche. But the story was about to take a dramatic turn—and his name was Dominic Ng.

III. The Dominic Ng Era Begins: Transformation (1991-1999)

Inflection Point #1: A Hong Kong Immigrant Takes the Helm

Dominic Ng (born 1959) is a Hong Kong-born American banker. Born in Hong Kong to Chinese parents as the youngest of six children, Ng immigrated to the United States to attend the University of Houston, where he earned a bachelor's degree, and later became a certified public accountant.

Before joining East West, Ng had carved out a distinctive career path. Prior to East West Bank, Ng spent 10 years in Houston and Los Angeles with Touche Ross, which later became Deloitte & Touche. He served in a senior role in the banking practice as well as a marketing role as Head of the Chinese Business Service Group. At the time, there was great potential for overseas investment in California. He also witnessed how the firm benefitted from the advisory service demand from Asia and saw parallel needs in financial services.

This background proved formative. That influenced his strategy when he joined East West Bank as CEO in 1992.

The bank's growth accelerated in 1991 when the Nursalim family of Indonesia acquired it, followed by the appointment of Dominic Ng as president and CEO in 1992.

In 1992, Ng became East West Bank's president and CEO. At the time, the bank was a $600 million savings and loan association. Ng expanded on the bank's original mission of financing underserved Chinese immigrants, growing the bank's business internationally.

The Vision: "Financial Bridge Between East and West"

Ng didn't just want to run a successful community bank. He wanted to transform East West into something that had never existed: a mid-sized American bank purpose-built for the emerging U.S.-China economic relationship.

When Ng became CEO of East West Bank in 1992, he felt that the bank had an obligation and responsibility to not just provide banking services, but to help immigrants expand beyond their communities and cross over into the mainstream. "I told the board that I wanted to make the bank recognized as the premier financial bridge between the East and West and acknowledged for delivering relationship-based solutions to an increasingly diverse and sophisticated customer base."

He leveraged his Asia connections with mainstream American companies and made East West a commercial bank in 1995, allowing it to handle international trade financing. Ng adapted the bank's mission to become what he describes as "the financial bridge between the East and the West".

Inflection Point #2: Charter Conversion & IPO

The first major structural move came during the savings and loan crisis, which Ng saw not as a threat but as an opportunity.

In 1991, during the savings and loan crisis, the company acquired Pacific Coast Savings, which increased the bank's assets from $600 million to $1 billion and expanded operations to San Francisco, California.

Ng converted East West's savings and loan charter into a commercial bank charter in 1995. "We had customers with business and family ties in Asia, so it made sense to support them with trade financing services. That expertise was not common at the time… In time, East West expanded its capabilities and grew to a size where we could compete with national banks."

East West became a state-chartered commercial bank on July 31, 1995.

In 1998, Ng engineered East West Bank's sale in a management-led buyout. He became the bank's chairman that same year. The bank's parent entity, East West Bancorp, went public in 1999.

Culture Building: The Spirit of Ownership

As Ng prepared for the IPO, he made a decision that would define the company's culture for decades.

Dominic Ng has served as chief executive of East West Bank for more than three decades, overseeing the bank's transition to a public company 25 years ago. As a part of the bank's transition to a public company, Ng started the Spirit of Ownership program where every East West employee – full time or part time and regardless of job title – receives the same amount of stock in the company every year.

He launched the Bank's "Spirit of Ownership" program in preparation for the Bank's public listing. The annual program grants every employee, whether full- or part-time, stock distributions at Lunar New Year—a time that celebrates the Bank's roots in the Asian American community.

"What is very important for me is that every single person gets stock, and every single person gets exactly the same amount," Ng said. "That's the whole idea about the Spirit of Ownership is that we all are shareholders of East West Bank. I, as CEO, work for every one of my employees because every one of them is a shareholder at East West Bank." Ng attributes the bank's sustainable growth in part to this program as he believes it empowers employees to perform their best as the bank's success is their success.

Currently, that translates to $2,000 in stock annually. For employees who began accumulating stock at the start of this program when a share cost around $5, the impact of this program can be vast as East West stock sat at $101.69.

By 1999, Ng had transformed a $600 million community thrift into a publicly traded commercial bank with international ambitions. The stage was set for the next phase: aggressive M&A.

IV. The Acquisition Machine (2000-2009)

Building Scale Through M&A

The early 2000s saw Ng execute a deliberate consolidation strategy, primarily targeting smaller Asian American-focused banks in California.

In 1999, the company acquired First Central Bank for $13.5 million in cash.

In 2004, East West acquired Trust Bank, a Chinese American bank based in Monterey Park, California, with four branches and $235 million in assets, for $32.9 million. In 2005, the company acquired United National Bank, a commercial bank headquartered in San Marino, California, with 11 branches and $665 million in loans receivable, for $177.9 million. In 2006, the company acquired Standard Bank, a Chinese-American bank headquartered in Monterey Park, California, with 6 branches and $923 million in assets, for $200 million.

The pattern was clear: East West was methodically absorbing competitors in its core niche, building density in markets with significant Asian American populations while acquiring trained staff and established customer relationships.

Inflection Point #3: The United Commercial Bank Acquisition (2009)

The 2008 financial crisis devastated the banking industry. But for Ng—who had already navigated the S&L crisis of the early 1990s—it presented a once-in-a-generation opportunity.

East West would not be where it is today if not for a critical turn two years ago. Dominic Ng, who took the helm of the bank in 1992 amid the savings and loan crisis, had an uneasy feeling about the weakening housing market in spring 2008. "I saw enough signs out there in the market that this crisis can potentially match what happened in the early '90s – and it turned out to be much worse, right?" recalled Ng. "I said, 'You know, we better get serious,' and that's what we did." So before its peers faced up to the severity of the looming troubles, East West decided to tackle its problems head-on.

When United Commercial Bank—East West's closest competitor and San Francisco's largest Asian American bank—began to fail, Ng moved quickly.

The California Department of Financial Institutions closed United Commercial Bank on November 6, 2009, and appointed the Federal Deposit Insurance Corporation as the bank's receiver. The bank's operations were merged into East West Bank.

East West Bancorp announced that it had acquired the banking operations of San Francisco, California based United Commercial Bank (UCB) in a Federal Deposit Insurance Corporation (FDIC) assisted transaction. Under the terms of the transaction, East West received $10.4 billion in assets, including $7.7 billion in loans, and assumed $9.2 billion in liabilities, including $6.5 billion in deposits of UCB. The FDIC and East West entered into a loss sharing agreement covering substantially all acquired loans. This strategically compelling and financially attractive transaction created the second largest independent bank headquartered in California and the largest bank in the nation focused on serving the Asian American community.

The brilliance of this deal lay in its structure. With the acquisition of the operations of UCB through an FDIC assisted transaction, East West substantially increased its asset size from $12.5 billion to approximately $19 billion with minimal credit risk on the acquired loan portfolio as a result of the loss sharing agreement. The $500 million in capital raised along with the FDIC loss sharing protection on the acquired loan portfolio positions East West with industry leading, fortress-like capital that further cements the safety and security of East West for all our customers.

In late 2009, the Federal Deposit Insurance Corp. contacted 51 banks requesting bids for United Commercial's assets, should it fail. Ng took immediate action, working the phones and trying to convince investors of the benefits of such an acquisition, which offered limited downside due to FDIC loss-sharing support. In a matter of days, East West raised $500 million. "We raised so much capital – well in excess of what was needed," Ng said.

The acquisition dramatically expanded East West's footprint, giving it branches in the Bay Area, as well as in New York, Boston, Atlanta, Seattle, Houston, Hong Kong and Shanghai. Along with the overseas branches, East West also gained a valuable and rare license to do business in Chinese currency, which had been held by United Commercial. The license, which can be difficult to obtain for U.S. businesses, will give East West greater ability to penetrate the Chinese market, Ng said.

The stock market and East West has seen the acquisition of UCBH as "highly accretive," and shares of East West jumped as much as 57% to touch a high of $13.57 on the first day of trading after the acquisition.

V. International Expansion & China Strategy (2003-2015)

Inflection Point #4: Full Banking License in China

While most American regional banks were content to serve domestic markets, Ng had grander ambitions. He recognized that serving Asian American entrepreneurs meant understanding their cross-border business needs.

It first opened a location in Beijing in 2003, and then based its China operations out of Shanghai in 2009. It's one of just a few U.S.-based banks to have a full banking license in China.

In China, East West has full-service branches in Shanghai, Shenzhen, Shantou and Hong Kong; and representative offices in Beijing, Guangzhou, Chongqing and Xiamen. East West also has a representative office in Singapore. For over 50 years, their financial bridge has extended and strengthened. Their unique cross-border infrastructure, deep understanding of U.S.-Asia markets, vast resources and connections have helped many companies expand to the global market.

The China subsidiary developed comprehensive capabilities. East West Bank (China) Limited is a wholly owned subsidiary of East West Bank and a locally incorporated foreign bank in mainland China. It is headquartered on the 33rd floor of Jin Mao Tower, a landmark building in Shanghai Lujiazui. East West Bank China is well positioned to meet the diverse financial needs of clients by leveraging its parent company's unique bridge banking strategy and vast resources and network. East West Bank China offers comprehensive commercial banking services for bilateral trade and investment activities from the U.S. to China and vice versa. They help U.S. companies enter the Chinese market by providing cash management and financial solutions. They also support Chinese companies' direct investment in the U.S. by providing specialized banking services and value-added services.

Trade Finance & Cross-Border Banking

CFO Christopher Del Moral-Niles has articulated why this international focus is so valuable for a regional bank.

"That's a role usually played sometimes by larger international banks, but for this sub market — for the Asian community, smaller businesses — we have played a key role, and have grown with many of those to be a sizable player in that cross border market," Del Moral-Niles said. "Which is somewhat unique for a regional bank."

Without much competition in this arena, Ng said East West is the "go-to" bank when it comes to Asian markets. He also identified this as a key factor in how the bank was able to double its assets in the last decade without any M&A activity.

MetroCorp Bancshares Acquisition (2014)

The acquisition strategy continued with geographic expansion into Texas.

In 2014, East West acquired MetroCorp Bancshares, which operated as MetroBank, for $268 million in cash and stock.

Key milestones included acquisitions such as Trust Bancorp in 2004, adding a $235 million asset bank in California; United National Bank in 2005, incorporating 11 branches in San Francisco; and MetroCorp Bancshares in 2013, enhancing presence in Texas markets including Houston and Dallas. These moves expanded the bank's footprint beyond California to national and international operations, with a focus on cross-border trade finance linking the U.S. and Asia.

VI. Diversification: Entertainment & New Verticals (2010-Present)

Inflection Point #5: Hollywood's Unlikely Banker

Perhaps the most surprising chapter in East West's evolution is its emergence as a major entertainment financier. The genesis was characteristically opportunistic.

After the 2008 financial crisis, Ng expanded the bank's financing into the entertainment industry.

East West is known for helping finance major films and television shows, including Everything Everywhere All at Once, Yellowstone, and Orange is the New Black.

The entertainment strategy leveraged East West's geographic positioning and cross-border expertise. East West Bank China has established solid and long-term relationships with Chinese TV and film studios and production companies, and has financed many local movies, TV shows and online TV series. East West Bank is headquartered in Los Angeles, one of the world's entertainment capitals. They have established solid relationships with major movie studios in the U.S. and financed the production of many Hollywood movies and TV series. These projects have performed well at the box office. Some also have been nominated for or have received Academy, Golden Globe or Emmy Awards.

Bennett Pozil, Executive Vice President at East West Bank, became the face of this initiative. Pozil oversees corporate banking in the U.S. and Asia for East West Bank and has financed many hours of programming in China on iQIYI, Youku, Tencent and Mango TV, including hit streaming series "The Knockout." In the U.S., Pozil shepherded financing for Tyler Perry's programming for BET, Netflix and Amazon, as well as content for Lionsgate and Starz.

The entertainment lending team has made over $1.8 billion in loans since 2011 to finance the production and distribution of film and TV products in the US and China markets. For example, East West Bank was the lead lender for the production of Crouching Tiger, Hidden Dragon: Sword of Destiny (2016), and worked with Le Vision Pictures in the financing of its share of the biggest US-China co-production Great Wall (2016). Other high profile financing projects include The Hunger Games franchise and Silver Linings Playbook (2012), several popular Netflix drama series including Orange is the New Black and Marco Polo.

Media and entertainment lending has expanded substantially under Pozil's leadership, making East West Bank one of the premier entertainment financers in both the US and Greater China, and the only bank with a significant presence in both markets. With strong ties in the entertainment industries of both countries, East West Bank is able to add value in financing and facilitating landmark partnerships.

Multi-Sector Expansion

Entertainment was just one dimension of an increasingly diversified commercial banking platform.

As of 2025, the company is involved in commercial banking, residential lending, private equity, media, entertainment, infrastructure, healthcare, clean energy, technology, manufacturing, commercial real estate, and other sectors.

Ng also focuses on biotech, clean technology, private equity, health care, real estate, renewable energy, sustainability financing, and cross-border business.

The clean energy push has been particularly notable. East West positions itself as the 'go-to' bank for commercial-scale renewable energy project financing.

Convergent Energy and Power, a leading provider of energy storage solutions in North America, announced that it has closed a programmatic tax equity financing deal with East West Bank. The funding will be used for Convergent's New York and Maryland energy storage portfolios, which can provide more cost-effective, reliable, and sustainable electricity to over 8,000 customers.

VII. Inflection Point #6: Surviving the 2023 Regional Banking Crisis

The Crisis Context

March 2023 brought the worst regional banking crisis since 2008. The headline-grabbing collapse of Silicon Valley Bank in March was the first warning sign of what some analysts are calling the first post-pandemic banking crisis. On Friday, March 10, 2023, Silicon Valley Bank failed after a bank run. The collapse of SVB was the 3rd largest bank failure in US history, and the largest since the dark days of the 2008 crash. One fact highlights the scale of the crisis: these three banks combined held more inflation-adjusted assets than the 25 banks that collapsed in the wake of the 2008 financial crisis—combined.

For East West, a California-based regional bank, the contagion risk was immediate and severe. The stock prices of other large regional banks, such as Western Alliance Bancorporation, First Horizon Corp, and East West Bancorp, also significantly dropped. The 2023 bank failures have raised concerns about a system-wide banking contagion.

East West's Moment of Truth

Dominic Ng, CEO of East West Bank, now the largest California-chartered bank, had a front row seat to that last year. Defending his company from the contagion of fear was like "being chased by a bear," Ng says he likes to joke. To outrun the bear, he told Axios, East West had to "somewhat overreact and over respond." That meant over-communicating to even its most loyal customers, and in some cases waiving fees and paying up on interest rates.

East West's chairman and CEO, Dominic Ng, said the regional bank added 40,000 commercial and consumer deposit accounts in 2023, driving loan and deposit growth throughout the second half of the year. No one envied the position regional banks like East West Bancorp of Pasadena, California, were in last year. California was hit hard by the turmoil that roiled the banking industry in the spring. Three of the four banks that failed in March and April were headquartered in the Golden State. Another California institution, PacWest Bancorp in Los Angeles, reported a sharp drop in deposits in the first quarter. Yet six months later, it seems East West has benefited handsomely from the disruption.

Why East West Survived—and Thrived

Once the regional-banking turmoil eased, Dominic Ng found himself head of the biggest surviving California-chartered bank. The deposit base at his Pasadena-based East West Bancorp Inc. grew by $921.4 million, or 2%, in the months after the collapse of its peers.

Since the day before Silicon Valley Bank failed in March 2023, East West has risen 10%, excluding dividends. Analysts say the Southern California bank — which recently reported record deposits — can weather a slowdown thanks to its conservative capital management. What's more, they say its leadership in the fastest-growing demographic in the U.S. bodes well for future growth.

"In part because the bank founders were fairly conservative, and in part because [CEO Dominic Ng] is fairly conservative, the entire approach has been first and foremost, 'let's remain one of the strongest, best capitalized banks in the industry.' From that position of strength, we can do what we need to do to drive the business," CFO Del Moral-Niles said. "And when your customers come to recognize you as that strong bank, then, when things start to go sideways for other banks, you become an attractive alternative for them."

The remaining lenders, including East West Bank, Popular Bank and New York Community Bank each have higher returns and could end up as acquirers rather than targets. KBW estimated banks' long-term returns including the impact of coming regulations.

Becoming California's Largest State-Chartered Bank

In 2023, East West Bank celebrated its 50th anniversary, marking five decades of operations since its founding in 1973. The milestone highlighted the bank's evolution into a major financial institution, with total assets reaching $69.6 billion by year-end, surpassing $68 billion amid strong growth in loans and deposits.

VIII. Current State & Performance (2023-2025)

Industry Recognition

In 2021, 2023, 2024, and 2025, East West earned recognition as the top performing bank in the $50 billion and above asset size category by Bank Director.

The company has been ranked the #1 performing U.S. bank with more than $10 billion in assets by S&P Global Market Intelligence, and the top performing bank in its asset size (in excess of $50 billion) by Bank Director for three straight years since 2023.

Record Financial Performance

Full year 2024 net income was $1.2 billion, or $8.33 per diluted share. Fourth quarter 2024 net income was $293 million, or $2.10 per diluted share. Full-year returns on average assets were 1.60%, returns on average common equity were 15.9%, and book value per share grew 12% year-over-year.

Key 2024 metrics include: Deposit Growth of $7 billion increase, 13% growth to $63.2 billion; Loan Growth where average loans grew by 6% for the year; Net Interest Margin stable at 3.24%; Fee Income Growth of 12% increase in 2024; Efficiency Ratio of 36.9% in the fourth quarter.

Second quarter 2025 net income was $310 million or $2.24 per diluted share. Total loans and deposits both reached new records as of June 30, 2025, at $55.0 billion and $65.0 billion respectively.

Nasdaq 25th Anniversary

In September 2024, the company marked its 25th anniversary on the Nasdaq stock exchange, with CEO Dominic Ng ringing the opening bell.

In his opening bell remarks, Ng highlighted that East West's Nasdaq listing was pivotal for both the public and the Bank's employees. "Getting listed on Nasdaq allowed the public to join us on our journey, and we wanted our associates to share in that as well," said Ng. He launched the Bank's "Spirit of Ownership" program in preparation for the Bank's public listing.

IX. The Playbook: Business & Strategy Lessons

1. Start With an Underserved Niche

East West found a genuine market gap—Chinese immigrants facing discrimination in banking—and built trust by genuinely serving that community. "East West Bancorp targets Asian Americans, so you're just less likely to switch banks if somebody literally speaks Mandarin, versus maybe another bank that doesn't," said CFRA Research analyst Alexander Yokum. "So, it's a big advantage they have just from a stickiness perspective." "Banking is obviously very competitive. There's thousands of banks in the United States. And if you can compete off something besides price, you have an advantage."

2. Visionary, Long-Tenured Leadership

Dominic Ng has served as chief executive of East West Bank for more than three decades, overseeing the bank's transition to a public company 25 years ago.

In 2006, the Los Angeles Times named Ng one of Southern California's 100 most influential people. In 2008, Forbes named Ng as one of 25 notable Chinese Americans. In 2017, American Banker named Ng its "Consistent Performer" in its Banker of the Year awards, noting East West's transformation and credit discipline.

3. Expand the Niche, Don't Abandon It

Without much competition in this arena, Ng said East West is the "go-to" bank when it comes to Asian markets.

With a $69.5 billion asset base and a 29% loan portfolio allocated to residential mortgages—a segment where it holds a near-monopoly among immigrant communities—the bank has mastered the art of serving a demographic that traditional institutions often overlook. As the Asian-American population grows at twice the rate of the U.S. population and commands a $1.2 trillion consumer market, EWBC's strategic positioning is not just defensible but compelling.

4. Opportunistic M&A with FDIC Partnership

The UCB acquisition showed how crisis creates opportunity for well-capitalized, well-managed institutions. The loss-sharing agreement with the FDIC minimized credit risk while providing instant scale.

5. Conservative Capital Management

East West Bank weathered the 2008 financial crisis better than many regional banks due to its conservative lending practices and strong capital position. The bank continued to grow during the recovery period, benefiting from increased U.S.-China trade and investment activity.

East West Bancorp's Common Equity Tier 1 (CET-1) ratio stands at 13%. A typical bank has a CET-1 ratio between 10.5% and 11%, Yokum said.

Current Common Equity Tier 1 Capital Ratio stands at 14.3%.

6. Employee Ownership Culture

The Spirit of Ownership program aligns employee interests with shareholder returns while building institutional loyalty—particularly valuable in relationship banking where client relationships are often tied to individual bankers.

7. Demographic Tailwinds

"Asian Americans are, generally speaking, above-average income, below average in terms of defaulting on their loans," CFRA's Yokum said. "So, it is a good demographic to go after."

X. Competitive Analysis: Porter's Five Forces & Helmer's Seven Powers

Porter's Five Forces Analysis

Threat of New Entrants: LOW The barriers to replicating East West's model are formidable. Building bilingual capabilities, cross-border infrastructure, and regulatory licenses in China takes decades. It's one of just a few U.S.-based banks to have a full banking license in China. Any new entrant would face enormous fixed costs to match East West's geographic footprint and cultural expertise.

Bargaining Power of Buyers (Customers): MODERATE While banking customers can theoretically switch to competitors, East West's niche focus creates switching costs. Customers are "just less likely to switch banks if somebody literally speaks Mandarin, versus maybe another bank that doesn't." The language and cultural barriers that initially excluded Asian Americans from mainstream banking now protect East West from competition.

Bargaining Power of Suppliers: LOW East West's primary "suppliers" are depositors and capital markets. With deposits growing by $7 billion, or 13% growth to $63.2 billion, the bank has demonstrated strong funding capabilities without dependence on any single source.

Threat of Substitutes: MODERATE Fintech companies and large national banks could theoretically serve Asian American communities through technology. However, East West's deep community ties, branch network, and cross-border capabilities create a differentiated offering that pure technology plays struggle to replicate.

Competitive Rivalry: MODERATE East West Bank's competitive advantage lies in its specialized focus on serving Asian American communities and facilitating U.S.-Asia cross-border business. In this niche, the bank competes with other Asian American banks such as Cambridge Bancorp and Cathay General Bancorp, though East West has established itself as the largest independent bank serving this market segment.

Hamilton Helmer's 7 Powers Framework

1. Scale Economies: PRESENT As the largest Asian American-focused bank, East West can spread fixed costs (compliance, technology, international operations) across a larger asset base than competitors like Cathay General Bancorp.

2. Network Effects: MODERATE East West's cross-border network creates some network effects—more customers on both sides of the Pacific make the network more valuable for trade finance and business referrals.

3. Counter-Positioning: STRONG Major banks could theoretically serve Asian American communities but choose not to prioritize this segment. Replicating East West's model would require major banks to develop specialized cultural competencies that conflict with their mass-market positioning.

4. Switching Costs: PRESENT Banking relationships are inherently sticky. Commercial lending relationships, in particular, involve significant switching costs related to credit history, relationship knowledge, and documentation.

5. Branding: STRONG Within Asian American communities, East West has become synonymous with culturally sensitive banking. The bank's 50-year history and community engagement create brand equity that competitors cannot easily replicate.

6. Cornered Resource: MODERATE The rare China banking license and decades of cross-border operational experience represent difficult-to-replicate assets.

7. Process Power: PRESENT East West's expertise in cross-border trade finance and entertainment financing represents accumulated process knowledge that provides sustainable competitive advantage.

XI. Risk Factors & Investment Considerations

Key Risks

1. Geopolitical Tensions To be sure, strong ties with China are also a potential challenge for East West as geopolitical and trade tensions rise between Washington and Beijing.

In light of former President Donald Trump being again elected to the White House this month, Gerard Hoberg, a professor of finance and business economics at USC Marshall, said East West's operations could be affected in a few ways. Trump has recently proposed a 10% tariff on all American imports and a 60% tariff on products made in China. "The most direct and perhaps largest impact would be reduced banking needs across international borders, an area that might be core to East West," Hoberg said.

2. Commercial Real Estate Exposure Like most regional banks, East West has meaningful CRE exposure. While the bank has demonstrated conservative underwriting, prolonged commercial real estate weakness could pressure asset quality.

3. Net Interest Margin Compression In a declining rate environment, net interest margins could face pressure. The bank has managed this well historically but remains exposed to interest rate dynamics.

4. Concentration Risk Heavy focus on Asian American communities and U.S.-China trade creates concentration risk. Economic or political disruptions affecting these segments would disproportionately impact East West.

5. Succession Planning Dominic Ng has led the bank for over 30 years. Succession planning is embedded in the bank's governance framework, with the Compensation Committee periodically reviewing talent development, recruitment, and internal promotions to ensure continuity. Recent examples include the 2023 promotions of Irene H. Oh to Chief Risk Officer and Christopher J. Del Moral-Niles to Chief Financial Officer, both from internal senior roles. However, leadership transition after three decades remains a material consideration.

Bull Case

- Fastest-growing demographic in America (Asian Americans) with above-average income and below-average loan defaults

- Unique cross-border positioning becomes more valuable as U.S.-Asia economic integration deepens

- Conservative capital management provides optionality for opportunistic M&A

- Entertainment and clean energy financing diversify revenue streams

- Top-tier operating metrics (1.60% ROA, 15.9% ROE, 36.9% efficiency ratio) suggest operational excellence

Bear Case

- Deteriorating U.S.-China relations could pressure cross-border business

- California CRE concentration creates tail risk in an extended downturn

- Competition from major banks with greater resources

- Fintech disruption of traditional banking relationships

- Key-person risk with 30+ year CEO tenure

XII. Key Performance Indicators to Track

For long-term investors monitoring East West Bancorp, three KPIs matter most:

1. Net Interest Margin (NIM)

Current: 3.24%

NIM is the bank's profitability engine. East West's ability to maintain NIM through interest rate cycles demonstrates pricing power and deposit franchise strength. Watch for compression below 3.0% as a warning sign.

2. Deposit Growth Rate

2024: 13% growth to $63.2 billion

Deposit growth reflects customer loyalty and the health of the core franchise. "We grew deposits by over $7 billion, reflecting the strength of our customer relationships." Sustained deposit growth above 5% annually would confirm the bank's competitive moat.

3. Common Equity Tier 1 (CET1) Ratio

Current: 14.3%

CET1 ratio measures capital strength. A typical bank has a CET-1 ratio between 10.5% and 11%. East West's materially higher ratio provides both a safety buffer and optionality for M&A or increased shareholder returns. Deterioration below 12% would warrant attention.

XIII. Conclusion: The Bridge to What's Next

Fifty-two years ago, eight Chinese American community leaders in Los Angeles dared to imagine a bank that would serve people the mainstream system had written off. Today, that same institution—transformed beyond recognition in scale but remarkably consistent in mission—stands as California's largest state-chartered bank and America's premier financial bridge to Asia.

The East West story offers lessons that extend beyond banking. It demonstrates how genuinely serving an underserved community can create a durable competitive moat. It shows how visionary, long-tenured leadership can compound value across decades. It proves that opportunistic M&A, executed with discipline, can accelerate strategic positioning without destroying shareholder value. And it reveals how crisis—whether the S&L crisis of the early 1990s, the financial crisis of 2008, or the regional banking panic of 2023—consistently creates opportunity for the prepared.

"We're never going to allow this shop to fall," Ng has said.

For investors, the question is whether East West can continue executing its playbook as geopolitical tensions reshape the U.S.-China economic relationship that has been the bank's runway for growth. The demographic tailwinds remain powerful—Asian Americans are the fastest-growing population segment in America. The competitive moat—cultural expertise, cross-border infrastructure, regulatory licenses—appears durable. And the capital position provides substantial optionality.

What began as a single branch in Chinatown has become a $78 billion institution spanning continents. The bridge between East and West, it turns out, was worth building.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube