Evercore: How an Ex-Treasury Official Built Wall Street's Premier Independent Advisory Firm

I. Introduction & Episode Roadmap

The calendar read December 31, 2008. While most of America celebrated New Year's Eve, investment banker David Ying sat in a conference room advising LyondellBasell Industries, the world's third-largest chemicals company, which stood on the brink of complete collapse. The only way to prevent a total shutdown was to raise $4.75 billion in debtor-in-possession financing—larger than any DIP loan in history. The impossible was accomplished. The deal closed.

This was not the work of Goldman Sachs or Morgan Stanley. This was Evercore.

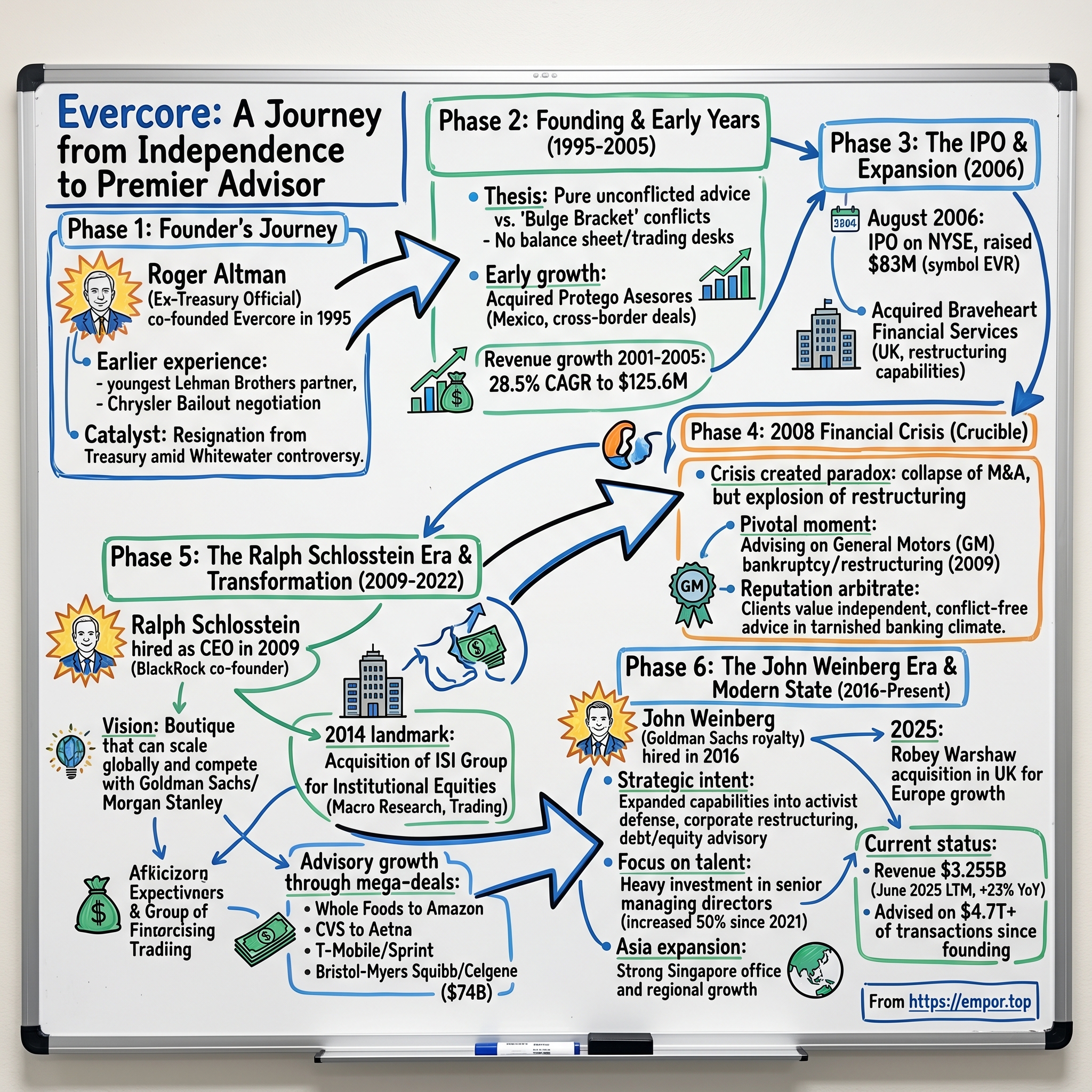

Evercore Inc., formerly known as Evercore Partners, is a global independent investment banking advisory firm founded in 1995 by Roger Altman, David Offensend, and Austin Beutner. The firm has advised on over $4.7 trillion of merger, acquisition, and restructuring transactions since its founding.

That's a staggering number. To put it in perspective, Evercore has advised on deals worth more than twice Japan's annual GDP. And here's what makes it remarkable: they did it without a balance sheet, without proprietary trading desks, without the conflicts of interest that plague bulge bracket banks.

The firm has "been number four in the world in advisory revenues for the last four years, behind Goldman Sachs, JP Morgan and Morgan Stanley." Let that sink in. An independent advisory firm—founded by someone who had just resigned from government amid scandal—now generates advisory revenues that compete with the mightiest names on Wall Street.

The central question driving this deep dive: How did a boutique advisory firm founded by a disgraced Treasury official become the #4 M&A advisor globally, outpunching Goldman Sachs-level competition?

Evercore Inc revenue for the twelve months ending June 30, 2025 was $3.255B, a 23.24% increase year-over-year. Evercore Inc annual revenue for 2024 was $2.996B, a 22.67% increase from 2023.

The themes that emerge from Evercore's story are fundamental to understanding modern finance: the power of independence in an era of conflicts, the premium clients will pay for unconflicted advice, the art of talent attraction in a people-driven business, and the strategic patience required to build something truly durable.

This isn't just a story about investment banking. It's a story about second acts, about counter-positioning against giants, and about what happens when someone decides the best revenge for public humiliation is building something that outlasts everyone who doubted them.

II. Roger Altman: The Founder's Journey

The Boston Kid Who Befriended a Future President

Roger Charles Altman was born in Brookline, Massachusetts, and was raised in Boston as a Catholic. His father, a food broker, died when he was 10 years old, and his mother, a librarian, raised Altman and his brother as a single mother. He attended the Roxbury Latin School.

Loss shapes leaders. Altman's father's death when Roger was just ten forced an early confrontation with life's fragility and the importance of self-reliance. The Roxbury Latin School—one of the oldest schools in America—instilled in him a classical education and an introduction to the East Coast establishment he would later master.

He attended Georgetown University, where he met future President Bill Clinton, and earned a Bachelor of Arts degree in 1967. This friendship—forged in the turbulent late 1960s—would prove fateful, opening doors that would later threaten to close permanently.

In 1969 he earned an MBA from the University of Chicago Booth School of Business, but took time off in 1968 to work in Indiana organizing volunteers for Robert F. Kennedy. The Kennedy campaign represented Altman's early political awakening—a commitment to public service that would alternate with his private sector career throughout his life.

Lehman Brothers: The Youngest Partner

After graduating from business school in 1969, Altman began working at Lehman Brothers, where he grew close to chairman Peter G. Peterson. In 1974, he was made general partner at the age of 28—the youngest in Lehman's history.

Consider what this meant. At 28, in an era when investment banking was dominated by gray-haired patricians, Altman had earned his seat at the table. His mentor, Pete Peterson, would later found Blackstone—a connection that would prove crucial to Altman's own trajectory.

The Chrysler Bailout: Government as Deal-Maker

He left Lehman in 1977 to serve as Assistant Secretary for Domestic Finance in the U.S. Treasury from 1977 to 1981 under President Jimmy Carter, for whom he had fundraised when Carter was Governor of Georgia, and campaigned for in 1976, as well as working on his transition team.

As Assistant Secretary, Altman played a "role in negotiating the Federal Government's $1.5 billion bailout of the Chrysler Corporation."

This was transformative experience. The Chrysler bailout taught Altman how to structure deals involving distressed companies, government stakeholders, unions, and multiple classes of creditors—skills that would later prove invaluable when Evercore advised on GM's bankruptcy three decades later. More importantly, it demonstrated that the government could be a deal counterparty, not just a regulator.

Return to Lehman and the Blackstone Years

In 1981, he returned to Lehman Brothers, where he became the co-head of investment banking and served on the board of the company and the management committee.

In 1987, Mr. Altman joined The Blackstone Group as Vice Chairman, head of the firm's advisory business and a member of its Investment Committee. Mr. Altman also had primary responsibility for Blackstone's international business.

Working alongside Steve Schwarzman and Pete Peterson at Blackstone provided Altman a masterclass in building an independent firm. Blackstone's advisory business was gaining traction just as the leveraged buyout boom was transforming Wall Street. Altman absorbed every lesson about what an independent franchise could become.

The Whitewater Catastrophe

Then came the moment that nearly destroyed everything.

He served as Assistant Secretary of the Treasury in the Carter administration from January 1977 until January 1981 and as Deputy Secretary of the Treasury in the Clinton administration from January 1993 until he resigned in August 1994, amid the Whitewater controversy.

He resigned in 1994, after it was revealed that Altman had notified the Clinton White House of the criminal referrals made by the Resolution Trust Corporation. After nearly 15 hours of testimony in February 1993 before the House and Senate Banking Committees, he submitted his resignation in August 1994, saying that he hoped his resignation would "help to diminish the controversy."

Fifteen hours of Congressional testimony. Public humiliation. The end of a promising government career. Most people would retreat to a quiet corner of Wall Street, collect their investment banking salary, and hope the world forgot.

Roger Altman had other plans.

The Crucial Pivot

In 1995, instead of returning to Blackstone, he co-founded Evercore, an "independent investment banking advisory firm" in New York City.

The decision not to return to Blackstone was telling. Altman had tasted what it meant to build something. At Blackstone, he would always be working for someone else. At Evercore, he would be building his legacy.

"The most meaningful thing I ever did in business was found and build up Evercore," Altman later said.

III. Founding & Early Years (1995-2005)

Building Without a Balance Sheet

The thesis behind Evercore was elegant in its simplicity: clients deserve advisors whose only interest is giving the best possible advice. At bulge bracket banks, the conflicts were endemic. The bank advising you on an acquisition might also be lending to your target, trading your securities, or hoping to win the financing mandate. How could you trust the advice?

Evercore would be different. Pure advisory. No balance sheet to deploy, no trading books to protect, no lending relationships to preserve.

In 1995, Roger Altman founded Evercore Partners as an independent investment banking advisory firm in New York City, drawing on his prior experience at Lehman Brothers and Blackstone to emphasize conflict-free advice for clients in mergers, acquisitions, and restructurings. The firm's model prioritized advisory services unbound by the lending or trading obligations of bulge-bracket banks, positioning it as a boutique alternative focused on senior-level counsel.

The other founding partners were David Offensend and Austin Beutner—both former Blackstone colleagues who believed in the vision. Beutner would later become Los Angeles' superintendent of schools, demonstrating the public service ethos that permeated the firm's culture.

The Early Credibility Challenge

Building a boutique advisory firm without a balance sheet requires one critical ingredient: credibility. CEOs and boards hire advisors they trust. Trust takes time to establish. Evercore needed to win early mandates to prove it could compete.

The firm emphasized something revolutionary for the time: senior bankers would do the actual work. At bulge brackets, senior partners won the pitch, then handed off execution to armies of associates. At Evercore, the people in the room when you signed the engagement letter would be the same people negotiating your deal.

Evercore provided advisory services to prominent multinational corporations on significant mergers, acquisitions, divestitures, restructurings and other strategic corporate transactions. The senior leadership comprised Roger Altman, the former U.S. Deputy Treasury Secretary and Vice Chairman of The Blackstone Group; Austin Beutner, a former General Partner of The Blackstone Group; and Eduardo Mestre, the former head of Citigroup's Global Investment Bank.

Eduardo Mestre, prior to joining Evercore, was chairman of Citigroup's investment banking division, head of investment banking at Citigroup and its predecessor firms, and co-head of Salomon Brothers' M&A department.

The hiring of Mestre was critical. This wasn't some scrappy startup—Evercore was assembling the finest minds in dealmaking, people who had run divisions at the world's largest banks and were choosing to work at an independent firm.

Geographic Expansion

In 2006, the firm integrated offices in Mexico City and Monterrey through its acquisition of Protego Asesores, bolstering capabilities in Latin American energy and project finance deals. These moves extended the firm's reach into high-growth markets, enabling it to handle an increasing volume of cross-border mandates; for instance, a 2008 strategic alliance with Brazil's G5 Advisors facilitated joint advisory on South American M&A, while a partnership with Mizuho Securities supported U.S.-Japan transactions.

These alliances demonstrated strategic foresight. M&A was becoming increasingly global. A firm that could advise on cross-border deals would have advantages over purely domestic competitors.

The firm achieved significant expansion, with revenues growing from $46.0 million in 2001 to $125.6 million in 2005 at a compound annual rate of 28.5%, reflecting an increase from its initial three senior managing directors to a broader professional team.

Compounding revenue at nearly 30% annually for five years demonstrated product-market fit. Clients wanted what Evercore was selling.

IV. The IPO & Going Public (2006)

Inflection Point #1: Access to Public Markets

On August 10, 2006, Evercore Partners Inc. announced that its initial public offering of 3,950,000 shares of its Class A common stock had been priced at $21.00 per share. The shares began trading August 11, 2006, on the New York Stock Exchange under the symbol "EVR."

In August 2006, Evercore completed its initial public offering (IPO) on the New York Stock Exchange, raising approximately $83 million. The IPO marked a significant milestone in the company's growth trajectory, providing capital for expansion and enhancing its profile in the financial services industry.

Trading debuted strongly, with shares rising 18% on the first day, reflecting investor confidence in Evercore's independent advisory model and its track record in high-value transactions.

Why go public? The answer reveals Altman's long-term thinking. Public currency enables acquisitions. Public markets impose discipline. Public disclosure attracts talent who want to see financial results tied to performance. And there was another benefit: permanence. A public company outlives its founders.

Lehman Brothers Inc. was the sole book-running manager for the offering. Goldman, Sachs & Co. and JPMorgan were joint lead managers.

The irony was delicious. Lehman Brothers—the firm where Altman started his career—led the IPO of the boutique that would ultimately benefit from Lehman's catastrophic collapse just two years later.

UK Expansion

Notable acquisitions following the IPO included Braveheart Financial Services (2006), which expanded Evercore's restructuring advisory capabilities.

The acquisition of Braveheart Financial Services Limited, a UK-based boutique, gave Evercore its first significant foothold in Europe. The timing proved prescient—building restructuring capabilities just before the greatest restructuring wave since the Great Depression.

V. The 2008 Financial Crisis: Crucible Moment

Inflection Point #2: Crisis Creates Opportunity

September 15, 2008. Lehman Brothers filed for bankruptcy. Roger Altman watched as the firm that had launched his career—the firm that had led Evercore's IPO just two years earlier—collapsed in the largest bankruptcy in American history.

Ever since the financial crisis brought down Lehman Brothers in 2008, boutiques have been steadily building their presence in the cut-throat business of advising on major mergers and acquisitions. Several were founded following that shakeout, but one of the oldest of the breed, Evercore, set up in 1995, coincidentally, by former Lehman investment banking co-head Roger Altman, has really come of age since the pandemic in 2020.

The crisis created a paradox. M&A activity collapsed—global deal volume fell to $2.9 trillion in 2008. But restructuring activity exploded. Companies that had loaded up on cheap debt during the boom suddenly couldn't service their obligations. Every distressed situation required advisors.

The Restructuring Pivot

As a senior restructuring banker, Celentano got a call in early March 2008 from Richard Metrick, a close confidant of Bear Stearns CEO Alan Schwartz. The firm was in deep trouble, and Metrick asked Celentano to prepare it for a possible bankruptcy filing. The day after the JPMorgan–Bear Stearns transaction closed, Celentano joined Evercore. He brought with him an extremely important engagement. Celentano was GM's adviser on the seemingly never-ending restructuring of Delphi, GM's largest auto-parts supplier and former subsidiary.

The GM engagement became the crown jewel of Evercore's crisis-era work. When General Motors filed for Chapter 11 in June 2009, Evercore was at the center of the action—guiding the largest restructuring in automotive history.

The government's intervention in and $50 billion assistance to GM began in December 2008 and wasn't completely wound down until December 2013, resulting in a $10.5 billion loss. This case discusses the bankruptcy, Treasury's DIP financing, and Treasury's unwinding of its equity stake in GM acquired as part of the restructuring.

Altman's experience on the Chrysler bailout three decades earlier proved directly relevant. He understood how government, creditors, unions, and companies could navigate impossible situations. That institutional knowledge was invaluable.

Building During the Downturn

While other firms were laying off bankers, Evercore was hiring. "Nearly 40 senior dealmakers have joined since 2020, giving the firm a roster of 145 senior managing directors. 'We heavily invested in the downturn. We are no longer an M&A boutique and have not been so for some time,' says Naveen Nataraj, co-head of US investment banking."

The crisis taught Evercore a critical lesson: distress is cyclical, and building capabilities during downturns positions you for the recovery. The restructuring expertise acquired in 2008-2009 became a permanent competitive advantage.

Reputational Arbitrage

Something more fundamental was happening. The crisis tarnished the reputations of bulge bracket banks. The very institutions that had packaged and sold toxic securities were now offering M&A advice to companies recovering from the damage. Clients noticed the contradiction.

These advantages, particularly its high-margin core advisory business and strong client relationships, are sustainable due to the inherent demand for conflict-free advice and the firm's entrenched position as a trusted advisor.

Independent advisors like Evercore offered something the bulge brackets couldn't credibly provide: advice untainted by conflicting interests. The post-crisis environment created structural demand for exactly what Evercore was selling.

VI. The Ralph Schlosstein Era & Transformation (2009-2022)

Inflection Point #3: Hiring a BlackRock Co-Founder as CEO

In 2009, Roger Altman made perhaps his most important hire: Ralph Schlosstein as President and CEO.

Ralph Schlosstein is chairman emeritus, a position he has held since February 2022. Prior to that, he served as president and CEO of Evercore for more than 11 years. Prior to joining the firm in 2009, Mr. Schlosstein was the CEO of HighView Investment Group, an alternative investment management firm. Before forming HighView in 2008, he served for almost 20 years as the president of BlackRock, the largest asset management firm in the world, with more than $8.5 trillion of assets under management. Mr. Schlosstein co-founded BlackRock in 1988, was a director since the company went public in 1999, chaired BlackRock's management committee and was a member of the executive and investment committees.

He founded a company with a friend: that friend was Larry Fink and the company they founded was called BlackRock.

Consider the implications. Schlosstein wasn't just a professional manager—he was a co-founder of what became the world's largest asset manager. He understood what it took to build an institution from scratch. He had worked alongside Larry Fink for two decades, creating one of the most important firms in global finance.

From 1977 to 1981, he worked for the federal government, initially as deputy to the assistant secretary of the Treasury Department, then as associate director of the White House Domestic Policy Staff, responsible for advising President Carter on urban policy, economic development and housing issues, as well as on the Chrysler loan guarantee program.

Remarkably, Schlosstein had also worked on the Chrysler bailout—just like Altman. Both had served in the Carter Treasury Department. Both understood how government intersected with finance. The cultural alignment was remarkable.

Schlosstein's Thesis

"My hypothesis was that, in this post-GFC world, it might just be possible for David to match up with Goliath." He believed "that one of the investment banking boutiques, of which Evercore was one, could scale and maybe break out to become a global independent investment banking advisory firm."

This was audacious. Schlosstein wasn't just looking to build a successful boutique—he was aiming to create something that could compete globally with Goldman Sachs and Morgan Stanley. The hypothesis was that post-crisis demand for unconflicted advice would create an opening for a scaled independent player.

Inflection Point #4: The ISI Acquisition (2014)

The deal was closed the following October to create Evercore ISI Institutional Equities, offering Macro and Fundamental Research, Sales, and Trading execution.

In August 2014, Evercore announced the acquisition of International Strategy & Investment ("ISI") Group for $440 million. The deal was closed the following October to create Evercore ISI Institutional Equities, offering Macro and Fundamental Research, Sales, and Trading execution.

This was a strategic pivot. Pure advisory firms couldn't participate in equity underwriting or provide institutional research. By acquiring ISI—an elite independent research firm—Evercore gained capabilities that would strengthen its investment banking franchise.

Founded in 1991, ISI is an elite independent institutionally-oriented investment research firm providing macroeconomic, policy and fundamental equity research. ISI's 28 research analysts are among the most highly regarded in the industry, providing fundamental research covering 345 companies in 10 major industry sectors. ISI currently has 226 employees operating from seven principal offices in the U.S., as well as an office in London; 32% of its analysts are ranked #1 or #2 by Institutional Investor.

In 2014, the firm secured the second highest number of Institutional Investor #1 positions, after J.P. Morgan, and also ranked No. 5 in total II positions.

The acquisition demonstrated that Evercore could be disciplined acquirers. The structure—with 70% of consideration dependent on performance over five years—aligned incentives and protected Evercore from overpaying.

Building Scale Through Landmark Deals

The decade following the financial crisis saw Evercore advise on increasingly transformational transactions:

In 2009, Evercore advised Wyeth in the largest deal of the year. In 2010 the firm advised Genzyme in the largest healthcare deal of the year.

In 2017, Evercore advised Coach, Inc. on its $2 billion acquisition of Kate Spade New York; Whole Foods Market on its $14 billion sale to Amazon; CVS on its acquisition of Aetna in the largest Healthcare deal of the year.

In 2018, Evercore advised the Independent Committee of the Board of Directors of T-Mobile U.S. on its $25.6 billion acquisition of Sprint Corporation, Takeda Pharmaceutical Company Limited on its $62.2 billion acquisition of Shire plc, and Comcast Corporation on its $39 billion acquisition of Sky plc.

In 2019, Evercore advised National Amusements, Inc. on its $12 billion combination of CBS Corp. and Viacom Inc., Anadarko Petroleum on its $55 billion sale to Occidental Petroleum, and Bristol-Myers Squibb on its $74 billion acquisition of Celgene Corporation in the largest M&A deal of the year.

Morgan Stanley & Co. LLC served as lead financial advisor to Bristol-Myers Squibb, and Evercore and Dyal Co. LLC were serving as financial advisors to Bristol-Myers Squibb.

The Bristol-Myers/Celgene transaction deserves special attention. At $74 billion, it was the largest pharmaceutical deal ever. Evercore was on it alongside Morgan Stanley. The boutique had earned its seat at the table for mega-deals.

VII. The John Weinberg Era & Modern Evercore (2016-Present)

Inflection Point #5: Hiring Goldman's Vice Chairman

John S. Weinberg is chairman of the board and chief executive officer of Evercore. Prior to joining Evercore in November 2016, Weinberg was vice chairman of Goldman Sachs from 2006 to 2015 and cohead of global investment banking from 2002 until 2015.

This hire sent shockwaves through Wall Street. John Weinberg wasn't just a senior banker at Goldman—he was Goldman royalty. Their son, John S. Weinberg, joined Goldman Sachs in 1983, became a partner in 1992, and was vice chairman from 2006 to 2015. John Livingston Weinberg was an American banker running Goldman Sachs from 1976 to 1990.

The Weinberg family is to Goldman Sachs what the Medici were to Florence. John's father and grandfather had run the firm. For a Weinberg to leave Goldman for an independent boutique was unprecedented.

Weinberg most recently was vice chairman of Goldman Sachs Group from June 2006 to October 2015. He was co-head of global investment banking from 2002 to 2014. Before that he was co-head of investment banking in the Americas. At Goldman Sachs, Weinberg provided strategic and financial advice to a number of leading companies, including Ford, General Electric and Boeing, and he advised on the IPOs of Visa and Under Armour.

Expanded Capabilities

The company has also greatly expanded its capabilities, growing from a mergers and acquisitions and restructuring firm into a leader in activist defense, corporate restructuring, debt advisory and equity advisory. "We are able to advise our clients on almost anything they want to do strategically or in capital markets," Ralph says.

"I can't name a sector where we don't have a banker," says Nataraj. "We also have product capabilities [in capital markets] which act as a balance sheet. We have a lot of the capabilities and the same breadth of a big bank but none of the conflicts."

This evolution is crucial. Evercore is no longer just an M&A boutique—it has become a full-service advisory platform. The firm can now advise on debt structure, equity raises, activist defense, and restructuring. This makes it a genuine alternative to bulge brackets for companies that want unconflicted advice.

Singapore and Asia

Since Mr. Magnus established Evercore's Singapore office in 2013 as its CEO, the firm has been awarded the title of "Best M&A Adviser" in Singapore six times at the Asset Triple A Awards. By 2021, Evercore was also named "Best M&A Adviser in Asia" and by 2023 had received over 16 awards from industry publications.

The Asian expansion demonstrates geographic discipline. Rather than spreading thin across multiple markets, Evercore built deep expertise in Singapore first, then expanded regionally. Awards followed execution.

The Robey Warshaw Acquisition (2025)

On July 30, 2025, Evercore announced that it has entered into an agreement to acquire Robey Warshaw, a highly successful independent advisory firm headquartered in the United Kingdom. Founded in 2013, Robey Warshaw has built a reputation as a trusted advisor to some of the most prominent multinational companies in Europe and has an impressive client franchise and track record.

The consideration for the transaction is GBP 146 million, or USD 196 million, payable in two tranches, with the first payment in Evercore stock at closing, and the second payment at the one-year anniversary in stock or cash as agreed between Evercore and Robey Warshaw. There is also potential additional consideration which is based on defined performance criteria over a multi-year period. Evercore expects the acquisition to be accretive to its Adjusted and GAAP EPS in the first full year together and thereafter.

Despite employing just 18 people in total, Robey Warshaw has made itself a mainstay in the UK, advising on some of the biggest UK deals in recent memory, including SoftBank's £24 billion acquisition of chipmaker Arm and AB InBev's $79 billion purchase of SABMiller.

The deal locks in each of Robey Warshaw's five partners, including the 65-year-old Robey, for at least six years.

This acquisition is strategically significant. The UK remains the largest M&A advisory market in Europe. Robey Warshaw punches far above its weight—18 people generating fees from multi-billion dollar deals. The six-year lockups on partners ensure continuity. With Robey Warshaw, Evercore will have more than 400 bankers across nine countries in the region.

VIII. Current State & Financial Performance

2024-2025 Results

Roger C. Altman, Founder and Senior Chairman, stated: "Evercore just had its second strongest year in terms of revenue and has considerable momentum going into 2025. The breadth and competitiveness of the Firm, at least in my view, has never been stronger."

In 2024, the Investment Banking & Equities segment generated $2.81 billion, or 97% of revenues.

The revenue concentration tells an important story. Unlike bulge brackets that generate significant revenues from trading and asset management, Evercore remains a pure-play advisory business. When advisory activity is strong, Evercore thrives. This concentration is both a strength (simplicity, focus) and a risk (cyclical exposure).

Advisory Fees – First quarter 2025 Advisory Fees increased $127.5 million, or 30%, year-over-year, reflecting an increase in revenue earned from large transactions and an increase in the number of advisory fees earned during the first quarter of 2025.

Talent & Scale

As of December 31, 2024, the company employed approximately 2,380 people. Approximately 1,800 employees were employed in the United States, with the remainder employed outside the United States, primarily in the Investment Banking & Equities segment.

As of December 31, 2024, the Investment Banking & Equities segment has 144 Investment Banking Senior Managing Directors and 40 Equities Senior Managing Directors with expertise and client relationships in a wide variety of sectors.

The hiring means that Evercore has increased its population of senior managing directors by 50% since 2021.

This SMD growth is remarkable. The firm has been aggressively recruiting senior talent even as advisory markets experienced cyclical weakness. The bet is that building capacity during downturns positions Evercore for outperformance when activity rebounds.

Research Excellence

Evercore ISI has been ranked No. 1 among all firms for top-ranked analysts on a weighted basis in the 2025 Extel (previously Institutional Investor) All-America Equity Research survey, marking its fourth consecutive year at the top.

Evercore ISI's research platform has been ranked #1 among independent firms in the 2025 Extel All-America Research Survey for the fourth consecutive year, with 44 analysts earning top 3 or runner-up positions across 47 categories.

Four consecutive years at the top is not luck—it's systematic excellence. The ISI acquisition has proven to be transformative, creating a research franchise that competes with (and beats) bulge bracket research departments.

IX. Business Model Deep Dive

How Evercore Makes Money

Evercore (NYSE: EVR) is a premier global independent investment banking advisory firm. We are dedicated to helping our clients achieve superior results through trusted independent and innovative advice on matters of strategic significance to boards of directors, management teams and shareholders, including mergers and acquisitions, strategic shareholder advisory, restructurings, and capital structure. Evercore also assists clients in raising public and private capital and delivers equity research and equity sales and agency trading execution, in addition to providing wealth and investment management services to high net worth and institutional investors.

Revenue streams break down as follows:

- Advisory Fees: The core business—fees earned for advising on M&A transactions, restructurings, and strategic matters

- Underwriting Fees: Fees for equity underwriting, where Evercore serves as bookrunner or participant

- Commissions and Trading: Revenue from institutional equities sales and trading

- Asset Management: Fees from wealth management and institutional asset management

The overwhelming majority of revenue (97%) comes from Investment Banking & Equities.

The Independence Advantage

Evercore differentiates itself through a specialized, independent, and client-focused advisory approach, contrasting with the broader service offerings of bulge bracket banks.

Why does independence matter? Consider a hypothetical scenario: A company is exploring a sale. Its investment bank is advising on the transaction. But that same bank has a $2 billion credit facility outstanding to a potential acquirer. Will the bank's advice be influenced by its desire to maintain the lending relationship? Even if the advice is unbiased, will the client trust it?

At Evercore, these conflicts don't exist. The firm has no lending book, no trading positions in client securities, no asset management relationships that might influence advice. This purity is the product.

The Talent Model

"An A+ person is worth one-and-a-half to two times an A and an A is worth one-and-a-half to two times what an A- is worth, in terms of the quality of the people. So attracting and developing and retaining the best talent is critical."

This philosophy explains why Evercore invests so heavily in senior talent. In advisory, the product is the people. A single senior banker can generate tens of millions in fees through relationships cultivated over decades.

"John and I can confidently sit in front of any recruit and assert that they can do significantly more business with their clients at Evercore than at any other independent firm."

Compensation Economics

Evercore also increased headcount, by nearly 9% to 2,525 people, so higher pay spending wasn't entirely directed towards current employees. Nonetheless, average pay at the firm is currently on track to reach $891k this year.

$891,000 in average compensation per employee. This is extraordinarily high, even by Wall Street standards. It reflects both the senior-heavy composition of the workforce and the firm's willingness to pay for talent.

The primary driver behind last 12 months revenue was the Investment Banking & Equities segment contributing a total revenue of US$2.90b (97% of total revenue). The largest operating expense was General & Administrative costs, amounting to US$2.20b (91% of total expenses).

Compensation is Evercore's largest expense by far—typical for an advisory firm. This creates operating leverage: when revenues grow, a larger proportion drops to the bottom line because compensation scales more slowly than revenue on big deals.

X. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

Threat of New Entrants: LOW-MODERATE

Investment banking requires decades of relationship-building. A CEO hiring an M&A advisor wants someone who has done dozens of similar deals, who understands their industry, who has relationships with potential counterparties. You can't build this overnight.

However, new boutiques can form when star bankers leave established firms. Ken Moelis left UBS to found Moelis & Company. Perella and Weinberg left Morgan Stanley to found Perella Weinberg Partners. This creates ongoing competitive pressure.

Evercore's scale—145 senior managing directors, global offices, research capabilities—creates meaningful barriers. A new entrant would need to replicate years of client relationships and infrastructure.

Bargaining Power of Suppliers: HIGH

The "suppliers" in advisory are senior bankers—the talent. They have enormous leverage. Star bankers can generate $20-50 million annually in fees. They're courted constantly by competitors. Evercore must pay top-quartile compensation to retain them.

This is Evercore's largest expense and its most critical competitive dynamic. A departing senior banker takes relationships with them. The firm has no choice but to pay market rates.

Bargaining Power of Buyers: MODERATE

Large corporations have choices among advisors. They run competitive bake-offs for major transactions. Switching costs are low—nothing prevents a company from using Goldman on one deal and Evercore on the next.

However, for transformational transactions, companies want the best. The advisor on a $50 billion merger will be central to outcomes. Price sensitivity decreases as deal complexity increases. Relationships create stickiness—CEOs and boards tend to return to advisors they trust.

Threat of Substitutes: LOW

For complex M&A, restructuring, and activist defense, there's no substitute for human advisory. AI may eventually impact research, but relationship-driven advisory remains fundamentally human. A CEO facing a hostile takeover wants to look a trusted advisor in the eye—not talk to a chatbot.

Investment banks have tried to productize advisory (standardized fairness opinions, for example), but complex situations require bespoke solutions. The threat of substitution is minimal.

Competitive Rivalry: HIGH

Its direct independent competitors include well-regarded entities such as Lazard, Moelis & Company, Houlihan Lokey, Perella Weinberg Partners, Centerview Partners, and Greenhill & Co. These independent firms often highlight their lack of conflicts of interest, a key differentiator when seeking client mandates. Houlihan Lokey, for example, is noted for its proficiency in financial restructuring and M&A advisory.

Competition is intense from both bulge brackets (Goldman, JPM, Morgan Stanley) and other independents. The market is large enough for multiple winners, but every mandate is contested. Pricing pressure exists, though it's moderated by quality differentiation.

Hamilton's 7 Powers

Scale Economies: WEAK

Advisory is relationship-based, not scale-driven. A 50-person boutique can advise on the same transaction as a 50,000-person bank. There are some advantages to global coverage and sector expertise, but scale economies are limited.

Network Effects: MODERATE

Talent attracts talent. Clients attract clients. When Evercore wins a major mandate, it generates publicity that attracts the next mandate. When a star banker joins, other bankers notice. This creates virtuous cycles, though they're weaker than classic network effects.

Counter-Positioning: STRONG

This is Evercore's core power. Bulge brackets cannot abandon their capital markets businesses that create conflicts. They have billions invested in trading floors, lending operations, and prime brokerage. These businesses generate meaningful revenues.

For a bulge bracket to match Evercore's independence, it would have to dismantle its integrated model—destroying shareholder value in the process. They're locked into their current structure. This is textbook counter-positioning.

Switching Costs: MODERATE

Relationships create stickiness. A CEO who has worked with an Evercore banker through multiple transactions has established trust. But nothing contractually prevents switching between deals. Switching costs are real but not prohibitive.

Branding: STRONG

As Ralph looks forward to being part of its future success in his new role, he says that Evercore has grown into a firm "that is truly a trusted adviser to the largest companies and private equity firms in the world, and that we will always do that in a way that is completely confidential and without any conflicts."

The Evercore brand now stands for independence and quality. When a company announces Evercore as advisor, it signals to the market that unconflicted advice was prioritized. This brand value took decades to build and would be difficult to replicate.

Cornered Resource: STRONG

The talent base is a cornered resource. Senior bankers with deep relationships cultivated over decades cannot be replicated. The relationships exist because of specific individuals. When Evercore hires John Weinberg from Goldman, it corners a resource Goldman can never recover.

Process Power: MODERATE

Evercore's focus on senior banker involvement creates process advantages. The firm emphasizes that the people who win the pitch do the work. This consistency creates better client outcomes and stronger relationships, though it's not proprietary.

XI. Key Risks & Investment Considerations

Cyclical Exposure

M&A activity is highly cyclical. In 2022-2023, deal volumes declined significantly as rising interest rates and economic uncertainty dampened activity. Evercore's revenues depend on deal flow. Extended downturns can pressure profitability.

Key Person Risk

While Evercore has institutionalized much of its culture, the firm remains dependent on key personnel. Roger Altman, now Senior Chairman, has been central to the firm's identity. John Weinberg is critical to client relationships. Departure of key figures could impact the business.

Compensation Expense

The firm's largest expense is compensation. Rising compensation costs could compress margins. Competition for talent means Evercore has limited ability to reduce compensation without losing people.

Geographic Concentration

Despite global expansion, North America remains Evercore's primary market. The Robey Warshaw acquisition addresses this, but European and Asian operations remain smaller than U.S. operations.

Regulatory Risk

Investment banking is heavily regulated. Changes in securities laws, M&A regulations, or tax treatment could impact deal activity. Cross-border transactions face increasing regulatory scrutiny.

XII. Key Metrics for Investors

For investors following Evercore, three KPIs matter most:

1. Advisory Revenue Per Senior Managing Director

This metric captures productivity of the firm's most important asset: senior bankers. Calculate by dividing advisory revenues by SMD count (with appropriate lag to account for ramp-up time).

Why it matters: Declining productivity suggests either market weakness or competitive pressure. Rising productivity suggests market share gains or improved deal economics.

2. Senior Managing Director Growth (Net Adds)

Track not just gross hires but net adds after departures. This reveals whether Evercore is successfully building capacity.

Why it matters: The firm's strategy depends on continuing to attract elite talent. Deceleration in SMD growth would signal competitive pressure or market saturation.

3. Advisory Market Share Among Independent Firms

Compare Evercore's advisory revenues to peer set (Lazard, Moelis, PJT, Houlihan Lokey, PWP). Market share trends reveal competitive positioning.

Why it matters: Evercore's thesis is that it can become the dominant independent. Losing share to peers would challenge this narrative.

XIII. Conclusion: The Long Game

Roger Altman is now 79 years old. He has been building Evercore for 30 years—longer than he worked anywhere else. The firm that emerged from personal disgrace is now valued at over $13 billion and competes with the world's most prestigious investment banks.

John S. Weinberg, Chairman and Chief Executive Officer, stated: "Evercore has never been better positioned. We continue to experience momentum across our businesses and remain committed to serving our clients."

Roger C. Altman, Founder and Senior Chairman, added: "The Evercore platform has been broadened relentlessly in recent years. The result is that the Firm is better positioned for volatile market conditions than it has ever been."

The Evercore story validates several investing principles:

Counter-positioning can create durable advantage. By structuring as a pure advisory firm, Evercore created a competitive position that bulge brackets cannot match without destroying their own business models.

Talent compounds. The decision to hire elite bankers and pay them generously has compounded over decades. Each new hire attracts the next.

Crisis creates opportunity. The 2008 financial crisis, which could have destroyed a small advisory firm, instead accelerated Evercore's growth by creating demand for unconflicted advice.

Patience matters. Building Evercore took 30 years. The firm went public in 2006 but didn't achieve true scale until well after 2015. This isn't a short-term story.

For investors, Evercore represents a bet on the continued demand for unconflicted advisory services. The structural advantages are real. The talent base is formidable. The question is whether advisory markets remain robust and whether Evercore can maintain its competitive position as it scales.

Its advisory business achieved $228 billion in transaction value across 118 deals in 2024—an increase of 15% from the previous year—reflecting both the scale and consistency of its performance in a competitive market.

What started as Roger Altman's second act has become one of Wall Street's most remarkable success stories. The disgraced Treasury official who resigned amid scandal built something that outlasted everyone who doubted him. In investment banking, as in life, the best revenge is living well—and Evercore is living very well indeed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube