The Ensign Group: Building a Skilled Nursing Empire Through Decentralized Excellence

I. Introduction & Episode Roadmap

Picture a skilled nursing facility in the late 1990s. The industry's reputation was tarnished—a sector known for cost-cutting, thin margins, and a revolving door of private equity owners looking to extract value rather than create it. Medicare fraud cases made headlines. Staff turnover was endemic. Families dreaded placing their loved ones in facilities that felt more like warehouses than care communities.

Into this landscape stepped three partners with a radical hypothesis: What if the problem with skilled nursing wasn't the industry itself, but how facilities were being managed?

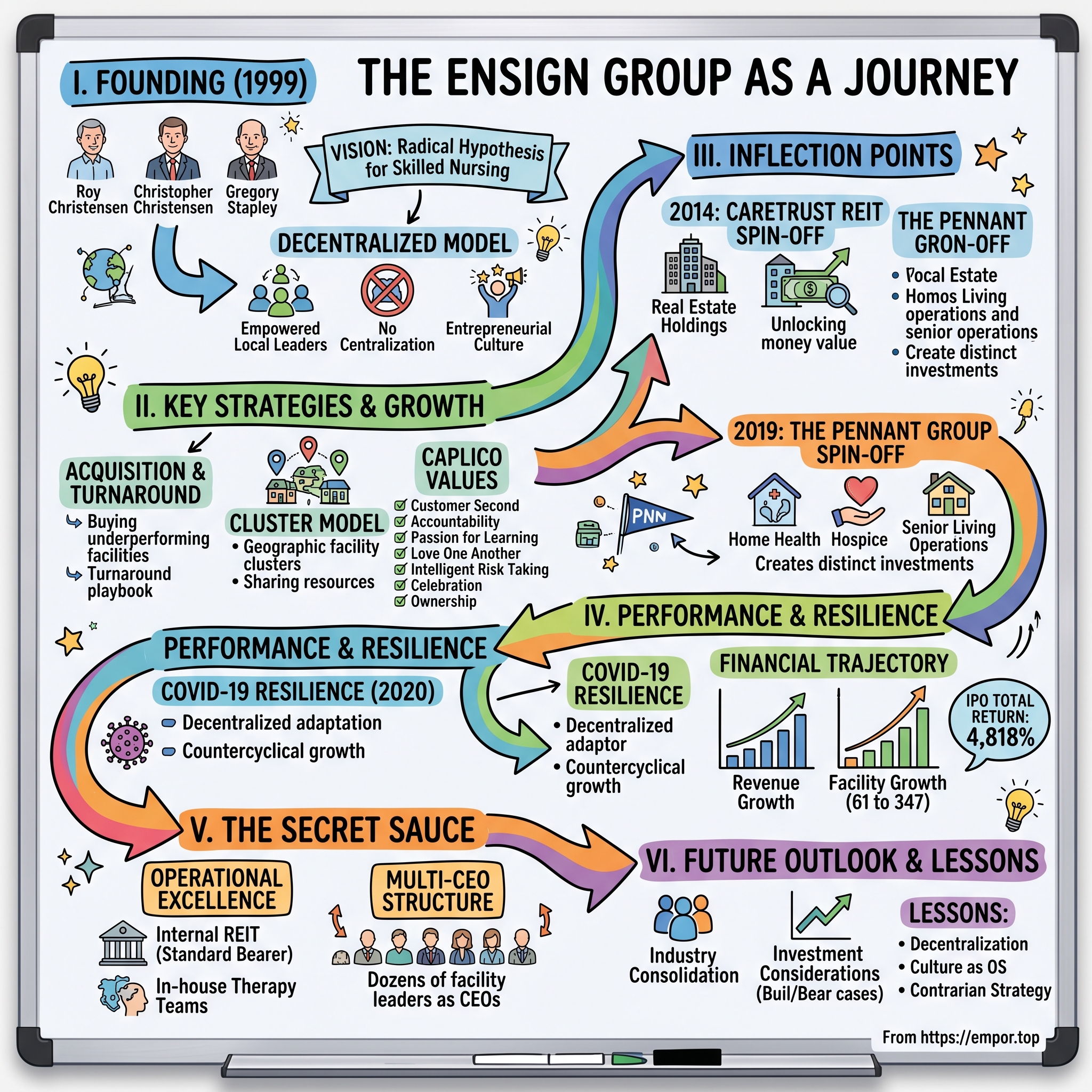

In 1999, Roy Christensen, Christopher Christensen, and Gregory Stapley established The Ensign Group in Mission Viejo, California, bringing together operational and healthcare expertise. Roy Christensen brought decades of healthcare experience to the venture, having previously founded Beverly Enterprises, once the largest nursing home company in the United States.

Today, The Ensign Group stands as a remarkable outlier in an industry that has systematically destroyed shareholder value. The company operates 347 healthcare facilities across 17 states, providing skilled nursing, senior living services, and various rehabilitative healthcare services. Ensign has delivered exceptional shareholder returns since its IPO in 2007, with a total return of 4,818%. More recent performance remains strong, with 10-year returns of 829% and 3-year returns of 98%.

The financial trajectory tells an extraordinary story. Consolidated GAAP revenues reached $4.26 billion in 2024, reflecting a 14.2% increase from the prior year. For 2025, the company raised its annual revenue guidance to $4.99 billion to $5.02 billion. GAAP net income reached $298 million for 2024, marking an increase of 42.3%.

This is not supposed to happen in skilled nursing. The sector has endured a brutal decade—facility closures, bankruptcies, workforce crises, and reimbursement pressures that have pushed many operators to the brink. Yet Ensign keeps expanding, acquiring, and posting record quarters.

The secret lies in a set of counterintuitive operating principles that would make most corporate strategists uncomfortable. Ensign empowers facility-level leaders with CEO-caliber authority. It pays these leaders like entrepreneurs, not middle managers. It refuses to centralize decision-making even as it scales to hundreds of facilities. And it codifies its culture into an acronym—CAPLICO—that puts employees ahead of customers in its explicit hierarchy of values.

This deep dive will explore how Ensign built its empire, why its model confounds conventional wisdom, and what the company's success reveals about value creation in heavily regulated, operationally intensive industries.

II. The Skilled Nursing Industry Context: Why Most Fail

Before understanding what makes Ensign exceptional, one must appreciate why skilled nursing is such a graveyard for operators and investors alike.

The skilled nursing industry sits at the intersection of healthcare's most challenging dynamics: heavy regulation, government-dominated reimbursement, labor-intensive operations, and a customer base with limited ability to pay. It is, by most financial metrics, a terrible business.

Since 2020, 774 nursing homes have closed, resulting in the loss of 62,567 beds and displacing 28,421 residents. This consolidation has largely benefited larger, more resilient operators, while smaller facilities face heightened competition and financial strain.

The Reimbursement Squeeze

The economics of skilled nursing are fundamentally constrained by who pays the bills. Most revenue comes from Medicare and Medicaid—government programs that set prices administratively rather than through market negotiation.

The Medicaid revenue portion (39.7% for 2024) raises concerns about dependency on government funding amid ongoing healthcare reforms. In FY2025Q2, the Medicaid business generated the highest revenue for Ensign Group, amounting to $473.90 million and accounting for 38.60% of total revenue.

The rise of Medicare Advantage has added a particularly painful dimension to this challenge. Skilled nursing facilities generally receive lower reimbursement rates under MA plans than under traditional Medicare. The Federal government, through CMS, pays MA plans a fixed, or 'capitated', monthly amount per beneficiary.

Medicare Advantage spend per beneficiary was only $448 compared to $841 per Medicare Fee-for-Service beneficiary. The SNF sector loses about $275 million annually for every 1 percentage point increase in the total proportion of Medicare beneficiaries enrolled in MA.

Labor: The Inescapable Challenge

Skilled nursing is irreducibly labor-intensive. You cannot automate personal care. You cannot offshore bedside nursing. The industry requires massive numbers of certified nursing assistants, licensed practical nurses, and registered nurses—workers who are increasingly scarce, increasingly expensive, and increasingly unwilling to work in institutional settings.

Over one-third of nurses are considering changing careers, signaling a potential job churn for the industry. Direct care nursing expenses reached $49.2 billion in 2023, driven by ongoing labor shortages and continued reliance on contract labor.

The pandemic accelerated these dynamics catastrophically. Nursing homes lost an estimated 200,000 workers during COVID-19, and the sector has struggled to rebuild. Agency staffing—temporary nurses hired at premium rates—has become endemic, further crushing margins for operators unable to retain permanent staff.

The Regulatory Gauntlet

Skilled nursing facilities operate under some of the most intensive regulatory oversight in healthcare. State surveyors conduct unannounced inspections. CMS quality ratings are publicly reported and directly affect referral patterns. The federal minimum staffing mandate—though currently facing legal challenges—represents yet another compliance burden.

The potential for increased closures was due to a challenging operating environment marked by staffing shortages, rising costs, and stringent regulations. "In the last several years since the pandemic, payment rates, government payers have not kept pace with the increasing costs. And the regulations from a survey and penalty perspective, have gotten much more harsh."

Why Ensign Sees Opportunity Where Others See Catastrophe

Here is where Ensign's worldview diverges sharply from the industry consensus. While trade associations lobby against regulations and competitors blame external forces for their struggles, Ensign's leadership offers a more provocative diagnosis: many operators brought their problems on themselves.

The company has been blunt about this perspective. Management has argued that many industry problems stem from owners who overpaid for facilities and saddled operators with rent escalators they had no chance of meeting—the classic financial engineering playbook that has destroyed value across healthcare real estate.

This is not merely positioning. It reflects a genuine strategic opportunity. The gap between financially stable operators and those facing challenges has grown wider. The report points to a combination of rising labor costs, increased reliance on Medicaid reimbursement, and the ongoing growth of Medicare Advantage as key drivers of this divide.

For Ensign, industry distress creates a steady pipeline of acquisition opportunities—facilities that can be purchased at attractive prices, turned around operationally, and transformed into contributors to the overall portfolio. The worse the industry performs, the better Ensign's acquisition economics become.

This dynamic creates a powerful flywheel: operational excellence generates cash flow, which funds acquisitions, which expand the platform, which creates more opportunities for turnaround expertise to generate returns. It is a virtuous cycle that rewards competence and punishes mediocrity—exactly the opposite of what happens in many consolidated industries.

III. Founding Story & Early Vision (1999–2007)

The Ensign story begins with a family that understood skilled nursing from the inside. The Ensign Group was founded in 1999 by Roy E. Christensen, Christopher R. Christensen, and Gregory K. Stapley with the acquisition of their first skilled nursing facility in Escondido, California.

Roy Christensen's background was particularly instructive. He had previously founded Beverly Enterprises, once the largest nursing home company in the United States. The Beverly experience—building a massive national platform—would have taught valuable lessons about both the opportunities and pitfalls of scale in post-acute care.

The company's name "Ensign" was chosen to represent a standard of excellence and leadership in healthcare services. The naval reference—an ensign is both a flag and a junior officer's rank—captured the dual nature of the founders' vision: a standard to rally around and a commitment to developing leaders from within.

The Core Insight

The founders' key insight was deceptively simple: nursing home management was broken not because of industry fundamentals, but because of how decisions were being made. Large chains had centralized authority in corporate offices far removed from individual facilities. Regional managers oversaw too many buildings. Administrators were treated as middle managers rather than business leaders.

This approach created a cascade of problems. Centralized decision-making was too slow to respond to local conditions. Administrators who lacked authority couldn't build relationships with hospital discharge planners or local physicians. Talented leaders fled to opportunities where they could actually run something.

The Ensign model flipped this entirely. Decentralized Operational Model: Empowering local leadership proved crucial. Facility leaders operate with significant autonomy, fostering an entrepreneurial culture and driving performance improvements at the ground level. This remains a core tenet of their success.

The Acquisition-Turnaround Model

From the beginning, Ensign was built to acquire struggling facilities rather than develop new ones. The company built its scale primarily by acquiring underperforming facilities and turning them around operationally and financially. This disciplined approach allowed for rapid, yet controlled, expansion.

This strategy required a specific set of capabilities. Ensign needed the ability to identify facilities with turnaround potential—distinguishing between those suffering from bad management versus fundamental market problems. It needed the operational playbook to quickly improve quality scores, staff retention, and census. And it needed the leadership development pipeline to populate newly acquired facilities with capable administrators.

From its humble beginnings with a single facility, Ensign expanded rapidly through a disciplined acquisition strategy, focusing on underperforming operations that could benefit from the company's operational expertise and patient-centered approach.

Geographic Expansion

1999: Founded with the acquisition of first skilled nursing facility in Escondido, California. 2002: Expanded operations beyond California into Arizona. 2003: Entered the Texas market with facility acquisitions.

This expansion pattern was methodical. Rather than pursuing geographic dispersion, Ensign built density in regional "clusters" where facilities could share resources, best practices, and talent. A facility in Phoenix could draw on the experience of the California operations. Texas leaders could learn from both.

The IPO: From Startup to Public Company

The company went public on November 8, 2007, with an initial public offering on the NASDAQ under the ticker symbol "ENSG." At the time of its IPO, Ensign operated 61 facilities across six states.

Nursing-home operator Ensign Group Inc. raised $64 million on Thursday with an initial public offering of stock. The 4 million share offering was priced at $16 per share.

The timing was precarious—the IPO closed just weeks before the financial crisis would begin reshaping capital markets. But Ensign's focus on operational performance rather than financial engineering served it well. While leveraged competitors struggled with debt service during the recession, Ensign continued building its platform.

Those 61 facilities and $64 million in IPO proceeds would become the foundation for a company that now operates nearly six times as many facilities and generates over $4 billion in annual revenue. The shareholder who bought at the IPO and held has generated returns that dwarf the broader market.

IV. The Secret Sauce: CAPLICO & Decentralized Operations

Walk into Ensign's corporate headquarters—now in San Juan Capistrano, California—and you'll encounter an organization that feels fundamentally different from typical healthcare corporations. Each one of the 300+ businesses is run independently by its own management team and employees, which is consistent with a field-driven, flat structure.

This is not marketing language. It reflects a genuine operating philosophy that permeates every aspect of how Ensign does business.

The CAPLICO Framework

The Ensign Group operates with a distinct set of core values, known as CAPLICO, which guide its operations and company culture. These principles are Customer Second, Accountability, Passion for Learning, Love One Another, Intelligent Risk Taking, Celebration, and Ownership.

The most striking element is the first principle: Customer Second. In an era when every corporation proclaims its customer-centricity, Ensign explicitly states that employees come first.

This core value emphasizes that prioritizing the well-being and empowerment of employees ultimately leads to superior patient care. It fosters a flat organizational structure where individuals are empowered to make decisions.

This is not naive idealism. It reflects a sophisticated understanding of service economics. In skilled nursing, the front-line caregivers—nursing assistants, nurses, therapists—deliver the product. Their motivation, competence, and stability determine patient outcomes. You cannot deliver excellent care with a demoralized, transient workforce.

Taking responsibility for results is central to this value, promoting a decentralized model where local leaders are empowered and held responsible for facility performance and quality.

The Multi-CEO Model: 80 CEOs and Counting

CEO Barry Port is hesitant to take the credit. Instead, he's content to chalk up Ensign's success to its legion of regional leaders, many of whom have also earned the title of CEO — nearly 80 in all. Empowered to make sweeping strategic decisions, and given financial incentives for developing Ensign's presence in new markets, the sprawling network of CEOs remains the core of the operator's strength.

This multi-CEO structure inverts typical corporate hierarchy. "Think about it as a franchise model, almost," Port explained.

The company's 78 CEOs — along with other leaders — are largely on their own to develop partnerships with referral sources and vendors, focus on specialty services, and hire staff without interference from the headquarters in Southern California. That autonomy is part of Ensign's pitch to potential leaders.

The rationale is brutally logical: "At the heart of that philosophy is the seemingly simple conclusion that running an individual nursing home is a difficult task that requires a leader with an active mind. Port drew a distinction between Ensign and other skilled nursing operators by pointing out that his company intentionally doesn't follow the traditional ladder of promoting solid building-level leaders into corporate roles — but instead incentivizes them to remain on the ground level. 'If you don't have a well-prepared, CEO-caliber leader to run these operations, you're really doing a disservice.'"

This has profound implications for organizational design. Most companies promote their best operators into management roles, removing them from the front lines where they created value. Ensign does the opposite—it creates career paths that keep talented leaders in operational roles, with compensation that reflects their impact.

The Cluster Model

The decentralized structure is not anarchy. Ensign organizes facilities into geographic "clusters" that provide mutual support while preserving local autonomy.

An influx of local leadership and decentralized transition model allows growth minus the "typical corporate bottlenecks."

"By applying lessons we had learned in years past, particularly from a large deal we did in Texas, our local leaders in California approached this deal as if it were six or seven smaller deals. Local market leaders in California took responsibility for buildings near existing building clusters."

The cluster model creates peer accountability without bureaucracy. Facility leaders in a cluster can share challenges, compare results, and call out underperformance—functions that would otherwise require layers of corporate oversight.

The Service Center: Central Support Without Central Control

Ensign Services, Inc. is a subsidiary of The Ensign Group, Inc whose affiliated entities are considered the national leaders in the skilled nursing and post-acute care industry. We provide service and support to over 360 facilities in the post-acute care continuum that employs over 55,000 employees. Ensign Services, known as the "Service Center", has created a family environment where we provide world class services including Accounting, Information Technology, Human Resources, Legal, Compliance, Construction and other centralized professional services.

The Service Center handles back-office functions that benefit from scale—payroll processing, IT systems, legal compliance, construction management—while leaving operational decisions to local leaders. This is classic Berkshire Hathaway-style decentralization: centralize what benefits from scale, decentralize everything else.

We are a constantly growing organization that focuses on supporting these operations so they can focus on what they do best – caring for the individual resident.

Why Decentralization Works in Healthcare

Healthcare is inherently local. The patients come from local hospitals. The staff come from local labor markets. The referral relationships are built through local networking. Government reimbursement rates vary by state and sometimes by county.

A centralized operator makes decisions based on averages and policies. A decentralized operator can tailor every aspect of operations to local conditions. This flexibility creates competitive advantage that compounds over time.

Meanwhile, local leaders continue to recruit future CEOs for Ensign-affiliated operations and the company has a "deep bench" of CEOs in training. An influx of local leadership and decentralized transition model allows growth minus the "typical corporate bottlenecks."

For investors, this structure creates both opportunities and risks. The opportunity: Ensign can scale without the diseconomies that typically afflict large service organizations. The risk: the model depends on culture, which is notoriously difficult to maintain as organizations grow.

V. Key Inflection Point #1: The CareTrust REIT Spin-off (2014)

The first major transformation in Ensign's corporate structure came in 2014, when the company spun off its real estate holdings into a separate publicly traded REIT.

The Ensign Group announced today the successful completion of its spin-off of CareTrust REIT, Inc. In the spin-off, Ensign stockholders received one share of CareTrust common stock for each share of Ensign common stock held at the close of business on May 22, 2014. The spin-off is effective from and after June 1, 2014.

The Strategic Logic

The decision to separate real estate from operations reflects a sophisticated understanding of capital markets and corporate structure. Healthcare real estate commands different valuation multiples than healthcare operations. REITs offer tax advantages and access to distinct investor bases. Separating the businesses allows each to optimize its capital structure.

As a spinoff, CareTrust REIT didn't raise initial venture capital in the traditional startup sense. It commenced operations with an initial portfolio of 94 healthcare-related properties valued at approximately $715 million, which were transferred from Ensign.

Mr. Christensen added, "The health of our balance sheet, our strong cash flow, favorable market conditions and the tax-free nature of the transaction have allowed us to establish capital structures for both companies that leave each not only quite healthy, but with plenty of potential for both near-term and long-term growth."

Post-Spin-off Trajectory

The spin-off proved extraordinarily successful for shareholders of both entities. CareTrust has grown into a substantial healthcare REIT with a diversified tenant base, while Ensign has continued its operational expansion.

Systematically reducing tenant concentration, particularly regarding Ensign. While Ensign remains a valued tenant, diversifying the operator base across numerous regional players enhanced portfolio resilience and reduced single-tenant risk.

The separation also allowed Ensign to develop Standard Bearer, its internal captive REIT, which would become an increasingly important component of the company's capital strategy.

Value Creation through Spin-offs: The decisions in 2014 and 2019 to spin off CareTrust REIT and The Pennant Group were transformative. These moves allowed ENSG to concentrate on its core skilled nursing and therapy operations while giving investors distinct investment opportunities.

For investors, the CareTrust spin-off demonstrated management's willingness to unlock value through corporate restructuring rather than hoarding assets. It established a template that would be repeated five years later.

VI. Key Inflection Point #2: The Pennant Group Spin-off (2019)

The second major separation came in October 2019, when Ensign spun off its home health, hospice, and senior living operations into The Pennant Group.

The effective date of the distribution is October 1, 2019. In the spin-off, Ensign stockholders received one share of Pennant common stock for every two shares of Ensign common stock held at the close of business on September 20, 2019.

What Was Separated

Before the spinoff, The Ensign Group was the parent company of 258 health care facilities, 28 hospice agencies, 26 home health agencies and nine home care businesses nationwide. Its home health and hospice assets lived within its Cornerstone Healthcare Inc. subsidiary. Now, 212 health care facilities remain under Ensign.

The Pennant Group, Inc. is a holding company of independent operating subsidiaries that provide healthcare services through 63 home health and hospice agencies and 52 senior living communities located throughout Arizona, California, Colorado, Idaho, Iowa, Nevada, Oklahoma, Oregon, Texas, Utah, Washington, Wisconsin and Wyoming. Each of these businesses is operated by a separate, independent operating subsidiary that has its own management, employees and assets.

The Philosophy of Separation

Christopher Christensen, Ensign's Executive Chairman and a Pennant director, said, "The spin-off of Pennant represents the culmination of a tremendous amount of work over many years from our local leaders and Service Center resources. It is also evidence that Ensign's culture and operating model—which is also the foundation for Pennant's home health, hospice and senior living businesses—is the reason for long-term, sustained growth."

The underlying logic was powerful: different healthcare businesses have different dynamics, different investor bases, and different growth opportunities. Keeping them bundled creates conglomerate discount and operational distraction.

"The business was started with the intention of growing it so it could eventually spin off from The Ensign Group," Walker said. "That's really where Pennant came from."

The Ensign Pennant Care Continuum (EPCC)

Rather than severing ties completely, the two companies maintained a framework for ongoing collaboration.

"The continuum will allow for Pennant and Ensign to share data and create pathways to better care for patients. Gochnour expects all Pennant operations in markets adjacent to Ensign operations to participate, as well as a 'high, high percentage' of Ensign operations. 'We see [EPCC] as something that will put us in a position where we're able to work strategically with payers, with hospital systems.'"

This arrangement preserved the clinical benefits of integrated care while allowing separate capital structures and management focus.

Equity Distribution to Local Leaders

One underappreciated aspect of the Pennant spin-off was how it enhanced equity participation for local leaders.

"Local leadership will have more opportunity to reap the benefits of equity compensation programs as a result of the spinoff. 'That equity is tied specifically to success and growth of the Pennant Group,' Walker said. 'When you're part of The Ensign Group and the SNF world is a much larger piece of the pie, it's harder to distribute equity as widely as we would normally do it.'"

This detail reveals how seriously Ensign takes ownership alignment. By creating a smaller, more focused public company, Pennant could offer equity stakes that were more meaningful to individual leaders—strengthening the same incentive structures that powered Ensign's own growth.

VII. Key Inflection Point #3: COVID-19 Resilience (2020)

The COVID-19 pandemic represented an existential threat to skilled nursing. Nursing homes became synonymous with tragedy—facilities where the virus spread with lethal efficiency among the most vulnerable populations.

Yet Ensign navigated the crisis with remarkable operational and financial performance.

The Ensign Group has been on a roll for countless quarters, and not even the early effects of a world-historic pandemic were enough to prevent the skilled nursing heavyweight from logging another record quarter to start 2020. The San Juan Capistrano, Calif.-based operator saw a 28.3% increase in its per-share earnings over the fourth quarter of 2019 — which itself represented another record. That earnings figure was also a 92.5% increase over the same time last year.

Financial Performance During the Crisis

Nursing home operator The Ensign Group, fresh off of a year of solid operational results that prompted another complete return of federal aid, on Thursday indicated a growing push to capitalize on the value of its owned real estate. The San Juan Capistrano, Calif.-based operator reported net income of $46.3 million in the fourth quarter of 2020 and $170.5 million for the year total.

Perhaps most remarkably, Ensign's results do not include any of the federal relief funds granted to skilled nursing providers under the CARES Act; it returned $33 million such funds in the fourth quarter and $5 million in January, after sending back about $109 million in such funds in July 2020.

The Ensign Group has returned about $110 million in federal coronavirus relief funding after experiencing another quarter of "record-breaking results." For the second-quarter in a row, Ensign achieved its highest earnings per share in history, of 78 cents — an 100% increase over the prior year quarter.

Why Decentralization Paid Off

The pandemic vindicated Ensign's decentralized approach. While centralized competitors struggled to implement uniform policies across diverse geographies, Ensign's local leaders could adapt to local conditions in real-time.

"It really is in times like these that Ensign's unique operating model really shines. Our leadership and our operational model are the reasons why we have adapted and will continue to adapt during this unprecedented time. Rather than attempting to rollout a one-size-fits-all approach across many markets with varying local restrictions, our CEO-caliber leaders and their clinical partners with the support of a world-class service center are very carefully working with local governments, hospitals and their managed care partners to be a solution to this pandemic."

"Ensign was born in times much like these, and our model is not only designed to survive, but to thrive and grow in the face of uncertainty," Port said.

Acquisition Opportunities

While competitors retrenched, Ensign saw opportunity.

"Turnaround opportunities could be in significant supply as the dust settles from COVID-19," Keetch noted. "We anticipate that there will be a significant influx of older and newer deals that come out of this pandemic, as we slowly begin to return to our pre-COVID plans."

In terms of deal flow, COVID-19 "put the brakes on all our acquisition efforts," Keetch said, but over the summer and fall, the company started to evaluate acquisition deals again. "We definitely are seeing deal flow pick up," he said. "I think we're probably on the front of the curve though, on what we think is coming, which is a lot of opportunities that will probably be enhanced by the fact that in the pandemic, occupancies are down."

This countercyclical posture—aggressively pursuing growth when competitors are focused on survival—has been a hallmark of Ensign's strategy throughout its history.

VIII. The Growth Story: From 61 to 347 Facilities

The numbers tell a story of relentless expansion.

At the time of its IPO in 2007, Ensign operated 61 facilities across six states. By mid-2025, that footprint had grown to 347 healthcare facilities across 17 states.

Financial Trajectory

Over the last five years, The Ensign Group grew its sales at a solid 15.7% compounded annual growth rate.

The acceleration has been remarkable: - 2023: Annual Revenue was $4.26 billion, a 14.2% increase year-over-year from 2023. - 2024: Revenue reached $4.26 billion with net income of $298 million - 2025 guidance: Annual revenue guidance of $4.99 billion to $5.02 billion

Since its IPO in 2007, the company has delivered a total shareholder return of 4,111%, with 1,525% over the past decade.

The Acquisition Engine

The company has completed 78 acquisitions since 2023, with 29.9% of its skilled nursing operations having been operated for less than three years. Ensign has demonstrated a consistent ability to improve newly acquired operations, with significant enhancements in skilled mix revenue, EBITDAR margins, and occupancy typically achieved within just five quarters of acquisition.

On the company's most recent earnings call, Port noted that the average turnaround building sees occupancy growth of 390 basis points over the first four quarters of Ensign control, along with a 440-basis-point gain in skilled mix revenue and an 80-point rise in EBITDAR margin. Over 45 quarters, those figures are 1,300, 1,400, and 470 basis points, respectively.

Recent Expansion

The Ensign Group on Wednesday announced eight facility acquisitions across six states – Utah, Arizona, Tennessee, Texas, Kansas and Iowa. The additions bring Ensign's growing portfolio to 310 healthcare operations across 14 states.

The Ensign Group acquired nine skilled nursing facilities in Tennessee and Alabama to expand its healthcare operations. The Ensign Group, Inc. has announced the acquisition of several skilled nursing facilities located in Tennessee and Alabama, which includes nine different operations. This acquisition enhances Ensign's presence in Tennessee and establishes its footprint in Alabama.

The pattern continues: disciplined acquisition of struggling facilities, rapid implementation of the Ensign operating model, and consistent improvement in clinical and financial metrics.

Standard Bearer: The Internal REIT

The Company continues to provide additional disclosure on Standard Bearer, which added 18 new assets during the year and since and is comprised of 129 owned properties. Of these assets, 97 are leased to an Ensign-affiliated operator and 33 are leased to third-party operators.

Standard Bearer represents an evolution of Ensign's capital strategy—building internal real estate value that can eventually be monetized through another spin-off or simply provide additional financial flexibility.

IX. Playbook: Business & Operating Lessons

Ensign's success offers several lessons that extend beyond skilled nursing.

Lesson 1: Decentralization as Competitive Advantage

Most companies centralize as they scale. Ensign has built its entire model on the opposite approach. This "facility-centered" approach has been a cornerstone of the company's success, allowing each operation to function as its own small business while benefiting from the resources and support of the larger organization.

This works because nursing home operations are fundamentally local. The relationships with referring hospitals, the labor market dynamics, the community reputation—all of these are hyperlocal. A centralized decision-maker will always be slower and less informed than a capable local leader.

The key insight: decentralization requires investing heavily in leadership development. You cannot delegate authority to people who are not prepared to exercise it responsibly.

Lesson 2: The Power of Integrated Therapy

Ensign-affiliates provide dedicated full-time in-house therapy teams—no outside agencies—so guests can rely on getting to know the same, caring therapists for the duration of their stay. The rehabilitation teams work with each guest, their family and their healthcare provider to determine the best care and treatment plans.

Owning therapy rather than outsourcing it creates several advantages: better coordination with nursing staff, more consistent quality, and improved economics. It also helps with the Medicare mix, as therapy-intensive patients generate higher reimbursement.

Lesson 3: Spin-offs as Value Creation

The decisions in 2014 and 2019 to spin off CareTrust REIT and The Pennant Group were transformative. These moves allowed ENSG to concentrate on its core skilled nursing and therapy operations while giving investors distinct investment opportunities.

The spin-off strategy reflects a clear understanding that conglomerate structures often destroy value. Different businesses have different optimal capital structures, different investor bases, and different strategic priorities. Forcing them together creates friction and inefficiency.

Lesson 4: Culture as Operating System

We rely on our culture to accomplish our mission of dignifying long term care. We have a unique set of core values, known as CAPLICO, that shape our organization.

Many companies talk about culture. Few invest as systematically in codifying and reinforcing it. CAPLICO is not just a poster on the wall—it is the framework through which decisions are made, performance is evaluated, and leaders are developed.

Lesson 5: Contrarian Acquisition Strategy

Industry consolidation has been a significant trend, with larger operators acquiring smaller, independent facilities. Ensign has benefited from this trend through its acquisition strategy, focusing on underperforming operations that can be improved through the implementation of its operating model. The company's strong balance sheet and operational expertise position it well to continue this growth strategy.

While competitors chase well-run facilities that command premium prices, Ensign systematically pursues the opposite: struggling operations that can be acquired cheaply and transformed through better management. This requires operational confidence that few organizations possess.

X. Porter's Five Forces Analysis

Understanding Ensign's competitive position requires examining the structural forces shaping the skilled nursing industry.

1. Threat of New Entrants: LOW-MODERATE

Barriers to entry in skilled nursing are substantial. Section 4432(a) of the Balanced Budget Act of 1997 modified how payment is made for Medicare skilled nursing facility services. Effective with cost reporting periods beginning on or after July 1, 1998, SNFs are no longer paid on a reasonable cost basis.

New entrants must navigate: - State licensing and certificate-of-need requirements - Medicare and Medicaid certification processes - Significant capital requirements for facilities - The operational expertise needed to manage complex clinical environments

However, individual facility entry remains possible for experienced operators, creating continuous competitive pressure at the local level.

2. Bargaining Power of Suppliers: MODERATE-HIGH

Labor is the critical input in skilled nursing, and the workforce has substantial leverage. When asked about their priorities in the workplace for 2024, nurses identified several key areas. Foremost among these was compensation, with 75% of respondents emphasizing the importance of better pay. Also, 68% of nurses expressed a desire for improved nurse-to-patient ratios, and 58% said they wanted better schedules.

The nursing shortage gives workers leverage that constrains margins across the industry. Operators who cannot attract and retain staff face compounding problems: agency labor is expensive, quality suffers, surveys deteriorate, and referrals decline.

3. Bargaining Power of Buyers: HIGH

The dominant buyers—Medicare and Medicaid—have essentially unlimited negotiating power. They set prices administratively, and providers can either accept the rates or exit the market.

Skilled nursing facilities generally receive lower reimbursement rates under MA plans than under traditional Medicare. The Federal government, through CMS, pays MA plans a fixed, or 'capitated', monthly amount per beneficiary.

This dynamic creates an ongoing squeeze on margins that can only be offset through operational excellence—exactly where Ensign excels.

4. Threat of Substitutes: MODERATE-HIGH

The threat of substitutes is increasing as healthcare moves toward lower-cost settings. Home health, hospital-at-home programs, and aging-in-place preferences all reduce demand for institutional care.

However, skilled nursing addresses a specific clinical need—patients who require intensive therapy and nursing care but do not need hospital-level intervention. For this population, there are limited alternatives.

5. Industry Rivalry: HIGH

As of 2023, Ensign operated approximately 2% of all skilled nursing beds in the United States, making it one of the larger operators in a highly fragmented market where the top 10 providers control less than 20% of total capacity.

The fragmented nature of the industry creates intense competition for: - Referrals from hospitals and physician groups - Staff, particularly nurses - Quality ratings that drive reimbursement and reputation

However, Ensign's scale provides advantages in this competitive environment, particularly in building relationships with managed care organizations and developing regional density.

XI. Hamilton's 7 Powers Analysis

Hamilton Helmer's framework identifies seven potential sources of durable competitive advantage. Ensign possesses several, though not all.

1. Scale Economies: MODERATE

Ensign's Service Center provides back-office efficiencies across its portfolio. Ensign Services provides service and support to over 360 facilities in the post-acute care continuum that employs over 55,000 employees.

However, care delivery is inherently local—you cannot centralize bedside nursing. Scale benefits are meaningful but limited primarily to support functions.

2. Network Economies: WEAK-MODERATE

The cluster model creates regional knowledge sharing and the EPCC provides care continuum benefits with Pennant. But this is not a traditional network effect business where each additional participant increases value for all others.

3. Counter-Positioning: STRONG

This is perhaps Ensign's most powerful strategic advantage. "At the heart of that philosophy is the seemingly simple conclusion that running an individual nursing home is a difficult task that requires a leader with an active mind. Port drew a distinction between Ensign and other skilled nursing operators by pointing out that his company intentionally doesn't follow the traditional ladder of promoting solid building-level leaders into corporate roles — but instead incentivizes them to remain on the ground level."

Incumbent competitors cannot easily adopt Ensign's decentralized model without dismantling existing structures. The transition costs—organizational disruption, cultural resistance, compensation restructuring—are prohibitive for established operators.

4. Switching Costs: LOW

Patients and families can choose different facilities. However, hospital referral relationships create meaningful stickiness at the institutional level.

5. Branding: WEAK-MODERATE

Local facility reputation matters more than corporate brand in skilled nursing. CMS Five-Star ratings create quality signaling that partially substitutes for brand recognition.

6. Cornered Resource: MODERATE

Ensign's most valuable cornered resource is its leadership pipeline. The company has spent decades developing facility-level leaders who can run operations with minimal corporate oversight. This human capital cannot be easily replicated.

Meanwhile, local leaders continue to recruit future CEOs for Ensign-affiliated operations and the company has a "deep bench" of CEOs in training. An influx of local leadership and decentralized transition model allows growth minus the "typical corporate bottlenecks."

7. Process Power: STRONG

Ensign's acquisition-turnaround playbook represents genuine process power. The ability to consistently improve acquired operations—documented through systematic performance tracking—is difficult to replicate and creates durable advantage.

Ensign has demonstrated a consistent ability to improve newly acquired operations, with significant enhancements in skilled mix revenue, EBITDAR margins, and occupancy typically achieved within just five quarters of acquisition. This pattern of improvement continues well beyond the initial integration period, with operations showing continued growth through the 45th quarter.

XII. Key Risks and Regulatory Considerations

No analysis of Ensign would be complete without acknowledging the material risks facing the business.

Reimbursement Risk

The company faces numerous risks outlined in the safe harbor statement, including potential regulatory changes, reduced reimbursement rates, and increased borrowing costs, which could adversely impact its future operations. There is potential vulnerability as indicated by the significant portion of Medicaid revenue (39.7% for 2024), raising concerns about dependency on government funding.

Medicaid reimbursement is set by states with varying budget pressures. Medicare Advantage plans continue to grow and reimburse at lower rates. Federal deficit concerns could lead to cuts in healthcare spending.

Regulatory Compliance

The skilled nursing industry operates under intense regulatory scrutiny. The SNF VBP Program is a pay-for-performance program. As required by statute, CMS withholds 2% of SNFs' Medicare fee-for-service Part A payments to fund the SNF VBP Program.

Historical Legal Matters

It is important to note that Ensign has faced legal challenges in its history. The Ensign Group Inc., a skilled nursing provider based in Mission Viejo, Calif., agreed to pay $48 million to resolve allegations that it knowingly submitted to Medicare false claims for medically unnecessary rehabilitation therapy services.

"The culture of the company emphasized profits over compliance and patient needs," said the whistleblower attorney. "Each facility administrator was required by company management to set what were called 'Big Hairy Audacious Goals' for the number of Medicare patients and the amount of Medicare reimbursement per day."

This 2018 settlement addressed issues from earlier in the company's history. Investors should monitor compliance practices as an ongoing concern, though Ensign has invested significantly in compliance infrastructure since then.

Labor Market Pressures

The healthcare sector faces challenges from high operational and labor costs, reimbursement pressures that squeeze margins, and regulatory uncertainty.

The nursing shortage represents a structural challenge that will persist for years. Companies that cannot attract and retain staff will face compounding problems.

Leadership Transition

Christopher Christensen, Executive Chairman and member of the Ensign Board of Directors, has provided notice to the board of his intent to retire from both his roles effective September 1, 2025. Barry R. Port, Ensign's Chief Executive Officer, has been appointed to serve as Chair of the Board of Directors.

While the transition appears orderly, any leadership change at a company built on culture carries execution risk. The average tenure of the management team and the board of directors is 11.3 years and 6.1 years respectively.

XIII. Critical KPIs for Ongoing Monitoring

For investors tracking Ensign's ongoing performance, three metrics deserve particular attention:

1. Same-Store Skilled Mix Revenue Growth

Skilled mix—the proportion of patients covered by higher-reimbursing Medicare rather than lower-reimbursing Medicaid—is the single most important driver of facility-level economics. Ensign reported skilled census for same store and transitioning operations increased by 7.4% and 13.5% respectively compared to Q2 2024. Improvements in turnover, lower staffing agency labor, and trusted partners all played a role.

Growing skilled mix in existing facilities demonstrates that Ensign's operating model continues to generate clinical and referral advantages.

2. Transitioning Facility Performance

Same Facilities and Transitioning Facilities managed care days for the quarter improved substantially from prior year.

The trajectory of newly acquired operations reveals whether Ensign's turnaround playbook remains effective. If transitioning facilities take longer to improve, or show smaller gains, it signals execution challenges.

3. Occupancy Trends

Occupancy rates improved, with same facilities increasing by 2.7% and transitioning facilities by 4.1% over the prior year.

Occupancy directly drives revenue and fixed-cost absorption. Post-COVID recovery in occupancy has been a key driver of margin expansion.

XIV. Investment Considerations: Bull and Bear Cases

The Bull Case

Ensign represents a rare combination: a well-managed operator in a fragmented, troubled industry. The investment thesis rests on several pillars:

-

Continued consolidation opportunity: Industry closures have accelerated, creating acquisition opportunities for well-capitalized operators.

-

Demographic tailwinds: An aging population will require more post-acute care, regardless of industry challenges.

-

Operational moat: The company's decentralized operating model, focus on clinical excellence, and disciplined acquisition approach have created a virtuous cycle that continues to drive performance.

-

Real estate optionality: Standard Bearer creates embedded value that could be monetized through future spin-offs.

-

Management quality: The depth of operational leadership and cultural continuity provides confidence in execution.

The Bear Case

Several factors could undermine the investment thesis:

-

Reimbursement pressure: Medicare and Medicaid cuts could compress margins faster than operational improvements can offset.

-

Labor market deterioration: If nursing shortages worsen or labor costs accelerate, the entire industry could face margin compression.

-

Medicare Advantage growth: Skilled nursing facilities generally receive lower reimbursement rates under MA plans than under traditional Medicare. Continued MA expansion represents an ongoing headwind.

-

Culture dilution: As Ensign scales, maintaining its decentralized culture becomes increasingly challenging.

-

Regulatory risk: The federal staffing mandate, while currently challenged, represents an existential threat if implemented.

-

Valuation: After years of strong performance, Ensign trades at premium multiples that leave limited margin of safety.

XV. Conclusion: What Ensign Teaches About Value Creation

The Ensign Group offers a compelling case study in value creation through operational excellence in a challenging industry.

The company's success stems not from financial engineering or regulatory arbitrage, but from a fundamentally different operating philosophy: empower local leaders, invest in culture, and build capabilities rather than extract value.

We look forward to 2025 with confidence that our partners will continue to manage and innovate while balancing the addition of newly acquired operations. When we consider the current health of our organization, combined with our culture and proven local leadership strategy, we are well-positioned to have another outstanding year in 2025.

For long-term investors, Ensign represents a rare opportunity: a well-managed operator with durable competitive advantages in a fragmented industry with substantial consolidation runway. The risks—reimbursement, labor, regulation—are real but manageable for an operator with Ensign's capabilities.

The broader lesson extends beyond skilled nursing. In any operationally intensive business, the quality of front-line leadership determines outcomes. Companies that invest in developing, empowering, and retaining those leaders create advantages that are difficult for competitors to replicate.

Ensign has spent a quarter-century proving that nursing homes can be run well—and that doing so creates substantial value for patients, employees, and shareholders alike. Whether the next quarter-century brings similar success depends on whether the company can maintain its culture as it scales, navigate an increasingly challenging reimbursement environment, and continue attracting the leadership talent that makes its model work.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube