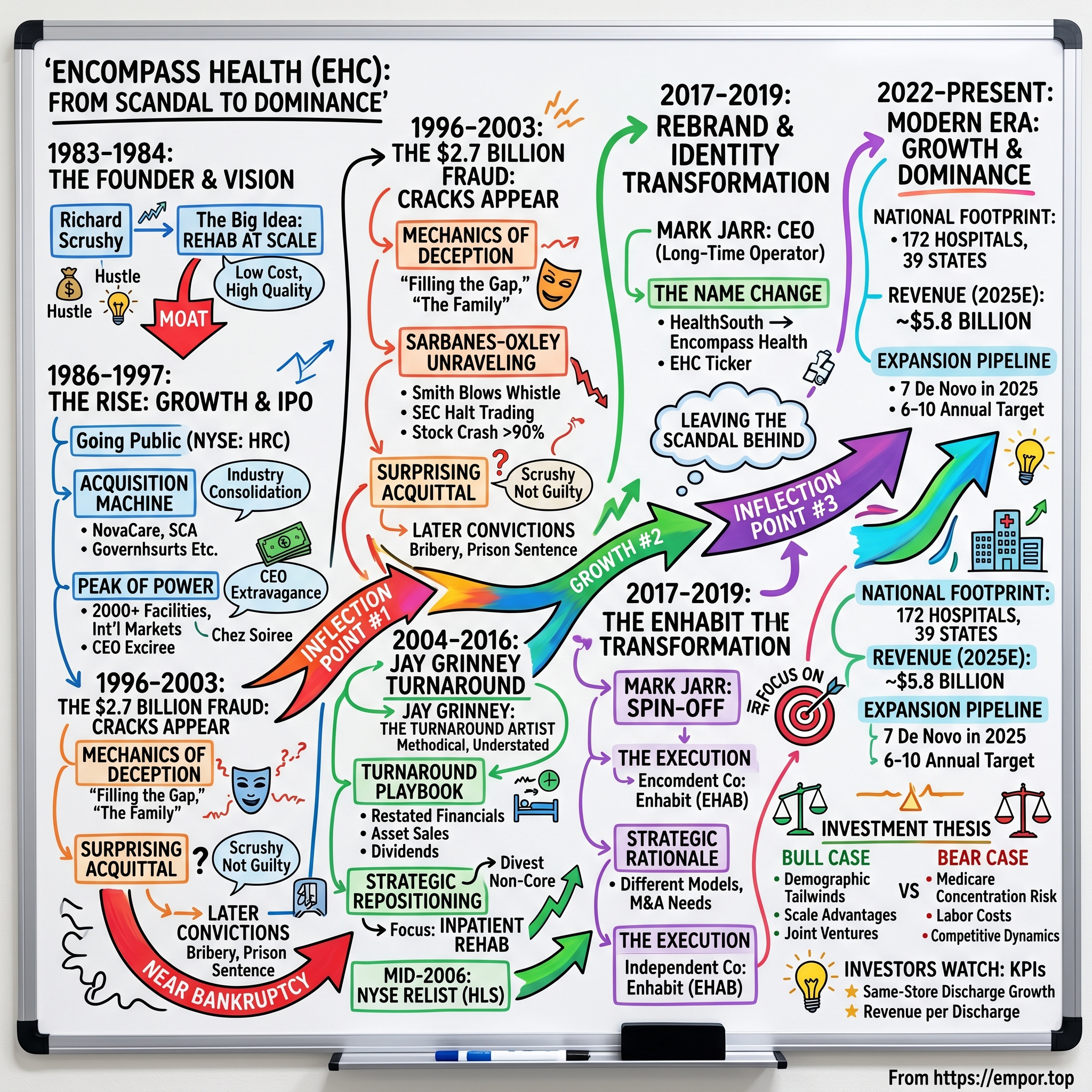

Encompass Health: From Scandal to Dominance in American Healthcare

Introduction: The Rehabilitation Empire

In a nondescript hospital room somewhere in America, a 77-year-old stroke survivor struggles to lift her left arm. Three hours of intensive therapy each day. Physical therapists guiding her through repetitive motions. Occupational specialists retraining basic life skills. Speech pathologists working to restore words that once flowed effortlessly. This scene plays out approximately 250,000 times each year within the walls of Encompass Health's rehabilitation hospitals.

The company operates 172 hospitals across 39 states and Puerto Rico, serving approximately one in three patients receiving inpatient rehabilitation services in the United States. The Birmingham, Alabama-based company stands as the largest owner and operator of inpatient rehabilitation hospitals in the nation, commanding a market position that would seem unassailable.

But the numbers tell only part of the story. Behind the current dominance lies one of the most remarkable corporate turnarounds in American healthcare history—a resurrection from the ashes of what was, at the time, one of the largest accounting frauds ever perpetrated on American investors.

The scheme added approximately $2.7 billion in fictitious income to the company's books and records during the course of the conspiracy. Fifteen executives pleaded guilty. The company's stock crashed by more than 90%. Bondholders threatened to call their loans. Bankruptcy loomed. And yet, two decades later, Encompass Health trades near all-time highs, generates over $5 billion in annual revenue, and continues to expand its physical footprint at a pace of 6-10 new hospitals per year.

The central question for investors is not merely whether this company recovered—it clearly did—but rather: What structural advantages allowed it to survive and thrive when so many scandal-ridden companies simply disappeared? And can those same advantages sustain dominance as America's healthcare landscape continues to shift?

This is a story about a charismatic founder who built an empire on audacious vision and apparently didn't care how the numbers were achieved; a turnaround artist who took a broken company and methodically rebuilt it brick by brick; and a quiet operator who inherited a clean slate and focused on nothing but execution. It's also a story about demographic tailwinds, regulatory moats, and the peculiar economics of rehabilitating America's aging population.

The Founder and the Vision (1983-1984)

Richard Scrushy: The Small-Town Hustler Who Dreamed Big

Born in the small town of Selma, Alabama and without a silver spoon in his mouth, young Richard Scrushy doesn't seem to indicate he'll one day be worth nearly $300 million. The son of a middle-class family, his father, Gerald Scrushy, worked as a cash register repairman and his mother, Grace Scrushy, worked as a nurse and respiratory therapist.

At an early age, Scrushy taught himself to play the piano and guitar and was earning money doing odd jobs by the time he was twelve years old. This early industriousness would become the defining characteristic of a man who, for better and ultimately for worse, never stopped hustling.

Scrushy earned a degree in respiratory therapy from the University of Alabama at Birmingham—not the typical pedigree of a future Fortune 500 CEO, but then Scrushy would never be typical of anything. In the late 1970s, following his time teaching at UAB and Wallace State, Scrushy was offered a position with Lifemark Corporation, a Houston, Texas-based health care company. Within a few years of being hired at Lifemark, Scrushy was part of a $100 million operation that included the pharmacy, physical rehabilitation, and hospital acquisition divisions.

At Lifemark, the young executive witnessed firsthand the fundamental shift reshaping American healthcare. The dominant trend was toward a reduction in reimbursement dollars available to traditional medical practitioners. Corporations and insurance companies were trying to cut health care expenditures while, at the same time, costs in the medical field were rising.

Scrushy saw an opportunity where others saw only pressure. "I saw the squeezing of reimbursement in the health care system and I wanted to take advantage of that change," Scrushy said in a 1990 Forbes article. "My idea was to provide high-quality hospital-type rehabilitation services in a low-cost setting."

The insight was simple but profound: patients recovering from strokes, injuries, and surgeries needed intensive rehabilitation, but they didn't need the full apparatus of an acute-care hospital. An outpatient facility could provide high-quality care at a fraction of the cost—and pocket the difference.

The Big Idea: Rehabilitation at Scale

Still working for Lifemark, Scrushy devised a plan for an outpatient diagnostics and rehabilitative health clinic chain. He presented the plan to Lifemark, but the company was unable to act on it due to a company merger that was already underway with American Medical International.

Corporate bureaucracy's loss would become Scrushy's gain. Scrushy left Lifemark in 1983 and founded Amcare, Inc within a year. The new company opened its first facility in Little Rock, Arkansas, and had initial capital between $50,000-$70,000.

The origin story of that capital has become part of business school legend. Scrushy's break came in a Houston restaurant, when a Citicorp venture capitalist overheard Scrushy outlining his business plan and eventually offered a $1 million grubstake, giving birth to what would become HealthSouth.

Whether the story is embellished or not, the result was real. With the assistance of four partners from Amcare Inc. and a one million dollar investment by Citicorp Venture Capital, Scrushy took the quickly growing company and founded HealthSouth Corporation in 1984.

Scrushy convinced four of his Lifemark associates to break ranks with him and move to Birmingham to build the company's first outpatient facility. Their company was incorporated in January 1984 as Amcare Inc. before its name was changed to HealthSouth Rehabilitation Corporation in May 1985.

The timing was fortuitous. Scrushy got into the rehabilitation industry at a good time. During the early 1980s people began to view rehabilitation as a means of reducing medical expenses. Medicare's prospective payment system, introduced in 1983, fundamentally changed hospital economics by paying fixed amounts based on diagnosis rather than cost-plus reimbursement. Suddenly, hospitals had powerful incentives to discharge patients faster—and those patients still needed somewhere to recover.

Scrushy positioned HealthSouth as the answer. The rehabilitation facilities could absorb patients discharged earlier from acute-care hospitals, providing the intensive therapy they needed at lower cost to the healthcare system while generating attractive margins for HealthSouth.

For investors evaluating today's Encompass Health, this original strategic insight remains relevant. The company continues to operate in that same structural position—receiving patients discharged from acute-care hospitals who need intensive rehabilitation but don't require the full resources of a traditional hospital setting. The regulatory and economic dynamics that created the opportunity in 1984 have only intensified over four decades.

The Rise: Rapid Growth and IPO (1986-1997)

Going Public: The Standing Ovation

The company changed its name to HealthSouth Rehabilitation Corporation in 1985 to distinguish itself from other healthcare companies in the market and purchased its first inpatient rehabilitation hospital in early 1986. This was followed by an initial public offering (IPO) on the Nasdaq later that year.

In 1986 the company went public with its initial public offering on the NASDAQ exchange under the ticker symbol HSRC. In September of 1988 the company moved to the New York Stock Exchange and became listed under the symbol HRC.

The IPO roadshow showcased Scrushy's extraordinary salesmanship. His presentations were legendary in their intensity, drawing in investors with visions of a revolutionary healthcare company that would transform how America delivered rehabilitation services. Investment bankers gave him standing ovations—a remarkable response from an audience trained to remain stoically impassive.

Two years after its founding, HealthSouth became a publicly traded company. The next year, HealthSouth expanded into two new fields, worker's compensation and sports medicine, allowing the company to double its earnings and obtain assets close to $100 million.

The Acquisition Machine

Once public, Scrushy showed that his appetite for growth was insatiable. By 1990 the company had expanded to 50 facilities across the U.S. HealthSouth finished out 1992 with $400 million in annual revenue. In 1993 the company made its first large acquisition when it bought 28 hospitals and 45 outpatient rehabilitation facilities from National Medical Enterprise for around $300 million in cash. In 1994 HealthSouth announced it would buy fellow Birmingham based ReLife for $180 million in stock.

The acquisition pace accelerated through the mid-1990s. HealthSouth entered the ambulatory surgery center business in early 1995 with the purchase of Surgical Health Corporation. One month later the company announced the purchase of NovaCare's rehabilitation hospital business. After additional surgery center acquisitions during 1995, including the $1.2 billion acquisition of Surgical Care Affiliates, HealthSouth became the nation's largest provider of outpatient surgery.

By 1994, HealthSouth surpassed the $1 billion mark in revenues. HealthSouth expanded into outpatient surgery services with the acquisition of Surgical Health Corporation in 1995.

The company wasn't just buying facilities—it was consolidating an entire industry. By October 1995, HealthSouth had agreed to purchase the rehabilitation services operations of Caremark International for $127 million in cash. The Caremark operations consisted of 123 outpatient rehabilitation facilities that were generating about $80 million in annual revenues. That gave the company a total of about 440 outpatient facilities and about 40 percent of the total rehabilitation market.

The Peak of Power

HealthSouth had over 2,000 facilities across all 50 states by the end of 1999 and was one of the nation's largest providers of healthcare services. It also had expanded into international markets through its many acquisitions, with facilities in the United Kingdom, Australia, Puerto Rico, Canada, and later Saudi Arabia.

At its peak, it recorded $4.4 billion in revenues, employed more than fifty thousand people worldwide, and operated eighty outpatient rehabilitation services and twelve home health agencies.

In 1998 he made BusinessWeek's list of the nation's highest paid CEOs, having raked in more than $106 million in salary and bonuses and exercising more than $90 million in stock options. He used the money to buy mansions, racing boats, a fleet of cars (including a $135,000 bullet-proof BMW), and a G-5 jet.

The yacht, the Chez Soiree, is just one extravagancy that Scrushy bought with his extreme wealth garnered from HealthSouth's success. He also purchased speedboats, classic cars, airplanes, four mansions and a Lamborghini Murcielago.

Scrushy's extravagance knew few bounds. There were few places in Birmingham that did not carry his name—from the Richard M. Scrushy Building at the University of Alabama to the Richard M. Scrushy Parkway; even an entire campus of Jefferson State Community College bore his name. As if those tributes were not enough, Scrushy built his own self-monument—a museum behind the HealthSouth headquarters in Birmingham that was devoted to his career.

The company's dominance wasn't just about ego—it provided real strategic advantages. The company's dominance as the largest provider in all its lines of business benefited HealthSouth when it came to negotiations with health insurance providers. Growth through acquisitions slowed by the end of the 1990s as the company had acquired many of its competitors.

But even at its height, warning signs were emerging for those willing to look closely. At its height in the late 90s, HealthSouth reported $4.5 billion in revenue—but those numbers were grossly inflated.

The $2.7 Billion Fraud: Cracks Appear (1996-2003)

The Mechanics of Deception

The fraud didn't begin with a single catastrophic decision. It started, as most corporate frauds do, with a small compromise that grew into something monstrous.

During a meeting in 1996, Aaron Beam, co-founder and CFO, told Scrushy they would have to finally report a bad quarter. Scrushy said no, and they devised a way to hide the earnings shortfall.

"I should have had the courage to stand up and say, 'No, we can't cross this line,'" Beam later said. Scrushy promised to deny everything if Beam reported the fraud and accused Beam of not being a team player. "I couldn't sleep," Beam added. "I didn't understand what crossing that line would do to me emotionally and mentally. I hated my job, hated myself. I started drinking more than I should."

The indictment alleges that between 1996 and 2003, internal reports by HealthSouth's corporate accounting staff showed that the company routinely failed to produce sufficient net income to meet the expectations of Wall Street securities analysts, the market and its own internal budgets—a failure that Scrushy and others allegedly referred to as "not making the numbers." According to the indictment, Scrushy and others devised a scheme to inflate HealthSouth's earnings by making false and fraudulent entries in HealthSouth's books and records, and to cover up the accounting fraud with false financial filings and statements.

Pursuant to the scheme, on a quarterly basis, HRC's senior officers would present Scrushy with an analysis of HRC's actual, but as yet unreported, earnings for the quarter as compared to Wall Street's expected earnings for the company. If HRC's actual results fell short of expectations, Scrushy would tell HRC's management to "fix it" by recording false earnings on HRC's accounting records to make up the shortfall. HRC's senior accounting personnel then convened a meeting to "fix" the earnings shortfall. At these meetings, HRC's senior accounting personnel discussed what false accounting entries could be made and recorded to inflate reported earnings to match Wall Street analysts' expectations.

According to the indictment, the co-conspirators referred to those methods as "filling the hole" or "filling the gap."

In the indictment, Scrushy was accused of using intimidation, threats, and cash payments to coerce top HealthSouth executives into committing fraud. These top executives called themselves "The Family" and referred to their creative accounting as "filling the gap." The group attempted to hide the false earnings by illegally inflating balances of accounts such as fixed assets and estimated insurance reimbursements.

HealthSouth added thousands of fictitious items to its assets. Most of these were valued under $5,000, since auditors rarely checked assets with such a low value.

From 1996 through 2002, Scrushy received approximately $267 million in compensation from HealthSouth, including $7.5 million in base salary, more than $53 million in bonuses, and stock options valued at more than $206 million when exercised.

Sarbanes-Oxley and the Unraveling

The fraud might have continued indefinitely had it not been for external events that changed the corporate landscape entirely.

Scandals at Enron, Tyco, and WorldCom pushed Congress to pass the Sarbanes-Oxley Act of July 2002, which mandated transparent financial reporting to protect investors from fraud. Scrushy abruptly sold $75 million in HealthSouth stock just as the legislation became law.

That law is what led Smith to blow the whistle on Scrushy and HealthSouth.

In 2003, FBI agents opened a federal investigation of accounting fraud on a massive scale at HealthSouth, with fraudulent entries mounting as high as $2.7 billion. Nearly put into bankruptcy, the company fired its CEO Richard Scrushy and spent three years restructuring its operations and financial reporting procedures.

On March 19, 2003, the SEC halted trading of HealthSouth on the New York Stock Exchange, charging that the company inflated its earnings by more than 10 percent and overstated its profits by nearly $2.5 billion between 1999 and 2002. The company was also removed from the Standard and Poor's 500 index. After trading as high as $30.81 in 1998, HealthSouth fell to $3.91 per share when trading was halted.

U.S. Attorney Alice Martin headed up the prosecution. She netted guilty pleas from all five CFOs in company history.

For nearly a decade, HealthSouth Corp., its investment bankers UBS Warburg and UBS Securities LLC, and its outside auditor Ernst & Young perpetrated the largest and most pervasive securities fraud in the history of U.S. healthcare, causing billions of dollars in losses to investors.

The Surprising Acquittal

Scrushy became the first CEO to be tried under the Sarbanes–Oxley Act when he was indicted by the U.S. Department of Justice.

Scrushy was charged with 36 of the original 85 counts but was acquitted of all charges on June 28, 2005, after a jury trial in Birmingham.

As trial began, Scrushy's colorful defense attorney, Jim Parkman, conceded to the jury that a fraud occurred at HealthSouth, but claimed that his client had no knowledge of the fraud, which was in fact executed by rogue and dishonest employees.

Richard Scrushy was found not guilty of directing an accounting fraud at HealthSouth, a chain of rehabilitation hospitals he founded 20 years ago. Fifteen former executives have pleaded guilty for their part in the fraud, including five former chief financial officers who testified against Scrushy during the trial.

The acquittal shocked observers. How could the CEO and Chairman, who received nearly $270 million in compensation during the fraud period, not have known about $2.7 billion in fictitious entries?

Despite multiple chief executives testifying against Scrushy, prosecutors were unable to produce any material evidence that he had been involved in the fraudulent accounting.

But justice, delayed, eventually arrived. Four months after his acquittal in Birmingham, on October 28, 2005, Scrushy was indicted by a federal grand jury in Montgomery, Alabama, along with former Alabama Governor Don Siegelman. The indictment included 30 counts of money laundering, extortion, obstruction of justice, racketeering, and bribery.

Scrushy was convicted on bribery charges and sentenced to seven years in prison. On June 18, 2009, Judge Horn ordered Scrushy to pay $2.87 billion in damages. Judge Horn stated, "Scrushy knew of and actively participated in the fraud" and referred to Scrushy as the "CEO of the fraud."

On July 25, 2012, Scrushy was released from federal custody.

Robbins Geller's prosecution led to UBS to pay $117 million and Ernst & Young paying $109 million to the shareholders. The combined recovery of $671 million from HealthSouth, UBS and E&Y is among the largest settlements in securities class action history.

Inflection Point #1: The Jay Grinney Turnaround (2004-2016)

The Crisis at Its Worst

In 2004, Jay was brought in to turn HealthSouth around following a massive accounting scandal. The company was in complete disarray—it had lost its SEC filing status, its stock price had fallen more than 90% and it was headed toward bankruptcy.

The situation facing the incoming CEO cannot be overstated. The company had lost the confidence of investors, regulators, employees, and patients. It couldn't file financial statements because nobody knew what the real numbers actually were. Bondholders were threatening to call their debt. The SEC was investigating. The FBI had raided headquarters. And fifteen executives had already pleaded guilty to various crimes.

Jay Grinney: The Turnaround Artist

Jay F. Grinney (born March 20, 1951) is an American health care executive. He is the former president and chief executive officer of Birmingham, Alabama-based HealthSouth Corporation, now known as Encompass Health Corporation.

Jay F. Grinney was born on March 20, 1951, in Milwaukee, Wisconsin. He was raised in Racine, Wisconsin. He graduated from St. Olaf College in 1973. He earned MBA and MHA degrees from Washington University.

Grinney came from an entirely different world than Scrushy. Where Scrushy was flamboyant and charismatic, Grinney was methodical and understated. Where Scrushy flew on private jets and collected mansions, Grinney was known for driving a modest car and living quietly in Birmingham.

In 1990, Grinney joined HCA. He served as the president of the Houston Division of Columbia Hospital Corporation until 1994, when Columbia announced a merger with Nashville, Tennessee-based Hospital Corporation of America. He then continued as the president of HCA's Eastern Group. In 2004, he was chosen by HealthSouth Corporation to serve as its president and chief executive officer.

"This is a great opportunity for Jay and we wish him well," said Jack O. Bovender, Jr., Chairman and Chief Executive Officer of HCA. "In his years at HCA he has proven to be an intelligent, principled and tenacious leader who is focused on patient care. These qualities will serve him very well as a chief executive."

The traits Bovender identified—intelligence, principle, tenacity, and patient focus—would all prove essential in the years ahead.

The Turnaround Playbook

Upon becoming CEO Grinney recruited a first-class management team and embarked on a multiple-year turnaround.

Jay Grinney, president of HCA's Eastern division, was brought in as HealthSouth's new president and CEO in 2004. U.S. Can Corporation executive John Workman was brought in to serve as the company's CFO, and Mike Snow, president of HCA's Gulf Coast division, joined as COO. The company sold or closed underperforming facilities and disposed of corporate waste accrued under Scrushy, including most of the company's fleet of corporate jets.

The turnaround effort required more than one million man-hours to achieve. The company had to restate two years of fraudulent financial statements and prepare new, audited financial statements from scratch. Imagine untangling $2.7 billion in fictitious entries spread across thousands of accounts in hundreds of facilities.

Grinney oversaw the divestitures of non-core businesses, created a strong and flexible balance sheet, and developed a capital allocation strategy that included investments in improving and growing the Company, the initiation of a quarterly dividend and the opportunistic repurchases of the Company's common stock. He also created a robust development pipeline and led many successful transactions, including the acquisitions of Encompass Home Health and Hospice, Reliant Hospital Partners, and CareSouth, successfully expanding the HealthSouth network to 34 states.

The settlements alone were staggering: $100 million to the SEC, $325 million to the Department of Justice, and $445 million to resolve the class action litigation.

By the mid to late 2006 HealthSouth completed its recovery and relisted its stock on the New York Stock Exchange under the symbol HLS.

Strategic Repositioning

Grinney's strategic insight was to recognize what HealthSouth actually was versus what Scrushy had tried to make it. Under Scrushy, the company had diversified into surgery centers, diagnostic imaging, occupational health, and acute care hospitals. Grinney methodically divested non-core businesses to focus on what the company did best: inpatient rehabilitation.

Grinney and his team then focused on growing the company by developing hospitals in new markets and acquiring competitors, including the $730 million purchase of Reliant Health Partners. This growth continued as HealthSouth expanded into home health and hospice services with the $750 million acquisition of Encompass Home Health and Hospice in 2014, followed by the $170 million purchase of CareSouth Home Health and Hospice a year later.

Leo I. Higdon Jr., Chairman of HealthSouth's Board of Directors, said, "Jay joined HealthSouth as President and CEO at a critical time in the Company's history and led HealthSouth through a successful turnaround and eventual repositioning as one of the nation's leading providers of post-acute services."

"Perhaps Jay's most enduring achievement has been establishing a corporate culture predicated on quality, integrity, compliance, and mutual respect," said Mr. Higdon.

That cultural transformation may have been Grinney's most important contribution. The company that emerged from the scandal was fundamentally different in its DNA—built on transparency, compliance, and doing things the right way rather than just making the numbers.

HealthSouth Corporation today announced that President and Chief Executive Officer, Jay Grinney, 65, will retire from the Company, effective December 31, 2016. HealthSouth's Board of Directors has appointed current Executive Vice President and Chief Operating Officer, Mark J. Tarr, 55, to succeed Mr. Grinney as President, Chief Executive Officer and a member of the Board upon his retirement.

Inflection Point #2: The Rebrand and Identity Transformation (2017-2019)

Leadership Transition

Mr. Tarr is a proven healthcare executive who has held a number of leadership positions at HealthSouth during his 23-year career with the Company. Mr. Tarr was named Executive Vice President and Chief Operating Officer on February 24, 2011, having served as Executive Vice President of Operations since October 1, 2007, and as President of the Company's Inpatient Division since September 2004.

Mark held various leadership roles at HealthSouth Corporation, including Executive Vice President and Chief Operating Officer, and played a crucial role in managing operations for numerous hospitals and acquisitions. Mark's career also includes administrative positions at Tenet Healthcare and Charter Medical, as well as an early career role at Georgia-Pacific. Mark earned a Bachelor of Science in Marketing from Ball State University and an MBA from Emory University's Goizueta Business School.

Mark Tarr was named President and Chief Executive Officer, Director on December 2016, having served as executive vice president of operations since Aug. 1, 2007, and as president of the company's inpatient division since September 2004. Tarr joined HealthSouth in 1993, and has held various management positions within the company, including serving as a senior vice president with responsibility for all inpatient operations in Texas, Louisiana, Arkansas, Oklahoma and Kansas from 1997 to 2004.

The transition from Grinney to Tarr was notably different from typical CEO transitions. Tarr wasn't a turnaround specialist brought in from outside—he was an operator who had spent 23 years inside the company, rising through the ranks from hospital administrator to CEO. He knew every aspect of the business intimately.

The Name Change

It acquired Encompass Home Health and Hospice of Dallas, Texas in late 2014 and changed its name to Encompass Health Corp. on January 2, 2018, altering its ticker symbol to EHC.

The 2018 name change from HealthSouth to Encompass Health was far more than cosmetic. The HealthSouth brand carried baggage that no amount of time could fully erase. Every news story about the company mentioned the fraud. Every investor presentation had to address the scandal's legacy. The name itself had become an anchor.

The establishment of Enhabit Home Health & Hospice will further strengthen Enhabit's focus on high-quality, cost-effective care delivered in the home setting. Enhabit Home Health & Hospice chose the name Enhabit because it intuitively is linked to the home. Drawn from the word "inhabit," the name evokes a sense of comfort and well-being with that promise enlivened by the quality of care Enhabit's clinicians bring to every patient's home. The "en" of Enhabit connects the company to its Encompass legacy.

The rebrand was part of a deliberate strategy to position the company for a new era. The "Encompass" name came from the home health and hospice acquisition, and the new identity reflected the company's integrated approach to post-acute care—a continuum from hospital to rehabilitation facility to home.

For investors, the name change marked the end of an era. The scandal was definitively in the past. The company could now be evaluated on its own merits rather than as a cautionary tale about corporate fraud.

Inflection Point #3: The Enhabit Spin-Off and Strategic Focus (2021-2022)

The Decision to Separate

The decision to split the businesses didn't come out of left field. During the third quarter's earnings call, President, CEO and Director Mark Tarr told investors to expect a spinoff, split-off or carve-out IPO during the first half of 2022. "We have thoroughly evaluated a broad array of public and private transaction alternatives and further believe that affecting the separation via the formation of an independent public company is superior to the other alternatives considered."

Encompass Health Corporation, a national leader in integrated healthcare, offering facility-based and home-based patient care through its network of inpatient rehabilitation hospitals and home health and hospice agencies, announced its intention to spin off its home health and hospice business to form an independent, publicly traded company and to rebrand the HH&H Business as Enhabit Home Health & Hospice. The Encompass Health Board of Directors believes that the separation of its inpatient rehabilitation business and the HH&H Business into two independent, publicly traded companies will provide significant benefits to both businesses and their stakeholders, including improving the strategic and operational flexibility of each business.

Strategic Rationale

Encompass decided to spin the business unit off because it has unique management, finance and M&A needs compared with the overall company. It believes the deal will "allow investors to more clearly understand the separate business models, financial profiles and investment identities of the two companies."

The home health business and the inpatient rehabilitation business, while both serving post-acute patients, operated under fundamentally different economic models. Home health involved sending clinicians to patients' homes—a dispersed, labor-intensive model with different capital requirements and growth dynamics. Inpatient rehabilitation involved building specialized hospitals with intensive therapy programs—a capital-intensive, facility-based model with different scale advantages.

The home health care portion of the company had net revenue of $1.1 billion in 2021, up from $507 million in 2015. The hospice business generated $209 million in revenue in 2021.

The Execution

Enhabit Home Health & Hospice, a leading national home health and hospice provider, announced it is now an independent, publicly traded company following the completion of its spin-off from Encompass Health Corporation. Enhabit began trading regular way on the New York Stock Exchange on July 1, 2022, under the ticker symbol "EHAB."

Under the terms, every Encompass Health shareholder received one Enhabit common share for every two EHC common shares held.

As of day one, Enhabit had 10,000 employees at 351 locations in 34 states.

The spin-off allowed Encompass Health to sharpen its focus exclusively on facility-based inpatient rehabilitation—its most profitable and core segment. Since the separation, Encompass Health has been a pure-play on inpatient rehabilitation, making it easier for investors to understand and value.

For investors evaluating Encompass Health today, the spin-off is significant because it removed a lower-margin, higher-growth business with different characteristics. What remains is a focused inpatient rehabilitation company with clearer economics and more predictable growth patterns.

The Modern Era: Growth and Dominance (2022-Present)

Current Scale and Position

With a national footprint that includes 172 hospitals in 39 states and Puerto Rico, the Company provides high-quality, compassionate rehabilitative care for patients recovering from a major injury or illness, using advanced technology and innovative treatments to maximize recovery.

As the largest operator of inpatient rehabilitation facilities, Encompass Health operates 170 hospitals across 39 states and Puerto Rico, generating approximately $5.8 billion in revenues as of September 30, 2025.

Encompass Health revenue for the twelve months ending June 30, 2025 was $5.669B, an 11.8% increase year-over-year. Encompass Health annual revenue for 2024 was $5.373B, an 11.91% increase from 2023. Encompass Health annual revenue for 2023 was $4.801B, a 10.41% increase from 2022.

Financial Performance

Fourth quarter 2024 revenue growth of 12.7% resulted primarily from discharge growth of 7.8%, including same-store growth of 5.8%. Net patient revenue per discharge grew 4.2%. Cash flows provided by operating activities increased 38.7% to $278.8 million.

Second quarter 2025 revenue growth of 12.0% resulted from increased discharges and pricing. Total discharges grew 7.2%, inclusive of same-store growth of 4.7%. Net patient revenue per discharge grew 4.2%.

"During the quarter, we further increased our capacity to serve patients in need of inpatient rehabilitation care by opening three new hospitals and adding 39 beds to existing hospitals," said President and Chief Executive Officer Mark Tarr in Q3 2025. "Our new hospitals include our first in Connecticut, a 40-bed hospital in Danbury; a 50-bed hospital in Daytona Beach, Florida; and a 50-bed hospital in Wildwood, Florida (The Villages)."

Expansion Pipeline

The company continues to expand aggressively. It plans to open seven de novo hospitals in 2025, along with a 50-bed satellite facility, and add 100-120 beds to existing hospitals, further strengthening its national footprint.

On November 21, 2025, Encompass Health Corp. announced plans to build a freestanding, 50-bed inpatient rehabilitation hospital in Fishers, Indiana.

In June 2025, Encompass Health announced preliminary plans to build a freestanding, 50-bed inpatient rehabilitation hospital in North Las Vegas, Nevada.

In August 2025, Encompass Health Corp. and BSA Health System announced a joint venture arrangement to own and operate a freestanding, 50-bed inpatient rehabilitation hospital in Amarillo, Texas.

For 2025-2027, Encompass Health has set ambitious growth targets, including 6-10 de novo hospitals per year, 80-120 bed additions annually, and a 6-8% compound annual growth rate in discharges.

Revenue Mix and Reimbursement

The company's revenue sources remain heavily concentrated in Medicare, which accounted for 64.1% of Q3 2025 revenue, followed by Medicare Advantage at 16.6% and Managed Care at 11.1%.

The rating agency expects Encompass Health's EBITDA margin to improve following an increase in Medicare reimbursement rates for inpatient rehabilitation facilities. Medicare rates for 2026 will increase by 2.6% for inpatient rehabilitation services, which should support margin expansion.

The demand for inpatient rehabilitation services remains considerably underserved and continues to grow as the U.S. population ages. The Medicare beneficiary population is the fastest growing segment of the US population. It is estimated that by 2030, one in five Americans, more than 70,000,000 people, will be aged 65 or older. The 65 or older population has been growing consistently at a CAGR of approximately 3%. The average age of our Medicare beneficiary patient is 77 years old, and the age 75+ population is growing at approximately 4%. Yet the supply of licensed IRF beds in the US has increased only nominally. As a result, the demand for treatment of complex medical conditions such as stroke necessitating IRF care intensity is significantly underserved.

Investment Thesis: Bull and Bear Cases

The Bull Case

Demographic Tailwinds: The 65+ population in America is growing at approximately 3% annually, with the 75+ cohort growing even faster at 4%. These are the patients most likely to need inpatient rehabilitation services following strokes, hip fractures, cardiac events, and other conditions. The company's average Medicare patient is 77 years old, placing Encompass squarely in the crosshairs of one of the most predictable demographic trends in developed economies.

Supply-Constrained Market: Despite growing demand, the supply of licensed inpatient rehabilitation facility beds has barely increased. Building a new rehabilitation hospital requires regulatory approvals (certificate of need in many states), substantial capital investment ($50+ million per facility), specialized staffing, and years to ramp to profitability. Encompass's existing footprint of 172 hospitals represents a significant barrier to entry.

Scale Advantages: As the largest operator, Encompass benefits from purchasing power, shared services infrastructure, best-practice sharing across facilities, and brand recognition with referral sources. CEO Mark Tarr stated, "The demand for inpatient rehabilitation services remains considerably underserved." He also highlighted, "We treat more patients with IRF-appropriate conditions than any other provider."

Joint Venture Model: The company increasingly partners with acute-care hospital systems through joint ventures, where Encompass operates the rehabilitation hospital and the health system provides patient referrals. This model aligns incentives, reduces capital requirements, and creates sticky referral relationships.

Medicare Reimbursement Stability: Medicare rates for 2026 will increase by 2.6% for inpatient rehabilitation services. While Medicare reimbursement is always subject to political risk, the IRF payment system has historically been more stable than other post-acute settings, partly because of the clinical intensity and regulatory requirements that distinguish IRFs from skilled nursing facilities.

Balance Sheet Strength: Moody's anticipates the company will maintain debt/EBITDA around 2.0 times while continuing to invest in growth through new hospitals and capacity expansion at existing facilities. The company's disciplined approach to creating a flexible capital structure, with no significant debt maturities until 2028, positions it well for sustained growth.

The Bear Case

Medicare Concentration Risk: Medicare accounted for 64.1% of Q3 2025 revenue, with Medicare Advantage adding another 16.6%. This concentration creates significant exposure to any adverse changes in federal reimbursement policy. A single legislative change could dramatically impact profitability.

Medicare Advantage Growth: The shift from traditional Medicare to Medicare Advantage plans represents a structural headwind. MA plans have more flexibility to deny or delay coverage, require prior authorization, and negotiate lower rates. While Encompass has managed this transition reasonably well, continued growth in MA penetration could pressure margins.

Labor Costs and Availability: Rehabilitation hospitals require specialized nurses, physical therapists, occupational therapists, and speech-language pathologists. Employees per occupied bed and the use of contract labor both reached record efficiency levels, although leaders noted these may normalize in future quarters. Labor and benefits costs did rise 14%.

Capital Intensity: Each new hospital requires $50-70 million in capital and 2-3 years to reach full productivity. The growth targets of 6-10 new hospitals annually require sustained capital investment that consumes a significant portion of free cash flow.

Competitive Dynamics: Encompass Health's main competitors include Select Medical Holdings, Kindred Healthcare (private), Vibra Healthcare (private), and rehabilitation units operated within major hospital systems like HCA Healthcare and Universal Health Services. While Encompass is the largest pure-play, integrated health systems can operate rehabilitation units as loss leaders to keep patients within their networks.

Geographic Saturation: Encompass Health's facilities are strategically concentrated in regions with higher populations of elderly residents, particularly in Florida and Texas. As the company expands to 172 hospitals, the best markets become increasingly saturated, and new hospital economics may be less attractive.

Porter's Five Forces Analysis

Threat of New Entrants (Low to Moderate): Certificate of need requirements, capital intensity, specialized staffing, and Medicare certification create meaningful barriers. However, large health systems can build rehabilitation units within existing hospitals, bypassing some barriers.

Bargaining Power of Suppliers (Moderate): Labor markets are tight for specialized therapists and nurses, giving workers meaningful bargaining power. Medical equipment suppliers have less leverage given the company's scale.

Bargaining Power of Buyers (High): Medicare and Medicare Advantage represent over 80% of revenue. The government and large insurers have substantial power to set reimbursement rates, though the regulatory process provides some predictability.

Threat of Substitutes (Low to Moderate): Skilled nursing facilities offer lower-intensity rehabilitation at lower cost, but cannot provide the three hours of daily therapy required for IRF designation. Home health represents an alternative for less acute patients. Long-term, robotics and telehealth could expand home-based rehabilitation options.

Competitive Rivalry (Moderate): The fragmented nature of the market (1,200+ facilities nationally with Encompass operating 172) creates opportunities for consolidation while limiting head-to-head competition in most markets.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Encompass benefits from spreading corporate overhead, IT systems, purchasing, and best practices across 172 hospitals. However, rehabilitation hospitals are relatively self-contained units, limiting scale economies compared to some industries.

Network Effects: Limited. Each hospital serves a local market, and patient volumes at one hospital don't meaningfully benefit others.

Counter-Positioning: Encompass's position as a pure-play inpatient rehabilitation operator creates some counter-positioning versus integrated health systems that operate rehabilitation units as part of broader operations. However, the counter-position is not particularly strong.

Switching Costs: Moderate. Referral relationships with acute-care hospitals and physicians create some stickiness, particularly for joint venture partners. However, patients can choose any provider, limiting switching costs at the consumer level.

Branding: Encompass Health is named America's Most Awarded Leader in Inpatient Rehabilitation by Newsweek and Statista and is ranked among Fortune's World's Most Admired Companies and Forbes' Most Trusted Companies in America. Brand matters more for employee recruitment and referral relationships than consumer choice.

Cornered Resource: The company's extensive real estate footprint, particularly in high-growth markets like Florida and Texas, represents a scarce resource that competitors cannot easily replicate.

Process Power: The company's clinical protocols, quality measurement systems, and operational playbooks represent meaningful process power developed over 40 years of operation. However, this is potentially replicable by well-resourced competitors.

What Investors Should Watch

Key Performance Indicators

Same-Store Discharge Growth: This metric isolates organic growth from new hospital openings, providing the clearest view of underlying demand and market share dynamics. Management targets 4-5% same-store discharge growth annually.

Revenue Per Discharge: Combines pricing power (reimbursement rates) and case mix (acuity of patients treated). Growth in this metric indicates either favorable reimbursement changes or a shift toward higher-acuity patients.

Adjusted EBITDA Margin: Measures operating efficiency. Labor costs represent the largest expense category, so margin trends signal the company's ability to manage staffing costs while maintaining quality.

Regulatory Monitoring

The Centers for Medicare and Medicaid Services (CMS) issues annual updates to inpatient rehabilitation facility reimbursement rates each August, effective October 1. These updates are the single most important external factor affecting company economics.

Additionally, changes to Medicare Advantage regulations, particularly around prior authorization and coverage requirements, can significantly impact patient access and payment timing.

Myth vs. Reality

Myth: The accounting fraud permanently damaged the company's competitive position. Reality: Twenty years of clean financial reporting, management turnover, and the rebrand have largely separated today's Encompass Health from the HealthSouth scandal. The company's market position is stronger than ever.

Myth: Demographic tailwinds guarantee growth. Reality: While the aging population provides structural support, growth is not automatic. Competition from health systems, Medicare Advantage penetration, and labor costs all create headwinds that require continuous operational excellence to overcome.

Myth: Medicare concentration makes the company too risky. Reality: The concentration is real and creates genuine risk. However, Medicare has proven to be a more stable payor than private insurance for rehabilitation services, and the political constituency of elderly voters makes significant cuts politically difficult.

Conclusion: The Anatomy of a Turnaround

The story of Encompass Health is, in many ways, a testament to the resilience of American capitalism. A company can be born from genuine innovation, corrupted by executive greed, nearly destroyed by scandal, and rebuilt through disciplined management into an industry leader.

Richard Scrushy saw a real opportunity in the healthcare system and built a company to capture it. That his methods ultimately included fraud doesn't negate the underlying insight—the demand for cost-effective rehabilitation services has only grown in the four decades since he founded Amcare in a Little Rock strip mall.

Jay Grinney inherited a company in ruins and restored it through methodical execution: fixing the books, settling with regulators, disposing of distractions, and focusing on the core business. His twelve-year tenure proved that corporate cultures can be transformed when leadership commits to integrity over expedience.

Mark Tarr has built on that foundation with steady expansion, completing the separation of home health through the Enhabit spin-off and focusing exclusively on facility-based rehabilitation. Under his leadership, the company has grown from 145 hospitals to 172, expanded into new markets, and delivered consistent double-digit revenue growth.

"Our value proposition and operating strategy continue to be validated and we remain highly optimistic about the long-term prospects of our business," CEO Mark Tarr stated in October 2025.

For investors, Encompass Health represents a company with clear competitive advantages, strong demographic tailwinds, and disciplined management—but also meaningful regulatory risk and capital intensity that moderate the upside. The company's history reminds us that even the most promising business models can be corrupted by executive misconduct, while its recovery demonstrates that fundamental business strength can survive even catastrophic governance failures.

The question is no longer whether Encompass Health survived the scandal—it clearly did. The question is whether it can continue to grow and generate returns for shareholders in a healthcare environment that grows more complex each year. The demographic trends favor the company. The regulatory environment remains supportive for now. And the management team has demonstrated consistent execution over nearly a decade.

The next chapter of this story remains unwritten. But for a company that once stood on the brink of bankruptcy, the current position—as the dominant player in a growing, essential healthcare service—represents something close to a corporate miracle.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube