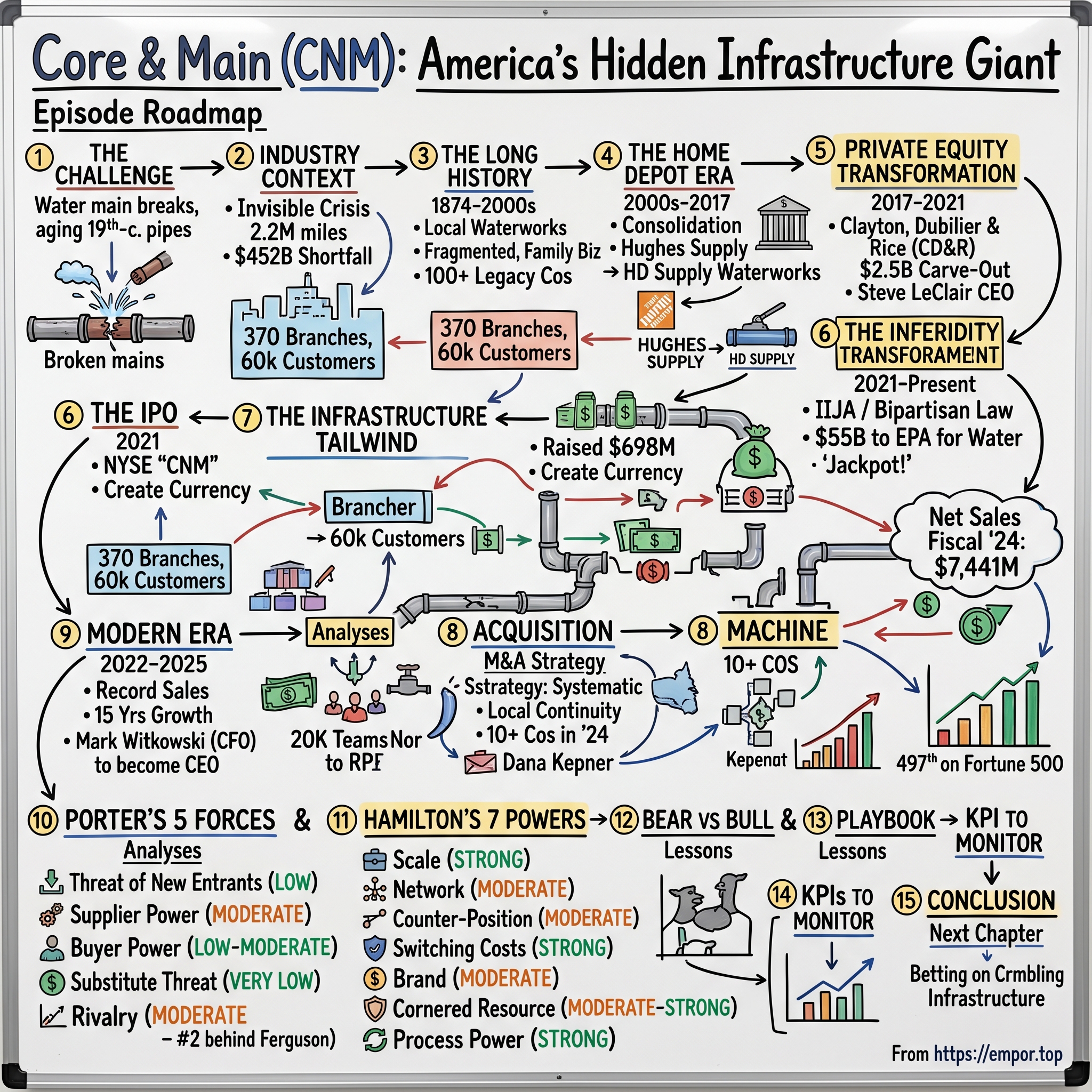

Core & Main: America's Hidden Infrastructure Giant

I. Introduction & Episode Roadmap

Every two minutes, somewhere in America, a water main breaks. In the quiet darkness beneath city streets and suburban cul-de-sacs, 2.2 million miles of pipes—many installed when Theodore Roosevelt was president—strain under the weight of age and neglect. This invisible crisis has created an unlikely Fortune 500 company that most Americans have never heard of: Core & Main.

The company has 370 branch locations in 49 U.S. states, 60,000 customers, and sells 225,000 products. Yet walk through any American city and you won't see a Core & Main billboard, storefront, or delivery truck emblazoned with consumer-friendly branding. That's because Core & Main operates in the unsexy, essential world of underground infrastructure—the pipes, valves, hydrants, and meters that make modern civilization possible.

Net sales for fiscal 2024 increased $739 million, or 11.0%, to $7,441 million compared with $6,702 million for fiscal 2023. To put that in perspective: this is a company generating nearly $7.5 billion in annual revenue from products you've probably never thought about unless your basement flooded or your street became a construction zone.

The company is ranked 497th on the Fortune 500. How did a carved-out division of a carved-out company become a Fortune 500 infrastructure powerhouse in less than a decade? The story involves a perfect storm of factors: shrewd private equity maneuvering, a once-in-a-generation infrastructure spending bill, and the inexorable truth that pipes don't last forever.

Core & Main is a leading specialized distributor of water, wastewater, storm drainage and fire protection products, and related services, built on the foundation of more than 100 legacy companies. These aren't products consumers buy at Home Depot. These are the critical components that municipalities, contractors, and water utilities need to keep communities functioning—products that become increasingly urgent as America's infrastructure continues to age.

The Core & Main story is a masterclass in private equity value creation, sector-specific expertise, and the power of being essential to something everyone takes for granted. It's also a bet on a simple premise: American water infrastructure is crumbling, billions of federal dollars are flowing toward repair and replacement, and somebody needs to supply the materials.

II. The Hidden World Beneath Your Feet: Industry Context

Picture this: You turn on your kitchen faucet to fill a glass of water. The journey that water takes—from treatment plant through miles of transmission mains, into your neighborhood's distribution pipes, and finally through your home's plumbing—involves infrastructure most people never see and rarely consider. Until it fails.

The nation's drinking water infrastructure comprises more than 2 million miles of underground pipes and are operated by nearly 150,000 public water systems. Drinking water infrastructure in the U.S. comprises more than 2 million miles of underground transmission and distribution lines. That's enough pipe to wrap around the Earth more than 80 times. And much of it is reaching the end of its useful life.

Some of the nation's oldest pipes were laid in the 19th century, and pipes laid post–World War II have an average lifespan of 75 to 100 years, meaning that many of even the newer pipe segments are reaching or have reached the end of their design life. As of 2023, the average life expectancy of these pipes is just over 78 years, which is 6 years less than in 2018.

This is the context that makes Core & Main's business so essential. Its products portfolio include pipes, valves, hydrants, fittings, and other products and services used for service, repair and replacement of underground water infrastructure; storm drainage products, such as corrugated HDPE and metal piping systems, retention basins, inline drains, manholes, grates, geosynthetics, erosion control, and other related products; fire protection products, including fire protection pipes, valves, fittings, sprinkler heads and other accessories, as well as fabrication and kitting services; smart meter products; and smart metering solutions.

The American Society of Civil Engineers 2021 Infrastructure Report Card graded U.S. infrastructure a C-, accounting for 17 categories. Drinking water infrastructure received a C-, which is an increase for the 2017 Infrastructure Report Card when the category received a D. Wastewater received a D+, the same grade it received four years ago. And for the first time ever Storm Water was included in the report card. It received a D.

The scale of neglect is staggering. Here, a break in the water pipework occurs every 2 minutes on average, losing 6 billion gallons of water every day. Each year, 2.1 trillion gallons of water are lost in the US due to breakdowns in the water infrastructure.

Notably, the report shows that 20% or 452,000 miles of water pipes in the US and Canada are beyond their useful lives and need to be replaced but have not been due to lack of funds. This represents a $452 billion shortfall.

So who buys all these pipes and valves? In fiscal 2024, 67% of the company's sales were pipes, valves, and piping and plumbing fittings, 16% of the company's sales were products for storm drainage, 8% of the company's sales were products for fire protection, and 9% of the company's sales were products for water metering. In fiscal 2024, 42% of sales were from the municipal construction sector, 38% of sales were from the non-residential construction sector, and 20% of sales were from the residential construction sector.

This diversified revenue mix is crucial. Municipal customers—cities, counties, water authorities—provide steady, less cyclical demand driven by maintenance needs rather than construction cycles. When a water main breaks in February, it doesn't matter whether the housing market is booming or busting; the pipe needs to be replaced.

Understanding this industry context is essential for investors: Core & Main doesn't compete with Amazon or Home Depot. It operates in a specialized distribution niche where technical knowledge, local relationships, and product availability matter more than price. A contractor installing a water main can't wait three days for shipping; they need the right 8-inch ductile iron pipe at the local branch tomorrow morning.

III. The Long History: 150 Years of Local Waterworks Companies (1874–2000s)

Core & Main, Inc. was founded in 1874 and is headquartered in Saint Louis, Missouri. That founding date places the company's earliest roots in the Reconstruction Era, when American cities were rapidly industrializing and discovering the urgent need for municipal water systems.

But that founding date is somewhat misleading. Founded in its current form in 2017, the firm is built on numerous legacy companies that have operated for many years in related areas. The 1874 date reflects the oldest constituent company that eventually became part of the Core & Main family—a lineage spanning 150 years of family-owned waterworks distributors across America.

The nature of waterworks distribution has always been intensely local. Consider what it meant to be a waterworks distributor in 1920: You needed to know every plumber, every city engineer, every water department superintendent in your territory. You needed inventory on hand because pipes couldn't be ordered and shipped quickly. You needed technical expertise to specify the right products for local soil conditions, water chemistry, and building codes. These relationships took decades to build and were virtually impossible to replicate.

This explains why the industry remained fragmented for so long. Unlike consumer goods distribution, where scale economics could overwhelm local players, waterworks distribution rewarded local expertise and relationships. A family business in Denver might serve the Front Range for three generations, knowing every quirk of Colorado's high-altitude water systems and the preferences of every major contractor.

Post-Civil War urbanization created explosive demand for water infrastructure. Cities like New York, Chicago, and Philadelphia built massive water systems in the late 1800s, creating a new industry of suppliers and distributors. By 1900, hundreds of small regional distributors had sprung up across the country, each serving a specific geographic area with deep local knowledge.

The industry structure that emerged was remarkably stable. The typical waterworks distributor profile: family-owned, multi-generational, with deep customer relationships built over decades. These companies might generate $10 million to $50 million in annual revenue, serving a regional market of a few counties or a single metropolitan area. They competed primarily on service, availability, and relationships rather than price.

This fragmentation persisted well into the 21st century. Even today, after significant consolidation, the waterworks distribution market remains highly fragmented. Core & Main is a leading specialized distributor of water, wastewater, storm drainage and fire protection products, and related services, built on the foundation of more than 100 legacy companies.

Those 100+ legacy companies represent generations of entrepreneurship, each with its own story of serving local communities. When Core & Main acquires a regional distributor today, they're not just buying inventory and customer lists—they're buying relationships that may stretch back decades, with salespeople who've known their customers' fathers and grandfathers.

Understanding this history illuminates Core & Main's current strategy: they're essentially industrializing what was once a cottage industry, bringing national scale and resources to bear while preserving the local relationships and expertise that make the business work.

IV. The Home Depot Era & HD Supply Formation (2000s–2017)

The waterworks distribution industry's consolidation began in earnest during the housing boom of the early 2000s. Home Depot, at the peak of its growth ambitions, decided to expand beyond its consumer retail stores into professional supply.

In 2005, Home Depot acquired National Waterworks Holdings. It was merged with Hughes Supply and became HD Supply Waterworks. In August 2017, Clayton, Dubilier & Rice acquired HD Supply Waterworks and changed its name to Core & Main.

Home Depot's acquisition spree was aggressive. The company believed it could apply its retail expertise and purchasing power to professional markets, creating a full-service supplier for contractors and municipalities. National Waterworks became part of this vision—a platform to consolidate the fragmented waterworks distribution industry.

The company was founded in 2007 as a division of HD Supply and became an independent company in 2017. Before becoming Core & Main, the company was known as HD Supply Waterworks. In 2013, HD Supply Waterworks acquired National Waterworks, a leading distributor of waterworks products. This acquisition helped HD Supply Waterworks become one of the largest distributors of waterworks products in the United States.

The National Waterworks acquisition in 2013 was a key inflection point. It transformed HD Supply Waterworks from a regional player into a true national platform. The combined entity had enough scale to negotiate better supplier terms, invest in technology, and pursue further acquisitions—a virtuous cycle that would accelerate under private equity ownership.

But Home Depot's professional supply strategy ultimately stumbled. The 2008 financial crisis devastated housing-related businesses, and Home Depot found itself overextended. The company began divesting non-core assets to focus on its retail business.

In 2016, HD Supply announced that it would spin off its Waterworks division, along with its Power Solutions division, to create a new independent company. The company was named Core & Main, Inc. and began operating as an independent company in 2017.

The sale followed HD Supply's pattern of shedding divisions. Interior Solutions was sold in 2016, Power Solutions in 2015. Waterworks was next on the block—a decision that would prove fortunate for whoever acquired it.

Clayton, Dubilier & Rice ("CD&R") today announced an agreement with HD Supply Holdings, Inc. (NASDAQ:HDS) to acquire its Waterworks business unit ("Waterworks"), the nation's largest distributor of water, sewer, storm and fire protection products, for $2.5 billion. Through a carve-out transaction, Waterworks will become an independent company, wholly-owned by CD&R funds. Waterworks is a leading U.S. distributor of industrial and construction products used to build and maintain underground water, wastewater and drainage infrastructure networks. The company operates a national network of 244 branches in 46 states with a sales team of more than 1,700 sales representatives serving a diverse customer base of more than 37,000 municipalities, private water companies and professional contractors.

At $2.5 billion, CD&R was paying roughly 7.5x EBITDA—a reasonable multiple for a stable distribution business with market leadership, but one that would require significant operational improvement and growth to generate strong returns.

The HD Supply era had accomplished something important: it had professionalized what was once a collection of family businesses, implementing standardized systems, ERP software, and centralized purchasing. But it had also constrained the business, limiting investment and strategic autonomy. Under private equity ownership, those constraints would disappear.

V. The CD&R Transformation: Private Equity Creates a Platform (2017–2021)

On August 1, 2017, the waterworks division of HD Supply became an independent company. Following its Aug. 1 completed $2.5 billion acquisition by private investment firm Clayton, Dubilier & Rice, HD Supply Waterworks is now its own standalone company, complete with a new name: Core & Main.

This was not Clayton, Dubilier & Rice's first encounter with the business. Mr. Berges was Chairman of HD Supply from 2007 to 2015. CD&R invested in HD Supply in 2007 and exited the investment in 2014. The private equity firm knew this business intimately—its strengths, its potential, and its constraints under corporate ownership.

Through our prior investment in HD Supply, we have a great appreciation for the strength and quality of the Waterworks business and the exceptionally talented Waterworks management team.

The reunion was intentional. "This transaction is an important milestone in the strategic growth of Waterworks," said LeClair. "The Waterworks team is very excited to reunite with CD&R to accelerate our growth and productivity initiatives."

Clayton, Dubilier & Rice is widely regarded as a pioneer of the operating partner model in private equity. Operations have been at the core of CD&R's business since its founding in 1978, at a time when most buyout firms focused mainly on financial engineering.

The management team brought continuity and experience. LeClair served as the Chief Executive Officer (CEO) for Core & Main from the time it became an independent company in August 2017 through March 2025. LeClair led the company through its separation from HD Supply in 2017 and through a successful IPO in 2021.

Steve LeClair's background was ideally suited for the challenge. Prior to that, he served as president of HD Supply Waterworks and president of HD Supply Lumber and Building Materials until its divestiture to ProBuild Holdings in 2008. LeClair joined HD Supply in 2005 as senior director of operations. Prior to that, he was senior vice president of General Electric (GE) Equipment Services. He held progressively responsible roles at GE Appliances and Power Generation in distribution, manufacturing and sales.

The GE pedigree mattered. GE's operational excellence culture, with its focus on metrics, continuous improvement, and leadership development, would shape Core & Main's approach to building a national platform.

Even the company's name reflected the PE transformation. When we formed our company, we went to our best resource, our associates, to find a name for our organization. Associate Quinton Carter's submission spoke to our DNA. As he explains it, "Core comes from our core values, and main not just for main water lines, but for being the main supplier - people want to come to us rather than our competitors."

"The name Core & Main allows us to continue our incredible journey as a leading distributor in the water infrastructure and fire protection industries as well as adjacent markets," Core & Main CEO Steve LeClair stated in a press release. "As an independent company, Core & Main has an exciting opportunity to accelerate our growth."

The CD&R playbook became clear: accelerate M&A, invest in organic growth initiatives, and build the platform to capitalize on infrastructure spending trends. The former HD Supply Waterworks Business announced the completion of its 11th acquisition since being formed in 2017 as an independent, private equity-backed distributor. The acquisition marks Core & Main's 11th transaction since becoming an independent company in August 2017.

By the time of the IPO filing, the transformation was evident. Core & Main had built a dedicated M&A team, expanded into adjacent product categories like smart meters, opened new greenfield locations, and invested in technology infrastructure. The company was no longer just maintaining its market position—it was actively consolidating the industry.

VI. The IPO & Public Market Debut (2021)

July 2021 was a remarkable month for IPOs. The market was frothy, valuations were elevated, and investor appetite for new issues seemed insatiable. Into this environment stepped Core & Main.

The shares are expected to begin trading on the New York Stock Exchange on July 23, 2021, under the ticker symbol "CNM."

Core & Main, Inc. ("Core & Main" or the "Company") (NYSE: CNM), a portfolio company of Clayton, Dubilier & Rice, LLC ("CD&R"), recently completed an initial public offering of 34,883,721 Class A common stock at a price of $20.00 per share. The offering generated gross proceeds of $697.7 million.

The Company will use the net proceeds from the initial public offering to repay certain indebtedness and for general corporate purposes. The primary use of proceeds—debt repayment—reflected Core & Main's leveraged balance sheet, a legacy of the private equity acquisition.

After the IPO is completed, CD&R is to control about 79.6 percent of the company. The IPO was primarily about creating public currency, establishing a market valuation, and providing partial liquidity—not a full exit. CD&R remained firmly in control.

We are one of only two national distributors operating across large and highly fragmented markets, which we estimate to represent approximately $27 billion in annual spend. Through our network of approximately 285 branch locations in 47 states and approximately 170 metropolitan statistical areas ("MSAs") across the U.S., we serve as a critical link between over 4,500 suppliers and a diverse and long-standing base of over 60,000 customers.

The positioning was compelling: duopoly market structure, essential products, fragmented customer base, aging infrastructure driving demand. These were the elements of a defensible business model.

There were 1,035 IPOs on the US stock market in 2021, an all-time record. In that crowded field, Core & Main stood out as one of the more successful offerings—a company with real revenue, real earnings, and a clear path to continued growth.

During my tenure, we transformed Core & Main from a division of HD Supply into a private equity-sponsored standalone business in 2017. We launched our initial public offering in 2021, one of the largest and most successful from that year.

The timing proved prescient. Just months after the IPO, President Biden would sign the Infrastructure Investment and Jobs Act, creating an unprecedented tailwind for Core & Main's business. The IPO had positioned the company to capitalize on the biggest infrastructure spending package in American history—with public currency to fund acquisitions and a clear valuation for management incentives.

VII. The Infrastructure Tailwind: IIJA & The Biggest Catalyst (2021–Present)

On November 15, 2021—less than four months after Core & Main's IPO—President Biden signed the Infrastructure Investment and Jobs Act into law. For a company built around water infrastructure, this was the equivalent of hitting the jackpot.

The Infrastructure Investment and Jobs Act (IIJA), also referred to as the Bipartisan Infrastructure Law (BIL), was signed into law on November 15, 2021. The $1.2 trillion IIJA reauthorizes the nation's surface transportation, drinking water, and wastewater legislation.

The Infrastructure Investment and Jobs Act (IIJA), enacted on November 15, 2021, appropriates $55B to the U.S. Environmental Protection Agency (EPA) to improve drinking water and wastewater infrastructure. According to the EPA, this investment represents the single largest federal investment in water in the nation's history.

To understand the magnitude, consider historical context. The level of DWSRF appropriations average $6.14 billion per fiscal year, nearly six times the level of recent DWSRF annual appropriations. Federal funding for drinking water was set to increase six-fold from historical norms.

The Infrastructure Investment and Jobs Act of 2021 (IIJA) provides for significant federal investments in transportation, broadband, water, and other types of infrastructure. Specifically, the IIJA delivers more than $50 billion to the Environmental Protection Agency (EPA) for water infrastructure investments to improve our nation's drinking water, wastewater, and stormwater infrastructure - the single largest investment in water that the federal government has ever made.

The timing created an extended runway for Core & Main. In many programs, the increased funding will flow to states, tribes, and communities over five years, beginning in 2022.

But translating federal appropriations into actual product demand takes time. Money must flow through state revolving funds, municipalities must bid projects, contractors must be hired, and materials must be ordered. By the law's second anniversary in November 2023, around $400 billion from the law, about a third of all IIJA funding, was allocated to more than 40,000 projects related to infrastructure, transport, and sustainability. By May 2024, the law's halfway mark, the numbers had increased to $454 billion (38 percent of the Act's funds) for more than 56,000 projects.

Can you provide insights into the municipal and non-residential end markets, particularly with the Infrastructure Investment and Jobs Act (IIJA) funds? Stephen LeClair, CEO: We observed stable and modest growth in the municipal sector, with increased bidding activity and backlog. IIJA funds are starting to flow, leading to project execution expected in 2025.

The IIJA is not just a one-time stimulus—it represents a structural change in federal water infrastructure investment. Chief among them is the Infrastructure Investment and Jobs Act, which was signed into law in November 2021 and authorizes $1.2 trillion for infrastructure spending between 2022 and 2026. With authorization expiring next year, Congress must decide how programs under the legislation will be funded going forward.

For investors, the IIJA thesis is compelling but requires patience. Federal infrastructure spending doesn't spike and crash like consumer demand—it builds gradually as projects move through bureaucratic pipelines, then provides sustained demand over construction periods that can span years. Core & Main is positioned to capture this demand across its national branch network.

VIII. The Acquisition Machine: M&A as a Core Strategy

If there's one capability that defines Core & Main's strategy, it's M&A execution. The company has turned acquisition into a systematic, repeatable process—a genuine competitive advantage in a fragmented industry.

We also welcomed 10 complementary businesses to the Corn Maine family, adding over 600,000,000 of annual sales while expanding our presence in key geographies, gaining access to new product lines and adding key talent. In terms of organic sales growth, we believe we outgrew the market by a couple hundred basis points in 2024.

The most significant recent acquisition demonstrates the scale Core & Main has achieved. Core & Main Inc. (NYSE: CNM), a leader in advancing reliable infrastructure with local service, nationwide, has closed its previously announced acquisition of Dana Kepner Company LLC, and associated entities. Dana Kepner is a distributor of water, wastewater, storm drainage and geotextile products, along with specialty tools and accessories which has locations operating in Arizona, Colorado, Connecticut, Massachusetts, Nevada, Rhode Island, Texas and Wyoming.

Founded in 1933 and based in Denver, Colorado, Dana Kepner has 19 locations across the U.S., operating in Arizona, Colorado, Connecticut, Massachusetts, Nevada, Rhode Island, Texas and Wyoming. The team offers a variety of waterworks products, including pipes, valves and fittings, as well as meters and meter accessories.

The Dana Kepner deal illustrates Core & Main's acquisition criteria: well-run regional businesses with strong local relationships, complementary geographic footprint, and cultural alignment with Core & Main's values. These aren't distressed acquisitions or turnaround situations—they're consolidation plays where scale creates value.

"The team at Dana Kepner recognizes the importance of providing local expertise to its customers in the waterworks industry. Like the Core & Main team, they add value by serving as knowledgeable and trusted advisors to municipalities and contractors," said Steve LeClair, chief executive officer of Core & Main. "We are excited about this opportunity to extend our geographic reach, expand the range of products and services that we offer, and add key talent into our organization."

The integration approach is central to Core & Main's M&A success. Unlike some roll-up strategies that strip out costs and rationalize operations immediately, Core & Main emphasizes cultural fit and local continuity. The acquired company's salespeople keep their relationships; the branch retains its local identity. What changes is back-office support, purchasing scale, and access to Core & Main's broader product portfolio.

Closed five acquisitions during and after the quarter: Eastern Supply, Dana Kepner, ACF West, EGW Utilities and Geothermal Supply Company. "With an addressable market totaling $39 billion across highly fragmented markets, we are actively managing a strong pipeline of M&A opportunities. Year-to-date, we have closed five acquisitions that offer expansion into new geographies, access to new product lines and the addition of key talent."

The math behind roll-up strategies in fragmented industries is straightforward: acquire companies at lower multiples than your own trading multiple, integrate them efficiently, and capture the valuation arbitrage. Core & Main's scale advantages—better purchasing terms, shared technology platforms, management expertise—allow acquired companies to perform better under the Core & Main umbrella than they could independently.

IX. Modern Era: Execution & Results (2022–2025)

The years since the IPO have tested Core & Main's resilience. Supply chain disruptions, inflation, interest rate increases, and economic uncertainty have challenged distribution businesses broadly. Core & Main's performance through this period reveals the quality of its business model.

We are pleased to achieve another record sales year for Core & Main, marking our fifteenth consecutive year of growth. The long term underlying trends of our end markets are strong and our products and services play a critical role in advancing reliable infrastructure. Fiscal twenty twenty four was a notable year for Core and Main and it marked our fifteenth consecutive year of positive sales growth. Our teams navigated a dynamic environment to deliver strong financial performance, including record net sales of over $7,400,000,000 adjusted EBITDA of $930,000,000 and operating cash flow of more than $620,000,000

Fifteen consecutive years of sales growth is remarkable for any company—it means the business has grown through the 2008 financial crisis, COVID-19 pandemic, and multiple economic cycles. This consistency reflects the essential nature of water infrastructure demand and Core & Main's execution capability.

The company has 370 branch locations in 49 U.S. states, 60,000 customers, and sells 225,000 products. Scale has increased significantly since the IPO: branch count has grown from 285 to over 370, and product SKUs have expanded dramatically.

Operating more than 370 branches nationwide, we combine local expertise with a national supply chain to provide contractors and municipalities innovative solutions for new construction and aging infrastructure. Core & Main's 5,700 associates are committed to helping their communities thrive with safe and sustainable infrastructure.

Private label is emerging as a meaningful margin lever. We continue to develop a scalable assortment of private label brands and products used in water, wastewater, geosynthetics and fire protection applications. We added over 30,000 square feet of distribution space and more than 1,000 private label SKUs to our offerings since the end of last year. We ended fiscal twenty twenty four with private label products representing approximately 4% of our sales with an opportunity for it to grow to 10% of our sales or more over time.

The leadership transition announced in 2025 reflects the company's maturation. After nearly two decades leading Core & Main, CEO Steve LeClair will transition to executive chair, advising the company and continuing to lead the board. Mark Witkowski, Core & Main's current CFO, will succeed LeClair as CEO and will also join the board. Roby Bradbury, senior VP of finance and investor relations, will take over Witkowski's role as CFO. All changes will take effect on March 31. Witkowski joined Core & Main in 2007, taking on roles of increasing responsibility before becoming CFO in 2016. The company said he played a key role in developing and executing its value creation strategies.

The internal succession—promoting the CFO to CEO rather than an external search—demonstrates the depth of management talent Core & Main has built. It also signals confidence in the existing strategy and execution approach.

X. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

Building a waterworks distribution business from scratch would be extraordinarily difficult. Core & Main is a leading specialized distributor of water, wastewater, storm drainage and fire protection products, and related services, built on the foundation of more than 100 legacy companies.

Those 100+ legacy companies represent decades of accumulated relationships, technical expertise, and geographic coverage. A new entrant would need to: - Establish supplier relationships with thousands of manufacturers - Build technical expertise across hundreds of product categories - Hire salespeople with decades of local relationships - Invest in branch infrastructure across 49 states - Compete for acquisitions against better-capitalized incumbents

The capital requirements alone would be enormous, but the real barrier is time. Municipal purchasing relationships are built over decades, not quarters.

2. Bargaining Power of Suppliers: MODERATE

Through our network of approximately 285 branch locations in 47 states and approximately 170 metropolitan statistical areas ("MSAs") across the U.S., we serve as a critical link between over 4,500 suppliers and a diverse and long-standing base of over 60,000 customers.

With 4,500+ suppliers, Core & Main has significant diversification—no single supplier can hold the company hostage. The company's scale provides purchasing leverage, and the growing private label program further reduces supplier dependency.

However, some specialized products (certain valve types, specialty fittings) have limited manufacturers, giving those suppliers more pricing power.

3. Bargaining Power of Buyers: LOW-MODERATE

Customers include municipalities, private water companies, and professional contractors. With 60,000 customers, no single buyer represents significant concentration risk.

More importantly, water infrastructure is critical. Municipalities prioritize reliability and service over pure price—they need products available when a water main breaks, not the cheapest option shipped next week. This creates natural switching costs.

4. Threat of Substitutes: VERY LOW

There is no substitute for underground pipes, valves, and hydrants. Unlike many industries facing digital disruption, water infrastructure cannot be "disrupted" by software or alternative technologies. The products are mandated by building codes, municipal regulations, and physical necessity.

Smart meters and monitoring technology represent evolution within the industry, not disruption—and Core & Main is actively expanding in these categories.

5. Competitive Rivalry: MODERATE

Waterworks: 21% share in a $28,000,000,000 market. Number 1 market position. Ferguson holds the #1 position in waterworks distribution with 21% market share.

Competition: While Core & Main is a market leader, it faces competition from other large players such as Ferguson plc (NYSE:FERG) and numerous smaller regional distributors.

The industry effectively has two national competitors (Ferguson and Core & Main) plus hundreds of regional players. Competition is primarily on service, availability, and relationships rather than price—healthy dynamics for incumbent margins.

XI. Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

Operating more than 370 branches nationwide, we combine local expertise with a national supply chain to provide contractors and municipalities innovative solutions for new construction and aging infrastructure.

Core & Main's scale creates advantages across purchasing, technology, management expertise, and capital access. A regional distributor cannot negotiate the same supplier terms, invest in the same systems, or attract the same management talent.

2. Network Effects: MODERATE

Not a traditional network effect business, but each branch added increases the value of the network for national contractors who want consistent service across projects. More product availability in one branch makes the entire network more valuable to customers.

3. Counter-Positioning: MODERATE

Core & Main's combination of national scale with local service would be difficult for traditional local distributors to replicate—they lack the capital and expertise. Large diversified distributors (think Grainger or Wesco) could enter but would lack the specialized waterworks expertise that customers require.

4. Switching Costs: STRONG

Deep integration with municipal purchasing systems, long-term sales relationships, technical support dependencies, and project history create meaningful switching costs. When a contractor has worked with the same Core & Main branch for 15 years, switching suppliers involves real risk and friction.

5. Branding: MODERATE

B2B brand rather than consumer-facing, but reputation matters significantly in municipal and contractor relationships. "The team at Dana Kepner recognizes the importance of providing local expertise to its customers in the waterworks industry. Like the Core & Main team, they add value by serving as knowledgeable and trusted advisors to municipalities and contractors."

6. Cornered Resource: MODERATE-STRONG

Core & Main's 5,700 associates are committed to helping their communities thrive with safe and sustainable infrastructure.

The true "cornered resource" is human capital—the salespeople and technical experts with decades of local relationships and product knowledge. This expertise cannot be hired or acquired quickly.

7. Process Power: STRONG

M&A integration is Core & Main's most distinctive process power. The company has refined its acquisition playbook across 100+ deals, developing institutional knowledge around target identification, due diligence, integration, and culture preservation that would take competitors years to replicate.

XII. Bear vs. Bull Case

Bull Case:

The bull case for Core & Main rests on several structural advantages:

The Infrastructure Investment and Jobs Act (IIJA), enacted on November 15, 2021, appropriates $55B to the U.S. Environmental Protection Agency (EPA) to improve drinking water and wastewater infrastructure. According to the EPA, this investment represents the single largest federal investment in water in the nation's history.

Beyond IIJA, aging infrastructure creates decades of replacement demand. Some of the nation's oldest pipes were laid in the 19th century, and pipes laid post–World War II have an average lifespan of 75 to 100 years, meaning that many of even the newer pipe segments are reaching or have reached the end of their design life.

We are pleased to achieve another record sales year for Core & Main, marking our fifteenth consecutive year of growth. Fiscal twenty twenty four was a notable year for Core and Main and it marked our fifteenth consecutive year of positive sales growth.

The company has demonstrated it can grow in any environment—recession, pandemic, supply chain crisis. Essential products plus dominant market position equals resilience.

"With an addressable market totaling $39 billion across highly fragmented markets, we are actively managing a strong pipeline of M&A opportunities." The acquisition runway remains long, with significant consolidation potential.

Private label expansion from 4% to potentially 10% of sales represents material margin upside without revenue growth.

Bear Case:

Persistent deflationary pressures could pose significant challenges for Core & Main's financial performance. In a deflationary environment, the company may struggle to maintain its pricing power, potentially leading to compressed margins. This could impact profitability and make it more difficult for Core & Main to achieve its long-term financial targets.

Municipal budgets can be constrained during recessions, delaying infrastructure projects. While maintenance is essential, new construction and expansion can be deferred.

Competition: While Core & Main is a market leader, it faces competition from other large players such as Ferguson plc (NYSE:FERG) and numerous smaller regional distributors. Ferguson has deeper resources and a broader product portfolio—competitive intensity could increase.

Interest rate sensitivity matters: The decrease in net income was primarily attributable to an increase in interest expense, related to increased borrowings to support acquisitions in fiscal 2024.

Political risk around federal infrastructure funding remains a consideration, particularly as IIJA authorization expires and Congress considers future appropriations.

XIII. Playbook: Business & Investing Lessons

The Power of Boring Businesses

Core & Main exemplifies a category of business that rarely makes headlines but creates durable value: essential infrastructure serving non-discretionary demand. Pipes, valves, and hydrants will never be glamorous, but they will always be necessary. For investors seeking businesses that compound over decades, "boring" can be beautiful.

Private Equity Value Creation Through Operational Excellence

Clayton, Dubilier & Rice is widely regarded as a pioneer of the operating partner model in private equity. Operations have been at the core of CD&R's business since its founding in 1978, at a time when most buyout firms focused mainly on financial engineering.

CD&R's transformation of Core & Main demonstrates how operational expertise—not just financial engineering—can unlock value in mature industries. The playbook: take a well-run division constrained by corporate ownership, liberate it with capital and strategic focus, accelerate organic initiatives and M&A, then take it public.

Industry Consolidation as Competitive Advantage

In fragmented industries with high customer switching costs, the acquirer with the best integration playbook wins. Core & Main's ability to acquire regional distributors, preserve their relationships, and improve their economics through scale creates a compounding advantage that widens over time.

The Importance of Management Continuity

Core & Main's CEO, CFO, and company presidents have worked together since HD Supply and made dozens of acquisitions. Long-tenured management teams with institutional knowledge outperform revolving doors of hired guns. The internal succession to Mark Witkowski reflects this philosophy.

XIV. Key Performance Indicators to Monitor

For long-term investors tracking Core & Main, three KPIs matter most:

1. Average Daily Sales Growth (Organic)

Core & Main reports both total sales growth (including acquisitions) and organic average daily sales growth. The organic number reveals whether the company is gaining market share and successfully implementing its growth initiatives (smart meters, storm drainage, private label). Target: low-to-mid single digits organic growth indicates healthy market position; double-digit organic growth would suggest accelerating share gains.

2. Adjusted EBITDA Margin

Adjusted EBITDA for fiscal 2024 increased $20 million, or 2.2%, to $930 million compared with $910 million for fiscal 2023.

EBITDA margin reveals whether scale advantages are translating to profitability. Key drivers include private label penetration (from 4% toward 10%), price optimization initiatives, and SG&A leverage as acquisitions are integrated. Watch for margin expansion over time as the benefits of scale compound.

3. Net Debt / Adjusted EBITDA

Core & Main's leveraged balance sheet creates both opportunity (capacity for acquisitions) and risk (interest expense sensitivity). The company targets deleveraging over time while maintaining capacity for opportunistic M&A. Monitor this ratio to assess financial flexibility and risk profile.

XV. Conclusion: The Next Chapter

Core & Main's journey from HD Supply division to Fortune 500 company illustrates several enduring business truths: essential products create durable businesses; local relationships and technical expertise matter in distribution; private equity can unlock value through operational focus; and timing matters—going public just before the largest infrastructure bill in American history wasn't luck, but it certainly helped.

"Leading Core & Main for the last decade has been the privilege of a lifetime and I am incredibly proud of what we have accomplished together," said Steve LeClair. "During my tenure, we transformed Core & Main from a division of HD Supply into a private equity-sponsored standalone business in 2017. We launched our initial public offering in 2021, one of the largest and most successful from that year, and we have delivered outstanding performance and significant value creation year-after-year since then. As proud as I am of the results we have generated, I am even more proud of the culture we have built, the great leadership talent and depth we have, and the opportunities we have charted for the future."

The company LeClair built now passes to new leadership. After nearly two decades with Core & Main, Steve LeClair, the Company's current chief executive officer, will transition to the role of executive chair, where he will act as an advisor to the business, while continuing to lead the board of directors of Core & Main as chair. Mark Witkowski, the Company's current chief financial officer, has been selected by the board of directors to succeed Steve LeClair as chief executive officer.

The internal succession signals continuity. The strategic priorities—organic growth in smart meters and storm drainage, M&A consolidation, private label expansion, margin improvement—remain unchanged. The infrastructure tailwinds continue blowing.

For long-term investors, Core & Main represents a bet on two simple propositions: American water infrastructure will need to be repaired and replaced for decades to come, and somebody needs to supply the materials. Core & Main has positioned itself—through scale, relationships, and execution—to be that somebody.

The company beneath our feet may be hidden, but its importance isn't. Every time you turn on a faucet, flush a toilet, or watch firefighters connect to a hydrant, Core & Main's products are at work. That's about as essential as a business can get.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube