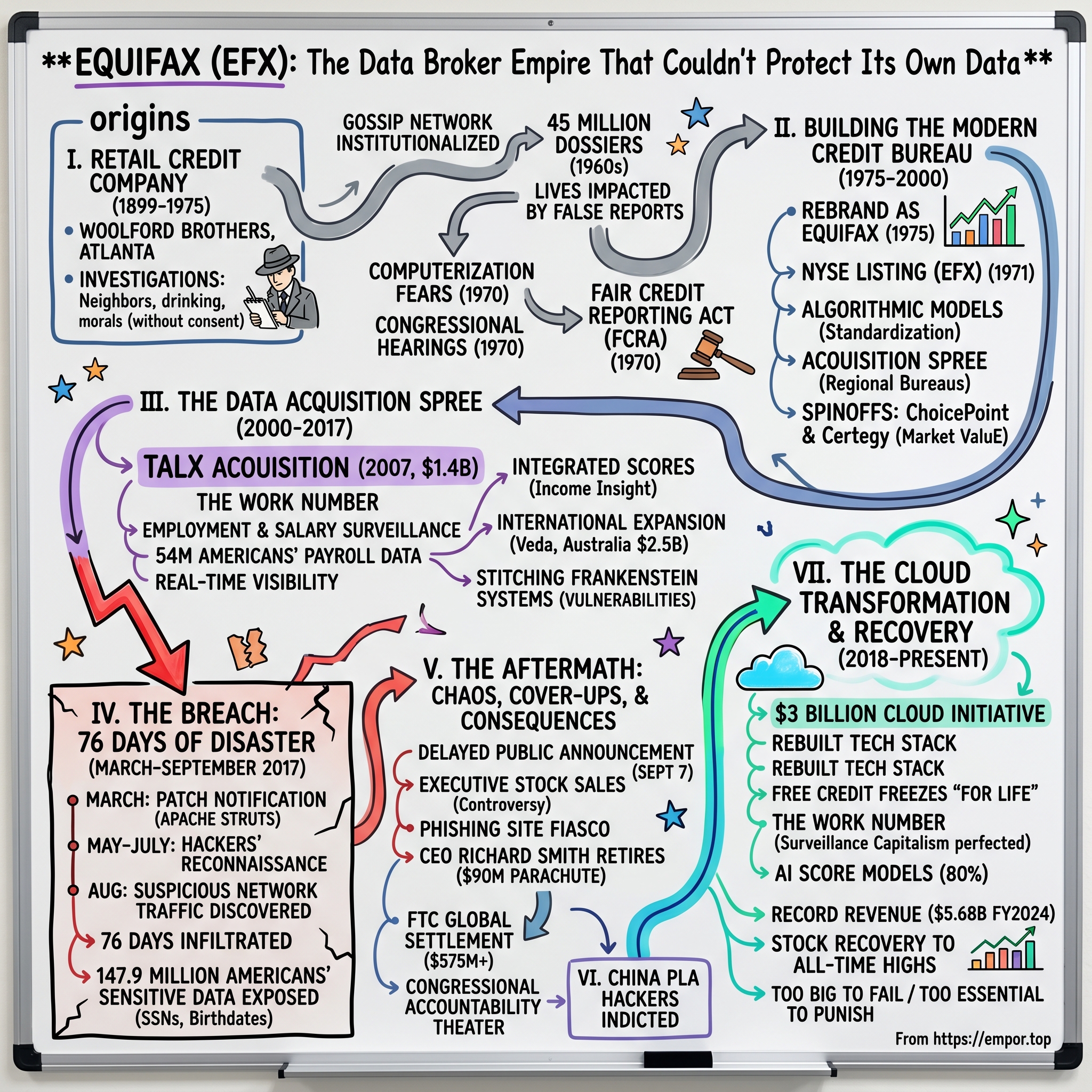

Equifax: The Data Broker Empire That Couldn't Protect Its Own Data

I. Introduction & Episode Roadmap

Picture this: It's September 7, 2017. You're scrolling through your phone when a breaking news alert stops you cold. Equifax—the company that knows your Social Security number, your credit card history, every loan you've ever applied for—has been breached. Not just breached, but hemorrhaging data for 76 days straight while executives sold stock. 147.9 million Americans' most sensitive information is now in the hands of hackers. The company whose entire business model is built on trust and data security has just become the poster child for corporate negligence.

But here's what makes this story truly fascinating: Equifax didn't just survive this catastrophe—it thrived. Today, the company generates nearly $5 billion in annual revenue, its stock trades higher than pre-breach levels, and it continues to collect data on 800+ million consumers worldwide. How does a company suffer one of history's worst data breaches and emerge stronger? That's the paradox we're unpacking today. Founded as Retail Credit Company in 1899, Equifax has evolved from a regional credit-checking service into one of the Big Three credit bureaus—alongside Experian and TransUnion—that form the invisible infrastructure of modern capitalism. The company generated $5.68 billion in revenue for fiscal year 2024, with operations spanning 24 countries and a workforce of approximately 14,000 employees.

What we're exploring today isn't just a cybersecurity cautionary tale. It's the story of how surveillance capitalism created entities so essential to the financial system that they're essentially too big to fail—even when they fail spectacularly. It's about how a company can violate the trust of nearly half the American population and emerge with record profits. And perhaps most intriguingly, it's about the peculiar economics of data monopolies where the product isn't sold to consumers but rather about them.

We'll trace Equifax's journey from its gossip-peddling origins through its transformation into a data empire, examine the systemic failures that led to the breach, and analyze why this company—despite everything—continues to thrive. Along the way, we'll uncover the TALX acquisition that quietly built one of America's most comprehensive employment surveillance systems, explore the company's audacious $3 billion cloud transformation, and examine what this all means for privacy, security, and capitalism in the digital age.

The themes we'll explore cut to the heart of modern economic life: How did we create companies that know everything about us but owe us nothing? What happens when critical infrastructure is run by for-profit entities with misaligned incentives? And in an age where data is the new oil, who really owns the wells?

II. The Retail Credit Company Origins (1899-1975)

The year is 1899. Atlanta is rebuilding from the ashes of the Civil War, transforming into the commercial hub of the New South. Two brothers, Cator and Guy Woolford, spot an opportunity that would reshape American capitalism: What if merchants could know, before extending credit, whether a customer would actually pay them back?

Their solution was elegantly simple and profoundly invasive. The Woolford brothers created the Retail Credit Company, essentially institutionalizing the local grocer's gossip network. They hired investigators—often housewives and retired men who knew their communities intimately—to compile detailed reports on their neighbors. These weren't just financial records. The investigators documented drinking habits, sexual preferences, political affiliations, cleanliness of homes, and the character of associates. They were paid by the report, with bonuses for "derogatory" information.

By 1920, the company had spread like kudzu across North America, with offices from Montreal to Mexico City. The business model was brilliant in its perversity: They collected information on citizens without consent, packaged it as a product, and sold it to insurance companies and employers who made life-altering decisions based on these reports. The subjects of these reports had no idea they existed, no right to see them, and no ability to correct errors.

The scale was staggering. By the 1960s, Retail Credit Company maintained files on 45 million Americans—roughly one in four citizens. They processed 35 million reports annually, making them one of the nation's largest credit bureaus. Their investigators, now numbering in the thousands, operated with the zeal of intelligence agents. Training manuals from the era reveal instructions to check medicine cabinets during home visits, interview neighbors about "moral character," and document any "peculiar" lifestyle choices.

The company's approach to LGBTQ individuals was particularly vicious. Internal documents later revealed that investigators were instructed to flag any signs of "homosexual tendencies," which could result in denial of employment, insurance, or housing. African Americans faced systematic discrimination, with reports often including coded language about "neighborhood character" that perpetuated redlining and economic exclusion.

But it was the computer that would prove to be Retail Credit's undoing—or rather, its salvation through transformation. In 1970, the company announced plans to computerize its vast paper archives, creating a centralized database of American lives. The prospect of 45 million dossiers accessible at the push of a button triggered a political firestorm.

Professor Alan Westin of Columbia University, testifying before Congress, called it "the beginning of a surveillance society that would make 1984 look primitive." Consumer advocate Ralph Nader warned that Retail Credit was creating "invisible prisons of data" that would trap Americans in their past mistakes forever. The company's representatives, attempting to defend their practices, only made things worse. One executive, when asked about accuracy, admitted they verified perhaps 10% of the derogatory information they collected.

The congressional hearings of 1970 were a watershed moment. Witness after witness testified about lives destroyed by false reports: the teacher fired because a neighbor mentioned she had wine with dinner, the veteran denied insurance because an investigator confused him with someone else, the young couple rejected for a mortgage because they attended civil rights meetings. Representative Cornelius Gallagher of New Jersey called Retail Credit "a fungus feeding on human misery."

The result was the Fair Credit Reporting Act of 1970, the first federal law attempting to regulate the data broker industry. It gave consumers the right to know what was in their credit reports, to dispute inaccurate information, and limited who could access these reports. For Retail Credit, it was both a existential threat and an opportunity for reinvention.

In 1975, the company made a decisive break with its past, rebranding as Equifax—a name suggesting fairness and facts, rather than surveillance and suspicion. The transformation was more than cosmetic. Under new leadership, Equifax embraced the FCRA's requirements, positioning itself as a responsible steward of consumer data rather than a corporate spy agency. They phased out the most invasive practices, standardized their reporting, and began the slow process of digitizing their records.

But the DNA of the original company remained. The fundamental business model—collecting data on individuals without their explicit consent and selling it to third parties—never changed. The gossip-mongers became database administrators, the index cards became magnetic tape, but the essential proposition endured: Equifax would know your secrets, and for the right price, would share them with those who held power over your economic life. This tension between public necessity and private profit would define everything that followed.

III. Building the Modern Credit Bureau (1975-2000)

The morning of May 11, 1971, marked a pivotal moment in Equifax's evolution. As trading opened on the New York Stock Exchange, the company's ticker symbol—EFX—appeared for the first time on the big board. The former gossip-peddler from Atlanta had arrived on Wall Street, carrying with it filing cabinets containing the financial DNA of millions of Americans.

The NYSE listing was more than symbolic. It represented a fundamental shift in how the company would operate. Now answerable to public shareholders, Equifax needed predictable revenue growth and expanding margins. The solution came through an insight that would reshape the entire credit industry: standardization through technology. If you could reduce human financial behavior to a set of standardized codes and scores, you could process millions of decisions at electronic speed.

The post-FCRA years forced a remarkable transformation. Where investigators once scribbled subjective notes about "character," Equifax now built algorithmic models. The company hired armies of programmers, many poached from IBM and the aerospace industry, to construct what would become one of the world's largest private databases. By 1980, they were processing 1.5 million credit reports daily, each one generated in seconds rather than the days it took in the paper era.

The computerization brought an unexpected benefit: plausible deniability. When accused of discrimination, Equifax could now point to "objective" algorithms. The fact that these algorithms were trained on decades of discriminatory data, perpetuating the biases of the past in silicon and code, was harder to see and prove. The computer, it turned out, was the perfect laundering mechanism for systemic prejudice.

Geographic expansion followed the technology. Equifax acquired regional credit bureaus across the United States, absorbing their files and relationships. Each acquisition was a data acquisition—millions of additional consumer files flowing into the growing mainframes in Atlanta. By 1985, the company had assembled complete financial profiles on 150 million Americans, tracking everything from credit card payments to court judgments.

But CEO Jack Rogers, who took the helm in 1987, saw an even bigger opportunity. Why limit Equifax to credit reporting? The same data infrastructure could support multiple verticals. The company launched into insurance information services, employment verification, and government benefits validation. Each new business line created another reason for organizations to feed data into Equifax's systems, creating a virtuous cycle of data accumulation.

The healthcare expansion exemplified this strategy. In 1994, Equifax acquired HealthChex, gaining access to medical payment histories. The acquisition of Osborn Laboratories added drug testing results to consumer files. Electronic Tabulating Services brought hospital billing records. Suddenly, Equifax knew not just your credit card balances but your medical debts, prescription histories, and health insurance claims.

This diversification strategy culminated in two massive spinoffs that would define Equifax's modern structure. In 1997, the company spun off ChoicePoint, its insurance and government services division, giving shareholders one share of the new company for every ten Equifax shares held. ChoicePoint took with it the most controversial aspects of the old Retail Credit Company—the background checks, the insurance investigations, the government contracts. Equifax kept the credit bureau, positioning itself as a purely financial services company.

The math was elegant. ChoicePoint's market cap quickly exceeded $1 billion, creating instant value for Equifax shareholders while removing regulatory headaches. Four years later, Equifax repeated the trick with Certegy, spinning off its payment processing division in a deal that created another billion-dollar company (later acquired by Fidelity National Information Services for $1.8 billion).

These spinoffs weren't just financial engineering—they were strategic positioning. By 2000, Equifax had transformed itself into a pure-play credit bureau, one third of what industry insiders called the "Big Three" oligopoly alongside Experian and TransUnion. This wasn't an accident but the result of careful market structuring.

The oligopoly operated on a principle of mutual dependence. Lenders wanted comprehensive credit histories, which meant they needed data from all three bureaus. But maintaining relationships with multiple bureaus was expensive, so the market naturally consolidated around three players—enough for redundancy, not so many that coordination became impossible. The bureaus, meanwhile, carefully avoided competing on price, instead differentiating through analytics and services.

The numbers told the story of this transformation. Revenue grew from $397 million in 1980 to $1.8 billion by 2000. The company's stock price increased thirty-fold. Most remarkably, Equifax had paid uninterrupted dividends since 1920—through the Great Depression, World War II, and every recession since. This wasn't just a business; it was an institution, as essential to American capitalism as the Federal Reserve.

By the turn of the millennium, Equifax had achieved something remarkable: It had become simultaneously invisible and indispensable. Most Americans had no idea the company existed, yet couldn't buy a car, rent an apartment, or get a job without passing through its systems. The transformation from neighborhood gossip to algorithmic arbiter was complete, setting the stage for an even more ambitious expansion into the digital age.

IV. The Data Acquisition Spree (2000-2017)

The email that landed in Bill Canfield's inbox in early 2007 was exactly what he'd been waiting for. Equifax wanted to buy TALX, the company he'd built from a small voice-response startup into the nation's largest employment verification service. The price tag: $1.4 billion. For Canfield, it was vindication. For Equifax, it was the key to unlocking a new dimension of surveillance capitalism.

But we're getting ahead of ourselves. To understand why Equifax would pay such a premium for TALX, we need to understand the strategic revolution happening in Atlanta. The credit bureau business, while profitable, was maturing. Growth required either taking market share from Experian and TransUnion—a dangerous game that could trigger price wars—or finding entirely new data streams to monetize. CEO Rick Smith, who took the reins in 2005, chose the latter.

The strategy was elegant in its ambition: become the central nervous system of American capitalism by capturing data at every economic touchpoint. Credit was just the beginning. Equifax would know where you worked, how much you earned, when you changed jobs, whether you received government benefits, and a thousand other data points that, when combined, created a real-time economic portrait of unprecedented resolution.

The acquisition spree began modestly. In 2010, Equifax bought Anakam, a pioneering SMS two-factor authentication company. On the surface, it seemed like a simple security play. But Anakam gave Equifax something more valuable: verified phone numbers linked to identities, creating another dimension in their consumer profiles. Every authentication was a data point, confirming not just identity but activity patterns and device ownership.

The 2011 acquisition of eThority added business intelligence capabilities, allowing Equifax to analyze the data it collected in new ways. But these were appetizers. The main course was TALX.

TALX's origin story reads like a case study in finding gold in overlooked markets. Founded in 1972 as Interface Technology Inc., the company initially built interactive voice response systems—those automated phone trees everyone loves to hate. But founder Bill Canfield saw an opportunity everyone else missed. In the late 1990s, HR departments were drowning in employment verification requests. Every mortgage, apartment rental, or credit application triggered phone calls to HR, each one eating 15-20 minutes of staff time.

Canfield's insight was brilliant: What if employers uploaded their payroll data to TALX, and verifiers could access it instantly for a fee? Employers saved HR costs, verifiers got instant accurate data, and TALX sat in the middle, collecting fees from both sides. They called it "The Work Number."

By 2007, The Work Number contained detailed employment and salary records for 54 million Americans—about one-third of the entire workforce. The database was updated with every payroll run, creating a real-time feed of American earnings. Major employers like Walmart, Amazon, and the federal government sent their entire payroll files to TALX. The data included not just current salary but complete earnings history, hire dates, termination reasons, even week-by-week income fluctuations. When the deal closed in May 2007, Bill Canfield joined Equifax as president of the TALX business unit and was elected to Equifax's board of directors. It was a masterstroke of vertical integration. The Work Number service contained over 147 million employment records, and Equifax now had real-time visibility into American paychecks.

The integration wasn't just about data—it was about creating new products impossible for competitors to replicate. By combining credit histories with employment data, Equifax could now offer "income insight" scores that predicted not just willingness to pay but ability to pay. They could spot job losses before missed payments, identify raises that might qualify someone for a larger loan, even detect patterns suggesting someone was about to switch jobs.

By 2010, integration was completed and in October 2012, Equifax changed the name of the TALX business unit to Equifax Workforce Solutions. The rebranding signaled the complete absorption of TALX into Equifax's DNA. What had been an independent company was now simply another data tentacle of the credit bureau octopus.

But the TALX story had a darker subplot that presaged Equifax's later troubles. In August 2004, TALX reached an agreement with the SEC to end an ongoing investigation, agreeing to pay a fine of $2.5 million. Separately, CEO William W. Canfield reached an agreement with the SEC to pay $859,999 in disgorgement and $100,000 in civil penalties. The issues involved revenue recognition problems—a warning sign about internal controls that Equifax apparently didn't heed.

The international expansion followed a similar playbook. In 2016, Equifax made its largest acquisition yet: Veda, Australia's dominant credit bureau, for $2.5 billion. Overnight, Equifax became the monopoly credit provider in Australia and New Zealand, adding 20 million consumer files and establishing a beachhead for Asian expansion. The pattern was consistent: find markets with fragmented credit data, consolidate them, then leverage the resulting monopoly.

Each acquisition wasn't just buying a company; it was buying a captive data stream. The 2011 purchase of eThority brought Brazilian credit data. The acquisition of multiple smaller firms brought everything from Canadian employment records to UK utility payment histories. By 2017, Equifax operated in 24 countries, each one feeding data back to the growing beast in Atlanta.

The numbers validated the strategy. Revenue grew from $1.4 billion in 2005 to $3.1 billion by 2016. The stock price more than doubled. Operating margins expanded as the company leveraged its scale—the marginal cost of adding another million consumer records was essentially zero, while the value to customers of comprehensive data kept rising.

But this relentless expansion came with a hidden cost. Each acquisition brought different technology stacks, security protocols, and data governance practices. Equifax was stitching together a Frankenstein monster of systems, held together by middleware and hope. The company that sold itself as the secure guardian of financial data was actually a patchwork of vulnerabilities waiting to be exploited.

Internal documents later revealed the chaos beneath the surface. The TALX systems used different authentication methods than Equifax legacy platforms. The Veda acquisition brought Australian data under U.S. servers without properly updating access controls. Employee turnover meant institutional knowledge about system interconnections was constantly being lost. The company was growing faster than it could secure itself.

By early 2017, Equifax was a colossus—but a fragile one. It controlled financial data on nearly a billion people worldwide, operated critical infrastructure for global lending, and generated massive profits for shareholders. It had achieved Rick Smith's vision of becoming indispensable to every financial decision. What it hadn't done was build the security infrastructure necessary to protect what it had assembled. The stage was set for catastrophe.

V. The Breach: 76 Days of Disaster (March-September 2017)

Susan Mauldin had been Equifax's Chief Security Officer for barely two years when the email arrived on March 8, 2017. The U.S. Computer Emergency Readiness Team was warning about a critical vulnerability in Apache Struts, a popular web application framework. The vulnerability, designated CVE-2017-5638, allowed attackers to execute code remotely—essentially giving them the keys to any system running the vulnerable software. Mauldin's team immediately sent notices to IT staff: patch everything within 48 hours.

What happened next would become a case study in how not to handle critical security updates. The patch notification went out through Equifax's internal ticketing system, but it was one of hundreds of alerts that month. No one tracked whether patches were actually applied. No one verified that all systems were updated. The company that held the financial DNA of America was operating on the honor system.

Meanwhile, in a different time zone, hackers—later identified as members of China's People's Liberation Army—were scanning the internet for unpatched Struts installations. They were patient, methodical, and very good at their jobs. On May 12, two months after the patch was released, they found what they were looking for: an Equifax dispute resolution portal still running the vulnerable version.

The initial breach was almost laughably simple. The hackers sent a specially crafted HTTP request to the vulnerable server. Within seconds, they had shell access. From there, they began their reconnaissance, moving laterally through Equifax's network with the patience of archaeologists on a dig. They weren't smashing and grabbing; they were methodically mapping the entire infrastructure. What the hackers discovered inside Equifax's network defied belief. On August 2, 2017, Equifax contacted a leading, independent cybersecurity firm, Mandiant, to assist in conducting a comprehensive forensic review to determine the scope of the intrusion—but by then the damage was done. The attackers had found databases protected with credentials that hadn't been changed in years. One particularly egregious discovery: a database containing unencrypted usernames and passwords, with the admin account literally set to "admin/admin." No two-factor authentication. No network segmentation. It was as if Equifax had left the keys to the kingdom under the doormat with a sign saying "keys here."

The hackers used these credentials to query databases containing the crown jewels: names, Social Security numbers, birth dates, addresses, and in some cases, driver's license numbers. They ran over 9,000 queries, carefully encrypting their traffic to avoid detection. Each query pulled back thousands of records. The exfiltration was massive but measured—designed to fly under the radar of whatever monitoring Equifax might have had in place.

What made this particularly damaging was Equifax's data architecture. Unlike a typical company breach where hackers might get customer records from one system, Equifax's entire business model involved aggregating data from thousands of sources. The hackers weren't just stealing Equifax's data; they were stealing data that Equifax had collected from banks, employers, courts, and government agencies. It was a one-stop shop for identity theft.

The unauthorized access occurred from mid-May through July 2017. The vulnerability was left unpatched until July 29, 2017 when Equifax's information security department discovered "suspicious network traffic" and on July 30, 2017, Equifax observed further suspicious activity and took the web application offline.

The detection itself was almost accidental. On July 29, an Equifax security analyst noticed unusual network traffic patterns—massive data transfers happening at odd hours to unfamiliar IP addresses. By the time they started investigating, the hackers had been inside their network for 76 days, methodically vacuuming up data on 147.9 million Americans, 15.2 million UK citizens, and nearly 20,000 Canadians.

The immediate response was chaos. Equifax executives huddled in crisis meetings, trying to understand the scope of the catastrophe. The company hired Mandiant, one of the world's premier cybersecurity firms, to conduct forensics. What Mandiant found was damning: this wasn't sophisticated hacking—it was negligence meeting opportunity.

But here's where the story takes an even darker turn. Between July 29, when the breach was discovered, and September 7, when it was publicly announced, several Equifax executives sold significant amounts of company stock. Chief Financial Officer John Gamble sold shares worth nearly $950,000. President of U.S. Information Solutions Joseph Loughran sold $584,000 worth. President of Workforce Solutions Rodolfo Ploder sold $250,000. They would later claim they were unaware of the breach when they made these trades, but the timing raised eyebrows across Wall Street and Washington.

The internal scramble during those 40 days between discovery and disclosure revealed the depth of Equifax's dysfunction. Executives couldn't even agree on basic facts: How many people were affected? What data was stolen? How did the hackers get in? The company's incident response plan, such as it existed, fell apart on contact with reality. Different departments gave conflicting information. The legal team wanted to say nothing; the PR team wanted to control the narrative; the security team just wanted to stop the bleeding.

When CEO Richard Smith was finally briefed on the full scope of the breach in late August, witnesses describe him as going pale. This wasn't just a data breach—it was an existential crisis. The company whose entire value proposition was trust had just proved itself catastrophically untrustworthy. The company that charged others for identity protection couldn't protect its own systems. The ironies were so thick you could cut them with a knife.

The 76 days of disaster weren't just about technical failure. They were about organizational failure at every level: governance that prioritized growth over security, a culture that treated IT as a cost center rather than critical infrastructure, and leadership that was apparently more concerned with stock prices than safeguarding the data of half the American population. The breach was over, but the real disaster was just beginning.

VI. The Aftermath: Chaos, Cover-ups, and Consequences

The morning of September 7, 2017, started like any other for most Americans. By noon, it had become a day they'd never forget. Equifax's announcement of the breach landed like a bomb, but it was the company's response that turned a disaster into a farce.

The first sign that Equifax was completely unprepared came with their remedy website: equifaxsecurity2017.com. Security experts immediately flagged it as suspicious—it looked exactly like a phishing site. The domain wasn't even registered to Equifax initially. Worse, Equifax's own Twitter account accidentally directed victims to "securityequifax2017.com"—a fake site that someone had set up as a joke. The company tasked with protecting financial identities couldn't even get its own website right.

Then came the terms and conditions fiasco. Buried in the fine print of the breach notification site was language that appeared to waive victims' rights to join class action lawsuits if they signed up for Equifax's "free" credit monitoring. The backlash was swift and brutal. Within hours, attorneys general from multiple states were threatening action. Equifax hastily backtracked, claiming the arbitration clause didn't apply to the breach—but the damage to their credibility was done.

The technical incompetence continued. In October, security researcher Brian Krebs discovered that Equifax's breach website was actually serving malware to visitors. The company responsible for one of history's worst data breaches was now actively infecting the computers of people seeking help. It was beyond parody.

Equifax announced that the Chief Information Officer and Chief Security Officer are retiring. Richard Smith retired as CEO on September 26, 2017 and the Board of Directors appointed Paulino do Rego Barros Jr. as Interim CEO. The exodus had begun. Susan Mauldin, the Chief Security Officer who had implemented Equifax's first patch management policy just two years earlier, "retired" immediately. Chief Information Officer David Webb followed her out the door.

But it was CEO Richard Smith's departure that captured the public's attention—and rage. On September 26, 2017, Equifax CEO Richard Smith retired, walking away with a $90 million golden parachute. His retirement package included $18 million in pension benefits, $24 million in stock options, and various other compensations. The man who had overseen the breach that exposed half of America's financial data was set for life.

The congressional hearings that followed were a masterclass in corporate accountability theater. Smith, called before multiple committees, deployed the classic CEO defense: he knew nothing, it was a technical issue, mistakes were made (passive voice doing heavy lifting), and he accepted full responsibility while accepting no actual consequences. Representative Greg Walden called it "a full-on sprint" of passing the buck.

One exchange captured the absurdity perfectly. When asked why Equifax hadn't encrypted Social Security numbers, Smith explained that the company considered them "public information" since they're widely available. The incredulous representative responded: "So your position is that the most sensitive piece of information Americans have is already public, so why bother protecting it?" Smith had no good answer. The financial fallout was initially devastating but ultimately manageable. In July 2019, Equifax agreed to pay at least $575 million, and potentially up to $700 million, as part of a global settlement with the Federal Trade Commission, the Consumer Financial Protection Bureau, and 50 U.S. states and territories. The company paid $300 million to a consumer fund, $175 million to states, and $100 million to the CFPB. For a company that generated over $3 billion in annual revenue, it was painful but not fatal.

The settlement itself became another debacle. The FTC had set aside $31 million for cash payments to affected consumers who already had credit monitoring, promising up to $125 per person. But when millions filed claims, it became clear that each person would receive only a small fraction of that amount. Victims of one of history's worst data breaches would get less than the cost of a pizza.

The stock market's reaction told the real story. Equifax shares plummeted from $142 before the breach announcement to $92 within days—a loss of over $5 billion in market value. But then something remarkable happened: the stock began recovering. Within 18 months, it had returned to pre-breach levels. By 2019, it was hitting new all-time highs. The market had decided that Equifax was indeed too big to fail. The China attribution added another layer to the story. In February 2020, the Department of Justice indicted four members of China's People's Liberation Army—Wu Zhiyong, Wang Qian, Xu Ke, and Liu Lei—for the hack. A federal grand jury charged four members of the Chinese People's Liberation Army (PLA) with hacking into the computer systems of the credit reporting agency Equifax, with the nine-count indictment naming Wu Zhiyong, Wang Qian, Xu Ke and Liu Lei as members of the PLA's 54th Research Institute.

The indictment revealed the hackers had run approximately 9,000 queries on Equifax's system, carefully routing traffic through 34 servers in nearly 20 countries to disguise their location. This wasn't just theft—it was espionage. The conspirators stored the stolen information in temporary output files, compressed and divided the files, and ultimately were able to download and exfiltrate the data from Equifax's network to computers outside the United States, running approximately 9,000 queries on Equifax's system, obtaining names, birth dates and social security numbers for nearly half of all American citizens.

Attorney General William Barr framed it as part of a pattern: "The Justice Department believes the Chinese were also responsible for breaching systems controlled by the Office of Personnel Management, Marriott hotels, and the health insurance company Anthem" with the data having "economic value" that could "feed China's development of artificial intelligence tools as well as the creation of intelligence-targeting packages". The stolen Equifax data wasn't being sold on the dark web—it was being weaponized by a nation-state.

Yet even this revelation didn't fundamentally damage Equifax. If anything, it provided cover. The company could now position itself as a victim of sophisticated state-sponsored cyber warfare rather than a negligent custodian of data. The narrative shifted from "Equifax failed" to "Equifax was attacked by the Chinese military." It was a subtle but crucial reframing.

The government contracts told the real story. Despite the breach, federal agencies continued using Equifax services. The IRS briefly suspended a $7.2 million contract but later resumed it. The Social Security Administration, Department of Defense, and other agencies maintained their relationships with the company. The message was clear: Equifax was too embedded in the American financial system to punish meaningfully.

By 2019, something remarkable had happened. The breach, rather than destroying Equifax, had accelerated its transformation. The company used the crisis as justification for massive infrastructure investments that it might have delayed for years. The disaster became, perversely, an opportunity. The aftermath wasn't just about damage control—it was about using catastrophe as a catalyst for change that would ultimately make Equifax stronger than before.

VII. The Cloud Transformation & Recovery (2018-Present)

Paulino do Rego Barros Jr. didn't look like a typical American CEO when he took the helm at Equifax in April 2018. The Brazilian executive, with his slight accent and background running Equifax's Asia-Pacific operations, seemed an unlikely choice to lead the recovery from an all-American disaster. But the board had made a calculated bet: they needed someone who could credibly claim distance from the old regime while understanding Equifax's global operations. His first promise to consumers was simple but revolutionary for the credit bureau industry: free credit freezes "for life."

It was a masterstroke of crisis management. The credit freeze—once a profit center that generated millions in fees—became a peace offering. But more importantly, it shifted the conversation from what Equifax had failed to do to what it was now doing for consumers. The company that had exposed America's financial data was now positioning itself as its protector.

Behind the scenes, Barros was orchestrating something far more ambitious: a complete technological transformation that would cost more than $3 billion. The Equifax Cloud initiative wasn't just about moving to cloud infrastructure—it was about rebuilding the company's entire technology stack from the ground up. Think of it as performing open-heart surgery while running a marathon.

The numbers were staggering. Equifax committed to spending $1.25 billion on technology and security between 2018 and 2020 alone. By 2024, total cloud transformation investments would exceed $3 billion. For context, this was more than half the company's entire annual revenue being poured into infrastructure. Any other company might have been crushed by such spending, but Equifax had one advantage: customers had nowhere else to go.

The technical transformation was genuinely impressive. Equifax migrated 90% of its applications to the cloud, consolidated data centers from 15 to 3, and implemented what it called "continuous compliance"—automated security checks that ran thousands of times per day. The company that once used "admin/admin" as a password now employed some of the world's most sophisticated security systems.

But here's what made the transformation truly clever: Equifax used the breach as cover to accelerate business changes it had wanted to make anyway. Moving to the cloud wasn't just about security—it enabled new products, faster processing, and most importantly, the ability to sell real-time data services that commanded premium prices. The company transformed its greatest failure into its business case for the future. The actual investment figures are staggering. The Equifax Cloud™ is a top-tier global technology and security infrastructure backed by an approximate $3 billion multi-year investment and is one of the largest Cloud initiatives ever undertaken in the industry. By 2024, Equifax was successfully defending against 15 million cybersecurity threats each day—750 hostile attacks per minute—a far cry from the company that couldn't patch a single vulnerability in 2017.

The Work Number, that TALX acquisition from 2007, became the crown jewel of the new Equifax. Now fully integrated into the cloud infrastructure, it provided real-time employment and income verification for over 136 million active employment records. Every payroll run from thousands of employers flowed directly into Equifax's systems, creating a continuously updated stream of the most valuable data in finance: proof of income.

The business model innovation was subtle but powerful. Rather than just selling static credit reports, Equifax could now offer dynamic, real-time insights. A lender could see not just that someone had a job, but whether their income was stable, trending up, or at risk. The company's new "continuous monitoring" services alerted lenders the moment a borrower's employment status changed. It was surveillance capitalism perfected.

The AI transformation added another dimension. Equifax set a goal to create 80% of their new scores and models in 2024 using AI and machine learning. These weren't just incremental improvements—they were entirely new products that only Equifax could offer because only Equifax had the combination of credit, employment, and utility data needed to train the models.

The regulatory environment, rather than constraining Equifax, actually strengthened its moat. New data protection regulations made it harder for startups to compete. Compliance costs that Equifax could easily absorb would crush smaller players. The company that had suffered history's worst data breach was now advising regulators on cybersecurity standards. It was a masterclass in regulatory capture.

Current CEO Mark Begor, who took over in 2018, articulated the vision clearly at the 2025 Investor Day: "It's hard to articulate for investors how much effort went into the last five years but then how unleashing it is for all of us to be able to pivot to leveraging the Cloud versus building it. It's really a new Equifax in our eyes and a next chapter that is focused on growth going forward".

The financial markets bought the story completely. By 2024, Equifax was generating US$5.68b in revenue (up 7.9% from FY 2023) with operating margins expanding despite the massive technology investments. The stock price reached all-time highs, trading at premium multiples that reflected not a company recovering from disaster but one positioned for dominance.

The international expansion accelerated post-breach. The cloud infrastructure made it easier to enter new markets, and the Equifax brand—rather than being toxic—actually carried weight with regulators who saw the company's transformation as a model for the industry. Operations expanded to 24 countries, each one feeding more data into the growing machine.

But perhaps the most remarkable aspect of the recovery was how completely the breach had been memory-holed. New customers signing up for Equifax services rarely mentioned it. Lenders continued to rely on Equifax data as if nothing had happened. The company that had exposed half of America's Social Security numbers was now trusted with even more sensitive data than before.

The transformation wasn't just technological—it was psychological. Equifax had successfully reframed itself from a company that had failed at security to one that had learned from failure and emerged stronger. The breach became part of the company's story of resilience rather than negligence. It was perhaps the greatest comeback in corporate history, achieved not through contrition but through sheer market power. The lesson was clear: in surveillance capitalism, you're not too big to fail—you're too essential to punish.

VIII. The TALX/Work Number Side Story

Bill Canfield was sweating bullets in the summer of 2004. The SEC investigators sitting across from him weren't interested in pleasantries. They wanted to know why TALX, the company he'd built from nothing into a NASDAQ darling, had been cooking its books. The specific allegation was damning: TALX had been recording revenue for products that hadn't been delivered, inflating earnings to meet Wall Street expectations.

But to understand how The Work Number became the most comprehensive employment surveillance system in America, we need to go back to 1972. That's when a group of engineers, including H. Richard "Rick" Grodsky, a professor at Washington University in St. Louis, founded Interface Technology Inc. Their initial product was mundane: interactive voice response systems, the automated phone trees that would later torment millions of callers worldwide.

For years, the company struggled along, building custom phone systems for corporations. The work was steady but uninspiring. Then in 1986, everything changed when Bill Canfield joined as President and CEO. Canfield wasn't an engineer—he was a salesman who understood something the founders didn't: the real value wasn't in the technology but in the data flowing through it.

The insight came from a mundane observation. HR departments were drowning in employment verification calls. Every mortgage application, every apartment rental, every background check triggered multiple calls to verify employment and income. Each call took 15-20 minutes of staff time. For large employers, it was a full-time job just answering these requests. Canfield saw opportunity where others saw annoyance.

TALX went public listing on the NASDAQ in an IPO in 1996 and offered 2,000,000 shares at $9 per share for a total offer amount of $18,000,000. But the real transformation came with The Work Number. Instead of employers answering verification calls, they would upload their entire payroll databases to TALX. Verifiers would pay to access the data instantly. Employers saved HR costs, verifiers got immediate accurate information, and TALX sat in the middle, collecting fees from both sides.

The genius was in the network effects. The more employers who joined, the more valuable the service became to verifiers. The more verifiers who used it, the more pressure on employers to participate. By 2002, TALX had critical mass. But success bred temptation.

The SEC investigation revealed a pattern of aggressive accounting that would presage Equifax's later security failures. In August 2004, TALX reached an agreement with the SEC to end the ongoing SEC investigation, agreeing that the company would pay a fine of $2.5 million. Separately, William W. Canfield, the company's president and chief executive officer, reached an agreement in principle with the SEC staff to settle its ongoing investigation against him in a related matter. Canfield agreed to pay $859,999 in disgorgement and $100,000 in civil penalties.

But the scandal barely dented TALX's growth. Between 2002 and 2005, the company went on an acquisition spree, buying Frick Company, Gates McDonald, and multiple HR services firms. Each acquisition brought more employer relationships and more data. TALX also provided a branded employment and income verification service, The Work Number for Everyone, that provided automated access to employment and salary records of large employers for purposes of loan and other credit approvals. In the early 2000s, the employment and income verification service, The Work Number, as it later became known, became the revenue and profit growth engine for the company.

The business model was almost perfect in its exploitation of information asymmetry. Employees had no idea their employers were sending complete payroll records to TALX. They couldn't opt out—participation was decided by their employer. They couldn't correct errors—only employers could update records. They couldn't even see what information was being shared—access required paying a fee.

By 2007, when Equifax came calling, The Work Number contained detailed employment records for 54 million Americans. The Work Number® service, created by TALX in 1995, is a leader in workplace verification and has over 147 million employment records. The database updated with every payroll run, creating a real-time feed of American earnings. It included not just current salary but complete earnings history, bonuses, deductions, even hours worked each week.

The integration with Equifax created surveillance capabilities that would have made the Stasi envious. Now a single company could see not just your credit history but your complete employment record. They knew if you'd been promoted, demoted, had your hours cut, received a raise, or changed jobs. They could predict with frightening accuracy who was about to default on a loan simply by watching for changes in income patterns.

In October 2017, security researcher Brian Krebs exposed a massive vulnerability in The Work Number. Anyone with a Social Security number and date of birth could access detailed salary histories. The same lax security that would characterize the Equifax breach was already present in TALX systems. The admin/admin passwords, the unencrypted databases, the assumption that obscurity was security—it was all there.

From April 2016 to March 2017, Equifax Workforce Solutions data including individuals' tax records was taken in a data breach. This earlier breach, which received far less attention than the main Equifax hack, exposed W-2 tax forms and other sensitive employment data. It was a preview of the catastrophe to come, ignored by both Equifax management and regulators.

The Work Number today is even more powerful than Canfield likely imagined. It covers over 136 million active employment records, processing millions of verifications annually. During the COVID-19 pandemic, it became essential infrastructure for unemployment verification and stimulus payment distribution. The government that should regulate it instead depends on it.

The system represents surveillance capitalism in its purest form. Workers have no relationship with Equifax, didn't consent to data sharing, and can't opt out. Their most sensitive financial information—income—is harvested and sold without their knowledge. Employers, meanwhile, have outsourced liability for data breaches while saving money on HR costs. It's a perfect machine for extraction, running 24/7, converting the daily labor of millions into data products for sale.

The TALX story is really three stories intertwined: a tale of innovation that solved a real problem, a cautionary example of how financial pressure leads to ethical compromises, and ultimately, a blueprint for building surveillance infrastructure so useful that its abuses become invisible. The Work Number isn't just a product—it's a paradigm, showing how surveillance capitalism transforms even the most basic human activities, like going to work, into data to be captured, processed, and sold.

IX. Playbook: Business & Security Lessons

The Equifax story reads like a Harvard Business School case study written by Franz Kafka. It's a masterclass in how to build an unassailable business position through regulatory capture, network effects, and systematic exploitation of information asymmetries. It's also a cautionary tale about how security theater replaces actual security when the incentives are misaligned. Let's dissect the playbook.

The Data Monopoly Playbook

The genius of the credit bureau model is that it inverts the normal business relationship. Equifax's true customers aren't the consumers whose data they collect—they're the lenders who pay for access. This creates what economists call a "two-sided market" with perverse incentives. Consumers can't choose not to participate, can't switch providers, and can't even see all the data collected about them without paying.

The regulatory moat is equally brilliant. After each scandal, new regulations emerge that Equifax helps write. These regulations inevitably require expensive compliance infrastructure that Equifax can afford but potential competitors cannot. The Fair Credit Reporting Act, meant to constrain credit bureaus, instead entrenched them. The post-breach security requirements will do the same.

Consider the switching costs. A bank using Equifax has integrated its systems, trained its staff, and built its risk models on Equifax data. Switching to another provider (if one existed) would cost millions and take years. But here's the key: even if they switched, they'd still need Equifax data because not all lenders use the same bureau. It's vendor lock-in perfected.

The network effects run deeper than most realize. Every piece of data Equifax collects makes its other data more valuable. Employment verification enhances credit data. Credit data improves identity verification. Identity verification enables employment screening. It's a virtuous cycle of surveillance where the whole is exponentially more valuable than the parts.

Security Theater vs. Security Reality

The Equifax breach revealed four critical security failures that pervade the industry. First, identification systems were a joke. The admin/admin password wasn't an anomaly—it represented a culture where security was an afterthought. When your entire business model depends on trust, you'd think security would be paramount. Instead, it was treated as a cost center.

Second, detection capabilities were essentially nonexistent. The hackers operated for 76 days without detection, running 9,000 queries and exfiltrating data from 147 million records. The only reason they were caught was accidental—a security analyst noticed unusual traffic patterns. There was no systematic monitoring, no behavioral analysis, no anomaly detection worthy of the name.

Third, network segmentation was a fantasy. Once the hackers breached the dispute portal, they had access to everything. The crown jewels—Social Security numbers, credit card numbers, employment records—were all accessible from a single entry point. It was like building a bank vault with steel walls but leaving the roof open.

Fourth, data governance was abysmal. Databases contained unencrypted credentials. Sensitive data wasn't masked or tokenized. Access controls were suggestions rather than requirements. The company that judged others' creditworthiness couldn't manage its own technical debt.

But here's the disturbing truth: these weren't bugs—they were features. Real security is expensive and creates friction. In a competitive market, the company that spends less on security and more on sales wins—until a breach occurs. But when the breach affects all competitors equally (since they all have terrible security), and customers can't leave, the incentive to improve disappears.

Crisis Management Anti-Patterns

Equifax's breach response was a masterclass in what not to do, yet they survived it. This paradox reveals important lessons about crisis management in monopolistic markets.

The stock sales controversy should have been devastating. Executives selling shares after learning of the breach but before public disclosure is insider trading in all but legal technicality. In a competitive market, this would trigger customer exodus. But Equifax customers—lenders—cared more about continued access to credit data than executive ethics.

The communication failures were equally instructive. The breach website that looked like a phishing site, the terms that waived lawsuit rights, the site serving malware—each mistake would normally destroy customer trust. But when customers have no alternative, trust becomes irrelevant. Equifax didn't need to maintain trust; it needed to maintain access.

The victim-blaming was perhaps most telling. Equifax consistently positioned consumers as responsible for protecting themselves from Equifax's failure. Free credit monitoring (from Equifax!) was positioned as generous compensation. The company that exposed the data would now profit from monitoring it. It's like an arsonist selling fire insurance.

The Resilience of Oligopolies

The three-bureau system creates a prisoner's dilemma that ensures stability. If one bureau significantly improved security, it would increase costs without gaining competitive advantage (since lenders need all three bureaus anyway). If one bureau lowered prices, others would match, reducing profits for all. The Nash equilibrium is to maintain the status quo.

This extends to innovation. Why invest in better fraud detection when you can simply pass breach costs to consumers? Why improve data accuracy when errors generate dispute fees? Why enhance security when breaches don't affect market share? The oligopoly structure removes normal market incentives for improvement.

The regulatory capture completes the circle. Equifax executives regularly rotate through government positions. They help write the laws that govern them. They fund the studies that evaluate them. They've created a system where the referees, players, and scorekeepers are all on the same team.

The ultimate lesson of Equifax isn't about cybersecurity—it's about market structure. In a truly competitive market, Equifax would have died after the breach. In a regulated monopoly, it thrived. The playbook isn't about building better products or services; it's about building unassailable market positions where failure becomes impossible because success doesn't require competence—just position.

X. Analysis & Investment Perspective

From a pure investment standpoint, Equifax presents a fascinating paradox: a company that catastrophically failed at its core competency yet emerged stronger. Understanding this requires examining both the bull and bear cases through the lens of market structure rather than operational excellence.

The Bull Case: Monopoly Power and Regulatory Moats

The bull thesis rests on a simple observation: Equifax is essentially a regulated utility with monopoly pricing power. Like electric companies or water utilities, it provides an essential service with no practical alternatives. But unlike traditional utilities, its marginal costs approach zero and its pricing power faces minimal regulatory constraint.

The oligopoly structure is virtually unbreakable. Starting a new credit bureau would require convincing thousands of lenders to report data, building consumer files from scratch, and achieving regulatory approval—a process that would take decades and billions of dollars. The last successful new entrant was over 40 years ago. The barriers to entry aren't just high; they're essentially insurmountable.

The cloud transformation, despite its massive cost, is already paying dividends. Operating margins are expanding as legacy infrastructure is decommissioned. New AI-driven products command premium prices with minimal incremental cost. The company that spent $3 billion on technology can now innovate at a fraction of competitors' costs.

The data accumulation continues accelerating. Every day, Equifax ingests millions of new records—employment updates, utility payments, rental histories. This data has compound value: the more historical information available, the better predictive models become. It's a perpetual motion machine of value creation.

International expansion offers decades of growth. Most countries lack comprehensive credit bureaus. As consumer lending globalizes, Equifax can replicate its monopoly position worldwide. The Veda acquisition in Australia showed the playbook: buy the dominant player, integrate the technology, extract monopoly rents.

The subscription model transformation is perhaps most compelling. Equifax is shifting from transactional credit reports to continuous monitoring services. This creates predictable, recurring revenue with higher margins and customer stickiness. It's the SaaS playbook applied to surveillance capitalism.

The Bear Case: Systemic Risks and Disruption Vectors

The bear thesis begins with regulatory risk finally materializing. Public anger over data breaches, combined with growing privacy awareness, could trigger meaningful regulation. Europe's GDPR shows what's possible. If America implemented similar rules—requiring explicit consent, enabling data portability, mandating deletion rights—Equifax's business model would shatter.

Cyber insurance costs are exploding. Post-breach, Equifax faces astronomical premiums and coverage exclusions. Future breaches—and there will be future breaches—could trigger uninsurable losses. The company has painted a massive target on its back for state-sponsored hackers and criminal organizations.

Technology disruption looms larger than most realize. Blockchain-based identity systems could enable individuals to control their own credit data. Decentralized finance (DeFi) doesn't need credit bureaus. Open banking regulations could force data portability. The technology to disrupt Equifax exists; it lacks only adoption.

The reputation liability is permanent. Every future breach, every scandal, every mistake will be viewed through the lens of 2017. Equifax has become synonymous with data incompetence. This reputation damage may not affect current revenues but limits future opportunities.

Concentration risk is extreme. Equifax depends on a small number of large financial institutions for most revenue. If major banks developed their own credit assessment systems or collaborated on an alternative, Equifax would face existential threat. The company's customer concentration makes it vulnerable to coordinated action.

Competitive Dynamics

The competition with Experian and TransUnion is best understood as choreographed dance rather than warfare. Price competition is minimal. Service differentiation is cosmetic. Innovation focuses on extracting more value from existing data rather than fundamentally improving products.

Experian, with its international presence and marketing services, has slightly different positioning but plays the same game. TransUnion, the smallest of the three, follows the leaders. None has incentive to disrupt the profitable equilibrium. They compete for marginal share while maintaining industry margins.

The real competitive threat comes from adjacent players. Amazon knows purchasing history. Apple has payment data. Google sees search patterns that predict financial distress better than credit scores. These tech giants have the data, technology, and capital to disrupt credit bureaus—if they chose to.

Financial Analysis

The numbers tell a story of resilience. Revenue has grown steadily post-breach, from $3.4 billion in 2017 to $5.7 billion in 2024. Operating margins have expanded despite massive technology investments. Return on equity exceeds 20%. These are monopoly-level returns.

The balance sheet is leveraged but manageable. Debt-to-EBITDA ratios remain within covenant levels. Free cash flow generation is robust, funding both dividends and growth investments. The company that seemed financially precarious post-breach now looks fortress-like.

Valuation multiples reflect market confidence. The stock trades at premium P/E ratios compared to historical averages. The market is pricing in continued growth and margin expansion. Either investors are wrong, or they understand something critics miss: Equifax is too essential to fail.

The Investment Decision

From a purely financial perspective, Equifax presents an uncomfortable truth: sometimes the worst companies make the best investments. The business model is exploitative, the security history is abysmal, and the social value is questionable. But the moat is undeniable, the margins are expanding, and the growth trajectory continues.

For value investors, the question isn't whether Equifax is a good company but whether it's a good investment. The two are startlingly different. The same factors that make Equifax problematic—monopoly power, regulatory capture, information asymmetry—make it profitable.

For growth investors, the AI transformation and international expansion offer compelling narratives. The company trading at growth multiples despite its mature market position suggests the market sees something beyond the current business.

For ESG-focused investors, Equifax presents a dilemma. It fails virtually every test of social responsibility and governance. Yet it's also essential infrastructure for financial inclusion, enabling lending to millions who would otherwise lack access to credit.

The ultimate investment insight may be this: Equifax is a bet on the continuation of surveillance capitalism. If you believe data collection will face meaningful restraint, consumer privacy will be protected, and market structure will be reformed, avoid the stock. If you believe the status quo will persist, that regulation will remain captured, and that data exploitation will continue expanding, Equifax offers monopoly returns in a digital age. The investment decision, like the company itself, forces uncomfortable choices about the world we're building and our complicity in its construction.

XI. Epilogue: What This Means for Society

Standing in the ruins of the 2017 breach, a fundamental question emerges: How did we create a system where three private companies hold absolute power over Americans' financial lives? The answer reveals uncomfortable truths about modern capitalism, regulatory failure, and the price we pay for convenience.

The paradox of data brokers is that they're simultaneously essential and existential threats. Without credit bureaus, modern lending would collapse. Mortgages would require massive down payments. Credit cards would disappear. Small business loans would become impossible. The democratization of credit that lifted millions from poverty depends on these institutions. Yet these same institutions create honeypots of data so valuable that nation-states dedicate military resources to stealing them.

Between October 2012 and September 2017, the Consumer Financial Protection Bureau received 57,000+ consumer complaints about Equifax—and that was before the breach. Consumers reported errors they couldn't fix, mysterious accounts they didn't open, identities stolen using Equifax data. The complaint patterns revealed a system optimized for data collection rather than accuracy, for profit rather than protection.

The regulatory response to the breach was theater. Congressional hearings generated soundbites but no structural reform. The FTC settlement grabbed headlines but didn't change business practices. States passed notification laws but didn't address root causes. The system that enabled the breach remains essentially unchanged. The revolving door between Equifax and government continues spinning.

Privacy has become a luxury good in surveillance capitalism. The wealthy can afford identity protection services, lawyers to fix errors, and financial cushions when things go wrong. The poor face cascading consequences from data errors: denied apartments, rejected job applications, predatory loan terms. The same system that promises financial inclusion creates digital redlining, where algorithms trained on biased data perpetuate historical discrimination.

The breach also exposed the fiction of corporate responsibility. Equifax collected data without consent, monetized it without compensation, exposed it through negligence, then profited from the aftermath by selling protection services. It's a business model that would make robber barons blush: create the problem, sell the solution, capture the regulators, repeat.

Yet the most disturbing aspect isn't Equifax's behavior—it's our acceptance of it. We've normalized a system where our most sensitive information is harvested, packaged, and sold without our participation. We've accepted that errors in these systems can destroy lives with little recourse. We've internalized the notion that surveillance is the price of participation in modern economy.

The technical solutions exist. Blockchain could enable self-sovereign identity where individuals control their own data. Homomorphic encryption could allow credit decisions without exposing underlying information. Zero-knowledge proofs could verify creditworthiness without revealing details. The technology to build a privacy-preserving credit system exists—what's missing is the will to implement it.

The international perspective is instructive. Europe's GDPR gives consumers rights Americans can only dream of: the right to access all data collected, the right to correct errors, the right to deletion, the right to portability. These aren't radical concepts—they're basic dignity in the digital age. Yet in America, the credit bureaus have successfully positioned such rights as threats to the financial system.

Can this system be reformed? History suggests not through traditional channels. Equifax and its peers have captured the regulatory apparatus. They fund the research that evaluates them. They write the rules that govern them. They've created a system where reform threatens not just their profits but the entire credit infrastructure. It's regulatory capture so complete that even victims defend their victimizers.

The path forward requires recognizing that credit bureaus aren't just businesses—they're utilities that should be regulated as such. Their data isn't just commercial information—it's digital identity that deserves protection. Their breaches aren't just corporate failures—they're national security incidents requiring military-grade response.

More fundamentally, we need to question whether three private companies should have monopoly control over financial identity. Should essential infrastructure be run for profit? Should data subjects have no say in how their information is used? Should errors that destroy lives be treated as acceptable business costs?

The next mega-breach isn't a question of if but when. The same factors that made Equifax vulnerable exist across the industry. The same perverse incentives that prioritized profit over security remain. The same regulatory capture that prevented meaningful reform continues. We're not just waiting for the next Equifax—we're enabling it.

The Equifax story ultimately asks us to confront what kind of society we want to be. Do we accept surveillance capitalism as inevitable, trading privacy for convenience? Do we allow essential infrastructure to operate without meaningful oversight? Do we continue pretending that self-regulation works when evidence screams otherwise?

The credit bureaus have made their choice. They've chosen profits over protection, surveillance over security, monopoly over innovation. The question now is whether we'll make a different choice—whether we'll demand a financial system that serves people rather than exploiting them, that protects data rather than weaponizing it, that treats identity as a right rather than a product.

The answer will determine not just the future of companies like Equifax but the kind of digital society we become. In an age where data is power, who controls that data controls everything. The Equifax breach wasn't just a corporate scandal—it was a preview of a future where our digital selves are stripped, packaged, and sold to the highest bidder. Whether we accept that future or fight for something better will define the next chapter of surveillance capitalism.

The irony is perfect: Equifax means "equity facts"—fair and factual information. Instead, it represents the opposite: a system where facts are malleable, fairness is absent, and equity is extracted rather than created. It's a name that mocks its victims, a brand that embodies everything wrong with modern capitalism. And yet, tomorrow, millions of Americans will have their financial fates determined by algorithms they'll never see, running on data they can't correct, controlled by a company that catastrophically failed to protect them.

That's not just a business model—it's a tragedy. And unlike the breach, it happens every single day.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube