Dynatrace: The Austrian Reinvention Machine

I. Introduction & Episode Roadmap

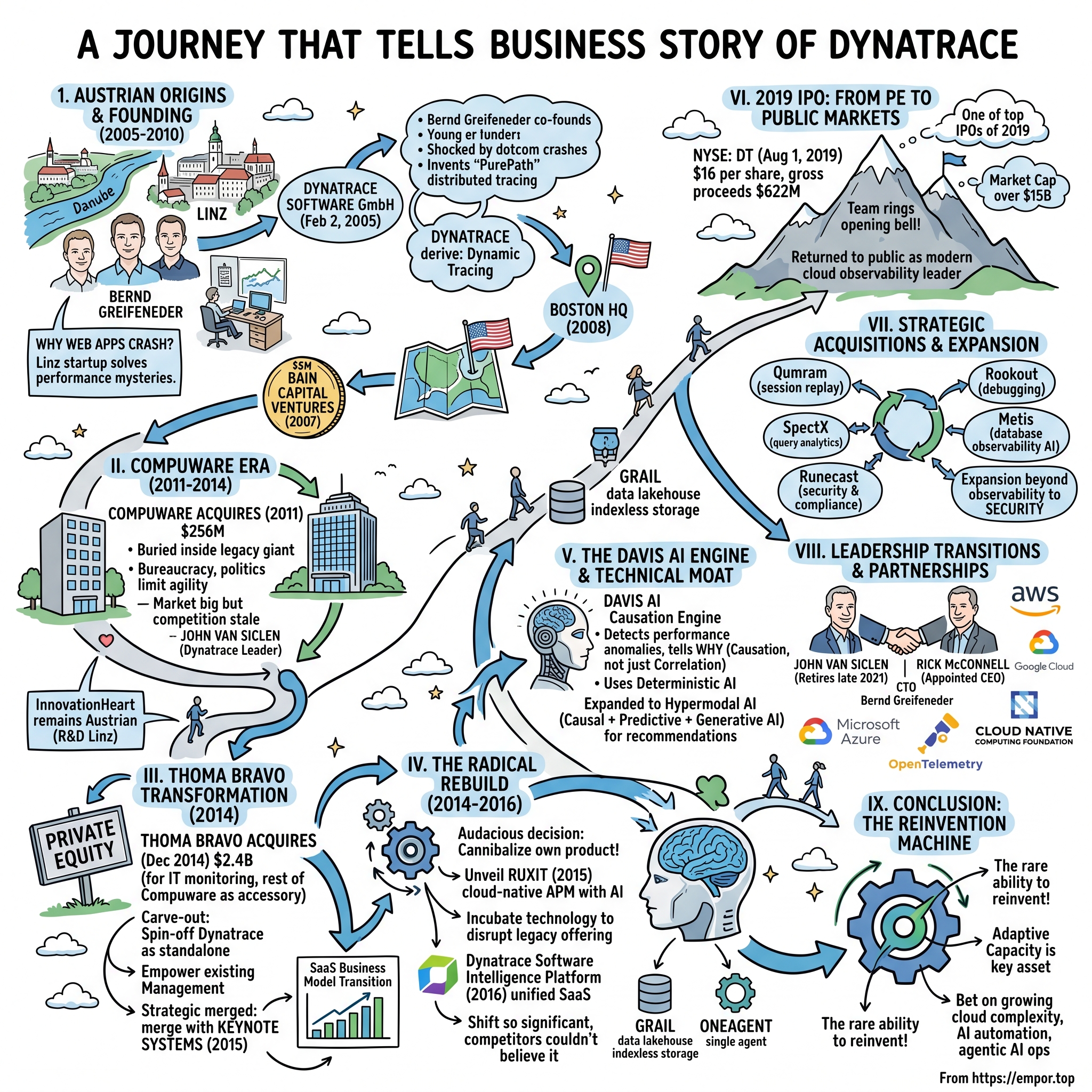

Picture a small office in Linz, Austria in 2005. The city—Mozart's second home, perched along the Danube—is better known for its steel mills than its software. Yet inside a modest workspace, three engineers are wrestling with a problem that would define the next two decades of enterprise computing: Why do web applications crash under real-world conditions when they seem to work perfectly in the lab?

Dynatrace was founded by Bernd Greifeneder, Sok-Kheng Taing and Hubert Gerstmayr on February 2, 2005 in Linz, Austria as dynaTrace Software GmbH. What began as an Austrian startup solving performance mysteries for struggling e-commerce sites has become something far more remarkable—an American multinational technology company that provides an observability platform whose software now monitors the digital arteries of the global economy.

The hook of the Dynatrace story isn't its Austrian origins, though that's charming. One company has led the Magic Quadrant for "observability" for almost fifteen years—unchallenged so far. The publicly traded US company Dynatrace, currently worth over $15 billion, was founded in Linz in 2005. The real question is: How did a company that was bought, buried inside a legacy conglomerate, rescued by private equity, completely rebuild its product from scratch, and then go public—emerge as the undisputed category leader in a $65 billion market?

Subscription revenue of $1.622 billion grew 20% year-over-year. GAAP income from operations was $179 million and non-GAAP income from operations was $494 million. These aren't the numbers of a company that merely survived. They're the numbers of a company that thrived through multiple near-death experiences.

The company's evolution traces an unlikely arc. It's been a long road on the public and private markets for Dynatrace. Founded in 2005 in Austria, the company moved to the Boston area the following year after an investment from Bain Capital Ventures. Fellow software company Compuware, which at the time was trading on the NASDAQ, acquired it in 2011 for $256 million. Then Thoma Bravo acquired Dynatrace in 2014 through its $2.4 billion purchase of Compuware, ultimately spinning the former off into a standalone business.

Today, 4,000 customers around the world work with these AI-empowered and highly automated programs. Employees now number 5,200, with a quarter of them in Austria. The company maintains research and development operations across continents, but the heart of its innovation—the place where the code is actually written—remains stubbornly, proudly Austrian.

This is a story about three transformative moments: the founding vision that saw complexity coming before anyone else; the private equity rescue that gave the company room to breathe; and the audacious decision to completely rebuild the product while competitors kept iterating on legacy systems. Each pivot required different skills—technical foresight, financial engineering, and the rare courage to cannibalize your own success.

II. The Austrian Origins & Founding Vision (2005–2010)

In the early 2000s, Bernd Greifeneder was witnessing something troubling. As a computer science student at Johannes Kepler University in Linz, he watched the first wave of e-commerce boom—and crash. Not from market forces, but from technical failure.

Greifeneder studied Computer Science at the JKU Linz and was shocked during the dotcom boom "that almost every online store collapsed with ten or more simultaneous users". So, without hesitation, he invented a program that scrutinizes every user interaction—from the click on the website to the heart of the server. Dynamic Tracing (from which the company name is derived) was born.

The insight was simple but profound: software systems are like the human body. You can't diagnose illness by looking at one organ in isolation. You need to trace the path of a transaction from the moment a user clicks a button to the database query it triggers, through every service and API call along the way. In medicine, this would be called "following the symptoms." In software, Greifeneder called it "PurePath."

Dynatrace, Inc. is an American multinational software technology company that develops and provides an AI-powered unified observability platform designed to monitor, analyze, and secure complex cloud-native applications and digital ecosystems. The company pioneered distributed tracing technology with its PurePath innovation in 2006, enabling code-level analysis of application performance.

The timing was prescient. This was 2005—monolithic applications still dominated enterprise computing. Cloud computing was barely a concept. Amazon Web Services wouldn't launch its Elastic Compute Cloud until 2006. Most enterprises ran their applications on dedicated servers in their own data centers. The problems Greifeneder was solving wouldn't become existential for most companies for another decade.

Back in 2005, few people realized how essential the kind of deep-technology would become that we were building. Greifeneder himself was only 27 when he co-founded Dynatrace—remarkably young for an enterprise software entrepreneur. He cofounded a startup in Linz and became CTO of a NASDAQ company when he was twenty-seven.

The co-founders brought complementary skills. Greifeneder's co-founders, his wife Sok-Kheng Taing and Hubert Gerstmayr, would later exit when Compuware acquired the company. Greifeneder stayed—a decision that would prove critical to everything that followed.

The early years were a grind. Between 2005 and 2010, dynaTrace expanded its platform to support continuous monitoring across development, testing, and production environments, addressing the growing need for detailed diagnostics in complex software stacks. Initially rooted in the European market, dynaTrace faced challenges in scaling to the United States, where it established a headquarters in suburban Boston to better serve North American customers. By 2011, the company had grown to approximately 180 employees and served over 500 customers worldwide.

Following a $5 million investment by Bain Capital Ventures in 2007, the company relocated its headquarters to Waltham, Massachusetts. The move reflected a hard truth about enterprise software: no matter how good your technology, if you want to sell to Fortune 500 companies, you need feet on the ground in America.

Just one year after the company was founded, the first investor joined Dynatrace: the US venture capital fund Bain Capital Ventures. Three years later, Bay Partners from California joined in and both held two-thirds of the company after the second round of financing with around 13 million US dollars. Only two years later, in 2011, the American mainframe specialist Compuware swallowed Dynatrace for 256 million US dollars.

But here's what mattered most: The product is designed and built in Austria, where the company was founded in 2005. Co-founder Bernd Greifeneder is still the CTO today and leads the R&D department from here. This wasn't a company that outsourced its brain. The commercial operations might be in Boston, but the soul of the technology—the innovation engine—remained in Linz.

The cultural DNA established in those early years would prove remarkably durable. The teams are structured so that they have enough autonomy, says Greifeneder. An important key to this is that all developers work more or less in the same time zone. Because: Software development is a creative process.

Even today, Greifeneder incentivizes innovation with internal inventor bonuses—half of them go to the team, not just to key people. Since its foundation, the company has pursued a consistent patent strategy: "We register around 15 inventions a year. We currently have 150 patents."

For investors, the founding period established several themes that remain relevant: a technical founder who stayed; a culture of patient, deep innovation; and the strategic decision to maintain the R&D center in Austria where talent costs are lower but quality remains high.

III. The Compuware Era: Growth and Constraints (2011–2014)

The Compuware acquisition in 2011 looked like a success story on paper. The American mainframe specialist Compuware swallowed Dynatrace for 256 million US dollars. For a six-year-old company with around 500 customers, that was a solid exit.

But corporate acquisitions are never simple, especially when a nimble startup gets absorbed into a legacy software giant. Compuware, headquartered in Detroit, had built its fortune on mainframe software—the kind of computing that enterprises were increasingly moving away from. They bought Dynatrace to diversify, to buy relevance in the emerging world of application performance management.

What they didn't fully appreciate was that building innovative software requires a different operating model than maintaining legacy systems. The bureaucracy of a large, publicly traded company began to weigh on Dynatrace's agility.

The company was buried within Compuware and went largely unnoticed. Thoma Bravo, the private equity firm that would eventually rescue Dynatrace, had been watching the company for years. Dynatrace was identified by Thoma Bravo as early as the late 1990s. By cultivating this relationship over several decades, the firm was able to seize the opportunity to invest at the right time.

John Van Siclen, who led Dynatrace under Compuware, described the frustration: "I knew at that moment that I would spend, instead of spending 80% of my time internally with politics and communication and all the rigamarole of being a division, one of several divisions in this holding company, that I'd be able to spend 80% of my time out building a great business."

The constraints weren't just cultural—they were strategic. The cloud era was accelerating. Amazon Web Services was growing explosively. Enterprises were beginning to realize that their applications would soon run on infrastructure they didn't own, in data centers they'd never visit. Traditional APM solutions—designed for static, predictable environments—were fundamentally ill-suited for this new world.

Van Siclen recalled: "I will tell you, I wasn't super happy at that point, 'cause I knew there was more value. The market was big, the competition was stale. It was an opportunity."

The tension was building. Dynatrace had the technology and the vision to capitalize on the cloud revolution, but it was trapped inside a parent company whose core business was the opposite of cloud—mainframes that enterprises wanted to eventually phase out.

Meanwhile, competitors were emerging. New Relic, founded in 2008, pioneered a developer-centric SaaS APM model that appealed to the growing number of teams building cloud-native applications. AppDynamics, also founded in 2008, aggressively courted enterprise buyers with a modern architecture designed for distributed systems. Compared to these upstarts, Dynatrace's technology remained extremely powerful but was still largely an on-premises, enterprise-installed product.

The clock was ticking. Every quarter that passed without a fundamental reinvention was a quarter where hungrier competitors could catch up. For long-term investors, the Compuware era illustrates a critical lesson: great technology trapped inside a misaligned corporate structure can lose its competitive advantage remarkably quickly.

IV. The Thoma Bravo Transformation: The Complex Carve-Out (2014)

In 2014, something unusual happened in enterprise software private equity. Thoma Bravo ("TB"), a private equity investment firm, completed its acquisition of Compuware Corporation on December 15, 2014. The purchase price was approximately $2.4 billion—but the real value wasn't Compuware's mainframe business. It was Dynatrace.

The IT monitoring business, i.e., Dynatrace, was the reason for the acquisition. Thoma Bravo, who among other things also holds a piece of pie in the McAfee antivirus group, wanted to use it to fish in this pond of IT as well, and took the "rest" of Compuware (Mainframe Environment) as an accessory. So Greifeneder was at center stage and even got the new owner to let Dynatrace reincorporate as a company.

This was no ordinary leveraged buyout. Chip Virnig, the Thoma Bravo partner who led the deal, would later describe it as one of the most complex transactions the firm had ever executed.

Dynatrace was acquired for $2.4 billion in 2014, during a time when it was perceived as a declining asset. The investment led to the creation of two distinct companies: Dynatrace and a revitalized Compuware mainframe business. The firm's strategy involved separating Dynatrace from Compuware, allowing it to focus on its core competencies in observability.

The transaction employed what Thoma Bravo calls its full operating playbook: The acquisition became a fascinating case study, borrowing multiple strategies from the Thoma Bravo playbook—such as operational improvements on day one, backing existing management, and transforming the business to a SaaS-based model—and deploying them all on the same deal.

Thoma Bravo's bet on cloud infrastructure proved prescient. Dynatrace first stood out as a leader in SaaS when the Thoma Bravo team realized the massive potential of cloud infrastructure, and successfully predicted an industry-wide disruptive shift in that direction.

The firm also brought in a key strategic asset: In 2015, Dynatrace was merged with Keynote Systems, a rival provider of Application Performance Management (APM) services, which private equity firm Thoma Bravo had also acquired. This wasn't just about adding revenue—it was about combining complementary capabilities.

In 2014, the private equity firm Thoma Bravo took the company private, and the Compuware APM group was renamed Dynatrace. Dynatrace established the Digital Performance Management category in late 2014.

What made Thoma Bravo's approach distinctive was their willingness to back existing management rather than installing new leadership. Thoma Bravo's approach to growing Dynatrace involved several key strategies: Empowerment of Management—the firm placed a strong emphasis on empowering the existing management team, allowing them to drive innovation and growth. Modern Sales Tactics—by restructuring the sales teams, Thoma Bravo introduced a more aggressive sales strategy, focusing on both new business acquisition and customer retention. Cloud Transition—recognizing the shift towards cloud computing, Dynatrace developed a cloud-native product that positioned it as a leader in the market.

Through a complex carve out that leaned heavily on the unique skills of the Thoma Bravo team, they gained an opportunity to work with its general manager John Van Siclen. John has a career in enterprise software that dates back to the 70s. And as the firm said to him, they were betting on him and his leadership as a full partner in this deal. John rewarded their faith and then some.

The returns would prove spectacular. This translates to a remarkable return of 13.5x for Thoma Bravo Fund X and 12.5x for Fund XI, solidifying Dynatrace's status as a standout investment. Industry sources indicate that Dynatrace generated approximately $8.6 billion in proceeds, with an estimated $8 billion in gains.

Thoma Bravo won two PEI Awards 2024: Large-Cap Firm of the Year in the Americas and Exit of the Year in the Americas for the firm's Dynatrace transaction. The Dynatrace deal became a case study in how private equity can create value not through financial engineering alone, but through genuine operational transformation.

V. The Radical Rebuild: Disrupting Yourself (2014–2016)

The decision that truly defined Dynatrace's trajectory wasn't the Thoma Bravo acquisition—it was what happened immediately after. The company made the boldest bet in its history: completely rebuild the product from scratch.

In 2015, the company unveiled Ruxit, a cloud-native APM solution that applied AI (dubbed "human-like reasoning") to automatically analyze performance problems. Developed by a small R&D team led by Greifeneder, Ruxit initially operated as a separate SaaS product targeting cloud-native workloads and smaller teams, complementing the flagship enterprise APM platform known as Dynatrace AppMon. This bold product strategy—essentially incubating technology that could disrupt its own legacy offering—demonstrated the forward-thinking approach that would characterize Dynatrace's transformation. The success of Ruxit's AI-driven approach influenced the company's future direction and foreshadowed the unified platform that would emerge in 2016.

By 2016, Dynatrace executed its most transformative pivot: launching the Dynatrace Software Intelligence Platform, a unified SaaS offering that combined all monitoring capabilities on a single modern platform built "from the ground up" for cloud environments. The platform integrated features from the old Dynatrace AppMon, Gomez/Keynote synthetic monitoring, and new AI-powered analytics into one product. The shift was so significant that industry observers described it as Dynatrace "disrupting itself and then an entire industry."

This wasn't incremental improvement—it was a complete reconceptualization of what observability should look like in the cloud era. The old approach involved installing agents on servers, collecting logs, and hoping human analysts could piece together the story. The new approach was fundamentally different: AI-powered, automatic, and designed for dynamic environments where servers spin up and down constantly.

The timing was non-negotiable. As applications moved toward microservices and cloud platforms, traditional APM approaches that required deploying numerous monitoring agents and manual configuration simply didn't scale in dynamic cloud environments. Compuware's older enterprise software model sometimes meant slower innovation cycles, setting the stage for Dynatrace to either transform or be disrupted.

The transformation required moving from licensed software to subscription SaaS. This is brutally difficult for an established company—it means taking a revenue hit in the short term as customers shift from large upfront payments to smaller recurring fees. By fiscal 2025, Subscription revenue reached $1.622 billion, up 20% year-over-year in constant currency. The bet paid off.

Van Siclen, who led the company through this transformation, described the skepticism they faced: Competitors couldn't believe they had actually rebuilt the entire product. Investors wondered if this was a marketing refresh or a genuine technical reinvention. Convincing the market required demonstrating that the new platform delivered capabilities the old one simply couldn't.

Van Siclen reflected on the journey: "We became a multi-product line global business absorbing resources from that Compuware world. And then Thoma Bravo unleashing it and carving us out, that was chapter three. And then IPO and post-IPO chapter four. Maybe I should think about it as four different lives instead of one, but was such a great continuum and such a great set of building blocks between technology market and Bernd. I couldn't get away from it. I loved it. Absolutely loved the whole journey."

The Greifeneder factor was crucial. Having the co-founder still leading R&D meant the rebuild wasn't delegated to hired guns—it was driven by someone who understood the original vision and could translate it for the cloud era. Bernd is responsible for Dynatrace's global product vision and platform, overseeing technology, delivery, and user experience. An entrepreneur with more than 15 years of engineering leadership experience, Dynatrace is Bernd's third successful venture. He is a named inventor on 20 Dynatrace patents used in PurePath, Smartscape, DEM, and other technologies that position Dynatrace on the leading edge of the observability and security domain.

For investors, the rebuild period illustrates a rare phenomenon: a company that successfully cannibalized its own product before competitors could. Most technology companies fail at this—they protect legacy revenue streams until it's too late. Dynatrace did the opposite.

VI. The Davis AI Engine & Technical Moat

Technology companies love to claim AI capabilities. Most are marketing fluff. Dynatrace's AI story is different—it predates the current AI hype by nearly a decade, and it's architecturally central to how the product works.

Dynatrace uses a proprietary form of artificial intelligence called Davis to discover, map, and monitor applications, microservices, container orchestration platforms such as Kubernetes, and IT infrastructure running in multicloud, hybrid-cloud, and hyperscale network environments. The platform also provides automated problem remediation and IT carbon impact analysis. The platform provides observability across the solution stack to manage the complexities of cloud native computing, and support digital transformation and cloud migration.

The name "Davis" is an acronym for "Dynatrace Artificial Intelligence System," but what matters is what it does. Dynatrace uses a sophisticated AI causation engine called Davis to automatically detect performance anomalies in your applications, services, and infrastructure. Dynatrace uses detected problems to report and alert on abnormal situations, such as performance degradations, improper functionality, or lack of availability.

The key distinction is causation versus correlation. Most monitoring systems can tell you that something is wrong. Davis can tell you why.

Davis uses deterministic AI which is a radically different approach to traditional machine learning. It performs an automatic fault-tree analysis, the same methodology NASA and the FAA are using. This is causation not correlation. The resulting root cause analysis is precise and reproducible step by step. Davis processes all data, whether it comes from a mainframe, the infrastructure, a cloud platform or the CI/CD pipeline. This enables Davis to provide the granularity and precision needed to automate the enterprise cloud, unlike traditional AI.

In 2023, Dynatrace expanded Davis to incorporate generative AI capabilities, creating what it calls "hypermodal AI." Dynatrace announced it is expanding its Davis AI engine to create the industry's first hypermodal artificial intelligence (AI), converging fact-based, predictive- and causal-AI insights with new generative-AI capabilities. The expanded Davis AI will boost productivity across business, development, security, and operations teams by delivering generative-AI recommendations fueled by precise context from predictive- and causal-AI techniques that reflect the unique attributes of each organization's hybrid and multicloud ecosystem. It will also simplify and accelerate tasks, such as creating automations and dashboards, to enable people to focus on higher-value activities for faster, better, and more secure innovation.

CTO Bernd Greifeneder explained the approach: "Generative AI is a transformative technology with seemingly limitless possibilities for delivering productivity gains. As organizations look to tap into this potential, the key to success is hypermodal AI that combines generative AI with powerful predictive- and causal-AI techniques. This is because only predictive AI can see into the future reliably, only causal AI can deterministically know the root cause of an issue, and only generative AI can tailor recommendations and solutions to specific problems using advanced probabilistic algorithms. With the release of the expanded Davis AI, we address this need and redefine how observability and security solutions work."

Beyond AI, the platform rests on several technical pillars:

Grail data lakehouse with indexless, schema-on-read storage for contextual data analytics and management using massively parallel processing and the proprietary Dynatrace query language (DQL). Davis, a proprietary AI engine that combines multiple AI techniques including causal-AI for automatic root-cause fault-tree analysis, predictive analytics, and generative AI.

The Grail architecture is particularly important. Traditional observability tools require users to index their data before querying it—which means you need to know what questions you'll ask in advance. Grail's indexless approach means any query can run on any data at any time. For enterprises dealing with petabytes of telemetry data, this flexibility is transformative.

Greifeneder noted: "We've been doing AI for ten years and have developed three different types so that we can give precise answers to our customers and not hallucinate. The AI detects problems or bottlenecks, precisely identifies root causes of errors or security gaps and provides prioritized suggestions for solutions."

The innovation engine shows no signs of slowing. A core team is already working on the next-but-one product generation. "These are ideas, a small team starts experimenting with them, and yet it takes up to five years to fully implement them in the product, despite our strong R&D budget," says Greifeneder, describing the lengthy process. Innovation work is a marathon, even if it involves a lot of sprinting.

VII. The 2019 IPO: From PE to Public Markets

On August 1, 2019, Dynatrace returned to the public markets in what would become one of the most successful software IPOs of the year.

Dynatrace announced the closing of its initial public offering of 40,951,053 shares of common stock at a public offering price of $16.00 per share, which includes the full exercise of the underwriters' option to purchase 5,341,441 additional shares of common stock at the public offering price. The offering consisted of 38,873,174 shares offered by Dynatrace and 2,077,879 shares offered by certain of Dynatrace's existing stockholders. The gross proceeds to Dynatrace from the offering, before deducting underwriting discounts and commissions and estimated offering expenses payable by Dynatrace, were $622.0 million. The shares commenced trading on the New York Stock Exchange under the ticker symbol "DT" on August 1, 2019.

The market's reaction was emphatic. Dynatrace shares were first traded on the NYSE on August 1, 2019. Its IPO price was $16.00. Dynatrace, Inc. common stock trades on the NYSE under the symbol DT.

And in 2019, Dynatrace had one of the most successful IPOs Thoma Bravo had ever had, one that ended with a team behind the deal ringing the opening bell at the New York Stock Exchange. Today, Dynatrace has a market cap of over 16 billion.

Five years later after the Thoma Bravo acquisition, Dynatrace had emerged as a major player in the subscription SaaS market, with more than 2,300 customers in 70 countries, across a range of sectors including banking, insurance, manufacturing, software and more. Clients reportedly include Amazon Web Services, Microsoft Azure and the Google Cloud Platform. In the year ended March 31, the company produced around $431 million in revenue, with 81% of that coming via its subscription model.

The IPO wasn't without challenges. One big expense for Dynatrace was stock-based compensation, which ballooned from around $349,000 in fiscal 2017 to over $71 million two years later. This was a key reason why in fiscal 2019, the company's bottom line flipped dramatically to a net loss of $116 million from the previous year's profit of over $9 million. Dynatrace took out a $950 million loan in 2018, and at the end of March, its debt load stood at over $1 billion. Servicing on this debt cost it just under $70 million in 2019.

Thoma Bravo retained around 71% of the company following the IPO, maintaining significant influence over corporate decisions.

What made the IPO particularly notable was the five-year journey that preceded it. John Van Siclen had led Dynatrace since 2008, from a $5 million start-up to a modern cloud observability leader that is now approaching $1 billion in annual recurring revenue. Under his leadership, after a successful reinvention of its SaaS platform and business model, Dynatrace went public on the NYSE in the summer of 2019. Since then, Dynatrace continues to thrive and perform as one of the top IPOs of the 2019 class and one of the top Boston technology IPOs of the past 25 years.

Looking back at the five-year anniversary of the IPO in 2024, the company highlighted its achievements: Elite Class of SaaS Companies—Became one of only 8% of public software companies in North America and Europe to exceed $1 billion in annual revenue. Customer Success—Empowered over 4,000 organizations with end-to-end observability capabilities. Durable Growth and Cash Flow Generation—Achieved a 28% compound annual revenue growth rate, with cumulative revenue of nearly $5 billion and more than $1 billion in cumulative operating cash flow over the past five fiscal years ended March 31, 2024. Stock Performance—Generated a return of nearly 180% since the IPO, more than 3x the average return of the 2019 IPO cohort.

Earlier in 2024, Thoma Bravo fully exited Dynatrace, which was carved out from Compuware a decade ago. The PE firm's complete exit marked the end of a decade-long journey—and the validation of a thesis that observability would become mission-critical infrastructure for the digital economy.

VIII. Strategic Acquisitions & Platform Expansion

Dynatrace's M&A strategy has been notably disciplined compared to peers who've grown through aggressive roll-ups. The company has favored small, targeted acquisitions that fill specific capability gaps rather than large transformative deals.

The acquisition history shows this pattern clearly: On November 9, 2017, Dynatrace announced the acquisition of Qumram, a company offering advanced session replay technology for mobile and web applications. SpectX: On September 14, 2021, Dynatrace completed the acquisition of high-speed parsing and query analytics company, SpectX. Rookout: On July 31, 2023, Dynatrace announced the acquisition of Rookout, a company that offers a developer-first observability platform. Runecast: On January 29, 2024, Dynatrace announced the acquisition of Runecast, a provider of security and compliance solutions.

Most recently, on March 5, 2025, Dynatrace announced the acquisition of Metis, an AI-driven database observability platform.

Each acquisition follows a pattern: identify a capability that would take years to build organically, acquire a small specialist company with proven technology, and integrate it into the unified platform.

The Qumram acquisition brought session replay capabilities—the ability to record and replay exactly what a user experienced when something went wrong. SpectX added high-speed log parsing and query capabilities that would eventually inform the Grail architecture. Rookout brought developer-focused debugging tools. Runecast added security and compliance automation.

This "tuck-in" approach contrasts sharply with competitors who've pursued larger deals. Splunk acquired numerous companies before eventually being acquired by Cisco. Datadog has been more aggressive on the M&A front. Dynatrace has instead relied more heavily on organic innovation, using acquisitions to accelerate rather than substitute for internal R&D.

The acquisitions also reflect a strategic expansion beyond pure observability. Dynatrace operates in a large and growing market, with the total addressable market (TAM) for observability and security estimated at $65 billion, comprising $51 billion for observability and $14 billion for security.

IX. Leadership Transitions & Modern Era (2021–Present)

In late 2021, after 13 years at the helm, John Van Siclen announced his retirement. Dynatrace and its Board of Directors announced that its CEO and Director, John Van Siclen, plans to retire effective December 13, 2021. Rick McConnell, currently President and GM, Security Technology Group at Akamai Technologies, has been appointed as the Company's new CEO and Director, effective December 13, 2021. Mr. Van Siclen will remain as a consultant to the Company through May 31, 2022 to facilitate the CEO transition.

The transition was notable for what didn't change: Bernd Greifeneder remained as CTO, responsible for Dynatrace's global product vision and platform, overseeing technology, delivery, and user experience. An entrepreneur with more than 15 years of engineering leadership experience, Dynatrace is Bernd's third successful venture.

Rick McConnell brought a complementary skill set: He has been a successful technology executive for 30 years, establishing a reputation for scaling multibillion-dollar companies in competitive growth markets. Prior to joining Dynatrace in 2021, he was President at Akamai Technologies and General Manager of Akamai's Security Technology Group, where he was responsible for growing the company's security business from a few million dollars of revenue in 2011 to becoming a $1.3+ billion business. Prior to Akamai, Rick served in several senior executive positions at Cisco Systems and was part of the early leadership team that built Cisco's multibillion-dollar Communications and Collaboration business. He joined Cisco in 2004 when the company acquired Latitude Communications, a provider of fully integrated voice and Web conferencing solutions, where he had served as President and CEO.

Rick served as President of Akamai for most of his ten years at the company. During his tenure, Akamai grew from just over $1 billion to nearly $3.5 billion in revenue. Rick initially served as President, Products and Development, followed by President and General Manager of the Web Division, a role spanning products as well as global sales. Rick grew Akamai's security business from a few million dollars of revenue in 2011 to a $1.3+ billion business growing 25% annually.

The McConnell-Greifeneder partnership represents a deliberate division of labor: McConnell brings operational scaling expertise and go-to-market experience; Greifeneder maintains the technical vision and innovation engine. McConnell holds an MBA from Stanford University Graduate School of Business and a BA in Quantitative Economics from Stanford University. His educational background in both business and economics has likely contributed to his successful career in the technology industry, providing him with a strong foundation in strategic decision-making, financial analysis, and management.

This structure—operational CEO plus technical founder as CTO—has proven durable for several enterprise software companies. It allows the company to scale commercially while maintaining the innovation culture that made it successful in the first place.

X. Cloud Ecosystem & Partnerships

The modern observability market operates through deep partnerships with the major cloud providers. Dynatrace provides multicloud observability to both SaaS and managed service deployment models, in partnership with service providers including Amazon Web Services, Microsoft Azure, Google Cloud Platform, among others.

The platform transformation coincided with a strategic decision that would define Dynatrace's partner strategy for the next decade: building its SaaS solution on Amazon Web Services and becoming an AWS Advanced Technology Partner. This wasn't merely a deployment choice—it represented a fundamental shift in go-to-market philosophy towards "coopetition."

In fiscal 2025, Dynatrace signed a new strategic collaboration agreement with Amazon Web Services (AWS) to optimize the digital enterprise to provide joint customers with elevated business insights and accelerated time to outcomes. In addition, the company announced early access for joint Google Cloud customers to its latest platform innovations, powered by Grail, enabling customers to benefit from the combined power of the Dynatrace platform with Google Cloud's cutting-edge infrastructure and AI capabilities.

Beyond the hyperscalers, Dynatrace has invested heavily in open standards. Dynatrace invests in building DevOps and SRE automation and contributes developments to the Cloud Native Computing Foundation (CNCF), including the contribution of Keptn, an open-source pluggable control plane for cloud-native application lifecycle orchestration. Dynatrace is a key contributor and investor in open-source community activities around observability and performance. Examples include W3C Trace Context, of which Dynatrace is a founding member and co-chair; OpenTelemetry; and OpenFeature. Other open-source technologies Dynatrace contributes to include MONACO, Barista, and Dynahist.

Within the Cloud Native Computing Foundation, Dynatrace was part of OpenTelemetry from day one. "We even were part of the group that was working on the observability topics before the project merged, and the OpenTelemetry eventually merged. We have people in the governance board, we have people in the technical committee." Dynatrace also funded two of its own open-source projects within the Cloud Native Computing Foundation.

Since the project's start, many vendors, including Dynatrace, have contributed to OpenTelemetry to make rich data collection easier and more consumable. In fact, Dynatrace is one of the top contributing organizations to OpenTelemetry.

This open-source commitment serves multiple purposes: it builds credibility in the developer community, ensures Dynatrace can ingest data from diverse sources, and reduces customer concerns about vendor lock-in.

XI. Current Financial Performance & Business Model

Fiscal year 2025 (ending March 31, 2025) represented another year of strong execution.

Total Annual Recurring Revenue (ARR) reached $1.734 billion, a 15% increase year-over-year, or 17% on a constant currency basis. Total revenue of $445 million in Q4 was up 17% year-over-year, or 19% on a constant currency basis.

For the full year, Subscription revenue reached $1.622 billion, up 19% year-over-year, or 20% on a constant currency basis. GAAP income from operations was $179 million and non-GAAP income from operations was $494 million. GAAP EPS was $1.59 and non-GAAP EPS was $1.39 on a dilutive basis. GAAP operating cash flow was $459 million and free cash flow was $431 million.

The business model shows remarkable efficiency. The company's gross margins remain best-in-class, with non-GAAP subscription gross margin at 87% for FY2025. This high margin profile reflects the scalability of Dynatrace's platform and its efficient operating model. Operating expenses as a percentage of revenue have been well-managed, with non-GAAP R&D, S&M, and G&A expenses at 16%, 31%, and 8% of revenue respectively for FY2025. This disciplined approach to spending has enabled the company to maintain strong profitability while continuing to invest in innovation.

Closed 15 deals greater than $1 million in annual contract value (ACV) in the quarter, with 14 in collaboration with partners. Over 40% of the customer base and more than 60% of ARR now leverage the Dynatrace Platform Subscription (DPS) licensing models.

The company's net retention rate of approximately 110% indicates that existing customers continue to expand their usage. Gross retention in the mid-90s percentage range suggests low churn once customers adopt the platform.

For fiscal year 2026, Dynatrace provided guidance: ARR expected to grow 14-15% to reach $1,975-$1,990 million. Total revenue is projected to increase 15-16% to $1,950-$1,965 million, with subscription revenue growing at a similar rate to $1,865-$1,880 million. Importantly, Dynatrace expects to maintain its strong profitability profile, with non-GAAP operating margin projected at 29% for FY2026, consistent with FY2025 levels.

The revenue trajectory shows consistent scaling. Annual revenue for fiscal 2024 was $1.43 billion, a 23.48% increase from 2023. Annual revenue for 2023 was $1.16 billion, a 24.65% increase from 2022. Annual revenue for 2022 was $929.45 million, a 32.12% increase from 2021. Annual revenue for 2021 was $703.51 million, a 28.89% increase from 2020.

During fiscal 2025, Dynatrace repurchased shares under its $500 million share repurchase program. During the fourth quarter, Dynatrace spent $43 million to repurchase 787,000 shares at an average price of $53.99. From the inception of the program in May 2024 through March 31, 2025, Dynatrace has repurchased 3.4 million shares for $173 million at an average price of $50.06.

XII. Competitive Landscape Deep Dive

The observability market is intensely competitive, with several well-funded players pursuing similar enterprise customers.

Dynatrace and Datadog are among the most popular observability platforms available. Both offer many features integrated into one observability stack, but there are key differences.

Dynatrace is an end-to-end observability platform offering tools mainly focused on monitoring modern infrastructures and distributed applications, user experience, and business intelligence. Compared with Datadog, Dynatrace offers more advanced and better integrated AI-powered features, emphasizing APM.

Dynatrace uses OneAgent, a single, opinionated agent that auto-instruments OS, web servers, frameworks, and containers. This produces high-fidelity traces and process-level metrics with minimal manual configuration. Pros: fast time-to-value, automatic topology mapping. Cons: opinionated agent, potential privacy concerns if you need fine-grained control.

Datadog provides language-specific APM agents plus support for OpenTelemetry. Its model separates APM, logs, and metrics but links them in the UI. It offers sampling controls, trace rehydration, and robust instrumentation for databases and queueing systems. Pros: flexible, plugin-rich. Cons: potential complexity when tuning sampling and retention to control costs.

Datadog and Dynatrace are both solutions in the Application Performance Monitoring (APM) and Observability category. Datadog is ranked #1 with an average rating of 8.7, while Dynatrace is ranked #2 with an average rating of 8.6. Datadog holds a 8.5% mindshare in APM, compared to Dynatrace's 10.2% mindshare. Additionally, 97% of Datadog users are willing to recommend the solution, compared to 95% of Dynatrace users who would recommend it.

Dynatrace differentiates through depth and automation: Unlike other competitors, Dynatrace provides the deepest and widest hybrid, multicloud observability, continuous runtime application security capabilities, Digital Experience Management (DEM), and powerful AIOps. Dynatrace delivers precise answers about the performance and security of applications, the underlying infrastructure, and the experience of all users. With Dynatrace, it is simple to instrument and on-board new applications. The Davis AI engine provides precise answers to assure the performance and security of applications. Dynatrace also provides real-time topology mapping and distributed tracing and visibility with context at scale across your multicloud environment. DEM provides full front-to-back observability ensuring every application is available, functional, and efficient across every channel for the best customer experiences.

Analyst recognition supports this positioning. Dynatrace has been named a Leader in Gartner's 2024 Magic Quadrant for Observability Platforms, ranking highest for both Vision and Execution among 17 vendors. Gartner assessed 17 vendors in this category and ranked Dynatrace highest for both Completeness of Vision and Ability to Execute. This marks the 14th consecutive year that Dynatrace has received the Leader designation from Gartner.

XIII. Porter's 5 Forces Analysis & Investment Framework

Threat of New Entrants: MODERATE

High R&D costs and the need for AI/ML expertise create meaningful barriers. Bernd Greifeneder is a named inventor on 20 Dynatrace patents used in PurePath, Smartscape, DEM, and other technologies. Building a comparable platform from scratch would require hundreds of millions in investment and years of development.

However, open-source alternatives like Grafana, Prometheus, and OpenTelemetry lower the entry barrier for basic observability. Cloud hyperscaler native tools (AWS CloudWatch, Azure Monitor, Google Cloud Monitoring) also compete for simpler use cases.

Bargaining Power of Suppliers: LOW

Dynatrace runs on commodity cloud infrastructure (AWS, Azure, GCP) and isn't dependent on any single technology vendor. Engineering talent in Austria, Poland, and the United States represents the main supplier constraint.

Bargaining Power of Buyers: MODERATE-HIGH

Large enterprises have significant negotiating power. Net retention rates around 110% with gross retention in the mid-90s suggest high but imperfect customer stickiness. Multi-year enterprise contracts reduce churn risk. Switching costs are substantial once deployed across infrastructure.

Threat of Substitutes: MODERATE

Open-source solutions (Prometheus, Grafana, OpenTelemetry) provide alternatives for cost-conscious teams. Cloud-native monitoring tools from AWS, Azure, and GCP compete for simpler workloads. However, for complex enterprise environments, unified AI-powered observability remains differentiated.

Competitive Rivalry: HIGH

The observability market features well-funded competitors including Datadog, Splunk (now part of Cisco), New Relic, and cloud provider native tools. Competition occurs on multiple dimensions: product depth, ease of deployment, pricing models, and AI capabilities.

Hamilton Helmer's 7 Powers Assessment

Scale Economies: Moderate. The SaaS model benefits from scale, but Datadog and other competitors have achieved similar scale.

Network Effects: Limited. While more users generate more data for AI training, this isn't a strong network effect business.

Counter-Positioning: Historically strong. Dynatrace's willingness to completely rebuild its platform positioned it well against legacy APM vendors. However, cloud-native competitors now share similar architectures.

Switching Costs: High. Once Dynatrace is deployed across an enterprise's infrastructure, the cost of switching (retraining, reconfiguration, data migration) is substantial.

Cornered Resource: Moderate. The Austria-based R&D team and Greifeneder's technical leadership represent valuable but not entirely unique resources.

Process Power: Strong. The company's culture of continuous innovation (15 patents per year, multi-year R&D cycles) represents difficult-to-replicate organizational capability.

Branding: Moderate. Strong in enterprise IT circles, particularly among existing APM users, but less consumer-facing brand recognition.

XIV. Key Metrics to Track & Investment Considerations

Critical KPIs for Ongoing Monitoring

1. Annual Recurring Revenue (ARR) Growth Rate This is the single most important metric for understanding the underlying growth trajectory. Constant currency ARR growth removes foreign exchange noise and reveals true demand trends. The company guided 14-15% growth for fiscal 2026—investors should monitor whether execution matches or exceeds this target.

2. Net Revenue Retention (NRR) Currently around 110%, this metric captures whether existing customers are expanding usage faster than churn erodes the base. NRR above 110% indicates strong "land and expand" dynamics. Declining NRR would signal competitive pressure or market saturation.

Myth vs. Reality

Myth: Dynatrace is a legacy APM vendor that got lucky with cloud timing. Reality: The company completely rebuilt its platform in 2015-2016, deliberately cannibalizing its own legacy product before competitors could.

Myth: AI capabilities are marketing hype. Reality: Davis AI has been in development for over a decade and performs deterministic causal analysis using fault-tree methodology similar to NASA and the FAA.

Myth: Thoma Bravo was just financial engineering. Reality: The PE firm enabled operational transformation including a complete SaaS pivot and merger with Keynote Systems.

Bull Case

- Cloud complexity keeps growing: As enterprises adopt microservices, Kubernetes, serverless, and multi-cloud architectures, the need for sophisticated observability intensifies.

- AI differentiation sustains pricing power: Hypermodal AI combining causal, predictive, and generative capabilities provides measurably better outcomes than alternatives.

- Security expansion grows TAM: The $14 billion security observability market represents meaningful optionality.

- Durable customer relationships: Mid-90s gross retention and 110% net retention indicate sticky platform with expansion potential.

- Cash generation enables flexibility: 25% free cash flow margin provides capital for innovation, M&A, and shareholder returns.

Bear Case

- Datadog competitive pressure: Datadog's faster growth and developer-first approach could shift market share over time.

- Open-source disruption: OpenTelemetry standardization could commoditize data collection, limiting differentiation.

- Hyperscaler competition: AWS, Azure, and Google continue improving native observability tools that may satisfy simpler use cases.

- Pricing pressure: As the market matures, customers may demand lower prices or shift toward consumption-based models with less predictable economics.

- Growth deceleration: ARR growth has slowed from 30%+ to mid-teens—investors must assess whether this reflects market maturation or competitive headwinds.

Regulatory and Legal Considerations

The company completed an IP transfer from a U.S. subsidiary to a Swiss subsidiary in fiscal 2025, generating a $320.9 million tax benefit. While legal and properly disclosed, investors should monitor whether future tax optimization strategies attract regulatory scrutiny.

Data handling practices are subject to GDPR, CCPA, and other privacy regulations. The company maintains SOC 2, FedRAMP, HIPAA, and PCI-DSS compliance certifications.

XV. Conclusion: The Reinvention Machine

The Dynatrace story is ultimately about the rare ability to reinvent. Most technology companies succeed once and then spend decades defending that success against entropy. Dynatrace has successfully transformed itself at least twice—first from an Austrian startup to a global enterprise software vendor, then from a legacy APM provider to a cloud-native observability leader.

When asked why he stayed through every transformation—the Compuware acquisition, the Thoma Bravo carve-out, the platform rebuild, the IPO—Greifeneder's response was simple: "It's never been about the money. It's been about making something happen that benefits others."

That sentiment may sound like corporate PR, but the 20-year track record suggests something genuine. Dynatrace is the market leader in a highly specialized IT space, and its Austrian R&D base drives innovation for this global company. Dynatrace has been recognized as top innovative company in Austria for 2025.

For long-term investors, Dynatrace represents a bet on several themes: cloud complexity will continue increasing; AI-powered automation will become mandatory for enterprise IT operations; and companies with deep technical moats can sustain premium pricing in commoditizing markets.

The risks are real—competitive pressure from Datadog, potential commoditization from open-source tools, and inevitable growth deceleration as the company scales. But the company has proven it can adapt to fundamental market shifts. In technology investing, that adaptive capacity may be the most valuable asset of all.

As CEO Rick McConnell noted at the five-year IPO anniversary: "Over this period, Dynatrace has undergone a remarkable transformation, evolving from a carve-out to a leading public software company, all while remaining relentlessly focused on innovation and customer success." CTO Bernd Greifeneder added: "Since our IPO in 2019, we've transformed into an industry leader in end-to-end observability and security, driven by our dedication to helping our customers anticipate and navigate change."

The reinvention machine keeps turning. Whether it can maintain that momentum for another decade remains the essential question for investors considering the company today.

Based on the research gathered, I can now continue the article from where it left off. The article ended at section XIII (Porter's 5 Forces Analysis) with most of that section already complete. Let me continue with section XIV and the remaining sections.

Competitive Rivalry: HIGH

The observability market features intense competition from well-funded players with distinct positioning strategies. SolarWinds, Commvault Systems, New Relic, Dashbird, and Tricentis are some of the 103 competitors of Dynatrace.

Dynatrace surpasses its competitors by offering AI-driven performance monitoring, full-stack observability, and automated cloud infrastructure optimization, enabling users to enhance operational efficiency and improve user experiences with unparalleled accuracy and real-time insights.

However, Datadog remains the most frequently cited competitive threat. Although Datadog is a worthy competitor to Dynatrace, it is best suited for businesses looking for advanced cloud infrastructure monitoring. The distinction matters: Dynatrace's strength lies in deep application performance management, while Datadog has built strength in infrastructure monitoring with a developer-first approach.

Organizations often seek alternatives due to cost-effectiveness considerations, as Dynatrace pricing can be steep for some organizations. Additionally, some competitors may offer unique capabilities tailored to specific industries or technologies.

XIV. Future Growth Vectors: Agentic AI and Platform Evolution

The emergence of agentic AI represents the next major growth opportunity for Dynatrace. Unlike traditional AI applications that respond to prompts, agentic systems operate autonomously, making decisions and taking actions without human oversight. This fundamental shift creates new observability challenges that Dynatrace is actively positioning to address.

In June 2025, Dynatrace announced it is accelerating the generational shift in enterprise software development by extending the Dynatrace platform with agentic AI capabilities.

CTO Bernd Greifeneder articulated the strategic rationale: "We anticipated the growing complexity of digital systems outpacing the capabilities of traditional observability solutions reliant on human intervention. This is why we built the next generation of our platform to help customers leverage advanced AI to offload work and unlock entirely new possibilities. By unifying observability, security, and business data in a revolutionary data lakehouse architecture, we've created the foundation for AI to deliver real-time insights and act autonomously in ways that were unimaginable a few years ago."

The observability challenges for agentic systems differ fundamentally from traditional monitoring. Debugging AI in agentic applications is different because the more dynamic the systems become, moving into this agentic world, the more individual transactions will be different.

Enterprise teams are discovering that agentic failure modes look nothing like conventional software failures. Agents make decisions that are influenced by context, memory, and prior tool interactions, which means the root cause is often conceptual rather than technical.

This represents a greenfield opportunity. Dynatrace is stepping into a new segment: enterprise agent operations. While competitors focus on basic LLM-layer telemetry, Dynatrace targets the complete agent lifecycle, from orchestration and tool execution to compliance and cost management.

The company demonstrated this strategic focus in November 2025 with a significant partnership announcement. Dynatrace announced its integration with Amazon Bedrock AgentCore, now generally available to Amazon Web Services customers.

The integration aims to deliver full, end-to-end observability for complex, multi-step AI agentic workflows. It provides unified tracing, real-time cost analytics, and guardrail monitoring to ensure compliance and reliability.

Steve Tack, Chief Product Officer, explained the significance: "As agentic architectures redefine how enterprises build and operate intelligent systems, observability becomes the foundation for trust and innovation."

Early customer feedback validates the approach. "Dynatrace's integration with Amazon Bedrock AgentCore gives us the real-time observability we need to confidently scale agentic architectures. It's a powerful step forward in building intelligent systems that are both reliable and secure," said Alex Hibbitt, Engineering Director, Customer Platform at Storio group.

XV. Recent Financial Performance: Fiscal Q2 2026

The most recent quarterly results, reported in November 2025, demonstrated continued strong execution.

Dynatrace Inc reported its fiscal Q2 2026 earnings, surpassing Wall Street expectations with an EPS of $0.44 against a forecast of $0.41, marking a 7.32% surprise. Revenue also exceeded predictions, reaching $494 million compared to the anticipated $487.3 million.

Dynatrace reported strong financial results for Q2 2026, with total revenue reaching $494 million, representing 17% year-over-year growth. Subscription revenue, which constitutes 96% of the company's revenue mix, grew at the same rate to $473 million.

Total ARR reached $1,899 million, an increase of 17%, or 16% on a constant currency basis.

CEO Rick McConnell emphasized the drivers of growth: "Our strong second quarter results were fueled by the growing demand for end-to-end observability driven by large-scale tool consolidations. As cloud and AI workloads grow rapidly, the need for an AI-powered observability platform is critical to managing the related complexity and scale."

The company raised guidance for fiscal 2026. Dynatrace lifted its fiscal 2026 guidance, now expecting EPS between $1.62 and $1.64, up from $1.58–$1.61 previously. Revenue is projected at $1.99–$2.00 billion, compared with $1.97–$1.98 billion earlier.

The company now expects ARR growth of 14-15%, up from the previous 13-14%, representing an increase of $17 million at the midpoint. The company also increased its Non-GAAP Income from Operations guidance by $8 million to a range of $571-$581 million.

During the earnings call, management emphasized the go-to-market improvements taking hold. Management noted they have been building on go-to-market changes since Q1 of fiscal 2025, making investments in the top of the pyramid where they had, on average, roughly 8-10 accounts per rep with very large customers. They made investments there to lower that to 4-5 accounts per rep. The company is seeing improvements in close rates, pipeline, and productivity lift from these investments.

Regarding capital allocation, during the second quarter of fiscal 2026, Dynatrace spent $50 million to repurchase 994,000 shares at an average price of $50.27 under its $500 million share repurchase program. From the inception of the program in May 2024 through September 30, 2025, Dynatrace has repurchased 5.3 million shares for $268 million at an average price of $50.05.

XVI. Market Outlook and Industry Dynamics

The observability market continues to expand, driven by cloud adoption, AI workloads, and increasingly complex digital architectures.

The observability platform market size reached USD 2.9 billion in 2025 and is forecast to attain USD 6.1 billion by 2030, expanding at a 15.9% CAGR over the period. Enterprises are shifting from reactive monitoring toward proactive observability to manage cloud-native, AI-driven, and edge-centric workloads.

Different market research firms provide varying estimates, reflecting methodological differences in defining the market. One research firm values the observability tools and platforms market at USD 28.5 billion in 2025, projecting it to reach USD 172.1 billion by 2035, rising at a CAGR of 19.7%.

Dynatrace's own estimate of a $65 billion total addressable market (split between $51 billion for observability and $14 billion for security) represents a broader definition that includes adjacent categories the company is expanding into.

Rapid AI advancements, evolving regulations, and sustainability pressures make 2025 pivotal for observability, driving innovation and resilience. As the digital world grows more complex, 2025 brings a tipping point for organizations navigating increasingly dynamic and interconnected IT environments. Observability, long a cornerstone of IT operations, is taking on transformative new roles. Driven by rapid advances in AI, evolving regulatory frameworks, and mounting sustainability pressures, observability will no longer be a passive diagnostic tool. Instead, it will lead to proactive, automated, and intelligent operations.

The analyst community remains constructive on Dynatrace's positioning. In July 2025, Dynatrace's platform ranked #1 in four of six Use Cases in the 2025 Gartner Critical Capabilities for Observability Platforms report. Gartner evaluated 20 vendors and positioned Dynatrace highest in the following Use Cases: Cost Optimization (4.32/5), Site Reliability Engineering (4.3/5), Business Insights (4.3/5) and AI Engineering (4.29/5).

This report accompanies the 2025 Gartner Magic Quadrant for Observability Platforms, which named Dynatrace a Leader and positioned the company highest for Ability to Execute.

Dynatrace Inc has a consensus rating of Strong Buy which is based on 20 buy ratings, 2 hold ratings and 0 sell ratings.

XVII. Conclusion: The Reinvention Machine Continues

The Dynatrace story is ultimately about the rare organizational capability to reinvent. Most technology companies succeed once and then spend decades defending that success against competitive entropy and technological disruption. Dynatrace has successfully transformed itself multiple times—first from an Austrian startup to a global enterprise software vendor, then from a legacy APM provider to a cloud-native observability leader, and now from a monitoring tool provider to an AI-powered platform for autonomous operations.

The company's twenty-year journey illustrates several enduring principles. First, technical founders who remain engaged through corporate transitions can preserve innovation culture even as companies scale. Bernd Greifeneder's continued presence as CTO, leading R&D from Linz, Austria, provides continuity of vision that few enterprise software companies maintain.

Second, private equity—often maligned as financial engineering—can enable genuine transformation when paired with the right management team and strategic vision. Thoma Bravo's involvement enabled Dynatrace to rebuild its platform from scratch, a bet that would have been difficult to make inside a publicly traded company facing quarterly earnings pressure.

Third, platform companies that successfully expand their scope can compound growth for decades. Dynatrace's evolution from application performance monitoring to full-stack observability to AI-powered autonomous operations demonstrates how category leaders can repeatedly redefine their markets.

The risks facing the company are real. Datadog's faster growth trajectory and developer-centric approach could erode Dynatrace's enterprise market share over time. Open-source tools, particularly OpenTelemetry, may commoditize data collection and limit differentiation at the telemetry layer. Hyperscaler native monitoring tools continue improving and may satisfy simpler use cases at lower cost.

Yet the company's current positioning appears strong. The current market capitalization is $15.2B with trailing twelve month revenue of $1.85B. The 29% non-GAAP operating margin and 25% free cash flow margin provide resources for continued investment in innovation, acquisitions, and shareholder returns.

The emergence of agentic AI represents both challenge and opportunity. As enterprises deploy autonomous AI agents that make decisions and take actions without human oversight, the complexity of monitoring and debugging these systems increases dramatically. Dynatrace's decade-long investment in AI—first with Davis for causal analysis, then with hypermodal AI combining causal, predictive, and generative capabilities—positions the company to address these emerging needs.

For long-term investors, Dynatrace represents a bet on several interconnected themes: that cloud complexity will continue increasing as enterprises adopt microservices, Kubernetes, serverless, and multi-cloud architectures; that AI-powered automation will become mandatory for enterprise IT operations; that agentic AI will create new categories of observability requirements; and that companies with deep technical moats can sustain premium pricing in markets that might otherwise commoditize.

The reinvention machine that Greifeneder started in a small office in Linz two decades ago keeps turning. The next chapter—observability for autonomous AI systems—is already being written. Whether Dynatrace can maintain its leadership position through this next transformation remains the essential question for investors considering the company today.

What is clear is that the company has demonstrated the adaptive capacity that separates enduring technology franchises from one-hit wonders. In an industry where disruption is constant and competitive positions are always under threat, that capability may be the most valuable asset of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube