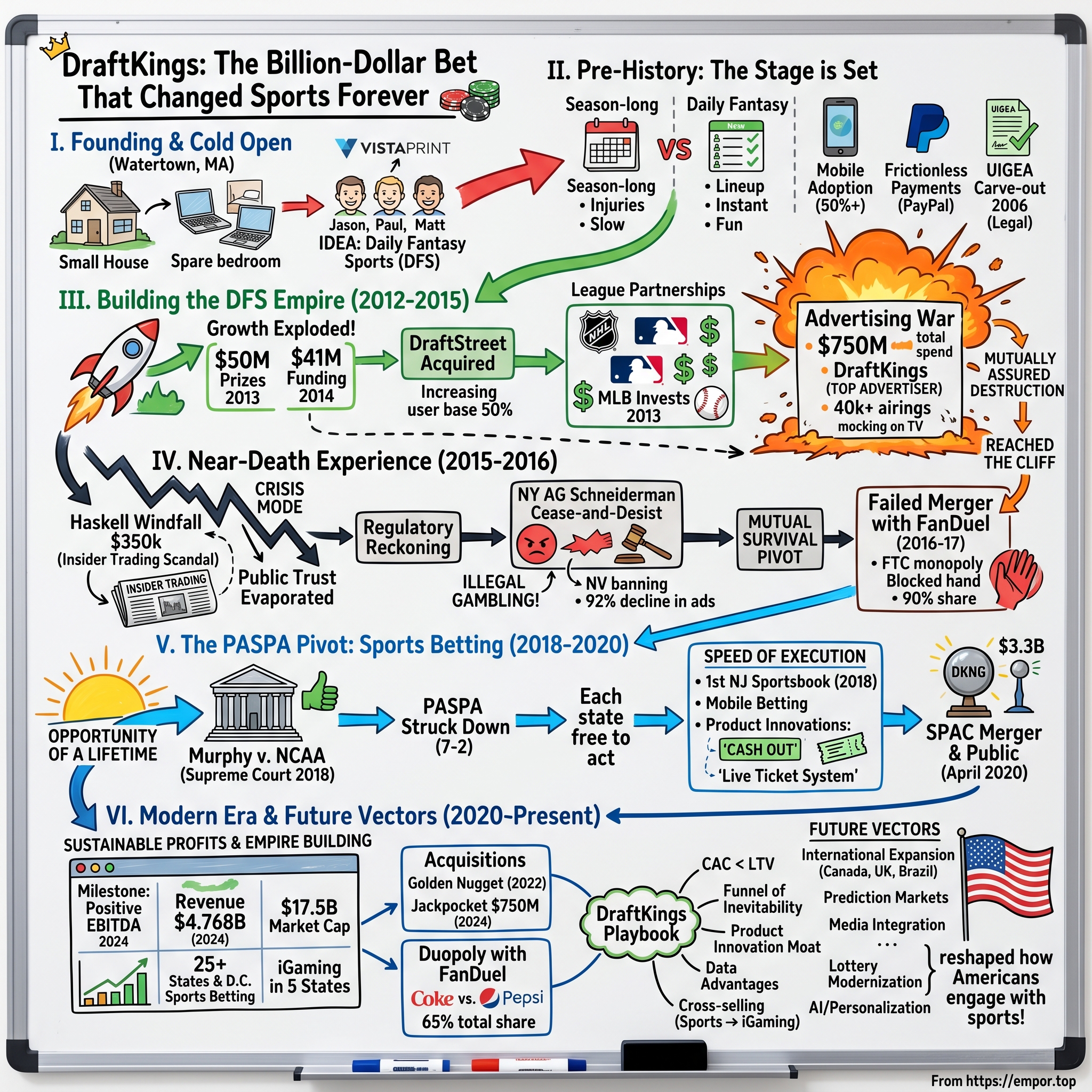

DraftKings: The Billion-Dollar Bet That Changed Sports Forever

I. Introduction & Cold Open

Picture this: September 2015. A Sunday afternoon in America. Turn on any TV, open any sports website, or flip through any magazine, and you couldn't escape them—DraftKings and FanDuel ads were everywhere. "Welcome to the big time," the commercials proclaimed, featuring regular guys who'd supposedly won millions playing daily fantasy sports. The two companies were burning through an astounding $750 million in combined advertising that year alone, carpet-bombing American sports fans with promises of instant riches.

This wasn't just aggressive marketing—it was corporate warfare at its most extreme. Two startups, locked in a battle so intense that industry insiders called it "mutually assured destruction." By October, the advertising blitz had become so overwhelming that ESPN's own personalities were openly mocking it on air. Within weeks, the entire industry would face an existential crisis that threatened to destroy both companies.

Yet from this near-death experience emerged something far more powerful. DraftKings, the scrappy Boston startup founded by three VistaPrint middle managers working out of a spare bedroom, would transform itself into a $17.5 billion sports betting powerhouse. When the company went public through a reverse merger in April 2020, valued at $3.3 billion, it marked not just a corporate milestone but a fundamental shift in how Americans engage with sports.

The central question isn't just how three corporate refugees with no gambling experience built one of the most valuable companies in sports entertainment. It's how they survived when everyone—regulators, competitors, even their own investors—thought they were finished. This is the story of perfect timing meeting relentless execution, of pivoting from fantasy sports to real-money betting at exactly the right moment, and of building a business model so powerful that it reshaped an entire industry.

What follows is a journey from that spare bedroom in Watertown, Massachusetts, to the commanding heights of American sports betting—a transformation that tells us as much about modern entrepreneurship as it does about our evolving relationship with sports and money.

II. The Pre-History: Setting the Stage

Before DraftKings revolutionized fantasy sports, millions of Americans were already hooked on a different version of the game. Season-long fantasy leagues had been around since the 1960s, when a group of Oakland Raiders fans created the first fantasy football league in a Manhattan hotel. By 2010, an estimated 32 million Americans were playing, managing virtual rosters over entire seasons, making trades, and competing for bragging rights—and sometimes money—with friends and coworkers.

But season-long fantasy had fundamental limitations. If you drafted poorly or suffered key injuries early, your season was essentially over by October. The commitment was substantial—months of lineup management, waiver wire monitoring, and trade negotiations. And perhaps most importantly for potential entrepreneurs, the business model was weak. Yahoo and ESPN dominated with free leagues, monetizing through ads rather than gameplay. The few companies charging fees struggled to differentiate or scale.

The three future DraftKings founders—Jason Robins, Paul Liberman, and Matt Kalish—were among these frustrated fantasy players. "We thought season-long fantasy was great," Robins would later recall. "But daily fantasy could be better." They weren't alone in this thinking, but they had something previous entrepreneurs lacked: perfect timing.

The regulatory landscape had shifted dramatically in 2006 with the Unlawful Internet Gambling Enforcement Act (UIGEA). While the law devastated online poker by making it illegal for financial institutions to process gambling transactions, it contained a crucial carve-out for fantasy sports. The law specifically exempted games where "all winning outcomes reflect the relative knowledge and skill of the participants and are determined predominantly by accumulated statistical results of the performance of individuals." This wasn't an accident—the NFL and other leagues had lobbied hard for the exception, seeing fantasy sports as fan engagement tools rather than gambling. Boston circa 2010-2012 was experiencing a renaissance in its startup ecosystem. Massachusetts entrepreneurs received more than $3 billion in funding in 2012 for 410 deals, accounting for more than 11 percent of the total investment capital distributed nationwide. Mayor Thomas Menino had just announced his vision for the waterfront Innovation District in early 2010, creating a physical hub that would attract startups, restaurants, and venture capital firms. Since 2010, the neighborhood attracted new businesses, with companies like Brightcove moving its headquarters to Boston's Innovation District in early 2012.

The ecosystem was particularly fertile for consumer-facing technology companies. MassChallenge, the global startup competition and accelerator, operated out of donated space in a high rise, symbolizing the collaborative spirit between established real estate players and emerging startups. Universities like MIT, Harvard, and Boston University provided not just talent but also legitimacy and connections. The city had everything an aspiring entrepreneur needed except one thing: patience for slow growth.

But why did timing work for daily fantasy sports specifically in the early 2010s when previous attempts had failed? Several factors converged perfectly. First, mobile adoption had reached critical mass—by 2012, over 50% of Americans owned smartphones, enabling real-time lineup management and instant deposits. Second, payment processing had become frictionless with companies like PayPal and emerging mobile payment solutions making micro-transactions viable. Third, and perhaps most crucially, the major sports leagues had shifted from viewing fantasy sports as a threat to embracing them as engagement tools.

Previous daily fantasy attempts in the mid-2000s had faced insurmountable challenges: clunky desktop-only interfaces, complex payment processing, and most importantly, active hostility from professional sports leagues who saw any form of gambling-adjacent activity as toxic to their brands. By 2012, that calculus had completely reversed. The leagues recognized that fantasy players watched more games, consumed more content, and spent more money on their products. The stage was perfectly set for someone to capitalize on this shift—and three friends from VistaPrint were about to seize the moment.

III. The Founding Story: From VistaPrint to Watertown

The conference room at Vistaprint's Waltham offices had seen better days. It was 2011, and Jason Robins, Paul Liberman, and Matt Kalish were ostensibly there to discuss marketing analytics for the online printing company. But their real agenda was different. They were plotting their escape.

"I had worked for almost a decade in corporate America, middle management jobs," Robins would later recount. "My two co-founders same. Matt and I worked at Capital One. Then all three of us worked together at a company that was called Vistaprint, now called Cimpress." The shared experience had bonded them, but it had also frustrated them. They were smart, ambitious guys watching from the sidelines as the startup revolution transformed Boston around them.

The timing had never been right before. "We always had this entrepreneurial pull but never had good timing," Robins explained. "I graduated college shortly after the bubble burst. When I was thinking about leaving Capital One, Matt and I discussed doing a start-up and it was about mid-2008 at that point. You can figure out how that went." The financial crisis had killed that dream before it started. But by 2011, with the economy recovering and venture capital flowing back into Boston, they sensed their moment had finally arrived.

There was just one problem. "The only thing is we didn't have an idea," Robins admitted. "We spent about six, 12 months just going out for drinks and dinner, batting around ideas." They considered everything—social networks, e-commerce plays, B2B software. Nothing clicked. They were three guys with complementary skills—Robins had the business acumen, Kalish the technical chops, and Liberman the operational expertise—but no mission.

Then came the breakthrough. "One day, Matt sat me down and said, 'Hey, I think I got it,' and he told me the basic idea of DraftKings." Kalish had been playing fantasy baseball obsessively, managing multiple season-long teams across different platforms. He'd noticed something: the most exciting part wasn't the months-long season but the daily roster decisions. What if you could compress that excitement into a single day? What if instead of being stuck with injured players or bad draft picks for months, you could start fresh every day?

The idea was elegantly simple: daily fantasy sports contests where users would pick new teams each day, competing for cash prizes based on that day's performance. It solved every pain point of traditional fantasy sports while potentially being far more lucrative. The UIGEA carve-out meant it was legal. The technology to build it existed. All they needed was the courage to quit their comfortable corporate jobs.

Kalish offered his spare bedroom in his Watertown, Massachusetts house as headquarters. The scene that followed would become part of DraftKings lore: three grown men hunched over laptops in a suburban bedroom, coding through the night. "We go there and work till about 1:00, 2:00 in the morning," Robins remembered. "Weekends, we'd wake up around 5:30, 6:00 and do the same thing, work all day."

The intensity was born of necessity. They were bootstrapping, living off savings, with no outside funding. Every day they delayed launch was a day competitors could beat them to market. They knew FanDuel already existed, having launched in 2009, but they believed they could build a better product. Where FanDuel had started with a complex, European-style interface reflecting its Scottish founders' sensibilities, DraftKings would be quintessentially American—simple, fast, and built for mobile from day one.

The technical architecture Kalish designed was remarkably sophisticated for a bedroom startup. Rather than just copying existing models, they built a proprietary scoring system, a real-time data pipeline for statistics, and most importantly, a matching algorithm that could pair users of similar skill levels—addressing one of fantasy sports' biggest problems: sharks feeding on minnows.

The company's first product was deliberately narrow: a one-on-one baseball competition, launched to coincide with Major League Baseball's opening day on April 5, 2012. Users could challenge friends or be matched with strangers, picking a lineup of MLB players for that day's games. Entry fees ranged from $1 to $500, with the winner taking all minus DraftKings' rake.

The launch was modest—just a few hundred users, mostly friends and family. But the engagement metrics were extraordinary. Users who tried the product came back the next day at rates above 40%. The average session time exceeded 30 minutes. These weren't just good numbers for a fantasy sports app; they were good numbers for any consumer product. The three friends in the Watertown bedroom had stumbled onto something special—they just didn't know yet how special it would become.

IV. Building the Daily Fantasy Empire (2012-2015)

The email landed in Jason Robins' inbox on a Tuesday morning in March 2013, and he had to read it three times to believe it was real. Major League Baseball wanted to invest in DraftKings. Not just partner with them, not just endorse them—actually put money into a one-year-old startup that was still operating out of a spare bedroom. In April 2013, Major League Baseball invested in DraftKings, becoming the first US professional sports league to invest in daily fantasy sports. The investment was not disclosed at the time. For a company that had launched just one year earlier with a simple baseball game, this was validation beyond their wildest dreams. MLB had reportedly held equity in DraftKings since 2013, marking a fundamental shift in how professional sports viewed fantasy gaming.

The investment transformed everything. Suddenly, DraftKings had credibility that money couldn't buy. They could walk into meetings with other leagues, with investors, with potential partners, and say: "MLB believes in us." The psychological impact on competitors was equally powerful—if America's pastime was backing DraftKings, who would bet against them?

Growth exploded. In February 2014, it was reported that the company awarded $50 million in prizes in 2013 to players in weekly fantasy football, daily fantasy baseball, daily fantasy basketball and daily fantasy hockey. The company also reported 50,000 active daily users and as many as one million registered players. These weren't just impressive numbers for a two-year-old company; they represented a fundamental shift in how Americans consumed sports entertainment.

The strategic brilliance of DraftKings' approach became clear in their acquisition strategy. In July 2014, it announced the acquisition of rival DraftStreet, owned at the time by IAC, the third largest player in the fantasy sports space. That key acquisition reportedly increased DraftKings' user base by roughly 50%. Rather than compete in a three-way race, they consolidated the market, absorbing DraftStreet's technology, user base, and most importantly, its liquidity.

The funding arms race was officially on. In August 2014, the company announced $41 million in funding from a variety of investors, including the Raine Group, as well as existing investors Redpoint Ventures, GGV Capital, and Accomplice. This wasn't just venture capital—it was war chest for the battle ahead. Every dollar raised would be deployed in a winner-take-all fight for market dominance.

League partnerships became the next battlefield. In November 2014, DraftKings reached a two-year deal to become the official daily fantasy sports service of the National Hockey League. The deal included sponsorships of video features and other content across the NHL's digital outlets, co-branded free games with fan-oriented prizes, and in-venue ad placements during marquee NHL events. Each partnership wasn't just about brand association; it was about data access, marketing rights, and most crucially, the implicit endorsement that daily fantasy was legitimate entertainment, not illegal gambling.

Then came the nuclear option in the advertising wars. In July 2015, DraftKings entered into a three-year advertising deal with ESPN Inc. valued at $250 million. To put this in perspective, the entire company had raised less than $100 million to that point. They were committing to spend more on a single media partnership than their entire company valuation just eighteen months earlier.

The transformation from bedroom startup to sports entertainment juggernaut was complete. By mid-2015, DraftKings was processing millions of entries daily, had partnerships with three major sports leagues, and was preparing for what would be the most aggressive marketing campaign in startup history. What nobody knew yet was that they were also racing toward a cliff—and the fall would nearly destroy everything they'd built.

V. The Great DFS War: DraftKings vs. FanDuel (2015)

The war room at DraftKings' Boston headquarters looked like something out of a Wall Street trading floor. Multiple screens displayed real-time metrics: user acquisition costs, competitor ad spending, deposit volumes, contest liquidity. It was March 2015, and Jason Robins was staring at a number that seemed impossible: $400 million.

That was the math. The number that had been rumored in early 2015, of how much DraftKings was planning to raise and spend that year, was then staggering: $100 million. And yet that amount wouldn't have made a dent in FanDuel's lead. They did the math on how much DraftKings would have to raise and spend to catch them, and the number was outrageous: north of $400 million. FanDuel had first-mover advantage, better brand recognition, and deeper liquidity pools. In a network effects business, being second place meant eventual death. What made the decision even more audacious was the competitive dynamic. FanDuel, founded in 2009, had first-mover advantage and a commanding 65-35 market share lead at the start of 2015. They had raised $275 million from investors including Time Warner, NBC Sports, and Google Capital. Their CEO, Nigel Eccles, was a Scottish entrepreneur who'd built the business methodically, even selling off his childhood collection of Krugerrand coins to make payroll in the early days.

But DraftKings had something FanDuel lacked: a willingness to bet everything on a single roll of the dice. They did the math on how much DraftKings would have to raise and spend to catch them, and the number was outrageous: north of $400 million. When Eccles heard through the grapevine that DraftKings was planning something "five hundred million dollars big," he had just one thought: "Oh, f---."

The advertising blitzkrieg that followed was unprecedented in startup history. DraftKings spent $131.4 million on ads for a total of 40,283 national airings. Over the same period, FanDuel spent $74.5 million for a total of 21,545 national airings through October 2015. The two companies spent an estimated $750 million combined on ads, marketing and related expenses in 2015. From Aug. 16 through the opening weekend of the NFL season, the two companies outspent the entire beer industry.

The saturation was total. Turn on any NFL game and you'd see the same ads: regular guys supposedly winning millions, attractive women celebrating jackpots, promises of instant wealth. DraftKings ads had aired a skull-clutching 16,259 times over the course of the month, which works out to 135 hours and 25 minutes of 30-second spots. The frequency became a cultural phenomenon—ESPN personalities openly mocked the relentless advertising on air, Twitter erupted with parodies, and "DraftKings commercial" became shorthand for advertising overkill.

With the NFL season in full swing, FanDuel's ad spend was actually 10% under its budget because of a lack of inventory: DraftKings had bought up everything. This wasn't just aggressive marketing; it was scorched earth strategy. DraftKings signed exclusive deals everywhere they could: a $250 million agreement with ESPN that would lock out FanDuel starting in 2016, another $250 million with Fox Sports, individual deals with NFL teams for in-stadium advertising.

The network effects made this spending war existential. In daily fantasy, liquidity is everything—more players mean bigger prize pools, which attract more players, creating a virtuous cycle. The company with the most users would eventually dominate, while the loser would spiral into irrelevance. As one industry analyst put it, this was "mutually assured destruction"—both companies were burning cash at rates that would bankrupt normal businesses, but neither could afford to blink first.

By September 2015, something remarkable had happened: DraftKings was the top advertiser, according to the rankings at iSpot.com, followed by AT&T, Warner Bros. and Geico. Only months earlier they held a commanding lead over DraftKings: a 65–35 market share. That lead was gone. In less than nine months, DraftKings had erased FanDuel's six-year head start.

The human cost of this war was staggering. Both companies were hemorrhaging money—neither was profitable, and they were giving out nearly ten times more in prize money than they generated in revenue. Employees worked hundred-hour weeks, venture capitalists watched their investments evaporate, and the founders aged years in months. The FanDuel founders knew the spending was outrageous, the deals value destructive. Still, at every turn, when asked if he would allow DraftKings to overtake them, the CEO always had the same answer: No f------ way.

What neither company realized was that their advertising war had awakened something far more dangerous than a competitor—it had caught the attention of regulators, law enforcement, and a public increasingly skeptical of their claims. The very visibility that was supposed to ensure victory would soon threaten to destroy them both. The clock was ticking toward October 5, 2015, when everything would change.

VI. The Insider Trading Scandal & Regulatory Reckoning (2015-2016)

Ethan Haskell was having the best week of his life. A mid-level content manager at DraftKings, he'd just won $350,000 playing on FanDuel—a life-changing sum for someone making less than $60,000 a year. But his celebration would be short-lived. Within days, his windfall would trigger the near-destruction of the entire daily fantasy sports industry.

On October 5, 2015, an article in The New York Times indicated that an employee at DraftKings admitted to inadvertently releasing data before the start of week three's NFL football games. That same employee had won $350,000 on rival fantasy site FanDuel the same week. The timing seemed damning. Haskell had access to what the industry called "ownership data"—information showing what percentage of DraftKings players had selected each NFL player for their lineups. Armed with this data before FanDuel's contests locked, a player could gain an enormous edge, picking contrarian plays that others had overlooked.

The story exploded across media with the force of a bomb. "INSIDER TRADING" screamed the headlines. The parallel to Wall Street scandals was irresistible—employees using proprietary information to fleece unsuspecting customers. Within hours, both companies were in full crisis mode. DraftKings' internal review concluded Haskell had obtained the data after lineups were locked and couldn't have used it unfairly, but the damage was done. Public trust, already fragile given the gambling-adjacent nature of the business, evaporated overnight.

Both DraftKings and FanDuel released statements saying that "Nothing is more important... than the integrity of the games we offer to our customers," and they would work with the entire fantasy sports industry "so that fans everywhere can continue to enjoy and trust the games they love." They immediately banned employees from playing on rival sites. But the bleeding had started, and it wouldn't stop.

The regulatory dominoes began falling immediately. The following day, New York attorney general Eric Schneiderman opened an inquiry into DraftKings and FanDuel, asking each site for a range of internal data and details on how they prevent fraud. Schneiderman wasn't just any attorney general—New York was the companies' most lucrative market, accounting for nearly 15% of their revenue. His investigation would set the tone for how other states responded. In November 2015, New York Attorney General Eric Schneiderman sent cease-and-desist letters to DraftKings and FanDuel, ordering both companies to immediately stop accepting wagers inside New York. The AG's action followed an investigation by his office that found DraftKings and FanDuel to be in violation of New York State law against illegal gambling.

The language in Schneiderman's letter was devastating: "Our investigation has found that, unlike traditional fantasy sports, daily fantasy sports companies are engaged in illegal gambling under New York law, causing the same kinds of social and economic harms as other forms of illegal gambling, and misleading New York consumers. Daily fantasy sports is neither victimless nor harmless, and it is clear that DraftKings and FanDuel are the leaders of a massive, multi-billion-dollar scheme intended to evade the law and fleece sports fans."

The companies fought back viciously. In its petition, DraftKings called Schneiderman's order to cease taking business from customers in New York a "shocking overreach." "He has unleashed an irresponsible, irrational and illegal campaign to destroy a legitimate industry," the filing said. Both companies alleged that Schneiderman didn't just write the cease-and-desist letter to them. Instead, his office contacted payment operators to encourage them to discontinue financial transactions to New York customers of the sites or face repercussions. DraftKings said that as a result, one payment processor, Vantiv, told them it would no longer work with New York customers.

The legal and political battle that followed was unprecedented in startup history. Both companies hired armies of lawyers, lobbyists, and public relations firms. They mobilized their user bases, sending push notifications urging players to contact their representatives. DraftKings and FanDuel, mortal enemies just weeks earlier, found themselves fighting side by side for survival.

But the damage spread like wildfire across the country. Within weeks of Schneiderman's action, attorneys general in Texas, Illinois, Hawaii, Mississippi, and Vermont launched their own investigations. Nevada's Gaming Control Board ruled that daily fantasy sports constituted gambling, forcing both companies out of the state. The advertising spigot turned off overnight—after spending $192.8 million on TV ads between September and November 2015, the companies spent just $15.7 million in the same period in 2016, a 92% decline.

The irony was excruciating. The very advertising blitz that was supposed to ensure market dominance had instead painted a target on their backs. The promises of easy money, the celebration of massive jackpots, the ubiquitous presence—everything that made them successful also made them vulnerable to charges of predatory behavior. Schneiderman's cease and desist letters highlighted two seemingly contradictory criticisms: on one hand, he contended that DFS games were mostly about chance and luck, but on the other, he criticized these games for being consistently won by only a small percentage of players. The ability of a relatively small group of DFS players to consistently win suggested that skill played an important role.

By early 2016, both companies were hemorrhaging cash, users, and credibility. The advertising war that had consumed $750 million had to stop. Venture capitalists who'd poured hundreds of millions into the companies watched their investments crater. The dream of building the next great American consumer company seemed to be turning into a nightmare.

Then came the ultimate admission of defeat. On November 18, 2016, DraftKings and FanDuel announced their intent to merge. The combined company would serve over five million users. The two companies that had spent the previous year trying to destroy each other would now combine forces. It was a stunning reversal—from mutually assured destruction to mutual survival.

On June 19, 2017, the Federal Trade Commission (FTC) announced that it would seek a preliminary injunction to block the proposed merger. The FTC felt that the proposed transaction would give the combined company 90% of the U.S. DFS market, which is considered to be a monopoly position. On July 13, 2017, the merger was officially called off due to the threat of litigation from the FTC. Even joining forces couldn't save them from regulatory scrutiny.

The companies had survived, but barely. They'd gone from the highest-flying startups in America to pariahs fighting for their existence. Yet unknown to anyone at the time, their salvation was already working its way through the courts. A case called Murphy v. NCAA was about to change everything.

VII. The PASPA Pivot: From DFS to Sports Betting (2018-2020)

Jason Robins was sitting in DraftKings' Boston headquarters on May 14, 2018, at 10:00 AM Eastern, surrounded by his executive team and lawyers. They'd been waiting for this moment for months, refreshing the Supreme Court's website every few seconds. When the decision finally appeared—Murphy v. NCAA, 7-2 in favor of New Jersey—the room erupted. But Robins stayed quiet, reading the opinion line by line. Then he saw it: the words that would change everything.

In May 2018, the U.S. Supreme Court struck down the Professional and Amateur Sports Protection Act (PASPA), the federal ban on sports betting everywhere but Nevada. It was like the heavens opened and shone down on DraftKings and FanDuel. Justice Samuel Alito's majority opinion was unequivocal: "Congress can regulate sports gambling directly, but if it elects not to do so, each state is free to act on its own. Our job is to interpret the law Congress has enacted and decide whether it is consistent with the Constitution. PASPA is not."

The irony was almost too perfect. The same regulatory environment that had nearly destroyed DraftKings three years earlier had just handed them the opportunity of a lifetime. While traditional casino operators would need months to build technology platforms, hire staff, and navigate state regulations, DraftKings already had everything: the technology infrastructure, the customer database, the brand recognition, and most importantly, the operational experience of handling millions of transactions daily. The speed of execution was breathtaking. DraftKings hustled into nearby New Jersey and became the first online sportsbook to open for business outside of Nevada in the United States. In August 2018 came DraftKings Sportsbook, the first legal, mobile, and online sports betting platform to launch in New Jersey. DraftKings is the first operator to roll out a mobile NJ sports betting platform. Bettors must be located within the state of New Jersey to place a wager on the app.

The preparation had been meticulous. DraftKings co-founder Matt Kalish told Legal Sports Report that development began well in advance of the ruling. "We started building our sportsbook product at the end of last year. That was sort of a big bet that the company was making, because we knew the Supreme Court was looking at the case that New Jersey had brought against PASPA. We wanted to be ready in the event that legal, regulated sportsbooks in the US became an option in terms of a product that we could offer. We wanted to be ready to go as close to day one as possible with the launch of that product".

It enjoyed a de facto monopoly over the Garden State's market for nearly a month before competitors began to appear. In that time, it secured a tremendous amount of market share. The daily fantasy sports company of around 500 people has beaten casino giants like MGM and Caesars in the race to mobile betting in NJ. The advantages of being first were enormous—every customer acquired in those early weeks would likely stay with DraftKings for years, given the switching costs and inertia in consumer behavior.

Product innovation became the differentiator. DraftKings was the first sportsbook app to offer a cash-out option. This option, initially known as the live ticket system, allowed bettors to close out their open tickets if their bets appeared likely to win. DraftKings is also the first US operator to include a live-ticket system, in which every bet essentially becomes an in-play bet. This wasn't just a feature—it was a philosophical statement about how sports betting should work in the mobile age.

The technology stack they'd built for daily fantasy translated perfectly to sports betting. The same systems that handled millions of fantasy lineups could process sports bets. The same fraud detection that prevented duplicate accounts in DFS could ensure betting integrity. The same customer service infrastructure that resolved fantasy disputes could handle betting questions. Years of operational experience that competitors would need to build from scratch gave DraftKings an insurmountable head start.

But the real masterstroke was the SPAC merger. In April 2020, DraftKings went public through a business combination with Diamond Eagle Acquisition Company and SBTech. DraftKings became a publicly traded company through a reverse merger with SBTech, a Bulgarian technology company, and special-purpose acquisition company Diamond Eagle Acquisition Corp in April 2020. The timing seemed terrible—the deal closed in the depths of the COVID-19 pandemic when sports had essentially stopped. But Robins saw opportunity where others saw disaster.

It began trading publicly in April 2020 under the symbol DKNG and a market capitalization of $3.3 billion. Initially, the fortunes of the company soared to incredible heights. At one point, its market capitalization exceeded $20 billion. The public markets gave DraftKings something it had never had before: unlimited access to capital. While competitors scrambled for venture funding or relied on casino parent companies for investment, DraftKings could tap the equity markets whenever it needed funds for expansion.

The transformation was complete. The company that had nearly been destroyed by regulatory action in 2015 had become one of the primary beneficiaries of regulation in 2020. The spare bedroom startup was now a publicly traded company worth billions. But the journey was far from over—the real battle for American sports betting supremacy was just beginning.

VIII. The Modern Era: Building a Sports Betting Empire (2020-Present)

The earnings call on February 16, 2024, was unlike any in DraftKings' history. For years, analysts had peppered Jason Robins with the same question: "When will you be profitable?" His answer had always been some variation of "growth first, profits later." But this time was different. "2024 was a milestone year for DraftKings," Robins announced, his voice betraying just a hint of satisfaction, "as we achieved our first year of positive Adjusted EBITDA."The numbers told a story of remarkable transformation. 2024 was a milestone year for DraftKings as we achieved our first year of positive Adjusted EBITDA. For the full fiscal year 2024, revenue reached $4.768 billion, up from $3.665 billion in 2023. But more importantly, DraftKings is raising the midpoint of its fiscal year 2025 revenue guidance and now expects revenue in the range of $6.3 billion to $6.6 billion. Our fiscal year 2025 revenue guidance equates to approximately 35% year-over-year growth.

The geographic expansion strategy had been executed with military precision. DraftKings is live with mobile sports betting in 25 states and Washington, D.C., and with iGaming in 5 states. Each new state launch followed the same playbook: be first or among the first to market, offer aggressive promotions to acquire customers quickly, then gradually optimize the promotional spend as market share solidified.

The business model had evolved dramatically from the fantasy sports days. In 2024, sports revenue was 61% of total sales, i-gaming 32%, and fantasy and lottery 7%. The diversification was deliberate—sports betting drove customer acquisition, iGaming provided higher margins, and fantasy maintained the original user base while serving as a low-cost entry point for new customers.

Strategic acquisitions accelerated the transformation. In May 2022, DraftKings acquired Golden Nugget Online Gaming, In February 2024, the company acquired lottery courier app Jackpocket for $750 million. Each acquisition wasn't just about adding revenue—it was about acquiring capabilities, entering new verticals, and most importantly, expanding the total addressable market.

The duopoly with FanDuel had solidified into something resembling the Coke vs. Pepsi dynamic of sports betting. DraftKings (DKNG) boasts a $17.5 billion market cap; FanDuel parent company Flutter Entertainment (FLUT) has a $28.4 billion (GBP) market cap. The two enjoy a combined 65% market share of U.S. online gaming revenue. The bitter enemies of 2015 had become comfortable oligopolists, competing fiercely but rationally, avoiding the mutually assured destruction of their fantasy sports war.

Customer metrics revealed the power of the model. Monthly Unique Payers ("MUPs") increased to 4.8 million average monthly unique paying customers in the fourth quarter of 2024, representing an increase of 36% compared to the fourth quarter of 2023. The growth wasn't just in volume—engagement metrics showed users betting more frequently, on more sports, and increasingly migrating from sports betting to higher-margin iGaming products.

The financial performance validated every strategic decision. The company achieved positive free cash flow for the first time in its history. DraftKings is reaffirming its fiscal year 2025 Adjusted EBITDA guidance of $900 million to $1.0 billion. For a company that had burned through hundreds of millions just years earlier, the transformation to profitability marked a fundamental shift in the business.

Product innovation remained the competitive edge. The integration of live betting, powered by acquisitions like Simplebet, transformed the user experience. Parlays and same-game parlays, which carried higher margins, became increasingly popular. The technology platform, now processing billions in wagers annually, had become one of the most sophisticated transaction processing systems in consumer technology.

But challenges loomed. A pair of lawmakers have sent a letter to the heads of two U.S. antitrust agencies raising concerns that DraftKings and FanDuel are blocking competition from emerging sports betting operators. State tax increases threatened margins—Illinois had raised its sports betting tax rate to 40%, and other states were considering similar moves. The regulatory environment that had enabled DraftKings' rise could just as easily constrain its future.

The modern DraftKings bore little resemblance to the spare bedroom startup of 2012. It was now a technology company that happened to be in gambling, a data company that happened to take bets, a entertainment company that happened to process wagers. The three friends who'd quit their corporate jobs to chase an entrepreneurial dream had built exactly what they'd envisioned: a company that fundamentally changed how Americans engage with sports.

IX. Playbook: The DraftKings Business Model

The conference room at DraftKings headquarters displays a simple equation on the wall: "CAC < LTV." Customer Acquisition Cost must be less than Lifetime Value. It's the fundamental law that governs every decision at the company. But what seems simple masks one of the most complex business models in consumer technology.

"It was something where people were going for entertainment," Jason Robins explained in a rare moment of reflection about the model. "They were looking at fun. If you could create a great product, a great user experience, and provide people with the fun and entertainment they were looking for, then that was the secret." But the real secret was deeper—DraftKings had built a three-sided marketplace connecting sports fans, sports content, and financial transactions in ways that created powerful network effects.

Customer acquisition starts with what insiders call the "funnel of inevitability." It begins with brand awareness—those ubiquitous ads during sports broadcasts aren't just marketing, they're psychological conditioning. Every touchdown, every three-pointer, every home run becomes associated with the possibility of winning money. The message is subtle but powerful: you're already watching, why not make it more interesting?

The genius is in the onboarding. New users typically receive a "risk-free" first bet or a deposit match—promotional offers that can cost DraftKings $300 or more per customer. Critics see this as unsustainable cash burning. But DraftKings knows something others don't: sports betting is habitual. Once someone places their first bet, the likelihood of a second bet exceeds 70%. By the tenth bet, they're typically hooked.

Retention strategies are equally sophisticated. The app sends perfectly timed push notifications—not too many to be annoying, not too few to be forgotten. "Boost" offers provide enhanced odds on popular bets, creating the illusion of value while maintaining house edge. VIP programs offer cash back, exclusive promotions, and even real-world experiences like Super Bowl trips. Every element is designed to increase engagement and lifetime value.

But the real innovation is in the product experience itself. "We also found in daily fantasy sports that having user liquidity was a huge thing," Robins noted. "It was basically a marketplace as well as a game. We were matchmaking among people who want to play, so having a lot of users who are playing actively was really important and it created tremendous network effects." These network effects, carried over from fantasy sports, make each additional user valuable not just for their own betting but for improving the experience for all users.

The technology stack is the hidden advantage. While competitors rely on third-party platforms, DraftKings controls its entire technology infrastructure. Real-time odds calculation, risk management, fraud detection, payment processing—everything runs on proprietary systems refined over a decade. This vertical integration provides margins competitors can't match and enables product innovations they can't replicate.

Regulatory navigation has become a core competency. DraftKings employs more than 100 people focused solely on compliance and government relations. They don't just follow regulations; they help write them. The company's executives testify before state legislatures, proposing frameworks that ensure market access while creating barriers for potential competitors. It's regulatory capture, Silicon Valley style.

Marketing efficiency has evolved from the scorched-earth spending of 2015. Today's approach is surgical. DraftKings knows the exact value of a customer acquired through ESPN versus Fox Sports, through Instagram versus Twitter, through a deposit match versus a risk-free bet. Every dollar spent is tracked, measured, and optimized. The company can tell you the three-year expected value of a customer acquired during March Madness versus one acquired during NFL playoffs.

The cross-selling opportunity is perhaps the most underappreciated aspect of the model. A customer acquired for sports betting costs roughly $300-400. That same customer, if successfully migrated to iGaming, generates 3-4x the lifetime value. DraftKings doesn't need to acquire iGaming customers directly—they convert sports bettors into casino players at virtually zero marginal cost.

Data advantages compound over time. DraftKings knows more about American sports betting behavior than anyone except perhaps FanDuel. They know which teams attract the most action, which bet types generate the highest margins, which customers are likely to develop problems. This data doesn't just improve the product; it becomes a moat that grows wider every day.

The unit economics tell the story. Average customer lifetime value now exceeds $1,000. Customer acquisition costs have dropped below $400 in mature markets. The payback period has shortened from over two years to under 18 months. These metrics, impossible during the fantasy sports wars, validate the entire strategy.

But perhaps the most important element of the playbook is discipline. After nearly destroying themselves with unsustainable spending in 2015, DraftKings learned to balance growth with profitability. They still invest aggressively in new markets, but only when the math works. They still innovate constantly, but only on features that drive measurable value. They still compete fiercely with FanDuel, but without the mutually assured destruction of their earlier battles.

The model isn't without vulnerabilities. Problem gambling concerns could trigger regulatory backlash. New competitors with deeper pockets could restart spending wars. Technology disruptions could obsolesce their platform advantages. But for now, DraftKings has built something remarkable: a business model that turns America's love of sports into a money-printing machine, all while providing genuine entertainment value to millions of users.

X. Analysis: Bull vs. Bear Case

Bull Case: The Path to $50 Billion

The investment thesis for DraftKings writes itself if you believe in the American appetite for gambling. Our fiscal year 2025 revenue guidance equates to approximately 35% year-over-year growth—in what other consumer category can you find that kind of growth at this scale? The company has cracked the code on digital entertainment, transforming passive sports viewing into active participation with real stakes.

Market leadership provides insurmountable advantages. With a $17.5 billion market cap and dominant position alongside FanDuel, DraftKings operates in a comfortable duopoly. The barriers to entry—regulatory requirements, technology infrastructure, brand recognition, and customer acquisition costs—make it virtually impossible for new entrants to achieve meaningful scale. This isn't a winner-take-all market; it's a winner-take-most market, and DraftKings has already won.

The total addressable market remains vastly underpenetrated. Only 25 states have legalized mobile sports betting, meaning nearly half the U.S. population can't legally access DraftKings' primary product. California alone, with 40 million residents and a massive sports culture, could add $1-2 billion to DraftKings' revenue once it legalizes. Texas and Florida represent similar opportunities. As these dominoes fall—and history suggests they will—DraftKings' revenue could double without any improvement in market share or customer monetization.

Product innovation advantages compound over time. DraftKings' proprietary technology platform, built over a decade, provides capabilities competitors can't match. Live betting, micro-markets, same-game parlays—each innovation increases engagement and margins. The recent acquisitions of Simplebet and Jackpocket aren't just revenue additions; they're capability expansions that widen the competitive moat.

The path to profitability has been definitively proven. 2024 was a milestone year for DraftKings as we achieved our first year of positive Adjusted EBITDA. With fiscal year 2025 Adjusted EBITDA guidance of $900 million to $1.0 billion, the company is demonstrating operating leverage. As revenue grows, margins expand exponentially—a classic software business model applied to gambling.

Multiple revenue streams provide resilience and growth vectors. Sports betting attracts customers, iGaming monetizes them at higher margins, and new products like lottery and prediction markets expand the addressable market. Each product reinforces the others, creating an ecosystem that becomes stickier over time.

International expansion remains a massive untapped opportunity. While focused on the U.S., DraftKings could eventually replicate its model globally. The worldwide sports betting market exceeds $200 billion—even capturing a small percentage would transform the company's scale.

Bear Case: The Regulatory Reckoning

The bear case starts with a simple observation: no vice industry has ever avoided regulatory backlash indefinitely. Tobacco, alcohol, opioids—each faced its reckoning. Sports betting's turn is coming, and when it does, DraftKings sits directly in the crosshairs.

The antitrust concerns are already materializing. A pair of lawmakers have sent a letter to the heads of two U.S. antitrust agencies raising concerns that DraftKings and FanDuel are blocking competition from emerging sports betting operators. The comfortable duopoly that bulls celebrate could become an antitrust liability. Forced divestments, market share caps, or interoperability requirements could destroy the business model's economics.

Tax burden increases are accelerating. Illinois' move to a 40% tax rate on sports betting revenue isn't an anomaly—it's a preview. States facing budget pressures see sports betting operators as easy targets. Unlike other businesses that can relocate, DraftKings must operate where customers are located. They're trapped, and politicians know it.

Customer acquisition costs remain stubbornly high. Despite claims of improving efficiency, DraftKings still spends hundreds of dollars to acquire each customer. In competitive markets, these costs show no signs of declining. The "funnel of inevitability" only works if you can afford to fill the top of the funnel—and that's becoming increasingly expensive.

Competition from established casino operators is intensifying. Companies like MGM, Caesars, and Penn Entertainment have deeper pockets, existing customer bases, and physical assets that provide competitive advantages. As the market matures, these incumbents' advantages—particularly in iGaming—could prove decisive.

Problem gambling concerns threaten the entire business model. Every suicide linked to sports betting, every bankruptcy caused by gambling addiction, every underage betting scandal brings regulatory scrutiny. The UK's experience—where regulations have crushed operator margins—provides a preview of what could happen in the U.S.

Market saturation is approaching faster than bulls acknowledge. There was a slowdown in handle growth across the industry in the fourth quarter of 2024. The easy growth from new state launches and customer acquisition is ending. Future growth must come from increasing bet sizes and frequency among existing customers—a much harder and potentially more problematic path.

Technology disruption could obsolesce current advantages. Blockchain-based betting platforms, peer-to-peer wagering, or AI-driven prediction markets could bypass traditional operators entirely. DraftKings' technology moat, impressive as it is, protects against yesterday's threats, not tomorrow's innovations.

The macro environment matters more than management admits. Sports betting is discretionary spending—in a recession, it's among the first expenses consumers cut. The COVID-19 sports shutdown demonstrated this vulnerability. Future economic downturns could devastate revenue just as fixed costs remain elevated.

Federal intervention remains a constant threat. A federal sports betting tax, interstate compact requirements, or advertising restrictions could materialize overnight. The industry's rapid growth and increasing visibility make it an attractive target for federal lawmakers seeking revenue or political wins.

The valuation assumes everything goes right. At current multiples, DraftKings is priced for perfection—continued rapid growth, margin expansion, new state launches, and no regulatory setbacks. Any deviation from this optimistic scenario could trigger a significant revaluation. The risk-reward, particularly after the stock's recent run-up, skews negative.

XI. Future Vectors & Strategic Options

The whiteboard in DraftKings' strategy room maps out possibilities that would have seemed like science fiction just years ago. International expansion. Prediction markets for everything from elections to weather. Media rights acquisition. Even cryptocurrency integration. Each vector represents billions in potential value—or costly distractions from the core business.

International expansion tempts with its massive scale. The global sports betting market dwarfs the U.S. opportunity, but DraftKings has deliberately remained focused domestically. The calculation is pragmatic: why fight established operators in mature markets when so much opportunity remains at home? But as U.S. growth slows, international markets become increasingly attractive. Canada provided proof of concept—DraftKings entered Ontario and quickly captured significant share. The UK, despite its competitive intensity, offers a £15 billion market. Brazil, with its passionate sports culture and emerging regulations, could be transformative.

New product categories blur the lines between gambling and other forms of speculation. Prediction markets—wagering on event outcomes beyond sports—represent a fascinating opportunity. Will inflation exceed 3%? Will a specific movie win Best Picture? Will it rain on the Fourth of July? These markets, popular on platforms like Polymarket and Kalshi, could integrate seamlessly with DraftKings' existing infrastructure. The regulatory pathway is unclear, but the potential is enormous.

Technology licensing emerges as a capital-light growth vector. DraftKings has built one of the world's most sophisticated sports betting platforms—why not license it to operators in markets where DraftKings doesn't compete directly? B2B opportunities could generate high-margin revenue without customer acquisition costs. This mirrors the evolution of companies like Shopify, which found more value in enabling commerce than conducting it directly.

Media and content integration could transform the business model. Imagine DraftKings acquiring broadcast rights to sporting events, integrating betting directly into the viewing experience. Every pitch, every play, every possession becomes a betting opportunity. The technology exists; only regulatory and rights issues prevent implementation. As media companies struggle with cord-cutting, partnerships or acquisitions could provide DraftKings with content while giving media companies new monetization methods.

The lottery opportunity is particularly intriguing. The Jackpocket acquisition provides entry into a $100 billion U.S. market that's even larger than sports betting. State lotteries, currently operated as government monopolies, face pressure to modernize. DraftKings could position itself as the technology provider that brings lotteries into the digital age, capturing a portion of massive, stable revenue streams.

Potential consolidation scenarios multiply as the market matures. While the failed FanDuel merger showed regulatory risks, other combinations might succeed. Acquiring regional operators, technology providers, or complementary businesses could accelerate growth. Conversely, DraftKings itself could become an acquisition target for media companies, casino operators, or technology giants seeking sports betting exposure.

AI and personalization represent the next frontier of product innovation. Imagine an AI that knows your betting patterns, risk tolerance, and favorite teams, automatically suggesting bets tailored to your preferences. Or predictive models that help casual bettors make more informed decisions. The data DraftKings possesses, combined with advancing AI capabilities, could create unprecedented user experiences.

Cryptocurrency integration, while currently limited, could revolutionize the industry. Instant settlements, reduced transaction costs, enhanced privacy, and global accessibility—crypto solves many of sports betting's friction points. While regulatory acceptance remains limited, a few states are warming to the idea. If crypto betting gains regulatory approval, DraftKings' technology platform is ready.

Strategic partnerships with sports leagues could deepen. The NBA has discussed integrity fees and data rights partnerships. The NFL, despite its historical gambling opposition, now embraces sports betting. Deeper partnerships—perhaps even equity stakes from leagues—could provide DraftKings with exclusive data, marketing rights, and competitive advantages.

The social and multiplayer evolution could transform betting from solitary to communal. Betting pools with friends, tournament-style competitions, social feeds showing others' bets—these features could increase engagement and acquisition through network effects. The generation that grew up with social media expects social features in every app.

But the most important strategic decision might be what not to do. The temptation to chase every opportunity, enter every market, build every feature is strong. But DraftKings' history shows that focus beats diversification. The company succeeded by doing daily fantasy better than anyone, then sports betting better than almost anyone. Maintaining that focus while selectively pursuing the highest-value opportunities will determine whether DraftKings becomes a $50 billion company or another cautionary tale of overexpansion.

The chess board is set. DraftKings has strong pieces, favorable position, and momentum. But the game is far from over. Each strategic choice—international expansion, new products, acquisitions, partnerships—moves pieces toward either victory or vulnerability. The next five years will determine whether DraftKings becomes the definitive platform for sports engagement or merely one player in an increasingly crowded field.

XII. Epilogue: Lessons & Reflections

Standing in DraftKings' Boston headquarters today, surrounded by screens showing real-time betting data from across the nation, it's hard to imagine that this empire started with three guys coding in a spare bedroom. The trajectory from that Watertown bedroom to a $17.5 billion public company offers lessons that extend far beyond sports betting.

The power of timing in entrepreneurship cannot be overstated. DraftKings didn't invent daily fantasy sports—FanDuel launched three years earlier. They didn't pioneer mobile betting—European operators had been doing it for years. What they did was recognize when multiple trends converged: smartphone ubiquity, payment infrastructure maturity, sports league acceptance, and eventual regulatory change. As Robins reflected on their earlier failed attempts: "We always had this entrepreneurial pull but never had good timing." When the timing finally aligned in 2012, they were ready.

Building in regulated industries requires a different playbook. Most Silicon Valley startups follow the "move fast and break things" philosophy. DraftKings couldn't afford to break things—breaking regulations meant destruction. Instead, they developed a nuanced approach: aggressive where legally clear, cautious where ambiguous, and always prepared to pivot. The 2015 regulatory crisis that nearly destroyed them became the education that enabled their sports betting success.

The eternal tension between growth and profitability defined DraftKings' journey. The 2015 advertising war—$750 million spent between two companies—remains a cautionary tale of growth at all costs. Yet without that spending, DraftKings might have lost to FanDuel permanently. The lesson isn't to avoid aggressive growth spending, but to understand when such spending creates lasting advantage versus temporary market share.

Network effects in consumer businesses create winner-take-most dynamics. DraftKings understood this from day one: more users meant more liquidity, which meant better experiences, which attracted more users. This virtuous cycle, once established, becomes nearly impossible for competitors to break. The comfortable duopoly with FanDuel exists not because others haven't tried to compete, but because network effects create insurmountable barriers.

Capital efficiency eventually matters, even in capital-intensive businesses. DraftKings' journey from burning hundreds of millions to generating positive EBITDA teaches that sustainable business models win long-term. The market rewards growth, but only if that growth leads somewhere profitable. The company's 2024 profitability milestone validated a decade of investment and strategic choices.

What the DraftKings story tells us about American culture is perhaps most revealing. We've always been a nation of dreamers and risk-takers, from frontier settlers to dot-com entrepreneurs. Sports betting simply channeled these impulses into a new medium. The rapid acceptance of sports betting—from taboo to mainstream in less than a decade—shows how quickly cultural norms can shift when technology and regulation align.

The transformation of sports consumption reflects broader entertainment trends. Passive viewing is dying across all media. Whether it's interactive streaming, social media engagement, or sports betting, audiences demand participation. DraftKings didn't just build a betting platform; they built an engagement layer for sports, transforming every game into a personalized experience with real stakes.

The regulatory arbitrage opportunity won't last forever. DraftKings benefited from state-by-state legalization that created first-mover advantages in each market. Future industries won't have this luxury. Federal frameworks, interstate compacts, and harmonized regulations will prevent the regulatory arbitrage that enabled DraftKings' rise. They were fortunate to build during a unique window of regulatory fragmentation.

Founder dynamics matter more than most admit. The partnership between Robins, Kalish, and Liberman survived challenges that destroy most founding teams: near bankruptcy, regulatory crises, competitive wars, and massive success. Their complementary skills—Robins' business acumen, Kalish's technical expertise, Liberman's operational excellence—created resilience. Solo founders might move faster, but founding teams endure more.

The platform possibility remains underexplored. DraftKings built incredible technology for sports betting, but that technology could power much more. Prediction markets, financial speculation, even decision-making tools—any domain requiring odds calculation, risk management, and real-time transaction processing could leverage DraftKings' platform. The company's future might lie not in what they bet on, but in becoming the infrastructure for all forms of speculation.

Luck versus skill—the eternal gambling question—applies to business too. Was DraftKings' success skill or luck? The PASPA repeal was fortunate timing, but being ready to capitalize required skill. The failed FanDuel merger was bad luck, but surviving and thriving independently demonstrated resilience. Like successful gambling itself, building DraftKings required both luck and skill, with skill determining how well they capitalized on lucky breaks.

The societal implications remain unresolved. DraftKings created enormous value—for shareholders, employees, users who enjoy the product, and states collecting tax revenue. But they also enabled problem gambling, contributed to financial distress, and changed how Americans relate to sports. The net societal benefit remains debatable. What's undebatable is that DraftKings permanently changed American culture.

Looking back, the DraftKings story reads like a Hollywood script: outsiders taking on the establishment, near-death experiences, dramatic pivots, and ultimate triumph. But the real story is more complex—a tale of timing, technology, regulation, and relentless execution combining to create something unprecedented. Three friends who quit their corporate jobs to build a fantasy sports website ended up reshaping American entertainment.

The journey from spare bedroom to sports betting empire offers a final lesson: transformation is possible, but it's never linear. DraftKings faced existential threats, competitive wars, and regulatory challenges that would have destroyed most companies. They survived through adaptation, discipline, and an unwavering belief that Americans wanted to engage more deeply with sports. They were right, and that insight built a billion-dollar empire.

The story isn't over. New challenges—regulatory, competitive, technological—await. But DraftKings has proven something important: with the right timing, team, and tenacity, it's possible to transform not just a company or industry, but culture itself. The three friends coding in a spare bedroom didn't just build a sports betting platform. They changed how America plays.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube