Comstock Resources: The Billionaire's Bet on America's Natural Gas Future

I. Introduction & Episode Roadmap

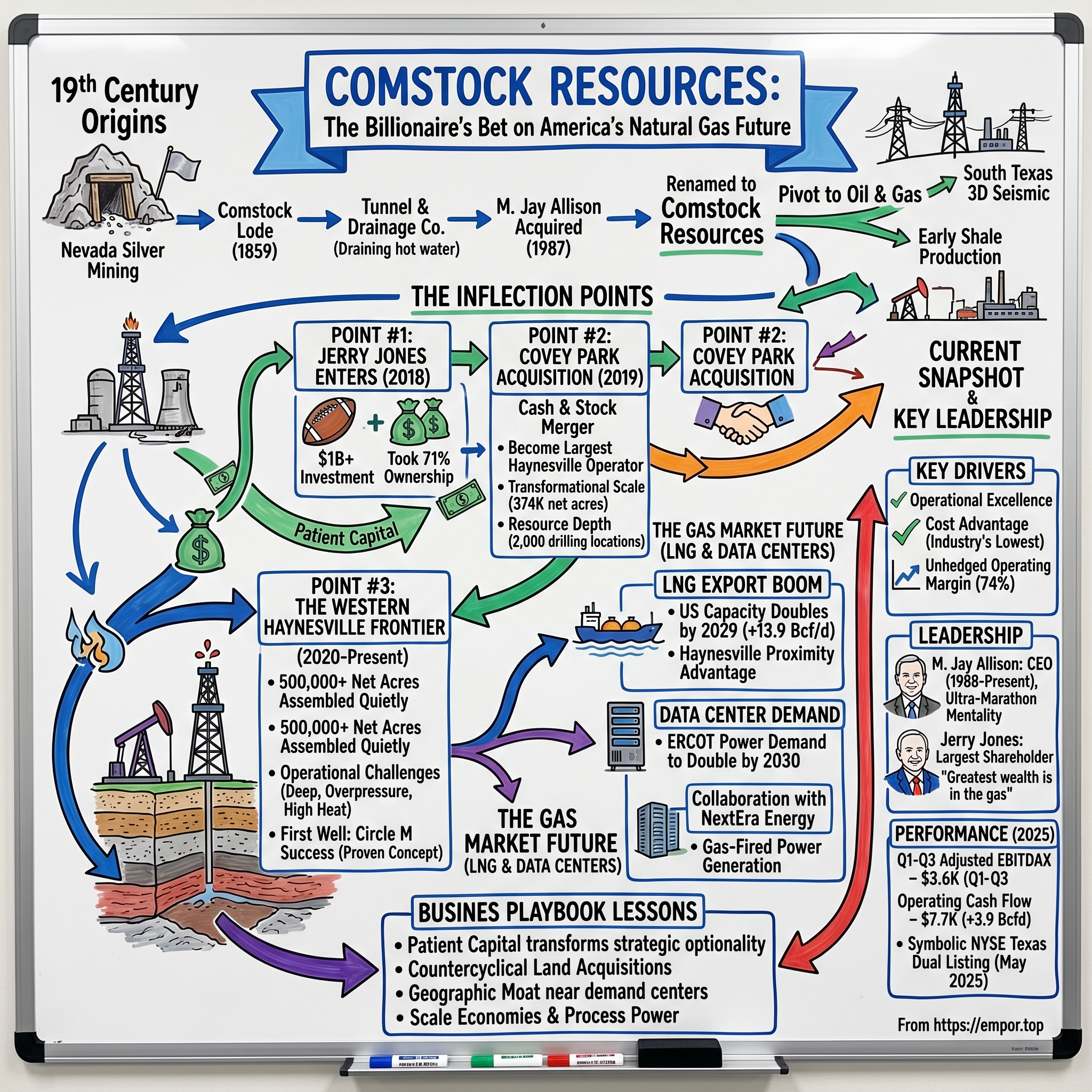

The improbable transformation of a 19th-century Nevada silver mine drainage company into one of America's largest natural gas producers begins with a simple question: How did Dallas Cowboys owner Jerry Jones—a man synonymous with professional football, Super Bowl championships, and stadium spectacles—become the dominant force in one of the most strategic energy basins on the planet?

Dallas Cowboys owner Jerry Jones invested over $1 billion in Comstock Resources to finance a major natural gas exploration initiative in East Texas, taking his ownership stake to 71%. This isn't a side bet or a portfolio diversification play. It's the largest concentrated wager by a single individual on American natural gas since the shale revolution began—and it's happening in what may be the most consequential moment for U.S. gas markets in a generation.

Comstock Resources, headquartered in Frisco, Texas, operates as a pure-play natural gas producer with an intense focus that borders on theological devotion to a single geological formation: the Haynesville Shale. The Haynesville Shale in East Texas and northwest Louisiana is the third-largest natural gas producer in the U.S., according to the U.S. Energy Information Administration.

The company's story weaves together multiple threads that define modern American energy: the shale revolution's maturation, the rise of LNG exports as a geopolitical instrument, the emergence of data centers as massive power consumers, and the timeless power of patient capital in a business defined by boom-and-bust cycles.

What makes Comstock particularly fascinating isn't just its scale—though controlling over 1 million gross acres in the Haynesville certainly qualifies as scale—but its strategic positioning. The collaboration with NextEra Energy Resources was disclosed in Comstock's second quarter results. As envisioned, the generation would be built near Comstock's western Haynesville area, which extends across several counties basically 100 miles each way between the two largest metropolitan areas: east of the Greater Houston area and south of the Dallas Metroplex.

The timing of Comstock's ascension couldn't be more fortuitous—or more deliberate. Liquefied natural gas exporters in the United States have announced plans to more than double U.S. liquefaction capacity, adding an estimated 13.9 billion cubic feet per day between 2025 and 2029. The United States is already the largest exporter in the world with 15.4 Bcf/d of capacity.

II. The Strange Origins: From Silver Mining to Oil & Gas

In the annals of corporate genealogy, few stories are as peculiar as Comstock Resources' origin. The company's name itself is a direct callback to one of the most legendary mineral discoveries in American history: the Comstock Lode.

The Comstock Tunnel and Drainage Company was located in the Comstock Lode of Virginia City, Nevada. It was founded in the late 1890s to pump water from greater depths in the mines to revive the silver mining industry.

The Comstock Lode, discovered in 1859, was the first major silver deposit discovered in the United States and triggered a rush that transformed Nevada from a desolate territory into a state, partly to secure its silver wealth for the Union during the Civil War. At its peak, Virginia City's population swelled to 25,000, making it one of the most important industrial cities between Denver and San Francisco.

The Comstock Tunnel and Drainage Company was a mining company of Virginia City, Nevada; organized in 1919 as a successor to the Comstock Tunnel Company.

The original entity's purpose was to drain hot water from the mines—an engineering challenge that had bedeviled miners since the Lode's earliest days. The tunnel was in use for fifty years and was a success as a means of draining hot water from the mines. Financially it was a loss, as stock became worthless with the decline of Comstock Lode.

Enter M. Jay Allison. In 1987, at the age of 30, he acquired Comstock Tunnel and Drainage, based in Virginia City, Nevada, which had subsidiary operations dating back to 1863. Named after the famous Comstock Lode, it owned an old silver mine and real estate in Nevada. Jay renamed it Comstock Resources and changed the business plan to acquire and drill oil and gas properties.

The decision to retain the Comstock name was more than mere sentimentality. It preserved the company's New York Stock Exchange listing and created a vehicle for Allison's vision: building an independent exploration and production company from scratch. In 1983, Allison co-founded a private independent oil and gas company which acquired Comstock Resources in 1987. He has experienced success first-hand through witnessing the rise of Comstock Resources, which is based in Frisco, Texas.

What followed was a three-decade journey through the cyclical brutality of the oil and gas business. "We've been through at least seven boom–bust cycles at Comstock, and we have emerged as one of the top 10 natural gas focused companies in North America."

The pivot from a Nevada mining shell to a Texas natural gas powerhouse wasn't immediate. The company evolved through multiple strategic phases—from acquisition-focused growth to exploration using 3D seismic technology in South Texas and the Gulf of Mexico, and eventually to shale production when the unconventional revolution arrived.

III. The Haynesville: Setting the Stage

To understand Comstock Resources, you must first understand the Haynesville Shale—a geological formation so consequential to American energy security that its discovery in 2008 rewrote assumptions about domestic natural gas supply.

In 2008, the Haynesville Shale was thought to be the largest natural gas field in the contiguous 48 states, with an estimated 250 trillion cubic feet of recoverable gas. While subsequent estimates revised that figure downward, the Haynesville remained—and remains—among the most prolific gas-producing formations in North America.

The Haynesville Shale is an informal, popular name for a Jurassic-Period rock formation that underlies large parts of southwestern Arkansas, northwest Louisiana, and East Texas. It lies at depths of 10,500–13,000 feet below the land's surface. The Haynesville Shale underlies an area of about 9,000 square miles and averages about 200–300 feet thick.

What makes the Haynesville strategically unique isn't just its size—it's geography. The formation sits within striking distance of the Gulf Coast's petrochemical complex and, crucially, its burgeoning LNG export infrastructure. The Haynesville formation is much deeper than other natural gas formations, making it more expensive to drill. Its proximity to LNG export terminals has led to drilling and infrastructure investments that result in natural gas production increases midway through the projection period.

Chesapeake Energy's 2008 discovery triggered what locals called a "land-leasing gold rush." Production has boomed since 2008, creating a number of new millionaires in the Shreveport, Louisiana, region.

The basin's history since then has been volatile. From 2009 to 2012, the Haynesville was the largest shale gas-producing region in the country. In November 2011, Haynesville regional production reached a record 10.4 Bcf/d. Beginning in early 2013, however, Haynesville output began to slip as natural gas prices declined. It was surpassed that year by Marcellus/Utica production.

Compared with Appalachian resources, Haynesville natural gas reservoirs are deeper, with formation depths ranging between 10,000 and 14,000 feet. This depth creates both challenges and opportunities: higher drilling costs, but also higher reservoir pressures that can deliver prolific initial production rates.

The basin experienced a significant production decline in 2024. The decline in shale gas production so far this year has been driven primarily by declines in production in the Haynesville and Utica plays. From January through September 2024, shale gas production decreased by 12% in the Haynesville and by 10% in the Utica compared with the same period in 2023.

But 2025 brought recovery. Gas production in the Haynesville Shale is on the climb as operators continue to turn deferred wells online in response to better pricing and the bullish outlook for LNG export demand. Higher prices in 2025, driven by rapid feedgas demand growth and an overall tightening of market fundamentals this winter, have enabled Haynesville producers in recent months to begin bringing on production they had held back in 2024.

The strategic significance of the Haynesville extends beyond current production. The basin represents a critical node in American energy infrastructure—positioned to feed the largest concentration of LNG export capacity on Earth and increasingly, to power the data centers that will define the next phase of technological expansion.

IV. Inflection Point #1: Enter Jerry Jones (2018)

The transformation of Comstock Resources from a mid-tier E&P into a Haynesville basin leader began with an unconventional partnership announced in April 2018. Jones took majority control of Comstock Resources four years ago during the depths of the natural gas bust. Since then, his more than $1 billion investment has more than doubled.

The deal structure revealed Jones's sophistication as a dealmaker. Rather than simply writing a check, he contributed producing oil and gas properties he already owned in exchange for equity. In 2018 Jones swapped 52.5 net producing oil wells and a series of uncompleted wells he owned in North Dakota's Bakken region for 88.57 million shares in publicly traded gas producer Comstock Resources worth $620 million.

Critics questioned the valuation. Arguably, Comstock overpaid, since those wells cost Jones $398 million, net of accounting write-downs including depletion and depreciation, according to Comstock's 2019 annual report.

When Jerry Jones acquired Comstock Resources in 2018, everybody thought he overpaid for a money-losing business. Sound familiar? The comparison to his Dallas Cowboys purchase was apt. In 1989, Jones paid $150 million for a money-hemorrhaging football franchise—more than anyone had ever paid for a sports team. Since 1989, the Cowboys have risen 5,000% in value.

Jones's rationale for the Comstock investment reflected both strategic insight and contrarian instinct. "This Haynesville area that we're in, in my mind, is the premier gas place to be anywhere, and it's the cheapest gas to produce. And we've got right there the export facilities for the U.S. to take it to Germany."

The timing was crucial. When Jones made his move, benchmark natural gas prices were low, about $3.25/mmbtu. When Jones doubled down in 2019, prices had fallen even further, to less than $3. Capital markets had largely abandoned the E&P sector.

An M&A analyst captured the strategic significance: "Comstock has a significant edge as a consolidator in the play with access to the deep pockets of Jones, who took control of the company last year. That allows them to circumvent capital markets, which are virtually closed to E&Ps right now."

Jones didn't just provide capital—he brought credibility and a long-term mindset that contrasted sharply with the short-term focus dominating public E&P investors. "One thing that is appealing to me about a public company, to make this kind of investment, is that when you're with the right people, I know that what they're telling you is correct. That's a big deal. You can have the confidence to really swing for the fences."

The partnership between Jones and Allison combined complementary strengths: Allison's operational expertise and industry relationships with Jones's patient capital and willingness to invest counter-cyclically.

V. Inflection Point #2: The Covey Park Acquisition (2019)

With Jones's backing secured, Comstock moved quickly to consolidate its position. Comstock closed the previously announced acquisition of Covey Park Energy LLC in a cash and stock merger valued at approximately $2.2 billion.

The multibillion-dollar acquisition of Denham Capital-backed Covey Park Energy was set to make Comstock Resources the largest Haynesville operator, analysts say.

The deal's strategic logic was compelling. By acquiring Covey Park, Comstock gained access to the three best parts of the Haynesville: the Caspiana Core in Louisiana, the Shelby Trough in East Texas, and the emerging Carthage sweet spot.

Jones's role in financing the acquisition demonstrated the power of having patient capital on hand. As part of this transaction Jerry Jones invested $475.0 million in the Company in exchange for 50,000,000 newly issued shares of Comstock common stock valued at $6.00 per share and $175.0 million of newly issued shares of convertible preferred stock. This equity investment brought Mr. Jones' total investment in Comstock to approximately $1.1 billion.

The combined company achieved transformational scale. Pro forma the Covey Park acquisition, Comstock expected its position to total roughly 374,000 net acres with over 1.1 billion cubic feet equivalent per day of net production. In the Haynesville, the company said it would have about 2,000 net drilling locations.

CEO Jay Allison described the strategic rationale: "After a year of evaluating several potential targets in the Haynesville shale, we believe we have found the perfect merger partner. This merger is an excellent fit with our existing acreage and continues our strategic plan of creating significant scale and resource depth in the Haynesville shale basin."

The transaction structure revealed sophisticated financial engineering. Comstock also assumed Covey Park's existing $625.0 million 7.5% senior notes, retired $380.0 million outstanding under Covey Park's bank credit facility and redeemed all outstanding previously issued Covey Park preferred equity for $153.4 million.

As a result of the transaction, Comstock is now the largest operator in the Haynesville Shale.

The Covey Park acquisition marked the end of Comstock's status as an also-ran and the beginning of its role as basin leader—a position it has defended and extended ever since.

VI. Inflection Point #3: The Western Haynesville Frontier (2020-Present)

If the Jones investment and Covey Park acquisition transformed Comstock into a Haynesville leader, what happened next may prove even more consequential: the discovery and development of the Western Haynesville.

Comstock Resources unveiled a massive new Haynesville and Bossier shale position north of Houston—more than 500,000 net acres assembled quietly over several years at an average of $600 per acre.

The Western Haynesville represents a new frontier—geologically related to the legacy Haynesville but presenting fundamentally different challenges. Drilling into the deep, high-pressure reservoirs of the Haynesville and Bossier formations in Texas' western Haynesville play, particularly in Robertson and Leon counties, presents operational challenges. These formations are characterized by extreme overpressure, with the Haynesville Shale exhibiting pressure gradients of 0.85 to 0.95 psi/ft, translating to pressures of approximately 10,200 to 13,300 psi at depths of 12,000 to 14,000 feet.

Comstock's first exploratory well, the Circle M, proved the concept. Comstock's Circle M #1H well, completed in 2022, has produced 13.4 billion cubic feet of gas over 19 months, with some wells in the area exceeding daily production rates of 35 million cubic feet per day thanks to extended lateral sections.

The success of the Circle M sparked enthusiasm that Comstock Resources was on to something big.

The economics present both opportunity and challenge. Drilling costs about twice as much as in the Haynesville, but wells yield twice as much output and are competitive at current gas prices, with potential cost reductions expected over time.

By 2025, Comstock had assembled a dominant position. The Western Haynesville footprint has grown to nearly 525,000 net acres, with 24 out of 29 drilled wells currently producing.

The Western Haynesville wells have demonstrated remarkable productivity. Five Western Haynesville wells turned to sales in the second quarter. These wells had an average lateral length of 10,897 feet and an average per well initial production rate of 36 MMcf per day. The five wells were drilled and completed at an average per well cost of $2,647 per completed lateral foot.

The company's long-term outlook is ambitious. Comstock Resources has projected 30 years of drilling inventory in the area, and CEO Miles Jay Allison highlighted the growth of its Western Haynesville footprint during the company's Q2 2025 earnings call.

The Western Haynesville isn't just about reserves—it's about positioning for the next wave of demand. "100 miles away from Dallas, 100 miles away from Houston, where you should have a data center," Allison explained.

VII. The LNG & Data Center Thesis

Comstock's strategic positioning intersects with two of the most powerful secular trends in American energy: the explosion of LNG exports and the insatiable power demands of data centers.

More broadly, LNG export capacity in North America is on track to increase from 11.4 Bcf/d at the beginning of 2024 to 28.7 Bcf/d in 2029, if projects currently under construction begin operations as planned.

This expansion represents a fundamental reshaping of American gas markets. Natural gas converted to LNG for export will increase to 9.8 trillion cubic feet, or almost 27 billion cubic feet per day, in 2037 compared with 4.4 Tcf in 2024.

Natural gas price changes mainly affect regions that produce mostly natural gas with limited co-production of crude oil and other liquids, such as in the Haynesville and Appalachia regions. As new LNG facilities on the Gulf Coast begin operating, natural gas production—particularly in the Haynesville region because of its proximity to these facilities—would increase to meet the increased demand.

The Haynesville's proximity advantage is quantifiable. Pipeline infrastructure connects the basin directly to Gulf Coast terminals, minimizing transportation costs and basis differentials that plague more distant basins.

Simultaneously, Texas electricity demand is surging. The EIA expects electricity demand in ERCOT to grow at an average rate of 11% in 2025 and 2026 while the PJM region grows by 4%.

Developers have proposed numerous data centers and large manufacturing facilities that could consume significant amounts of electricity, and many of these projects are concentrated in the ERCOT and PJM regions.

ERCOT estimates that demand for power will nearly double by 2030, largely due to population growth, more extreme weather and the increase of large users such as crypto mines, data centers and electrifying oil and gas operations.

Comstock is positioning to serve this demand directly. Haynesville Shale pure-play Comstock Resources Inc. is making the leap from producing natural gas to generating power in a collaboration to use its considerable East Texas output to keep the lights on at a plethora of data centers in the state.

"We're also excited to announce that we're working with NextEra Energy, who leads the nation in the development of power generation, to explore the development of gas-fired power generation assets near our growing Western Haynesville area that can power potential data center customers. We believe our location, which is 100 miles from the Dallas Metroplex, is an ideal site with natural gas, water, and electrical grid infrastructure—resources that could support data center development."

The convergence of LNG export demand and data center power consumption creates a structural demand story for Haynesville gas that extends decades into the future—exactly the kind of long-duration thesis that patient capital can exploit.

VIII. Recent Developments & Financial Performance

The first three quarters of 2025 demonstrated Comstock's operational execution and the impact of improved natural gas pricing.

Natural gas and oil sales, including realized hedging gains, were $405 million for Q1 2025. Operating cash flow was $239 million or $0.81 per diluted share. Adjusted EBITDAX for the quarter was $293 million.

The company achieved natural gas and oil sales of $344 million in Q2, with operating cash flow of $210 million and adjusted EBITDAX of $260 million. Natural gas and oil sales, including realized hedging gains, were $344 million for the quarter. Operating cash flow was $210 million or $0.71 per diluted share. Adjusted EBITDAX for the quarter was $260 million.

Natural gas and oil sales, including realized hedging gains, were $335 million for Q3 2025. Operating cash flow was $190 million or $0.65 per diluted share. Adjusted EBITDAX for the quarter was $249 million.

The company maintained impressive margins. Comstock's unhedged operating margin was 74% during the first nine months of 2025 and 75% after hedging.

Operating efficiency remained strong. Comstock has turned 28 wells to sales to date in 2025 in its Legacy Haynesville area with an average lateral length of 11,919 feet and a per well initial production rate of 25 MMcf per day.

Comstock also moved to optimize its portfolio. On October 10, 2025, the Company entered into an agreement to sell its Shelby Trough properties in Nacogdoches, San Augustine and Shelby counties in Texas for $430.0 million to an unaffiliated third party.

"The transaction is expected to close in December 2025, with proceeds earmarked for debt reduction."

A symbolic milestone came in May 2025. Comstock Resources announced a dual listing of its common stock on NYSE Texas, the newly launched fully electronic equities exchange headquartered in Dallas, Texas.

The company joins as a Founding Member of NYSE Texas, demonstrating its commitment to Texas's economic growth.

IX. Key Players & Leadership

M. Jay Allison: The Ultra-Marathon CEO

M. Jay Allison has been a director since 1987, and our Chief Executive Officer since 1988. Mr. Allison was elected Chairman of the board of directors in 1997. From 1988 to 2013, Mr. Allison served as our President and before that he served as our Vice President and Secretary.

Allison's background combined legal expertise with entrepreneurial instinct. From 1981 to 1987, he was a practicing oil and gas attorney with the firm of Lynch, Chappell & Alsup in Midland, Texas.

Jay, a native of Texas, is one of its longest-tenured CEOs in the oil and gas industry. He earned his undergraduate degree, master's degree in economics and his law degree at Baylor University, then worked at law firm Lynch, Chappell & Alsup representing oil and gas companies for about five years.

His character reveals itself in unexpected ways. The ups and downs associated with growing from a small startup to the phenomenally successful business Comstock Resources is today took substantial endurance; something which Jay is no stranger to, having been an accomplished ultra-marathon runner. Just as he embraced the challenge of the races, so he has embraced the challenge of surviving and thriving in the challenging and ever-changing oil and gas industry in North America.

"Playing football under Coach Grant Teaff taught me to continue to give my best – no matter what," he said. "I remember my freshman year at Baylor, we were behind at half-time against the University of Texas and overcame a 24-point deficit to beat them."

Jerry Jones: Patient Capital Personified

Strategic relationship with successful Dallas businessman Jerry Jones, the company's largest shareholder, whose investment to date in Comstock totals $1.1 billion.

Jones's investment philosophy reflects lessons learned from decades in both oil and gas and professional sports. "I do think that if you can be where the rocks are, if you can have it cheap, if you can aggregate it to a point where you can put it out there when people need it but yet you can hold your own when they don't need it, then that's a good place to be."

"The greatest wealth is in the gas," Jones said. "It's much bigger than the Cowboys."

His approach to hedging reveals operational philosophy: "The best way I know to hedge is to not owe any money. Since the day that I got into Comstock, I've been doing everything we can do to get to where you don't have to have the gas to sell to make your balance sheet work."

The Allison-Jones partnership represents an unusual but effective combination: operational expertise meeting patient capital, long institutional memory meeting long-term investment horizons.

X. Playbook: Business & Strategy Lessons

Comstock's evolution offers a masterclass in E&P strategy during an era of capital market hostility toward the sector.

Lesson 1: Patient Capital Transforms Strategic Optionality

When capital markets closed to E&Ps in the late 2010s, most companies faced impossible choices: stop drilling, sell assets at distressed prices, or pursue high-cost capital structures. Jones's backing gave Comstock a third path—continuing to invest counter-cyclically while competitors retrenched.

Lesson 2: Countercyclical Acquisition

The Western Haynesville land grab exemplifies the power of buying when others are fearful. "We added 98,000 net acres at $550 an acre," Allison says. By comparison, other notable Haynesville players were paying as much as $30,000 an acre when the leasing land rush in the Haynesville first began some 15 years ago.

Lesson 3: Geographic Moat

Not all gas basins are created equal. The Haynesville's proximity to LNG export terminals and Gulf Coast industrial demand creates structural advantages that distant basins cannot replicate regardless of their geological quality.

Lesson 4: Consolidation Strategy

Allison claims Comstock Resources' strategy is "completely different" from other companies, as the company is focused on exploration to find reserves while most of its competitors are focused on acquisitions to add drilling inventory.

Lesson 5: Operational Excellence Under Extreme Conditions

The Western Haynesville pushed drilling technology to its limits—400°F+ temperatures, 19,000-foot depths, extreme pressures. The unforgiving conditions of the play: deep, overpressured and hot require cutting edge drilling technology and high proppant loads, making wells structurally very expensive. Producers have thus far made some strides in bringing down drilling days. Early wells consistently took about 80 days from spud to total depth, with some as high as 133.

XI. Competitive Analysis: Porter's 5 Forces

Threat of New Entrants: LOW

The Haynesville is dominated by large publics, international players (BP, TG Natural Resources, Sabine Oil & Gas) and an expensive private (Aethon Energy).

The list of likely Haynesville sellers is short and quickly getting shorter. Privately held Aethon Energy, the Haynesville's second-largest producer, continues to explore its options.

High capital requirements, established infrastructure, and limited acreage availability create substantial barriers. The basin's consolidation makes meaningful entry nearly impossible without paying premium valuations.

Supplier Power: MODERATE

Oilfield services companies—drilling contractors, completion crews, equipment providers—retain pricing power during high-activity periods. However, Comstock's scale provides negotiating leverage that smaller operators lack.

Buyer Power: LOW-MODERATE

Haynesville producers benefit from proximity to multiple demand centers. LNG export terminals provide additional offtake options, reducing buyer concentration. Henry Hub pricing mechanisms ensure relatively transparent markets.

Threat of Substitutes: MODERATE-HIGH

Renewable energy growth presents long-term substitution risk for power generation. However, natural gas remains critical for baseload power, industrial heat, and chemical feedstock—applications where substitution is difficult or impossible. The LNG export market provides global demand exposure that partially diversifies domestic substitution risk.

Competitive Rivalry: MODERATE

Public majors, like Expand Energy, Comstock Resources and BPX, are deep in Haynesville for the long haul. So are institutionally backed players like TGNR and Sabine Oil & Gas, majority owned by Japanese utility Osaka Gas.

Basin consolidation has reduced the cutthroat competition that characterized earlier periods. Most remaining operators focus on capital discipline rather than market share gains.

XII. Hamilton's 7 Powers Analysis

Scale Economies: STRONG

As basin leader, Comstock spreads fixed costs across the largest production base, achieving the industry's lowest cost structure. Comstock maintains that it has the "industry's lowest producing cost structure," which positions it well to benefit from natural gas price recoveries.

Network Effects: WEAK

Commodity production doesn't exhibit network effects. Gas molecules are fungible; customers don't benefit from other customers using Comstock gas.

Counter-Positioning: STRONG

"We're going to grow it organically, not with M&A." While peers focus on capital discipline and returning cash to shareholders, Comstock's growth-oriented strategy represents a fundamentally different bet—one enabled by patient capital that public market investors typically won't provide.

Switching Costs: WEAK

Natural gas is a commodity product. Buyers can switch suppliers freely based on price and availability.

Branding: WEAK

Commodity products don't command premium pricing. A molecule of methane from Comstock is identical to one from any other producer.

Cornered Resource: STRONG

Comstock's Western Haynesville position—500,000+ net acres assembled at attractive prices—represents a resource that competitors cannot easily replicate. The new Bossier and Haynesville shale play north of Houston is delivering wells with some 20 Bcf in just three years—more than 3 Bcf per 1,000 lateral feet.

Jerry Jones's capital backing is itself a cornered resource—patient capital willing to fund counter-cyclical investment when public markets won't.

Process Power: MODERATE-STRONG

Comstock has developed proprietary techniques for extreme Western Haynesville conditions. Comstock's unhedged operating margin was 73% in the second quarter of 2025 and 74% after hedging.

Dominant Powers: Cornered Resource (Western Haynesville acreage + patient capital) and Scale Economies

XIII. Competitive Landscape

The Haynesville competitive landscape has consolidated dramatically, with a handful of large operators controlling most production.

Already the fourth-largest Haynesville gas producer and the largest producer on the East Texas side of the basin by year-end 2024, TG Natural Resources announced an acquisition of 70% of Chevron's East Texas assets in April.

Key competitors include:

Expand Energy (merged Chesapeake/Southwestern): The largest public gas producer in the U.S., with substantial Haynesville exposure alongside Appalachian assets. With Comstock and Mitsui drilling outside of this initial area and Expand leasing acreage to the east, results should soon begin to come in signaling to what extent this performance can be replicated north and eastward.

Aethon Energy: Privately held Aethon Energy, the Haynesville's second-largest producer, continues to explore its options. The company is rumored to be for sale or pursuing an IPO in the range of $10 billion.

TG Natural Resources: Tokyo Gas subsidiary with growing Haynesville presence.

BP: International major with significant Haynesville exposure.

Comstock's differentiation centers on pure-play Haynesville focus, Western Haynesville frontier development leadership, and patient capital backing.

XIV. Bear vs. Bull Case

Bull Case

Bulls point to a looming wall of demand, mostly from new LNG projects but also from data centers, AI and power generation.

The LNG export capacity expansion is structural and largely committed. Plaquemines LNG Phase 1 shipped its first cargo in December 2024, while Plaquemines Phase 2 and Corpus Christi Stage III began shipping earlier in 2025 but have not yet entered commercial operation. Five additional US LNG projects have reached final investment decision and are under construction.

Western Haynesville success could add decades of inventory at attractive economics. The data center power thesis provides an additional demand catalyst beyond LNG.

Bear Case

The energy transition presents long-term demand uncertainty. Regulatory and ESG pressures may increase, potentially affecting access to capital and permitting timelines.

Comstock has outspent operating cash flows in recent periods, relying on bank borrowings to fund development. While Jerry Jones's backing provides financial flexibility, leverage remains elevated relative to peers focused on capital discipline.

Single-basin concentration creates geographic risk—regulatory changes, infrastructure constraints, or geological disappointments in the Western Haynesville could disproportionately impact the company.

The additional infrastructure from both basins will increase scope for competition between Haynesville and Permian producers. Associated gas from Permian oil drilling represents low-marginal-cost supply that could pressure gas prices regardless of demand growth.

Key Performance Indicators to Monitor

For investors tracking Comstock's progress, three metrics deserve closest attention:

-

Natural Gas Realized Prices vs. Hedging Position: Comstock hedges approximately 50% of near-term production. The spread between unhedged and hedged realizations reveals both commodity exposure and hedging effectiveness.

-

Western Haynesville Well Performance and Cost Trends: Initial production rates, estimated ultimate recoveries, and drilling/completion costs per lateral foot will determine whether the Western Haynesville achieves economic parity with legacy positions.

-

Leverage Ratio Trajectory: Net debt to EBITDAX reveals whether cash flows are sufficient to fund development while reducing leverage—or whether the company remains dependent on external capital.

XV. Epilogue: What's Next?

Comstock Resources stands at an inflection point. The next three years will determine whether the company's Western Haynesville bet produces transformational returns or proves a bridge too far.

CEO Jay Allison expressed strong confidence: "We have never been more positive about the Western Haynesville."

The LNG export thesis is finally materializing after years of delay. Commodity Insights analysts expect LNG feedgas to climb by roughly 3 Bcf/d in 2025 alone relative to last year's average of 13.2 Bcf/d.

The data center partnership with NextEra represents a potential new revenue stream and demand source. The Juno, FL-based unit of NextEra added 3.2 GW to its backlog in 2Q2025, including 1 GW-plus serving hyperscalers.

The fundamental question remains: Can Comstock convert its acreage advantage into sustainable free cash flow? The company has assembled one of the most compelling resource positions in American energy. Executing on that potential while managing leverage and commodity volatility will define the next chapter of this improbable corporate saga.

From a Nevada silver mine drainage company to a potential energy infrastructure platform serving America's insatiable demand for natural gas—Comstock Resources embodies both the creative destruction and reinvention that define American capitalism. Whether Jerry Jones's biggest bet outside of professional football produces another 5,000% return remains to be seen. But the stage is set, the pieces are in place, and the demand wave is arriving.

XVI. Further Reading

Top 10 Resources for Further Study:

- Comstock Resources Investor Relations – SEC filings, investor presentations, earnings transcripts

- "The Prize" by Daniel Yergin – Essential context on energy industry history

- EIA Haynesville Shale Region Drilling Productivity Report – Monthly basin production data

- Hart Energy DUG Gas Conference Coverage – Industry perspectives on Haynesville development

- Natural Gas Intelligence – Daily Haynesville and LNG market coverage

- RBN Energy Blog – Deep dives on natural gas market dynamics

- Comstock's Western Haynesville Technical Presentations – Geological and operational details

- "The Frackers" by Gregory Zuckerman – History of the shale revolution

- EIA LNG Export Capacity File – Tracking U.S. liquefaction capacity expansion

- D CEO Magazine Profiles – Texas business journalism on the Allison-Jones partnership

Comstock Resources represents one of the most fascinating transformation stories in American energy. From its origins as a 19th-century Nevada mining relic to its current position as a dominant force in one of America's most strategic natural gas basins, the company embodies the power of patient capital, operational excellence, and strategic positioning. The next chapter—LNG exports, data center power demand, and Western Haynesville development—may prove the most consequential yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube