Cincinnati Financial: The Agent's Insurance Company

I. Introduction & Episode Roadmap

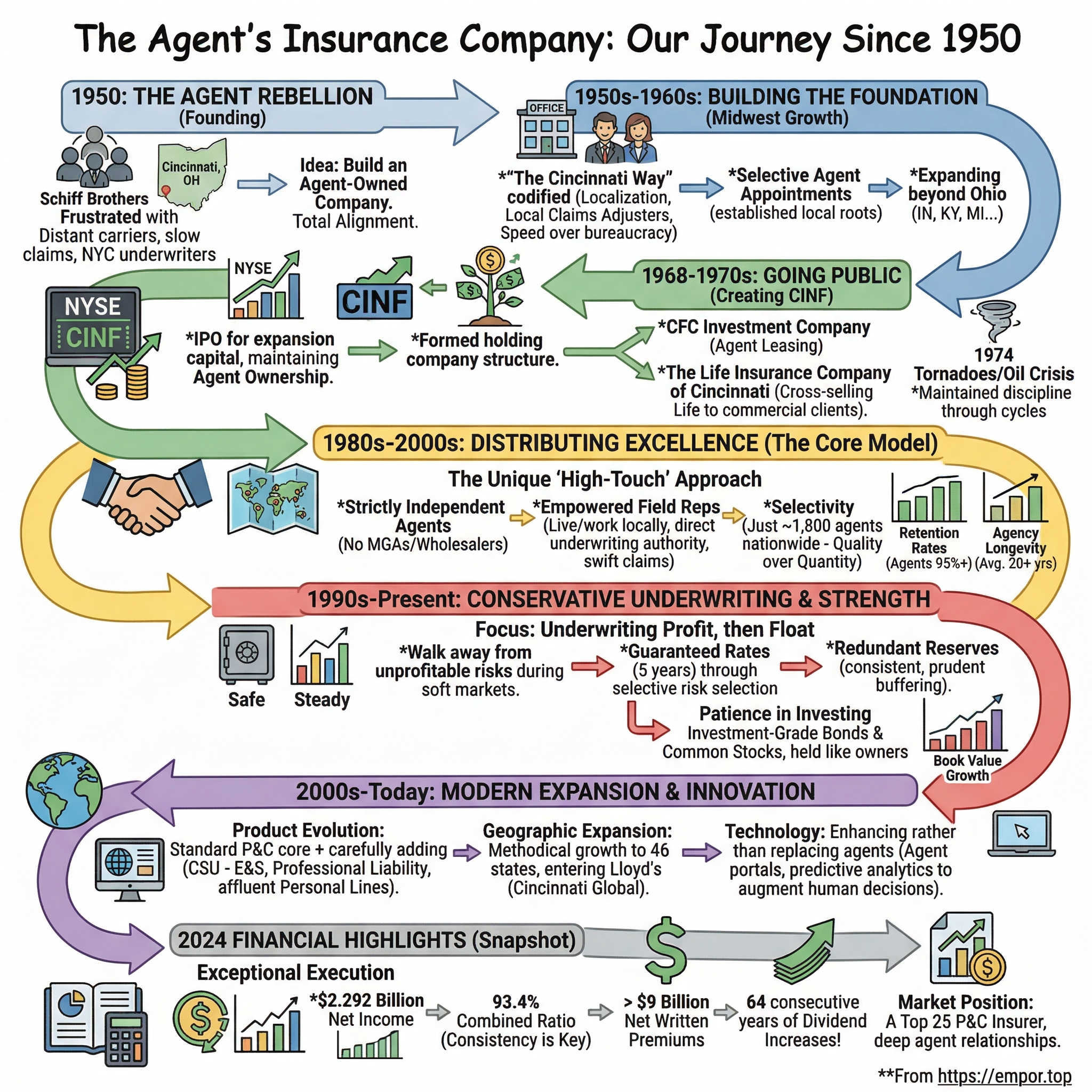

Picture this: It's 1950 in Cincinnati, Ohio. Four insurance agents are sitting around a table, frustrated. They're tired of distant insurance companies treating them like order-takers rather than partners. Tired of slow claims payments that make them look bad to their neighbors. Tired of underwriters in New York or Hartford who've never set foot in Ohio telling them which risks to write. So they do something radical—they start their own insurance company.

Among these rebels are the Schiff brothers—John Jack and Robert Cleveland—whose names would become synonymous with a different way of doing insurance. Their creation, Cincinnati Insurance Company, would grow from this moment of frustration into something remarkable: a top 25 property casualty insurer commanding over $9 billion in net written premiums, all while staying true to that original vision of putting agents first.

The paradox is striking. In an era where State Farm, GEICO, and Progressive have spent billions convincing Americans to buy insurance directly online or through captive agents, Cincinnati Financial has thrived by doing the opposite—doubling down on independent agents as the centerpiece of their strategy. While InsurTech startups promise to "disrupt" insurance with AI and algorithms, Cincinnati quietly generates 19.8% value creation ratios by having real people answer the phone in small towns across America.

This is a story about patience in an impatient world. About relationships in a transactional industry. About how a company that started as an agent rebellion became the agent's insurance company—and why that matters more today than ever. We'll trace the journey from that founding moment through public markets, geographic expansion, and digital transformation, all while never losing sight of the original insight: insurance is ultimately about trust between neighbors.

Key themes will emerge throughout: the power of aligned incentives when agents become owners, the competitive advantage of conservative underwriting across cycles, and how patient capital can compound value over decades. Most importantly, we'll explore why "boring" insurance—done right—can be one of the best businesses in the world.

II. The Agent Rebellion: Founding Story (1950)

The year is 1950. Harry Truman is president. The Korean War has just begun. And in Cincinnati, the insurance industry is experiencing its own kind of conflict—a quiet rebellion brewing in the offices of independent agents across Ohio.

To understand the frustration, you need to understand post-WWII America's insurance landscape. The big Eastern companies—Hartford, Travelers, Aetna—dominated the market. They operated through independent agents but treated them as disposable distribution channels. Claims adjusters might take weeks to arrive from distant cities. Underwriting decisions came down from ivory towers with little regard for local conditions. Agents who'd built relationships over decades watched helplessly as their carriers pulled out of states or canceled long-standing customers over minor claims.

John Jack Schiff saw this differently. A Cincinnati native and independent agent himself, he understood something the Eastern establishment missed: insurance in Middle America wasn't about actuarial tables and standardized policies. It was about the agent who coached your kid's Little League team writing your auto policy. It was about getting your barn roof claim paid quickly so you could get the harvest in. It was about trust.

Jack and his brother Robert Cleveland Schiff had grown up in Cincinnati's tight-knit business community. Their father had been in insurance. They knew every agent, every business owner, every banker in town. And they kept hearing the same refrain: "Why can't we have an insurance company that actually understands Ohio?"

The brothers' solution was audacious: create the first insurance company owned exclusively by Ohio insurance agents and Cincinnati businessmen. Not just another mutual or stock company that happened to use agents—but a company where agents were literal shareholders, board members, and strategic partners.

The initial capitalization came from an extraordinary coalition. Nearly 1,000 independent agencies across Ohio pooled resources. Local Cincinnati business leaders—manufacturers, retailers, bankers who were tired of sending premium dollars east—joined in. The message was clear: this would be Ohio's insurance company, run by Ohioans, for Ohioans.

But the Schiffs' vision went beyond geography. They were betting on a radical philosophy: treat agents not as distribution costs to be minimized, but as partners to be empowered. Give them real equity—not just commissions but actual ownership stakes. Let them influence underwriting decisions. Most importantly, back them up with the fastest claims service in the industry.

The founding charter, drafted in those first months of 1950, embedded these principles. Unlike traditional insurers who might have hundreds of products and complex rate structures, Cincinnati would keep things simple. They would write standard risks that agents understood. They would price fairly and stick to those prices—no bait-and-switch tactics. Claims would be handled by local adjusters who lived in the communities they served.

One early employee recalled the first company meeting: "Jack Schiff stood up and said, 'Gentlemen, we're not building an insurance company. We're building a partnership. Every agent in this room isn't just selling our policies—you own this company. When a customer has a claim, it's your reputation and our reputation on the line together.'"

This agent-centric DNA would manifest in countless small decisions. While other insurers required agents to funnel all communication through regional offices, Cincinnati gave agents direct phone lines to underwriters. While competitors might take 30-60 days to pay claims, Cincinnati aimed for same-week payments. While others treated appointment as an agent like a privilege they could revoke, Cincinnati viewed it as a marriage—for better or worse.

The early months were lean. Operating out of a modest office in downtown Cincinnati with just a handful of employees, the company wrote its first policy in 1950. The premium was small—a few hundred dollars for a commercial property risk. But what mattered wasn't the size; it was the principle. An Ohio agent had placed business with an Ohio company that he partially owned, and both had skin in the game to make it work.

The radical bet on relationship-based insurance would be tested immediately. That first year, several claims came in that tested their resolve. A factory fire. A tornado that hit a farm. Each time, Cincinnati's adjusters were on-site within hours, checks in hand. Word spread through the agent network: this new company actually delivered on its promises.

By year's end, Cincinnati Insurance had written just over $1 million in premiums—tiny by industry standards. But something more valuable had been established: proof that insurance could work differently. Agents started moving more business to Cincinnati. Policyholders began asking for Cincinnati specifically. The rebellion had found its foothold.

III. Building the Foundation: Early Growth (1950s-1960s)

By 1952, Cincinnati Insurance had been operating for two years, exclusively through independent agents who agreed that insurance was fundamentally a relationship business. But Jack Schiff knew that philosophy alone wouldn't build a company. They needed to codify what would become known as "The Cincinnati Way."

The first principle was radical localization. While Hartford might have one claims adjuster covering three states from a regional office, Cincinnati embedded claims people in every town where they had significant business. These weren't just contractors or part-timers—they were full employees who lived, worked, and raised families in these communities. When the hardware store on Main Street had a fire, the adjuster who showed up wasn't a stranger with a clipboard but Tom from the Rotary Club.

An agent from Dayton recalled the difference: "I had a customer with tornado damage to his grain silos. With our previous carrier, it took three weeks to get an adjuster out from Cleveland, another two weeks for approval, then another month for payment. With Cincinnati, Bill—who lived two towns over—was there that afternoon with a check. The farmer was back in business before the other carriers had even finished their paperwork."

This speed wasn't accidental. The Schiff brothers had designed the company with minimal bureaucracy. Claims under certain thresholds could be approved by field staff immediately. No committees, no multiple sign-offs, just trust in their people's judgment. This occasionally led to overpayment, but the goodwill generated far exceeded the cost.

The second principle was selectivity in agent appointments. While other insurers chased growth by appointing any agent with a license, Cincinnati was deliberately choosy. They looked for established agencies with deep community roots, multi-generational businesses where the owner's name was on the door. The vetting process was intense—financial reviews, community reputation checks, even assessment of the agent's civic involvement.

"We weren't looking for order-takers," explained an early executive. "We wanted partners who understood that every policy they wrote reflected on both of us. If an agent wasn't willing to stake their reputation on our claims service, we didn't want them."

This selectivity paid dividends in quality. Cincinnati's loss ratios consistently ran below industry averages, not because they had better actuarial models, but because their agents knew their communities intimately. The agent in Zanesville knew which business owners cut corners on maintenance. The agent in Springfield knew which intersection flooded every spring. This ground-level intelligence was worth more than any predictive model.

Growing through the Midwest in the 1950s meant expanding one relationship at a time. The company would identify a target town—say, Fort Wayne, Indiana. They'd spend months researching the best agencies, understanding the local economy, learning which industries dominated. Then Jack or Robert Schiff would personally visit, often multiple times, building relationships over dinner and golf before ever discussing business.

The approach was intentionally patient. In Columbus, it took eighteen months of courtship before the leading commercial lines agency agreed to appointment. In Louisville, they waited two years for the right personal lines partner rather than settling for second-best. This discipline meant slower growth but higher quality.

By 1960, the company had expanded throughout Ohio and into neighboring states—Indiana, Kentucky, Michigan. Premium volume had grown to $25 million, still small by national standards but representing steady, profitable growth. More importantly, they'd proven the model could scale beyond Cincinnati while maintaining its cultural DNA.

The 1960s brought new challenges. The interstate highway system was transforming America, creating new risks and opportunities. Shopping centers were replacing downtown retail districts. Suburban sprawl meant new homes, new drivers, new businesses—all needing insurance. Cincinnati had to evolve while staying true to its roots.

They responded by deepening agent support. While other carriers were cutting commission rates to improve margins, Cincinnati introduced profit-sharing arrangements that gave agents additional upside when their books performed well. They established training programs, bringing agents to Cincinnati for multi-day sessions on underwriting, claims, and risk management. They even helped agents with financing for office expansions and technology upgrades.

One innovation was the field marketing representative role. These weren't sales managers in the traditional sense—they were former agents themselves who now worked full-time supporting other agencies. Living in the territories they covered, they became bridges between home office and Main Street, translating corporate initiatives into local language and carrying field feedback back to Cincinnati.

The investment in relationships showed remarkable returns. By the late 1960s, Cincinnati's retention rates—both for policies and agents—far exceeded industry norms. Agencies that appointed Cincinnati rarely terminated the relationship. Policyholders renewed at rates approaching 90%. In an industry where a few percentage points of retention could make or break profitability, these numbers were gold.

The company also began experimenting with product innovation, but always through the lens of agent needs. When agents reported losing commercial accounts because they couldn't offer comprehensive package policies, Cincinnati developed BusinessOwner Policy (BOP) products. When personal lines agents needed simplified underwriting for preferred risks, Cincinnati created streamlined applications that could be completed in minutes.

Every innovation was road-tested with select agencies before broad rollout. Feedback was genuinely incorporated, not just collected. Agents began to see Cincinnati not just as a carrier but as a true partner invested in their success.

By decade's end, the foundation was solid. Premium volume approached $100 million. The company operated in seven states. Most remarkably, agents now owned approximately 20% of the company's equity—a tangible stake that aligned interests perfectly. The agent rebellion had become an agent partnership, setting the stage for the next phase: taking this unique model public.

IV. Going Public: Creating Cincinnati Financial Corporation (1968-1970s)

The late 1960s were intoxicating times on Wall Street. The Dow had crossed 1,000 for the first time. Conglomerates were the rage. Americans, fueled by post-war prosperity, sought new ways to build and protect their financial security. Go-go stocks promised instant wealth. Against this backdrop, the Schiff brothers faced a dilemma that would define Cincinnati's next chapter.

The company needed capital to fund expansion, but taking outside investment risked diluting the very agent ownership that made them special. The solution was elegant: form a holding company structure that could access public markets while preserving the agent-centric culture. In 1968, Cincinnati Financial Corporation was born as an Ohio corporation, with Cincinnati Insurance Company as its primary subsidiary.

The IPO roadshow was unlike anything Wall Street had seen. Instead of emphasizing growth projections and market disruption, Jack Schiff talked about relationships and patient underwriting. When analysts asked about technology investments, he discussed the importance of local claims adjusters. When they pressed on expansion plans, he explained their deliberate, relationship-first approach to entering new markets.

"The investment bankers thought we were crazy," recalled a board member. "Here's the stock market on a tear, everyone wanting the next hot growth story, and we're talking about moving slowly and empowering insurance agents. But Jack insisted: 'We're not changing who we are to please Wall Street.'"

The offering was modest by contemporary standards but revolutionary in structure. Existing agent-shareholders were given first priority to maintain their ownership stakes. Many doubled down, seeing public listing not as an exit opportunity but as validation of their long-term bet. The prospectus itself read more like a partnership agreement than a typical securities filing, emphasizing the company's commitment to agent relationships over quarterly earnings.

Public listing brought unexpected benefits. The transparency required by SEC filings actually strengthened agent relationships—partners could now see exactly how their company was performing. The liquidity of public shares made it easier for younger agents to buy in, refreshing the ownership base. And the discipline of regular earnings calls forced management to articulate their strategy clearly, reinforcing the cultural values.

But the Schiffs understood that insurance companies needed diversification beyond just property-casualty lines. In 1970, they established CFC Investment Company, a subsidiary designed to manage real estate investments and, crucially, to further support agents through vehicle and equipment leasing programs. This wasn't about financial engineering—it was about solving real agent problems. Many agencies needed to finance computers, company cars, even office furniture. CFC Investment could provide attractive lease terms, keeping more economics within the Cincinnati family.

The real strategic leap came in 1972 with the formation of The Life Insurance Company of Cincinnati. The decision to enter life insurance wasn't made lightly. Life insurance required different expertise, different reserves, different distribution dynamics. But agents had been asking for years: their commercial clients needed key person insurance, their personal lines customers wanted term life, and they were losing these relationships to other carriers.

The life insurance debut was overshadowed by Cincinnati's first significant merger—though "merger" might overstate what was really an acquisition of a small, troubled Ohio life insurer that provided the necessary licenses and infrastructure. Rather than impose Cincinnati Insurance's property-casualty approach wholesale, they spent months understanding life insurance's unique requirements. They hired experienced life underwriters, built separate systems, created distinct products.

But the distribution strategy remained consistent: life products would be sold exclusively through Cincinnati's existing property-casualty agents. This created powerful cross-selling opportunities. An agent could now handle all of a small business's insurance needs—property, liability, workers' compensation, and key person life—with one carrier relationship.

The 1970s brought external challenges that tested the newly public company. The 1973 oil crisis triggered inflation that wreaked havoc on insurance economics. The 1974 tornado season was particularly devastating across Cincinnati's Midwest footprint. Investment markets gyrated wildly. Through it all, Cincinnati maintained its steady approach: conservative underwriting, quick claims payment, agent partnership.

One defining moment came in 1975 when several major carriers pulled out of Ohio after the state implemented new rate regulations. While competitors saw crisis, Cincinnati saw opportunity. They kept writing business, even accepting some transfers from departing carriers. Agents who had been abandoned by national carriers suddenly found Cincinnati willing to stand by them. The loyalty this generated would last decades.

The public market structure also enabled Cincinnati to pioneer innovative compensation approaches. In 1976, they introduced an agent stock purchase program that provided financing for agencies to acquire Cincinnati Financial shares. The terms were generous—below-market interest rates, extended payment periods—because the company understood that agent-owners were their best ambassadors.

By 1978, the transformation was complete. Cincinnati Financial Corporation had successfully transitioned from private agent-owned insurer to public company while maintaining its cultural DNA. The company now operated in twelve states, offered both property-casualty and life insurance, and had developed a sophisticated investment operation. Annual revenues exceeded $500 million. The stock had appreciated steadily, rewarding both institutional investors who bought the IPO and agents who held from the beginning.

Yet visiting headquarters, you wouldn't know this was a public company. The executive offices remained modest. Jack Schiff still answered his own phone. Claims adjusters still had authority to write checks on the spot. Board meetings included numerous agent-directors who weren't afraid to challenge management on behalf of the field.

The decade closed with a symbolic moment. At the 1979 annual meeting, an analyst asked Jack Schiff whether Cincinnati would ever abandon the independent agent channel for the faster-growing direct distribution model. Schiff's response was immediate: "We are successful because of our agents, not despite them. The day we forget that is the day we stop being Cincinnati." The room—filled with agents who were also shareholders—erupted in applause.

V. The Agent-Centric Model: Distribution Excellence

To truly understand Cincinnati Financial's enduring success, you need to spend a day with Tom Richardson, a field representative based in Fort Wayne, Indiana. It's 6 AM, and Tom's already at his kitchen table, reviewing loss runs for an agency he's visiting today. By 7 AM, he's on the phone with an underwriter in Cincinnati, advocating for a risk that doesn't quite fit the standard guidelines but makes sense because he knows the business owner personally. By 8 AM, he's at the agency, not in a corporate conference room but in the back office where the real work happens, sleeves rolled up, helping a young producer understand why a particular risk was declined and how to reshape it for approval.

This is the independent agent channel strategy that Cincinnati has perfected over seven decades: distribute insurance products through locally based independent agencies who have deep relationships in their communities and irreplaceable marketplace intelligence. But what Cincinnati does differently is how they support these agents.

Unlike most carriers who rely on wholesalers, Managing General Agents (MGAs), or Managing General Underwriters (MGUs) to reach smaller agencies, Cincinnati maintains a strict policy: distribute only through appointed agents of Cincinnati Insurance. No intermediaries. No delegated underwriting authority to third parties. Every risk is evaluated by a Cincinnati employee. Every claim is handled by Cincinnati staff. Every agent relationship is direct.

"We've had private equity firms approach us about using MGAs to accelerate growth," explains a senior executive. "They show us models where we could triple our premium in three years. But that's not who we are. The moment you insert intermediaries, you lose the direct connection to the risk. You lose the alignment of interests. You lose control of the customer experience."

The field representative model is the cornerstone of this direct relationship. These aren't traditional sales managers measured on premium growth and new appointments. Cincinnati's field reps—about 200 of them—work from their homes in the same communities as their agents and policyholders. They're measured on agency profitability, retention, and satisfaction scores. Many have been in their territories for decades, becoming fixtures in the local insurance community.

The model creates powerful advantages. When Hurricane Ike swept through Ohio in 2008—yes, a hurricane in Ohio—Cincinnati's field reps were deployed as emergency adjusters. They knew every damaged property, every business owner, every local contractor who could handle repairs. Claims that might have taken weeks with out-of-state adjusters were settled in days. One agent remarked: "My Cincinnati rep was at my biggest client's warehouse before I was. He had emergency funding approved before lunch. Try getting that from a carrier based in Hartford."

Agent selection remains deliberately exclusive. While the company now operates in 46 states, they have just over 1,800 appointed agencies—a tiny number compared to competitors. Progressive has over 35,000 independent agency relationships. Travelers has over 13,000. Cincinnati's average agency produces five times the premium volume of industry norms because the company invests so heavily in each relationship.

The vetting process for new agents has evolved but remains intense. Financial stability reviews. Five-year business plans. Site visits to observe operations. Reference checks with other carriers. Even assessment of succession planning—Cincinnati wants agencies that will last generations, not just until the current owner retires.

"We turned down an agency last year that was writing $50 million in premium," notes a field underwriting manager. "The numbers looked great, but when we visited, we saw corners being cut. Quick-quote shops focused on price, not coverage. High turnover in their service staff. That's not our kind of partner."

Once appointed, agents enter what Cincinnati calls the "partnership phase." This isn't just rhetoric. Agencies get access to proprietary analytics showing their book's performance versus peer agencies. They receive regular profitability consultations—not sales calls, but genuine advisory sessions on improving their economics. Cincinnati even helps with agency perpetuation planning, financing junior partners' buy-ins to ensure continuity.

The company's approach to empowering field representatives is equally distinctive. While most carriers centralize authority, Cincinnati pushes decision-making to the field. Representatives have underwriting authority up to significant limits. They can approve rate exceptions. They can authorize claims payments. They can even commitment to multi-year rate guarantees for important accounts.

This empowerment requires trust but generates enormous returns. Response times are measured in hours, not days. Agents get answers while customers are still in their offices. Field reps become genuine partners in agency success rather than corporate enforcers of home office edicts.

The human touch extends to technology deployment. While Cincinnati has invested hundreds of millions in digital capabilities, they've done so in ways that enhance rather than replace personal relationships. Their agent portal isn't designed to eliminate phone calls but to make conversations more productive by putting information at everyone's fingertips. Their automated underwriting doesn't remove human judgment but accelerates routine decisions so underwriters can focus on complex risks.

The contrast with direct writers and captive agent models is stark. State Farm agents can only sell State Farm products. GEICO eliminates agents entirely. Even independent agency carriers like Travelers or The Hartford often seem to view agents as necessary evils—costs to be managed rather than partners to be cultivated.

Cincinnati's model shows in the numbers. Their agent retention rate exceeds 95% annually—virtually unheard of in an industry where carriers routinely cull agencies and agents regularly move books between carriers. The average Cincinnati agency relationship is over 20 years old. Many span three generations of family ownership.

But perhaps the most telling statistic comes from surveys: when asked to rank their carriers, over 70% of Cincinnati's appointed agents rate them as their "#1 preferred market"—not just for certain products or customer segments, but overall. In an industry built on relationships, Cincinnati has made itself the relationship carrier of choice.

VI. Conservative Underwriting & Financial Strength

In 2008, while AIG teetered on collapse and required $182 billion in federal bailouts, Cincinnati Financial quietly reported an underwriting profit. While competitors chased growth by loosening standards and cutting prices, Cincinnati maintained discipline. The philosophy hasn't changed since the Schiff brothers' era: underwriting profit first, investment income second. In insurance, this is almost heretical.

Most insurers operate on the "cash flow underwriting" model—accept break-even or even unprofitable premium to generate float, then invest aggressively to create returns. It works until it doesn't. When investment markets crash or catastrophes spike, companies without underwriting discipline face existential crisis. Cincinnati plays a different game entirely.

"We assume we'll make zero on investments," explains a senior underwriter, exaggerating only slightly. "Every risk needs to stand on its own merits. If we can't price it to make an underwriting profit, we don't write it. Period."

This discipline manifests in specific practices. During the soft market of 2015-2018, when commercial insurance prices dropped 20% or more, Cincinnati walked away from millions in premium rather than chase market share. They watched competitors buy business with unsustainable pricing and waited. When the market inevitably hardened, Cincinnati was positioned to grow profitably while competitors scrambled to fix broken books.

The company's approach to guaranteed rates illustrates their conservatism. In the 1990s, Cincinnati pioneered policies with premiums that wouldn't increase for up to five years—an almost unheard-of commitment in commercial lines. Competitors thought they were crazy. How could you guarantee rates without knowing future loss trends, inflation, or regulatory changes?

The answer was conservative initial pricing and selective underwriting. Cincinnati would rather lose business upfront than write it cheaply and face ugly renewal conversations later. Agents loved it because they could promise clients stability. Customers loved it because they could budget accurately. And Cincinnati made it work by being right about risk more often than wrong.

The company's reserving practices are similarly conservative. While regulations require reserves sufficient to pay expected claims, Cincinnati consistently maintains reserves 10-15% above actuarial best estimates. This "redundancy" costs money—it reduces reported earnings and returns on equity. But it provides a fortress balance sheet that weathers any storm.

During the 2004-2005 hurricane seasons—Katrina, Rita, Wilma—Cincinnati paid out hundreds of millions in claims. But unlike some competitors who needed emergency capital raises or reinsurance bailouts, Cincinnati simply absorbed the losses and kept writing. Their conservative reserves meant catastrophes were painful but never existential.

The investment strategy perfectly complements this underwriting philosophy. While some insurers chase yield through complex derivatives, private equity, or high-yield bonds, Cincinnati keeps things simple. As of 2024, their portfolio consists primarily of investment-grade bonds and common stocks of dividend-paying companies. No derivatives. No hedge funds. No complex structured products.

The equity allocation—roughly 30% of invested assets—is particularly distinctive. Most insurers avoid significant equity exposure because of volatility. Cincinnati embraces it because they invest like owners, not traders. They've held positions in companies like Fifth Third Bank and Procter & Gamble for decades. The unrealized gains on these positions—over $4 billion—provide additional financial flexibility.

"We're not trying to outsmart the market," notes the chief investment officer. "We're trying to compound wealth over generations. That means owning great businesses for long periods, collecting dividends, and occasionally trimming when valuations get extreme."

This patient approach to both underwriting and investing creates a powerful flywheel. Conservative underwriting generates steady profits. Profits fund investments. Investments appreciate and pay dividends. Investment income supports competitive pricing while maintaining underwriting standards. The cycle perpetuates, building book value year after year.

The numbers tell the story. Cincinnati's book value per share has grown from under $10 in 1990 to $77.06 in 2024—a compound annual growth rate exceeding 6% despite multiple catastrophes, financial crises, and soft markets. Investment income alone now exceeds $1 billion annually, providing a cushion that allows the company to be patient in pricing cycles.

The financial strength shows in ratings. Cincinnati maintains 'A+' ratings from AM Best and Standard & Poor's—ratings they've held for decades. During the 2008 financial crisis, while other insurers faced downgrades, Cincinnati's ratings never wavered. Rating agencies cite consistent operating performance, conservative reserves, and a simple, transparent business model.

But perhaps the best evidence of financial strength is what Cincinnati doesn't do. They don't rely heavily on reinsurance—keeping more risk but also more profit. They don't financial engineer their results through reserve releases or accounting gymnastics. They don't chase hot markets or trendy products. They simply block and tackle, year after year, building value through discipline.

An industry analyst put it perfectly: "Cincinnati is boring in the best possible way. No surprises. No blown quarters. No emergency capital raises. Just consistent execution of a strategy that's worked for 75 years. In insurance, boring is beautiful."

The approach requires patience that public markets rarely reward. When competitors report 20% premium growth, Cincinnati's steady mid-single digits looks pedestrian. When others tout new initiatives in cyber insurance or InsurTech partnerships, Cincinnati's focus on traditional lines seems outdated. But over full cycles—not quarters—the tortoise beats the hare.

VII. Modern Expansion: Products, Geography & Innovation (2000s-Today)

The year 2008 marked a pivotal moment in Cincinnati Financial's evolution. While the world focused on financial system collapse, Cincinnati quietly launched Cincinnati Specialty Underwriters (CSU), their entry into excess and surplus lines insurance. It was classic Cincinnati timing—moving into a new market when others were retrenching, but doing so with characteristic deliberation.

Excess and surplus lines—coverage for risks that standard markets won't touch—might seem antithetical to Cincinnati's conservative DNA. This is the insurance of last resort: nightclubs, haunted houses, demolition contractors. But Cincinnati saw opportunity in bringing discipline to an undisciplined market.

"Everyone thought E&S meant cowboy underwriting," recalls CSU's founding president. "Write anything, charge enough, hope for the best. We believed you could apply Cincinnati's relationship model and underwriting rigor to non-standard risks."

The results vindicated the strategy. CSU has posted 12 straight years of combined ratios at 94 or better, with an average combined ratio over the last 12 years of 81.8—extraordinary profitability in a segment known for volatility. They achieved this by staying true to Cincinnati principles: careful agent selection, local decision-making, fast claims payment, and patient growth.

The geographic expansion over the past two decades tells a similar story of measured ambition. From their Midwest base, Cincinnati methodically moved into new states—but only when they could replicate their model. Entering California in 2004 took three years of preparation. They studied earthquake risk, understood regulatory quirks, built relationships with quality agencies, and hired local talent before writing a single policy.

Today, Cincinnati operates in 46 states, missing only Alaska, Hawaii, Massachusetts, and New York. But the expansion wasn't about planting flags. In many states, they operate in select counties where they have strong agency relationships rather than seeking statewide coverage. Quality over quantity, always.

The international expansion through Lloyd's of London represents Cincinnati's boldest geographic move. In February 2019, they acquired MSP Underwriting, rebranding it Cincinnati Global Underwriting Ltd. This wasn't about abandoning their U.S. focus but about following their commercial clients overseas. When a Cincinnati-insured manufacturer opened a facility in Germany, they previously had to find local coverage. Now Cincinnati could maintain the relationship globally.

Operating through Lloyd's required adaptation. The London market moves faster, relies more on brokers, embraces complexity that Cincinnati typically avoids. But rather than impose their way wholesale, Cincinnati learned from Lloyd's while teaching their relationship approach. The synthesis is working—Cincinnati Global has grown profitably while maintaining underwriting discipline.

Product evolution reveals how Cincinnati balances tradition with innovation. The core remains remarkably consistent—standard commercial property, general liability, commercial auto, workers' compensation. These aren't sexy products, but they're the backbone of American business, and Cincinnati understands them deeply.

But around this stable core, they've carefully added capabilities. Professional liability for small businesses. Cyber coverage for mid-market companies. Executive risk products for private companies. Each addition followed the same pattern: extensive research, careful pilot programs with select agents, gradual rollout, continuous refinement based on field feedback.

The personal lines evolution is particularly interesting. Historically, Cincinnati focused on commercial insurance, viewing personal lines as accommodation business for commercial clients. But agents kept asking for robust personal lines products to capture entire household relationships. Cincinnati listened.

Rather than launch a mass-market personal lines assault competing with GEICO on price, Cincinnati developed products for affluent households—the business owners, professionals, and executives who were already commercial clients. Higher limits, broader coverage, premium service. The same agents writing a business owner's commercial package could now handle their homeowners, auto, and umbrella coverage.

Technology investments reveal Cincinnati's pragmatic approach to innovation. While InsurTech startups promise to revolutionize insurance with artificial intelligence and blockchain, Cincinnati focuses on practical improvements that enhance their model rather than replace it.

Their agent portal evolution exemplifies this philosophy. Instead of forcing agents onto a single platform, Cincinnati built APIs that integrate with whatever agency management systems agents prefer. Instead of replacing phone underwriting with algorithms, they use predictive analytics to help underwriters make better decisions. Instead of eliminating field representatives with digital tools, they equip reps with mobile capabilities to be more effective in the field.

The company's approach to data and analytics is telling. They've invested heavily in capturing and analyzing data—every claim, every risk characteristic, every agency interaction. But the output isn't black-box algorithms making autonomous decisions. It's actionable intelligence that helps humans—underwriters, claims adjusters, field reps—do their jobs better.

"We're not trying to eliminate the human element," explains the chief technology officer. "We're trying to augment it. When an underwriter can instantly see how similar risks have performed, they make better decisions. When an agent can visualize their book's profitability by segment, they write better business. Technology should enhance relationships, not replace them."

The COVID-19 pandemic became an unexpected proof point for Cincinnati's balanced approach. While purely digital insurers struggled with complex business interruption claims that required human judgment, Cincinnati's field representatives pivoted to virtual meetings while maintaining personal relationships. Their technology investments allowed seamless remote work, but their relationship foundation meant agents and customers still felt supported.

Recent initiatives show continued evolution within consistent strategy. Cincinnati Re, launched in 2023, allows the company to reinsure other carriers' risks—leveraging their underwriting expertise in a new way. Cincinnati Private Client targets ultra-high-net-worth individuals with bespoke coverage. Cincinnati Risk Management Services provides loss control consulting to large accounts.

Each initiative extends existing capabilities rather than departing from core competency. The company that started writing straightforward property coverage for Ohio businesses now offers sophisticated global solutions, but the DNA remains unchanged: relationships, underwriting discipline, claims service, patient growth.

VIII. Financial Performance & Market Position

The numbers for 2024 tell a story of exceptional execution in challenging times. Full-year net income of $2.292 billion, or $14.53 per share. Non-GAAP operating income up 26% to $1.197 billion. It's the kind of performance that makes Wall Street analysts reach for superlatives, but for Cincinnati, it's simply the continuation of seven decades of compound growth.

Let's start with the combined ratio—the gold standard metric in property-casualty insurance. Cincinnati posted 93.4% for full year 2024, meaning they earned 6.6 cents of underwriting profit for every premium dollar. In an industry where 100% is breakeven and many carriers routinely exceed it, this is exceptional. But what's more impressive is the consistency: Cincinnati has generated underwriting profits in 30 of the last 35 years, including every year since 2009.

The components reveal the model's strength. The loss ratio of 60.1% reflects disciplined underwriting and favorable reserve development. The expense ratio of 33.3% might seem high versus direct writers like Progressive (around 20%), but it includes agent commissions that direct writers avoid. When you consider that Cincinnati's agents handle customer acquisition and service, the economics are compelling.

Premium growth tells another story. Net written premiums increased 15% for the year to more than $9 billion, with fourth-quarter acceleration to 17%. This isn't growth for growth's sake—it's profitable growth in hardening markets where Cincinnati's disciplined underwriting over soft cycles pays dividends. While competitors scramble to fix underpriced books, Cincinnati grows selectively at adequate rates.

The composition of growth matters. Commercial lines—the historical strength—grew 14% to $5.8 billion. Personal lines grew 18% to $2.1 billion, reflecting the success of their affluent household strategy. Excess and surplus lines surged 26% to $623 million, demonstrating that specialty markets can be both fast-growing and profitable when approached correctly.

Investment income reached a milestone: $1 billion for the year, up 14% from 2023. This isn't from reaching for yield or taking excessive risk. It's the natural result of a growing investment portfolio (now exceeding $20 billion) invested conservatively but wisely. The equity portfolio's unrealized gains of $4.2 billion provide a war chest for future opportunities or challenges.

The value creation ratio—a Cincinnati-specific metric that combines underwriting profit, investment income, and capital appreciation—reached 19.8% for 2024. This holistic measure captures what traditional metrics miss: Cincinnati doesn't optimize for underwriting profit or investment returns in isolation but manages them together for long-term value creation.

Market positioning reveals competitive strength. In commercial lines, Cincinnati ranks among the top 10 writers nationally, with particular strength in small-to-middle market segments where relationships matter most. They're the #1 or #2 carrier for over 40% of their appointed agencies—extraordinary loyalty in an industry where agencies typically spread business across dozens of carriers.

Geographic concentration, once seen as weakness, has become strength. While national carriers struggle with California wildfire exposure or Florida hurricane risk, Cincinnati's Midwest focus provides relative stability. Ohio, Indiana, and Illinois—representing about 35% of premium—face weather risks but not the existential catastrophe exposure of coastal states.

The competitive moat is multilayered. The agent relationships built over decades can't be replicated quickly. The conservative balance sheet allows patient pricing when competitors chase growth. The local market knowledge accumulated over 75 years provides underwriting advantages no algorithm can match. The reputation for fast, fair claims payment becomes self-reinforcing as satisfied customers generate referrals.

Capital allocation demonstrates shareholder focus. Cincinnati has paid dividends for 64 consecutive years, increasing the payout annually since 1961—one of only 41 companies in the S&P 500 with such consistency. The current annual dividend of $3.20 per share yields about 2.2%, attractive in a low-rate environment. Share buybacks supplement dividends, with $200 million repurchased in 2024 at attractive valuations.

But Cincinnati doesn't sacrifice growth for distributions. They maintain capital levels well above regulatory requirements and rating agency standards, providing flexibility for opportunities or adversity. The debt-to-capital ratio of 11% is among the lowest in the industry, eliminating refinancing risk and interest coverage concerns.

Peer comparison illuminates Cincinnati's distinctiveness. Progressive generates higher returns on equity through direct distribution and superior pricing algorithms, but faces technology investment requirements and potential disruption. Travelers offers greater scale and product breadth but struggles with commercial lines profitability. Chubb dominates high-net-worth personal lines but trades at premium valuations. Cincinnati occupies a sweet spot: profitable niche focus, sustainable competitive advantages, reasonable valuation.

The outlook remains constructive. Commercial insurance pricing continues firming after years of soft markets. Social inflation—rising jury awards and litigation costs—favors disciplined underwriters who reserved conservatively. The aging of independent agents creates opportunities as Cincinnati becomes the natural acquirer of books from retiring agents without succession plans.

Technology investments are bearing fruit. Online policy issuance for small commercial risks reduces costs while maintaining the agent relationship. Predictive analytics improve risk selection without eliminating human judgment. Digital claims tools accelerate settlements while field adjusters handle complex situations.

Management's guidance reflects confidence without hubris. They project mid-single-digit premium growth, combined ratios in the low-90s, and steady investment income growth. No hockey-stick projections or transformation initiatives—just continued execution of a proven model.

An insurance analyst summarized it perfectly: "Cincinnati doesn't have the highest returns, the fastest growth, or the most innovative products. What they have is predictability, sustainability, and compounding. In a world of quarterly capitalism, they practice decade capitalism. For long-term investors, that's invaluable."

IX. Playbook: Business & Investment Lessons

Every business school teaches the principal-agent problem—the conflict when managers' interests diverge from owners' interests. Cincinnati Financial solved it elegantly: make the agents literal principals. When independent agents own meaningful equity stakes, every policy written affects their net worth. Every claim paid impacts their investment. This alignment creates behaviors that spreadsheets can't model and contracts can't enforce.

Consider the counterfactual. If Cincinnati had remained privately held by its founders, agents would be vendors optimizing their own economics. If it had sold to private equity, agents would face pressure for premium growth over profitability. If it had gone the mutual route, the ownership would be too diffuse to matter. The public company structure with significant agent ownership threads the needle perfectly—liquid enough for entry and exit, concentrated enough for influence, transparent enough for trust.

The long-term thinking in a quarterly world deserves deeper examination. Public companies face relentless pressure for immediate results. Cincinnati somehow resists. They'll walk away from millions in premium during soft markets, knowing they'll recoup it during hard markets. They'll maintain excess reserves that depress returns, knowing those reserves prevent existential risk. They'll invest in agent relationships that take years to pay off, knowing the terminal value exceeds any DCF model.

How do they get away with it? First, the shareholder base self-selects for patience. Day traders don't buy insurance stocks. Cincinnati's investors—many holding for decades—understand the model. Second, management sets appropriate expectations. No promises of transformation, no hockey-stick projections, just steady execution. Third, the track record earns credibility. After 64 consecutive years of dividend increases, investors trust management's judgment.

The relationship business in a digital age presents fascinating tensions. Every InsurTech startup promises to eliminate friction, reduce human intervention, accelerate decisions through algorithms. Cincinnati doubles down on humans. But here's the insight: they use technology to enhance relationships, not replace them. When an agent can get an automated quote in seconds for simple risks, they have more time for complex situations requiring judgment. When claims can be photographed and estimated digitally for fender-benders, adjusters can focus on traumatic losses where empathy matters.

This isn't Luddite resistance to progress. It's recognition that insurance—especially commercial insurance—involves too many variables for pure automation. Every business is unique. Every claim has context. Every relationship has history. Technology can augment human judgment but rarely replace it. Cincinnati's approach suggests that in professional services, the winning formula might be "high-tech and high-touch" rather than choosing between them.

Conservative underwriting as competitive advantage challenges conventional strategy thinking. Business schools teach differentiation or cost leadership. Cincinnati practices disciplined focus. They don't write the most innovative products, serve the largest companies, or offer the lowest prices. They write standard risks for middle-market companies at fair prices with superior service. It sounds boring. It is boring. That's the point.

In insurance, excitement usually means trouble. Exciting growth often means underpriced risk. Exciting investments often mean speculation. Exciting innovations often mean untested exposures. Cincinnati's boring consistency compounds value precisely because it avoids the disasters that periodically reset competitors' progress. Warren Buffett's rules—don't lose money, and don't forget rule one—find perfect expression in Cincinnati's approach.

Why "boring" insurance can be a great business requires understanding the industry's economics. Insurance enjoys float—premiums paid today for claims paid later. Invested wisely, float generates returns. Insurance also exhibits winner-take-all dynamics within niches—the best underwriter attracts the best risks, generating profits that fund better service, attracting better risks. The cycle is virtuous for winners, vicious for losers.

Cincinnati wins its chosen game: relationship-driven insurance for middle-market businesses and affluent individuals through independent agents. They don't need to be everything to everyone. They need to be the best at their specific strategy. The focused excellence generates returns that diversified mediocrity never could.

Capital allocation demonstrates mastery of what Buffett calls "the most important management skill." Cincinnati doesn't just generate capital; they deploy it wisely. Dividends reward patient shareholders. Buybacks exploit market pessimism. Organic growth investments compound returns. Acquisitions are rare but strategic (like MSP Underwriting for Lloyd's access). They resist the siren songs of diversification, financial engineering, or empire building.

The discipline shows in what they don't do. No massive acquisitions to gain scale. No ventures into unrelated businesses. No special dividends or aggressive buybacks that compromise financial strength. Every capital decision reflects the same patient, conservative philosophy that guides underwriting.

Building trust through consistency across cycles might be Cincinnati's greatest achievement. Insurance is promises—promises to pay claims, to renew coverage, to be there when needed. Trust can't be manufactured through marketing. It must be earned through decades of kept promises.

Cincinnati keeps promises others break. When competitors non-renew entire states after catastrophes, Cincinnati stays. When soft markets tempt carriers to slash prices unsustainably, Cincinnati maintains discipline. When hard markets allow price gouging, Cincinnati increases reasonably. This consistency makes them the carrier of last resort and first choice—a paradox that explains their success.

X. Bear vs. Bull Case & Future Challenges

The Bear Case: Structural Headwinds

The pessimist's view starts with distribution. Independent agents are a declining channel, and the trends are accelerating. In personal auto—the largest insurance line—direct writers like GEICO and Progressive now command over 40% market share, up from 20% two decades ago. Younger consumers, raised on Amazon and Netflix, expect to buy everything online without human intermediation. They don't know their local agent and don't care to.

The economics are stark. Direct writers operate with expense ratios around 20% versus Cincinnati's 33%. That 13-point disadvantage is structural, not operational. No amount of efficiency can close the gap when you're paying agents commissions that direct competitors avoid. In commoditized lines like auto insurance, where price dominates purchase decisions, this cost disadvantage proves fatal.

Technology disruption looms larger. InsurTech startups have raised over $30 billion since 2015, all aimed at reimagining insurance. Root uses telematics to price driving behavior in real-time. Lemonade uses AI to underwrite and settle claims in seconds. Hippo embeds smart home technology to prevent losses before they occur. These aren't incremental improvements—they're fundamental reimaginations of insurance.

Cincinnati's technology investments, while substantial, feel incremental by comparison. They're digitizing existing processes rather than reimagining them. They're enhancing agent relationships rather than questioning whether agents are necessary. They're using data to improve human decisions rather than replacing humans with algorithms. In a world where software eats everything, Cincinnati looks like the next course.

Catastrophe exposure presents growing challenges. Climate change isn't just environmental rhetoric—it's actuarial reality. Severe convective storms—tornadoes, hail, derechos—are increasing in frequency and severity across Cincinnati's Midwest footprint. The infamous "tornado alley" is shifting eastward into Cincinnati's core markets. What were once "100-year storms" now occur every decade.

The company's conservative reserving helps but doesn't eliminate the risk. A single catastrophic event—say, an EF5 tornado hitting downtown Columbus or Cincinnati—could generate losses exceeding annual earnings. Unlike coastal insurers who can buy sophisticated catastrophe bonds and reinsurance, Midwest wind risk is harder to hedge. Cincinnati retains more risk than peers, amplifying both upside and downside.

Scale disadvantages compound over time. Cincinnati's $9 billion in premium sounds substantial until you compare it to State Farm's $80 billion or Berkshire Hathaway's insurance operations at $50 billion. Scale matters in insurance—for spreading risk, negotiating reinsurance, investing in technology, attracting talent. Cincinnati operates sub-scale in every line versus specialists, lacking the focused excellence that might overcome size disadvantages.

Geographic concentration, while providing focus, creates vulnerability. Cincinnati generates about 35% of premium from Ohio, Indiana, and Illinois—states facing economic headwinds. Manufacturing employment continues declining. Population growth lags the Sun Belt. Major cities like Chicago and Detroit struggle with finances and infrastructure. If the Rust Belt rusts further, Cincinnati's premium base erodes.

The talent challenge lurks beneath the surface. Cincinnati's relationship-based model requires experienced underwriters and claims adjusters who understand local markets and build long-term relationships. But the insurance industry faces a talent crisis—half of all workers are over 45, millennials show little interest in insurance careers, and Cincinnati competes with tech companies offering remote work and stock options. The human capital that drives Cincinnati's model is literally aging out.

The Bull Case: Enduring Advantages

The optimist's rebuttal starts with performance. Over the past decade, Cincinnati has generated tremendous profitable growth, adding products, capabilities, and geographies while staying anchored to their agent-centered strategy. The combined ratio averaged 94% over the last ten years. Book value per share compounded at 7% annually. The dividend grew every year. If this is decline, shareholders will take it.

The death of independent agents has been predicted for 30 years, yet they still distribute 35% of property-casualty premium—roughly stable for a decade. Why? Because commercial insurance isn't personal auto. Small businesses need advice on coverage limits, risk management, claims handling. They value relationships with trusted advisors who understand their operations. The complexity that technology startups see as inefficiency, business owners see as necessary customization.

Cincinnati's agents aren't just any agents—they're the best agents. The company's selectivity means they work with established, sophisticated agencies that aren't competing on price alone. These agencies offer risk management consulting, claims advocacy, and strategic advice that no website can replicate. Their affluent personal lines customers value the same relationship and expertise. The channel might be shrinking overall, but Cincinnati operates in the profitable, defensible segment.

Strong combined ratios demonstrate sustainable advantage. Cincinnati's 93.4% combined ratio in 2024 wasn't a fluke—it's consistent excellence. They've generated underwriting profits in 30 of 35 years. This isn't luck or timing. It's disciplined underwriting, careful risk selection, and conservative reserving that compounds over time. While InsurTech startups burn billions chasing growth, Cincinnati prints money.

Investment portfolio strength provides ballast. With over $20 billion in investments generating $1 billion in annual income, Cincinnati has financial flexibility that startups can't match. They can price competitively while maintaining standards. They can weather catastrophes without capital raises. They can invest in technology without sacrificing dividends. The portfolio—built over decades—is a competitive moat that time only deepens.

Geographic concentration might be strength, not weakness. While others chase growth in catastrophe-prone coastal markets, Cincinnati dominates the stable Midwest. Yes, tornadoes are bad, but they're localized compared to hurricanes or earthquakes. Yes, the Rust Belt faces challenges, but it's also home to millions of small businesses that need insurance. Cincinnati's deep local knowledge and relationships in these markets create advantages that scale alone can't overcome.

Agent loyalty and distribution advantages compound. When 70% of your appointed agents call you their #1 carrier, you're doing something right. These agents steer their best risks to Cincinnati. They advocate for Cincinnati in competitive situations. They provide market intelligence that no amount of data analytics can replicate. This loyalty, earned over decades, can't be bought or replicated quickly.

Conservative balance sheet and financial flexibility enable optionality. With minimal debt, excess capital, and strong ratings, Cincinnati can play offense or defense as conditions warrant. They can acquire specialty MGAs to enter new niches. They can buy books of business from struggling competitors. They can increase buybacks when the stock is cheap. They can maintain dividends through any crisis. This flexibility is valuable in an uncertain world.

The cultural moat might be strongest of all. Cincinnati's culture—patient, conservative, relationship-focused—has survived 75 years and multiple generations of leadership. It's embedded in every process, every decision, every interaction. Competitors can copy products, prices, even people. They can't copy seven decades of accumulated trust and reputation.

XI. Recent News

The recent developments paint a picture of consistent execution despite significant challenges. In Q3 2024, Cincinnati reported net income of $820 million, or $5.20 per share, with full-year 2024 net income reaching $2.292 billion, or $14.53 per share. The catastrophe environment proved challenging, with the company responding to 20 weather-related catastrophes across the U.S. in the third quarter, including Hurricane Helene, which swept through 11 states.

Hurricane Milton's impact demonstrated both the company's exposure and resilience. Management estimated pre-tax incurred losses between $75 million and $125 million, net of any applicable reinsurance recoveries, with Cincinnati Insurance Company representing less than $15 million of that estimate while Cincinnati Re represents more than half. This distribution highlights how the reinsurance operation, while profitable overall, bears significant catastrophe volatility.

On the leadership front, the company completed its planned executive transition smoothly. As of the May 4, 2024 Annual Meeting, President Stephen M. Spray assumed the title of chief executive officer, with Steven J. Johnston remaining as executive chairman. This orderly succession—announced well in advance and executed without drama—exemplifies Cincinnati's culture of stability and long-term planning.

The board also underwent changes, with Thomas J. Aaron resigning from the board in November 2024, prompting the board to reduce its size to 13 members. The company continues to evolve its governance while maintaining continuity of strategy.

Operationally, the company demonstrated strong momentum. Consolidated property casualty net written premiums grew 17% for Q3 2024, with particularly strong performance in personal lines despite challenging market conditions. Investment income grew by 15% for the third quarter, supported by a 21% increase in bond interest income, validating the conservative investment strategy.

Looking ahead, California wildfire exposure emerged as a concern. Management disclosed that Q1 2025 results will be impacted by California wildfires, with claims associates already making substantial payments to help insured parties rebuild. While specific loss estimates weren't provided, the proactive disclosure and emphasis on claims service reflects Cincinnati's transparency and customer focus.

The market's response has been measured. Despite strong fundamental performance, the stock trades at reasonable valuations, reflecting both the company's steady growth profile and the market's concerns about catastrophe exposure and distribution channel dynamics. Analyst coverage remains generally positive, focusing on the company's consistent execution and strong balance sheet while noting the structural challenges facing the independent agent channel.

XII. Epilogue: What Makes Cincinnati Different

Seventy-five years ago, four frustrated insurance agents in Cincinnati decided to build something different. Not just another insurance company, but a true partnership between agents, companies, and communities. As 2025 marks the 75th anniversary of the Cincinnati Insurance Company, the company has come to understand the importance of stability, consistency, and financial strength.

What they built defies modern business logic. In an era of digital disruption, Cincinnati doubles down on human relationships. While competitors chase scale through acquisitions, Cincinnati grows organically one agent at a time. As markets demand quarterly performance, Cincinnati manages for decades. The model shouldn't work, yet it thrives.

The enduring power of the agent-centric model reveals itself in crisis. When hurricanes strike, Cincinnati's local adjusters—neighbors helping neighbors—arrive with checks, not paperwork. When markets harden, Cincinnati's agents have a carrier that won't abandon them. When businesses need advice, not just coverage, Cincinnati's field representatives provide it. Technology can augment these relationships but rarely replace them.

The lessons for building a century-spanning financial institution are deceptively simple yet difficult to execute. Culture beats strategy—Cincinnati's conservative, relationship-focused DNA survived public markets, leadership transitions, and industry upheaval because it's embedded in every process and decision. Patience beats speed—by accepting slower growth during soft markets, Cincinnati maintains profitability across cycles. Alignment beats control—by making agents literal owners, Cincinnati creates incentives that contracts can't replicate.

Why culture and relationships still matter in insurance becomes clear when you understand what insurance really is. It's not a commodity product that can be optimized through algorithms. It's a promise—to rebuild homes, restore businesses, protect families. These promises require trust, and trust requires relationships. Cincinnati understands that insurance, at its core, is neighbors protecting neighbors. Technology can make this more efficient but can't replace the human element.

The final thoughts on value creation through patience and discipline challenge conventional investing wisdom. Cincinnati doesn't maximize any single metric—not growth, not returns on equity, not combined ratios. Instead, they optimize for sustainability across all dimensions. The result is a compounding machine that generates wealth not through brilliant moves but through consistent execution.

Consider the math: $1,000 invested in Cincinnati Financial at its 1968 IPO, with dividends reinvested, would be worth over $500,000 today—a 500-fold return achieved not through explosive growth but through steady compound returns averaging about 10% annually for over five decades. No pivots, no transformations, no "betting the company" moments. Just blocking and tackling, year after year.

The Cincinnati story offers a counternarrative to modern capitalism's emphasis on disruption and transformation. It suggests that in certain businesses—particularly those built on trust and relationships—the old ways might still be the best ways. That boring can be beautiful. That slow can be fast over long periods. That focusing on all stakeholders—agents, policyholders, employees, communities, shareholders—creates more value than optimizing for any single constituency.

As we look forward, Cincinnati faces real challenges. The independent agent channel continues declining. Climate change intensifies catastrophe risk. Technology enables new competitors. Yet Cincinnati has faced existential challenges before—the liability crisis of the 1980s, the dot-com bubble, the financial crisis—and emerged stronger by staying true to its principles.

The company that started as an agent rebellion became something more: proof that business can be done differently. That relationships matter more than transactions. That patience beats speed. That trust, once earned, becomes an unassailable competitive advantage. In a world of quarterly capitalism, Cincinnati Financial practices century capitalism—and the results speak for themselves.

For investors, Cincinnati offers something increasingly rare: a business you can understand, run by people you can trust, generating returns you can count on. Not the highest returns, not the fastest growth, but sustainable value creation across cycles. In insurance, as in investing, boring is beautiful. Cincinnati Financial has been beautifully boring for 75 years—and there's every reason to believe they'll remain so for decades to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube