Citizens Financial Group: From Rhode Island Roots to Super-Regional Powerhouse

I. Introduction & Episode Roadmap

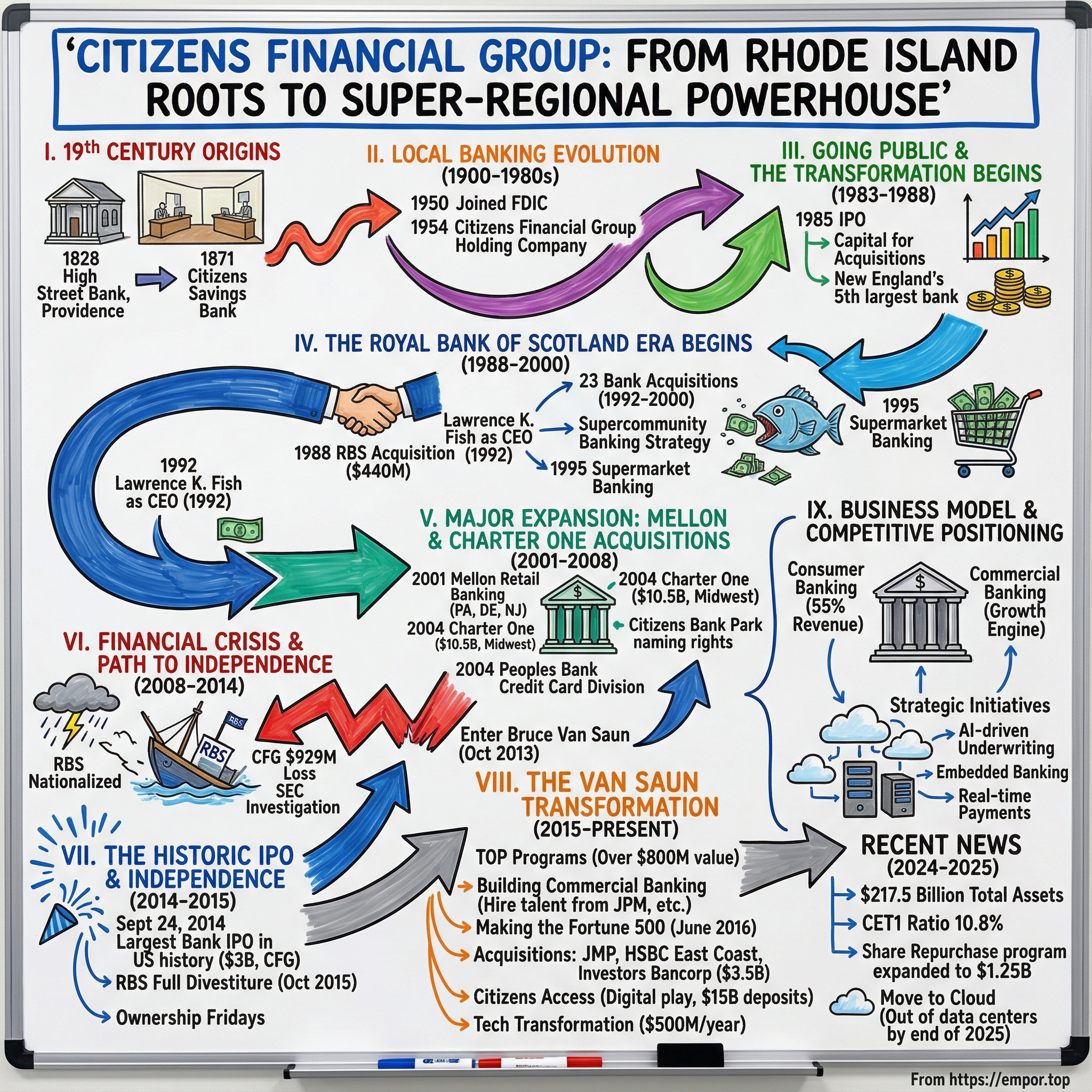

Picture this: September 24, 2014. The opening bell rings at the New York Stock Exchange, and a 186-year-old bank that most Americans outside New England had never heard of begins trading under the ticker CFG. The offering raises $3 billion—the largest commercial bank IPO in U.S. history and the biggest bank IPO since the financial crisis. The kicker? This wasn't some Silicon Valley fintech or a glossy new challenger bank. This was Citizens Financial Group, a Providence institution older than the telegraph, completing one of the most unlikely journeys in American banking.

Here's the central question that makes this story so compelling: How did a small Rhode Island thrift founded when Andrew Jackson was president transform into the 18th largest bank in America—by way of Scottish ownership, no less—and then successfully return to independence just when everyone thought regional banks were dead?

The numbers alone are staggering. When High Street Bank opened its doors in 1828, it operated from two rooms in a Providence residence. Today, Citizens commands $218 billion in assets, operates across 14 states plus DC, and serves millions of customers through over 1,000 branches. But the real story isn't about size—it's about survival, transformation, and timing.

This is a tale of patient capital meeting American ambition. It's about how a conservative New England savings bank became the proving ground for one of Europe's most aggressive banking strategies. It's about cultural transformation so complete that employees who lived through it describe it as working for two entirely different companies. And ultimately, it's about what happens when a bank decides to bet everything on a model—the super-regional bank—that Wall Street had already declared obsolete.

The themes we'll explore read like a playbook for modern banking: the power of patient, strategic capital (RBS held Citizens for 27 years); the art of complex integrations (absorbing Charter One doubled the bank overnight); and the delicate dance of maintaining local relationships while building national scale. We'll see how supermarket banking went from radical experiment to competitive advantage, how a Scottish parent's crisis became an American subsidiary's opportunity, and how leadership transitions can fundamentally reshape an institution's DNA.

II. 19th Century Origins: High Street Bank & Citizens Savings

The year 1828 marked a peculiar moment in American finance. The Second Bank of the United States was fighting for its life against Andrew Jackson's populist crusade. Local banking was the Wild West—state charters were political prizes, failures were common, and the very idea of deposit insurance wouldn't exist for another century. Into this chaos stepped a group of Providence merchants with a simple proposition: create a bank that would serve the actual needs of a booming industrial city.

High Street Bank's founding location tells you everything about its ambitions. Hoyle Square wasn't just busy—it was the nerve center of Providence commerce, where textile merchants rubbed shoulders with shipbuilders and the new industrial class was literally inventing American capitalism. The bank's founders secured two rooms in a residence on High Street, hung out their shingle, and began the slow work of building trust, one local relationship at a time.

Rhode Island in the 1820s was experiencing something unprecedented. The Blackstone River Valley had become the birthplace of America's Industrial Revolution. Samuel Slater's mills were churning out textiles, creating wealth at a scale the young republic had never seen. Providence merchants were getting rich, yes, but more importantly, a new class of workers needed somewhere safe to put their wages. High Street Bank positioned itself as the bridge between old merchant banking and this emerging retail opportunity.

The bank's early ledgers, preserved in the Rhode Island Historical Society, reveal a fascinating clientele: mill owners depositing thousands, workers depositing dollars, ship captains settling accounts before long voyages. One entry from 1835 shows a $12 deposit from "Mrs. E. Blackstone, widow"—likely her entire savings—alongside a $5,000 commercial loan to a textile concern. This wasn't just a bank; it was becoming the financial infrastructure of a transforming economy.

Then came 1871, and with it, a second act. The Rhode Island legislature granted a charter for Citizens Savings Bank—not a competitor to High Street, but a parallel institution serving a different need. The mutual savings bank model was revolutionary in its simplicity: depositors were owners, profits were shared, and the focus was squarely on serving savers rather than speculators.

This dual-track approach—High Street handling commercial banking, Citizens focusing on savings—created an unusually stable foundation. While other banks chased the booms and busts of the Gilded Age, these twin institutions quietly accumulated deposits, made conservative loans, and built something increasingly rare in 19th-century American banking: a reputation for not failing.

By 1900, the combined institutions held $8 million in deposits—modest by New York standards but representing an enormous concentration of Rhode Island wealth. They had survived the Panic of 1873, the depression of the 1890s, and countless local crises. The playbook was established: slow growth, deep relationships, conservative lending. It would serve them well for another 80 years—until everything changed.

III. The Quiet Century: Local Banking Evolution (1900–1980s)

The first half of the 20th century was when Citizens perfected the art of being brilliantly boring. While money-center banks financed wars and built empires, Citizens methodically opened branches across Rhode Island—29 by 1950, each one a careful bet on a growing suburb or mill town. The expansion map, when overlaid with Rhode Island's industrial development, shows remarkable strategic patience: follow the growth, never lead it, always be the second or third bank in town but the most reliable.

The 1950 decision to join the FDIC deserves its own Harvard Business School case study. Citizens became the first mutual savings bank to voluntarily submit to federal insurance—a move that seems obvious now but was controversial then. Mutual banks had their own state insurance funds; joining FDIC meant federal oversight, higher costs, and standardized practices. But Citizens' leadership saw what others missed: in a world of increasing mobility and sophistication, the FDIC seal would become the ultimate trust marker.

Four years later came the masterstroke: establishing Citizens Financial Group as a holding company through the acquisition of The Greenville Trust Company. This wasn't just paperwork—it was architectural. The holding company structure would allow Citizens to acquire other banks while maintaining their local identities, expand across state lines when regulations changed, and eventually provide the corporate scaffolding for one of banking's great expansion stories.

George Graboys took the helm in 1974, and with him came a vision that seemed almost laughably ambitious for a $500 million Rhode Island bank. Graboys had spent time studying the emerging "super-regional" banks in the South—NationsBank, First Union—and became convinced that New England needed its own champion. His famous quote to the board in 1979: "We can stay small and probably get eaten, or we can grow smart and do the eating."

By 1981, the numbers told a story of comfortable success: 29 branches, $971 million in assets, dominant market share in Rhode Island. But Graboys saw those same numbers as a trap. Rhode Island's population was stagnant, its industrial base eroding, and Connecticut and Massachusetts banks were eyeing expansion opportunities. The choice was stark: transform or be transformed.

The boardroom debates of 1982-1983 were fierce. Old-guard directors wanted to preserve the mutual structure—why risk 150 years of stability? Younger members saw opportunity in going public, accessing capital markets, making acquisitions. Graboys navigated between them with a simple argument: "The question isn't whether we'll face competition from larger banks. The question is whether we'll face it as a mutual with one hand tied behind our back or as a public company with access to currency for acquisitions."

IV. Going Public & The Transformation Begins (1983–1988)

The first commercial loan office outside Rhode Island opened in Boston in 1983, and you could practically hear the collective gasp from Providence society. Citizens? Our Citizens? Setting up shop in Boston? For conservative Rhode Islanders, it was like the local church announcing it was opening a casino. But Graboys had done his homework: Boston businesses were increasingly doing business in Rhode Island, and not having a Boston presence meant losing those relationships entirely.

The real revolution came in 1984-1985, a two-year period that transformed Citizens from a sleepy mutual into a public company with acquisition currency. The mechanics were complex—first converting from mutual to stock savings bank, then creating Citizens Financial Group as the holding company, then the IPO itself—but the psychology was simple: we're playing offense now.

The IPO prospectus from 1985 makes for fascinating reading. Assets of $1.5 billion (roughly $4 billion in today's dollars), stock priced at $23 per share, and language that seems almost quaint: "The Company believes that opportunities may exist for expansion through acquisition of other financial institutions." The underwriters—local Boston firms, not Wall Street giants—priced it conservatively. The offering sold out in two days.

With fresh capital came fresh ambition. The acquisition of Gulf States Mortgage gave Citizens a mortgage origination platform beyond its branches. Fairhaven Savings Bank added Massachusetts presence. Each deal was small—$50 million here, $100 million there—but the pattern was establishing: disciplined, accretive, always maintaining capital ratios.

The integration playbook developed during this period would prove invaluable later. Keep the local brand for 18 months, gradually introduce Citizens products, retain the best local talent, achieve 30% cost savings within two years. It wasn't sexy, but it worked. By 1988, Citizens had quietly become the fifth largest bank in New England with $4 billion in assets.

Then came the call that changed everything. Sir George Mathewson, deputy chief executive of the Royal Bank of Scotland, had been studying the American market for years. RBS had tried and failed to buy a California bank, been rebuffed in Texas, and was growing frustrated. New England, with its Scottish heritage and conservative banking culture, felt more familiar. And Citizens, with its proven acquisition track record and clean balance sheet, looked like the perfect platform.

The initial approach in early 1988 was almost comically formal—a letter on RBS letterhead suggesting "a discussion of mutual interest." Graboys flew to Edinburgh, expecting a partnership proposal. What he got was a blank check: "Name your price, keep your management team, and help us build something special in America."

V. The Royal Bank of Scotland Era Begins (1988–2000)

The acquisition price—$440 million for a bank with $4 billion in assets—raised eyebrows on both sides of the Atlantic. RBS was paying 1.5 times book value when American banks were trading at 1.2 times. The Scottish press called it "Mathewson's Folly." The Providence Journal ran the headline: "Rhode Island Bank Sold to Scots." But both sides were missing the real story: this wasn't an acquisition, it was an investment in a platform.

RBS's strategy was brilliantly counterintuitive. While other foreign banks tried to impose their culture on American acquisitions (usually failing spectacularly), RBS took the opposite approach: learn from Citizens, fund its growth, and stay out of the way. Mathewson would later say, "We bought American expertise, not American assets. The last thing they needed was Scottish bankers telling them how to bank in New England."

The real game-changer came in 1992 with the appointment of Lawrence K. Fish as CEO. Fish was a curious choice—a lawyer by training, not a banker, who had spent his career at Columbia Pictures and various financial services firms. But he understood something fundamental: banking was becoming a consumer business, and consumer businesses needed brand, scale, and distribution.

Fish's first executive committee meeting has become Citizens legend. He walked in with a map of New England covered in red dots (competitor branches) and blue dots (Citizens branches). The blue dots were overwhelmingly concentrated in Rhode Island. "This," he said, "is what losing looks like. We're the biggest bank in the smallest state." Then he pulled out a second map, this one showing projected blue dots across all six New England states. "This is what winning looks like. RBS has given us the capital. Let's go shopping."

The acquisition pace under Fish was breathtaking. Between 1992 and 2000, Citizens bought 23 banks. Not troubled banks sold by the FDIC, but healthy, profitable community banks whose owners saw the consolidation wave coming. Fish's pitch was consistent: "Sell to us, keep your local president, maintain your community relationships, but get our scale in technology and products."

The "supercommunity" banking strategy was Fish's masterstroke—a term he coined to thread the needle between conflicting needs. Citizens would have the scale of a regional bank but maintain the community focus of a local bank. Branch managers had lending authority. Local boards were maintained as advisors. The Citizens name might be on the door, but the face behind the counter was still local.

But the real innovation came in 1995: supermarket banking. The deal with Shaw's Supermarkets to open bank branches inside grocery stores was either brilliant or insane, depending on who you asked. Traditional bankers were horrified—banking next to the broccoli? But Fish saw what they missed: Americans go to the grocery store 2-3 times per week but visit bank branches once a month. Why not be where the customers already are?

The numbers validated the strategy. Supermarket branches cost 60% less to build, stayed open seven days a week, and acquired customers at twice the rate of traditional branches. By 2000, Citizens operated 150 supermarket branches, more than any other bank in America. What started as an experiment had become a competitive moat.

VI. Major Expansion: Mellon & Charter One Acquisitions (2001–2008)

The Mellon deal in 2001 was when Citizens stopped being a New England story and started being a Mid-Atlantic one. For $2 billion, Citizens acquired Mellon's entire retail banking division—450 branches, $14 billion in deposits, and suddenly Citizens was the second-largest bank in Pennsylvania. The integration challenge was staggering: different core systems, different product sets, different cultures. Pennsylvania banking was relationship-based, handshake deals, knowing your customers' grandparents. New England banking was increasingly automated, standardized, efficient.

Fish's integration team, led by a young executive named Bruce Van Saun (remember that name), developed what they called the "Best of Both" approach. Pennsylvania's relationship model would be preserved in commercial banking. New England's efficiency would drive retail. The supermarket banking model would expand into Giant and Stop & Shop stores. It took 18 months, but when the dust settled, Citizens had successfully digested a bank nearly half its size while maintaining 96% customer retention.

The 2003 purchase of naming rights to the Philadelphia Phillies' new ballpark seemed like corporate excess to some—why spend precious marketing dollars on a baseball stadium? But Fish understood something about Pennsylvania that outsiders missed: this was a state where local identity mattered, where being seen as carpetbaggers would be fatal. Citizens Bank Park wasn't just advertising; it was a $95 million declaration that Citizens was here to stay.

Then came the deal that would define Citizens' future: Charter One Financial. The Cleveland-based bank was everything Citizens wasn't—Midwestern, aggressive in subprime lending, heavily invested in adjustable-rate mortgages. But it also had $44 billion in assets, 600 branches across six states, and would make Citizens the 12th largest bank in America overnight.

The $10.5 billion price tag in August 2004 was the second-largest bank acquisition that year. RBS funded it entirely, didn't blink at the valuation, and gave Fish carte blanche on integration. The strategic logic was compelling: Citizens would have scale from Maine to Michigan, could spread technology costs across twice as many customers, and would finally have the heft to compete with the money-center banks.

But the cultural integration was brutal. Charter One was entrepreneurial where Citizens was methodical, risk-taking where Citizens was conservative, decentralized where Citizens was increasingly standardized. The decision to maintain dual brands—Citizens in the East, Charter One in the Midwest—was supposed to be temporary. It lasted over a decade, creating confusion in markets, complexity in systems, and essentially running two banks under one roof.

The 2004 acquisition of People's Bank credit card division was a small deal that revealed big ambitions. For the first time, Citizens could issue its own credit cards rather than partnering with third parties. It seems trivial now, but in 2004, having your own card platform was the difference between being a full-service bank and being a glorified branch network.

By 2008, Citizens looked unstoppable: $161 billion in assets, over 1,500 branches, 28,000 employees. Fish's retirement announcement in 2007 was accompanied by victory laps in the financial press. The Providence Journal called him "the architect of modern Citizens." The American Banker named Citizens "Bank of the Year." Even the skeptics had to admit: the RBS-Citizens combination had created something special.

VII. Financial Crisis & The Path to Independence (2008–2014)

The first sign of trouble came in February 2008, when Citizens quietly increased its loan loss provisions by 40%. The press release buried the news in paragraph four, but insiders knew: Charter One's mortgage portfolio was toxic. Those aggressive Cleveland lenders had written billions in subprime mortgages, adjustable-rate loans to borrowers who could only afford the teaser rates, commercial real estate deals predicated on ever-rising values.

By September 2008, as Lehman Brothers collapsed and the financial world burned, Citizens posted a $929 million loss. The SEC opened an investigation into the bank's subprime mortgage practices. Customers lined up at branches, not quite a run on the bank but close enough to terrify executives. The great expansion machine had blown an engine just as the race got difficult.

But Citizens' crisis was nothing compared to its parent's catastrophe. RBS posted a £24.1 billion loss for 2008—the biggest in British corporate history. The UK government injected £45 billion to prevent collapse, effectively nationalizing the bank. Sir Fred Goodwin, RBS's aggressive CEO who had championed global expansion, was vilified in Parliament, stripped of his knighthood, and became the face of banking excess.

For Citizens, having a nationalized British bank as your parent was like having your dad go to prison—embarrassing, constraining, and potentially fatal to your own ambitions. The UK government wanted RBS to shrink, focus on British banking, and divest "non-core" assets. Citizens, despite being profitable again by 2010, was definitely non-core.

The Federal Reserve's 2014 stress test failure was the final straw. Citizens' capital plan was rejected not because the bank was weak—it had rebuilt its balance sheet admirably—but because its capital planning process was deemed inadequate. The message from regulators was clear: you need to be independent or have a parent that can properly support you. RBS, struggling with its own regulatory issues, couldn't do either.

Enter Bruce Van Saun in October 2013. Van Saun had been CFO at RBS during the crisis, had helped engineer its recovery, and understood both sides of the Atlantic divide. His mandate was elegant in its simplicity: prepare Citizens for independence, execute an IPO, and create value for RBS while building a standalone American bank.

Van Saun's first all-hands meeting became the stuff of Citizens legend. "We have 90 days to convince the market we're worth investing in," he said. "Not RBS's castoff American subsidiary, but a real, independent, American bank with a compelling future." He laid out three priorities: fix the basics (technology, risk management, efficiency), define the strategy (what kind of bank would Citizens be?), and change the culture (from subsidiary to owner).

The IPO preparation was a masterclass in financial engineering. Citizens had to separate its systems from RBS, establish independent risk management, build a standalone board, and convince investors that a regional bank—a model everyone said was dead—could thrive. Van Saun's pitch was contrarian: "Everyone's chasing wealth management and investment banking. We're going to be really, really good at boring banking."

VIII. The Historic IPO & Independence (2014–2015)

The roadshow for the September 2014 IPO was brutal. Van Saun and his team visited 87 investors in 10 days, answering the same questions over and over: Why should we believe in regional banking? How will you compete with JPMorgan? What happens when rates rise? The skepticism was palpable—one hedge fund manager reportedly asked, "Aren't you just rearranging deck chairs on the Titanic of regional banking?"

The numbers in the prospectus told a mixed story. The good: $137 billion in assets, strong market shares in attractive geographies, a rebuilt balance sheet. The bad: efficiency ratio of 68% (terrible by industry standards), returns well below peers, and technology systems that one analyst described as "held together with duct tape and prayer."

IPO day itself—September 24, 2014—was high theater. The stock priced at $21.50, below the expected range of $23-25. It opened at $21.90, traded as high as $22.50, and closed at $22.22. Not exactly a ringing endorsement, but not a disaster either. The offering raised $3 billion, valuing Citizens at roughly $11 billion—a fraction of what RBS had invested over 26 years.

But Van Saun saw something the market missed. "We're not asking investors to bet on transformation," he told the board that evening. "We're asking them to bet on execution. And nobody executes like Citizens."

The progressive divestiture by RBS was strategically brilliant. Rather than dump all shares at once, RBS sold in tranches: 45.6% retained after the IPO, reduced to 23.4% by July 2015, fully divested by October 2015. Each sale was oversubscribed, each priced higher than the last. By the final sale, CFG was trading at $26, generating an additional $500 million for RBS.

The cultural transformation during this period was profound. For 26 years, Citizens employees had been able to blame Edinburgh for unpopular decisions. Now, they owned their own destiny. Van Saun instituted "Ownership Fridays"—weekly communications about what it meant to be independent. Stock options were pushed deep into the organization. The message was consistent: we sink or swim on our own merits now.

The first earnings call as a fully independent company in January 2016 was Van Saun at his best. Revenue up 5%, efficiency ratio improved to 65%, commercial loan growth of 12%. But the real message was strategic: "We're not trying to be all things to all people. We're going to be the best bank for mass affluent consumers and middle-market companies in our footprint. Period."

IX. The Van Saun Transformation: Building a Super-Regional Bank (2015–Present)

The TOP (Tapping Our Potential) programs launched in 2016 sounded like typical corporate buzzword bingo, but the execution was ruthless. TOP I focused on costs: $185 million in savings through branch consolidation, vendor renegotiation, and process automation. TOP II targeted revenue: $125 million in new fee income through repricing, new products, and cross-selling. TOP III and IV pushed further into efficiency and growth. By 2020, the programs had generated over $800 million in value—real money, not PowerPoint projections.

The commercial banking build-out was Van Saun's biggest bet. Citizens had always been a retail bank that did some commercial lending. Van Saun wanted to flip that: become a commercial bank with a powerful retail franchise. He hired dozens of bankers from larger competitors, paying top dollar for talent. The pitch was simple: "At JPMorgan, you're a small fish. Here, you can build something."

The 2015 rebranding of Charter One branches as Citizens was more than cosmetic. It was the final admission that running dual brands was unsustainable. The integration took 18 months, cost $145 million, but finally created one bank with one system, one culture, one destiny.

Making the Fortune 500 in June 2016 was symbolic but important. Citizens was now officially "big league"—able to recruit differently, compete differently, be seen differently. Van Saun celebrated by taking out a full-page ad in the Wall Street Journal with a simple message: "From Rhode Island to the Fortune 500. Just getting started."

The acquisition strategy under independence was surgical. The 2021 purchase of JMP Group added West Coast wealth management capabilities. The HSBC East Coast branches—80 locations for just $2.2 billion—was the deal of the decade, adding $9 billion in deposits at a 3% premium when most deals were pricing at 10%+. The 2022 Investors Bancorp acquisition for $3.5 billion added New York metro presence and $27 billion in assets.

Citizens Access, launched in 2018, was the digital play everyone said Citizens needed. An online-only savings platform offering high yields to attract national deposits. Within three years, it had gathered $15 billion in deposits at a fraction of the cost of branch-based gathering. Not revolutionary, but evidence that stodgy Citizens could play the digital game.

The technology transformation was less visible but more important. Citizens spent $500 million annually on technology from 2016-2020, rebuilding core systems, launching mobile apps that actually worked, and creating digital account opening that took minutes, not hours. By 2021, 48% of deposit accounts were opened digitally—up from 5% in 2015.

Today's Citizens is unrecognizable from the bank that went public in 2014. With $218.3 billion in assets as of June 2025, returns on equity consistently above 10%, and an efficiency ratio now below 60%, it has become exactly what Van Saun promised: a boring bank that executes brilliantly.

X. Business Model & Competitive Positioning

The two-segment structure—Consumer Banking and Commercial Banking—sounds simple but represents a fundamental strategic choice. Unlike peers who chase wealth management fees or investment banking glory, Citizens focuses on bread-and-butter banking: checking accounts, mortgages, middle-market loans, cash management. The margins are thinner, but the relationships are stickier.

Consumer Banking, generating roughly 55% of revenue, serves 5 million customers through 1,078 branches across 14 states plus DC. The branch footprint, once seen as an albatross, has become a competitive advantage as digital-only banks struggle with customer acquisition costs and money-center banks retreat from less profitable markets. The sweet spot is mass affluent households—$100,000 to $1 million in wealth—who want digital convenience but also value personal relationships.

Commercial Banking, the growth engine, targets companies with $10 million to $3 billion in revenue. These middle-market firms are too small for money-center banks to care about but too complex for community banks to serve. Citizens' pitch is compelling: the capabilities of a large bank with the service of a regional player. The numbers back it up—commercial loans have grown 8% annually since 2015, well above peer averages.

The supermarket banking leadership—still operating 450 in-store branches—seems anachronistic in the digital age. But the math works: these branches generate equal deposits at 60% of the cost of traditional locations. More importantly, they serve as customer acquisition funnels, opening 30% of all new checking accounts despite representing just 15% of the network.

Fee businesses now generate 35% of total revenue, up from 28% in 2014. Capital markets fees from middle-market companies, mortgage banking income from the retail side, and wealth management fees from the combined platform. Nothing spectacular, but steady, predictable, and growing faster than the balance sheet.

The technology stack, rebuilt at enormous cost, is now a competitive advantage. The mobile app consistently ranks in the top quartile for regional banks. Digital account opening takes under 10 minutes. Commercial clients can manage complex cash positions through sophisticated portals. It's table stakes in 2025, but Citizens had to spend billions to get here from its 2014 starting point.

The cultural transformation from RBS subsidiary to independent bank might be the most underappreciated achievement. Employee engagement scores have risen 30 percentage points since 2014. Turnover in key positions is below industry averages. The bank attracts talent from money-center competitors. As one executive who lived through both eras put it: "Under RBS, we were playing not to lose. Now we're playing to win."

XI. Playbook: Lessons from the Citizens Story

The value of patient, strategic capital cannot be overstated. RBS held Citizens for 27 years, invested billions, and ultimately lost money on the deal. But during that ownership, Citizens grew from a $4 billion Rhode Island bank to a $140 billion super-regional. The lesson? Sometimes the best capital is patient capital, even if it doesn't generate the highest returns for the provider.

Managing complex integrations while maintaining business momentum is Citizens' superpower. The bank has absorbed 30+ acquisitions, each with different systems, cultures, and client bases. The playbook is consistent: maintain local leadership, take 18-24 months for system integration, achieve 30% cost saves, keep 90%+ of customers. It's not sexy, but it's repeatable.

Timing the market matters more than anyone admits. The 2014 IPO came just as the market was ready to believe in banks again but before valuations got frothy. The HSBC branch purchase happened during COVID when nobody wanted branches. The Investors Bancorp deal closed just before the 2023 regional banking crisis. Luck? Maybe. But as Van Saun says, "Good operators create their own luck."

Building capabilities while maintaining profitability is the eternal challenge. Citizens spent $2 billion on technology while improving returns. How? By funding investment through efficiency gains, not hoping for growth to bail them out. Every dollar saved in branches funded two dollars in technology. Painful, but sustainable.

The super-regional model, declared dead multiple times, lives on through disciplined execution. Citizens proves you don't need to be giant or tiny—you can succeed in the middle if you're clear about your value proposition. Serve the customers money-center banks ignore but community banks can't handle. Be digital enough for convenience but physical enough for complexity.

Leadership transitions can transform culture if handled correctly. Van Saun didn't just replace Fish; he reimagined what Citizens could be. New metrics (focusing on returns, not just size), new talent (hiring from bigger banks), new mindset (owners, not subsidiaries). The lesson: sometimes you need an outsider who understands the inside.

XII. Analysis: Bull vs. Bear Case

The Bull Case starts with geography. Citizens dominates attractive, growing markets—Boston's biotech corridor, Philadelphia's diversified economy, New York's endless appetite for banking. These aren't dying Rust Belt cities but dynamic metros with growing populations and incomes. The franchise value alone—1,000+ branches in prime locations—would cost tens of billions to replicate.

The M&A integration capability is arguably best-in-class among regionals. While peers struggle to integrate single acquisitions, Citizens has absorbed three major deals since independence, each accretive within 18 months. With regional consolidation inevitable, Citizens is more likely to be acquirer than acquired, using its currency and capability to grow through selective deals.

Van Saun's track record speaks for itself—stock up 3x since the IPO, returns consistently above peers, efficiency ratio improved 15 percentage points. He's 66 but shows no signs of slowing down, and has built a deep bench of potential successors. The cultural transformation from sleepy subsidiary to aggressive competitor is complete and probably irreversible.

Scale advantages in technology spending are real and growing. Citizens spends $600 million annually on tech—impossible for smaller regionals but sufficient to compete with larger banks in digital capabilities. As technology becomes table stakes, subscale players will struggle to keep up, driving consolidation that benefits scaled players like Citizens.

The Bear Case begins with concentration risk. Despite geographic expansion, Citizens is still overwhelmingly a Northeast/Mid-Atlantic story. A regional recession, particularly in commercial real estate, could hit harder than diversified nationals. The ghost of 2008's Charter One crisis still haunts—what hidden risks lurk in the loan book?

Competition from both ends is intensifying. JPMorgan and Bank of America are pushing down-market, using superior technology and unlimited capital to win middle-market clients. Digital natives like Square and Stripe are unbundling commercial banking. Community banks compete on relationships. Citizens is fighting a multi-front war with no clear competitive moat.

Interest rate sensitivity remains acute. Citizens' asset-sensitive balance sheet benefited enormously from rising rates in 2022-2023, but that tailwind is becoming a headwind. Net interest margins are compressing, deposit costs are rising, and the easy money from rate hikes is over. Can Citizens grow earnings in a flat-rate environment?

Credit cycle concerns loom large. Commercial real estate, particularly office, represents 28% of the commercial loan book. Credit cards and auto loans are showing early signs of stress. Citizens' underwriting has been conservative, but every bank looks smart until the cycle turns. The next recession will test whether the cultural transformation included risk management.

The succession question is unavoidable. Van Saun has been CEO for 11 years—extraordinary tenure in modern banking. When he leaves, does the culture revert? Can anyone else execute the boring-but-brilliant strategy? The stock trades at a "Van Saun premium"—what happens when he's gone?

XIII. Epilogue & Looking Forward

The future of super-regional banking is being written in real-time, and Citizens has a pen in hand. The model—too big to be small, too small to be huge—only works with flawless execution. Citizens has proven it can execute, but the margin for error is shrinking as technology democratizes capabilities and regulations favor the very large or very small.

Consolidation opportunities abound. There are still 4,500 banks in America—absurd by global standards. Citizens, with its integration expertise and currency, could be a serial acquirer. The question isn't whether to buy but what to buy: in-market deals for efficiency, new market entries for growth, or capability acquisitions for competence?

Digital transformation is never complete, only current. Citizens must spend $600+ million annually just to maintain competitive parity. The next frontier—AI-driven underwriting, embedded banking, real-time payments—will require billions more. Can a $220 billion bank match the innovation of trillion-dollar titans or venture-funded fintechs?

What would we do if we were running Citizens? Double down on the middle market commercial franchise—it's differentiated and defensible. Shrink the branch network another 20% and reinvest in digital. Make one transformational acquisition—perhaps a trust bank or specialty lender—to add new capabilities. And start preparing for the next crisis now, because it's not a question of if but when.

The Citizens story is far from over. From two rooms in Providence to the Fortune 500, from Scottish subsidiary to independent powerhouse, from mutual savings bank to super-regional leader—each transformation seemed impossible until it wasn't. The next chapter is being written now, and if history is any guide, it will surprise everyone except those paying attention.

XIV. Recent News### **

Latest Quarterly Earnings** Citizens reported fourth quarter 2024 net income of $401 million with earnings per share of $0.83. CEO Bruce Van Saun highlighted "solid performance in Q4 given strong execution of our key initiatives and nice improvement in our net interest margin," noting that the balance sheet remains strong with CET1 at 10.8%, loan-to-deposit ratio below 80%, and credit metrics all trending favorably.

The bank's Private Bank reached year-end balances of $7 billion in deposits, $3.1 billion in loans, and $4.7 billion in assets under management, tracking well to targets. As of December 31, 2024, Citizens reported total assets of $217.5 billion, reflecting the continued execution of its strategic initiatives despite the challenging rate environment.

Capital Management Updates

The 2024 Federal Reserve stress test determined Citizens' preliminary Stress Capital Buffer at 4.5%, implying a regulatory minimum CET1 ratio of 9%, up from 8.5% in 2023. Citizens was among the 31 U.S. banks that successfully passed the stress test, demonstrating the resilience of its balance sheet and business model.

The company's board expanded the capacity of its common share repurchase program by an additional $656 million, bringing the total authorized capacity to $1.25 billion. CFO John Woods noted that the stress test results "illustrate Citizens' strong capital position, which is well in excess of our regulatory minimum," and the increased authorization "reflects confidence in our ability to deliver strong financial performance while continuing to invest across our businesses and deliver attractive returns to shareholders".

Strategic Technology Initiatives

Citizens recently held an executive gathering featuring "a whole afternoon segment on getting everybody up to speed on AI, so they could be more alert for opportunities about how to deploy it inside the bank". The bank is moving toward all applications becoming cloud-based, with Van Saun stating Citizens should be out of all physical data centers by the end of 2025.

Van Saun emphasized that strategy is one of the top challenges for banks when it comes to AI, advising to "make sure that you're focused on the big use cases that align with your strategy, that have the maximum kind of benefits". The bank sees opportunities for AI use in assisting developers in writing code and bolstering fraud detection.

Leadership Continuity

Van Saun has led "a successful initial public offering of Citizens in September 2014, followed by a dramatic transformation journey over recent years, including the build out of the Commercial Bank, the launch of Citizens Private Bank, and the expansion into New York Metro through the strategic acquisition of HSBC's east coast branches and Investors Bancorp". His continued leadership provides stability as the bank navigates the evolving banking landscape and executes on its super-regional banking strategy.

XV. Links & Resources

SEC Filings and Investor Materials: - Citizens Financial Group Investor Relations: investor.citizensbank.com - Latest 10-K and 10-Q filings: SEC EDGAR database - Quarterly earnings presentations and supplements - Annual proxy statements and governance documents

Historical Banking Resources: - Rhode Island Historical Society archives on High Street Bank - Federal Reserve Bank of Boston historical banking data - FDIC Historical Bank Data Tool - Royal Bank of Scotland Group archives (Edinburgh)

Industry Reports and Analysis: - S&P Global Market Intelligence regional banking reports - Moody's Investors Service bank rating reports - Federal Reserve stress test results and methodology - Conference of State Bank Supervisors publications

Academic Papers on Regional Banking: - "The Evolution of U.S. Community Banks and Its Impact on Small Business Lending" (Federal Reserve) - "Regional Bank Consolidation and Small Business Lending" (Journal of Financial Economics) - "The Competitive Effects of Interstate Banking" (Review of Economics and Statistics)

Books on Banking History: - "The House of Morgan" by Ron Chernow (context on American banking evolution) - "Shredded: Inside RBS, The Bank That Broke Britain" by Ian Fraser (RBS crisis perspective) - "Too Big to Fail" by Andrew Ross Sorkin (financial crisis context) - "The Bankers' New Clothes" by Anat Admati and Martin Hellwig (banking regulation)

Market Data and Analysis: - Bloomberg Terminal: CFG US Equity - S&P Capital IQ platform - SNL Financial (now part of S&P Global) - American Banker Data Store

Regulatory Resources: - Federal Reserve Board supervision and regulation - Office of the Comptroller of the Currency publications - Consumer Financial Protection Bureau data - Basel Committee on Banking Supervision frameworks

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube