Cadence Design Systems: The Invisible Foundation of Every Chip

I. Introduction & Episode Roadmap

Picture this: Inside every smartphone, every Tesla, every data center powering ChatGPT, there's a hidden truth. Before a single transistor was etched, before any silicon was fabricated, teams of engineers spent years designing these chips using software from a company most people have never heard of. That company is Cadence Design Systems—a $100 billion market cap giant that's as essential to the technology industry as it is invisible to consumers.

Here's the paradox: Cadence doesn't make chips. It doesn't sell devices. Yet without Cadence and its competitors, the entire $600 billion semiconductor industry would grind to a halt. Every advanced chip designed in the last three decades—from the processors in your iPhone to the AI accelerators training large language models—was created using Electronic Design Automation (EDA) software. And Cadence commands roughly 30% of this critical market.

The story we're about to tell is one of academic rebels who saw the future before anyone else, of a company that nearly died from scandal and mismanagement, and of a transformation so complete that the Cadence of 2024 would be unrecognizable to its founders. It's a story about selling picks and shovels in the greatest gold rush of our time—the relentless march of Moore's Law and the explosion of artificial intelligence.

How did two struggling startups founded by Berkeley professors become the invisible foundation enabling every chip in the world? How did a company that almost sold itself for $1.6 billion in 2008 become worth $100 billion today? And why might Cadence—boring, B2B, utterly unsexy Cadence—be one of the most important companies shaping our technological future?

The answer starts in the computer science labs of UC Berkeley in the 1970s, where a group of professors realized something profound: chip design was about to hit a wall. Not a physical wall—Moore's Law would keep marching for decades—but a human one. The complexity of chips was growing exponentially, but human capacity to design them wasn't. Without a revolution in design tools, the semiconductor industry would strangle on its own success.

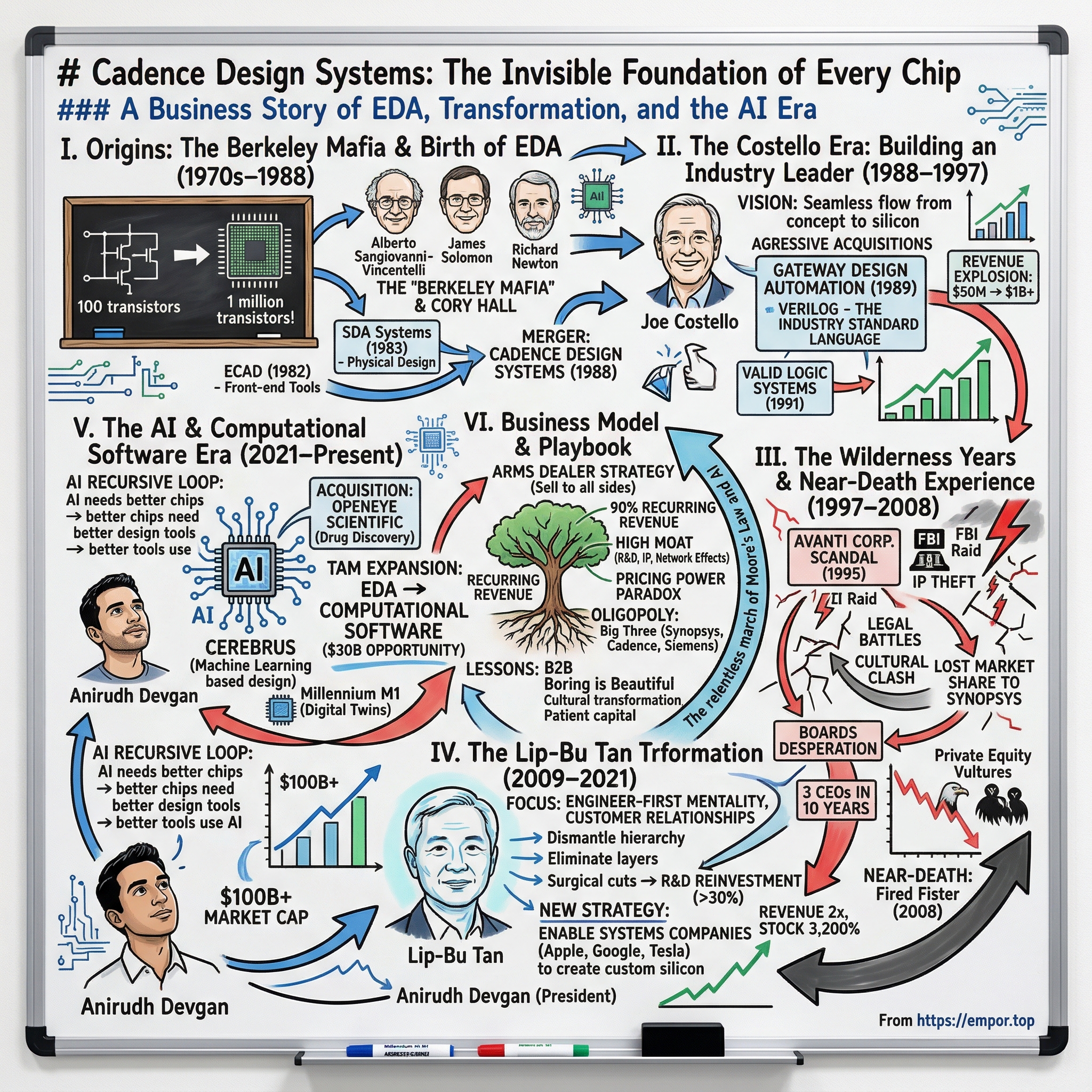

II. Origins: The Berkeley Mafia & Birth of EDA (1970s–1988)

The fluorescent lights hummed in Cory Hall at UC Berkeley as Professor Alberto Sangiovanni-Vincentelli sketched circuit diagrams on a blackboard in 1975. His students were designing a simple chip with a few hundred transistors—a process that took weeks of painstaking manual layout. "What happens," he asked the class, "when chips have a million transistors?" The room fell silent. Everyone knew the answer: it would be impossible.

This wasn't idle speculation. Gordon Moore's famous observation—that transistor density doubles every two years—was already proving true. But there was a corollary no one talked about: design complexity was growing even faster than transistor count. A chip with twice as many transistors might have four times as many potential interactions, eight times as many timing paths to verify. The mathematics were brutal and unforgiving.

Sangiovanni-Vincentelli wasn't alone in recognizing this crisis. Down the hall, James Solomon was working on circuit simulation algorithms. Richard Newton was developing new approaches to logic synthesis. Together, this triumvirate of Berkeley professors would spawn an entire industry. Their students would go on to found or lead virtually every major EDA company of the next generation. The "Berkeley Mafia," as they'd later be known, didn't just predict the future—they built the tools to create it.

The academic work was groundbreaking, but turning research into products required entrepreneurs. Enter Joseph Costello and Jim Solomon, who founded SDA Systems in 1983. SDA focused on physical design tools—the software that determined where transistors and wires would actually go on a chip. Meanwhile, across the San Francisco Bay, another group of engineers founded ECAD in 1982, specializing in schematic capture and simulation—the front-end of the design process.

Both companies struggled initially. The EDA market in the early 1980s was fragmented and immature. Chip designers were skeptical of automation, preferring their tried-and-true manual methods. Sales cycles stretched for months. Revenue was lumpy and unpredictable. By 1987, both SDA and ECAD were burning cash and facing tough choices.

The semiconductor industry, however, was about to explode. The personal computer revolution was driving unprecedented demand for chips. Intel's 80386 processor, released in 1985, contained 275,000 transistors—a number that would have seemed like science fiction just a decade earlier. Design teams were drowning in complexity. Manual methods that worked for thousands of transistors were breaking down at hundreds of thousands. The crisis Sangiovanni-Vincentelli had predicted was here.

In late 1987, ECAD's board made a bold decision: acquire SDA Systems for $72 million in stock. It was a merger of equals in everything but name—two struggling companies hoping that together they could build something neither could achieve alone. ECAD had strong front-end tools but weak physical design. SDA had the opposite. Combined, they could offer something revolutionary: an integrated suite covering the entire chip design flow.

The merger closed in 1988, creating Cadence Design Systems. The name itself was carefully chosen—"cadence" suggesting rhythm, flow, and coordination. The company had 400 employees, annual revenue of about $50 million, and a vision that seemed almost absurdly ambitious: to become the Microsoft of chip design software.

Joe Costello, SDA's president, emerged as the leader of the combined entity. At 35, he was young, aggressive, and utterly convinced that EDA was about to become one of the most important software markets in the world. "Every single electronic product will need our tools," he told employees at the first all-hands meeting. "We're not just automating design—we're enabling the entire digital revolution."

The timing couldn't have been better. The late 1980s saw an explosion in chip complexity that made EDA tools not just useful but essential. Application-Specific Integrated Circuits (ASICs) were becoming common, allowing companies to design custom chips for specific products. The number of chip design starts was growing exponentially. And perhaps most importantly, venture capital was pouring into semiconductor startups, all of whom needed design tools.

But Cadence faced formidable competition. Mentor Graphics, founded in 1981, was already the market leader with over $200 million in revenue. Synopsys, founded by another Berkeley Mafia member, Aart de Geus, in 1986, was growing rapidly with its revolutionary logic synthesis technology. Valid Logic Systems and Daisy Systems rounded out the "big five" EDA vendors. The battle for dominance was just beginning.

What set Cadence apart wasn't just its technology but its philosophy. While competitors focused on building the best individual tools, Costello was obsessed with integration. He understood that chip designers didn't want to stitch together products from multiple vendors—they wanted a seamless flow from concept to silicon. This vision would drive Cadence's strategy for the next decade: acquire the best point tools and integrate them into a unified platform.

The Berkeley connection remained strong. Sangiovanni-Vincentelli joined Cadence's board and would serve for over three decades. The company hired aggressively from Berkeley's graduate programs. Research partnerships kept Cadence at the cutting edge of academic developments. This university-industry symbiosis would become a defining characteristic of the EDA industry.

By the end of 1988, Cadence had gone public, raising $45 million at a valuation of about $200 million. The prospectus painted a picture of unlimited opportunity: "The increasing complexity of integrated circuits... requires sophisticated design automation tools... The Company believes the market for its products will continue to grow rapidly."

They had no idea how right they were. The digital revolution was just beginning, and Cadence had positioned itself at the very center of it. But first, Joe Costello would have to transform a merger of two struggling startups into the undisputed leader of an entire industry.

III. The Costello Era: Building an Industry Leader (1988–1997)

Joe Costello stood before Cadence's board in January 1989 with an audacious proposal: spend $72 million—nearly half the company's market cap—to acquire Gateway Design Automation. The board members shifted uncomfortably. Gateway had just 100 employees and $10 million in revenue. But Gateway had something priceless: Verilog, a hardware description language that was rapidly becoming the industry standard.

"This isn't about buying revenue," Costello argued, his intensity filling the boardroom. "It's about owning the language that every chip designer will use for the next twenty years." He was right. Verilog would become to chip design what C became to software—the fundamental language of an entire industry. The acquisition closed in December 1989, and suddenly Cadence controlled the standard around which the entire ecosystem would organize.

Costello's acquisition strategy was unlike anything the EDA industry had seen. Previous leaders had grown organically or made small tactical purchases. Costello thought bigger. In 1990, he bought Automated Systems Inc., adding critical simulation capabilities. In 1991, came the blockbuster: Valid Logic Systems for $200 million. Valid was a struggling competitor with strong products but weak execution. Costello saw opportunity where others saw risk.

The Valid acquisition was transformative not just for what Cadence gained but for what it signaled to the market. The EDA industry had long believed in a "natural law"—that no EDA company could exceed $300-400 million in revenue. The market was too fragmented, customers too demanding, technology cycles too short. Costello was determined to shatter this ceiling.

His management style was legendary—and polarizing. Employees described him as a force of nature who could inspire and terrify in the same conversation. He instituted a culture of "aggressive accountability." Every quarter, he'd gather the entire company and publicly celebrate wins while brutally dissecting failures. "Joe didn't just want to win," recalled one early employee. "He wanted to destroy the competition and salt the earth behind us."

The numbers told the story. Revenue grew from $91 million in 1989 to $429 million in 1994, then exploded to over $1 billion by 1997. Cadence wasn't just growing—it was defining an entire industry. The company pioneered the "design reuse" methodology, allowing engineers to incorporate pre-designed blocks into their chips. This seemingly simple concept would save the industry billions of dollars and years of effort.

But Costello's true genius lay in understanding the customer's complete journey. While competitors sold tools, Cadence sold solutions. They didn't just provide software; they offered training, consulting, and design services. When customers struggled with complex designs, Cadence engineers would literally sit beside them, sometimes for months, ensuring success. This "high-touch" model was expensive but created unbreakable customer loyalty.

The company's R&D investment was staggering—consistently over 30% of revenue, among the highest ratios in all of software. Costello believed that in EDA, technology leadership was everything. "Our customers are designing products that won't ship for three years," he'd say. "We need to be designing tools for problems they don't even know they'll have."

By 1995, Cadence had emerged as the undisputed leader in EDA. The company commanded nearly 40% market share in key segments. Its customer list read like a who's who of technology: Intel, IBM, Sony, Motorola, Texas Instruments. The Cadence design flow had become the de facto standard for chip design worldwide.

The financial markets took notice. Cadence's stock price increased over 1,000% during Costello's tenure. Wall Street analysts coined a new term: "the Cadence premium"—the higher valuation multiple the company commanded compared to its peers. The company was generating over $200 million in annual cash flow with operating margins approaching 30%.

Yet Costello was becoming restless. He'd achieved everything he'd set out to do and more. Cadence was a billion-dollar company, the undisputed king of EDA. But he was increasingly drawn to education reform and social causes. He joined boards of education nonprofits and started speaking more about technology's role in transforming learning.

In 1997, Chief Executive Magazine named Costello the #1 CEO in America—ahead of Jack Welch, Andy Grove, and Bill Gates. It was the ultimate validation of his decade-long transformation of Cadence. But it was also, in a sense, a farewell. Within months, Costello announced he was stepping down to pursue his passion for education reform.

His departure speech to employees was uncharacteristically emotional. "We didn't just build a company," he said. "We built the foundation for the entire digital age. Every chip, every device, every innovation for the next generation will flow through the tools we created."

The board appointed Ray Bingham, Costello's hand-picked successor, as CEO. Bingham was a steady operator, a sharp contrast to Costello's volcanic personality. The transition seemed smooth. Cadence was at its peak—dominant market position, strong technology, loyal customers. What could go wrong?

As it turned out, everything. The next decade would test Cadence in ways no one could have imagined. The company that Costello built to be invincible was about to face existential threats from within and without.

IV. The Wilderness Years & Near-Death Experience (1997–2008)

The FBI raid came at dawn on May 9, 1995, but its full impact wouldn't detonate until after Costello's departure. Armed federal agents swept through the offices of Avanti Corporation, a Cadence competitor founded by former employees. They were looking for evidence of the most brazen theft of intellectual property in Silicon Valley history—and they found it.

The scandal that would consume Cadence for the next decade had begun innocuously enough. In 1991, several Cadence engineers led by Stephen Wuu left to start Avanti, taking with them, prosecutors would later prove, millions of lines of Cadence source code. They didn't just steal snippets or concepts—they took entire products, changed variable names, and sold them as their own. It was corporate theft on an almost incomprehensible scale.

Under Ray Bingham's leadership, Cadence pursued Avanti relentlessly through the courts. The legal bills mounted—over $100 million by some estimates. The distraction was even costlier. While Cadence's executives were consumed with depositions and legal strategy, a formidable competitor was rising. Synopsys, led by Aart de Geus, was executing flawlessly, gaining market share month after month.

The Avanti saga took a surreal turn in 2001 when Cadence agreed to acquire its nemesis for $265 million. The industry was stunned. Why would Cadence buy a company built on stolen code? The answer was pragmatic: hundreds of customers had designed chips using Avanti tools. Forcing them to switch would cause chaos. Better to swallow pride—and Avanti—than risk customer defection.

But the integration was a disaster. Avanti employees, many of whom had spent a decade as Cadence's bitter enemies, now had to work alongside the people they'd wronged. The cultural clash was toxic. Key engineers left. Product roadmaps stalled. Customers complained about confusion and lack of direction.

Bingham resigned in April 1999, replaced by H. Raymond Bingham (confusingly, no relation). The new Bingham lasted just five years before being pushed out in 2004. The board then turned to Mike Fister, a Intel veteran with no EDA experience. It was a bewildering choice that signaled the board's desperation for fresh thinking.

Fister's tenure was marked by ambitious visions that never materialized. He talked about transforming Cadence into a "systems company" but couldn't articulate what that meant. He launched expensive initiatives into new markets that generated little revenue. Most damaging, he seemed disconnected from the core EDA business that still generated most of Cadence's profits.

The numbers told a story of steady decline. While revenue grew modestly from $1.2 billion in 2000 to $1.4 billion in 2007, Synopsys rocketed past Cadence to become the industry leader. Cadence's stock price languished, falling from over $30 in 2000 to under $15 by 2007. Operating margins compressed as the company struggled with bloated costs and confused strategy.

By 2007, Cadence was in play. Private equity firms circled like vultures. KKR and Blackstone engaged in serious takeover discussions, with bids rumored around $1.6 billion—a fraction of the company's peak value. The board was divided. Some directors wanted to sell and end the misery. Others believed Cadence's technology and customer relationships were worth fighting for.

The financial crisis of 2008 ended the buyout talks, but it also precipitated a full-blown crisis at Cadence. Revenue guidance was slashed. The stock price cratered to under $5. In October 2008, Fister was unceremoniously fired, leaving Cadence rudderless in the worst economic environment since the Great Depression.

The company that Joe Costello had built to dominate forever was now fighting for survival. Employee morale was shattered. Customer confidence was evaporating. Competitors were openly predicting Cadence's demise or dismemberment. The board faced an existential question: bring in another outside CEO for yet another reset, or find someone who understood Cadence's DNA and could restore its former glory?

They chose an unlikely savior: Lip-Bu Tan, a board member since 2004 and successful venture capitalist with no experience running a public company. It was either inspired or desperate—possibly both. As 2008 ended, Cadence's future had never been more uncertain.

V. The Lip-Bu Tan Transformation (2009–2021)

Lip-Bu Tan's first all-hands meeting as CEO in January 2009 was unlike anything Cadence employees had experienced. Instead of grand pronouncements, Tan asked questions. Instead of PowerPoints, he listened. An engineer raised his hand: "Why should we believe this turnaround will be different?" Tan's response was disarming: "Because I'm not here to transform you into something else. I'm here to help you remember what made Cadence great."

Tan was an unusual choice by any measure. Born in Malaysia, educated at MIT, he'd spent his career as a venture capitalist at Walden International, not as an operating executive. But he understood something crucial that his predecessors had missed: EDA wasn't just about technology—it was about deep, almost intimate relationships with customers who were betting their companies on your tools.

His first move was symbolic but powerful. He instituted "customer days" where every employee, from engineers to accountants, would spend time with actual users of Cadence products. The stories that came back were sobering. Customers felt abandoned. They complained that Cadence had become arrogant, unresponsive, more interested in legal battles than solving design challenges.

Tan's transformation started with culture. He dismantled the command-and-control hierarchy that had calcified during the wilderness years. He pushed decision-making down to teams closest to customers. He eliminated layers of middle management that had emerged during the confused strategies of his predecessors. Most importantly, he rekindled the engineering-first mentality that had defined early Cadence.

The financial engineering was equally dramatic. Tan inherited a bloated cost structure and scattered product portfolio. He made surgical cuts—not the broad layoffs that destroy morale, but targeted elimination of redundant projects and underperforming acquisitions. He reinvested every dollar saved into R&D, pushing investment back above 30% of revenue.

But Tan's masterstroke was recognizing a shift that others had missed. The semiconductor industry's center of gravity was moving. It wasn't just chip companies designing chips anymore—it was systems companies. Apple was designing its own processors. Google was building TPUs for machine learning. Amazon was creating custom silicon for AWS. These companies didn't think like traditional semiconductor firms. They needed different tools, different support models, different partnerships.

In 2011, Tan made a prescient observation at an investor conference: "The future of EDA isn't just about making chip design easier. It's about enabling companies that have never designed chips before to create custom silicon." This insight would drive Cadence's strategy for the next decade.

The acquisition strategy under Tan was radically different from Costello's empire-building. Each deal was laser-focused on specific capability gaps. In 2013, Cadence bought Tensilica for $380 million, gaining crucial IP for embedded processors. In 2014, Forte Design Systems brought high-level synthesis capabilities. In 2019, AWR Corporation added RF design tools just as 5G was taking off. The numbers validated Tan's strategy spectacularly. During his time as CEO, Cadence more than doubled its revenue, expanded operating margins and delivered a stock price appreciation of more than 3,200%. From the crisis depths of 2009, when the company was worth less than $2 billion, Cadence's market cap soared past $50 billion by Tan's departure.

The transformation wasn't just financial—it was technological. In 2021, Cadence launched an artificial intelligence platform to streamline processor development. This wasn't AI as buzzword but AI solving real problems: chip designs that once took months could be optimized in days. Reinforcement learning algorithms explored design spaces no human could comprehend, finding solutions that were 10-20% better on key metrics like power and performance.

Perhaps most remarkably, Tan achieved this while maintaining Cadence's engineering culture. R&D spending remained above 30% of revenue throughout his tenure. The company continued hiring the best graduates from Berkeley, MIT, and Stanford. Patents filed annually doubled. Customer satisfaction scores, which had cratered during the wilderness years, reached all-time highs.

The China strategy under Tan was both opportunity and minefield. By 2015, China represented nearly 15% of Cadence's revenue. The company established major R&D centers in Shanghai and Beijing. Chinese semiconductor companies, desperate to catch up with Western competitors, were willing to pay premium prices for cutting-edge tools. But this success would later become a liability as U.S.-China tensions escalated.

Tan's leadership style was distinctly different from the volcanic Costello or the disconnected Fister. Employees described him as quietly intense, always listening, quick to give credit to others. He maintained apartments near major customer sites and would show up unannounced to hear directly from users. His venture capital background gave him unique insights into emerging technologies and startup customers that traditional semiconductor executives might miss.

The cultural transformation extended to diversity and inclusion—areas where the semiconductor industry had historically struggled. Under Tan, Cadence significantly increased hiring of women and underrepresented minorities in engineering roles. The company consistently ranked among the best places to work in technology. This wasn't just virtue signaling—diverse teams designed better products for an increasingly global customer base.

By 2020, Tan had accomplished everything he'd set out to do and more. Cadence was financially strong, technologically advanced, and culturally vibrant. The company that had nearly been sold for parts in 2008 was now worth over $40 billion. But at 61, Tan was ready for new challenges. He'd proven that a financial investor could successfully run a deep technology company. Now it was time for a technologist to take Cadence into the AI era.

Around 40% of Cadence's revenue by 2022 came from customers who were "systems" oriented, or seeking products tailored for various industries that utilized chips in a central role. This shift from pure semiconductor companies to systems companies—achieved under Tan's leadership—would define Cadence's next chapter.

The board's choice for Tan's successor was inspired: Anirudh Devgan, Cadence's president since 2017, who had spent his entire career at the company. Devgan represented continuity with Tan's strategy but brought deep technical expertise in the very areas—machine learning, cloud computing, system design—that would define the next decade. In December 2021, the torch was passed to a new generation.

VI. The AI & Computational Software Era (2021–Present)

Anirudh Devgan's first day as CEO in December 2021 coincided with a seismic shift in the semiconductor industry. OpenAI had just unveiled GPT-3, demonstrating capabilities that seemed like magic. Every technology company suddenly needed AI chips—not in five years, but immediately. The demand for EDA tools capable of designing these massively complex processors was about to explode in ways no one fully anticipated.

Devgan brought a technologist's precision to the CEO role. With a PhD from Carnegie Mellon and 30 years at Cadence, he understood the company's products at a molecular level. More importantly, he recognized that artificial intelligence wasn't just another customer vertical—it was going to transform how chips themselves were designed. "We're entering a recursive loop," he told investors in early 2022. "AI needs better chips, better chips need better design tools, and better design tools increasingly rely on AI."

The Intelligent System Design strategy Devgan unveiled was audacious in scope. Instead of viewing Cadence as an EDA company that sold to chip designers, he repositioned it as a computational software company that enabled intelligent systems across multiple industries. The addressable market wasn't just the $11 billion EDA industry anymore—it was a $30 billion opportunity spanning semiconductors, systems, and even life sciences.

Cerebrus was released in 2021, and is a machine learning-based chip design software which utilizes reinforcement learning and is meant to automatically optimize the Cadence digital design flow. This wasn't incremental improvement—it was revolutionary. Design teams reported 10X productivity gains on complex blocks. Samsung used Cerebrus to design a mobile processor that was 20% more power-efficient than anything their human designers had achieved.

The most surprising move came in September 2022. Cadence acquired OpenEye Scientific Software for $500 million in September 2022, rebranding the company OpenEye Cadence Molecular Sciences and making it into a business unit. To outsiders, it seemed bizarre—what did drug discovery have to do with chip design? But Devgan saw the connection clearly: both were fundamentally computational problems involving massive complexity and optimization. The same AI techniques that could route billions of transistors could potentially identify promising drug compounds. The customer base transformation that Tan had initiated was accelerating under Devgan. By late 2022, Cadence had clients such as Tesla and Apple Inc. These weren't traditional semiconductor companies—they were systems companies designing their own chips for competitive advantage. Tesla's Full Self-Driving chip, designed using Cadence tools, demonstrated performance that traditional automotive suppliers couldn't match.

The Cadence.AI portfolio, powered by GenAI agents, AI-driven optimization and the big data analytics JedAI platform, was delivering unparalleled quality of results and productivity benefits. Revenue nearly tripled over the last year for AI-related products. This wasn't just incremental improvement—customers were achieving design goals that would have been impossible with traditional methods.

In February 2024, Cadence "quietly stepped into the supercomputer business," launching the Millennium M1 platform for creating digital twins. This move signaled Devgan's ambition to expand beyond chip design into full system simulation. Aerospace companies could now model entire aircraft, automotive companies could simulate complete vehicles, all using Cadence's computational platform.

The financial performance under Devgan has been exceptional. Cadence generated $4.6 billion in revenue for fiscal year 2024, up 8% from a year ago. Electronic design automation systems used by chipmakers comprise about 70% of the company's total revenue, according to an earnings report. Annual net income totaled about $1 billion. The company exited 2024 with a record backlog of $6.8 billion, indicating strong demand for its AI-driven chip-to-systems portfolio.

But the China challenge loomed large. Cadence has seen strong growth across its domestic and international businesses, except for China, which had a decline of more than $100 million from 2023 to 2024, John Wall, SVP and CFO, said on the call. The company has only reported three down years for China over its history, and they have never been consecutive. Export restrictions and geopolitical tensions were creating uncertainty in what had been a crucial growth market.

The competitive landscape was also evolving. Synopsys remained the market leader by revenue, but Cadence was closing the gap in key technologies. More concerning was the emergence of open-source EDA tools and the possibility that hyperscalers might develop their own design software. Google had already created internal tools for its TPU designs. Would others follow?

Devgan's response was to double down on what Cadence did best: solving the hardest problems in chip design. The company's focus on AI wasn't just about using machine learning to improve existing tools—it was about fundamentally reimagining the design process. "We're not competing with open source," Devgan explained. "We're enabling designs that are literally impossible without our technology."

The partnership strategy under Devgan was particularly sophisticated. The California-based company has been working closely with clients including Apple, Nvidia, Intel and AMD on next-generation chip designs. These weren't just customer relationships—they were deep technical collaborations where Cadence engineers were embedded in customer design teams, co-developing next-generation methodologies.

Looking ahead, Devgan has positioned Cadence at the intersection of multiple exponential trends. The explosion in AI model sizes is driving demand for ever-more-powerful chips. The shift to chiplet architectures is creating new design challenges that only sophisticated EDA tools can address. The emergence of quantum computing will require entirely new design paradigms. And perhaps most intriguingly, the convergence of biology and silicon—exemplified by the OpenEye acquisition—could open entirely new markets.

The transformation from a traditional EDA company to a computational software platform is nearly complete. Cadence's market cap has soared past $100 billion, making it one of the most valuable software companies in the world. Yet most people have still never heard of it. This invisibility might be Cadence's greatest strength—while others chase headlines, Cadence quietly enables the entire technology industry's future.

VII. Business Model & Competitive Dynamics

The genius of Cadence's business model becomes apparent when you examine a single customer relationship. Take a major semiconductor company like Broadcom. They sign a three-year, $100 million contract for Cadence's complete digital design flow. But here's the catch: it takes 3-5 years to design a complex chip, another 2-3 years of production, and the chip might be in the market for a decade. Once Broadcom's engineers are trained on Cadence tools, once their methodologies are built around Cadence's flow, once their IP is formatted for Cadence's systems, switching to a competitor isn't just expensive—it's almost unthinkable.

This is the subscription model on steroids. Unlike typical SaaS companies that worry about monthly churn, Cadence's customer relationships span decades. The company transitioned from perpetual licenses to time-based licenses in the early 2000s, a move that initially depressed revenue but created the predictable, recurring revenue stream that investors prize. Today, over 90% of revenue is recurring, giving Cadence visibility that most software companies can only dream of.

The pricing power paradox is fascinating. A cutting-edge chip design might cost $500 million to develop. The fab will charge $10,000 per wafer. The end product might generate billions in revenue. In this context, Cadence's software—perhaps $20-30 million over the life of the project—is a rounding error. Yet without it, the chip simply cannot be designed. This creates an unusual dynamic: customers will pay almost any price for tools that work, but they demand absolute reliability and support in return.

The oligopoly structure of the EDA industry isn't an accident—it's an inevitability. The R&D investment required to stay competitive is massive. Cadence spends over $1.5 billion annually on R&D, more than the total revenue of all but the largest EDA companies. This creates an insurmountable moat. A startup might create a brilliant point tool, but customers don't want point tools—they want integrated flows. The startup's exit strategy is almost always acquisition by Cadence, Synopsys, or Siemens (which bought Mentor Graphics).

Consider the competitive dynamics between the Big Three. Synopsys, with about 35% market share, leads in digital design and verification. Cadence, with roughly 30% share, is strongest in custom analog design and PCB tools. Siemens EDA (formerly Mentor), with about 15% share, has particular strength in automotive and aerospace. The remaining 20% is fragmented among dozens of smaller players, most focusing on niche tools.

But here's what's interesting: the Big Three rarely compete on price. Instead, they compete on technology, support, and ecosystem. A typical large customer uses tools from all three vendors, choosing best-in-class solutions for different parts of their flow. Intel might use Synopsys for logic synthesis, Cadence for analog simulation, and Mentor for PCB design. This "coopetition" is unique in enterprise software.

The IP business adds another layer to the model. Cadence doesn't just sell tools—it sells pre-designed circuit blocks that customers can incorporate into their chips. Need a USB interface? A memory controller? A high-speed SerDes? Cadence has pre-verified IP that can save months of design time. This IP generated over $600 million in revenue in 2023, with gross margins exceeding 90%. It's the ultimate high-margin, sticky revenue stream.

Customer concentration is both a risk and a moat. Cadence's top 20 customers account for roughly 40% of revenue. Losing any one of them would be devastating. But these relationships are so deep, so intertwined, that departure is almost impossible. When Apple decided to design its own chips, it didn't build its own EDA tools—it became one of Cadence's largest customers. The switching costs aren't just financial—they're organizational, technical, and temporal.

The cloud transition represents both opportunity and threat. Cadence has been moving its tools to the cloud, allowing customers to access massive compute resources for verification and simulation. This reduces the customer's capital requirements and allows Cadence to charge based on usage rather than licenses. But it also opens the door for new competitors who might offer cloud-native solutions without legacy code constraints.

The services component is often overlooked but crucial. Cadence generates nearly $500 million annually from design services—essentially acting as a contract design house for companies that need extra expertise. This isn't just revenue—it's market intelligence. By working directly on customer designs, Cadence engineers understand exactly what features and capabilities the next generation of tools needs.

The capital efficiency of this model is extraordinary. Cadence generates over $1 billion in free cash flow on less than $200 million in annual capex. The company doesn't need factories, doesn't carry inventory, doesn't have working capital requirements. It's almost pure intellectual property monetization. The return on invested capital consistently exceeds 30%, among the highest in all of software.

Network effects compound over time. Every customer using Cadence tools generates data that helps improve the tools. Every design completed successfully becomes a reference for future customers. Every engineer trained on Cadence tools becomes an advocate when they change jobs. Every university using Cadence in its curriculum creates future customers. It's a virtuous cycle that's been building for 35 years.

The "arms dealer" strategy—selling to all sides in technology wars—has proven brilliant. When AMD and Intel battle for datacenter dominance, both use Cadence tools. When Qualcomm and MediaTek compete in mobile, both are Cadence customers. When Apple and Samsung race to build better chips, Cadence wins regardless of the outcome. This position above the competitive fray provides both stability and growth opportunities.

Yet the model isn't without vulnerabilities. Open-source EDA tools, while still primitive, are improving. In-house tool development by hyperscalers could fragment the market. Most concerning, the consolidation of the semiconductor industry means fewer customers with more negotiating power. If the industry consolidates from 50 major chip companies to 20, Cadence's customer concentration risk increases dramatically.

The beauty of Cadence's business model is its recursive nature. The more complex chips become, the more essential Cadence's tools become. The more essential the tools, the more pricing power Cadence has. The more pricing power, the more R&D investment. The more R&D investment, the better the tools. It's a flywheel that's been accelerating for three decades, and the AI revolution is adding rocket fuel to an already powerful engine.

VIII. Playbook: Lessons for Founders & Investors

The Cadence story offers a masterclass in building and sustaining a platform business in deep technology. The first lesson is perhaps the most counterintuitive: in B2B software, boring is beautiful. Cadence doesn't make headlines like Tesla or capture imaginations like SpaceX. It sells tools to engineers who design chips. Yet this "boring" business has created more sustained shareholder value than most "exciting" consumer technology companies.

The platform transition that Costello orchestrated in the 1990s remains a template for enterprise software companies. He understood that customers don't want to manage relationships with dozens of vendors—they want integrated solutions from trusted partners. But building a platform through M&A is treacherous. Of Cadence's 70+ acquisitions, perhaps half could be considered true successes. The key was Costello's discipline: acquire for technology and talent, not revenue. Integrate immediately and completely. Kill overlapping products ruthlessly. And most importantly, maintain cultural coherence even as the company grows through acquisition.

The cultural transformation under Lip-Bu Tan demonstrates that even 30-year-old companies can reinvent themselves. Tan didn't try to impose a new culture—he revealed the culture that had always existed but had been obscured by years of mismanagement. Engineers want to build great products. Salespeople want to help customers succeed. Leaders want to create value. By removing barriers and bureaucracy, Tan unleashed energy that had been dormant for a decade. The lesson for leaders: sometimes transformation isn't about change—it's about returning to first principles.

The capital efficiency of Cadence's model should be studied by every software entrepreneur. The company generates 30%+ operating margins while spending 30%+ of revenue on R&D. This seems impossible—how can you invest heavily in innovation while maintaining profitability? The answer lies in the recurring revenue model and the discipline to say no. Cadence doesn't chase every opportunity. It doesn't enter markets where it can't be #1 or #2. It doesn't compromise on pricing to win deals. This discipline creates a virtuous cycle: high margins fund R&D, R&D creates differentiated products, differentiated products command premium pricing.

The "arms dealer" strategy—selling to all participants in a market—is powerful but requires careful execution. The temptation is always to pick winners, to go deeper with the market leaders. But Cadence learned that today's leader might be tomorrow's laggard. By maintaining neutrality, by being equally committed to all customers, Cadence became essential infrastructure. The lesson extends beyond EDA: in any market with fierce competition, the suppliers of essential tools often capture more value than the competitors themselves.

Riding technology waves requires anticipation, not reaction. Cadence didn't wait for AI to transform chip design—it began investing in machine learning tools a decade ago. It didn't wait for cloud computing to mature—it began moving tools to the cloud when customers were still skeptical. This anticipatory investment is expensive and risky. Many bets won't pay off. But the ones that do create generational opportunities. The lesson: in deep tech, you need to skate where the puck will be in five years, not where it is today.

The M&A integration excellence that Cadence developed is worth examining closely. Most acquisitions fail because companies try to preserve what they bought. Cadence does the opposite—it completely digests acquisitions, breaking them apart and reassembling the pieces within its platform. This is brutal for the acquired company's identity but essential for platform coherence. Employees from acquired companies are scattered across Cadence teams. Products are renamed and integrated. Sales forces are combined. Within 18 months, it's impossible to tell what was acquired and what was built internally.

The network effects in B2B software are different from consumer networks but equally powerful. Every engineer trained on Cadence tools becomes a node in the network. Every successful design becomes a reference architecture. Every customer problem solved becomes institutional knowledge. These effects compound slowly—over years and decades, not months. But once established, they're nearly impossible to displace. The lesson: in B2B, network effects are about expertise and relationships, not just user counts.

The pricing power paradox—being simultaneously essential and a tiny fraction of customer cost—is a position every B2B company should aspire to. But achieving it requires genuine value creation. Cadence's tools don't just automate existing processes—they enable designs that would be literally impossible otherwise. This expansion of the possible, not just efficiency gains, justifies premium pricing. The lesson: don't just make your customers faster or cheaper—make them capable of things they couldn't do before.

The balance between engineering excellence and customer obsession that Tan achieved is delicate but crucial. Pure engineering companies build brilliant products that no one wants. Pure sales companies make promises they can't keep. Cadence under Tan achieved something rare: world-class technology guided by deep customer intimacy. Engineers spend time with customers. Salespeople understand the technology. Everyone understands that customer success is the only metric that matters.

The geographic expansion strategy offers lessons in globalization. Cadence generates roughly 50% of revenue outside the United States, with significant operations in Europe, Asia, and historically, China. But this isn't just sales offices—it's real R&D, real innovation happening globally. The best analog circuit designers might be in Europe. The most sophisticated verification engineers might be in India. By building true global capabilities, not just sales channels, Cadence accesses talent and markets that purely domestic companies miss.

For investors, Cadence demonstrates the power of investing in "picks and shovels" businesses. During the California Gold Rush, most miners went broke, but the suppliers of picks and shovels got rich. Similarly, most chip companies face brutal competition and cyclical downturns, but Cadence prospers regardless. The lesson: in any gold rush, consider investing in the infrastructure, not the miners.

The transformation from perpetual licenses to subscriptions that Cadence navigated in the 2000s is a playbook for enterprise software transitions. The company accepted short-term revenue pain for long-term gain. It educated investors on new metrics. It restructured sales compensation. It rebuilt financial systems. This transition took five years and was often painful, but it created the predictable, high-margin business model that investors value today.

For founders, perhaps the most important lesson from Cadence is the power of patient capital and long-term thinking. The company has survived multiple near-death experiences, technology transitions, and management crises. What sustained it was a focus on fundamental value creation: helping customers design better chips. Everything else—the business model, the go-to-market strategy, the organizational structure—was secondary to this mission.

IX. Bear vs. Bull Case

The Bear Case: Why Cadence Could Stumble

The bears argue that Cadence is a mature company in a mature industry, trading at historically high valuations with limited growth prospects. The EDA market has grown at roughly GDP plus a few percentage points for decades. Why should that suddenly change? At 20x revenue and 50x earnings, Cadence is priced for perfection in a world full of imperfections.

Customer concentration presents an existential risk that bulls consistently underestimate. If Intel continues to struggle and reduces spending, if Apple decides to build internal tools, if even one major customer defects, the impact would be devastating. The semiconductor industry is consolidating—fewer customers means more negotiating power and pressure on pricing. The days of automatic 5-10% annual price increases may be ending.

Open-source EDA tools, while primitive today, follow the same trajectory as every other software category. Linux destroyed proprietary Unix. Kubernetes killed proprietary container orchestrators. PyTorch and TensorFlow dominate AI frameworks. Why should EDA be different? Universities are increasingly using open-source tools for teaching. A generation of engineers is learning alternatives to commercial EDA. Google has released OpenROAD, an open-source digital design flow. The threat isn't immediate, but it's real and growing.

The China risk cannot be overstated. Revenue from China has already declined by over $100 million, and further restrictions seem likely. More concerning, China is pouring billions into developing domestic EDA capabilities. Companies like Empyrean and Primarius are still far behind, but they have unlimited government support and a captive domestic market. In five years, Chinese companies might not need Cadence at all.

The geopolitical landscape is fracturing the global semiconductor industry that Cadence depends on. Export restrictions, friend-shoring, and techno-nationalism are creating separate technology stacks. A bifurcated world with Western and Chinese semiconductor ecosystems would fundamentally challenge Cadence's global platform strategy. The company could be forced to choose sides, limiting its addressable market.

In-house tool development by hyperscalers poses an existential threat. Google designs its own chips with largely internal tools. Amazon is building EDA capabilities. If Microsoft, Meta, and others follow suit, a significant portion of the most advanced chip design could happen outside Cadence's ecosystem. These companies have the resources and talent to build alternatives. They also have motivations—controlling their destiny, optimizing for their specific needs, avoiding vendor lock-in.

The valuation multiple expansion has been extraordinary—from 15x earnings in 2015 to over 50x today. This isn't supported by fundamentals—growth hasn't accelerated that much. It's multiple expansion driven by low interest rates and AI hype. When the music stops, when rates normalize, when AI disappointments emerge, Cadence could see a violent multiple compression. A return to historical valuations implies a 50% stock price decline.

Technology disruption could come from unexpected directions. Quantum computing might require entirely new design tools. Neuromorphic chips might make traditional digital design obsolete. Optical computing could bypass electronic design altogether. Cadence's massive investment in current-generation tools could become a liability if the underlying technology paradigm shifts.

The AI bubble parallels are concerning. Every company is now an "AI company." Every product has "AI capabilities." This happened before with the internet, mobile, and cloud. Most of the promises won't materialize. When AI reality fails to meet AI hype, companies like Cadence that have been revalued based on AI potential will suffer disproportionately.

The Bull Case: Why Cadence Could Soar

The bulls see Cadence as the indispensable foundation of a $600 billion semiconductor industry that's growing exponentially. AI isn't just another technology trend—it's a fundamental transformation requiring orders of magnitude more compute. Every AI model, every autonomous vehicle, every metaverse experience requires custom silicon. And every custom chip requires Cadence's tools. The company isn't riding a wave; it's providing the surfboards.

The TAM expansion from $11 billion to $30 billion isn't financial engineering—it's real market opportunity. System companies designing their own chips represent a massive new customer base. The OpenEye acquisition opens the $10 billion computational drug discovery market. Digital twin simulation could be a $5 billion opportunity. Cadence is no longer just an EDA company—it's a computational software platform addressing multiple exponentially growing markets.

The subscription model transition is still underappreciated by the market. Over 90% recurring revenue with 110%+ net retention rates creates a compounding machine. Every year, the base grows. Every year, customers spend more. This isn't the volatile, cyclical EDA business of the past—it's a SaaS juggernaut with better metrics than most pure-play cloud companies. As investors fully recognize this transformation, multiple expansion could continue.

The AI design revolution is just beginning. Current AI tools improve productivity by 10-20%. Next-generation tools could automate 50-80% of design tasks. This isn't job destruction—it's capability expansion. Engineers will design 10x more chips, 10x more complex chips, in the same time. The demand for design tools won't shrink—it will explode. Cadence, with its Cerebrus and JedAI platforms, is years ahead of competitors in AI-driven design.

Customer stickiness is even stronger than bears realize. It's not just switching costs—it's ecosystem lock-in. Thousands of engineers trained on Cadence tools. Millions of lines of code in Cadence formats. Decades of design IP in Cadence databases. Methodologies built around Cadence flows. Switching isn't just expensive—it's organizational suicide. No CTO would risk their career on a tool transition that could delay products by years.

The China situation, while challenging, is manageable. China represents less than 15% of revenue and declining. Meanwhile, U.S. government initiatives like the CHIPS Act are driving massive domestic semiconductor investment. Every new fab in Arizona or Texas needs design tools. The reshoring of semiconductor manufacturing could actually increase Cadence's addressable market as new players enter the industry.

The competitive moat is widening, not narrowing. Cadence spends $1.5 billion annually on R&D—more than most competitors' total revenue. This spending is accelerating. The company's 12,000+ patents create a thicket of IP protection. The integration of 70+ acquisitions has created a platform that would take decades and tens of billions to replicate. Open source might nibble at the edges, but it can't match the integrated platform Cadence offers.

The financial metrics are simply extraordinary. 40%+ operating margins. 30%+ return on invested capital. 25%+ free cash flow margins. These aren't peak numbers—they're sustainable given the business model. As revenue scales from $5 billion to $10 billion over the next five years, operating leverage will drive margins even higher. This is one of the highest-quality business models in all of the software.

The venture capital and private equity interest in semiconductor companies is creating new customers for Cadence. Every SPAC that takes a chip company public, every venture round in an AI semiconductor startup, every private equity rollup in the industry creates demand for EDA tools. The democratization of chip design—from hyperscalers to startups—expands Cadence's market faster than traditional semiconductor growth.

The valuation, while high on trailing metrics, is reasonable on forward estimates. If Cadence achieves its stated goal of $10 billion in revenue by 2028 with 45% operating margins, the stock is trading at less than 15x 2028 earnings. For a company with this quality, growth, and moat, that's not expensive—it's fair. The multiple expansion reflects a quality rerating that's justified by the business transformation.

The strategic value to potential acquirers is enormous. Microsoft, Google, or Amazon could justify paying $150+ billion for Cadence to control critical infrastructure. While regulatory approval would be challenging, the strategic logic is compelling. Even without an acquisition, the possibility provides valuation support.

The Synthesis

The truth likely lies between these extremes. Cadence faces real challenges—customer concentration, geopolitical risks, and valuation concerns are valid. But the company also has extraordinary strengths—market position, customer relationships, and financial performance that few software companies can match.

The key question isn't whether Cadence is a good company—it clearly is. The question is whether it's a good investment at current prices. Bears focus on the price paid today. Bulls focus on the value created tomorrow. Both perspectives have merit.

For long-term investors who believe in the continued exponential growth of semiconductor complexity and the AI revolution, Cadence represents a way to bet on the entire ecosystem without picking individual winners. For value investors concerned about multiples and mean reversion, patience might be rewarded with better entry points.

What's clear is that Cadence will remain central to the semiconductor industry for the foreseeable future. Whether that centrality is worth $100 billion or $150 billion or $75 billion is the debate. But the company's importance to the technology industry is beyond debate.

X. The Future: What Happens Next

The year is 2030. In a glass-walled design center in Cupertino, an engineer speaks to her computer: "Design a neural processing unit optimized for transformer models, 3 nanometer process, under 10 watts." The AI responds not with suggestions but with a complete chip design, simulated, verified, and ready for fabrication. This isn't science fiction—it's the future Cadence is building today.

Quantum computing presents both an existential opportunity and an existential threat. Quantum chips require entirely different design paradigms—superposition, entanglement, and error correction replace transistors and logic gates. Cadence has quietly assembled a quantum design team, acquiring key talent from IBM and Google. The company's bet: classical and quantum computing will coexist for decades, and both will need design tools. Early partnerships with quantum startups like PsiQuantum and Rigetti position Cadence to dominate this nascent market. But if quantum computing remains perpetually "five years away," these investments could prove worthless.

The biology-silicon convergence accelerated by the OpenEye acquisition could transform Cadence from an EDA company into something unprecedented: a computational platform for designing both chips and drugs. The same optimization algorithms that route billions of transistors can search vast molecular spaces for drug candidates. The same verification techniques that ensure chip functionality can predict drug interactions. By 2030, Cadence could generate as much revenue from pharmaceutical companies as from semiconductor firms. Or this grand vision could prove to be an expensive distraction from the core business.

The China question will define the next decade. Three scenarios seem plausible. In the optimistic case, tensions ease, trade normalizes, and Cadence resumes growth in the world's largest semiconductor market. In the pessimistic case, complete decoupling forces Cadence to abandon China entirely, losing 15% of revenue permanently. In the most likely case, a messy middle ground emerges—restricted access to cutting-edge tools but continued sales of mature technologies, constant navigation of export controls, and gradual share loss to domestic competitors. Cadence is preparing for all three scenarios, but only one will materialize.

Consolidation endgame calculations occupy every strategic planning session. With Cadence valued at $100 billion and Synopsys at $85 billion, a merger would create a $185 billion EDA monopoly. Antitrust concerns would be enormous, but the industrial logic is compelling. Combined, they would have 65% market share, pricing power would be absolute, and R&D efficiency would improve dramatically. More likely is the acquisition of Siemens EDA (formerly Mentor Graphics), valued around $10 billion. This would give Cadence undisputed leadership while potentially passing regulatory scrutiny. But the most intriguing possibility is acquisition by a hyperscaler—Microsoft or Google buying Cadence to ensure chip design sovereignty.

The AI designing AI chips recursive loop is accelerating faster than anyone anticipated. Cadence's latest tools don't just assist human designers—they autonomously explore design spaces humans never imagined. The philosophical implications are profound. If AI can design better chips than humans, and those chips run AI that designs even better chips, where does human creativity fit? Cadence is betting that human intuition and AI optimization will remain complementary, but this assumption might prove naive. The company could be automating itself out of relevance, or it could be creating tools so powerful that human designers become even more valuable as creative directors rather than implementers.

New architectural paradigms are emerging that could reshape the entire industry. Chiplet designs, where multiple small chips are combined into one package, require entirely new design and verification methodologies. Neuromorphic computing, mimicking brain structures, needs tools that don't yet exist. Photonic chips, using light instead of electrons, demand fundamentally different design approaches. Cadence is investing in all these areas, but resources are finite. Betting wrong could cede leadership to more focused competitors.

The edge AI explosion could dwarf the datacenter opportunity. Every smartphone, every car, every security camera, every industrial sensor will have AI capabilities. These chips have different requirements—ultra-low power, real-time processing, cost sensitivity. Cadence is adapting its tools for edge design, but this market might require fundamentally different approaches. Startups like Edge Impulse are creating specialized tools for edge AI. If they gain traction, Cadence's datacenter-centric platform could miss the bigger opportunity.

Environmental and sustainability pressures are reshaping chip design priorities. The semiconductor industry consumes enormous amounts of energy and water. Regulators are demanding greener chips, greener fabs, greener design processes. Cadence is positioning itself as the leader in sustainable design—tools that optimize for energy efficiency, that minimize material usage, that enable circular economy principles. This could become a major differentiator, or it could be expensive virtue signaling that customers don't value.

The talent war will intensify. Cadence needs the world's best computer scientists, but so does every technology company. The company's location in expensive Silicon Valley is both advantage and handicap. Access to Stanford and Berkeley talent is crucial, but cost of living drives talent elsewhere. Cadence is expanding R&D centers in lower-cost locations—Austin, Pittsburgh, Bangalore—but maintaining culture and collaboration across geographic boundaries is challenging. The company that once benefited from the Berkeley Mafia might struggle to attract the next generation of academic superstars.

The metaverse and spatial computing could create demand for entirely new chip categories. Rendering virtual worlds requires massive parallel processing. Augmented reality needs ultra-low latency. Brain-computer interfaces need unprecedented precision. These aren't incremental improvements to existing chips—they're new categories requiring new tools. Cadence's partnership with Meta on custom silicon is an early bet, but the metaverse might be another false dawn like 3D TV or Google Glass.

Looking at the next decade, Cadence faces a fundamental choice: remain a pure-play EDA company, the best at what it does, or transform into something broader—a computational software platform serving multiple industries. The focused approach preserves the core business but limits growth. The platform approach offers massive expansion but risks losing focus.

The most likely scenario is that Cadence continues its careful evolution, adding adjacent capabilities while maintaining EDA leadership. Revenue grows from $5 billion to $10 billion by 2030. The company remains independent but explores strategic partnerships with hyperscalers. China becomes a smaller part of the business, offset by growth in India and reshored U.S. manufacturing. AI tools automate routine design tasks but create demand for more chips, not fewer tools.

But the beauty of Cadence's position is that it wins in almost any future. If AI transforms everything, Cadence enables the chips that run AI. If quantum computing arrives, Cadence designs quantum chips. If biology and silicon merge, Cadence bridges both worlds. If the metaverse explodes, Cadence creates the tools to build it. The company isn't betting on any single future—it's positioning itself as essential infrastructure for all of them.

The ultimate question isn't whether Cadence will remain relevant—it will. The question is whether it will remain independent. As chips become more strategic, as nations compete for semiconductor supremacy, as companies seek to control their silicon destiny, Cadence becomes too important to remain neutral. Someone—a government, a hyperscaler, a consortium—might decide that Cadence is too critical to remain independent. That day might be the ultimate validation of everything Joe Costello, Lip-Bu Tan, and Anirudh Devgan built—a company so essential that the world can't afford to let it remain free.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube