Crown Holdings: The 133-Year Packaging Empire That Seals the World's Beverages

How a Baltimore Bottle Cap Inventor Built a Fortune 500 Sustainability Play—and What Investors Need to Know Today

I. Introduction & Episode Roadmap

Picture this: you crack open an ice-cold Coca-Cola on a summer afternoon. The satisfying psssht of escaping carbonation. The metallic glint of the aluminum can catching the light. In that mundane moment, you're holding the product of 133 years of relentless innovation, near-death experiences, and strategic brilliance.

The company behind that can? Crown Holdings, Inc.—an American multinational packaging company headquartered in Tampa, Florida, that designs and manufactures rigid-metal packaging including aluminum beverage cans, metal food cans, aerosol cans, and specialty packaging. In 2024, Crown reported net sales of $11.801 billion, making it the second-largest producer of beverage cans in the world. The company ranks No. 359 on the Fortune 500 list for 2025.

But here's what makes Crown Holdings a fascinating case study: this is a company that almost went bankrupt in 1957, diversified into ice cube trays, experimented with plastic bottles, took a $1.21 billion write-down in 2001, and somehow emerged as one of the most compelling sustainability plays in industrial America.

The central question we'll explore: How does a 133-year-old bottle cap company become a Fortune 500 sustainability play?

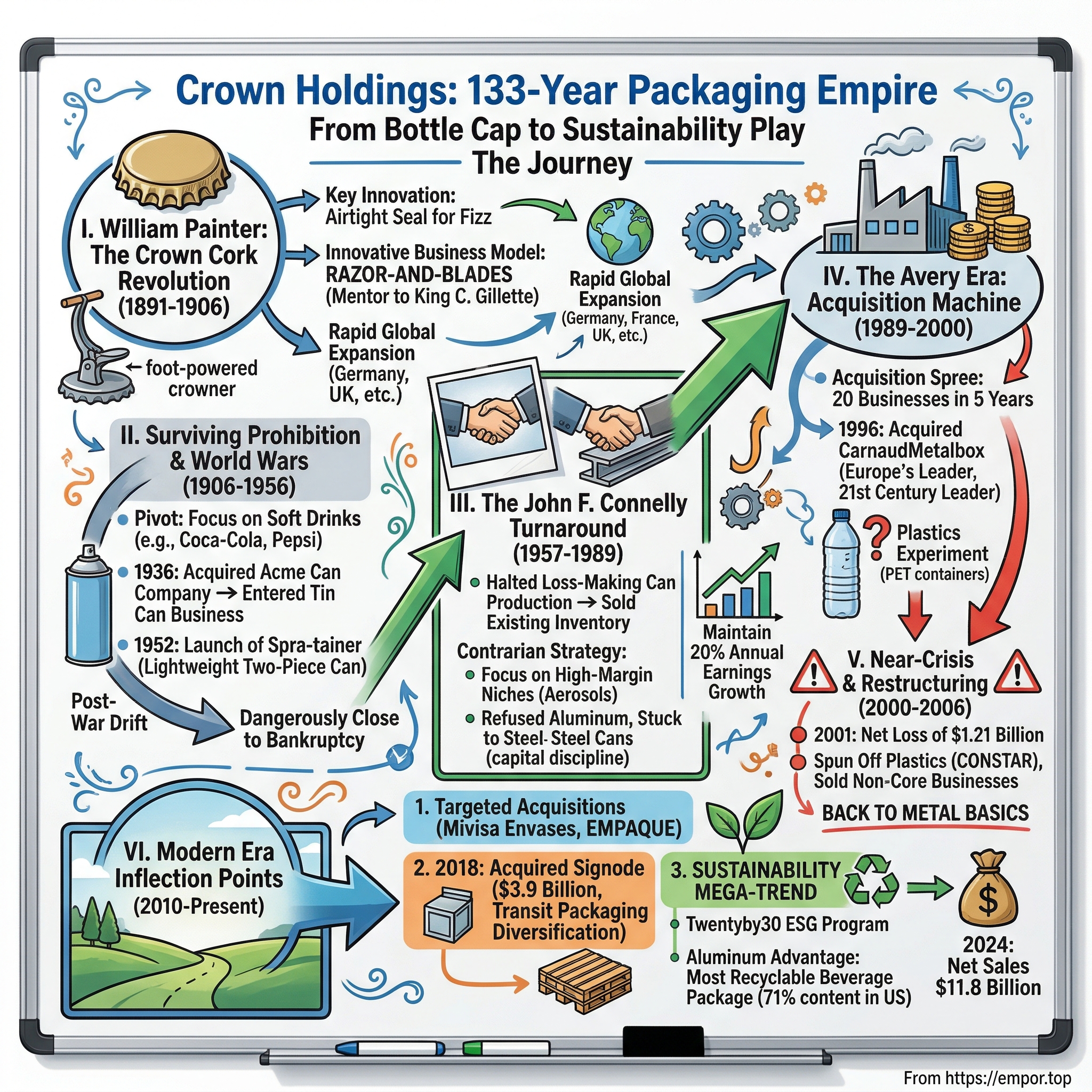

The answer lies in a series of strategic pivots, contrarian bets, and leadership transitions that read like a masterclass in industrial capitalism. Founded in 1892 as the Crown Cork & Seal Company by a Quaker inventor with just $200, the company has navigated Prohibition, two World Wars, the aluminum revolution, a leveraged acquisition spree, and now the global sustainability mega-trend.

The themes that emerge from Crown's story are universal: innovation in "boring" industries, turnaround stories when all seems lost, consolidation playbooks that create global champions, and the sustainability mega-trend reshaping consumer preferences. Whether you're a long-term investor, a business strategist, or simply curious about the hidden giants that make modern life possible, Crown Holdings offers lessons that transcend the packaging industry.

Let's begin where all great stories do—with a problem that needed solving.

II. William Painter & The Crown Cork Revolution (1891-1906)

The Inventor from Maryland

In the late 1880s, carbonated beverages were exploding in popularity, but bottlers faced a maddening problem: keeping the fizz in the bottle. Cork stoppers, rubber seals, and various contraptions had all been tried, but nothing worked reliably. Carbonation escaped. Products spoiled. Customer complaints mounted.

Enter William Painter, a Quaker from Maryland with an inventor's obsession. Painter wasn't a beverage industry insider—he was a machinist and tinkerer who had already patented dozens of inventions, from counterfeit coin detectors to passenger car seats. But he saw the bottling problem as a solvable engineering challenge.

His breakthrough came in 1891: the crown cork bottle cap. This simple crimped metal cap with a cork liner created an airtight seal that preserved carbonation indefinitely. Painter obtained patents on February 2, 1892, and immediately recognized he had something transformational.

But Painter's true genius wasn't just the cap itself—it was the business model.

The Razor-and-Blades Model Before Gillette

Painter started the Crown Cork & Seal Company of Baltimore with a mere $200. Most entrepreneurs would have focused on selling caps. Painter thought bigger.

By 1898, he had created a foot-powered crowner device to sell to bottlers and retailers so that they could seal bottles with his caps quickly and easily. The machines were priced affordably. The caps—the consumable—were where the profit lived. Bottlers who bought Painter's sealing machines became locked into his cap ecosystem.

This was the razor-and-blades model a full decade before King C. Gillette made it famous with disposable razor blades. In fact, the connection is more than coincidental: Gillette was inspired while working as a salesman for Crown Cork & Seal to create a disposable product—the safety razor blade. Painter had effectively mentored one of business history's most influential innovators.

Global Expansion at Remarkable Speed

What's remarkable about Painter's early years is the speed of internationalization. Most companies of that era remained regional for decades. But Painter quickly expanded the company overseas, and by the time of his death in 1906, Crown Cork & Seal had manufacturing operations in Germany, France, the United Kingdom, Japan, and Brazil.

Why the rush to go global? Painter understood that carbonated beverages were a worldwide phenomenon waiting to happen. Coca-Cola was already spreading across America. European brewers needed better sealing technology. The patent protection that made Crown's position defensible in the U.S. needed replication abroad before competitors emerged.

Painter's death in 1906 marked the end of the founder's era, but the company he built had established a template: technological innovation, smart business model design, and global ambition. These would prove to be enduring characteristics, even as the company faced challenges Painter could never have imagined.

For investors, the Painter era illustrates a timeless principle: sustainable competitive advantage often comes not from the product itself, but from how the product is sold. Crown's early lock-in with the crowning machine created switching costs that protected margins for decades. The lesson would be tested severely in the years to come.

III. Surviving Prohibition & The World Wars (1906-1956)

When the Core Market Vanishes

On January 17, 1920, the Eighteenth Amendment took effect, and Crown Cork & Seal faced an existential crisis. The company had built its business on sealing beverages—and a substantial portion of those beverages were now illegal. Brewers shuttered. Bottling lines went silent. The crown cap market contracted overnight.

To address market changes after World War I and Prohibition, Crown focused heavily on soft drinks. This pivot proved prescient. While alcohol consumption went underground, legitimate soft drink companies like Coca-Cola and Pepsi-Cola experienced explosive growth. Americans still wanted cold, carbonated refreshment—they just couldn't have alcohol in it.

Crown Cork & Seal survived by following its customers to legal beverages. But the company's leadership recognized that relying solely on bottle caps was a vulnerability. Diversification became the strategy.

The Tin Can Acquisition

In 1936, Crown acquired the Acme Can Company of Philadelphia, enabling the company to enter the tin can business for the first time. This was a pivotal moment—Crown was no longer just a closure company but a container company.

The timing was fortuitous. The following year, in 1937, Crown perfected the electrolytic tin plating process and launched the Crowntainer, a two-piece necked-in steel can sealed with a crown. This hybrid innovation combined Crown's closure expertise with its new canning capabilities.

The Crowntainer represented something new: vertical integration of packaging solutions. Rather than selling components, Crown could now offer complete packaging systems. This capability would prove essential during the coming global conflict.

War Production and Innovation

During World War II, Crown produced war products such as the Kork-N-Seal, the Pour-N-Seal, and the Merit Seal, as well as gas mask canisters. The company's metal fabrication expertise translated directly to military applications.

But the war years also accelerated innovation. Aerosol technology, developed for military insecticide delivery, would eventually transform consumer products. Crown was paying attention.

In 1952, the Spra-tainer, a lightweight two-piece aerosol can for the food, personal care, household, and insecticide markets, made its debut. This wasn't just a new product—it was entry into an entirely new category with massive growth potential. Hair spray, deodorant, cooking spray, cleaning products—the aerosol can would become ubiquitous in American households.

Post-War Drift

Yet despite these innovations, the company drifted in the post-war years. Management allowed unprofitable product lines to accumulate. Corporate focus scattered across too many initiatives. The entrepreneurial energy of the Painter era had faded into bureaucratic complacency.

By the mid-1950s, Crown Cork & Seal lacked strong leadership and was dangerously close to bankruptcy. The company that had pioneered the crown cap, survived Prohibition, and contributed to the war effort was now on the verge of collapse.

What the company needed was a leader willing to make painful decisions. What it got was John F. Connelly—and one of the most remarkable turnarounds in American industrial history.

IV. The John Connelly Turnaround: A Harvard Business School Case Study (1957-1989)

The Near-Death Experience

In 1957, John F. Connelly, an Irishman and the son of a Philadelphia blacksmith, became president of Crown Cork & Seal. What he inherited was a disaster.

The company suffered a first-quarter loss of over $600,000. Bankers Trust was calling in a $2.5 million loan, with an additional $4.5 million due by the end of the year. Crown Cork & Seal was, in the blunt language of finance, dangerously close to bankruptcy.

Connelly was not a typical executive. He had no Ivy League pedigree, no McKinsey playbook. What he had was a blacksmith's son's understanding of hard work, a ruthless practicality, and the courage to do what needed doing—no matter how painful.

Ruthless Triage

Connelly took dramatic measures immediately. His first move was counterintuitive: he halted can production altogether. Rather than continuing to manufacture at a loss, Connelly filled the company's remaining orders with a large stockpile of unpurchased cans that had been allowed to accumulate. The customers did not object, and the money saved by selling old inventory instead of producing new cans brought Crown Cork close to solvency.

This was brilliant crisis management. Connelly recognized that continuing to produce would only accelerate losses. Better to monetize existing inventory while buying time to restructure.

Next came the cuts. Unprofitable and unpromising product lines, such as ice cube trays, were immediately discontinued. Why was Crown Cork & Seal making ice cube trays? Exactly—nobody could answer that question coherently, which was precisely why the product line had to go.

Connelly also reduced overhead costs, particularly those incurred by redundant labor. In one 20-month span, the payroll was cut by 25 percent, with pink slips issued to managers and unskilled workers alike. There was no sentimentality, no protecting favored departments. Everyone was measured against contribution.

The moves were drastic but necessary. By the end of 1957—the same year Connelly took over—the company was making both cans and profits. The following year, Crown Cork moved its corporate headquarters to Philadelphia, symbolizing a fresh start.

The Contrarian Strategy

What happened next is what made the Connelly era legendary—and why Crown Cork & Seal became a Harvard Business School case study.

Crown Cork & Seal was an enigma within the container business because it had achieved financial results that contradicted industry logic. Profit margins in can manufacturing had been small and shrinking for decades, and can makers like American and Continental had been relying on diversification and economies of scale to create profits.

The conventional wisdom was clear: diversify beyond cans, acquire competitors to gain scale, and spread fixed costs across multiple product lines. Crown Cork & Seal, on the other hand, had neither expanded into noncontainer fields nor sought to augment its own can making program by purchasing other small can operations.

Yet it managed to maintain an earnings growth rate of 20 percent a year.

How? Connelly's strategy had several distinctive elements:

Focus on High-Margin Niches: Once the initial bankruptcy crisis had passed, Connelly directed Crown Cork & Seal with renewed energy into two areas within which Crown had traditionally held an advantage: aerosol cans and foreign container markets. In the years immediately preceding Connelly's tenure, the company, while not neglecting these markets, had not pursued them with the vigor they warranted.

Crown Cork & Seal had pioneered the aerosol can in 1946, and Connelly was shrewd enough to recognize its potential. Aerosol cans were more complex to manufacture than standard beverage cans, which meant higher margins and less price competition. They also required technical service relationships with customers—creating switching costs that commodity cans lacked.

International Expansion: While competitors focused on the mature U.S. market, Connelly aggressively expanded overseas. Emerging markets needed packaging capacity, and Crown could provide it without the cutthroat competition of the American market.

By 1977, with 60 plants globally, Crown became one of the world's leading producers of cans and crowns. Net sales reached $1 billion.

Technology Contrarianism: Perhaps most remarkably, Connelly once again went against industry trends when the aluminum two-piece can emerged as the industry's future. Just as he had refused to participate in the diversification trend years before, he steered Crown Cork clear of the aluminum two-piece can. He decided instead to concentrate on the old-style three-piece steel can that had been the mainstay of the industry for years.

This seemed crazy at the time. Aluminum cans were lighter, cheaper to ship, and increasingly preferred by customers. But Connelly recognized that the capital investment required for aluminum conversion was massive—and that steel cans still had years of profitable life ahead. He would let competitors bear the capital costs and risks of the transition.

The Connelly Management Philosophy

Beyond strategy, Connelly embodied a distinctive management style that became embedded in Crown's culture. He was legendary for cost consciousness—famously keeping corporate headquarters spartan while competitors built gleaming office towers. He believed in promoting from within, creating loyalty and institutional knowledge. He made decisions quickly and expected the same from subordinates.

Most importantly, Connelly understood that in a low-margin business, operational excellence was everything. A 1% improvement in can yield or a 2% reduction in aluminum waste meant the difference between profit and loss. Crown under Connelly became obsessed with these incremental gains.

For investors, the Connelly era offers a powerful lesson: conventional wisdom is often wrong, and the courage to be contrarian can generate extraordinary returns. Crown's refusal to diversify looked foolish at the time—until it didn't. The company's focus on niches and international markets created defensible positions that broad-line competitors couldn't easily attack.

But Connelly was mortal, and by the late 1980s, his health was failing. The question of succession loomed over a company that had been defined by one man's vision for three decades.

V. The Avery Era: Acquisition Machine (1989-2000)

The Successor's Dilemma

In 1989, after a period of diminishing health, John Connelly died, and William Avery took over the company. Avery faced a challenge familiar to successors of legendary founders: how do you maintain momentum without the person who defined the company's identity?

Avery was clear-eyed about the situation. He remarked: "When I became president in 1989, I had to light a fire and get the company going again. The company's growth had slowed down in the 1980s. John Connelly's health was not good, the company had no debt, and we were very vulnerable to a takeover."

That last point was crucial. Connelly's debt aversion had left Crown with a pristine balance sheet—which, in the leveraged buyout era of the late 1980s, made it a target. Any acquirer could use Crown's own debt capacity to fund a hostile takeover. Avery needed to put that balance sheet to work before someone else did.

The Acquisition Spree

Avery began acquiring companies at a rapid pace. In five years, he purchased 20 businesses with combined sales in the billions. Under Avery, Crown's revenues doubled to $3.8 billion in 1993 and reached almost $4.5 billion in 1994.

The logic was clear: consolidation was reshaping the packaging industry, and Crown needed scale to compete. Continental Can's Canadian, U.S., and overseas plants were purchased in three deals, costing a total of $791 million. Each acquisition added manufacturing capacity, customer relationships, and geographic reach.

But Avery's most consequential deal was still to come.

The CarnaudMetalbox Transformation

In 1996, Crown acquired CarnaudMetalbox, Europe's leading manufacturer of metal and plastic packaging, and became the world's packaging leader.

This was a transformational transaction. CarnaudMetalbox was itself the product of a merger between Carnaud of France and MetalBox of the UK—two of Europe's most established packaging companies. The acquisition gave Crown dominant positions across Western Europe overnight.

The completion of the Carnaud purchase vaulted Crown Cork into the top position in the global packaging market. The combined operations seemed to fit nearly perfectly, with Crown a major player in the United States, Carnaud a major player in Europe, and both companies with small but growing presences in Asia.

The deal also provided Crown with a foothold in the specialty packaging area of cosmetics and perfume packaging—a high-margin niche that aligned with Connelly's original philosophy of seeking premium applications.

The Plastics Experiment

Avery wasn't content with metal alone. In 1992, CONSTAR International was acquired, expanding the company's reach into the PET plastic containers market in the beverage, food, and household sectors.

This was a bet on diversification—the very strategy Connelly had rejected. The logic was that customers increasingly wanted packaging solutions across multiple substrates. If Crown could offer both metal and plastic, it would be a more valuable supplier.

The timing seemed reasonable. PET bottles were growing rapidly, taking share from glass in many applications. But the acquisition would prove problematic for reasons that weren't immediately apparent.

The Integration Challenge

By the late 1990s, Crown was a very different company than Connelly had built. Revenues had grown explosively. The geographic footprint spanned the globe. The product portfolio included metal cans, plastic bottles, aerosols, closures, and specialty packaging.

But integration was proving difficult. CarnaudMetalbox brought different management cultures, legacy systems, and operational practices. The plastics business had different economics than metal packaging. And the debt load from acquisitions—while manageable in good times—created vulnerability if conditions deteriorated.

For investors, the Avery era illustrates both the power and the peril of acquisition-driven growth. Buying can be faster than building, but integration risk is real. Crown had assembled a global empire; whether it could operate that empire profitably remained to be seen.

VI. Near-Crisis & Restructuring (2000-2006)

The Debt Hangover

The early 2000s brought a reckoning. The acquisition spree had created a global champion, but it had also created a highly leveraged company in an industry with thin margins.

In 2001, Crown suffered a net loss of $972 million—a staggering reversal for a company that had been consistently profitable under Connelly. But that was just the beginning. Constar, the plastics business, was spun off through an initial public offering. A $1 billion charge was taken to write down the value of the CarnaudMetalbox acquisition. When the dust settled, Crown recorded a net loss of $1.21 billion.

The write-down was an implicit admission: Crown had overpaid for CarnaudMetalbox. The synergies projected at acquisition hadn't materialized. The integration had been more costly and disruptive than anticipated. And market conditions had turned unfavorable.

This was a humbling moment for a company that prided itself on financial discipline. The Connelly-era balance sheet prudence had been replaced by Avery-era leverage, and now the consequences were apparent.

The Restructuring

Management recognized that dramatic action was required. In 2003, a $3.2 billion refinancing plan was completed, and Crown Holdings, Inc. was formed as a new public holding company. This wasn't just financial engineering—it was a comprehensive restructuring of the company's capital structure and operations.

The message to creditors and shareholders was clear: Crown was committed to survival and would take whatever steps necessary to restore financial health.

In 2005-2006, Crown sold its global plastic closures and cosmetics packaging businesses. These were the specialty businesses that had been part of the CarnaudMetalbox rationale. Selling them was painful, but necessary. Crown needed to focus on what it did best—metal packaging—rather than spreading resources across multiple substrates.

Back to Metal Basics

The strategic pivot was explicit: "Back to metal basics." Crown would be a metal packaging company, focused on beverage cans, food cans, and aerosol cans. The plastics experiment was over. The specialty packaging diversification was reversed.

This was, in essence, a return to Connelly's philosophy. Focus on core competencies. Excel at what you do best. Don't chase adjacencies that dilute management attention and capital.

The irony was not lost on Crown veterans. The company had spent a decade diversifying, acquiring, and expanding—only to conclude that the original strategy had been right all along. Billions of dollars and years of management attention had been devoted to a strategic detour.

For investors, the 2000-2006 period offers a cautionary tale about acquisition integration and the seduction of diversification. Crown's survival was never truly in doubt, but shareholder value was destroyed by overpaying for acquisitions and venturing into businesses the company didn't understand as well as its core.

The question now was whether Crown could rebuild from this chastened position—and whether the metal packaging market offered enough growth to support a company of Crown's scale.

VII. Modern Era Inflection Points (2010-Present)

Inflection Point #1: The Return to Growth Through Targeted Acquisitions

By 2010, Crown had stabilized. The debt had been refinanced. The non-core businesses had been divested. The company was focused again on metal packaging. But organic growth in mature markets was limited. Management recognized that disciplined acquisitions—very different from the 1990s spree—could add value.

In 2014, Crown purchased Mivisa Envases, SAU, a leading Spanish manufacturer of two- and three-piece food cans and ends. This acquisition significantly built upon the company's existing position in the strategically important European food can segment.

The strategic logic was sound. Food cans were a stable, if unglamorous, business with steady demand and established customer relationships. Mivisa added scale in a region where Crown was already present, creating procurement and operational synergies.

In 2015, Crown acquired EMPAQUE, a leading Mexican manufacturer of aluminum cans and ends, bottle caps, and glass bottles for the beverage industry, from Heineken N.V. This deal significantly enhanced the company's position in beverage cans regionally and globally.

These were bolt-on acquisitions, not transformational bets. Management had learned from the CarnaudMetalbox experience. Smaller deals with clear integration paths and identifiable synergies were lower risk than mega-mergers.

Inflection Point #2: The $3.9 Billion Signode Acquisition (2018)

On October 30, 2018, Crown announced it had agreed to acquire Signode, a global leader in transit packaging, for $3.9 billion. This was Crown's largest deal since CarnaudMetalbox—and it represented a strategic evolution.

Timothy J. Donahue, President and CEO of Crown, stated: "With this acquisition, we add a portfolio of premier transit and protective packaging franchises to our existing metal packaging business, thereby broadening and diversifying our customer base and significantly increasing our cash flow. Signode's products supply critical in-transit protection to high value, high volume goods across a number of end-markets, including metals, food and beverage, corrugated, construction, and agriculture."

With pro forma sales and adjusted EBITDA of $2.3 billion and $384 million, respectively, Signode was the world's leading supplier of transit packaging systems and solutions. This wasn't consumer packaging—it was the strapping, wrapping, and protective materials that secure goods during shipping.

Why transit packaging? Several factors made it attractive:

Diversification Without Distraction: Unlike the plastics experiment, transit packaging shared operational characteristics with metal packaging—industrial B2B customers, global footprint, consumables-based business model.

Cash Flow Enhancement: Signode's business was less capital intensive than beverage can manufacturing, with strong free cash flow generation. Adding it improved Crown's overall cash conversion.

Counter-Cyclical Balance: Transit packaging served different end markets than beverage cans, providing some diversification against consumer demand fluctuations.

The deal closed in April 2019, and integration proceeded more smoothly than the CarnaudMetalbox acquisition two decades earlier. Management had applied the lessons learned.

Inflection Point #3: The Sustainability Mega-Trend

Perhaps the most significant development of the modern era is one that Crown didn't engineer but has profited from enormously: the global shift toward sustainable packaging.

In 2020, Crown launched Twentyby30, an ambitious, comprehensive sustainability program that outlines twenty measurable environmental, social, and governance (ESG) goals to be completed by 2030 or sooner. The program covers emissions reduction, water stewardship, waste minimization, and social responsibility.

But Crown's sustainability story isn't primarily about corporate programs—it's about the inherent advantages of aluminum.

In recent years, aluminum beverage can manufacturers have seen increased demand for environmentally friendly containers by current and new beverage brands. Beverage cans are in-demand and represent roughly 78% of the worldwide metal can market, projected to grow at a compound annual growth rate of 2.3% from 2024-2032.

Long-standing customers are moving away from plastic bottles and other packaging substrates to cans due to environmental and sustainability reasons. This isn't greenwashing—it reflects genuine differences in recycling economics.

The average recycled content of an aluminum can made in the United States stands at 71%, far exceeding glass bottles at 23% and plastic bottles at 3-10%. The aluminum can remains by far the most valuable beverage package in the recycling bin, with a value of $1,338 per ton compared to $215 per ton for PET and a negative value of $23 per ton for glass.

This last point is crucial. Recyclers want aluminum cans. They pay to acquire them. Glass and plastic, by contrast, often cost more to recycle than the recovered materials are worth. This economic reality means aluminum recycling actually happens at scale, while plastic recycling rates remain stubbornly low.

Recent Performance and Progress

In 2024, Crown Holdings reported net sales of $11.8 billion, with beverage cans accounting for 67% of its revenue, followed by transit packaging at 18%.

The sustainability initiatives are showing measurable progress. By the end of 2024, Crown Holdings achieved a 26% reduction in Scope 1 and Scope 2 GHG emissions from the 2019 baseline, representing over half of the 2030 goal. The company also achieved a 16% reduction in Scope 3 emissions—the harder-to-control emissions from supply chains and product use.

For investors, the sustainability mega-trend represents perhaps the most important tailwind in Crown's history. After decades of competing with plastic on cost and convenience, metal packaging now has a compelling environmental advantage that resonates with consumers, regulators, and brand owners alike. This isn't a short-term marketing trend—it's a structural shift in how the world thinks about packaging.

VIII. How the Business Works Today

Segment Breakdown

Crown operates through four primary segments: Americas Beverage, European Beverage, Asia Pacific, and Transit Packaging.

The company's revenue breakdown highlights its core beverage can operations, which account for approximately 67% of total net sales. Key segments include Americas Beverage at $5.15 billion (about 43%), European Beverage at $1.94 billion (16%), Asia Pacific at $1.30 billion (11%), Transit Packaging at $2.26 billion (19%), and Other at $1.37 billion (11%).

Americas Beverage is by far the largest segment, reflecting the maturity and scale of the North American and Latin American beverage markets. This segment serves major customers including Coca-Cola, PepsiCo, and Anheuser-Busch InBev, as well as numerous craft beverage producers who have driven growth in recent years.

European Beverage benefits from strong sustainability regulation that has accelerated the shift from plastic to aluminum. The European Union's aggressive plastic reduction targets have made metal packaging increasingly attractive to brand owners.

Asia Pacific represents the highest growth potential, as emerging market consumers increase beverage consumption and sustainability consciousness spreads. Crown has been investing in capacity expansion throughout the region.

Transit Packaging, the Signode business, provides diversification and stable cash flows. This segment serves industrial customers across metals, food and beverage, corrugated, construction, and agriculture.

Global Footprint

As of 2024, Crown employs over 23,000 people at 189 plants in 39 countries. This geographic diversity is both a competitive advantage and an operational necessity.

Can manufacturing economics require proximity to customers. Shipping empty cans long distances is uneconomical—they're mostly air. Crown's plant network is therefore designed to locate manufacturing capacity close to filling operations. When Coca-Cola or AB InBev builds a new bottling plant, they need a can supplier nearby.

With the purchase of Signode, the company also has a presence in a wide variety of protective transport packaging. Although it's headquartered in the United States, the vast majority of Crown's sales come from its operations in Europe, South America, and Southeast Asia.

This international exposure provides both opportunities and risks. Currency fluctuations can significantly impact reported results. Political instability in certain markets creates operational challenges. But international markets also offer growth rates unavailable in mature regions.

Customer Relationships

Crown's products are used by manufacturers and marketers of packaged consumer goods, including beverage companies such as Anheuser-Busch InBev, Coca-Cola, and Pepsi-Cola.

The customer base is highly concentrated. A handful of global beverage companies account for a substantial portion of Crown's revenue. This creates relationship intensity—Crown's executives know their counterparts at major customers personally, and contracts are negotiated over years rather than days.

The concentration also creates risk. Losing a major customer would be severely damaging. But the switching costs described later in this analysis provide some protection.

Operational Model

Crown Holdings operates through a decentralized management structure with manufacturing facilities located close to customer operations to minimize transportation costs and improve service.

The company emphasizes sustainability, focusing on reducing energy consumption, minimizing waste, and promoting the recyclability of its metal packaging. These aren't just marketing claims—they represent operational imperatives that affect costs and customer relationships.

Manufacturing excellence is the core competency. Crown's plants are constantly optimizing—reducing aluminum gauge while maintaining can integrity, improving fill rates, minimizing downtime, and reducing energy consumption per can produced. In a commodity business, these operational improvements determine profitability.

For investors, Crown today is a focused, global, operationally excellent company with strong market positions in beverage cans and transit packaging. The chaos of the early 2000s is long past. The question now is whether the company can continue growing in a world increasingly concerned about packaging sustainability—and whether that growth will translate into shareholder returns.

IX. Competitive Positioning: Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

Building a beverage can manufacturing facility requires massive capital investment—hundreds of millions of dollars for a single plant. The specialized equipment, quality certifications, and technical expertise create formidable entry barriers.

More importantly, new entrants face a chicken-and-egg problem: customers won't commit to long-term contracts without proven manufacturing capability, but building capability without customer commitments is financial suicide.

The geographic proximity requirement creates another barrier. A new entrant can't serve the market from a single low-cost location—they need facilities near customer filling plants across multiple regions. This multiplies the capital requirement.

Technical expertise accumulates over decades. Crown has 133 years of experience in metal forming, coating, sealing, and high-speed manufacturing. A new entrant would be competing against deeply embedded process knowledge.

For investors, low threat of new entrants is positive. Existing players don't face constant disruption from well-funded startups or tech companies entering the space.

2. Bargaining Power of Suppliers: MODERATE

Aluminum and steel are commodity inputs with multiple global suppliers. Crown isn't dependent on any single aluminum producer, and global commodity markets provide price transparency.

However, input costs can be volatile. Aluminum producers cut output and raised prices starting in 1994, demonstrating that supply discipline can affect packaging economics. The strength of the U.S. dollar can also reduce the value of overseas sales while potentially affecting input costs differently across regions.

Crown manages supplier risk through hedging strategies and long-term supply agreements. These don't eliminate volatility but do provide planning visibility.

The moderate supplier power means that Crown can't entirely control its cost structure—aluminum prices affect profitability regardless of operational excellence.

3. Bargaining Power of Buyers: HIGH

This is Crown's greatest structural challenge. The customer base is concentrated among major beverage companies like Coca-Cola, AB InBev, and PepsiCo. These are sophisticated procurement organizations with immense purchasing power.

Customers can switch suppliers, though switching costs exist due to co-located facilities and technical integration with filling lines. But the threat of switching provides negotiating leverage even if switching is rare.

Crown's products are inputs to its customers' products—there's no consumer awareness or preference for Crown specifically. If Coca-Cola switched can suppliers tomorrow, consumers wouldn't notice or care.

The high buyer power constrains pricing. Crown can't simply pass through cost increases—customers push back. Profitability depends on operational efficiency rather than pricing power.

4. Threat of Substitutes: MODERATE-LOW (and declining)

Historically, aluminum cans competed with plastic bottles, glass bottles, and cartons. Each substrate had advantages for certain applications.

But the sustainability mega-trend is changing this calculus. An alternative material to replace plastics and ease environmental concerns is aluminum, since it is recyclable, sustainable, and produces low carbon emissions when recycled.

Plastic bottles are being displaced by cans due to sustainability concerns. Major beverage brands are actively seeking to reduce plastic usage, driven by consumer preferences, regulatory pressure, and corporate ESG commitments.

Glass is heavy and expensive to transport. For many applications, it's simply not cost competitive with aluminum—regardless of sustainability considerations.

Cartons exist for some applications but lack aluminum's recyclability advantages and aren't suitable for carbonated beverages.

The declining substitute threat is perhaps the most important structural improvement in Crown's competitive position in decades. After years of defending against plastic encroachment, aluminum is now taking share back.

5. Industry Rivalry: HIGH

O-I Glass, Amcor, Ball, Silgan Holdings, and Greif are some of the competitors of Crown Holdings. The beverage can market specifically is dominated by Crown and Ball Corporation, with intense competition for major contracts.

Consolidation has reduced the number of players, but competition remains intense. Price competition in commoditized segments can erode margins quickly.

The rivalry manifests primarily in negotiations with major customers. When Coca-Cola's supply contract comes up for renewal, both Crown and Ball compete aggressively. The winner secures years of volume; the loser faces capacity utilization challenges.

For investors, the Five Forces analysis suggests a business with structural challenges (buyer power, rivalry) offset by structural advantages (entry barriers, declining substitute threat). This isn't a business that will generate software-like margins, but it can generate attractive returns through operational excellence and disciplined capital allocation.

X. Strategic Advantages: Hamilton's 7 Powers Framework Analysis

1. Scale Economies: STRONG

Crown's 189 plants in 39 countries provide massive manufacturing scale that competitors struggle to match. This scale creates advantages in several dimensions:

Procurement: Crown purchases aluminum in quantities that command attention from global suppliers. Volume discounts and priority allocation during shortages create cost advantages.

R&D Leverage: Research and development costs are spread across enormous production volumes. An innovation that reduces aluminum gauge by 0.1mm benefits billions of cans annually.

Administrative Efficiency: Corporate overhead is spread across massive revenues, reducing SG&A as a percentage of sales.

Scale economies are the foundation of Crown's competitive position and have been since the Connelly era.

2. Network Economics: MODERATE

Crown doesn't benefit from direct network effects in the traditional sense—more customers don't make the product more valuable to other customers.

However, geographic density of plants creates logistics advantages. Crown's network allows it to serve customers across multiple locations from nearby facilities, reducing transportation costs and improving service responsiveness.

The network also creates information advantages. Crown observes beverage trends across dozens of markets, providing insights that inform capacity planning and innovation priorities.

3. Counter-Positioning: HISTORICALLY STRONG

Crown Cork & Seal was an enigma within the container business because it had achieved financial results that contradicted industry logic. Under Connelly, Crown refused to diversify when competitors did—a classic counter-position that paid off.

The counter-positioning power has diminished over time as the industry consolidated and strategies converged. But the historical counter-positioning demonstrates management's willingness to deviate from consensus when the analysis supports it.

4. Switching Costs: MODERATE-HIGH

Several factors create switching costs for Crown's customers:

Co-located Manufacturing: Crown builds facilities near major customer filling operations. If a customer switches suppliers, they may need to accept higher transportation costs or wait for a new supplier to build nearby capacity.

Technical Integration: Can filling lines are optimized for specific can dimensions and specifications. Changing suppliers requires recalibration and testing.

Qualification Processes: Beverage companies require extensive qualification testing before approving new suppliers. The time and expense of qualification discourages switching.

Long-term Supply Agreements: Multi-year contracts lock in relationships and provide switching barriers during the contract term.

These switching costs don't prevent switching entirely—major customers have sufficient leverage to demand competitive terms. But they create friction that benefits incumbents.

5. Branding: WEAK

As a B2B business, Crown has limited consumer awareness. Crown Holdings' current tagline is "Packaging that protects your brand and our world"—but few consumers have heard it or would recognize the company name.

Brand value lies in reliability and quality reputation among industrial customers. Procurement managers at beverage companies know Crown's track record. But this is reputation rather than brand in the consumer sense.

The weak branding is inherent to the business model. Crown's job is to make someone else's brand look good—not to build its own consumer franchise.

6. Cornered Resource: LIMITED

Crown has no proprietary access to aluminum or steel. The raw materials are globally traded commodities available to any competitor.

However, patents on specific can designs and technologies provide some protection. More importantly, geographic facility locations near key customers are hard to replicate. When Crown has the only can plant within economical shipping distance of a major filling facility, that location is effectively a cornered resource.

7. Process Power: STRONG

Process power—the accumulated organizational learning that creates cost or quality advantages—is arguably Crown's strongest competitive moat.

Early focus on innovation traces back to William Painter's invention of the bottle cap and the crowning machine. This heritage established a culture of continuous improvement that persists today.

Crown's expertise in lightweighting cans—reducing aluminum content while maintaining structural integrity—has been refined over decades. Each generation of cans is lighter than the last, saving aluminum costs while maintaining performance.

High-speed manufacturing capabilities allow Crown's plants to produce millions of cans daily with minimal waste and downtime. This operational excellence is embedded in equipment, training, and organizational culture—it can't be easily copied by a new entrant.

For investors, the 7 Powers analysis reveals a company with strong scale and process advantages, moderate switching costs and network benefits, and limited branding and cornered resource powers. This is a defensible but not impregnable position—consistent with a mature industrial business.

XI. Bull and Bear Cases

The Bull Case

Sustainability Tailwind Is Structural: The shift from plastic to aluminum isn't a fad—it's driven by fundamental recycling economics, regulatory pressure, and consumer preferences. As plastic becomes increasingly stigmatized, aluminum's market share gains will accelerate. Crown is positioned to capture this growth across its global footprint.

Operational Excellence Drives Margin Expansion: Crown has decades of accumulated process knowledge. Continued lightweighting, energy efficiency improvements, and automation can expand margins even in a mature market. Management's track record since the 2000s restructuring demonstrates discipline.

Free Cash Flow Generation Supports Returns: The Signode acquisition enhanced Crown's cash conversion. Combined with beverage can stability, the company generates substantial free cash flow that can fund dividends, buybacks, or strategic acquisitions.

Emerging Market Growth: While developed markets are mature, emerging markets in Asia, Africa, and Latin America offer growth as per-capita beverage consumption increases and infrastructure improves. Crown's existing presence positions it to capture this growth.

Underappreciated Sustainability Credentials: Crown's Twentyby30 program and progress toward emissions reduction aren't fully reflected in valuation. As ESG investing becomes mainstream, companies with genuine sustainability stories may receive premium multiples.

The Bear Case

Customer Concentration Risk: Dependence on a handful of global beverage companies creates vulnerability. If a major customer relationship deteriorates, revenue and earnings could be significantly impacted.

Commodity Input Exposure: Aluminum prices are volatile and largely beyond Crown's control. Extended periods of high aluminum prices compress margins, as customers resist pass-through pricing.

Industry Rivalry Intensifies: Competition with Ball Corporation is already intense. Price wars, aggressive capacity additions, or irrational competitor behavior could erode profitability industry-wide.

Technology Disruption: While unlikely in the near term, breakthrough materials or packaging technologies could eventually challenge aluminum's position. New biodegradable materials or radically improved plastic recycling could reduce aluminum's sustainability advantage.

Execution Risk on Growth Investments: Crown is investing in capacity expansion to meet sustainability-driven demand. If demand growth disappoints or expansion projects encounter delays, returns on these investments could underwhelm.

Economic Sensitivity: Beverage consumption correlates with economic conditions. A severe recession could reduce demand for discretionary beverages, impacting Crown's volumes.

Competitive Landscape Summary

Crown competes in a oligopolistic market where the primary rival is Ball Corporation. Both companies have global scale, strong customer relationships, and operational excellence. Competition primarily manifests in contract negotiations rather than public price wars.

Other competitors like Ardagh, Canpack, and regional players provide alternatives for customers but lack the global footprint and scale of Crown and Ball. The duopoly structure provides some pricing discipline, though customer concentration limits pricing power.

XII. Key Performance Indicators for Investors

For long-term investors tracking Crown Holdings, three metrics deserve particular attention:

1. Beverage Can Volume Growth

This is the most important indicator of Crown's core business health. Volume growth reflects both market share dynamics and overall category growth driven by the sustainability shift from plastic to aluminum.

Watch for: Year-over-year volume changes by segment, new customer wins, and commentary on capacity utilization. Consistent mid-single-digit volume growth would validate the sustainability thesis. Flat or declining volumes would suggest the tailwind is weaker than expected.

2. EBITDA Margin

In a capital-intensive, commodity-input business, margins reveal operational execution and pricing discipline. Crown's ability to maintain or expand EBITDA margins despite input cost volatility demonstrates competitive positioning.

Watch for: Segment-level margin trends, commentary on aluminum cost pass-through, and productivity initiative benefits. Margin compression would signal either competitive pressures or operational challenges.

3. Free Cash Flow Conversion

Crown's investment thesis partly depends on generating substantial free cash flow from its mature businesses. FCF conversion (free cash flow as a percentage of net income or EBITDA) measures capital efficiency and sustainability of shareholder returns.

Watch for: Capital expenditure levels relative to depreciation, working capital trends, and management's capital allocation priorities. Strong FCF conversion supports ongoing dividends and opportunistic buybacks.

XIII. Risks and Regulatory Considerations

Legal and Regulatory Overhangs

Crown operates in a heavily regulated environment across 39 countries. Key regulatory considerations include:

Environmental Compliance: Manufacturing operations are subject to environmental permits and regulations. Violations could result in fines, operational disruptions, or remediation costs.

Food Safety Standards: Packaging that contacts food and beverages must meet strict safety standards. Quality failures could damage customer relationships and create liability exposure.

Antitrust Scrutiny: As one of two dominant global beverage can producers, Crown faces potential antitrust oversight. Any perception of anti-competitive behavior could invite regulatory action.

Trade Policy: International operations expose Crown to tariffs, trade restrictions, and geopolitical tensions. Changes in trade policy could affect the economics of certain markets or supply chains.

Accounting Considerations

Goodwill Impairment Risk: Crown's balance sheet carries substantial goodwill from acquisitions, particularly CarnaudMetalbox and Signode. Economic deterioration or strategic setbacks could require write-downs.

Pension Obligations: Legacy defined benefit pension plans create long-term obligations that depend on actuarial assumptions. Changes in discount rates or investment returns affect funded status.

Currency Translation: With the majority of operations outside the U.S., currency fluctuations significantly affect reported results. Investors should distinguish between operational performance and currency translation effects.

XIV. Conclusion: What Crown Holdings Reveals About Industrial Capitalism

The Crown Holdings story is, in many ways, the story of American industrial capitalism itself—compressed into 133 years of invention, crisis, consolidation, and reinvention.

William Painter's crown cork solved a genuine problem and created a business model that inspired Gillette. The company survived Prohibition by pivoting to soft drinks. John Connelly's turnaround demonstrated that disciplined focus could outperform diversified conglomerates. William Avery's acquisition spree built global scale but also nearly broke the company. The restructuring of the 2000s proved that corporate redemption is possible. And now, the sustainability mega-trend provides a tailwind that few could have predicted a decade ago.

What can investors take away from this journey?

First, "boring" industries can produce extraordinary returns. Crown isn't a technology platform or a viral consumer brand. It makes metal containers. But consistent execution in an essential category, combined with disciplined capital allocation, has generated substantial long-term value.

Second, strategic flexibility matters. Crown has reinvented itself multiple times—from bottle caps to cans, from domestic to global, from diversified to focused. The willingness to change strategy when circumstances demand it has been essential to survival.

Third, sustainability is real. The shift toward aluminum packaging isn't corporate marketing—it's grounded in recycling economics and consumer behavior. Companies positioned on the right side of this trend have structural advantages over those that aren't.

Fourth, execution trumps strategy in mature industries. Crown and Ball pursue similar strategies. The difference in outcomes will largely be determined by operational excellence—who runs the best plants, manages costs most effectively, and serves customers most reliably.

Crown Holdings at 133 years old is not a growth stock in the traditional sense. But for investors seeking exposure to packaging sustainability trends, global consumer staples demand, and consistent cash flow generation, it represents a well-positioned industrial franchise with a remarkable history and defensible competitive position.

The bottle cap that William Painter invented in 1891 has evolved beyond recognition. But the company he founded with $200 continues to seal the world's beverages—and to adapt to whatever challenges the next 133 years may bring.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube