Blackstone: The Rise of Alternative Asset Management's Trillion-Dollar Empire

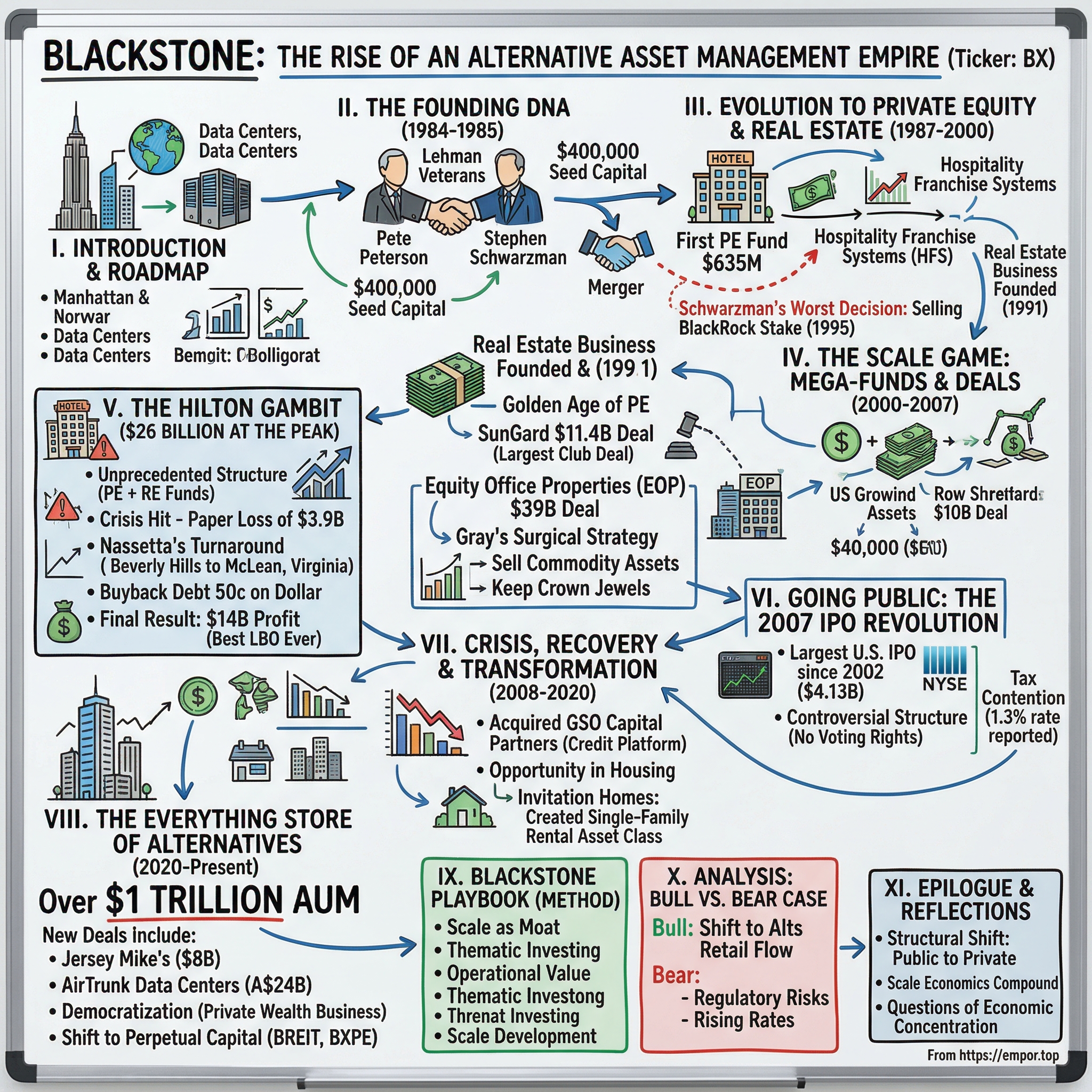

I. Introduction & Episode Roadmap

Picture this: It's a Tuesday morning in Manhattan, and inside a gleaming Park Avenue tower, a team is simultaneously closing a $24 billion data center deal in Australia, restructuring a European logistics portfolio worth $15 billion, and deploying fresh capital into American suburban rental homes. The firm orchestrating this financial symphony manages more money than the GDP of most countries—over $1 trillion in assets. This is Blackstone Group, and its scale defies comprehension.

How did two Lehman Brothers refugees with $400,000 in startup capital build what would become the defining institution of modern finance? The answer isn't just about lucky timing or financial engineering. It's about recognizing that the entire architecture of capitalism was shifting—from public to private, from trading to ownership, from quarterly earnings to decade-long value creation.

Today's story traces an arc from a two-man M&A boutique in 1985 to the everything store of alternative investments. We'll explore how Pete Peterson and Stephen Schwarzman didn't just ride the private equity wave—they helped create it. We'll dissect the deals that defined eras: the audacious Hilton gambit at the market peak, the contrarian real estate bets during the financial crisis, and the recent push to democratize alternatives for everyday investors.

This isn't just a corporate biography. It's a window into how power and capital flow in the 21st century, where a single firm can own everything from your local Bumble Bee tuna brand to the data centers powering your Netflix stream. Along the way, we'll decode the Blackstone playbook: why scale became their moat, how they turned cyclical deal-making into recurring fee streams, and what their trajectory reveals about where capitalism itself is heading.

II. The Founding DNA: Peterson, Schwarzman & Lehman's Legacy

The year was 1984, and inside Lehman Brothers' wood-paneled boardroom, the air crackled with tension. Pete Peterson, the firm's chairman and a former U.S. Secretary of Commerce, sat across from his protégé Stephen Schwarzman, the 37-year-old head of global M&A who had just orchestrated some of Wall Street's splashiest deals. Both men sensed what was coming—Lehman was fracturing, torn between its trading desks and banking divisions. By spring, American Express would sell the firm to Shearson, and Peterson and Schwarzman would find themselves with golden parachutes but no platform.

"We should start something together," Schwarzman proposed over lunch at the Four Seasons. Peterson, then 58, had already conquered Washington and Wall Street. But Schwarzman painted a different vision: not another investment bank churning out deal fees, but something more permanent, more powerful. They would advise on deals, yes, but also invest their own capital—becoming principals, not just agents. The partnership crystallized in 1985 with just $400,000 in seed capital—Peterson and Schwarzman each contributing $200,000. The firm's name itself was a linguistic merger: "Schwarz" meaning black in German, "petros" meaning stone in Greek, creating Blackstone. It was more than clever wordplay; it symbolized the fusion of two formidable minds.

Originally formed as a mergers and acquisitions advisory boutique, their timing was exquisite. The mid-1980s were witnessing the dawn of the leveraged buyout era, with Michael Milken's junk bonds providing rocket fuel for corporate raiders. But Peterson and Schwarzman saw beyond the frenzy. They envisioned building something permanent in a world of transactions.

Their first major hire signaled serious intent: Roger Altman, another Lehman veteran and managing director, joined in 1987. The trio represented deep Wall Street credibility—Peterson with his government pedigree, Schwarzman with his deal-making prowess, and Altman with his banking relationships. Their first significant advisory assignment, the 1987 merger of E.F. Hutton and Shearson Lehman Brothers, netted a $3.5 million fee—validation that they could compete with the bulge bracket firms.

But here's what separated Blackstone from every other startup boutique: From the outset in 1985, Schwarzman and Peterson planned to enter the private equity business but had difficulty raising their first fund because neither had ever led a leveraged buyout. This obstacle would have deterred most. Instead, they spent two years building credibility through advisory work, studying every LBO, learning the mechanics, and cultivating relationships with potential limited partners.

Schwarzman brought a particular intensity to the enterprise. Colleagues described him as someone who processed information at superhuman speed, who could see three moves ahead in any negotiation. Peterson, meanwhile, provided gravitas and connections—his Rolodex included CEOs, senators, and sovereign wealth fund chiefs. Together, they embodied a paradox: establishment credentials with insurgent ambitions.

The culture they established from day one would define Blackstone for decades: perfectionism bordering on obsession, a zero-tolerance policy for mediocrity, and a belief that every deal should be a reference point for excellence. They didn't just want to participate in the buyout boom—they intended to redefine it.

III. Evolution into Private Equity & Real Estate (1987–2000)

The transformation from advisory boutique to principal investor began with a revelation. In late 1987, as Blackstone closed its first private equity fund with $635 million in commitments—remarkable for a firm with no buyout track record—Schwarzman noticed something peculiar. The advisory fees, while lucrative, paled compared to the carry that KKR and Forstmann Little were earning on their funds. "We were selling advice for thousands while they were making millions on ownership," he later reflected. The real breakthrough came in 1991 with an unexpected architect: Henry Silverman, who accepted a position as partner at Blackstone Group and would leave in 1991 to head Hospitality Franchise Systems, an investment of Blackstone's that he had overseen. Silverman was a dealmaker's dealmaker—a Brooklyn-born entrepreneur who had previously built and sold Days Inn for $585 million. At Blackstone, he saw opportunity where others saw distress.

While at Blackstone, Silverman created Hospitality Franchise Systems (HFS) which would acquire hotel franchises including Ramada and Howard Johnson's, as well as Days Inn for $290 million (almost half what he had sold it for) after bankruptcy in 1991, and picked up Days Inns of America in 1991 for $250 million. The genius wasn't just in buying distressed assets—it was recognizing that hotel franchising, not ownership, was the scalable model. HFS picked up Super 8 Motels for $125 million in 1993.

This hotel franchise play taught Blackstone a crucial lesson: Real estate wasn't just about trophy properties—it was about cash flows, operational excellence, and seeing value where others saw decay. Blackstone's real estate business was founded in 1991 and has grown significantly, with the firm investing in real estate since 1991.

Meanwhile, the private equity side was gaining momentum. Blackstone made notable investments in the early and mid-1990s, including Great Lakes Dredge and Dock Company (1991), Six Flags (1991), US Radio (1994), Centerplate (1995), MEGA Brands (1996). Each deal refined their playbook: find companies with stable cash flows, improve operations, use leverage judiciously.

But the defining moment of this era was actually a mistake—one that would haunt Schwarzman for decades. In 1987, Blackstone had partnered with Larry Fink and Ralph Schlosstein to create BlackRock, initially a fixed-income investment subsidiary. By 1995, as BlackRock's assets ballooned, Blackstone made what seemed like a prudent decision: sell its stake in BlackRock to PNC Financial Services for $250 million. Schwarzman later described the selling of BlackRock as his worst business decision ever. Between 1995 and 2014, PNC reported $12 billion in pretax revenues and capital gains from BlackRock. Today, BlackRock manages over $10 trillion—ten times Blackstone's AUM.

The late 1990s marked acceleration. In 1998, Blackstone sold a 7% interest in its management company to AIG, valuing Blackstone at $2.1 billion. In 1997, Blackstone completed fundraising for its third private equity fund, with approximately $4 billion of investor commitments and a $1.1-billion real estate investment fund. The firm was no longer a boutique—it was becoming an institution.

IV. The Scale Game: Mega-Funds & Mega-Deals (2000–2007)

The millennium opened with Schwarzman sensing an inflection point. Cheap debt was flooding the market, pension funds were desperate for yield, and corporate America was ripe for restructuring. "We're entering the golden age of private equity," he declared at Blackstone's 2003 annual meeting. The next four years would prove him prophetic—and nearly catastrophic.

The 2005 SunGard deal announced their arrival on the mega-deal stage. A consortium organized by Silver Lake Partners that included Blackstone acquired SunGard Data Systems for $11.4 billion in cash—the second largest leveraged buyout ever completed at that time, surpassed only by RJR Nabisco. Blackstone partnered with Silver Lake Partners, Bain Capital, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts, Providence Equity Partners, and TPG Capital in what became the largest club deal completed to that point.

The SunGard transaction revealed Blackstone's evolution. No longer content with mid-market deals, they were now orchestrating symphonies of debt and equity that required multiple private equity giants to collaborate. The consortium invested $3.5 billion in equity, with leverage representing 7.4x EBITDA—aggressive but not reckless by the standards of 2005.

On the real estate front, Blackstone was methodically building a hospitality empire. Blackstone acquired Prime Hospitality and Extended Stay America in 2004, followed by the acquisition of La Quinta Inns & Suites in 2005. These weren't glamorous trophy properties—they were cash-flowing, recession-resistant assets in the budget and mid-market segments. The strategy reflected a core Blackstone principle: predictable cash flows beat prestige every time. Then came the deal that would define the era: the Equity Office Properties (EOP) bidding war. In November 2006, Blackstone announced it would acquire Sam Zell's EOP for $36 billion. What followed was a masterclass in deal-making under pressure. Vornado Realty Trust, headed by Steve Roth, entered with a competing bid, triggering a three-month bidding war. Following negotiations and a bidding war with Vornado Realty Trust, Blackstone upped their original offer of $47.50 to $55.50 per share for a total amount of $38.7 billion.

The EOP victory in February 2007—at $39 billion (including debt)—wasn't just about size. It was about vision. Jonathan Gray, then a 36-year-old Blackstone partner who orchestrated the deal, saw what others missed: many of EOP's assets in Los Angeles, San Francisco, Boston, and New York City were irreplaceable, trophy properties which would attain high prices if sold to local REITs, pension funds and sovereign funds who had long been eyeing some of EOP's individual buildings.

Gray's strategy was surgical. Even before closing, Blackstone had lined up buyers for portions of the portfolio. By the end of 2007, it had sold $27B of assets across the country to multiple buyers, equating to 70% of the portfolio. This wasn't panic selling—it was risk management at its finest. They kept the crown jewels and sold the commodity assets at peak prices.

During the buyout boom of 2006 and 2007, Blackstone completed some of the largest leveraged buyouts. The firm was writing bigger checks, taking bigger swings, and fundamentally reshaping what private equity could be. They weren't just financial engineers anymore—they were becoming operational experts, real estate magnates, and masters of timing.

V. The Hilton Gambit: $26 Billion at the Peak

The scene was the Waldorf Astoria ballroom in July 2007, where Hilton's board gathered for what they thought would be a routine strategy session. Instead, Jonathan Gray and Michael Chae from Blackstone presented an offer that left directors speechless: $47.50 per share in cash, representing a premium of 40% over yesterday's closing stock price. The $26 billion deal would become Blackstone's defining moment—both its greatest triumph and its closest brush with disaster.

The transaction structure was unprecedented: Blackstone's real estate and corporate private equity funds collaborated on the acquisition of Hilton, demonstrating Blackstone's unique ability to undertake such a transaction. This wasn't just one fund stretching—it was the entire firm mobilizing for a single bet. The financing was equally audacious: $5.6 billion in equity and $20.5 billion in debt from 26 different lenders, with Bear Stearns leading the syndicate. The timing couldn't have been worse. Weeks after the July 3, 2007 announcement, the economy started to spasm. By the time the deal closed in October, Bear Stearns—the lead bank on the financing—was wobbling. A year later, it would collapse entirely. Gray had built the real estate group into Blackstone's biggest and most profitable division, but now his signature deal threatened to destroy his reputation.

The crisis hit Hilton like a tsunami. By 2009, actual EBITDA came in at half of what projections had assumed. Revenue fell by 15% and the equity value held by Blackstone fell by a full 70%—a paper loss of $3.9 billion. Media headlines branded Hilton as Blackstone's "black eye." The hospitality giant was ripe for a makeover—by 2007, Hilton was an also-ran in the hotel industry, profitable but a shadow of its 1950s and 1960s heyday when its brand was as recognizable as Coca-Cola.

Enter Christopher Nassetta. Gray had worked with Nassetta at Host Hotels & Resorts and saw in him the operational savior Hilton needed. As Nassetta took the helm in October 2007, he found a company that was "broken"—fragmented silos, misalignment, a Balkanized collective of regions and hotels with no central accountability. The company was headquartered in Beverly Hills, where a milieu of lassitude pervaded the top brass.

Nassetta's turnaround began with radical surgery. He moved Hilton's headquarters from Beverly Hills to McLean, Virginia—a decision that saw 80% personnel turnover. "We became complacent. We got so far ahead in the 1960s and 1970s that we started thinking there is no competition," Nassetta reflected. His mission: transform Hilton from an asset-heavy, operationally scattered company into a lean, franchise-focused global powerhouse.

But the masterstroke came during the darkest hour. At the height of the financial crisis, when Hilton's debt traded at deep discounts, Blackstone did something extraordinary: they found more than $800 million of new money, which they used not to invest in Hilton directly, but to buy back debt from bond investors at 50 cents on the dollar. This wasn't just financial engineering—it was battlefield surgery performed under fire.

The restructuring allowed Blackstone to maintain control when standard practice would have seen equity wiped out. By 2010, as the economy stabilized, Hilton began its ascent. Nassetta's operational improvements—shifting to an asset-light franchise model, improving technology, expanding internationally—started bearing fruit. "Chris maintained his equanimity throughout the tough days of 2008-2009," Gray noted. "There were stressful moments, but Chris was rock solid."

The vindication came in December 2013 when Blackstone took Hilton public at a valuation $7 billion higher than the acquisition price. The IPO raised $2.35 billion—at the time, the largest hotel company IPO ever. Blackstone's 76 percent ownership stake was worth about $16 billion, resulting in a paper profit of more than $9.5 billion.

By 2018, when Blackstone fully exited, they had generated an estimated $14 billion profit from the acquisition, tripling their initial $5.6 billion equity investment. Bloomberg labeled it "the best leveraged buyout ever." The deal that should have killed Blackstone had instead become their crowning achievement—proof that in private equity, operational excellence and crisis management matter as much as financial engineering.

VI. Going Public: The 2007 IPO Revolution

The morning of June 21, 2007, marked a watershed moment not just for Blackstone but for American capitalism itself. As Stephen Schwarzman rang the opening bell at the New York Stock Exchange, novelist Tom Wolfe, observing from the gallery, reportedly quipped to a companion: "This is the end of capitalism as we know it." He was witnessing the transformation of private equity from shadowy dealmaker to public spectacle.

On June 21, 2007, Blackstone became a public company via an initial public offering, selling a 12.3% stake in the company for $4.13 billion, in the largest U.S. IPO since 2002. The shares, priced at the top of their range at $31, immediately surged, closing the first day up 13% at $35.06. The market had spoken: investors wanted in on the private equity gold rush.

The personal windfall was staggering. Schwarzman, the firm's CEO and largest shareholder, sold shares worth almost $700 million. He retains 24 percent of the total stock, worth about $8.8 billion at the trading price. Peterson, at 81 and preparing for retirement, sold most of his shares in the IPO, collecting $1.8 billion in a single day.

But the IPO represented more than personal enrichment—it was a philosophical statement. Private equity, which had made fortunes taking companies private, was itself going public. The irony wasn't lost on observers. As one Wall Street veteran noted, "They're selling transparency while their business model depends on opacity."

The structure Blackstone chose was revolutionary and controversial. They created a publicly traded partnership that gave shareholders economic interest but virtually no voting rights. The founding partners retained absolute control while accessing permanent capital from public markets. It was financial engineering at its most audacious—having your cake and eating it too.

Almost immediately, the IPO triggered a political firestorm. The New York Times reported that Blackstone earned $1.1 billion in operating income in the first quarter of 2007 and paid only $14 million in taxes, about 1.3 percent. The revelation that private equity titans paid lower tax rates than their secretaries—15% capital gains versus 35% corporate rates—sparked congressional hearings and proposed legislation.

The timing, in retrospect, was either brilliant or catastrophically lucky. Blackstone went public at the absolute peak of the credit bubble, extracting maximum value before the crash. Within months, credit markets would freeze, and the IPO window would slam shut for years. The Blackstone offering would be the last of its scale until well after the financial crisis.

Yet the IPO also marked a transformation in Blackstone's business model. Public company status brought quarterly earnings calls, regulatory scrutiny, and pressure for consistent growth. The firm responded by diversifying beyond traditional buyouts into credit, real estate, hedge funds, and eventually retail products. The IPO proceeds didn't fund expansion—they went directly to founders' pockets—but public company discipline forced Blackstone to become more than a buyout shop.

Perhaps most significantly, the IPO created currency—publicly traded stock—that Blackstone could use for acquisitions and talent retention. It marked the beginning of Blackstone's evolution from partnership to institution, from dealmakers to asset managers. The firm that had started with $400,000 was now worth over $30 billion, and this was just the beginning.

VII. Crisis, Recovery & Transformation (2008–2020)

The Lehman Brothers collapse on September 15, 2008, should have been Blackstone's death knell. Their stock, which had debuted at $31 just 15 months earlier, cratered to $3.55 by February 2009. The firm that had epitomized the leveraged buyout boom now faced existential questions about its survival. Yet what followed wasn't collapse but calculated transformation.

The first strategic move came even before Lehman fell. In March 2008, Blackstone acquired GSO Capital Partners, a credit-oriented alternative asset manager, for $620 million in cash and stock and up to $310 million through an earnout over the next five years. The combined entity created one of the largest credit platforms in the alternative asset management business, with over $21 billion under management. Schwarzman's timing was prescient: "Given the current dislocation in the credit markets, this is an ideal time to create a more powerful, diversified platform."

During the 2008 financial crisis, Blackstone closed only a few transactions—but the ones they did were strategic. In January 2008, they made a small co-investment in Harrah's Entertainment. Other notable investments included AlliedBarton, Performance Food Group, Apria Healthcare, and CMS Computers. These weren't headline-grabbing mega-deals but carefully selected, recession-resistant businesses with stable cash flows. The real genius move came in housing. While others saw disaster in the foreclosure crisis, Blackstone saw opportunity. In 2012, with home prices remaining near bottomed-out levels, Blackstone founded Invitation Homes with the intention of acquiring tens of thousands of single family homes. Between 2012 and 2016, Blackstone acquired almost 50,000 single family homes in thirteen markets for purchase prices totaling $8.3 billion—at times spending over $150 million a week.

This wasn't bottom-feeding—it was institutional-scale transformation of an asset class. Blackstone created a vertically-integrated company with in-house capabilities of acquiring, renovating, leasing, maintaining, and managing single family homes. They spent $10 billion acquiring homes and another $2 billion fixing them up, turning vacant, distressed properties into rental homes for families.

The financial engineering was as impressive as the operational execution. In November 2013, Invitation Homes pioneered a new form of securitized financing for residential rental homes—essentially creating residential mortgage-backed securities backed by rental income rather than homeowner mortgages. This innovation reduced borrowing costs and created a new asset class for institutional investors.

The vindication came in 2017 when Blackstone took Invitation Homes public, raising $1.5 billion. By 2019, when Blackstone fully exited, they had made about $7 billion from the investment—transforming what critics called disaster capitalism into institutional-quality rental housing.

Meanwhile, the credit platform acquired through GSO was bearing fruit. When Blackstone first acquired GSO in 2008, the group had $9.6 billion in assets under management and fewer than 150 employees. As part of Blackstone, it became one of the world's largest credit-oriented asset managers, with $135 billion in AUM by 2020 and a 350+ person team.

The transformation wasn't just about new business lines—it was about changing Blackstone's DNA. The firm evolved from a cyclical, deal-dependent private equity shop into a diversified alternative asset manager with multiple revenue streams. Fee-related earnings, which provided stable income regardless of market conditions, became increasingly important. The firm launched perpetual capital vehicles like BREIT (Blackstone Real Estate Income Trust) that didn't have the J-curve dynamics of traditional private equity funds.

By 2020, Blackstone had emerged from the crisis stronger than ever. They had turned defensive moves during the downturn into offensive platforms for growth. The firm that had started with $400,000 now managed over $500 billion. But this was just the prelude to their next act.

VIII. The Everything Store of Alternatives (2020–Present)

The July 2023 announcement was vintage Schwarzman understatement: "Blackstone is the first alternative manager to surpass $1 trillion of assets under management." The milestone, reached three years ahead of internal projections, marked not an endpoint but an inflection point. As of May 2024, Blackstone has more than $1 trillion in total assets under management, making it the world's largest alternative investment firm.

The scale is staggering. The company owns 12,500+ real estate assets and 250+ portfolio companies. But the recent acceleration has been breathtaking. Blackstone deployed $134 billion in 2024, an 81% annual increase, while its AUM reached $1.13 trillion by Q4's end. The recent mega-deals showcase Blackstone's evolution into what Schwarzman calls "the everything store of alternatives." On November 19, 2024, Jersey Mike's Subs announced that Blackstone would acquire a majority ownership position in a deal valued at approximately $8 billion including debt. The sandwich chain founder Peter Cancro will maintain a significant equity stake and continue to lead the business—a classic Blackstone playbook of partnering with successful founders.

In September 2024, Blackstone entered into a definitive agreement to acquire AirTrunk, a leading data center platform in the Asia-Pacific region, for an enterprise value of over A$24 billion—one of the largest infrastructure deals in history. This represents Blackstone's conviction that data centers are the new railroads, essential infrastructure for the AI revolution.

The transformation isn't just about size—it's about democratization. About a quarter of their total AUM ($240 billion) now comes from individual investors via their private wealth business. Blackstone's head of private wealth Joan Solotar predicted in 2018 that retail investors would make up half of the firm's AUM in five to 10 years—a prediction increasingly looking prescient.

The business lines now span the entire alternatives universe: private equity, real estate, credit, infrastructure, hedge funds, secondaries, growth equity, and insurance solutions. Each vertical operates with scale that would make it a major firm on its own. The credit business alone manages $135 billion. Real estate controls over $300 billion in assets.

But perhaps the most significant evolution is the shift to perpetual capital. Vehicles like BREIT (Blackstone Real Estate Income Trust) and BXPE (Blackstone Private Equity Strategies) don't have the traditional private equity J-curve or fixed fund life. They provide permanent capital that can be deployed opportunistically without the pressure of fundraising cycles or forced exits.

The operational sophistication has evolved dramatically. Blackstone portfolio companies now benefit from what they call "portfolio operations"—shared services in procurement, technology, talent management, and ESG. A Blackstone-owned company can tap into purchasing power across hundreds of portfolio companies, accessing economies of scale previously available only to the largest corporations.

Leadership transition planning is also underway. Jonathan Gray, now President and COO, is widely seen as Schwarzman's successor. Gray, who orchestrated both the EOP and Hilton deals, represents the next generation—still hungry, still paranoid, but now operating with resources that dwarf most sovereign wealth funds.

IX. Playbook: The Blackstone Method

After four decades and over $1 trillion deployed, the Blackstone playbook has crystallized into a replicable, scalable system that transcends any single deal or fund. It's not just about financial engineering—it's about building institutional advantages that compound over time.

Scale as Competitive Advantage: Only a handful of firms globally can write $20+ billion checks. This isn't just about having capital—it's about having the operational infrastructure, risk management systems, and portfolio company expertise to deploy it effectively. When Blackstone enters a bidding process for a mega-deal, sellers know they can close with certainty. This reputation for execution often allows them to win deals without being the highest bidder.

The "One-Firm" Culture: Unlike many competitors organized as federations of independent businesses, Blackstone operates as a single organism. Real estate principals sit on private equity deal committees. Credit teams source opportunities for the buyout funds. This cross-pollination creates information advantages—patterns spotted in real estate might inform private equity strategy, credit market dislocations might signal buyout opportunities.

Thematic Investing: Blackstone doesn't just react to deals—they develop multi-year investment themes and systematically pursue them. The single-family rental strategy wasn't opportunistic—it was a calculated bet on demographic shifts, homeownership trends, and the institutionalization of residential real estate. Current themes include logistics (e-commerce driving warehouse demand), data centers (AI computing needs), life sciences (aging demographics), and energy transition (infrastructure transformation).

Operational Value Creation vs Financial Engineering: While early private equity relied heavily on leverage, Blackstone's playbook now emphasizes operational transformation. Portfolio companies get access to Blackstone's portfolio operations team—experts in procurement, digital transformation, talent management, and international expansion. The firm claims operational improvements drive 70% of value creation, with financial engineering contributing just 30%.

Long-term Aligned Incentives: Partners typically have significant personal capital invested alongside limited partners. Carried interest vests over years, aligning managers with long-term performance rather than quick flips. The firm has never had a flagship fund lose money—a track record that creates enormous fundraising advantages.

Building Permanent Capital: Traditional private equity's weakness is the fundraising cycle—returns depend partly on when you're forced to exit. Blackstone's perpetual vehicles solve this. BREIT can hold properties indefinitely, selling only when optimal. This patient capital approach has generated superior returns by avoiding forced sales during downturns.

Network Effects: With 250+ portfolio companies employing millions, Blackstone has visibility into real-time economic trends that no government statistics can match. When their restaurant chains see traffic patterns shift, their real estate team knows mall valuations might change. When their logistics companies report capacity constraints, the infrastructure team sees opportunity. This information advantage compounds with scale.

The playbook also includes what Blackstone doesn't do. They rarely engage in hostile takeovers. They avoid turnarounds requiring fundamental business model changes. They don't chase fads—no SPACs during the SPAC boom, minimal crypto exposure despite pressure. This discipline, choosing what not to do, may be their greatest strength.

X. Analysis & Bear vs. Bull Case

Bull Case:

The secular shift toward alternatives represents a multi-trillion-dollar opportunity. Institutional investors currently allocate about 25% to alternatives, but many are targeting 40-50%. Individual investors, controlling $80 trillion globally, allocate just 1-2% to alternatives. Even modest increases would drive hundreds of billions in new AUM. Blackstone, with its brand, track record, and distribution, is best positioned to capture this flow.

First-mover advantage in retail distribution creates powerful moats. Building the technology, compliance infrastructure, and advisor relationships to serve individual investors takes years and billions in investment. Blackstone's head start, with dedicated teams and products like BREIT and BXPE, will be difficult for competitors to overcome.

The scale advantages are unassailable. In real estate, Blackstone can renovate properties 20-30% cheaper than small landlords due to national vendor contracts. In private equity, they can hire better executives, invest more in digital transformation, and provide strategic advantages smaller firms can't match. These advantages widen with each fund cycle.

Crisis navigation track record suggests durability. Blackstone has thrived through the 1990s recession, dot-com crash, 2008 financial crisis, and COVID—each time emerging stronger. This isn't luck—it's systematic risk management, diversification, and the ability to deploy capital when others are paralyzed.

Fee-related earnings growth reduces cyclicality. As AUM grows and more shifts to perpetual vehicles, management fees become increasingly predictable. This recurring revenue stream, now over $5 billion annually, provides stability even during deal droughts. The business looks increasingly like a high-margin asset management firm rather than a volatile transaction shop.

Bear Case:

Peak private equity valuations threaten future returns. With entry multiples at historic highs and interest rates elevated, the math of private equity becomes challenging. Achieving 20% IRRs when buying at 15x EBITDA requires heroic assumptions about growth and exit multiples. Limited partners may reduce allocations if returns disappoint.

Regulatory scrutiny intensifies globally. The carried interest tax loophole faces bipartisan opposition. SEC oversight of fees, valuations, and conflicts of interest is increasing. European regulators are examining market concentration. Any major regulatory change could significantly impact economics.

Key person risk remains enormous despite planning. Schwarzman, at 77, remains the firm's spiritual leader, largest shareholder, and primary government relationship manager. While Gray is capable, Schwarzman's relationships and reputation took decades to build. The transition, whenever it occurs, will test whether Blackstone is an institution or still dependent on its founder.

Public market correlation is increasing. As private equity strategies become more mainstream and technology enables faster mark-to-market pricing, the diversification benefits of alternatives diminish. During March 2020's COVID selloff, private equity portfolios declined nearly as much as public markets, just with a lag.

Rising interest rates fundamentally challenge the model. Private equity thrived in a declining rate environment from 1982-2022. With rates potentially higher for longer, leverage becomes more expensive, valuations face pressure, and the equity risk premium narrows. The next decade's returns may disappoint investors accustomed to the past four decades' performance.

Competition from new entrants and sovereign wealth funds intensifies. Middle Eastern sovereign funds now compete directly for mega-deals. Tech entrepreneurs are launching new investment firms with different models. Traditional asset managers like BlackRock are building alternatives capabilities. Blackstone's competitive advantages, while significant, face erosion.

XI. Epilogue & Reflections

Standing in Blackstone's lobby at 345 Park Avenue, you're surrounded by the artifacts of modern capitalism—deal tombstones for transactions that reshaped industries, photographs of properties housing millions, the quiet hum of a machine that moves more money daily than many countries' GDP. This is what $400,000 and four decades of compounding ambition built.

The Blackstone story reveals fundamental truths about modern capitalism. First, the shift from public to private markets isn't temporary—it's structural. Public companies, burdened by quarterly earnings pressure and activist shareholders, increasingly can't compete with private equity's patient capital and operational focus. Second, scale economics in finance are more powerful than ever. Information, talent, and capital compound in ways that make the big bigger and the powerful more so.

For entrepreneurs, the lessons are paradoxical. Schwarzman and Peterson started with virtually nothing, proving entrepreneurial success remains possible. Yet they built something that now makes it harder for the next generation to compete. The very existence of Blackstone—able to pay any price, hire any talent, deploy any amount of capital—changes the competitive dynamics for everyone else.

The societal implications demand consideration. Blackstone owns companies employing millions, homes housing hundreds of thousands, infrastructure serving billions. This concentration of ownership in private hands, however efficiently managed, raises questions about economic democracy. When a single firm can influence housing costs in entire cities or employment terms across industries, traditional market dynamics shift.

Can the model survive generational transition? History suggests few financial firms successfully navigate founder succession. Goldman Sachs and JPMorgan managed it by becoming true institutions with cultures transcending individuals. Blackstone, still dominated by Schwarzman's personality and relationships, faces this test imminently.

Is $10 trillion AUM possible? The math suggests yes—if alternatives grow from 10% to 20% of global portfolios, if individual investor adoption accelerates, if new strategies like insurance and infrastructure scale. But trees don't grow to the sky. At some point, Blackstone becomes the market rather than operating within it, and returns normalize to market rates.

The ultimate judgment of Blackstone's legacy won't be its size or returns but its impact on capitalism itself. Did it make markets more efficient or more concentrated? Did it create value or merely extract it? Did it democratize alternatives or institutionalize inequality? These questions don't have clean answers, which perhaps explains why Blackstone remains simultaneously admired and controversial, imitated and investigated, essential and questioned.

What's certain is that Stephen Schwarzman and Pete Peterson didn't just build a firm—they architected a new form of capitalist institution, one that may define how money and power flow for generations. Whether that's triumph or cautionary tale depends on where you stand in the system they helped create. The machine at 345 Park Avenue keeps humming, deals keep closing, capital keeps compounding. The story, far from over, continues to be written with each transaction, each fund raised, each company transformed.

In the end, Blackstone represents both capitalism's greatest triumph—the ability to create immense value from modest beginnings—and its greatest challenge—the concentration of economic power in ever fewer hands. Understanding Blackstone isn't just about understanding one firm; it's about understanding where capitalism itself is heading. And in that sense, we're all stakeholders in the empire that $400,000 built.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube