Booking Holdings: The Accidental Empire That Conquered Travel

I. Cold Open & Episode Thesis

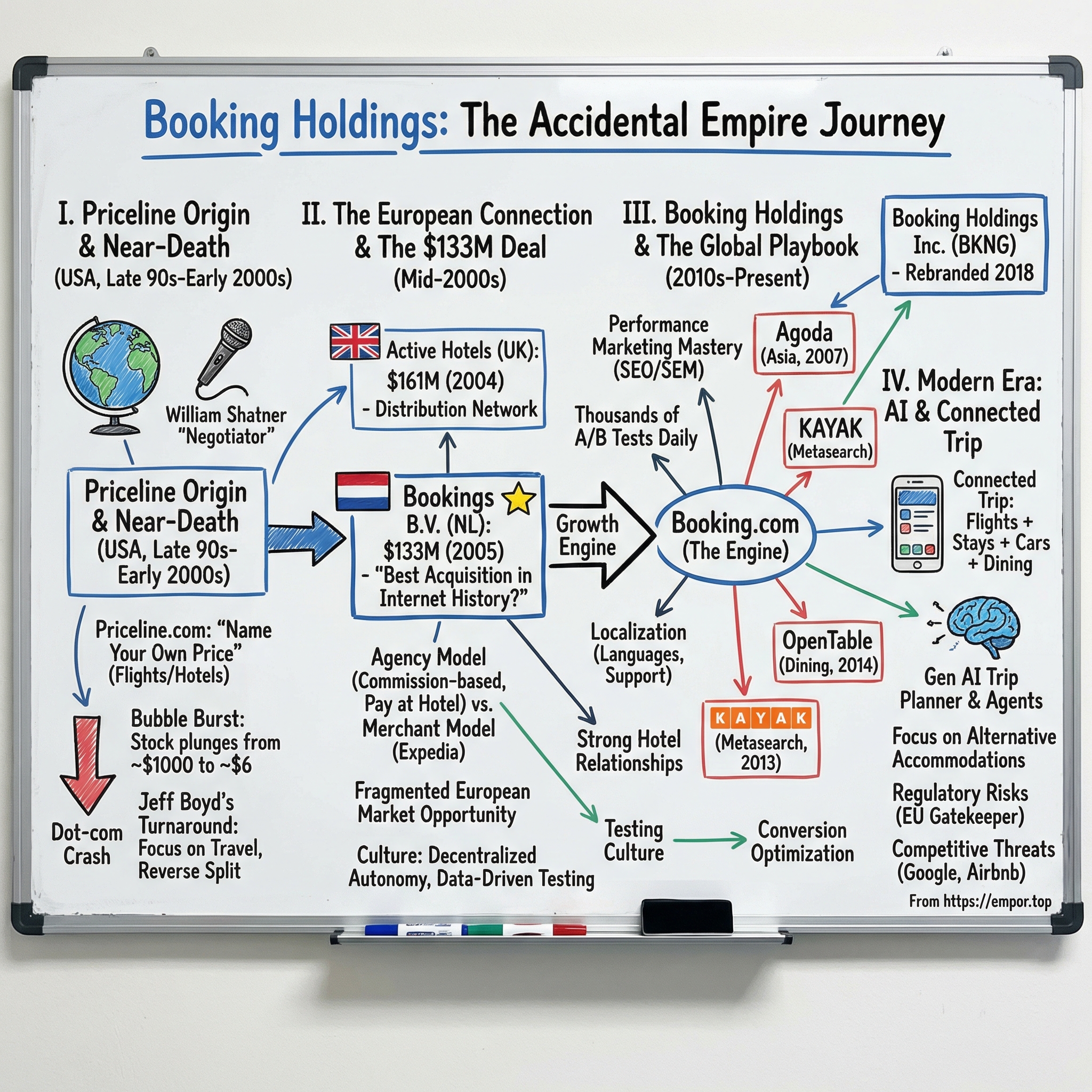

In the summer of 2005, a press release went out from Norwalk, Connecticut, Cambridge, and Amsterdam simultaneously. Priceline.com, the company Americans knew best for William Shatner haggling over hotel rooms on television, had acquired a Dutch startup called Bookings B.V. for approximately $133 million in cash. The deal barely made headlines. Priceline was a dot-com survivor trading at a fraction of its bubble-era peak. Bookings was a modest European hotel reservation service that most Americans had never heard of. It seemed like a footnote in a busy week of tech M&A.

Two decades later, that footnote has been called "the best acquisition in Internet history." It is a claim that deserves serious scrutiny, and by the end of this deep dive, you will understand why it might actually hold up.

Consider the numbers. In 2024, the entity now called Booking Holdings booked over 1.1 billion room nights of accommodation worldwide. It generated $23.7 billion in revenue. In 2025, revenue climbed to $26.9 billion. Its market capitalization, even after a significant pullback in early 2026, sits at roughly $135 billion. The company is ranked 243rd on the Fortune 500. And the engine powering nearly all of this is Booking.com, the little Dutch company that Priceline acquired for the price of a mid-tier Manhattan office building.

But the story of how this happened is far stranger and more instructive than a simple tale of a brilliant acquisition. It is a story about a company that nearly died, a founder who never wanted to be in the hotel business, a deal scout who saw something in Europe that nobody else did, and a management philosophy so counterintuitive that it might be the single most important lesson in the history of internet platform building.

That lesson: sometimes the best thing a parent company can do is get out of the way.

The playbook that built Booking Holdings defied every instinct of American corporate management. Be decentralized, not centralized. Be European, not Silicon Valley. Be commission-based, not merchant-based. Let your acquisition compete with your own brand. Run thousands of A/B tests instead of trusting executive instinct. These were not obvious choices. They were, in many cases, the opposite of what Priceline's larger competitor Expedia was doing at the same time. And they made all the difference.

This is the story of how an accidental empire was built, one counterintuitive decision at a time.

II. The Priceline Origin Story & Near-Death Experience

The late 1990s produced no shortage of grandiose visions for how the internet would remake commerce. But few were as audacious, or as entertainingly bizarre, as the one hatched by Jay S. Walker inside a nondescript office complex in Stamford, Connecticut.

Walker was not a technologist. Born in 1955 in Yonkers, New York, he studied industrial relations at Cornell and had made his first fortune co-founding Synapse, a company that used credit card processing networks to revolutionize the magazine subscription business. By the early 1990s, Synapse had built a customer database of 25 million active buyers, and Walker had developed a deep conviction that the internet could be used to fundamentally restructure how buyers and sellers found each other.

In 1994, Walker founded Walker Digital Corp., hiring computer engineers, cryptographers, and patent lawyers with a singular mission: invent new methods of internet commerce. The company would eventually hold over 750 patents. But one idea captivated Walker above all others. He called it the "demand collection system," a concept so simple it sounded almost naive. What if, instead of sellers setting prices and buyers deciding whether to accept, buyers could name the price they were willing to pay, and sellers could decide whether to accept?

Walker poured $500,000 of his own money into building this idea, and in 1997, Priceline.com was formally incorporated in Norwalk, Connecticut. The product launched in April 1998, initially focused on airline tickets. A customer would name a price for a flight, say $200 round-trip from New York to Los Angeles, and Priceline would shop that bid to airlines with unsold seats. If an airline accepted, the deal was done. The customer got a cheap flight, the airline sold a seat that would have otherwise flown empty, and Priceline took a cut.

The concept needed credibility to gain airline partnerships, so Walker recruited Richard Braddock, the former president of Citicorp, as CEO. Braddock's Rolodex and reputation helped convince Delta to sign on as the first major airline partner.

But the real masterstroke was the marketing. Unable to pay a celebrity spokesperson in cash, Priceline offered William Shatner 125,000 shares of stock instead. The former Captain Kirk accepted, and what followed was one of the most memorable advertising campaigns in American business history.

The early Shatner ads featured the actor performing spoken-word renditions of popular songs, echoing his famously eccentric 1968 album "The Transformed Man." They were absurd, self-aware, and impossible to ignore. Shatner's character eventually evolved into "The Priceline Negotiator," a leather-jacketed action hero who would burst through walls, rappel from helicopters, and parachute into scenes to save consumers from overpaying for travel. In a particularly memorable 2012 spot, the Negotiator was dramatically "killed off" in an exploding bus, only to be resurrected in later campaigns. The self-parody was pitch-perfect: Shatner, the aging Star Trek icon, brought a winking grandeur to the act of saving forty dollars on a hotel room.

The campaign ran for twenty years across television, radio, and print, and gave Priceline something almost no other dot-com company achieved: genuine, lasting brand recognition among mainstream American consumers. Reports that Shatner made $600 million from his stock compensation became the stuff of Silicon Valley legend, though the reality was more modest: he sold approximately half his shares at prices well below the stock's peak, and the rest declined sharply during the crash. Still, the partnership between Shatner and Priceline remains one of the most successful celebrity endorsement deals in advertising history.

The timing was exquisite. By early 1999, Priceline was booking over a thousand airline tickets and a thousand hotel rooms per week. First-quarter 1999 sales reached nearly 200,000 tickets, fifty percent more than the company had sold in its entire first nine months.

On March 30, 1999, Priceline went public on the NASDAQ at $16 per share. The opening trade was $26.625. Within hours, the stock hit $85. It closed the day at $69, a 331 percent first-day gain, valuing the company at roughly $13 billion, the highest first-day market capitalization for a new corporation at the time. Jay Walker, who owned approximately 35 percent of the company, was instantly a multi-billionaire. One month later, on April 30, the stock closed at $162.37. By May 1999, shares peaked near $165, pushing the valuation toward $19 billion.

Then the world changed.

What happened next is a cautionary tale about the difference between a good idea and a sustainable business. Flush with confidence and investor enthusiasm, Priceline decided that if Name Your Own Price worked for airline tickets, it should work for everything. The company launched into groceries, gasoline, home mortgages, and automobiles through a partially owned affiliate called WebHouse Club.

WebHouse had raised between $200 and $300 million, but the economics were catastrophic. Brand-name packaged-goods manufacturers viewed permanent discounting as an existential threat to their pricing power. The grocery and gasoline business attracted two million customers and signed up over seven thousand grocery stores and six thousand gas stations in less than a year, but it was burning cash at a rate that demanded at least another $100 million to reach profitability. In October 2000, WebHouse announced it was ceasing operations. Priceline's stock plunged 38 percent on the news.

But WebHouse was only the most spectacular failure. The broader dot-com crash was already underway, and Priceline's stock, which had peaked near $165, began a sickening descent. By the end of 2000, shares had fallen to approximately $6.37. After the September 11, 2001 terrorist attacks devastated the travel industry, the stock fell further still. From its adjusted peak near $1,000 (accounting for a later reverse split), Priceline's shares collapsed to approximately $6.60, and its market capitalization shrank from $24 billion to roughly $250 million. The stock repeatedly flirted with the $1 mark, putting it at risk of NASDAQ delisting. The company that had briefly been worth more than several major airlines combined was now worth less than a single 747.

Through a revolving door of leadership, Daniel Schulman served as CEO from mid-2000, growing revenues from $20 million to roughly $1 billion annually, before being replaced in 2001 by the returning Richard Braddock. But the turnaround that would ultimately matter began in 2002, when Jeffery H. Boyd was named chief executive officer.

Boyd was the anti-Jay Walker. Where Walker was a showman and patent evangelist, Boyd was methodical, operational, and ruthlessly focused. A lawyer by training who had served as Priceline's general counsel before ascending to the top job, Boyd approached the company's problems with the precision of someone drafting a contract rather than pitching a vision. His first major act was to strip away the failed product experiments and return Priceline to its core: travel. In 2003, he executed a 1-for-6 reverse stock split, taking the share price from around $3.50 to $22 and restoring the company's standing on the NASDAQ. The grocery dreams and gasoline experiments were dead. Priceline was going to be a travel company, period.

Boyd also recognized that while the Name Your Own Price model made for great television, the real money in online travel was in the standard retail model: showing travelers available rooms at set prices and taking a commission. He quietly built out Priceline's retail hotel booking capabilities alongside the signature bidding product, creating a more conventional revenue engine while Shatner continued to promote the brand on television. The Name Your Own Price feature for flights would ultimately survive until 2016, for rental cars until 2018, and for hotels until 2020, but it became an increasingly small share of the company's revenue as the retail model scaled.

But Boyd understood something else: Priceline's future was not going to be built in the United States alone. The American online travel market was becoming fiercely competitive, with Expedia, Orbitz, and Travelocity all fighting for share. Europe, by contrast, was a vast and largely untapped market where online penetration of hotel bookings remained low and no single platform had established dominance. Priceline needed a different engine, and a different geography. And the engine Boyd would find was not in Norwalk, Connecticut. It was 3,600 miles away, in a university town in the Netherlands.

III. Meanwhile in Europe: The Booking.com Genesis

On November 12, 1996, six months after Jay Walker incorporated Walker Digital, a recent graduate of the University of Twente named Geert-Jan Bruinsma sat down with his former internship supervisor, Jan Willem Smeenk, for a dinner that would change the trajectory of global travel.

Bruinsma had studied at Universiteit Twente in the eastern Netherlands, graduating in 1994 with a degree in business and technology. He was not a hospitality industry veteran. He was not a Silicon Valley entrepreneur. He was a twenty-something Dutch techie with a modem and an idea. Smeenk, over dinner, suggested that Bruinsma look into hotel reservations as a potential internet business. The Netherlands, with its dense network of small hotels, bed-and-breakfasts, and canal-side guesthouses, seemed like a natural testing ground.

Bruinsma set up a server under his desk and launched Bookings.nl, a website where travelers could search for and reserve hotel rooms in the Netherlands. The concept was elegant in its simplicity: aggregate hotel inventory, present it to consumers in a searchable format, and take a commission when a booking was made. There was no Name Your Own Price gimmickry, no bidding war, no theatrical marketing. Just a clean interface connecting travelers to hotels.

The early years were modest. Bruinsma did not hire his first employee until 1999. By 2002, the company had grown to about fifty people. But the business was quietly building something that would prove far more valuable than Priceline's consumer brand: a direct, commission-based relationship with thousands of independent European hotels.

This distinction matters enormously, and understanding it is key to understanding everything that followed. In the American online travel market of the late 1990s and early 2000s, the dominant model was the "merchant" model, pioneered by Expedia and Hotels.com. Under this model, the online travel agency (OTA) negotiated a discounted rate with the hotel, collected payment from the guest upfront, and then remitted a portion to the hotel after the stay. The OTA controlled the customer relationship, the payment, and the data. Hotels got filled rooms, but they gave up margin and, crucially, they gave up the relationship with their own guests.

Booking.com took the opposite approach. Under its "agency" model, the guest paid the hotel directly, typically at checkout. Booking.com never touched the money. Instead, the hotel paid Booking.com a commission, typically between ten and twenty-five percent, after the guest completed their stay. This sounds like a small difference, but its implications were profound.

To understand the practical difference, imagine you are a small hotel owner in Bruges, Belgium. Under the merchant model, an OTA books your room for 120 euros per night, collects payment from the guest, and then sends you 90 euros weeks later, after deducting their margin. You have no idea what the guest paid, you have no direct relationship with the guest, and if the OTA goes bankrupt before remitting your share, you are out of luck. Under the agency model, the guest pays you 120 euros directly at checkout. You then pay Booking.com a commission of, say, 15 percent, or 18 euros. You keep the relationship, you control the cash, and you know exactly what the guest paid. For a family-run hotel operating on thin margins, this difference was not academic. It was existential.

For Booking.com, the agency model had its own advantages. It was lighter on capital, since the company never had to float large amounts of money between payment and remittance. And it aligned incentives beautifully: Booking.com only made money when hotels made money. There was no perverse incentive to drive down hotel rates, because Booking.com's commission was a percentage of the room price. Higher prices meant higher commissions. This alignment created a fundamentally different dynamic between platform and supplier than what existed in the U.S. market, and it is one of the core reasons Booking.com was able to sign up independent European hotels at a pace its American competitors could not match.

In 2000, the company took a significant step forward when Bookings.nl merged with Bookings Online, a company founded by Sicco Behrens, Alec Behrens, Marijn Muyser, and Bas Lemmens. The merged entity was rebranded as Booking.com, and Stef Noorden was appointed CEO. The merger combined complementary capabilities and set the stage for expansion beyond the Netherlands.

What made Booking.com's European context so advantageous was the very fragmentation that American companies found daunting. Europe's hotel market was, and remains, overwhelmingly independent. Unlike the United States, where large chains like Marriott, Hilton, and Hyatt dominate and maintain their own sophisticated reservation systems, European accommodations are a patchwork of family-owned hotels, boutique guesthouses, and small chains. A pension in Prague operates nothing like a villa in Sardinia, which operates nothing like a canal house in Amsterdam. No single booking system served them all. This fragmentation was the opportunity.

By 2005, Booking.com had established local support offices in the United Kingdom, France, Spain, Portugal, and Germany. The company was not just listing hotels; it was building on-the-ground relationships in each market, understanding local customs, speaking local languages, and earning trust with hoteliers who had never worked with an online platform before.

This ground game was deeply unglamorous. It meant sending account managers door-to-door in Seville and Salzburg. It meant building customer support in languages from Finnish to Greek. It meant understanding that a three-star hotel in France had entirely different expectations and needs than a three-star hotel in Poland. But this labor-intensive approach would prove to be an almost insurmountable competitive advantage, because once a hotelier trusted Booking.com and integrated it into their daily operations, the switching costs were real.

The founders and early team at Booking.com were techies, not hoteliers. They knew very little about the hotel industry's traditional ways of doing business. In retrospect, this was a feature, not a bug. Unburdened by industry convention, they built their platform around data, testing, and relentless iteration. They treated the hotel booking experience as an engineering problem to be optimized, not a hospitality tradition to be respected. This mindset would become the company's defining characteristic, and it was about to attract the attention of an unlikely suitor across the Atlantic.

IV. Active Hotels: The Forgotten Piece

Before Booking.com entered the picture, there was Active Hotels, a startup that history has largely forgotten but that played a pivotal role in connecting the dots between Priceline and the European hotel market.

In 1999, two cousins named Andy Phillipps and Adrian Critchlow founded Active Hotels in Cambridge, England. Phillipps had just completed an MBA at INSEAD in France and was looking for his next venture. Critchlow had the original idea for the business, an online platform for booking independent European hotel rooms, but was running another company at the time. He invited his cousin to serve as chief executive while he contributed as a partner. Their first office was at 3 Wellington Court in Cambridge, described by those who worked there as a very small suburban house with two floors and one toilet.

Like Bruinsma in the Netherlands, Phillipps and Critchlow were techies who knew very little about the hotel industry. And like Bruinsma, they saw the fragmentation of Europe's independent hotel market as the opportunity of a lifetime. Active Hotels built relationships with approximately eight thousand properties across the United Kingdom and continental Europe, ranging from bed-and-breakfasts to five-star luxury hotels, including both independents and major international chains.

What made Active Hotels particularly valuable was its distribution network. Beyond its own consumer-facing websites, including activereservations.com, the company powered hotel bookings on approximately fifteen hundred partner websites across Europe. This white-label distribution capability meant that Active Hotels' hotel inventory was exposed to a wide surface area of European travelers, even if few of them had ever heard the Active Hotels brand name. The company had been profitable since the first quarter of 2003, a notable achievement for an early-2000s internet startup.

Here is where the story converges. Glenn Fogel, then working in corporate development at Priceline, had been making regular reconnaissance trips to European tech conferences and travel industry events. Fogel was a Wharton-educated former investment banker who had worked at Kidder, Peabody and Morgan Stanley before joining Priceline in February 2000, right at the onset of the dot-com crash. He had the analytical rigor of Wall Street and an unusual gift for building personal relationships in an industry where trust mattered.

Those who worked with Fogel during this period describe him in remarkably consistent terms. As one contemporary put it, "Glenn's a hugely personable, well-connected and great guy, and he was very, very well-connected to the European tech scene. And probably, crucially, we trusted him. He's got very high integrity as an individual." In an industry full of sharp-elbowed dealmakers, Fogel's earnestness and genuine curiosity about European travel technology set him apart.

The connection to Active Hotels reportedly came together in a remarkably straightforward way. Shane Whaley, associated with Active Hotels, simply reached out to Priceline directly. As one account has it, Whaley "called up Priceline and said, 'Oh, do you want to do a deal with us so we can give you all this inventory of independent hotels in Europe?'"

Priceline, which had already been evaluating European expansion strategies under Fogel's guidance, had probably come to the conclusion that an acquisition was the right thing to do. Building a European presence from scratch would take years and require navigating dozens of local markets, languages, and regulatory environments. Buying an established player with existing hotel relationships was faster, surer, and ultimately cheaper.

On September 21, 2004, Priceline announced it had acquired Active Hotels for approximately $161 million in cash. The target's revenues for the twelve months ending September 30, 2004, were expected to be approximately $22 million, up about 115 percent year-over-year.

By the standards of the time, this was a substantial price for a small European internet company, representing roughly seven times trailing revenue. But Priceline was buying more than revenue. It was buying a beachhead in the European hotel market, a proven team with deep relationships across the continent, and in Andy Phillipps, a leader who would play a crucial role in the next, far more consequential acquisition.

After the deal closed, Phillipps was elevated to CEO of Priceline's non-U.S. business. From this perch, he could see the competitive landscape of European online travel in granular detail. And what he saw, just a few hundred miles southeast in Amsterdam, was a company that was growing faster, had deeper hotel relationships, and was building something that Active Hotels alone could not match. The acquisition of Active Hotels was important in its own right. But its greatest legacy was opening the door to Booking.com.

V. The $133 Million Deal That Changed Everything

On July 14, 2005, a press release went out simultaneously from Norwalk, Connecticut, Cambridge, and Amsterdam. Priceline.com announced it had acquired Amsterdam-based Bookings B.V., one of Europe's leading internet hotel reservation services, in a cash transaction valued at approximately 110 million euros, or $133 million.

To put that price in perspective: $133 million was less than Priceline had paid for Active Hotels the previous year. It was less than the cost of a single luxury hotel property in central London. It was, in 2005 dollars, a rounding error for a company like Google or Microsoft. And it would turn out to be, dollar for dollar, perhaps the most lucrative acquisition in the history of the internet.

But at the time, the deal was far from obvious. Booking.com was a strong business, but it was not yet dominant. Its revenues were modest. Its brand was known primarily in the Netherlands and a handful of other European markets. The online travel industry was consolidating rapidly, and the conventional wisdom held that scale and brand recognition, the attributes that Expedia possessed in abundance, would determine the winners.

Which raises the natural question: why did Expedia pass?

The precise reasons have never been fully detailed in public, but the outlines are clear. Andy Phillipps, newly installed as head of Priceline's international business, had been in contact with Expedia about potential deals in the European market. Expedia, then led by Dara Khosrowshahi (who would later become CEO of Uber), was pursuing its own European strategy, but its approach was fundamentally different. Expedia favored the merchant model and was building a more centralized, U.S.-centric organizational structure. The prospect of acquiring a Dutch company running an agency model with a fiercely independent team may not have fit neatly into Expedia's playbook. Whatever the specifics, Expedia's decision not to acquire Booking.com ranks alongside Excite's rejection of Google as one of the great missed opportunities in internet history.

For Priceline, the deal was driven by Glenn Fogel's conviction, Phillipps's on-the-ground knowledge, and Jeff Boyd's willingness to let the European team operate on their own terms. The deal structure reflected a level of mutual commitment that went beyond a simple cash acquisition. Booking.com's six top executives reinvested a portion of their acquisition proceeds back into the business, keeping skin in the game and signaling to their teams that this was not a corporate takeover but a partnership.

The integration that followed was, by all accounts, both remarkable and occasionally turbulent. In 2006, Priceline merged Active Hotels and Bookings to create a unified Booking.com brand. As one participant recalled, "In the grand scheme of things, the integration went remarkably well, although it was at times a tough marriage between Active and Bookings. There were cultural differences and clashes among the teams."

The cultural friction was real. Cambridge was British: polite, process-oriented, and structured. Amsterdam was Dutch: direct, flat-hierarchied, and allergic to corporate formality. The teams had different ideas about everything from how to prioritize product features to how to negotiate with hotel partners. Some Active Hotels employees felt their contributions were being subsumed; some Bookings employees felt the Cambridge team was too traditional. But the friction was productive, not destructive. The combined entity ended up stronger than either piece alone. Active Hotels brought distribution partnerships, its network of fifteen hundred affiliate websites, and deep UK market penetration. Bookings brought the superior technology platform, the agency model, deeper continental European relationships, and a relentless data-driven culture that would come to define the merged organization.

The single most important strategic decision Priceline made, arguably more important than the acquisition itself, was what happened after the deal closed. Most acquiring companies, especially American ones buying foreign targets, impose their own management, their own systems, and their own culture. Priceline did the opposite. The company's leadership adopted a philosophy that one observer summarized as: "The philosophy of the holdings was to let its constituent companies execute independently and even compete."

This was not benign neglect. It was a deliberate strategy rooted in Boyd and Fogel's recognition that Booking.com's Dutch team understood the European market far better than anyone in Norwalk, Connecticut, ever could. The Amsterdam team was given the autonomy to set its own product roadmap, hire its own people, and make its own decisions about how to compete. Priceline provided capital, strategic guidance, and the occasional assist with things like payment processing and supplier negotiations. But day-to-day, Booking.com was run by its own people, in its own city, according to its own instincts.

This autonomy would prove to be the foundation of everything that followed. The Booking.com team used it to build a culture of relentless experimentation, data-driven decision-making, and performance marketing mastery that would turn a $133 million acquisition into the most valuable travel company on earth.

VI. The Booking.com Playbook: Data, Testing, and Relentless Execution

If there is a single word that captures the culture Booking.com built in Amsterdam, it is "testing." Not testing in the casual sense of trying things out, but testing as an organizational religion, a fundamental belief that data, not intuition, should drive every product decision.

At its peak, Booking.com was running thousands of A/B tests simultaneously on its platform. Every element of the user experience, the color of a button, the phrasing of a call to action, the placement of a price guarantee badge, the number of photos shown for a property, was subject to rigorous experimentation. Changes were not rolled out because a product manager had a hunch or a VP had a strong opinion. They were rolled out because a statistically significant test showed they improved conversion rates, booking value, or customer satisfaction.

This testing culture had its roots in the DNA of the founding team. The early Booking.com employees were engineers and data scientists, not hospitality industry veterans. They approached hotel booking the way a Silicon Valley startup would approach optimizing an e-commerce checkout flow, with one critical difference: they were doing it in dozens of languages, across dozens of markets, with cultural nuances that no single product team could fully understand. The solution was to let the data speak. Run the test in German and French and Italian and Dutch simultaneously. Let each market's consumers reveal their preferences through their behavior, not through focus groups or executive assumptions.

The results were extraordinary. The agency model, combined with this testing-driven product approach, created a virtuous cycle that became almost impossible for competitors to replicate. The cycle worked like this: more hotel inventory on the platform attracted more consumers. More consumers meant more bookings. More bookings generated more data. More data enabled better testing. Better testing improved conversion rates. Higher conversion rates made the platform more attractive to hotels, because they saw more bookings per listing. More hotels joined the platform. And the cycle repeated, each revolution compounding the advantage.

The financial trajectory tells the story. When Priceline acquired Bookings and Active Hotels, the parent company was barely profitable, having posted a loss of $19 million in 2002. By 2011, Priceline's profit had surged to $1.1 billion. This transformation was not driven by the Priceline brand in the United States. It was driven almost entirely by Booking.com's explosive growth in Europe and, increasingly, across the rest of the world.

Several specific elements of the Booking.com playbook deserve attention, each of which contributed to the compounding advantage that competitors found so difficult to replicate.

Performance marketing and SEO dominance. Booking.com became one of the largest buyers of Google search advertising in the world. The company approached paid search with the same data-driven rigor it applied to product testing: every keyword, every bid, every ad copy variation was tested, optimized, and scaled based on return on investment. But Booking.com also invested heavily in organic search optimization, building hundreds of thousands of landing pages for specific cities, neighborhoods, and hotel types. If you searched for "hotels near the Eiffel Tower" or "bed and breakfast in Tuscany," Booking.com's pages were almost always at or near the top of the results. This combination of paid and organic search dominance created a customer acquisition engine of staggering efficiency.

Incentive-aligned commissions. The commission model aligned incentives in a way that the merchant model could not. Because Booking.com earned a percentage of the room rate, it had every incentive to help hotels succeed. Higher occupancy, higher rates, and better reviews all meant higher commissions. Booking.com invested in tools that helped hotels manage their listings, respond to reviews, and optimize their pricing. This partnership dynamic created loyalty among hoteliers that was difficult for competitors to disrupt.

The Dutch advantage in international expansion. International expansion benefited enormously from the company's Dutch roots. The Netherlands has a long tradition of multilingualism and international commerce. The Dutch, by necessity and culture, speak multiple languages and are comfortable navigating diverse business environments. Booking.com's team brought this cosmopolitan sensibility to its expansion strategy, building truly localized experiences for each market rather than simply translating an English-language interface. The company hired native speakers, established local offices, and built customer support capabilities in dozens of languages. This approach resonated with both travelers and hoteliers in ways that a more U.S.-centric company could not easily match.

Conversion optimization as a science. The product itself was relentlessly optimized for conversion. Booking.com pioneered many of the psychological nudges that are now standard in e-commerce: "Only 2 rooms left at this price," "15 people are looking at this hotel right now," "Last booked 3 minutes ago." These urgency signals were not arbitrary; they were the output of thousands of tests showing that social proof and scarcity messaging significantly increased booking rates. Critics called these practices manipulative. Booking.com's response was that they were simply providing transparent, real-time information that helped consumers make decisions.

For investors, the key insight from this era is that Booking.com's competitive advantage was not any single feature or technology. It was a system, a tightly integrated combination of the agency model, the testing culture, performance marketing expertise, and international localization that was greater than the sum of its parts.

Replicating any one element was straightforward. Any company can run A/B tests. Any company can buy Google ads. Any company can adopt an agency model. But replicating the entire system, with its compound learning effects, network dynamics, and decades of accumulated data and supplier relationships, was nearly impossible. This systemic advantage is the reason Booking.com became, and remains, the dominant online travel platform globally.

VII. The Portfolio Expansion: KAYAK, Agoda, and OpenTable

With Booking.com generating extraordinary growth and profitability from its European base, Priceline's leadership turned to a question that every successful platform company must eventually confront: how to grow beyond the core.

The answer, characteristically, was not to try to build everything internally. It was to acquire companies with strong market positions, talented teams, and complementary capabilities, and then apply the same philosophy of operational autonomy that had worked so spectacularly with Booking.com.

The first major addition to the international portfolio actually predated the Booking.com acquisition in strategic importance, even if it was smaller in scale. In November 2007, Priceline acquired Agoda, a Thailand-based online hotel booking platform focused on the Asian market. Founded in 2005 in Phuket by Michael Kenny and Robert Rosenstein, Agoda had built a strong position in Southeast Asia's rapidly growing travel market. Its gross bookings through October 2007 were approximately $36 million, up 122 percent year-over-year. CEO Jeff Boyd acknowledged the scale differential candidly: "Agoda, while relatively small today, will be an important part of Priceline.com's expansion into Asia."

Agoda was Priceline's third international acquisition after Active Hotels and Bookings, and it reflected a clear geographic strategy. Booking.com would dominate Europe. Priceline.com would serve the United States. Agoda would conquer Asia. Each brand would operate independently, optimized for its own market, competing against local players with local knowledge and local relationships.

The Agoda acquisition illustrates a pattern that would become central to the Priceline playbook: buying small companies in markets where they had deep local knowledge, then giving them the capital and autonomy to scale. Agoda understood the nuances of Asian travel, from the preference for pay-at-property in Japan to the mobile-first behavior of Southeast Asian consumers, in ways that a headquarters in Connecticut never could. Rather than try to impose a one-size-fits-all product, Priceline let Agoda build a platform tailored to Asian consumers while sharing the backend infrastructure and supply relationships that came with being part of a larger group.

In 2010, the company quietly acquired TravelJigsaw, a car rental comparison service later rebranded as Rentalcars.com. The purchase price was not publicly disclosed, but the acquisition added a complementary vertical that would later become important as the company pursued its vision of a unified travel experience.

The next blockbuster deal came in 2013, when Priceline acquired KAYAK for $1.8 billion. KAYAK was a different animal from Booking.com or Agoda. It was not an OTA that took bookings directly. It was a metasearch engine, a platform that allowed travelers to compare prices across multiple booking sites (including Priceline and Booking.com) and then click through to the OTA or airline of their choice to complete the transaction. KAYAK's business model was built on advertising revenue and referral fees, not commissions.

The strategic logic was subtle but important. Metasearch was becoming an increasingly powerful force in travel, and Google was aggressively expanding its own travel search capabilities. By owning KAYAK, Priceline could capture traveler demand at the top of the search funnel, before consumers had committed to a specific booking platform. It was a defensive move against Google and an offensive move to capture incremental demand that might otherwise flow to competitors.

In 2014, the acquisitions continued with OpenTable, the leading online restaurant reservation platform, purchased for $2.6 billion. This was the most debated deal in the company's history. OpenTable had a dominant position in restaurant reservations, with a network of tens of thousands of restaurants and millions of diners. But the strategic connection to travel was less obvious than with KAYAK or Agoda.

Was it cross-selling, offering travelers the ability to book restaurants alongside hotels? Was it data synergy, combining travel and dining behavior to build richer customer profiles? Or was it simply a case of a company flush with cash buying a strong marketplace business because it could? In hindsight, the acquisition looks like it was partly ahead of its time. The Connected Trip vision that CEO Glenn Fogel would later articulate, in which a traveler books every component of their journey through a single platform, provides the strategic rationale that was harder to see in 2014.

The jury remains out on whether the price was right. OpenTable has continued to operate as an independent brand within the portfolio, and the company has recently launched new initiatives including an international expansion and a media product for restaurant advertising. But the transformative synergies that might have justified a $2.6 billion price tag have been slower to materialize than the extraordinary returns generated by the Booking.com acquisition.

In the midst of this acquisition activity, the parent company underwent two significant name changes that reflected the shifting balance of power within the portfolio. On April 1, 2014, priceline.com Incorporated became The Priceline Group Inc., creating a clear distinction between the Priceline brand (one subsidiary among several) and the corporate holding company. Then, on February 21, 2018, the company changed its name again, to Booking Holdings Inc., and its NASDAQ ticker symbol from PCLN to BKNG, with trading under the new symbol beginning February 27, 2018.

The second name change was particularly telling. Priceline was the company that Americans knew, the brand William Shatner had promoted for two decades. But in Shanghai, Tokyo, Paris, and Berlin, consumers were far more familiar with Booking.com. The subsidiary had outgrown the parent.

The rebranding acknowledged what the financial statements had made obvious for years: Booking.com was the engine, generating approximately 89 percent of the holding company's gross profit. The child had not just outgrown the parent; it had become the parent. For investors and analysts, the name change also served a practical purpose: it signaled that the company's future lay in its global, Booking.com-led strategy rather than in the U.S.-centric Priceline brand.

One acquisition that did not come to fruition deserves mention. In November 2021, Booking Holdings agreed to acquire eTraveli Group, a Sweden-based flight booking platform, from CVC Capital Partners for approximately 1.63 billion euros. The deal would have significantly strengthened Booking's flight booking capabilities, a critical component of the Connected Trip vision. But in September 2023, the European Commission blocked the acquisition, citing "conglomerate effects" concerns, the first time the Commission had ever prohibited a merger on those grounds alone. Booking Holdings appealed the decision, with a two-day hearing held in July 2025 and a ruling expected in 2026. In the meantime, the two companies signed an eight-year partnership extension, ensuring continued collaboration even without the formal merger.

VIII. The Modern Era: AI, Alternative Accommodations & The Connected Trip

On January 1, 2017, Glenn D. Fogel officially became chief executive officer and president of Booking Holdings, succeeding Jeff Boyd after a brief interim period following Darren Huston's resignation in April 2016. The appointment was a poetic culmination: the deal scout who had identified Booking.com and championed its acquisition was now running the entire empire.

Fogel brought a distinctive leadership style shaped by his diverse background. With a Wharton degree, Harvard Law education, and years in investment banking at Kidder Peabody and Morgan Stanley, he combined financial sophistication with the relational skills that had made him so effective in the European deal-making circuit. In June 2019, he added the title of CEO of Booking.com itself, unifying the corporate and operational leadership in a way that signaled a new phase of strategic integration.

Fogel's tenure began with strong momentum as Booking Holdings continued its growth trajectory through 2017, 2018, and 2019. But his first major challenge was not one anyone anticipated.

In late March 2020, Fogel tested positive for COVID-19, experiencing a 101-degree fever and headaches. His entire family was affected. He continued performing his duties as CEO while quarantined, a personal experience that gave him an intimate understanding of the crisis that was simultaneously devastating the travel industry worldwide.

The pandemic's impact on Booking Holdings was swift and brutal. In the first quarter of 2020, gross travel bookings fell 51 percent. By the second quarter, with borders closed and planes grounded worldwide, bookings nosedived 91 percent to just $2.1 billion. To grasp the magnitude: a company that had been processing tens of millions of transactions per quarter saw its business nearly vanish overnight. Full-year 2020 revenues fell 55 percent to $6.8 billion. Net income collapsed 99 percent to just $59 million.

The human toll was equally stark. Booking.com was forced to lay off approximately 25 percent of its global workforce, roughly four thousand employees, to save an estimated $250 to $300 million annually. For a company whose Amsterdam headquarters had become famous for its buzzing, international work culture, these were devastating cuts. KAYAK, OpenTable, and Agoda also reduced headcount by approximately 22 percent, including furloughed employees.

The recovery, when it came, was faster and stronger than many expected. Pent-up demand for travel, particularly in Europe where Booking.com was strongest, fueled a remarkable rebound. By the third quarter of 2021, adjusted earnings per share were growing over 205 percent year-over-year, with revenues and gross bookings each climbing roughly 77 percent. By 2022, the business had largely returned to pre-pandemic levels. And by 2024, Booking Holdings was posting record results that surpassed anything achieved before COVID, demonstrating the resilience of the platform model and the durability of the competitive advantages built over the prior two decades. The pandemic proved, perhaps more clearly than any other test could have, that the demand for travel is extraordinarily resilient and that Booking.com's marketplace position was not easily dislodged, even by a global crisis.

But the pandemic also accelerated strategic shifts that were already underway, most notably the push into alternative accommodations. The rise of Airbnb had exposed a vulnerability in Booking.com's historically hotel-centric model. Travelers, particularly younger ones, were increasingly interested in apartments, vacation homes, and unique stays. Booking.com's response was to aggressively build its alternative accommodations inventory, leveraging its existing hotelier relationships to encourage property managers to list non-traditional properties.

The results have been meaningful. By the fourth quarter of 2024, alternative accommodations listings reached 7.9 million, up 8 percent year-over-year. By late 2025, that number had grown to approximately 8.6 million listings. Alternative accommodations represented 37 percent of total room nights and accounted for over 30 percent of room night growth. While Airbnb retained a larger share of the short-term rental market at 44 percent versus Booking.com's 18 percent, the gap had narrowed considerably from 2019 levels.

The most ambitious strategic initiative under Fogel's leadership is the Connected Trip, a vision to transform Booking.com from a hotel booking platform into a comprehensive travel super-app. Think of it this way: today, most travelers plan a trip by visiting five or six different apps and websites. They search flights on Google or KAYAK, book a hotel on Booking.com, reserve a rental car on a separate platform, and find restaurants on yet another app. Each of these interactions is a separate, disconnected transaction. The Connected Trip vision is to bring all of these components into a single, integrated experience where each element of the trip is aware of the others, so that the platform can proactively suggest airport transfers at the right time, recommend restaurants near the hotel, and rebook connecting flights when disruptions occur.

The Connected Trip is not just a product feature; it is a strategic bet on customer lifetime value and engagement. A traveler who books only a hotel through Booking.com can easily comparison-shop on the next trip. A traveler who has booked their flight, hotel, rental car, and restaurant reservations through a single connected experience has far higher switching costs and generates far more revenue per trip.

The early metrics are encouraging. Connected trip transactions, defined as trips where a traveler booked more than one travel component, grew in the high-20-percent range in 2025. Multi-vertical transactions now represent a low-double-digit percentage of total Booking.com transactions. Flights have been a particular growth engine, with gross bookings reaching $16.8 billion in 2025, up 37 percent year-over-year. Attraction ticket bookings grew approximately 80 percent off a smaller base.

Underpinning the Connected Trip vision is a massive investment in artificial intelligence, particularly generative AI. In June 2023, Booking.com launched an AI Trip Planner, a conversational interface that allows travelers to describe their ideal trip in natural language and receive personalized recommendations and booking options. The company has since expanded its AI capabilities significantly, partnering with OpenAI, Microsoft, Google, Amazon, and Salesforce.

In October 2025, Booking.com debuted its first customer-facing agentic AI innovations: Smart Messenger, which autonomously handles guest communications by gathering partner and property information, and Auto-Reply, which enables partners to define custom responses for common guest questions. CEO Fogel has highlighted the concept of "Autonomous Rebooking," where AI can proactively rebook a traveler's flight or hotel during a disruption without the user ever opening the app, an experience that transforms the platform from reactive tool to proactive travel assistant.

To understand why AI matters so much for Booking Holdings, think about what the company really is: a matching engine that connects travelers with the right accommodation, at the right price, at the right time. Traditional search and filter interfaces require the traveler to do the matching work themselves, scrolling through dozens of listings, comparing prices, reading reviews. Generative AI has the potential to automate much of this process: a traveler describes what they want in plain language, "a quiet hotel near the beach in Barcelona for under 150 euros a night, pet-friendly, with good breakfast reviews," and the AI does the matching. For a company with billions of data points on traveler preferences and property characteristics, this is a natural evolution, and a formidable competitive advantage over rivals with less data to train on.

The AI investment is not just customer-facing. On the operational side, AI-powered tools have reduced customer service costs by approximately 10 percent even as booking volumes grew. The company's broader Transformation Program, which includes AI-driven efficiency improvements, achieved approximately $550 million in annual run-rate savings, hitting the high end of prior guidance, with full realization expected by the end of 2026. Roughly one-third of those savings came from headcount reductions, while the remainder reflected process automation and operational streamlining. In 2025, Booking.com implemented additional layoffs as part of this program, cutting approximately 10 percent of its Amsterdam workforce, roughly 900 employees, in April 2025, with about 1,000 positions eliminated globally by July.

For 2026, Booking Holdings has committed to reinvesting approximately $700 million above its baseline in generative AI, Connected Trip development, U.S. and Asia expansion, advertising business development, OpenTable international expansion, and fintech and loyalty initiatives. Management targets this investment to generate approximately 100 basis points of faster revenue growth. Fogel was named Fortune's 2024 CEO of the Year and received the Yale Legend in Leadership Award in 2025, recognition of his role in navigating the company through the pandemic and positioning it for the AI era.

IX. Financial Analysis & Business Model Deep Dive

To understand Booking Holdings as a business, start with the simplest possible description: the company takes a commission every time someone books a room through one of its platforms. That commission, typically between 12 and 15 percent of the room rate, is the engine that generates tens of billions in revenue with remarkably little capital investment. Booking Holdings does not own hotels. It does not operate airlines. It does not employ housekeeping staff or maintain swimming pools. It operates a digital marketplace, and its primary assets are its technology platform, its brand, and its relationships with millions of accommodation providers worldwide.

For the year ended December 31, 2024, Booking Holdings reported revenues of $23.7 billion on gross bookings of $166 billion. In 2025, revenues grew 13 percent to $26.9 billion on gross bookings of $186.1 billion. The take rate, the percentage of gross bookings that Booking Holdings captures as revenue, has been remarkably stable at approximately 14 to 15 percent. This stability is itself a competitive signal: it suggests that the company has found an equilibrium where its commission rates are high enough to generate substantial profit but low enough that hotels prefer listing on the platform to the alternatives. If Booking.com tried to raise commissions significantly, hotels would shift volume to competitors or invest more in direct bookings. If commissions fell, profitability would erode. The stability of the take rate reflects a marketplace in balance.

The profitability of this model is exceptional by any standard. In 2025, adjusted EBITDA reached $9.9 billion, up 20 percent year-over-year, representing a margin of 36.9 percent. This margin expansion, from 35.0 percent in 2024, reflects both operating leverage and the savings from the Transformation Program. Adjusted earnings per share reached $228.06, up 22 percent. Free cash flow was approximately $9.1 billion.

These are not just good numbers for a travel company. They are exceptional numbers for any company in any industry. A nearly 37 percent EBITDA margin on $27 billion in revenue, combined with low capital expenditure requirements and strong free cash flow conversion, creates an economic engine of extraordinary power. For comparison, Marriott International, which operates and franchises thousands of physical hotels, generated roughly $6.1 billion in revenue in its most recent fiscal year with far higher capital intensity. Booking Holdings generates four times the revenue without owning a single hotel room.

The cost structure reveals where the money goes and, just as importantly, where it does not. The dominant expense category is sales and marketing, which in 2024 amounted to $7.3 billion, representing the single largest line item. By some measures, marketing costs represent approximately 72 percent of the company's total operating expenses. This figure can appear alarming in isolation, but context matters. Nearly all of Booking Holdings' marketing spend is performance-based, meaning the company pays for advertising (primarily Google search ads) only when it generates a measurable return. The company does not spend billions on brand advertising in the hope that awareness will eventually translate to bookings. It spends billions on performance marketing with real-time measurement of return on ad spend.

This performance-marketing dependency is both a strength and a vulnerability. It is a strength because it creates a disciplined, ROI-driven customer acquisition engine that scales efficiently. It is a vulnerability because it creates a structural dependence on Google, which controls the search ecosystem through which the majority of online travel demand is expressed. Any change in Google's algorithms, pricing, or competitive behavior directly affects Booking Holdings' customer acquisition costs.

The geographic breakdown adds nuance. Booking Holdings generates the majority of its revenue from Europe, where Booking.com is the dominant platform. Asia contributes a growing share through Agoda and Booking.com's expansion, while the Americas, anchored by the Priceline brand, represents a smaller but still significant portion. This international diversification is a strategic asset, providing exposure to multiple economies and travel markets while reducing dependence on any single country. It is also a natural hedge: when European demand softens, Asian travel often strengthens, and vice versa.

To put the scale in competitive context: the top four online travel agencies, Booking Holdings, Expedia Group, Airbnb, and Trip.com, collectively accounted for 96 percent of the OTA sector's $58 billion in revenue in 2024. Booking Holdings alone captured roughly 41 percent of that total. The four companies collectively invested a record $17.8 billion in sales and marketing in 2024, up $1 billion from the prior year, reflecting both the intensity of competition and the scale of the customer acquisition opportunity. Booking.com led globally in online travel traffic with approximately 563 million average monthly visitors, a testament to the compounding effects of its SEO and brand investments.

Capital allocation under Fogel's leadership has been aggressive and shareholder-friendly. In 2024, the company repurchased $6.5 billion in stock and paid $1.2 billion in cash dividends. Since 2014, share repurchases have reduced the outstanding share count by almost 39 percent. In January 2025, the board approved a new $20 billion buyback authorization, and in February 2026, it announced a 25-for-1 stock split effective April 2, 2026, the first stock split in the company's history, designed to improve share accessibility for retail investors.

The marketplace dynamics create powerful network effects that reinforce the company's competitive position. More hotel listings attract more travelers, because consumers prefer platforms with the widest selection. More travelers attract more hotel listings, because hoteliers want access to the largest pool of potential guests.

The data generated by this two-sided marketplace adds a third dimension to the flywheel. Billions of searches, hundreds of millions of bookings, and reviews in dozens of languages create a feedback loop that continuously improves the product through AI and machine learning. Each booking teaches the algorithm something about traveler preferences, seasonal patterns, and pricing sensitivity. This data advantage compounds over time, making the platform incrementally better at matching travelers with the right properties, which in turn drives higher conversion rates, which attracts more supply, which generates more data.

The two to three key performance indicators that best track Booking Holdings' ongoing performance are: room nights booked (a measure of volume that captures both market share and demand trends), and take rate (revenue as a percentage of gross bookings, which captures pricing power and the health of the commission model). A third metric worth monitoring is the share of connected trip transactions, which measures the company's progress toward its Connected Trip vision and the resulting increase in revenue per customer.

X. Playbook: Lessons for Founders & Investors

The Booking Holdings story offers a masterclass in how to build a durable competitive advantage in a marketplace business. Several lessons stand out as broadly applicable.

The power of focus. Before Booking.com tried to be a travel super-app, it spent years being the best hotel booking platform in the world. The discipline to resist premature diversification, to be "just" accommodations before expanding into flights, rental cars, and restaurants, allowed the company to build depth in its core market that no horizontal competitor could match. Priceline's failed experiments with groceries and gasoline in 2000 provide the perfect contrast: the same company that almost died from over-diversification was saved by a subsidiary that succeeded through relentless focus.

Decentralized autonomy for acquired companies. The conventional M&A playbook calls for rapid integration: consolidate systems, standardize processes, eliminate redundancies, and impose the parent company's culture. Priceline did the opposite, and it worked. By letting Booking.com, Agoda, and KAYAK operate independently, the holding company preserved the entrepreneurial energy, local market knowledge, and distinct competitive advantages that made each acquisition valuable in the first place. The brands were even allowed to compete with one another, on the theory that intra-portfolio competition kept each team sharp and ultimately captured more of the market than a single unified brand could.

The advantage of starting international. American technology companies tend to build for the U.S. market first and expand internationally as an afterthought. Booking.com's Dutch origins gave it an inherent advantage in international markets. The team was multilingual by default, culturally sensitive by necessity, and unencumbered by the U.S.-centric assumptions that handicapped competitors. This international DNA enabled Booking.com to build localized experiences in dozens of markets simultaneously, a capability that U.S.-based competitors have struggled to replicate.

Incentive alignment through the agency model. The decision to let hotels collect payment directly and pay Booking.com a commission after the fact was not just a business model choice. It was a trust-building mechanism that aligned the platform's interests with those of its suppliers. Hotels saw Booking.com as a distribution partner, not a competitor. This alignment fostered the deep, long-term relationships with independent hoteliers that became the foundation of Booking.com's inventory advantage.

Performance marketing mastery and the testing religion. Booking.com's approach to customer acquisition and product development was fundamentally different from the intuition-driven decision-making that characterizes many companies. By making data the arbiter of every product decision and demanding measurable ROI from every marketing dollar, the company built a culture where optimization was continuous and compounding. The thousands of simultaneous A/B tests were not a gimmick; they were a systematic method for extracting value from the platform's massive data advantage.

Patient capital and long-term thinking. Priceline's willingness to let Booking.com grow at its own pace, to invest in market expansion and product development without demanding immediate returns, was essential. The European hotel market was enormous but fragmented, and building dominant market share required years of patient, market-by-market execution. A more impatient parent might have pushed for premature profitability or forced integration decisions that would have undermined Booking.com's autonomy and growth trajectory. Consider the contrast with many private equity-backed acquisitions, where the imperative to generate returns within a three-to-five-year fund cycle can force premature cost-cutting or strategic pivots. Priceline, as a public company with a long-term oriented management team, had the luxury of thinking in decades rather than fund cycles.

Industry observers have ranked Priceline's acquisition of Bookings B.V. as the fifth greatest deal in internet history, and some have argued it deserves an even higher ranking when the full magnitude of value creation is considered. From $133 million to an enterprise responsible for the vast majority of a $135 billion company's earnings, the return on investment is difficult to overstate.

XI. Bull Case vs. Bear Case

Bull Case

Booking Holdings occupies what may be the most defensible position in consumer internet. The bull case rests on several reinforcing pillars.

Scale advantages and network effects are formidable. With over 28 million listings across 220-plus countries and territories, including 8.6 million alternative accommodations, Booking.com offers the widest selection of any accommodation platform. This breadth attracts more consumers, which attracts more supply, creating a classic two-sided network effect that is extremely difficult to disrupt. In Hamilton Helmer's 7 Powers framework, this constitutes both Network Economies (value to each user increases with scale) and Scale Economies (fixed costs like technology development are spread across an enormous transaction base).

The Connected Trip vision, if executed successfully, could dramatically expand the addressable market and deepen the competitive moat. Flights grew 37 percent year-over-year in 2025, airline tickets booked rose 52 percent in Q4 2024, and attraction bookings grew approximately 80 percent. Each additional vertical increases revenue per customer and raises switching costs. A traveler whose entire trip is managed through a single platform has far less incentive to comparison-shop than one who books only a hotel.

AI integration is creating new forms of competitive advantage. The investment in generative AI and agentic AI, from the Trip Planner to Autonomous Rebooking, positions Booking.com to transform from a search-and-book tool into a proactive travel assistant. The company's massive proprietary data set of traveler preferences, booking patterns, and property information creates a training advantage that new entrants would need years to replicate. This is what Helmer would call Cornered Resource, proprietary data that competitors cannot access.

Cash generation and capital returns are exceptional. With $9.1 billion in free cash flow in 2025, the company has enormous financial flexibility to invest in growth, return capital through buybacks and dividends, and weather economic downturns. The share count has been reduced by nearly 39 percent since 2014, creating significant per-share value creation even if the business merely maintains its current scale.

Applying Porter's Five Forces to the OTA industry further illuminates the bull case. The threat of new entrants is low because the combination of network effects, brand recognition, supply relationships with millions of properties, and performance marketing expertise creates barriers to entry that are measured in billions of dollars and decades of accumulated data. Buyer power (travelers) is moderate: individual travelers have low switching costs between OTAs, but the breadth of selection and the convenience of a familiar platform create meaningful inertia. Supplier power (hotels) is fragmented, which is advantageous for Booking.com. With millions of independent properties on the platform, no single hotel or chain can exert meaningful pricing pressure. The threat of substitution, direct booking through hotel websites, has been a perennial concern but has not materially eroded OTA market share, in part because hotels themselves recognize the customer acquisition value that OTAs provide. Industry rivalry is intense but rational: the top four OTAs collectively account for 96 percent of the sector's revenue, and while marketing spending is significant, the leading players have found a stable equilibrium.

Compared to its direct competitors, Booking Holdings has several structural advantages. Against Expedia, which generated approximately $14 billion in revenue in 2024, Booking Holdings has superior international diversification, a more capital-efficient agency model, and stronger margin expansion. Expedia's heavy reliance on the U.S. domestic market makes it more vulnerable to regional economic slowdowns. Against Airbnb, which dominates the alternative accommodation brand, Booking.com's advantage lies in the breadth of its inventory (hotels plus alternatives), its B2B relationships with professional hoteliers, and its strength in European and Asian markets. Against Trip.com, Booking Holdings benefits from a larger global footprint and deeper brand recognition outside of Greater China.

Bear Case

The bear case centers on several genuine and emerging risks that warrant careful monitoring.

Google represents the single largest competitive and structural threat. As the gatekeeper to online search, Google controls the channel through which the majority of Booking Holdings' customers discover and reach the platform. Google's own travel products, including Google Hotels, Google Flights, and increasingly AI-powered travel planning, directly compete with Booking's core offerings. Any algorithm change that deprioritizes OTA results in favor of Google's own products, or any increase in the cost-per-click for travel-related keywords, directly impacts Booking Holdings' customer acquisition costs and margins. In Porter's Five Forces terms, this is supplier power at its most acute: Google is the supplier of customer attention, and it faces no competitive constraint on how it prices or allocates that supply. The February 2026 selloff in OTA stocks, driven by fears that AI agents from Google and OpenAI could bypass traditional booking platforms entirely, illustrates how seriously the market takes this risk.

Regulatory scrutiny in Europe is intensifying. The European Commission designated Booking.com as a "gatekeeper" under the Digital Markets Act in May 2024, placing it alongside Alphabet, Amazon, Apple, ByteDance, Meta, and Microsoft. Compliance obligations include allowing hotels to offer better prices on other channels and providing data portability. Non-compliance could result in fines up to 10 percent of worldwide turnover, or 20 percent for repeat violations. Additionally, over 15,000 European hotels have joined a class-action lawsuit alleging that Booking.com's now-banned rate parity clauses violated EU competition law, with claims potentially exceeding 8 billion euros. The EU has also initiated scrutiny under the Digital Services Act, assessing Booking.com's efforts to combat online financial fraud and fake listings.

Marketing dependency remains a structural concern. While performance marketing is highly efficient, the sheer scale of spending, roughly $7 billion annually, creates a structural dependence on paid channels that constrains margin expansion and leaves the company vulnerable to cost increases in the digital advertising ecosystem.

Airbnb's brand strength with younger travelers represents a long-term competitive threat. While Booking.com has made significant progress in alternative accommodations, Airbnb retains the stronger brand association with unique, experience-driven travel among millennial and Gen Z consumers. If travel preferences continue to shift toward experiences over traditional accommodations, Airbnb's brand advantage could translate into sustained market share gains in the highest-growth segments.

Finally, AI disruption from new entrants could reshape the competitive landscape in unpredictable ways. If generative AI enables new interfaces that aggregate and book travel without sending users to traditional OTA platforms, the value of Booking.com's hard-won SEO and SEM advantages could erode. The company is investing aggressively to be on the right side of this shift, but the outcome is uncertain.

XII. Epilogue: What Would Geert-Jan Bruinsma Think?

In 1996, a young Dutch graduate set up a server under his desk and built a website that let people book hotel rooms in the Netherlands. He did not have a grand vision for conquering global travel. He did not have venture capital, a board of directors, or a team of Stanford-educated engineers. He had an internet connection, a suggestion from his former internship supervisor, and the pragmatic Dutch instinct for commerce.

Three decades later, the company that grew from that server under a desk is the world's largest online travel platform. Booking.com operates in over 220 countries, in 43 languages, with 28 million listings. Its parent company generates nearly $27 billion in annual revenue and ranks among the most profitable internet companies on earth. The stock, adjusted for the upcoming 25-for-1 split, has returned thousands of percent since its post-crash lows, making it one of the greatest comeback stories in stock market history.

The trajectory from Bookings.nl to Booking Holdings is one of the great emergent strategies in business history. It was not planned by a visionary founder with a PowerPoint deck. It emerged from a series of decisions, some brilliant, some lucky, and some that seemed insignificant at the time, that compounded over decades. A student builds a booking website. A dot-com survivor bets on Europe. A deal scout with high integrity finds a company nobody else wants. An acquiring parent makes the counterintuitive choice to step back and let its acquisition run itself. A culture of relentless testing turns a commission-based marketplace into a data machine. And the whole thing compounds, year after year, because the incentives are aligned at every level.

The mission of Booking Holdings today is "to make it easier for everyone to experience the world." It is a lofty statement that could sound hollow from a lesser company. But when you trace the history, from Jay Walker's bidding experiments to Geert-Jan Bruinsma's server under a desk to Glenn Fogel's AI-powered Connected Trip, it describes a genuine through line: the ongoing effort to reduce friction between people and the places they want to go.

Whether Booking Holdings can maintain its dominance in the AI era remains an open question. Google, OpenAI, and a generation of AI-native startups are building tools that could fundamentally change how travelers discover and book their trips. The regulatory environment in Europe is tightening. The competitive landscape continues to evolve.

But consider the arc of the company's history. It survived the dot-com crash when most of its peers did not. It built a global travel empire not through the brute force of Silicon Valley capital but through the quiet, methodical cultivation of relationships with millions of hoteliers. It navigated a pandemic that reduced its business by 91 percent in a single quarter and emerged stronger than before. At every inflection point, the company found a way to adapt, not because it had the best strategy document, but because it had built a culture and a system that was capable of learning and evolving faster than the competition.

The company enters this next chapter with advantages that took decades to build: the largest accommodation inventory in the world, a two-sided marketplace with powerful network effects, a culture of data-driven execution, and the financial resources to invest billions in the future while returning billions to shareholders.

The ultimate lesson of Booking Holdings is not about travel, or technology, or even about making smart acquisitions. It is about what happens when incentives align: when a platform makes money only when its partners make money, when an acquiring company has the discipline to let its best asset run independently, when a culture prizes data over opinion, and when patient capital gives compounding the time it needs to work.

Great businesses are not always built by visionaries with grand plans. Sometimes they are built by pragmatists with good instincts, operating in fragmented markets, making one small, smart decision at a time. Sometimes the best empires are the accidental ones.

XIII. Recent News

Booking Holdings reported fourth-quarter 2025 results on February 18, 2026, posting revenue of $6.35 billion, up 16.1 percent year-over-year and above analyst consensus. Full-year 2025 revenue reached $26.9 billion, with adjusted EBITDA of $9.9 billion representing a 36.9 percent margin. Room nights for the fourth quarter grew 9 percent, while gross bookings rose 16 percent to $43 billion.

The company announced a 25-for-1 stock split, the first in its history, set to take effect on April 2, 2026, with split-adjusted trading beginning April 6. The board also declared a quarterly cash dividend of $10.50 per share, a 9.4 percent increase from the prior level of $9.60.

On the leadership front, KAYAK appointed Peer Bueller as CEO in February 2026, with co-founder Steve Hafner transitioning to executive chair and a new role leading AI innovation initiatives across Booking Holdings. Chief Accounting Officer Susana D'Emic announced plans to retire at the end of March 2027.

Regulatory developments continue to shape the landscape. The European Commission's September 2023 decision to block Booking Holdings' acquisition of eTraveli Group remains under appeal, with a ruling expected in 2026. Under the Digital Markets Act, Booking.com enacted compliance changes including the removal of parity requirements in July 2025. The EU also initiated scrutiny under the Digital Services Act in September 2025. Meanwhile, the class-action lawsuit brought by over 15,000 European hotels over allegedly anticompetitive rate parity clauses moved to substantive hearings in late 2025, with full legal arguments expected in 2026.

Despite strong operating results, Booking Holdings shares experienced significant pressure in early 2026, falling approximately 24 percent in February alone to 16-month lows. The primary driver was investor concern about AI disruption, particularly the possibility that generative AI tools from Google and OpenAI could disintermediate traditional online travel platforms by enabling users to plan and book travel through conversational AI agents that bypass OTA search interfaces entirely.

Additional pressure came from the company's announcement of $700 million in incremental 2026 investments, which compressed near-term margin expectations. For 2026, management has guided for first-quarter revenue growth of 14 to 16 percent and full-year constant-currency revenue growth in the low double digits, with adjusted EBITDA growth expected to outpace revenue and adjusted EPS growth in the mid-teens.

XIV. Links & References

SEC Filings and Investor Presentations: - Booking Holdings SEC filings via EDGAR (CIK: 1075531) - Q4 2025 Earnings Release (February 18, 2026) - Q4 2024 Earnings Release - Annual Report (Form 10-K) for fiscal years 2024 and 2025

Key Interviews and Leadership: - Glenn Fogel, Fortune 2024 CEO of the Year profile - Glenn Fogel, Yale Legend in Leadership Award (2025) - Skift Oral History of the Booking.com Acquisition - Andy Phillipps, Stanford Digital Cities Initiative fellowship profile

Acquisitions and Corporate History: - Priceline.com acquisition of Active Hotels press release (September 21, 2004) - Priceline.com acquisition of Bookings B.V. press release (July 14, 2005) - Priceline.com acquisition of Agoda press release (November 2007) - Booking Holdings corporate history page (bookingholdings.com/about/history) - Booking.com "Our Story" (news.booking.com/our-story)

Founding Stories: - Geert-Jan Bruinsma profile, University of Twente Alumni - Jay S. Walker biography via EBSCO and Lemelson-MIT - FundingUniverse company history of Priceline.com Incorporated

Industry Reports and Analysis: - PhocusWire analysis of online travel marketing spend (2024) - Skift research on OTA market share trends - European Commission Digital Markets Act gatekeeper designation (May 2024) - European Commission decision blocking eTraveli acquisition (September 2023)

Media Coverage: - Fortune, "How Jeffery Boyd Took Priceline from Dot-Bomb to High-Flier" (2012) - CBS News, "The Rise and Fall and Rise of Priceline.com" - Travel Weekly, Shatner retrospective on 20 years as Priceline pitchman - PhocusWire, "Why Priceline's Purchase of Booking.com Was the Most Profitable Travel Deal of the 2000s"

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube