BNY Mellon: The American Financial System's Foundation

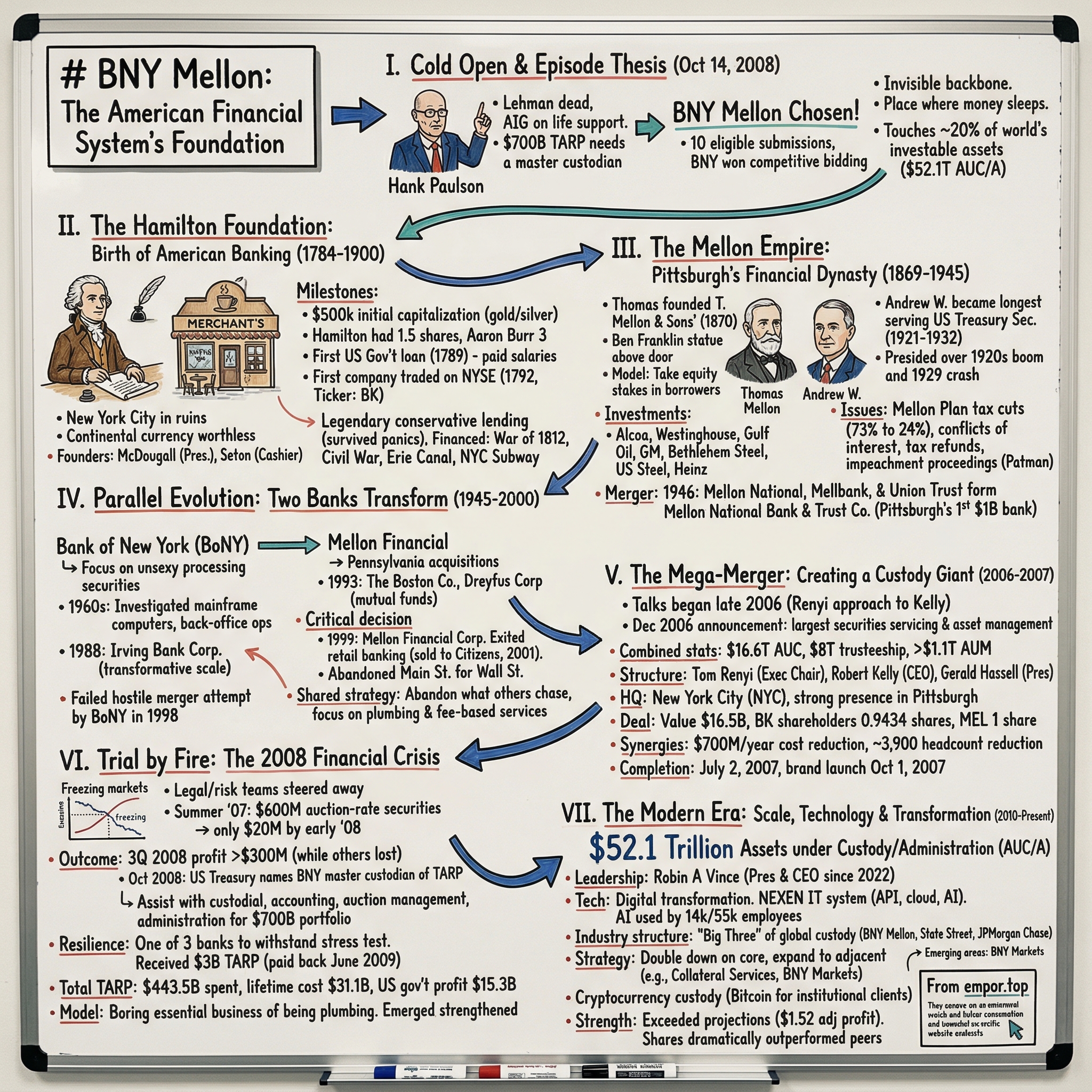

I. Cold Open & Episode Thesis

The date is October 14, 2008. Lehman Brothers has been dead for a month. AIG is on government life support. Morgan Stanley and Goldman Sachs have just converted to bank holding companies to avoid collapse. In Washington, Treasury Secretary Hank Paulson is orchestrating the largest financial rescue in American history—the $700 billion Troubled Asset Relief Program. But who would actually handle the money? Who could be trusted to custody, track, and distribute hundreds of billions in taxpayer funds during the worst financial panic since the Great Depression?

The answer came through a competitive bidding process that almost nobody noticed: Bank of New York Mellon, a company that had existed in its current form for barely fifteen months. While household names like Citigroup and Bank of America were taking emergency capital injections, BNY Mellon was quietly chosen as the master custodian for TARP—the institution that would literally hold America's financial rescue in its vaults.

Here's the provocative question that should keep every investor up at night: How did a bank founded by Alexander Hamilton in a Wall Street coffeehouse become the invisible backbone of global finance? How does a company that most people have never heard of touch nearly 20% of the world's investable assets—over $50 trillion—every single day?

The answer isn't just about scale or longevity. It's about building the most boring, essential business in finance: being the place where money sleeps. BNY Mellon doesn't make headlines for trading profits or consumer banking innovations. It makes money by being the trusted intermediary for everyone else's money—from pension funds to sovereign wealth funds, from mutual funds to central banks. It's the financial equivalent of owning the pipes in a gold rush while everyone else digs for gold. This is a story of invisible power. While Lehman Brothers and Bear Stearns made headlines for their spectacular collapses, while AIG became a punchline for taxpayer bailouts, BNY Mellon quietly became the master custodian of the government's Troubled Asset Relief Program (TARP) during the 2008 financial crisis. The Treasury had received 70 submissions for the role, but only 10 met the eligibility requirements—and BNY Mellon won through competitive bidding to assist with custodial, accounting, auction management and other administration duties for the $700 billion portfolio.

What we're about to explore is how this 240-year-old institution—one that literally helped create the American financial system—built the most essential and boring business in global finance. Today, BNY has $2.1 trillion in assets under management and $52.1 trillion in assets under custody and administration, making it the first bank to surpass $50 trillion. The company touches nearly 20% of the world's investable assets.

This isn't a story about trading prowess or consumer banking innovation. It's about becoming the ultimate trust business—the place where the world's money sleeps at night. From Alexander Hamilton's founding vision to serving over 90% of Fortune 100 companies, from surviving every American financial panic to becoming the backbone of global capital markets, BNY Mellon represents something unique: a company that wins by being essential infrastructure rather than seeking glory.

Let's begin where all great American financial stories begin—with Alexander Hamilton and a group of merchants meeting in a Wall Street coffeehouse, trying to build a nation from scratch.

II. The Hamilton Foundation: Birth of American Banking (1784–1900)

Picture New York City in February 1784. The British have evacuated just three months earlier. The city is in ruins—literally. A quarter of Manhattan has been destroyed by fire during the seven-year occupation. Commerce is dead. The Continental currency is worthless—"not worth a Continental" has become the phrase of the day. Into this chaos steps Alexander Hamilton, just 27 years old, with an audacious idea: create a bank that would resurrect New York's economy and, by extension, help birth American capitalism itself. On February 23, 1784, Hamilton convened a meeting at the Merchant's Coffee House on the corner of Wall and Water Streets. The shipping industry in New York City chafed under the lack of a bank, and investors envied the 14% dividends that Bank of North America paid, and months of local discussion culminated in a June 1784 meeting at a coffee house on St. George's Square which led to the formation of the Bank of New York company. The group that gathered included some of New York's most prominent merchants—men who had survived the war but now faced economic ruin without access to credit or stable currency.

Hamilton didn't just found a bank; he wrote its constitution—a document so revolutionary in its governance structure that it would serve as the template for American banking for the next century. Hamilton authored its pioneering constitution, which would serve as a model for banks established in later years across the country. The constitution established clear voting rights based on shareholdings, mechanisms for removing corrupt directors, and strict penalties for embezzlement—innovations that seem obvious today but were radical for the time.

The initial capitalization target was ambitious: $500,000 in gold or silver. The initial plan was to capitalize the company with $750,000, a third in cash and the rest in mortgages, but after this was disputed the first offering was to capitalize it with $500,000 in gold or silver. When the bank opened on June 9, 1784, the full $500,000 had not been raised; 723 shares had been sold, held by 192 people. Among the shareholders: Aaron Burr had three of them, and Hamilton had one and a half shares. Yes, the man who would later kill Hamilton in a duel was an early investor—Wall Street has always made for strange bedfellows.

The bank's first president was Alexander McDougall, a Revolutionary War general, with William Seton serving as cashier. The first president was Alexander McDougall and the Cashier was William Seton. Its first offices were in the old Walton Mansion in New York City. But the real power was Hamilton, who understood something fundamental: a nation without credit cannot grow, and credit requires trust, and trust requires institutions.

The Bank of New York's early days read like a financial thriller. Operating without a state charter for its first seven years—essentially as a rogue financial institution—it nonetheless became the mechanism through which American capitalism would be born. The bank provided the United States government its first loan in 1789. The loan was orchestrated by Hamilton, then Secretary of the Treasury, and it paid the salaries of United States Congress members and President George Washington. Think about that: the federal government's first loan came from a bank that technically wasn't even legally chartered yet. In 1792, when the New York Stock Exchange was founded with the signing of the Buttonwood Agreement under a sycamore tree at 68 Wall Street, The Bank of New York was the first company to be traded on the New York Stock Exchange when it first opened in 1792. The first stock traded on the exchange was that of Hamilton's Bank of New York, whose ticker symbol BK continues as it was then. Think about that legacy: the same ticker symbol, representing the same institution, for over 230 years.

But Hamilton's bank wasn't just about making money—it was about building a nation. Perhaps the Bank of New York's most critical role at the turn of the 19th century was to stabilize currency by displaying exchange rates for the myriad types of money still in use during the republic's early years. In an era when Spanish doubloons, British pounds, and dozens of other currencies circulated alongside worthless Continental paper, the Bank of New York became the arbiter of value, the institution that told merchants what their money was actually worth.

The bank's conservative lending practices became legendary. During the 19th century, the bank was known for its conservative lending practices that allowed it to weather financial crises. While other banks failed in the Panic of 1837, the Panic of 1857, the Panic of 1873, and the Panic of 1893, the Bank of New York survived them all. This wasn't luck—it was discipline. The bank's directors, following Hamilton's original constitution, maintained higher capital ratios and more conservative lending standards than their competitors. But the Bank of New York's real genius was in financing the infrastructure that would transform America from a collection of coastal settlements into a continental power. It was involved in the funding of the Morris and Erie canals, and steamboat companies. When DeWitt Clinton needed $7 million to build the Erie Canal in 1817—a project Thomas Jefferson had dismissed as "madness"—the Bank of New York was there. Among the investors in the canal bonds was another pet project of De Witt Clinton, the Bank for Savings in the City of New York. This was a bank created to encourage thrift among poorer savers; it bought $263,000 in canal bonds in 1820. By 1821, it held almost 30% of the canal bonds outstanding.

The Erie Canal transformed American commerce, reducing shipping time from New York to Buffalo from three weeks to eight days and dropping costs from $90 to $4 per ton. The Bank of New York didn't just lend money; it created the financial architecture that made such projects possible. The bank helped finance both the War of 1812 and the Union Army during the American Civil War. Following the Civil War, the bank loaned money to many major infrastructure projects, including utilities, railroads, and the New York City Subway.

By 1900, the Bank of New York had survived and thrived through every American financial panic, had helped finance two wars, and had funded the infrastructure that connected a continent. The bank continued to profit and pay dividends throughout the Great Depression, and its total deposits increased during the decade. But as we'll see, another financial dynasty was rising in Pittsburgh—one that would ultimately merge with Hamilton's bank to create the modern custody giant.

III. The Mellon Empire: Pittsburgh's Financial Dynasty (1869–1945)

If the Bank of New York represented East Coast establishment banking—conservative, steady, institutional—then the Mellon empire was its opposite: aggressive, entrepreneurial, and intimately tied to the industrial transformation of America. Picture Thomas Mellon in 1869, a retired judge in Pittsburgh who had accumulated wealth through real estate and lending, deciding at age 56 to formalize his banking operations. While Hamilton's bank served merchants and government, Mellon would serve industrialists and innovators. Thomas Mellon founded T. Mellon & Sons' Bank on January 2, 1870, with his sons Andrew W. and Richard B. Above the cast iron door of the original bank building at 145 Smithfield Street was placed a near life-sized statue of his inspiration, Benjamin Franklin. This wasn't just ornamentation—it was a statement of philosophy. Like Franklin, Mellon believed in self-improvement through industry and thrift, but unlike Franklin's public-spirited approach, the Mellons would perfect the art of using other people's companies to build their fortune.

The genius of the Mellon model was that they didn't just lend money—they took equity stakes in their borrowers. When Henry Clay Frick needed capital for his coke ovens in 1871, the Mellons provided a $10,000 loan that would become the foundation of an industrial empire. Shrewd investments included real estate holdings in downtown Pittsburgh, coal fields, and a $10,000 loan to Henry Clay Frick in 1871, which would provide the coke for Andrew Carnegie's steel mills. The scale of what the Mellons built is staggering. The bank invested in and helped found numerous industrial firms in the late 1800s and early 1900s including Alcoa, Westinghouse, Gulf Oil, General Motors and Bethlehem Steel. Both Gulf Oil and Alcoa are, according to the financial media, considered to be T. Mellon & Sons' most successful financial investments. U.S. Steel (the world's first billion-dollar corporation), Heinz, General Motors, Koppers and ExxonMobil (as Rockefeller's Standard Oil) were born and nurtured by Mellon.

Consider the aluminum story. In 1889, when the Pittsburgh Reduction Company (later Alcoa) was struggling to commercialize a new process for producing aluminum, Andrew Mellon didn't just provide the requested $4,000 loan. Mellon agreed to loan $25,000 to the Pittsburgh Reduction Company, a fledgling operation seeking to become the first successful industrial producer of aluminum. He took board seats, provided ongoing capital, and essentially built the global aluminum industry from scratch. By 1907 it was renamed Alcoa and would dominate global aluminum production for decades.

The Gulf Oil story is even more dramatic. When Texas wildcatter James Guffey struck massive oil deposits at Spindletop in 1901, he needed capital to build the infrastructure to extract and refine it. The Mellons provided the money but also took control. The Mellons later removed Guffey as the head of his company, and in 1907 they reorganized the Guffey Company as Gulf Oil and installed William Larimer Mellon Sr. (a son of Andrew Mellon's older brother, James Ross Mellon) as the head of Gulf Oil. Andrew, Dick and W.L. held 70 percent of the stock in the still-private Gulf Oil Company, the largest company ever to come out of Pittsburgh.

In 1882, Thomas turned over full ownership of the bank to his son Andrew. On January 5, 1882, he retired from day-to-day management of the bank's affairs, handing it to his 26-year-old son, Andrew. Under A.W. and R.B.'s management, Mellon Bank was by the end of the century the largest banking institution in the country outside of New York. In 1902, T. Mellon & Sons' name was changed to the Mellon National Bank. But Andrew Mellon's most consequential role was yet to come. In 1920, Andrew left his leadership post of the bank to become the longest serving U.S. Treasury Secretary in history (serving under three separate administrations). He served as United States Secretary of the Treasury from March 9, 1921, to February 12, 1932, presiding over the boom years of the 1920s and the Wall Street Crash of 1929. One admiring congressman referred to Mellon as the "greatest Secretary of the Treasury since Alexander Hamilton."

The irony is perfect: the man whose bank Hamilton founded would be succeeded at Treasury by the man whose bank would eventually merge with Hamilton's creation. But where Hamilton used government power to build financial infrastructure, Mellon used it to enrich the already wealthy. His tax reform scheme, known as the Mellon Plan, reduced taxes for business. The top marginal tax rate fell from 73 percent in 1922 to 24 percent in 1929.

More troubling were the conflicts of interest. Mellon had, as treasury secretary and thus boss of the Bureau of Internal Revenue, given his own companies tax refunds. He held bank stocks while serving as chair of the Federal Reserve. He also owned a massive distillery while enforcing Prohibition, and illegally traded with the Soviet Union. He blocked antitrust action against Alcoa. The FTC didn't bother to look into Gulf Oil, or any of Mellon's other vast holdings.

In early 1932, Congressman Wright Patman of Texas initiated impeachment proceedings against Mellon, contending that Mellon had violated numerous federal laws designed to prevent conflicts of interest. Hoover removed Mellon from Washington by offering him the position of ambassador to the United Kingdom. The Great Depression had destroyed Mellon's reputation, but not his bank.

In 1946, Mellon National, Mellbank, and the Union Trust Company merged to form Mellon National Bank and Trust Company, and was Pittsburgh's first US$1 billion bank. The Mellon empire had survived its founder's disgrace, the Great Depression, and World War II. As we entered the post-war era, both the Bank of New York and Mellon National Bank would begin transformations that would ultimately bring them together.

IV. Parallel Evolution: Two Banks Transform (1945–2000)

The post-World War II era should have been disastrous for both banks. The rise of money center banks like Chase Manhattan and Citibank, the emergence of regional banking powerhouses, and the technological revolution in finance all threatened to make these two historic institutions irrelevant. Instead, both banks made the same counterintuitive bet: abandon what everyone else was chasing and focus on what nobody wanted to do.

For the Bank of New York, the transformation began in the 1960s when the bank started to realize that its future lay not in competing for corporate loans or retail deposits, but in the unsexy business of processing securities. While other banks were building branch networks and chasing consumers, Bank of New York was investing in mainframe computers and building the infrastructure to handle the back-office operations that other banks considered beneath them. The 1988 acquisition of Irving Bank Corporation was transformative. The vigorous expansion was marked especially by the 1988 takeover of the giant Irving Bank Corporation (founded 1851). This gave Bank of New York the scale and capital to compete in the custody business globally. By the 1990s, the bank was making acquisitions at a dizzying pace—33 acquisitions from 1993 to 1998 alone.

The genius of this strategy was that as trading volumes exploded and financial markets became more complex, somebody had to handle the back office. Every mutual fund needed a custodian. Every pension fund needed someone to process trades, handle foreign exchange, and manage securities lending. The Bank of New York positioned itself as that somebody.

Meanwhile, in Pittsburgh, Mellon was undergoing its own transformation, though it took a different path to the same destination. Mellon Bank acquired multiple banks and financial institutions in Pennsylvania during the 1980s and 1990s. In 1992, Mellon acquired 54 branch offices of Philadelphia Savings Fund Society, the first savings bank in the United States, founded in 1819. In 1993, Mellon acquired The Boston Company from American Express and AFCO Credit Corporation from The Continental Corporation. The following year, Mellon merged with the Dreyfus Corporation, bringing its mutual funds under its umbrella.

The critical decision came in 1999, when Mellon Bank Corporation became Mellon Financial Corporation. Two years later, it exited the retail banking business by selling its assets and retail bank branches to Citizens Financial Group. This was a shocking move—a bank founded to serve the steel workers and industrialists of Pittsburgh was abandoning Main Street entirely to focus on Wall Street.

Both banks had discovered the same truth: in modern finance, the real money wasn't in taking deposits and making loans. It was in the plumbing—the unsexy, complex, technology-intensive business of moving money and securities around the global financial system. While other banks chased glamorous investment banking deals or built retail branch networks, Bank of New York and Mellon built the infrastructure that made everyone else's business possible. Ironically, the two banks had tried to merge once before—and failed spectacularly. In 1998, Bank of New York made an unsolicited $24 billion bid for Mellon that turned hostile. That year, the bank made an unsolicited $24 billion bid for competitor Mellon Bank Corp. The proposal was dropped, however, when the Mellon board rejected the offer, claiming they did not have confidence in Renyi as a leader. The Pittsburgh establishment rallied around Mellon, and the deal collapsed in acrimony.

But by 2006, the logic of combination had become overwhelming. Both banks had transformed themselves into custody and asset management specialists. Both had abandoned traditional banking for fee-based services. And both faced the same competitive pressures from State Street and JPMorgan Chase. These two companies, along with State Street, followed essentially the same evolution. All were originally large diversified financial service providers, particularly in the corporate banking space in the regions they were located in. However, competition in the corporate loans and retail banking businesses saw them jettison these operations in favor of what were believed to be more stable, fee based business.

The stage was set for one of the most consequential mergers in financial history—one that would create the world's largest custody bank just in time for the greatest financial crisis since the Great Depression.

V. The Mega-Merger: Creating a Custody Giant (2006–2007)

The phone call that would create the modern BNY Mellon came in late 2006, but not from where you'd expect. Talks began when Tom Renyi approached Robert Kelly about a possible amalgamation between the Bank of New York and Mellon Financial Corporation. This time, it wasn't hostile. This time, both sides knew they needed each other.

Robert Kelly, who had become CEO of Mellon in February 2006, was a different breed from the Pittsburgh banking establishment that had rejected Bank of New York eight years earlier. A former CFO of Wachovia, Kelly understood that scale was destiny in the custody business. Every basis point mattered when you were competing for trillion-dollar mandates. Technology investments that cost hundreds of millions could only be justified with massive scale.

The December 2006 announcement came at a fascinating time in financial history. The Bank of New York Company, Inc. (NYSE: BK) and Mellon Financial Corporation (NYSE: MEL) announced on December 4, 2006, they had entered into a definitive agreement to merge, creating the largest securities servicing and asset management firm globally. The new company would be the world's leading asset servicer with $16.6 trillion in assets under custody and corporate trustee with $8 trillion in assets under trusteeship, and would rank among the top 10 global asset managers with more than $1.1 trillion in assets under management.

The governance structure revealed a carefully negotiated balance of power. Thomas A. Renyi, currently chairman and chief executive of The Bank of New York, would serve as executive chairman of The Bank of New York Mellon Corporation for 18 months following the close of the transaction with overall responsibility for the integration of the two companies. Robert P. Kelly, currently president, chairman and chief executive officer of Mellon, would serve as chief executive officer of the new company and would succeed Mr. Renyi as chairman of the board. Gerald L. Hassell, currently president of The Bank of New York, would hold the same position in the new company.

The board composition reflected the merger of equals narrative: The board of directors would comprise 10 members designated by The Bank of New York and eight members designated by Mellon. Meanwhile, the headquarters decision showed New York's dominance: The new company's headquarters would be based in New York City while maintaining a strong and growing presence in Pittsburgh.

The financial engineering of the deal was precise. The deal was valued at $16.5 billion and under its terms, the Bank of New York's shareholders received 0.9434 shares in the new company for each share of the Bank of New York that they owned, while Mellon Financial shareholders received 1 share in the new company for each Mellon share they owned. This exchange ratio effectively gave Bank of New York shareholders a slight majority stake in the combined entity.

What made this merger particularly compelling was the projected synergies. The companies expected to reduce total pre-tax costs by approximately $700 million per year, or approximately 8.5% of the estimated 2006 combined expense base. The integration would be undertaken by a dedicated and experienced group of senior executives in a thoughtful and deliberate manner over a three year period following the close of the transaction. The transaction would involve restructuring charges of approximately $1.3 billion. The companies combined employee base of 40,000 was expected to be reduced by approximately 3,900 over a three-year period following the transaction.

The timing couldn't have been more critical. After regulatory and shareholder approval, the banks completed the merger on July 2, 2007. The new entity launched just as the subprime mortgage crisis was beginning to metastasize into a full-blown financial catastrophe. The new venture launched its brand identity on October 1, 2007.

VI. Trial by Fire: The 2008 Financial Crisis

The newly merged BNY Mellon faced its baptism by fire almost immediately. While other banks were loading up on subprime mortgages and complex derivatives, BNY Mellon's legal and risk management teams were quietly steering the bank away from disaster. In the summer of 2007, the bank held $600 million worth of auction-rate securities. By the time the market froze in early 2008, a cautious BNY Mellon held only $20 million worth.

This wasn't luck—it was discipline. The bank's conservative DNA, inherited from both Hamilton's Bank of New York and the Mellon empire's survival through the Great Depression, served it well. The bank ended the third quarter of 2008 with a profit of more than $300 million, despite a write-off of more than twice that sum—while other financial institutions posted huge losses.

Then came the call that would define BNY Mellon's role in the crisis. Last October the U.S. Department of the Treasury chose BNY Mellon as the sole provider of a broad range of custodial and trustee services for the government's bailout plan, called the Troubled Asset Relief Program (TARP). In October 2008, the U.S. Treasury named BNY Mellon the master custodian of the Troubled Asset Relief Program (TARP) bailout fund during the 2008 financial crisis.

The selection process was rigorous. The Treasury had received 70 submissions for the role, but only 10 met the eligibility requirements. BNY Mellon won through competitive bidding, beating out rivals to manage what would become the most important financial rescue program in American history. President George W. Bush signed the bill into law within hours of its congressional enactment, creating the $700 billion Troubled Asset Relief Program (TARP) to purchase failing bank assets.

What's remarkable is that BNY Mellon wasn't just surviving the crisis—it was one of the few banks strong enough to help solve it. According to the results of a February 2009 stress test conducted by federal regulators, BNY Mellon was one of only three banks that could withstand a worsening economic situation. The other major banks were taking massive TARP injections just to stay alive. The banks agreeing to receive preferred stock investments from the Treasury include Goldman Sachs, Morgan Stanley, JPMorgan Chase, Bank of America (which had just agreed to purchase Merrill Lynch), Citigroup, Wells Fargo, Bank of New York Mellon and State Street Corporation. The Bank of New York Mellon is to serve as master custodian overseeing the fund.

BNY Mellon did receive TARP funds—not because it needed them, but because regulators wanted all major banks to participate to avoid stigmatizing the truly desperate institutions. The company received $3 billion from TARP, which it paid back in full in June 2009, along with US$136 million to buy back warrants from the Treasury in August 2009. This made BNY Mellon one of the first banks to fully exit TARP, signaling its financial strength.

The crisis revealed something fundamental about BNY Mellon's business model. While investment banks were collapsing from proprietary trading losses and commercial banks were drowning in bad loans, custody banks like BNY Mellon continued collecting fees for moving and safeguarding other people's money. The bank provides financial services for a fee to institutions, corporations, pension funds, endowments, and wealthy individuals. It is the largest U.S. corporate trustee, and offers other services, such as handling payrolls, stock transfers, closings and foreign exchange.

The TARP custodian role was particularly complex. BNY Mellon had to track hundreds of billions in government investments across hundreds of financial institutions, manage the unwinding of complex securities, and provide transparency to Congress and the public about where taxpayer money was going. It was the ultimate test of the bank's operational capabilities—and it passed with flying colors.

By the time the dust settled, TARP had disbursed $443.5 billion and ultimately cost taxpayers $31.1 billion after all repayments and profits. As of September 30, 2023, when all TARP-funded programs were fully wrapped up, the total amount spent was $443.5 billion. After repayments, sales, dividends, interest, and other income, the lifetime cost of TARP-funded programs was $31.1 billion. Through the Treasury, the U.S. government actually booked $15.3 billion in profit, as it earned $441.7 billion on the $426.4 billion invested.

The crisis fundamentally validated BNY Mellon's strategy. While others chased higher returns through proprietary trading and subprime lending, BNY Mellon stuck to its boring, essential business of being the plumbing of global finance. It emerged from the crisis not just intact but strengthened, with competitors weakened and clients more aware than ever of the importance of choosing a stable custodian.

VII. The Modern Era: Scale, Technology & Transformation (2010–Present)

The post-crisis decade transformed BNY Mellon from a custody bank into something more profound: the operating system of global finance. The numbers tell the story of unprecedented scale. BNY Mellon has become the first bank in history to surpass $50 trillion in assets under custody and administration. BNY Mellon's total assets under custody and/or administration reached $52.1 trillion. To put that in perspective, that's more than twice the GDP of the United States and represents nearly 20% of the world's investable assets.

The leadership transitions reflected the bank's evolution. Charles W. Scharf was appointed CEO in July 2017 and became Chairman after former CEO and chairman Gerald Hassell retired at the end of 2017. Hassell had been Chairman and CEO since 2011, after serving as BNY Mellon's president from 2007 to 2012 and as the president of the Bank of New York from 1998 until its merger. Scharf stepped down in 2019 to become the new CEO of Wells Fargo. Thomas "Todd" Gibbons served as BNY Mellon's CEO from 2020 to 2022. Robin A. Vince was appointed president and CEO in August 2022, succeeding Gibbons.

Under Robin Vince's leadership, the bank has embraced a radical digital transformation. In 2013, the bank started building a new IT system called NEXEN. NEXEN uses open source technology and includes components such as an API store, data analytics, and a cloud computing environment. The bank's proprietary artificial intelligence is already being used by 14,000 of its 55,000 employees, fundamentally changing how custody and asset servicing work.

The competitive landscape has intensified but also clarified. BNY Mellon, State Street, and JPMorgan Chase have emerged as the "Big Three" of global custody, with Northern Trust as a distant fourth. Together, these firms control the vast majority of institutional custody assets globally. The barriers to entry have become almost insurmountable—the technology investment alone requires billions of dollars, and the regulatory requirements post-2008 make it nearly impossible for new entrants to achieve the necessary scale.

BNY Mellon's response has been to double down on what it does best while expanding into adjacent businesses. In June 2014, the company combined its global markets, global collateral services and prime services to create the new Markets Group, also known as BNY Markets. This division has become crucial as collateral management and securities lending have grown in importance post-crisis.

The asset management side has seen its own transformation. BNY Investments manages nearly $2 trillion in assets through a multi-boutique model that includes Newton, Insight Investment, and Mellon Investments. While not as large as BlackRock or Vanguard, BNY's asset management benefits from unique synergies with its custody business—it can see flow patterns and market trends that pure asset managers cannot.

Technology disruption remains both a threat and an opportunity. Blockchain technology promises to revolutionize custody and settlement, potentially eliminating the need for traditional intermediaries. BNY Mellon has responded by becoming one of the most aggressive traditional banks in exploring digital assets. The bank was among the first major custodians to announce plans to custody Bitcoin and other cryptocurrencies for institutional clients, recognizing that digital assets are becoming a permanent part of the investment landscape.

The regulatory environment has become increasingly complex. BNY Mellon is designated as a Global Systemically Important Bank (G-SIB), subjecting it to the highest levels of capital requirements and regulatory scrutiny. In the results of the Federal Reserve's Dodd-Frank stress test in 2013, the bank was least affected by hypothetical extreme economic scenarios among banks tested. It was also a top performer on the same test in 2014.

Recent performance has been exceptional. The bank exceeded Wall Street's projection of $1.42 per share by reporting an adjusted profit of $1.52. The assets under custody and administration were $52.1 trillion, a 14% increase from the previous year. The stock market has noticed: BNY's shares have dramatically outperformed peers, reflecting investor confidence in the stability and growth potential of the custody model.

VIII. Business Model Deep Dive: The Custody Banking Playbook

To understand BNY Mellon's power, you need to understand what custody actually means in modern finance. At its core, custody is about safekeeping assets, but that dramatically understates the complexity. When a pension fund buys Japanese government bonds, someone needs to handle the foreign exchange, ensure the trade settles correctly, collect the interest payments, handle tax withholding, manage corporate actions, and report all of this to regulators in multiple jurisdictions. That someone is BNY Mellon.

The revenue model is elegantly simple but operationally complex. Custody fees are typically charged as basis points on assets under custody—perhaps 1-5 basis points for a large institutional client. On $52 trillion, even a few basis points generates billions in revenue. But that's just the beginning. The real money comes from the ancillary services that clients need once their assets are in custody.

Securities lending is a perfect example. BNY Mellon holds trillions in securities that are just sitting there. The bank can lend these securities to short sellers and other market participants, splitting the lending fees with the asset owner. In a world of complex derivatives and hedging strategies, securities lending has become a multi-billion dollar business.

Foreign exchange is another massive revenue generator. When that pension fund buys those Japanese bonds, someone needs to convert dollars to yen. When a European mutual fund receives dividends from American stocks, someone needs to convert dollars to euros. BNY Mellon handles trillions in foreign exchange transactions annually, earning spreads on each trade.

Cash management adds another layer. Institutional investors always have cash sitting in their accounts—proceeds from sales waiting to be reinvested, dividend payments accumulating, collateral for derivatives positions. BNY Mellon sweeps this cash into money market funds or other short-term investments, earning fees or spreads on the float.

The network effects are powerful. The more assets BNY Mellon custodies, the more securities it can lend. The more foreign exchange it handles, the better pricing it can offer. The more clients it serves, the more valuable its data becomes for analytics and risk management services. It's a virtuous cycle that becomes increasingly difficult for competitors to break.

The switching costs are enormous. Moving custody is not like switching checking accounts. It involves re-papering thousands of legal agreements, updating systems at hundreds of counterparties, retraining staff, and accepting massive operational risk during the transition. Once a large institution chooses BNY Mellon as custodian, they rarely leave.

Technology is both the moat and the investment sink. BNY Mellon spends billions annually on technology—not on flashy consumer apps or trading algorithms, but on the boring, essential systems that ensure trades settle correctly, assets are properly segregated, and reports are delivered accurately. This technology stack, built over decades and constantly updated, would cost tens of billions to replicate from scratch.

The trust factor cannot be underestimated. When sovereign wealth funds and central banks need a custodian for their reserves, they don't choose based on price. They choose based on the confidence that their assets will be there tomorrow, next year, and next decade. BNY Mellon's 240-year history, survival through every American financial crisis, and role as TARP custodian during 2008 make it the ultimate "sleep at night" choice for risk-averse institutions.

IX. Power Dynamics & Industry Structure

The global custody industry represents one of the most concentrated sectors in finance. Three firms—BNY Mellon, State Street, and JPMorgan Chase—control the vast majority of institutional custody assets globally. This concentration isn't an accident; it's the inevitable result of massive economies of scale and network effects.

BNY Mellon's client list reads like a who's who of global finance. The bank serves over 90% of Fortune 100 companies, either through custody, asset management, or corporate trust services. It acts as custodian for many of the world's largest sovereign wealth funds, central banks, and pension funds. When these institutions move money, BNY Mellon is usually involved.

The regulatory dynamics are fascinating. On one hand, BNY Mellon benefits from regulations that make it harder for new entrants to compete. The compliance costs alone for a global custodian run into hundreds of millions annually. On the other hand, being designated a systemically important financial institution brings massive regulatory burden and capital requirements that constrain profitability.

The "too boring to fail" paradox is real. BNY Mellon is systemically important not because of risky activities but because it's so deeply embedded in the financial system's plumbing. If BNY Mellon's systems went down for even a day, trillions in trades wouldn't settle, markets would freeze, and the knock-on effects would be catastrophic. This makes the bank essentially unexpendable—regulators would never allow it to fail.

Client relationships in custody are unique. Unlike retail banking where customers might interact with their bank weekly, or investment banking where deals create intense but brief relationships, custody clients work with BNY Mellon every single day, often through automated systems. The relationship becomes so operationally intertwined that separation becomes almost unthinkable.

The competitive threats are real but manageable. Blockchain technology promises to eliminate the need for custodians by creating immutable, distributed ledgers. But the transition would require every market participant to adopt new technology simultaneously—a coordination problem that could take decades to solve. Meanwhile, BNY Mellon is investing heavily in blockchain itself, positioning to be the custodian of digital assets just as it custodies traditional ones.

Chinese banks represent another threat, particularly as China's capital markets open up. Industrial and Commercial Bank of China and Bank of China have massive balance sheets and government backing. But custody isn't just about size—it's about trust, technology, and global reach. Breaking into the Western institutional market requires decades of relationship building and massive technology investment.

The fintech disruption narrative is overplayed in custody. While companies like Charles Schwab and Robinhood have revolutionized retail brokerage, institutional custody is fundamentally different. The regulatory requirements, operational complexity, and risk management needs of institutional clients create barriers that no fintech has successfully overcome.

X. Bear vs. Bull Case & Valuation Framework

The Bull Case: BNY Mellon sits at the center of an inexorable trend—the financialization of everything. As more assets move from physical to financial form, as more countries develop capital markets, as more institutions need sophisticated custody and asset servicing, BNY Mellon benefits. The $52 trillion under custody could double in the next decade through market appreciation and new client wins.

The operational leverage is tremendous. Once the technology infrastructure is built, adding new assets under custody has minimal marginal cost. As interest rates normalize from their post-2008 lows, net interest margins expand dramatically. The bank's deposit base, largely from institutional clients, is far stickier and less rate-sensitive than retail deposits.

The competitive moat is widening, not narrowing. Every year, regulations become more complex, technology requirements more demanding, and scale advantages more important. The Big Three custody banks are pulling away from smaller competitors, and new entrants face insurmountable barriers.

Digital assets represent a massive opportunity, not a threat. If cryptocurrencies and tokenized assets become mainstream, institutions will need custodians more than ever. BNY Mellon's early moves into digital asset custody position it to capture this emerging market while maintaining its traditional business.

The Bear Case: Fee compression is relentless. As passive investing dominates and institutional clients become more cost-conscious, custody fees trend toward zero. The basis points BNY Mellon charges today will be half that in a decade. Competition from State Street and JPMorgan intensifies as everyone chases the same institutional clients.

Technology disruption is real, just delayed. Blockchain and distributed ledger technology will eventually eliminate the need for traditional custodians. Smart contracts will automate the services BNY Mellon provides. The bank's massive technology infrastructure becomes a stranded asset, a relic of pre-digital finance.

Regulatory burden continues mounting. Being a G-SIB means ever-higher capital requirements, limiting return on equity. Compliance costs eat into margins. The next financial crisis brings more regulations that further constrain profitability.

The China threat materializes. As Chinese capital markets mature and Chinese banks modernize, Western institutions become more comfortable using them for custody. BNY Mellon loses its monopoly on trust and sees assets flow to lower-cost competitors.

Valuation Framework: BNY Mellon trades at a significant discount to both traditional banks and pure-play asset managers. At roughly 10-12x forward earnings, it's priced like a slow-growth, mature bank. But the business quality suggests it should trade closer to exchanges or asset managers at 15-20x earnings.

The return on equity of 10-12% seems pedestrian but is actually impressive given the regulatory capital requirements. More importantly, it's highly stable—custody fees don't disappear in recessions like trading revenues or loan losses. This stability should command a premium valuation.

The efficiency ratio around 70% has room for improvement as technology investments pay off. If BNY Mellon can drive this below 65% while maintaining service quality, earnings could grow faster than revenues. The operating leverage in the model is underappreciated by the market.

Book value understates the true worth of the franchise. The client relationships, technology infrastructure, and regulatory approvals that took decades to build couldn't be replicated for any price. The replacement cost of BNY Mellon's capabilities would be hundreds of billions, yet it trades at less than 1.5x book value.

XI. Lessons & Legacy

What would Alexander Hamilton think of the institution he founded 240 years ago? The man who created America's financial system to fund a revolutionary government would likely marvel at how his bank now moves trillions globally with the click of a button. Yet the fundamental principle remains unchanged: trust is the foundation of finance, and institutions that maintain trust through centuries accumulate immense power.

The BNY Mellon story teaches us about the power of patience in business building. While Silicon Valley celebrates disruption and rapid scaling, BNY Mellon accumulated its $52 trillion under custody over centuries. Each financial crisis that destroyed competitors added to BNY Mellon's reputation for stability. Time became the ultimate competitive advantage.

The custody banking model reveals something profound about modern capitalism: the real power often lies not with those who take risks but with those who manage risk for others. BNY Mellon doesn't make bold bets on markets or technologies. It provides the infrastructure that allows everyone else to make those bets. It's the arms dealer in the financial wars, selling to all sides and prospering regardless of who wins.

Scale economics in custody banking demonstrate winner-take-most dynamics at their purest. Unlike consumer businesses where local preferences matter, or technology where innovation can disrupt incumbents, custody rewards scale above all else. The bigger you are, the lower your unit costs, the better pricing you can offer, the more clients you win, the bigger you become. It's a flywheel that, once spinning, becomes nearly impossible to stop.

The boring infrastructure play has proven more durable than glamorous business models. While investment banks like Lehman Brothers and Bear Stearns collapsed, while retail banks needed bailouts, while fintech unicorns struggle to find profitability, BNY Mellon just keeps processing transactions and collecting fees. There's a lesson here for investors: sometimes the best businesses are the ones nobody talks about at cocktail parties.

Building essential infrastructure creates a unique form of market power. BNY Mellon doesn't need to advertise, doesn't need to innovate constantly, doesn't need to worry about consumer preferences changing. It just needs to keep the pipes flowing. Once you become the plumbing of global finance, you become indispensable.

The merger of Bank of New York and Mellon Financial also teaches us about strategic timing. Both banks independently recognized that custody was the future and transformed themselves accordingly. Their merger created the scale necessary to dominate globally. Sometimes in business, one plus one really does equal three.

Looking forward, BNY Mellon faces the innovator's dilemma. How does a 240-year-old institution adapt to digital assets, artificial intelligence, and blockchain without destroying the trust and stability that made it successful? The answer likely lies in what BNY Mellon has always done: move slowly, carefully, and let others take the early risks while positioning to provide infrastructure for whatever emerges.

The ultimate lesson from BNY Mellon is that in finance, as in life, the race doesn't always go to the swift or the battle to the strong. Sometimes it goes to those who show up every day, do the essential work that others consider beneath them, and compound their advantages over centuries. Hamilton's bank has outlived empires, currencies, and entire economic systems. It will likely outlive us all.

XII. Recent News & Developments

The most significant recent development is BNY Mellon's historic milestone of becoming the first bank to surpass $50 trillion in assets under custody and administration. This achievement, announced in October 2024, represents not just a numerical milestone but a validation of the custody banking model's resilience and growth potential.

Under CEO Robin Vince's leadership since August 2022, the bank has accelerated its digital transformation while maintaining its conservative risk management. The emphasis on artificial intelligence and automation aims to reduce costs while improving service quality—a delicate balance in an industry where operational errors can be catastrophic.

The cryptocurrency custody initiative represents a fascinating evolution. BNY Mellon is attempting to bring the same institutional-grade custody services it provides for traditional assets to the wild west of digital assets. If successful, this could open an entirely new revenue stream as institutional adoption of cryptocurrencies accelerates.

Recent financial performance has exceeded expectations, with the bank benefiting from both higher interest rates and continued asset gathering. The stock price performance—up over 40% year-to-date in 2024—reflects growing investor appreciation for the stability and growth potential of the custody model.

XIII. Final Thoughts

BNY Mellon represents something unique in American business: a company that has literally grown with the nation, from Hamilton's founding through the industrial revolution, two world wars, the emergence of modern capital markets, and now the digital transformation of finance. It has survived not through brilliance or innovation but through the patient accumulation of trust and the careful management of other people's wealth.

The next decade will test whether this 240-year-old institution can adapt to a world of digital assets, artificial intelligence, and instant global money movement while maintaining the stability and trust that define its value proposition. The early signs are promising—BNY Mellon is investing heavily in technology while maintaining its conservative culture.

For investors, BNY Mellon offers something increasingly rare: a business model that generates steady, predictable returns through economic cycles, backed by enormous competitive moats and serving essential functions that cannot easily be disrupted. It may not be exciting, but in a world of financial uncertainty, boring can be beautiful.

The story of BNY Mellon is far from over. As global wealth continues to grow, as financial markets become more complex, as new forms of assets emerge, the need for trusted custodians only increases. Hamilton's bank, having survived everything from the War of 1812 to the 2008 financial crisis, seems well-positioned to prosper for another 240 years. In finance, as in evolution, sometimes the key to survival isn't being the strongest or the smartest—it's being the most essential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube