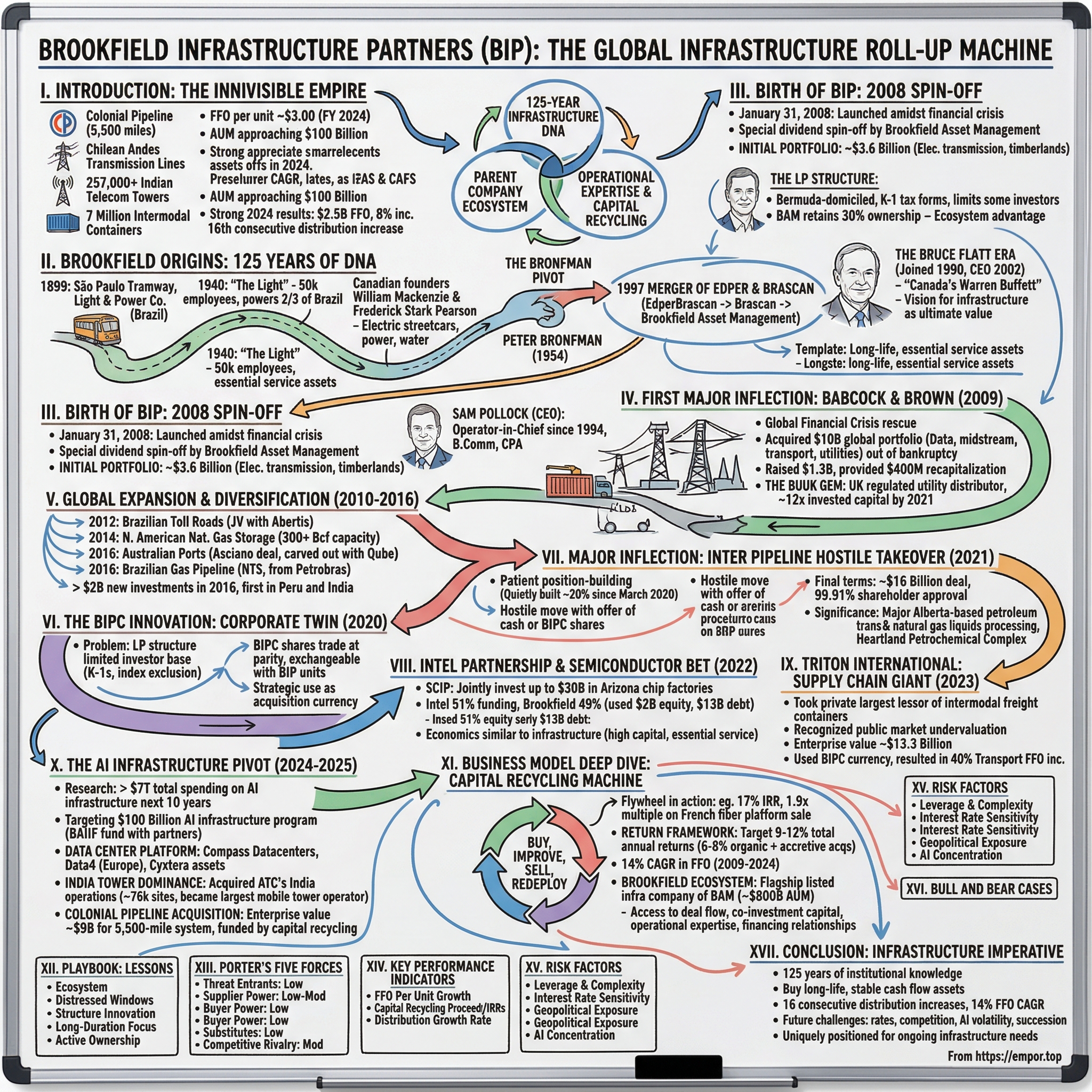

Brookfield Infrastructure Partners: The Global Infrastructure Roll-Up Machine

I. Introduction: The Invisible Empire

Picture yourself driving along the 5,500-mile Colonial Pipeline that delivers gasoline from Texas refineries to gas stations in New Jersey. Flip on a light switch powered by transmission lines stretching across the Chilean Andes. Scroll through your phone using signals bouncing off one of 257,000 telecom towers across India. Ship goods in one of seven million intermodal containers crisscrossing the world's oceans. Each of these essential services shares a common thread—they're all owned or controlled by an entity most investors have never heard of: Brookfield Infrastructure Partners.

With Funds From Operations (FFO) per unit reaching approximately $3.00 in fiscal year 2024 and overseeing a diverse portfolio with assets under management approaching $100 billion dedicated to infrastructure, BIP stands as a leader in owning and operating essential services across utilities, transport, midstream, and data sectors globally. Yet despite this remarkable scale, the company remains remarkably under-followed—a characteristic its management has learned to exploit.

Brookfield Infrastructure Partners reported strong financial results for 2024, with Funds from Operations reaching $2.5 billion, an 8% increase from 2023. The Board declared a quarterly distribution of $0.43 per unit, representing a 6% increase compared to the previous year, marking their 16th consecutive distribution increase.

The central question this analysis explores: How did a spin-off from a Canadian asset manager grow from $3.6 billion to nearly $100 billion in assets in just 17 years through relentless deal-making? And more importantly, is this capital recycling machine sustainable, or is it a house of cards waiting to collapse under its own complexity?

The answer lies in understanding three interlocking elements: a 125-year infrastructure DNA that traces back to Brazilian tramways, a parent company ecosystem that provides unmatched deal flow and expertise, and a management team that has mastered the art of buying distressed assets, improving operations, and recycling capital into new growth opportunities.

From the Global Financial Crisis rescue of Babcock & Brown to the AI infrastructure buildout of 2025, this is the story of how patient capital, operational expertise, and structural innovation created one of the world's most important infrastructure franchises—and what it means for investors seeking stable, growing cash flows in an uncertain world.

II. The Brookfield Origins: 125 Years of Infrastructure DNA

The story of Brookfield Infrastructure Partners doesn't begin in a Toronto boardroom in 2008. It begins in São Paulo, Brazil, in 1899, when two Canadian engineers saw opportunity in chaos.

In 1899, the São Paulo Tramway, Light & Power Co. is founded by Canadian investors after introducing the first electric streetcars to São Paulo and Rio de Janeiro. The company was founded by William Mackenzie and Frederick Stark Pearson. It operated in the construction and management of electricity and transport infrastructure in Brazil.

This wasn't just another colonial-era resource extraction venture. Mackenzie and Pearson weren't mining copper or growing coffee—they were building the invisible systems that would allow a rapidly industrializing nation to function. Electric trams. Power generation. Water distribution. The foundational infrastructure that separates a functioning economy from chaos.

By 1940, "The Light" employs more than 50,000 people and supplies two-thirds of Brazil's electric power. Think about that for a moment: two Canadian entrepreneurs, starting with electric streetcars, built an organization that powered the majority of Latin America's largest economy within four decades. This wasn't just scale—it was monopoly-grade infrastructure dominance.

Brookfield's origins date back more than 100 years, to 1899 and the founding of The São Paulo Tramway, Light and Power Co. in Brazil—which established an early template for our longstanding focus on owning and operating long-life assets that provide essential services globally.

The Bronfman Pivot

In 1954, our founder, Peter Bronfman, establishes an investment company with proceeds from the sale of shares in the Seagram Company. Ten years later, the company begins focusing on real assets, establishing the foundation for our firm's global investment approach.

The Bronfman name carries weight in Canadian business history. Peter Bronfman's investment vehicle would eventually merge with the successor company to Brazilian Traction, creating a platform that combined operational expertise in real assets with sophisticated capital markets capabilities.

The current Brookfield Corporation is the creation of the 1997 merger of Edper and Brascan. At its inception, the company was known as EdperBrascan, then changed its name to Brascan in 2000, and Brookfield Asset Management in 2005.

The Bruce Flatt Era

The transformation into a modern infrastructure powerhouse came under one man: Bruce Flatt.

James Bruce Flatt (born June 10, 1965) is a Canadian businessman and the CEO of Brookfield Asset Management. He joined Brookfield in 1990 and became CEO in 2002. He has been referred to as "Canada's Warren Buffett" due to his "value" investment style, extended tenure as CEO, and large investment in Brookfield.

Mr. Flatt joined Brookfield in 1990 and became CEO in 2002. Under his leadership, Brookfield has developed a global operating presence in more than 30 countries.

Flatt's strategic genius was recognizing that infrastructure—the boring pipes, wires, and roads that society depends on—represented the ultimate value investment. These assets generate predictable cash flows, face limited competition due to massive capital requirements, and often benefit from regulatory protection. While his peers chased high-flying tech stocks, Flatt built an empire of essential services.

"When we spoke about the opportunities in infrastructure, we were met with a lot of blank looks," Brookfield CEO Bruce Flatt said. "Infrastructure just didn't exist for investors back then."

This template—buying essential infrastructure, improving operations, and generating stable returns—would become the playbook for everything that followed. The DNA encoded in those São Paulo tramways would prove remarkably durable across time, geography, and asset class.

III. The Birth of BIP: 2008 Spin-Off & Initial Portfolio

January 31, 2008. The global economy stands on the precipice of its worst crisis since the Great Depression. Bear Stearns would collapse in two months. Lehman Brothers would fall in eight. Yet on this day, Brookfield Asset Management chose to launch one of its most important strategic initiatives: spinning off its infrastructure assets into a dedicated publicly traded vehicle.

Brookfield Asset Management announced the completion of its previously-announced spin-off of a newly created publicly-traded partnership named Brookfield Infrastructure Partners L.P. The spin-off was implemented by way of a special dividend of a 60% interest in Brookfield Infrastructure to holders of Brookfield's Class A and Class B Limited Voting shares as of the record date, January 14, 2008.

The timing seemed questionable. Why launch a new investment vehicle into the teeth of a financial crisis? The answer reveals the Brookfield playbook: crises create opportunities, and having a dedicated, publicly-traded vehicle with access to capital markets would allow them to capitalize on distress that others couldn't touch.

The Initial Portfolio

BIP commenced operations with an initial portfolio of high-quality infrastructure assets valued at approximately $3.6 billion, primarily focused on electricity transmission and timberlands, transferred from Brookfield Asset Management.

Brookfield Infrastructure operates high quality, long-life assets that generate stable cash flows, require relatively minimal maintenance capital expenditures and, by virtue of barriers to entry and other characteristics, tend to appreciate in value over time. Its current business consists of the ownership and operation of premier electricity transmission systems and timberlands in North and South America.

This initial portfolio, while modest, embodied the core investment thesis that would guide BIP for the next seventeen years: essential services, stable cash flows, minimal maintenance capital, and barriers to entry that protect against competition.

Sam Pollock: The Operator-in-Chief

Sam Pollock is Chief Executive Officer of Brookfield's Infrastructure business and Brookfield Infrastructure Partners. Since joining Brookfield in 1994, Mr. Pollock has held a number of senior positions across the organization, including leading Brookfield's corporate investment group and its private equity business.

In this role, he is responsible for investments, operations and the expansion of the Infrastructure business. Mr. Pollock holds a Bachelor of Commerce degree from Queen's University and is a Chartered Professional Accountant.

Pollock's background as both an accountant and operator proved essential. Unlike financial engineers who view assets as numbers on a spreadsheet, Pollock approaches infrastructure as a business builder. His experience across Brookfield's corporate investment group and private equity business gave him the tools to identify distressed opportunities, negotiate complex transactions, and—crucially—improve operations after acquisition.

The LP Structure

Brookfield Infrastructure Partners L.P. was established in January 2008. The partnership was formed under the laws of Bermuda, with its operational headquarters effectively managed by its general partner, an entity of Brookfield Corporation, based in Toronto, Canada.

Why Bermuda? The limited partnership structure offered several advantages: tax efficiency for international operations, flexibility in distribution policy, and structural simplicity for complex cross-border deals. But this structure also created a problem that would take over a decade to solve—many institutional investors and tax-advantaged accounts simply couldn't hold it.

Until a spin-off in January 2008, Brookfield Infrastructure was an operating unit of Brookfield Asset Management, which retains a 30 percent ownership and acts as the partnership's general manager.

The retained 30% ownership is critical to understanding the Brookfield ecosystem advantage. Unlike standalone infrastructure investors, BIP benefits from Brookfield Corporation's deal origination capabilities, operational expertise across sectors, and co-investment capital. When BIP finds a deal too large for its balance sheet alone, it can partner with Brookfield's private funds and institutional investors.

IV. First Major Inflection: The Babcock & Brown Distressed Acquisition

By September 2008, Lehman Brothers had collapsed and the Global Financial Crisis was in full swing. Asset prices plummeted as leveraged vehicles faced margin calls and forced sales. One of the highest-profile casualties was Babcock & Brown, an Australian-headquartered infrastructure and structured finance firm that had been dubbed "Mini Macquarie."

At the end of 2008 Babcock & Brown LP had a market capitalisation of just over $8.5 billion, and in 2007 its market capitalisation peaked at above $9.1 billion. However, by October 2008 the share price had collapsed by 95% to $1.30 and by December 2008 by 99.6% to $0.14, representing a market capitalisation of less than $50 million.

This was distress at its most extreme—a company that had been worth $9 billion reduced to less than $50 million in market value. Yet beneath the overleveraged corporate structure lay something valuable: a globally diversified portfolio of high-quality infrastructure assets.

In September 2008, the company announced it would expand and diversify its global operations by buying infrastructure holdings from distressed Babcock & Brown, thus adding approximately US$8 billion of assets under management.

The Opportunistic Strike

2008: Brookfield takes its infrastructure business public as Brookfield Infrastructure Partners. 2009: Brookfield expands its infrastructure reach via the acquisition of Babcock & Brown out of bankruptcy, acquiring a $10 billion global portfolio of data, midstream, transport and utility assets.

In 2009, Babcock & Brown was on the brink of liquidation. Brookfield went to work and raised $1.3 billion in the public markets, in addition to providing $400 million to recapitalize Babcock's infrastructure holdings, which gave us a 40% interest.

This transaction established the Brookfield playbook that would be repeated again and again: identify distressed sellers, raise capital quickly, structure creative deals that provide downside protection, and acquire high-quality assets at a discount to intrinsic value.

The Toronto-based investor has added $8bn of infrastructure assets onto its books as a result of the deal, a recapitalisation of debt-laden Babcock & Brown Infrastructure. Babcock has re-branded as Prime Infrastructure as part of the deal.

The BUUK Gem

One of the most valuable assets extracted from the Babcock wreckage was BUUK Infrastructure, a UK utility that would become one of Brookfield's most successful investments.

In 2009, as part of the restructuring of Babcock & Brown Infrastructure, we acquired a regulated U.K. distributor connecting homes to the main utility grid. In 2012, we merged the operation with another U.K. company and have since achieved considerable growth through operational improvements and additional product lines—creating a formidable utility franchise in a highly sought after jurisdiction.

Three years later, we acquired a 40% interest in infrastructure manager Babcock & Brown. From there, we acquired BUUK Infrastructure, which designs, constructs, owns and operates last-mile utility networks in the U.K. BUUK would become one of our most successful infrastructure investments, generating 12 times the invested capital by 2021.

Twelve times invested capital. This single transaction, extracted from the rubble of a collapsed financial firm, generated returns that most private equity investors can only dream of. The secret? Buying at distressed prices, then executing the operational playbook: improve efficiency, add product lines, expand the customer base, and benefit from regulated returns.

In 2010 the company completed a merger with Australian company Prime Infrastructure in which it held a minority interest.

The Babcock/Prime transactions transformed BIP from a small spin-off focused primarily on electricity transmission and timber into a globally diversified infrastructure platform with exposure to utilities, transport, and midstream assets across multiple continents.

V. Global Expansion & Diversification (2010-2016)

The Babcock acquisition proved that BIP could execute transformational deals. The next challenge was building scale across multiple verticals while maintaining disciplined capital allocation. The period from 2010 to 2016 saw BIP evolve from an opportunistic acquirer into a systematic platform builder.

Brazilian Toll Roads and Spanish Partnerships

In 2012, the company participated in a joint venture with Spain's Abertis Infraestructuras to purchase 60 percent of toll operator Obrascon Huarte Lain Brasil in a deal valued at US$1.7 billion.

This partnership demonstrated a key element of Brookfield's approach: working with local operators who bring on-the-ground expertise while BIP provides capital and governance. Rather than trying to operate Brazilian toll roads from Toronto, Brookfield partnered with Abertis, a Spanish infrastructure giant with extensive Latin American experience.

North American Natural Gas Storage

Energy infrastructure represented a massive opportunity as the North American shale revolution transformed gas markets. BIP moved aggressively to build a platform.

By 2014, Brookfield Infrastructure had assembled a platform of over 300 billion cubic feet of natural gas storage capacity across eight facilities in the U.S. and Canada. The thesis was contrarian: natural gas storage had seen significant build-out during a period of high prices, leaving the sector depressed. Brookfield bought assets that others viewed as yesterday's news, positioned for the inevitable rebalancing of supply and demand.

Australian Ports: The Asciano Deal

The container port assets remained under the Patrick brand in a joint venture with Qube, while the bulk and automotive port services assets rebranded to Linx Cargo Care Group under a Brookfield-led consortium of investment partners.

The 2016 Asciano transaction exemplified the complexity of Brookfield's deal-making. Asciano was an Australian rail and port operator with multiple attractive business lines but a complicated ownership structure. Rather than acquiring the entire company, Brookfield partnered with Qube Holdings to carve out the most attractive pieces while leaving others to different buyers.

Brazilian Gas Pipeline from Petrobras

That same year, the company also announced that it and its investment partners would acquire a 90% stake in a Brazilian natural gas pipeline from Petroleo Brasileiro SA for US $5.2 billion.

Petrobras, the Brazilian state oil company, was under immense pressure during Brazil's corruption scandal and falling oil prices. BIP swooped in to acquire the NTS pipeline network—critical infrastructure for Brazil's natural gas market—at a price that reflected Petrobras's distress rather than the asset's intrinsic value.

Brookfield has already invested in global pipeline assets. It owns a controlling stake in Brazil's NTS pipeline that spans more than 2,000 kilometers.

Geographic and Sector Diversification

The company made over $2 billion of new investments in 2016, including its first ventures into businesses in Peru and India. The company also invested in organic projects valued at $850 million, growing the size of its utilities rate base, road and rail networks and energy systems.

By the end of 2016, BIP had transformed from a North American-focused electricity transmission company into a global infrastructure platform spanning utilities, transport, midstream, and the emerging data infrastructure sector. This diversification reduced risk while expanding the opportunity set for capital deployment—a critical advantage when recycling capital requires finding attractive new investments.

VI. The BIPC Innovation: Creating the Corporate Twin (2020)

For more than a decade, BIP faced a structural problem that limited its investor base and constrained its acquisition currency. As a Bermuda-domiciled limited partnership, BIP generated K-1 tax forms, couldn't be held in certain tax-advantaged accounts, and was excluded from many institutional mandates that prohibited LP structures.

The solution: create a corporate doppelgänger.

In March 2020, Brookfield Infrastructure Partners (BIP) created Brookfield Infrastructure Corporation (BIPC), an entity that provides certain institutional investors who cannot hold a Bermuda-based Limited Partnership the ability to access the portfolio of BIP assets. In addition, by issuing eligible dividends rather than partnership distributions, BIP felt that BIPC would provide a more attractive and favourable tax treatment for retail investors.

BIPC began trading on the Toronto and New York Stock Exchanges on March 31, 2020.

Why This Matters: Acquisition Currency

The creation of BIPC solved the investor access problem, but its strategic importance goes far beyond expanding the investor base. BIPC shares can be used as acquisition currency in deals where LP units cannot.

Consider the structure: BIPC shares trade at parity with BIP units and can be exchanged for each other. When BIP wants to acquire a company, it can offer BIPC shares to target shareholders who might be prohibited from holding LP units. This dramatically expands the universe of potential targets and improves BIP's competitive position in auction processes.

The timing—March 2020—coincided with the COVID-19 market crash, which meant BIPC launched at depressed valuations. This would prove fortuitous, as the subsequent recovery created an attractive currency for acquisitions.

The Mechanics

BIPC is economically equivalent to BIP—same assets, same cash flows, same growth trajectory. The difference is purely structural: BIPC is a Canadian corporation that issues dividends and generates standard 1099 tax forms, while BIP is a Bermuda LP that issues distributions and generates K-1s.

For investors, the choice depends entirely on tax situation and account type. For Brookfield, having both vehicles provides maximum flexibility in structuring transactions.

VII. Major Inflection: Inter Pipeline Hostile Takeover (2021)

The Inter Pipeline acquisition represents BIP's most aggressive deal ever—a hostile takeover that showcased every element of the Brookfield playbook: patient position-building, opportunistic timing, structural innovation, and relentless execution.

Building the Position

Brookfield Infrastructure is currently the largest investor in IPL with an aggregate economic interest in 84,341,555 IPL Shares, representing approximately 19.65% of the issued and outstanding Shares of IPL on an undiluted basis. Brookfield Infrastructure began to accumulate a position in the Company for investment purposes beginning in March 2020.

March 2020—exactly when COVID-19 crashed energy asset values to multi-year lows. While other investors fled energy exposure, Brookfield began quietly building a nearly 20% position in Inter Pipeline, waiting for the right moment to strike.

The Hostile Move

Brookfield Infrastructure announces today its intention to pursue a privatization transaction in respect of Inter Pipeline Ltd., pursuant to which it will offer to acquire all of the outstanding common shares of the Company not already owned by Brookfield Infrastructure, at a price per IPL Share of C$16.50 in cash or 0.206 of a Brookfield Infrastructure Corporation class A exchangeable share.

The use of BIPC shares as acquisition currency proved critical. By offering target shareholders either cash or BIPC shares, Brookfield created a structure that provided flexibility while conserving cash. Shareholders who wanted immediate liquidity could take cash; those who believed in the combined platform could roll into BIPC and continue participating in the growth story.

The Final Terms

On October 28, 2021, Brookfield Infrastructure Partners L.P., together with its institutional partners, completed the strategic acquisition of Inter Pipeline Ltd. (IPL) in a deal valued at approximately $16 billion.

The Arrangement was approved by 99.91% of the votes cast by holders of common shares of Inter Pipeline present in person (virtually) or represented by proxy at the special meeting.

99.91% approval—near unanimity. This wasn't just a successful deal; it was a validation that Brookfield's offer represented the best path forward for Inter Pipeline shareholders, despite initial resistance from the target's board.

Why Inter Pipeline Mattered

In 2021, we acquired Inter Pipeline, a strategic long-haul pipeline network with interests in petrochemical facilities and bulk storage assets. A major Alberta-based petroleum transportation and natural gas liquids processing business, Inter Pipeline owns and operates energy infrastructure assets across Western Canada, including the Heartland Petrochemical Complex.

The Heartland Petrochemical Complex is critical. This facility converts propane into polypropylene—a higher-value end product—adding manufacturing upside to what would otherwise be a pure transportation business. BIP didn't just buy pipelines; it bought integrated energy infrastructure with growth embedded.

VIII. The Intel Partnership & Semiconductor Bet (2022)

In August 2022, Brookfield Infrastructure announced something unprecedented: a partnership with Intel to co-invest in semiconductor fabrication facilities. For an infrastructure investor known for pipes, ports, and power lines, chip factories seemed like a radical departure.

Intel signs agreement with Brookfield to jointly invest up to $30 billion in leading-edge chip factories in Arizona.

Intel Corporation today announced a first-of-its-kind Semiconductor Co-Investment Program (SCIP) that introduces a new funding model to the capital-intensive semiconductor industry. As part of its program, Intel has signed a definitive agreement with the infrastructure affiliate of Brookfield Asset Management, one of the largest global alternative asset managers, which will provide Intel with a new, expanded pool of capital for manufacturing build-outs.

The Structure

Under the terms of the agreement, the companies will jointly invest up to $30 billion in Intel's previously announced manufacturing expansion at its Ocotillo campus in Chandler, Arizona, with Intel funding 51% and Brookfield funding 49% of the total project cost. Intel will retain majority ownership and operating control of the two new leading-edge chip factories in Chandler.

Brookfield, a major infrastructure investor, put up $2 billion in equity and borrowed $13 billion from a mix of foreign banks, pension funds and sovereign wealth funds.

The structure is classic Brookfield: use a modest equity commitment to control a much larger asset base through leverage. By putting up $2 billion in equity and arranging $13 billion in debt, Brookfield achieved exposure to a $30 billion project while maintaining capital discipline.

Why Semiconductors?

"By combining Brookfield's access to large-scale capital with Intel's industry leadership, we are furthering the advancement of leading semiconductor production capabilities," Sam Pollock, CEO of Brookfield Infrastructure, said. "Leveraging our partnership experience in other industries, we are pleased to come together with Intel in this important investment that will form part of the long-term digital backbone of the global economy."

Semiconductor fabs may seem different from pipelines, but the underlying economics are remarkably similar: massive capital requirements that create barriers to entry, long asset lives, and essential services that customers cannot do without. Intel operates the facility and bears technology risk; Brookfield provides capital and receives a stream of returns backed by Intel's balance sheet and the physical asset.

The U.S. CHIPS and Science Act unlocks up to $52 billion in incentives for the U.S. semiconductor industry. The CHIPS Act provided additional tailwind, offering government incentives that improved project economics and reduced risk for all parties.

IX. Triton International: Becoming a Supply Chain Giant (2023)

If the Intel deal showed BIP could expand into new asset classes, the Triton International acquisition demonstrated mastery of a more traditional infrastructure thesis: buying an undervalued public company and taking it private.

Triton International Limited is the world's largest lessor of intermodal freight containers. With a container fleet of over 7 million twenty-foot equivalent units, Triton's global operations include acquisition, leasing, re-leasing and subsequent sale of multiple types of intermodal containers and chassis.

On April 12, 2023, Brookfield Infrastructure Partners L.P., through its subsidiary Brookfield Infrastructure Corporation and its institutional partners, and Triton International Limited jointly announced a definitive agreement for Triton to be acquired in a cash and stock transaction valuing its common equity at approximately US$4.7 billion and reflecting a total enterprise value of approximately US$13.3 billion.

The Undervaluation Thesis

Brookfield capitalized on this by taking a $6 billion container shipping company private; it had one analyst covering it, fit no indexes, and traded far below intrinsic value.

We acquired Triton from the public markets in 2023 after recognizing that its value was not fully reflected by public equities investors. The business is the world's largest owner and lessor of intermodal containers, managing a global fleet of over 7 million units.

This is the passive investing arbitrage that Brookfield exploits repeatedly. When a company doesn't fit neatly into stock indexes, doesn't attract analyst coverage, and has complex business dynamics, public market investors often misprice it. Brookfield buys these companies, takes them private, and captures the gap between market price and intrinsic value.

BIPC Currency in Action

Successful completion of the acquisition was announced on September 28, 2023, following approval from Triton's shareholders on August 24, 2023. In connection with the completion of the transaction, Triton common shareholders were entitled to receive a per share consideration equal in value to US$68.50 in cash and 0.3895 BIPC class A exchangeable shares.

The BIPC shares issued in the Triton deal allowed target shareholders to either cash out or roll into Brookfield's platform—exactly as designed when BIPC was created three years earlier.

Segment performance showed mixed results: Transport FFO increased 40% to $1,224 million, Data segment grew 21% to $333 million.

The 40% increase in Transport FFO reflects Triton's contribution—exactly the accretive growth that BIP promised when announcing the deal.

X. The AI Infrastructure Pivot (2024-2025)

The next chapter of BIP's story is being written in real-time: the AI infrastructure buildout that management believes could rival the construction of the modern power grid.

Citing its own internal research, Brookfield said that total spending on AI-related infrastructure will exceed $7 trillion in the next 10 years. Brookfield believes that $4tn will be spent on chips (including fabs and supply chains) and $2tn on AI data centers. $500bn will go to power & transmission, and another $500bn will go to broader tech such as dedicated fiber connectivity, cooling solutions, and robotics manufacturing.

The $100 Billion AI Infrastructure Program

Brookfield Artificial Intelligence Infrastructure Fund, which launches today with a target of $10 billion of equity commitments to invest in the backbone of artificial intelligence. BAIIF has already received $5 billion of capital commitments from a select group of institutional and industry partners, including Brookfield, NVIDIA and KIA. BAIIF, together with additional capital from its co-investors and prudent financing, will acquire up to $100 billion of AI infrastructure assets, deploying investment across every stage of the value chain—from energy and land to data centers and compute.

As one of the world's leading owners and operators of AI infrastructure assets, with over $100 billion already invested in digital infrastructure and clean power, Brookfield is uniquely positioned to deliver integrated infrastructure solutions.

Data Center Platform

Brookfield made three more data center investments last year. It acquired a co-controlling stake in North American data center developer Compass Datacenters. It also acquired European data center operator Data 4. Finally, Brookfield bought a portfolio of U.S. data centers out of bankruptcy from Cyxtera and the underlying real estate from third-party landlords.

Brookfield announced a €20 billion infrastructure investment program to support the deployment of artificial intelligence infrastructure in France. The Brookfield investment will be targeted across data centers and associated infrastructure sectors which are vital for AI deployment. Up to €15 billion of data center investment will be led by Brookfield's portfolio company, Data4, one of Europe's largest data center developers.

India Tower Dominance

Data Infrastructure Trust ("DIT"), an Infrastructure Investment Trust sponsored by Brookfield Asset Management along with affiliates of investors including British Columbia Investment Management Corporation (BCI) and GIC today completed the acquisition of 100% of American Tower's operations in India. This transaction comprises the buyout of approximately 76,000 communications sites in India for an enterprise value of INR 182 billion (~$2.2 billion).

With the completion of this acquisition, Brookfield has now overtaken Indus Towers, which currently operate 225,910 sites as of September 2024, to become India's largest mobile tower operator.

The Colonial Pipeline Acquisition

Brookfield Infrastructure Partners reached a definitive agreement to acquire 100% of the world-class midstream asset portfolio Colonial Enterprises ("Colonial"), which includes the Colonial Pipeline, for an enterprise value of approximately $9 billion or 9x EBITDA.

The Colonial Pipeline runs for 8,850 kilometers (5,500 miles) from Texas to New Jersey, and is the main source of gasoline, diesel and jet fuel for the East Coast.

"You could not replicate the Colonial pipeline system today," Colonial CEO Melanie Little said during CERAWeek. "While dealmaking in the midstream sector has been mostly small scale, there are signs that's changing."

BIP's equity investment will be $500 million, approximately 15% of the total equity investment, funded through recent capital recycling initiatives. BIP is funding its $500 million equity investment entirely through proceeds from recently announced capital recycling initiatives.

This is the capital recycling machine in action: sell mature assets, deploy proceeds into new growth opportunities like Colonial Pipeline, and maintain financial discipline throughout.

XI. Business Model Deep Dive: The Capital Recycling Machine

Understanding BIP requires understanding its unique business model: a perpetual motion machine of buying, improving, selling, and redeploying capital.

The Flywheel

"Brookfield Infrastructure continues to deliver solid results while achieving its strategic objectives, including successfully reaching our $2 billion capital recycling target for the year," said Sam Pollock.

The company completed its targeted $2 billion capital recycling initiatives and has already secured $850 million in proceeds from asset sales in early 2025.

In April, we signed binding documentation to sell the fiber platform within our French Telecom Infrastructure business to a financial buyer. The transaction has an enterprise value of over €1 billion (approximately €175 million net to BIP) and is expected to result in an IRR of 17% and a multiple of capital of approximately 1.9x.

17% IRR and 1.9x multiple on the French fiber platform—acquired in 2015, grown through operational improvements, and sold to a financial buyer at a substantial premium. This is the playbook executed across dozens of transactions.

Return Framework

To deliver targeted returns, Brookfield Infrastructure aims for 9-12% total annual returns, comprising 6-8% from organic growth—driven by inflation-linked revenues, volume increases, and commissioned capital—and the balance from accretive acquisitions.

Since its inception, BIP has grown through strategic acquisitions, operational enhancements, and asset recycling, achieving a compound annual growth rate (CAGR) of 14% in funds from operations (FFO) from 2009 to 2024.

14% FFO CAGR over 15 years—significantly above the stated 9-12% target. This outperformance reflects both the quality of capital allocation decisions and the tailwind from falling interest rates over most of this period.

The Brookfield Ecosystem

Brookfield Infrastructure is the flagship listed infrastructure company of Brookfield Corporation, a global alternative asset manager with approximately $800 billion of assets under management.

BIP doesn't operate in isolation. It benefits from:

- Deal origination: Brookfield's global network surfaces opportunities that smaller investors never see

- Co-investment capital: When deals exceed BIP's capacity, Brookfield's private funds and institutional partners provide additional equity

- Operational expertise: Brookfield's 180,000+ employees include specialists across every infrastructure sector

- Financing relationships: Decades of deal-making have built deep relationships with lenders worldwide

Weighted Average Debt Maturity: Eight years, with 90% of debt at fixed rates. Capital Recycling Proceeds 2024: Achieved $2 billion.

Eight-year weighted average debt maturity with 90% at fixed rates provides substantial protection against interest rate volatility—a lesson learned from watching overleveraged competitors blow up during rate spikes.

XII. Playbook: Business & Investing Lessons

Lesson 1: The Ecosystem Advantage

Bruce Flatt is the Chief Executive Officer of Brookfield, a global investment firm focused on alternative asset management, wealth solutions, and its operating businesses, with over $1 trillion in assets under management.

Being part of a trillion-dollar platform provides advantages that standalone infrastructure investors cannot match. Deal flow, expertise, co-investment capital, and credibility with sellers—all stem from the Brookfield ecosystem.

Lesson 2: Distressed Investing Windows

The Babcock & Brown acquisition during the GFC, the Inter Pipeline position built during COVID, the AI infrastructure buildout during the current demand surge—Brookfield has repeatedly demonstrated that timing matters. Patient capital, combined with the ability to move quickly when opportunities emerge, creates asymmetric return profiles.

Lesson 3: Structure Innovation

In March 2020, Brookfield Infrastructure Partners created Brookfield Infrastructure Corporation, an entity that provides certain institutional investors who cannot hold a Bermuda-based Limited Partnership the ability to access the portfolio of BIP assets.

The BIPC innovation shows how solving investor problems—tax treatment, account eligibility—creates strategic advantages. BIPC shares have become critical acquisition currency, enabling deals that wouldn't be possible with LP units alone.

Lesson 4: Long-Duration Asset Focus

Brookfield Infrastructure operates high quality, long-life assets that generate stable cash flows, require relatively minimal maintenance capital expenditures and, by virtue of barriers to entry and other characteristics, tend to appreciate in value over time.

The focus on assets with minimal maintenance capital is underappreciated. Unlike manufacturing businesses that require constant reinvestment just to maintain competitive position, infrastructure assets often generate growing cash flows from a fixed asset base.

Lesson 5: Active Ownership

Our infrastructure business has been able to deliver consistent, attractive returns with operations that have stable, regulated cash flows underpinned by long-term, inflation-linked contracts. Following the same strategy we developed for real estate, we leverage our infrastructure investments prudently to ensure they can withstand market uncertainty.

BIP is not a passive owner. The operational improvements at BUUK (12x returns), the integration of acquisitions into existing platforms, the organic growth projects across the portfolio—all reflect active management rather than financial engineering.

XIII. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

Infrastructure investing has among the highest barriers to entry of any asset class:

- Capital requirements: Building a diversified infrastructure platform requires tens of billions of dollars

- Regulatory barriers: Permits, environmental approvals, government concessions—all create multi-year timelines before new capacity can come online

- Relationship intensity: Major infrastructure transactions are relationship-driven; buyers without track records struggle to compete

- Operational expertise: Actually running ports, pipelines, and power lines requires deep operational capabilities that take decades to build

"When Colonial was constructed in the 1960s, it took 18 months to permit, build and start operations and today we can't get a permit in 18 months."

This quote captures the regulatory moat: existing infrastructure cannot be easily replicated, giving incumbent owners pricing power and competitive protection.

2. Bargaining Power of Suppliers: LOW-MODERATE

Most equipment suppliers (pipes, towers, cables) operate in competitive markets with limited pricing power. However, specialized contractors for mega-projects and scarce resources like land with power access can command premiums in tight markets—particularly relevant for the current AI data center buildout.

3. Bargaining Power of Buyers: LOW

Brookfield Infrastructure is one of the largest owners and operators of critical global infrastructure networks which facilitate the movement and storage of energy, water, freight, passengers and data.

Essential services with captive customers face minimal buyer power. Shippers don't negotiate container rates with Triton—they need containers to move goods. East Coast refineries don't have alternatives to Colonial Pipeline—it's the only way to get fuel to market. Regulated utilities operate under approved rate structures that guarantee returns on capital.

4. Threat of Substitutes: LOW

Physical infrastructure has few substitutes: - Data centers are the backbone of digital services—there's no alternative to housing servers somewhere - Pipelines cannot be economically replaced by trucking or rail for volume bulk commodities - Container shipping enables global trade in a way that no other mode can match

5. Competitive Rivalry: MODERATE

While operating infrastructure faces limited competition (monopoly/duopoly characteristics in most cases), acquiring infrastructure assets is intensely competitive.

Brookfield Asset Management stands as one of GIP's primary competitors, with approximately $130 billion in infrastructure assets under management through its Brookfield Infrastructure Partners division. Brookfield's infrastructure portfolio spans utilities, transport, energy, and data infrastructure across the Americas, Europe, and Asia-Pacific regions. The firm's scale and diversification make it a consistent competitor to GIP in major infrastructure transactions globally.

KKR Infrastructure has emerged as an increasingly significant competitor, with approximately $40 billion dedicated to infrastructure investments. KKR has been particularly active in digital infrastructure and energy transition assets.

BXINFRA's sponsor, Blackstone, is the world's largest alternative asset manager with more than $1.2 trillion in assets under management and $140B+ AUM across infrastructure strategies.

The competitive landscape has intensified significantly since BIP's founding. Blackstone, KKR, Macquarie, and the recently-merged BlackRock/GIP all compete aggressively for attractive assets. This competition compresses returns on new acquisitions and requires increasingly sophisticated deal structures.

Hamilton Helmer's 7 Powers Assessment

- Scale Economies: Present in operational synergies across portfolio companies and financing capabilities

- Network Effects: Limited direct network effects, though the Brookfield ecosystem provides information and relationship advantages

- Counter-Positioning: BIP's willingness to own complex, illiquid assets that public equity investors avoid represents a form of counter-positioning

- Switching Costs: Extremely high for infrastructure customers—once a region depends on specific transmission lines or pipelines, switching is essentially impossible

- Branding: Moderate importance; the Brookfield name carries weight with sellers and co-investors

- Cornered Resource: Existing infrastructure cannot be replicated at any price due to regulatory and physical constraints

- Process Power: BIP's operational playbook—the systematic approach to improving acquired assets—represents genuine process power developed over decades

XIV. Key Performance Indicators

For investors monitoring BIP's ongoing performance, three metrics matter most:

1. Funds From Operations (FFO) Per Unit Growth

Management uses funds from operations per unit (FFO per unit) as a key measure to evaluate operating performance.

FFO strips out non-cash items like depreciation and mark-to-market adjustments to reveal underlying cash generation. The target is 6-9% annual growth from organic operations plus accretive acquisitions.

Why it matters: FFO per unit directly drives distribution coverage and growth capacity. Tracking this metric over time reveals whether the capital recycling machine is actually generating accretive returns or merely churning assets.

2. Capital Recycling Proceeds and Reinvestment IRRs

The transaction has an enterprise value of over €1 billion and is expected to result in an IRR of 17% and a multiple of capital of approximately 1.9x.

BIP discloses IRRs and multiples on asset sales. These metrics reveal whether management is selling at attractive prices and whether the overall recycling strategy creates value.

Why it matters: The entire business model depends on buying low, improving operations, and selling high. If realized IRRs consistently fall below targets, the model breaks down.

3. Distribution Growth Rate

The Board declared a quarterly distribution of $0.43 per unit, representing a 6% increase compared to the previous year, marking their 16th consecutive distribution increase.

With an attractive distribution yield and a distribution growth target of 5-9% annually, Brookfield Infrastructure offers income-oriented investors a stream that grows faster than inflation.

Why it matters: Distribution growth reflects management confidence in sustainable cash flow generation. Cutting or stalling distributions would signal problems with the underlying business model.

XV. Risk Factors & Regulatory Considerations

Leverage and Complexity

"The debt levels are higher than stated on the asset balance sheet due to the unique structure of Brookfield entities that creates additional leverage at multiple levels. We estimate total debt including proportional amounts at holding companies and up to Brookfield Infrastructure Partners, but not above, to exceed $A2.2 billion."

Critics have noted that Brookfield's layered corporate structure creates leverage that isn't always apparent from consolidated financial statements. Each layer of holding company can add debt, potentially creating a more leveraged structure than headline metrics suggest.

Interest Rate Sensitivity

Long-term interest rates have increased, and inflation remains a concern, potentially impacting future financial performance.

While BIP's operations benefit from inflation-linked revenues, its financing costs rise with interest rates. The eight-year average debt maturity provides protection, but eventually refinancing higher-rate debt will impact returns.

Geopolitical Exposure

While geopolitical events have captured the attention of global investors, our business continues to perform well amidst the uncertainty. This uncertainty is in part due to the fact that over half of the world's population will be participating in democratic elections this year. Ours is largely insulated due to the combination of a highly diversified portfolio of critical infrastructure, deliberate selection of countries in which we invest and a focus on investing behind three mega trends that to date have garnered broad political support.

BIP operates in multiple countries with varying political and regulatory environments. While essential infrastructure typically enjoys protection regardless of which party governs, nationalization risk, changing regulatory frameworks, and currency exposure all require monitoring.

AI Infrastructure Concentration Risk

The announcement by DeepSeek, a Chinese AI company, has raised questions about the future demand for data centers, potentially affecting BIP's investments. Development premiums for hyperscale data centers have started to compress, indicating increased competition in the sector.

Sam Pollock, CEO: "We evaluate opportunities on a risk-adjusted basis. We don't build large projects on spec and manage land inventory to avoid overexposure. Our strategy focuses on building facilities with contracts in hand."

Management's response—building only with contracts in hand, avoiding speculative development—provides some protection, but the massive pivot toward AI infrastructure represents concentration risk if AI investment cycles prove more volatile than expected.

XVI. Bull and Bear Cases

Bull Case: The Essential Services Compounder

The bull case rests on three pillars:

1. Megatrend Exposure

Bruce Flatt reveals how his firm built a trillion-dollar empire by focusing on downside protection while capitalizing on three megatrends: digitalization, energy transition, and deglobalization.

BIP owns assets that benefit from digitalization (data centers, telecom towers, fiber), decarbonization (renewable power interconnections, gas infrastructure as transition fuel), and deglobalization (North American manufacturing infrastructure, supply chain assets). These trends have broad political support and multi-decade duration.

2. Capital Recycling Alpha

The track record of 17% IRRs on asset sales and 14% FFO CAGR suggests genuine value creation rather than financial engineering. If management can continue executing at similar returns, the flywheel accelerates over time.

3. AI Infrastructure Optionality

BAIIF, together with additional capital from its co-investors and prudent financing, will acquire up to $100 billion of AI infrastructure assets. As one of the world's leading owners and operators of AI infrastructure assets, with over $100 billion already invested in digital infrastructure and clean power, Brookfield is uniquely positioned.

Brookfield's existing position in power, land, and data centers creates a unique platform for capturing AI infrastructure demand. If AI investment continues scaling, BIP sits at the intersection of every enabling infrastructure layer.

Bear Case: The House of Cards

1. Leverage Opacity

The layered structure makes true leverage difficult to assess. If asset values decline significantly—as they did during the GFC—highly leveraged structures can face margin calls and forced sales. The Babcock & Brown collapse that BIP profited from was itself caused by excessive leverage in infrastructure assets.

**2. Competition Intensifies

Brookfield Asset Management stands as one of GIP's primary competitors, with approximately $130 billion in infrastructure assets under management.

Every major alternative asset manager now has an infrastructure strategy. BlackRock's acquisition of Global Infrastructure Partners created a $150+ billion competitor. Competition compresses returns on new acquisitions and may force BIP into riskier deals to maintain growth targets.

3. Rising Rate Environment

The fifteen-year period of falling interest rates that coincided with BIP's existence provided a massive tailwind. If rates remain elevated or rise further, asset values compress, financing costs increase, and the capital recycling machine may generate lower returns.

4. AI Demand Volatility

The AI infrastructure buildout is happening at unprecedented speed and scale. If AI adoption disappoints, training efficiencies reduce compute requirements, or geopolitical factors disrupt supply chains, BIP's aggressive pivot toward this sector could generate losses rather than returns.

XVII. Conclusion: The Infrastructure Imperative

From Brazilian tramways in 1899 to AI factories in 2025, Brookfield Infrastructure Partners represents 125 years of institutional knowledge about owning and operating essential services. The company has navigated World Wars, financial crises, and technological revolutions while maintaining a consistent focus: buy long-life assets that generate stable cash flows and tend to appreciate over time.

"During 2024 we generated strong financial results and closed on all of our capital recycling initiatives, showcasing the resilience and durability of our business strategy," said Sam Pollock.

The results speak for themselves: 16 consecutive distribution increases, 14% FFO CAGR since inception, transformation from a $3.6 billion spin-off to a nearly $100 billion asset platform. This is not a story of financial engineering or momentum trading—it's a story of patient capital, operational expertise, and relentless execution.

Yet the future presents challenges that differ from the past. Interest rates may remain elevated. Competition for infrastructure assets has intensified dramatically. The AI infrastructure pivot represents concentration risk in a nascent sector. Management succession—Sam Pollock has led BIP since inception—remains an open question.

For investors, BIP offers a rare combination: exposure to essential infrastructure with professional management, structural flexibility through the BIP/BIPC dual structure, and a track record of disciplined capital allocation. The distribution yield provides income while the growth targets offer capital appreciation potential.

The infrastructure imperative that drove Canadian investors to build Brazilian tramways 125 years ago remains unchanged: modern economies require physical networks to function. Someone must own, operate, and expand these networks. Brookfield Infrastructure Partners has built a platform uniquely positioned to do so—whether that translates into outsized returns depends on continued execution, disciplined capital allocation, and the durability of the megatrends management has identified.

In an investment universe increasingly dominated by passive index funds and momentum algorithms, BIP represents something different: a bet on operational expertise, patient capital, and the physical backbone of the global economy. That bet has paid off handsomely for the past seventeen years. The next seventeen will depend on whether the playbook that worked during an era of falling rates and limited competition can adapt to whatever comes next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube