Best Buy: From Sound of Music to Big Box Dominance

I. Introduction & Episode Roadmap

Picture this: It's 2012, and Wall Street has written Best Buy's obituary. The stock trades at $11, down from $56 just five years earlier. Amazon is eating retail alive. Circuit City's corpse is still warm, having declared bankruptcy in 2008. CompUSA is gone. RadioShack is dying. Every smart analyst knows exactly what happens next—the last big-box electronics retailer falls to the digital guillotine.

Except that's not what happened.

Today, Best Buy operates over 1,000 stores across North America, generates $43 billion in annual revenue, and its stock has delivered a 335% return since that 2012 nadir—crushing the S&P 500's 104% gain over the same period. The company that everyone thought would be Amazon's next victim instead became its partner, hosting Amazon boutiques inside its stores and becoming a critical last-mile delivery partner for the e-commerce giant.

How did a Minnesota stereo shop founded by a guy who mortgaged his house survive when every other electronics retailer died? How did Best Buy transform from the ultimate "showrooming" victim—where customers would browse in-store then buy on Amazon—into a retail fortress that even Jeff Bezos couldn't breach?

The answer involves tornadoes, non-commissioned salespeople, a French CEO who spent his first week working the shop floor, and the radical idea that in an age of digital disruption, physical stores might actually be an asset, not a liability. This is the story of retail's greatest escape artist—a company that faced death three separate times and emerged stronger each time.

We'll trace Best Buy's evolution through five distinct eras: the scrappy Sound of Music origins under founder Dick Schulze, the superstore revolution that crushed regional competitors, the epic Circuit City wars that defined electronics retail in the 1990s, the near-death experience when Amazon almost killed them, and finally, the remarkable human-centered turnaround that offers a masterclass in corporate reinvention.

Along the way, we'll unpack the strategic moves that separated winners from losers in retail's most brutal sector, examine why Best Buy's international expansion failed spectacularly while its domestic business thrived, and explore what this survivor's tale teaches us about adaptation, leadership, and the surprising durability of physical retail in the digital age.

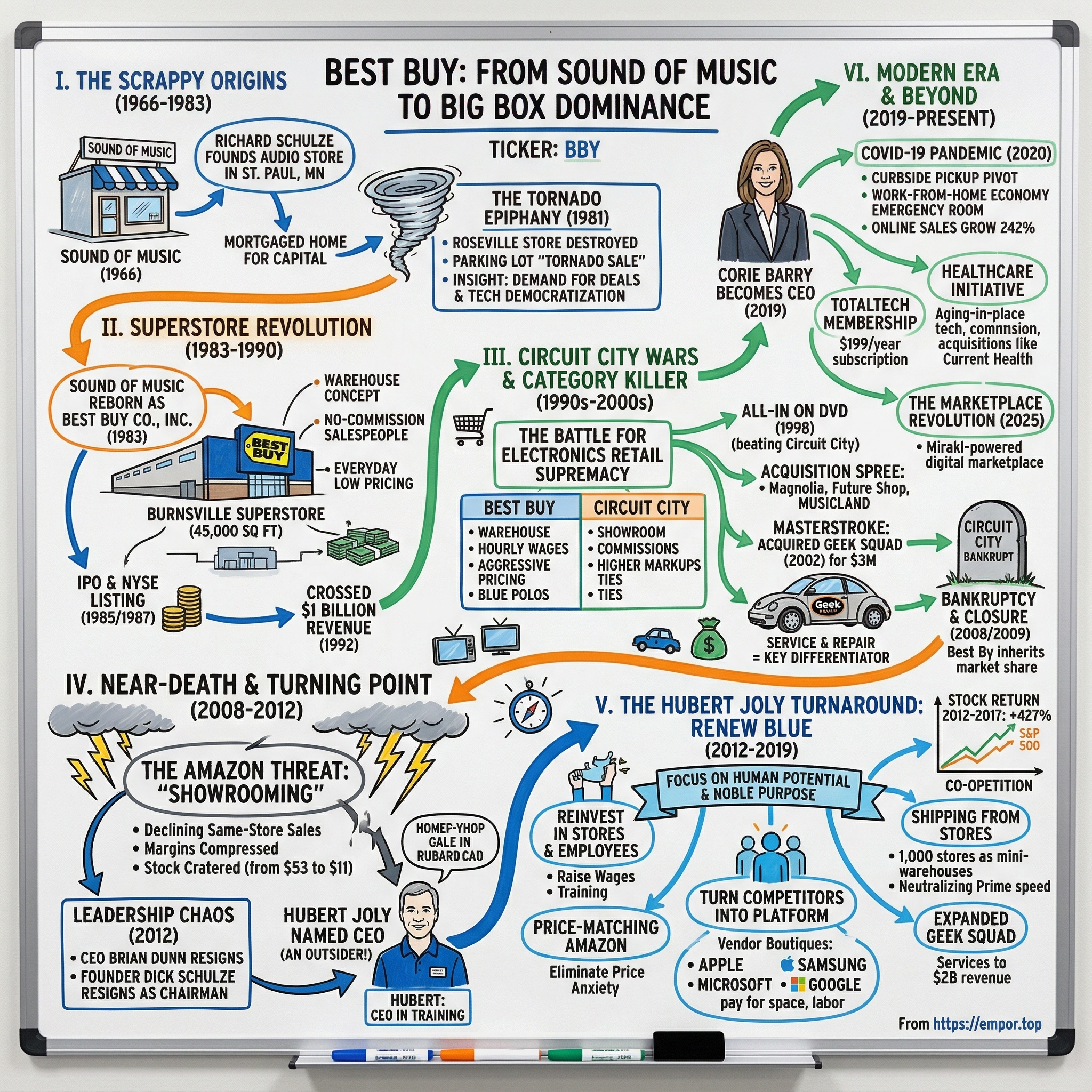

II. Sound of Music: The Schulze Origin Story (1966–1983)

The year is 1966. The Beatles are topping charts with "Paperback Writer," and in St. Paul, Minnesota, a 25-year-old named Richard Schulze is about to make a bet that will define his life. Schulze doesn't come from money—his father was a farmer who lost everything in the Depression. But Dick has an idea: Americans are falling in love with high-fidelity stereo systems, and he wants to be their dealer.

On August 22, 1966, Schulze and a business partner open Sound of Music, a specialty audio equipment store. The financing? Schulze's entire life savings plus a second mortgage on his family home. His wife must have thought he was insane—betting the house, literally, on selling stereos to Minnesotans. But something about the timing was perfect. The post-war boom had created a middle class hungry for entertainment, and stereo systems were transitioning from luxury items to middle-class aspirations.

That first year validated Schulze's instinct spectacularly: Sound of Music generated $1 million in revenue and $58,000 in profits. For context, that's roughly $9 million in revenue and $520,000 in profits in today's dollars—extraordinary returns for a single-store startup with borrowed capital. Schulze had found product-market fit before Silicon Valley invented the term.

By 1969, Sound of Music had expanded to three stores, and Schulze made his first major strategic move: buying out his business partner. This wasn't just about control—it was about vision. Schulze saw something bigger than a regional stereo chain. He was already thinking about scale, about how to democratize access to consumer electronics beyond just the audiophile crowd.

The 1970s saw steady expansion across Minnesota. By 1978, Sound of Music operated nine stores throughout the state, establishing itself as the dominant player in the Twin Cities audio market. Schulze had developed a reputation for aggressive pricing and knowledgeable staff—a combination that would later become Best Buy's calling card. But the company was still fundamentally a specialty retailer, focused on a narrow product category in a limited geography.

Then came June 14, 1981—a date that would transform everything.

A tornado ripped through the Twin Cities, devastating the Roseville store, Sound of Music's most profitable location. The showroom was destroyed, but the stockroom remained intact. Most retailers would have seen disaster. Schulze saw opportunity. Rather than wait for insurance claims and reconstruction, he decided to hold a "Tornado Sale" in the parking lot, selling damaged and undamaged goods at deep discounts directly from trucks and tents.

The response was unlike anything Schulze had witnessed in 15 years of retail. Customers drove from across the state, creating traffic jams for blocks. The four-day sale generated more revenue than the store typically saw in a month. Lines stretched around the block. Local news covered it as an event, not just a sale. And in those chaotic, exhilarating days, Schulze had an epiphany that would reshape American retail.

The Tornado Sale revealed three critical insights. First, customers would drive significant distances and wait in lines for truly exceptional deals. Second, the traditional retail model—with its expensive showrooms, commissioned salespeople, and high markups—was ripe for disruption. Third, and most importantly, there was massive latent demand for consumer electronics if you could crack the pricing and experience equation.

Standing in that parking lot, watching customers haul away stereos and televisions with genuine excitement, Schulze realized he'd been thinking too small. Sound of Music wasn't in the stereo business—it was in the business of democratizing technology. The tornado hadn't destroyed his store; it had blown away his limitations.

In 1983, Schulze made the decision that would define his legacy: Sound of Music would be reborn as Best Buy Co., Inc. The name change signaled more than rebranding—it was a declaration of war on traditional retail. The first Best Buy superstore opened that same year in Burnsville, Minnesota, spanning 45,000 square feet—roughly five times larger than a typical Sound of Music location.

But size was just the beginning. Schulze reimagined every aspect of the retail experience. Products were displayed on the floor where customers could touch and try them, not locked behind glass cases. Prices were clearly marked—no haggling, no games. The store carried everything from washing machines to boom boxes, transforming from audio specialist to electronics generalist. Within a year, this single superstore captured 42% of the Twin Cities consumer electronics market.

The transformation from Sound of Music to Best Buy represented more than evolution—it was revolution. Schulze had taken a natural disaster and transformed it into a blueprint for retail disruption. The guy who mortgaged his house to open a stereo shop was about to challenge the biggest names in American retail. And he was just getting started.

III. The Superstore Revolution & Going Public (1983–1990)

The Burnsville superstore was a 45,000-square-foot middle finger to conventional retail wisdom. While competitors like Circuit City maintained traditional showroom floors with commissioned salespeople hovering over customers, Schulze built what looked more like a warehouse—concrete floors, industrial shelving, and products stacked to the ceiling. Customers could wander freely, touch products without asking permission, and—most radically—shop without being stalked by salespeople desperate for commissions.

Wall Street didn't get it. Retail analysts in 1984 looked at Best Buy's model and saw chaos. How could you sell complex electronics without expert salespeople guiding purchases? Wouldn't customers just steal everything? Who would buy a $2,000 stereo system from a warehouse? But Schulze understood something the experts missed: consumers were becoming more educated about technology and increasingly resented the high-pressure sales tactics that defined electronics retail.

The numbers silenced the skeptics. By 1985, just two years after the rebrand, Best Buy was ready for its initial public offering. The company raised $8 million—modest by today's standards but transformative for a regional retailer. Schulze used the capital to accelerate expansion, opening new superstores across Minnesota and into Wisconsin. Each new location followed the same playbook: massive footprint, rock-bottom prices, and no commissioned sales staff.

But the real innovation came in 1986 with what Schulze called "Concept II"—a radical reimagining of the electronics retail experience that would become the template for modern big-box retail. Concept II stores eliminated the service counter entirely. Customers could grab products directly off shelves, load them into shopping carts (another radical innovation for electronics retail), and check out at centralized registers like a grocery store.

The psychology was brilliant. By removing the friction of the sales process, Best Buy transformed electronics shopping from an intimidating negotiation into something approaching fun. Families would spend Saturday afternoons browsing, comparing prices on boom boxes and VCRs without pressure. Kids could play with display models while parents actually enjoyed the shopping experience. It was retail as entertainment—a concept that would later define everything from Apple Stores to Tesla showrooms.

In 1987, Best Buy achieved another milestone: listing on the New York Stock Exchange. The ticker symbol BBY represented more than access to capital markets—it was validation that this Minnesota upstart was playing in the big leagues. Circuit City, the undisputed king of electronics retail, was forced to pay attention. Trade publications started covering this "warehouse concept" that was stealing market share in every city it entered.

The expansion accelerated through the late 1980s. Best Buy added entertainment software to its product mix—VHS tapes, compact discs, and even video game cartridges for the emerging Nintendo Entertainment System. This wasn't just product line extension; it was a strategic bet that consumer electronics and entertainment content would converge. While competitors saw themselves as appliance retailers who happened to sell some music, Best Buy positioned itself at the intersection of technology and entertainment.

By 1989, Best Buy operated 40 stores across seven states, with revenues approaching $500 million. The company's same-store sales growth—the holy grail metric of retail—consistently exceeded 20% annually. For comparison, Circuit City, with ten times the store count, was celebrating single-digit growth. Something fundamental was shifting in American retail, and Best Buy was riding the wave.

The culmination came in 1992 when Best Buy crossed $1 billion in annual revenue—a psychological barrier that transformed it from regional player to national force. From that tornado-damaged parking lot in 1981 to billion-dollar revenues just 11 years later, Schulze had built something unprecedented: a retail model that gave customers what they actually wanted rather than what retailers thought they should want.

But success attracted competition. Circuit City, watching its market share erode in every market where Best Buy operated, was preparing its counterattack. Highland Superstores was expanding aggressively from Detroit. Crazy Eddie was imploding spectacularly in New York but leaving market share up for grabs. The 1990s would determine whether Best Buy was a brilliant regional anomaly or the future of American retail.

The battle lines were drawn. Circuit City had the scale, the brand recognition, and the Wall Street backing. But Best Buy had something more powerful: a business model aligned with how consumers actually wanted to shop. The war for electronics retail supremacy was about to begin, and the weapons would be real estate, inventory management, and a radical idea called everyday low pricing.

IV. The Circuit City Wars & Category Killer Era (1990s–2000s)

In 1988, Circuit City executives made a decision they would regret for the rest of their corporate lives—which, as it turned out, wouldn't be very long. Best Buy, still a regional player with just a few dozen stores, was available for purchase at $30 million. Circuit City's board looked at the offer, looked at their dominant market position, and passed. "Why buy a warehouse operator in Minnesota when we own electronics retail?" they reasoned. It was the retail equivalent of Blockbuster passing on Netflix.

By 1990, Circuit City was the undisputed emperor of consumer electronics, operating 200+ stores and generating $2 billion in annual revenue. Their "Superstore" format, launched in 1975, had crushed regional competitors from coast to coast. They pioneered commissioned sales, extended warranties, and in-house financing—the trinity of electronics retail profitability. CEO Rick Sharp was featured on magazine covers as the merchant prince of the new economy.

But Best Buy was playing a different game entirely. While Circuit City built marble-floored showrooms with mood lighting and salespeople in ties, Best Buy kept opening warehouses. While Circuit City's commissioned sales force averaged $50,000 annual salaries, Best Buy paid hourly wages to college kids in blue polo shirts. The contrast was stark: shopping at Circuit City felt like buying a car; shopping at Best Buy felt like buying groceries.

The first direct confrontation came in Chicago in 1989. Circuit City had dominated the market for years, but Best Buy opened three superstores simultaneously—a retail blitzkrieg that grabbed 30% market share within 18 months. Circuit City's response revealed their fundamental misunderstanding: they offered bigger commissions to their salespeople, assuming customers needed more "guidance" to make purchase decisions. Best Buy just cut prices further.

By 1995, the war had gone national. Best Buy and Circuit City were locked in a real estate arms race, each trying to secure the best locations in every major market. The battles were fierce and sometimes absurd—both companies would sometimes open stores directly across the street from each other, turning suburban strip malls into electronics battlegrounds. The casualty list grew: Highland Superstores, Incredible Universe, Nobody Beats the Wiz—all crushed between the two titans.

The late 1990s brought a technological disruption that would tip the scales decisively: the Digital Versatile Disc. In 1998, Best Buy became the first major retailer to sell DVDs and DVD players, beating Circuit City to market by six crucial months. While Circuit City's buyers debated whether this new format would succeed, Best Buy went all-in, dedicating massive floor space to DVDs and pricing players at break-even to drive adoption.

The DVD decision exemplified the strategic differences between the companies. Circuit City, run by merchants trained in the high-margin appliance business, couldn't understand selling products at cost. Best Buy, shaped by Schulze's tornado sale mentality, understood that today's loss leader was tomorrow's ecosystem. Every DVD player sold meant years of DVD purchases—and customers returning to Best Buy rather than Circuit City.

Meanwhile, Best Buy was quietly building capabilities that would prove decisive. Their inventory management system, developed in partnership with Accenture, could track product movement in real-time across all stores. While Circuit City managers still faxed weekly sales reports to headquarters, Best Buy executives could see hourly sales data and adjust inventory accordingly. This meant Best Buy rarely ran out of hot products while Circuit City's shelves gathered dust with last year's models.

The acquisition spree began in 2000. Best Buy purchased Magnolia Hi-Fi for $88 million, adding high-end audio expertise. In 2001, they acquired Musicland Stores Corporation for $425 million, instantly becoming America's largest music retailer. Future Shop in Canada followed for $368 million. But the masterstroke came in 2002: acquiring Geek Squad for a mere $3 million.

Geek Squad was tiny—just 60 employees fixing computers in a handful of cities. But Best Buy saw what others missed: as technology became central to American life, installation and repair services would become as valuable as the products themselves. Within five years, Geek Squad would employ 20,000 "agents" and generate over $1 billion in annual revenue—a 300x return on investment.

Circuit City's response to Geek Squad revealed their doom. They launched "Firedog" in 2006—a blatant copycat with a terrible name and worse execution. While Geek Squad agents drove Volkswagen Beetles and cultivated a quirky, approachable brand, Firedog felt corporate and sterile. Customers didn't want their computers fixed by a "Firedog technician"—they wanted the Geek Squad.

By 2007, the war was effectively over. Best Buy operated 900 stores generating $35 billion in revenue. Circuit City, despite its head start and first-mover advantage, had fallen behind on every metric: sales per square foot, inventory turns, customer satisfaction, and most critically, profitability. The company that had the chance to buy Best Buy for $30 million now watched its competitor's market cap exceed $20 billion.

The denouement came swift and brutal. In November 2008, amid the financial crisis, Circuit City filed for bankruptcy. By March 2009, all 567 stores were closed, 34,000 employees were terminated, and the second-largest electronics retailer in America simply ceased to exist. Best Buy had won the war so decisively that they inherited Circuit City's entire market share almost overnight.

Standing in 2009, Best Buy looked invincible. They had vanquished Circuit City, absorbed dozens of smaller competitors, and built a vertically integrated electronics empire. Schulze's warehouse concept had evolved into the definitive model for electronics retail. But a new threat was emerging from Seattle, one that would make the Circuit City wars look like a preliminary bout. Amazon was coming, and this time, Best Buy's physical stores wouldn't be an advantage—they'd be an anchor.

V. International Ambitions & Strategic Missteps (2006–2011)

Flush with victory from the Circuit City wars, Best Buy's leadership looked at their domestic dominance and asked the dangerous question that has destroyed countless American retailers: "Why can't we do this everywhere?" The board, drunk on success and facing market saturation in the U.S., approved an international expansion strategy that would ultimately burn billions and teach painful lessons about the limits of retail imperialism.

The China gambit began in May 2006 with the $180 million acquisition of Jiangsu Five Star Appliance, a regional player with 136 stores. The logic seemed bulletproof: China's middle class was exploding, consumer electronics adoption was accelerating, and Best Buy's superstore model had crushed competitors everywhere it went. They'd be the Circuit City of China, except this time they'd be first.

The first Best Buy-branded store opened in Shanghai in January 2007, a gleaming 86,000-square-foot temple to consumer electronics in the Xujiahui district. Executives flew in from Minneapolis for the grand opening, watching thousands of curious Chinese consumers stream through the doors. The early sales numbers looked promising. The press coverage was glowing. Everything was going according to plan.

Except it wasn't. Chinese consumers, it turned out, didn't shop for electronics like Americans. They didn't browse—they researched extensively online then negotiated aggressively in person. They didn't trust fixed prices—haggling was both expected and enjoyed. They didn't want sprawling selections—they wanted specific brands at the lowest possible price. Best Buy's entire model, built on self-service and non-negotiable pricing, was antithetical to Chinese retail culture.

While Best Buy struggled with cultural translation, local competitors like Gome and Suning were eating their lunch. These Chinese retailers understood that electronics shopping in China was a social experience. Their stores were cramped, chaotic, and loud—everything Best Buy's weren't. Salespeople fought for customers' attention, prices changed hourly, and buying a television was an event involving extended family consultations. Best Buy's quiet, organized stores felt sterile and unwelcoming by comparison.

But China was just the appetizer for international disaster. In December 2008, with the financial crisis ravaging global markets, Best Buy made its boldest and ultimately most catastrophic move: spending $2.1 billion for a 50% stake in Carphone Warehouse's European retail business. The plan was to bring American-style big-box electronics retail to Europe, starting with the United Kingdom.

The timing alone should have killed the deal. Lehman Brothers had collapsed three months earlier. Consumer spending was cratering worldwide. The pound was in freefall. But Best Buy's board, perhaps suffering from deal fever, pressed ahead. They would launch Best Buy UK as a joint venture with Carphone Warehouse, combining American scale with local knowledge.

The first Best Buy UK store opened in Thurrock in April 2010, followed quickly by ten more locations across greater London and the Midlands. The stores were massive—40,000 square feet of gleaming displays, interactive demonstrations, and helpful blue-shirted associates. They looked exactly like successful Best Buy stores in suburban Minneapolis or Dallas. That was precisely the problem.

British consumers looked at Best Buy UK and saw American excess. The stores were too big for a country where most people lived in small flats. The parking lots were too large for a nation that relied on public transport. The product selection was baffling—why did anyone need seventeen different television brands? Meanwhile, local competitors like Currys and Argos, despite inferior stores and service, understood British shopping habits: research online, reserve for pickup, minimal browsing.

The numbers were brutal. Best Buy UK lost £62 million in its first year, £75 million in its second. Same-store sales never exceeded 60% of projections. The Thurrock flagship, built for 1,000 customers daily, averaged fewer than 300. By November 2011, just 18 months after the grand opening, Best Buy announced the closure of all eleven UK stores. The European experiment was over.

The retreat from China came simultaneously. In February 2011, Best Buy closed all nine branded stores, merging operations with Five Star. The company that was supposed to conquer Chinese retail barely lasted four years. The accumulated losses from international operations exceeded $500 million, not counting the opportunity cost of management attention and capital that could have been deployed domestically.

The international implosion revealed uncomfortable truths about Best Buy's model. The company's success wasn't just about superior operations or better pricing—it was intrinsically tied to American consumer culture, suburban geography, and specific shopping behaviors that didn't translate globally. The superstore that conquered Minneapolis and Chicago was alien in Shanghai and London.

But the international failures were symptoms of a larger disease. While Best Buy was burning cash overseas, a more existential threat was metastasizing at home. Amazon's revenue had grown from $10 billion to $34 billion between 2006 and 2010. Every quarter, more Americans were buying electronics online. The international adventures hadn't just failed—they'd distracted Best Buy from the fight that actually mattered.

By 2011, Best Buy was in full retreat. International expansion was dead. Domestic same-store sales were declining. The stock price had fallen 40% from its 2006 peak. And somewhere in Seattle, Jeff Bezos was looking at Best Buy's 1,000+ stores not as assets but as opportunities—expensive showrooms where customers could touch products before buying them cheaper on Amazon. The existential crisis was about to begin.

VI. The Near-Death Experience (2008–2012)

The term "showrooming" entered the retail lexicon in 2010, but Best Buy employees had been watching it happen for years. A customer would walk in, spend forty minutes with a blue shirt learning about television specifications, carefully examine display models, maybe even watch a demonstration—then pull out their phone, scan the barcode, and order it from Amazon while still standing in the store. The Best Buy associate would watch their commission-free hourly wage job transform into unpaid labor for Jeff Bezos.

The numbers were devastating. Between 2008 and 2012, Best Buy's same-store sales declined for four consecutive years. Margins compressed from 25% to 19%. The stock price cratered from $53 to $11. Wall Street analysts competed to write the cleverest obituary. "Best Buy is gradually becoming a showroom for Amazon," wrote Colin McGranahan of Bernstein Research, coining a phrase that would haunt the company.

The perfect storm had multiple fronts. The 2008 financial crisis crushed consumer spending just as Best Buy needed resources to fight Amazon. Circuit City's bankruptcy in 2009, rather than providing relief, actually accelerated the digital shift—customers who might have gone to Circuit City didn't default to Best Buy; they went online. Meanwhile, manufacturers like Apple started opening their own stores, cherry-picking the highest-margin customers Best Buy desperately needed.

Inside Best Buy headquarters in Richfield, Minnesota, the response was paralysis masquerading as action. Management launched initiative after initiative—Best Buy Mobile to capture phone sales, Best Buy Connect for home services, Best Buy Express for airports—each one a expensive distraction from the core problem. The company was being disrupted and had no idea how to respond beyond doing more of what wasn't working.

Then, in April 2012, the scandal broke that would nearly deliver the killing blow. CEO Brian Dunn, hand-picked successor to founder Dick Schulze, abruptly resigned amid an internal investigation. Within days, the details leaked: Dunn had been conducting an inappropriate relationship with a 29-year-old female employee. Worse, founder and chairman Schulze knew about it and failed to inform the board.

The investigation's findings were damning. Dunn had used company resources to facilitate the relationship. Schulze, the man who built Best Buy from nothing, had violated his fiduciary duty by covering for his protégé. The board forced Schulze to resign as chairman—imagine Steve Jobs being forced out of Apple, except Apple was already dying. The company lost both its CEO and founding chairman in the span of weeks, just as it faced existential threat.

The leadership vacuum was filled by interim CEO Mike Mikan, whose primary qualification seemed to be availability. Morale cratered. Store managers openly discussed which competitors were hiring. The company's Net Promoter Score—a measure of customer loyalty—fell to negative territory, meaning more customers were warning friends away from Best Buy than recommending it. Best Buy was dying in real-time, and everyone could see it.

The stock market certainly could. By August 2012, Best Buy's market capitalization had fallen to $5.5 billion—less than the company's annual revenue. Wall Street was literally valuing Best Buy at less than the cash it generated, a clear vote of no confidence in any future. Credit default swaps on Best Buy's debt—essentially insurance against bankruptcy—spiked to levels suggesting a 40% chance of default within two years.

Meanwhile, Schulze wasn't going quietly. In August 2012, he announced plans to take Best Buy private in a leveraged buyout, partnering with private equity firms to raise $8 billion. The offer was both a lifeline and an insult—the founder thought his company was worth saving but only if he could run it again. The board was trapped between a founder they'd just fired trying to buy the company and a business model that appeared irreversibly broken.

The employee experience during this period was particularly brutal. Store associates watched customers use Best Buy as Amazon's showroom daily. They knew the products, provided expert advice, and offered genuine service—none of which mattered when Amazon was 20% cheaper. Many employees started quietly recommending that customers buy online, figuring honesty might at least preserve some dignity in defeat.

By September 2012, Best Buy looked like a corporate death spiral case study. Leadership was in chaos, strategy was non-existent, employees were demoralized, customers were defecting, and the stock was in free fall. The company that had killed Circuit City was about to join it in retail heaven. The board, desperate and out of options, decided to take one last gamble on an outsider CEO who'd never worked a day in retail.

The board's choice was so unexpected that when it leaked, Best Buy's stock actually fell further. Hubert Joly, a French executive who'd run hospitality and travel companies, was named CEO. The reaction from retail experts was brutal. "What does a hotel guy know about fighting Amazon?" asked one analyst. "Best Buy just signed its own death warrant," declared another. When Joly called friends to share the news, they universally told him he was crazy to take the job.

What nobody knew was that Joly had a radical theory about Best Buy's problem. It wasn't that the company's stores were obsolete—it was that nobody had figured out how to make them relevant. The conventional wisdom said Best Buy needed to close stores, cut costs, and somehow out-Amazon Amazon. Joly believed the opposite: Best Buy's stores weren't the problem; they were the solution. He just had to figure out how.

VII. The Hubert Joly Turnaround: Renew Blue (2012–2019)

Hubert Joly's first day as CEO of Best Buy wasn't spent in the executive suite in Richfield. It wasn't spent with Wall Street analysts or strategic consultants. The French executive who'd never worked retail spent it in a Best Buy store in St. Cloud, Minnesota, wearing a blue polo shirt and a name tag that said "Hubert: CEO in Training."

For a week, Joly worked the floor. He helped confused grandmothers pick out tablets. He hauled televisions to customers' cars. He stood helplessly as customers showroomed products on their phones. He listened to employees explain why the company's systems were broken, why the website didn't match store inventory, why they had to tell customers "I don't know" a dozen times each shift. One veteran associate told him bluntly: "We all know we're going to die. We're just waiting for you to tell us when."

This wasn't corporate theater. Joly had a hypothesis that would have gotten him laughed out of any strategy consulting firm: Best Buy's problem wasn't its business model—it was that the company had forgotten its purpose. "Everybody thought we were going to die," Joly would later recall. "The board thought we were going to die. The employees thought we were going to die. I had friends calling me saying 'Hubert, are you crazy?' But walking those stores, talking to those people, I saw something different. I saw human potential being wasted."

In November 2012, Joly unveiled "Renew Blue," his turnaround strategy. The name itself was telling—not "Digital Transformation" or "Store Rationalization" but renewal, implying Best Buy had strengths worth preserving. The plan had five pillars, but the first one shocked everyone: reinvest in stores and employees. While every retail consultant preached cutting costs and closing locations, Joly wanted to spend more on the very assets Wall Street considered liabilities.

The price-matching announcement came first and hit like thunder. Best Buy would match any price from any competitor, including Amazon, no questions asked. The CFO warned it would destroy margins. The board worried about a race to the bottom. Analysts called it surrender. But Joly understood something crucial: showrooming only worked because of price anxiety. Remove the price difference, and suddenly Best Buy's immediate availability and human expertise became advantages, not overhead.

The operational improvements were unglamorous but revolutionary. Best Buy's website and store inventory systems didn't communicate—online might show a product available that stores didn't have, or vice versa. Fixing this basic infrastructure took eighteen months and $400 million, but it eliminated the customer fury of driving to a store for a product that didn't exist. "We were breaking $200 million worth of TVs every year through shipping damage," Joly discovered. "By improving packaging, we reduced that by 50 percent. That's $100 million straight to the bottom line from bubble wrap."

But the masterstroke was transforming Best Buy from competitor to platform. Rather than fight Apple, Samsung, Microsoft, and Google, Joly invited them in. Best Buy would create store-within-store boutiques where these brands could showcase products with their own aesthetic and trained specialists. The vendors would pay for the space, the training, and even some of the labor. Best Buy would get guaranteed traffic, vendor support, and most critically, exclusive products and pricing that Amazon couldn't match.

The vendor partnerships went deeper than retail. When Samsung wanted to understand why certain TVs weren't selling, Best Buy's floor associates had the answers. When Microsoft needed feedback on Surface tablets, Best Buy provided real customer insights. When Apple needed someone to help customers transfer data from Android phones, Best Buy's employees became unofficial Apple support. The companies that were supposedly disrupting Best Buy became dependent on it for customer intelligence and service delivery.

The Geek Squad transformation exemplified Joly's human-centered approach. Rather than cut the service as an expensive anachronism, he expanded it dramatically. Geek Squad agents became "Chief Technology Officers" for customers' homes, offering everything from TV mounting to smart home installation to tech support subscriptions. The service that Best Buy bought for $3 million was generating $2 billion annually by 2018—a 667x return that would make any venture capitalist weep.

Employee investment was perhaps the most counterintuitive element. While other retailers were cutting wages and benefits, Joly raised Best Buy's minimum wage, expanded training programs, and created career advancement paths. "You never start with finance," Joly explained. "You start with people. The frontline employees are the ones who create the customer experience. If they're miserable, your customers will be miserable. If they're engaged, magic happens."

The financial engineering was equally bold. Best Buy used its stores as mini-warehouses, shipping online orders from the nearest location rather than central distribution centers. This cut delivery times from a week to one day in many markets, neutralizing Amazon's Prime advantage. The company's 1,000 stores suddenly became 1,000 distribution nodes, turning supposed liabilities into logistical assets that even Amazon envied.

The results defied every prediction. Same-store sales grew for five consecutive years starting in 2013. Online revenue doubled to $6.5 billion. The Net Promoter Score went from negative to industry-leading. Operating margins expanded despite price matching. The stock price rose from $11 in 2012 to $58 by 2017—a 427% gain that crushed every retail peer and most tech stocks.

But the numbers only told part of the story. Best Buy had achieved something supposedly impossible: it had made physical retail relevant in the age of Amazon. When customers needed a laptop that day for a presentation tomorrow, Best Buy had it. When grandparents couldn't figure out their new iPhone, Geek Squad helped. When someone wanted to actually see how a 65-inch TV would look before spending $2,000, Best Buy provided that experience.

The partnership model reached its apex with an announcement that would have been unthinkable in 2012: Amazon would open boutiques inside Best Buy stores, selling Echo devices and Fire TVs. The company that was supposed to kill Best Buy was now paying rent to it. Jeff Bezos needed Best Buy's physical presence to showcase products that required demonstration. The student had become the teacher, or perhaps they'd become something new entirely—co-opetitors in a retail landscape neither could dominate alone.

By 2019, when Joly handed the CEO role to protégé Corie Barry, Best Buy's transformation was complete. The company that everyone thought would die had instead redefined what physical retail could be in the digital age. Revenue hit $42 billion. The stock traded at $75. Best Buy employed 125,000 people who weren't just surviving but thriving. The French executive who knew nothing about retail had saved American retail's least likely survivor.

Joly's parting wisdom captured the essence of the turnaround: "We didn't try to be Amazon. We didn't try to be Apple. We became the best version of Best Buy—a company with a noble purpose to enrich lives through technology. When you're clear about your purpose and you unleash human potential, amazing things happen. That's not business strategy—that's human truth."

VIII. Modern Era: The Pandemic Boom & Beyond (2019–Present)

Corie Barry's CEO appointment in June 2019 represented continuity with ambition. A Best Buy lifer who'd started as a financial analyst in 1999, Barry had been Joly's strategic architect, engineering the vendor partnerships and omnichannel operations that powered the turnaround. Her pitch to the board was evolution, not revolution: Best Buy had proven stores mattered, now it needed to prove they were essential.

Nobody could have predicted that nine months later, a global pandemic would test that thesis with existential force.

March 2020 arrived like a tornado—sudden, devastating, and transformative. Within 72 hours, Best Buy went from normal operations to crisis mode. Stores were forced to close to customers. Employees were sent home. The stock market crashed. Analysts immediately downgraded Best Buy, assuming a consumer electronics retailer dependent on physical stores couldn't survive lockdowns. The stock fell 40% in three weeks.

Barry's response revealed the resilience Joly had built into Best Buy's DNA. Within days, the company pivoted to curbside pickup only—a capability that existed but had never been tested at scale. Employees who'd been selling TVs became personal shoppers, taking phone orders and running products to parking lots. The Geek Squad pivoted to virtual consultations, walking customers through router setups via video chat. The website, rebuilt during the Joly years, handled a 250% surge in traffic without crashing.

The pandemic revealed something nobody had anticipated: Best Buy wasn't just convenient—it was critical infrastructure. When millions of Americans suddenly needed to work from home, they needed laptops, monitors, and webcams immediately, not in two days via Amazon Prime. When schools went virtual, parents needed tablets for their kids that afternoon. When grandparents needed to video chat with family, they needed someone to help them set it up. Best Buy became the emergency room of the work-from-home economy.

The numbers were staggering. Q2 2020 online sales grew 242% year-over-year. Curbside pickup, which barely existed before March, accounted for 40% of online revenue by May. Despite stores being closed to browsing for months, comparable sales grew 5.8% for the full year. Best Buy gained market share in every major category—something that wasn't supposed to happen during a pandemic that theoretically advantaged pure-play online retailers.

But Barry saw beyond the pandemic boom. While competitors hired aggressively to meet surging demand, she maintained discipline, knowing the work-from-home gold rush wouldn't last forever. When stimulus checks drove television sales to record heights, she didn't expand floor space, understanding these were pulled-forward purchases, not sustainable growth. This discipline would prove prescient when demand normalized in 2022, leaving Best Buy healthier while competitors struggled with bloated cost structures.

The post-pandemic period brought new challenges that tested Barry's strategic vision. Inflation hit consumer electronics hard—when groceries cost 20% more, that TV upgrade could wait. The work-from-home boom reversed as offices reopened, crushing demand for home office equipment. Supply chain disruptions made inventory planning nearly impossible. By 2023, same-store sales were declining again, and Wall Street's pandemic enthusiasm evaporated.

Barry's response was to double down on what differentiated Best Buy: services and experiences that pure-play online retailers couldn't match. The company launched totaltech, a $199 annual membership program that included unlimited tech support, extended warranties, and exclusive member pricing. Within two years, totaltech had 5 million members generating $1.5 billion in recurring revenue—transforming Best Buy from transaction-based retailer to subscription service provider.

The healthcare initiative represented Barry's boldest bet. Best Buy acquired Current Health and began positioning itself at the intersection of technology and aging. The thesis was compelling: as Baby Boomers aged, they'd need technology to remain independent—medical alert devices, remote monitoring systems, smart home health tools. Best Buy's combination of Geek Squad expertise, national footprint, and trusted brand could make it the gateway for healthcare technology adoption.

In 2024, Best Buy made another strategic pivot that would have seemed impossible during the dark days of 2012: relaunching its third-party marketplace. The company had tried and failed with a marketplace from 2011 to 2016, but the landscape had changed. Best Buy now had the digital infrastructure, the customer trust, and most importantly, the fulfillment capabilities to compete with Amazon's marketplace while offering something Amazon couldn't: the option for customers to see products in stores before buying from third-party sellers.

The announcement in January 2025 that the marketplace would relaunch by summer represented a full-circle moment. Best Buy was no longer defending against digital disruption—it was embracing it while maintaining its physical advantage. Third-party sellers would get access to Best Buy's customer base and optional fulfillment services. Best Buy would get expanded selection without inventory risk. Customers would get the best of both worlds: infinite selection with local availability.

The Canadian expansion through Best Buy Express, launched in 2024 via rebranded Source stores operated by BCE, showed Barry's pragmatic approach to growth. Rather than repeat the international disasters of 2006-2011, Best Buy licensed its brand and systems while letting local operators handle day-to-day management. It was expansion without exposure, growth without the crushing capital requirements that had nearly killed the company before.

Looking at Best Buy in 2025, the transformation is complete yet ongoing. The company that was supposed to be Amazon's victim has instead become something unprecedented: a physical retailer that thrives because of digital commerce, not despite it. With $43 billion in revenue, 90,000 employees, and a market cap approaching $20 billion, Best Buy has achieved what Circuit City, RadioShack, and countless others couldn't: relevance in the age of Amazon.

But challenges remain acute. Consumer electronics spending remains pressured by inflation. The product refresh cycles that drive upgrades—new gaming consoles, innovative smartphones, revolutionary TVs—have slowed. Amazon continues to gain share in categories Best Buy once dominated. The commercial real estate footprint that became an asset during the pandemic could become an anchor if shopping patterns shift again.

Barry's Best Buy is betting that the future of retail isn't physical or digital—it's both, delivered seamlessly based on customer preference. Need a phone today? Store pickup in an hour. Want to browse? Come touch and feel products with expert guidance. Confused by setup? Geek Squad will handle it. Prefer delivery? It'll come from the nearest store, possibly within hours. This omnichannel excellence, powered by human expertise and vendor partnerships, is Best Buy's moat against digital disruption.

The pandemic proved Best Buy's stores weren't just relevant—they were essential. The question now is whether that essentiality was a crisis-driven anomaly or a sustainable competitive advantage. Barry's bet, backed by billions in investment and decades of survival, is that in an increasingly digital world, human connection and physical presence become more valuable, not less.

IX. Playbook: Business & Investing Lessons

The Power of Retail Reinvention vs. Retail Rigidity

The Best Buy-Circuit City divergence offers a masterclass in organizational adaptability. Both companies faced identical market forces—Amazon's rise, margin compression, changing consumer behavior—yet produced opposite outcomes. Circuit City died clinging to commissioned sales and extended warranties; Best Buy survived by abandoning its original model entirely. The lesson isn't that change guarantees survival, but that rigidity guarantees death.

Consider the commissioned sales decision. Circuit City's entire P&L depended on salespeople pushing high-margin accessories and warranties. When Best Buy eliminated commissions, Circuit City's executives literally couldn't comprehend it—their financial models broke without 40% warranty attachment rates. They saw Best Buy's model as unsustainable charity. But Best Buy understood something profound: when you remove the adversarial dynamic from retail, customers buy more, return less, and most importantly, come back.

The real insight is that business model innovation in retail isn't about technology or operations—it's about aligning incentives with customer psychology. Circuit City optimized for extracting maximum revenue per transaction; Best Buy optimized for lifetime customer value before that term existed. One model scales with trust; the other destroys it.

Human-Centered Turnarounds: Why Joly Succeeded Where Traditional Playbooks Failed

Every turnaround consultant would have given Best Buy the same prescription in 2012: close stores, cut costs, reduce headcount, and focus on digital. Joly did the opposite—investing in stores, raising wages, and expanding services. The conventional wisdom said he was insane. The results suggest the conventional wisdom misunderstands what companies actually are.

"In a turnaround, you have to create energy," Joly explained. "A company is a human organization made up of individuals working together in pursuit of a goal." This sounds like management seminar pablum until you examine what he actually did. While competitors treated employees as costs to minimize, Joly treated them as assets to unleash. A Best Buy employee who understands customer needs and feels valued becomes a competitive advantage Amazon can't replicate.

The wage increases weren't charity—they were ROI calculations. Best Buy's employee turnover fell from 50% to 30% during Joly's tenure. At $5,000 per employee to recruit and train replacements, reducing turnover by 20 percentage points across 50,000 store employees saved $50 million annually. Higher wages cost $30 million. The math was simple once you looked at employees as investments rather than expenses.

The "Coopetition" Model: Enemies as Ecosystems

Joly's masterstroke wasn't fighting Amazon, Apple, and Google—it was recognizing they needed Best Buy as much as Best Buy needed them. When Amazon opens boutiques in your stores, when Apple pays for dedicated floor space, when Samsung funds your employee training, you've transformed from competitor to platform.

This required abandoning retail's zero-sum mentality. Traditional retailers see vendors as suppliers to squeeze and competitors as enemies to destroy. Joly saw them as ecosystem partners with aligned interests. Samsung wanted to sell TVs; Best Buy wanted to sell TVs; customers wanted to buy TVs. Instead of fighting over margin points, why not collaborate to grow the pie?

The vendor boutiques generate $2 billion in annual revenue while vendors pay for space, labor, and training. Best Buy gets guaranteed traffic, exclusive products, and marketing support. Vendors get customer insights, demonstration capabilities, and service infrastructure. Customers get better experiences. This isn't just win-win; it's win-win-win—the hallmark of sustainable business model innovation.

Store-as-a-Platform: From Product Seller to Experience Provider

Best Buy's stores in 2012 were liabilities—expensive real estate boxes filled with depreciating inventory. Today, they're platforms that monetize in seven different ways: product sales, service revenue, vendor rent, membership fees, fulfillment services, installation revenue, and data insights. The physical footprint didn't change; the business model built on top of it transformed completely.

Consider a single transaction: A customer buys a Samsung TV. Samsung pays for the boutique space. Best Buy earns product margin. Geek Squad installs it for $199. The customer joins totaltech for ongoing support. The store fulfills three online orders while the customer browses. Vendor partners receive aggregated shopping pattern data. One visit, seven revenue streams—that's platform thinking applied to physical retail.

The lesson extends beyond retail: any asset becomes more valuable when you stop thinking about its primary use case and start imagining complementary monetization. Best Buy's stores were designed to sell products; now they're showrooms, warehouses, service centers, event spaces, and marketing platforms simultaneously.

Omnichannel Excellence: Using Stores as Mini-Warehouses

The conventional wisdom in 2010 was that online and offline retail were separate businesses requiring different capabilities. Best Buy proved they're actually the same business experienced differently. The breakthrough was recognizing stores weren't competing with the website—they were fulfillment nodes that made the website better.

When Best Buy started shipping online orders from stores instead of central warehouses, delivery times dropped from 5-7 days to 1-2 days for 70% of the population. Inventory turns improved because products weren't sitting in warehouses. Shipping costs decreased because packages traveled shorter distances. Customer satisfaction increased because they got products faster. The stores that were supposed to be obsolete became competitive advantages.

This omnichannel excellence requires operational complexity that pure-play retailers can't match. Amazon has to build warehouses near cities; Best Buy already has stores there. Amazon has to predict inventory needs weeks in advance; Best Buy can shift products between stores in hours. The physical infrastructure that was supposed to kill Best Buy became the moat protecting it.

Purpose-Driven Profits: The Power of Noble Intent

"We will do well by doing good" sounds like corporate PR speak until you examine Best Buy's actual decisions. When the pandemic hit, Best Buy could have price gouged on suddenly-essential work-from-home equipment. Instead, they maintained prices and expanded access. When semiconductor shortages created scarcity, Best Buy implemented fair allocation systems instead of auction dynamics. When customers needed help setting up technology for remote learning, Geek Squad provided free consultations.

These decisions built trust that translated into financial returns. Best Buy's Net Promoter Score went from negative in 2012 to industry-leading by 2019. Customer acquisition costs dropped as word-of-mouth referrals increased. Vendor partners offered better terms because they knew Best Buy would protect their brand equity. Employees worked harder because they believed in the mission.

The lesson isn't that purpose replaces profits but that purpose drives profits when authentically implemented. Customers can sense the difference between marketing slogans and genuine values. In an age of infinite choice and perfect information, trust becomes the ultimate differentiator. Best Buy survived because when customers needed technology help during crisis, they remembered who had helped them before.

Capital Allocation: The Discipline of Saying No

For every successful initiative Best Buy launched, they killed three others. The company tested and abandoned: Best Buy Mobile standalone stores, Best Buy Express vending machines, Best Buy Connect home installation services, European expansion, Chinese expansion, and dozens of other "strategic initiatives" that consumed capital without generating returns.

The discipline to admit failure and cut losses is what separates survivors from casualties. Circuit City couldn't abandon commissioned sales because it was too invested. RadioShack couldn't close stores because of lease obligations. But Best Buy under Joly and Barry developed a culture of experimentation with brutal honesty about results. If something didn't work, they killed it fast and moved on.

This extends to capital structure decisions. Best Buy could have leveraged up to fund aggressive expansion or acquisitions. Instead, they maintained a conservative balance sheet that provided flexibility during crises. When COVID hit, Best Buy had the financial strength to maintain operations while competitors scrambled for liquidity. Boring balance sheet management enabled extraordinary strategic flexibility.

X. Analysis & Bear vs. Bull Case

Bull Case: The Last Fortress Standing

Best Buy isn't just surviving in the age of Amazon—it's thriving as the sole remaining big-box electronics retailer in a $420 billion market. With Circuit City, RadioShack, and CompUSA dead, Best Buy inherited an effective monopoly on physical electronics retail. The 1,000+ stores that analysts called liabilities have become moats that would cost competitors tens of billions to replicate.

The vendor partnership model creates switching costs that run deeper than consumer preference. Samsung, Apple, Microsoft, and Google have invested hundreds of millions in Best Buy boutiques, training programs, and exclusive product arrangements. These partnerships aren't easily transferable—they represent years of relationship building, systems integration, and operational refinement. When Apple needs someone to help customers switch from Android, they don't call Amazon; they call Best Buy.

The services business, anchored by Geek Squad, generates $3 billion in annual revenue with margins exceeding 30%—double the product margin. This isn't commoditized break-fix work but comprehensive technology consulting for increasingly complex home ecosystems. As homes get smarter and technology gets more integrated, the need for expert installation and support grows exponentially. Best Buy owns this market with 20,000 trained agents and decades of consumer trust.

Omnichannel capabilities provide sustainable advantage against pure-play competitors. Best Buy can offer one-hour pickup, same-day delivery, instant returns, and in-person support—services Amazon struggles to match despite unlimited capital. The ship-from-store model means Best Buy's inventory is always optimally positioned near customers. During peak seasons like Black Friday, when Amazon's delivery network strains, Best Buy's stores become differentiators.

The totaltech membership program, with 5 million subscribers paying $199 annually, creates predictable recurring revenue approaching $1 billion. These members spend 2.5x more than non-members and shop 3x more frequently. The lifetime value math is compelling: acquire a customer for $50, generate $500 annually for multiple years. This subscription layer transforms Best Buy's economic model from transactional to relational.

Demographics favor Best Buy's human-centered approach. As Baby Boomers age, they need help navigating increasingly complex technology. Millennials might be digital natives, but when they're buying a $3,000 TV or setting up a smart home, they want expert guidance. Gen Z values experiences and immediate gratification—both Best Buy strengths. The "death of physical retail" narrative ignores that humans remain physical beings who value tangible experiences.

Bear Case: The Slow Bleed of Structural Decline

The uncomfortable truth is that Best Buy's core categories face secular decline. Smartphone sales have plateaued as upgrade cycles extend from two to four years. Television innovation has slowed—the jump from 4K to 8K isn't compelling like HD to 4K was. Computer sales spike during refresh cycles then crater. Gaming consoles release every seven years. Best Buy is fundamentally tied to product categories with lengthening replacement cycles and declining innovation rates.

Amazon's threat compounds rather than diminishes over time. Every year, more consumers become comfortable buying electronics online without seeing them first. Amazon's private label electronics, from Fire TVs to Echo devices, directly compete with Best Buy's vendor partners. Prime membership, approaching 200 million globally, creates loyalty that Best Buy's totaltech can't match. When Amazon achieves same-day delivery at scale, Best Buy's speed advantage evaporates.

Price matching, while necessary for competitive parity, structurally destroys margins. Best Buy essentially allows competitors to set their prices—a dynamic that only worsens as price transparency increases. The company bears all the costs of physical stores, trained employees, and premium locations while matching the prices of online-only competitors with minimal overhead. This math eventually breaks.

Real estate represents an increasingly problematic fixed cost structure. Best Buy operates massive stores in expensive locations with long-term leases. As shopping patterns shift toward smaller format urban stores or pure online, these big boxes become anchors. The company has already shrunk average store size from 40,000 to 30,000 square feet, but lease obligations limit flexibility. If foot traffic continues declining, the store platform thesis collapses.

Vendor relationships, currently a strength, could become vulnerabilities. Apple, Samsung, and Microsoft increasingly sell direct-to-consumer through their own channels. They fund Best Buy boutiques today because they need physical presence, but as their own store networks expand, this need diminishes. The vendor partnership model assumes aligned interests that may diverge as partners become competitors.

The generational transition presents existential risk. Gen Z, the first truly digital-native generation, shows little attachment to physical retail. They research on TikTok, buy on apps, and value convenience over consultation. Best Buy's human expertise advantage means nothing to consumers who trust algorithm recommendations over salesperson guidance. As this generation becomes the primary consumer base, Best Buy's value proposition erodes.

The Verdict: Profitable Decline or Sustainable Niche?

Best Buy exists in a peculiar strategic position—too successful to die quickly but too constrained to grow meaningfully. The bull and bear cases aren't mutually exclusive; they're simultaneously true. Best Buy will likely remain profitable for years, possibly decades, serving customers who value immediate availability and human expertise. But that customer base shrinks annually while the cost of serving them remains fixed.

The company's strategic options are limited. Geographic expansion failed internationally and faces saturation domestically. Category expansion into healthcare and smart home services makes sense but won't offset declining electronics sales. Digital transformation is necessary but insufficient—Best Buy can't out-Amazon Amazon. The most likely path is managed decline: maintaining profitability through operational excellence while returning cash to shareholders.

This isn't necessarily a bad outcome for investors. Best Buy could generate $2-3 billion in annual free cash flow for the next decade while slowly shrinking its footprint. With a $20 billion market cap, that's a 10-15% cash yield—attractive in a world of zero interest rates. The company becomes a melting ice cube that melts slowly enough to be profitable.

The wildcard is technological disruption that reignites growth. Virtual reality, autonomous vehicles, or breakthrough consumer robotics could create new categories that benefit from Best Buy's demonstration and service capabilities. But betting on unknown future products to save a retailer is hope, not strategy.

XI. Epilogue & "What Would We Do?"

The ultimate lesson from Best Buy's survival isn't about retail strategy or digital transformation—it's about organizational resilience. The same company that rode the tornado sale to superstore dominance, crushed Circuit City through operational excellence, nearly died from Amazon disruption, then reinvented itself as a platform, demonstrates that corporate DNA matters more than market position.

Dick Schulze built adaptability into Best Buy's culture from the beginning. When that tornado destroyed his store in 1981, he didn't see disaster—he saw opportunity. That mindset, transmitted through decades and leaders, is why Best Buy survived while Circuit City, despite every advantage, collapsed. Companies aren't strategies or business models; they're collections of people making decisions. Best Buy's people consistently made better decisions.

If we were running Best Buy today, we'd embrace the reality that traditional consumer electronics retail is a declining business and pivot toward where technology and human needs intersect. Healthcare technology represents a $50 billion opportunity as America ages. Smart home installation and maintenance could generate recurring revenue streams. Business-to-business technology services for small companies lacking IT departments offers massive untapped potential.

The key insight is that Best Buy's asset isn't its inventory or real estate—it's trusted expertise at the intersection of humans and technology. Every technological advancement, from smartphones to smart homes to whatever comes next, requires translation for normal consumers. Best Buy's 90,000 employees represent the largest technology consultation force in America. That human capital, properly deployed, is invaluable.

We'd also radically reimagine the store footprint. Instead of 1,000 big boxes, we'd operate 500 experience centers in premium locations, 2,000 neighborhood consultation offices, and 10,000 pickup lockers. The experience centers would showcase cutting-edge technology—VR demos, smart home installations, gaming lounges. The consultation offices would offer Geek Squad services and product pickup in convenient locations. The lockers would enable instant gratification for online orders.

The subscription model needs aggressive expansion. Totaltech at $199 annually is underpriced for the value delivered. We'd create tiers: totaltech basic at $99 for support, totaltech plus at $299 for unlimited installations, totaltech premium at $599 for white-glove service. With 10 million members averaging $250 annually, that's $2.5 billion in recurring revenue with 40% margins—a business worth $20 billion on its own.

Most radically, we'd separate Best Buy into three companies: retail operations, services platform, and technology ventures. Retail operations would manage the declining but profitable electronics business. Services platform would build the Geek Squad ecosystem into the Uber of technology support. Technology ventures would invest in startups that need physical demonstration and service capabilities. This structure would allow each business to optimize independently while maintaining synergies.

The future of physical retail in an AI/AR world isn't about selling products—it's about creating experiences and solving problems. When AI assistants can answer any product question and AR can visualize any product in your space, the need for traditional retail disappears. But the need for human expertise, physical demonstration, and trust-based relationships intensifies. Best Buy's future isn't as a retailer but as a technology services platform that happens to sell products.

Why Best Buy Survived While Others Failed

Circuit City died because it couldn't abandon commissioned sales. RadioShack died because it couldn't escape mall leases. CompUSA died because it couldn't transition from computers to broader electronics. Each company faced disruption with rigid adherence to what had worked before. They optimized their way to extinction.

Best Buy survived because it repeatedly killed its own business model before competitors could. The tornado sale killed the specialty audio shop. Superstores killed the tornado sale model. Non-commissioned sales killed the superstore model. Vendor partnerships killed the adversarial supplier model. Omnichannel killed the pure physical retail model. Each transformation was painful, expensive, and risky. Each was also necessary.

The meta-lesson is that survival requires preemptive self-disruption. By the time market forces demand change, it's usually too late. Best Buy's leaders, from Schulze to Joly to Barry, consistently changed before they had to. They saw trends early and moved aggressively, accepting short-term pain for long-term positioning. This proactive evolution, not reactive adaptation, separates survivors from casualties.

But perhaps the deepest insight is about purpose and people. Best Buy survived because employees believed in something beyond quarterly earnings. When Joly talked about "enriching lives through technology," when Barry emphasized "building meaningful connections," they weren't spouting corporate speak. They were articulating why Best Buy matters in human terms. Companies that reduce themselves to financial engineering eventually engineer their own irrelevance. Companies that serve human needs with genuine purpose find ways to evolve and endure.

Best Buy's journey from Sound of Music to omnichannel platform spans nearly 60 years, multiple existential crises, and complete business model transformation. It's a story of resilience, adaptation, and the surprising durability of human expertise in an algorithmic age. Whether Best Buy thrives for another 60 years or slowly fades into retail history, its survival against overwhelming odds offers timeless lessons about leadership, strategy, and the fundamentally human nature of business.

The tornado that destroyed Dick Schulze's store in 1981 didn't just inspire a new retail model—it revealed a fundamental truth about business. Destruction creates opportunity for those willing to rebuild differently. Best Buy has been rebuilding differently ever since, and that, more than any strategy or tactic, explains why the last big box is still standing.

XII. Recent News

Based on the search results, here are the key recent developments for Best Buy:

Q4 FY25 Performance (March 2025)

Best Buy reported fourth-quarter revenue of $13.95 billion versus $13.70 billion expected, with adjusted earnings per share of $2.58 versus $2.40 expected. The company saw comparable sales rise 0.5% year over year for the quarter, marking the first positive comparable sales growth in several quarters.

Tariff Concerns and Price Outlook

CEO Corie Barry delivered a stark warning about pricing in the current political environment. On Best Buy's earnings call, Barry said price increases are "highly likely" after President Donald Trump's tariffs on China and Mexico go into effect, noting that China and Mexico are the company's top two supply chain sources, with about 55% and 20% of its products sourced from those countries, respectively. The company's FY26 guidance notably excludes any tariff impact.

The Marketplace Revolution (August 2025)

In a major strategic shift, Best Buy launched its digital marketplace on August 19, 2025, more than doubling the number of products available online and marking the largest expansion ever of Best Buy's product assortment. The marketplace, powered by Mirakl, adds entirely new brands, categories and products including seasonal décor, automotive tech, office and home, and movies and music.

This represents Best Buy's second attempt at a marketplace—the first ran from 2011 to 2016 but failed due to low sales and operational issues. The new platform is fundamentally different, with customers able to return products purchased through a Marketplace seller at their local Best Buy store, addressing one of the key pain points from the previous attempt.

Financial Outlook and Strategic Positioning

For fiscal 2026, the company issued full-year guidance of $41.4 billion to $42.2 billion in revenue and comparable sales growth of 0% to 2% year over year. The company continues to navigate a challenging environment where consumers remain "resilient but still dealing with high inflation that is driving expenses up across their lives, making them value focused and thoughtful about big ticket purchases," while still "willing to spend on high price point products when they need to or when there is technology innovation".

Q2 FY25 Turnaround Signals (August 2024)

Earlier in fiscal 2025, Best Buy showed signs of stabilization. The company reported Q2 earnings per share of $1.34 versus $1.16 expected and revenue of $9.29 billion versus $9.24 billion expected. Notably, Best Buy posted comparable sales growth of 6% in the domestic tablet and computing categories, driven by AI-enabled laptops and replacement cycles.

XIII. Links & Resources

Key Sources: - Best Buy Investor Relations: investors.bestbuy.com - Corporate News & Information: corporate.bestbuy.com - SEC Filings: sec.gov/edgar - Marketplace Platform: bestbuy.com/marketplace

Essential Reading: - "The Heart of Business" by Hubert Joly (2021) - Former CEO's account of the turnaround - "Good to Great to Gone" by Alan Wurtzel - Circuit City's perspective on the retail wars - McKinsey Retail Reports on omnichannel transformation

Notable Interviews & Analysis: - Hubert Joly Harvard Business Review interviews (2019-2021) - Corie Barry CNBC appearances on retail strategy - Wall Street analyst reports from Wedbush, Morgan Stanley on BBY

Industry Resources: - National Retail Federation reports on electronics retail - Consumer Technology Association market data - Gartner research on technology adoption cycles

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube