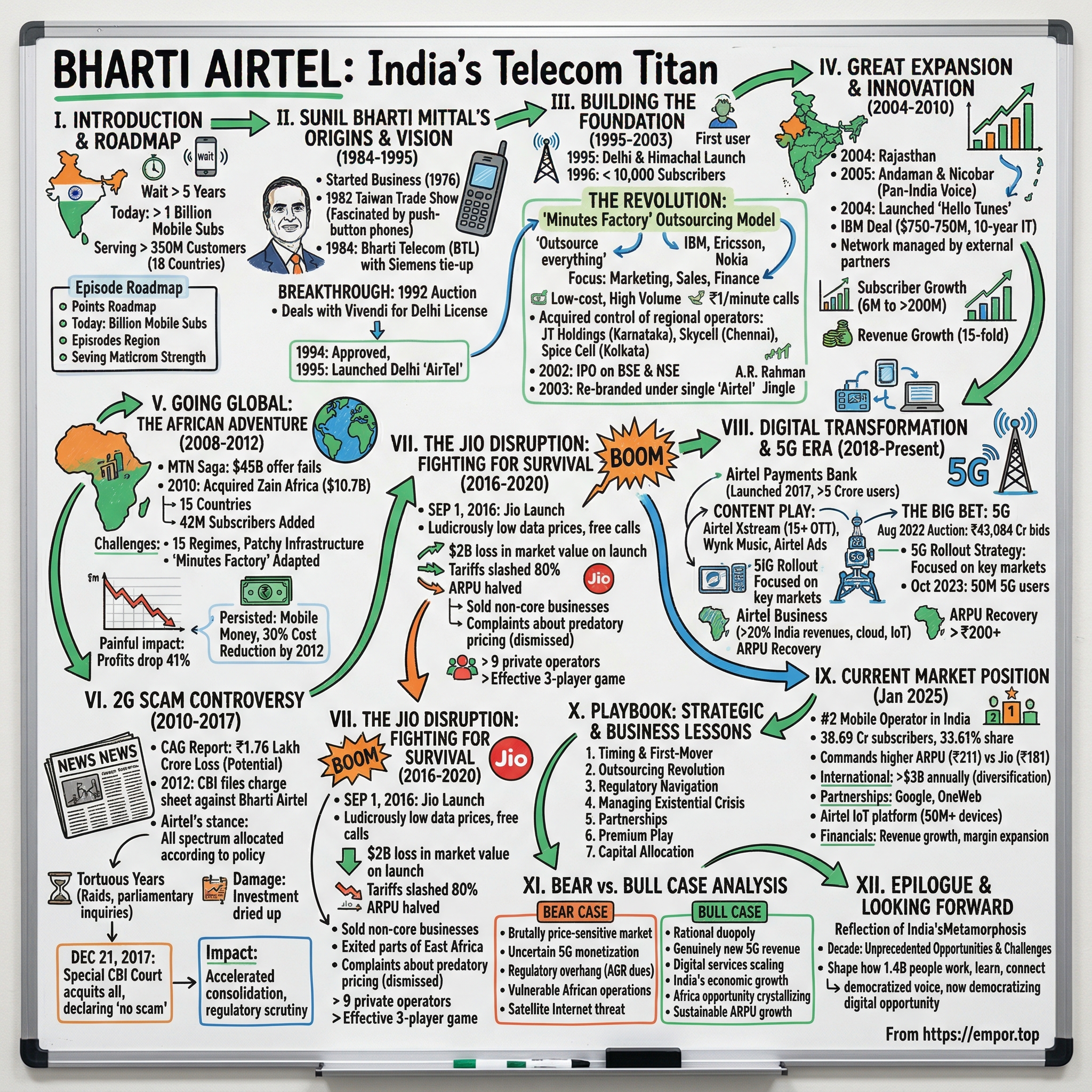

Bharti Airtel: India's Telecom Titan

I. Introduction & Episode Roadmap

Picture this: A nation of 1.4 billion people where, just three decades ago, getting a telephone connection required a five-year wait and knowing someone in government. Today, that same nation boasts over one billion mobile subscribers with data prices among the lowest in the world. At the heart of this transformation stands Bharti Airtel—a company that began by importing push-button phones and evolved into India's second-largest telecom operator, serving over 350 million customers across 18 countries.

The story begins in 1984 when a 27-year-old Delhi entrepreneur named Sunil Bharti Mittal attended a trade show in Taiwan. There, he saw a push-button phone for the first time in his life and became determined that he would bring the technology back to India. At that time, India's telecommunications landscape was a monument to inefficiency: rotary phones that barely worked, years-long waiting lists for connections, and a government monopoly that saw telecom as a luxury rather than necessity.

What unfolded over the next four decades is a masterclass in entrepreneurial vision, regulatory navigation, and sheer survival instinct. From launching India's first private mobile network in Delhi in 1995 to pioneering the revolutionary "minutes factory" outsourcing model that transformed global telecom economics, from aggressive international expansion into Africa to nearly being crushed by Jio's disruption in 2016—Airtel's journey mirrors India's own economic transformation.

This is a story about timing, tenacity, and transformation. It's about how a trading company pivoted into manufacturing, then services, then digital platforms. It's about surviving government investigations, weathering price wars that decimated competitors, and emerging stronger from existential threats. Most importantly, it's about how entrepreneurial vision can reshape not just a company or an industry, but an entire nation's trajectory.

II. Sunil Bharti Mittal's Origins & Early Vision (1984–1995)

Sunil Mittal started his first business in April 1976 at the age of 18, with a capital investment of ₹20,000 borrowed from his father. After ventures in bicycle parts and yarn factories, Mittal's life changed during a 1982 Taiwan trade show. Mittal was fascinated by push-button phones he saw there and wondered if he could introduce this technology in India, where rotary phones were still the norm.

The timing couldn't have been more perfect—or challenging. India's telecom sector in the early 1980s was a study in Soviet-style central planning gone wrong. A single landline connection could take five years to obtain. Making an international call required booking a trunk call hours in advance. The entire country had fewer than 2 million phone connections for 800 million people. But Mittal saw opportunity where others saw impossibility.

In 1984, he started assembling push-button phones in India through Bharti Telecom Limited (BTL), which entered into a technical tie-up with Siemens AG of Germany for the manufacture of electronic push-button phones. He named his first model 'Mitbrau'—a portmanteau reflecting the German partnership. By the early 1990s, Sunil was making fax machines, cordless phones and other telecom gear.

The real breakthrough came in 1992 when India's government, under economic liberalization, decided to auction four mobile phone network licenses. Mittal successfully bid for one of the four licenses, but faced a critical hurdle: one of the conditions for the Delhi cellular license was that the bidder have some experience as a telecom operator. So, Mittal clinched a deal with the French telecom group Vivendi.

What followed was a three-year regulatory marathon. His plans were finally approved by the Government in 1994 and he launched services in Delhi in 1995, when Bharti Cellular Limited (BCL) was formed to offer cellular services under the brand name AirTel. The brand name itself was carefully chosen—'Air' suggesting wireless freedom and 'Tel' maintaining the telecom connection.

The economics of that first launch were staggering by today's standards. Early mobile calls cost Rs 16 per minute for outgoing calls and Rs 8 per minute for incoming—when the average Indian's daily wage was less than Rs 100. A mobile handset cost Rs 45,000, equivalent to a small car. Yet Mittal understood something fundamental: this wasn't about serving the elite forever. This was about building infrastructure for India's inevitable economic transformation.

III. Building the Foundation: The Early Mobile Era (1995–2003)

Bharti Airtel launched mobile services during 1995-96 for the first time in Delhi and Himachal Pradesh. The early days were anything but smooth. With fewer than 10,000 subscribers in the first year, critics questioned whether mobile telephony had any future in a country where per capita income was less than $400.

But Mittal was playing a different game. Within a few years, Bharti became the first telecom company to cross the 2 million mobile subscriber mark. The key to this growth wasn't just expanding coverage—it was reimagining the entire business model.

The revolution began with pricing. Bharti brought down the STD/ISD cellular rates in India under the brand name 'IndiaOne'. But the real game-changer was what became known as the "minutes factory" model—arguably Airtel's greatest contribution to global telecom.

Here's how it worked: Instead of the traditional model where operators bought equipment upfront and managed everything in-house, Airtel outsourced everything except marketing, sales, and finance. Ericsson agreed for the first time to be paid by the minute for installation and maintenance of their equipment rather than being paid upfront, which allowed Airtel to provide low call rates of ₹1/minute.

Airtel is credited with pioneering the strategic management of outsourcing all of its business operations except marketing, sales and finance and building the 'minutes factory' model of low cost and high volumes. This wasn't just cost-cutting—it was a fundamental reimagining of what a telecom company should be. Why own towers when you could lease them? Why manage IT when IBM could do it better? Why maintain networks when equipment manufacturers had better expertise?

Strategic expansion followed. In 1999, Bharti Enterprises acquired control of JT Holdings, and extended cellular operations to Karnataka and Andhra Pradesh. In 2000, Bharti acquired control of Skycell Communications, in Chennai. In 2001, the company acquired control of Spice Cell in Kolkata.

The year 2002 marked a crucial milestone: Bharti Enterprises went public in 2002, and the company was listed on Bombay Stock Exchange and National Stock Exchange of India. The IPO was oversubscribed 7.5 times, signaling market confidence in Airtel's unconventional model.

By 2003, something remarkable had happened. In 2003, the cellular phone operations were re-branded under the single Airtel brand. From fragmented regional operations, Airtel had become India's first truly national mobile brand. The iconic A.R. Rahman jingle—that simple, memorable tune—became the soundtrack of India's mobile revolution, played 400 million times a day across the country.

IV. The Great Expansion & Innovation Phase (2004–2010)

In 2004, Bharti acquired control of Hexacom and entered Rajasthan. In 2005, Bharti extended its network to Andaman and Nicobar. This expansion allowed it to offer voice services all across India. Airtel had achieved what government-owned BSNL had taken decades to accomplish—true pan-India coverage.

But coverage was just the beginning. Innovation became Airtel's calling card. Airtel launched "Hello Tunes", a caller ring back tone service (Ringing Tone), in July 2004 becoming the first operator in India to do so. The Airtel theme song, composed by A.R. Rahman, was the most popular tune in that year.

The innovation wasn't just in consumer services. Airtel's outsourcing model evolved further. IBM took over complete IT operations in a 10-year deal worth $750-750 million. Networks were managed by Ericsson, Nokia, and Huawei. Even call centers were outsourced. Airtel essentially became a marketing and finance company that happened to be in telecom—a model studied in business schools worldwide.

In 2001, Airtel was the first private operator to launch mobile services in India. By 2010, mobile penetration in India had crossed 50%. Airtel had played a crucial role in this transformation, but the company's ambitions extended beyond Indian borders.

The introduction of 3G services in 2010 marked another significant milestone. By 2015, Bharti Airtel had launched 4G services across multiple regions. Each technology transition required billions in investment, but Airtel's asset-light model meant it could make these investments while maintaining healthy margins—at least for now.

The numbers told a remarkable story. From 2004 to 2010, Airtel's subscriber base grew from 6 million to over 200 million. Revenue increased fifteen-fold. The company that started by importing phones was now one of the world's five largest mobile operators by subscriber count. But Mittal wasn't satisfied with conquering India alone.

V. Going Global: The African Adventure (2008–2012)

The MTN saga reads like a corporate thriller. Financial Times reported that Bharti was considering offering US$45 billion for a 100% stake in MTN, which would be the largest overseas acquisition ever by an Indian firm. But there was a twist: the talks fell apart as MTN Group tried to reverse the negotiations by making Bharti almost a subsidiary of the new company.

After the MTN failure, most CEOs would have retreated. Mittal doubled down. In 2010, opportunity knocked again—this time from Kuwait. Zain, struggling with debt, was selling its African operations. In June 2010, Bharti acquired the African business of Zain Telecom for $10.7 billion, making it the largest ever acquisition by an Indian telecom firm and making Airtel the world's fifth largest wireless carrier by subscriber base.

The acquisition brought operations in 15 countries: Burkina Faso, Chad, Democratic Republic of the Congo, Republic of the Congo, Gabon, Ghana, Kenya, Madagascar, Malawi, Niger, Nigeria, Sierra Leone, Tanzania, Uganda and Zambia. Overnight, Airtel added 42 million subscribers and became a truly global player.

But Africa wasn't India. The challenges were immense: 15 different countries meant 15 different regulatory regimes, 15 different currencies, and 15 different competitive landscapes. Infrastructure was patchy—many areas lacked reliable electricity, let alone telecom towers. Governments were sometimes unstable. Local competitors knew the terrain better.

Airtel's response was to deploy the "minutes factory" model with local adaptations. Instead of replicating Indian operations, the company partnered with local entrepreneurs for distribution. The "recharge anywhere" model from India was adapted to Africa's mobile money ecosystem. Voice remained the primary service, unlike India's rapid shift to data.

The financial impact was immediate and painful. Net profits dropped by 41% from US$470 million in 2009 to US$291 million in 2010 due to a US$188 million increase in radio spectrum charges in India and an increase of US$106 million in debt interest. The Africa operations bled money for years, leading many to question whether this global ambition was Mittal's folly.

Yet Mittal persisted. By 2012, Airtel Africa was showing signs of turnaround. The company had introduced mobile money services, partnering with banks to provide financial services to the unbanked. It had reduced operational costs by 30% through the outsourcing model. Most importantly, it had learned to operate in challenging markets—a skill that would prove invaluable when disruption hit home.

VI. The 2G Scam Controversy & Its Aftermath (2010–2017)

In November 2010, India's telecom sector was rocked by what media called the "biggest scam in Indian history." The CAG report estimated that the exchequer lost Rs 1.76 lakh crore in potential revenue by selling 2G spectrum in 2008 at 2001 prices. The controversy centered on spectrum allocated during 2007-2008, but investigations expanded to examine allocations going back years.

For Airtel, the controversy was particularly sensitive. CAG found Sunil Mittal-led Bharti to be the biggest beneficiary, among private players, with 32.4 MHz in 13 circles, followed by Vodafone-Essar with 19.6 MHz. In December 2012, CBI filed charge sheet against Bharti Airtel for alleged irregularities in allocation of excess spectrum during the NDA regime, for causing loss of about Rs 846 crore to the national exchequer.

Airtel's defense was straightforward but firm. The company maintained that all spectrum was allocated strictly according to stated government policy at the time. Unlike some competitors who had allegedly obtained licenses through fraudulent means, Airtel had followed every rule, paid every fee, and built real networks serving real customers.

The investigation years were tortuous. CBI raids, parliamentary inquiries, media trials—Airtel faced them all. Share prices volatility became routine. International investors questioned India's regulatory stability. The brand that had spent decades building trust faced daily headlines questioning its integrity.

Then came the vindication. On December 21, 2017, a Special CBI Court acquitted all the persons accused in the case, declaring that "a huge scam was seen by everyone when there was none." But the damage was done—not just to Airtel, but to the entire industry. Investment dried up. Network expansion slowed. India's telecom revolution, which had been the envy of emerging markets, stuttered.

The 2G controversy's lasting impact wasn't legal but structural. It accelerated industry consolidation, increased regulatory scrutiny, and most importantly, created the perfect storm for a new entrant to disrupt everything. That entrant was already preparing its assault, backed by India's richest man and promising to make voice calls free forever.

VII. The Jio Disruption: Fighting for Survival (2016–2020)

On 1st September 2016, as chairman Mukesh Ambani launched Jio at the Reliance Industries Limited AGM, telecom giants Bharti Airtel, Idea Cellular and Reliance Communications lost a whopping $2 billion in the stock market. What followed was nothing short of industry carnage.

Jio was touted as an industry disrupter for its ridiculously low data prices and for doing away entirely with charges for domestic calls. The telecom major's offers was nothing short of audacious – unlimited free voice calls throughout the country and data priced cheap at Rs. 50 per GB. To understand the disruption: At one point in 2016, before Jio entered the market, 1 gigabyte of data in India cost approximately 225 rupees ($3).

The impact on Airtel was immediate and brutal. The company was forced to slash tariffs by up to 80% for prepaid services. Share price tanked over 8.5% on Jio's launch day alone. 28 months on, Jio's entry forced Bharti Airtel into posting its first quarterly loss in over 15 years.

The numbers painted a grim picture. In 2016, the average revenue per user (ARPU) for the major Indian telecoms providers was close to $2. By 2019, it was nearly half of that. Airtel's carefully constructed business model—built on voice revenues subsidizing network expansion—collapsed overnight.

Survival required drastic measures. In 2017, Bharti Airtel sold off parts of its non-core businesses and many of its brick-and-mortar stores. By December of that year, Airtel had partially exited its East African markets in order to boost its margins and focus on holding ground on market shares in India.

The company also filed complaints about predatory pricing, arguing Jio was using oil money to subsidize telecom losses. But regulators sided with the consumer benefits of low prices. The market had spoken—free voice and cheap data were the new normal.

Yet Airtel adapted with remarkable agility. It accelerated 4G rollout, covering 75% of India by 2018. It bundled content through partnerships with Netflix, Amazon Prime, and others. Most crucially, it focused on quality—betting that as the free offers ended, customers would pay for better network experience.

The consolidation became inevitable. The most significant fallout was the Vodafone–Idea merger in 2018, as rivals struggled to withstand Jio's aggressive pricing model. From nine private operators in 2015, India's telecom market became an effective three-player game by 2020. Airtel hadn't just survived—it had emerged as the only credible alternative to Jio's dominance.

VIII. The Digital Transformation & 5G Era (2018–Present)

The post-Jio era forced a fundamental reimagining of Airtel's business. Voice revenues were dead. The future lay in data, digital services, and enterprise solutions. The transformation was swift and decisive.

Airtel Payments Bank, launched in 2017, became a cornerstone of the digital strategy. By FY 2022-2023, it had over 5 crore users and was processing over Rs 10,000 crore in deposits. This wasn't just about payments—it was about owning the customer relationship beyond connectivity.

The content play expanded aggressively. Airtel Xstream aggregated 15+ OTT platforms. Wynk Music competed with Spotify and YouTube Music. Airtel Ads created a digital advertising business leveraging customer data. The company that once sold minutes was now selling digital experiences.

But the biggest bet was on 5G. In the August 2022 spectrum auction, Bharti Airtel made bids worth Rs 43,084 crore to acquire 19867.8 MHz spectrum in 900 MHz, 1800 MHz, 2100MHz, 3300 MHz and 26 GHz frequency bands. This wasn't just spectrum buying—it was strategic positioning.

The 5G rollout strategy differed markedly from Jio's. While Jio promised rapid nationwide coverage, Airtel focused on quality in key markets. Services launched on October 1, 2022, in eight cities. Within 30 days, Airtel crossed 1 million unique 5G users. By October 2023, the number had reached 50 million.

The enterprise transformation was equally dramatic. Airtel Business grew to contribute over 20% of India revenues. From simple connectivity, the portfolio expanded to include cloud services, IoT solutions, cyber security, and data center services. The acquisition of strategic data center assets positioned Airtel as a full-stack enterprise technology provider.

International operations also stabilized. Africa turned profitable after years of losses. The focus shifted from subscriber growth to value creation—mobile money, data services, and enterprise solutions. The painful lessons from the initial years had created a leaner, more agile international operation.

By 2024, the transformation metrics were compelling: ARPU had recovered to Rs 200+ levels, data consumption per user exceeded 20GB monthly, and digital services contributed 15% of revenues. The company that nearly collapsed under Jio's assault had emerged stronger, more diversified, and better positioned for the digital future.

IX. Current Market Position & Competitive Dynamics

As of January 2025, Airtel is the second largest mobile network operator in India and the second largest mobile network operator in the world. With 38.69 crore Indian subscribers and a 33.61% market share, Airtel has solidified its position as the premium alternative to Jio's mass-market approach.

The duopoly dynamics with Jio have created an interesting equilibrium. While Jio leads in subscriber numbers, Airtel commands higher ARPU—Rs 211 versus Jio's Rs 181. This premium positioning reflects Airtel's strategic focus on quality customers who value network experience over just price.

The company operates in 18 countries across South Asia and Africa. The international operations, once seen as Mittal's expensive mistake, now contribute significantly to both revenues and strategic value. Africa operations generate over $3 billion annually and provide diversification from Indian market volatility.

Recent strategic moves signal continued evolution. The partnership with Google for cloud services positions Airtel in the enterprise digitalization wave. Collaboration with OneWeb for satellite broadband addresses rural connectivity gaps. The Airtel IoT platform serves over 50 million connected devices, from vehicles to smart meters.

Financial performance has also recovered strongly. FY 2023-24 showed revenue growth of 8.3% to Rs 1.46 lakh crore. More importantly, operating margins expanded to 32%, among the highest globally for telecom operators. The debt-to-EBITDA ratio improved to 2.8x from over 4x during the Jio disruption period.

But challenges remain intense. Jio's financial muscle—backed by Reliance's conglomerate strength—remains formidable. Regulatory pressure for lower tariffs conflicts with investment needs for 5G expansion. New technologies like satellite internet threaten to disrupt again. The question isn't whether Airtel can survive—it's proven that. The question is whether it can thrive in an industry where disruption has become the only constant.

X. Playbook: Strategic & Business Lessons

The Power of Timing and First-Mover Advantage Airtel's success began with impeccable timing. Entering mobile telephony in 1995, just as India was liberalizing, created compound advantages. Early spectrum was cheaper, customer acquisition costs were lower, and brand loyalty had time to build. But being first wasn't enough—execution had to match ambition.

The Outsourcing Revolution Airtel is credited with pioneering the business strategy of outsourcing all of its business operations except marketing, sales and finance and building the 'minutes factory' model of low cost and high volumes. This wasn't mere cost-cutting. It was recognizing that in capital-intensive industries, owning assets is less important than controlling customer relationships. The model influenced telecoms globally—from Latin America to Southeast Asia.

Regulatory Navigation as Core Competency Through multiple government changes, policy shifts, and investigations, Airtel survived while peers collapsed. The key was maintaining relationships across political spectrums while never compromising on compliance. When the 2G investigation peaked, Airtel's clean record became its shield.

Managing Through Existential Crisis The Jio disruption could have killed Airtel. Instead, it catalyzed transformation. The playbook: preserve cash through asset sales, focus on profitable customers over market share, accelerate technology upgrades, and diversify revenue streams. Most importantly—never panic, never surrender.

Building Through Partnerships From Vivendi for the initial license to Ericsson for network management to Google for cloud services—Airtel mastered the art of strategic partnerships. Each partnership brought capabilities that would have taken years to build internally.

The Premium Play in Commoditized Markets When price wars commoditize the core product, the answer isn't to win on price—it's to change the game. Airtel's focus on network quality, customer service, and bundled offerings created differentiation even when the core service (connectivity) became commoditized.

Capital Allocation in Capital-Intensive Industries The spectrum auction strategy reveals masterful capital allocation. While Jio spent Rs 88,000 crore in the 2022 5G auction, Airtel spent Rs 43,000 crore but secured similar coverage potential. The difference? Surgical bidding focused on profitable circles rather than nationwide bragging rights.

Technology Transition Management From 2G to 5G, each technology transition risked stranding billions in investments. Airtel's approach—sweating existing assets while selectively upgrading—balanced customer experience with capital efficiency. The company never led technology adoption but was never fatally late either.

XI. Bear vs. Bull Case Analysis

Bear Case:

The structural challenges facing Airtel are formidable. The Indian market remains brutally price-sensitive, with ARPU at $2.5 compared to $30+ in developed markets. This pricing pressure shows no signs of abating, especially with government viewing telecom as essential infrastructure that should be affordable for all.

The 5G investment cycle requires massive capital—over Rs 43,000 crore already spent with more needed for network densification. Yet monetization remains uncertain. Enterprise 5G use cases are nascent. Consumer willingness to pay premiums for 5G speeds is unproven. The risk of stranded assets looms large.

Regulatory overhang persists. Adjusted Gross Revenue (AGR) dues, though restructured, still amount to tens of thousands of crores. Any adverse regulatory change—spectrum pricing, license fees, or tariff caps—could devastate economics. The government's track record suggests populism often trumps industry health.

African operations, while profitable, remain vulnerable. Currency fluctuations, political instability, and infrastructure challenges create constant volatility. The $10.7 billion investment has yet to deliver returns commensurate with the risk.

Technology disruption threats multiply. Satellite internet from Starlink or Amazon could bypass traditional infrastructure. WhatsApp calling already cannibalized voice revenues—what happens when satellite internet makes mobile data redundant? The pace of disruption continues accelerating.

Bull Case:

The Indian telecom market structure has fundamentally transformed. From destructive competition among nine players, it's now a rational duopoly. Both Airtel and Jio have signaled focus on profitability over market share. Tariff hikes of 20-25% implemented successfully in 2024 prove pricing power exists.

5G opens genuinely new revenue streams. Enterprise solutions—private networks, IoT, edge computing—represent multi-billion dollar opportunities. Airtel's early enterprise relationships and credibility position it better than Jio for B2B growth. Consumer AR/VR applications, though nascent, could drive data consumption 10x current levels.

Digital services are scaling rapidly. Airtel Payments Bank, Wynk Music, Xstream—each creates stickiness beyond connectivity. As these services mature, they transform Airtel from a utility to a platform. Margins in digital services far exceed traditional telecom.

India's economic growth trajectory supports telecom expansion. With GDP per capita projected to double by 2030, telecom spending as percentage of income could increase substantially. Rural penetration remains under 60%, providing growth runway. Data consumption per capita is still 1/10th of developed markets.

The Africa opportunity is finally crystallizing. Mobile money adoption is accelerating. 4G penetration remains under 30%, providing upgrade potential. Most importantly, Airtel has learned to operate profitably in challenging markets—a competency few global telecoms possess.

ARPU growth trajectory looks sustainable. From the Rs 145 trough in 2020 to Rs 211 in 2024, with potential for Rs 300 by 2027. Even modest ARPU growth, given the subscriber base, translates to substantial profit expansion. Operating leverage means incremental revenues flow directly to bottom line.

XII. Epilogue & Looking Forward

Bharti Airtel's transformation from a push-button phone importer to a global telecom giant spanning 18 countries is more than a corporate success story—it's a reflection of India's own economic metamorphosis. The company that began when making a phone call was luxury has evolved into a digital platform serving nearly 500 million people globally in an era where connectivity is considered a fundamental right.

The next decade presents both unprecedented opportunities and existential challenges. India's digital economy is projected to reach $1 trillion by 2030. 5G applications—from autonomous vehicles to smart cities—remain largely uninvented. The enterprise digitalization wave has just begun. Yet technology disruption accelerates, regulatory pressures intensify, and competition from both traditional and unexpected quarters grows fiercer.

Key decisions loom ahead. Should Airtel double down on India or expand internationally again? How aggressively should it pursue digital services versus connectivity? Should it partner with or compete against global tech giants? The answers will determine whether Airtel remains relevant in 2035.

The broader lessons from Airtel's journey transcend telecom. In emerging markets, entrepreneurial vision can overcome infrastructure deficits. Business model innovation matters more than technology innovation. Surviving disruption requires reimagining identity—from product company to platform, from asset owner to service orchestrator. Most importantly, resilience through crisis creates competitive advantages that prosperity cannot.

As India stands at the cusp of its digital decade, Airtel's role extends beyond corporate performance. The infrastructure it builds, services it enables, and innovations it drives will shape how 1.4 billion people work, learn, entertain, and connect. The company that democratized voice communication now aims to democratize digital opportunity.

The story that began with Sunil Mittal's fascination with a push-button phone in Taiwan has evolved into one of emerging market capitalism's most instructive cases. It demonstrates that in industries considered natural monopolies, entrepreneurial companies can not only compete but transform entire nations' trajectories. As Airtel enters its fourth decade, its greatest chapters may still be unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube