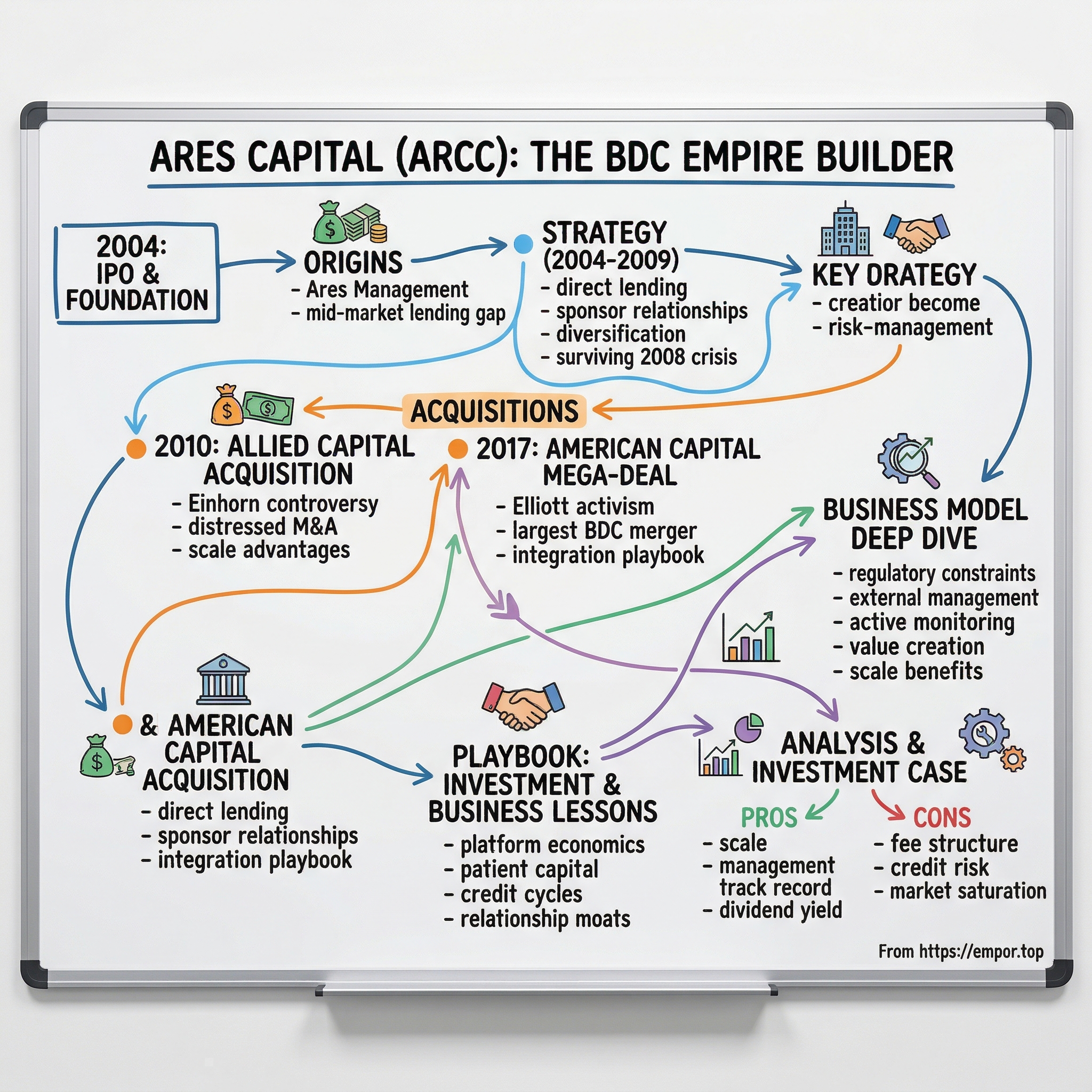

Ares Capital Corporation: The BDC Empire Builder

I. Introduction & Episode Roadmap

Picture this: October 8, 2004. The New York Stock Exchange trading floor buzzes with its usual chaos, but today marks something different. A new type of financial vehicle is making its debut—Ares Capital Corporation, trading under the ticker ARCC. The opening bell rings at $15 per share. Few could have imagined that this startup Business Development Company, born from a Los Angeles-based alternative asset manager's ambition, would become the undisputed titan of middle-market lending in America.

Fast forward to today: Ares Capital commands a portfolio valued at approximately $27.9 billion, spanning 566 companies across virtually every sector of the American economy. It's not just the largest publicly traded BDC by market capitalization—it's a lending machine that has fundamentally reshaped how mid-sized companies access capital in the United States. While banks retreated from middle-market lending after 2008, and while traditional private equity firms focused on mega-deals, Ares Capital quietly built an empire in the gap between them.

The central question isn't just how they got here—it's how a company operating in one of the most regulated, dividend-constrained structures in finance managed to build such dominant market position. This is a story about patient capital triumphing over hot money, about strategic acquisitions that others deemed too messy to touch, and about the power of platform economics in an industry most investors still don't fully understand.

Business Development Companies occupy a peculiar niche in American finance. Created by Congress in 1980 to democratize access to private company investments, BDCs operate under strict regulatory constraints: they must distribute 90% of taxable income as dividends, maintain specific leverage ratios, and invest primarily in U.S. companies. It's like running a marathon with ankle weights—yet Ares Capital not only finished the race but lapped the field multiple times.

What makes this story particularly fascinating for students of business strategy is the deliberate, almost methodical way Ares Capital approached growth. While Silicon Valley celebrates blitzscaling and winner-take-all dynamics, Ares Capital represents something different: compound advantages built over decades, relationships cultivated across hundreds of private equity sponsors, and a lending discipline that survived—and thrived—through multiple credit cycles.

Today's journey will take us from the late 1990s alternative asset management landscape through two transformative acquisitions that redefined the BDC industry. We'll examine how external management—often criticized as conflicted—became a strategic advantage. We'll dissect the investment playbook that allowed them to deploy billions while maintaining credit discipline. And we'll explore what this all means for investors contemplating the future of private credit markets.

Three key themes will emerge throughout this story. First, the power of being early to recognize structural shifts—in this case, the post-2000 retreat of banks from middle-market lending. Second, the value of strategic M&A in financial services, where cultural integration matters as much as financial engineering. Third, the compounding effects of scale in relationship-driven businesses, where reputation and track record create nearly insurmountable competitive moats.

For investors, this isn't just a history lesson—it's a masterclass in how regulated financial institutions can create value within constraints. For operators, it's a blueprint for building dominant market position through patience and discipline rather than disruption and speed. And for anyone interested in American capitalism, it's the story of how a new form of financial intermediary emerged to fill a critical gap in the economy's credit infrastructure.

II. Origins: The Ares Management Story & BDC Formation

The late 1990s were heady times for alternative asset management. Wall Street's finest were spinning out of bulge bracket firms, armed with rolodexes and reputations, ready to capture the extraordinary returns available in less efficient markets. Into this landscape stepped Antony Ressler, who had already co-founded Apollo Global Management with Leon Black in 1990, but saw an opportunity to build something different. In 1997, he partnered with Michael Arougheti, David Kaplan, John H. Kissick (a former Apollo colleague), and Bennett Rosenthal (from Merrill Lynch's leveraged finance group) to establish Ares Management.

The timing was prescient. Banks were consolidating rapidly following the repeal of Glass-Steagall, creating massive institutions focused on large corporate clients and consumer banking. Middle-market companies—those with EBITDA between $10 million and $250 million—found themselves increasingly orphaned. Traditional relationship banking was dying, replaced by syndication desks and securitization machines. This wasn't just a market gap; it was a fundamental restructuring of American corporate finance.

Ares Management spent its first seven years building credibility in traditional credit strategies—high yield bonds, leveraged loans, distressed debt. But by 2003, the partners recognized a bigger opportunity. The Business Development Company structure, created by Congress in 1980 to democratize private company investing, had been largely dormant for two decades. BDCs offered unique advantages: permanent capital, public market liquidity, and tax-efficient dividend distribution. The constraints were significant—leverage limits, distribution requirements, investment restrictions—but Ares saw these as features, not bugs. They would force discipline in a business where discipline created value.

Ares Capital Corporation was founded on April 16, 2004, initially funded on June 23, 2004, and completed its initial public offering on October 8, 2004, raising approximately $288 million in net proceeds. The IPO price of $15 per share reflected appropriate skepticism—this was an untested vehicle from a seven-year-old manager entering a sleepy regulatory structure.

The BDC framework imposed strict guardrails. As a Regulated Investment Company (RIC), Ares Capital had to distribute at least 90% of taxable income as dividends, limiting retained earnings for growth. Leverage was capped at 1:1 debt-to-equity (later raised to 2:1 in 2018). At least 70% of investments had to be in eligible portfolio companies—primarily U.S. businesses with market values below $250 million. These weren't just technical requirements; they fundamentally shaped the business model.

The external management structure—Ares Capital Management LLC serving as investment adviser—created both opportunity and controversy. Critics saw inherent conflicts: management fees regardless of performance, potential for affiliated transactions, misaligned incentives. But Ares viewed it differently. External management provided instant access to Ares Management's origination network, due diligence infrastructure, and workout expertise. In a relationship business, these advantages compounded over time.

The early investment thesis was elegantly simple: provide flexible capital to middle-market companies abandoned by consolidating banks but too small for capital markets. The fund would invest through revolvers, first lien loans, warrants, unitranche structures, second lien loans, mezzanine debt, private high yield, junior capital, subordinated debt, and non-control preferred and common equity, with investments typically ranging from $10 million to $100 million. This wasn't about financial engineering or leverage arbitrage—it was about becoming the trusted capital provider for America's economic backbone.

What distinguished Ares Capital from the handful of existing BDCs wasn't just fresh capital or modern systems. It was the recognition that middle-market lending had evolved from a banking product to an investment strategy. Banks lent based on relationships and cross-selling opportunities. Ares would lend based on fundamental credit analysis and portfolio construction. Banks focused on interest income. Ares would capture both interest and equity upside through warrants and co-investments.

The regulatory framework that constrained BDCs also protected them. Unlike hedge funds or private credit funds, BDCs couldn't chase hot money strategies or engage in excessive leverage. They had to build sustainable, dividend-producing portfolios. In an industry obsessed with IRRs and multiples, Ares Capital would focus on a different metric: dividend coverage through economic cycles.

By choosing the BDC structure, Ares made a profound strategic bet: that patient, regulated capital would ultimately outcompete fast, unregulated capital in middle-market lending. It was a contrarian view in 2004. Two decades later, with a portfolio approaching $28 billion, it looks prophetic. The foundation was set for building America's next great financial institution—not through disruption or innovation, but through discipline, relationships, and compound advantages built one loan at a time.

III. Building the Foundation: Early Years & Strategy (2004–2009)

The conference room at Ares Capital's Los Angeles headquarters in November 2004 felt both exhilarating and daunting. The IPO had closed successfully a month earlier, but now came the real work: deploying $288 million into a market where everyone else was chasing the same deals. The team, led by founding members who would later become industry legends, faced a fundamental challenge—how to differentiate when every competitor had access to the same capital markets.

The answer came through a contrarian insight. While other BDCs and credit funds were fighting over syndicated deals and club transactions, Ares Capital would focus on bilateral, privately negotiated investments. This meant more work—extensive due diligence, custom documentation, direct negotiations—but it also meant better economics and stronger creditor protections. The portfolio construction philosophy was simple yet revolutionary for the BDC space: treat each investment as if it were the only one in the portfolio.

Early deals reflected this discipline. Rather than chase market share, the team focused on companies with predictable cash flows, tangible assets, and management teams who understood the value of patient capital. Investments ranged from $10 million to $100 million, structured through revolvers, first lien loans, warrants, unitranche structures, second lien loans, and mezzanine debt. Each structure was tailored to the specific company's needs rather than forcing borrowers into standardized products.

The origination strategy diverged sharply from traditional banking models. Instead of relying solely on investment banks or brokers, Ares Capital built direct relationships with private equity sponsors. By 2006, they had established connections with over 100 sponsors, creating a proprietary deal flow that competitors couldn't replicate. The message to sponsors was consistent: "We're not just a lender, we're a partner who understands your business model and timeline."

Building this sponsor network required patient cultivation. The team attended every relevant conference, hosted dinners in every major city, and most importantly, demonstrated reliability on initial transactions. When a sponsor needed certainty of execution for a time-sensitive acquisition, Ares Capital delivered. When documentation needed to be flexible for a complex carve-out, they found solutions. This wasn't about being the cheapest capital—it was about being the most reliable.

The competitive landscape in these early years was surprisingly thin. Most traditional BDCs were still operating with pre-2000 playbooks, focusing on mezzanine debt and equity co-investments. Banks were rapidly retreating from middle-market lending as Basel II capital requirements made these loans less attractive. The emerging direct lending funds were still raising their first vehicles. Ares Capital occupied a sweet spot: the permanent capital of a BDC, the sophistication of a credit fund, and the relationships of an investment bank.

Then came 2007. The early warning signs were subtle—wider spreads on leveraged loans, longer syndication times, nervous whispers about subprime mortgages. By early 2008, the whispers had become shouts. Bear Stearns collapsed in March. Credit markets seized. Suddenly, the disciplined portfolio construction of the previous four years looked prescient.

September 15, 2008: Lehman Brothers filed for bankruptcy. When investment bank Lehman Brothers went bankrupt in September 2008, there was much uncertainty as to which financial firms would be required to honor the CDS contracts on its $600 billion of bonds outstanding. The financial world shifted from concern to panic. For Ares Capital, this was both the ultimate test and the ultimate opportunity.

The portfolio held up remarkably well compared to competitors. While the broader credit markets saw massive losses—by the end of 2008, 80% of the CDOs by value rated "triple-A" were downgraded to junk. Bank writedowns and losses on these investments totaled $523 billion—Ares Capital's focus on senior secured loans to stable middle-market companies provided crucial downside protection. Non-accruals increased, certainly, but not catastrophically. The bilateral nature of most investments allowed for proactive restructuring rather than chaotic liquidations.

More importantly, the crisis created unprecedented opportunities for those with capital and courage. As banks retreated entirely from middle-market lending and other BDCs focused on survival, Ares Capital found itself virtually alone in providing new capital. Spreads widened from LIBOR +400 to LIBOR +800 or higher. Equity co-investment opportunities emerged at valuations unthinkable just months earlier. Companies that had previously dismissed BDC capital as too expensive were now grateful for any financing source.

The team made a crucial decision during the darkest days of the crisis: keep lending. While others hoarded cash, Ares Capital continued originating new investments, albeit with even more stringent underwriting standards and wider spreads. This wasn't recklessness—it was calculated opportunism based on a simple observation: great companies still needed capital, and the best vintage years for credit investing often come during crises.

By mid-2009, as the National Bureau of Economic Research declared June 2009 as the end date of the U.S. recession, and Federal Open Market Committee noted that "the pace of economic contraction is slowing" and "conditions in financial markets have generally improved in recent months," though "household spending has shown further signs of stabilizing but remains constrained by ongoing job losses, lower housing wealth, and tight credit", Ares Capital emerged from the financial crisis not just intact but strengthened. The portfolio had been stress-tested under extreme conditions. Sponsor relationships had been cemented through reliable partnership during turbulent times. Most importantly, the team had proven that disciplined underwriting and patient capital could generate attractive returns even through a generational financial crisis.

The lessons learned during this period would fundamentally shape Ares Capital's approach for the next decade. First, portfolio diversity across industries and structures provided essential resilience. Second, bilateral negotiations and customized structures created value that syndicated deals couldn't match. Third, maintaining lending capacity during market dislocations generated the best risk-adjusted returns. Fourth, the BDC structure's permanent capital base, despite its constraints, provided a crucial advantage over funds facing redemptions.

As 2009 drew to a close, Ares Capital had not only survived but positioned itself for dramatic expansion. The company had proven its model through the ultimate stress test. Competitors were weakened or eliminated. The middle-market lending gap had widened into a chasm. And most intriguingly, distressed opportunities were emerging that would reshape the entire BDC industry. The stage was set for the transformative acquisition that would establish Ares Capital's market dominance: Allied Capital.

IV. The Allied Capital Acquisition: First Major Deal (2009–2010)

May 14, 2002. The Grand Hyatt Hotel in midtown Manhattan. David Einhorn, then just 33 years old, stepped up to the podium at the Sohn Investment Research Conference—a charity event for children's cancer research—and delivered what would become one of the most famous short presentations in Wall Street history. He recommended shorting a mid-cap financial company called Allied Capital, and the day after the speech the company's stock went down by 20 percent. His warning would echo through the industry for years: "People who are willing to lie about small things have no problem lying about big things."

Allied Capital wasn't just any BDC—it was the establishment incarnate. Founded in 1958, Allied Capital Corporation completed its first public offering of stock in 1960 on the OTC and was listed on the New York Stock Exchange in 2001. By 2007, at its peak it had just over $5 billion in assets. The company projected stability, paying consistent dividends that kept investors satisfied and markets open to new capital raises.

But beneath the surface, Einhorn had uncovered something deeply troubling. Allied Capital's many investments might have been mismarked. Assets described as performing were often underperforming. In one of the worst cases, Allied Capital carried subordinated debt investments at full value when more senior lenders held their investments at zero. While one mismarked asset might have been an error, the appearance of several mismarked assets suggested this was a companywide problem—Allied was dramatically overstating its financial condition.

The problems ran deeper than mismarked assets. Allied had created wholly controlled investments, a relatively new practice over the last couple of years. In ordinary GAAP accounting, when you own a controlling investment in a company, you have to consolidate the results. Transactions between you and your wholly controlled subsidiary are called intercompany transactions and they are eliminated in the consolidation. Not so in Allied's RIC accounting. They do not consolidate these controlled investments, and they do not eliminate the intercompany transactions from the consolidated results. One thing Allied does do with these controlled investments is provide services, such as investment banking, for which they charged fees.

The most egregious example was Business Loan Express, Allied's wholly owned subsidiary. Even though Business Loan Express is 100% owned by Allied, which is a public company, Allied provides no data on Business Loan Express. We don't know how much it earns, we don't know how its portfolio of risky small business loans has performed during the recession. We don't even know how large the portfolio is, or how much leverage it uses. What we do know is that Business Loan Express pays Allied a 25% rate of interest, or $20 million a year, on an $80 million investment that Allied has lent to Business Loan Express. Since Allied owns all of the equity, I guess they can decide what the interest rate on the loan will be. And what they charge in their fees. But in my opinion, this is the sort of thing, those sort of left pocket to right pocket, that explains why intercompany transactions are eliminated under most accounting systems.

The ensuing battle between Einhorn and Allied became legendary in financial circles. Allied said that Einhorn was engaging in market manipulation, and illegally accessed his phone records using pretexting. Regulatory bodies proved frustratingly ineffective. In June 2007, after a lengthy investigation by the U.S. Securities and Exchange Commission, it found that Allied broke securities laws relating to the accounting and valuation of illiquid securities it held. However, it did not issue any fines or penalties, and Allied settled without admitting or denying the allegations.

The financial crisis of 2008 became Allied's undoing. The house of cards truly began to collapse when the financial crisis hit its worst in 2009, requiring more writedowns on Allied's investments on top of writedowns to correct artificially inflated values in prior years. Having dumped its winners to generate taxable income, marginal borrowers that remained in the portfolio faced a rapidly deteriorating economic environment. The stock price told the story: from its 2007 peak above $30, Allied was trading near $3 by early 2009—a decline of nearly 90%.

Enter Ares Capital. On November 5, 2009, the companies announced a definitive merger agreement. The terms were devastating for Allied shareholders but represented extraordinary value for Ares. Allied shareholders would receive approximately 0.325 shares of Ares Capital common stock for each share of Allied common stock owned—valuing Allied at just $3.47 per share. For a company that had traded above $30 just two years earlier, it was a humiliating end.

But the deal was about more than just price. In a separate transaction, Ares Capital reached an agreement to acquire Allied's interests in its Senior Secured Loan Fund LLC for $165 million in cash. With approximately $3.6 billion of committed capital, the SL Fund was formed in December 2007 to invest in unitranche securities of middle-market companies. The SL Fund currently held unitranche loans totaling approximately $900 million.

On April 1, 2010, Ares Capital announced that it had completed its merger with Allied Capital Corporation, becoming the largest business development company measured by market capitalization and total portfolio companies under management. The sale to Ares was finalized with Allied closing for the last time at $5 a share. At closing, Ares Capital retired in full Allied's $250 million senior secured term loan arranged by J.P. Morgan Securities Inc. on January 29, 2010. Ares Capital also assumed all of Allied's other outstanding debt obligations, including approximately $745 million in Allied's publicly traded unsecured notes.

The strategic rationale was compelling. Allied's portfolio, while troubled, contained valuable assets and relationships. The company had deep connections with middle-market sponsors that Ares could leverage. Most importantly, the acquisition would create immediate scale advantages in a business where size matters for both cost of capital and origination capabilities.

Integration proved challenging but ultimately successful. Ares methodically worked through Allied's portfolio, separating performing assets from problem loans. The most toxic positions were restructured or sold. The valuable sponsor relationships were cultivated and expanded. Within 18 months, the combined entity was generating returns that validated the acquisition thesis.

The lessons from the Allied acquisition were profound. First, distressed M&A in financial services requires not just capital but operational expertise to realize value. Second, reputation matters—Ares's clean record allowed it to rehabilitate relationships tainted by Allied's practices. Third, scale creates compound advantages in lending businesses through lower funding costs, broader origination networks, and greater portfolio diversification.

David Einhorn would later reflect on the Allied saga with mixed emotions. "What we've seen a year later is that Allied was the tip of an iceberg; that this kind of questionable ethic, philosophy and business practice was far more widespread than I recognized at the time ... Our country, our economy, is paying a huge price for that." His six-year battle had exposed systemic problems in financial markets, but the bruising fight only netted Greenlight a profit of $35 million.

For Ares Capital, however, the Allied acquisition marked a turning point. The company had proven it could execute complex M&A, integrate troubled assets, and emerge stronger. The BDC industry took notice—consolidation was possible, even beneficial, when executed properly. And most importantly, Ares Capital had established itself as the natural acquirer for any distressed BDC assets. This reputation would prove invaluable when the next opportunity emerged: American Capital.

V. Scaling the Platform: Growth & Evolution (2010–2016)

The post-Allied years represented a golden age for Ares Capital. With the integration largely complete by mid-2011, the company possessed something unique in the BDC landscape: genuine scale advantages combined with institutional credibility. The portfolio had grown from approximately $2.5 billion pre-merger to over $5 billion, but more importantly, the quality of both assets and origination capabilities had transformed.

The first strategic move was building out Ivy Hill Asset Management, a subsidiary that would become Ares Capital's secret weapon. Unlike traditional BDC investments, Ivy Hill operated as an asset management platform, taking minority stakes in other credit funds and CLO managers. This wasn't just portfolio diversification—it was information arbitrage. Through Ivy Hill, Ares Capital gained visibility into deal flow, market pricing, and competitive dynamics across the entire middle-market lending ecosystem. By 2012, Ivy Hill was managing over $2 billion in assets, generating both management fees and carried interest that provided uncorrelated returns to the core lending portfolio.

The origination network expansion followed a hub-and-spoke model that would have been impossible without the Allied acquisition's scale. Beyond the Los Angeles headquarters, Ares Capital established or expanded offices in New York, Chicago, Dallas, and San Francisco. But physical presence was just the beginning. Each office became a node in an intelligence network, with professionals maintaining relationships not just with sponsors but with regional banks, law firms, and industry consultants. By 2013, the company was seeing over 3,000 potential transactions annually, a threefold increase from 2009.

Product innovation became the third pillar of growth. While competitors remained focused on traditional senior and mezzanine structures, Ares Capital pioneered the unitranche product—a single facility combining senior and subordinated debt. For borrowers, it meant one lender, one set of documents, one negotiation. For Ares Capital, it meant higher yields, better economics, and most crucially, control. By 2014, unitranche facilities represented over 30% of new originations, with yields averaging 200-300 basis points above traditional first lien loans.

The rise of direct lending during this period wasn't just a trend—it was a fundamental restructuring of corporate finance. Banks, constrained by Dodd-Frank and Basel III regulations, retreated further from middle-market lending. The void they left wasn't temporary; it was structural. Ares Capital positioned itself as the solution, offering not just capital but certainty, speed, and flexibility that banks could no longer provide. The company's average hold size increased from $25 million in 2010 to over $50 million by 2015, reflecting both greater capital resources and sponsor confidence.

Competition evolved but remained manageable. Other BDCs like Apollo Investment Corporation and Prospect Capital grew aggressively, but often through lower-quality originations or riskier structures. The first generation of direct lending funds—GSO, Antares, Churchill—emerged as formidable competitors, but they lacked permanent capital and public market access. Ares Capital occupied a unique position: the stability of permanent capital, the sophistication of institutional investors, and the flexibility of private negotiations.

In May 2014, Ares Management completed its initial public offering and is currently listed on the New York Stock Exchange. This created an interesting dynamic for Ares Capital. The external manager was now publicly traded, theoretically aligning interests through stock ownership while also creating potential conflicts through the pressure for fee growth. Critics argued this structure enabled Ares Management to benefit regardless of Ares Capital's performance. Supporters countered that the reputational linkage created powerful incentives for prudent management.

The market positioning strategy during this period reflected sophisticated game theory. Rather than competing on price—a race to the bottom that would destroy returns—Ares Capital competed on certainty and solutions. When a sponsor needed to close an acquisition in 30 days, Ares Capital could commit $200 million without syndication requirements. When a portfolio company needed to refinance but had complex collateral, Ares Capital had the expertise to structure around it. This wasn't about being the cheapest capital; it was about being the most valuable partner.

By late 2015, the platform had achieved remarkable scale. The portfolio exceeded $8 billion across more than 200 companies. The dividend had been maintained or increased every quarter since the Allied acquisition. The stock traded at a consistent premium to book value, rare for BDCs. But management saw clouds forming. Credit spreads had tightened to pre-crisis levels. Covenant packages were loosening. New entrants were flooding the market with capital. The next phase of growth would require another transformative move.

That move was already in motion. Throughout 2015, Ares Capital's team had been monitoring American Capital, another large BDC struggling with portfolio problems and activist pressure. The parallels to Allied were obvious, but the scale was different—American Capital had over $20 billion in assets under management. It would be the largest BDC acquisition in history, and it would either cement Ares Capital's dominance or overwhelm its carefully built infrastructure.

VI. The American Capital Mega-Deal (2016–2017)

The boardroom at American Capital's Bethesda, Maryland headquarters on November 16, 2015, was tense. Management had just received a bombshell: Elliott Management Corporation, the feared activist hedge fund run by Paul Singer, had disclosed an 8.4% stake and launched a proxy campaign opposing the company's planned spinoff. Elliott created the website www. BetterACAS.com and publicly released a scathing letter: "We believe ACAS's share price could be worth in excess of $23." For a stock trading around $13, it was a declaration of war.

American Capital's troubles ran deep. Founded by Malon Wilkus in 1986, the company had gone public in 1997 at $15 per share, raising $155 million and becoming the first private equity firm to go public in the United States. At its peak, American Capital had over $100 billion of assets under management. But the financial crisis had ravaged the portfolio, and by 2015, the company was a shadow of its former self.

Elliott's critique was devastating and precise. Median analyst price targets for ACAS point to a 10% discount to NAV, compared to a 48% and 7% premium for comparable internally managed BDCs and externally managed BDCs, respectively. The activist highlighted multiple governance failures: "With an average Board tenure of 15 years and limited professional investment experience, the Board lacks the relevant expertise to govern the behavior of the investment team and hold management accountable." Most damning was the compensation structure: "ACAS has consistently paid excessive compensation for poor performance, as evidenced by the Company receiving F grades in Glass Lewis pay-for-performance model for each of the last four years (and no better than a D since 2008)."

The proposed spinoff that triggered Elliott's campaign was particularly controversial. Management wanted to separate the BDC assets from the asset management business, a move Elliott saw as self-serving entrenchment rather than value creation. The activist's five-step plan was blunt: withdraw the spinoff proposal, strengthen the board, review portfolio and capital allocation, and essentially, admit failure and start over.

What happened next stunned even seasoned Wall Street observers. In mid-November 2015, Elliott sent a public letter to American Capital while simultaneously revealing an 8.4% stake; the company caved just nine days later, announcing it was beginning a sale process. Nine days. That's all it took for a 29-year-old company with over $20 billion in assets to capitulate completely.

The strategic review process attracted multiple bidders, but Ares Capital had unique advantages. The successful integration of Allied Capital provided a proven playbook. The platform could handle the scale. Most importantly, Ares Management was willing to provide financial support that made the economics compelling for all parties.

On May 23, 2016, the announcement came: Under the terms of the Ares transaction, American Capital shareholders will receive approximately USD3.43 billion in total cash and stock consideration or USD14.95 per fully diluted share. The structure was complex but elegant—American Capital shareholders will receive USD1.470 billion in cash from Ares Capital, or USD6.41 per share, plus 0.483 Ares Capital shares for each American Capital share, resulting in approximately 110.8 million Ares Capital shares, or USD1.682 billion in value or USD7.34 per share based on Ares Capital's closing stock price of USD15.19 as of Friday, 20 May, 2016, issued in exchange for approximately 229.3 million American Capital shares.

Crucially, As part of the aggregate consideration, Ares Management, L.P. (NYSE:ARES) will provide financial support to the transaction. Through its subsidiary, Ares Capital Management LLC, which serves as the investment adviser to Ares Capital, Ares Management will provide USD275 million of cash, or USD1.20 per fully diluted share, to American Capital shareholders—a masterstroke that aligned interests while providing additional consideration.

Elliott's support proved decisive. "Elliott Management, holder of a 14.4% interest in American Capital, strongly supports the transactions and will vote its shares in favor at the upcoming Special Meeting. Portfolio Managers Jesse Cohn and Pat Frayne said in a statement, 'We are pleased with the result of the Strategic Review and thank the Independent Board Committee of ACAS for its hard work and success in delivering an excellent outcome for shareholders. We believe this transaction represents the best path forward for ACAS shareholders and creates a tremendous opportunity for value creation as shareholders of Ares Capital after the deal is completed.'"

The strategic rationale echoed the Allied playbook but at massive scale. Kipp deVeer, CEO of Ares Capital, made the connection explicit: "Similar to the strategy we successfully utilized in our acquisition of Allied Capital in 2010, we plan to leverage our robust origination platform to redeploy American Capital's portfolio into directly-originated investments generating a higher level of current income and ultimately improved risk-adjusted returns."

The deal closed on January 3, 2017, with The purchase price, including the sale of American Capital Mortgage Management, totaled $4.1 billion. In a separate but related transaction, American Capital Mortgage Management was sold to American Capital Agency for $562 million, which closed on June 30, 2016. The combined company created a behemoth—over $12 billion in assets, the undisputed leader in BDC lending.

Integration proceeded more smoothly than Allied, partly because the playbook was established, partly because market conditions were favorable. American Capital's broadly syndicated loan portfolio—liquid but low-yielding—was systematically rotated into directly originated middle-market loans. Underperforming equity positions were restructured or sold. The best sponsor relationships were preserved and expanded.

The financial impact was immediate and substantial. Core earnings per share increased in the first quarter post-close. The dividend was maintained and eventually increased. Most importantly, the scale advantages predicted in the merger presentation materialized—lower funding costs, larger hold sizes, better terms from borrowers who valued certainty.

For the BDC industry, the American Capital acquisition marked a watershed. It demonstrated that even the largest, most complex BDCs could be successfully acquired and integrated. It showed that activist investors, traditionally skeptical of BDCs, saw value in the structure when properly managed. And it cemented Ares Capital's position as the industry's natural consolidator.

But perhaps the most important lesson was about timing and preparation. Ares Capital didn't pursue American Capital because it was available; it was ready when American Capital became available. The Allied integration had built the muscles. The platform expansion had created the infrastructure. The sponsor relationships provided the deal flow to redeploy capital. When opportunity knocked—in the form of Elliott Management's activism—Ares Capital was prepared to answer.

VII. Modern Era: Market Dominance & New Challenges (2017–Present)

The transformation of Ares Capital post-American Capital has coincided with—and benefited from—one of the most dramatic shifts in corporate finance history. The private credit market, in which specialized non-bank financial institutions such as investment funds lend to corporate borrowers, topped $2.1 trillion globally last year in assets and committed capital, with about three-quarters of this was in the United States, where its market share is nearing that of syndicated loans and high-yield bonds. For context, Private credit expanded to approximately $1.5 trillion at the start of 2024, up from $1 trillion in 2020, and is estimated to soar to $2.6 trillion by 2029.

This explosive growth created both opportunity and challenge for Ares Capital. The opportunity was obvious—more borrowers, larger deals, better terms. The challenge was subtler but equally important: how to maintain discipline and differentiation when seemingly every asset manager was launching a direct lending fund. As of June 30, 2025, Ares Capital Corporation's portfolio had a fair value of approximately $27.9 billion, and consisted of 566 portfolio companies backed by 247 different private equity sponsors—a testament to both scale and diversification achieved through two decades of patient building.

The rising rate environment that began in 2022 proved particularly favorable for Ares Capital's floating-rate loan portfolio. As the Federal Reserve raised rates to combat inflation, the company's net interest margins expanded dramatically. Unlike fixed-income investors who suffered massive mark-to-market losses, Ares Capital's floating-rate assets repriced higher while its leverage costs remained manageable due to prudent hedging and term financing. More than one-third of borrowers now have interest costs exceeding their current earnings, creating both risk and opportunity for disciplined lenders.

Competition intensified from multiple directions. Traditional banks, after years of retreat, began returning to leveraged lending, drawn by the attractive spreads. The rapid growth of private credit has recently spurred increased competition from banks on large transactions. Insurance companies, seeking yield in a low-rate environment, allocated billions to private credit strategies. Perhaps most significantly, the mega-funds—Apollo, Blackstone, KKR—built direct lending platforms that dwarfed even Ares Capital in size, though not in middle-market expertise.

Ares Capital's response was strategic focus rather than blind growth. While competitors chased larger deals and tighter spreads, the company doubled down on its core middle-market franchise. The typical investment remained $50-150 million, to companies with EBITDA of $25-75 million—a sweet spot where relationship banking still mattered and where Ares Capital's speed and certainty provided genuine value. The company also expanded into complementary strategies—asset-based lending, life sciences finance, venture debt—that leveraged existing expertise while providing portfolio diversification.

Technology became an unexpected differentiator. While BDCs aren't typically associated with innovation, Ares Capital quietly built sophisticated data analytics capabilities. Machine learning models analyzed thousands of data points across portfolio companies, identifying early warning signs of stress and opportunities for additional investment. Automated reporting systems provided real-time visibility into portfolio performance. Digital origination platforms streamlined the underwriting process from weeks to days for certain transaction types.

The regulatory environment evolved favorably. In 2018, the Small Business Credit Availability Act allowed BDCs to increase leverage from 1:1 to 2:1 debt-to-equity, effectively doubling their lending capacity. Ares Capital was among the first to receive shareholder approval for the increased leverage, though management committed to operating below the maximum to maintain financial flexibility. The additional capacity proved valuable not for aggressive growth but for opportunistic investments during market dislocations.

ESG considerations, once peripheral to leveraged lending, became increasingly central. Ares Capital developed comprehensive ESG scoring for portfolio companies, not from regulatory pressure but from recognition that sustainable businesses make better borrowers. The company began declining investments in certain industries—coal, predatory lending, weapons manufacturing—while actively supporting portfolio companies' sustainability initiatives. This wasn't virtue signaling; it was risk management dressed in modern terminology.

Recent market dynamics have created new challenges. In the United States, we expect that an additional $5 trillion to $6 trillion of such assets could shift into the nonbank ecosystem over the next decade, provided that the following three assumptions hold: interest rates remain elevated above pandemic-level troughs; yield assets continue to perform in line with their historical range (and do not, for instance, experience accelerating credit losses); and the current regulatory environment for banks persists. This massive shift represents both opportunity and risk—opportunity to capture market share, risk of deteriorating underwriting standards as competition intensifies.

The private credit boom has also attracted regulatory scrutiny. Given that this ecosystem is opaque and highly interconnected, and if fast growth continues with limited oversight, existing vulnerabilities could become a systemic risk for the broader financial system. Ares Capital, as the largest public BDC, finds itself at the center of these discussions—both as a potential systemic risk and as a model for how non-bank lenders can operate safely within appropriate constraints.

Looking forward, Ares Capital faces a market fundamentally different from its founding era. Middle-market lending has evolved from a niche opportunity to a mainstream asset class. The competitive advantages that drove early success—access to capital, sponsor relationships, underwriting expertise—have been commoditized to varying degrees. Yet the company's current dominance suggests that scale, reputation, and execution still matter in relationship-driven businesses. The next chapter will test whether those advantages can sustain market leadership as private credit matures from alternative to essential.

VIII. Business Model Deep Dive

Understanding Ares Capital's business model requires appreciating a fundamental tension: it operates within one of finance's most restrictive regulatory frameworks while competing against unconstrained private funds. Every strategic decision reflects this reality—how to generate superior returns while distributing 90% of taxable income, maintaining regulated leverage ratios, and investing primarily in qualifying assets.

The investment process begins long before any capital is deployed. Deal sourcing through the Ares network represents the first and perhaps most important competitive advantage. With relationships across 247 private equity sponsors, regional investment banks, and industry advisors, Ares Capital sees approximately 4,000 potential transactions annually. But volume isn't the goal—quality is. The company maintains a disciplined filter, seriously evaluating perhaps 10% of opportunities and ultimately investing in less than 2%.

Due diligence at Ares Capital operates like a multi-stage filtration system. Initial screening eliminates companies in challenged industries, with excessive leverage, or with management teams lacking clear vision. Detailed financial analysis follows, but numbers tell only part of the story. The team conducts extensive primary research—customer calls, supplier checks, competitor analysis—to understand the business beyond spreadsheets. Legal and structural review ensures appropriate creditor protections. Environmental and regulatory diligence identifies hidden liabilities. This process typically takes 4-6 weeks for new platforms, though add-on investments to existing portfolio companies can move faster.

Active portfolio monitoring distinguishes Ares Capital from passive lenders. Each portfolio company submits monthly financial statements, quarterly compliance certificates, and annual budgets. But monitoring goes beyond document collection. Portfolio teams maintain regular dialogue with management, attend board meetings as observers, and visit facilities. When performance deviates from plan—and it always does somewhere—early intervention prevents minor issues from becoming major problems. This intensive oversight model requires significant human capital but generates returns through both loss mitigation and value creation opportunities.

The value creation model extends beyond interest income. While coupon payments provide the foundation—typically SOFR +500-700 basis points for first lien loans—additional returns come from multiple sources. Original issue discounts generate immediate gains. Prepayment penalties compensate for early exits. Amendment fees reward flexibility. Most importantly, equity co-investments and warrants provide upside participation. In successful exits, these equity instruments can generate multiples of the original debt investment, transforming good returns into exceptional ones.

The external management structure remains controversial but arguably essential. Ares Capital Management LLC, the external advisor, receives a base management fee of 1.5% on gross assets up to 1:1 leverage, stepping down above that threshold. The incentive fee structure is more complex: 17.5% of pre-incentive fee net investment income above a 7% hurdle, plus 17.5% of realized capital gains net of realized and unrealized losses. Critics argue these fees are excessive and create misaligned incentives. Supporters counter that access to Ares Management's platform—500+ investment professionals, global origination network, institutional infrastructure—would be impossible to replicate internally.

Capital allocation at Ares Capital follows a disciplined framework that prioritizes risk-adjusted returns over absolute yields. The portfolio construction philosophy emphasizes diversification across multiple dimensions: industry (no sector exceeds 15% of portfolio), geography (presence across all major U.S. markets), sponsor (largest relationship under 5% of portfolio), and position size (largest single investment under 3% of fair value). This diversification isn't just risk management—it's information advantage, providing real-time insight into economic conditions across sectors and regions.

Risk management operates through multiple layers of protection. Structural safeguards include senior secured positions (over 70% of portfolio), meaningful equity cushions below the debt, and comprehensive covenant packages. Portfolio-level protections include industry limits, sponsor concentration guidelines, and maximum hold sizes. Financial protections include matched-term funding, interest rate hedges, and maintaining leverage well below regulatory limits. But the most important protection is cultural: a willingness to say no to attractive yields when structures don't compensate for risks.

The power of scale in direct lending manifests in ways both obvious and subtle. Obvious advantages include lower funding costs—Ares Capital's unsecured bonds trade tighter than smaller BDCs—and ability to lead larger transactions. Subtle advantages matter more: the information advantage from seeing thousands of deals, the negotiating leverage from being a repeat player, the operational efficiency from established systems and processes. Scale also enables specialization—dedicated teams for different industries, strategies, and portfolio management functions—impossible for subscale competitors.

Dividend policy represents the ultimate expression of the BDC model's constraints and opportunities. Required to distribute 90% of taxable income, Ares Capital has limited flexibility in capital retention. Yet this constraint becomes a feature, not a bug, for income-focused investors. The company targets consistent quarterly dividends supplemented by special dividends when realized gains permit. Since 2004, Ares Capital has paid over $10 billion in dividends while still growing net asset value—proof that the distribution requirement doesn't preclude growth when combined with disciplined investment and periodic capital raises.

The regulatory framework that defines BDCs creates both limitations and advantages. Investment restrictions—70% qualifying assets, diversification requirements, affiliated transaction rules—limit flexibility but also prevent style drift. Leverage limits constrain growth but ensure sustainability. Distribution requirements reduce retained earnings but create tax efficiency. Reporting obligations increase costs but provide transparency. These regulations don't just constrain Ares Capital; they define its competitive moat, creating barriers to entry that pure private funds can't replicate.

The external versus internal management debate continues to evolve. Internally managed BDCs like Main Street Capital demonstrate that alternative models can succeed. Yet Ares Capital's sustained outperformance suggests the external model's benefits—platform access, operational leverage, aligned incentives through ownership—outweigh its costs for larger-scale operations. The key isn't the structure itself but the execution within that structure.

Looking beneath the surface, Ares Capital's business model represents a sophisticated arbitrage. It arbitrages information asymmetry through proprietary deal flow. It arbitrages capital efficiency through permanent capital and prudent leverage. It arbitrages operational scale through the external manager platform. And it arbitrages regulatory constraints by turning limitations into competitive advantages. This multi-layered arbitrage, refined over two decades and two transformative acquisitions, explains how a company operating within strict constraints became the dominant force in middle-market lending.

IX. Playbook: Investment & Business Lessons

The Ares Capital story offers a masterclass in building competitive advantages within constraints. While Silicon Valley celebrates disruption and reinvention, Ares Capital demonstrates that sustainable value creation often comes from patient execution of proven strategies. The lessons extend far beyond BDCs or even financial services.

Platform economics in alternative asset management follow different rules than traditional businesses. Unlike software where marginal costs approach zero, or manufacturing where scale drives unit cost reduction, alternative asset management scales through relationships and reputation. Every successful investment strengthens sponsor relationships, creating preferential access to future deals. Every workout handled professionally, even when painful, builds credibility for the next restructuring. Ares Capital understood this dynamic early—success compounds not through technology or patents but through trust accumulated over thousands of interactions.

The M&A strategy that transformed Ares Capital from ambitious startup to industry titan offers profound lessons about financial services consolidation. Both Allied and American Capital were distressed sellers, but distress alone doesn't create value. The magic was in the integration—rotating low-yielding assets into higher-returning investments, eliminating redundant costs, and most crucially, rehabilitating damaged relationships. The lesson: in financial services M&A, the acquisition price matters less than the execution capability. Ares Capital paid seemingly low prices for both deals, but the real value creation came post-close through operational transformation.

Patient capital's value becomes most apparent during volatile markets. When credit spreads blow out and competitors retreat, patient capital providers can achieve extraordinary returns. But patience requires preparation. Ares Capital maintained conservative leverage during good times, providing dry powder for dislocations. It built systems and teams during calm markets, enabling rapid deployment during chaos. It cultivated sponsor relationships continuously, ensuring deal flow when others had none. The lesson: patient capital without operational readiness is just lazy capital.

Building competitive advantages through scale and relationships seems obvious but proves difficult in practice. Scale without relationships leads to commoditization—competing on price alone. Relationships without scale lack credibility for large transactions. Ares Capital achieved both through deliberate sequencing. Early years focused on relationship building with smaller deals. The Allied acquisition provided scale. American Capital cemented market leadership. Each phase built on the previous, creating cumulative advantages competitors couldn't quickly replicate.

Managing through credit cycles requires embracing paradox. The best vintage years for lending often coincide with the worst economic conditions. The riskiest loans get made during the best times. Ares Capital navigated this paradox through systematic rather than heroic decision-making. Underwriting standards remained consistent regardless of market conditions. Portfolio monitoring continued even when everything performed. Work-out capabilities stayed sharp during benign periods. The lesson: credit cycles are inevitable, but credit losses aren't if discipline remains constant.

The external versus internal management debate misses the larger point about alignment. Structure matters less than incentives. Ares Management's public listing created transparency. Significant insider ownership aligned interests. Long-term track records built trust. The controversy over fees obscures the value creation—Ares Capital generated superior returns even after fees. The lesson: in principal-agent relationships, alignment comes from shared success, not just shared structure.

Building in regulated industries requires embracing rather than fighting constraints. Ares Capital turned every regulatory requirement into competitive advantage. Distribution requirements attracted income-focused investors. Investment restrictions prevented style drift. Leverage limits ensured sustainability. Reporting obligations created transparency. Rather than viewing regulations as limitations, Ares Capital saw them as defining features of a differentiated product. The lesson: constraints can create clarity, and clarity can create value.

The information advantage in financial markets compounds differently than operational advantages in other industries. Every loan Ares Capital makes generates data about industries, business models, and economic conditions. Every workout provides insight into stress scenarios. Every exit reveals valuation dynamics. This information doesn't depreciate like technology or equipment—it accumulates, creating pattern recognition capabilities that improve decision-making. The lesson: in information-intensive businesses, experience creates exponential rather than linear advantages.

Relationship moats prove more durable than most competitive advantages. Technology can be replicated. Strategies can be copied. Teams can be poached. But relationships built over decades of reliable execution can't be quickly rebuilt. Ares Capital's 247 sponsor relationships weren't just names in a database—they represented thousands of successful transactions, timely fundings, and problems solved together. Competitors could match Ares Capital's terms, but they couldn't match its history. The lesson: in relationship businesses, time and trust create the deepest moats.

The power of boring businesses deserves appreciation in an era obsessed with disruption. Ares Capital does essentially the same thing today as in 2004—lending money to middle-market companies. No pivots. No reinventions. No transformations. Just consistent execution refined over time. This boring consistency generated extraordinary returns precisely because it was boring. Predictability attracted capital. Reliability attracted borrowers. Stability attracted talent. The lesson: in volatile markets, boring can be beautiful.

Risk management through diversification seems elementary but proves complex in practice. Diversification across industries protects against sector downturns but may miss correlated risks. Geographic diversification spreads regional exposure but can't prevent systemic shocks. Sponsor diversification reduces relationship risk but increases monitoring complexity. Ares Capital achieved true diversification not through simple metrics but through understanding correlation dynamics. The lesson: effective diversification requires understanding not just what could go wrong, but what could go wrong simultaneously.

These lessons culminate in a broader insight about building enduring financial institutions. Success comes not from genius insights or brilliant timing but from systematic execution of sound strategies. Ares Capital didn't invent middle-market lending or pioneer innovative structures. It simply executed traditional lending with modern discipline, appropriate scale, and strategic patience. In finance, as in life, extraordinary outcomes often result from ordinary actions repeated with extraordinary consistency.

X. Analysis & Investment Case

Evaluating Ares Capital as an investment requires reconciling impressive historical performance with legitimate structural concerns. The company trades at a persistent premium to book value—rare among BDCs—yet faces questions about fee structures, credit quality, and market saturation. Understanding the investment case demands examining both quantitative metrics and qualitative factors that drive long-term value creation.

Financial performance metrics tell a story of consistent execution. Since the IPO in 2004, Ares Capital has generated a total return exceeding 400%, outperforming both the S&P 500 Financial Sector and BDC peers. The dividend yield typically ranges from 8-10%, supported by net investment income that consistently covers distributions. Return on equity averages 10-12% through cycles, respectable for a regulated financial institution. Credit losses, the key risk metric, averaged less than 1% annually over the past decade—remarkable given the middle-market focus.

Competitive positioning versus other BDCs reveals structural advantages. Ares Capital's $27.9 billion portfolio dwarfs the next largest competitor. This scale enables lower funding costs—unsecured bonds price 50-100 basis points tighter than smaller BDCs. Diversification exceeds peers across every dimension—industries, sponsors, geography. Operating efficiency, measured by operating expenses to assets, benefits from scale economies. Most importantly, proprietary deal flow from sponsor relationships generates better risk-adjusted opportunities than broadly syndicated transactions.

The comparison with private credit funds presents a more complex picture. Private funds like those managed by Apollo, Blackstone, and KKR have raised vehicles exceeding Ares Capital's entire market capitalization. These funds face no regulatory constraints, can use unlimited leverage, and retain all earnings. Yet Ares Capital maintains advantages: permanent capital eliminates fundraising risk, public listing provides liquidity for investors, and BDC structure offers tax efficiency through dividend distributions. The competition is real but not existential.

The bull case for Ares Capital rests on three pillars. First, scale advantages in a relationship business create compounding competitive moats. Larger portfolio generates more information, better information drives superior underwriting, superior underwriting attracts more capital, and the cycle continues. Second, proven management through multiple cycles demonstrates resilience. The same team that navigated 2008 and COVID-19 remains in place, with institutional knowledge that can't be replicated. Third, dividend yield in a low-rate world attracts permanent capital. Where else can investors find 9% yields with monthly liquidity and regulatory oversight?

The bear case raises equally valid concerns. Fee structure remains the primary criticism—why pay 1.5% management fees plus 17.5% incentive fees when internally managed BDCs charge nothing? The answer—access to Ares Management's platform—satisfies some but not all investors. Credit risk looms larger as the cycle ages. With private credit markets flooded with capital, underwriting standards have loosened industry-wide. When the next downturn arrives, will Ares Capital's discipline prove sufficient? Regulatory changes pose ongoing risks. Congress could modify BDC rules, eliminate tax advantages, or impose additional constraints.

Market saturation represents perhaps the greatest long-term challenge. The global private credit market has surpassed US$3trn AUM, with more capital raised than quality deals available. This supply-demand imbalance pressures returns, loosens terms, and increases risk. Ares Capital's size provides some insulation—it can be selective while smaller competitors chase deals—but nobody remains immune from market forces.

The future of middle-market lending will be shaped by structural forces beyond any single company's control. Bank regulation continues pushing lending to non-banks, favorable for BDCs. Technology enables faster underwriting and lower costs, but also commoditizes standard products. Demographics drive capital toward income-producing assets, supporting BDC valuations. Economic cycles remain inevitable, creating both risks and opportunities for patient capital providers.

Potential disruption scenarios deserve consideration. Could technology platforms disintermediate traditional lenders? Possibly, but relationship-driven middle-market lending resists commoditization. Could regulatory changes eliminate BDC advantages? Perhaps, but the structure has survived 40 years and multiple administrations. Could a severe recession trigger massive credit losses? Certainly, but Ares Capital survived 2008 and emerged stronger. The most likely disruption isn't dramatic but gradual—slow erosion of returns as capital floods the market.

Valuation requires wrestling with the premium to book value. Ares Capital typically trades at 1.05-1.15x book, while many BDCs trade at discounts. This premium reflects superior ROE, consistent dividend coverage, and management credibility. But premiums can evaporate quickly if credit issues emerge or market sentiment shifts. Investors must decide whether paying above book value for quality makes sense given their risk tolerance and return requirements.

The investment decision ultimately depends on individual objectives and beliefs about credit cycles. For income investors seeking yield with moderate growth, Ares Capital offers compelling value despite structural concerns. For total return investors comparing against broader equities, the case weakens given limited capital appreciation potential. For credit-focused investors worried about late-cycle risks, current valuations may not compensate for potential losses.

The most balanced view acknowledges both strengths and limitations. Ares Capital has built the premier franchise in BDC lending through disciplined execution over two decades. The business model generates attractive returns for patient investors comfortable with credit risk. But structural headwinds—fee drag, market saturation, regulatory constraints—limit upside potential. This isn't a growth story or a disruption play. It's a yield vehicle with quality management navigating an increasingly competitive market. Investors should calibrate expectations accordingly.

XI. Epilogue & Looking Forward

Standing at the intersection of past and future, Ares Capital represents both triumph and question mark. The company that started with $288 million in 2004 now manages almost $28 billion, having successfully navigated two major acquisitions, multiple credit cycles, and the transformation of private credit from niche to mainstream. Yet the very success that brought market leadership also creates new challenges that will define the next chapter.

What would different strategic choices have meant? Imagine if Ares Capital had remained internally managed, avoiding the fee controversy but lacking platform access. It might resemble Main Street Capital—successful but subscale, generating solid returns but missing transformative growth. Or consider if Ares Capital had passed on Allied Capital, leaving that distressed portfolio for competitors. Prospect Capital seized the opportunity, acquiring American Capital's competitor, but never achieved the same integration success. The road taken matters, but equally important were the roads not taken.

The evolution of private credit markets from alternative to essential represents a generational shift in corporate finance. What began as a gap-filling solution for orphaned middle-market companies has become a $2 trillion global market competing directly with banks and public markets. Ares Capital didn't just benefit from this evolution—it helped catalyze it, demonstrating that non-bank lenders could provide reliable capital through cycles while generating attractive returns for investors.

Potential future M&A or strategic initiatives will likely differ from past transformative deals. The universe of large, distressed BDCs has been exhausted. Future growth must come through either international expansion—European middle markets remain underpenetrated—or vertical integration into adjacent strategies. The recent build-out of asset-based lending and venture debt capabilities suggests management recognizes that pure middle-market corporate lending faces saturation.

Management succession looms as an underappreciated risk. The founding generation that built Ares Capital remains largely in place, providing continuity but raising questions about transition planning. The next downturn will test whether institutional knowledge has been successfully transferred to younger professionals who lack the scar tissue from 2008. Cultural preservation during generational transition often determines whether financial institutions sustain excellence or drift toward mediocrity.

The lasting impact on the BDC industry cannot be overstated. Ares Capital proved that BDCs could achieve institutional scale, attract blue-chip sponsors, and generate consistent returns through cycles. It demonstrated that external management, despite conflicts, could create value through platform access. Most importantly, it showed that patient execution of traditional lending could generate extraordinary outcomes without extraordinary risk. Every BDC formed today benchmarks against Ares Capital's template.

Technology's role in future evolution remains uncertain but inevitable. While relationship lending resists full automation, technology can enhance every aspect of the business—origination through data analytics, underwriting through machine learning, monitoring through automated reporting, and workout through predictive modeling. Ares Capital's scale provides resources for technology investment that smaller competitors can't match, potentially widening competitive gaps rather than narrowing them.

The next credit cycle will provide the ultimate test of post-crisis positioning. The past decade of generally benign credit conditions, interrupted briefly by COVID-19, hasn't truly stress-tested portfolios built in the post-2008 era. When spreads widen, defaults spike, and capital retreats, will Ares Capital's discipline prove sufficient? History suggests yes, but each cycle brings unique challenges that past experience can't fully anticipate.

Regulatory evolution could reshape the competitive landscape. Proposals for additional oversight of private credit recognize the sector's systemic importance. New regulations could increase compliance costs, limit leverage, or restrict certain investments. Alternatively, regulatory changes could level playing fields between banks and non-banks, intensifying competition. Ares Capital's regulatory expertise provides advantages in navigating changes, but nobody benefits from increased constraints.

The societal implications of private credit's growth deserve consideration. As banks retreat from middle-market lending, companies increasingly depend on alternative lenders for growth capital. This shift transfers credit allocation from regulated, deposit-funded institutions to market-based, institutional capital providers. The implications for financial stability, economic growth, and capital access remain unclear but profound.

Environmental, social, and governance factors will increasingly influence capital allocation. While ESG in leveraged lending might seem oxymoronic, stakeholders increasingly demand that lenders consider sustainability in underwriting decisions. Ares Capital's scale enables dedicated ESG resources that smaller competitors can't afford, potentially creating differentiation in sponsor relationships and investor appeal.

Key takeaways for investors and operators crystallize around several themes. First, competitive advantages in financial services come from reputation and relationships, not products or technology. Second, scale matters, but only when combined with operational excellence and cultural discipline. Third, regulatory constraints can create opportunities for those who embrace rather than fight them. Fourth, patient capital and disciplined execution generate superior long-cycle returns despite appearing suboptimal in short periods.

The ultimate judgment of Ares Capital's legacy awaits future writing. Has it built an enduring franchise that will thrive for decades, or did it simply benefit from unrepeatable conditions during private credit's emergence? Will disciplined underwriting preserve capital through the next severe downturn, or will credit losses reveal hidden vulnerabilities? Can the business model adapt to market saturation, or will returns inexorably decline toward commodity levels?

These questions lack definitive answers, but the weight of evidence suggests cautious optimism. Ares Capital has demonstrated resilience through multiple challenges, adapted to changing conditions while maintaining core discipline, and built competitive advantages that, while not impregnable, resist easy replication. The next chapter won't replicate the extraordinary growth of the first twenty years—no company maintains 20% compound returns indefinitely—but it may prove that boring, disciplined execution in essential financial services can generate attractive returns for patient investors even in mature markets.

The story of Ares Capital ultimately transcends any single company. It's the story of how American finance evolved after the financial crisis, how private markets democratized access to alternative investments, and how patient capital can thrive within regulatory constraints. Whether viewed as triumphant success or cautionary tale depends on perspective and time horizon. But undeniably, Ares Capital transformed middle-market lending from banking backwater to institutional asset class, forever changing how American businesses access growth capital. That transformation, more than any financial metric, may prove its most lasting legacy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube