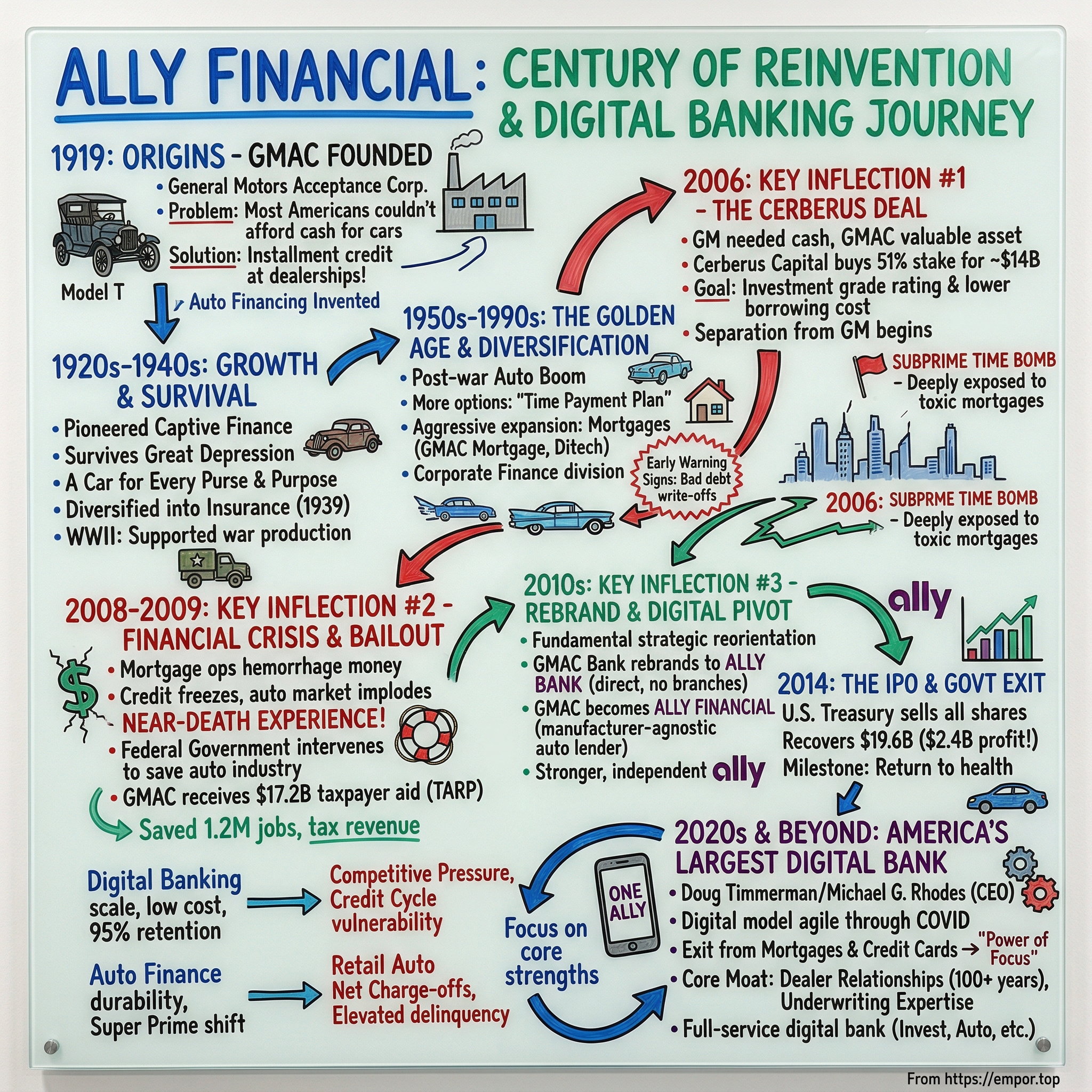

Ally Financial: From GM's Financing Arm to America's Largest Digital Bank

I. Introduction: A Bailout Bet That Paid Off

Picture Detroit in the winter of 2008. The American auto industry stands at the precipice of collapse. General Motors, the company that once symbolized American industrial might, is hemorrhaging cash. But it's not just the carmaker that's in trouble—it's GMAC, GM's 89-year-old financing arm, which has strayed dangerously far from its roots into the toxic waters of subprime mortgages.

General Motors, Chrysler Group and Ally Financial (the finance firm then known as GMAC) together received $79.7 billion in help in 2008 and 2009. Of this staggering sum, about $17 billion of that amount was invested in GMAC (now Ally Financial).

The central question of this story is deceptively simple: How did General Motors' captive financing arm—bailed out with $17.2 billion in taxpayer money during the worst financial crisis since the Great Depression—become America's largest all-digital bank?

Today, Ally is one of the largest car finance companies in the U.S., providing car financing and leasing for 4.0 million customers and originating 1.2 million car loans in 2024. The company serves approximately 11 million customers through a full range of online banking services and securities brokerage and investment advisory services.

The transformation is remarkable not just for its scale, but for its thoroughness. This is a company that invented consumer auto financing in 1919, pioneered installment credit, nearly died in 2008, and reinvented itself as a digital-first bank that eschews physical branches entirely.

The Ally story touches on some of the most important themes in American business history: the birth of consumer credit, the rise and fall of Detroit, the 2008 financial crisis, and the digital disruption of traditional banking. It's also a story about whether a company with deep institutional scars can truly transform itself—or whether the ghosts of the past will eventually catch up with it.

II. The Origins: GMAC and the Birth of Auto Financing (1919-1945)

The Founding Vision

To understand GMAC's founding, you have to understand the automotive marketplace of 1919. The invention of the assembly line changed the way the auto industry did business. To keep factories running smoothly, manufacturers needed auto dealers to buy vehicles in large quantities.

Henry Ford had cracked the code of manufacturing. His Model T rolled off assembly lines at a pace that seemed almost miraculous. But there was a problem: most Americans couldn't afford to pay cash for an automobile. And Ford, with his moralistic views about debt, refused to offer financing.

Enter John Jakob Raskob, one of the most influential—and ultimately controversial—financial minds of his era. Raskob was hired in 1901 by Pierre S. du Pont as a personal secretary. In 1911, he became assistant treasurer of DuPont, in 1914 treasurer, and in 1918 president for finance of both DuPont and General Motors.

Raskob had been an early investor in General Motors and had engineered DuPont's ownership of 43% of GM, purchased from the financially troubled William C. Durant. While with GM, he led the creation of GMAC (now Ally Financial), the company that allowed GM dealers to offer installment credit directly to customers.

In 1919, GMAC opened its doors as a division of GM, to help dealers finance and maintain their inventory and keep up with consumer demand.

The Problem GMAC Solved

The genius of GMAC lay in recognizing a market failure. In the early 1920s, people looking to buy a car or truck had to pay cash or secure their own financing from banks that didn't typically issue loans for automobiles. GMAC made it convenient for customers to get financing right at the dealership.

As Chairman of General Motors' Finance Committee, Raskob had established GMAC in 1919. General Motors was the first automobile manufacturer to allow its dealers to offer a line of credit directly to customers.

When the concept was first proposed, skeptics abounded. "When first proposed, many criticized GMAC as folly. They argued that most working class Americans couldn't really afford new cars and would default on their loans in large numbers. GMAC was seen as an 'incentive for extravagance.'"

Many of the early auto loans required a 35 percent down payment, with the rest due in installments over the course of a year (before repair bills started stacking up). This was called selling cars "on time."

The impact was transformative. "Americans wanted fancy cars, ones they could buy on credit. So Ford lost." General Motors overtook Ford as the leading American car maker. By 1928, Ford Motor Company set up its own auto loan subsidiary. Americans gobbled up the increasingly-available credit for durable goods. By 1930, most appliances, radios and furniture were bought on the installment plan, including more than two-thirds of all automobiles.

GMAC's early operations were centered in Detroit, Michigan, with additional offices quickly established in key cities such as New York City, Chicago, San Francisco, and Toronto. The company's business model was designed to facilitate car sales by providing credit options, allowing customers to finance their purchases directly through dealerships. This approach significantly boosted the accessibility of GM vehicles.

GMAC became a pioneer in captive finance models, with the automotive boom originating 4 million retail financing contracts by 1928 and extending operations internationally with a branch in Great Britain launched in 1920.

Surviving the Great Depression

The 1929 crash and subsequent Depression tested GMAC's model severely. The Great Depression of the 1930s posed severe challenges, with plummeting auto sales—U.S. production fell from 4.6 million vehicles in 1929 to under 1.4 million by 1932—straining GMAC's portfolio of repossessions and delinquencies, though its ties to General Motors provided relative stability compared to independent lenders.

During the Great Depression, car manufactures began segmenting vehicles by cost, from low-price to luxury models. GM and GMAC adapted with the famous slogan "A car for every purse and purpose," offering financing options across price tiers.

Recovery aligned with New Deal policies and industry rebound, leading GMAC to enter the insurance sector in 1939 to cover installment sales risks. This diversification into insurance—which remains a core business today—demonstrated the company's ability to expand its value proposition within the dealer ecosystem.

World War II Contribution

During World War II, GMAC helped support the war effort as the financing arm of GM, which supplied the Allies with submarine engines, airplanes, trucks and tanks. Back home, GMAC helped financially troubled railroads stay in business by renting and financing locomotives.

Financing shifted toward supporting wartime production and deferred civilian auto loans, with GMAC adapting to rationing and military contracts that bolstered General Motors' output of over $12 billion in defense materials by 1945.

The war years demonstrated a crucial characteristic of GMAC: its ability to pivot its financing capabilities to meet changing circumstances. This adaptability would prove essential in the decades to come.

Investor Takeaway from Origins: GMAC's founding represents one of the most successful financial innovations in American history. The company didn't just create a new product—it created a new category of consumer behavior. The captive finance model became the template for manufacturers across industries. But it also embedded a fundamental tension: GMAC existed to serve GM's interests, not necessarily to maximize its own value as a standalone entity.

III. The Golden Age of American Motoring & Diversification (1945-1990s)

The 1950s: America's Love Affair with Cars

Post-war prosperity fueled an explosion in auto demand. Postwar prosperity fueled GMAC's growth through the 1950s and 1960s, as surging consumer demand—U.S. vehicle sales exceeded 7 million annually by the mid-1950s—drove expanded retail financing, insurance underwriting, and diversification into commercial lending.

In the 1950s, GMAC diversified and worked with participating household appliance retailers and extended financing to customers who couldn't afford to buy a refrigerator, washer or stove outright. Americans' love for cars was on the rise during the golden years of automobile design. With the slogan, "Enjoy financing where you buy," more people took advantage of getting the car they wanted and the financing they needed at the same place.

In 1956 GMAC introduced "Buying cars on time" with its Time Payment Plan and gave over 2 million customers more options to finance a vehicle with a payment plan that fit their budget.

The insurance business expanded in tandem. As car manufacturers pushed innovation and style, auto prices rose and insurance became an increasingly important part of GMAC's products and services offering. Motors Insurance Corporation provided dealers with physical damage coverage to protect the vehicles they sold, and in the mid 1960s became the first insurance company to offer comprehensive coverage to dealers' customers.

By the late 20th century, the General Motors Acceptance Corporation had loaned out more than a trillion dollars to car buyers.

1980s-1990s: Aggressive Diversification

Under Roger Smith's leadership, GM embarked on an ambitious diversification strategy—and GMAC was a key part of that effort. In a continuation of its diversification plans, GMAC formed GMAC Mortgage and acquired Colonial Mortgage as well as the servicing arm of Norwest Mortgage in 1985. This acquisition included an $11 billion mortgage portfolio.

The expansion into mortgages seemed logical at the time. GMAC had the capital, the underwriting expertise, and the infrastructure to originate and service loans. Why limit that capability to automobiles?

In 1999, GMAC Mortgage acquired Ditech. This acquisition would later become infamous during the subprime crisis, as Ditech became synonymous with aggressive, often questionable mortgage lending practices.

In the late 1990s, GMAC purchased The Bank of New York's lending unit, leading to the creation of its Corporate Finance division. This business—focused on providing capital to equity sponsors and middle-market companies—remains one of Ally's strongest segments today.

In 2000, the company formed GMAC Bank, a direct bank. This decision to establish an online deposit-taking entity would prove prescient, laying the groundwork for Ally's eventual transformation into an all-digital bank.

Early Warning Signs

Not all was well during these years of expansion. In 1991, the company was forced to write-off $275 million in bad debt as part of a $436 million loss suffered from fraud committed by John McNamara, who ran a Ponzi scheme.

This episode foreshadowed a recurring challenge: as GMAC expanded beyond its core auto financing expertise, risk management became increasingly difficult. The company was building a conglomerate of financial services businesses, but the institutional knowledge that made it excellent at auto lending didn't automatically transfer to other credit products.

Investor Takeaway from the Golden Age: The diversification strategy of the 1980s and 1990s planted the seeds of GMAC's near-destruction in 2008. Entering the mortgage business seemed like a natural extension of financing capabilities, but it exposed GMAC to entirely different risk dynamics. The lesson: being good at lending doesn't mean being good at all lending.

IV. Key Inflection Point #1: The Cerberus Deal & Separation from GM (2006)

The Strategic Context

By the mid-2000s, General Motors was in serious trouble. The company was bleeding money on its automotive operations, burdened by massive legacy costs from pension and healthcare obligations. GM needed cash—and GMAC was one of the few valuable assets available to monetize.

The sale of a majority stake in GMAC's financing arm was part of a strategy to return GMAC's credit rating to investment grade, which would lower its cost of borrowing—essential for a finance company to remain competitive. The sale would also provide a cash infusion to parent GM, which was struggling under the weight of a massive fixed cost structure and fierce competitive pressures.

The Deal Details

Private investment firm Cerberus Capital Management LP and other investors completed the purchase of a 51 percent stake in General Motors Corp.'s financial unit, GMAC, for about $14 billion in cash, to be paid over three years. The deal was struck in April and completed on Nov. 30. The acquisition was led by Cerberus, along with Citigroup Inc. and Aozora Bank Ltd.

GM expected to receive approximately $14 billion in cash from this transaction over three years, including distributions from GMAC, with an estimated $10 billion by closing. The transaction strengthens GMAC's ability to support GM's automotive operations, improves GMAC's access to cost-effective funding, provides significant liquidity to GM and allows GM to continue to participate in the profitability of GMAC over the long term through its 49-percent ownership stake.

Cerberus acquired 51% of GMAC, General Motors' finance arm, in 2006 for $7.4 billion. It appointed Ezra Merkin as nonexecutive Chairman.

Cerberus, named after the three-headed dog guarding the gates of the Underworld in Greek mythology, was led by the intensely private Steve Feinberg. The firm had built a reputation for buying distressed assets and turning them around through aggressive operational improvements.

The Simultaneous Real Estate Spin-offs

GMAC's real estate empire was also restructured. GMAC sold a controlling interest of GMAC Commercial Holdings, its real estate division that was renamed Capmark, to Goldman Sachs, Kohlberg Kravis Roberts, and Five Mile Capital Partners. GMAC Real Estate was sold to Brookfield Asset Management.

In 2005, the company formed GMAC ResCap as a holding company for its mortgage operations.

The Subprime Time Bomb

The timing of the Cerberus deal could not have been worse. In 2006, the U.S. housing market was at its peak. Subprime mortgages—loans made to borrowers with poor credit histories—were being originated at record volumes and packaged into securities that were sold to investors worldwide.

GMAC, through its ResCap subsidiary and the recently acquired Ditech operation, was deeply exposed to this market. At the time, however, few recognized the magnitude of the risk. Real estate prices seemed to only go up. Defaults were low. The models said everything was fine.

What Cerberus thought it was buying was a diversified financial services company with a strong auto lending franchise. What it actually bought was a company with a ticking time bomb embedded in its mortgage operations.

Investor Takeaway from the Cerberus Deal: Private equity timing is notoriously difficult to control. Cerberus's thesis—that GMAC could be separated from GM and run more efficiently as an independent entity—was sound in principle. But the thesis assumed a relatively stable economic environment. When that assumption proved false, the entire investment was imperiled.

V. Key Inflection Point #2: The 2008 Financial Crisis & Government Bailout

The Collapse

The 2008 financial crisis struck GMAC with brutal force. The company's mortgage operations were hemorrhaging money as home prices collapsed and defaults skyrocketed. Simultaneously, the auto market was imploding as credit froze and consumers stopped buying cars.

"GMAC LLC, the auto and home lender seeking federal aid, hasn't obtained enough capital to become a bank holding company and may abandon the effort, casting new doubt on the firm's ability to survive. A $38 billion debt exchange by GMAC and its Residential Capital LLC mortgage unit to reduce the company's outstanding debt and raise capital hasn't attracted enough participation."

GMAC's exposure to the gap in residual values was around $3.5 billion. In December 2008, Cerberus subsequently informed GMAC's bondholders that the financial services company may have to file for bankruptcy if a bond-exchange plan is not approved. The company had previously said it may fail in its quest to become a bank holding company because it lacks adequate capital.

The Emergency Measures

The federal government intervened to prevent a complete collapse of the American auto industry—and GMAC was a critical piece of that industry's infrastructure.

On December 24, 2008, the Federal Reserve accepted the company's application to become a bank holding company. This conversion was crucial: as a bank holding company, GMAC could access the Federal Reserve's lending facilities and potentially participate in TARP.

On December 29, 2008, Treasury announced that GMAC also was to receive a $5 billion capital injection through preferred share purchases. But this initial injection was just the beginning.

Additional loans for GM and Chrysler were made before and during the two companies' bankruptcies, and GMAC received additional capital through preferred share purchases as well. At the end of 2009, GM had received approximately $50.2 billion in direct loans and indirect support; Chrysler had received $10.9 billion in loans and indirect support; GMAC had received $17.2 billion in preferred equity purchases and loans.

Why GMAC Mattered for the Auto Industry

The bailout wasn't just about saving GMAC as a standalone entity—it was about preserving the circulatory system of the American auto industry. Without GMAC's floor-plan financing, dealers couldn't maintain inventory. Without consumer financing, buyers couldn't purchase vehicles. The entire ecosystem depended on credit flowing through the system.

GM was not the only company that received TARP funds as a result of the 2008-2009 financial crisis. More than 700 institutions received support, with the U.S. government taking ownership stakes in five large companies: GM, Chrysler, GMAC (now called Ally Financial), AIG, and Citigroup.

A study by the Center for Automotive Research found that the GM bailout saved 1.2 million jobs and preserved $34.9 billion in tax revenue.

Cleaning Up the Mess

In January 2009, the company shut down Nuvell Financial Services, its subprime lending division.

In 2009, Capmark filed for bankruptcy and its North American loan origination and servicing business was acquired by Berkadia, a joint venture of Leucadia National and Berkshire Hathaway.

The mortgage operations remained deeply troubled. ResCap would eventually file for bankruptcy in 2012, with its legal issues taking years to resolve. In December 2013 the bankruptcy proceedings of Ally Financial's mortgage subsidiary, Residential Capital LLC (ResCap), were substantially resolved.

Investor Takeaway from the Crisis: The 2008 bailout demonstrates both the systemic importance of auto financing and the dangers of diversification into unfamiliar credit products. GMAC's core auto lending business was stressed but survivable; its mortgage operations nearly destroyed the entire company. The lesson for financial companies is clear: stick to what you know, or develop genuine expertise before expanding into new markets.

VI. Key Inflection Point #3: The Rebrand & Digital Banking Pivot (2009-2014)

The Strategic Reset

From the ashes of the financial crisis emerged a fundamentally transformed company. The leadership recognized that simply surviving wasn't enough—GMAC needed to reinvent itself entirely.

As Sathish Muthukrishnan, Ally's chief information and technology officer, explained: "Ally was started right after the worst financial crisis the country has ever seen, in 2008. We are the largest direct-to-consumer digital bank in the U.S. We started not because consumers needed a bank; they needed a better bank. So, from day one, transformation and making it better have been in our DNA."

The crisis was an opportunity to review the business model, define competitive advantages, and build on core strengths. The world didn't need another bank—it needed a better one.

The Rebrand

In May 2009, its deposit-taking subsidiary, previously GMAC Bank, rebranded as Ally Bank to emphasize direct banking services without physical branches.

In May 2010, GMAC re-branded itself as Ally Financial.

In 2010, the company rebranded as Ally Financial and transformed its auto finance business into Ally Auto—a premier independent finance provider offering dealers of many vehicle makes, including RVs, the most comprehensive suite of products and services available.

The rebrand wasn't just cosmetic. It signaled a fundamental shift in strategy: from a captive finance company serving primarily GM and Chrysler dealers to an independent provider serving dealers across all brands. This transformation freed Ally from its dependence on the fortunes of any single automaker.

Return to Profitability

Michael Carpenter, who joined as CEO in 2009, led the turnaround effort. According to Chairman Franklin Hobbs: "Michael Carpenter has done an outstanding job as CEO and as a Board member since joining us at an especially difficult and pivotal time in 2009. Among many other accomplishments, he led our rebranding as Ally; strengthened our financial and market position; restructured a former captive finance company to be the premier, independent auto finance provider; and made Ally a leader in the growing direct banking space."

The IPO & Government Exit

In April 2014, Ally completed its initial public offering—a milestone that marked both the company's return to health and the beginning of the end for government ownership.

Ally Financial, the auto loan giant that received taxpayer assistance during the depths of the financial crisis, fell nearly 4% in its public debut Thursday. At an IPO price of $25 per share, the deal raised $2.4 billion, making it the biggest IPO of the year. All 95 million shares offered in the IPO were sold by the U.S. Treasury. The proceeds from the sale went directly to the government.

The U.S. Department of the Treasury announced that it had agreed to sell 95,000,000 shares of Ally Financial Inc. common stock at a price to the public of $25.00 per share, for $2.375 billion in proceeds to taxpayers from Ally's initial public offering. Prior to the IPO, taxpayers held approximately 37 percent of common stock in the company, or 177,311,010 shares. After the closing of the offering, taxpayers will hold approximately 17 percent of common stock.

The Treasury sold its last stake in the company in 2014, recovering $19.6 billion from its $17.2 billion investment.

The Treasury invested an additional $17.2 billion into GM's former financing company, GMAC (now Ally Financial). The shares in Ally were sold on December 18, 2014, for $19.6 billion netting the government $2.4 billion in profit, including dividends.

The taxpayer profit on the Ally investment stands in stark contrast to the losses on GM itself, where the government lost approximately $10.3 billion. Ally's recovery was one of the genuine success stories of the auto bailout.

Investor Takeaway from the Rebrand: The rebrand represented more than a name change—it was a complete strategic reorientation. By pivoting to digital banking and becoming manufacturer-agnostic in its auto lending, Ally positioned itself for long-term growth independent of GM's fortunes. The IPO and government exit demonstrated that the turnaround was real.

VII. Building the Digital Bank (2014-2020)

Jeffrey Brown's Leadership

In February 2015, Ally announced that Jeffrey J. Brown had been named chief executive officer, effective immediately. Brown, who most recently served as president and CEO of Ally's Dealer Financial Services business, also joined Ally's Board of Directors. Brown succeeded Michael A. Carpenter who was retiring as chief executive and from the Board.

Brown had joined the company in 2009 as corporate treasurer. In 2011, he became executive vice president of finance and corporate planning, where he oversaw the company's finance, treasury and corporate strategy activities.

Brown would lead Ally for nearly nine years, presiding over its transformation into a digital banking powerhouse. "After 14 years at Ally, including nearly 9 years as CEO, I am so proud of how we transformed the company from the days of GMAC to who we are today, a more strategically, operationally and financially sound organization," Brown said upon announcing his departure.

Strategic Acquisitions & Divestitures

In 2012, the company sold its Canadian banking operations to Royal Bank of Canada for $3.8 billion. This divestiture continued the strategy of focusing on core U.S. operations.

In June 2016, Ally acquired TradeKing, a stockbrokerage, for $275 million. The platform was rebranded as Ally Invest, giving the company an entry into the investment services space.

In May 2016, Ally Bank re-entered the mortgage business with the launch of its direct-to-consumer offering called Ally Home. This decision would later be reversed as the company refocused on its core competencies.

The Technology Transformation

Ally's recent transformation began about 15 years ago when the company's leadership saw an opportunity to leverage their strong position in auto financing to create something new: one of the world's first all-digital banks.

The technological starting point was humbling. "Looking back, it would be hard to believe that five years ago, we were still running on mainframes. We still had a network that was plug-and-play hardware-enabled. We had six different apps. For a digital bank, we had six different apps."

The "One Ally" Initiative

"A few years ago, we had six different mobile apps supporting different products and businesses that we had, all the way from auto to bank products, investing, mortgage, et cetera. We had to move at an unprecedented pace so we could satisfy customer expectations. For that to happen, we could not have such a complicated ecosystem of apps. At the same time, we were also seeing customers overlapping with the different products we were offering. Customers on the bank side would open an investment account or a mortgage account. We launched this initiative called One Ally. Part of that punch line was: We now have a single app facing all of our customers across all business lines and products that we offer."

This consolidation was essential for the customer experience. A truly digital bank couldn't function as a collection of separate product silos—it needed to present a unified interface.

Investor Takeaway from the Digital Build: Ally's digital transformation required massive technology investments and organizational change. The company had to overcome its legacy systems while maintaining service quality. The success of this transformation—measured in customer growth and retention rates—became a key competitive advantage.

VIII. The COVID Era & Modern Challenges (2020-2025)

COVID Response Agility

The pandemic became an unexpected proving ground for Ally's digital capabilities. "In response to COVID-19 and stay-at-home orders, Ally was able to within two days launch an application to allow customers to apply for forbearance. Once a customer enrolled, it automatically connected to all the backend financial systems. It was all done in a weekend. That is the level of nimbleness mainframe modernization enables."

"Multiple decades of digital transformation happened within those two years of COVID, because everybody was becoming digital."

While traditional banks scrambled to serve customers remotely, Ally's entirely digital model became a significant advantage. The company had no branches to close, no physical infrastructure to maintain during lockdowns.

Leadership Transition

Jeffrey J. Brown stepped down at the end of January 2024 after nearly nine years as CEO. Doug Timmerman, Ally's President of Dealer Financial Services, served as interim CEO since Brown's departure.

Ally Financial announced that Michael G. Rhodes would be its new Chief Executive Officer, starting at the company on April 29, 2024. He would also be appointed as a member of Ally's board of directors at that time.

Prior to joining Ally in April 2024, Rhodes served as the CEO and president of Discover Financial Services and president of Discover Bank, as well as a member of the board of directors of Discover Financial Services and Discover Bank.

Rhodes brings to Ally over 25 years of experience across retail and consumer banking and has a track record of delivering transformative digital, data, and technology strategies.

Recent Strategic Moves: A Return to Focus

Under Rhodes' leadership, Ally has executed a significant strategic pivot—essentially a return to roots.

Higher-for-longer mortgage rates claimed their first victim of 2025 when Ally Financial announced it would exit the mortgage origination business as part of a broader strategy to pursue higher returns on investments.

The company is expected to make a full exit of the mortgage business by the end of the first quarter of the year. The move is part of a reorganization of the large lender, which is also planning to sell its credit card business in the first quarter.

Ally will soon stop making new mortgage loans, and it said Wednesday it sold its credit card business after a brief foray into the sector. "These actions simplify and streamline the company," said CEO Michael Rhodes, who joined the company in April of last year. He said the path toward higher profitability is through the "power of focus." Ally has agreed to sell the credit card business to the fintech firm Cardworks, which also owns the $3 billion-asset Merrick Bank, in a deal expected to close this year.

Ally's pivots aren't a result of its struggles last year in auto-loan quality, Hutchinson said, instead referring to them as "long-term strategic decisions" that better align the business with its strengths. In addition to its consumer auto portfolio, the company offers loans to auto dealers and other non-auto corporations. It also offers auto insurance and has built a large deposit franchise through its online bank. The company is focusing on areas "we have competitive advantage, we have relevant scale, and where we have a track record, where we've proven we can win," Hutchinson said.

2024-2025 Financial Performance

Ally Financial Inc delivered adjusted EPS of $2.35, core pre-tax income of $1 billion, and revenues of $8.2 billion in 2024.

Ally's auto finance segment remains its cash engine. Q1 auto loan originations hit $10.2 billion, with a record 3.8 million applications, fueled by a 9.8% originated yield. A key shift: 44% of originations now come from Super Prime borrowers (FICO 760+), up significantly from prior years.

Current Challenges

Retail auto net charge-offs increased to 234 basis points, reflecting ongoing challenges in the consumer finance space. The company carries an elevated population of late-stage delinquent accounts, posing a risk to future credit performance.

"There was a real fear that it was just going to keep going," said Brian Foran, an analyst at Truist Securities, but the improved outlook signals the company may have hit "peak losses." Losses ticked up slightly again in the fourth quarter, with net charge-offs on its retail auto loans increasing to an annualized rate of 2.34%, from 2.21% a year earlier. But Ally executives said they expect that figure to be between 2% and 2.25% this year, an improvement from earlier guidance that losses would be closer to 2.3%.

Investor Takeaway from the Modern Era: Rhodes' strategic refocus represents a recognition that diversification for its own sake doesn't create value. The exit from mortgages and credit cards—both businesses where Ally lacked competitive scale—allows capital and management attention to concentrate on the auto and digital banking franchises where Ally has genuine advantages.

IX. Playbook: Business Model & Competitive Advantages

The Digital Banking Model

Ally's digital bank, the largest all-digital bank in the U.S., now serves 3.4 million customers with $143 billion in deposits. Its 92% FDIC-insured deposit base and customer-centric model provide a critical edge over traditional banks like Bank of America and JPMorgan Chase.

Ally's scale in digital deposits (90% of funding) and dealer relationships could be framed as impenetrable barriers, especially against legacy banks and fintech upstarts.

The digital model offers several structural advantages:

Lower Cost Structure: Without branches to maintain, Ally can offer more competitive rates on deposits and loans. This creates a virtuous cycle: better rates attract more deposits, which fund more loans, which generate more income.

Customer Acquisition Efficiency: Digital channels scale more efficiently than physical branches. Adding the marginal customer costs very little.

Data Advantage: Digital interactions generate data that can improve underwriting, detect fraud, and personalize products.

The digital bank's emphasis on customer experience helped fuel a 95% customer retention rate in the third quarter. The bank reached 3.3 million primary deposit customers as of Sept. 30, up from 3 million a year earlier.

The Auto Finance Moat

Ally's auto finance business benefits from several competitive advantages rooted in its 100-year history:

Dealer Relationships: Originating from the former General Motors Acceptance Corporation (GMAC), Ally has over a century of deep, entrenched relationships with auto dealers. This network is a powerful and consistent source of loan volume, driving Q3 2025 consumer auto applications to 4 million.

Full-Service Platform: Ally offers dealers not just financing but insurance, remarketing, and ancillary services—creating switching costs and deepening relationships.

Underwriting Expertise: A century of auto lending has generated enormous data and institutional knowledge about vehicle depreciation, borrower behavior, and loss patterns.

Ally Financial ranked highest in overall dealer satisfaction in the subprime category for the fourth consecutive year.

Competitive Landscape

The auto finance market remains highly competitive. Toyota Financial Services, Ally Financial Inc., Ford Motor Credit Co., Volkswagen Financial Services AG and Santander Consumer Finance, S.A. are the major companies operating in this market.

The global car finance market features intense competition among major players like Wells Fargo, Toyota Financial Services, Ally Financial, and Ford Credit. These key players leverage their vast networks, robust financial solutions, and customer-centric approaches to capture a significant market share.

Ally Financial processed 14.6 million applications in 2024 after re-platforming its origination stack to cloud-native microservices, while reporting that 44% of volume came from top-tier credit segments.

The competitive threat from captive finance companies (Ford Credit, GM Financial, Toyota Financial Services) is significant because they can subsidize rates to support parent company vehicle sales. Independent lenders like Ally must compete on service quality, relationship depth, and operational efficiency rather than subsidized pricing.

X. Investment Framework: Bull & Bear Cases

The Bull Case

1. Digital Banking Scale Advantage Ally's position as the largest all-digital bank creates genuine economies of scale. Customer acquisition costs are lower, operating leverage is higher, and the company can offer competitive rates while maintaining margins.

2. Auto Finance Leadership With nearly a century of experience and relationships with over 22,000 dealers, Ally's auto finance franchise represents a durable competitive advantage. The shift toward super-prime borrowers (44% of originations) reduces credit risk while maintaining attractive yields.

3. Strategic Focus The exit from mortgages and credit cards allows management to concentrate on businesses with genuine competitive advantages. Capital allocation becomes cleaner, and the company's earnings become more predictable.

4. Interest Rate Tailwinds Looking ahead, Ally could be a major beneficiary as interest rates start to come down. Not only does Ally's deposit cost move lower as the Fed cuts rates, but lower interest rates are typically accompanied by higher demand for auto loans.

5. Valuation Ally trades at a price-to-tangible book value of 1.2x, below peers like Discover Financial at 1.4x.

The Bear Case

1. Credit Cycle Vulnerability Auto lending is inherently cyclical. In a recession, unemployment rises, loan losses increase, and collateral values (used car prices) typically decline. Ally's concentration in auto lending magnifies this exposure.

2. Competitive Pressure Captive finance companies can subsidize lending rates to support vehicle sales. If OEMs become more aggressive with financing incentives, Ally's margins could compress.

3. Digital Banking Competition The "digital first" advantage is eroding as traditional banks improve their digital offerings and fintech competitors proliferate. What was once differentiation is becoming table stakes.

4. Deposit Stability Uncertainty Ally's deposit base has grown impressively, but these deposits are largely rate-sensitive. If competitors offer higher rates or if economic stress causes depositors to seek perceived safety, Ally could face funding pressure.

5. Regulatory Overhang Ally has faced regulatory challenges, including a $80 million settlement with the Consumer Financial Protection Bureau in 2015 for discriminatory auto loan pricing disproportionately affecting minority borrowers and a $52 million resolution in 2016 for misleading disclosures in mortgage-backed securities issuances.

Porter's Five Forces Analysis

Threat of New Entrants: Medium While fintech entrants are emerging, the capital requirements, regulatory complexity, and need for dealer relationships create meaningful barriers. The threat is higher in consumer deposits than in wholesale auto lending.

Bargaining Power of Suppliers: Low Ally's "suppliers" are primarily capital (depositors and wholesale funding markets). As a large, well-capitalized institution, Ally has strong access to funding at competitive rates.

Bargaining Power of Buyers: Medium-High Auto dealers have significant bargaining power because they control the point of sale. Ally must continuously earn dealer loyalty through service quality and competitive pricing.

Threat of Substitutes: Medium Direct lending from OEM captives, credit union competition, and emerging point-of-sale lending platforms all represent substitutes. The used car market (where OEM captives are less active) provides some protection.

Industry Rivalry: High Competition among large auto lenders is intense, with limited differentiation on price. Service quality, technology, and relationship management are the key differentiators.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Present Ally's digital banking model exhibits strong scale economies—each incremental deposit or loan requires minimal additional cost. The auto finance business benefits from scale in origination, servicing, and risk management.

Network Effects: Weak Unlike payment networks or social platforms, lending exhibits weak network effects. More borrowers don't make the product more valuable to other borrowers.

Counter-Positioning: Present (Fading) Ally's branchless model initially represented counter-positioning against traditional banks, which couldn't easily eliminate their branch networks. However, as digital banking becomes standard, this advantage is fading.

Switching Costs: Moderate Dealer switching costs exist due to system integration and relationship depth. Consumer switching costs are lower—deposits can move quickly—though inertia and account complexity create some friction.

Branding: Moderate The Ally brand has positive associations with digital convenience and competitive rates, but lacks the emotional connection of traditional banking brands or the tech cachet of newer fintechs.

Cornered Resource: Present (Dealer Relationships) Ally's century-old dealer relationships represent a cornered resource that competitors cannot easily replicate. These relationships generate origination volume and data that improves underwriting.

Process Power: Present Ally's underwriting expertise—built over 100+ years of auto lending—represents genuine process power. The company can price risk more accurately than less experienced competitors.

XI. Key Metrics to Watch

For investors tracking Ally's performance, three metrics deserve particular attention:

1. Retail Auto Net Charge-Off Rate

This metric captures the percentage of auto loan balances that Ally writes off as losses. It's the single most important indicator of credit quality in the core business.

Current Level: 2.34% in Q4 2024 2025 Guidance: 2.00%-2.25% Why It Matters: Higher-than-expected charge-offs directly reduce earnings and may signal broader credit deterioration. Conversely, better-than-expected charge-offs indicate underwriting discipline is paying off.

2. Net Interest Margin (NIM)

NIM measures the difference between what Ally earns on its assets (loans) versus what it pays for its liabilities (deposits and other funding). It's the fundamental measure of lending profitability.

Current Level: 3.33% in Q4 2024 2025 Guidance: 3.40%-3.50% Why It Matters: NIM reflects both competitive dynamics and interest rate positioning. Improvement signals pricing power and efficient balance sheet management.

3. Deposit Customer Growth and Retention

The digital bank's health is best measured by customer metrics rather than just balance totals. Growing the base of engaged customers creates long-term value.

Current Level: 3.4 million primary deposit customers; 95% retention rate Why It Matters: Customer growth indicates competitive positioning in digital banking. High retention suggests the value proposition is working. Declining retention could signal vulnerability to competitors.

XII. Conclusion: A Century of Reinvention

The Ally Financial story is, at its core, a story about institutional adaptability. The company that invented consumer auto financing in 1919 has reinvented itself multiple times: from GM captive to diversified financial services company, from bailout recipient to independent public company, from traditional lender to digital banking pioneer.

The 2008 financial crisis nearly destroyed the company, but it also forced a fundamental rethinking that led to the Ally of today. The lessons of that near-death experience—particularly the dangers of straying from core competencies—appear to be informing current strategy under Michael Rhodes.

The exit from mortgages and credit cards represents a bet that focused excellence beats diversification. Whether that bet pays off depends on Ally's ability to:

- Maintain its dealer relationships and auto origination volume against well-funded captive competitors

- Continue growing its digital deposit franchise despite increasing competition

- Navigate credit cycles without catastrophic losses

- Generate returns on equity sufficient to justify the capital required for banking operations

For investors, Ally represents an intriguing combination: a century of institutional knowledge, a genuinely differentiated digital banking model, and a management team committed to focus and discipline. The stock's valuation below tangible book value suggests the market remains skeptical about the sustainability of these advantages.

That skepticism may be warranted—the ghost of 2008 still haunts this company's DNA. But for those who believe in Ally's execution and strategic direction, the current valuation provides a margin of safety.

GMAC was founded to solve a simple problem: helping Americans buy cars they couldn't quite afford. A century later, Ally Financial is still in that business—but now it's also America's largest digital bank, serving 11 million customers who need a better way to manage their money. The transformation from "GM's financing arm" to "America's digital bank" represents one of the more remarkable corporate reinventions in modern business history.

The question for the next century is whether Ally can continue to adapt—or whether the competitive pressures of digital banking and auto finance will eventually compress its advantages to zero. Based on its history of reinvention, betting against this company's adaptability seems unwise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube