Aflac: The Duck That Built an Empire

I. Introduction & Episode Roadmap

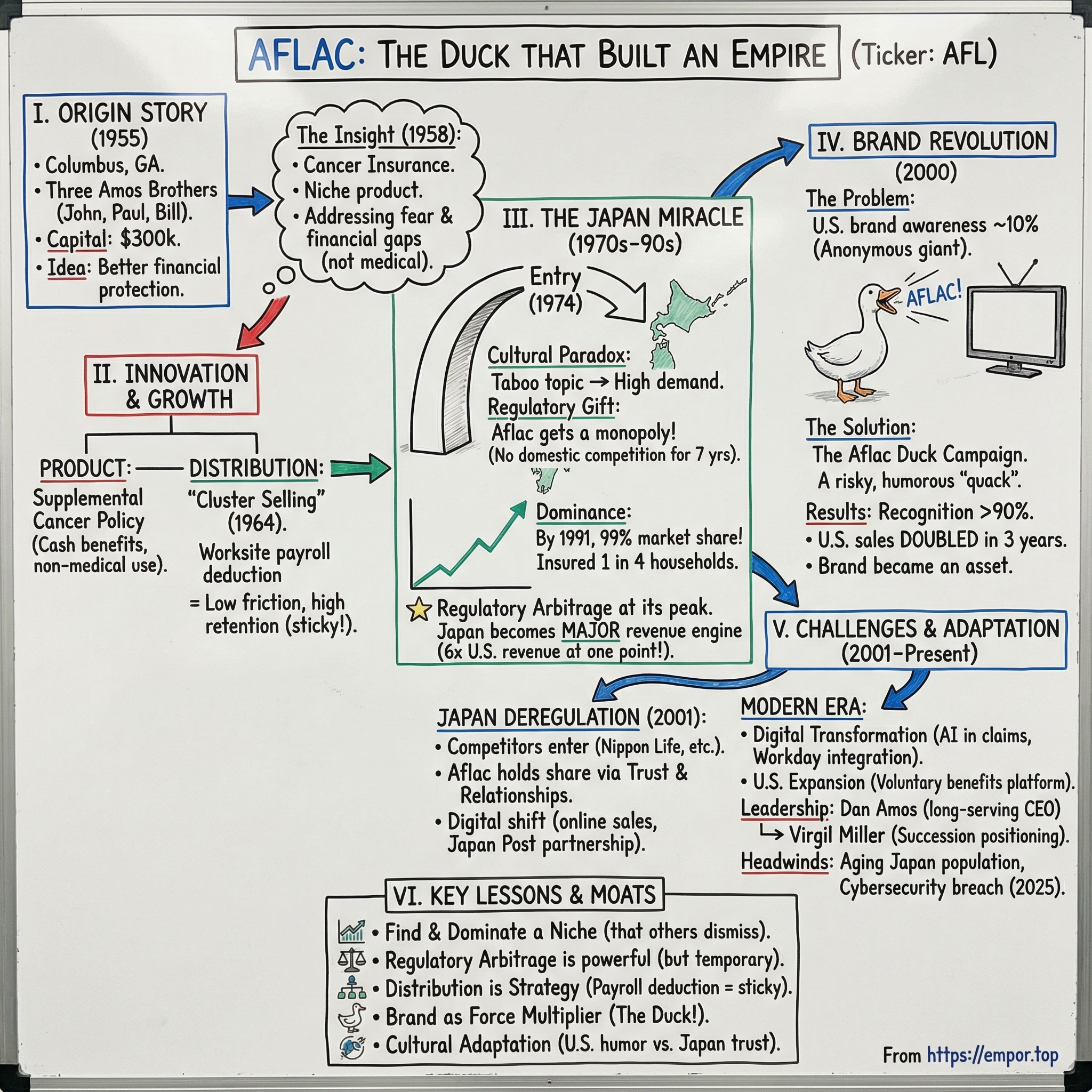

Picture this: a white duck waddles across your television screen, opens its beak, and screams a single word that somehow sounds exactly like a company name you have never heard of. It is the year 2000. The internet bubble is about to pop, financial services advertising is stiff and humorless, and a Fortune 500 company that most Americans cannot name is about to pull off one of the greatest brand-building stunts in marketing history. Within three years, that duck will double the company's sales. Within a decade, brand recognition will leap from under ten percent to above ninety. But here is the twist that makes this story truly remarkable: the duck is not even the most interesting part of the Aflac story.

Aflac Incorporated is a nearly nineteen-billion-dollar-a-year supplemental insurance colossus headquartered in Columbus, Georgia, a mid-sized city in the western part of the state that most people drive through on their way to somewhere else. The company provides financial protection to more than fifty million people worldwide. It is the number one provider of supplemental health insurance in the United States and, astonishingly, the largest individual insurance company in Japan, a country where it generates roughly sixty percent of its adjusted revenue and holds seventy-seven percent of its total assets.

The central question of this story is one that sounds almost absurd when you say it out loud: How did three brothers from a small town in the American South build the single largest foreign insurance company in Japan, a market that had been virtually impenetrable to outsiders for decades? The answer involves a father's death from cancer, a product nobody else wanted to sell, a trade deal that inadvertently gifted Aflac a monopoly, and, eventually, a duck that changed everything.

The themes that run through this narrative are universal ones for students of great businesses: the power of finding and dominating a niche before anyone else realizes it matters, the art of regulatory arbitrage, the compounding advantage of distribution innovation, and the way a single marketing insight can unlock decades of latent brand equity. Along the way, we will trace the arc of a family business that has now spanned three generations, survived the death of its founder, navigated Japan's lost decades, weathered deregulation, and emerged into the modern era as a company that returns nearly five billion dollars a year to shareholders while grappling with demographic headwinds, cybersecurity crises, and a competitive landscape that grows more crowded by the quarter.

To understand supplemental insurance for those unfamiliar with the concept, think of it this way: your regular health insurance is like the walls and roof of your house. It covers the big structural things. But when a storm hits, water gets through the cracks, the gaps around the windows, the seams in the foundation. Supplemental insurance covers those gaps. It pays cash benefits directly to the policyholder when a covered event occurs, money that can be used for anything: mortgage payments, groceries, gas to drive to treatment, or the thousand small expenses that pile up when a family member is fighting a serious illness. The product does not replace primary insurance. It sits alongside it, catching what falls through.

This is the story of Aflac.

II. The Amos Brothers & Founding Vision

In the spring of 1955, three brothers drove into Columbus, Georgia, with roughly three hundred thousand dollars in capital, a handful of insurance licenses, and a conviction that there was a better way to protect American families from financial ruin. The eldest, John Beverly Amos, was thirty years old. He had been born in Enterprise, Alabama, a town whose most famous landmark is a monument to the boll weevil, the pest that destroyed cotton farming and forced local farmers to diversify into peanuts. The metaphor is almost too perfect: John Amos would spend his career forcing an entire industry to diversify into a product nobody wanted to touch.

John's path to insurance was anything but linear. As a teenager in Milton, Florida, he set type for a local newspaper and eventually published his own tabloid, the Jay Tribune, displaying an entrepreneurial streak that would define his career. He attended the University of Miami, where he met his wife, Elena Diaz-Verson, a Cuban emigrant whose family would later play their own role in the company's story. He earned a law degree from the University of Florida and launched his career as a city attorney in Fort Walton, Florida. In 1952, he ran for political office and lost. That defeat turned out to be one of the most consequential failures in American business history, because it pushed Amos toward a different path entirely.

After the campaign, he became general counsel to the Southern Governors Association and special attorney to the governor of Florida. Through that legal work, he was hired to negotiate agreements for establishing a gas pipeline system serving Okaloosa County, Florida. The legal fees from that engagement totaled forty thousand dollars, a sum that in 1955 carried real weight. That money became the seed capital for what would become one of the most profitable insurance companies on the planet.

John, along with his brothers Paul and Bill, chose Columbus, Georgia, for several practical reasons that reveal the strategic thinking that characterized the early company. Georgia had a respected insurance regulatory department. The climate for the insurance business was friendly. Columbus had enough population to support a new insurer but did not already have one headquartered there.

They incorporated as the American Family Life Insurance Company of Columbus, Georgia, a name so long and forgettable that it would eventually become part of the company's origin myth. The city of Columbus itself was an unlikely place to build a global insurance empire. Situated on the Chattahoochee River at the Alabama border, it was known more for its textile mills and Fort Benning than for financial services. But John Amos did not need a financial capital. He needed a place where regulators would welcome a new entrant and where the cost of doing business was low enough to stretch three hundred thousand dollars as far as it could go.

The first years were brutal. The three brothers sold life, health, and accident insurance door-to-door across Georgia and Alabama, grinding through the kind of rejection that only door-to-door salespeople truly understand. Picture the summer heat of rural Georgia in the 1950s, John Amos in a suit and tie knocking on screen doors, competing for attention against the television sets that were just beginning to dominate American living rooms.

In their first full year, they signed 6,426 policyholders, a respectable number but hardly the foundation for an empire. The problem was not effort or talent. The problem was that the Amos brothers were selling the same commoditized products that dozens of other small insurers were selling, competing on nothing more than personality and persistence in a market where the established players had deeper relationships and longer track records.

Three years of this struggle forced a reckoning. John Amos was not the kind of person who accepted a slow grind toward mediocrity. He began looking for a niche, a product category where the competition was thin and the need was real. The insight that would change everything came from the most personal of places: his own father had died of cancer, and John had watched the disease devastate not just his father's health but the family's finances. In the late 1950s, cancer was becoming America's second-leading cause of death, but the insurance industry treated it as just another illness covered, inadequately, under general health policies. Most comprehensive health insurance covered only about seventy percent of cancer treatment costs. The remaining thirty percent, plus indirect expenses like travel, lost income, and childcare, could be ruinous. A single cancer diagnosis could push a middle-class family into bankruptcy, not because of the disease itself but because of the financial weight it imposed on everyone around the patient.

John Amos looked at that gap and saw an opportunity that no one else in the industry was willing to pursue. The major insurers considered standalone cancer coverage too morbid, too niche, and too difficult to underwrite profitably. They also worried about adverse selection, the risk that only people who suspected they might get cancer would buy the product, which would make the risk pool unprofitable. Amos believed these concerns were overblown. If you sold cancer insurance broadly enough, through workplaces and organizations rather than to worried individuals, the risk pool would be diverse enough to make the economics work.

What made this insight so powerful was not just the identification of an unmet need. It was the recognition that fear, specifically the deep, primal fear of cancer, could be channeled into a product that offered genuine peace of mind. The Amos brothers were not selling insurance in the traditional sense. They were selling protection against a nightmare, and that emotional resonance would prove to be far more durable than any actuarial advantage. Every American family knew someone who had been touched by cancer. Every family could imagine the financial devastation it could bring. The product sold itself because the need was visceral.

III. The Cancer Insurance Innovation

In 1958, John Amos sat down and designed a product that the rest of the insurance industry considered either too morbid or too risky to touch. He modeled it on the polio insurance policies that had been popular in previous decades, during the years when polio terrorized American families in much the same way that cancer did in the late 1950s. The logic was elegant: if families had been willing to buy standalone coverage for a single dreaded disease before, they would do it again for a disease that was even more common and even more expensive to treat.

The cancer insurance policy that Aflac introduced was not designed to replace comprehensive health insurance. It was designed to supplement it, covering the expenses that fell through the cracks: the co-pays, the deductibles, the travel to treatment centers, the lost wages when a breadwinner could not work.

This distinction, supplemental rather than primary, would become the conceptual foundation of everything Aflac would build over the next seven decades. It was also, crucially, the reason regulators would eventually allow Aflac into markets that were closed to conventional insurers. Because Aflac was not competing with primary health insurers, it occupied a different regulatory category. It was not threatening to replace existing coverage. It was adding a layer on top. This positioning gave Aflac access to markets and distribution channels that a primary insurer would have been locked out of.

The results in the first year were encouraging. Aflac's 150 licensed agents sold 5,810 cancer care policies, nearly matching the total number of all policyholders the company had accumulated in its first year of selling general insurance. The cancer product had found an audience.

By 1959, premiums reached nine hundred thousand dollars and operations expanded into Florida. By 1967, premiums hit seven million dollars. The product was working, but it was working slowly, constrained by the limitations of door-to-door sales in a handful of Southern states. Aflac needed a way to reach more people, more efficiently, without proportionally increasing its sales force.

The breakthrough in distribution came in 1964, when Aflac developed what it called "cluster selling," a technique that would prove to be one of the most important innovations in insurance distribution history. Instead of knocking on residential doors, agents approached a company or organization and asked for permission to present policies to its employees or members. The agent would make a group sales pitch, often with the implicit endorsement of the employer. John Amos understood the psychology perfectly: "Sooner or later, there's going to be a cancer in the group. If he's insured, he's satisfied. If not, he thinks, 'If I'd only bought insurance from that fellow when he came through.'" The social proof was built into the product's very nature.

This worksite model was transformative for several reasons.

First, it dramatically lowered the cost of customer acquisition. Instead of visiting one household at a time, an agent could present to dozens or hundreds of employees in a single session. The economics of insurance sales are brutal when done door-to-door: the cost of acquiring each customer eats into the already-thin margins on a supplemental policy. By concentrating prospects in a single location, the worksite model made the math work.

Second, it introduced payroll deduction as the payment mechanism, which reduced lapse rates and created a recurring revenue stream that was far more predictable than individual premium collection.

Third, and most subtly, it shifted the buying psychology from an individual decision made in isolation to a social decision made in the context of one's workplace, where the implicit endorsement of the employer and the visible participation of colleagues created powerful behavioral nudges. When you see your coworker signing up for cancer insurance, the question shifts from "Should I buy this?" to "Can I afford not to?"

The payroll deduction model became so dominant that by 2003, more than ninety-eight percent of Aflac's policies in the United States were issued on that basis. Think about what that means from a business model perspective: nearly the entire revenue base was collected automatically, with minimal friction, through a channel that the customer interacted with every two weeks regardless. The churn characteristics of that model are fundamentally different from, say, a direct-to-consumer insurance product where the customer must actively choose to renew. In the language of recurring revenue businesses, payroll deduction created what amounted to a negative churn dynamic: the default action was to keep paying, and cancellation required a deliberate, somewhat inconvenient effort. This is the same principle that makes gym memberships and SaaS subscriptions so sticky, applied to an insurance product decades before anyone coined the term "subscription economy."

The worksite model also created a natural expansion mechanism. Once Aflac had a relationship with an employer, it could layer additional products onto the same distribution channel. An agent who initially sold cancer insurance to a company's workforce could return the following enrollment period offering accident, hospital indemnity, or critical illness coverage, all collected through the same payroll deduction. Each new product increased the revenue per employer relationship without proportionally increasing the sales cost.

The cancer insurance product also attracted criticism, and the controversy is worth examining because it shaped the company's political and communications capabilities in ways that proved essential later.

In the late 1970s and 1980s, multiple regulatory bodies questioned whether cancer insurance was exploitative, preying on fear to sell a product of limited value. Congressional committees investigated. The FTC and several state insurance departments raised concerns. Some states, including Missouri, New York, New Jersey, and Connecticut, placed restrictions on dread-disease policies.

Aflac defended its product vigorously, noting that millions of informed customers continued purchasing coverage voluntarily, and even filed lawsuits against ABC and Changing Times magazine over critical coverage that the company considered unfair. The company argued, with some justification, that the critics were confusing the product's narrow scope with a lack of value. Cancer insurance was never meant to cover everything. It was meant to cover the specific financial gaps that cancer created, and for families facing those gaps, the product delivered real and measurable benefit.

The regulatory battles taught Aflac something important: the supplemental insurance niche existed in a gray zone between primary health insurance and pure financial products, and navigating that gray zone required both political sophistication and an unshakeable conviction in the product's value. These skills would prove essential when the company turned its attention to a market that made the American regulatory environment look simple by comparison.

IV. The Japan Opportunity & Entry

In 1970, John Amos boarded a plane to Osaka for the World's Fair, known as Expo '70, Japan's grand showcase to the world. The fair attracted sixty-four million visitors and was meant to demonstrate Japan's arrival as a modern technological power. Amos went for the spectacle but came home with something far more valuable: a conviction that Japan would be the perfect market for cancer insurance.

The insight was counterintuitive on its surface. Japan's insurance market was one of the most protected and insular in the world. Foreign companies found it virtually impossible to obtain licensing from the Ministry of Finance. The domestic insurers were enormous, deeply connected to Japan's corporate conglomerates, and had no interest in sharing their market with American upstarts. No U.S. insurance company had been licensed to operate in Japan since the Allied occupation following World War II.

But Amos saw something that the conventional wisdom missed entirely. Japan had a unique cultural relationship with cancer that created both enormous demand for cancer insurance and a complete absence of supply. Cancer in Japan was not just a disease. It was, in the fullest sense of the word, unspeakable. The prospect of cancer, mixed with the deep currents of stoicism and reserve that ran through Japanese culture, made the disease virtually unmentionable. Physicians would not even necessarily inform patients that they had cancer, considering the diagnosis too dispiriting to share. A 1992 survey of Japanese physicians found that only thirteen percent communicated cancer diagnoses to their patients. The Japanese language itself reflected this aversion: there was a precise word, "pokkuri shinu," meaning roughly "popping off," and specific temples called "pokkuri dera" where elderly Japanese prayed for a quick, no-fuss death rather than the prolonged suffering that cancer represented.

This cultural context meant that no Japanese insurance company was willing to develop or sell a standalone cancer insurance product. The subject was too taboo, the product too closely associated with the unmentionable disease. As one industry analyst later put it, "Aflac was the only company willing to write cancer insurance, or even discuss it."

Japanese policymakers, looking at this obscure product category that no domestic company wanted, essentially shrugged and decided to give it to the Americans. Their reasoning, as it would later be characterized, was straightforward: "Nobody is going to buy dreaded disease insurance, so let's give it to the Americans."

It was one of the most spectacularly wrong regulatory assumptions in the history of financial services. The policymakers were correct that no Japanese company wanted to sell the product. They were catastrophically wrong about whether anyone would want to buy it.

Amos was not deterred by the barriers to entry. He quickly formulated a plan that demonstrated the same practical ingenuity that had characterized his career. Rather than fighting the Japanese establishment, he would co-opt it. His choice of company officers included many luminaries of the Japanese insurance industry, lending the venture credibility and connections that a purely foreign operation could never have achieved. He forged strategic alliances with major domestic entities, including some of the largest Japanese conglomerates: Mitsui, Mitsubishi, Dai-Ichi Kangyo, and Sanwa banks would serve as distribution agents.

Four years of persistence, relationship-building, and bureaucratic navigation followed Amos's initial visit to Osaka. He made repeated trips to Tokyo, cultivating relationships within the Ministry of Finance, the Japanese insurance establishment, and the political sphere. He recruited Japanese industry veterans to serve on his board and in executive positions, demonstrating respect for local expertise and creating powerful advocates within the system.

In June 1974, the Ministry of Finance granted Aflac a license to sell insurance in Japan. The company became only the second U.S. insurer to be licensed in Japan in more than two decades, and the first to actually operate there since the occupation era. This was not just a business milestone. It was a geopolitical anomaly, a small company from Columbus, Georgia, threading a needle that multinational giants had failed to penetrate. The major American insurers, with all their resources and political connections, had been unable to crack the Japanese market. A family company from the Deep South, with a niche product that the Japanese establishment considered unmarketable, had done what the giants could not.

Aflac's approach to the Japanese market reflected a deep understanding of local culture and business practices. Rather than importing American sales techniques wholesale, the company employed retired workers as its agents, a move that proved brilliant on multiple levels. Retired workers had existing relationships with former colleagues, who were natural prospects for cancer insurance. They had credibility born of decades of professional experience. And the practice impressed the Ministry of Finance, which viewed it as a socially responsible approach to the problem of aging workers seeking purpose and income in retirement.

The timing was also exquisite, though some of that was luck rather than design. Cancer awareness in Japan was beginning to expand just as Aflac arrived with a product specifically tailored to address it. The taboo around the disease was starting, ever so slowly, to erode, and with that erosion came a growing recognition among Japanese families that they were financially vulnerable to a disease they could not bring themselves to name. Japan's national health insurance system, while comprehensive by global standards, still left gaps in coverage that a supplemental cancer policy could fill, particularly for expensive treatments, extended hospital stays that were common in Japanese medical practice, and the indirect costs that accompany any serious illness.

There is an important business lesson embedded in Aflac's Japan entry that deserves attention. Most companies trying to enter a protected foreign market approach the problem as a negotiation: how do we convince regulators to let us in? Amos approached it as an alignment problem: how do we offer something that serves the regulators' interests? By bringing a product that no domestic company wanted to sell, by employing retired workers who needed income, and by staffing leadership positions with respected Japanese insurance veterans, Amos made it easy for the Ministry of Finance to say yes. He removed every objection before it could be raised. This is a masterclass in market entry strategy that remains relevant for any company contemplating expansion into a protected market.

V. Building the Japanese Empire

When Aflac opened for business in Japan in 1974, it introduced cancer insurance to a country that had never seen such a product. What happened next was one of the most remarkable competitive advantages in the history of the insurance industry: for seven years, from 1974 through 1981, Aflac was the only company selling cancer insurance in Japan. It had a literal monopoly, not because of any patent or proprietary technology, but because no domestic insurer wanted the product and regulators saw no reason to license additional foreign competitors for a category they considered marginal.

Then, in 1981, something shifted that would transform Aflac's trajectory permanently: cancer became the leading cause of death in Japan. The disease that Japanese culture had struggled to name was now the country's number one killer. Media coverage intensified. Public health campaigns began, hesitantly, to address prevention and early detection. And suddenly every family in Japan had a reason to think about financial protection against the disease that had long been whispered about but never discussed openly.

Aflac was already there, established, trusted, and the only name associated with cancer insurance. The growth that followed was explosive even by the standards of high-growth markets.

By 1986, Aflac Japan's policies had increased to 5.4 million, compared with just 731,000 a decade earlier, a sevenfold increase that reflected both the expanding awareness of cancer and Aflac's first-mover advantage.

By 1987, the Japanese market accounted for two-thirds of Aflac's total revenues and seventy percent of after-tax earnings. Pause on that for a moment. A small insurance company from Georgia, founded by three brothers with no international experience, was now generating the vast majority of its profits from a country on the other side of the world, in a product category that the Japanese establishment had dismissed as unmarketable. It was one of the most improbable geographic transformations in American corporate history.

The market share numbers were staggering. By 1988, Aflac Japan controlled eighty-eight percent of the cancer insurance market. By 1991, that figure had climbed to ninety-nine percent. These are monopoly-level numbers in a major developed economy, achieved not through predatory pricing or anticompetitive behavior, but through the simple fact that Aflac had created and defined the category. When competitors finally did enter, they were competing against a company that had already insured a significant fraction of the Japanese population.

To put this dominance in context, consider what it means to control ninety-nine percent of a major insurance product category in the world's second-largest economy. It means that virtually every cancer insurance policy in Japan had the Aflac name on it. It means that the company's claims-paying reputation was built on millions of individual experiences, families who had received payments during their darkest hours and who told friends, neighbors, and colleagues about it. It means that Aflac did not just sell a product in Japan. It created a category, defined its terms, and became synonymous with it in a way that few companies in any industry have ever achieved.

The trade dynamics between the United States and Japan during this period inadvertently reinforced Aflac's dominance. Thanks to wrangling between the two countries over trade issues, Japanese regulators kept large domestic insurance companies from competing in supplemental insurance products until 2001. The 1996 U.S.-Japan trade agreement explicitly protected companies already established in "niche" markets, effectively making the cancer insurance sector off-limits to domestic Japanese firms for another five years. This was regulatory arbitrage at its most powerful: Aflac benefited from American trade negotiators pushing for market access in Japan, while simultaneously enjoying protection from Japanese competition in the very niche it had created.

By 1994, Aflac's cancer life policy covered one out of every four Japanese households. Think about that number for a moment. In a country of 125 million people, organized into roughly fifty million households, one in four had an Aflac policy. For a foreign company operating in one of the most insular markets on earth, this level of penetration was almost without precedent in any industry.

By 1995, premium income from Japan was 5.2 billion dollars, compared with 860 million in the United States, a ratio of more than six to one. The tail was now wagging the dog in the most dramatic fashion imaginable: a company headquartered in Columbus, Georgia, was earning six times as much revenue from Japan as from its home country.

In June 1997, the company became the first foreign insurer in Japan to exceed two trillion yen in gross assets. And by 1999, Aflac had established policies with employees at ninety-five percent of the companies listed on the Tokyo Stock Exchange. That last statistic deserves emphasis: virtually every major corporation in Japan was an Aflac client.

During this period, the company also expanded its product line in Japan beyond pure cancer insurance. In 1990, it introduced the "Super Cancer" policy with upgraded benefits. In 1992, the "Super Care" policy extended coverage to nursing home care and non-cancer conditions. These product extensions leveraged the brand trust that Aflac had built through cancer insurance to create a broader supplemental insurance platform, a strategy that would become even more important as competition eventually arrived.

The corporate structure evolved to reflect the growing importance of the Japanese business. In 1973, American Family Corporation was formed as a holding company. The company was listed on the New York Stock Exchange in 1974, the same year it received its Japanese license, giving it access to public capital markets at precisely the moment it needed funds to finance its Japan expansion.

In 1989, the company adopted the trade name "Aflac," a decision driven partly by the need for a brand that worked in both English and Japanese. On January 1, 1992, the holding company was officially renamed Aflac Incorporated. These were not just cosmetic changes. They signaled a company that understood its identity was increasingly defined by its Japanese operations and needed a brand architecture to match.

In 2000, Aflac Japan formed a major strategic marketing alliance with Dai-ichi Mutual Life Insurance Company, Japan's second-largest life insurer, which had more than 1,900 sales offices and over 50,000 licensed salespeople. This partnership gave Aflac access to a distribution network that would have taken decades to build organically, and it signaled that the Japanese insurance establishment had come to view Aflac not as a foreign interloper but as a permanent and valued part of the landscape.

The company also made a significant corporate decision in 1997, divesting its entire broadcasting unit to Raycom for 485 million dollars. Aflac had acquired television stations in the late 1970s as a diversification play, a common strategy for cash-rich companies at the time. But by the late 1990s, with the Japanese business generating extraordinary returns and the U.S. insurance business poised for growth, management concluded that broadcasting was a distraction from the core franchise. The divestiture was a sign of strategic maturity: the company was willing to shrink to grow, shedding a profitable but non-core business to concentrate resources on what it did best.

The story of Aflac in Japan during this quarter-century is ultimately a story about the power of being first in a market that turned out to be enormous. John Amos's original insight, that cancer fear could be channeled into an insurance product, combined with the regulatory accident that gave Aflac a protected monopoly, created one of the most durable competitive advantages in the global insurance industry. Net income grew over twenty percent annually between 1992 and 2002, a decade of compounding that transformed Aflac from a regional American insurer into a global financial powerhouse. The company that three brothers had started with three hundred thousand dollars was now managing tens of billions in assets across two continents, and its cancer insurance product had touched the lives of tens of millions of families. But even as the Japanese empire was being built, the company faced a very different kind of challenge back home: nobody in America knew who they were.

VI. The Duck Revolution

In the late 1990s, Aflac had a problem that was almost comically ironic. The company was one of the most successful insurers in the world, a Fortune 500 company with billions in revenue and a dominant position in the world's third-largest economy. And almost nobody in America had heard of it. Despite nine years of traditional advertising campaigns, featuring the kind of earnest, forgettable creative work that characterizes most financial services marketing, Aflac's national brand awareness hovered stubbornly between six and twelve percent. For a company whose entire U.S. business model depended on worksite sales, this obscurity was not just embarrassing. It was a genuine competitive handicap. Agents could not sell a product from a company that nobody recognized.

In 1999, the company hired a new advertising agency, the Kaplan Thaler Group, a New York firm known for its "Big Bang" approach to advertising, the belief that campaigns succeed most when they fundamentally alter consumers' perception of a brand. Two creative agents from the agency were sitting on a bench in Central Park, brainstorming ideas for the Aflac account, when they heard ducks quacking in the nearby pond. The quacking sounded, improbably but unmistakably, like "Aflac." One version of the story has an art director walking around the park muttering the company's name aloud, "Aflac, Aflac," and suddenly realizing the phonetic similarity. Either way, the duck concept was born from one of those accidents of creative insight that look obvious in retrospect but required someone to actually notice it.

The idea was presented to Dan Amos and the Aflac leadership team, and the reception was, to put it diplomatically, cool. "We knew we were making fun of our name and we were not sure how that would turn out," Amos later said. "Nobody was doing humor in financial services ads to a great degree. There was a dead look on everyone's faces when we first showed it." The internal resistance was understandable. Insurance is a product built on trust, and trust is traditionally communicated through gravitas, not comedy. Making your company's name the punchline of a joke felt like a gamble that could easily backfire.

Daniel Amos, the son of co-founder Paul Amos and the company's CEO since 1990, deserves significant credit for what happened next. He was forty-eight years old at the time, a University of Georgia graduate who had earned an MBA from Emory and had joined Aflac in 1973, working his way up through the sales ranks where he became the company's top performer before being named president in 1983 and CEO seven years later. He had spent his entire adult life in the insurance business, which made his willingness to approve an advertising campaign built around a screaming duck all the more remarkable. "We took a big chance making fun of our name, because you're not just doing it, you're actually making fun of your name," he told Yahoo Finance years later. "And yet, it forever changed our life."

The first commercial, called "Park Bench," aired on December 31, 1999, voiced by the comedian Gilbert Gottfried, whose nasally, abrasive delivery turned the duck's quack into something simultaneously annoying and unforgettable. The premise of the ad was simple: two people sitting on a park bench discuss their insurance needs while a frustrated duck tries, unsuccessfully, to get their attention by shouting "Aflac!" The humor lay in the disconnect between the duck's obvious answer and the humans' obliviousness, a dynamic that resonated with anyone who had ever felt invisible or unheard.

On January 1, 2000, Americans got their first real glimpse of the campaign, and the response was immediate and overwhelming. In the first two weeks of 2000, the company received more sales leads than in all of 1998 and 1999 combined. Annualized premium sales jumped 28.5 percent in the second quarter of 2000. Agents reported that for the first time, prospects were coming to them rather than the other way around.

The brand recognition numbers told the most dramatic story. Before the campaign, Aflac's awareness among American consumers sat at roughly twelve percent. After the duck's introduction, it shot to seventy-one percent. As the campaign continued through the following years, recognition soared above ninety percent, eventually reaching ninety-four percent by 2014. Aflac had gone from one of the most anonymous Fortune 500 companies in America to one of the most recognized in a span of just a few years, and it had done so by embracing the very thing that most companies would consider a liability: a name that sounded like a barnyard animal.

The financial impact was equally transformative. Within three years of the first ad, Aflac's sales in the United States doubled. The duck mascot has been credited with generating approximately two hundred million dollars in shareholder value over its lifetime, a calculation based on the stock's appreciation from roughly twenty-eight million dollars in market value at the campaign's launch to multiples of that figure. The duck was inducted into the Advertising Walk of Fame in 2004, made its first appearance in the Macy's Thanksgiving Day Parade in 2011, and became one of the most recognizable corporate mascots in American advertising history, alongside the Geico Gecko and the Energizer Bunny.

There was one notable stumble. In March 2011, Gilbert Gottfried, who had been the voice of the duck for over a decade, tweeted twelve jokes about the devastating earthquake and tsunami that had struck Japan three days earlier. Given that Aflac derived roughly seventy-five percent of its business from Japan, the company fired Gottfried immediately. He was replaced by Daniel McKeague, who won a nationwide casting call by doing an impression of Gottfried's voice. The episode was a reminder that the duck was not just a marketing gimmick. It was a strategic asset whose value depended on careful stewardship, and any association with insensitivity toward Japan was an existential risk for a company whose fortune was built there.

The deeper lesson of the duck campaign, and the reason it succeeded where nine years of conventional advertising had failed, lies in how insurance purchasing decisions actually work. Insurance is what economists call a "low-involvement category." People do not wake up excited to buy supplemental insurance. They do not browse insurance products for fun. The purchase decision is typically triggered by an external prompt: an enrollment period at work, a friend's health scare, or, crucially, simple brand recognition at the moment of decision. The duck did not explain Aflac's products. It did not make a rational case for supplemental coverage. What it did, brilliantly, was make the name unforgettable. And in a category where the purchase decision happens in a narrow window of attention, being unforgettable is everything. The duck turned Aflac from a company that needed to be explained into a company that was already familiar, and that familiarity collapsed the sales cycle in ways that no amount of rational advertising could have achieved.

VII. Japan Deregulation & Competition

The calendar turned to January 1, 2001, and with it came the moment that Aflac had been dreading and preparing for in equal measure. Japan's third-sector insurance market, the regulatory category that included cancer, nursing care, and medical treatment coverage, was formally opened to the country's large domestic insurers. The protections that had shielded Aflac for decades were gone.

The response from domestic competitors was swift and aggressive. Giant Japanese insurer Nippon Life moved immediately, racking up 180,000 cancer insurance policies in the first three months alone. The number of companies offering standalone cancer and medical insurance more than doubled in the years following deregulation.

After nearly three decades of operating in what amounted to a protected sanctuary, Aflac Japan suddenly found itself in a competitive market for the first time.

The conventional wisdom at the time was that Aflac's market share would erode rapidly. The domestic Japanese insurers were enormous, deeply embedded in the country's corporate relationships, and had distribution networks that dwarfed anything a foreign company could build. Tokio Marine, MetLife Alico, and a host of other competitors entered the supplemental insurance space with aggressive pricing and marketing. The question was not whether Aflac would lose share, but how much and how fast.

What actually happened surprised nearly everyone. Aflac's share of the cancer insurance market did decline from its peak, but the decline was far more gradual than predicted. By the mid-2000s, Aflac still controlled roughly fifty percent of the cancer insurance market, and it maintained its position as the largest individual insurance provider in all of Japan.

The first-mover advantage that had seemed fragile in theory proved remarkably durable in practice, for reasons that illuminate fundamental truths about how insurance markets actually work.

First, insurance is an intensely relationship-driven business, and Aflac had spent decades building relationships with Japanese corporations, government entities, and individual policyholders. Those relationships did not evaporate simply because new competitors appeared. Second, the Aflac brand in Japan carried a level of trust and recognition in the cancer insurance category that new entrants could not easily replicate. Aflac had insured one in four Japanese households. That kind of penetration creates network effects, as more people buy the product, more people know someone who has received a claim payment, which reinforces the brand's credibility.

Third, Aflac demonstrated genuine strategic adaptability. In 2003, the same year that deregulation was fully taking effect, the company introduced its own duck-based marketing campaign in Japan. The results mirrored what had happened in the United States: sales increased twelve percent that year, and the duck became a cultural phenomenon in Japan just as it had in America. "Today we insure one out of every four Japanese households and took the title from Nippon Life, which had held it for more than one hundred years," Dan Amos noted, referring to Aflac's position as the largest individual insurer in the country.

Aflac Japan also moved aggressively into digital distribution. It was among the first companies to take advantage of a 1996 law that allowed insurance companies to sell policies online and by mail, a channel that became increasingly important as Japan's consumer behavior shifted toward digital commerce.

This was not a trivial adaptation. Japanese insurance had traditionally been sold through face-to-face relationships, and the willingness to embrace direct channels reflected a company that understood the need to evolve even as it defended its traditional strengths. The digital channel also allowed Aflac to reach younger Japanese consumers who were less likely to respond to traditional agent-based selling.

The Japan Post partnership, which evolved over several years, became one of Aflac's most important strategic assets in the post-deregulation era.

An initial agreement in 2008 grew into a comprehensive distribution arrangement by 2013, when Japan Post expanded its sale of Aflac cancer insurance from 1,000 to all 20,000 postal outlets. Japan Post Insurance also entered into an agency contract to distribute Aflac's cancer products at its seventy-nine directly managed sales offices.

Then, in December 2018, Japan Post Holdings agreed to purchase approximately a seven percent strategic stake in Aflac Incorporated for roughly 2.4 billion dollars. Under the shareholder agreement, Japan Post had a ten percent ownership cap and standstill restrictions.

But the investment signaled something more important than the financial terms: one of Japan's most iconic institutions, a quasi-governmental entity with roots stretching back to the Meiji era, had decided to tie its future to Aflac's. For a foreign insurer in Japan, there is no stronger endorsement than being embraced by the postal system that touches every community in the country.

There is a broader insight here about the nature of competitive moats in insurance. Insurance, at its core, is a commodity. Any company can write a policy with the same terms and the same actuarial pricing. The product itself is undifferentiated. What creates durable competitive advantage is everything around the product: the distribution relationships that determine who gets to present the product to potential buyers, the brand trust that determines whether the buyer says yes, the claims-paying reputation that determines whether existing policyholders renew, and the operational infrastructure that determines whether the company can deliver on its promises profitably. Aflac's regulatory protection gave it the time to build all four of these advantages in Japan, and by the time competitors arrived, they found that catching up on decades of relationship-building and trust accumulation was far harder than simply launching a competing product.

The post-deregulation era demonstrated that Aflac's competitive advantage was not merely regulatory. The regulatory protection had been the catalyst, providing the time and space for the company to build genuine moats: brand trust, distribution depth, product expertise, and cultural integration. When the protection was removed, those moats held, not perfectly, but well enough to sustain a dominant and highly profitable market position for another quarter-century. Aflac Japan still controlled approximately seventy percent of the cancer insurance market as of 2025, a quarter-century after deregulation. That durability speaks to the quality of the moats that were built during the protected period.

VIII. Modern Era: Digital Transformation & Evolving Markets

In 2009, as the global financial crisis was reshaping the insurance industry, Aflac made a quiet acquisition that signaled its ambitions for the U.S. market. The company purchased Continental American Insurance Company for one hundred million dollars, gaining the ability to sell supplemental insurance on both individual and group platforms. This was more than a product expansion. It was an acknowledgment that the U.S. supplemental insurance market was evolving from a purely voluntary, individual-focused model to one where group benefits and employer-sponsored platforms were becoming the primary distribution channel.

The U.S. business, which had long lived in the shadow of Japan's outsized contribution to the bottom line, began receiving renewed strategic attention. The logic was straightforward: if Japan's demographic headwinds were going to constrain growth in the company's largest market over the long term, the U.S. business needed to become a more meaningful contributor.

In 2019, Aflac acquired Argus Dental and Vision, expanding its value proposition on employee benefits enrollment platforms. The following year, it purchased Zurich North America's U.S. Corporate Life and Pensions business, adding group life, disability, and absence management products for less than two hundred million dollars with annualized premium of approximately 120 million.

These acquisitions reflected a deliberate strategy to transform Aflac U.S. from a single-product supplemental insurer into a comprehensive voluntary benefits platform. The idea was to become a one-stop shop for employers seeking to offer a full suite of voluntary benefits, rather than a niche player that only provided cancer and accident coverage. This positioning would become increasingly important as the competitive landscape shifted toward platform-based benefits solutions where breadth of product offering is a key differentiator.

In Japan, the demographic picture presents both the company's greatest long-term challenge and, paradoxically, a near-term tailwind. Japan's population is declining and aging faster than anywhere else in the world. The country's median age has risen past forty-eight, and the birth rate continues to fall below replacement levels.

For an insurance company, this creates a fundamental tension. An aging population means more cancer diagnoses and more claims, which drives demand for the product. But a shrinking pool of younger, healthier policyholders means less premium income to offset those claims over time.

The actuarial math of insurance depends on having enough healthy people subsidizing the costs of sick people, and Japan's demographic trajectory threatens that balance. It is like a swimming pool that is slowly draining from one end while water pours in from the other. Right now the pool is still full, but the physics are working against it.

Dan Amos has addressed this challenge directly. "We have continued to focus on third sector products as well as introducing these policies to new and younger customers," he said. In March 2025, Aflac Japan launched "Miraito," a new cancer insurance product that drove a 35.6 percent sales gain in cancer insurance for the full year. A companion product called "Anshin Palette" offered customizable medical coverage options designed to appeal to younger consumers who wanted flexibility rather than one-size-fits-all policies. These product innovations contributed to a sixteen percent increase in Japan sales for full year 2025, suggesting that the company's efforts to attract younger policyholders were gaining traction.

The digital transformation of Aflac has been characterized by what CIO Shelia Anderson described as a deliberately conservative approach. "We will never be first to market with new AI technology," she stated, a philosophy that contrasts sharply with the move-fast-and-break-things ethos of Silicon Valley.

This conservatism makes sense for a company whose brand is built on trust and whose primary asset is a portfolio of long-duration promises to policyholders. An insurance company that processes a claim incorrectly because of an AI error is not just losing money. It is breaking a promise to someone who is potentially fighting for their life. The stakes of getting technology wrong in insurance are fundamentally different from the stakes in most consumer technology applications.

Aflac's digital initiatives have therefore focused on practical, proven applications: machine learning for claims processing automation, AI copilots for customer service, and partnerships with Amazon Web Services and Salesforce for infrastructure. In Japan, the company built a digital contact center combining AI avatars with human agents, the first of its kind in Japanese insurance. The approach is incremental rather than revolutionary, but it reflects a company that understands the unique risks of its business.

The company's most significant recent technology initiative was its integration with Workday Wellness in January 2026, embedding Aflac's supplemental health products into Workday's AI-driven benefits platform. This kind of platform integration represents the modern evolution of Aflac's original worksite distribution model. Instead of agents walking into offices to make group presentations, the company is embedding its products directly into the software that employers already use to manage benefits enrollment, reducing friction and reaching employees at the moment they are making benefits decisions.

Revenue from Japan accounted for seventy-seven percent of Aflac's total revenue in 2012, a concentration that the company has been working to rebalance. By 2025, Japan contributed approximately fifty-five percent of adjusted revenue, still a dominant share but one that reflects the growing importance of the U.S. business. Full year 2024 revenue reached 18.93 billion dollars with net income of 5.44 billion. Full year 2025 showed total revenue of 17.16 billion with adjusted earnings per share of 7.49, a 3.9 percent increase over the prior year on an adjusted basis despite GAAP volatility driven by investment gains and losses.

A note on the gap between GAAP and adjusted earnings, which has been a recurring topic among analysts: insurance companies hold large investment portfolios, and under current accounting standards, unrealized gains and losses on those portfolios flow through the income statement. In 2024, GAAP net income was 5.44 billion dollars. In 2025, it dropped to 3.65 billion, a thirty-three percent decline that sounds alarming until you understand that the underlying insurance operations, the premiums collected, the claims paid, the policies sold, were essentially stable. Adjusted earnings, which strip out the investment portfolio noise, rose modestly. For an investor evaluating Aflac, the adjusted figures are far more informative about the health of the franchise than the GAAP numbers, which can swing wildly based on interest rates and bond prices that have nothing to do with how many policies the company is selling or how well it is managing claims.

The share buyback program has been a particularly important component of the capital return story. In 2025, Aflac deployed 3.5 billion dollars to repurchase shares, steadily reducing the share count and amplifying per-share earnings growth even during periods of flat or declining revenue. Combined with dividends, total shareholder returns exceeded 4.8 billion for the year. The dividend has been increased for forty-two consecutive years, a streak that qualifies the company as a Dividend Aristocrat and signals management's confidence in the durability of the underlying cash flows.

The leadership structure evolved to reflect the company's maturation. In October 2024, Virgil R. Miller was promoted to President of Aflac Incorporated, a move widely interpreted as succession positioning. Miller, a former U.S. Marine who started his Aflac career in the company's call center in 2004, now oversees approximately 116 billion dollars in assets, thirty-seven million customer policies, thirteen thousand employees, and 150,000 sales agents. Dan Amos, who turned seventy-four, remains Chairman and CEO with more than thirty-five years in the role, making him the longest-serving CEO in the Fortune 250 following Warren Buffett's retirement from Berkshire Hathaway.

One major challenge emerged in June 2025 when Aflac identified a cybersecurity breach that ultimately affected 22.65 million individuals, making it the largest confirmed healthcare data breach of the year. The threat actor, believed to be affiliated with the Scattered Spider cyber-criminal organization, accessed names, dates of birth, Social Security numbers, and medical information before being stopped within hours.

Aflac completed its investigation by December 2025 and offered twenty-four months of credit monitoring and identity protection to affected individuals. The incident underscored the operational risks inherent in managing vast databases of sensitive personal and medical information. For a company whose brand is built on the promise of being there during a crisis, experiencing its own crisis of data security created an uncomfortable irony. The long-term impact on customer trust and potential litigation costs remains a monitoring point for investors.

IX. Playbook: Business & Investing Lessons

The Aflac story contains a remarkably concentrated set of strategic lessons that apply far beyond the insurance industry.

Finding and dominating a niche. The most fundamental lesson is the power of identifying a product category that established competitors dismiss as too small, too weird, or too risky, and then owning it completely before anyone realizes it matters. When John Amos created cancer insurance, the product was considered morbid and unmarketable by mainstream insurers. That disdain was Aflac's greatest gift, providing years of uncontested market development in the United States and, even more dramatically, in Japan. The lesson is not simply "find a niche." It is "find a niche that incumbents are embarrassed to pursue, because their embarrassment is your moat."

The power of regulatory arbitrage. Aflac's Japan story is perhaps the clearest example in modern business history of how regulatory frameworks can create durable competitive advantages. Japanese policymakers handed Aflac a protected monopoly in cancer insurance because they genuinely believed the category was insignificant. When they realized their mistake, trade agreements between the U.S. and Japan prevented them from correcting it for another two decades. Aflac did not create these regulatory dynamics, but it recognized them, positioned itself to benefit from them, and used the protected period to build genuine competitive moats that survived deregulation. For investors, the lesson is that regulatory advantages are powerful but temporary. The question is whether the company uses the protected period to build something lasting or simply extracts rents until the protection expires.

Distribution as strategic advantage. Aflac's two most important distribution innovations, worksite payroll deduction in the U.S. and retired-worker agents in Japan, both reduced friction in the buying process while simultaneously building structural advantages that competitors could not easily replicate. The payroll deduction model created automatic recurring revenue with minimal churn. The retired-worker agent model in Japan leveraged existing social trust networks that no foreign competitor could build from scratch. In both cases, the distribution model was not just a channel. It was a competitive moat.

Marketing as a force multiplier. The duck campaign demonstrated that in a commodity market, brand recognition can be a decisive competitive advantage. Insurance products are difficult to differentiate on features or price. But a consumer who recognizes your name and associates it with a positive emotional response is dramatically more likely to enroll when your agent shows up at their workplace. The jump from twelve percent to over ninety percent brand recognition did not just increase sales. It fundamentally changed the economics of Aflac's U.S. business by reducing the cost of every customer acquisition.

Geographic concentration as a double-edged sword. Aflac's heavy dependence on Japan, which has contributed more than half of the company's earnings for decades, has been both its greatest strength and its most significant structural risk. The strength is obvious: Japan is the world's third-largest economy with a culture that deeply values insurance protection. The risk is equally clear: currency fluctuations, demographic decline, and regulatory changes in a single country can have outsized impacts on the entire company. This tension has no clean resolution. It is simply a feature of Aflac's business that investors must accept and price accordingly.

Family business succession. Three generations of Amos family leadership have provided Aflac with a continuity of vision and culture that is rare in public companies. John Amos founded the company and identified the cancer insurance niche. His brother Paul served as chairman. Dan Amos, Paul's son, has led the company as CEO for thirty-five years, an extraordinary tenure that has provided strategic consistency through multiple business cycles, competitive disruptions, and market crises.

The challenge now is whether the company can maintain its distinctive culture and strategic clarity as it transitions to professional management for the first time in its history. John Amos died of cancer in 1990, the same disease that had inspired him to create the company's signature product. The poignancy of that fact speaks to the deeply personal connection between the founding family and the business they built.

Cultural adaptation as competitive advantage. Perhaps the most underappreciated lesson from Aflac's story is the company's ability to operate effectively in two radically different cultures simultaneously. The U.S. business relies on humor, brand recognition, and a screaming duck mascot. The Japan business was built on quiet relationship-building, cultural sensitivity, and a willingness to employ local talent in leadership positions. Few companies have demonstrated this kind of bicultural fluency, and it remains one of Aflac's least replicable competitive advantages.

X. Analysis: Bear vs. Bull Case

The Bull Case

Aflac's bull case rests on several structural pillars that, taken together, make it one of the most defensible franchises in the global insurance industry.

First, the company's position in Japan's aging society is paradoxically strengthened by the very demographic trends that threaten the broader market. An aging population means more cancer diagnoses, more demand for supplemental coverage, and a deepening cultural awareness of the need for financial protection against medical events.

Aflac still controls approximately seventy percent of Japan's cancer insurance market, a position reinforced by decades of brand trust, the Japan Post distribution partnership, and a product innovation pipeline that has shown recent vitality with the Miraito launch driving double-digit sales growth.

Second, the brand moat in both markets is extraordinary. Above ninety percent name recognition in the United States and dominant awareness in Japan create a level of consumer trust that new entrants cannot replicate through advertising spending alone. In insurance, trust is the product. When a consumer must choose between an unfamiliar insurer offering a slightly lower premium and a company whose name they have known for decades, the established brand wins the vast majority of the time.

Third, the distribution architecture is deeply embedded and difficult to displace. In the U.S., Aflac's products are woven into the benefits platforms of hundreds of thousands of employers, with payroll deduction creating automatic renewal dynamics. In Japan, the Japan Post network of 20,000 outlets and the Dai-ichi partnership provide reach that no competitor can easily match. The January 2026 Workday Wellness integration represents the next evolution of this embedded distribution strategy.

Fourth, the capital return program is among the most generous in the insurance industry. Aflac returned approximately 4.8 billion dollars to shareholders through dividends and buybacks in 2025. The company has increased its dividend for forty-two consecutive years, qualifying as a Dividend Aristocrat, and the buyback program has steadily reduced the share count, amplifying per-share earnings growth even during periods of flat revenue.

Through the lens of Hamilton Helmer's Seven Powers framework, Aflac possesses several durable advantages.

Its brand power is evident in the ninety-plus percent recognition that functions as a demand-side scale economy. The more people who recognize the Aflac name, the easier and cheaper it is to sell to the next customer.

Its switching costs are embedded in the payroll deduction model that makes cancellation require active effort from policyholders. Inertia is a powerful force in consumer financial products, and Aflac's distribution model harnesses it systematically.

Its counter-positioning in Japan, where the company offered a product that incumbents were culturally unwilling to sell, created a decades-long advantage that competitors could not attack without contradicting their own market positioning. By the time domestic insurers were willing to enter the cancer insurance market, Aflac had already built an insurmountable lead.

And the Japan Post partnership functions as a form of cornered resource, providing exclusive access to a distribution network of twenty thousand postal outlets that no other foreign insurer can replicate. This is the insurance equivalent of having exclusive shelf space in every grocery store in the country.

The Bear Case

The most formidable bear argument centers on Japan's demographic trajectory. Japan's population peaked in 2008 and has been declining since, with projections suggesting a drop from 125 million to below 100 million by 2050. The working-age population is shrinking even faster.

For an insurance company whose business model depends on a growing pool of premium-paying policyholders, this is a structural headwind that no amount of product innovation can fully offset. The company's recent success in attracting younger Japanese customers is encouraging but insufficient to reverse the macro trend. Every year, there are simply fewer potential policyholders in Japan, and no marketing campaign or product launch can create people who do not exist.

Concentration risk compounds the demographic concern. Despite efforts to grow the U.S. business, Japan still represents more than half of adjusted revenue and more than three-quarters of total assets. This concentration creates exposure to yen fluctuations, Japanese regulatory changes, and economic cycles in a single country.

The yen's weakness against the dollar in recent years has been a persistent drag on reported results, with the average yen-dollar rate weakening to 154.20 in the fourth quarter of 2025. To illustrate the currency impact: when Aflac Japan earns one hundred yen in profit, that profit is worth fewer dollars today than it was a decade ago. The underlying Japanese business can be performing well while the reported dollar earnings decline simply because of exchange rate movements. This creates a confusing signal for investors who focus on headline numbers.

The competitive landscape is intensifying on both fronts. In the U.S., the supplemental benefits market has become what analysts describe as a "crowded and contested battlefield." MetLife has invested billions in digital-first benefits platforms. Unum's Total Leave Management platform creates employer stickiness that Aflac does not fully replicate. Colonial Life, a Unum subsidiary, positions itself as the "personal" alternative to the duck, marketing the human advisor rather than a mascot, and directly attacks Aflac's small-business roots.

In Japan, every major domestic insurer now competes in cancer and medical insurance, and their distribution advantages within the traditional corporate relationship networks, the deep ties between Japanese banks, insurers, and industrial conglomerates that define the country's business landscape, are formidable.

Through Porter's Five Forces lens, the industry dynamics present a mixed picture.

Buyer power is moderate to high because employers, Aflac's primary distribution channel, can switch supplemental insurance providers during annual enrollment periods. An employer with ten thousand workers who is unhappy with Aflac's service can move the entire account to a competitor with relatively low switching costs.

Supplier power is low, as insurance is fundamentally a financial product with no physical supply chain. Aflac's "raw materials" are capital and actuarial talent, both of which are widely available.

Threat of substitutes is real and growing: health savings accounts, critical illness riders on primary health policies, and government health insurance expansions all compete with standalone supplemental coverage for the consumer's healthcare dollar. If primary health insurance becomes more comprehensive, the gap that supplemental insurance fills could shrink.

Threat of new entrants is moderate, limited by regulatory barriers and the capital requirements of insurance, but insurtech companies are testing digital-first models that could eventually disrupt traditional distribution.

Competitive rivalry is high and intensifying in both markets.

The June 2025 data breach, affecting 22.65 million individuals, introduces a wild card. The direct financial costs are manageable for a company of Aflac's size, but the reputational impact in an industry built on trust, particularly for a company that holds the most sensitive category of personal data, medical records, is harder to quantify. The long-term effect on policyholder retention and new customer acquisition will take several years to fully assess. This is worth watching closely because Aflac's entire value proposition, in both markets, is built on the promise of being there when things go wrong. A breach that exposes the personal medical information of twenty-two million people tests that promise in a way that no competitive or demographic challenge can.

The Myth vs. Reality Check

There are two consensus narratives about Aflac that deserve scrutiny. The first is that Aflac is "just" a Japan story, entirely dependent on a single foreign market for its prosperity. The reality is more nuanced. While Japan remains the dominant contributor to earnings, the U.S. business has been growing steadily and the company's acquisitions of Continental American, Argus, and Zurich's group benefits business have materially diversified the domestic product portfolio. The U.S. generated nearly 1.6 billion dollars in new sales in 2025, and group products now represent twenty percent of new sales. The rebalancing is real, even if Japan will likely remain the larger contributor for years to come.

The second narrative is that Aflac's best days are behind it, that the combination of Japan's demographic decline and market deregulation will inevitably erode the franchise. The counterpoint is that Aflac has been hearing this prediction for twenty-five years, since deregulation in 2001, and has managed to maintain a dominant market position, grow adjusted earnings, and return massive amounts of capital to shareholders throughout. The company's adjusted earnings per share grew 3.9 percent in 2025 despite revenue headwinds. The Miraito product drove a 35.6 percent increase in cancer insurance sales. The bull case is not that these headwinds are imaginary, but that Aflac has demonstrated the ability to manage them effectively over extended periods.

Key Performance Indicators

For investors tracking Aflac's ongoing performance, two metrics matter most. First, premium persistency rates, which measure the percentage of policies that renew from year to year. Think of persistency as the insurance equivalent of a SaaS company's net revenue retention: it tells you whether the existing book of business is stable, growing, or leaking. In Japan, persistency was 93.4 percent in the most recent quarter, an exceptional number that reflects deep policyholder satisfaction and the structural stickiness of the product. In the U.S., it was 79.2 percent, lower but consistent with industry norms for voluntary benefits. A decline in either metric by more than a percentage point or two would signal genuine franchise deterioration and should prompt serious scrutiny.

Second, new annualized premium sales growth in both markets, which indicates whether Aflac is successfully attracting new policyholders to offset natural attrition and Japan's demographic decline. This metric is the leading indicator of future revenue growth. The sixteen percent growth in Japan sales for 2025, driven by the Miraito product launch, is a strong data point, but sustainability across multiple years, particularly as the new-product tailwind fades, is what matters. In the U.S., the trajectory of group product sales as a percentage of total new sales indicates whether the strategic pivot toward comprehensive voluntary benefits is gaining traction.

XI. Epilogue

Dan Amos sits in his office in Columbus, Georgia, the same city his uncle John chose seventy-one years ago for its friendly regulatory climate and lack of competition. He has been CEO for thirty-five years, a tenure that has seen the company grow from 2.7 billion dollars in revenue to nearly nineteen billion. The total return to shareholders under his leadership has exceeded 21,500 percent, compared with roughly 4,200 percent for the S&P 500 over the same period. The company he inherited from his uncle has been named one of the world's most ethical companies for nineteen consecutive years, the only insurer to appear every year since the award's inception.

The strategic priorities for the next decade are clear, even if the execution path is not. The U.S. business must continue its evolution from a single-product supplemental insurer to a comprehensive voluntary benefits platform, competing against diversified giants with far larger product portfolios.

The Japan business must find ways to grow in a shrinking population, whether through product innovation like Miraito, digital distribution that reaches younger consumers, or expansion into adjacent product categories. The company's conservative approach to artificial intelligence, preferring to validate business impact before deployment, reflects the same institutional patience that has characterized Aflac since the founding, but the pace of technological change in insurance may eventually require more aggressive adoption.

There is also the question of ESG and social impact, an area where Aflac has historically been a leader. The company has been named one of the World's Most Ethical Companies by the Ethisphere Institute for nineteen consecutive years, the only insurance company to appear every year since the award's inception in 2007. That recognition reflects a genuine corporate culture rooted in the founding family's values, but maintaining it through a leadership transition and amid growing scrutiny of corporate ESG claims will require continued vigilance.

The question of geographic expansion beyond the U.S. and Japan is one that Aflac has considered and, so far, declined to pursue aggressively. Other Asian markets, particularly those with aging populations and underdeveloped supplemental insurance sectors, represent theoretical opportunities. South Korea, Taiwan, and parts of Southeast Asia share some of the demographic and cultural characteristics that made Japan such fertile ground for supplemental health insurance. But the company's experience in Japan demonstrated that success in a foreign market requires decades of patient relationship-building, deep cultural adaptation, and a willingness to invest through long periods with uncertain returns. The Japan success was not a playbook that could be replicated quickly in new markets. It was the product of a unique confluence of regulatory conditions, cultural dynamics, and patient capital that may not be reproducible. Whether the next generation of Aflac leadership has the appetite for that kind of commitment remains to be seen.

The question of what constitutes the next "duck moment," the equivalent marketing or strategic innovation that could unlock the next phase of growth, is harder to answer. The duck worked because it solved a specific problem: brand anonymity in a low-involvement product category. The next breakthrough may look entirely different. It might come from embedding Aflac's products so deeply into employer benefits platforms that enrollment becomes automatic rather than opt-in. It might come from using AI to personalize coverage recommendations based on individual health profiles. It might come from a product innovation that addresses a fear as primal and universal as cancer was in 1958, perhaps cybersecurity insurance for individuals, or long-term care coverage redesigned for a generation that expects digital-first experiences. Whatever form it takes, Aflac's history suggests that the company's next great leap forward will come from the same source as every previous one: the willingness to see an opportunity that others dismiss.

The succession question looms over everything. Virgil Miller's promotion to President in January 2025 was the clearest signal yet that Aflac is preparing for life after Dan Amos. Miller's background, from Marine to call center employee to president of a 116-billion-dollar enterprise, is a quintessentially American rise that mirrors the company's own improbable trajectory. Whether he or another executive ultimately succeeds Amos, the transition will mark the end of an era. For the first time in its history, Aflac will be led by someone who is not a member of the founding family.

In the end, the Aflac story is about the power of seeing what others refuse to see. John Amos saw a product in cancer insurance that the industry considered too distasteful to sell. He saw a market in Japan that everyone else considered too closed to enter. Dan Amos saw a marketing opportunity in a duck that his own team considered too ridiculous to approve.

At every turning point, the company's greatest asset was not its actuarial models or its distribution networks or even its regulatory advantages. It was the willingness to pursue opportunities that looked absurd to everyone else, and the patience to let those opportunities compound over decades into something extraordinary.

Seventy-one years after three brothers drove into Columbus, Georgia, with a quarter-million dollars and a dream, the company they built protects fifty million people on two continents, manages over a hundred billion dollars in assets, and employs a duck that may be the most effective salesperson in the history of financial services.

XII. Recent News

Aflac's fourth quarter and full year 2025 results, reported in February 2026, showed the continued tension between GAAP volatility and operational stability that has characterized the company's recent financial reporting.

Full year revenue came in at 17.16 billion dollars, down 9.3 percent from the prior year's 18.93 billion, while net income declined to 3.65 billion from 5.44 billion. On the surface, these numbers look concerning. But the decline was driven almost entirely by investment portfolio fluctuations rather than deterioration in the core insurance business.

Adjusted earnings per share, which strip out the investment noise, rose 3.9 percent to 7.49 dollars, reflecting the steady underlying performance of the insurance operations. The company deployed 800 million dollars to repurchase 7.2 million shares in the fourth quarter alone and returned a combined 4.8 billion to shareholders for the full year through dividends and buybacks.

In Japan, the Miraito cancer insurance product continued to drive momentum with a 35.6 percent full-year sales gain in cancer insurance. The yen remained a headwind, averaging 154.20 to the dollar in the fourth quarter. In the U.S., new sales approached 1.6 billion dollars with group products accounting for twenty percent of the total, reflecting the strategic shift toward comprehensive voluntary benefits.

On the leadership front, Dan Amos officially became the longest-serving CEO in the Fortune 250 following Warren Buffett's departure from Berkshire Hathaway. The company announced a 5.2 percent increase in its first quarter 2026 dividend to 0.61 dollars per share, extending its streak of consecutive annual dividend increases to forty-two years.