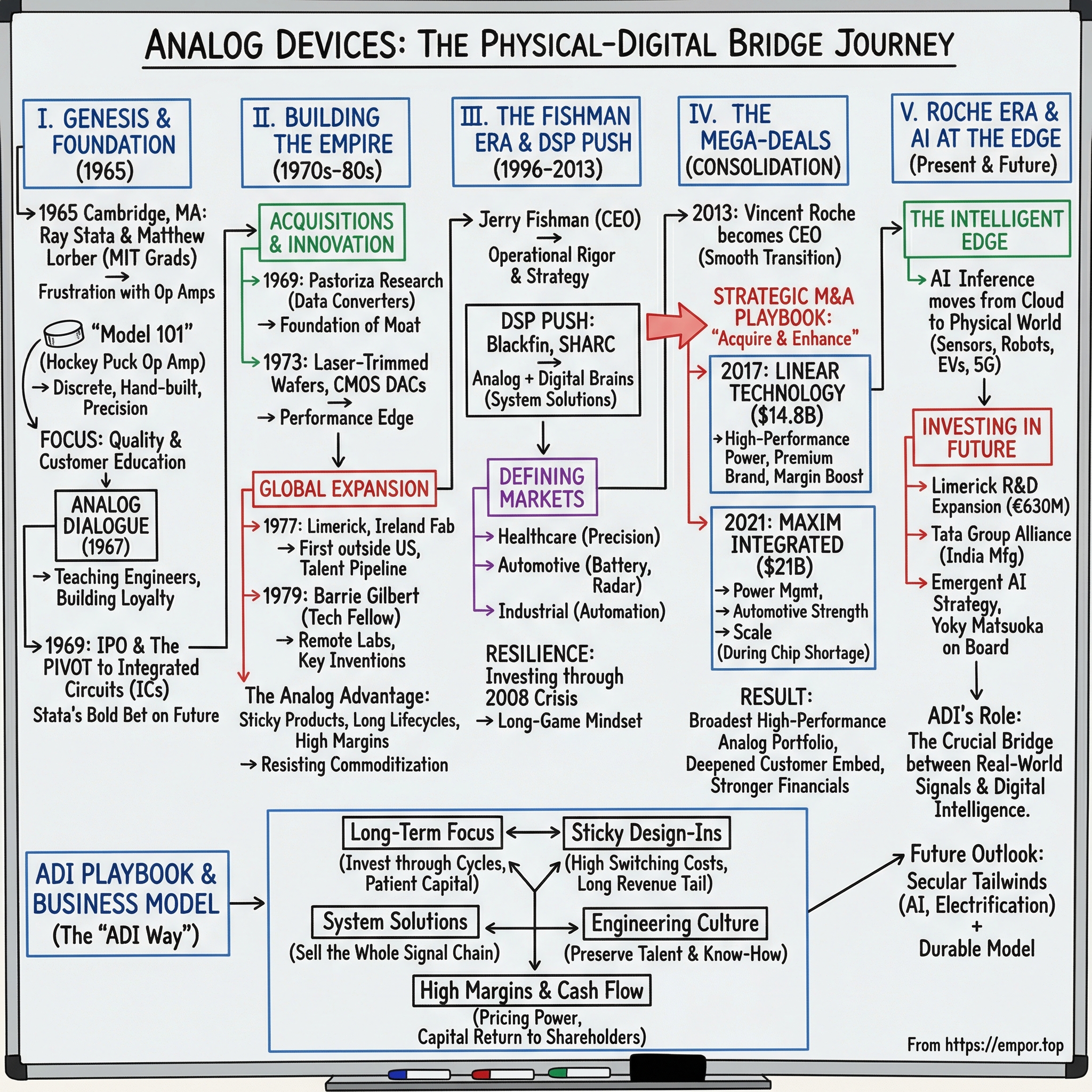

Analog Devices: The Semiconductor Pioneer That Bridges the Physical and Digital Worlds

I. Introduction

In the age of artificial intelligence, autonomous vehicles, and 5G, the world tends to obsess over the digital: faster processors, bigger data centers, more powerful GPUs. But there’s a reality underneath all of it that rarely gets top billing. Every bit of “digital” information starts life as something analog. Temperature. Pressure. Sound. Light. Motion. The physical universe speaks in continuous signals, not ones and zeros. And for nearly sixty years, one company has built a franchise on translating between those two worlds.

Analog Devices, headquartered in Wilmington, Massachusetts, is one of the semiconductor industry’s quiet giants. In fiscal 2024, it generated $9.33 billion in revenue and served more than 100,000 customers. ADI’s chips don’t usually end up in flashy consumer gadgets or viral products. They live deeper in the stack: inside factory automation systems, inside electric vehicle battery management, inside MRI machines, inside 5G base stations, and inside the infrastructure that makes modern computing useful in the real world. Without this class of technology, the digital revolution wouldn’t just slow down. It would be deaf, blind, and numb.

The question at the heart of this story sounds simple: how did two MIT graduates—starting with a hockey-puck-sized amplifier module in 1965—build one of the most enduring franchises in all of semiconductors? The answer is a mix of relentless focus on the hardest, least glamorous problems in chip design; a culture that kept investing through downturns; and a disciplined acquisition playbook that eventually pulled two of the industry’s most respected names into the fold.

ADI has lived through every semiconductor cycle since the Vietnam era, survived the dot-com crash, adapted through the mobile boom, and now sits at a new inflection point: intelligence moving out of the cloud and into the physical world, at the edge. This is the story of how analog—supposedly yesterday’s technology—became some of the most valuable real estate in the digital age.

II. The MIT Genesis Story

Cambridge, Massachusetts, 1965. The Vietnam War was escalating, the Great Society was ramping up, and across the Charles River from Harvard, two MIT electrical engineering graduates were about to start a company that would outlast almost every tech venture of their era.

Ray Stata and Matthew Lorber weren’t first-time founders. Along with a third MIT classmate, Bill Linko, they’d already built Solid State Instruments, a company that made instruments and controls—and eventually sold it to Kollmorgen Corporation. But while running that business, Stata and Lorber kept running into the same irritation: the modular operational amplifiers they had to buy from suppliers were expensive and disappointing. They were convinced they could do better. So they did the most MIT thing imaginable: they turned that frustration into a new company.

Their first product was the Model 101, a general-purpose operational amplifier. If you don’t live and breathe electronics, an op amp is one of the most important “primitive” parts in the analog world—a versatile building block that lets engineers amplify, filter, and condition real-world signals. The Model 101 was about the size of a hockey puck and built from discrete transistors, resistors, and capacitors. Integrated circuits were still early in their life, and there were no linear ICs available. In other words: every op amp was effectively hand-built, and performance came down to component precision and design skill.

The market couldn’t have been better. Scientific instruments and test equipment were booming, fueled by Cold War defense spending and the space race. Engineers needed accurate analog electronics to measure and control everything from missile telemetry to reactor systems. ADI didn’t have to invent demand. It just had to deliver performance.

Still, plenty of small analog companies were cropping up around Boston. What made Analog Devices different wasn’t just what it sold—it was how Stata thought about selling it. He fixated on two things: technical quality and customer education. In 1967, only two years in, ADI launched Analog Dialogue, a technical journal that became one of the longest-running publications in the electronics industry. It wasn’t glossy marketing copy. It was practical engineering teaching—how to design better circuits, how to think about real-world signal problems, how to get results. And it worked. Engineers who learned analog the “ADI way” tended to keep choosing ADI parts when it came time to design.

The growth came fast. By 1968, ADI had reached $5.7 million in sales. In 1969, it went public, securing access to capital at a moment when semiconductors were still young enough for a focused specialist to stand out on Wall Street.

But 1969 brought something else—something more dangerous. That was the year the first integrated-circuit op amps hit the market. They weren’t great at first. They couldn’t match the performance of ADI’s hand-assembled modules. But they were dramatically cheaper, and they were improving quickly. Stata saw what this really was: not competition, but a clock.

If ADI stayed a boutique module maker, it would eventually lose.

So Stata pushed to move into semiconductors. And when his board refused to approve the investment—too risky—he didn’t drop it. He personally funded a semiconductor startup and structured it so Analog Devices could buy it later. He took the risk onto his own balance sheet when the company wouldn’t. Within two years, the board relented and acquired the venture. Within eight years, integrated circuits made up more than half of ADI’s revenue.

That move—betting on the transition from discrete modules to ICs, and using personal capital to force the option open—captures who Ray Stata was. Not just an engineer-founder, but a strategist with the nerve to act early. He would go on to serve as CEO from 1973 to 1996 and as chairman from 1973 until 2022—nearly half a century at the center of the company.

Between the IPO and the semiconductor pivot, ADI had its two essential ingredients for endurance: capital to keep investing, and a technology platform that could scale. It wasn’t just making excellent modules anymore. It was becoming a semiconductor company—and choosing, deliberately, the highest-performance corner of analog, the part that’s hardest to replicate and least likely to become a commodity. That focus would define everything that came next.

III. Building the Analog Empire

The 1970s and 1980s were when Analog Devices stopped looking like a promising Boston-area upstart and started looking like a franchise. Not because it stumbled into a hot market, but because it kept making a series of deliberate bets: buy the right capabilities early, push manufacturing further than competitors thought necessary, and expand internationally before “global” became table stakes.

One of the earliest moves set the tone. In 1969, ADI acquired Pastoriza Research, a specialist in integrated circuits that converted analog signals to digital and back again. Data converters—the translators between the continuous real world and the discrete language of computers—became ADI’s signature category and, over time, the foundation of its moat. Decades later, ADI still held a leading position in converters, an unusually long reign in semiconductors.

Converters have stayed defensible for a simple reason: they’re closer to physics than fashion. High-precision conversion demands mastery across semiconductor process technology, circuit design, and system-level realities like noise, power, and signal integrity. At higher resolutions, the chip has to reliably distinguish between an enormous number of tiny voltage steps. Doing that at speed, with low power, at a manufacturable cost, is brutally hard—and it doesn’t get easier just because the industry can pack in more transistors. That’s why converters never followed the same commoditization curve as many digital chips.

In 1973, ADI doubled down on that performance edge. It became the first company to introduce laser-trimmed wafers and the first CMOS digital-to-analog converter. Laser trimming mattered because it let ADI calibrate circuits directly on the wafer, correcting for inevitable manufacturing variations that would otherwise drag down accuracy. This wasn’t a lab trick; it translated into better specs and better yields. In a business where performance is the product, that combination is exactly how you separate from the pack.

Then came a geographic bet that looked unconventional at the time but aged extremely well. In 1977, ADI opened its first manufacturing plant outside the United States—in Limerick, Ireland. It wasn’t merely an overseas outpost. It was the first semiconductor fabrication facility in the entire country. ADI was drawn by Irish government incentives, a well-educated talent pipeline from the University of Limerick, and the strategic logic of being closer to European customers. Over time, Limerick became one of ADI’s most important sites—and ADI’s presence helped Ireland’s broader emergence as a major technology hub.

In 1979, ADI made another move that signaled what kind of company it wanted to be: it named Barrie Gilbert its first Technology Fellow. Gilbert was already a legend—a self-taught English circuit designer who had invented the Gilbert cell mixer at Tektronix in the 1960s. The Gilbert cell became a foundational circuit for frequency translation, and variations of it show up throughout modern wireless communications. ADI attracted him by letting him build the company’s first remote design center in Oregon, which evolved into the Northwest Labs. That kind of arrangement wasn’t common then, but it secured ADI one of the most productive analog minds in the industry. Gilbert went on to earn more than 100 patents, became a Life Fellow of the IEEE, and stayed with ADI until his death in 2020.

By 1982, the results were hard to ignore: $156 million in annual sales, more than 200 products, and 15,000 customers. Ray Stata went on record predicting the company would reach $1 billion in revenue within eight years. The timing proved a bit optimistic, but the direction wasn’t. ADI had momentum, and it had chosen categories where momentum compounds.

What made the analog business model so attractive—especially ADI’s corner of it—was how stubbornly it resisted commoditization. In digital semiconductors, Moore’s Law turns today’s breakthrough into tomorrow’s bargain-bin part. But analog didn’t behave that way. These designs could stay relevant for decades, and customers didn’t swap them casually. Once a converter or amplifier is designed into a system, replacing it can mean months of requalification and debugging, with real risk of noise, offset, or linearity problems surfacing only after the system is built. That friction creates switching costs, and switching costs create pricing power.

The payoff was a business that could sustain unusually strong gross margins—often in the mid-sixties to low-seventies percent range—even as the broader semiconductor industry swung through punishing cycles. ADI had found a sweet spot that’s rare in tech: products that were genuinely hard to build, and customers who had every reason to keep buying once they’d committed. That formula would carry the company through the next few decades—and set the stage for the even bigger bets to come.

IV. The Fishman Era and the Digital Signal Processing Push

On March 28, 2013, Jerald “Jerry” Fishman, Analog Devices’ CEO, died suddenly of a heart attack. He was sixty-seven. He’d led the company for seventeen years, and the news hit the semiconductor world with the kind of force you usually reserve for founders, not executives. Fishman wasn’t just the person at the top; he was one of the people who had built ADI into what it was.

His path to that job was classic New York grit. He came up through the city’s public schools—Bronx High School of Science, then City College of New York for engineering. He joined ADI in 1971 in product marketing and kept stacking credentials while working full time: a master’s in engineering from Northeastern, an MBA from Boston University, and a law degree from Suffolk. It wasn’t academic collecting. It reflected how he operated—comfortable in engineering detail, business tradeoffs, and the messy realities of contracts, customers, and competition.

By the time he became president and COO in 1991 and then CEO in 1996, Fishman had already spent a quarter-century inside the company. He knew ADI end to end: the products, the manufacturing realities, the sales channels, the way engineers think, and the way customers buy.

Fishman’s style was unmistakable. Direct. Sometimes blunt. Often funny. Not remotely precious. He earned plenty of outside recognition—Electronic Business magazine named him CEO of the Year in 2004, and Brown University awarded him an honorary doctorate in 2009—but the more telling reputation came from people who worked with him. He could cut through a complicated argument in minutes and land on the point that actually mattered. And even when disagreements got intense, the respect tended to remain.

Strategically, Fishman pushed ADI hard to widen its aperture beyond pure analog. The bet was digital signal processing: if the world was becoming software-defined and data-driven, the best analog signals in the world wouldn’t matter unless you could process them intelligently. ADI built out a full DSP lineup—Blackfin for low-power embedded uses, SHARC for audio and industrial processing, and TigerSHARC for high-performance military and telecom. The rationale was simple and forward-looking: as systems got more complex, customers didn’t want a bag of parts. They wanted a solution, with the analog front end and the digital brains designed to work together.

ADI also went after MEMS—microelectromechanical systems—tiny sensors that measure things like acceleration, rotation, and pressure. ADI’s MEMS accelerometers landed in automotive airbag systems and consumer electronics. But over time, the business exposed an uncomfortable truth: consumer MEMS was a brutal, high-volume, low-margin fight, and that wasn’t where ADI historically won. In 2013, ADI sold its consumer MEMS business to InvenSense, a clear admission that not every adjacency, even a trendy one, deserved permanent capital.

While that was happening, Fishman helped deepen ADI’s position in the markets that would define its modern identity: healthcare, automotive, and industrial. In healthcare, ADI’s precision components showed up across devices—from blood glucose monitors to CT scanners. In automotive, ADI chips helped manage battery systems, radar sensors, and audio processing. In industrial automation, ADI’s converters and amplifiers sat inside the nervous system of process control, robotics, instrumentation, and factory equipment.

The moment that best captured Fishman’s long-game mindset came during the 2008 financial crisis. As demand fell and fear took over, many semiconductor companies protected near-term earnings by cutting R&D. Fishman didn’t. He kept investing, betting that the downturn would pass—but that the products designed during it could stay in customers’ systems for years. In analog, that’s not optimism. That’s strategy.

Over his tenure, ADI’s revenue more than doubled and its share price grew more than threefold. But the more durable legacy was cultural: Fishman brought discipline and operational rigor that complemented Ray Stata’s strategic instinct, creating a company that could innovate without losing its edge on execution.

When Fishman died, the baton passed to Vincent Roche, a quiet Irishman who had joined ADI in Limerick in 1988 and risen through the organization over twenty-five years. The transition was notably smooth—a sign of how much institutional strength Stata and Fishman had built, and a hint that ADI’s next era wouldn’t be about reinvention so much as compounding.

V. The Linear Technology Mega-Deal

In the summer of 2016, Analog Devices announced what would become the defining acquisition in modern analog semiconductors: it would buy Linear Technology for $14.8 billion.

To see why that was such a big swing, you have to understand what Linear represented. Founded in 1981 by Bob Swanson, a former National Semiconductor executive, Linear was a Silicon Valley legend—and one of the most admired businesses in all of chips. Swanson ran it from day one until he retired, and he built the company around a deceptively simple idea: make the best analog parts, charge accordingly, and never confuse “more volume” with “better business.”

It worked almost absurdly well. In the first half of the 2010s, Linear regularly posted gross margins north of 75%. In a sector where even excellent digital chip companies often lived in the mid-fifties, Linear looked less like a semiconductor manufacturer and more like a luxury brand. The engine behind those margins was familiar to anyone who understood ADI: high-performance analog is hard, the parts stay in systems for a long time, and once customers design them in, switching is painful. Linear just pushed that logic to its extreme, concentrating on the toughest applications in power management, data conversion, and signal conditioning.

The structure of the deal reflected both the price and the ambition. Linear was valued at roughly $60 per share. Shareholders would get $46 in cash plus 0.2321 shares of ADI for each Linear share. To fund it, ADI issued about 58 million new shares and took on $7.3 billion of new debt. Overnight, the balance sheet flipped: ADI went from roughly $7 per share of net cash to about $22 per share of net debt, with leverage around 3.8x. This wasn’t a tidy bolt-on. It was a bet-the-company move—one that would either create the category leader or leave a very expensive scar.

Strategically, the logic was straightforward. Together, ADI argued, the two companies could offer “the most comprehensive suite of high-performance analog offerings” in the industry. ADI brought leadership in data converters and amplifiers. Linear brought dominance in power management and precision signal conditioning. The portfolios fit together cleanly, and there was enough customer overlap to make cross-selling more than a PowerPoint promise.

The deal closed on March 10, 2017, after clearing regulators, with China’s MOFCOM as the final approval. Swanson joined ADI’s board. Much of the integration planning had been done before the closing, and the combined team moved quickly from paperwork to execution.

But culturally, this was never going to be plug-and-play. ADI was a Massachusetts company with an engineering culture shaped by MIT and decades of collaboration. Linear was Silicon Valley through and through: fiercely independent, intensely proud, and famously uncompromising about its products. Making the merger work meant threading a needle—preserving what made each organization exceptional while still removing enough duplication to justify the premium ADI was paying.

One of the most consequential early moves was decidedly unsexy: consolidating global distribution under Arrow Electronics. It streamlined a patchwork go-to-market setup, simplified logistics, and improved leverage across the supply chain—cost and complexity out, without breaking customer relationships.

The payoff showed up where it mattered. The combined company’s gross margins landed in the high-sixties to low-seventies—below Linear’s standalone peak, but meaningfully above what ADI had achieved on its own. More important than the accounting, though, was the strategic shift: with a broader portfolio, ADI could increasingly sell complete analog solutions instead of isolated components. That deepened customer relationships and made those already-sticky switching costs even stickier.

In hindsight, Linear didn’t just make ADI bigger. It clarified ADI’s modern M&A playbook: buy a best-in-class analog franchise with complementary products, protect its engineering DNA, integrate the back office and distribution, and use the expanded catalog to become more embedded in customers’ systems. And once that muscle was built, ADI was ready to use it again—on an even larger stage—just a few years later.

VI. The Maxim Integration Gambit

If the Linear Technology deal was audacious, the Maxim Integrated acquisition was a statement of intent. In July 2020—while the world was still lurching through the first year of COVID—Analog Devices announced it would acquire Maxim Integrated Products in an all-stock transaction valued at roughly $21 billion.

On paper, the timing looked almost reckless. The global economy was unstable. Supply chains were breaking in real time. And the semiconductor industry was heading into what became the worst chip shortage in memory. Yet ADI was stepping up to do its second mega-deal in four years—one that would create an analog heavyweight with trailing twelve-month revenue of more than $9 billion.

Maxim, founded in 1983 by Jack Gifford, had built its reputation on power management ICs, interface circuits, and voltage regulators. The fit was crisp. ADI led in data converters and amplifiers. Linear had brought world-class precision power. Maxim broadened the mixed-signal catalog and strengthened ADI where it wanted to lean in hardest, particularly in automotive and industrial.

The market-share math made the strategic message even clearer. Before the deal, ADI generated about $5.1 billion in analog revenue and Maxim about $1.9 billion. Together, that put the combined company at roughly 12.4% of the global analog market—still behind Texas Instruments at about 16.6%, but suddenly within striking distance.

ADI also structured the deal to avoid repeating the balance-sheet stress of Linear. Each Maxim share would be exchanged for 0.63 shares of ADI common stock. No new debt. That gave ADI more flexibility coming out of the leverage-heavy Linear transaction, and it turned Maxim shareholders into long-term partners in whatever the combined company became.

The transaction closed on August 26, 2021, after more than a year of regulatory review. Two Maxim leaders joined ADI’s board: Tunç Doluca, Maxim’s former president and CEO, and Mercedes Johnson, a longtime semiconductor finance executive who had previously served as CFO of Avago Technologies.

The combined scale was enormous: more than 10,000 engineers, 62 design centers, 23,000 employees, and roughly $1.5 billion in annual R&D spending. ADI projected $275 million in annual cost synergies within two years of closing and said the deal would be accretive to adjusted earnings within twelve months—six months earlier than it had initially expected.

But the real test wasn’t the synergy target. It was the moment. Integration landed right in the middle of the 2021–2022 chip shortage—one of the most chaotic periods the industry had seen in decades. ADI had to merge two large organizations while demand surged, manufacturing capacity tightened, and customers competed for limited supply. Management was juggling integration workstreams, customer allocation decisions, and investment in capacity expansion—all at once, with very little room for error.

Maxim’s contribution mattered most in power, and power was increasingly the center of gravity in automotive. As cars electrified and loaded up on advanced driver-assistance systems, the need for precision power management, battery monitoring, and sensor interfaces surged. Maxim’s portfolio didn’t just add revenue—it strengthened ADI’s position with major automakers by filling product gaps and deepening how embedded ADI could become inside a vehicle’s electrical architecture.

With Linear and Maxim now folded in, ADI had effectively consolidated a huge piece of the analog industry’s top tier. The company could offer a broader set of high-performance analog building blocks than anyone else: data conversion, amplification, power management, signal conditioning, and interface. The question was no longer whether ADI could go toe-to-toe with Texas Instruments. It was whether it could catch—and eventually pass—the category leader.

VII. The Vincent Roche Era and AI at the Edge

Vincent Roche’s path to the CEO office didn’t start in Silicon Valley or on Boston’s Route 128. It started in Limerick, Ireland, where he joined ADI in 1988 as a young engineer. Over the next twenty-five years, he climbed through the organization—field applications engineering, product line management, regional leadership—building the kind of institutional understanding you only get by living the business from the inside.

When Jerry Fishman died suddenly in 2013, Roche stepped in as interim CEO. The “interim” part didn’t last long. What followed was a decade of steady execution that pushed ADI from being seen as a best-in-class component supplier to something closer to a system-level partner.

The core of Roche’s strategy is what he calls the Intelligent Edge: the idea that as AI spreads, more of the most important computing will happen near where data is created, not in distant data centers. Picture a factory floor where sensors have to interpret signals instantly to control robotic arms. Or a vehicle where radar and lidar data needs to be processed in microseconds. Or a 5G base station where analog-to-digital conversion starts right at the antenna. In each case, the “edge” isn’t abstract—it’s physical. And ADI sits right at the handoff point between messy real-world signals and clean digital processing.

That positioning only got more valuable as the AI boom accelerated. The headlines have been dominated by GPUs training massive models in the cloud, but there’s an equally important shift happening underneath: inference, where trained models run on real-world data, increasingly happens at the edge. Edge AI puts a premium on precision, reliability, and power efficiency—exactly the dimensions where analog expertise matters, and where ADI has spent decades building an advantage.

Roche didn’t just articulate the vision; he funded it. In May 2023, ADI announced a €630 million investment to build a new R&D and manufacturing facility on its existing Limerick campus. The site, about 45,000 square feet, was expected to triple ADI’s European wafer production capacity and add 600 jobs to its roughly 1,500-person Ireland workforce. The move also lined up with the European Union’s push to strengthen local semiconductor manufacturing through Important Projects of Common European Interest.

Then, in September 2024, ADI announced a strategic alliance with the Tata Group to explore semiconductor manufacturing opportunities in India. The memorandum of understanding spanned three Tata companies: Tata Electronics, which is building India’s first semiconductor fab in Dholera, Gujarat, backed by an $11 billion investment; Tata Motors, focused on power electronics and energy storage for electric vehicles; and Tejas Networks, aimed at network infrastructure components. It was also a sign of the times: a deliberate effort to broaden ADI’s manufacturing and partnership footprint beyond the United States, Europe, and East Asia as geopolitics reshaped what “secure supply” means.

Financially, Roche’s era has been defined by resilience through the cycle. In fiscal 2024, the year ending November 2, 2024, revenue fell to $9.43 billion, down more than 23% from the prior year as the industry worked through a painful inventory correction. Customers who had over-ordered during the 2021–2022 shortage were burning down excess stock and pulling back on new orders. Even so, ADI kept operating margins above 40% and generated $3.1 billion in free cash flow. In a downturn of that magnitude, that level of profitability isn’t luck—it’s the payoff from sticky design-ins, pricing power, and a portfolio that’s hard to replace.

The following year brought a sharp rebound. Fiscal 2025, ending November 1, 2025, saw revenue climb to more than $11 billion, up 17% year over year, with double-digit growth across all end markets. Gross margins rose to 69.3%, operating margins reached 41.9%, and free cash flow hit a record $4.3 billion. The fourth quarter was particularly strong, with revenue of $3.08 billion, up 26% year over year, led by industrial and communications.

Through it all, ADI kept spending on what makes an analog company durable: innovation. In fiscal 2024, R&D totaled $1.97 billion, nearly 19% of revenue. Roche also emphasized AI-specific capabilities. CTO Alan Lee, who joined from AMD, led what ADI called its Emergent AI strategy, aimed at making sure ADI’s technology could meet the power and thermal realities of next-generation AI systems. And in January 2026, ADI added Dr. Yoky Matsuoka to its board—a MacArthur Genius Award recipient whose background spans Google X, Nest, and Panasonic—an appointment that underscored how seriously the company was taking AI and robotics as long-term drivers.

ADI’s own 2026 AI predictions, published by its technical leadership, sketched a future where analog computing re-emerges as an enabler of edge AI, humanoid robots rely on decentralized intelligence with neuromorphic sensors, and “micro-intelligences”—small, specialized models—run efficiently outside the cloud. Whether or not those exact predictions come true, the message is clear: ADI doesn’t see analog as a legacy category. It sees it as the infrastructure layer for what comes next.

VIII. Financial Performance and Business Model Analysis

Strip away the buzzwords and the hype cycles, and the financials tell a simple story: Analog Devices makes unusually good money selling unusually unglamorous chips. The products may be invisible to most people, but the economics are very visible once you look under the hood.

Start with where revenue comes from. In fiscal 2025, ADI generated about $11 billion in sales, spread across four end markets: Industrial at roughly 46% of revenue, Automotive at about 24%, Communications at around 17%, and Consumer at roughly 13%. That mix matters. Industrial and automotive together make up about 70% of the business, and those markets tend to reward long design cycles, high reliability, and “once you’re in, you’re in” supplier relationships. It’s a very different profile than chasing fast-turn consumer demand.

The customer base reinforces that stability. ADI sells to more than 100,000 customers, and no single customer dominates the revenue line. That’s a structural advantage in an industry where many digital-focused chip companies live and die by a handful of hyperscalers. A long tail of customers doesn’t just reduce concentration risk—it changes the power dynamic. ADI can’t be held hostage by any one buyer, and it can compound across thousands of smaller, sticky design-ins.

Then there’s pricing power, and gross margin is where it shows up. ADI’s fiscal 2025 gross margin of 69.3% reflects what the company has become post-Linear and post-Maxim: a consolidated portfolio of high-performance analog and mixed-signal products, many with long lifetimes and high switching costs. These aren’t “we have a good quarter” margins. They’re “the product is hard to replicate and the customer can’t easily move” margins.

Cash generation is where the model really starts to look exceptional. In fiscal 2025, ADI produced $4.8 billion in operating cash flow and $4.3 billion in free cash flow—about a 39% free cash flow margin. And it didn’t sit on that cash. The company returned roughly 96% of free cash flow to shareholders, with $2.2 billion in repurchases and $1.9 billion in dividends, including an 8% dividend increase. ADI has now raised its dividend for twenty consecutive years.

That kind of capital return only works if two things are true at once: the business is highly profitable, and it doesn’t require massive reinvestment just to stay in place. ADI checks both boxes. It spends heavily on R&D—around $2 billion per year—yet it doesn’t need Intel-style capital expenditures because it runs a “fab-lite” model. ADI owns key manufacturing sites (notably in Wilmington, Massachusetts, and Limerick, Ireland) while also using external foundries for a meaningful share of production. That hybrid approach gives flexibility: enough internal control to protect the high-performance edge, without the full fixed-cost burden of being totally vertically integrated like Texas Instruments or Intel.

Even the downturn dynamics underscore the point. Fiscal 2024 brought a brutal, inventory-driven reset—revenue fell more than 23%—and yet the business didn’t break. ADI kept operating margins above 40% at the trough, then rebounded to roughly $11 billion in revenue in fiscal 2025 as customer inventories normalized. Looking ahead, management guided fiscal 2026’s first quarter to revenue of $3.1 billion with adjusted operating margins around 43.5% and adjusted EPS of $2.29, signaling that the recovery was continuing.

Underneath all of this is the most misunderstood advantage in analog: the way R&D pays back. In digital, leading-edge chips can cost enormous sums to design and may get obsoleted quickly as process nodes advance. In analog, designs are typically cheaper to develop and can stay in production for a decade or longer. That changes the math. R&D in analog doesn’t just replace last year’s products—it accumulates. Each new design adds to a growing library of parts that can generate high-margin revenue for years with relatively little incremental investment. ADI’s catalog runs to tens of thousands of products, and many of them are exactly that kind of long-lived, compounding asset.

IX. Playbook: The ADI Way

Analog Devices has survived—and compounded—for six decades in an industry that routinely wipes out yesterday’s winners. If you strip the story down to its repeatable moves, you get a playbook that sounds straightforward on paper and is brutally hard to pull off in practice.

First: think long-term in a business built on cycles. Semiconductor demand doesn’t glide upward; it lurches—inventory builds, corrections, macro shocks, sudden pauses. The typical response in a downturn is to protect the quarter by cutting costs, and the first big line item on the chopping block is usually R&D. ADI has made a habit of doing the opposite. Under Jerry Fishman, it kept investing through the 2008 financial crisis. Under Vincent Roche, it spent $1.97 billion on R&D even as fiscal 2024 revenue fell more than 23%. The underlying logic is simple: in analog, products can live for decades. If you starve the pipeline during a downturn, you don’t just lose momentum—you mortgage years of future revenue.

Second: “acquire and enhance.” ADI’s two defining deals—Linear Technology and Maxim Integrated—weren’t random grabs for scale. They followed a consistent pattern: buy premium analog franchises with complementary portfolios, deep engineering benches, and strong margins. Then protect what makes them special while integrating what shouldn’t be unique—back office functions, distribution, and go-to-market operations. The bet is that the most valuable assets in analog aren’t factories or brand names. They’re accumulated design expertise and long-lived product libraries. If you integrate without breaking those, you don’t just get bigger—you get better.

Third: build switching costs by selling the whole signal chain, not a single chip. Over time, ADI deliberately moved from being a component vendor to being a system partner. Take an electric vehicle battery management system: ADI can supply voltage measurement, current sensing, temperature monitoring, and communication—an end-to-end solution. Once a customer designs that full chain into a platform, ripping it out isn’t a quick swap. It’s months of redesign, requalification, and risk. That’s how a one-time design win turns into a long annuity.

Fourth: stay close to customers, even at massive scale. Serving more than 100,000 customers across tens of thousands of products only works if the go-to-market machine is world-class. ADI blends direct sales with field applications engineers—specialists who sit with customer design teams and help them win in the real world—plus a streamlined distribution backbone anchored by its partnership with Arrow Electronics. Those field teams are the quiet engine of the model: “free” design support that converts into design-ins, and design-ins that can lock in revenue for years.

Fifth: preserve the engineering culture—especially through mergers. After two mega-deals, ADI managed to keep the vast majority of its engineering talent. That isn’t an HR victory; it’s a business necessity. In analog, the productive asset is institutional knowledge: the hard-earned intuition for making a high-resolution converter behave across temperature swings, voltage variation, noise, and manufacturing realities. That capability takes decades to develop and is almost impossible to replace on a spreadsheet-driven timeline.

And tying it all together is patient capital. ADI operates like a company that understands its own physics: long development cycles, slow qualification processes, and payoffs that can arrive five or ten years after the investment is made. If you can live on that clock—and still return excess cash to shareholders along the way—you get a compounding machine: invest through the cycle, deepen customer embed, and harvest durable returns.

X. Bear vs. Bull Case and Competitive Analysis

To underwrite Analog Devices, you have to hold two truths at once. This is a business with real structural advantages—durable margins, sticky design-ins, and a portfolio that’s hard to replicate. It’s also a business exposed to some of the biggest sources of uncertainty in global technology: geopolitics, semiconductor cycles, and the relentless pressure of scale competitors. Looking at ADI through frameworks like Porter’s Five Forces or Hamilton Helmer’s 7 Powers can help, but the real work is weighing what’s likely to persist against what could break.

The Bear Case

The biggest overhang is geopolitical. ADI has meaningful exposure to China, and the U.S.–China technology competition injects risk that doesn’t show up neatly in a spreadsheet. Export controls could limit what ADI can ship to certain customers. At the same time, Chinese industrial policy is pushing hard to build domestic semiconductor alternatives—especially in strategic categories like industrial and automotive—creating a long-term threat to share and pricing.

Then there’s the simple fact that semiconductors are cyclical. Fiscal 2024 was the reminder: an inventory correction can hit even the best analog franchises. Revenue fell more than 23% in a single year. ADI held margins impressively well, but the top line can still swing sharply, and those swings tend to cascade into earnings volatility and stock-price volatility.

Integration risk is the quieter bear argument, but it’s not trivial. ADI pulled off two large integrations—Linear and Maxim—without the typical “merger hangover.” Still, running a company built from multiple major engineering cultures creates ongoing complexity. Keeping talent, avoiding internal friction, and deciding which products to rationalize and which to protect are not one-time events. They’re permanent management challenges.

And finally, there’s Texas Instruments. TI is the heavyweight of analog, and its strategy is very different: invest aggressively in manufacturing scale—particularly 300-millimeter fabs in Texas—then use cost advantages to compete hard over time. If TI’s capacity strategy delivers meaningfully lower costs at full utilization, that could pressure pricing in the less differentiated parts of the analog market and gradually squeeze industry economics. ADI’s defense is performance and stickiness, but TI’s offense is scale.

The Bull Case

The bull case starts with the demand backdrop: the world needs more analog. Edge AI, electric vehicles, renewable energy, 5G infrastructure, industrial automation, and precision healthcare all expand the number of sensors, power rails, and signal paths in the real world—and every one of those needs conditioning, conversion, and management. ADI sits exactly where those systems touch physics.

Then there’s the moat. Through Helmer’s lens, ADI’s advantage shows up in several “powers” that are unusually durable in semiconductors. Switching costs are real: once ADI is designed into a platform, replacing it isn’t a quick supplier swap—it’s a redesign and requalification process with meaningful risk. There’s also a cornered resource: decades of accumulated analog expertise and a catalog that runs to tens of thousands of proven products. Add process power—the refinement of design and manufacturing know-how over sixty years—and you get a capability set that competitors can’t simply buy or copy on a fast timeline. And ADI’s focus on high-performance analog can also function as counter-positioning: it’s a difficult business for companies optimized around digital scale to replicate without changing their own DNA.

Porter’s view points in the same direction. The threat of new entrants is low because credibility in high-performance analog is earned over decades, not quarters. Customer power is limited because ADI sells into a highly diversified base and because switching is painful. Substitutes are rare: there’s no software-only alternative to a precision converter in a physical system. Rivalry is real, but concentrated among a handful of scaled players, in a large market that can support multiple profitable franchises.

And the financial engine matters. ADI’s ability to generate large free cash flow—while still investing heavily in R&D—gives it strategic flexibility. In fiscal 2025, free cash flow reached $4.3 billion, and management has shown a willingness to return capital to shareholders. That combination—secular tailwinds plus consistent cash return—is part of what makes ADI compelling over a full cycle.

The KPIs That Matter

If you want two numbers that capture whether the ADI story is on track, focus on these.

First: book-to-bill, the ratio of orders received to products shipped. It’s one of the cleanest leading indicators for where revenue is headed and how healthy the analog cycle is. Sustained levels above 1.0 usually mean demand is building; sustained levels below 1.0 tend to foreshadow a digestion phase.

Second: gross margin. It’s the clearest proxy for ADI’s competitive position because it reflects product mix, pricing power, and the strength of switching costs. If gross margins stay comfortably above the mid-sixties, it suggests the moat is intact. If they start sliding meaningfully, it’s a sign to ask why—more pricing pressure, more mix shift toward lower-differentiation products, or a competitor forcing the market to compete on cost instead of performance.

XI. Epilogue: The Future of the Physical-Digital Bridge

What would Ray Stata and Matthew Lorber think if they could see what their hockey-puck op amp company became? A $60-billion-plus enterprise with more than $11 billion in annual revenue, roughly 25,000 employees, and components that quietly sit inside countless systems that touch the physical world. The Model 101 is long gone from the catalog, but the mission it stood for—translating between analog reality and digital computation with the highest possible fidelity—still runs through everything ADI does, six decades later.

The next frontier is AI inference at the edge. As artificial intelligence spreads beyond cloud data centers and into factories, vehicles, hospitals, and homes, the demand for precision signal capture, conditioning, and conversion only grows. That’s ADI’s home turf. The appointment of AI veteran Dr. Yoky Matsuoka to the board and the push behind the Emergent AI strategy under CTO Alan Lee were clear tells: management expected this shift, and it planned to build for it.

Then there’s the energy transition. Electric vehicles don’t just need more chips; they need better power management, sensing, and high-reliability mixed-signal systems—especially in battery management, where ADI has spent years building credibility. Renewable generation and grid-scale storage create the same kind of pull: precise power conversion, monitoring, and control, deployed into infrastructure that has to work for decades.

Could ADI overtake Texas Instruments as the world’s largest analog semiconductor company? It’s within reach, but it’s not preordained. TI’s scale and manufacturing investments are real advantages. ADI’s counterweight is different: a relentless focus on the highest-performance segments, a portfolio that increasingly sells as full signal-chain solutions, and a proven ability to integrate transformative acquisitions without diluting the engineering DNA that made those companies great in the first place.

The deeper lesson of Analog Devices is that solving hard problems compounds. While much of the industry chased Moore’s Law and the next digital wave, ADI built a franchise on a stubborn truth: the physical world will always need to be measured, interpreted, and translated with precision. That premise has held for sixty years. And the forces shaping the next decade—AI, electrification, 5G, industrial automation—suggest it will matter even more in the decades to come.

The analog world isn’t going away. If anything, the more digital our lives become, the more valuable the bridge gets. And at that bridge, Analog Devices still sits in the tollbooth.

XII. Recent News

In January 2026, Analog Devices appointed Dr. Yoky Matsuoka to its board of directors. Matsuoka, a MacArthur Genius Award recipient and an executive officer at Panasonic Holdings, brought a rare blend of AI, robotics, and neuroscience experience from roles spanning Google X, Nest, Carnegie Mellon University, and the University of Washington. Her appointment took effect on January 20, 2026, expanded ADI’s board to eleven members, and came alongside the retirement announcement of director Susie Wee.

ADI’s fiscal 2025 results, reported in November 2025, underscored just how quickly the company snapped back after the prior year’s inventory correction. Full-year revenue rose to $11 billion, up 17 percent, and free cash flow hit a record $4.3 billion. ADI returned more than $4 billion to shareholders through dividends and repurchases, including an 8 percent dividend increase. Looking to the first quarter of fiscal 2026, management guided to $3.1 billion in revenue and adjusted earnings per share of $2.29.

On the Street, sentiment stayed constructive. In late January 2026, Wells Fargo reiterated a Buy rating on ADI, and JPMorgan flagged the company as one of its top AI chip picks heading into the next earnings report. ADI’s next quarterly results were expected on February 18, 2026.

XIII. Links and Resources

- Analog Devices Investor Relations

- ADI Fiscal 2025 Fourth Quarter Results

- Ray Stata Op Amp Articles Collection

- 4 Secrets to Business Longevity from Ray Stata — MIT Sloan

- Analog Devices Limerick Investment Announcement

- Tata and ADI Strategic Alliance

- Linear Technology Acquisition Completion

- Maxim Integrated Acquisition Completion

- Yoky Matsuoka Board Appointment

- ADI 2026 AI Predictions

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube