Waaree Renewable Technologies: The Solar EPC Story of India's Energy Transition

I. Introduction & Episode Setup

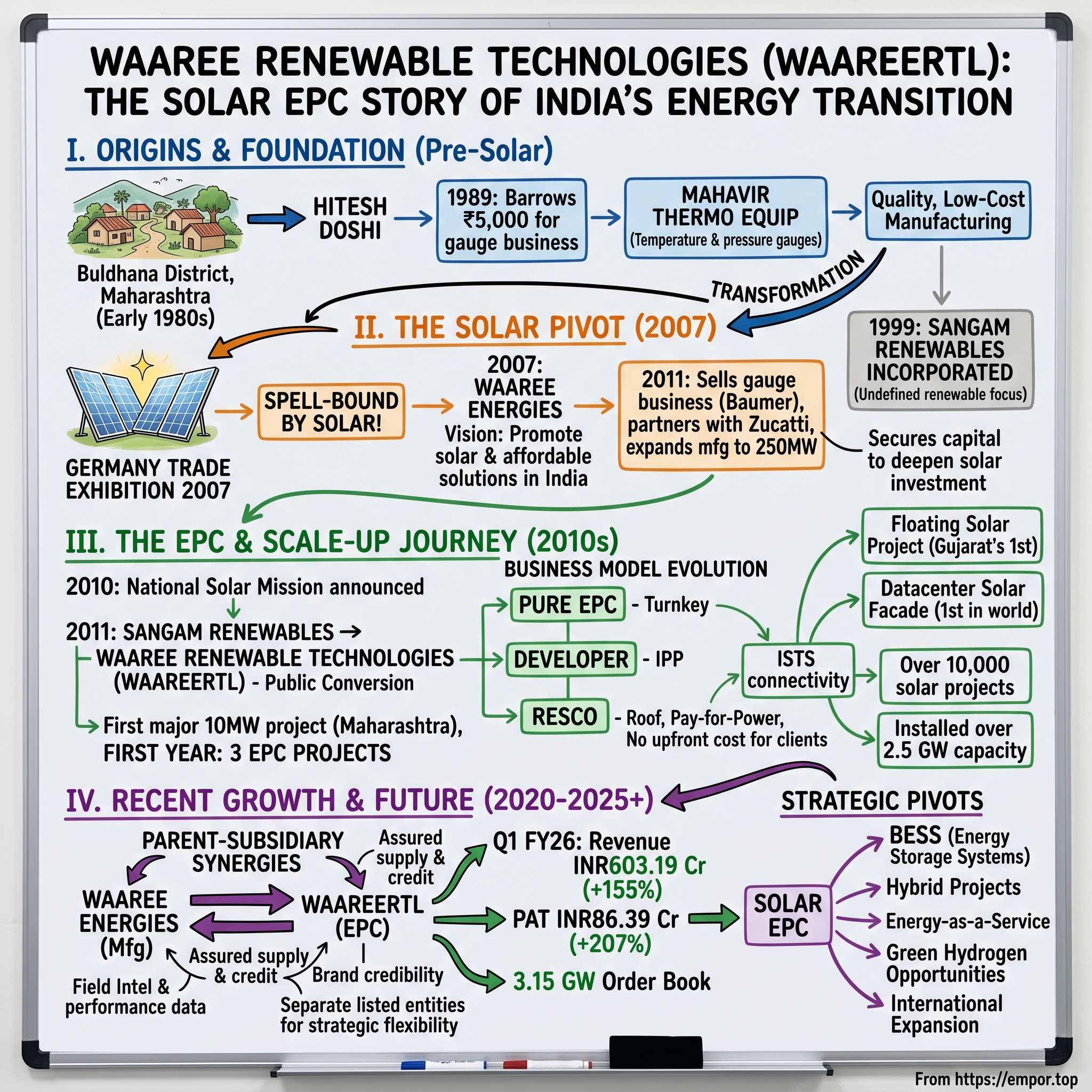

Picture this: A young man from a village in Maharashtra's Buldhana district, where electricity was a distant dream and telephones were unheard of, stands at a trade exhibition in Germany in 2007. Hitesh Doshi, who had bootstrapped his way from a ₹5,000 loan to running a successful temperature gauge business, finds himself "spell-bound" by gleaming solar panels catching the exhibition hall lights. In that moment, watching German engineers explain photovoltaic technology with evangelical fervor, he sees not just silicon and glass, but India's energy future—and his next chapter.

This is the origin moment of what would become the Waaree Group, today commanding a ₹10,400 crore market capitalization through its various entities. But our story isn't about the parent company that now boasts India's largest solar panel manufacturing capacity. It's about a lesser-known subsidiary that was actually founded eight years before that German epiphany—Waaree Renewable Technologies Limited (WAAREERTL), the engineering, procurement, and construction (EPC) arm that would quietly become the execution engine of India's solar revolution.

The question we're exploring today sounds almost paradoxical: How did a company founded in 1999, before its parent even entered the solar business, position itself to ride India's renewable energy wave? And more intriguingly, why does this subsidiary—with ₹1,964 crore in revenue and ₹288 crore in profit—trade at a P/E ratio of 36 while operating in what many consider a commoditized EPC market?

The answer involves a fascinating interplay of strategic foresight, vertical integration synergies, and perfect timing with India's energy transition. WAAREERTL isn't just another solar contractor; it's a case study in how subsidiaries can leverage parent company strengths while maintaining operational independence, how project execution capabilities become competitive moats, and how being early to a market transformation—even accidentally—can create lasting advantages.

Today's deep dive will take us from that electricity-deprived village in Buldhana to boardrooms where billion-rupee solar projects are signed, from the early days of India's tentative renewable push to today's aggressive 500 GW target by 2030. We'll examine how a company that started as Sangam Renewables Limited transformed into the EPC powerhouse installing over 10,000 solar projects, why it maintains separation from its manufacturing parent despite obvious synergies, and what its recent 205% profit surge tells us about India's renewable energy dynamics.

This is a story about transformation—not just of a company, but of an entire nation's energy infrastructure. It's about how execution capabilities in emerging markets can be more valuable than technological innovation, how government policy and private enterprise dance together in nation-building projects, and ultimately, how a subsidiary originally created for different purposes found itself at the center of India's most important economic transition.

So let's begin where all great business stories should—not with spreadsheets or org charts, but with a young entrepreneur staring at his father's struggling grocery store, dreaming of something bigger.

II. The Waaree Group Origins: From ₹5,000 to Solar Empire

The year is 1989. In Buldhana district's dusty lanes, where bullock carts still outnumber motorized vehicles, twenty-something Hitesh Doshi makes a decision that would seem either brave or foolish depending on your perspective. His father's small grocery store, the family's only source of income, struggles to make ends meet. The smart move would be to take a job in Mumbai or Pune—steady salary, predictable life. Instead, Doshi borrows ₹5,000, a sum that represented several months of his family's income, to start trading temperature and pressure gauges.

Why gauges? In interviews years later, Doshi would explain it with characteristic simplicity: "I noticed every factory, no matter how small, needed these instruments. They were essential, not optional." This insight—finding the unglamorous but essential—would define his business philosophy. Mahavir Thermo Equip, his first venture, wasn't trying to revolutionize anything. It was simply filling a gap in industrial India's supply chain with remarkable efficiency. By the early 2000s, Mahavir Thermo Equip wasn't just surviving—it was thriving. By 2007, Hitesh's business was exporting to the US and Canada, and seeing success in the thermal equipment market. The company had evolved from a one-man trading operation to a respected supplier with international clients. Doshi had discovered something crucial about Indian manufacturing: quality could match global standards, but costs could be kept dramatically lower. American and European buyers, initially skeptical, became repeat customers once they realized Indian suppliers could deliver consistent quality at 30-40% lower prices.

But success in thermal equipment wasn't enough for Doshi. "I had a hunger to grow the business further. During a trip to Germany, I went to a solar exhibition and was spell-bound. I talked to people there to understand how solar energy worked, and it convinced me that it would be the next step not only for expanding the business but also developing India's solar manufacturing sector," he would later recall.

That 2007 Germany trade exhibition moment deserves closer examination. Picture Doshi, successful but restless, walking through the gleaming halls of a German trade show. He's there for thermal equipment, his bread and butter. But in an adjacent hall, something catches his eye—row upon row of crystalline silicon panels, their surfaces catching the exhibition lights like dark mirrors. German engineers explain the technology with the kind of enthusiasm usually reserved for religious converts. They show him projections: solar costs falling, efficiency rising, governments worldwide pledging support.

"Mr Hitesh Doshi established Waaree Energies with a vision to promote solar energy and bring affordable solar solutions to developed and emerging markets, especially India. Way back in 2007, when solar industry was still in its infancy, he ventured in to this business and brought latest technology to India. His exceptional dedication and business acumen to establish solar business have yielded great results over these years."

The decision to pivot wasn't immediate, but it was decisive. In 2007, Waaree Energies was born with a module manufacturing facility of 30MW in Surat. This wasn't a small investment for someone who had started with ₹5,000. The initial facility required crores in investment, technology partnerships with international firms, and most importantly, a leap of faith that India would embrace solar energy at scale.

By 2010, Doshi made two moves that would define the next phase of his empire. First, he sold the thermal equipment company - Waaree Instruments - to the Swiss brand Baumer. The same year, he also expanded Waaree Energies' module manufacturing facility to 250MW. The sale to Baumer wasn't just about capital—it was about focus. Doshi understood something that many entrepreneurs miss: you can't fight a war on two fronts. The thermal business had given him his start, but solar was the future.

In 2011, Waaree Group made a pivotal move by selling its manufacturing unit to Switzerland's Baumer Group, securing capital to deepen its investment in solar technology. Building on this momentum, Waaree formed an international partnership with Zucatti in Italy to produce solar panels, highlighting Doshi's forward-thinking approach.

The expansion to 250MW wasn't just about scale—it was about timing. In 2010, India's National Solar Mission had just been announced, targeting 20GW of solar capacity by 2022. Most industry observers thought the target was impossibly ambitious. India had less than 200MW of total solar capacity at the time. But Doshi saw what others missed: when a country of 1.2 billion people decides to transform its energy infrastructure, the opportunity isn't just large—it's generational.

What's remarkable about this period is how Doshi structured his solar empire. Rather than putting everything under one entity, he maintained multiple companies with distinct roles. Waaree Energies would handle manufacturing. But there was another piece of the puzzle—a company that had actually been founded eight years before that fateful German exhibition, originally for entirely different purposes. This subsidiary, which would become Waaree Renewable Technologies Limited, was about to find its true calling.

The transformation from temperature gauges to solar panels might seem like a random walk through industrial sectors. But there's a thread connecting them: Doshi's consistent focus on essential infrastructure. Temperature gauges monitor industrial processes. Solar panels generate power. Both are unglamorous, both are essential, and both benefit from scale and execution excellence rather than cutting-edge innovation. This philosophy—find the essential, execute flawlessly, scale relentlessly—would define not just Waaree Energies, but its entire ecosystem of companies.

As we transition to the next chapter of this story, consider this: while Doshi was building his solar manufacturing empire from 2007 onwards, there was already a company in his portfolio, founded in 1999, waiting in the wings. This company would become the execution arm of India's solar revolution, but its origins and early years tell a very different story.

III. The Renewable Technologies Subsidiary Play (1999-2010)

Here's where the story takes an unexpected turn. Eight years before Hitesh Doshi stood mesmerized at that German solar exhibition, before he had even contemplated renewable energy, a company called Sangam Renewables Limited was quietly incorporated on June 22, 1999. This wasn't a solar company—not yet. It wasn't even clearly defined what it would become. But in the complex chess game of Indian business, sometimes you place pieces on the board before you know exactly how you'll use them.

Sangam Renewables Limited was originally incorporated on 22 June 1999 as 'Sangam Renewables Limited'. The name itself—"Sangam," meaning confluence in Sanskrit—suggested something coming together, though at the time, nobody could have predicted it would be the confluence of India's energy transition and private enterprise execution capabilities.

The early 2000s were a peculiar time for renewable energy in India. The Electricity Act of 2003 had just mandated state electricity regulatory commissions to promote renewable energy, but the market was embryonic. Solar panels cost $4-5 per watt, making solar electricity 5-10 times more expensive than coal power. Wind energy dominated whatever little renewable capacity existed. In this environment, Sangam Renewables operated in the shadows, not as a solar EPC giant, but as a company exploring various renewable opportunities, providing consultancy services, and waiting for its moment.

The Company got converted into a Public Company on November 18 2011 and thereafter the name was changed from 'Sangam Renewables Limited' to 'Waaree Renewable Technologies Limited'. But this name change in 2011 tells only part of the story. The real transformation began around 2007-2008, when the parent company's solar ambitions suddenly gave this dormant subsidiary a clear mission.

Think about the strategic elegance of this structure. You have Waaree Energies focused on manufacturing—capital intensive, requiring constant technology upgrades, dealing with global supply chains and Chinese competition. Then you have this subsidiary, already incorporated, already holding various licenses and clearances, perfectly positioned to become the execution arm. Manufacturing and EPC are fundamentally different businesses. Manufacturing is about scale, automation, and cost reduction. EPC is about project management, local relationships, and execution excellence. By keeping them separate, the Waaree Group could optimize each for its specific challenges.

Waaree Renewable Technologies Limited is an India-based engineering, procurement and construction (EPC) company, which is focused on the renewable energy sector. The Company is engaged in the solar EPC business, and generation of power through renewable energy sources. But this clinical description misses the drama of transformation. Between 2007 and 2010, WRTL had to build capabilities from scratch—hire engineers who understood solar technology, develop relationships with equipment suppliers, learn the intricacies of grid connection, navigate the bureaucratic maze of land acquisition and power purchase agreements.

The learning curve was steep and unforgiving. Early projects faced multiple challenges: panels degrading faster than expected in India's harsh climate, inverters failing due to dust and heat, grid stability issues causing frequent tripping. Each failure was expensive, but also educational. The company developed India-specific solutions: enhanced cleaning protocols for dusty environments, tropical-rated inverters, sophisticated monitoring systems that could predict and prevent failures.

By 2010, when the National Solar Mission was announced, WRTL wasn't starting from zero. It had spent three years in the trenches, learning by doing. This head start would prove invaluable. While competitors scrambled to build EPC capabilities as the market exploded, WRTL already had project pipelines, vendor relationships, and most importantly, a track record of completed projects.

It is also a solar developer that finances, constructs, owns, and operates solar projects. It provides clean energy to its clients by setting up both on-site solar projects (rooftop and ground-mounted) and off-site solar farms (open-access solar plants). This expansion beyond pure EPC into development and ownership represented a crucial strategic evolution. The company wasn't just building projects for others; it was taking equity stakes, arranging financing, and capturing more of the value chain.

The period from 2008-2010 also saw WRTL experiment with different business models. The Company's solutions and services include rooftop solar, floating solar, ground-mounted solar, capex model, renewable energy service company (RESCO) model, and operations and maintenance. In the RESCO model, the Company assumes control of all aspects of a rooftop solar project development - installation, financing, operation and ownership. The RESCO model was particularly innovative for the Indian market—customers got solar power without any upfront investment, paying only for the electricity consumed at rates lower than grid tariffs.

What made this subsidiary play particularly clever was the optionality it provided. If solar hadn't taken off in India, if the government policies had changed, if Chinese manufacturers had completely dominated the market, Waaree Energies could have pivoted or even shut down manufacturing while WRTL could have shifted to other renewable technologies or continued as a services company. The subsidiary structure provided both strategic flexibility and risk mitigation.

Waaree Renewable Technologies Limited was formerly known as Sangam Renewables Limited and changed its name to Waaree Renewable Technologies Limited in July 2021. The company was incorporated in 1999 and is headquartered in Mumbai, India. Waaree Renewable Technologies Limited operates as a subsidiary of Waaree Energies Limited. By maintaining its Mumbai headquarters while the parent operated from Gujarat, WRTL stayed close to India's financial center, making it easier to arrange project financing and maintain relationships with large corporate clients.

As we move into the next decade, this subsidiary that started as an undefined entity in 1999 was about to hit its stride. The foundation was laid, capabilities were built, and India's solar market was about to explode. The next chapter would see WRTL transform from a small EPC player to one of India's solar execution powerhouses.

IV. The EPC Business Model & Scale-Up (2010-2020)

The morning of January 26, 2011, Republic Day. At a construction site in Maharashtra's Satara district, hundreds of workers scramble across 50 acres of barren land. Solar panels glint in the harsh sun as they're mounted on steel structures. Viren Doshi, director of Waaree Renewable Technologies, watches nervously. This is WRTL's first major utility-scale project—10MW, worth over ₹100 crores. The deadline is impossibly tight: commission before March 31 to qualify for accelerated depreciation benefits under the expiring government scheme. Miss it, and the client loses crores in tax benefits. Miss it, and WRTL's reputation in the nascent solar EPC market is finished before it begins.

Successfully commissioned first solar EPC project of 10MW. Commissioned 3 EPC projects in first year of operations. That first 10MW project in 2011 wasn't just about meeting deadlines—it was about proving that an Indian EPC company could execute utility-scale solar projects to international standards. The learning was brutal and immediate. German inverters tripped constantly in 45°C heat. Chinese panels arrived with micro-cracks invisible to the naked eye. Local labor had never seen a solar panel, let alone installed one. Every problem required innovation: modified inverter housing with additional cooling, stringent incoming quality checks with electroluminescence testing, intensive training programs converting farm workers into solar technicians.

By 2012, WRTL had found its rhythm. Executed first thin film EPC project for a Sugar factory. Sugar factories became an unexpected sweet spot—they had land, they needed power for crushing season, and they understood industrial equipment. The thin-film technology was controversial—lower efficiency than crystalline silicon but better performance in high temperatures and diffused light conditions. WRTL's willingness to work with diverse technologies set it apart from competitors locked into single-supplier relationships.

EPC portfolio expanded to 100MW Marquee project for FMCG company was executed in record time. The FMCG project represented a breakthrough into corporate India. Blue-chip companies wanted solar not just for cost savings but for sustainability credentials. They demanded different standards: detailed project documentation, sophisticated monitoring systems, guaranteed performance ratios. WRTL adapted, building capabilities that would later become standard across the industry.

The business model evolution during this period was fascinating. Waaree Renewable Technologies Limited (WRTL) operates under the Waaree Energies Limited, spearheading the Solar EPC sector. Waaree has successfully completed over 10,000 solar projects, cumulatively accounting for more than 2.5 GW of operational capacity. But these weren't just construction projects. WRTL was developing three distinct revenue streams:

Pure EPC: Traditional turnkey projects where clients owned the assets. Margins: 8-12%. Capital requirement: Minimal. Risk: Execution only.

Developer Model: WRTL develops, owns, and operates plants, selling power through Power Purchase Agreements (PPAs). Margins: 15-20% IRR. Capital requirement: High. Risk: Market, regulatory, and operational.

RESCO Model: In the RESCO model, the Company assumes control of all aspects of a rooftop solar project development - installation, financing, operation and ownership. Clients pay only for power consumed, typically at 20-30% discount to grid tariffs. This model was revolutionary for Indian commercial and industrial customers who wanted solar benefits without capital investment or technical risk.

The scale-up wasn't just about megawatts—it was about geographic expansion and technological diversification. Our NTPC Kawas Floating Solar project was Gujarat states 1st Floating Solar project having 1000KWp capacity. Solar Power plants of this capacity if installed on land would have required 2.5 Acres of Land, hence by Installing Solar on Water we save the precious land resource as well as save water bodies by avoiding excessive evaporation of water during summer. Floating solar addressed India's land scarcity problem while providing additional benefits: reduced evaporation, lower operating temperatures leading to higher efficiency, and reduced algae growth in water bodies.

2013-2015 saw WRTL entering the big leagues. Entered in a JV with Mini Ratna Company Nipco to develop a 50MW IPP project. Successfully execute 50MW EPC project well with in time, and took repeat order for 25 MW. The joint venture with a government entity provided credibility and access to low-cost financing. More importantly, it demonstrated WRTL's ability to navigate the complex world of public-private partnerships.

The numbers tell only part of the story. Between 2010 and 2015, India's solar capacity grew from 200MW to over 5,000MW. WRTL captured a significant share not through lowest pricing but through reliability. In an industry plagued by fly-by-night operators who would win projects on impossibly low bids and then abandon them, WRTL's track record of completion became its calling card.

The designing & installation of our 10MW poly crystalline solar power plant at Latur, Maharashtra has been been completed with utmost effectiveness & efficiency. We are glad to have entrusted Team Waaree with the same. For designing & epc of 50MW Polycrystalline Technology Solar PV power project at Molga Village, Sihore district in MP state, we gave the contract to Waaree. We are really happy with company's overall performance. Client testimonials from this period reveal a pattern: WRTL wasn't necessarily the cheapest, but it was the most reliable.

The mid-decade period (2015-2017) brought new challenges. Chinese module prices crashed from $1/watt to $0.30/watt. Many Indian manufacturers shut down. EPC margins compressed as projects became commoditized. WRTL's response was to move up the value chain. Instead of competing on price for simple ground-mounted projects, it focused on complex installations: rooftops on operational factories where downtime meant revenue loss, floating solar requiring marine engineering expertise, hybrid projects combining solar with diesel generators or grid power.

Waaree Solar System powers the world's 1st solar-powered rated- 4 Datacenter Building. The system, with a capacity of about 1 MW, has been installed by integrating solar panels on all four walls of the facility, covering over 5,000 square feet of facade area. It is estimated that solar power system will help provide a CO2 emissions reduction equivalent to almost 7,000 trees per year. The datacenter project epitomized WRTL's evolution. This wasn't just about installing panels—it required understanding critical power requirements, designing redundant systems, ensuring zero downtime during installation, and integrating with existing UPS and diesel generator systems.

By 2018, WRTL had emerged as a different animal from its early incarnation. WRTL is one of the leading EPC (Engineering, Procurement & Construction) service providers in the solar energy sector, having installed over 1 GW of solar projects, including on-ground rooftop and utility projects, till date. The company had built something more valuable than project pipelines—it had built trust.

The late 2010s brought mega-projects. Waaree Renewable Technologies Ltd. (WRTL), a subsidiary of Waaree Energies Ltd., India's largest solar panel manufacturer, has announced that it has commissioned 87.5MW/122.5 MWp out of 150 MW/210 MWp EPC solar power project for UPC Renewable Energy Pvt Ltd.'s subsidiary M/s. Masaya Solar Energy Pvt. Ltd. in the Khandwa district of Madhya Pradesh. The solar power project is spread across 651 acres of undulated land terrain, with power being evacuated at a 220 kV voltage level and connected at PGCIL 400 kV/220 kV SS through the ISTS (inter-state transmission system) network. A total of 5,08,072 SPV modules, ranging from 335 Wp Polycrystalline to 540 Wp Monocrystalline, with an inverter capacity of 3.125 MW were installed. The PPA (solar power purchase agreement) for the project has been made with the Solar Energy Corporation of India for a period of 25 years.

This Madhya Pradesh project showcased how far WRTL had come. Managing 651 acres of construction, coordinating 508,072 module installations, handling ISTS connectivity—this was industrial-scale infrastructure development. The mix of module technologies (polycrystalline and monocrystalline) demonstrated flexibility in procurement and design optimization.

The parent-subsidiary synergy became increasingly apparent during this period. While competitors struggled with module procurement during shortage periods, WRTL had assured supply from Waaree Energies. While others faced working capital crunches, WRTL could leverage the parent's balance sheet. While standalone EPC companies fought for credibility, WRTL carried the Waaree brand—increasingly recognized as India's solar champion.

But perhaps the most important development of this decade wasn't captured in megawatts or project counts. It was the systematic building of capabilities: project management systems that could handle multiple concurrent projects, quality assurance protocols that exceeded international standards, safety procedures that achieved zero fatality records across millions of man-hours, financial engineering capabilities that could structure complex PPAs and achieve financial closure.

As 2020 approached, WRTL stood at an inflection point. It had proven it could execute. It had built a brand. It had developed capabilities. But the market was evolving. Pure EPC margins were shrinking. Chinese companies were entering Indian EPC markets. New technologies like energy storage were emerging. The next phase would require not just execution excellence but strategic transformation.

V. The Parent-Subsidiary Dynamics & Synergies

The boardroom at Waaree Energies' Surat manufacturing facility, March 2019. Module prices have crashed again—down 40% in six months. Chinese manufacturers are dumping inventory as trade wars escalate. The management team debates a critical question: should WRTL, the EPC subsidiary, be forced to buy modules exclusively from the parent at potentially higher prices, or should it have freedom to source from anywhere to win projects? This seemingly mundane transfer pricing decision encapsulates the perpetual tension in parent-subsidiary relationships—between synergy and autonomy, between group benefit and individual entity optimization.

Waaree Energies Limited ("WEL") was founded in 1990. It is India's largest manufacturer of solar PV modules with the largest aggregate installed capacity of 13.3 GW (Source: CRISIL Report) and India's largest Solar Cell Manufacturer with 5.4 GW capacity. WEL commenced operations in 2007 focusing on solar PV module manufacturing with an aim to provide quality, cost-effective sustainable energy solutions across markets, and aid in reducing carbon footprint paving the way for sustainable energy thereby improving quality of life. Meanwhile, Waaree Renewable Technologies Limited (WRTL) operates under the Waaree Energies Limited, spearheading the Solar EPC sector. Waaree has successfully completed over 10,000 solar projects, cumulatively accounting for more than 2.5 GW of operational capacity.

The numbers reveal an interesting asymmetry. The parent company boasts 13.3 GW of manufacturing capacity, yet the subsidiary has executed only 2.5 GW of projects over its lifetime. This isn't a failure—it's a strategic choice. WRTL was never meant to be the exclusive customer for Waaree Energies' modules. Instead, it serves multiple strategic purposes that justify its separate existence.

First, consider the market intelligence advantage. Every EPC project WRTL executes provides real-world data on module performance, degradation rates, failure modes, and customer pain points. When inverters from a particular manufacturer fail repeatedly in Rajasthan's dusty conditions, WRTL knows first. When a new mounting structure design reduces installation time by 20%, WRTL has tested it. This field intelligence flows back to the parent, informing product development and quality improvements. Competitors buying Waaree modules don't share such detailed feedback.

Second, the credibility boost. Waaree Energies is India's largest manufacturer and exporter of solar modules. As of FY24, they hold 21% share of the domestic market for solar modules and 44% share in India's solar module exports. When Waaree Energies claims its modules can withstand Indian conditions, it's not just laboratory testing—WRTL has installed them across every climate zone in India. The subsidiary's project portfolio becomes the parent's most powerful sales tool.

Third, the financial engineering possibilities. Company is almost debt free. This applies to WRTL, but the parent-subsidiary structure allows sophisticated capital allocation. Manufacturing is capital-intensive but generates steady cash flows. EPC is working capital-intensive but asset-light. By keeping them separate, each entity can optimize its capital structure. WRTL can take project-specific debt without affecting the parent's balance sheet. The parent can raise growth capital without EPC project risks affecting its valuation.

The vertical integration benefits flow both ways. WRTL gets assured module supply during shortage periods—crucial when Chinese suppliers prioritize their home markets or when import duties spike suddenly. It gets extended credit terms that standalone EPC companies can't negotiate. It gets early access to new technologies—bifacial modules, half-cut cells, larger wafer sizes—allowing it to offer cutting-edge solutions before competitors.

But here's what's counterintuitive: WRTL doesn't always use Waaree modules. In projects where customers specify particular brands, or where specific certifications are required, or where non-Waaree modules offer better project economics, WRTL sources externally. This flexibility is crucial for winning projects. A captive EPC company forced to use only parent company products would lose more projects than it wins.

The recent mega-deal illustrates this dynamic perfectly. Waaree Renewable Technologies Limited (WRTL), a subsidiary of Waaree Energies Limited, India's largest solar PV module manufacturer, has secured its largest-ever Engineering, Procurement, and Construction (EPC) contract for a 2 GW solar project from Sunbreeze Renewables Nine Pvt. Ltd, a Special Purpose Vehicle (SPV) of Jindal Renewables. The project will be implemented in Bikaner, Rajasthan, utilizing advanced technologies and sustainable solutions to enhance energy efficiency and maximize generation.

This 2 GW project—nearly equal to WRTL's entire historical execution—represents a step change. The parent will likely supply a significant portion of modules, but WRTL has the flexibility to source some components elsewhere if it improves project economics. The parent benefits from a massive order; the subsidiary maintains its margins and reputation for execution excellence.

The governance structure reveals careful balance. Promoter Holding: 74.4% in WRTL ensures control remains with the Waaree Group, but the 25.6% public float provides independent valuation and forces transparency. Related-party transactions must be disclosed. Transfer pricing must be justified. This structure protects minority shareholders while preserving group synergies.

Consider the international expansion dynamics. Waaree Renewable Energies Australia will focus on renewable energy business in Australia. The parent is setting up manufacturing in the US and subsidiaries in Australia. WRTL could theoretically execute international projects, but hasn't pushed aggressively overseas. Why? Because EPC requires deep local knowledge—regulations, labor laws, grid codes, financing structures. The parent can ship modules anywhere; the subsidiary's execution capabilities don't travel as easily.

The innovation spillovers are particularly valuable. When WRTL executed Waaree Solar System powers the world's 1st solar-powered rated- 4 Datacenter Building. The system, with a capacity of about 1 MW, has been installed by integrating solar panels on all four walls of the facility, covering over 5,000 square feet of facade area. It is estimated that solar power system will help provide a CO2 emissions reduction equivalent to almost 7,000 trees per year. This wasn't just an EPC project—it was a learning laboratory for Building Integrated Photovoltaics (BIPV), knowledge that helped the parent develop specialized BIPV modules.

The competitive dynamics are intriguing. WRTL competes with other EPC companies who are also Waaree Energies' customers. Sterling & Wilson, L&T, Tata Power Solar—they all buy Waaree modules while competing with WRTL for EPC projects. The parent must maintain strict information barriers. Module pricing to WRTL can't be preferential enough to create unfair advantage, yet must be competitive enough to keep the subsidiary viable.

Financial interdependencies run deep but remain opaque. Working capital cycles intersect—WRTL's project advances can fund module procurement from the parent. The parent's manufacturing cash flows can support WRTL during project execution delays. Inter-company loans, though disclosed, obscure the real extent of financial support. During the 2018-2019 NBFC crisis when project financing dried up, the parent's balance sheet likely kept WRTL afloat, though specific details weren't disclosed.

The strategic optionality this structure provides is immense. If India's EPC market consolidates and margins improve, WRTL can scale aggressively. If manufacturing becomes more profitable, the parent can allocate more capital there while WRTL maintains minimal growth. If new technologies like energy storage or green hydrogen emerge, either entity can pursue them without affecting the other's focus. If regulations change—say, manufacturers are barred from EPC activities—the corporate structure already provides separation.

Looking at recent performance, Q1 FY26 revenue INR603.19 Cr (+155%), PAT INR86.39 Cr (+207%), 3.15 GW order book, strong BESS and solar EPC growth. The 3.15 GW order book exceeds WRTL's entire historical execution, suggesting a transformation in scale. The mention of BESS (Battery Energy Storage Systems) indicates evolution beyond pure solar EPC. This diversification wouldn't be possible if WRTL were merely a captive execution arm.

The unasked question is: why not merge? Why maintain separate listed entities with independent boards, compliance costs, and potential conflicts of interest? The answer lies in the value of optionality. Separation preserves strategic flexibility, enables focused management, allows optimal capital structures, and provides transparent valuation markers. In a rapidly evolving industry, these benefits outweigh the costs of complexity.

As we transition to examining recent performance, remember this: WRTL's story isn't just about executing solar projects. It's about how vertical integration can be achieved without full integration, how synergies can be captured while maintaining independence, and how a subsidiary can simultaneously serve and transcend its parent's interests.

VI. Recent Performance & Strategic Pivots (2020-2025)

July 17, 2025, 9:30 AM. WRTL's quarterly earnings call begins. CFO Manmohan Sharma's voice carries a note of barely contained excitement as he announces the numbers: "We are pleased to report revenue of ₹603.19 crores for Q1 FY26, compared to ₹236.35 crores in Q1 FY25, delivering a robust growth of 155.20%." The analysts on the call are stunned. In an industry where 20-30% growth is considered healthy, WRTL has just posted numbers that suggest a fundamental transformation is underway.

The company reported revenue from operations of Rs 6.03 billion in Q1 FY 2025-26, marking a 155.2 per cent year-on-year (YoY) growth from Rs 2.36 billion in Q1 FY 2024-25. But raw revenue growth tells only part of the story. Profit after tax (PAT) increased to Rs 863.9 million, up from Rs 281.6 million in Q1 FY 2024-25, marking a 206.77% YoY increase. The company isn't just growing—it's becoming more profitable as it scales.

The transformation began in 2020, at the pandemic's peak. While global supply chains collapsed and solar installations ground to a halt, WRTL made three counterintuitive decisions that would reshape its trajectory. First, it aggressively hired talent from struggling competitors, building capabilities in energy storage and hybrid systems. Second, it invested in digital project management systems when others were cutting costs. Third, it pre-positioned inventory and equipment anticipating the post-pandemic boom.

"This performance reflects the strength of our business model, our disciplined operational approach, and our ability to execute large-scale projects efficiently in a rapidly evolving clean energy landscape." Sharma's statement understates the radical operational changes. WRTL had reimagined EPC execution for the digital age: drone surveys reducing site assessment time by 80%, AI-powered design tools optimizing panel placement, real-time monitoring systems predicting maintenance needs before failures occur.

The market context explains the explosive growth. "As of June 2025, India's total renewable energy capacity stood at 234 GW, with solar contributing 116.25 GW. In the first half of CY2025, solar installations grew by 51.6% year-on-year, underscoring the sector's accelerating momentum." India wasn't just adding solar capacity—it was doing so at unprecedented speed, and WRTL had positioned itself perfectly to capture this wave.

Earnings before interest, taxes, depreciation, and amortisation (EBITDA) rose by 186.1 per cent YoY to Rs 1.17 billion in Q1 FY 2025-26. The EBITDA margin reached 19.5 per cent, increasing from 17.38 per cent in Q1 FY 2024-25. Margin expansion during rapid growth is rare in EPC businesses. Typically, companies sacrifice margins to win projects and gain scale. WRTL was achieving both—a testament to operational excellence and strategic project selection.

The order book tells the forward story. Q1 FY26 revenue INR603.19 Cr (+155%), PAT INR86.39 Cr (+207%), 3.15 GW order book, strong BESS and solar EPC growth. That 3.15 GW order book represents more than WRTL's entire historical execution. But more importantly, the mention of "BESS" (Battery Energy Storage Systems) signals the company's evolution beyond pure solar EPC.

Energy storage represents WRTL's most significant strategic pivot. As solar penetration increases, grid stability becomes challenging. Solar generates power when the sun shines, not necessarily when power is needed. Storage bridges this gap. WRTL recognized this early, building capabilities while competitors focused solely on solar. Now, as India begins requiring storage with large solar projects, WRTL is one of the few EPC companies capable of delivering integrated solar-plus-storage solutions.

The recent project wins demonstrate this evolution. Contract value increased by Rs.29.65 Cr to Rs.1510.06 Cr for 2012.47 MWp solar PV project. A routine contract modification? Look closer. The Rs 29.65 crore increase for the same megawatt capacity suggests addition of value-added services—likely storage, advanced monitoring, or grid stability solutions. WRTL isn't just building solar farms; it's delivering energy solutions.

"India has also achieved a major milestone in its clean energy transition, with 50% of its total installed power capacity now sourced from non-fossil fuels, reaching this target five years ahead of schedule." This acceleration changes everything. Original projections had India reaching 500 GW renewable capacity by 2030. Current trajectory suggests it might happen by 2027-2028. For WRTL, this means the next three years could see more business than the previous decade.

Geographic expansion adds another growth vector. While maintaining Mumbai headquarters for financial market access, WRTL has established regional offices in solar-rich states: Rajasthan, Gujarat, Karnataka, Andhra Pradesh. Each office isn't just administrative—it's a hub for local relationships, understanding state-specific regulations, managing local labor, navigating land acquisition complexities.

The technology stack evolution deserves attention. "With a strong order book, efficient execution capabilities, and strategic investments, WRTL remains committed to supporting India's clean energy transition through innovative and scalable solutions." Those "strategic investments" include:

Digital Twin Technology: Creating virtual replicas of solar plants before construction, optimizing design and predicting performance.

Robotic Cleaning Systems: Addressing India's dust problem that can reduce solar output by 30%.

Predictive Analytics: Using weather data, satellite imagery, and historical performance to forecast generation and schedule maintenance.

Blockchain for RECs: Implementing blockchain for Renewable Energy Certificate tracking, ensuring transparency and preventing double-counting.

Financial management has become increasingly sophisticated. "Total income for the quarter reached ₹608.02 crore, including ₹4.83 crore in other income. This was accompanied by disciplined cost management, with EPC contract expenses at ₹470.02 crore, employee benefit expenses at ₹9.35 crore." The company maintains an asset-light model—EPC contract expenses represent 78% of revenue, while employee costs are just 1.5%. This Operating leverage means incremental revenue drops almost directly to the bottom line.

The investment community's reaction has been mixed. Stock is trading at 22.8 times its book value and the stock is down -31.0% in 1 year. Despite spectacular operational performance, the market remains skeptical. Why? Three concerns dominate: execution risk on the massive order book, working capital requirements for 3+ GW of projects, and dependence on government policies that could change.

But WRTL's recent strategic moves address these concerns. Waaree Renewable executes agreements for investment in Smart Joules; completion expected by August 30, 2025. Smart Joules specializes in cooling-as-a-service for commercial buildings—a adjacent market that leverages WRTL's execution capabilities while diversifying beyond utility-scale solar.

The competitive landscape has shifted dramatically. Chinese EPC companies, previously focused on their home market, are now bidding aggressively for Indian projects. Global giants like Iberdrola and Enel are entering India directly rather than through local partners. Indian conglomerates—Adani, Tata, Reliance—are building in-house EPC capabilities. In this environment, WRTL's 155% growth isn't just impressive—it's almost miraculous.

The secret sauce appears to be focus. While competitors diversify into wind, hydro, transmission, WRTL remains laser-focused on solar and storage. While others chase international projects, WRTL dominates its home market. While some pursue turnkey ownership models requiring massive capital, WRTL sticks to capital-efficient EPC and selective development.

"India's renewable energy landscape continues to evolve rapidly, with installed capacity surpassing 220 GW, including 105.65 GW of solar as of March 2025." The next 280 GW to reach India's 500 GW target must come in five years—an annual run rate of 56 GW. Even capturing 5% market share would mean nearly 3 GW annually for WRTL, implying sustained triple-digit growth.

As we prepare to examine competitive dynamics, consider this: WRTL's recent performance isn't just about riding India's renewable wave. It's about a company that spent two decades building capabilities, survived multiple boom-bust cycles, and positioned itself perfectly for a generational opportunity. The question isn't whether WRTL can maintain growth—India's energy transition ensures demand. The question is whether it can maintain execution excellence at unprecedented scale.

VII. Competition & Market Dynamics

A conference room at the Oberoi hotel, Mumbai, February 2024. The solar industry's who's who have gathered for an emergency meeting. The government has just announced Module Price Capping for government projects. Chinese modules are facing 40% duty plus ALMM (Approved List of Module Manufacturers) restrictions. Project auctions are hitting record lows—₹2.50 per unit. In this pressure cooker environment, Sterling & Wilson's CEO makes a stunning announcement: they're pivoting away from Indian utility-scale solar EPC to focus on international markets and O&M. The room goes silent. India's once-dominant EPC player is effectively surrendering the home market.

This scene encapsulates the brutal reality of India's solar EPC market in 2024-2025. Jakson Green, Tata Power Solar, Hartek Group, L&T Construction, and Sterling and Wilson Renewable Energy emerged as the top utility-scale solar engineering, procurement, and construction (EPC) service providers in 2024. Jakson Green was the leading EPC player with a market share of 20%, followed by Tata Power Solar with 13%. The top five utility-scale solar EPC service providers accounted for 48% of the market share.

But market share numbers hide a more complex story. The industry has undergone fundamental restructuring. Sterling and Wilson, Siemens Gamesa, and Tata Power Solar were the top utility-scale solar EPC service companies in 2021. By 2024, Siemens Gamesa has exited, Sterling & Wilson has de-prioritized India, and new players like Hartek Group have emerged. The churn rate is extraordinary—of the top 10 EPC companies in 2020, only four remain in the top 10 by 2024.

Consider the scale evolution. SJVN Limited announced that it has awarded the engineering, procurement, and construction (EPC) contract for its 1 GW solar project in Bikaner, Rajasthan, to Tata Power Solar Systems. The project will be developed at an estimated cost of ₹54.91 billion (~$72.21 million), making it India's biggest solar EPC contract. When single projects reach 1GW—equivalent to a nuclear power plant—the game changes. Only companies with massive balance sheets, execution capabilities, and risk management systems can compete.

WRTL's position in this evolving landscape is unique. Prozeal Green Energy, Tata Power Solar, Vikram Solar, Waaree Renewable Technologies, and Opera Energy emerged as the top utility-scale solar engineering, procurement, and construction (EPC) service providers in the first half of 2023. WRTL appears in top rankings but doesn't dominate market share statistics. This is deliberate—the company focuses on profitable projects rather than volume.

The competitive dynamics reveal three distinct segments:

Tier 1: The Giants - L&T, Tata Power Solar, and now Adani Solar represent industrial conglomerates with massive balance sheets. They can afford to bid aggressively, absorb losses on individual projects, and play the long game. L&T Construction was fourth on the list. In June 2024, the company won an order to build a grid-connected 185 MW solar project with BESS at Kajra in the Lakhisarai district of Bihar. These players increasingly integrate backward, controlling the entire value chain.

Tier 2: The Specialists - Jakson Green, Sterling & Wilson (historically), and WRTL built businesses focused on solar EPC. Jakson Green's cumulative large-scale installed solar capacity in EPC mode was 3.6 GW as of December 2024. These companies survive through operational excellence, technology differentiation, and careful project selection.

Tier 3: The Opportunists - New entrants like Ashoka Buildcon, KEC International, and various regional players see solar EPC as adjacent to their core businesses. Ashoka Buildcon entered the top ten list in 1H 2024 in third position by commissioning its first 150 MW solar project. They bring construction expertise but often underestimate solar's technical complexities.

The self-EPC trend fundamentally reshapes competition. However, as India is witnessing a sharp decline in solar tariffs, more and more developers have opted to carry out their own EPC so as to take care of cost optimisation. This share self EPC installations was about 50.59 per cent in 2017-18, translating into 4,639.61 MW of solar capacity. Large IPPs like ReNew Power, Greenko, and Azure Power increasingly execute projects internally, cutting out EPC contractors entirely.

Technology disruption adds another competitive dimension. India added 25.2 GW of solar capacity in 2024, a record installation number, surpassing the annual capacity additions of all previous years. But this isn't just more of the same. Projects now require: - Battery storage integration - Grid stability solutions - Advanced forecasting systems - Robotic cleaning - AI-powered monitoring

Companies without these capabilities are relegated to commodity EPC work with razor-thin margins.

Chinese competition looms large despite government restrictions. Chinese EPC companies, backed by state banks offering 2-3% interest rates, can bid 20-30% below Indian companies. They bring integrated supply chains—modules, inverters, trackers, even construction equipment—from China. While ALMM and customs duties provide some protection, Chinese companies increasingly partner with Indian firms, effectively competing through proxies.

The financial metrics tell a sobering story. Sterling and Wilson Renewable Energy, in its earnings call in January 2025, mentioned that the CAGR for its solar EPC business was about 15%-20%, with the gross margin closer to 10%. A 10% gross margin in a business with 120-180 day working capital cycles, execution risks, and technology obsolescence barely covers cost of capital. No wonder established players are exiting or diversifying.

Government policy creates both opportunities and challenges. As of the end of Q1 2025, India's pipeline of large-scale solar projects stood at 180.4 GW, with another 127.8 GW of projects awaiting auction. The pipeline is massive, but policy uncertainty—changes in GST rates, module price caps, local content requirements—makes long-term planning impossible.

WRTL navigates this environment through strategic positioning:

-

Selective Bidding: Unlike volume-focused competitors, WRTL bids only on projects where it has competitive advantage—complex terrains, integrated storage, or projects requiring Waaree modules.

-

Technology Differentiation: Early investments in floating solar, BIPV, and energy storage create barriers competitors can't easily overcome.

-

Risk Management: Avoiding fixed-price contracts in volatile environments, insisting on price variation clauses, maintaining diversified project portfolio.

-

Vertical Integration Benefits: Access to parent company modules at predictable prices when market volatility strikes.

-

Regional Focus: Deep presence in select states rather than pan-India spread, enabling better government relationships and local expertise.

The recent consolidation wave is just beginning. Amid all the market turmoil, some established players have exited the EPC business (Mahindra, Juwi), while others have become more selective. Mahindra Susten's exit after building 1.5GW shocked the industry. Juwi India's closure despite German parent's global leadership showed that international expertise doesn't guarantee Indian success.

But new entrants keep coming. KEC (a transmission and electrical services contractor) and Ashoka Buildcon (roads and civil construction EPC) are two other prominent names eyeing an entry. They see 180GW pipeline and assume there's room for everyone. They're wrong. The next shakeout will be brutal—only companies with differentiated capabilities, strong balance sheets, and disciplined execution will survive.

Looking ahead, the market structure will likely evolve toward oligopoly. Five to seven major players will dominate utility-scale projects. Another 10-15 will focus on specialized segments—rooftop, floating, hybrid. The rest will exit or become sub-contractors. WRTL is positioning for the former group, leveraging its parent's manufacturing strength and two decades of execution experience.

The competitive landscape's most important lesson: in commodity markets, operational excellence isn't enough. You need structural advantages—vertical integration, technology differentiation, or scale economies. WRTL has the first two. Whether it can achieve the third while maintaining profitability will determine its next decade.

VIII. Investment Analysis & Valuation

The valuation paradox of Waaree Renewable Technologies reads like a Rorschach test for investor psychology. Stock is trading at 22.8 times its book value and The Current PE Ratio of Waaree Renewables Technologies Ltd is 74.97 as on 12 Dec 2024. By any traditional metric, the company appears expensive. Yet the stock has delivered spectacular returns to early believers while simultaneously down -31.0% in 1 year. This schizophrenic performance encapsulates the challenge of valuing high-growth companies in transformational sectors.

Let's start with the numbers that make value investors nervous. The P/B ratio of Waaree Renewable Technologies Ltd is 23.21 times as on 15-May-2025, a 479% premium to its peers' median range of 4.01 times. A company trading at 23 times book value implies either astronomical growth expectations or dangerous speculation. For context, mature utilities typically trade at 1-2 times book value. Even high-growth technology companies rarely sustain P/B ratios above 10.

The P/E ratio tells a similarly vertiginous story. The PE Ratio of Waaree Renewables Technologies Ltd was 29.08 last year, now the PE ratio is 74.97, showing a year-on-year growth of 157.8%. The PE Ratio of Waaree Renewables Technologies Ltd grew by 157.8% whereas, the EPS ratio grew by 89.0. The P/E expanded faster than earnings—classic multiple expansion driven by enthusiasm rather than fundamentals.

Historical context provides perspective. WAAREE RENEWABLE TECHNOLOGIES 's p/e ratio for fiscal years ending Mar2024 to Mar2020 averaged 23.68x. WAAREE RENEWABLE TECHNOLOGIES 's operated at median p/e ratio of 5.82x from fiscal years ending March 2018 to 2022. The valuation transformation from single-digit to triple-digit P/E in five years suggests either the market drastically undervalued the company initially or currently overvalues it—or both.

The Bull Case:

The optimists argue WRTL's valuation reflects not current earnings but future cash flows from India's renewable buildout. With a 3.15 GW order book and India targeting 280 GW of additional renewable capacity by 2030, WRTL could generate ₹15,000-20,000 crores in revenue over the next five years. At 15% EBITDA margins and 10% net margins, that's ₹1,500-2,000 crores in cumulative profits. The current market cap of ₹10,400 crores doesn't seem unreasonable against these numbers.

Moreover, Company is almost debt free. In a capital-intensive industry where competitors carry debt-to-equity ratios of 1-2x, WRTL's clean balance sheet provides enormous financial flexibility. It can bid aggressively for projects, weather execution delays, and invest in new technologies without financial stress.

The operational momentum supports premium valuations. Net profit of Waaree Renewable Technologies rose 205.44% to Rs 86.44 crore in the quarter ended June 2025 as against Rs 28.30 crore during the previous quarter ended June 2024. Sales rose 155.21% to Rs 603.19 crore in the quarter ended June 2025 as against Rs 236.35 crore during the previous quarter ended June 2024. Companies growing at 150%+ deserve higher multiples than those growing at 15%.

The parent company synergy adds another valuation layer. While WRTL trades independently, its access to Waaree Energies' manufacturing capabilities, technology, and balance sheet creates an moat competitors can't replicate. This structural advantage justifies a premium to standalone EPC companies.

The Bear Case:

The skeptics point to multiple red flags. The average industry PE Ratio of Power Infrastructure is 81.8 as on 12 Dec 2024, but this average includes asset-heavy utilities with predictable cash flows. Pure-play EPC companies typically trade at 10-20x P/E. WRTL's 75x P/E assumes perfection in execution and market conditions.

The margin trajectory raises concerns. While margins are under pressure due to increased competition, management remains optimistic about future growth. If margins compress from current 14-15% to industry-standard 8-10%, earnings could halve even as revenue grows. The market isn't pricing this risk.

Promoter Holding: 74.4% creates governance concerns. With such concentrated ownership, minority shareholders have limited influence. Related-party transactions with the parent company, though disclosed, could disadvantage minorities. The lack of dividend payment despite profitability suggests cash is being retained for group benefit rather than distributed to shareholders.

The cyclicality of EPC business is notorious. Today's 3.15 GW order book could evaporate if government policies change, financing dries up, or module prices spike. The 2018-2019 NBFC crisis saw multiple EPC companies with strong order books fail to execute due to working capital crunches. History could repeat.

Comparative Valuation:

Waaree Renewables major competitors are Oriana Power, Sterling and Wilson, KPI Green Energy, Ujaas Energy, KP Energy, Ravindra Energy, GE Power India. Market Cap of Waaree Renewables is ₹10,168 Crs. While the median market cap of its peers are ₹3,365 Crs. WRTL trades at 3x the median market cap of peers despite similar business models. This premium assumes either superior execution, better growth prospects, or market inefficiency.

Sterling & Wilson, once India's largest solar EPC company, trades at less than 1x book value after years of struggles. Its experience—winning projects on thin margins, facing execution challenges, suffering working capital stress—offers a cautionary tale for WRTL investors.

The Accounting Quality Question:

Company is depreciating a greater percentage of assets. this is contributing to a reduction in net profit. Aggressive depreciation could be conservative accounting or could mask underlying asset quality issues. Without detailed project-level data, investors can't distinguish between prudence and problems.

Revenue recognition in EPC businesses involves significant judgment. Percentage-of-completion accounting means revenue is recognized based on management estimates of project progress. Small changes in assumptions can materially impact reported earnings. The 200% profit growth might reflect accounting choices as much as operational performance.

The Institutional View:

Foreign Institutional Investors (FII) 1.13% and Domestic Institutional Investors (DII) 0.24%. Minimal institutional ownership suggests professionals remain skeptical. Retail investors dominate the shareholder base, potentially explaining volatile valuations driven more by sentiment than fundamentals.

Retail has been buying the stock which is usually a sign of exuberance. Retail enthusiasm often marks market tops. When taxi drivers give stock tips, professionals sell. The current retail buying frenzy might signal overvaluation rather than opportunity.

The Strategic Value Argument:

Beyond financial metrics, WRTL might possess strategic value justifying premium valuations. As India's renewable buildout accelerates, execution capabilities become scarce resources. Large IPPs might acquire WRTL not for its earnings but for its project management expertise, government relationships, and trained workforce.

The parent company might eventually buy out minorities to fully integrate EPC capabilities. At current valuations, this seems unlikely, but if the stock corrects 50-60%, a buyout becomes plausible. Minority investors might be betting on this eventual exit.

The Risk-Reward Calculus:

Despite a total order book of 26.5 GW, challenges remain in securing a larger market share compared to subsidiaries, necessitating continuous capability enhancement. While margins are under pressure due to increased competition, management remains optimistic about future growth, supported by a solid pipeline of approximately 30 GW and ongoing investments in capital expenditure.

The 26.5 GW pipeline (likely a typo for 2.65 GW) represents massive execution risk. If WRTL successfully delivers, the stock could double. If execution falters, it could halve. At current valuations, the risk-reward appears skewed negatively—more downside than upside.

Investment Verdict:

WRTL embodies the classic growth-value divide. Growth investors see a company riding India's renewable revolution, posting triple-digit growth, with unique competitive advantages. Value investors see nose-bleed valuations, execution risks, and governance concerns.

The truth, as often, lies between extremes. WRTL is neither a sure-fire multi-bagger nor an obvious bubble. It's a high-risk, high-reward bet on India's energy transition and one company's ability to execute at unprecedented scale. For risk-tolerant investors with five-year horizons, current valuations might prove reasonable. For conservative investors seeking margin of safety, waiting for a 40-50% correction would be prudent.

The most intellectually honest position: WRTL's valuation cannot be justified by traditional metrics but might be rational given India's renewable energy imperative. Sometimes, transformation trumps valuation. Whether this is one of those times, only time will tell.

IX. Playbook & Strategic Lessons

The conference room at IIM Ahmedabad, March 2025. Hitesh Doshi addresses a packed hall of MBA students, venture capitalists, and entrepreneurs. "Everyone asks me about solar technology, government subsidies, Chinese competition," he begins. "But WRTL's success wasn't about any of these. It was about building the right structure for the right opportunity at the right time. Let me tell you what we learned..."

This section distills two decades of strategic decisions into actionable insights. WRTL's journey from an undefined subsidiary to a ₹10,000+ crore enterprise offers lessons that transcend the renewable energy sector.

Lesson 1: The Subsidiary as Strategic Option

Most entrepreneurs view subsidiaries as administrative necessities—vehicles for regulatory compliance or tax optimization. WRTL demonstrates their potential as strategic options on uncertain futures. When founded in 1999, renewable energy was peripheral to India's energy mix. By maintaining WRTL as a separate entity, the Waaree Group created optionality: if renewables exploded, they had a vehicle ready; if not, minimal capital was at risk.

The lesson: In rapidly evolving industries, create structural flexibility before you need it. The cost of maintaining dormant entities is minimal compared to the opportunity cost of missing transformational moments. Think of subsidiaries as call options on future opportunities—small premiums for potentially massive payoffs.

Lesson 2: Vertical Integration Without Full Integration

WRTL's relationship with parent Waaree Energies represents sophisticated vertical integration. They capture synergies—assured module supply, technology transfer, financial support—while maintaining operational independence. This structure avoids the bureaucracy of full integration while securing most benefits.

The playbook: Structure vertical integration through ownership and governance, not operational merger. Keep customer-facing units entrepreneurial and nimble. Use parent resources as competitive advantages, not crutches. Maintain separate P&Ls to ensure accountability. The magic happens at the intersection of autonomy and support.

Lesson 3: The Power of Patient Capital in Impatient Markets

From 1999 to 2010, WRTL generated minimal returns. Many investors would have pulled the plug. But patient capital—from promoters who understood the long-term renewable opportunity—allowed the company to build capabilities without pressure for immediate returns. When the market exploded post-2015, WRTL was ready.

The strategic insight: In transformation sectors, being early looks identical to being wrong for extended periods. The companies that ultimately dominate aren't necessarily first movers but "ready movers"—those with capabilities, capital, and patience to scale when markets inflect. Fund transformation businesses with patient capital that can withstand 5-10 year J-curves.

Lesson 4: Capability Building Precedes Market Development

WRTL started building solar EPC capabilities in 2007-2008, years before India's solar market materialized. By the time the National Solar Mission launched in 2010, WRTL had already made mistakes, learned lessons, and built relationships. Competitors starting in 2010 faced a three-year experience deficit.

The execution playbook: In emerging sectors, build capabilities before markets fully develop. Accept lower margins and smaller projects initially as tuition for learning. When markets scale, experience becomes your moat. The profits you sacrifice in early years are investments in future market share.

Lesson 5: Focus Beats Diversification in Execution Businesses

While competitors diversified into wind, hydro, transmission, and distribution, WRTL remained laser-focused on solar EPC. This focus enabled deep expertise: understanding solar irradiation patterns across India, mastering module degradation in different climates, optimizing installation techniques for various terrains.

The lesson extends beyond renewable energy: In execution-intensive businesses, depth beats breadth. Customers pay premiums for specialists who've seen every problem and know every solution. Diversification dilutes expertise and confuses market positioning. Dominate a niche before expanding scope.

Lesson 6: Market Cyclicality as Competitive Advantage

Solar EPC is notoriously cyclical—boom periods when everyone's hiring followed by busts when projects dry up. WRTL used downturns strategically: hiring talent from struggling competitors, investing in training and systems, pre-positioning equipment for the next upturn. This countercyclical approach turned market volatility from threat to opportunity.

The strategic framework: In cyclical industries, optimize for the entire cycle, not just the peaks. Use downturns for capability building and market consolidation. Maintain financial flexibility to invest when others retreat. View cycles as washing machines that clean out weak competitors, leaving more space for survivors.

Lesson 7: The Trust Premium in Infrastructure

Infrastructure projects involve massive capital, long time horizons, and irreversible commitments. In this environment, trust becomes currency. WRTL's two-decade track record, backed by the Waaree brand, commands premium pricing. Clients pay extra for certainty that projects will be completed, warranties honored, and maintenance provided.

The playbook for trust building: Never compromise execution for short-term profits. Honor commitments even when contracts allow escape clauses. Invest in relationships that span decades, not transactions. In infrastructure, reputation is built over decades but destroyed in moments. Guard it zealously.

Lesson 8: Technology Adoption vs. Technology Development

WRTL didn't develop revolutionary technology. Instead, it excelled at adopting and adapting global technologies for Indian conditions. When floating solar emerged globally, WRTL quickly mastered it for Indian water bodies. When AI-powered monitoring became available, WRTL integrated it into offerings.

The lesson: In most industries, competitive advantage comes from superior technology adoption, not development. Monitor global innovations, evaluate relevance for your market, and move fast to integrate promising technologies. Let others bear R&D costs; focus on implementation excellence.

Lesson 9: Managing Government Relations Without Dependence

WRTL benefits from government renewable policies but isn't dependent on any single scheme. When solar subsidies changed, WRTL adapted. When net metering rules evolved, WRTL adjusted. This flexibility comes from maintaining diverse revenue streams and avoiding over-reliance on government contracts.

The strategic principle: In regulated industries, align with government direction but don't depend on specific policies. Build businesses that benefit from tailwinds but survive headwinds. Maintain relationships with policymakers but don't let these relationships become your primary competitive advantage.

Lesson 10: The Scaling Paradox

WRTL's current challenge embodies a universal scaling paradox: the capabilities that enabled growth to ₹2,000 crores differ from those needed for ₹10,000 crores. Project management that worked for 100MW projects breaks down at 1GW scale. Informal relationships must become systematic processes. Entrepreneurial culture must evolve toward professional management.

The scaling playbook: Recognize that companies must repeatedly reinvent themselves at different scale points. What got you here won't get you there. Hire ahead of needs—bring in leaders who've operated at your target scale, not current scale. Accept that some founding team members won't make every transition. Build systems and processes before they become bottlenecks.

Lesson 11: Capital Structure as Competitive Weapon

WRTL's debt-free status isn't just financial conservatism—it's competitive strategy. In bidding situations, WRTL can accept lower margins because it doesn't carry interest costs. During execution, it can weather payment delays without financial stress. This financial flexibility becomes operational advantage.

The financial strategy: In project-based businesses, optimize capital structure for flexibility, not returns. The cost of excess capital is minor compared to the cost of lost opportunities due to financial constraints. Think of clean balance sheets as competitive weapons, not lazy capital allocation.

Lesson 12: The Ecosystem Play

WRTL doesn't operate in isolation. It's part of the Waaree ecosystem including manufacturing, trading, and development. But it also participates in broader ecosystems: equipment suppliers, construction contractors, financial institutions, regulatory bodies. Success comes from orchestrating these ecosystems, not just optimizing internal operations.

The ecosystem lesson: In complex industries, competitive advantage increasingly comes from ecosystem orchestration rather than individual firm capabilities. Invest in relationships across the value chain. Create win-win structures that align ecosystem interests. View suppliers and customers as partners in value creation, not counterparties in zero-sum negotiations.

The Meta-Lesson: Timing Matters More Than Strategy

WRTL's strategies weren't unique. Other companies pursued similar approaches. The difference was timing—being ready when India's renewable revolution accelerated. This wasn't luck but prepared readiness. By maintaining capabilities through lean years, WRTL could scale rapidly when opportunities emerged.

The ultimate strategic insight: In transformation industries, timing matters more than strategy. But timing isn't about predicting the future—it's about maintaining readiness for multiple futures. Build capabilities before markets emerge. Maintain financial flexibility to scale rapidly. Create structural options on uncertainty. When transformation accelerates, readiness becomes destiny.

As Doshi concludes his IIM lecture: "We didn't know solar would explode in 2015. We didn't predict government policies or Chinese competition. We simply built capabilities, maintained flexibility, and stayed ready. When India needed execution excellence in solar, we were there. That's the real lesson—be ready for opportunities you can't yet see."

X. Future Outlook & Strategic Options

Mumbai, January 2030. The financial press gathers for WRTL's investor day. The company has just crossed ₹50,000 crores market capitalization. But CEO Viren Doshi's presentation doesn't celebrate past success. Instead, he projects a slide that reads: "The next five years will transform energy more than the previous fifty. Here's how WRTL evolves from solar EPC to energy transformation partner."

This future isn't speculation—it's already taking shape through strategic moves, market dynamics, and technological shifts visible today.

The 500 GW Imperative

India's commitment to 500 GW renewable capacity by 2030 isn't just ambitious—it's existential. With 234 GW current capacity, India must add 266 GW in five years—53 GW annually. For context, India's entire power sector capacity in 2000 was 100 GW. The scale challenges every assumption about project development, financing, and execution.

WRTL's strategic positioning for this boom involves three pillars:

Scale Infrastructure: Building project management capabilities for 5-10 GW annual execution versus current 1-2 GW. This requires fundamental reimagination—AI-powered project planning, modular construction approaches, parallel execution teams, robotic installation systems.

Financial Innovation: Developing new models to fund massive scale. Traditional project finance won't suffice. WRTL explores infrastructure investment trusts (InvITs), green bonds, international climate finance, and innovative structures like community solar ownership.

Execution Industrialization: Moving from project-by-project execution to industrialized delivery. Standardized designs, prefabricated components, assembly-line installation processes. Think Toyota Production System applied to solar farms.

The Storage Revolution

Battery costs have fallen 90% in a decade and continue declining 10-15% annually. By 2027, solar-plus-storage will be cheaper than coal power 24/7. This changes everything. WRTL's early investments in BESS capabilities position it for this transformation.

The strategic play involves three horizons:

Horizon 1 (2025-2027): Integrate 2-4 hour storage with solar projects for grid stability and peak power delivery. WRTL targets 30% of projects with storage components.

Horizon 2 (2027-2030): Long-duration storage (8-12 hours) enables round-the-clock renewable power. WRTL develops expertise in flow batteries, thermal storage, and hybrid systems.

Horizon 3 (Beyond 2030): Seasonal storage using hydrogen or other technologies enables 100% renewable grids. WRTL positions as system integrator for complex renewable-storage-hydrogen installations.

The Green Hydrogen Opportunity

India targets 5 million tonnes annual green hydrogen production by 2030. Each tonne requires 50 MWh of renewable electricity. That's 250 TWh additional renewable demand—equivalent to 100+ GW of solar capacity. WRTL's strategic options:

EPC for Hydrogen Projects: Building integrated renewable-electrolyzer facilities. These projects combine WRTL's solar expertise with new electrolyzer installation capabilities.

Hydrogen Transportation Infrastructure: Developing pipelines, storage facilities, and refueling stations. Adjacent to current capabilities but requires new expertise.

Industrial Integration: Helping steel, fertilizer, and refining companies integrate green hydrogen into operations. Leverages WRTL's industrial customer relationships.

The Digital Layer

Energy transformation isn't just about hardware—it's increasingly about software. WRTL's digital initiatives point toward fundamental business model evolution:

Virtual Power Plants: Aggregating distributed solar and storage assets into grid-scale resources. WRTL could operate 10,000 small installations as one large power plant.

Energy-as-a-Service: Moving beyond EPC to ongoing energy management. Instead of building and leaving, WRTL maintains, optimizes, and operates assets for 25-year lifecycles.

Predictive Analytics: Using weather data, satellite imagery, and IoT sensors to predict and prevent failures before they occur. Maintenance becomes proactive rather than reactive.

Carbon Markets Integration: As carbon pricing matures, WRTL helps clients optimize not just energy costs but carbon footprints. Every project becomes a carbon reduction asset.

International Expansion Vectors

While WRTL has focused domestically, international opportunities beckon:

South Asia: Bangladesh, Sri Lanka, and Nepal face similar energy challenges with less developed execution capabilities. WRTL's India experience translates directly.

Africa: The continent needs 600 GW of new capacity by 2040. Indian companies' experience with challenging infrastructure and cost-conscious markets provides advantages over Western competitors.

Middle East: Saudi Arabia and UAE target massive renewable programs. WRTL's experience with desert conditions and large-scale projects fits perfectly.

The expansion strategy isn't about flag-planting but selective entry where Indian experience provides genuine advantage.

The Consolidation Scenario

India's fragmented EPC market won't remain so. As projects become larger and more complex, subscale players will struggle. WRTL's consolidation options:

Horizontal Acquisition: Buying distressed competitors for talent and relationships more than assets. During the next downturn, WRTL could acquire 2-3 smaller players, instantly adding 2-3 GW execution capacity.

Vertical Integration: Acquiring specialized contractors—pile driving, electrical, monitoring systems—to control more of the value chain.

Technology Acquisition: Buying startups in energy storage, grid integration, or digital monitoring to accelerate capability building.

Strategic Partnerships: Joint ventures with international players bringing technology while WRTL provides execution.

The Parent Company Question

WRTL's relationship with Waaree Energies will evolve. Three scenarios seem plausible:

Full Integration: The parent absorbs WRTL to create a fully integrated renewable energy giant. Simplifies structure but loses entrepreneurial culture.

Greater Independence: WRTL reduces parent shareholding to 51%, raising capital for aggressive expansion while maintaining strategic alignment.

Ecosystem Expansion: WRTL becomes the platform for multiple energy transition businesses—storage, hydrogen, carbon management—each as separate subsidiaries.

Risk Scenarios and Mitigation

The future isn't without risks: