Ujjivan Small Finance Bank: From Microfinance Pioneer to Universal Banking Aspirant

I. Introduction & Episode Setup

The trading floor at the National Stock Exchange erupted on December 12, 2019. Ujjivan Small Finance Bank's IPO had just closed with bids worth ₹1.28 lakh crore against an issue size of ₹750 crore—a staggering 170 times oversubscription. Retail investors had bid 50 times, institutional investors 177 times. It was the best banking IPO performance in four years, and for a bank that had existed for less than three years, it was nothing short of miraculous.

But here's what made this moment truly extraordinary: just five years earlier, Ujjivan wasn't even a bank. It was a microfinance institution whose typical customer was a vegetable vendor in Bangalore earning ₹300 a day, or a rickshaw puller in Bihar supporting a family of five on ₹8,000 a month. The journey from serving India's economically active poor to becoming a publicly-traded bank competing for universal banking status represents one of the most ambitious transformations in Indian financial history.

This is a story about financial inclusion meeting public market capitalism—two forces that often pull in opposite directions. How do you maintain a social mission while satisfying quarterly earnings expectations? How do you serve customers who've never had a bank account while building technology infrastructure that rivals established banks? And perhaps most critically: what happens when your entire customer base—the daily wage earners, street vendors, and small shopkeepers—suddenly loses all income during a global pandemic?

The Ujjivan story matters because it's really three stories in one. First, it's about the maturation of Indian microfinance from a charitable endeavor to a profitable business model. Second, it's about regulatory evolution—how the Reserve Bank of India created an entirely new category of banks to bridge the financial inclusion gap. And third, it's about resilience—surviving when your business model is tested by the most severe economic shock in a century.

What we're about to explore isn't just another fintech success story or banking transformation tale. It's about building trust in communities where formal finance has never reached, creating social collateral where financial collateral doesn't exist, and proving that serving the underserved can be both impactful and profitable—until suddenly, it almost wasn't.

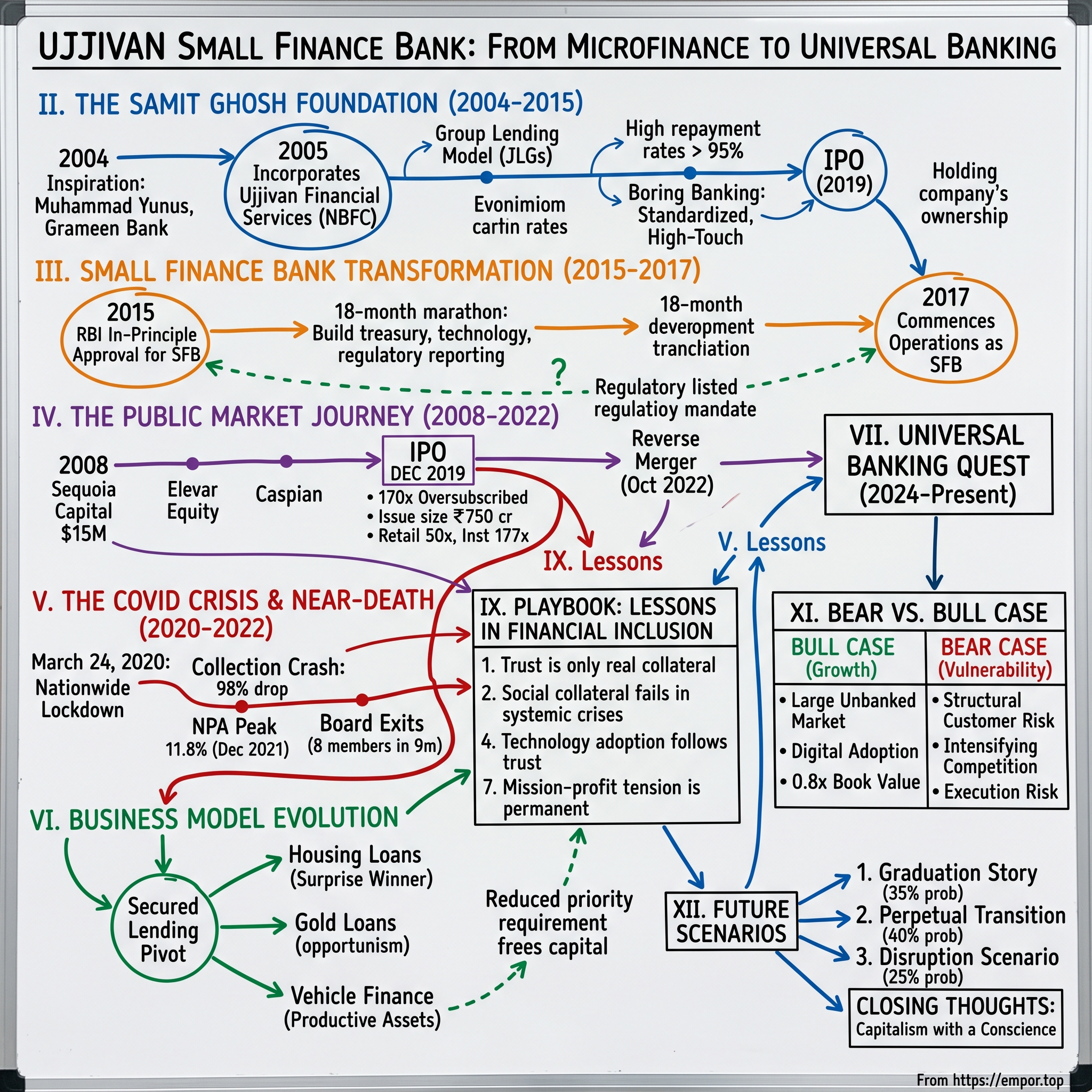

II. The Samit Ghosh Foundation Story

In 2004, Samit Ghosh was 55 years old and had already lived three professional lives. He'd spent decades at Citibank and Standard Chartered, run retail banking operations across the Middle East and South Asia, and pioneered consumer finance in India when credit cards were still exotic. By any measure, he'd earned the right to a comfortable semi-retirement, perhaps a few board seats, maybe some advisory work. Instead, he decided to start from zero.

The inspiration came from an unlikely source: Muhammad Yunus's Grameen Bank model in Bangladesh. Ghosh had been studying microfinance for years, fascinated by its counter-intuitive economics—lending to people with no collateral, no credit history, and irregular income streams, yet achieving repayment rates above 95%. But he saw something others missed: India's microfinance sector was dominated by non-profits and NGOs treating it as charity. What if someone applied professional banking discipline to serving the poor?

On October 28, 2005, Ghosh incorporated Ujjivan Financial Services as a non-banking financial company (NBFC) in Bangalore. The name came from Sanskrit, meaning "arise" or "uplift"—aspirational without being patronizing. His mission statement was deliberately precise: "To provide financial services to the economically active poor who are not adequately served by financial institutions."

The early model was pure microfinance orthodoxy. Groups of 5-20 women would form joint liability groups (JLGs). No member could get a loan unless all members agreed to guarantee each other's repayments. Loans started at ₹10,000, disbursed in cash, collected weekly in person. The genius wasn't the structure—it was the execution.

Ghosh recruited field officers from the same communities they would serve. A field officer managing vegetable vendors in Chickpet understood the rhythms of the wholesale market, knew when onion prices spiked, recognized which vendors had loyal customers versus those who constantly switched locations. This hyperlocal knowledge became Ujjivan's edge. While banks saw risk in a woman selling flowers outside a temple, Ujjivan's field officer knew she'd been there fifteen years and never missed a day.

The Karnataka beginnings were deliberately methodical. Instead of rushing to scale, Ghosh spent the first year perfecting the model in Bangalore's outskirts—Kolar, Tumkur, Mandya. Each branch opening followed a ritual: community meetings explaining the group lending concept, financial literacy sessions teaching basic accounting, and most importantly, delivering exactly what was promised. If Ujjivan said loan disbursement would happen Tuesday at 2 PM, it happened Tuesday at 2 PM. In communities where moneylenders changed terms arbitrarily and banks meant endless waiting, this predictability built trust faster than any marketing campaign.

By 2010, Ujjivan had crossed one million customers. The economics were fascinating: average loan size of ₹15,000, interest rates around 24% annually (high by banking standards, revolutionary compared to the 60-120% charged by moneylenders), operational costs at 8-10% of assets, and net margins of 4-5%. The high-touch model was expensive—each field officer could manage only 400-500 clients, meeting them weekly—but the near-zero default rates made it profitable.

The growth trajectory was remarkable: from zero to 2.6 million customers by 2015, loan book expanding from ₹100 crore to ₹5,000 crore, operations spreading across 24 states. But what made Ujjivan different wasn't just scale—it was discipline. While competitors chased growth, Ghosh insisted on what he called "boring banking": standardized processes, rigorous training (every field officer underwent 21-day residential training), and technology adoption (handheld devices for collections by 2012, biometric authentication by 2014).

The social impact was undeniable. Independent studies showed Ujjivan clients increased household income by 20-30% within two years, children's school enrollment rates jumped, and perhaps most tellingly, clients started refusing loans from moneylenders even when offered. One client in Tamil Nadu told researchers: "Earlier I was scared of the moneylender. Now he's scared I won't need him."

By 2015, Ujjivan had proven something revolutionary: you could run microfinance like a professional financial institution, achieve social impact at scale, and generate returns that attracted serious capital. The next question was whether they could become something even more ambitious—an actual bank.

III. The Small Finance Bank Transformation (2015-2017)

On September 16, 2015, at 3:30 PM, ten microfinance institutions across India simultaneously received phone calls that would change their destinies. The Reserve Bank of India was informing them they'd been selected for something unprecedented: in-principle approval to set up small finance banks. Among them was Ujjivan Financial Services, and for Samit Ghosh, it was validation of a decade-long bet that banking for the poor could be done differently.

The timing was no accident. The RBI had released draft guidelines for small finance banks on July 17, 2014, with final guidelines coming on November 27, 2014. The central bank's vision was revolutionary: create a new category of banks specifically mandated to serve the unserved and underserved. The objectives included provision of savings vehicles and supply of credit to small business units, small farmers, micro and small industries. Out of 72 applicants, only ten made the cut.

What made Ujjivan's selection remarkable was its scale at the time of approval. The company had already serviced over 2.6 million customers from 464 branches in 24 states. This wasn't a startup hoping to build a bank—it was an established microfinance institution with proven execution capability. The in-principle approval meant Ujjivan had 18 months to transform itself from a lending-only NBFC into a full-service bank.

The preparation marathon that followed was grueling. Banking isn't just lending with a different license—it's an entirely different universe of complexity. Ujjivan needed to build capabilities it had never possessed: treasury operations, payment systems, regulatory reporting frameworks that satisfied not just microfinance regulations but full banking supervision. They had to create technology infrastructure capable of handling millions of daily transactions, not just weekly loan collections. Most challenging was the human element—training field officers who'd spent years doing group meetings to become bankers who could explain fixed deposits, sell insurance, and operate complex banking software.

The technology transformation alone was staggering. Ujjivan's existing systems were designed for batch processing of microfinance loans. Banking required real-time transaction capability, integration with payment networks, ATM infrastructure, and regulatory reporting systems that could satisfy RBI's stringent requirements. They partnered with multiple technology vendors, often discovering that solutions designed for traditional banks didn't work for customers who might be illiterate or uncomfortable with technology.

On November 11, 2016, Ujjivan received the final license from the Reserve Bank of India. The timing was surreal—this was just three days after demonetization had thrown India's cash economy into chaos. While the country grappled with currency shortages, Ujjivan was preparing to launch banking operations in an environment where its primarily cash-dependent customers were struggling to conduct basic transactions.

February 1, 2017 marked the official commencement of operations as Ujjivan Small Finance Bank. That first day was orchestrated chaos—265 branches across 24 states simultaneously transitioning from microfinance operations to full banking. Customers who'd only known loan products suddenly had access to savings accounts, fixed deposits, remittance services. The transformation wasn't just operational; it was psychological. For many customers, this was their first real bank account, their first ATM card, their first experience of formal financial inclusion beyond borrowing.

The regulatory framework for small finance banks was both an opportunity and a burden. On one hand, they could accept deposits—a game-changer for funding costs. Previously, Ujjivan borrowed from banks at 10-12% to lend at 24%. Now they could gather deposits at 6-7%, dramatically improving their net interest margins. They could offer payment services, insurance distribution, and wealth products—multiple revenue streams beyond just interest income.

But the restrictions were equally significant. Small finance banks had to maintain 75% of their loan book as priority sector lending—essentially continuing to serve the same underserved segments. They couldn't lend more than 10% of capital to any single borrower, limiting their ability to do corporate lending. For the first three years, they couldn't open more than 25% of branches in urban areas. These weren't just rules—they were guardrails ensuring small finance banks remained true to their inclusion mandate.

The competitive dynamics also shifted dramatically. As an NBFC, Ujjivan competed with other microfinance institutions for customers and capital. As a bank, they suddenly faced competition from everyone—established banks expanding into microfinance, other small finance banks, payment banks, and increasingly, digital lending apps. The moat they'd built through relationships and trust remained valuable, but technology was democratizing access to credit in ways that threatened their traditional model.

What Ujjivan and the other nine institutions had achieved was historic—they were the first cohort of small finance banks in India, pioneers in a new model of banking. The transformation from microfinance to banking represented not just regulatory evolution but a fundamental reimagining of how financial services could reach India's masses. The question now was whether this model could survive contact with public markets.

IV. The Public Market Journey & Capital Story

Before Ujjivan ever dreamed of public markets, it had to convince private capital that lending to rickshaw pullers was investable. The early believers were a fascinating mix: impact investors who cared about social returns, and sophisticated funds who saw opportunity where others saw only risk.

The institutional capital journey began in 2008 when Sequoia Capital India led a $15 million round—not their typical technology bet, but a recognition that financial inclusion could scale like software. Elevar Equity (formerly Unitus) followed, bringing not just capital but deep microfinance expertise from their global portfolio. By 2014, Caspian had joined, and together these investors had pumped $154 million into Ujjivan, making it one of the best-capitalized microfinance institutions globally.

But the cap table told a deeper story. Unlike typical venture investments where founders retain significant stakes, Samit Ghosh had diluted aggressively to attract institutional capital. By the time of the small finance bank transformation, Ujjivan Financial Services (the holding company) was owned primarily by financial investors, with management holding less than 10%. This would prove both a strength—professional governance from day one—and a complication when navigating the public markets.

The IPO decision in 2019 was driven by regulatory compulsion more than choice. RBI mandated that small finance banks be listed within three years of reaching ₹500 crore net worth—Ujjivan had crossed that threshold. But the timing seemed perfect: the Indian markets were buoyant, financial inclusion was a hot theme, and Ujjivan had just posted its best-ever quarterly results.

The December 2019 IPO was structured carefully. At ₹750 crore raised at ₹37 per share, it wasn't a large offering by banking standards. But what happened next stunned everyone. The retail portion was oversubscribed 50 times, the institutional portion 177 times. The grey market premium touched 40%. For context, established private banks typically see 10-20x oversubscription. This was different—this was euphoria.

The investor presentation told a compelling story: 9% net interest margins (among India's highest), 2.5% gross NPAs (better than many established banks), 20% ROE potential, and massive untapped market opportunity. Analysts saw Ujjivan as the perfect play on India's formalization story—as the economy formalized, millions would need banking services, and who better positioned than India's largest small finance bank?

But the ownership structure created immediate complications. Ujjivan Financial Services held an 80% stake in the bank, with only 20% public float. This meant two things: limited liquidity in the stock, and a complex two-tier structure where investors could own either the holding company or the bank, but the value flows were unclear.

The stock's early performance was volatile. It listed at ₹55, a 48% premium to issue price, then gyrated wildly as investors struggled to value this unique entity. Was it a high-growth fintech that deserved technology multiples? A risky microfinance company that should trade at a discount? Or a bank that should be valued on book multiples? The market couldn't decide.

Then COVID hit, and everything changed. The stock crashed from ₹55 to ₹12 in March 2020—a 78% decline that wiped out ₹3,000 crore in market value. The retail investors who'd bid 50 times were devastated. The institutional investors who'd seen this as a demographic play watched their thesis crumble as Ujjivan's customers—daily wage earners—lost all income overnight.

The capital crisis that followed was existential. Ujjivan needed fresh capital to provide for ballooning NPAs, but who would invest in a microfinance-focused bank during a pandemic that had destroyed its customers' livelihoods? The board considered multiple options: rights issue (but would shareholders participate?), preferential allotment (but to whom?), or strategic sale (but at what valuation?).

The solution came through corporate restructuring. In October 2022, the board approved a reverse merger of Ujjivan Financial Services into the bank. This simplified structure eliminated the holding company discount, improved liquidity, and made the bank more attractive to institutional investors. The share swap ratio gave holding company shareholders 1.15 shares of the bank for each share held—a fair exchange that avoided minority exploitation.

The post-merger capital structure was cleaner but still challenging. Promoter holding had to be brought down to 26% per regulatory requirements. Foreign ownership was capped at 74%. The bank needed to maintain 9% tier-1 capital but also fund growth. It was a complex optimization problem: raise too much capital and dilute returns, raise too little and constrain growth.

Recent capital moves reflect this balancing act. The bank has raised ₹500 crore through qualified institutional placements, carefully timing issuances to minimize dilution. They've used retained earnings to build capital buffers, choosing lower growth over excessive dilution. The stock has recovered to ₹35-40 range, but still trades below book value—suggesting markets remain skeptical about the model's sustainability.

The public market journey illustrates a fundamental tension: markets want growth and returns, but Ujjivan's mission requires patience and social commitment. Every quarter, analysts ask about fee income growth and cost ratios. But behind these metrics are decisions about whether to serve a remote village that will never be profitable, or whether to forgive loans to flood victims who lost everything. The public market demands efficiency; financial inclusion demands empathy. Navigating both simultaneously would prove to be Ujjivan's greatest challenge.

V. The COVID Crisis & Near-Death Experience (2020-2022)

March 24, 2020, 8 PM. Prime Minister Modi announced a nationwide lockdown with four hours' notice. For most banks, this meant closing branches and shifting to digital channels. For Ujjivan, it meant 68% of their loan book—₹11,000 crore lent to street vendors, daily wage earners, and small shopkeepers—had just become uncollectable. Not difficult to collect. Not stressed. Uncollectable. Their customers had zero income.

The pre-COVID position had seemed robust. Gross NPAs at 2.5%, provision coverage at 65%, capital adequacy at 19%. The loan book was growing 20% annually, margins were healthy, and the stock was trading at 1.5x book value. Management had guided for 25% ROE by 2022. Those projections now seemed like fantasy.

The first collection day after lockdown was April 7, 2020. Of ₹150 crore due that day, Ujjivan collected ₹3 crore—a 98% drop. Field officers couldn't reach customers—movement was restricted, public transport shut down. Even when they could reach customers, there was nothing to collect. The flower seller had no temple visitors. The vegetable vendor had no market. The rickshaw puller had no passengers. The entire informal economy had simply stopped.

By May 2020, the situation was catastrophic. Collections had improved marginally to 20% of pre-COVID levels, but that meant 80% of dues were unpaid. Under normal circumstances, a 30-day default triggered NPA classification. The RBI provided temporary relief through moratoriums, but Ujjivan's management knew this was just delaying the inevitable. When moratoriums ended, NPAs would explode.

The human crisis was even worse than the financial one. Field officers reported customers selling jewelry to buy food, families surviving on one meal a day, children dropping out of school to work. The same communities Ujjivan had spent 15 years lifting from poverty were sliding back. The bitter irony wasn't lost on anyone—the bank built to provide financial inclusion was watching its customers face financial extinction.

Internal modeling suggested disaster. If collections remained at 20% for six months, NPAs would hit 35%, requiring ₹4,000 crore in provisions—more than the bank's entire net worth. Even the optimistic scenario of 50% collections meant NPAs of 15%, requiring provisions that would wipe out three years of profits. The bank that had never posted a quarterly loss was staring at potential insolvency.

The board meetings during this period were exercises in crisis management. Eight board members resigned in nine months—some citing personal reasons, others clearly losing faith in the model's viability. The CEO, Nitin Chugh, who'd joined just before COVID, faced an impossible situation: cut costs aggressively and abandon customers when they needed support most, or maintain operations and risk running out of capital.

The strategy that emerged was pragmatic desperation. First, preserve capital at all costs. New loan disbursements dropped to near zero. The bank stopped all expansion, froze hiring, cut marketing spending by 80%. Second, restructure everything possible. Using RBI's COVID restructuring framework, Ujjivan restructured ₹3,000 crore of loans, essentially admitting these customers couldn't pay on original terms. Third, pivot the business model entirely.

The pivot was dramatic. From 68% unsecured lending (microfinance) pre-COVID, Ujjivan shifted aggressively toward secured lending. Housing loans, which were 15% of the book, became the priority. Gold loans, which Ujjivan had never offered, were launched in 2022. Vehicle loans, stopped during COVID, were restarted with stricter underwriting. The bank that built its reputation on unsecured group lending was becoming a secured retail lender.

By December 2021, NPAs had peaked at 11.8%—not the 35% doomsday scenario, but devastating nonetheless. The improvement came from unexpected resilience. As lockdowns eased, customers prioritized loan repayment even over household expenses. The social collateral of group lending—peer pressure and community standing—proved stronger than anyone expected. Women's groups would pool resources to prevent any member from defaulting.

The financial hit was severe but survivable. Q4 FY22 saw write-offs of ₹200 crore, the largest in Ujjivan's history. Total provisions exceeded ₹1,000 crore over two years. The bank posted its first annual loss in FY21. Market capitalization fell below book value, implying investors thought the bank was worth more dead than alive.

But Q4 FY22 marked the turning point—the first profitable quarter after six consecutive losses. Collections had recovered to 95% of pre-COVID levels. New disbursements were growing again, though now 60% secured versus 30% pre-COVID. The bank had survived, but it was fundamentally transformed.

The COVID crisis revealed uncomfortable truths about microfinance. The model worked brilliantly when customers had steady informal income, but any systemic shock to the informal economy was potentially fatal. The high margins that attracted investors were necessary because the risks were genuinely high. And most troublingly, the customers who most needed financial inclusion were also most vulnerable to economic disruption.

Management drew hard lessons. Concentration risk in unsecured lending was existential. Geographic diversification didn't matter when the entire informal economy shut down simultaneously. Technology adoption, forced by lockdown, proved customers could use digital channels when necessary. Most importantly, survival required abandoning dogma—the bank built for unsecured microfinance had to become something else to live.

The near-death experience changed Ujjivan's DNA. The missionary zeal of financial inclusion remained, but tempered by commercial pragmatism. The bank that emerged from COVID was more diversified, more digital, more conservative—and perhaps less true to its original mission. Whether this transformation was evolution or betrayal would depend on what Ujjivan did with its second chance.

VI. The Business Model Evolution

The Ujjivan that emerged from COVID bore little resemblance to its pre-pandemic incarnation. Where once stood a focused microfinance institution with 68% unsecured lending, now stood a diversified small finance bank juggling six distinct business lines, each with its own economics, risks, and customer segments. This wasn't evolution—it was metamorphosis under extreme pressure.

The microfinance business, once Ujjivan's crown jewel, had become its problem child. The portfolio shrank from ₹11,000 crore to ₹8,000 crore, and management guided for it to stabilize at 50% of total lending versus the previous 68%. But the changes went deeper than just proportion. Average ticket sizes increased from ₹30,000 to ₹45,000—partly inflation, partly deliberate strategy to serve slightly better-off customers who'd proven more resilient. The joint liability group model remained, but with modifications: smaller groups (5-8 women versus 15-20), shorter tenures (12 months versus 24), and stricter geographic concentration limits.

The economics had also shifted. Pre-COVID, microfinance loans yielded 22-24% with 2% credit costs, delivering 20% pre-tax returns. Post-COVID, yields dropped to 19-21% (regulatory pressure and competition), credit costs normalized at 4-5%, delivering 14-15% returns—still attractive, but no longer spectacular. The high-touch model became higher-tech: tablets replaced paper, WhatsApp groups supplemented physical meetings, and digital collections grew from 5% to 35%.

Housing finance emerged as the surprise winner. From ₹2,000 crore pre-COVID, the portfolio exploded to ₹5,500 crore by 2024. These weren't traditional home loans but affordable housing finance—₹5-10 lakh loans for semi-urban property purchase or construction. The customer remained similar (household income ₹25,000-40,000 monthly) but the risk profile was transformed. Secured by property, even if informal, these loans showed 0.5% NPAs versus 5% for microfinance.

The origination process for housing loans revealed Ujjivan's competitive advantage: deep community presence. Traditional banks required formal income proof, property documents, and complex paperwork. Ujjivan's field officers knew which properties had clear title, which customers had stable informal income, which construction was genuine versus speculative. They'd conduct site visits, verify construction progress, and release funds in tranches—labor-intensive but effective.

The gold loan launch in 2022 was pure opportunism. As COVID ravaged household finances, gold became the asset of last resort. Ujjivan saw opportunity: instant liquidity for customers, secured lending for the bank. Within 18 months, the gold loan book reached ₹1,200 crore. The economics were attractive—12-15% yields, near-zero credit losses, 3-month average tenure allowing rapid redeployment. But it also highlighted strategy drift: was a small finance bank meant to do pawnbroking?

Vehicle finance, restarted post-COVID, focused on commercial vehicles—three-wheelers, small goods carriers, tractors. The logic was compelling: these were productive assets generating income to service loans. But execution proved challenging. Unlike microfinance where Ujjivan had 15 years' experience, vehicle finance required new capabilities: asset valuation, repossession networks, secondary market understanding. Early NPAs hit 7%, forcing management to slow growth and tighten underwriting.

The MSME and agriculture portfolio remained subscale despite regulatory requirements. Small finance banks must lend 10% to micro enterprises and 10% to small farmers. Ujjivan struggled with both. MSMEs wanted larger tickets and working capital facilities the bank couldn't provide. Small farmers were even harder—seasonal income, weather dependence, and political interference (loan waivers) made it structurally challenging. These portfolios existed more for compliance than commercial logic.

Digital transformation, forced by COVID, became permanent. The bank offered internet banking, phone banking and mobile banking facilities. The mobile app, available in five languages, saw monthly active users grow from 100,000 to 2 million. But digital adoption varied dramatically by product. Savings account customers embraced digital channels—70% used mobile banking monthly. Microfinance customers remained analog—only 20% ever logged into digital channels, preferring human interaction for loan-related activities.

The branch network strategy also evolved. Pre-COVID, Ujjivan opened 50-70 branches annually in rural and semi-urban areas. Post-COVID, new branches were selective—urban locations for deposit gathering, rural only where digital couldn't reach. The 752-branch network was optimized rather than expanded. Branches in metros became deposit-focused, offering premium savings products. Rural branches remained lending-focused but with smaller staff, supplemented by roving field officers.

By February 2018, Ujjivan served over 3.7 million customers, and this grew to 9.5 million by 2025. But composition changed dramatically. Pre-COVID, 80% were borrowers, 20% depositors. By 2024, it was 60% borrowers, 40% depositors. The depositor growth came from urban areas where Ujjivan offered competitive rates—7.25% for savings accounts versus 3-4% at large banks. These deposits funded lending, reducing dependence on wholesale borrowing.

The business model evolution raised fundamental questions. Was Ujjivan still a microfinance institution that happened to have a banking license? Or had it become a small bank that happened to do microfinance? The answer mattered for strategy, valuation, and mission. Management insisted the core purpose remained financial inclusion, but the portfolio composition suggested otherwise. The secured lending pivot improved asset quality and profitability but served relatively better-off customers.

The tension played out in product design. Should Ujjivan offer credit cards? Technically capable but philosophically questionable—credit cards could trap vulnerable customers in debt. Should they do corporate lending? The universal banking application suggested yes, but did they have capabilities? Should they acquire fintech partnerships? Digital lenders offered reach and technology, but their aggressive collection practices conflicted with Ujjivan's community-based approach.

What emerged was neither pure microfinance nor traditional banking but something uniquely Indian: a mass-market bank serving the lower-middle pyramid through a combination of high-touch relationship banking and selective digital adoption. Whether this hybrid model was sustainable or simply a transitional phase toward becoming another generic bank remained the central strategic question.

VII. The Universal Banking Quest (2024-Present)

On February 4, 2025, Ujjivan Small Finance Bank submitted its application to the Reserve Bank of India for a universal banking license. The Bengaluru-based lender became the second SFB after AU SFB to apply for a universal banking license under the voluntary transition route. The moment represented eight years of methodical preparation since becoming a bank, and potentially the final transformation in Ujjivan's remarkable journey from microfinance to mainstream banking.

The quest for universal status wasn't vanity—it was strategic necessity. Small finance banks operate under significant restrictions: 75% priority sector lending requirements, limits on single borrower exposure, constraints on branch expansion in urban areas. These made sense for financial inclusion but increasingly constrained Ujjivan's growth ambitions. As management explained to analysts, they'd reached the limits of what could be achieved within the SFB framework.

To secure a universal banking license, Ujjivan SFB had to fulfill various conditions, such as being listed on a recognized stock exchange, having a net worth of at least ₹1,000 crore, and meeting capital requirements. The bank was also required to demonstrate profitability over the past two years and ensure its gross and net non-performing asset ratios were within stipulated thresholds. By early 2024, Ujjivan had checked every box: listed since 2019, net worth exceeding ₹3,000 crore, profitable post-COVID, and NPAs under control.

The competitive landscape added urgency. Among the existing SFBs, only AU SFB and Ujjivan Small Finance Bank currently met the eligibility criteria for conversion. AU Small Finance Bank had already applied in September 2024, potentially gaining first-mover advantage in the universal banking space. Jana Small Finance Bank was preparing to apply once eligible. The window for differentiation was closing rapidly.

What would change with universal status? Everything and nothing. The core customer base would remain—Ujjivan couldn't abandon the communities that built it. But the product suite would explode. Corporate lending, currently prohibited, could provide higher-ticket, lower-cost growth. International banking, forex services, and sophisticated treasury operations would become possible. Most importantly, the priority sector lending requirement would drop from 75% to 40%, freeing capital for more profitable segments.

The strategic implications were profound. Universal banks compete on scale, technology, and product breadth—areas where Ujjivan lagged established players. HDFC Bank had 7,000+ branches and ₹20 lakh crore in assets; Ujjivan had 750 branches and ₹30,000 crore. The David versus Goliath metaphor was inadequate—this was more like a corner shop competing with a hypermarket.

But Ujjivan's leadership saw opportunity in the gaps. India's corporate lending was dominated by a handful of banks, leaving mid-sized companies underserved. The MSME segment, despite government focus, remained credit-starved. Even in retail, products like wealth management and insurance were underpenetrated outside metros. A universal Ujjivan could be the bridge between large banks that ignored smaller customers and small banks that couldn't serve larger ones.

The regulatory perspective added complexity. RBI's stance on SFB-to-universal conversion remained opaque. While guidelines existed, no small finance bank had successfully completed the transition. Bandhan Bank, which started as a microfinance company and became a universal bank directly, provided the only precedent—but through a different route. The RBI would scrutinize not just financial metrics but strategic intent: would Ujjivan remain committed to financial inclusion, or would universal status mean abandoning its founding mission?

Internal preparations for universal banking had begun years earlier. The technology stack was upgraded to handle corporate banking complexity. Risk management systems were enhanced to evaluate larger exposures. Talent was recruited from established banks—a head of corporate banking from ICICI, a treasury head from Standard Chartered. These weren't just hires; they were capability transplants, bringing DNA Ujjivan had never possessed.

The cultural challenge was equally significant. Ujjivan's 20,000 employees were trained for high-touch, community-based banking. Universal banking required different skills: relationship managers who could discuss working capital with CFOs, product specialists who understood derivatives, technology teams capable of building corporate internet banking platforms. The transformation wasn't just regulatory—it was organizational metamorphosis.

Market reaction to the universal banking application was mixed. The stock rose 5% on announcement day, suggesting investor optimism about growth potential. But analysts remained cautious. Universal banking meant higher capital requirements, increased competition, and execution risk. The consensus view: right direction, uncertain destination.

As CEO Sanjeev Nautiyal stated, "The Bank has consistently demonstrated strong financial performance and a commitment to financial inclusion, serving a diverse customer base across the country. Securing the universal banking licence, if approved, will strengthen Ujjivan's efforts to provide holistic financial services".

The timeline remained uncertain. RBI's review could take 6-18 months. Even approval would come with conditions—capital raising requirements, business plan commitments, possible restrictions during transition. The universal banking quest represented not an end but another beginning, the next phase in Ujjivan's perpetual transformation.

VIII. Financial Performance & Unit Economics

The numbers tell two different stories about Ujjivan. The first is a high-margin, fast-growing financial services company with industry-leading returns. The second is a volatile, high-risk lender whose economics work until they catastrophically don't. Both stories are true, which makes Ujjivan simultaneously attractive and terrifying to investors.

Start with the revenue model. Ujjivan generates income from three sources: net interest income (85% of revenue), fee income (10%), and other income (5%). The net interest margins of 8-9% are among India's highest—compare that to HDFC Bank at 4.5% or SBI at 3.5%. These margins exist because Ujjivan operates in a different universe: lending at 19-24% to customers banks won't touch, funded by deposits at 6-7% from urban savers seeking higher returns.

The lending rate breakdown reveals the economics. Microfinance loans yield 19-21% (down from 24% pre-COVID due to regulatory caps). Housing loans yield 11-13%. Vehicle loans 14-16%. Gold loans 12-14%. The blended yield on advances is approximately 16%, which sounds usurious until you understand the cost structure required to serve these segments.

Cost of funds has been Ujjivan's hidden advantage. As an NBFC, they borrowed at 10-12%. As a bank, they gather deposits at 6-7%. Current and savings account deposits (CASA) are 27% of total deposits—not great by universal bank standards (HDFC at 45%) but improving steadily. The cost of funds at 6.8% gives them a raw spread of 9%+ before operating costs and provisions.

Operating costs are where the model gets challenging. The cost-to-income ratio hovers around 65-70%, compared to 40-45% for efficient private banks. This isn't inefficiency—it's the reality of high-touch banking. Each field officer manages 400-500 clients, visiting them weekly. Branch staff work extended hours to accommodate customers who can only visit after work. The technology infrastructure must support multiple languages and offline functionality. Financial literacy programs, a regulatory requirement and business necessity, add cost without direct revenue.

Asset quality has been a rollercoaster. Pre-COVID gross NPAs were 2.5%, impressive for unsecured lending. COVID peaked at 11.8%, existential crisis territory. Current gross NPAs at 2.5% suggest full recovery, but the underlying volatility remains. The provision coverage ratio at 92% with ₹260 crore floating provisions suggests management expects future stress—prudent or pessimistic depending on your view.

The provision expense line item tells the real story. In good years (FY18-19), credit costs were 2% of assets. During COVID (FY21-22), they spiked to 8-9%. Current credit costs at 3-4% are neither the best nor worst case—they're the normalized reality of lending to vulnerable segments. This volatility makes earnings inherently unpredictable.

Fee income remains underdeveloped at 10% of revenue versus 20-25% for universal banks. The sources are limited: processing fees on loans, account maintenance charges (politically sensitive given the customer base), and nascent insurance distribution. The universal banking transition partly aims to address this—corporate banking generates substantial fee income from cash management, trade finance, and advisory services.

Profitability metrics swing wildly with asset quality cycles. Return on assets ranged from 2.5% (pre-COVID) to -2% (COVID trough) to 1.5% (current). Return on equity showed similar volatility: 20% to -15% to 12%. The through-cycle ROE is probably 12-15%, attractive but not spectacular considering the risks.

Capital adequacy at 22% seems robust, but context matters. Unsecured microfinance lending requires higher capital buffers—RBI might impose additional requirements anytime. Growth consumes capital rapidly; 20% loan growth requires 2-3% annual capital accretion just to maintain ratios. The universal banking transition might require additional capital to fund new businesses.

The unit economics of different products vary dramatically. A ₹30,000 microfinance loan generates ₹6,000 annual interest, costs ₹3,000 to originate and service, faces ₹1,000 expected credit loss, and yields ₹2,000 pre-tax profit—great when multiplied by millions, devastating when credit losses double. A ₹10 lakh housing loan generates ₹120,000 annual interest, costs ₹20,000 to originate and service, faces minimal credit loss, and yields ₹100,000 pre-tax profit—but Ujjivan can only do thousands, not millions of these.

Digital initiatives promise to improve economics but haven't yet delivered. Digital origination reduces costs 30% but works for only 20% of customers. Digital collections save field officer time but reduce the personal touch that ensures repayment. The mobile app has 2 million users but generates minimal revenue. The digital transformation is necessary but not sufficient—the core business remains stubbornly physical.

Comparative analysis with peers reveals Ujjivan's unique position. Among small finance banks, it has the highest NIMs but also highest operating costs. Compared to microfinance institutions, it has lower yields but better funding costs. Against universal banks, it's a high-risk, high-return outlier. There's no perfect comparable because there's no business quite like Ujjivan.

The investment case reduces to a fundamental question: are these economics sustainable? Bulls argue the margins reflect genuine value creation in underserved segments. Bears see unsustainable returns that will compress as competition increases and regulation tightens. The truth, as usual, lies somewhere between—the economics work until the next crisis reveals they don't.

IX. Playbook: Lessons in Financial Inclusion

After two decades and multiple near-death experiences, Ujjivan has inadvertently written the playbook for financial inclusion in emerging markets. These aren't theoretical frameworks from business schools but hard-won lessons from serving 9.5 million customers who banks traditionally won't touch.

Lesson 1: Trust is the only real collateral. When Ujjivan lends ₹30,000 to a vegetable vendor with no assets, no credit history, and informal income, what exactly secures that loan? It's not legal enforcement—trying to recover ₹30,000 through courts would cost more than the principal. It's not financial incentive—the customer could default and borrow from moneylenders tomorrow. It's trust, carefully cultivated through years of predictable interaction. Ujjivan discovered that trust scales differently than technology: slowly, locally, and through human relationships.

Lesson 2: Social collateral beats financial collateral—until it doesn't. The joint liability group model works through peer pressure. When five women guarantee each other's loans, default means social ostracism. This worked brilliantly for 15 years, achieving 98% repayment rates that seemed to defy financial gravity. Then COVID hit, and entire groups had no income simultaneously. Social collateral works in idiosyncratic crises (one member's husband falls ill) but fails in systemic ones (everyone loses income together). The lesson: diversification must happen above the group level.

Lesson 3: High-frequency, small-ticket transactions require different economics. Traditional banking assumes customers visit monthly, transact in thousands, and self-serve digitally. Ujjivan's customers visit weekly, transact in hundreds, and need assisted service. This requires 5x the touch points of normal banking. The only way to make this profitable is through density—300 customers within walking distance of each field officer, 50 groups meeting at the same location, shared costs across multiple products. Geography is destiny in microfinance.

Lesson 4: Technology adoption follows trust, not the reverse. Ujjivan spent millions building digital channels, assuming customers would embrace the convenience. Adoption remained below 30% for years. Then COVID forced digital interaction, and adoption jumped to 70%—but only for customers who'd been with Ujjivan for years. New customers still required face-to-face onboarding. The pattern was clear: establish trust physically, then migrate to digital. Silicon Valley's "digital-first" doesn't work when your customer has never used an ATM.

Lesson 5: Financial literacy is a product, not a feature. Banks treat financial literacy as corporate social responsibility—occasional workshops, token efforts. Ujjivan learned it's core to the business model. A customer who understands compound interest borrows responsibly. One who can read a bank statement catches errors. One who knows their rights doesn't fall for predatory alternatives. Ujjivan spends ₹50 crore annually on financial literacy—not charity but customer acquisition cost.

Lesson 6: Crisis management in inclusive finance means choosing whom to save. When COVID hit, Ujjivan faced an impossible choice: attempt to collect from devastated customers and survive, or provide relief and risk insolvency. They chose a middle path—aggressive collection from customers with capacity, complete forbearance for the devastated, and restructuring for everyone else. This segmented approach saved the bank but revealed an uncomfortable truth: financial inclusion means accepting that some customers will pull others down in a crisis.

Lesson 7: The mission-profit tension is permanent, not solvable. Every strategic decision at Ujjivan involves trade-offs between social impact and financial returns. Serve a remote village (mission-aligned) or focus on semi-urban areas (profitable)? Forgive loans during floods (compassionate) or enforce collections (sustainable)? Maintain high-touch service (effective) or digitize aggressively (efficient)? The tension can be managed but never resolved. Pretending otherwise leads to either mission drift or financial failure.

Lesson 8: Regulation shapes reality more than strategy. Ujjivan's evolution from NBFC to small finance bank to universal bank aspirant wasn't primarily strategic choice—it was regulatory adaptation. Interest rate caps determine pricing. Priority sector requirements determine customer mix. Capital requirements determine growth rates. In regulated industries serving vulnerable populations, strategy is largely about optimizing within regulatory constraints rather than blue-sky thinking.

Lesson 9: Competition from digital lending is both threat and opportunity. Digital lenders can approve loans in minutes while Ujjivan takes days. They can serve customers remotely while Ujjivan requires physical presence. But they also charge 36%+ interest, use aggressive collection practices, and create debt traps. Ujjivan's value proposition shifted from "we'll give you credit" to "we'll give you responsible credit." In a market flooded with predatory options, being the boring, reliable choice became competitive advantage.

Lesson 10: Public market expectations and social missions require careful translation. When Ujjivan went public, analysts wanted to discuss cost-to-income ratios and ROE targets. Management wanted to discuss villages covered and lives impacted. The earnings calls became exercises in translation—explaining why serving a tea stall owner with a ₹20,000 loan was strategically smart, not just socially worthy. The companies that succeed in inclusive finance learn to tell both stories simultaneously without losing credibility with either audience.

The metalesson from Ujjivan's journey is that financial inclusion at scale requires accepting paradoxes rather than resolving them. You must be both commercial and social, both high-touch and high-tech, both standardized and flexible. The organizations that fail in this space are usually those that lean too heavily in one direction—pure social mission (unsustainable) or pure commercial focus (mission drift).

X. Competition & Market Dynamics

The small finance bank sector in India is less a market than a laboratory—ten institutions simultaneously experimenting with different models of inclusive banking, watched closely by regulators, investors, and increasingly, Big Tech. Understanding Ujjivan requires understanding this competitive ecosystem where everyone is both rival and fellow traveler.

AU Small Finance Bank represents the opposite end of the spectrum. Started as a vehicle finance company in Rajasthan, AU focused on secured lending to slightly better-off customers from day one. Their gross NPAs never exceeded 5% even during COVID. They were first to apply for universal banking. With ₹90,000 crore in assets versus Ujjivan's ₹30,000 crore, AU proves that starting higher up the economic pyramid accelerates growth. But they serve 3 million customers versus Ujjivan's 9.5 million—scale versus impact, the eternal trade-off.

Equitas Small Finance Bank mirrors Ujjivan's journey—microfinance origins, Chennai-based, similar customer segments. But Equitas diversified earlier, with microfinance now below 20% of their book versus Ujjivan's 50%. Their COVID experience was less traumatic, validating the diversification strategy. Yet their NIMs at 7% lag Ujjivan's 8-9%, suggesting diversification comes at a profitability cost. The question: is lower risk worth lower returns?

Suryoday Small Finance Bank represents the cautionary tale. Also microfinance-originated, they struggled with asset quality even pre-COVID, saw NPAs spike to 15% during pandemic, and barely survived. Their stock trades at 0.3x book value—the market essentially values them as zombies. The lesson: in inclusive finance, the difference between success and failure is often just slightly better execution or timing.

ESAF and Utkarsh Small Finance Banks focused on specific geographies—Kerala and Uttar Pradesh respectively. This concentration strategy provided deep local knowledge but increased vulnerability to regional shocks. When Kerala faced floods or UP saw political turmoil, these banks suffered disproportionately. Geographic diversification, expensive and complex as it is, proved its value during systemic crises.

The threat from established banks is intensifying. HDFC Bank launched "Sustainable Livelihood Initiative," targeting the same customers as Ujjivan but with vastly superior resources. ICICI Bank's business correspondent model reaches 500,000 villages. SBI's financial inclusion initiatives dwarf the entire small finance bank sector. These banks treat microfinance as corporate social responsibility or regulatory obligation rather than core business, but their scale alone makes them formidable.

Digital lending apps represent the new-age disruption. Companies like MoneyTap, CASHe, and PaySense approve loans in minutes using alternative data—mobile usage patterns, social media behavior, digital transaction history. They charge higher rates (30-40% versus Ujjivan's 20%) but offer unmatched convenience. For young, urban, digitally-savvy customers, these apps are becoming the first choice, forcing Ujjivan to compete on dimensions beyond just access to credit.

The most intriguing competition comes from non-lending players. Paytm Payments Bank can't lend but reaches 300 million users with savings and payment products. WhatsApp Pay could theoretically add lending tomorrow to 500 million Indian users. These platforms have customer relationships and data that dwarf traditional lenders. If regulation permits them to lend, the entire competitive landscape changes overnight.

Microfinance institutions remain relevant competitors despite Ujjivan's banking transformation. Bandhan Bank (the successful precedent), Arohan Financial Services, Fusion Microfinance—these players compete for the same customers, often in the same villages. The competitive intensity in some districts is absurd—five different lenders chasing the same vegetable vendor, creating over-indebtedness that threatens everyone's asset quality.

The market dynamics are shaped by three secular trends. First, formalization of the economy post-demonetization and GST means more customers have documented income, making them attractive to traditional banks. Second, digital public infrastructure (Aadhaar, UPI, Account Aggregator) is democratizing access to financial services. Third, regulatory tightening post-COVID is increasing compliance costs and forcing consolidation.

Market share analysis reveals uncomfortable truths. Small finance banks collectively have less than 2% of Indian banking assets. In microfinance specifically, despite being the largest SFB player, Ujjivan has only 8% market share. The fragmentation means no player has real pricing power—customers can easily switch lenders, keeping margins under pressure.

The competitive positioning question for Ujjivan is existential: what's the sustainable differentiation? It's not technology—Big Tech will always be superior. It's not scale—established banks are 10x larger. It's not just relationships—digital lenders are proving those can be built virtually. The answer might be the unique combination: tech-enabled relationship banking for customers graduating from poverty to lower-middle class. But whether this positioning is defensible remains uncertain.

Regional dynamics add complexity. In South India, Ujjivan faces intense competition from established players and high digital adoption. In North and East India, the opportunity is greater but operations are harder and risks higher. The strategic choice—double down on strongholds or expand into virgin territories—has no clear answer.

The competitive endgame likely involves consolidation. Ten small finance banks serving similar segments with similar models isn't sustainable. Either some will fail (as Suryoday nearly did), or merge (as AU and Fincare are doing), or get acquired by larger banks seeking quick financial inclusion credibility. Ujjivan's universal banking quest is partly about avoiding becoming an acquisition target by becoming too large to easily absorb.

XI. Bear vs. Bull Case

The investment debate around Ujjivan is unusually polarized, with bulls seeing a demographic megatrend play and bears seeing a house of cards awaiting the next crisis. Both sides marshal compelling evidence, making this one of the most interesting and contentious stories in Indian finance.

The Bull Case:

India's financial inclusion gap represents one of the world's largest addressable markets. With 200 million adults still unbanked and 500 million underbanked, the runway for growth extends decades. Ujjivan, with its proven execution capability and established brand in underserved communities, is perfectly positioned to capture this opportunity. The demographics are destiny argument: as India's per-capita income doubles from $2,500 to $5,000 over the next decade, millions will graduate from informal to formal finance, and Ujjivan will be their bridge.

The universal banking license, once obtained, changes everything. Removal of lending restrictions, ability to serve corporate clients, and reduced priority sector requirements will unleash growth while improving risk diversification. Think of it as Ujjivan graduating from non-profit-like constraints to full commercial freedom. The precedent of Bandhan Bank, which saw its valuation triple post-universal license, provides the template.

The competitive moat is deeper than it appears. While anyone can lend money, few can profitably serve customers earning ₹10,000 monthly. Ujjivan's community relationships, built over two decades, can't be replicated by technology or capital alone. Their 20,000 field officers represent human infrastructure that would take competitors years and billions to build. In financial inclusion, distribution still beats product.

Digital adoption is hitting inflection point. With 70% of customers now digitally active, the cost-to-serve is plummeting while maintaining the high-yield asset base. Operating leverage will drive ROE from current 12% to 20%+ as digital transactions replace physical touches. The combination of high margins and declining costs creates explosive earnings potential.

Asset quality concerns are overblown. Yes, COVID was traumatic, but Ujjivan survived a black swan event that should have killed it. The post-COVID portfolio is battle-tested, risk management strengthened, and provision buffers robust. The shift to secured lending (50% of book versus 30% pre-COVID) structurally reduces risk while maintaining attractive yields.

Valuation at 0.8x book value is absurdly cheap for a bank growing at 20% with 9% NIMs. Comparable financial inclusion players globally trade at 2-3x book. Even stressed Indian PSU banks trade at 1x book. The market is pricing in another COVID-like crisis which is extremely unlikely. Mean reversion alone could drive 100% returns.

The Bear Case:

The customer base vulnerability isn't fixable—it's structural. Ujjivan's borrowers are daily wage earners, street vendors, and micro-entrepreneurs who operate in the informal economy. Any economic shock—pandemic, demonetization, climate events—devastates their income instantly. COVID wasn't a black swan; it was a preview of inherent fragility. The next crisis might come from climate change, political upheaval, or technology disruption of informal jobs.

Regulatory risk is existential and unpredictable. Microfinance in India faces constant political pressure—loan waivers, interest rate caps, collection practice restrictions. The Andhra Pradesh microfinance crisis of 2010 destroyed an entire industry overnight through regulatory action. Similar risks persist in every state where populist politics meets indebted voters. One adverse regulation could crater the business model.

Competition is intensifying from every direction. Big Tech will eventually crack lending to the masses—when they do, Ujjivan's relationship moat evaporates. Traditional banks are moving down-market with superior technology and unlimited capital. Digital lenders are moving up-market with better user experience. Ujjivan is caught in a vice with no clear escape route.

The economics are deteriorating, not improving. NIMs compressed from 10% to 9% and will continue falling as competition increases. Operating costs remain stubbornly high despite digital initiatives. Credit costs normalized at 4% are optimistic—the next crisis could easily push them to 8-10%. The ROE story requires everything going right, which never happens in financial services.

Execution risk in universal banking transition is massive. Ujjivan has zero experience in corporate banking, limited treasury capabilities, and no investment banking DNA. They're competing against institutions with decades of experience and established relationships. The capital required to build these businesses will dilute returns for years. Bandhan's success isn't replicable—they had first-mover advantage Ujjivan lacks.

The stock is a value trap, not a value play. It's traded below book value for three years for good reason—the market doesn't believe the book value is real. One crisis could necessitate write-offs that eliminate half the net worth. Low valuation reflects appropriate skepticism about sustainability, not market inefficiency.

Management quality remains uncertain. The founder CEO left, the COVID-era CEO struggled, and current leadership hasn't been tested through a full cycle. The board exodus during COVID raises governance concerns. The cultural challenge of transforming from social mission to commercial banking while maintaining both is perhaps impossible.

The Verdict:

The bull-bear debate ultimately reduces to timeframe and risk tolerance. Over 10 years, India's financial inclusion story seems inevitable and Ujjivan well-positioned to benefit. Over 10 months, anything could happen—regulatory changes, competitive disruption, economic shocks. The asymmetry is clear: enormous upside if everything works, total destruction if key assumptions break.

For fundamental investors, Ujjivan represents a fascinating study in transformation risk. It's simultaneously a demographic play, a regulatory bet, a digital transformation story, and a social impact investment. The inability to cleanly categorize it explains both the opportunity and the danger.

XII. Future Scenarios & Closing Thoughts

As we look toward Ujjivan's next chapter, three scenarios seem plausible, each with roughly equal probability—a reminder that in emerging market finance, the future is genuinely uncertain rather than merely unknown.

Scenario 1: The Graduation Story (35% probability) Ujjivan successfully obtains universal banking license by mid-2025, executes a smooth transition to diversified banking, and emerges as India's leading mass-market bank. The customer base gradually moves up the economic ladder, borrowing for homes instead of working capital, saving for children's education instead of emergencies. By 2030, Ujjivan has 20 million customers, ₹100,000 crore in assets, and trades at 2x book value. The microfinance origins become historical footnote as Ujjivan competes directly with HDFC and ICICI for the great Indian middle class. This is management's vision and the bull case foundation.

Scenario 2: The Perpetual Transition (40% probability) Universal banking approval comes with extensive conditions, forcing Ujjivan to maintain significant financial inclusion commitments. The bank becomes stuck in the middle—too large and regulated to maintain microfinance economics, too small and specialized to compete in universal banking. Growth slows to 10-12% annually, ROE stabilizes at 10-12%, and the stock perpetually trades at 0.8-1x book value. Ujjivan becomes a profitable but unexciting utility, serving a necessary function without spectacular returns. It survives but never thrives, caught between two worlds.

Scenario 3: The Disruption Scenario (25% probability) A combination of Big Tech entry, regulatory tightening, and economic shock creates an existential crisis. WhatsApp launches lending services that instantly reach 500 million Indians. RBI caps microfinance rates at 15%, destroying margins. Another pandemic-like event pushes NPAs to 20%. Ujjivan requires emergency capital, diluting existing shareholders by 50%. The bank survives but as a shadow of its former self, eventually acquired by a larger institution seeking a financial inclusion subsidiary. The social mission continues but shareholder value is destroyed.

The next five years will likely determine which scenario plays out. Key markers to watch: RBI's decision on universal banking (expected by December 2025), success in corporate banking build-out (measurable by 2026), digital adoption reaching 80%+ (critical for cost reduction), and most importantly, whether India's informal economy formalizes as predicted or remains stubbornly cash-based and vulnerable.

The technological wild cards could change everything overnight. If India's Account Aggregator framework enables instant, accurate credit assessment of informal sector workers, Ujjivan's field officer model becomes obsolete. If Central Bank Digital Currency replaces cash, the entire microfinance collection infrastructure needs reimagining. If artificial intelligence can predict loan defaults better than community knowledge, the relationship banking moat evaporates.

India's digital public infrastructure—Aadhaar, UPI, DigiLocker—represents both opportunity and threat. These tools could enable Ujjivan to serve customers at radically lower cost, or they could enable Big Tech to bypass Ujjivan entirely. The critical question: does financial inclusion require human touch or just financial access? Ujjivan is betting on the former, but evidence increasingly supports the latter.

The macro environment adds another layer of complexity. India's demographic dividend could drive sustained growth, or climate change could create perpetual crisis in rural areas. Political stability could enable long-term planning, or populist pressures could trigger loan waivers and interest rate caps. The formal economy could absorb informal workers, or automation could destroy their livelihoods entirely.

Final Reflections:

Ujjivan's story matters beyond its investment merits because it represents a grand experiment in capitalism with a conscience. Can you build a large, profitable, publicly-traded company whose primary purpose is serving people traditional capitalism ignores? The answer remains frustratingly ambiguous.

The successes are undeniable. Ujjivan has brought 9.5 million people into formal finance, enabled hundreds of thousands of small businesses, and proven that the poor are bankable. They've survived crises that should have been fatal, adapted to regulations that seemed impossible, and maintained focus on mission despite market pressures. This alone is remarkable.

But the contradictions are equally clear. The highest margins come from the most vulnerable customers. Growth requires expanding beyond the original mission. Public markets demand quarterly performance from businesses with decade-long development cycles. Every strategic choice involves compromising either commercial success or social impact.

For founders considering similar ventures, Ujjivan offers sobering lessons. Mission-driven businesses in regulated industries face constraints that pure commercial or pure social enterprises avoid. The talent required—equally comfortable in village meetings and board rooms—is scarce. The capital needed—patient enough for social returns, demanding enough for financial returns—is limited. Most challenging, success changes the very communities you serve, potentially eliminating your market.

For investors, Ujjivan presents a fascinating puzzle. The fundamentals suggest deep value, but the risks are genuinely existential. It's a leveraged bet on India's development trajectory, regulatory evolution, and the resilience of informal economy workers. The asymmetry is extreme—potential multi-bagger returns or complete capital loss, with limited middle ground.

The broader lesson might be that financial inclusion as a business model remains unproven at scale. Grameen Bank required constant donor support. Kenya's M-Pesa succeeded through mobile money, not credit. China's Ant Financial was curtailed by regulators. Ujjivan's attempt to square this circle through universal banking is audacious, necessary, and uncertain.

Perhaps the most important insight from Ujjivan's journey is that financial inclusion isn't a problem to be solved but a condition to be constantly managed. The poor will always exist in some form, their needs will constantly evolve, and serving them profitably will remain challenging. Companies like Ujjivan don't eliminate poverty; they make it more bearable and escapable for some.

As we conclude this analysis, Ujjivan stands at its most pivotal moment since inception. The universal banking decision will determine whether it becomes a mainstream financial institution or remains a specialized inclusion vehicle. The next crisis will test whether the post-COVID resilience is permanent or temporary. The competitive dynamics will reveal whether relationship banking can survive digital disruption.

What's certain is that Ujjivan's experiment is far from over. Whether it ends in triumph, failure, or something in between, it will have generated invaluable lessons about the possibilities and limitations of market-based solutions to social problems. In a world grappling with inequality, climate change, and technological disruption, these lessons matter far beyond one bank's share price.

The story of Ujjivan is ultimately the story of Indian aspiration—millions of people working their way from poverty toward dignity, one small loan at a time. Whether public markets can sustainably support this journey remains an open question. The answer will shape not just Ujjivan's future but the future of financial inclusion globally.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube