Tata Teleservices (Maharashtra): The Telecom Phoenix Rising from the Ashes

I. Introduction & Episode Framing

Picture this: A telecom company with a market capitalization of ₹11,536 crores, yet bleeding red ink with losses of ₹1,277 crores. The stock that once touched ₹290 in January 2022, plummeted to ₹1.80 in the dark days of March 2020—a 99% collapse that would make most investors run for the exits. Yet here we are, watching retail investors pile into TTML shares, pushing them up 35% in recent months. What do they see that the financials don't show?

This is the paradox of Tata Teleservices (Maharashtra) Limited—a company that by all conventional metrics should be dead, yet refuses to die. It's a story that defies the typical corporate narrative arc. While Bharti Airtel and Reliance Jio carved up India's telecom market between them, TTML did something almost unheard of in business: it sold its entire consumer mobile business, walked away from millions of subscribers, and bet everything on becoming an enterprise telecom player in just two Indian states.

The question isn't just how a company survives selling its crown jewels—it's why the market believes this particular phoenix can rise from the ashes. Is this irrational exuberance from retail traders chasing a turnaround story, or are we witnessing the early stages of one of India's most improbable corporate reinventions?

To understand TTML today, we need to rewind to 1995, when it wasn't even called TTML, and trace a journey through India's most brutal industry consolidation, international partnership dramas worthy of a Netflix series, and strategic pivots that would make most CEOs dizzy. This isn't just a telecom story—it's a masterclass in corporate survival when every odd is stacked against you.

The threads we'll pull: How Hughes became Tata. Why NTT Docomo poured billions into a regional player. What really happened when Jio turned the industry upside down. And most intriguingly, why Tata Group—known for its conservative approach—is still backing this venture with 74.4% ownership when the numbers scream "exit."

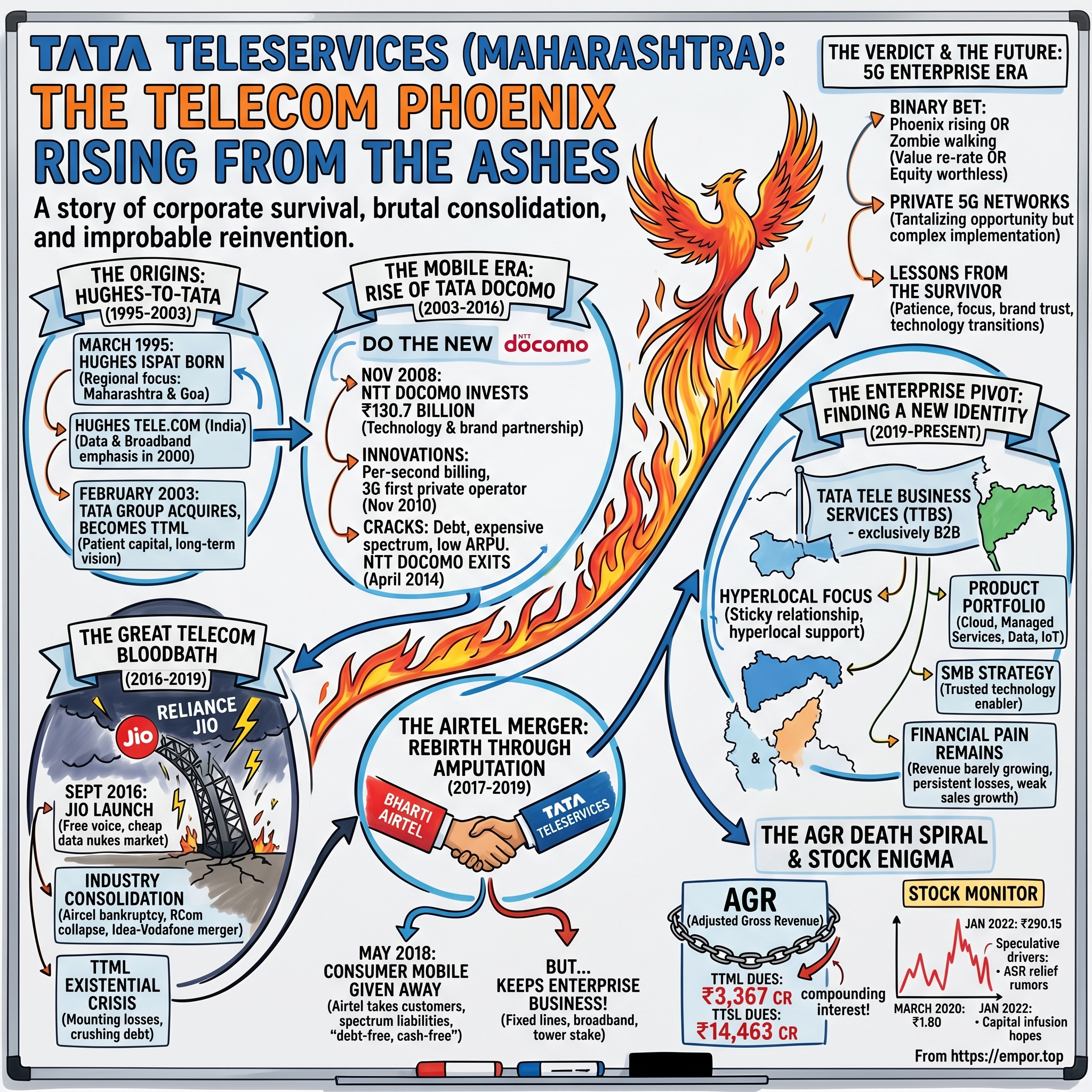

II. Origins: The Hughes-to-Tata Transformation (1995-2003)

March 13, 1995. The liberalization era of Indian telecom was just beginning. While everyone was chasing all-India licenses and dreaming of national networks, a company called Hughes Ispat Limited was quietly born with a much more modest ambition: provide telecom services in Maharashtra and Goa. The founders weren't thinking about conquering India—they were thinking about dominating India's commercial capital and its surrounding region.

The Hughes connection wasn't accidental. Hughes Network Systems, the American satellite and networking giant, saw opportunity where others saw limitation. Maharashtra wasn't just another state—it housed Mumbai, India's financial nerve center, Pune's emerging IT corridor, and Goa's tourism goldmine. The combined GDP of these regions rivaled entire countries. Hughes understood something that would only become clear decades later: sometimes regional depth beats national breadth.

By April 2000, the company shed its industrial-sounding "Ispat" suffix to become Hughes Tele.com (India) Limited. The rebranding wasn't cosmetic—it signaled a fundamental shift. While competitors were building voice networks, Hughes was laying fiber and thinking about data. Remember, this was 2000—the dot-com bubble was bursting globally, yet here was a regional Indian telco betting on broadband when most Indians hadn't even heard the term.

The real transformation came in February 2003. Tata Group, which had been eyeing the telecom sector with characteristic patience, acquired the company. The rechristening to Tata Teleservices (Maharashtra) Limited wasn't just about slapping the Tata name on the door. Ratan Tata had a vision that went beyond the obvious mobile play everyone else was chasing. He saw TTML as a laboratory—a place to experiment with technologies and business models before rolling them out through Tata Teleservices Limited (TTSL), the group's national telecom arm. The strategic positioning was clear from day one. Initially it received licences to provide telephony services in Maharashtra and Goa, but this wasn't a limitation—it was focus. While national players spread themselves thin across 23 circles, TTML could concentrate resources, experiment with new technologies, and achieve operational excellence in a concentrated geography. The company's early emphasis on broadband and data services, reflected in the April 2000 name change to Hughes Tele.com (India) Limited to reflect its emphasis on broadband services, proved prescient. This was years before smartphones existed, when dial-up internet was still common, and "broadband" was more aspiration than reality for most Indians.

The Tata acquisition brought more than just a prestigious name. It brought patient capital, technological expertise from the broader Tata ecosystem, and most importantly, a long-term vision that went beyond quarterly earnings. The group saw TTML as a piece in a larger telecom chess game—one that would involve partnerships, technology transitions, and eventually, dramatic strategic pivots that no one could have predicted in 2003.

What emerged from this transformation was a company with split personality by design: innovative enough to experiment with cutting-edge technology, yet conservative enough to survive the brutal economics of Indian telecom. This duality would define TTML's journey through boom, bust, and eventual reinvention. As we'll see, the company that started as a regional wireline player would soon find itself at the center of one of the most ambitious international partnerships in Indian telecom history.

III. The Mobile Era: Rise of Tata Docomo (2003-2016)

November 2008. The global financial crisis was decimating markets worldwide, Lehman Brothers had just collapsed, and most companies were battening down the hatches. Yet in Mumbai, executives from Japan's NTT Docomo were signing what would become one of the largest foreign investments in Indian telecom history. NTT Docomo acquired a 26 per cent equity stake in Tata Indicom, a subsidiary of Tata Teleservices, for about ₹130.7 billion (US$1.5 billion). The enterprise value? A staggering ₹502.69 billion.

This wasn't just a financial investment—it was a technology and brand partnership that promised to revolutionize Indian mobile services. NTT Docomo wasn't any ordinary telecom company. In Japan, they had pioneered mobile internet with i-mode, launched 3G services when most of the world was still on 2G, and built a reputation for innovation that made them the envy of global operators. Their decision to enter India through Tata wasn't random—they saw an opportunity to replicate their Japanese success in the world's fastest-growing telecom market.

The partnership birthed "Tata Docomo"—a brand that would become synonymous with innovation in Indian telecom. The tagline "Do the New" wasn't just marketing fluff. Within months of the partnership, Tata Docomo introduced per-second billing in India, shaking up an industry that had grown comfortable with per-minute charges. Competitors scrambled to match, but the damage was done—Tata Docomo had positioned itself as the consumer champion.

The real coup came in November 2010, when Tata Teleservices became the first private operator to launch 3G services in India. This wasn't just a technology milestone—it was a statement of intent. While competitors were still figuring out 3G spectrum auctions and network rollouts, Tata Docomo was already offering video calls, mobile TV, and high-speed internet. The Japanese technology transfer was working exactly as planned. On 5 November 2010, Tata Docomo became the first private sector telecom company to launch 3G services in India, timing the launch with Diwali festivities—a masterstroke of marketing that associated cutting-edge technology with tradition and celebration. Ryuji Yamada, President and CEO of NTT DoCoMo, said: "After nearly a decade of success in providing 3G service in Japan, we are delighted to have lent our technical and business knowhow to TTSL", underlining the depth of technology transfer involved.

The numbers told a story of rapid growth. By March 2017, Tata Docomo had about 49 million users—not bad for a company that started with regional ambitions. The brand wasn't just competing; it was innovating. Per-second billing, value-added services from Japan, and aggressive pricing strategies made Tata Docomo the disruptor before "disruption" became a buzzword in Indian telecom.

But beneath the surface, cracks were appearing. The 3G spectrum auctions had been expensive—Tata Teleservices paid ₹5,864.29 crores for spectrum in 10 circles. The competition was intensifying with every player rushing into 3G. And most ominously, the business model assumptions that justified NTT Docomo's massive investment were proving optimistic. Indian consumers loved low prices more than high-speed data. The Average Revenue Per User (ARPU) that made sense in Japan simply didn't materialize in India.

By 2014, the honeymoon was over. NTT DoCoMo announced on 25 April 2014 that they would sell their shares in Tata Indicom to Tata Teleservices and exit the Indian market. The company had reported a loss of $780 million during financial year ending 31 March 2014. What followed was a saga that would drag on for years—regulatory complications, valuation disputes, and international arbitration that would cost Tata Group billions.

The Docomo era had transformed TTML and its parent TTSL from regional players into national brands, brought world-class technology to Indian consumers, and created innovations that the entire industry would adopt. But it also loaded the companies with debt, created unsustainable cost structures, and set the stage for the existential crisis that was about to unfold. The storm clouds gathering on the horizon had a name: Reliance Jio.

IV. The Great Telecom Bloodbath (2016-2019)

September 5, 2016. Mukesh Ambani took the stage at Reliance's annual general meeting and announced what would become the nuclear bomb of Indian telecom: Jio's commercial launch with free voice calls forever and data at prices that made competitors' spreadsheets spontaneously combust. Within hours, telecom stocks crashed, executives held emergency meetings, and an entire industry realized that the rules of the game had fundamentally changed.

For TTML and TTSL, already weakened by the Docomo exit saga and mounting losses, Jio's entry wasn't just disruptive—it was potentially fatal. The math was brutal: Jio was offering 1GB of 4G data for what competitors charged for 100MB of 3G. Voice, which had been the cash cow of Indian telecom for two decades, became worthless overnight. The industry consolidation that analysts had predicted for years happened in months, not decades. The statistics were staggering. On 1st September 2016, as chairman Mukesh Ambani launched Jio after a 45 minute speech at the Reliance Industries Limited (RIL) AGM, telecom giants Bharti Airtel, Idea Cellular and Reliance Communications lost a whopping $2 billion in the stock market. On September 2016, Mukesh Ambani launched Jio with an address at Reliance Industry's 42nd Annual General Meeting. In it, he made four announcements that would forever change the Indian telecom industry. First, Jio would never charge for voice calls within India. The first 100 SMS each day would be free.

The bloodbath was immediate and merciless. Within six months of Reliance Jio's launch, India became the top mobile data user across the world consuming over 1 billion GB of data every month in comparison with 200 million GB earlier. For TTML and TTSL, this wasn't just competition—it was an extinction event. Their carefully built 3G networks, the Docomo brand equity, the enterprise and consumer segments—all suddenly seemed obsolete in a world where 4G data was practically free.

Meanwhile, the NTT Docomo exit was turning into a corporate nightmare of epic proportions. Since Tata was unable to find a buyer for the shares, they sought the approval of the RBI, in November 2014, to buy back the shares from NTT Docomo for $1.1 billion (at ₹58.045 per share), half the price paid by them in 2009. The RBI had approved the deal in January 2015, but reversed their decision and rejected the deal in March 2015, citing FEMA regulations. Following the RBI decision, the Tata Group offered to purchase Docomo's stake at ₹23.34 a share on the basis of a fair market value determined on 30 June 2014 by PwC.

The dispute escalated to international arbitration. NTT Docomo then moved the London Court of International Arbitration seeking a valuation of ₹58 a share. On 28 February 2017, Tata and NTT Docomo resolved their dispute, after the former announced that it would pay the latter US$1.18 billion in exchange for NTT Docomo's shares in the joint venture. On 31 October, $1.27 billion was paid to NTT Docomo by Tata Sons, thus ending the dispute.

But the real crisis was existential. 28 months on, Jio's entry has forced India's largest merger with Vodafone-Idea, cornered Bharti Airtel into posting its first quarterly loss in over 15 years, and put as many as five telecom providers out of business. Industry consolidation wasn't happening over years—it was happening in quarters. Aircel filed for bankruptcy. Reliance Communications, once the jewel in Anil Ambani's crown, collapsed. Sistema's MTS India shut down. Videocon Telecom liquidated. Telenor exited.

For TTML, watching competitors fall like dominoes while bleeding cash themselves, the choice became stark: find a buyer or die. The company that had once dreamed of conquering India's telecom market was now just trying to survive the next quarter. The debt burden was crushing, spectrum payments were due, and customer acquisition in the Jio era was virtually impossible. The stage was set for what would become one of the most complex mergers in Indian telecom history.

V. The Airtel Merger: Death and Rebirth (2017-2019)

October 12, 2017. The press release was clinical, almost antiseptic in its language: Bharti Airtel announced that it would acquire the consumer mobile businesses of Tata Teleservices Ltd (TTSL) and Tata Teleservices Maharastra Ltd (TTML) in a debt-free cash-free deal. The deal will essentially be free for Airtel which will only incur TTSL's unpaid spectrum payment liability. What those dry words didn't capture was the end of an era—Tata Group was essentially giving away a business it had spent decades and billions building.

The structure of the deal was unprecedented in Indian corporate history. This wasn't a traditional acquisition where assets are bought for a price. Airtel wasn't paying anything for the customer base, the infrastructure, or the brand. They were simply taking on the spectrum liabilities—and even that came with conditions. The message was clear: in the post-Jio world, telecom assets without scale weren't assets at all—they were liabilities.

But here's where the story takes an interesting turn. While everyone focused on what TTML was giving up, few noticed what it was keeping. TTSL will continue to operate its enterprise, fixed line and broadband businesses and its stake in tower company Viom Networks. This wasn't an oversight or a negotiation failure. This was strategy.

The regulatory approval process became a saga in itself. The deal received approval from the Competition Commission of India (CCI) in mid-November 2017. On 29 August 2018, Bharti Airtel, got its shareholders approval for the merger proposal with Tata Teleservices. On 17 January 2019 NCLT Delhi gave final approval merger between Tata Docomo and Airtel. Department of Telecom (DoT), and Competition Commission of India (CCI) gave green signals for merger deal between Bharti Airtel and Tata Teleservices.

The transition was surreal for customers. In November 2017, Tata Teleservices customers transitioned to the Airtel mobile network under an Intra Circle Roaming (ICR) arrangement. SIM cards and billing plans remained the same. One day you were a Tata Docomo customer; the next day, your phone showed Airtel's network, but your SIM card still said Tata. It was corporate shape-shifting in real-time. The financial gymnastics behind the merger were extraordinary. The Tata Group paid lenders and the government about Rs 50,000 crore ($7.3 billion) to help complete the deal announced in October 2017. Tata Sons, the group holding company, paid the Department of Telecommunications Rs 10,000 crore late last month, soon after settling all pending loans worth Rs 40,000 crore owed by unit TTML. Think about that—Tata Group paid ₹50,000 crores to give away a business. This wasn't a sale; it was paying someone to take your problems.

The official merger date was July 1, 2019. Following the Hon'ble TDSAT's order directing the DOT to take the merger on record and approval of the schemes of arrangement by Hon'ble NCLT, Delhi and Hon'ble NCLT, Mumbai, the schemes of arrangement became effective on 1st July 2019. Consequently, all customers, assets, spectrum and agreed liabilities of the Consumer Mobile Businesses of TTSL and TTML now stand merged with Airtel.

But here's the twist that everyone missed: TTSL will continue to operate its enterprise, fixed line and broadband businesses and its stake in tower company Viom Networks. While the consumer mobile business died, TTML didn't disappear. It morphed. The company that had once dreamed of conquering India's consumer telecom market was now betting everything on a completely different game: enterprise services.

The strategic logic was counterintuitive but brilliant. In the consumer market, TTML was competing against Jio's unlimited data and Airtel's massive scale—a losing proposition. But in the enterprise market? Different rules applied. Enterprises didn't care about ₹99 unlimited plans. They cared about reliability, service level agreements, security, and customization. They needed managed services, not commodity connectivity. And most importantly, they were willing to pay premium prices for premium services.

TTML's wireline infrastructure, which seemed like a liability in the mobile era, suddenly became an asset again. Those old copper lines and fiber networks that everyone had written off? They were exactly what enterprises needed for dedicated connectivity. The fixed-line business that seemed obsolete? It was the backbone of enterprise communications. The company that had failed at B2C was positioning itself for a B2B resurrection.

The shareholder treatment was almost an afterthought. 970,668 equity shares (in aggregate including fractional entitlements) fully paid up of face value of Rs 5 per share of the company to the eligible equity shareholders of TTML in the ratio of 1 equity share of the company for every 2,014 equity shares held in TTML by eligible equity shareholders of TTML. One Airtel share for every 2,014 TTML shares—a conversion ratio that spoke volumes about value destruction.

Yet Tata Group held on. With 74.4% ownership, they weren't just keeping TTML alive—they were investing in its transformation. The merger wasn't the end of TTML's story. It was the painful but necessary surgery that would allow it to be reborn as something entirely different. The consumer telecom company was dead. Long live the enterprise services company.

VI. The Enterprise Pivot: Finding a New Identity (2019-Present)

Post-July 2019, TTML faced an existential question: What do you become when your core business has been amputated? The answer emerged not from boardroom strategy sessions but from what was left behind—the unsexy, overlooked parts of the business that Airtel didn't want. Fixed lines. Enterprise connections. Broadband infrastructure in two states. Assets that seemed like relics in the age of 5G, but contained the seeds of reinvention.

Tata Teleservices (Maharashtra) Limited (TTML) is a leading player in the connectivity and communication solutions market serving enterprise customers. With services ranging from connectivity, collaboration, cloud, security, IoT and marketing solutions, it offers a comprehensive portfolio of ICT services for businesses in India under the brand name Tata Tele Business Services (TTBS). The transformation wasn't gradual—it was immediate and total. TTML went from being a consumer brand to exclusively B2B overnight.

The new TTML wasn't trying to be Airtel or Jio for enterprises. It was positioning itself as something more fundamental: the plumbing of India's digital economy in its most important economic regions. Maharashtra and Goa might be just two states, but they account for nearly 20% of India's GDP. Mumbai alone houses the headquarters of most major corporations, the stock exchanges, and the financial infrastructure of the country.

According to The Economic Times report In 2018, Tata Tele Business Services introduced VPN solutions intended for small and medium-sized enterprises (SMEs). In 2019, Tata Tele Business Services introduced SmartOffice. These weren't moonshot products—they were practical solutions for real business problems. While Jio and Airtel fought over consumer market share, TTML was quietly building sticky, high-margin enterprise relationships.

The product portfolio evolution tells the story of transformation. The company provides cloud and SaaS services which comprises smart cloud, google workplace, Microsoft azure and Microsoft 365, smartflo and smartflo UCaaS; voice services including Centrex, PRI, SIP trunk, SmartOffice, and international bridging service. It also offers data services which includes smart internet, Ill burstable bandwidth, SD-WAN iFLX, smart VPN-MPLS, EZ cloud connect, leased line-P2P, tele Wi-Fi, ultra-LOLA, and business and retail broadband.

This wasn't random product proliferation—it was careful curation. Each service addressed a specific enterprise pain point. SD-WAN for companies struggling with multi-location connectivity. Cloud services for digital transformation. IoT solutions for Industry 4.0 initiatives. Marketing solutions leveraging telecom data. TTML wasn't selling connectivity; it was selling business enablement.

The strategy had three pillars that distinguished it from larger competitors:

Deep Local Presence: While Airtel Business and Jio Business operated nationally, TTML could offer hyperlocal support in Maharashtra and Goa. Their sales teams knew every major enterprise in Mumbai personally. Their service engineers could be on-site within hours, not days. In enterprise services, proximity matters.

Tata Trust Premium: The Tata brand carried weight in enterprise circles that transcended telecom. CFOs trusted Tata with sensitive financial data. CIOs knew Tata wouldn't disappear overnight. In a market where vendor stability mattered as much as service quality, the Tata pedigree was invaluable.

Solution Integration: Rather than selling individual services, TTML positioned itself as a single-window solution provider. TTBS provides integrated telecom solutions to enterprises that go beyond the purview of connectivity into offering one-stop-shop business solutions and managed services. The solutions allow enterprises to be resilient and maintain business continuity in a flexible, scalable and secure manner.

The customer segmentation was surgical. It serves BFSI, IT/ITES, manufacturing, services, education, healthcare, telecom, media, entertainment, retail, and other industries. But within these sectors, TTML wasn't chasing everyone. They focused on mid-to-large enterprises that valued service over price, companies undergoing digital transformation, and businesses requiring custom solutions that larger telcos wouldn't provide.

The SMB strategy deserves special mention. It follows a progressive approach of partnering with Small & Medium Businesses ('SMBs') as their trusted technology enabler, empowering them with a comprehensive portfolio of connectivity and digital solutions. This wasn't charity—it was smart business. SMBs in Mumbai and Pune were growing rapidly, had less negotiating power than large enterprises, and once onboarded, rarely switched providers.

Yet the financial performance remained challenging. Revenue: 1,269 Cr · Profit: -1,277 Cr · Company has low interest coverage ratio. The company has delivered a poor sales growth of 3.95% over past five years. The numbers painted a stark picture: revenues barely growing while losses persisted. The enterprise pivot was logical strategically but wasn't yet delivering financially.

The competitive landscape was daunting. Airtel Business had national scale and could bundle enterprise services with mobile plans. Jio was aggressively entering the enterprise market with predatory pricing. Specialized players like Sify and Netmagic had deeper technical expertise. Global players like AT&T and Verizon served multinational corporations. TTML was caught in the middle—too small to compete on scale, too generalist to win on specialization.

The technology transitions added complexity. As enterprises moved to cloud, traditional connectivity revenues declined. As video conferencing replaced voice calls, PRI lines became obsolete. As SD-WAN virtualized networks, MPLS revenues shrank. TTML was transforming its portfolio while its legacy revenues evaporated—a challenging balancing act.

But there were green shoots. The COVID-19 pandemic accelerated digital transformation. Work-from-home created demand for secure connectivity solutions. Cloud adoption exploded. IoT projects that had been theoretical became urgent. Suddenly, TTML's integrated solutions approach found receptive audiences. The question was whether these tailwinds could translate into sustainable profitability before patience—and capital—ran out.

VII. The Stock Market Enigma

The TTML stock chart from 2020 to 2024 looks like a heart monitor during cardiac arrest—violent spikes followed by dramatic crashes, with no apparent correlation to business fundamentals. Mkt Cap: 11,407 Crore for a company losing over ₹1,200 crores annually defies conventional valuation logic. The all-time high of ₹290.15 in January 2022 and all-time low of ₹1.80 in March 2020 represent a 160x swing—volatility that would make cryptocurrency traders nervous.

What drives such irrational price movements? The answer lies not in TTML's enterprise pivot or operational performance, but in three letters that haunt India's telecom sector: AGR (Adjusted Gross Revenue). The Supreme Court's 2019 ruling on AGR dues created a ₹1.5 lakh crore liability overhang for the sector. For TTML, with its complicated history of consumer business transfers and spectrum trades, the AGR calculation became a Schrödinger's cat—simultaneously dead and alive depending on regulatory interpretation. The AGR saga reads like a Kafka novel. TTSL has to pay ₹19,256 crore adjusted gross revenue (AGR) along with other dues to the central government by March 2026. With a negative net worth of ₹17,876 crore and steep accumulated losses, TTSL is in no position to meet its obligations without support. According to Care Ratings, as of March 2024, the AGR dues were Rs 17,830 crore. This includes Rs 3,367 crore under Tata Teleservices Maharashtra Ltd (TTML) and Rs 14,463 crore under TTSL. Now, the dues have gone up to Rs 19,256 crore.

The speculation driving TTML's stock price becomes clearer. TTML's share price recorded a 12% spike on reports that the government could provide relief on AGR dues by cutting interest and waiving penalties. Every rumor of government relief, every whisper of a bailout package, every Supreme Court hearing sends the stock into violent gyrations. Tata Teleservices (TTML) shares surged over 30% in two days amid capital infusion speculation from Tata Sons, despite weak fundamentals and mounting AGR dues.

The retail investor psychology is fascinating. They're not buying TTML for its enterprise business or revenue growth. They're making a binary bet: either Tata Group will bail out TTML (again), or the government will provide AGR relief. Given Tata's track record—The rating firm said until June 2019, Tata Sons had infused ₹46,595 crore into TTSL and continues to issue a support letter to the company—the first scenario isn't implausible. Given political pressures and the telecom sector's strategic importance, the second isn't impossible either.

The volatility creates its own momentum. Shares of TTML have surged 473% in three months, 524% in six months and whooping 2712% in the last one year as on January 12, 2022. These aren't investment returns; they're lottery ticket payoffs. The stock has become a favorite among day traders and speculators who thrive on circuits—both upper and lower.

The technical patterns tell a story of pure speculation. From a technical perspective, the stock is exhibiting strong bullish signals, trading above all its key moving averages, including the 5-day to the 200-day Simple Moving Average (SMA). But technicals mean nothing when a stock's fate depends on Supreme Court judgments and government policy decisions.

The volume spikes are particularly telling. The surge in share price has been accompanied by a significant spike in trading volumes. Around 88.62 lakh shares changed hands on the BSE, substantially higher than the two-week average of 12.12 lakh shares. Turnover on the counter reached ₹65.99 crore. These aren't long-term investors accumulating positions; they're traders riding momentum.

The January 2022 episode deserves special attention. Shares of Tata Teleservices (Maharashtra) were locked in 5 per cent lower circuit on the BSE in Wednesday's intraday trade after the company on Tuesday said it will opt for conversion of the interest related to AGR dues into equity. The government becoming a shareholder in TTML—a possibility that seemed to spook investors—highlighted the bizarre nature of the AGR overhang.

The fundamental disconnect is stark. TTML reports a negative price-to-earnings (P/E) ratio of 11.51 and a negative price-to-book (P/B) value of (-)0.77. Earnings per share (EPS) are in the red at (-)6.54, while the return on equity (RoE) is a modest 6.72. These aren't just bad numbers; they're numbers that suggest the equity might be worthless.

Yet the market cap persists at over ₹11,000 crores. Why? Because in the casino of Indian stock markets, TTML has become the ultimate speculation vehicle—a proxy bet on regulatory outcomes, judicial decisions, and the Tata Group's willingness to protect its reputation. It's not investing; it's gambling with a corporate wrapper.

VIII. Business Model Deep Dive

Strip away the speculation and examine what TTML actually does today, and you'll find a business model that's both more focused and more fragile than it appears. Total Income from telecommunication stood at ₹1,093.80 crore in FY2022-23 compared to ₹1,078.82 crore in the preceding financial year. Earnings before interest, depreciation, tax and amortisation (EBITDA) stood at ₹499.67 crore in FY23, up 4.11% year-on-year, compared to ₹479.09 crore reported in the previous fiscal. The EBITDA margins hovering around 45% would be impressive if not for the crushing debt service that turns operational profits into net losses.

The revenue streams break down into distinct categories, each with different economics:

Enterprise Connectivity (40-45% of revenues): This is the bread and butter—dedicated leased lines, MPLS networks, and point-to-point connections for corporate clients. Margins are healthy (60-70% gross) because once installed, these connections require minimal maintenance. The challenge? This market is shrinking as enterprises shift to cloud-based alternatives and SD-WAN solutions.

Cloud and Managed Services (25-30% of revenues): The growth engine, but also the margin killer. TTML resells Microsoft Azure, Google Workspace, and other cloud services, acting more as a systems integrator than a technology provider. Gross margins here are thin (15-20%) because TTML is essentially a middleman. The value-add comes from bundling, local support, and single-invoice convenience.

Voice Services (15-20% of revenues): The dying legacy. PRI lines, SIP trunking, and toll-free numbers still generate cash, but volumes decline 10-15% annually as enterprises shift to cloud-based communications. These services have fantastic margins (80%+) but face inevitable obsolescence.

Broadband and Last-Mile (10-15% of revenues): TTML provides voice solutions like PBX, toll-free numbers and unified communications for businesses to increase their operational efficiency. The company offers Microsoft Azure cloud services and Smartflo, a cloud-based collaboration platform for various tasks like storage, networking, document sharing, video conferencing and voice messaging among others. The Cloud and SaaS offering of the company allow businesses to access computing resources and applications on-demand, without the need for upfront investment in infrastructure. This segment serves both SMBs and residential customers in select areas, providing steady but unspectacular returns.

Marketing and Value-Added Services (5-10% of revenues): The marketing solutions of TTML include both traditional and latest technology driven solutions. Under its digital marketing services the company helps businesses in search engine optimisation (SEO), social media marketing, and email marketing. The company is engaged in outdoor, television and print advertising solutions. An odd addition to a telecom portfolio, but it leverages customer relationships and generates high-margin revenues.

The capital allocation strategy post-merger reveals management's priorities. With the consumer business gone, TTML no longer needs to spend billions on spectrum or network expansion. Annual capex has dropped to ₹50-100 crores, mostly for maintenance and selective fiber expansion. This asset-light approach makes sense given the company's financial constraints, but it also limits growth potential.

The working capital dynamics are surprisingly favorable. Enterprise customers typically sign multi-year contracts with quarterly advance payments. This negative working capital cycle provides crucial liquidity for a cash-strapped company. However, customer concentration is high—losing a few major accounts could be devastating.

The cost structure remains problematic. Despite the merger, TTML still carries legacy costs: - Network maintenance for aging infrastructure - Spectrum payments for airwaves now used by Airtel - Employee costs for a workforce sized for a larger company - Regulatory compliance for licenses across multiple service categories

The path to profitability isn't mysterious—it's just difficult. TTML needs to: 1. Grow revenues faster than 5% annually (current rate: 3.95%) 2. Reduce operational costs by 20-30% 3. Resolve AGR dues without massive dilution 4. Generate enough cash to service debt

The competitive positioning is nuanced. Against Airtel Business and Jio Business, TTML can't compete on scale or price. But against niche players like Sify or Netmagic, TTML has advantages: the Tata brand, integrated service portfolio, and existing customer relationships. The sweet spot is mid-sized enterprises that want a single vendor for multiple services but don't need pan-India coverage.

The 5G opportunity presents both promise and peril. Private 5G networks for enterprises could be a game-changer, but TTML lacks spectrum and capital to build its own networks. Partnering with Airtel or Jio means sharing economics. Going alone means massive investment. It's a Catch-22 that epitomizes TTML's strategic dilemmas.

The margin structure tells the real story. EBITDA margins of 45% should translate to healthy profits, but interest costs eat up all operational profits and more. It's a business that works operationally but fails financially—a company that would be viable if not for the sins of its past.

IX. Playbook: Lessons from the Survivor

TTML's journey from regional wireline operator to national mobile player to enterprise services provider offers a masterclass in corporate survival—and cautionary tales about strategic overreach. The lessons aren't always what they seem.

Lesson 1: Patient Capital Can Be a Curse and a Blessing

Tata Group's willingness to pump ₹46,595 crore into TTSL/TTML kept the company alive when any rational investor would have pulled the plug. This patient capital allowed for strategic pivots that wouldn't have been possible under quarterly earnings pressure. But it also enabled bad decisions to persist longer than they should have. The Docomo partnership might have been unwound earlier with less patient owners, saving billions.

The key insight: Patient capital works when it funds transformation, not when it subsidizes failure. TTML survived because Tata Group eventually forced radical change (the Airtel merger), not because it kept funding the status quo.

Lesson 2: Sometimes You Have to Amputate to Survive

The decision to sell the consumer mobile business to Airtel for essentially nothing was brutal but necessary. Most companies can't psychologically write off their core business—they keep trying to fix it until bankruptcy. TTML's willingness to perform radical surgery saved the company, even if it destroyed shareholder value.

The playbook: When an industry undergoes structural change (like Jio's entry), incremental adjustments won't work. You need to fundamentally reimagine the business or exit. TTML did both—exiting consumer while reimagining itself as an enterprise player.

Lesson 3: Geographic Focus Can Be Strategic

TTML's limitation to Maharashtra and Goa seemed like a weakness in the pan-India mobile era. But in enterprise services, this concentration became a strength. Deep local presence, personal relationships, and rapid response times matter more than national coverage for many business customers.

The principle: In commodity markets (like consumer mobile), scale is everything. In service markets (like enterprise telecom), depth can beat breadth. TTML couldn't win the scale game, so it changed to a game where scale mattered less.

Lesson 4: Brand Value Transcends Business Models

The Tata name kept TTML relevant even as its business model collapsed. Enterprise customers trusted Tata to honor contracts, provide support, and remain stable. This brand equity was worth more than any technology or infrastructure.

The application: In B2B markets, especially in emerging economies, corporate brand can be the ultimate differentiator. TTML leveraged trust when it couldn't compete on product or price.

Lesson 5: Regulatory Overhangs Create Opportunities and Traps

The AGR dues situation created massive uncertainty, depressing TTML's valuation but also creating speculative opportunities. Investors who bought at ₹1.80 in March 2020 and sold at ₹290 in January 2022 made 160x returns—not from business improvement but from regulatory speculation.

The lesson: In heavily regulated industries, regulatory changes can matter more than operational performance. Understanding regulatory dynamics becomes as important as understanding business fundamentals.

Lesson 6: Technology Transitions Are Dangerous Moments

TTML navigated the 2G to 3G transition successfully but was crushed by the 4G transition. Each technology generation creates winners and losers, and past success doesn't guarantee future survival. The company that pioneered 3G in India couldn't compete in 4G.

The framework: During technology transitions, incumbents face the innovator's dilemma—their existing assets and capabilities become liabilities. TTML's 3G network and spectrum became worthless almost overnight when Jio launched with 4G-only infrastructure.

Lesson 7: International Partnerships Are Complex

The NTT Docomo partnership brought capital, technology, and credibility but also created massive liabilities when it unwound. Cultural differences, divergent expectations, and regulatory complications turned a strategic alliance into a financial nightmare.

The warning: International JVs in emerging markets often fail because partners underestimate regulatory complexity, market dynamics, and exit difficulties. The cost of divorce can exceed the benefits of marriage.

Lesson 8: Pivot Timing Matters More Than Pivot Direction

TTML's pivot to enterprise services was strategically sound but came too late. By 2019, Airtel Business and Jio Business were already established, and specialized players had captured niche markets. Being right about the direction doesn't help if you're wrong about the timing.

The insight: Strategic pivots need to happen before crisis forces them. Voluntary transformation has higher success rates than involuntary restructuring.

Lesson 9: Financial Engineering Has Limits

Despite creative structures (debt-free transfers, spectrum swaps, government equity conversion), TTML couldn't engineer its way out of fundamental business problems. Financial creativity can buy time but can't substitute for operational viability.

The reality: In the end, businesses need to generate cash from customers, not financial gymnastics. TTML's survival depends on making the enterprise business profitable, not on AGR relief or capital infusions.

Lesson 10: Survival Isn't Success

TTML survived where Aircel, RCom, and others died. But survival at any cost isn't victory. Shareholders who bought at IPO are down 90%+. Employees have endured years of uncertainty. Customers have seen service disruptions.

The sobering truth: Sometimes the survivors envy the dead. TTML lived to fight another day, but the cost of survival might exceed the value of victory.

X. Bull vs. Bear Case Analysis

The Bull Case: Phoenix Rising

The optimists see TTML as a coiled spring, compressed by temporary challenges but ready to explode higher when conditions align. Their thesis rests on multiple catalysts converging:

5G Private Networks Revolution: Enterprises globally are deploying private 5G networks for manufacturing, logistics, and campus connectivity. TTML, with its enterprise focus and Tata Group relationships, is perfectly positioned. Tata Motors, Tata Steel, and other group companies could become anchor customers, providing credibility for winning external contracts. The addressable market could reach ₹10,000 crores by 2027.

AGR Resolution: The court said the pleas had no legal grounds. However, it allowed the government to provide some relief to the telecom companies if it wishes to. The government has political incentives to provide relief—letting TTML fail would concentrate the telecom market further, and Tata Group's importance to India's economy gives it leverage. A 50% waiver on penalties and interest could eliminate ₹10,000 crores of liabilities overnight.

Asset-Light Transformation: With no spectrum costs, minimal capex needs, and infrastructure already built, TTML can generate 60%+ EBITDA margins on incremental revenue. Every ₹100 crore of additional revenue could add ₹60 crores to EBITDA—a leverage that few companies possess.

Tata Group Synergies: As Tata Group companies undergo digital transformation, TTML could become the preferred technology partner. TCS for software, TTML for connectivity, Tata Power for data centers—an integrated offering that competitors can't match. The captive market alone could double revenues.

Valuation Arbitrage: At ₹11,500 crore market cap for a company with ₹500 crore EBITDA, TTML trades at 23x EBITDA. Peers like Bharti Airtel trade at 10-12x EBITDA, but that's for a capital-intensive consumer business. Asset-light B2B companies typically trade at 15-20x EBITDA. If TTML achieves ₹800 crore EBITDA (feasible with 15% revenue growth), it could be worth ₹16,000 crores—a 40% upside.

Hidden Assets: TTML's fiber network in Mumbai and Pune has replacement value exceeding ₹2,000 crores. The customer relationships, especially in BFSI sector, have strategic value. The licenses and regulatory approvals would take years for new entrants to obtain. These intangible assets aren't reflected in book value.

The Bear Case: Zombie Company Walking

The pessimists see TTML as the corporate equivalent of the walking dead—technically alive but fundamentally unviable. Their concerns are grounded in harsh realities:

Structural Decline: The company has delivered a poor sales growth of 3.95% over past five years. This isn't cyclical weakness; it's structural decay. Enterprise connectivity is commoditizing, cloud services have razor-thin margins, and voice revenues are evaporating. TTML is fighting gravity.

Competitive Impossibility: Airtel Business has 10x the scale, Jio Business has unlimited capital, and specialized players have better technology. TTML is subscale in a scale business, undercapitalized in a capital-intensive industry, and unfocused in specialized markets. It can't win anywhere.

AGR Death Spiral: Even with Tata Sons support, paying ₹19,256 crores is nearly impossible. With a negative net worth of ₹17,876 crore and steep accumulated losses, TTSL is in no position to meet its obligations without support. Government equity conversion would massively dilute existing shareholders. Default would trigger license cancellation. There's no good outcome.

Customer Concentration Risk: A handful of large enterprises drive majority revenues. Losing even 2-3 major accounts would devastate financials. In enterprise services, customer churn is low but impact is high. One bad quarter could trigger a liquidity crisis.

Technology Obsolescence: TTML's infrastructure is aging, its technology stack is outdated, and it lacks capital for upgrades. While competitors deploy AI, edge computing, and 5G, TTML struggles to maintain legacy systems. The technology gap widens daily.

Management Attention Deficit: With constant firefighting on AGR, debt, and losses, management has no bandwidth for strategy. The company is in permanent crisis mode, making long-term planning impossible. This creates a vicious cycle where short-term survival prevents long-term viability.

The Math Doesn't Work: Even assuming 10% revenue growth (double the historical rate), 50% EBITDA margins (higher than current), and zero interest costs (impossible given debt), TTML would generate ₹200 crores of net profit by 2027. At a generous 20x P/E, that's ₹4,000 crores market cap—65% below current levels.

The Verdict: Binary Outcome

TTML isn't a normal investment—it's a binary bet. Either AGR relief comes and the company re-rates dramatically, or it doesn't and the equity becomes worthless. There's no middle ground.

For fundamental investors seeking steady compounding, TTML is uninvestable. The business quality is poor, the competitive position is weak, and the financial leverage is dangerous. Warren Buffett wouldn't touch this with a ten-foot pole.

For special situation investors comfortable with binary outcomes, TTML offers asymmetric risk-reward. The downside is 100% (already priced in given negative book value), but the upside could be 200-300% if AGR relief materializes. It's venture capital returns in public markets.

For traders riding momentum, TTML is paradise. The volatility creates opportunities for 10-20% moves weekly. The thin float and retail concentration amplify price swings. Just don't be holding when the music stops.

The meta-lesson: TTML exemplifies the danger of investing based on narrative rather than numbers. The story of Tata Group's backing and potential turnaround is compelling. The financial reality is terrifying. In the long run, reality wins.

XI. What's Next: The 5G Enterprise Era

The future of TTML hinges on a technology it doesn't own, can't afford, and might not survive long enough to deploy: 5G. Yet paradoxically, the 5G enterprise revolution could be TTML's salvation—if it can navigate the next 24 months without imploding.

Private 5G networks represent a paradigm shift in enterprise connectivity. Unlike public networks that serve consumers, private 5G creates dedicated, secure, ultra-low latency networks for specific enterprise use cases. Manufacturing plants use it for autonomous robots. Ports deploy it for crane automation. Hospitals enable remote surgery. The global market is projected to reach $40 billion by 2030.

For TTML, the opportunity is tantalizing but complex. Without its own 5G spectrum (sold to Airtel), TTML must partner with spectrum holders or rely on unlicensed spectrum bands. Three models are emerging:

Network-as-a-Service: Partner with Airtel or Jio to resell their 5G capacity with TTML's enterprise relationships and system integration capabilities. Margins would be thin (10-15%) but capital requirements minimal. This is the safest but least rewarding path.

Hybrid Infrastructure: Build edge computing infrastructure that connects to partners' 5G networks. TTML would own the compute layer while partnering for connectivity. This requires moderate investment (₹200-300 crores) but offers better margins (25-30%) and differentiation.

Spectrum Leasing: Lease spectrum from operators or use CBRS/unlicensed bands to build genuine private networks. This needs significant investment (₹500+ crores) but could generate 40%+ margins and create sustainable competitive advantage.

The Tata Group ecosystem provides natural advantages. Tata Steel's Kalinganagar plant needs private 5G for automation. Tata Motors' Sanand facility requires ultra-low latency for collaborative robots. Indian Hotels wants seamless connectivity across properties. These captive customers could provide proof-of-concept before external expansion.

Edge computing amplifies the opportunity. 5G's low latency enables computation at the network edge rather than distant data centers. TTML's presence in Mumbai—India's financial capital—positions it perfectly for edge deployments in trading, banking, and media. A single edge node in BKC could serve dozens of financial institutions.

The IoT explosion multiplies the addressable market. India is projected to have 5 billion IoT devices by 2030. Each device needs connectivity, management, and security. TTML's integrated platform could capture value across the stack—connectivity revenues from SIM cards, platform revenues from device management, and service revenues from security and analytics.

But execution challenges are severe. TTML lacks the technical expertise for cutting-edge 5G deployments. Hiring talent is difficult given financial uncertainty. Partners might bypass TTML and go direct to customers. The window of opportunity is narrow—first movers will lock in enterprise contracts for 5-7 years.

M&A scenarios could accelerate or obviate the transformation. Potential acquirers include:

Strategic Buyers: Airtel might acquire TTML's enterprise business to eliminate competition and gain customer relationships. Estimated value: ₹3,000-4,000 crores (0.6-0.8x revenue).

Financial Buyers: Private equity could take TTML private, restructure operations, and sell to strategic buyers in 3-5 years. Precedent: Carlyle's acquisition of Hexaware. Estimated value: ₹5,000-6,000 crores (1x revenue, assuming AGR resolution).

Technology Players: Cloud providers like AWS or Azure might acquire TTML for last-mile access to Indian enterprises. Precedent: Microsoft's acquisition of Affirmed Networks. Estimated value: ₹8,000-10,000 crores (1.5-2x revenue given strategic value).

Government Intervention: If AGR dues prove unmanageable, the government might nationalize TTML, merge it with BSNL/MTNL, and create a public sector enterprise champion. Shareholders would likely face massive dilution.

The most intriguing possibility is TTML becoming India's enterprise connectivity champion—the Snowflake or Datadog of telecom. By focusing exclusively on B2B, building specialized capabilities, and leveraging Tata Group relationships, TTML could create a defensible niche. Success would require:

- Resolve AGR dues through negotiation, conversion, or payment

- Raise growth capital of ₹500-1,000 crores for 5G and edge infrastructure

- Acquire capabilities through partnerships or acquisitions

- Execute flawlessly on enterprise contracts

- Achieve profitability by FY2027

The probability of threading this needle is low—perhaps 20-30%. But the payoff could be substantial. A profitable, growing enterprise connectivity player could be worth ₹25,000-30,000 crores (5-6x revenue at SaaS multiples). That's a 3x return from current levels.

More likely, TTML muddles through—surviving but not thriving, generating enough cash to service debt but not enough to invest for growth, maintaining relevance but not achieving excellence. It's not an inspiring vision, but after the trauma of the past decade, mere survival might be victory enough.

The 5G enterprise era will create winners and losers. Whether TTML joins the winners depends less on technology than on execution, less on market opportunity than on financial capacity, and less on strategy than on survival. The next 24 months will determine whether TTML's transformation story has a triumphant final chapter or merely an extended epilogue.

XII. Recent News**

Supreme Court Dismisses AGR Relief Petition (May 2025)**: On Monday, the Supreme Court rejected the petitions of Tata Teleservices, Vodafone Idea, and Bharti Airtel. These companies had asked for a waiver on interest and penalties related to AGR dues. The court said the pleas had no legal grounds. However, it allowed the government to provide some relief to the telecom companies if it wishes to. This ruling effectively ended hopes for judicial relief, putting the ball in the government's court for any potential waiver.

Capital Infusion Speculation Drives Volatility (May 2025): Tata Teleservices (TTML) shares surged over 30% in two days amid capital infusion speculation from Tata Sons, despite weak fundamentals and mounting AGR dues. The primary catalyst behind this recent surge appears to be growing speculation surrounding a potential capital infusion into Tata Teleservices Ltd (TTSL) by its parent company, Tata Sons Ltd. The market's reaction showed how sentiment-driven TTML's valuation has become.

DoT Penalty for Compliance Violations (June 2025): Tata Teleservices has received penalty orders totaling Rs 3.8 crore from the Department of Telecommunications for violating subscriber verification norms. The company is evaluating its options, including potential appeals. While minor in quantum, this highlighted ongoing regulatory challenges even in the enterprise business.

Q3 FY2025 Financial Results: The firm posted a standalone net loss of Rs.315.11 crore for Q3 FY2025, up from Rs.307.69 crore in the same period last year, while revenue rose by 12.41% to Rs.332.77 crore. The revenue growth acceleration to double-digits offered hope that the enterprise strategy was gaining traction, though losses continued to mount.

Board Changes (August 2025): Director Ankur Verma resigns; Nalin Rana appointed Additional Director from August 7, 2025, subject to approval. Director Ankur Verma resigns; Nalin Rana appointed Additional Director from August 7, 2025, subject to shareholder approval. Director Ankur Verma resigns; Nalin Rana appointed additional director from August 7, 2025. Board reshuffles suggested Tata Group was refreshing leadership for the next phase of transformation.

AGR Dues Continue to Mount: According to Care Ratings, as of March 2024, the AGR dues were Rs 17,830 crore. This includes Rs 3,367 crore under Tata Teleservices Maharashtra Ltd (TTML) and Rs 14,463 crore under TTSL. Now, the dues have gone up to Rs 19,256 crore. The compounding interest meant that even without new liabilities, the AGR burden grew heavier each quarter.

Stock Volatility Continues: The stock reached a record high of Rs 111.48 on July 19, 2024, and a 52-week low of Rs 50.01 on April 7, 2025. The 123% swing within a year reflected the binary nature of TTML's prospects—either spectacular recovery or total collapse.

The recent news paints a picture of a company in limbo—operationally improving but financially deteriorating, strategically sound but structurally challenged, backed by Tata Group but abandoned by the market. The next 12 months will likely determine whether TTML emerges as a focused enterprise player or becomes another casualty of India's telecom wars.

XIII. Links & Resources

Official Company Resources

Regulatory & Legal Documents

- TRAI Performance Indicators Reports

- Department of Telecommunications Orders

- Supreme Court AGR Judgment (2019)

- NCLT Merger Orders

Industry Reports & Analysis

- "Indian Telecom Services Performance Indicators" - TRAI Quarterly Reports

- "The Indian Telecom Story" - ICRIER Working Papers

- "5G: The Catalyst to Digital Revolution in India" - Deloitte/CII Report

- "Enterprise Connectivity Market in India" - IDC India

Books for Context

- "Telecom Man: Leading From the Front in India's Digital Revolution" by Sunil Mittal

- "The Tatas: How a Family Built a Business and a Nation" by Girish Kuber

- "Ambani & Sons" by Hamish McDonald (for Reliance Jio context)

- "The Platform Revolution" by Geoffrey Parker, Marshall Van Alstyne, and Sangeet Paul Choudary

Recommended Podcast Episodes

- "The Jio Effect" - The Seen and the Unseen by Amit Varma

- "India's Telecom Wars" - Capitalmind Podcast

- "The Business of Telecom" - Business Wars (Wondery)

- "Tata Group's Century of Business" - Business Breakdowns

Academic Papers

- "Market Structure and Competition in Indian Telecommunications" - Economic and Political Weekly

- "The Impact of Spectrum Allocation on Telecom Industry Structure" - Indian Institute of Management Studies

- "Corporate Restructuring in Distressed Firms: Evidence from Indian Telecom" - Journal of Emerging Market Finance

News Sources for Updates

Financial Data Platforms

Historical Context

- Telecom Regulatory Authority of India Archive

- India's Telecom Revolution Timeline

- NTT Docomo Historical Reports

For Fundamental Investors

- Focus on AGR resolution timeline and government policy announcements

- Track enterprise revenue growth and EBITDA margin trends

- Monitor Tata Sons' annual reports for commitment to TTML

- Watch for M&A activity in enterprise telecom space

For Traders

- Key levels: Support at ₹50, Resistance at ₹110

- Volume spikes often precede major moves

- Supreme Court hearing dates trigger volatility

- Government policy announcements drive sentiment

Disclaimer: Telecommunications Sector Analysis for Educational Purposes

This analysis reflects publicly available data and should not be construed as investment advice. The telecommunications sector faces significant regulatory, competitive, and financial risks. Investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions. Past performance does not guarantee future results, and investing in distressed companies carries substantial risk of permanent capital loss.

The TTML story continues to evolve. What started as a regional wireline operator became a national mobile player, transformed into a failed consumer business, and now attempts rebirth as an enterprise services provider. Whether this phoenix truly rises from the ashes or remains forever smoldering depends on factors beyond anyone's control—regulatory decisions, competitive dynamics, and the patience of its storied parent. In the annals of Indian business, few companies have survived such trauma. Even fewer have thrived after it. TTML's next chapter remains unwritten, but its past chapters offer lessons in resilience, the cost of ambition, and the price of survival in one of the world's most brutal industries.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube