Covestro: From Bayer's Laboratory to the €16 Billion ADNOC Deal

How a German chemical division, carved out of Bayer, became the largest Middle Eastern acquisition of a European company in history

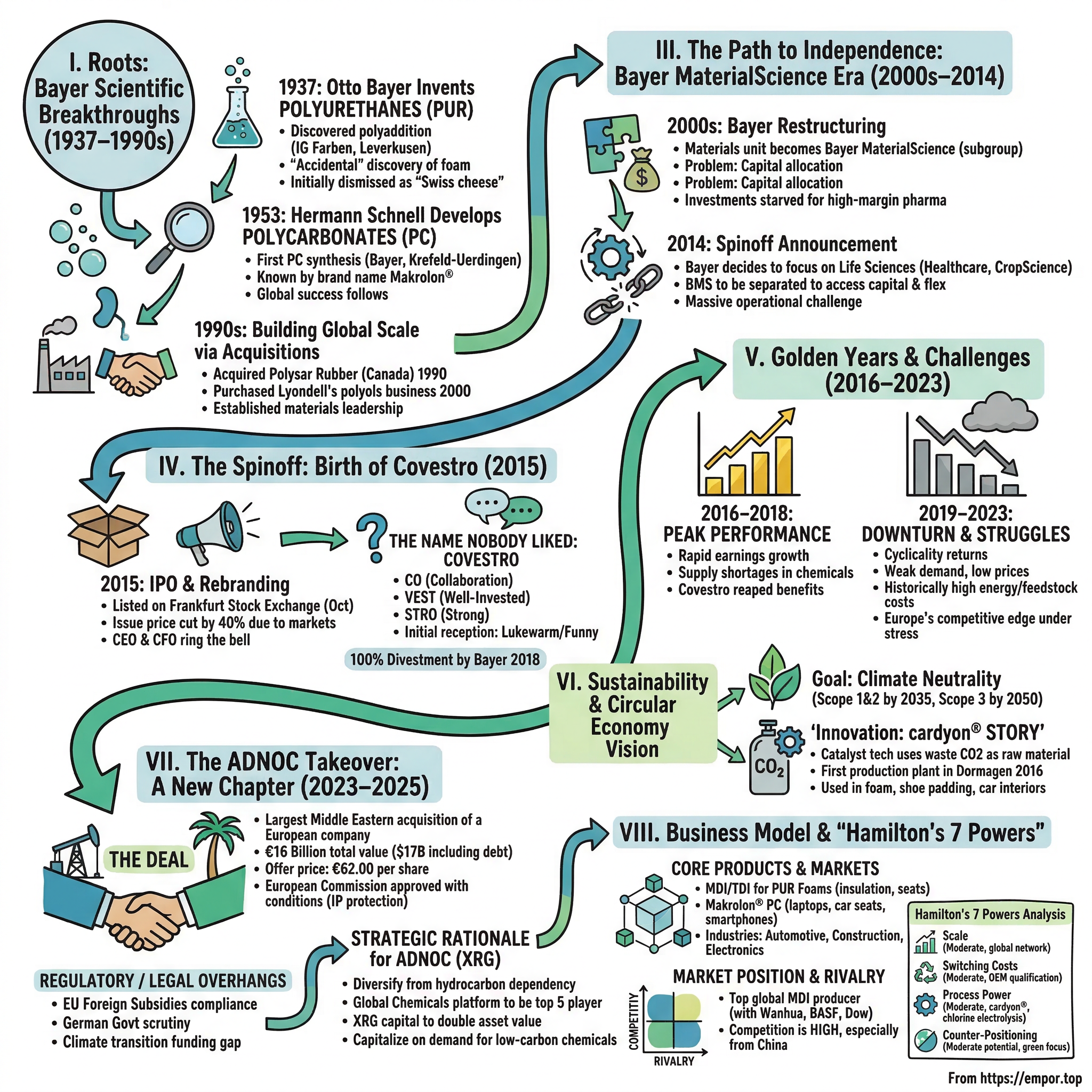

I. Introduction & Episode Roadmap

In a laboratory in Leverkusen, Germany, in the autumn of 1937, a chemist named Otto Bayer was attempting to synthesize something groundbreaking. What emerged from his experiments—a bubbly, foam-like substance—was dismissed by colleagues as fit only for "imitations of Emmental cheese." Nearly nine decades later, the legacy of that accidental discovery culminated in one of the most significant transactions in European industrial history: the €16 billion acquisition of Covestro by Abu Dhabi's state oil giant, ADNOC.

Covestro generated sales of €14.2 billion in fiscal year 2024, operating 46 production sites worldwide with approximately 17,500 employees. The company supplies the invisible infrastructure of modern life—the insulation in your refrigerator, the polycarbonate in your laptop case, the foam in your car seat, the protective coating on your smartphone.

The ADNOC deal represented "one of the largest cash transactions in the chemicals industry ever, as well as the first time a company part of the DAX 40 blue-chip index in Germany would be acquired by a state company from the Gulf." This is the story of how that came to be: from Otto Bayer's foam experiments through Hermann Schnell's polycarbonate breakthrough, from a contentious spinoff that nobody wanted to celebrate, to a transformation program struggling against industry headwinds, and finally to a deal that represents the shifting tectonic plates of global energy and industrial power.

The narrative arc contains all the elements of an industrial epic: serendipitous invention, corporate politics, identity crises, cyclical booms and busts, and the collision of European industrial heritage with Gulf petrochemical ambitions. But underlying these dramatic moments is a more fundamental question: what happens when a company built on decades of German chemical engineering excellence becomes a strategic asset in ADNOC's quest to become a top-five global chemicals player?

II. The Deep Roots: Bayer's Scientific Breakthroughs (1937–1990)

The Polyurethane Revolution

Otto Bayer (4 November 1902 – 1 August 1982) was a German industrial chemist at IG Farben who was head of the research group that in 1937 discovered the polyaddition for the synthesis of polyurethanes out of poly-isocyanate and polyol. Notably, Bayer was not related to the founding family of Bayer Corp.—a coincidence that has caused confusion for generations of chemistry students.

The origin story has the texture of legend. Otto Bayer, born in Frankfurt am Main on November 4, 1902, began his chemistry studies there and concluded in 1924 with a doctorate. His mentor was Julius von Braun, who arranged his first industrial position at the Cassella Farbwerke of I.G. Farbenindustrie. After registering early research achievements in vat and sulfur dyes, he was unexpectedly appointed to management at age 29, then two years later transferred to Bayer in Leverkusen to head the Central Scientific Laboratory. At just 32 years old, he was the youngest member of the team.

Otto Bayer's greatest achievement was ultimately the invention of polyurethane chemistry. The principle of polyaddition using diisocyanates is based on his research, yet at first, his closest colleagues were very skeptical. Although the production of macromolecular structures was already a line of research that held promise for the future, Otto Bayer's basic idea of mixing small volumes of chemical substances together to obtain dry foam materials was seen as unrealistic.

He stubbornly pursued his goal of enhancing the efficiency of plastics manufacturing and en route discovered polyurethane chemistry, which became his passion. He even stuck to his guns when his superiors shook their heads at the bubbly mass he produced in his experiments, saying it was at most a "substitute for Swiss cheese."

The fact that polyurethane could form bubbles during synthesis was discovered by accident. Otto Bayer's discovery of polyurethane in 1937 might have been accidental but the substance's subsequent triumph can be attributed to persistent innovation. A fellow chemist's sneering judgment after the first results was that the material was "at best good for making imitations of Emmental cheese." Otto Bayer and his team refused to be discouraged—they added some water to the reactive mix, causing the carbon dioxide to separate and small bubbles to form, and the first polyurethane foam was born.

As head of a research group at IG Farben, Leverkusen, Germany, he discovered the polyaddition for the synthesis of polyurethane out of poly-isocyanates and polyols in 1937. The German patent was published on November 13, 1937.

But after numerous technical difficulties, Bayer eventually succeeded in synthesizing polyurethane foam. It was to take 10 more years of development work before customized materials could be manufactured on the basis of his invention.

The Polycarbonate Breakthrough

The second pillar of what would become Covestro arrived sixteen years later, in a laboratory in Krefeld-Uerdingen. Sometimes it only takes two months to turn the world upside down. Hermann Schnell (1916–1999) did just that. In 1953, the chemist moved to the main scientific laboratory of the then Bayer plant in Krefeld-Uerdingen. A few weeks later, the academic foster son of Nobel Prize winner Hermann Staudinger developed the world's first polycarbonate—the start of a global success story.

The Bayer chemist, working at the Group's Central Scientific Laboratory in Krefeld-Uerdingen, succeeded in synthesizing polycarbonate more or less at the first attempt. The event passed almost unnoticed, except in specialist circles. But just five years later, Bayer would begin producing the transparent and versatile plastic, known by its brand name Makrolon®, on an industrial scale.

It was not until 1953 that Hermann Schnell and his team, working at the Bayer facility in Uerdingen, Germany, created the version of polycarbonate that became the platform for its current commercial success. One week later, Dan Fox at General Electric independently stumbled upon the same compound while working to develop a new wire-insulating material. The two versions of the polymer were chemically the same but differed structurally. The Bayer material, trade named Makrolon in 1955, was a linear polymer, while the GE discovery was a branched material.

The nearly simultaneous development of the polymer by two large companies could be expected to produce significant legal activity. But unlike the 30-year saga of legal action that characterized the development of HDPE and PP, the potential battle over the rights to PC was settled relatively quickly with an agreement that the firm ultimately given priority would grant a license to the other company. The priority was given to Bayer.

Nevertheless, the years after the discovery were heady times. Production of polycarbonate began at Bayer in 1958 and at General Electric in 1960. Applications developed rapidly in the electrical and electronics fields, construction and lighting, food packaging, the automotive and aerospace industries, and medical devices.

Building Global Scale Through Acquisition

By the 1990s, Bayer's materials division had evolved from laboratory curiosity to industrial powerhouse, but achieving true global leadership required scale that only acquisition could provide.

The importance of North America to the Bayer Group continued to increase. In Canada, Bayer acquired Toronto-based Polysar Rubber Corporation in 1990—the most significant acquisition in the company's history up to that point. The transaction made Bayer the world's biggest supplier of raw materials for the rubber industry.

The company was privatized in 1988 with its sale to NOVA Corp which, in turn, sold Polysar Rubber in 1990 to Bayer AG of Germany. In 1990, the Polysar rubber operations were sold to Bayer AG of Germany for C$1.25 billion.

Acquisition of the polyols business of Lyondell Chemical Company, United States, made Bayer the world's biggest producer of raw materials for polyurethanes in 2000. This move made the German group and later Bayer MaterialScience the world's biggest producer of raw materials for polyurethanes.

These acquisitions established a pattern that would define the materials business: while innovation remained central to identity, scale and market leadership came through strategic deal-making. The business that would eventually become Covestro was being assembled piece by piece, even if no one yet knew that it would someday stand alone.

III. Bayer MaterialScience Era & the Path to Independence (1990s–2014)

By the early 2000s, Bayer had reorganized itself into three distinct operating pillars. Historically, Bayer consisted of three individual pillars—healthcare, crop science, and material science. MaterialScience was positioned to be spun off into a separate company.

Bayer AG underwent a comprehensive restructuring process. The plastics unit became Bayer MaterialScience, an independent subgroup. This organizational clarity, however, masked a growing strategic tension.

The problem was capital allocation. The spinoff was necessary because Bayer was deploying most of its capital and generally paying more attention to the other two business units, which were generating higher profit margins.

The MaterialScience business had been at risk of being starved of investments while Bayer funneled the bulk of its development and research into the more profitable pharmaceuticals business. This wasn't malice—it was simply rational capital deployment. Healthcare products like blockbuster drugs commanded vastly higher margins than commodity chemicals. For Bayer's management and shareholders, the choice was obvious.

MaterialScience earned about $740 million on $15.5 billion in sales in 2014. In September 2014, Bayer announced it was spinning off its MaterialScience unit so it could focus on its life sciences businesses, such as its pharmaceutical and CropScience units.

Bayer A.G. announced it would spin off its MaterialScience plastics group into a separate, publicly-traded company within 12 to 18 months. The German chemical giant confirmed reports that the split would allow the main company to operate as a life sciences business. "The board of management of Bayer A.G. plans to focus the Bayer Group entirely on the Life Science businesses—HealthCare and CropScience—and float MaterialScience on the stock market as a separate company."

The decision arrived with the force of an earthquake. Jerry MacCleary, who has been with the company for 37 years, was celebrating his 25th wedding anniversary in California when he got the call that Bayer AG had decided to spin off its material science division. It was September 17, 2014.

An independent MaterialScience business would have better access to capital and greater flexibility. As a separate company, MaterialScience could align its organizational and process structures and corporate culture toward its own industrial environment and business model. Additionally, the separation gives MaterialScience the opportunity to be more flexible in the face of global competition.

The rationale was sound, but it created enormous operational challenges. The materials business was deeply embedded in Bayer's corporate infrastructure. Separating required building, essentially from scratch, the administrative apparatus of a standalone Fortune 500 company.

IV. The Spinoff: Birth of Covestro (2015)

The IPO & Rebranding Challenge

Since October 6, 2015, the shares of Covestro AG have been listed in the Prime Standard on the Frankfurt Stock Exchange. The opening price was €26.00, exactly €2.00 higher than the issue price of €24.00 which the company set on October 2 for new shares issued by way of a capital increase.

Covestro AG gained as much as 12 percent on the first day of trading after slumping global stock markets forced the plastics maker owned by Bayer AG to cut the size of its initial public offering by 40 percent. The stock rose 11 percent at 26.55 euros at 10:39 a.m. in Frankfurt. Shares in the Leverkusen, Germany-based company had been priced at 24 euros after cutting the range from an originally targeted 26.50 euros to 35.50 euros.

The sale was more than three times over-subscribed, according to CFO Frank Lutz.

CEO Patrick Thomas and CFO Frank H. Lutz were on the trading floor at the Stock Exchange to celebrate the initial share price in the traditional way—by ringing the bell. To reflect Covestro's colorful new image, the trading floor was decorated with thousands of colored beakers and a sculpture of a bull to symbolize increasing share prices—all specially made from high-performance polycarbonate, one of Covestro's main products.

The Name Nobody Liked

When Covestro LLC was announced as the new name for Bayer MaterialScience—after being spun off from the Bayer Group—it wasn't met with enthusiasm. Saying the reception was lukewarm would be being positive, says Jerry MacCleary, president of Covestro in North America. "We had employees who said, 'Can we do a do-over again and come up with a new name?'" While people appreciated the colorful logo's visual impact, MacCleary says their customers and his colleagues, CEOs in the Pittsburgh community, made fun of it. They asked him how to pronounce it and what it had to do with a chemical company.

The name Covestro is made from a combination of words that reflect the identity of the new company. The letters C and O come from collaboration, while VEST signifies the company is well invested in state-of-the-art manufacturing facilities. The final letters, STRO, show the company is strong in innovation, strong in the market and with a strong workforce.

The name Covestro was announced in June and the global carve-out was complete by September. There was a lot of hype around the reveal of the new name and when people first heard it, it felt anti-climactic, says Alice Sox, manager of external communications. Plus, while Covestro built up its organization and hired 50 or 60 people, she says they had to introduce the new culture, the new identity, and get employees to buy in. "A lot of anxiety set in and then, of course, the question is how can we be successful on our own without Bayer and a big name and the large company behind it?"

Building a Standalone Company

The operational challenges of standing up an independent company were immense. Under Bayer, most corporate functions had been centralized across the three operating units. Covestro inherited a manufacturing and R&D operation but lacked the administrative backbone to function independently.

Covestro would use the proceeds from the IPO primarily to repay its debt to Bayer and thus establish its target capital structure. Immediately after the capital increase, net debt together with pension liabilities should be around €4 billion. With target net debt together with pension liabilities at 2.5 to 3 times adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) for fiscal 2015, Covestro was seeking an investment-grade credit rating.

Covestro shares were first offered on the Frankfurt Stock Exchange in October 2015. Bayer sold its entire remaining stake in May 2018, while Bayer's pension fund had a 6.8% stake managed separately.

The complete divestment by 2018 marked Covestro's transition from corporate stepchild to truly independent entity. The company that nobody could pronounce correctly was now standing on its own.

V. The Golden Years & Subsequent Challenges (2016–2023)

Peak Performance (2016-2018)

Before 2019, Covestro enjoyed rapid earnings growth following supply shortages of chemicals used in foams. The years immediately following the IPO proved remarkably favorable. Global supply constraints in key polyurethane raw materials drove prices higher, and Covestro, as one of the world's largest producers, benefited disproportionately.

With 2017 sales of EUR 14.1 billion, Covestro was among the world's largest polymer companies.

The company had positioned itself well. Management's focus on operational efficiency and strategic investment paid dividends in a tight market. The Makrolon brand continued its dominance in polycarbonates, while the polyurethanes business rode the construction and automotive cycles upward.

The Downturn (2019-2024)

The favorable conditions proved temporary. The chemical industry's fundamental cyclicality reasserted itself with a vengeance.

The industry struggled with weak demand throughout 2023, which caused chemical prices to drop at a time of historically high costs, particularly for energy and feedstocks and exacerbated by heavy labor and regulatory expenses. The impact on Europe-based companies' financial results was harsh and they saw no significant upturn until mid-2024 at the earliest. The trough coincided with overcapacity in many petrochemical value chains. This exposed Europe's lack of competitiveness, most notably in petrochemicals.

Markus Steilemann, president of German chemical industry association VCI and CEO of Covestro, noted: "High energy and raw material prices as well as the lack of orders will continue to weigh on business. Therefore, our companies are forced to cut their costs—whether by shutting down production plants, giving up some individual business segments or shifting investments abroad."

Sales fell by 1.4% to €14.2 billion (previous year: €14.4 billion) mainly due to low selling prices. EBITDA remained stable, falling by 0.8% to €1.1 billion, and was thus within the expected range. Net income amounted to €-266 million (previous year: €-198 million), while the free operating cash flow (FOCF) reached €89 million (previous year: €232 million). ROCE above WACC was -7.4 percentage points (previous year: -6.1 percentage points).

The energy costs are still the Achilles' heel of the European chemical industry and no other region in the world has been impacted like ours. This, along with high feedstock costs, is causing the industry to lose its competitive edge in global chemical markets. While in other regions companies look forward to invest again, especially in the USA and the Gulf, investments in Europe are under huge stress.

Transformation Efforts

Covestro launched the transformation program STRONG aimed at making the company even more efficient and driving digitalization forward. By the end of 2028, Covestro plans to achieve annual global savings of €400 million in material and personnel costs. €190 million of these will be in Germany.

Covestro is responding to conditions with cost discipline and efficiency, while at the same time pursuing opportunities for further targeted growth. The STRONG transformation programme launched in 2024 is already showing significant progress: with total savings of around €320 million realised by the end of 2025, Covestro is well on track to achieve its target of €400 million annually by 2028. Around €250 million of this will be achieved in 2025.

Dr. Markus Steilemann, CEO of Covestro says: "The last few years have been challenging for the chemical industry and for Covestro. Despite all the challenges, we have continued to drive forward our 'Sustainable Future' strategy. With STRONG, we are systematically continuing our transformation, making the company even more efficient and accelerating digitalization."

VI. Sustainability & Circular Economy Vision

Covestro has positioned sustainability not merely as a regulatory compliance exercise but as a strategic differentiator. The company is geared completely to the circular economy. Covestro aims to achieve climate neutrality for its Scope 1 and Scope 2 emissions by 2035, and the Group's Scope 3 emissions are also set to be climate neutral by 2050.

Innovation Highlights: The cardyon® Story

Perhaps no innovation better illustrates Covestro's sustainability ambitions than cardyon®—polyols manufactured using captured carbon dioxide as a raw material.

For nearly half a century, scientists sought to capture CO2 and transform it from an inert pollutant into commercially viable products that could drive growth and innovation. Scientists at Covestro developed a breakthrough technology—a catalyst that makes it possible to harness waste CO2 and convert it into a precursor for flexible polyurethane foam. In 2016, Covestro opened a production facility in Germany that sources waste CO2 gas from an adjacent power plant and uses it to manufacture a CO2-based polyol—branded cardyon®—to make flexible foam found in everyday products, like mattresses and furniture. The CO2 content in the cardyon® polyol grades is currently up to 20 percent.

The particularly sustainable new material, called cardyon®, is a polyol produced with up to 20 percent CO₂. Covestro brought this groundbreaking technology to market several years ago.

Since June 2016, Covestro has been operating its own production plant for the innovative polyols at its site in Dormagen, Germany. It has an annual capacity of 5,000 metric tons. The CO2 processed is a waste product from a neighboring chemical facility.

Cardyon® is now also used to produce padding for shoes and car interiors, flexible foam for mattresses and adhesives for sports floors.

Markus Steilemann, CEO at Covestro, said: "The use of carbon dioxide as a new raw material is a promising approach for making production in the chemical and plastics industries more sustainable. This way, we use CO2 in a closed-loop process and save oil. On this basis, we want to offer a comprehensive product portfolio for as many areas of application as possible."

Greenhouse gas emissions fell to 4.7 million metric tons of CO₂ equivalents (previous year: 4.9 million metric tons).

VII. The ADNOC Takeover: A New Chapter (2023–2025)

The Courtship

The approach from ADNOC arrived in September 2023, inserting Covestro into a much larger strategic narrative about Gulf states' diversification away from pure hydrocarbon dependency.

Based on the open-ended talks with the Abu Dhabi National Oil Company (ADNOC), the Board of Management of Covestro AG resolved on June 24, 2024, following consultation with the Supervisory Board, to enter into concrete negotiations about a possible transaction and the possible conclusion of an investment agreement. On October 1, 2024, Covestro AG signed an investment agreement with certain companies of the ADNOC Group, including XRG P.J.S.C. The investment agreement specifies, among other things, that the Bidder will submit to the shareholders of Covestro AG a public takeover offer for all outstanding shares of Covestro at a price of €62.00 per share.

The Deal

The European Commission approved with conditions the $17-billion acquisition by Abu Dhabi National Oil Company (ADNOC) of Germany's chemicals giant Covestro, following an investigation into foreign subsidies it feared would distort competition. At the end of last year, Abu Dhabi's oil company agreed to buy Covestro in a deal worth $17 billion (14.7 billion euros) including debt.

ADNOC International, now operating under the name XRG, successfully acquired a 91.3% stake in Covestro AG, following the completion of the additional acceptance period for its voluntary public takeover offer. The bid, which included 172,591,806 shares, exceeded the minimum acceptance threshold of 50% plus one share.

Regulatory Approval

The European Commission said Friday that an offer from ADNOC to maintain Covestro's intellectual property in Europe as well as concessions on the company's unlimited state guarantee from the UAE settled its earlier fears. Those commitments are valid for 10 years. "Commitments offered by ADNOC effectively address the potential negative effects by allowing market participants to access key Covestro patents in the field of sustainability," EU competition chief Teresa Ribera said.

Abu Dhabi state oil firm ADNOC and Germany's Covestro received the final outstanding regulatory approval from the German economy ministry for their 14.7 billion euro ($16.9 billion) takeover deal. Covestro said all closing conditions for the takeover by ADNOC were fulfilled, and that the transaction was expected to close in the coming days.

Covestro will remain headquartered in Leverkusen and led by its current management team. XRG said it will maintain existing employee agreements, including collective bargaining and co-determination structures.

Strategic Rationale for ADNOC

XRG aims to more than double its asset value over the next decade by capitalizing on demand for low-carbon energy and chemicals driven by three megatrends: the transformation of energy, exponential growth of AI, and the rise of emerging economies. Building on ADNOC's expertise and transformational international acquisitions, the independently operated investment company will initially focus on developing three core strategic value platforms, including Global Chemicals which aims to be a top 5 global chemicals player.

XRG's Global Chemicals platform aims to be a top five global chemicals player, producing and delivering chemical and specialty products essential for modern life, to meet the projected 70% increase in global demand by 2050.

This acquisition aligns with XRG's broader strategy to enhance its position in the performance materials and specialty chemicals sectors, marking a critical step towards its goal of becoming a top five global chemicals player. Covestro, a global leader in high-performance polymers and sustainable material solutions, is now set to become a cornerstone of XRG's Performance Materials and Specialty Chemicals business.

VIII. Business Model Deep Dive

Core Products & Applications

Covestro AG is a German company producing polyurethane and polycarbonate raw materials. Products include isocyanates and polyols for cellular foams, thermoplastic polyurethane and polycarbonate pellets, as well as polyurethane based additives used in the formulation of coatings and adhesives.

The main industries served are automotive manufacturing and supply, electrical engineering and electronics, construction and home products, and sports and leisure. Their products include coatings and adhesives, polyurethanes that are used in thermal insulation, electrical housings, and as a component of footwear and mattresses, and polycarbonates such as Covestro's Makrolon, which are highly impact-resistant plastics.

Covestro adds scale through 46 production sites, 13 research centres and 17,500 employees. The company produces more than 10,000 polymer materials used across mobility, electronics, construction, renewable energy and other industries.

Market Position

Covestro's main competitors are BASF, Dow Chemical, Huntsman, Mitsubishi, Saudi Basic Industries Corporation (SABIC), and Wanhua Chemical.

At present, the total global MDI production capacity is about 10.41 million tons/year, and the top five producers are Wanhua Chemical (2.65 million tons/year), BASF (1.81 million tons/year), Covestro (1.77 million tons/year), Dow Chemical (1.36 million tons/year) and Huntsman (1.35 million tons/year). These five companies together account for more than 88% of the market share.

The biggest structural change by far to the sector in recent years is the rise of several Chinese petrochemical producers. Rongsheng Petrochemical, Hengli Petrochemical, and Wanhua Chemical Group rose in the ranking because of additional revenues garnered from big recent plant expansions.

IX. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

The barriers to entry in polyurethane and polycarbonate production are formidable. Capital requirements run into the billions for world-scale facilities. The chemistry and process know-how that Covestro traces back to Otto Bayer's 1937 discoveries represents decades of accumulated intellectual property. Qualification processes with automotive OEMs typically take two to three years, creating customer stickiness that new entrants cannot easily overcome.

Since Bayer developed the industrialization technology of polyurethane in 1937, the MDI industry has developed rapidly. Currently, MDI production technology is the sixth generation, and Wanhua Chemical's seventh generation technology is under development.

However, Asian competitors—particularly China's Wanhua Chemical—have demonstrated that these barriers, while significant, are not insurmountable for well-capitalized, strategically focused competitors.

2. Supplier Power: MEDIUM

Feedstocks are tied to the petrochemical value chain (crude oil, natural gas derivatives). The energy costs are still the Achilles' heel of the European chemical industry. This, along with high feedstock costs, is causing the industry to lose its competitive edge in global chemical markets.

Energy Prices: The energy-intensive nature of the chemical industry has made it particularly vulnerable to the recent rise in energy costs. In 2023, the energy costs for the industry surged by an estimated 30-50 per cent, putting pressure on profit margins, particularly in commodity chemicals.

3. Buyer Power: MEDIUM-HIGH

Large automotive OEMs (VW, BMW, etc.) have significant negotiating leverage. Construction and electronics sectors are more fragmented, creating more balanced dynamics. Price transparency in commodity-grade products increases buyer leverage, though switching costs exist for specialized formulations.

4. Threat of Substitutes: LOW-MEDIUM

Makrolon® polycarbonate is extremely robust, lightweight with glass-like transparency and is impact resistant—even at low temperatures. It also has a high dimensional stability and is easily molded, yet displays excellent heat resistance with a glass transition temperature of up to 148ºC.

Few direct substitutes match polycarbonate's combination of transparency and impact resistance. Polyurethane foam has limited substitutes for insulation applications. However, sustainability pressures could drive adoption of bio-based alternatives over time.

5. Competitive Rivalry: HIGH

BASF holds one of the top three market positions in around 80% of the business areas in which it is active. Most important global competitors include Arkema, Bayer, Clariant, Corteva, Covestro, Dow, Dupont, DSM, Evonik, Huntsman, Lanxess, SABIC, Sinopec, Solvay, Sumitomo Chemical, Syngenta, Wanhua and many hundreds of local and regional competitors. We expect competitors from Asia and the Middle East in particular to continue to grow in significance in the years ahead.

X. Hamilton's 7 Powers Framework Analysis

1. Scale Economies: MODERATE

Covestro generated sales of EUR 14.4 billion in fiscal 2023. At the end of 2023, the company had 48 production sites worldwide and employed approximately 17,500 people.

Global production network with 46 sites creates cost advantages. However, competitors like BASF and Dow have similar or greater scale. Wanhua has achieved competitive scale in Asia with lower cost structures. The ADNOC acquisition, with its feedstock cost advantages, could fundamentally alter this calculus.

2. Network Economies: WEAK

Limited network effects exist in chemical manufacturing. This is not a platform business; it's a traditional B2B supplier model. Some value in customer technical service relationships exists but does not constitute a structural moat.

3. Counter-Positioning: MODERATE (Potential)

Sustainability focus could become counter-positioning if incumbents cannot pivot. Covestro plans to expand its portfolio of CO2-based polyols for use in rigid and thermoplastic polyurethanes and coatings. Cracking the catalytic barrier needed to convert CO2 into a raw material has opened a world of low-carbon, energy-saving possibilities. Covestro and its research partners are studying catalysis with other C1 molecules, like methane and carbon monoxide, to develop sustainable solutions.

ADNOC ownership creates potential counter-position vs. other European chemical majors (feedstock cost advantage). The combination of Gulf feedstock economics with German engineering excellence could prove powerful.

4. Switching Costs: MODERATE

Qualification processes with automotive OEMs take 2-3 years. Custom formulations for specific applications create stickiness. However, commodity grades can be switched more easily. The breadth of the product portfolio (10,000+ materials) does create some lock-in through customer reliance on technical support.

5. Branding: WEAK-MODERATE

Makrolon® has been trusted for decades and continues to pave the way for tomorrow's product innovations.

Brand recognition exists in polycarbonates with Makrolon®. However, B2B chemical brands have limited consumer visibility and thus limited pricing power derived from brand alone.

6. Cornered Resource: WEAK

While Covestro has strong R&D capabilities and sustainability patents (which had to be shared with competitors as condition of EU approval), these do not constitute cornered resources in the Hamilton Helmer sense.

7. Process Power: MODERATE

Covestro has developed a method for using the greenhouse gas CO2 to synthesize polyurethane components. It markets these raw materials, known as polyols, under the brand name cardyon™. Up to 20 percent of the fossil raw materials previously used in these products have been replaced by carbon dioxide.

Process innovations like cardyon® and oxygen-depolarized cathode chlorine electrolysis represent genuine process improvements. However, these are replicable given sufficient investment by competitors.

XI. Bull Case and Bear Case

Bull Case

1. ADNOC Ownership Transforms Cost Structure The acquisition fundamentally alters Covestro's competitive position. Gulf feedstock costs are structurally lower than European alternatives. The strategic partnership with ADNOC is timely and precisely the right step for Covestro. With ADNOC as a long-term partner, we will be better positioned to execute our 'Sustainable Future' strategy and accelerate our ongoing transformation."

2. Sustainability Leadership Creates Differentiation As regulations tighten and customers demand lower-carbon products, Covestro's early investments in circular economy technologies (cardyon®, recycling innovations) position it ahead of competitors still reliant on conventional processes.

3. Industry Cycle at Trough The severe downturn in European chemicals has depressed valuations and profitability across the sector. Historical patterns suggest cyclical recovery will eventually arrive.

4. Essential Products in Long-Duration Growth Markets Polyurethane insulation is critical to building energy efficiency. Polycarbonates enable EV lightweighting. These secular trends extend beyond typical cyclical demand patterns.

Bear Case

1. Structural European Cost Disadvantage The chemicals industry in Europe has continued to struggle this year, owing to a challenging combination of higher energy costs, slower growth, the ongoing effect of the Russia–Ukraine war on prices of natural gas and crude oil, and competition from lower-cost exports.

Even with ADNOC's feedstock advantages for some inputs, European manufacturing costs may remain structurally uncompetitive. The production footprint is heavily concentrated in high-cost Germany.

2. Chinese Competitive Pressure Intensifies Wanhua Chemical Group has been undertaking projects to shore up its core polyurethane business and to diversify into other lines. Wanhua has already surpassed Covestro in MDI capacity and continues aggressive expansion.

3. Integration Risk State-owned enterprises from the Gulf have limited track record managing complex European industrial operations with strong works councils and co-determination requirements.

4. Commodity Chemical Trap Despite innovation investments, much of Covestro's revenue comes from products with limited differentiation and high price transparency. Margin expansion requires either capacity discipline across the industry (unlikely) or product mix shift toward specialties (slow and capital-intensive).

XII. Key Performance Indicators to Track

For investors monitoring Covestro's trajectory under ADNOC ownership, three KPIs deserve particular attention:

1. EBITDA Margin This metric captures both pricing power and operational efficiency. Covestro's EBITDA fell to €1.07 billion in 2024 on €14.2 billion of sales—roughly a 7.5% margin. Historical peak margins during the 2017-2018 supercycle exceeded 15%. Recovery toward double-digit margins would signal either industry normalization or successful execution of cost programs. The combination of STRONG program savings (€400 million target by 2028) and potential feedstock synergies from ADNOC should provide visibility into margin trajectory.

2. Volumes Sold Growth vs. Industry The company sold greater volumes worldwide thanks to targeted measures to increase plant availability. Volume growth relative to industry growth reveals market share trends. In a cyclical industry, maintaining or gaining share during downturns positions for disproportionate upside during recovery. Plant availability and utilization rates serve as leading indicators.

3. Greenhouse Gas Emissions Intensity By 2030, Covestro aims to reduce energy consumption per metric ton manufactured by 20 percent compared to 2020 levels, saving the equivalent of 550,000 metric tons of CO2 emissions. As carbon pricing tightens and customer sustainability requirements intensify, emissions per unit of production becomes both a cost driver and competitive differentiator. Progress toward 2035 climate neutrality targets will increasingly affect customer decisions and regulatory positioning.

XIII. Conclusion: A New Chapter Begins

The story of Covestro is, in many ways, the story of European industrial chemistry itself. It begins with accident and perseverance—Otto Bayer mixing chemicals in a laboratory in 1937, stubbornly pursuing a foam that colleagues dismissed. It continues through Hermann Schnell's polycarbonate breakthrough, through decades of patient scale-building via acquisition and organic growth, through the trauma of a spinoff nobody wanted and a name nobody liked.

In the third quarter 2025, Covestro celebrated its tenth anniversary—a milestone that marks the company's transformation into a global leader in innovation, sustainability and the circular economy in the chemical industry. The anniversary was not only a moment for reflection, but also for looking ahead.

Now, as Covestro enters the orbit of Abu Dhabi's XRG, it faces perhaps its most profound transformation yet. The question is no longer whether the company can survive as an independent entity—that question was answered in the affirmative during the decade since its IPO. The question now is whether German engineering excellence, combined with Gulf petrochemical economics and strategic patience, can create something greater than the sum of its parts.

Dr. Sultan Ahmed Al Jaber, ADNOC Managing Director and Group CEO, said: "In line with our Board mandate to prioritize transformational growth, XRG marks a bold new chapter for ADNOC. Building on our unrivalled track record in energy and investments, network of global partners, and strategic market access, XRG will drive sustainable economic growth, foster technological innovation, and deliver the energy and products needed to improve lives around the world."

From Otto Bayer's "Swiss cheese" foam to materials in every smartphone, every EV, every refrigerator—the journey has been remarkable. What happens next, as a German industrial champion becomes part of a Gulf petro-state's ambition to dominate global chemicals, will shape not just Covestro's future but perhaps the trajectory of European industrial policy itself. The €16 billion question remains: can ADNOC's billions and Covestro's brains together create a chemicals champion for the 21st century?

Material Regulatory and Legal Overhangs

-

EU Foreign Subsidies Regulation Compliance: The conditional approval requires ADNOC to maintain commitments for 10 years, including sharing sustainability patents with competitors and removing unlimited state guarantees. Violation could trigger regulatory enforcement.

-

German Foreign Investment Screening: While approved, the acquisition demonstrated increased German government scrutiny of strategic industrial assets. Future capital allocation decisions may face similar review.

-

Climate Transition Costs: According to Accenture, to transition to net zero in Europe, chemical companies will need to increase their capital expenditure by 70% and maintain this level of investment annually until 2050. Between 2021 and 2050, the European chemical industry will have a total decarbonization funding gap of $550 billion.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube