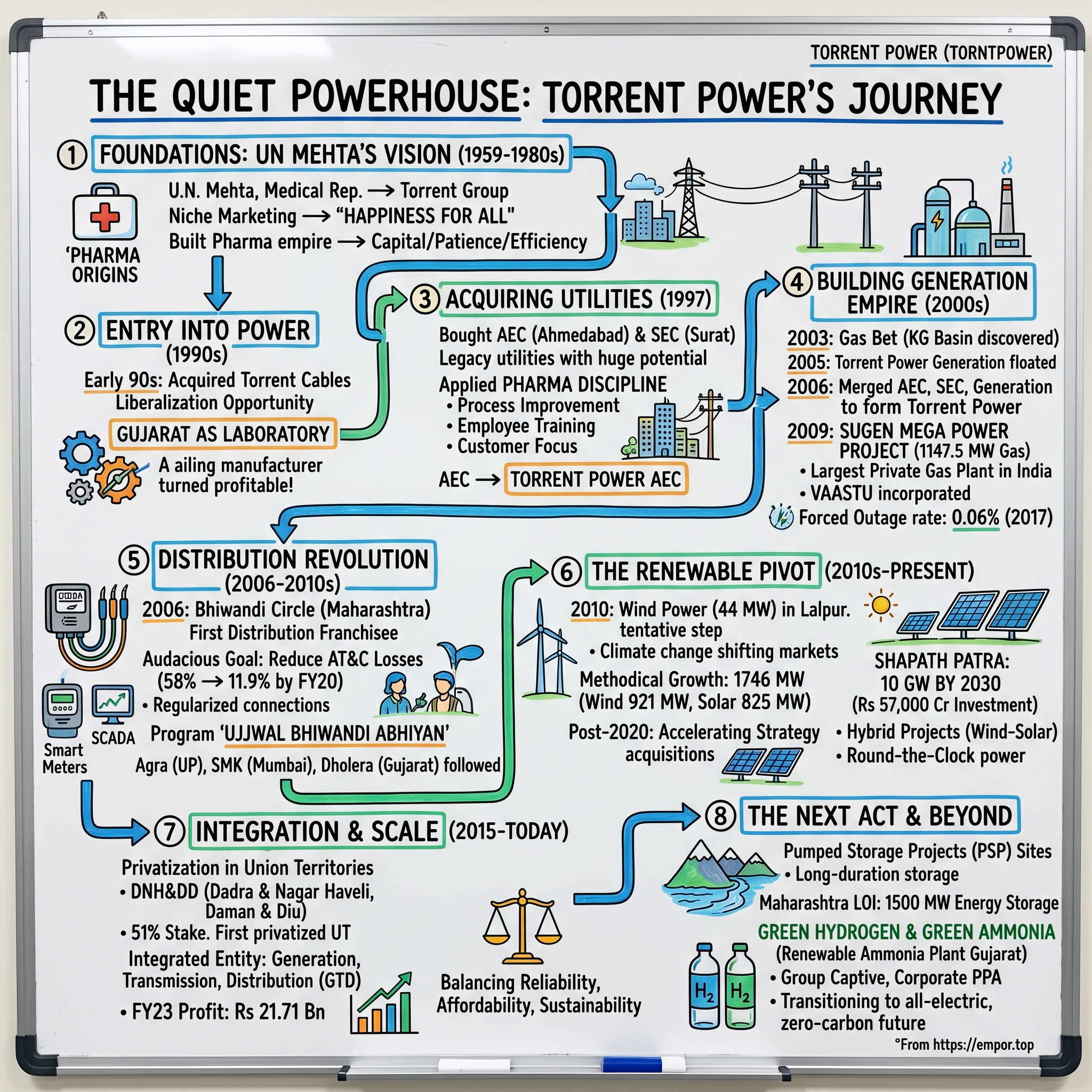

Torrent Power: The Quiet Powerhouse of India's Energy Transformation

I. Introduction & Episode Roadmap

Picture this: In the gleaming boardrooms of Mumbai and Delhi, where India's energy titans plot their next moves, one name consistently flies under the radar despite commanding a ₹67,311 crore market capitalization. While Adani and Tata Power grab headlines, Torrent Power has quietly built one of India's most efficient power utilities—a vertically integrated machine spanning generation, transmission, and distribution that serves 38.5 lakh customers across multiple states.

The story begins not in the power sector at all, but with a medical representative's dream in post-independence India. Today, Torrent Power stands as the crown jewel of the $25 billion Torrent Group conglomerate, a testament to patient capital, operational excellence, and the art of turning around distressed assets. From acquiring century-old electricity companies in Gujarat to pioneering India's distribution franchisee model, from building the country's largest private gas plant to pivoting toward a 10 GW renewable future—this is a masterclass in infrastructure investing.

How did a pharmaceutical entrepreneur's son build one of India's most efficient private power utilities? The answer lies in a uniquely Indian playbook: combining family business values with professional management, marrying operational excellence with strategic opportunism, and most importantly, understanding that in India's complex regulatory maze, execution beats strategy every time.

This deep dive will trace Torrent's evolution from the liberalization opportunity of the 1990s through today's energy transition, examining how they've consistently achieved T&D losses among the lowest in the country while their peers struggled. We'll explore their contrarian bets—why they went all-in on gas when others chased coal, how they cracked the distribution code that stumped utilities nationwide, and why they're now betting ₹57,000 crore on renewables while simultaneously exploring pumped storage and green hydrogen.

Along the way, we'll unpack the business lessons: the power of vertical integration in capital-intensive sectors, the art of regulatory navigation across multiple states, and perhaps most intriguingly, how a family-controlled conglomerate maintained governance standards that put many professionally-run companies to shame. This isn't just another infrastructure story—it's a blueprint for building enduring value in India's most challenging sectors.

II. The Torrent Group Origins & U.N. Mehta's Vision

The year was 1959. As Nehru's India grappled with its industrial identity, a young medical representative named U.N. Mehta made a decision that would echo through generations. Having spent years with Swiss pharmaceutical giant Sandoz, observing how Western companies marketed medicines, Mehta saw an opportunity others missed: India didn't just need medicines—it needed a new way of selling them. With borrowed capital and boundless ambition, he founded what would become the Torrent Group, built on a philosophy that sounds almost quaint today: "Happiness for All."

But Mehta wasn't just another entrepreneur riding the License Raj wave. His background as a medical representative in the 1940s had given him something invaluable—an understanding of India's healthcare gaps and the trust required to fill them. While others focused on manufacturing, Mehta made niche marketing his core competency, identifying underserved therapeutic areas and building relationships with doctors that competitors couldn't replicate. It was a strategy that would define Torrent's approach across all its future ventures: find the overlooked opportunity, execute with precision, and build for the long term.

Through the 1960s and 70s, as India lurched between socialist idealism and economic reality, Mehta methodically built his pharmaceutical empire. Torrent Pharmaceuticals grew from a small marketing outfit to a formidable player, eventually becoming one of India's top pharmaceutical companies. But the real genius wasn't just in building a successful pharma business—it was in recognizing that the skills required to navigate India's complex regulatory environment, manage working capital efficiently, and build trust with stakeholders were transferable.

By the late 1980s, with sons Sudhir and Samir Mehta joining the business, U.N. Mehta began contemplating diversification. The pharmaceutical business had taught them patience—drug development takes years, regulatory approvals even longer. They understood capital cycles, the importance of operational efficiency, and most critically, how to turn around underperforming assets. These weren't just business lessons; they were the foundation of what would become the Torrent playbook.

The strategic shift to infrastructure wasn't random. Mehta had watched India's power sector struggle through decades of underinvestment and inefficiency. State electricity boards were bleeding money, transmission losses were astronomical, and power cuts were so common that generators had become middle-class necessities. Where others saw intractable problems, the Mehtas saw opportunity. After all, if you could navigate India's pharmaceutical regulations, how hard could electricity be?

The entry point came through an unlikely avenue: cables. In the early 1990s, Torrent Group acquired Mahendra Electricals, an ailing power cable manufacturer on the brink of collapse. Within three years, renamed Torrent Cables Ltd., it was profitable and growing. The turnaround wasn't achieved through financial engineering or cost-cutting alone—it was operational excellence, the same discipline that had built their pharmaceutical empire. They fixed procurement, streamlined manufacturing, and most importantly, built relationships with power utilities across Gujarat.

What emerged by the mid-1990s was a ₹45,000 crore conglomerate with a unique characteristic: each business reinforced the others. Pharmaceutical profits provided patient capital for infrastructure investments. The discipline of regulated industries created operational excellence. The relationships built over decades opened doors that money alone couldn't. As India stood on the cusp of liberalization, Torrent was perfectly positioned for what came next—not through luck, but through three decades of methodical preparation.

The founding philosophy of "Happiness for All" might have seemed like corporate rhetoric, but it encoded something deeper: a belief that business success came from solving real problems for real people. Whether providing affordable medicines or reliable electricity, the Mehta family understood that in India, sustainable profits came from genuine value creation. It's a lesson that would prove invaluable as they prepared to enter one of India's most challenging sectors.

III. Entry into Power: The 1990s Liberalization Opportunity

The summer of 1991 was a watershed moment for India. As foreign exchange reserves dwindled to barely three weeks of imports and the IMF's structural adjustment loomed, a quiet revolution was beginning in the power sector. While Narasimha Rao and Manmohan Singh undertook structural reforms including the abolition of licenses, authorization of foreign investment, and liberalization of foreign trade, a new paradigm for power sector reform emerged in the 1990s, drawing inspiration from the "World Bank template" for electricity liberalization—emphasizing restructuring of utilities, creation of regulators, participation of private sector, and establishment of competitive power markets.

For the Mehta family, watching from their Ahmedabad headquarters, this wasn't just policy change—it was the opportunity they'd been preparing for. Gujarat, under progressive leadership, had already begun positioning itself as the laboratory for India's power reforms. The State Electricity Board (GEB) of Gujarat was one of the better performers compared to other State Electricity Boards, yet the state was facing severe shortage of electricity and financial crunch, leading to initiation of Power Sector Reforms. The state's proactive approach created an environment where private players could finally enter what had been a government monopoly for decades.

The entry point came through two century-old utilities that most investors wouldn't touch. The Ahmedabad Electricity Company (AEC) and Surat Electricity Company (SEC) weren't just old—they were relics from the British era, laden with legacy issues, inefficient operations, and political baggage. But where others saw liabilities, Torrent saw diamonds in the rough. These companies had something invaluable: established distribution networks, customer relationships, and most importantly, licenses that would take years for new entrants to obtain.

In 1997, the company completed its acquisition of the Ahmedabad Electricity Company by purchasing the entire 28.89% stake held by the Gujarat government, forming what was then known as Torrent Power AEC Limited. The deal, structured at a time when most Indian businesses were still skeptical about power sector investments, demonstrated Torrent's contrarian approach. They weren't buying assets—they were buying the right to serve Gujarat's commercial capital.

The Surat acquisition followed a similar pattern. The high points of Torrent's foray into power were the acquisitions of two of India's oldest utilities—The Surat Electricity Company Ltd and The Ahmedabad Electricity Company Ltd. These weren't glamorous deals that made headlines. The utilities were bleeding money, infrastructure was decades old, and employee morale was at rock bottom. But Torrent had learned from turning around Mahendra Electricals that operational excellence could transform even the most challenged assets.

What happened next surprised everyone. Torrent turned them into first-rate power utilities, in terms of operational efficiencies and reliability of power supply. The transformation wasn't achieved through massive capital infusion or workforce reduction. Instead, Torrent applied the same discipline that had built their pharmaceutical empire: systematic process improvement, employee training, and most crucially, a focus on customer service that was unheard of in Indian utilities.

The Gujarat government's approach was equally crucial. Gujarat became the first State to unbundle the SEB after enactment of Electricity Act 2003, with the Gujarat Electricity Regulatory Commission constituted on 12th November, 1998 under provisions of Electricity Regulatory Commissions Act, 1998. This regulatory clarity provided the stable framework Torrent needed to make long-term investments.

The timing was fortuitous. Gujarat's 2005 Rural Feeder Segregation Programme bifurcated transmission lines catering to rural areas into those serving households and those meant for farms, providing subsidized power to farms on single-phase lines for fixed hours while supplying costlier power to residential consumers on three-phase lines throughout the day, eliminating diversion of subsidized power for household use. This innovative approach to managing agricultural subsidies—a challenge that had bankrupted utilities across India—created a more sustainable operating environment for distribution companies.

By the end of the 1990s, Torrent had established itself as a serious power sector player. They'd acquired two of India's oldest utilities, turned them profitable, and demonstrated that private ownership could deliver both efficiency and public service. But this was just the foundation. The real test would come in the next decade, as they moved from distribution into generation, betting billions on a fuel that others considered too risky: natural gas.

The liberalization opportunity of the 1990s had given Torrent its entry ticket into power. What they did with that opportunity would define not just their future, but offer a template for how Indian conglomerates could build infrastructure businesses that balanced profitability with public purpose. As India entered the new millennium, the stage was set for Torrent's most ambitious play yet.

IV. Building the Generation Empire: Gas, Coal & Early Growth (2000–2010)

The boardroom at Torrent's Ahmedabad headquarters was unusually quiet on a humid morning in 2003. Sudhir Mehta, who had taken over as Chairman after his father's passing in 1998, stared at a map of India's gas pipeline network. The recently discovered Krishna Godavari basin gas fields promised to transform India's energy landscape. While others hesitated—coal was king, gas was unproven at scale—Torrent saw an opportunity that aligned perfectly with their contrarian DNA. The decision to build the massive gas plant was based on the potential of a newly discovered gas field in the Krishna Godavari basin in southern India in the early 2000s.

In 2005, the parent company, Torrent Group floated the company Torrent Power Generation to further expand into the power business. This wasn't just organizational restructuring—it was preparation for what would become their most ambitious project yet. In 2006, the three power-related companies of Torrent Group, Torrent Power AEC Ltd, Torrent Power SEC Ltd, and Torrent Power Generation Ltd were merged to form Torrent Power. The consolidation created a unified entity with the scale and balance sheet to compete with India's power giants.

But it was the SUGEN project that would define Torrent's generation ambitions. From its inception in 2005, the SUGEN combined cycle power plant was destined to be a one-of-a-kind project. Located in Akhakhol village near Surat, this wasn't just another power plant—it would become the largest private sector gas based power plant in India. The numbers were staggering: Construction of the Rs30,960m (€500m) plant began in 2005.

What set SUGEN apart wasn't just its scale but its approach to execution. In a decision that raised eyebrows across the industry, Torrent incorporated vaastu shastra—ancient Indian architectural principles—into the plant's design. Beyond principles governing physical order, vaastu pervades into the psychological and spiritual order of the plant's day-to-day work culture. "Vaastu is about positive energy and proactivity—that is, harnessing the resources you have to best perform in total harmony with your natural surroundings," he said. Critics called it superstition; Torrent called it creating the right environment for operational excellence.

The first unit was commissioned in 2008 and the last in 2009. When the company fully commissioned their ambitious SUGEN Mega Power Project in August 15, 2009, the 1147.5 MW SUGEN Mega Power Project was dedicated to the nation on September 30, 2009. The plant consisted of three power blocks of 382.5 MW capacity each comprising of one advanced class gas turbine (Siemens' SGT5 4000F), one steam turbine and a common generator connected in single shaft configuration along with a Heat Recovery Steam Generator.

The achievement was remarkable on multiple fronts. The SUGEN Plant has the distinction of having one of the lowest per MW capital cost of generation in the country. This wasn't achieved through cutting corners but through meticulous planning and execution. "An operability study and single-point failure analysis was carried out for the entire plant, and all identified weaknesses were suitably mitigated." Some key changes, perceived by in-house engineers through experience and foresight, required convincing the original equipment manufacturer to change its conventional plant design, even if it resulted in higher initial costs.

The operational metrics vindicated this approach. "In 2017, the forced outage rate of SUGEN was 0.06%," Lalwani said. "I'm really proud of that," he said, noting it is one of the only metrics that adequately measure O&M performance. "You cannot believe how difficult it is to achieve such a low rate of unscheduled outages for a 10-year-old plant." For context, the industry average forced outage rate for gas plants in India hovers around 5-7%.

But SUGEN's story also illustrated the challenges of India's gas market. While that potential did not pan out to its full capacity, and the sparse gas produced from the basin was eventually increasingly routed to fertilizer plants and city gas distribution portals, Torrent had to navigate volatile fuel supply scenarios. The plant's strategic location helped—it had access to all major sources of Natural Gas / LNG in the country through the pipeline connectivity of Gujarat State Petronet Limited (GSPL).

Parallel to the gas bet, Torrent maintained its presence in coal generation through the Sabarmati Thermal Power Station, with 362 MW (1 unit of 120 MW and 2 units of 121 MW each) coal based capacity. This diversification would prove prescient as gas availability fluctuated through the decade.

The success wasn't just technical—it was cultural. Torrent introduced a "position qualification system," in which engineers are tested before being tasked with plant assignments. All tasks at the plant are performed by in-house engineers—except for long-term service contract jobs executed by Siemens. This focus on building internal capabilities rather than outsourcing critical functions became a hallmark of Torrent's operational philosophy.

Safety achievements matched operational excellence. Over the past five years, SUGEN completed 6.2 million man-hours without incidents, an achievement that garnered it a "Sword of Honour" award in 2012 from the British Safety Council. In an industry where accidents can destroy reputations overnight, this track record built trust with regulators and communities alike.

By 2010, Torrent had established itself as a serious generation player with a unique edge: the ability to manage complex, capital-intensive projects with world-class efficiency. The SUGEN project alone had demonstrated that an Indian private company could build and operate infrastructure matching global standards. But as the decade ended, Torrent faced a new challenge—how to leverage this generation capacity to transform India's most intractable problem: distribution losses that were bleeding utilities dry across the country.

V. The Distribution Franchisee Revolution

The scene at Bhiwandi in December 2006 was dystopian even by Indian standards. This textile hub in Maharashtra, just 35 kilometers from Mumbai's gleaming financial district, was hemorrhaging electricity like a severed artery. Aggregate technical and commercial (AT&C) losses stood at 58%—meaning for every 100 units of power supplied, only 42 were paid for. Mandatory load shedding stretched to 6 hours at the time of takeover and subsequently increased to 8 hours. The distribution transformer failure rate hit 40%. Power theft wasn't just common; it was an industry unto itself.

Into this chaos stepped Torrent Power with a proposition so audacious that even seasoned industry observers called it corporate suicide. Torrent Power created history by entering into the country's first distribution franchisee agreement with Maharashtra State Electricity Distribution Company Limited for Bhiwandi Circle in December 2006. This wasn't privatization—the assets remained with the state utility. It was something entirely new: a distribution franchisee model where Torrent would buy power in bulk and handle everything downstream—billing, collection, maintenance, and crucially, loss reduction.

The model was elegantly simple yet revolutionary. TPL agreed to purchase power from MSEDCL at the input point to Bhiwandi circle at year-wise fixed input energy rate (Rs./kWh) for a contract period of 10 years and execute distribution responsibilities including metering, billing, revenue collection, repair, maintenance, O&M cost of network, consumer service, capital expenditure, allocating new connections. If Torrent could reduce losses and improve collections, they kept the difference. If they failed, they absorbed the losses.

What happened next stunned the power sector establishment. With operations commenced from 26th Jan 2007, TPL completed a successful milestone of 3 years of its operations with ATC loss reduction from 58% to now 18.5%. By 2015-16, losses had fallen to 25%, and by FY20, T&D losses in its Bhiwandi franchisee area in Maharashtra dropped to 11.93 per cent. This wasn't achieved through magic but through systematic execution that drew from Torrent's pharmaceutical DNA.

The transformation started with something basic: accurate metering. The percentage of accurate metered sales increased from 23% at the time of handover to 95%. But Torrent understood that in areas like Bhiwandi, technical solutions alone wouldn't work. They launched 'Ujjwal Bhiwandi Abhiyan'—a program to regularize electricity connections in slums. Instead of treating power theft as a law enforcement problem, they treated it as a customer acquisition opportunity. Illegal connections were converted to legal ones with affordable payment plans.

The technical interventions were equally sophisticated. Since the takeover of operations, TPAL invested over 250 crores towards improving the network and services in the Bhiwandi circle. Underground cables replaced overhead lines in theft-prone areas. Smart meters and SCADA systems brought real-time visibility to a network that had operated in the dark for decades. The distribution transformer failure rate reduced from 40% at the time of handover to 7.5% at the end of FY 2009.

The financial impact was transformative. Revenue increased from Rs. 272 cr. in FY2007 to Rs. 618 cr. in FY2009. But perhaps more importantly, A Customer Satisfaction Survey conducted by Prayas Energy Group revealed that approximately 68% of the representative consumers felt satisfied—a remarkable achievement in an area where the utility was previously seen as the enemy.

The Bhiwandi success opened floodgates. In 2009 it was awarded the distribution franchise for Agra in Uttar Pradesh. Agra presented different challenges—a city of Mughal monuments and marble craftsmen where losses touched 58.77%. Torrent applied the same playbook but adapted to local conditions. In a city where electricity theft had cultural sanction, they worked with community leaders and trade associations. Torrent Power managed reduction in AT&C losses in Agra from 58.77% at the time of takeover to 16.11% in FY 2018-19.

The innovation wasn't just operational—it was financial. The distribution franchisee model solved a fundamental problem of Indian power: state utilities couldn't invest in loss reduction because they were bankrupt, and they were bankrupt because of high losses. By bringing in private capital and expertise while keeping assets public, the model broke this vicious cycle. Torrent could invest because they had a clear path to returns through loss reduction.

During FY 19 the Company was awarded a distribution license for Dholera Special Investment Region (in Gujarat) and distribution franchise for Shil, Mumbra & Kalwa (SMK) area in Mumbai Metropolitan Region of Maharashtra. Each new franchise added to Torrent's expertise in turnarounds. They developed a playbook: map the network, install meters, regularize connections, upgrade infrastructure, engage communities, and relentlessly focus on service quality.

The model also had its critics. Labor unions opposed private involvement in distribution. Politicians worried about losing a patronage tool. Some argued that cherry-picking urban areas left rural regions behind. But the results were hard to argue with. In area after area, Torrent demonstrated that efficient distribution wasn't a technical problem—it was a management problem.

By 2020, the distribution franchisee model had spread across India, with other companies following Torrent's lead. But Torrent maintained its edge through continuous innovation. They pioneered prepaid metering in low-income areas, developed mobile apps for bill payment before smartphones became ubiquitous, and created customer service standards that matched private telecom companies rather than government utilities.

The distribution franchisee revolution proved something fundamental: India's power problems weren't unsolvable. They required patient capital, operational excellence, and most importantly, treating electricity consumers as customers rather than supplicants. As Torrent looked toward the next decade, they had proven they could fix broken distribution. The question now was whether they could navigate an even bigger transition—from fossil fuels to renewable energy.

VI. The Renewable Energy Pivot (2010s–Present)

The morning of December 12, 2015, was unseasonably warm in Paris as negotiators emerged bleary-eyed from COP21 with the Paris Agreement. For Torrent Power's leadership watching from Ahmedabad, the message was clear: the age of fossil fuels was ending. Not in decades, but in years. The company that had bet big on gas-fired generation now faced an existential question—how to pivot a capital-intensive infrastructure business toward renewables without destroying shareholder value?

The answer began quietly. The company forayed into the thrust area of renewable energy by conceptualizing the 44 MW wind power generation project in 2010, signing an agreement with Enercon (India) Ltd to commission this project at Lalpur, District Jamnagar, Gujarat. It was a tentative step, almost experimental—could the same operational excellence that made SUGEN a success translate to managing wind turbines scattered across rural Gujarat?

By 2015, the experiment had become strategy. Climate change wasn't just an environmental issue—it was reshaping global capital markets. Insurance companies were divesting from coal, banks were tightening fossil fuel lending, and renewable energy costs were plummeting faster than anyone predicted. Solar module prices had fallen 90% since 2010. Wind turbine efficiency had doubled. Suddenly, renewables weren't just politically correct—they were economically superior.

Torrent's renewable portfolio grew methodically: 1746 MW Renewable plants (Wind - 921 MW and Solar - 825 MW) spread across Jamnagar, Charanka, Akhakhol near Surat, Kutch, Rajkot, Bhavnagar in Gujarat; Gulbarga & Raichur in Karnataka and Osmanabad in Maharashtra. But unlike their gas plant strategy of building mega projects, renewables required a different approach—distributed, opportunistic, and increasingly driven by acquisitions.

The company acquired 100% of the share capital and all securities of Sunshakti Solar Power Projects Private Limited (SSPPPL) and 100% Equity Share Capital of Wind Two Renergy Private Limited (WTRPL). The company also acquired 100% equity stake of Solapur Transmission Limited (STL), making it a wholly owned subsidiary of the Company w.e.f. March 20, 2024. Each acquisition brought not just capacity but learning—understanding wind patterns, managing grid integration, navigating state-specific renewable policies.

The real acceleration came post-2020, as India committed to net-zero by 2070 and the economics of renewables became undeniable. Gujarat-based power company Torrent Power disclosed its plans to achieve a 5 GW renewable energy portfolio over the next three to five years through inorganic acquisitions and greenfield projects. The company had been allocated 6,000 hectares of land in Gujarat, where it plans to set up ~3 GW of renewable projects encompassing both solar and wind energy.

But the most dramatic announcement came at RE-Invest 2024 in Gandhinagar. The company submitted a 'Shapath Patra' to achieve 10 Gigawatt (GW) of installed Renewable Energy (RE) capacity by 2030, with an investment of Rs 57,000 crore. This investment is expected to generate direct and indirect employment for around 25,000 people. For context, this single commitment exceeded Torrent's entire market capitalization just five years earlier.

The strategy wasn't just about adding solar panels and wind turbines. Torrent Power won the auction for the purchase of 300 MW of power from wind-solar hybrid energy projects, with a greenshoe option of up to 150 MW from its own distribution unit by quoting ₹3.65 (~$0.044)/kWh. The tender mandated that the chosen projects incorporate a 2:1 ratio of wind to solar technologies (66.67% wind and the remaining solar). As a minimum of 50% annual capacity utilization factor (CUF) must be maintained throughout the PPA tenure, Torrent Power plans to install an overall 725 MW of combined wind and solar capacity.

This hybrid approach—combining wind and solar to ensure round-the-clock renewable power—showcased Torrent's evolution from merely installing capacity to solving grid integration challenges. Wind peaks at night, solar during the day; together, they could provide the baseload power that critics claimed renewables couldn't deliver.

The renewable pivot also brought Torrent into new territories—literally and figuratively. The company is actively pursuing corporate PPA market opportunities and has already executed 20 MW of PPAs. It is also considering the group captive arrangement for selling renewable power, which involves setting up subsidiaries within Torrent Power. Corporate buyers, from data centers to manufacturing giants, were bypassing utilities entirely to secure clean power directly from generators.

Torrent Power is actively pursuing opportunities to develop Green Hydrogen and Green Ammonia Production projects to cater to the export and domestic markets. The company wasn't just thinking about electricity anymore—they were positioning for the entire green energy value chain. Torrent has made a commitment to develop a 100,000 tons per-year renewable ammonia production plant in Gujarat, supported by an investment of $860 million.

The financial performance validated the strategy. Torrent Power's profit increased by 371% YoY to ₹21.71 billion (~$262.36 million) in FY23, mainly due to reduced transmission and distribution losses and higher generation throughout the quarters. The market noticed—renewable energy was becoming Torrent's growth engine, even as their gas plants provided stable cash flows.

But challenges remained formidable. Land acquisition for renewable projects faced local opposition. Grid integration required massive transmission investments. State distribution companies, already bankrupt, struggled to honor power purchase agreements. Battery storage, essential for renewable reliability, remained prohibitively expensive despite falling costs.

Yet Torrent's approach to these challenges reflected their DNA—patient, systematic, operational. They didn't chase the highest returns or the biggest projects. Instead, they focused on what they'd always done: acquiring undervalued assets, improving operations, and building for the long term. The renewable revolution wasn't just about technology—it was about execution at scale. And after three decades in Indian power, Torrent knew execution.

As 2024 ended, with global temperatures hitting record highs and renewable energy becoming the cheapest source of power in history, Torrent's pivot seemed prescient. The company that had started with cables, mastered distribution, conquered gas generation, was now positioning itself for an all-electric, zero-carbon future. The question was no longer whether renewables would dominate, but whether Torrent could maintain its edge in an increasingly competitive landscape.

VII. Modern Era: Integration & Scale (2015–Today)

The announcement came on a humid February morning in 2021, buried in the business pages: Torrent Power had emerged as the highest bidder in February 2021 to acquire a controlling stake in the union territory DISCOM. For most observers, it was just another privatization deal. For Torrent, it represented something far more significant—the culmination of their evolution from a regional player to a national power infrastructure champion.

DNH&DD becomes the first Union Territory to be privatized under the Government of India's ambitious program to privatize the distribution network in Union Territories through a competitive bidding process. The symbolism wasn't lost on anyone. After decades of failed state-run distribution, the government was essentially admitting that private operators like Torrent had cracked the code that had eluded public utilities.

The deal structure was classic Torrent—careful, balanced, politically astute. Torrent Power will own 51 per cent stake and Hon'ble Administrator of the Union Territory of Dadra & Nagar Haveli, Daman and Diu will own the balance 49 per cent stake. This wasn't a complete takeover but a partnership, allowing the government to maintain oversight while bringing in private efficiency.

DNHDD Power Distribution Company will have a customer base of 1.5 lakh, annual sales of 9 billion units (kwh) of power and annual revenue of about Rs.4,500 crore. The numbers might seem modest compared to Torrent's existing operations, but the strategic value was immense. This was the government's test case for privatization—if Torrent succeeded here, larger opportunities would follow.

But the path wasn't smooth. Torrent Power had emerged as the winner in this auction, which was later placed on hold by the Bombay High Court after a public interest litigation was filed against the privatization of DISCOMs. The legal challenges reflected deep-seated resistance to privatization, fears about job losses, tariff increases, and loss of government control over essential services.

Yet by April 2022, Torrent had navigated the legal maze and formally taken over operations. The privatization of the DISCOMs is expected to provide better services to over 145,000 consumers across the UT with operational improvements and functional efficiencies. With the acquisition, Torrent Power's output will increase to 24 billion units (BU) of electricity per annum to over 3.85 million customers across 12 cities spread across three states — and cater to a peak demand of over 5 GW.

The modern era wasn't just about scale—it was about integration. The company distributes power to over 38.5 lakh customers annually in its distribution areas of Ahmedabad, Gandhinagar, Surat, Dahej SEZ and Dholera Special Investment Region in Gujarat; Dadra and Nagar Haveli and Daman and Diu UT; Bhiwandi, Shil, Mumbra and Kalwa areas of Mumbai Metropolitan Region in Maharashtra and Agra in Uttar Pradesh. Each market required different approaches, different relationships with regulators, different consumer expectations.

Technology became the great enabler. Smart grids weren't just buzzwords but essential tools for managing distributed renewable generation, reducing losses, and improving reliability. Torrent deployed SCADA systems across their networks, implemented automated meter reading, and developed mobile apps that turned bill payment from a chore into a convenience. Torrent Power is also the first and only Power Distribution Company in India to win the prestigious 5 Star Rating for Environmental Sustainability, as well as the Sword of Honour for Occupational Health and Safety from the British Safety Council UK. Besides, Torrent Power is also one of the few power utilities to have implemented an Integrated Management System covering ISO 9001:2015 – Quality Management System, 140001:2015-Environment Management System., 45001:2018-Occupational Health and Safety Management System, 50001:2018- Energy Management System and 55001:2014-Asset Management System.

The financial engineering matched the operational sophistication. Torrent Power's profit increased by 371% YoY to ₹21.71 billion (~$262.36 million) in FY23, mainly due to reduced transmission and distribution losses and higher generation throughout the quarters. This wasn't just growth—it was profitable growth, a rarity in Indian infrastructure.

Managing the energy trilemma—reliability, affordability, and sustainability—required constant balancing. In affluent areas of Ahmedabad, customers demanded 24x7 power and were willing to pay for it. In the industrial clusters of Dadra & Nagar Haveli, competitive tariffs mattered more than premium service. In the slums of Bhiwandi, the challenge was regularizing connections without triggering social unrest.

Competition intensified as success attracted rivals. Adani Power, backed by the group's vast resources, bid aggressively for distribution franchises. Tata Power leveraged its century-old brand and Mumbai operations. JSW Energy brought steel industry connections and deep pockets. Yet Torrent maintained its edge through operational excellence rather than financial muscle.

The regulatory landscape grew more complex with each new territory. Different states had different tariff structures, subsidy regimes, and political dynamics. The T&D losses in license areas of the company is amongst the lowest in the country—a testament to Torrent's ability to navigate this complexity while maintaining operational standards.

Digital transformation went beyond customer interfaces. Predictive analytics identified potential equipment failures before they caused outages. Machine learning algorithms optimized power procurement, balancing spot market purchases with long-term contracts. Blockchain pilots explored peer-to-peer power trading, anticipating a future where every rooftop solar panel could be a mini power plant.

The corporate culture evolved too. From a family-run business with pharmaceutical roots, Torrent had become a professional organization attracting talent from IITs and IIMs. Yet the family values persisted—long-term thinking, conservative financial management, and an almost obsessive focus on execution.

As 2024 progressed, Torrent faced new challenges. Climate change made weather patterns unpredictable, affecting both renewable generation and demand patterns. Cybersecurity threats targeted critical infrastructure. Electric vehicles promised to transform load profiles. Battery storage costs were falling but still not economical at grid scale.

Yet these challenges were also opportunities. Each problem Torrent solved created a moat that competitors would struggle to cross. The combination of generation assets, distribution networks, and customer relationships created synergies that pure-play companies couldn't match. The patient capital from pharmaceutical profits allowed long-term bets that quarterly-focused corporations couldn't make.

The integration story was far from complete. India needed $500 billion in power sector investment by 2030. State distribution companies still lost ₹90,000 crore annually. Rural electrification remained incomplete despite government claims. The energy transition required not just new generation but entirely new grid architecture.

For Torrent, the path forward was clear: continue the patient accumulation of assets, the relentless focus on operational excellence, and the careful navigation of India's complex political economy. They had proven that private companies could deliver public services efficiently. Now they had to prove they could do it at a scale that mattered to a nation of 1.4 billion people aspiring for developed country living standards. The next act wouldn't just be about growing bigger—it would be about reimagining what an energy company could be in the age of climate change and digital transformation.

VIII. The Next Act: Green Hydrogen, Storage & Beyond

The conference room at Torrent's headquarters hummed with nervous energy on a September morning in 2024. Outside, Gujarat's monsoon had finally broken, but inside, the leadership team was contemplating a bet that would dwarf everything they'd done before. The company has already announced that it intends to install about 5-8 GW of PSP capacity entailing investment of Rs 25,000-35,000 crore. For context, this single commitment to pumped storage exceeded the cost of building their entire SUGEN complex three times over.

The logic was inescapable. India's renewable revolution had a fatal flaw—the sun doesn't shine at night, and the wind doesn't always blow. Battery costs were falling but remained prohibitive for grid-scale, long-duration storage. Pumped storage—using excess power to pump water uphill, then releasing it through turbines when needed—was century-old technology. But in the age of intermittent renewables, it had become cutting-edge again.

Torrent Power has identified pumped storage project (PSP) sites in multiple states. Each site required a unique combination of geography (elevation difference), geology (rock stability), hydrology (water availability), and proximity to transmission infrastructure. It was like solving a four-dimensional puzzle across India's diverse terrain.

The breakthrough came with Maharashtra. Torrent Power Ltd has emerged as a successful bidder and has received Letter of Intent (LOI) from Maharashtra State Electricity Distribution Co. Ltd (MSEDCL) on 17th September 2024 for procurement of 1,500 MW/12,000 MWh Energy Storage Capacity from Pumped Hydro Storage Project. This wasn't just another contract—it validated Torrent's storage strategy at a scale that mattered.

The pumped hydro storage project will supply power to MSEDCL for 40 years as part of the deal. Four decades—longer than most solar panels would last, longer than any battery technology on the horizon. This was infrastructure investing at its most fundamental: patient capital meeting societal needs.

By October, the momentum accelerated. This 2,000 MW capacity is inclusive of 1,500 MW capacity for which letter of intent was already issued by MSEDCL on September 17, 2024. Torrent Power has now received allotment of additional 500 MW capacity under the tender taking the total capacity allocated to 2,000 MW. The market was validating what Torrent had seen coming—storage wasn't optional in a renewable future; it was essential.

But pumped storage was just one piece of the puzzle. Torrent Power is actively pursuing opportunities to develop Green Hydrogen and Green Ammonia Production projects to cater to the export and domestic markets. Green hydrogen represented the holy grail of energy transition—a carbon-free fuel that could replace fossil fuels in industries where electrification wasn't feasible: steel, cement, long-distance shipping, aviation.

The second 'Shapath Patra' was submitted for setting up a 1,00,000 Kilo Tonnes Per Annum (KTPA) green ammonia production facility with an investment of Rs 7,200 crore and employment generation for around 1,000 people. Ammonia wasn't just fertilizer anymore—it was becoming a hydrogen carrier, a way to transport green energy across oceans to energy-hungry markets in Japan, Korea, and Europe.

The technical challenges were formidable. Electrolyzers—the devices that split water into hydrogen and oxygen—were expensive and energy-intensive. The round-trip efficiency of making hydrogen, converting it to ammonia, shipping it, and converting it back was barely 30%. But Torrent understood that first-movers in nascent markets often captured outsized returns as technology improved and costs fell.

It is also considering the group captive arrangement for selling renewable power, which involves setting up subsidiaries within Torrent Power. This wasn't just about generating power—it was about creating entirely new business models. Group captive arrangements allowed industrial consumers to partially own renewable projects, bypassing distribution companies entirely. It was distribution disruption from within.

Battery storage exploration proceeded in parallel. While pumped storage worked for large-scale, long-duration needs, batteries excelled at frequency regulation, voltage support, and rapid response. Torrent began pilot projects, testing different chemistries—lithium-ion for performance, sodium-ion for cost, flow batteries for safety. Each technology had its place in the storage ecosystem they were building.

The corporate PPA market opened new frontiers. The company is actively pursuing corporate PPA market opportunities and has already executed 20 MW of PPAs. Tech giants needed clean power for data centers. Manufacturing companies faced pressure from global customers to decarbonize supply chains. Torrent could offer not just renewable power but firm, reliable, round-the-clock clean electricity—combining solar, wind, and storage into baseload renewable power.

The integration of all these elements—renewable generation, pumped storage, batteries, hydrogen production—created synergies competitors couldn't match. Excess solar power during the day could pump water uphill or produce hydrogen. Wind power at night could charge batteries or continue hydrogen production. The portfolio effect smoothed out intermittency and maximized asset utilization.

Risk management became increasingly sophisticated. Weather derivatives hedged against low wind or cloudy periods. Power purchase agreements included inflation adjustments and force majeure clauses. Geographic diversification across states reduced regulatory and weather concentration risk. Financial engineering matched the complexity of physical assets.

The human capital transformation was equally dramatic. Torrent recruited electrochemists from IITs, hired trading teams from commodity markets, brought in data scientists from tech companies. The company that had started with pharmaceutical salesmen and electrical engineers now employed specialists in everything from satellite weather forecasting to blockchain-based energy trading.

Regulatory navigation required new skills. Each state had different renewable purchase obligations, storage mandates, and hydrogen policies. The central government pushed ambitious targets while states worried about grid stability and consumer tariffs. Torrent's approach—patient engagement, technical competence, and willingness to share risks—opened doors that remained closed to more aggressive competitors.

The competitive landscape was evolving rapidly. Oil companies like Indian Oil and Reliance were betting billions on green hydrogen. Global giants like TotalEnergies and Shell were entering Indian renewables. Chinese manufacturers were driving down equipment costs while threatening to dominate supply chains. Torrent's edge wasn't scale or capital—it was integration and execution.

Looking ahead, the challenges were as large as the opportunities. Climate change made weather patterns increasingly unpredictable, affecting both renewable generation and pumped storage hydrology. Cybersecurity threats targeted increasingly digital and distributed energy infrastructure. Technology evolution—from solid-state batteries to direct air capture of CO2—could disrupt carefully laid plans.

Yet Torrent's history suggested they would adapt. They'd navigated from cables to distribution, from distribution to generation, from gas to renewables. Each transition built on previous capabilities while adding new ones. The next act—green hydrogen, storage, and beyond—wasn't a departure from their journey but its logical continuation.

As 2025 dawned, with India hosting COP33 and the world watching its energy transition, Torrent Power stood at an inflection point. The investments they were making—₹57,000 crore in renewables, ₹35,000 crore in storage, ₹7,200 crore in green ammonia—would define not just their future but India's energy landscape for decades. The quiet powerhouse from Gujarat was betting that in the intersection of renewable energy, storage, and green molecules lay the future of not just power, but the entire energy economy.

IX. Playbook: Business & Investing Lessons

The most striking aspect of Torrent Power's journey isn't what they built—it's how they built it. In an industry littered with bankrupt utilities, stranded assets, and regulatory capture, Torrent created a ₹67,311 crore enterprise that consistently delivers both profits and public service. Their playbook offers lessons that extend far beyond power into any capital-intensive, regulated industry.

The Torrent Approach: Patient Capital Meets Operational Excellence

Torrent's foundational insight was that infrastructure investing isn't about financial engineering—it's about operational excellence compounded over decades. When they acquired the Ahmedabad and Surat electricity companies in 1997, they didn't flip them for quick profits. Instead, they spent years fixing basic issues: installing meters, training linemen, computerizing billing. The 58% loss reduction in Bhiwandi didn't happen overnight—it took systematic effort over years, with returns that only materialized after patient investment.

This patience stemmed from their pharmaceutical heritage. Drug development takes 10-15 years; power infrastructure operates on similar timescales. The Torrent family understood that sustainable returns come from solving real problems, not from financial arbitrage. Their willingness to accept lower returns initially for higher returns eventually became their moat.

Vertical Integration as Competitive Advantage

While consultants preached focus and specialization, Torrent built across the entire value chain—generation, transmission, distribution, and now storage. This wasn't empire-building but strategic positioning. Owning distribution gave them guaranteed offtake for generation. Generation assets provided bargaining power with fuel suppliers. Transmission investments connected their assets and captured value others left on the table.

The integration created information advantages. Distribution operations revealed consumption patterns that informed generation investments. Customer complaints highlighted grid weaknesses that guided transmission upgrades. Real-time data from smart meters optimized power procurement. In an industry where information asymmetry drives profits, vertical integration provided an information edge.

More subtly, integration created operational synergies. Engineers moved between generation and distribution, cross-pollinating best practices. Procurement teams leveraged scale across divisions. Financial teams optimized capital allocation across the portfolio. The whole became greater than the sum of its parts.

Managing Regulatory Complexity Across States

India doesn't have one electricity market—it has 28 state markets, each with unique regulations, politics, and economics. Gujarat favors private participation; West Bengal remains skeptical. Maharashtra offers lucrative urban markets; Uttar Pradesh presents governance challenges. Navigating this complexity requires more than legal expertise—it requires cultural intelligence.

Torrent's approach was deceptively simple: align with state objectives, deliver visible results, and build trust through consistency. In Gujarat, they partnered with the government's industrialization agenda. In Maharashtra, they solved Mumbai's satellite city power problems. In Uttar Pradesh, they brought order to Agra's chaotic distribution. Each market required different strategies, but the underlying principle remained constant—solve the state's problems, and regulatory support follows.

They also understood that regulators are people with careers, pressures, and constituencies. Rather than adversarial negotiations, Torrent engaged in technical dialogue, sharing data transparently and proposing solutions that balanced consumer, utility, and state interests. This collaborative approach opened doors that aggressive tactics would have closed.

The Distribution Franchisee Model Innovation

Torrent didn't invent the distribution franchisee model, but they perfected it. The innovation wasn't technical but structural—finding a way for private efficiency to coexist with public ownership. By taking over operations while leaving assets with the state, they sidestepped political opposition to privatization while capturing operational upside.

The model's genius lay in alignment of incentives. Torrent made money by reducing losses; consumers got better service; state utilities shed loss-making operations; politicians avoided privatization backlash. Everyone won—a rarity in zero-sum infrastructure battles.

The franchisee model also provided optionality. If operations improved, Torrent could bid for ownership. If regulations turned adverse, they could exit without stranded assets. This capital-light approach generated returns on equity exceeding 20% while traditional distribution utilities struggled to cover costs.

Capital Allocation Discipline: When to Build vs. Buy

Torrent's capital allocation reveals sophisticated thinking about build versus buy decisions. They built SUGEN when gas was cheap and competitors focused on coal. They bought renewable assets when developers faced financial stress. They acquired distribution franchisees when states desperately needed operational expertise.

The pattern suggests a framework: Build when you have operational advantages and patient capital. Buy when markets are distressed and sellers need exits. Partner when regulatory complexity exceeds operational benefits. Exit when competitive advantages erode or better opportunities emerge.

This discipline extended to saying no. Despite opportunities, Torrent avoided international expansion, coal mining, and equipment manufacturing. They understood their circle of competence—operating Indian power infrastructure—and stayed within it. In a industry full of conglomerate sprawl, focus became a differentiator.

Family Business Governance Done Right

The Torrent story challenges conventional wisdom about family businesses. Rather than nepotism and short-termism, they demonstrated that family ownership could provide patient capital and long-term thinking that public markets couldn't match. The key was governance structure that combined family vision with professional management.

The Mehta family retained strategic control while delegating operations to professionals. Board positions went to independent directors with relevant expertise. Succession planning began years in advance, with next-generation family members gaining experience across divisions before taking leadership roles. Minority shareholders' interests aligned with family interests through transparent reporting and consistent dividends.

This governance model provided stability in a volatile industry. While listed peers faced quarterly earnings pressure, Torrent could make decade-long bets. While private equity-owned infrastructure flipped assets for quick returns, Torrent built for generations. The family's reputation became an asset, opening doors and building trust that money couldn't buy.

Balancing Growth with Profitability in Capital-Intensive Sectors

Infrastructure investing typically faces a cruel tradeoff: growth requires capital, but capital demands returns. Many infrastructure companies grow themselves into bankruptcy, with debt servicing consuming cash flows. Others remain subscale, unable to compete with larger players.

Torrent threaded this needle through portfolio optimization. Stable distribution operations generated cash for generation investments. Efficient operations improved returns without additional capital. Government partnerships reduced capital requirements while maintaining control. Asset recycling—selling mature assets to fund growth—provided capital without dilution.

The renewable pivot exemplified this balance. Rather than abandoning profitable gas plants for fashionable renewables, Torrent used gas plant cash flows to fund renewable investments. They didn't chase growth at any cost but grew at sustainable returns. The result: industry-leading growth without balance sheet stress.

The Operational Excellence Dividend

Ultimately, Torrent's playbook reduces to operational excellence. In an industry where 15-20% T&D losses are normal, achieving 6% creates enormous value. When forced outage rates average 5%, achieving 0.06% provides competitive advantage. Where customer satisfaction scores languish below 50%, achieving 68% builds pricing power.

This excellence wasn't achieved through innovation but through execution. Basic blocking and tackling—meter reading, bill collection, maintenance scheduling, inventory management—done consistently well. Small improvements compounded: 1% annual efficiency gains over 20 years double productivity. In capital-intensive industries with long asset lives, operational excellence provides the highest returns.

The lesson for investors is profound. In glamorous sectors, operational excellence gets competed away. In regulated, capital-intensive, politically complex industries, operational excellence becomes a moat. Torrent found a space where their capabilities matched market needs, then executed relentlessly for decades. The result wasn't just a successful company but a template for infrastructure investing in emerging markets.

As India requires $500 billion in power sector investment and similar amounts in roads, ports, airports, and urban infrastructure, the Torrent playbook becomes increasingly relevant. Patient capital, operational excellence, regulatory navigation, and stakeholder alignment—these aren't just business strategies but national imperatives. Torrent Power proved that private companies could deliver public goods profitably. In that proof lies the future of not just Indian infrastructure but emerging market development globally.

X. Analysis & Bear vs. Bull Case

Every investment thesis contains its own contradiction. Torrent Power's strengths—operational excellence, regulatory relationships, integrated operations—could become weaknesses in a rapidly evolving energy landscape. The bull and bear cases aren't just about Torrent but about India's energy future and the role of traditional utilities in an increasingly distributed, digital, and decarbonized world.

Bull Case: The Compounder's Dream

The bull case starts with India's structural energy deficit. Despite adding 200 GW of capacity in the past decade, per capita electricity consumption remains at 1,200 kWh annually—one-third of the global average, one-tenth of developed countries. As 400 million Indians enter the middle class by 2030, electricity demand will double. Someone has to meet this demand, and Torrent's track record suggests they'll capture more than their share.

Torrent Power, the Rs 27,183-crore integrated power utility of the Rs 41,000-crores Torrent Group, is one of the largest companies in the country's power sector with presence across the entire power value chain -- generation, transmission, and distribution. This integration becomes more valuable as the energy system grows complex. Distributed solar needs grid stability. Electric vehicles require charging infrastructure. Green hydrogen demands renewable power. Companies that can orchestrate across the value chain will capture premium returns.

The renewable pipeline validates the growth trajectory. With 1,746 MW operational and 3,279 MW under development, Torrent already has visibility to doubling renewable capacity. The company has submitted a Shapath Patra' to achieve 10 Gigawatt (GW) of installed Renewable Energy (RE) capacity by 2030, with an investment of Rs 57,000 crore. This investment is expected to generate direct and indirect employment for around 25,000 people. At current valuations, this pipeline alone justifies the market capitalization.

Distribution remains the crown jewel. While generation faces commodity risk and transmission offers regulated returns, distribution provides pricing power. Torrent's 38.5 lakh customers across affluent markets generate predictable cash flows. The T&D losses in license areas of the company is amongst the lowest in the country—this operational efficiency gap widens as peers struggle with aging infrastructure and political interference.

The pumped storage opportunity could be transformative. The company has already announced its intentions to install about 5 to 8 GW of pumped storage capacity with an investment of INR 25,000 to INR 35,000 crore. With renewable penetration increasing, storage becomes essential infrastructure. Early movers will lock in sites, permits, and contracts that create 40-year annuity streams. Torrent's operational expertise in complex infrastructure projects provides an edge in this nascent market.

Green hydrogen represents optionality with asymmetric upside. Torrent has further made a commitment to develop a 100,000 tons per-year renewable ammonia production plant in Gujarat, supported by an investment of $860 million. If green hydrogen becomes competitive with grey hydrogen by 2030—as costs curves suggest—early positions could generate venture-like returns. If not, the investment is small enough to absorb without material impact.

Market Cap: 67,311 Crore suggests the market hasn't fully valued this pipeline. Trading at 2.5x book value while generating 18% ROE, Torrent offers growth at a reasonable price. Compare this to global renewable pure-plays trading at 4-5x book with similar returns, and the valuation gap becomes apparent.

The Torrent Group backing provides financial flexibility. With pharmaceutical cash flows and family wealth, Torrent can weather downturns that would bankrupt leveraged competitors. This patient capital advantage compounds over cycles—buying distressed assets in downturns, investing counter-cyclically, and maintaining operational standards when others cut corners.

Regulatory relationships built over decades create switching costs. Regulators know Torrent delivers on commitments. States trust them with critical infrastructure. This reputational capital takes decades to build and provides preferential access to opportunities. In a relationship-driven market like India, trust is the ultimate moat.

Bear Case: Disruption and Regulatory Quicksand

The bear case begins with technological disruption. Distributed solar plus batteries could make centralized generation obsolete. Peer-to-peer energy trading through blockchain could eliminate distribution utilities. Electric vehicles with vehicle-to-grid capability could provide storage cheaper than pumped hydro. Torrent's integrated utility model could become the electricity equivalent of landline telephones.

Regulatory risks multiply across states. Each election brings new energy ministers with different priorities. Populist pressures for free electricity intensify. Agricultural subsidies bankrupt distribution companies. Renewable purchase obligations change arbitrarily. Operating across multiple states multiplies these risks—one adverse regulatory change could contaminate the entire portfolio.

Fuel supply dependencies remain concerning. Despite renewable growth, 2,730 MW of gas capacity depends on imported LNG prices. Global gas markets face volatility from geopolitical tensions. Domestic gas allocation policies change with political priorities. A sustained spike in gas prices could strand these assets or force losses on fixed-price contracts.

Competition intensifies from all directions. Adani Green Energy, backed by the group's infrastructure ecosystem, bids aggressively for renewable projects. ReNew Power brings international capital and pure-play focus. State utilities, under political pressure, might reverse privatization initiatives. Chinese manufacturers integrate forward into development. Oil companies leverage balance sheets to buy market share. Torrent's advantages erode as capital floods the sector.

Capital intensity of new projects pressures returns. Pumped storage requires ₹35,000 crore investment with 40-year paybacks. Green hydrogen needs technology bets that might not materialize. Grid modernization demands continuous investment. Unlike software businesses that scale with minimal capital, infrastructure investing requires constant feeding of the capital beast.

Technology transition risks compound. Torrent must simultaneously manage legacy thermal assets, scale renewable generation, develop storage solutions, and explore green hydrogen. Each technology has different skills, suppliers, and success factors. Organizational complexity increases exponentially. The company that mastered gas turbines might struggle with battery chemistry.

Stranded asset risk looms large. The 362 MW coal plant faces premature retirement as climate policies tighten. Gas plants might become uneconomical as renewable plus storage costs decline. Transmission infrastructure could be bypassed by distributed generation. Distribution networks might be leapfrogged in rural areas by solar microgrids. Billions in book value could evaporate as energy transitions accelerate.

Corporate governance concerns persist despite improvements. Family control limits hostile takeovers that might unlock value. Related-party transactions with other Torrent Group companies raise questions. Succession planning depends on family dynamics. Minority shareholders remain vulnerable to decisions prioritizing family over financial returns.

ESG pressures might limit capital access. Despite renewable growth, fossil fuel exposure could trigger divestment. International capital markets increasingly screen out companies with coal assets. Green bonds require extensive disclosure and use restrictions. The cost of capital could increase relative to pure-play renewable competitors.

Execution risk scales with ambition. Managing 10 GW renewable development while building pumped storage and exploring hydrogen stretches organizational capacity. Each project faces land acquisition challenges, environmental clearances, and local opposition. One high-profile failure could damage the reputation built over decades.

The Verdict: Gradual Then Sudden

The reality likely lies between these extremes. Torrent faces real disruption risks but has time to adapt. India's energy transition will be gradual then sudden—slow infrastructure changes punctuated by technology tipping points. Companies that navigate this transition successfully will generate enormous value; those that don't will become case studies in disruption.

Torrent's integrated model provides transition options. Distribution operations generate cash to fund new technologies. Operational excellence culture can be applied to new domains. Regulatory relationships open doors for emerging opportunities. Patient capital allows riding out volatility. The question isn't whether Torrent can survive disruption but whether they can profit from it.

For investors, Torrent represents a bet on execution over innovation, operations over financial engineering, and India's energy transition being evolutionary rather than revolutionary. It's a compounder's stock—steady returns from operational excellence rather than spectacular gains from disruption. In a portfolio context, it provides defensive exposure to India's structural energy growth while maintaining optionality on emerging technologies.

The bear case risks are real but manageable. The bull case upside is significant but not spectacular. This asymmetry—limited downside with steady upside—defines Torrent's investment appeal. It's not a moonshot but a steady climber, not a disruption but an adaptation story. In the infrastructure investing universe, where many promise and few deliver, Torrent Power's track record of execution makes it a rare find: a boring business in an exciting industry, generating exciting returns from boring operations.

XI. Epilogue & Final Reflections

Standing at the SUGEN plant on a clear winter morning, watching the sun rise over endless rows of solar panels while gas turbines hummed in the background, you can see India's entire energy transition in microcosm. The old and new coexist, not in conflict but in careful orchestration. This is the Torrent story—not disruption but integration, not revolution but evolution, not headlines but execution.

The Quiet Execution Story vs. High-Profile Peers

While Adani makes global headlines with renewable acquisitions and Reliance announces hydrogen moonshots, Torrent quietly reduces losses in Bhiwandi by another percentage point. The contrast is instructive. In infrastructure, the tortoise often beats the hare. Torrent's below-the-radar approach avoided regulatory scrutiny, political interference, and market speculation that plagued higher-profile peers.

This quietness was strategic. Every announced project attracted competition, regulatory attention, and local opposition. By maintaining a low profile, Torrent could negotiate better terms, move faster through approvals, and avoid bidding wars. Their largest victories—the distribution franchisees, the DNHDD privatization—were won before competitors knew there was a contest.

The financial markets are belatedly recognizing this value. While story stocks gyrated with newsflow, Torrent compounded steadily. A ₹1,000 investment at listing would be worth ₹15,000 today, excluding dividends. Not spectacular by tech standards, but remarkable for a utility. This is the paradox of infrastructure investing: the best returns come from the most boring operations.

What Torrent Power Tells Us About India's Energy Future

Torrent's evolution maps India's energy trajectory. From addressing basic reliability in the 1990s to efficiency in the 2000s to sustainability in the 2020s, each phase required different capabilities. The companies that survive aren't those with the best technology or most capital, but those that adapt to India's unique context—federal complexity, price sensitivity, infrastructure deficit, and rapid growth.

India's energy future won't follow Western templates. Distributed solar will coexist with coal plants. Electric two-wheelers will proliferate before cars. Digital payments will leapfrog smart meters. Green hydrogen might succeed in niches while failing broadly. This messy, pragmatic, incremental transition favors operators over innovators, execution over strategy.

Torrent's success suggests what works in India: patient capital, operational excellence, regulatory navigation, and stakeholder alignment. What doesn't work: technology for technology's sake, financial engineering without operational improvement, and ignoring political economy. These lessons extend beyond power into all infrastructure sectors.

Lessons for Infrastructure Investors Globally

The Torrent playbook translates across emerging markets. Whether Indonesian toll roads, Brazilian water utilities, or African telecom towers, the principles remain constant: infrastructure investing is about operations, not finance. Regulatory relationships matter more than technology. Local knowledge beats global expertise. Patient capital outperforms smart money.

The vertical integration lesson challenges conventional wisdom. In developed markets with stable regulations and mature infrastructure, specialization makes sense. In emerging markets with regulatory uncertainty and infrastructure gaps, integration provides resilience. Controlling your inputs and outputs, understanding the full value chain, and maintaining operational flexibility matter more than theoretical efficiency.

The family ownership model deserves reconsideration. While public markets provide capital and discipline, family ownership provides patience and commitment. The optimal structure might be Torrent's hybrid: family control with professional management, public listing with concentrated ownership, growth with governance. This model is replicable across emerging market infrastructure.

The Family Business Evolution Model

The Mehta family's journey from pharmaceutical sales to infrastructure champion illustrates successful business evolution. Each generation built on the previous while adapting to new opportunities. The founder created entrepreneurial culture. The second generation professionalized operations. The third generation drives technological transformation. This isn't preservation but renewal.

The key was avoiding the three curses of family businesses: nepotism, complacency, and conflict. Torrent mandated external experience before family members joined. They maintained meritocratic culture despite family control. They separated ownership from management. They planned succession years in advance. These governance innovations allowed family businesses advantages—patience, commitment, reputation—without typical disadvantages.

This model offers hope for India's thousands of family businesses facing generational transitions. Rather than selling to private equity or listing prematurely, they can professionalize while maintaining control. Rather than avoiding complex sectors, they can build capabilities gradually. Rather than family or professional management, they can have both.

Biggest Surprises from the Research

The first surprise was the consistency of execution across decades and domains. From cables to distribution to generation to renewables, Torrent maintained operational excellence. This wasn't luck but systematic capability building. They didn't just learn lessons; they institutionalized them.

The second surprise was the sophistication behind the simplicity. Torrent appears boring—no cutting-edge technology, no financial innovation, no global ambitions. But beneath this simplicity lies sophisticated thinking about risk, optionality, and value creation. They understood that in infrastructure, boring is beautiful.

The third surprise was the absence of major mistakes. Every infrastructure company has stranded assets, failed projects, or regulatory disasters. Torrent's record is remarkably clean. This wasn't conservatism—they made bold bets on gas, distribution franchisees, and now storage. But they sized bets appropriately, managed risks carefully, and executed relentlessly.

The Path Forward

As India accelerates toward developed country status, infrastructure becomes destiny. The companies that build, operate, and modernize this infrastructure will shape India's future. Torrent Power, with its proven execution, patient capital, and integrated operations, is positioned to play a central role.

But success isn't guaranteed. The energy transition accelerates. Technology disrupts. Regulations shift. Competition intensifies. Torrent must evolve from operational excellence in stable technologies to innovation in emerging ones. They must balance the efficiency of algorithms with the wisdom of experience. They must serve shareholders while solving societal challenges.

The next decade will test whether Torrent can maintain its edge as the industry transforms. Can they lead in green hydrogen while managing gas plants? Can they pioneer storage while maintaining distribution? Can they stay entrepreneurial while growing institutional? These questions will determine whether Torrent remains a quiet powerhouse or becomes another infrastructure incumbent disrupted by change.

Final Thoughts

In the end, Torrent Power's story is about more than business success. It's about how private enterprise can solve public challenges. It's about how operational excellence beats financial engineering. It's about how patient capital creates lasting value. It's about how family businesses can modernize without losing their soul.

As the world grapples with energy transition, climate change, and infrastructure gaps, the Torrent model offers lessons. Not every problem needs disruption; some need patient execution. Not every company needs to be a unicorn; some need to be workhorses. Not every investment needs to be spectacular; some need to be sustainable.

The quiet powerhouse from Gujarat reminds us that in infrastructure, the race goes not to the swift but to the steady, not to the brilliant but to the diligent, not to the disruptors but to the operators. In a world obsessed with the new, Torrent proves the enduring value of doing the basics brilliantly. That might be the most important lesson of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube