Titagarh Rail Systems: From Tea Estate Accountant to Train Manufacturing Titan

I. Introduction & Cold Open

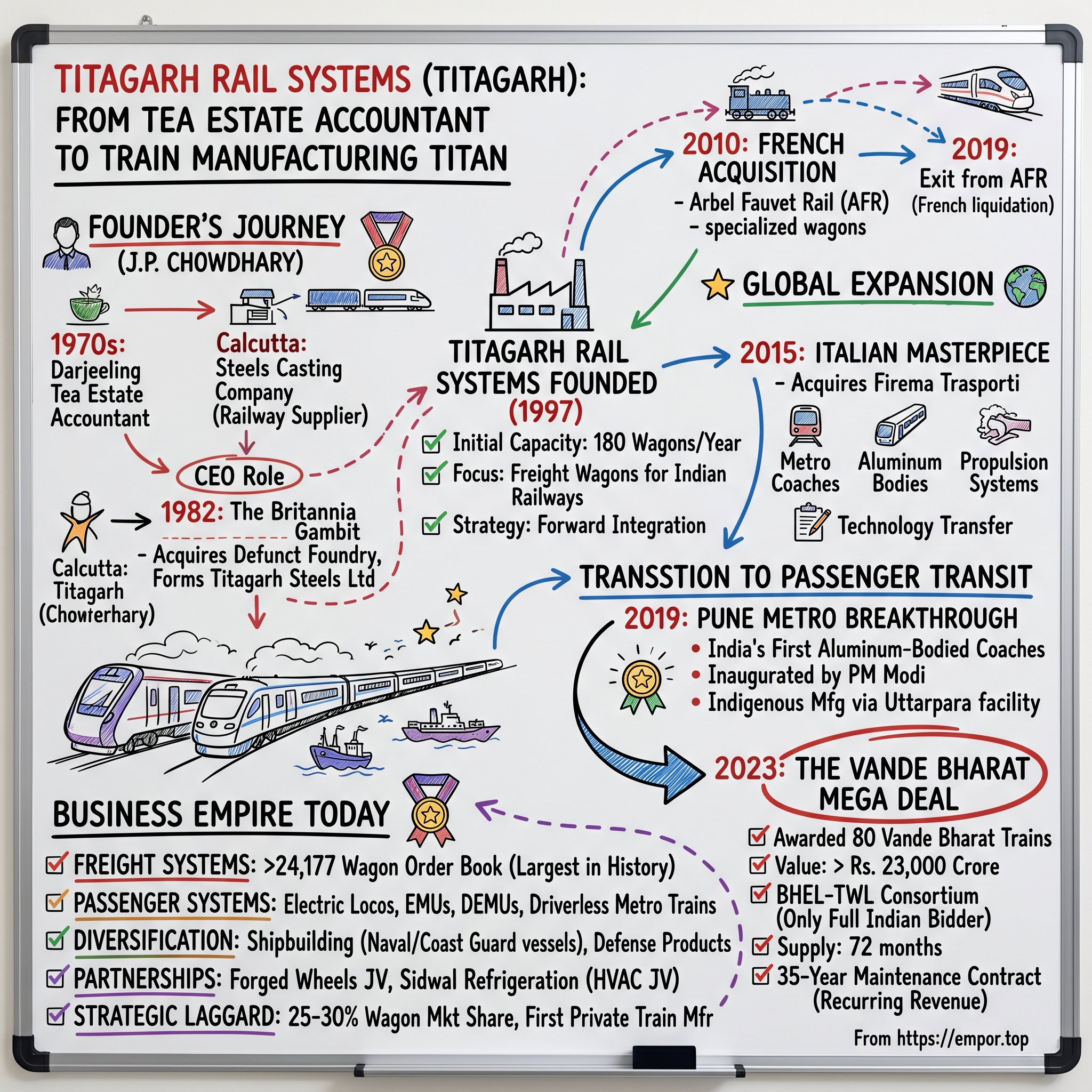

Picture this: A young accountant hunched over ledgers in a misty Darjeeling tea estate in the 1970s, meticulously tracking bushels and wages, dreams bigger than the Himalayan foothills surrounding him. Four decades later, that same man's company would manufacture the aluminum-bodied coaches that Prime Minister Narendra Modi would personally inaugurate, build Vande Bharat trains that symbolize India's railway modernization, and command a quarter of India's wagon manufacturing market. This is the improbable story of Jagadish Prasad Chowdhary and Titagarh Rail Systems.

How does an accountant with no engineering background build India's largest private rail manufacturing empire? How does a company that started with 180 wagons per year end up with an order book of 24,177 wagons—the largest in Indian railway history? And perhaps most intriguingly, how does a firm from Barrackpore, West Bengal, end up owning Italian metro manufacturers and earning one of Italy's highest civilian honors? Today, Titagarh Rail Systems Limited stands as India's engineering marvel—incorporated in 1997, it has grown into the nation's largest private rail manufacturing empire with a market capitalization of ₹10,905 crore, revenue of ₹3,644 crore, and profit of ₹239 crore. The company is the only Indian company that manufactures both wagons and coaches, commanding a market share of 25-30% in the wagon manufacturing industry. But the numbers only tell part of the story.

This is a tale of audacious acquisitions from Barrackpore to Italy, of turning around bankrupt foundries into profitable enterprises, of a company that dared to dream beyond India's borders while staying deeply rooted in the vision of Atmanirbhar Bharat. It's about how a firm that began producing 15 wagons per month in 1997 would go on to win contracts for 24,177 wagons and 80 Vande Bharat trains worth over ₹23,000 crore.

As we dive into this six-hour journey through Titagarh's history, we'll explore how strategic government relationships, international technology acquisitions, and perfect timing with India's infrastructure supercycle created one of the most compelling industrial stories in modern India. From foundries to freight, local to global, wagons to Vande Bharat—this is the Titagarh playbook.

II. The Founder's Journey: Jagadish Prasad Chowdhary

The mist rolls through the tea gardens of Darjeeling in the early 1970s. Among the ledgers tracking tea production and worker wages sits a young account assistant named Jagadish Prasad Chowdhary. The work is steady but unremarkable—recording transactions, balancing books, watching the seasonal rhythms of the plantation economy. Yet something stirs within him, a restlessness that the mountain air cannot quiet. Chowdhary makes the decision that would define his life—he leaves the mountains for the chaos of Calcutta (now Kolkata). He takes up work as an accountant at a steel casting company that supplied materials to the Indian Railways. Here, in the industrial heartland of Bengal, surrounded by the clang of metal and the constant movement of freight, Chowdhary gets his first real taste of the railway ecosystem. The numbers he tracks are no longer about tea bushels but about bogies, couplers, and the intricate supply chain that keeps India's lifeline—its railways—running.

What separates Chowdhary from countless other accountants of his generation is his ability to see beyond the ledger. While others saw numbers, he saw inefficiencies. While others saw a steady job, he saw opportunities. He eventually rises to become Chief Executive Officer (CEO) of the steel castings company, learning not just the financial mechanics but the operational intricacies of supplying to one of the world's largest railway networks.

The Britannia Gambit

Then comes 1982—the year that changes everything. The government-owned Britannia Engineering lies defunct, its foundry division in Titagarh, Barrackpore, under liquidation. Where others see industrial decay, Chowdhary sees potential. He acquires the defunct foundry division, renaming it Titagarh Steels Limited (TSL), and begins production of railway casting components, specifically bogies and couplers & crossings, turning around the operations of the foundry in record time.

This isn't just a business acquisition; it's a resurrection story. The foundry that couldn't survive under government ownership begins to thrive under Chowdhary's leadership. He understands something fundamental: Indian Railways needs reliable suppliers, and reliability in this business isn't just about product quality—it's about understanding the bureaucratic labyrinth, building relationships, and most importantly, delivering on time.

The Paper Mill Interlude

Chowdhary's reputation as a turnaround specialist grows. In 1994, he's invited to present a rehabilitation plan for two paper mills of the sick Titagarh Paper Mills Company Limited, which are subsequently spun off into separate companies through a court-sanctioned scheme. This experience in corporate restructuring and working with the Board for Industrial and Financial Reconstruction (BIFR) would prove invaluable in his future acquisitions.

Beyond Business: The Institution Builder

But Chowdhary isn't content with just business success. He serves as President of the Confederation of Indian Industry (CII), President of the All India Management Association, President of the Indian Chamber of Commerce from 1994 to 1995, and President of the All India Organization of Employers. These aren't ceremonial positions—they represent his evolution from entrepreneur to industry statesman, building the networks and credibility that would prove crucial when Titagarh needed government contracts and international partnerships.

Now aged 76 years, Jagadish Prasad Chowdhary serves as the executive chairman of the company, having built not just a business but an institution. His journey from tea estate accountant to railway magnate isn't just about personal ambition—it's about understanding that in India's infrastructure story, the real opportunity lies not in following the established players but in finding the gaps they've left behind.

The foundry in Titagarh continues to operate today, a testament to a vision that began in the ledgers of a Darjeeling tea estate. But this was just the beginning.

III. The Birth of Titagarh Rail Systems (1997)

July 3, 1997. India is six years into economic liberalization. The Sensex hovers around 4,000. The railway sector, long dominated by government-owned production units and a handful of established players, seems impenetrable to newcomers. Yet on this day, Jagadish Prasad Chowdhary founds Titagarh Rail Systems Limited to manufacture railway wagons, starting with an annual production capacity of just 180 wagons.

To put this in perspective, Indian Railways at the time needed thousands of wagons annually. Starting with 180 wagons per year—that's 15 wagons per month—seemed almost quixotic. But Chowdhary understood something his competitors didn't: the post-liberalization Indian economy would need exponentially more freight capacity, and the government's own production units couldn't keep pace.

The Strategic Pivot

The real genius wasn't in entering wagon manufacturing—it was in how Chowdhary approached it. The founder decided to add more value to his propositions, venturing into making entire wagons for freight, moving beyond just manufacturing railway components. This vertical integration strategy meant Titagarh could control quality from foundry to finished product, a crucial differentiator when bidding for Indian Railways contracts.

The company began producing 15 wagons per month with a vision to become the leader in the Indian market, embarking on a gradual but determined path, with forward integration from foundry manufacturing enabling it to achieve its goal and become a significant exporter of freight wagons and components from India.

The Infrastructure Context

The late 1990s were a peculiar time for Indian infrastructure. The economy was growing, but railway investment hadn't kept pace. Freight movement was becoming a bottleneck for economic growth. Coal needed to move from mines to power plants. Steel needed to reach construction sites. Agricultural produce needed to reach ports. The existing wagon fleet was aging, and replacement demand was building up like pressure in a boiler.

Indian Railways' own production units—Hindustan Engineering in Kolkata, Bharat Wagon in Muzaffarpur—were struggling with inefficiencies and couldn't meet the growing demand. Private players like Texmaco and Jessop were present but focused on their traditional segments. This gap in the market was Titagarh's opportunity.

Building the Foundation

The early years were about establishing credibility. Every wagon delivered on time was a reference. Every quality certification was a calling card. The company's location in Titagarh, West Bengal, wasn't accidental—it was close to the eastern railway headquarters, near the coal belt, and had access to skilled labor familiar with heavy engineering.

The business was structured into what would become four core divisions: - Railway Freight: The bread and butter, focusing on wagons for coal, iron ore, cement - Railway Transit: A future aspiration that would materialize later - Engineering: Leveraging the foundry capabilities for specialized components - Shipbuilding: Added subsequently through acquisitions

The Order Book Build

The transformation from 180 wagons per year to becoming India's largest private player didn't happen overnight. It was a methodical expansion:

- Phase 1 (1997-2000): Establishing production processes, achieving quality certifications

- Phase 2 (2000-2005): Scaling up capacity, diversifying wagon types

- Phase 3 (2005-2010): Becoming a significant player, competing for large orders

By the mid-2000s, Titagarh wasn't just another wagon manufacturer—it was becoming a force to reckon with. The company had cracked the code of working with Indian Railways: understanding their procurement processes, meeting their technical specifications, and most importantly, delivering consistently.

The Competitive Advantage

What set Titagarh apart wasn't just manufacturing capability—it was the integrated approach:

- Backward Integration: Control over raw material through the foundry

- Design Capabilities: In-house design team understanding Indian Railways' evolving needs

- Financial Strength: Ability to handle long working capital cycles typical of railway contracts

- Relationship Capital: Chowdhary's decades of credibility with Indian Railways

The company also pioneered several wagon designs suited for Indian conditions—higher payload capacity, better brake systems, designs optimized for Indian rail tracks. These weren't just products; they were solutions to specific Indian Railways problems.

The Numbers Tell the Story

From 180 wagons in 1997, the company's capacity would grow exponentially. By 2010, Titagarh would be producing thousands of wagons annually. The revenue trajectory was even more impressive—from a few crores in the late 1990s to hundreds of crores by the end of the first decade.

But perhaps the most important number was market share. The company would eventually command 25-30% of the wagon manufacturing industry, making it the dominant private player in a sector once thought impregnable.

The foundation laid in 1997 wasn't just for a wagon manufacturing company—it was for an industrial conglomerate that would eventually manufacture everything from metro coaches to naval vessels. But first, Titagarh needed to look beyond India's borders.

IV. The International Expansion Playbook (2010-2019)

French Acquisition - Arbel Fauvet Rail (2010): The First Overseas Gambit

July 2010. The European debt crisis is in full swing. French industry is reeling. In this chaos, Titagarh makes a move that would have seemed unthinkable a decade earlier—an Indian wagon manufacturer acquiring a European rail company.

Titagarh Rail Systems purchases French rail wagon maker Arbel Fauvet Rail (AFR) for €15 million (its first overseas acquisition), which had gone into receivership in February 2009. Titagarh turns around AFR with the subsidiary's revenue rising from ₹99.5 million in 2010-11 to ₹1.64 billion in 2011-12, and employee headcount almost doubling from 85 to 150.

The acquisition wasn't just about buying assets—it was about acquiring European technology, certifications, and market access. AFR brought with it decades of engineering expertise in specialized wagons, particularly for the European market where specifications and safety standards were fundamentally different from India.

The Turnaround Playbook

The AFR turnaround followed a pattern Chowdhary had perfected in India: - Immediate cash injection to restart operations - Retention of key technical talent (hence the doubling of headcount) - Leveraging Indian cost advantages for components while maintaining European assembly - Using AFR's certifications to bid for European contracts

The revenue surge from ₹99.5 million to ₹1.64 billion in just one year wasn't organic growth—it was resurrection. Orders that had been on hold during receivership were reactivated. Customers who had written off AFR returned.

The French Exit

But not all acquisitions end in triumph. A French commercial court ordered AFR's liquidation in July 2019, and Titagarh announced its exit the next month. Vice-chairman Umesh Chowdhary stated that AFR had been making losses of €4-5 million annually for the past three years and would have required more capital to reach profitability. Titagarh had invested ₹1 billion in AFR since acquiring it.

The AFR experience was expensive education. European rail markets were more challenging than anticipated—entrenched competition, different procurement processes, and the high cost of European operations. But the lessons learned would prove invaluable for the next, more successful European adventure.

Italian Masterpiece - Firema Acquisition (2015): The Game Changer

If AFR was education, Firema was graduation with honors.

On July 16, 2015, Titagarh acquired a 90% stake in Italian rail equipment firm Firema Trasporti for an estimated €25 million, with the remaining 10% held by Adler Plastics SpA. In June 2017, Titagarh acquired the 10% stake from Adler Plastics for an undisclosed amount, and the company was subsequently renamed Titagarh Firema SpA.

Firema wasn't just another distressed asset—it was a century-old company with capabilities Titagarh desperately needed: metro coach manufacturing, aluminum body construction, and propulsion systems. This acquisition marked a significant milestone, making Titagarh the first private Indian company to gain access to cutting-edge technology in modern passenger rolling stock and propulsion systems, integrating Firema's extensive 100-year industry experience.

The Umesh Chowdhary Factor

This is where the second generation makes its mark. Umesh Chowdhary was central to the firm's inroads into the Italian market, with his impact so immense that Italy bestowed one of its highest civilian awards on him, the Cavaliere Ordine della Stella d'Italia (Knight of the Order of the Star of Italy).

The Firema acquisition wasn't just managed better than AFR—it was transformational. Unlike AFR, which remained a standalone European operation, Firema became integrated into Titagarh's global strategy. Technology transfer began immediately. Italian engineers traveled to India. Indian engineers trained in Italy. The fusion of Italian design elegance with Indian cost engineering created a powerful combination.

The Strategic Acquisitions Portfolio

Beyond the headline European acquisitions, Titagarh was building a portfolio of strategic capabilities:

Titagarh acquired Corporated Shipyard in 2012 and merged it into Titagarh Marines to manufacture ships for the Indian Navy, with Corporated Shipyard winning its first defence contract in 2017.

In 2015, Titagarh acquired the brand name and know-how of French cast steel bogie manufacturer Sambre et Meuse.

Each acquisition added a piece to the puzzle: - Corporated Shipyard: Entry into defense and naval contracts - Sambre et Meuse: Advanced bogie technology crucial for modern rolling stock

The Technology Transfer Dividend

The real value of international expansion wasn't in European revenues—it was in capability building. The aluminum body construction technology from Firema would enable Titagarh to win the Pune Metro contract. The propulsion systems expertise would be crucial for Vande Bharat. The European certifications would open doors to global markets.

By 2019, Titagarh had transformed from an Indian wagon manufacturer to a global rail systems company. The international expansion playbook—acquire distressed assets, transfer technology, integrate capabilities—had mostly worked. AFR was a costly lesson, but Firema was a masterpiece.

The stage was now set for Titagarh to leverage these international capabilities for its biggest domestic opportunities yet.

V. The Pune Metro Breakthrough & Technology Evolution

The Aluminum Revolution

2019 marks a watershed moment in Titagarh's evolution. The company is awarded the contract to supply 102 aluminum-bodied metro rail coaches for Pune Metro by Maha Metro, with 3 of the total 34 rakes manufactured at the Firema plant in Italy and the remaining 31 trainsets manufactured at TRSL's facility in Uttarpara, Kolkata.

This wasn't just another metro contract. This was India's first indigenously manufactured aluminum-bodied metro coach project—a technological leap that would typically be the domain of global giants like Bombardier, Alstom, or Siemens. The aluminum body construction, compared to traditional stainless steel, offered several advantages: 15-20% weight reduction, better corrosion resistance, and improved energy efficiency—crucial for urban transit systems where acceleration and deceleration are constant.

The Technology Transfer Symphony

The Pune Metro project exemplified the fruit of the Firema acquisition. Italian expertise in aluminum welding—a specialized skill requiring different techniques than steel—was transferred to the Uttarpara facility. Italian technicians spent months in Kolkata. Indian engineers completed specialized training in Italy. The first three rakes manufactured in Italy served as the template, the learning laboratory for the Indian operations.

The company proudly unveiled India's pioneering aluminum-bodied metro coaches, produced indigenously for the Pune Metro project, in alignment with India's Make In India and Atmanirbhar Bharat initiatives.

The Prime Minister's Validation

The aluminum-bodied coaches became the first in the country, an achievement regarded as so significant that the route's opening was inaugurated by Prime Minister Narendra Modi. When the Prime Minister of the world's largest democracy inaugurates your product, you've transcended from supplier to nation-builder. This wasn't just political theater—it was validation of indigenous capability in high-technology manufacturing.

Building Credibility for Bigger Orders

The Pune Metro success created a demonstration effect. Other metro corporations—traditionally conservative in vendor selection—took notice. If Titagarh could deliver aluminum-bodied coaches matching global standards, what else could they do?

The credibility cascade began: - Technical Credibility: Aluminum body construction proved Titagarh could handle complex manufacturing - Project Management Credibility: On-time delivery of a complex, high-visibility project - Political Credibility: Alignment with national manufacturing priorities - Quality Credibility: Coaches performing at par with international standards

The Technology Evolution Blueprint

The Pune Metro project revealed Titagarh's technology absorption model:

- Acquire Technology (through Firema acquisition)

- Pilot in Controlled Environment (3 rakes in Italy)

- Transfer to India (31 rakes in Kolkata)

- Indigenize and Optimize (local supplier development)

- Scale and Compete (bid for more metro projects)

This wasn't technology transfer in the traditional sense—it was technology transformation. The aluminum coaches manufactured in Kolkata weren't mere copies of Italian designs. They were adapted for Indian conditions: higher passenger density, different climate considerations, and local maintenance capabilities.

The Ripple Effects

Post-Pune, the order pipeline began filling rapidly. In April 2023, the company secured a ₹3.5 billion contract to supply rolling stock for the Ahmedabad Metro. The Pune success had opened doors that had been closed to Indian manufacturers for decades.

But more importantly, it changed the conversation. Titagarh was no longer competing on price alone—it was competing on technology. The company that started with basic freight wagons was now in the same conversation as global transit giants.

The Indigenous Innovation Leap

Titagarh delivered its first indigenously manufactured driverless train set for BMRCL's Yellow Line, marking a historic milestone in India's rail manufacturing journey. From aluminum bodies to driverless systems—each project pushed the technological envelope further.

The evolution wasn't happening in isolation. Each project built capabilities for the next. The aluminum expertise from Pune enabled lighter, more efficient designs. The driverless technology demonstrated automation capabilities. The cumulative effect was a company rapidly climbing the technology ladder.

Strategic Implications

The Pune Metro breakthrough fundamentally repositioned Titagarh in the market hierarchy:

- From Vendor to Partner: Metro corporations began seeing Titagarh as a technology partner, not just a supplier

- From Follower to Leader: First indigenous aluminum coaches positioned Titagarh as an innovation leader

- From Local to Global: International manufacturers started viewing Titagarh as a serious competitor

The technology evolution also changed the company's margin profile. Metro coaches commanded better margins than freight wagons. The maintenance contracts that came with metro projects provided long-term revenue visibility. The shift from freight to transit was a shift up the value chain.

As 2019 drew to a close, Titagarh stood transformed. The company that had acquired struggling European firms was now transferring their technology to India and competing for the country's most prestigious projects. But the biggest opportunity—and challenge—was yet to come.

VI. The Vande Bharat Mega Deal (2023)

The Stage is Set

- India's railway modernization has shifted into highest gear. The Vande Bharat Express, launched in 2019, has captured the nation's imagination—sleek, semi-high-speed trains symbolizing a new India. The government announces one of the largest railway tenders in history: 200 Vande Bharat trains. The stakes couldn't be higher.

The Tender Process and Competition Landscape

The bidding arena looked like a Who's Who of global rail manufacturing. French rolling stock major Alstom, Medha Servo with Swiss firm Stadler Rail, German major Siemens with state-owned BEML, BHEL JV, and TMH-RVNL, having qualified in the technical round. Against this formidable competition, the BHEL-Titagarh Wagons Ltd. (BHEL-TWL) consortium positions itself.

BHEL-TWL consortium has been awarded an order for 80 Vande Bharat Trains in one of the biggest Railway tenders for manufacturing-cum-maintenance of Vande Bharat Trains. In the prestigious tender for 200 trains, the BHEL-led consortium emerged as the L2 bidder against stiff competition, and has been awarded a contract for 80 Vande Bharat Trains, valued at more than Rs.23,000 Crore.

The Numbers That Matter

The scale is staggering: The order value comprises supply of trainsets for Rs.9,600 Crore and balance for maintenance of the same for a period of 35 years. This isn't just about manufacturing trains—it's about creating a 35-year revenue stream, fundamentally changing Titagarh's business model from transaction to relationship.

The RVNL-Transmashholding consortium had a bid of Rs 120 crore per Vande Bharat train and is looking to manufacture all 200 steel Vande Bharat rakes while the consortium of Bharat Heavy Electricals Ltd (BHEL) and Titagarh Wagons emerged as the second lowest bidder (L2) with a bid of Rs 139.8 crore per train.

The Atmanirbhar Angle

In a tender dominated by foreign giants, The BHEL-Titagarh Wagons consortium was the only fully homegrown Indian bidder amongst the five bidders, and is a big step towards achieving the vision of Aatmanirbhar Bharat. This wasn't just corporate messaging—it was strategic positioning. In an environment where "Make in India" had become national priority, being the only fully Indian consortium carried weight beyond the bid numbers.

Umesh Chowdhary captures the moment: "We are committed to becoming a modest contributor to the Prime Minister's AatmaNirbhar vision. Vande Bharat trains have revolutionized the way we travel, and we are proud to be a part of the government's Make in India initiative".

Manufacturing Strategy: The Chennai-Latur Equation

The execution strategy reveals sophisticated planning: The trains' final assembly must be done at the Railway facilities of Chennai and Latur as per the contract. This isn't Titagarh building new facilities—it's upgrading existing government infrastructure, a model that reduces capital expenditure while demonstrating public-private partnership.

The final assembly, testing and commissioning of the Vande Bharat sleeper trains will be done at the Indian Railway's facilities in Chennai. There will be 16 coaches in each train, with an approximate capacity to accommodate more than 880 passengers in total.

The Technology Division

The consortium structure leverages each partner's strengths: BHEL's scope will cover supply of propulsion system, i.e., IGBT-based traction converter-inverter, auxiliary converter, train control management system, motors, transformers, and mechanical bogies. Titagarh Wagons Limited, being the rolling stock manufacturer for Indian Metros and Indian Railways, shall be responsible for the mechanical coach building.

Long-term Maintenance: The Recurring Revenue Revolution

The 35-year maintenance component transforms the economics. Traditional manufacturing is lumpy—you build, deliver, and wait for the next order. But Technology Partner, a consortium formed by BHEL and Titagarh Wagons, will supply sleeper-class Vande Bharat trains in 72 months and look into their upkeep for 35 years after supplies.

This creates: - Predictable Revenue: Maintenance contracts provide steady cash flows - Customer Lock-in: 35-year relationships create switching costs - Data Advantage: Operating trains provides insights for future designs - Margin Stability: Service margins often exceed manufacturing margins

Strategic Implications

The Vande Bharat contract represents multiple transformations:

- From Freight to Prestige: Vande Bharat isn't just another train—it's a national symbol

- From Vendor to Partner: 35-year maintenance makes Titagarh integral to operations

- From Domestic to Dominant: Competing against global giants and winning

- From Manufacturing to Services: Maintenance revenues change the business model

The contract also validates every previous strategic move. The Firema acquisition provided passenger coach expertise. The Pune Metro project demonstrated aluminum construction capabilities. The years of working with Indian Railways built trust. Everything converged in this moment.

As Titagarh commenced dedicated production lines for the prestigious Vande Bharat trains, the company that started with 180 wagons per year was now manufacturing India's most advanced trains, maintaining them for 35 years, and doing it as the only fully Indian consortium in competition with global giants.

VII. The Business Empire Today

Scale and Market Position

Walk through Titagarh's facilities today—from the foundries of Barrackpore to the high-tech assembly lines in Uttarpara, from the Italian operations in Caserta to the shipyards on India's coast—and you witness an industrial empire that defies easy categorization. Mkt Cap: 10,905 Crore · Revenue: 3,644 Cr · Profit: 239 Cr, the numbers tell one story. But the real narrative lies in the transformation from a single-product wagon manufacturer to India's most diversified rail systems company.

Titagarh is the first private company in India engaged in the manufacturing of trains for the Indian Railways since 2007. That 'first' matters—it represents breaking into a market long considered the preserve of government units and established players. Today, It commands a market share of 25-30% in the wagon manufacturing industry, making it the dominant private player.

The Mega Order Book: Numbers That Stagger

The order book reads like fantasy: Titagarh has secured the largest-ever order from the Indian Railways, totalling 24,177 wagons. This significant order will be fulfilled over a span of three years. This milestone marks a pivotal moment in the nation's development journey and underscores the Indian Railways' crucial role as an essential contributor to the Make in India initiative.

Think about that number—24,177 wagons. If you lined them up, they'd stretch over 400 kilometers. The contract value of INR 7,838 crore plus taxes represents not just revenue visibility but validation of Titagarh's manufacturing capabilities at unprecedented scale.

Add to this the Vande Bharat contract worth approximately Rs 24,000 crores for 80 train sets and 35-year maintenance, metro contracts across multiple cities, and you have an order book that provides visibility well into the next decade.

Product Portfolio Evolution: From Castings to Complete Systems

The product range today would bewilder someone who knew Titagarh from its early days. The company operates in two main segments—Freight Rail Systems and Passenger Rail Systems—but within these lie remarkable diversity:

Freight Rail Systems: - Loco shells, couplers, draft gears, cast bogies, cast manganese steel crossing products - Automobile-carrying, flat, hopper, tank, box, covered, and special purpose wagons - Brake vans

Passenger Rail Systems: - Over time, Titagarh has delivered more than 350 transit systems to the Indian Railways, marking the highest number achieved by any private rolling stock manufacturer in India - Electric locomotives, EMU trainsets, DEMU trainsets - Metro trains with aluminum bodies - Semi-high-speed trains (Vande Bharat) - Propulsion and electrical equipment

Beyond Rails: The company's diversification extends beyond railways. It engages in shipbuilding comprising coastal research vessels, naval vessels, passenger ships, tugs, and inland water transport vessels. Additionally, it manufactures modular panel bridges, bailey bridges, unibridges, and matière X bridges; and defense products.

Titagarh has successfully delivered the inaugural warship for the Indian Coast Guard, 'Kamla Devi,' as part of a collaborative effort with GRSE. The maritime division isn't a side project—it's strategic diversification leveraging heavy engineering capabilities.

Manufacturing Infrastructure: The Physical Foundation

The manufacturing footprint spans continents:

India Operations: - Main facility at Titagarh, West Bengal - Passenger coach facility at Uttarpara, Kolkata - Expanded foundry capacity to 25,000 metric tons from 12,000 metric tons - Dedicated production lines for Vande Bharat trains

International Operations: - Titagarh Firema SpA facilities at Caserta, Spello, and Tito in Italy - Technology center for aluminum construction and propulsion systems

The Technology Stack

Today's Titagarh is as much a technology company as a manufacturing one: - Aluminum body construction (from Firema acquisition) - Driverless train technology (delivered for BMRCL's Yellow Line) - Propulsion systems including IGBT-based traction converters - Train control and monitoring systems - Specialized welding techniques for different materials

Global Presence and Export Markets

While India remains the primary market, Titagarh's global footprint is expanding. The Italian subsidiary provides access to European markets. The company exports wagons to neighboring countries and Africa. The combination of Indian cost advantages and European technology creates a compelling proposition for emerging markets seeking railway modernization.

Financial Architecture

The financial structure reflects a maturing industrial company: - Pre-tax margin of 10% is healthy, ROE of 12% is good. The company has a reasonable debt to equity of 2%, which signals a healthy balance sheet - Long-term maintenance contracts providing revenue visibility - Diversified revenue streams reducing dependence on any single product line - Working capital management remains a challenge with Debtor days have increased from 50.1 to 63.3 days

Strategic Partnerships and Joint Ventures

The company's growth strategy increasingly relies on partnerships: - BHEL consortium for Vande Bharat - The consortium of Ramkrishna Forgings Limited and Titagarh Rail Systems Limited (RKFL-TRSL Consortium) has signed the contract for Manufacturing and Supply of Forged Wheels under Aatma-Nirbhar Bharat. The total quantity of Forged Wheels to be supplied will be around 15,40,000 wheels over a period of 20 years

These aren't just supplier relationships—they're strategic alliances that provide technology access, risk sharing, and market credibility.

The Order Pipeline

Recent wins demonstrate continued momentum: - Titagarh Rail Systems Limited has signed the contract with Gujarat Metro Rail Corporation (GMRC) Limited for Design, Manufacturing, Supply, Testing, Commissioning and Training of 72 standard gauge cars for the Surat Metro Rail. The order value for this project is approximately Rs 857 crores - Ahmedabad Metro contracts - Ongoing wagon orders from Indian Railways

The empire today is unrecognizable from the 180-wagon operation of 1997. It's a testament to strategic vision, perfect timing with India's infrastructure boom, and the ability to evolve from component supplier to system integrator. But empires need succession planning, and that brings us to the next generation.

VIII. Leadership Transition & Second Generation

The Succession Symphony

In the conference rooms of Titagarh's Kolkata headquarters, two generations of leadership coexist in a delicate dance of tradition and transformation. The company was founded in 1997 by Chowdhary's father, initially manufacturing 180 wagons annually. Chowdhary's father, Jagdish Prasad Chowdhary, is currently Executive Chair and has overseen the rapid expansion from the get-go through diversification, high product quality and a number of acquisitions. Umesh Chowdhary has been with the company from the start, and was central to the firm's inroads into the Italian market.

This isn't the typical Indian family business succession story of reluctant heirs or boardroom battles. Umesh Chowdhary didn't parachute in with an foreign MBA to modernize the family firm—he built his credibility project by project, acquisition by acquisition, country by country.

The Italian Maestro

Umesh's defining moment came not in India but in Italy. His impact there has been so immense that Italy bestowed one of its highest civilian awards on him, the Cavaliere Ordine della Stella d'Italia (Knight of the Order of the Star of Italy) in recognition of his outstanding contribution to bilateral ties with India.

When a foreign government knights an Indian businessman for strengthening bilateral ties, you know this isn't just about running factories—it's about economic diplomacy. Umesh understood something his father's generation might have missed: in the global rail industry, technology transfer isn't just about buying machines, it's about building trust across cultures.

Different Generations, Complementary Strengths

The generational dynamics at Titagarh reveal complementary capabilities:

Jagadish Prasad Chowdhary (The Founder):

- Deep relationships with Indian Railways built over decades

- Understanding of Indian bureaucracy and procurement processes

- Credibility from successful turnarounds (Britannia Engineering, Paper Mills)

- Institution building through industry associations (CII President)

Umesh Chowdhary (The Globalizer): - International business acumen demonstrated through Italian operations - Technology focus—understanding that future competition is about innovation - Modern manufacturing practices and global quality standards - Ability to navigate both Indian and international business environments

Building on the Founder's Vision

Umesh Chowdhary said "We are committed to becoming a modest contributor to the Prime Minister's AatmaNirbhar vision. Vande Bharat trains have revolutionized the way we travel, and we are proud to be a part of the government's Make in India initiative. Our focus on adopting the latest technology to boost our engineering prowess will help us build state-of-the-art railway trainsets, at par with global standards".

Notice the language—"modest contributor," "proud to be a part." This isn't the brash talk of a second-generation scion. It's calculated positioning that respects the founder's relationships while signaling technological ambition. The mention of "global standards" isn't accidental—it's Umesh signaling that Titagarh won't be content with being an Indian champion.

Professional Management with Family Oversight

The leadership structure reveals sophisticated governance: - Family provides strategic direction and key relationships - Professional managers run day-to-day operations - Board includes independent directors for governance - Clear division between ownership and management in operational decisions

This isn't the stereotypical Indian family business where every cousin has a corner office. It's professional management with family providing strategic continuity—a model that reassures both institutional investors and government clients.

The Pune Metro Moment

In 2019 Chowdhary's team won an order to design and manufacture trains for the Pune Metro in Maharashtra. They became the first coaches in the country with aluminum bodies, an achievement regarded as so significant that the route's opening last year was inaugurated by the Prime Minister, Narendra Modi.

This achievement belongs to Umesh's era—complex technology transfer, international collaboration, and delivery of a product that warranted prime ministerial attention. It demonstrated that the second generation could deliver not just continuity but elevation.

Balancing Tradition with Innovation

The transition challenge at Titagarh is unique: - Tradition: Deep relationships with Indian Railways, understanding of government procurement - Innovation: Aluminum bodies, driverless trains, propulsion systems

The company needs both. You can't win Indian Railways contracts without relationships, but you can't compete globally without technology. The two-generation leadership provides this balance—Jagadish Prasad's gravitas with government combined with Umesh's technological ambition.

Institutionalizing Success

The real test of second-generation leadership isn't just maintaining what exists—it's institutionalizing capabilities so they survive beyond individuals. Evidence of this institutionalization: - Technology transfer processes that don't depend on specific individuals - Quality systems certified to global standards - Partnerships and joint ventures that outlast personal relationships - Order book visibility that extends beyond political cycles

The Next Generation Challenges

As Umesh takes greater operational control, several challenges loom: 1. Maintaining Government Relations: Can the relationships built by the founder transfer to the next generation? 2. Technology Leadership: Can Titagarh stay ahead as global giants enter India? 3. Cultural Integration: Managing Italian operations, Indian manufacturing, and global ambitions 4. Capital Allocation: Balancing growth investments with shareholder returns 5. Talent Retention: Keeping technical talent in an increasingly competitive market

The Succession Report Card

By most metrics, Titagarh's leadership transition is succeeding: - ✓ Smooth operational continuity - ✓ Major contract wins (Vande Bharat, Metro projects) - ✓ International recognition (Italian knighthood) - ✓ Technology capability building - ✓ Maintained stakeholder confidence

But one concern persists: Promoter holding has decreased over last 3 years: -6.81%. Is this strategic dilution for growth capital, or confidence wavering? Time will tell.

The leadership transition at Titagarh isn't complete—such transitions never really are. But the evidence suggests a thoughtful evolution rather than revolution, building on the founder's foundation while reaching for global relevance. The company that began with one man's vision in a defunct foundry now spans continents, technologies, and generations.

IX. Playbook: Key Business Lessons

Starting Small, Thinking Big: The Compound Effect

The Titagarh story begins with 180 wagons per year—15 wagons per month. In an industry where Indian Railways needed thousands of wagons annually, this seemed almost insignificant. But Chowdhary understood something fundamental: in industrial businesses, credibility compounds.

Every wagon delivered on time became a reference. Every quality certification became a calling card. Every satisfied procurement officer became an advocate. The progression from 180 wagons to 24,177 wagons wasn't linear—it was exponential, built on compounding trust.

The Lesson: In B2B industrial markets, starting small isn't a disadvantage if you're building trust. Unlike consumer businesses that need scale from day one, industrial businesses can grow geometrically as credibility compounds.

Strategic M&A: The Distressed Asset Arbitrage

Titagarh's acquisition strategy reveals a pattern:

- 1982: Defunct Britannia Engineering foundry

- 2010: Arbel Fauvet Rail in receivership

- 2015: Struggling Firema Trasporti

- 2012: Corporated Shipyard

This isn't bottom fishing—it's strategic arbitrage. Distressed industrial assets often have three characteristics: valuable physical assets, technical knowledge, and broken business models. Titagarh's playbook: acquire the assets and knowledge, fix the business model, integrate the capabilities.

The Lesson: In industrial sectors, distressed assets aren't just cheap—they're often mispriced because financial investors can't evaluate technical capabilities. Operational buyers like Titagarh can see value where others see scrap.

Government Relations: The Invisible Moat

Titagarh's relationship with Indian Railways isn't just about winning contracts—it's about understanding the customer's unstated needs. When Indian Railways needed wagons, Titagarh provided wagons. When they needed complete train systems, Titagarh evolved. When Make in India became priority, Titagarh positioned as the indigenous champion.

This isn't lobbying—it's alignment. Chowdhary's roles in CII and other industry bodies weren't just titles—they were platforms for understanding policy direction and positioning accordingly.

The Lesson: In infrastructure businesses, government isn't just a customer—it's a stakeholder. Companies that align with government priorities don't just win contracts; they shape specifications.

Technology Absorption: Beyond Transfer

The Firema acquisition demonstrates technology absorption done right: 1. Acquire the capability (Firema purchase) 2. Pilot in controlled environment (3 Pune Metro rakes in Italy) 3. Transfer to India (31 rakes in Kolkata) 4. Indigenize through local suppliers 5. Innovate beyond the original (driverless trains)

This isn't technology transfer—it's technology transformation. The aluminum coaches made in Kolkata aren't Italian copies; they're Indo-Italian hybrids optimized for Indian conditions.

The Lesson: Technology acquisition without absorption is just expensive machinery. True competitive advantage comes from adapting foreign technology to local conditions and cost structures.

Vertical Integration: The Control Premium

From casting components to complete trains, Titagarh's vertical integration provides multiple advantages: - Quality Control: From raw material to finished product - Cost Advantage: Eliminating supplier margins - Supply Security: No dependence on component availability - Design Freedom: Ability to customize at component level

But more importantly, vertical integration in industrial businesses creates switching costs. When you supply complete systems, not just components, customer dependence increases geometrically.

The Lesson: In industrial markets, vertical integration isn't about cost savings—it's about control. Control over quality, delivery, and customer dependency.

Long-term Contracts: The Annuity Business Model

The Vande Bharat contract structure—manufacturing plus 35-year maintenance—transforms Titagarh's business model. Traditional manufacturing is transactional: build, deliver, collect, repeat. Maintenance contracts create relationships: continuous engagement, recurring revenue, customer lock-in.

The mathematics are compelling: - Manufacturing: ₹9,600 crore one-time - Maintenance: ₹14,400 crore over 35 years - Total: ₹24,000 crore contract value

The Lesson: In industrial businesses, the real money isn't in selling products—it's in maintaining them. Maintenance contracts provide revenue visibility, customer stickiness, and often better margins than manufacturing.

Riding Government Policy: The Tailwind Strategy

Titagarh's growth trajectory aligns perfectly with government initiatives: - Post-1991 Liberalization: Private sector entry into wagon manufacturing - Railway Modernization (2000s): Capacity expansion opportunities - Make in India (2014+): Indigenous manufacturing priority - Atmanirbhar Bharat (2020+): Self-reliance in critical sectors

This isn't luck—it's positioning. Titagarh consistently aligned its capabilities with emerging policy priorities, riding tailwinds rather than fighting headwinds.

The Lesson: In regulated industries, strategy isn't just about competitive advantage—it's about regulatory alignment. Companies that anticipate and align with policy direction get tailwinds; those that don't face headwinds.

The Meta-Lesson: Patience and Persistence

The journey from tea estate accountant to rail manufacturing titan took four decades. The progression from 180 wagons to 24,177 wagons took 25 years. The evolution from components to complete train systems took two decades.

This isn't Silicon Valley-style disruption—it's industrial evolution. In heavy engineering, competitive advantages aren't built in quarters; they're built in decades. Relationships compound over years. Capabilities accumulate over projects. Credibility builds over cycles.

The Ultimate Lesson: In industrial businesses, time is the ultimate competitive advantage. Not because things move slowly, but because real capabilities—technical expertise, government relationships, manufacturing excellence—take time to build and even longer to replicate.

The Titagarh playbook isn't revolutionary—acquire distressed assets, build government relationships, integrate vertically, absorb technology, align with policy. But execution over four decades with patience, persistence, and perfect timing? That's the difference between a playbook and a championship.

X. Bear vs. Bull Case Analysis

Bull Case: Riding the Infrastructure Supercycle

India's Massive Railway Modernization Program

The numbers are staggering. India plans to invest ₹10 lakh crore in railway infrastructure by 2030. The dedicated freight corridor project alone requires thousands of wagons. The plan for 400 Vande Bharat trains. Metro systems in 50+ cities. If even half these plans materialize, Titagarh's order book could double from current levels.

This isn't speculative—India's railway underinvestment is real. India has 67,000 km of railway tracks for 1.4 billion people. China has 146,000 km for similar population. The catch-up investment required is enormous, multi-decade, and politically essential.

Only Company Manufacturing Both Wagons and Coaches

It is the only Indian company that manufactures both wagons and coaches. This unique positioning matters more than it appears. When Indian Railways floats integrated tenders, Titagarh can bid for complete projects. When metro corporations need multiple products, Titagarh offers one-stop solutions. This isn't just convenience—it's competitive advantage in a market where procurement processes favor integrated suppliers.

Vande Bharat and Metro Expansion Tailwinds

The Vande Bharat contract isn't just about 80 trains—it's about establishing Titagarh as a credible semi-high-speed manufacturer. Success here opens doors to future high-speed rail projects. Similarly, successful metro deliveries in Pune create demonstration effects for other cities.

India plans to expand metro networks from current 800 km to 2,000 km by 2026. Each kilometer needs 6-8 coaches. That's potentially 10,000+ coaches. Even 10% market share means 1,000 coaches—significant for a company that currently makes hundreds.

Strategic Italian Subsidiary for Technology Access

Titagarh Firema isn't just a subsidiary—it's a technology gateway. European rail technology is 20 years ahead of India in certain areas. Having an Italian subsidiary provides: - Access to European technology without licensing fees - Ability to bid for European projects - Credibility with global customers who might not trust purely Indian manufacturers - Technology testing ground before Indian deployment

Long-term Maintenance Contracts Provide Visibility

The 35-year Vande Bharat maintenance contract fundamentally changes Titagarh's risk profile. Recurring revenue streams make the business more predictable, valuations more sustainable, and growth investments more feasible. As more contracts include maintenance components, Titagarh transforms from cyclical manufacturer to annuity-like service provider.

Bear Case: The Structural Challenges

Heavy Dependence on Government Orders

Government dependency is Titagarh's blessing and curse. Indian Railways and metro corporations account for majority revenues. Government procurement means: - Payment delays (note the increase in debtor days) - Political risk (change in government priorities) - Pricing pressure (L1 bidding system) - Tender uncertainties (technical specifications can change)

If government priorities shift from railways to highways, or fiscal constraints limit railway investment, Titagarh's growth story stumbles.

Capital Intensive Business with Long Working Capital Cycles

Debtor days have increased from 50.1 to 63.3 days. In a business where projects run for years and payments are milestone-based, working capital is a constant strain. Each new order requires upfront investment in materials and manufacturing before payments arrive. Growth paradoxically increases capital needs.

The capital intensity shows in returns—while ROE of 12% is decent, it's not spectacular for the execution risk involved. Compare this to asset-light businesses earning 30%+ ROE, and Titagarh looks less attractive to growth investors.

Promoter Holding Decrease

Promoter holding has decreased over last 3 years: -6.81%. Decreasing promoter stake raises questions: - Is the family losing confidence? - Are they monetizing at peak valuations? - Is dilution necessary for growth capital?

In family-run businesses, promoter commitment matters. Decreasing stake, whatever the reason, sends mixed signals to minority shareholders.

Competition from Global Players

Alstom, Siemens, Bombardier—these aren't just competitors; they're giants with decades of experience, global scale, and deep pockets. As India's rail market grows, these players will intensify focus. They can: - Underbid to gain market entry - Offer better financing terms - Provide superior technology - Leverage global government relationships

Titagarh competed successfully when foreign players were tentative about India. As the market becomes more attractive, competition will intensify.

Execution Risks on Large Order Book

A ₹26,000 crore order book sounds impressive until you consider execution complexity: - 24,177 wagons to be delivered - 80 Vande Bharat trains to be manufactured - Multiple metro projects running simultaneously - 35-year maintenance commitments

Any execution slippage—quality issues, delivery delays, cost overruns—could trigger penalty clauses, reputation damage, and future order losses. In government contracts, one failure can blacklist you from future tenders.

The Balanced View

The bull case rests on macro tailwinds—India's infrastructure needs are real, urgent, and politically essential. The bear case highlights micro challenges—execution complexity, working capital strain, and competitive intensity.

The truth, as always, lies between extremes. Titagarh will likely benefit from India's infrastructure boom but not without challenges. Government orders will continue but with pressure on margins. Technology advantages will help but need constant investment to maintain.

For investors, the question isn't whether Titagarh will grow—it almost certainly will. The question is whether that growth will translate to shareholder value after accounting for capital needs, execution risks, and competitive pressures.

The stock's volatility—52-week range from ₹654 to ₹1,896—reflects this uncertainty. Bulls see a infrastructure play at the beginning of a supercycle. Bears see a capital-intensive manufacturer with government dependency and execution risks.

Both are right. Both are wrong. The answer depends on time horizon, risk tolerance, and belief in India's infrastructure story. What's certain is that Titagarh's next decade will look nothing like its last—for better or worse.

XI. The Future & Closing Thoughts

India's Infrastructure Supercycle Thesis

Stand at Mumbai's Chhatrapati Shivaji Terminus during rush hour. Watch millions squeeze into trains designed for thousands. Visit any Indian city—the same story. India's urban population will double to 800 million by 2050. These people need to move. Goods need to flow. The economy needs circulation.

This isn't a trend—it's demographic destiny. India adds an Australia to its population every year. Each person needs transportation. Each ton of production needs logistics. The railway investment isn't discretionary; it's existential. Countries don't skip infrastructure stages in development—they build through them.

Titagarh sits at the intersection of this inevitability. When infrastructure spending is politically essential, economically necessary, and demographically destined, suppliers don't just grow—they transform. The company that made 180 wagons annually now makes that in a week. What happens when India really starts building?

Semi-High-Speed Rail Revolution Potential

Vande Bharat is just the beginning. India's semi-high-speed ambitions include: - 75 Vande Bharat routes by 2024 - High-speed corridors (Mumbai-Ahmedabad bullet train) - Regional rapid transit systems - Dedicated freight corridors at higher speeds

Each evolution requires new technology, fresh investment, and—crucially—local manufacturing capability. Titagarh's successful Vande Bharat execution positions it for this revolution. But potential isn't position—execution will determine if Titagarh leads or follows this transformation.

Export Opportunities in Developing Markets

India's infrastructure challenges aren't unique. Bangladesh needs wagons. Africa needs metro systems. Southeast Asia needs rail modernization. These markets can't afford European prices but need better than Chinese quality. India—and Titagarh—sits in the sweet spot.

The Italian subsidiary provides European credibility. Indian manufacturing provides cost advantage. The combination could unlock markets that neither could access alone. Imagine Titagarh providing metros to Lagos, trains to Dhaka, wagons to Kenya—not fantasy but logical extension of capabilities.

Technology Partnerships and Joint Ventures

The consortium of Ramkrishna Forgings Limited and Titagarh Rail Systems Limited has signed the contract for Manufacturing and Supply of Forged Wheels under Aatma-Nirbhar Bharat. The total quantity of Forged Wheels to be supplied will be around 15,40,000 wheels over a period of 20 years.

This wheel manufacturing JV isn't just about components—it's about strategic positioning. Wheels are to trains what chips are to computers—critical components that determine performance. Controlling wheel supply means controlling a key input, reducing dependency, and potentially supplying competitors.

Future partnerships could include: - Signaling systems (the next technology frontier) - Battery technology for hybrid trains - Automation systems for driverless operations - Predictive maintenance using IoT

Biggest Surprises from the Research

Surprise #1: The Italian Knighthood An Indian businessman receiving one of Italy's highest civilian honors for industrial cooperation? This isn't typical. It suggests Titagarh's Italian operations aren't just successful—they're strategically important to Italy. That's leverage.

Surprise #2: The Shipbuilding Division A railway company building warships for the Indian Navy? The diversification seems random until you realize it's not about ships—it's about heavy engineering capabilities and government relationships. Same customer (government), same capabilities (heavy manufacturing), different product.

Surprise #3: The Maintenance Mathematics 35-year maintenance contracts worth more than manufacturing? This transforms understanding of the business model. Titagarh isn't selling trains; it's selling transportation-as-a-service with a 35-year customer lock-in.

Surprise #4: The Only One Being the only Indian company manufacturing both wagons and coaches seems like trivia until you understand procurement dynamics. Integrated tenders favor integrated suppliers. This unique positioning is a moat that's hard to replicate.

What This Story Teaches About Indian Manufacturing

The Titagarh story isn't just about one company—it's about Indian manufacturing's evolution:

From Labor Arbitrage to Technology Integration The old model: cheap Indian labor. The new model: Italian technology plus Indian engineering plus cost optimization. Titagarh shows Indian manufacturing moving up the value chain.

From Local to Global Indian companies aren't just import substituters anymore—they're global players. Titagarh owning Italian manufacturers reverses decades of flow. This isn't just business success; it's geopolitical shift.

From Product to Solution Selling wagons is product business. Providing 35-year maintained transport systems is solution business. The evolution from vendor to partner changes everything—margins, relationships, valuations.

The Patient Capital Lesson Forty years from tea estate to rail empire. This isn't venture capital timeline—it's industrial timeline. Real manufacturing capabilities aren't built in funding rounds; they're built over decades. In an era of quick flips, Titagarh reminds us that some moats take generations to build.

The Closing Perspective

Picture that accountant in Darjeeling again, squinting at ledgers in mountain mist. Could he have imagined Italian subsidiaries, Prime Ministers inaugurating his trains, or orders for 24,000 wagons? Probably not. But he understood something fundamental: India would grow, growth needs infrastructure, infrastructure needs suppliers.

That insight—simple, patient, profound—built an empire. Not through disruption but through evolution. Not through revolution but through execution. Not through shortcuts but through four decades of compound progress.

Titagarh's story isn't finished. The next chapters—high-speed rail, export markets, technology evolution—remain unwritten. But the pattern is clear: aligned with India's growth, integrated with global technology, committed for the long term.

For investors, Titagarh represents a bet on India's infrastructure future. For entrepreneurs, it's a masterclass in patient empire building. For India, it's validation that indigenous companies can compete globally in complex manufacturing.

The train that started in Titagarh hasn't reached its destination. Given India's infrastructure needs, it might just be leaving the station.

XII. Recent News### **

Q1 FY26 Performance Update**

Net profit of Titagarh Rail Systems declined 53.95% to Rs 30.86 crore in the quarter ended June 2025 as against Rs 67.01 crore during the previous quarter ended June 2024. Sales declined 24.78% to Rs 679.30 crore in the quarter ended June 2025 as against Rs 903.05 crore during the previous quarter ended June 2024.

The sharp decline reflects the lumpy nature of railway contracts and timing of project execution. On segmental front, revenue from freight rail systems stood at Rs 601.87 crore (down 28.53% YoY) and revenue from passenger rail systems stood at Rs 77.43 crore (up 27.22% YoY), during the quarter. The passenger segment growth indicates the gradual ramp-up of metro and Vande Bharat production.

Order Book Momentum Continues

In the first quarter, the company secured new orders worth Rs 2,092 crore (excluding GST), bringing the total order book to Rs 26,000 crore. This massive order visibility provides revenue runway for the next 3-4 years.

Vande Bharat Production Line Launch

Titagarh Rail Systems, in partnership with BHEL, inaugurated a production line for Vande Bharat Sleeper trains under a ₹24,000 crore contract. Despite this, shares fell up to 5%, and the company reported a decline in revenue and net profit. Analysts recommend buying the stock due to its robust order book and capacity expansion plans.

Strategic Expansion Initiatives

Kavach and Shipbuilding Push: Titagarh Rail Systems is pursuing partnerships for Kavach development and expanding its shipbuilding vertical. The company is exploring locations for new dockyards and aims to ramp up activities in both sectors over the next few months. Kavach, India's indigenous train collision avoidance system, represents a significant opportunity as Indian Railways mandates its installation across the network.

Bangalore Metro Milestone: Titagarh has signed a contract with Bangalore Metro Rail Corporation Limited (BMRCL) for manufacturing and delivering 34 of the 36 driver-less, stainless-steel trainsets for Bengaluru Metro's 21km Yellow Line corridor (RV Road to Bommasandra). Upon completion, this line is expected to significantly improve urban mobility for the city's residents. The first "Make-in-India" trainset was handed over in January 2025.

Joint Venture with Sidwal Refrigeration

Binding definitive agreements have been entered amongst, Sidwal Refrigeration Industries Private Limited (Sidwal) and Titagarh Rail Systems Limited and its promoters and Shivaliks Mercantile Private Limited (Shivaliks), an existing company within the meaning of the Companies Act 2013, for undertaking investment by Sidwal & TRSL in Shivaliks, which will become a Joint Venture - Special Purpose Vehicle Company (JV-SPV), to carry on the business of railway components and sub systems for the rolling stock industry in India and overseas. Pursuant to the said definitive agreements, the proposed JV-SPV - Shivaliks will be controlled equally by Sidwal and Titagarh.

Both TRSL and Sidwal, will invest upto INR 1,200 million each in the JV-SPV in one or more tranches. This JV focuses on HVAC systems for rolling stock—a critical component as India moves toward air-conditioned trains.

Capacity Expansion at Uttarpara

The additional land, contiguous to its existing 34-acre Uttarpara manufacturing facility, is strategic and critical for the expansion of the company's passenger rolling stock business in the Indian infrastructure sector. This includes the production of metro coaches, Vande Bharat trains, and specialized rolling stock for the Indian defence, all of which are currently being executed by the company.

Stock Performance and Valuation

The stock has seen significant volatility: Titagarh Rail Systems Ltd share price moved down by 45.09% on BSE over the last 12 months. However, over the last 3 years, Titagarh Rail Systems Ltd share price moved up by 560.65% on BSE. The long-term performance reflects the structural growth story, while recent correction suggests profit-booking after the spectacular run.

Analyst Sentiment

85.71% of analysts recommend a 'BUY' rating for Titagarh Rail Systems Ltd. The bullish consensus reflects confidence in the long-term order book and India's infrastructure story, despite near-term execution challenges.

XIII. Links & Resources

Official Company Resources: - Company Website: www.titagarh.in - BSE Listing: BSE Code 532966 - NSE Symbol: TITAGARH

Key Financial Metrics: - Market Cap: ₹10,905 Crore - Revenue (TTM): ₹3,644 Crore - Net Profit: ₹239 Crore - Order Book: ₹26,000 Crore - Promoter Holding: 40.4%

Major Subsidiaries: - Titagarh Firema SpA (Italy) - Titagarh Singapore Pte. Ltd. - Titagarh Marines (Shipbuilding)

Recent Contract Wins: - 80 Vande Bharat Trains: ₹24,000 Crore - 24,177 Railway Wagons: ₹7,838 Crore - Forged Wheels JV: 15,40,000 wheels over 20 years - Surat Metro: ₹857 Crore for 72 cars - Bangalore Metro Yellow Line: 34 driverless trainsets

Investment Considerations: - Strong order book visibility (3-4 years) - Beneficiary of India's infrastructure push - Technology capabilities through Italian subsidiary - Long-term maintenance contracts provide recurring revenue - Execution risks given large order book - Working capital intensive business model - Competition from global players intensifying

Note: This analysis is for informational purposes only and should not be considered investment advice. Market conditions and company fundamentals can change rapidly. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube