Star Cement: The Cement King of India's Northeast Frontier

I. Introduction & Episode Setup

Picture this: A cement truck navigating hairpin turns through the misty hills of Meghalaya, its cargo worth 20% more per ton than identical cement just 500 kilometers away in Bengal. The driver knows these roads like scripture—every pothole, every blind corner where oncoming trucks might appear from the fog. This isn't just logistics; it's the physical manifestation of one of India's most fascinating regional monopolies.

How did a company founded in 2001, spun out from a plywood manufacturer, become the uncontested champion of one of India's most challenging markets? Star Cement controls over 23% of Northeast India's cement market—a region where most national giants fear to tread. The paradox is striking: operating in terrain with infrastructure nightmares, monsoon-induced transport breakdowns, and political complexities that would make most CEOs run for the hills, Star Cement not only survives but commands a pricing premium of ₹5-10 per bag over competitors.

This is a story about frontier economics—about building castles where others see only mountains. It's about two plywood entrepreneurs who saw opportunity where Birla and Ambani saw headaches. And now, with UltraTech Cement's recent 8.69% stake acquisition for ₹851 crore, it's become a chess piece in India's great cement consolidation war.

The themes we'll explore resonate far beyond cement: How do you build a moat using geography itself? What happens when conglomerate synergies meet regional expertise? And perhaps most intriguingly—when the giants finally come calling with their checkbooks, do you sell the kingdom you built in the mountains, or do you dig in deeper?

From its origins as a Century Plyboards subsidiary to its current status as acquisition bait for India's cement titans, Star Cement's journey illuminates how regional champions create value in markets that spreadsheets say shouldn't exist. The Northeast frontier isn't just Star's market—it's Star's fortress. And the walls are made of more than just cement.

II. Pre-History: The Century Group Origins

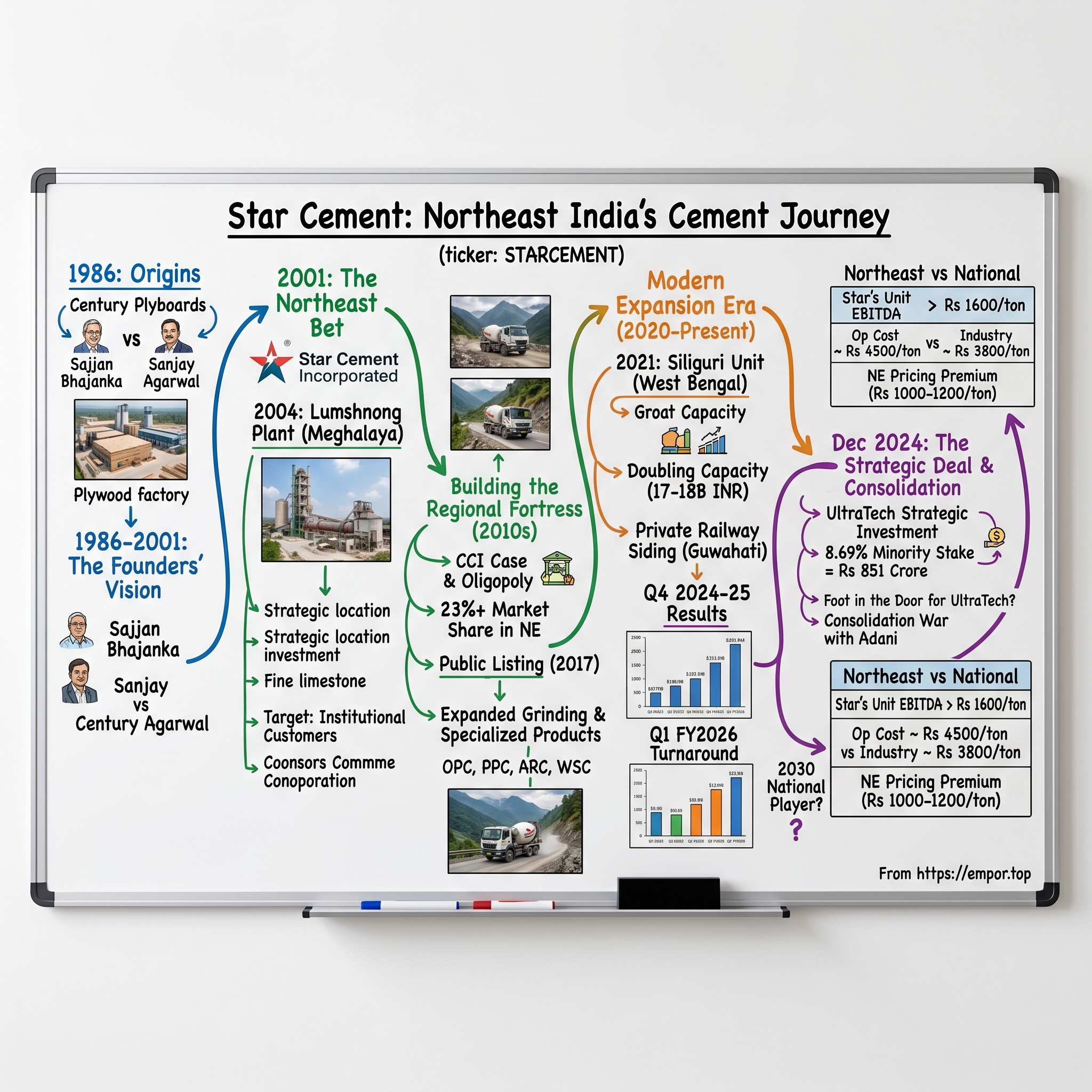

The Kolkata boardroom, 1986. Sajjan Bhajanka sketches on a notepad while Sanjay Agarwal runs numbers on a calculator. Outside, monsoon rain hammers the windows of their plywood factory office. They're discussing an idea that sounds absurd: making cement in India's Northeast, where roads barely exist and the nearest railway station might as well be on the moon. Century Plyboard was founded in 1986 by Sajjan Bhajanka and Sanjay Agarwal in Kolkata, but these entrepreneurs were already thinking beyond wood panels.

The Bhajanka-Agarwal partnership reads like a classic Indian business origin story. A mutual acquaintance led Bhajanka to meet Sanjay Agarwal, who was setting up a panel door factory in 1986. "When I saw the plot and the factory, it was like love at first sight," says Bhajanka. The two eventually built their venture up into what is today Century Plyboards. Bhajanka brought the vision and industry connections; Agarwal brought operational excellence and marketing acumen. Together, they would build the largest plywood player in India, with a 25 per cent share in the organised market.

But why cement? The answer lies in the peculiar economics of Northeast India circa 2001. The region imported virtually all its cement from Bengal and Bihar, with transport costs adding 30-40% to the final price. Every infrastructure project—every bridge, every government building, every power plant—paid this geography tax. For two entrepreneurs who'd built a plywood empire by identifying and exploiting market inefficiencies, this screamed opportunity.

Star Cement Ltd (formerly, Cement Manufacturing Company Ltd) was earlier a subsidiary of Century Plyboard (India) Ltd. It commenced operations in December 2004. After a demerger in April 2012, Century Plyboard transferred its cement, ferroalloy, and power divisions to its wholly owned subsidiary "Star Ferro and Cement Ltd". The structure was complex—a web of subsidiaries and cross-holdings typical of Indian conglomerates—but the strategy was simple: dominate a market everyone else ignored.

The Seven Sisters states—Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, and Tripura—represented India's final frontier. Cut off from mainstream India by the narrow Siliguri Corridor (the "Chicken's Neck"), plagued by insurgencies, blessed and cursed with torrential rains, the region seemed designed to repel industrial investment. The nearest major cement plants were 500+ kilometers away in Bengal. During monsoons, that might as well have been 5,000 kilometers.

"Apart from that, we have also started a cement plant in the Northeast. That is also the biggest project in the Northeast", Bhajanka would later reflect on the venture. The decision wasn't just about cement—it was about betting on a region's future. The Northeast's infrastructure deficit wasn't a bug; it was the feature that would protect Star Cement's margins for decades.

Consider the operational challenges they signed up for: Limestone had to be mined from hills accessible only by roads that washed away annually. Skilled engineers had to be convinced to relocate to places where mobile phones didn't work and the nearest multiplex was a day's journey away. Equipment had to be transported through territories where bandhs (strikes) could shut down movement for weeks. This wasn't just building a cement plant; it was building an entire ecosystem from scratch.

The plywood-to-cement pivot also revealed something profound about Indian conglomerate thinking. Unlike Western corporate strategy, which preaches focus, Indian business houses thrive on adjacencies—not operational adjacencies, but network adjacencies. Century Plyboards had dealers, political relationships, and credibility in the Northeast from their plywood operations. Star Cement could leverage all of this while appearing to be an entirely different business.

By 2001, when Star Cement was formally incorporated, the pieces were in place. The Bhajanka-Agarwal duo had identified their Normandy Beach—Meghalaya, with its vast limestone reserves and strategic location at the heart of the Northeast. They would build their first plant in Lumshnong, a place so remote that they'd essentially have to build a town around it. The established cement giants—Birla, Ambani, even the Tatas—watched with bemused interest. Let them try, the thinking went. The Northeast had swallowed bigger dreams than this.

What the giants didn't understand was that Bhajanka and Agarwal weren't just building a cement plant. They were building a fortress, with geography itself as the moat. The same logistical nightmares that made the Northeast uninvestable for others would become Star Cement's competitive advantage. In the land of infrastructure deficits, the company that could build its own infrastructure would be king.

III. The Founding Years & Northeast Bet (2001–2010)

December 23, 2004. The kilns at Lumshnong roar to life for the first time, producing clinker in a place where locals had never seen industrial machinery of this scale. This plant has been producing clinker from 23rd Dec.2004 and cement from 2nd Feb.2005. Originally incorporated as Cement Manufacturing Company Limited, the entity that would become Star Cement was making history: Star Cement was recognized by the Meghalaya state government for its pioneering cement plant in the backward area of Lumshnong in 2005. It was, quite literally, the first to bring large-scale cement manufacturing to India's Northeast.

The Lumshnong location wasn't chosen by accident. The plant is strategically positioned in Meghalaya, close to its mines that produces India's finest lime stones ensuring very high-quality cement. But "strategic" is a generous term for what was essentially virgin industrial territory. The company had to build roads to connect the plant to the nearest highway. They had to create housing colonies for workers who couldn't commute from non-existent nearby towns. They installed generators because the power grid was more aspiration than reality.

The early operational challenges read like a logistics textbook's nightmare scenario. Spare parts that would take a day to procure in Gujarat took weeks to reach Lumshnong. During monsoons—which in Meghalaya means half the year—trucks would get stuck for days on roads that dissolved into mud rivers. The company learned to stockpile everything: cement bags, diesel, even food for workers. This wasn't just-in-time manufacturing; this was just-in-case-civilization-doesn't-reach-us manufacturing.

Yet by 2005, Star Cement wasn't just surviving—it was thriving. The companys plant at Lumshnong has been producing clinker from 23rd Dec.2004 and cement from 2nd Feb.2005. This is the largest cement plant in North East India. The company had cracked a code that larger players hadn't even attempted: how to profitably manufacture cement where the cost of building the plant alone would make most CFOs faint.

The product portfolio was deliberately simple initially: Presently the company is marketing super quality clinker to different grinding units located in India, Nepal & Bhutan, along with 3 types of cement such as Ordinary Portland Cement 43 grade, Ordinary Portland Cement 53 grade, Portland Pozzolana Cement Part I Fly ash based. No fancy specialty cements, no premium brands—just solid, reliable product for a market starved of local supply.

The distribution strategy was equally pragmatic. Rather than trying to build a massive dealer network from scratch, Star Cement targeted institutional customers first: The Companys institutional customers comprise Larsen & Tourbo, National Hydro Power Corporation, Public Works Department, Indian Railways and Ministry of Defense. These weren't just customers; they were anchors that provided steady demand and, crucially, credibility. When L&T uses your cement for a hydroelectric project, every local contractor takes notice.

The real genius, however, was in understanding the Northeast's peculiar market dynamics. Star Cement's manufacturing plants are located in Khliehriat and Guwahati. The company has occupied more than 500 to 1,000 hectares of land in Jaintia Hills district. This wasn't just about having land; it was about controlling the entire value chain in a region where each link was fragile.

Consider coal procurement: It obtains coal from the local market for fuel at a price of 8,000 rupees per ton—a fraction of what imported coal would cost after transportation. But "local market" in Meghalaya meant dealing with small-scale miners, navigating tribal land rights, and managing supply chains that could be disrupted by everything from local festivals to insurgent activity. Star Cement didn't just buy coal; they became part of the local economic ecosystem.

By 2010, what started as a 0.6 MTPA (million tonnes per annum) plant had evolved into something far more significant. The company had built not just production capacity but an entire infrastructure network—from limestone mines to power plants to transportation systems. They'd proven that the Northeast, despite its challenges, could support world-class manufacturing.

The moat was already forming, not from superior technology or brand power, but from the sheer difficulty of replication. Any competitor looking to enter would face the same infrastructure challenges Star had overcome, but without the first-mover advantage of vacant land, government support, and grateful customers. In the Northeast cement market, Star hadn't just built a plant—they'd built a fortress. And the walls were getting higher every year.

IV. Building the Regional Fortress (2010–2020)

The 2010s would test whether Star Cement's early infrastructure investments could transform into sustainable competitive advantage. Due to the topography of the North Eastern states, transporting cement from Eastern states is not very cost effective. Hence, the inflow of cement has considerably reduced. This geographic reality was Star's moat—but moats need constant reinforcement.

By 2012, the competitive landscape was crystallizing. Star Cement, along with Calcom Cement India Ltd. (Dalmia Brand) and TOPCEM India, which together have a market share of 60% in Assam, had effectively oligopolized the Northeast market. The AREIDA had filed a case with the Competition Commission of India (CCI) on September 2, 2016 alleging that three companies — Topcem Cement, Star Cement and Dalmia Cement have been leading the nefarious syndicate. While competitors cried cartel, Star saw it differently—this was rational pricing in a market where logistics costs justified premiums.

The numbers told the real story: Star Cement is the largest cement player in North East with a market share of over 23%. The average retail price of cement brands like Topcem, Star, Amrit and Dalmia, which are produced in Assam and Meghalaya, were found to be much higher than the national brands in the Guwahati market. Retail price of Topcem Cement on Monday in Guwahati was found to be between Rs 400 and 420, while Star Cement bags ranged between Rs 405 and 425. This wasn't price gouging—it was the market recognizing the value of local availability and reliable supply.

The company's strategy during this period was methodical expansion of grinding capacity near consumption centers. In 2013, the clinkerisation unit, Star Cement Meghalaya Ltd. (SCML), was commissioned in Lumshnong, Meghalaya with a capacity of 1.75 million tonnes per annum, while Guwahati Grinding Unit (GGU), located in Sonapur, Assam started operations with a capacity of 2 million tonnes per annum. This split manufacturing model—clinker in Meghalaya, grinding near markets—optimized both raw material access and distribution costs.

Then came the pivotal moment: public listing. Listing date: 16 Jun, 2017. The IPO wasn't just about raising capital; it was about legitimacy. As a listed entity, Star could access cheaper capital, attract institutional investors, and most importantly, signal to potential acquirers that it was a serious, transparent business worthy of premium valuations.

In line with terms of Scheme of Amalgamation, 29,54,90,077 equity shares of the company were allotted on 8 April 2017 to the shareholders of erstwhile Star Ferro and Cement Limited in the ratio of 1.33 equity shares of Re 1 each of the company for every 1 (one) equity share of Re 1 each of erstwhile Star Ferro and Cement Limited held by them as on the record date i.e. 3d April 2017. The Company has initiated steps to list its shares with National Stock Exchange of India Limited and BSE Limited. The complex restructuring preceding the listing cleaned up the corporate structure, separating the cement business from the ferroalloy operations.

Product evolution kept pace with market sophistication. Beyond the basic OPC and PPC grades, Star introduced specialized products: Product Offerings[1] Ordinary portland cement (OPC), Portland Pozzolana cement(PPC), Anti-rust cement (ARC), Portland Composite Cement (PCC) and Weather Shield Cement (WSC). The Anti-rust cement, in particular, addressed the Northeast's perpetual humidity problem—a classic example of product-market fit born from deep local understanding.

Distribution strategy evolved from institutional focus to retail penetration. It has a strong presence in the eastern and north-eastern regions of India, with a network of over 3000 dealers. But this wasn't just about numbers. Each dealer relationship in the Northeast was cultivated carefully—credit terms adjusted for local cash flow patterns, inventory support during monsoon stockpiling, technical training for masons unfamiliar with modern cement grades.

The pricing dynamics during this period revealed the true nature of Star's competitive advantage. A market study of whole sale prices prevailing in Siliguri (West Bengal) market during the month of August, 2016 reveals that the same bag of Topcem /Dalmia /Star Cement was available in the open market at a much lower price in Siliguri (West Bengal) as compared to the prevailing prices of the same in Assam. Selling cement in Siliguri at prices lower than those at Guwahati by all the three companies, in spite of additional transportation cost, establishes the collusion and cartelization between the companies. What regulators saw as collusion, economists might recognize as the Hotelling model in action—spatial competition creating natural price differentiation.

By 2020, Star Cement wasn't just surviving in the Northeast—it was thriving with EBITDA margins that made larger players envious. The fortress was complete: production capacity, distribution network, brand recognition, and most importantly, the accumulated knowledge of how to operate profitably in India's most challenging geography. The question was no longer whether Star could defend its territory, but whether it could expand beyond it.

V. The Modern Expansion Era (2020–Present)

The pandemic years could have been Star Cement's crisis moment. Instead, they became its coming-out party. In January 2021, it expanded its business to East India by opening a new plant in West Bengal worth 4.5 billion. This wasn't just capacity addition—it was a declaration that Star was ready to compete beyond its Northeast fortress.

Siliguri Grinding Unit (SGU) at Mohitnagar near Siliguri started operations with a capacity of 2 million tonnes per annum. Commissioned in 2021, Star Cement's Grinding Unit in Mohitnagar near Jalpaiguri town, in addition to cement manufacturing units in Lumshnong in Meghalaya and Sonapur near Guwahati has augmented cement manufacturing capacity to 5.7 million tonnes per annum (MTPA). Spread over 45 acres, Siliguri Grinding Unit is a Greenfield project set up with the latest state of the art German Technology having a capacity of 2 million tonnes per annum (MTPA).

The West Bengal plant represented a strategic inflection point. For two decades, Star had perfected the art of operating in difficult terrain. Now it was testing whether those capabilities could translate to competitive markets. West Bengal wasn't the Northeast—here, every major cement player had presence. Star's pitch was different: regional understanding, faster delivery times, and the relationships built over years of serving Bengal from across the border.

Then came the massive capacity expansion announcement. In June 2022, the company invested 17–18 billion rupees in doubling the capacity of clinker. This wasn't incremental growth—this was Star preparing for something bigger. The company announced plans to expand production capacity to 12 million tonnes per annum (MTPA) by fiscal year 2027, with longer-term ambitions even more audacious: intend to increase capacity to 25 MTPA by 2030.

Financial performance during this period validated the expansion strategy. Star Cement Ltd's net profit jumped 40.49% since last year same period to ₹123.17Cr in the Q4 2024-2025. Star Cement's consolidated net sales for March 2025 reached Rs 1,052.09 crore, up 15.17% YoY. Net profit rose 40.49% to Rs 123.17 crore, while EBITDA increased by 42.76%. EPS improved to Rs 3.05 from Rs 2.17. The stock closed at Rs 231.26 on May 20, 2025, reflecting a 33.69% return over six months.

The Q1 FY2026 results showed continued momentum: Star Cement reported a standalone net profit of US$2.76m in the first quarter of the 2026 financial year from April - June 2025, compared to a net loss of US$1.50m in the same period in 2024. Sales rose by 13% to US$62.15m from US$54.81m. Operating profit rose by 401% to US$11.44m from US$2.28m previously. The turnaround from loss to profit in just one year demonstrated operational leverage kicking in as volumes grew.

Product innovation accelerated during this period. During the year 2020, Company launched Star Anti Rust Cement across the markets of North East, North Bengal & East Bihar. The Anti Rust Cement wasn't just another SKU—it was a targeted solution for the high-humidity environments that defined Star's core markets. This deep understanding of local conditions, accumulated over two decades, was now being productized and monetized.

Infrastructure improvements complemented capacity expansion. Private Railway Siding was commissioned at Guwahati Works bringing in operational efficiencies and cost savings. In a region where road transport could be paralyzed by landslides or strikes, rail connectivity wasn't just logistics—it was insurance.

The distribution network evolved from regional to quasi-national. A strong network of 12000+ cement dealers and retailers spread across North East India, Bengal & Bihar helping us with consistent growth and profit enabling leadership position in the market. With a dominant presence in 10 states, Star Cement has done the largest private sector investment in the North East Region of INR 2093+ Crores.

Leadership transition marked organizational maturation. The founding generation began passing the baton to professional management, though family members retained key positions. This blend of entrepreneurial DNA and professional expertise positioned Star for its next phase—one where it might no longer be independent.

The modern era numbers tell a story of transformation: Revenue: 3,324 Cr, up from less than 2,000 Cr just five years ago. Market capitalization crossed ₹11,000 crore, making Star a meaningful player in India's cement sector. The company that started as a subsidiary of a plywood manufacturer was now valuable enough to attract India's cement giants.

But challenges remained. The company has delivered a poor sales growth of 11.4% over past five years. Company has a low return on equity of 9.31% over last 3 years. These metrics suggested that while Star had built an impressive regional franchise, translating that into superior financial returns remained a work in progress. The question now wasn't whether Star could survive outside its fortress, but whether it should remain independent at all.

VI. The UltraTech Strategic Investment & Industry Consolidation

December 27, 2024. The announcement landed like a thunderclap in cement circles: UltraTech Cement made a significant move by picking up an 8.69% non-controlling minority stake in Star Cement for Rs 851 crore at Rs 235 per share. For Star's promoters, this wasn't just a stake sale—it was the beginning of the endgame.

The timing was no accident. India's cement industry was in the throes of unprecedented consolidation. Two titans—UltraTech and Adani—were locked in an acquisition arms race, hoovering up regional players to build national dominance. Earlier this month, UltraTech completed its acquisition of India Cements to make the South India cement maker its subsidiary in a deal of Rs 7,100 crore. Just days before the Star Cement announcement, the Competition Commission of India (CCI) approved UltraTech's acquisition of ICL, which was initially announced in July 2024.

For UltraTech, Star represented a strategic gap-fill. UltraTech lacks a significant foothold in Northeast India. Its target of increasing capacity from 155 mtpa to 200 mtpa makes Star Cement a strategic addition. The Northeast wasn't just another market—it was the final frontier for a company with pan-India ambitions. UltraTech is India's largest cement maker, with 150.7 million tonnes of capacity in India as of October 2024. The Aditya Birla Group company plans to expand capacity to 200 MTPA by 2028.

The price paid—₹235 per share—represented a significant premium to Star's recent trading levels. This wasn't distressed asset buying; this was strategic value recognition. Post this announcement, shares in Star Cement gained around 7% at ₹245.23, giving its 2024 price growth 40%. The market understood: this 8.69% stake was likely just the appetizer.

The backdrop to this deal was India's broader cement consolidation narrative. Billionaire Gautam Adani's conglomerate is locked in a fierce battle with UltraTech Cement as the rivals snap up smaller firms in a bid to capitalise on expectations of heavy government spending on infrastructure. The Adani Group had acquired Swiss firm Holcim with a near 70 million tonne capacity in 2022. Some of its large acquisitions include Saurashtra-based Sanghi Industries and Penna Industries and Orient Cement.

For Star's promoters, the calculus was complex. Some promoter and promoter group entities of Star Cement have approached it to sell their equity holding. As of September 2024, promoters held a 66.47 per cent stake in the cement firm. Selling 8.69% to UltraTech was both a liquidity event and a strategic positioning—aligning with India's largest cement player while retaining control, at least for now.

The strategic logic for UltraTech was compelling: Acquiring a non-controlling stake could be UltraTech's way of "getting a foot in the door" and pre-emptively keeping Adani out. In the high-stakes game of cement consolidation, denying assets to competitors was as important as acquiring them yourself. The announcement triggered significant market activity, with 3.36 crore shares or 8.3% equity in Star Cement, valued at Rs 766 crore, exchanging hands through block deals.

Industry dynamics made consolidation inevitable. Analysts forecast 8% sales growth for the cement sector in 2025, supported by increased government spending on large infrastructure projects. The industry is also expected to benefit from improved sales realizations and higher profit margins, providing a favourable outlook for market leaders like UltraTech. In this environment, subscale players like Star faced a choice: get acquired or get marginalized.

The Northeast's unique economics added another dimension. Logistical constraints have led to higher pricing of Rs 1,000-1,200 per tonne compared to other regions. For UltraTech, acquiring Star meant buying into these premium economics. The investment in Star Cement reinforces UltraTech's presence in East India, a region known for its demand for infrastructure and housing projects.

What made this deal particularly interesting was its structure—a minority stake rather than outright acquisition. This could be tactical patience: building a relationship before a full takeover. Or it could reflect regulatory concerns about market concentration. The Indian cement industry is witnessing a wave of consolidation as leading players aim to strengthen their market positions amid rising competition.

For Star's remaining independent shareholders, the UltraTech investment was both validation and warning. Validation that their company had strategic value worth paying up for. Warning that independence might be temporary. The market reacted positively to UltraTech's strategic investment in Star Cement, with the latter's stock witnessing significant gains.

The deal also highlighted the premium attached to regional dominance. Star Cement is the largest manufacturer with the highest market share in the North East with an installed capacity of 7.7 mtpa (million tonnes per annum). In a consolidating industry, being number one in your region—even a challenging region like the Northeast—commanded value.

As 2024 ended, Star Cement stood at an inflection point. No longer fully independent but not yet absorbed, it occupied a liminal space in India's cement landscape. The question wasn't whether Star would eventually be fully acquired, but when, by whom, and at what price. The fortress built over two decades in the Northeast mountains had proven its worth. Now it was time to negotiate terms of surrender—or perhaps, terms of alliance.

VII. Unit Economics & Business Model Deep Dive

The economics of cement manufacturing in India tells a story of commoditization fighting against differentiation, of scale battling geography, of technology confronting tradition. Star Cement's unit economics reveal both the genius and limitations of its regional dominance strategy.

Start with the basics: cement is a terrible business on paper. The product is undifferentiated—one company's PPC is chemically identical to another's. Transportation costs eat 15-30% of realization because you're essentially shipping rocks. Capital intensity is crushing—it takes around US$ 120-140 per tonne to set up a cement plant, up from US$ 100 per tonne just a few years ago. And demand is cyclical, tied mercilessly to construction activity and monsoon patterns.

Yet Star Cement managed to turn these disadvantages into moats. Operational cost per ton approximately INR 4,500, compared to industry average of INR 3,800. Wait—higher costs are an advantage? In Star's case, yes. That ₹700 premium reflects the cost of operating in the Northeast: higher freight for raw materials, premium wages to attract skilled workers, infrastructure investments the company had to make itself. But these same costs create an entry barrier that's worth far more than ₹700 per ton.

The regional monopoly premium manifests in pricing power. Logistical constraints have led to higher pricing of Rs 1,000-1,200 per tonne compared to other regions. When your nearest competitor's plant is 500 kilometers away through mountain roads, you're not really competing on price—you're competing on availability. During monsoons, when roads wash out, Star's cement might be the only cement. That's pricing power that transcends economics textbooks.

Consider the EBITDA mathematics. Break-even EBIDTA, for instance, for a 1 MTPA capacity, operating at 80% utilization, and assuming a 70:30 debt to equity ratio, works out to around US$ 21 per tonne. Pan India players – the most profitable ones, given their brand strength and economies of scale – currently earn around US$ 13-16 EBITDA per tonne. Star Cement, operating in its Northeast fortress, consistently exceeds ₹1,600 per ton in EBITDA—roughly US$ 20, well above industry averages despite higher operational costs.

The clinker strategy adds another layer of economic sophistication. Star produces clinker—the key ingredient in cement—at its Meghalaya plants where limestone is abundant, then grinds it into cement at locations closer to consumption centers. This split manufacturing model optimizes both raw material costs and distribution expenses. The clinker can also be sold directly to other grinding units, providing revenue flexibility.

Cement demand in the region grew at a CAGR of 8-9% between FY19 and FY24, compared to 5-6% nationally. This isn't just population growth—it's catch-up economics. The Northeast's infrastructure deficit means every new road, bridge, or building represents incremental demand that wouldn't exist in saturated markets like Tamil Nadu or Gujarat. Star isn't just selling cement; it's selling development.

The vertical integration story extends beyond manufacturing. Star Cement controls limestone mines, operates captive power plants (critical in power-deficit regions), and even manages its own transportation fleet. In markets where supply chains are fragile, owning every link isn't inefficiency—it's insurance. During the 2020 lockdowns, when third-party transporters vanished, Star's captive fleet kept cement moving.

But the unit economics also reveal vulnerabilities. Low return on equity of 9.31% over last 3 years suggests that while Star generates decent operating profits, the capital intensity of the business dilutes returns. In a capital-abundant world where cost of capital matters more than access to capital, this is Star's Achilles heel. UltraTech, with its superior scale and lower cost of capital, can accept lower returns and still create shareholder value.

The competitive dynamics in the Northeast present a fascinating game theory problem. Star, Dalmia, and TopCem Together have a market share of 60% in Assam. They could compete aggressively, driving down prices and profits for everyone. Or they could practice "rational competition"—maintaining price discipline while competing on service and availability. The CCI's investigations into alleged cartelization suggest which path the companies chose.

Power and fuel costs, which account for 25%-30% of the total operating costs, are particularly challenging in the Northeast. While pan-India players benefit from coal linkages and proximity to ports for imported coal, Star relies heavily on local coal from Meghalaya's small-scale miners. The quality is inconsistent, the supply is erratic, but it's available—and in the Northeast, availability trumps efficiency.

The government infrastructure spending multiplier effect can't be ignored. Every rupee of government infrastructure spending in the Northeast generates more cement demand than in developed regions because the base is so low. A new highway doesn't just need cement for construction; it enables cement demand by making previously inaccessible areas developable. Star isn't just benefiting from infrastructure spending—it's leveraging it exponentially.

The grinding unit economics deserve special attention. A grinding unit costs roughly 40% of an integrated plant but can capture 60-70% of the value addition. Star's grinding units in Guwahati and Siliguri aren't just production facilities—they're market-capture devices, positioned to serve demand centers while keeping transportation costs manageable.

The sustainability narrative, often dismissed as ESG theater, has real economic implications for Star. In water-stressed, ecologically fragile Northeast India, environmental compliance isn't just regulation—it's social license to operate. Star's investments in pollution control and community development aren't charity; they're protection payments for operational continuity in sensitive regions.

As consolidation accelerates, Star's unit economics face a reckoning. In a fragmented industry, regional champions could maintain premium pricing. But if 3-4 players control 70-80% of capacity, the economics shift from regional monopolies to national oligopoly. Pricing might remain disciplined, but the premiums Star enjoyed from geographic isolation will erode as larger players build or acquire capacity in the Northeast.

The verdict on Star's unit economics is nuanced: brilliant for its context, challenging for its future. The company built a business model perfectly adapted to the Northeast's unique challenges, turning every disadvantage into a moat. But moats built on geography and infrastructure deficits are vulnerable to bridges—literal and metaphorical. As India develops and consolidates, Star's premium economics face compression. The question isn't whether Star's unit economics are good or bad, but whether they're sustainable in a consolidating, developing India. The UltraTech investment suggests the answer: valuable enough to buy, vulnerable enough to sell.

VIII. Playbook: Lessons in Regional Dominance

The Star Cement story offers a masterclass in building and monetizing regional dominance—lessons that extend far beyond cement, far beyond the Northeast. This is about turning constraints into competitive advantages, about finding monopolies hiding in plain sight, about the patient accumulation of small advantages that compound into impregnable positions.

First-Mover Advantages in Challenging Markets

The conventional wisdom says: go where the market is large, growing, and accessible. Star Cement did the opposite. They went where nobody else wanted to go, enduring short-term pain for long-term gain. The lesson isn't to seek difficulty for its own sake, but to recognize that difficult markets filter out weak competitors.

When Star built its Lumshnong plant in 2004, they weren't just building a cement factory—they were building optionality on an entire region's development. Every competitor who looked at the Northeast and decided it was "too hard" increased Star's future pricing power. The first-mover advantage wasn't about being first to market; it was about being first to commit irreversibly to a market others could still walk away from.

Building Infrastructure as a Moat

Most companies use existing infrastructure. Star had to build its own—roads, power plants, housing colonies, even basic utilities. This wasn't inefficiency; it was moat construction. Every piece of infrastructure Star built raised the bar for future entrants. A competitor couldn't just build a cement plant; they'd have to rebuild everything Star had spent decades creating.

The infrastructure moat has a multiplier effect. Star's roads didn't just serve Star's plants—they became critical arteries for the local economy. Star's housing colonies didn't just house Star's workers—they became centers of economic activity. The company embedded itself so deeply in the regional economy that extracting it would be like removing bones from a body.

The Conglomerate Advantage: Cross-Holdings and Synergies

The Century Plyboards connection wasn't just about capital—it was about capabilities. The plywood business had taught the founders how to operate in the Northeast: managing tribal relations, navigating complex regulations, dealing with infrastructure deficits. These soft skills, impossible to acquire quickly, gave Star a decade's head start over pure-play cement companies.

Conglomerate structures, unfashionable in Western business thinking, make perfect sense in frontier markets. Different businesses share not just capital but relationships, knowledge, and credibility. When Star Cement needed land, Century Plyboards' reputation opened doors. When Century needed cement for construction, Star provided it at transfer prices. The synergies weren't on spreadsheets—they were in trust networks.

Managing Stakeholders in Politically Sensitive Regions

The Northeast isn't just economically challenging—it's politically complex, with insurgencies, ethnic tensions, and center-state conflicts. Star's playbook for managing this complexity is instructive: Be local in employment, national in standards. Hire from the community but train to global standards. Pay taxes locally and visibly. Support local institutions—schools, hospitals, festivals—not as CSR but as community membership.

When protests or bandhs occur, Star's local relationships mean they're often exempted or given advance warning. This isn't corruption—it's community integration. The company isn't seen as an outside exploiter but as a local employer and contributor. In politically sensitive regions, this social license to operate is worth more than any physical asset.

When to Sell vs When to Stay Independent

The UltraTech investment presents Star's controlling shareholders with the classic dilemma: sell now at a good price or hold out for a great price later? The playbook here requires brutal honesty about competitive dynamics.

Star should consider selling if: The infrastructure deficit that created their moat is disappearing. National players can now replicate their local advantages. The capital required for the next phase of growth exceeds their access. The premium offered reflects scarcity value that won't last. Management succession is uncertain or problematic.

Star should stay independent if: They believe the Northeast's growth will accelerate dramatically. They can expand beyond the Northeast while maintaining their core fortress. They can access capital markets efficiently for expansion. The cultural and operational uniqueness provides sustainable advantage. Family commitment to the business remains strong across generations.

The Role of Patient Capital in Industrial Businesses

Star Cement took seven years from incorporation to meaningful profitability. Two decades to regional dominance. This timeline is incompatible with venture capital, challenging for private equity, and frustrating for public markets. But for patient capital—often family capital in emerging markets—it's perfect.

The playbook lesson: Industrial businesses in frontier markets require patient capital that understands J-curves, accepts cyclicality, and values strategic position over quarterly earnings. The Century group's ability to fund Star through its gestational period, using cash flows from the plywood business, exemplifies this patient capital advantage.

Sustainability Initiatives and ESG Considerations

In the Northeast, sustainability isn't a nice-to-have—it's existential. The region's ecological fragility means environmental violations could trigger immediate shutdown. Star's early investments in environmental compliance, initially seen as costs, became competitive advantages as regulations tightened.

The ESG playbook for frontier markets: Exceed local environmental standards even when enforcement is weak. Today's lax enforcement is tomorrow's retroactive liability. Invest in community development that creates economic stakeholders in your success. Document everything—ESG reporting that seems excessive today becomes table stakes tomorrow. Build sustainability into operations, not just reports. When ESG becomes mandatory, you're already compliant while competitors scramble to catch up.

The Meta-Lesson: Strategic Arbitrage

Star Cement's deepest lesson is about strategic arbitrage—profiting from the gap between perception and reality. The Northeast was perceived as uninvestable; the reality was a rapidly growing market with limited competition. Cement was perceived as commoditized; the reality was regional differentiation. Family businesses were perceived as unsophisticated; the reality was deep local knowledge and patient capital.

The playbook for strategic arbitrage: Look for markets where conventional wisdom creates systematic mispricings. Bad geography, difficult logistics, complex regulations—these aren't bugs to avoid but features to leverage. Find the structural reason why smart competitors stay away, then determine if you have an unfair advantage in overcoming that reason. Build positions slowly and quietly before perception catches up to reality. Sell (possibly) when the arbitrage closes—when perception finally matches reality.

Star Cement's journey from a plywood company's side project to a potential crown jewel in India's largest cement company's portfolio demonstrates these principles in action. They didn't just build a cement company—they built a playbook for turning the undesirable into the unassailable. Whether that playbook remains relevant in a consolidating, developing India is the question that will determine Star's final chapter.

IX. Bear vs Bull Case Analysis

The investment case for Star Cement exists at the intersection of regional monopoly economics and national consolidation dynamics. Both bears and bulls have compelling arguments, making this a fascinating study in market dichotomy.

Bull Case: The Northeast India Infrastructure Supercycle

The bulls see Star Cement as a leveraged bet on India's final frontier. The Northeast, historically neglected, is experiencing an infrastructure awakening. The government's Act East policy isn't just rhetoric—it's backed by real capital allocation. Since 1st January, 2021, 30 projects worth Rs. 413.63 Crore have been sanctioned in various North Eastern States under North East Special Infrastructure Development Scheme (NESIDS).

But this is just the beginning. The Northeast requires everything: highways, railways, airports, urban infrastructure, industrial facilities. Each project creates multiplicative cement demand. The region's infrastructure deficit is so severe that even reaching 50% of the national average would require decades of aggressive construction. Star Cement, as the largest cement player in North East with a market share of over 23%, captures a disproportionate share of this growth.

The moat remains robust despite UltraTech's minority investment. Geography hasn't changed—the Himalayas still make logistics challenging. During monsoons, transport from outside remains impossible for months. Star's 20-year head start in building local infrastructure, relationships, and operational knowledge can't be replicated quickly. The company enjoys a pricing premium of Rs 5-10 more than Dalmia in most markets—this isn't disappearing anytime soon.

The UltraTech investment itself is bullish. When India's largest cement company pays ₹235 per share—a significant premium—it validates Star's strategic value. This could be the first step toward a full acquisition at an even higher premium. UltraTech's capacity target of 200 MTPA requires Northeast presence; Star provides instant market leadership in a region where organic entry would take decades.

Expansion potential remains massive. Star intends to increase capacity to 25 MTPA by 2030—a 4x increase from current levels. The Northeast alone could absorb this capacity given the infrastructure pipeline. Additionally, Star's expansion into West Bengal and Bihar opens new markets where their operational expertise in challenging geographies provides competitive advantage.

The ESG angle strengthens the bull case. As environmental regulations tighten, Star's early investments in sustainability become competitive advantages. In ecologically sensitive Northeast India, companies without strong environmental credentials won't receive permits for expansion. Star's position as an ESG leader in the region ensures continued license to grow.

Bear Case: Structural Challenges in a Consolidating Industry

The bears see a company trapped between regional limitations and national competition. Poor sales growth of 11.4% over past five years despite operating in supposedly high-growth markets raises questions about execution. If Star can't grow faster than the national average while enjoying regional dominance, what happens when competition intensifies?

The return metrics are concerning. Low return on equity of 9.31% over last 3 years in a capital-intensive industry suggests structural profitability challenges. Operational cost per ton approximately INR 4,500, compared to industry average of INR 3,800—this 18% cost disadvantage becomes crushing if pricing power erodes. In a commodity business, the low-cost producer wins long-term.

Geographic concentration is a critical vulnerability. The core market of North East India contributes 76% of its sales. This concentration makes Star vulnerable to regional economic shocks, political instability, or weather events. One bad monsoon, one extended bandh, one policy change could devastate earnings. Diversification attempts into West Bengal and Bihar face intense competition from entrenched players.

The UltraTech investment might be bearish, not bullish. Why did promoters sell if prospects were so bright? As of September 2024, promoters held a 66.47 per cent stake—selling 8.69% suggests either capital needs or pessimism about independence. UltraTech's entry, even as a minority shareholder, could constrain strategic flexibility. Major decisions might now require informal UltraTech approval.

New entrants threaten the regional monopoly. With improved infrastructure, the Northeast becomes accessible to national players. Adani's aggressive expansion could target the Northeast next. The announcement triggered significant market activity, with 3.36 crore shares or 8.3% equity in Star Cement, valued at Rs 766 crore, exchanging hands through block deals—suggesting some investors are exiting.

High operational costs limit competitiveness outside the Northeast. In West Bengal and Bihar, Star faces UltraTech, Dalmia, and others without geographic advantages. The company's high-cost structure, justified in protected Northeast markets, becomes a liability in competitive markets. Expansion beyond the core region might destroy rather than create value.

The Balanced View: Timing and Price Matter

The reality likely lies between extremes. Star Cement is neither the next multibagger nor a value trap—it's a decent business at an inflection point where strategic value might exceed standalone value.

The bull case depends on execution and independence. Can Star maintain pricing discipline while growing volumes? Can management navigate the UltraTech relationship while pursuing independent strategy? Can expansion beyond the Northeast succeed without destroying margins? If yes, the stock could double as infrastructure spending accelerates.

The bear case reflects legitimate structural concerns. Regional champions often struggle to become national players. The cement industry's consolidation typically favors acquirers over targets. Star's operational disadvantages won't disappear—geography is destiny in cement.

The investment decision ultimately depends on three factors:

Time Horizon: Short-term (1-2 years), Star likely benefits from Northeast infrastructure spending and potential acquisition premium. Long-term (5-10 years), structural challenges might dominate unless the company transforms its cost structure or gets acquired.

Risk Tolerance: Star is a leveraged bet on Northeast India. High reward if the region develops rapidly, high risk if development disappoints or competition intensifies. Conservative investors should recognize this isn't a defensive play despite the regional moat.

Acquisition Probability: If you believe UltraTech will acquire Star fully within 2-3 years, current prices might offer 30-40% upside. If Star remains independent, returns depend on operational execution in an increasingly competitive market.

The meta-question is whether Star Cement is a business or an asset. As a business, it faces structural challenges that limit long-term returns. As an asset—a strategic foothold in Northeast India—it has scarcity value in a consolidating industry. The UltraTech investment suggests the market is pricing Star more as an asset than a business. Whether that's appropriate depends on your view of India's cement industry endgame.

X. Epilogue & "What Would We Do?"

Standing at the crossroads of independence and absorption, Star Cement's board faces perhaps the most consequential decision in the company's history. The UltraTech minority investment isn't just capital—it's a courtship that could end in marriage or tears. Let's think through this as if we were in the boardroom, weighing not just spreadsheets but destinies.

Should the founders take UltraTech's offer if it comes?

The arithmetic is seductive. If UltraTech paid ₹235 per share for 8.69%, a full acquisition might command ₹280-300, implying a 40-50% premium to current levels. For promoters holding 57.7%, this represents ₹6,000-7,000 crore in value—generational wealth by any measure. After two decades of building in challenging terrain, this might be the harvest season.

But the emotional calculus is complex. Star Cement isn't just a business—it's a testament to entrepreneurial courage, to betting on India's forgotten frontier when nobody else would. Selling wouldn't just transfer assets; it would end a legacy. The Bhajanka-Agarwal families would go from industrialists to investors, from builders to bystanders.

The strategic logic, however, might be irresistible. Cement consolidation isn't a possibility—it's happening now. Standalone regional players face a stark future: marginalization as national giants build competing capacity, or absorption at progressively lower premiums as bargaining power erodes. Selling to UltraTech today at peak strategic value might be better than selling to Adani tomorrow at distressed prices.

If we were in their position? We'd seriously consider selling, but with structure and conditions. Not a outright sale, but a phased transaction: UltraTech acquires 51% now at a premium, with puts and calls for the remaining stake based on performance milestones. This provides liquidity, ensures professional management continuity, and preserves upside if the Northeast boom materializes. The founders could retain board seats, ensuring Star's regional DNA isn't lost in UltraTech's national machine.

The Northeast India infrastructure story—next 10 years

The Northeast's development isn't optional—it's inevitable. Geography makes it India's gateway to Southeast Asia. The Act East policy requires the Northeast to be developed, not as charity but as strategic necessity. The region's hydroelectric potential, natural resources, and tourism assets remain largely untapped.

Infrastructure investment will likely follow an S-curve: slow initial progress as base infrastructure develops, then rapid acceleration as network effects kick in, finally plateauing as the region approaches national averages. We're likely entering the acceleration phase now. The next decade could see the Northeast's infrastructure stock double or triple.

For cement demand, this translates to sustained 10-12% annual growth—nearly double the national average. Star Cement, with its established position, will capture disproportionate value. But—and this is crucial—new capacity will also enter. The premium pricing Star enjoys will compress, though volume growth should more than compensate.

Can Star Cement become a national player?

Honestly? Probably not as an independent entity. The unit economics don't support it. Star's high-cost structure, justified in the protected Northeast, becomes a liability in competitive markets. The company lacks the balance sheet to fund massive expansion. Most critically, it lacks the operational DNA of national competition—the sophistication in procurement, logistics, and marketing that UltraTech and Dalmia have perfected over decades.

Star's destiny is regional dominance, not national presence. This isn't failure—it's focus. Being the undisputed champion of a growing region might create more value than being a subscale national player. The attempt to expand into West Bengal and Bihar should be seen as negotiating leverage and optionality, not core strategy.

Climate change and cement industry transformation

Climate change presents both crisis and opportunity for Star. The crisis: cement production accounts for 8% of global CO2 emissions. Regulatory pressure will intensify. Carbon taxes could devastate high-cost producers. The opportunity: Star's relatively modern plants and early ESG investments position it better than older, more polluting competitors.

The Northeast's abundant rainfall and hydroelectric potential could make it India's green manufacturing hub. Star could position itself as India's "green cement" producer, commanding premiums from environmentally conscious consumers. This requires investment in carbon capture, alternative fuels, and possibly breakthrough technologies like LC3 (Limestone Calcined Clay Cement) that reduce clinker requirements.

The role of regional champions in India's development

Star Cement represents something beyond business—it's a development catalyst. In regions where government capacity is limited and national corporations are absent, regional champions become quasi-infrastructure. They build not just factories but ecosystems. They create not just jobs but middle classes.

India needs its Star Cements—companies willing to build where others won't, to invest where returns are distant, to commit where risks are high. The financialization of everything, the obsession with quarterly earnings, threatens this patient capital model. If every regional champion sells to national giants, who will develop the next frontier?

Final takeaways on building monopolies in frontier markets

Star Cement's journey offers timeless lessons wrapped in temporal specifics:

Geography is destiny, until it isn't. Star built a monopoly on the Northeast's inaccessibility. But infrastructure development and industry consolidation are eroding geographic moats everywhere. The lesson: milk geographic advantages aggressively but prepare for their eventual disappearance.

First-mover advantages are real but perishable. Star's two-decade head start created enormous value. But first-mover advantages have half-lives. The lesson: being first matters, but staying ahead matters more.

Patient capital enables impatient strategies. Star could afford to lose money for years because Century Plyboards provided patient capital. This patience enabled aggressive expansion that impatient capital wouldn't tolerate. The lesson: capital structure determines strategy more than strategy determines capital structure.

Regional monopolies attract national predators. Success makes you a target. Star's regional dominance made it strategic for UltraTech. The lesson: build your castle knowing someone bigger will eventually want it.

Culture eats strategy, but economics eats culture. Star's entrepreneurial culture built the business, but consolidation economics might end independence. The lesson: respect culture, but respect economics more.

What would we do? The honest answer:

If we were Star's controlling shareholders, we'd engineer a structured sale to UltraTech within 18-24 months. Not because Star is a bad business, but because it's a good business at peak strategic value. The Northeast will develop with or without Star's independence. UltraTech's resources could accelerate Star's potential while providing founders with liquidity and legacy preservation.

The structure would be crucial: immediate sale of 51%, providing control premium and liquidity. Performance earnouts based on Northeast volume growth over 3-5 years. Board seats and regional autonomy guarantees. Potential buyback rights if UltraTech fails to develop the region. This isn't surrender—it's strategic alliance.

If we were minority shareholders, we'd hold for the acquisition premium but prepare to exit post-transaction. Star's value lies in its strategic position, not its standalone prospects. Once absorbed into UltraTech, that strategic value transfers to the acquirer.

The broader lesson transcends Star Cement: In consolidating industries, regional champions face a binary choice—become a consolidator or become consolidated. Star lacks the scale to consolidate. Better to choose your partner than have one chosen for you. Better to sell at strategic value than financial value. Better to preserve legacy through integration than lose it through marginalization.

Star Cement's story isn't ending—it's transforming. From family enterprise to professional corporation. From regional champion to national strategic asset. From independent entity to (likely) division of India's largest cement company. This isn't failure—it's the natural evolution of successful regional businesses in globalizing economies.

The entrepreneurs who built Star Cement in the mountains of Meghalaya achieved something remarkable: they developed a region, created thousands of jobs, and built enormous value from nothing. If the final chapter involves selling to UltraTech, it's not capitulation—it's completion. The fortress they built in the Northeast will stand. It will just fly a different flag.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube