Strides Pharma Science: The Scarcity Hunter's Playbook

I. Introduction & Episode Roadmap

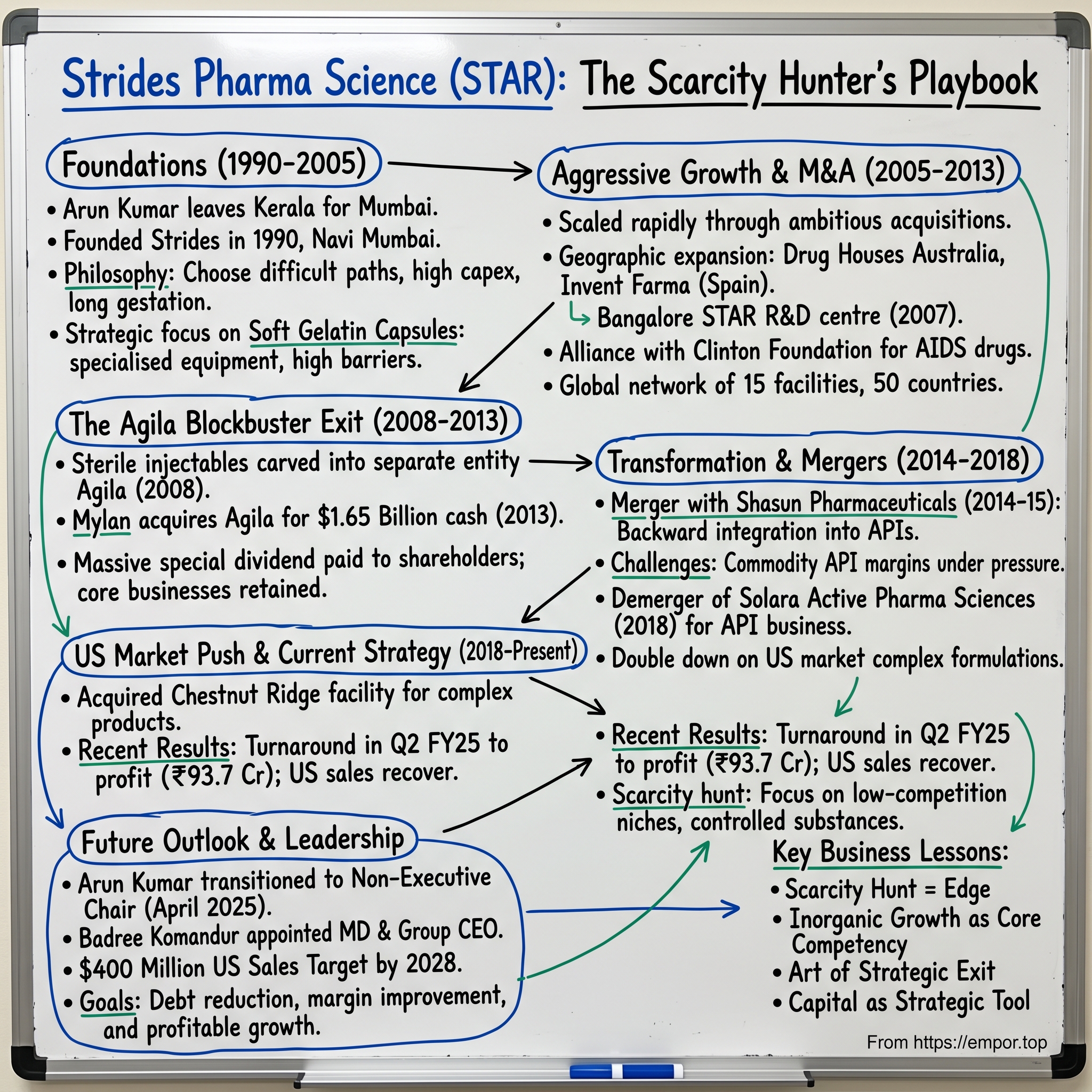

Picture this: A 21-year-old from Kerala, son of a government servant, leaves the hills of Ooty with nothing but ambition and heads to Mumbai in the early 1980s. No family business, no pharma legacy, no safety net. Fast forward four decades—that same person has built, sold, and rebuilt pharmaceutical businesses worth billions, including one blockbuster exit that netted $1.65 billion from Mylan. This is the story of Arun Kumar and Strides Pharma Science, a ₹7,414 crore market cap company that sells medicines in over 100 countries today.

But here's what makes this story fascinating for students of business strategy: Kumar didn't build Strides by competing where everyone else was competing. He developed an almost contrarian philosophy—actively seeking out the most difficult, capital-intensive, long-gestation businesses that others avoided. "We look at areas where there is scarcity," he once explained, "in manufacturing, around a particular domain or technology, or in a particular market." This scarcity-hunting approach would define every major strategic decision over three decades.

The central question we'll explore isn't just how a first-generation entrepreneur built one of the world's leading producers of soft gelatin capsules—it's how he mastered the art of building businesses in spaces others considered too hard, too expensive, or too risky. And perhaps more intriguingly, how he developed the discipline to know exactly when to sell, when to merge, and when to rebuild.

This episode traces three distinct acts in the Strides story. First, the foundation years from 1990 to 2005, when Kumar established the company's DNA of pursuing complex generics. Second, the inorganic growth machine era from 2005 to 2013, culminating in the spectacular Agila sale. And third, the transformation period from 2014 to present, marked by the Shasun merger, US market expansion, and Kumar's recent transition from executive to non-executive chairman in April 2025.

What emerges is a playbook for building value in pharmaceutical markets through a combination of technical complexity, strategic acquisitions, and impeccable timing. It's also a case study in how emerging market entrepreneurs can compete globally not by being cheaper, but by being willing to tackle what others won't.

II. The Founder's Journey: From Kerala to Pharma Empire

The monsoon rains of 1982 were particularly heavy when Arun Kumar arrived in Mumbai, carrying a single suitcase and the kind of determination that only comes from having no backup plan. Born to a government servant father in Kerala and raised in the colonial hill station of Ooty, Kumar had grown up watching the disciplined, predictable life of public service. But something in him craved the opposite—the chaos, risk, and potential of business.

Those first eight years in Mumbai's pharmaceutical industry were his real education. Working for various pharma companies, Kumar wasn't just learning the technical aspects of drug manufacturing; he was studying the industry's blind spots. He noticed how most Indian pharma companies in the 1980s were content being contract manufacturers or focusing on simple generics. The complex stuff—soft gels, sterile injectables, controlled substances—was left to multinational corporations. Why? Because these required massive capital investment, sophisticated technology, and years before seeing returns.

Where others saw barriers, Kumar saw opportunity. In 1990, at age 29, he founded Strides Arcolab Limited in Vashi, Navi Mumbai, with a philosophy that would seem counterintuitive to most entrepreneurs: deliberately choose the hardest path. "We consciously went after difficult-to-operate domains," Kumar would later reflect. "High capex, long gestation—these scared others away but created scarcity value for those willing to persist."

The early recognition came quickly. By 2000, just a decade after founding Strides, Kumar was named Ernst & Young's Entrepreneur of the Year for Healthcare. But awards don't capture what really distinguished him in those early years. Former colleagues describe a leader who would spend hours on factory floors, obsessing over production yields and quality metrics. One early employee recalled Kumar personally supervising the installation of the company's first soft gel manufacturing line, sleeping in the factory for three straight nights to ensure everything was calibrated perfectly.

This hands-on approach extended to business development. Kumar didn't just send salespeople to international markets; he personally traveled to Africa, Southeast Asia, and Latin America, building relationships with distributors and understanding local regulatory requirements. In an era before LinkedIn and video calls, he was building a global network through handshakes and face-to-face meetings.

But perhaps the most revealing aspect of Kumar's entrepreneurial philosophy was his attitude toward debt and risk. Unlike many first-generation entrepreneurs who remained conservative with capital structure, Kumar was comfortable leveraging the balance sheet for growth. "Debt is just a tool," he once told investors. "The question is whether you're using it to build something scarce and valuable." This comfort with leverage would enable rapid expansion but also create challenges that would test the company's resilience.

By 2005, Strides had established itself as a serious player in complex generics, but Kumar was just getting started. The foundation was built—now it was time to scale aggressively through what would become one of the most ambitious acquisition sprees in Indian pharma history.

III. Building the Foundation (1990-2005)

The year 1996 marked a turning point. Strides had survived its first six years—no small feat for a bootstrap startup in capital-intensive pharma—but Kumar knew survival wasn't enough. That year, he made a decision that would define the company's trajectory: instead of competing in the crowded simple generics market, Strides would focus exclusively on products others found too difficult to manufacture.

The strategy crystallized around soft gelatin capsules, a delivery form that requires specialized equipment, expertise, and significant upfront investment. While tablets could be made with relatively simple compression machines, soft gels needed sophisticated encapsulation technology, precise temperature controls, and expertise in managing liquid and semi-solid formulations. The global market was dominated by a handful of players, creating exactly the kind of scarcity Kumar was hunting for. The rapid expansion from 1996 to 2006 was breathtaking in its ambition. Strides wasn't just adding capacity; it was building an entire ecosystem. New manufacturing facilities, R&D centers, quality control labs—each investment added another layer of complexity but also another barrier to competition. It emerged as one of the world's largest manufacturers of soft gelatin capsules, a position that would become central to its identity.

But growth came with a price. By 2005, the company had accumulated significant debt from its expansion. The balance sheet was stretched, and Kumar faced a choice that would define many entrepreneurs: pull back and consolidate, or double down and expand further. He chose the latter, but with a twist—growth would now come primarily through acquisitions rather than organic expansion.

One partnership from this period deserves special attention: the alliance with the Clinton Foundation for supplying AIDS drugs. This wasn't just another contract; it represented Strides' entry into the institutional business of supplying life-saving medicines to developing countries. The margins were lower than branded generics, but the volumes were massive, and more importantly, it gave Strides credibility in global health circles that money couldn't buy.

The technical capabilities being built were impressive. Beyond soft gels, Strides was developing expertise in controlled substances, sterile manufacturing, and complex release mechanisms. Each new capability required not just equipment but trained personnel, quality systems, and regulatory expertise. A former quality director recalled the company hiring consultants from the US and Europe, not just to train staff but to instill a culture of precision that would meet the standards of the world's strictest regulators.

By 2005, Strides had also begun to crack the code on international regulatory approvals. Getting a drug approved by the US FDA or European regulators isn't just about meeting quality standards; it's about documentation, consistency, and the ability to handle inspections that can make or break a company. Strides invested heavily in this unglamorous but critical capability, building teams that could navigate the labyrinthine requirements of multiple regulatory agencies simultaneously.

The numbers tell part of the story—revenues had grown from virtually nothing to hundreds of crores—but the real achievement was strategic positioning. Strides had emerged as one of the world's leading producers of soft gelatin capsules, competing with companies many times its size. It had also established a reputation for taking on products others wouldn't touch: drugs with complex manufacturing requirements, products needing special handling, formulations requiring sophisticated technology.

As 2005 drew to a close, Kumar had proven his thesis: there was indeed value in pursuing scarcity. But he was about to embark on an even more ambitious phase—using mergers and acquisitions not just to grow, but to fundamentally transform what Strides could become.

IV. The Inorganic Growth Machine (2005-2013)

The boardroom at Strides' Mumbai office in early 2006 witnessed a heated debate. Kumar had just proposed acquiring Drug Houses of Australia (Asia) Private Limited, a move that would stretch the company's already leveraged balance sheet even further. The CFO was nervous, investment bankers were cautious, but Kumar saw something others didn't: a footprint in Asia-Pacific that would take years to build organically.

The company's inorganic growth strategy over the years resulted in foray into new markets, addition of new business segments, therapy segments and manufacturing infrastructure. This wasn't random deal-making; it was strategic assembly of capabilities. Each acquisition was chosen for specific reasons: geographic presence, product portfolio, manufacturing technology, or regulatory approvals.

The Drug Houses acquisition gave Strides instant access to markets across Southeast Asia and established relationships with hospital chains and pharmacy groups that had taken the Australian company decades to build. But Kumar wasn't done. Within months, he was in Spain, negotiating a joint venture with Invent Farma. The Spanish connection wasn't about market access—it was about European regulatory expertise and a bridge to Latin American markets through historical and linguistic ties.

Then came what employees still call "the Bangalore moment"—the 2007 inauguration of the STAR global R&D centre in India's tech capital. This wasn't just another R&D facility; it was Kumar's statement of intent. The center, built at considerable expense, housed sophisticated analytical equipment, formulation development labs, and pilot-scale manufacturing capabilities. More importantly, it became a magnet for talent, attracting scientists from Indian institutes and returning professionals from the US and Europe.

The pace of deals accelerated. Between 2008 and 2012, Strides completed over a dozen acquisitions and partnerships, each adding a piece to Kumar's puzzle. A facility in Poland for access to Eastern European markets. A partnership in Kenya for East African distribution. A manufacturing plant in Brazil for Latin American presence. The company was transforming from an Indian manufacturer with export ambitions to a truly global pharmaceutical company.

But the real masterstroke was happening quietly in the background. In 2008, Kumar began consolidating all of Strides' sterile injectable capabilities into a separate division called Agila Specialties. While the market saw this as internal restructuring, Kumar was actually preparing one of the most audacious moves in Indian pharma history.

The company built 15 manufacturing sites in six countries and marketing presence in 50 countries. This wasn't just expansion; it was strategic positioning. Each facility was chosen for specific capabilities: high-potency products in one location, controlled substances in another, large-volume parenterals in a third. The complexity was staggering—different regulatory requirements, quality standards, and market dynamics in each location.

The human cost of this rapid expansion often goes untold. Executives were constantly traveling, integration teams were permanently on the road, and the organization was in perpetual transformation. One senior manager recalled working on three acquisitions simultaneously, flying from India to Italy to Brazil in a single week. The stress was immense, but so was the excitement of building something unprecedented in Indian pharma.

Financial engineering became as important as pharmaceutical manufacturing. Kumar and his CFO structured deals creatively—part cash, part stock, earnouts based on performance, vendor financing. They raised debt in multiple currencies, tapped international markets, and constantly refinanced to optimize capital structure. The balance sheet became increasingly complex, but it enabled acquisitions that would have been impossible through conventional financing.

The product portfolio expanded to include softgel capsules, hard-gel capsules, tablets and dry and wet injectables. Each product category required different expertise, equipment, and regulatory approvals. Managing this complexity required sophisticated systems and processes that Strides had to build on the fly.

By 2012, the transformation was complete. Strides had gone from a single-country manufacturer to a global pharmaceutical company with operations spanning continents. The company that had started with one factory in Navi Mumbai now controlled a network of facilities producing everything from simple tablets to complex injectables. But Kumar's biggest move was yet to come—and it would shock even those who thought they understood his ambitions.

V. The Agila Blockbuster: Building and Selling (2008-2013)

February 2013. The news hit Bloomberg terminals at 6:47 AM Indian time: "Mylan to Acquire Agila Specialties for $1.65 Billion." Portfolio managers across Mumbai's financial district did double-takes. Agila was Strides' injectable division—how could selling a division be worth more than three times the entire company's revenue?

The story of Agila begins five years earlier, in 2008, when Kumar made a decision that puzzled many observers. He began carving out all of Strides' sterile injectable assets into a separate entity. Not just the obvious ones—the manufacturing facilities and product portfolios—but also the best R&D scientists, the most experienced quality teams, and critically, the pending US FDA approvals for complex injectable products.

"We're creating focus," Kumar told analysts at the time. But he was actually creating optionality. By structuring Agila as a distinct entity with its own P&L, management team, and growth strategy, he was building something that could either become Strides' crown jewel or, if the price was right, provide the exit that would fund the company's next transformation.

The injectable market in 2008-2012 was experiencing a perfect storm of opportunity. Manufacturing failures at major suppliers had created shortages. The US FDA was cracking down on quality issues, taking several facilities offline. Hospitals were desperate for reliable suppliers of critical injectables—cancer drugs, anesthetics, antibiotics. Agila positioned itself perfectly: high quality, reliable supply, and most importantly, the ability to manufacture products others couldn't or wouldn't.

By 2011, Agila had become a force in the global injectables market. It operated seven world-class manufacturing facilities, including FDA-approved plants. The product portfolio included over 100 injectable products with another 150 in development. Revenue had grown to over $400 million annually. But what really caught Mylan's attention was the pipeline—complex injectables, biosimilars in development, and a series of first-to-file opportunities in the US.

The negotiation with Mylan was a masterclass in value creation. Kumar didn't just sell current revenue; he sold future potential. He demonstrated how Agila's capabilities in complex injectables could complement Mylan's oral solid dose portfolio. He showed how Agila's emerging market presence could accelerate Mylan's global expansion. Most cleverly, he created competitive tension by engaging multiple potential buyers simultaneously.

The final deal terms were staggering: $1.65 billion in cash, with $1.35 billion paid upfront. For perspective, Strides' entire market capitalization before the announcement was less than $500 million. The company declared a special dividend of Rs. 500 per share—about $8.50 at the prevailing exchange rate—resulting in a pre-tax distribution of $525 million to shareholders.

But here's what made the Agila sale truly brilliant: Kumar retained Strides' core soft gel and oral solid dose businesses. He essentially sold one leg of a three-legged stool for more than three times what the market valued the entire stool. And he immediately redeployed capital into strengthening the remaining businesses and reducing debt.

The market reaction was euphoric but also puzzled. Why sell such a profitable, growing business? Kumar's answer revealed his philosophy: "I'm passionate about building businesses, but pragmatic enough to know when someone else can create more value." He saw that injectables were becoming increasingly capital-intensive, requiring constant investment in new facilities and technology. Mylan had deeper pockets and global scale. For Strides shareholders, taking the cash now was better than competing against giants later.

The Agila sale also demonstrated Kumar's ability to see around corners. Within two years of the sale, the US injectable market became brutally competitive. The FDA approved multiple new facilities, ending shortages. Pricing collapsed. Several companies that had rushed into injectables faced massive losses. Mylan itself would later face challenges with the Agila assets, including FDA warning letters and facility remediations.

For Strides, the Agila sale provided something invaluable: a war chest for the next phase of growth and the credibility that comes from executing a billion-dollar exit. Kumar had proven he could not just build businesses but also monetize them at peak value. This reputation would prove crucial in the transformative deals that followed.

VI. The Shasun Merger & Transformation (2014-2018)

September 2014. Just eighteen months after the Agila windfall, Kumar surprised the market again. Strides would merge with Shasun Pharmaceuticals, a Chennai-based API and formulations company. The deal structure was complex: an all-stock merger that would create an entity with combined revenues exceeding ₹2,500 crores. But complexity was Kumar's comfort zone.

Shasun brought what Strides lacked: backward integration into active pharmaceutical ingredients (APIs) and a strong presence in the custom synthesis business. The merger wasn't just about size; it was about creating a vertically integrated pharmaceutical company that could control its entire value chain from raw materials to finished doses.

The integration challenged even Kumar's experienced team. Shasun had its own culture, shaped by its South Indian roots and its founders' conservative approach. Strides was aggressive, deal-driven, comfortable with leverage. Merging these cultures while maintaining business momentum required delicate handling. Kumar spent months traveling between Bangalore, Mumbai, and Chennai, personally overseeing integration committees and addressing employee concerns.

By November 2015, the merged entity officially became Strides Shasun Limited. The numbers looked impressive: 15 manufacturing facilities, presence in over 100 countries, and a product portfolio spanning the entire pharmaceutical value chain. But beneath the surface, challenges were emerging. The API business, particularly the commodity APIs that Shasun brought, faced intense Chinese competition. Margins were eroding, and the expected synergies were proving elusive.

Kumar's response was characteristically bold: if parts of the business didn't fit the strategy, divest them. In 2018, Strides announced the demerger of its commodity API business into a separate entity called Solara Active Pharma Sciences. Shareholders received Solara shares proportionally, but Strides could now focus on its core strength: complex finished formulations for regulated markets.

The demerger was financially and operationally complex, requiring separation of manufacturing facilities, employee transfers, and customer contract assignments. But it achieved Kumar's objective: a leaner, more focused Strides that could compete in high-margin regulated markets without the drag of commodity businesses.

During this period, Strides also doubled down on the US market. The pharma generics business was driven by IP-based product licensing and global partnerships, specializing in niche generic formulations in various dosage forms for regulated markets including the United States, Europe, and Australia. The company invested heavily in R&D for complex generics, particularly products with limited competition due to manufacturing difficulties or regulatory barriers.

The transformation wasn't without casualties. Debt levels remained elevated despite the Agila proceeds. Some acquisitions didn't deliver expected returns. The stock price remained volatile, frustrating long-term shareholders who had expected consistent returns after the Agila success. But Kumar was playing a longer game, positioning Strides for what he saw as the next wave of opportunity in global generics.

VII. The US Market Push & Current Strategy (2018-Present)

August 2021, Chestnut Ridge, New York. Kumar stood in the sprawling facility that had once belonged to Endo Pharmaceuticals, now acquired by Strides for $24.9 million—a fraction of its replacement cost. The facility represented both opportunity and risk: opportunity to establish US-based manufacturing for controlled substances and complex products, risk in turning around an underutilized asset in America's highly competitive generic market. The US business had become critical, representing 36% of revenues, but performance was inconsistent. Revenue reports showed US sales targets of $400 million by 2028, ambitious given current challenges. The business had hit quarterly highs in Q2 FY25, but maintaining momentum proved difficult in the face of intense pricing pressure and competition from both Indian peers and Chinese manufacturers entering the US generics market.

In April 2022, Kumar made another strategic move that surprised observers: he returned as Executive Chairman and Managing Director. The founder, now in his sixties, was taking direct operational control again. The message was clear—Strides needed experienced leadership to navigate increasingly complex market dynamics. Under his renewed leadership, the company focused on debt reduction, margin improvement, and selective product launches rather than volume-driven growth. But the most significant transition came in April 2025. Arun Kumar transitioned to Non-Executive Chairperson effective April 5, 2025, after successfully handing over executive responsibilities to Badree Komandur, who had been appointed Managing Director and Group CEO in June 2024. This wasn't a retirement—Kumar remained deeply involved as a board member—but it marked the end of an era of founder-led operational management.

The current strategy reflects lessons learned from three decades of pharmaceutical warfare. Rather than chasing volume in commoditized products, Strides focuses on complex generics with limited competition. The US facility acquired from Endo specializes in controlled substances—products requiring special DEA licenses and handling procedures that create natural barriers to entry. The company targets products where only 2-3 competitors exist rather than those with 10-15 players fighting for market share.

Q1 FY26 revenue hit ₹1120 Cr with 19.5% EBITDA margin, with $400mn US sales target reaffirmed by 2028. This ambitious target requires nearly doubling US revenues from current levels, but management believes the pipeline of complex products and operational improvements make it achievable.

The debt reduction strategy has shown results. Years of high leverage that funded acquisitions are finally being unwound through improved cash flows and selective asset sales. The company's focus has shifted from growth at any cost to profitable growth with strong return metrics.

Recent performance has been encouraging. In Q2 FY25, the company reported a consolidated net profit of Rs 93.7 crore, a turnaround from a loss of Rs 149.45 crore in the same period last year, with revenue rising 20% year-on-year to Rs 1,201 crore. The US business showed signs of recovery, though sustaining momentum remains challenging.

Looking ahead, Strides faces both opportunities and headwinds. The focus on complex generics positions it well for higher margins, but execution risk remains high. Each product launch requires significant investment and regulatory approval with no guarantee of commercial success. Competition from both established players and new entrants, particularly from China, continues to intensify. Yet Kumar's philosophy of pursuing scarcity—now embedded in the company's DNA—continues to guide strategic decisions even as operational leadership transitions to the next generation.

VIII. Product Portfolio & Manufacturing Excellence

Walking through Strides' Bangalore facility feels like entering a pharmaceutical United Nations. In one section, technicians carefully monitor the production of soft gelatin capsules containing vitamin supplements bound for Australia. Next door, a sterile suite produces anti-malarial drugs destined for sub-Saharan Africa through WHO programs. Down the hall, scientists work on complex modified-release formulations targeting the US market. This diversity isn't accidental—it's the result of decades of strategic capability building.

Strides has emerged as one of the world's largest manufacturers of soft gelatin capsules, a position that provides both competitive advantage and pricing power. The soft gel technology requires precise control of multiple variables: gelatin composition, fill material viscosity, sealing temperature, and drying conditions. Small variations can lead to leaking capsules, inconsistent drug release, or stability issues. This complexity creates a moat—while anyone can buy tablet presses, mastering soft gel manufacturing takes years of experience and continuous refinement.

The numbers tell the story of scale: 15 manufacturing sites in six countries and marketing presence in 50 countries. But raw capacity means little without regulatory approvals. Strides' facilities have been inspected and approved by the world's toughest regulators—US FDA, European Medicines Agency, UK MHRA, Australian TGA. Each approval represents years of work and millions in investment, creating barriers that protect margins even as competition intensifies.

The product portfolio reflects Kumar's scarcity-hunting philosophy. Rather than competing in high-volume antibiotics or simple pain relievers where dozens of manufacturers fight for market share, Strides focuses on niches. Controlled substances that require special DEA licensing. Hormone products needing dedicated facilities to prevent cross-contamination. Complex modified-release formulations that most generic companies lack the expertise to develop.

Products include softgel capsules, hard-gel capsules, tablets and dry and wet injectables. Each category serves different strategic purposes. Soft gels leverage the company's core manufacturing expertise. Tablets and hard capsules provide portfolio breadth for customer relationships. The remaining injectable capacity (post-Agila sale) focuses on niche products rather than competing in commoditized segments.

The institutional business deserves special attention. Partnering with organizations like the Clinton Foundation and becoming a WHO pre-qualified supplier for anti-HIV drugs provides steady revenue with predictable demand. While margins are lower than commercial generics, the volumes are substantial and payment terms reliable. More importantly, this business provides social impact that resonates with employees and stakeholders—Strides' drugs help treat millions of patients in developing countries who would otherwise lack access to life-saving medicines.

Manufacturing excellence at Strides goes beyond equipment and facilities. The company has developed sophisticated quality systems that can handle the complexity of multiple products, markets, and regulatory requirements simultaneously. A single batch might need to meet US FDA standards for the American market, EU GMP for Europe, and WHO prequalification for institutional sales. Managing this complexity requires IT systems, documentation protocols, and training programs that took decades to build.

The R&D center in Bangalore, inaugurated as the STAR facility in 2007, has evolved into a critical competitive advantage. With over 200 scientists, it focuses not on breakthrough drug discovery but on solving complex formulation challenges. How do you make a soft gel that remains stable in tropical climates without refrigeration? How do you develop a generic version of a drug with dozens of patents covering various aspects of its formulation? These aren't glamorous questions, but answering them successfully can mean the difference between a blockbuster product and an expensive failure.

Recent developments show continued evolution. The company has invested in capabilities for nasal sprays, topical formulations, and transdermal patches—all delivery forms with higher barriers to entry than simple oral solids. Each new capability requires not just equipment but expertise in formulation, analytical methods, stability testing, and clinical bioequivalence studies.

The manufacturing network's geographic distribution provides both opportunities and challenges. Having facilities in the US enables faster response to market opportunities and reduces supply chain complexity for controlled substances. Italian operations provide access to European markets with local manufacturing advantages. But managing quality and compliance across multiple jurisdictions requires sophisticated systems and constant vigilance—a single FDA warning letter can shut down an entire facility and destroy years of investment.

IX. Financial Performance & Market Position

The numbers tell a story of transformation, volatility, and gradual stabilization. Strides Pharma's current market capitalization stands at ₹7,414 crore, with revenue of ₹4,631 crore and profit of ₹354 crore. But these headline figures mask a more complex narrative of financial engineering, strategic pivots, and the ongoing challenge of balancing growth with profitability.

The Agila sale in 2013 created a financial anomaly that still reverberates. The $1.65 billion transaction price was extraordinary—more than three times Strides' total revenue at the time. The special dividend of Rs. 500 per share returned massive value to shareholders, but it also reset expectations. How do you follow an act that spectacular? The answer, it turns out, is that you don't try to replicate it—you build something different.

Post-Agila, Strides faced the challenge of deploying capital wisely while managing investor expectations. The Shasun merger in 2014-2015 was partly about scale but also about narrative—showing markets that Strides could still do transformative deals. The subsequent demerger of the commodity API business to Solara in 2018 demonstrated discipline, acknowledging that not all revenue is good revenue if it comes with low margins and high capital requirements.

The company has delivered a poor sales growth of 10.6% over past five years, a figure that frustrates growth-oriented investors. But this number requires context. The divestment of Agila removed high-revenue injectables. The Solara demerger stripped out commodity APIs. The US market faced unprecedented pricing pressure. When adjusted for these factors, the underlying business shows more resilience than headline growth suggests.

The return metrics tell a more positive story. ROE improvement shows a 3-year average of 50.4%, exceptional for a capital-intensive pharmaceutical manufacturer. This improvement comes from multiple sources: better product mix favoring higher-margin complex generics, operational efficiency improvements, and crucially, a more disciplined approach to capital allocation.

Promoter holding stands at 28.3%, providing skin in the game while leaving room for institutional investors. Institutional investors hold 47%, with foreign investors at 39.46%—one of the highest in the pharma sector. This ownership structure reflects both confidence from sophisticated investors and the company's success in attracting international capital.

But challenges persist. Promoters have pledged 50.1% of their holding, a red flag for governance-conscious investors. While pledging doesn't necessarily indicate distress—it might simply reflect personal leverage for other investments—it creates overhang risk if share prices fall significantly.

The debt situation has improved but remains a focus area. Years of acquisition-fueled growth left Strides with elevated leverage that has taken time to unwind. The company has made progress through asset sales, improved cash generation, and more disciplined capital allocation, but achieving a truly conservative balance sheet remains a work in progress.

Quarterly performance shows volatility that reflects both market dynamics and execution challenges. The US business, critical at 36% of revenues, saw peak quarterly sales of $58 million but has fallen below $40 million. This decline reflects brutal pricing pressure in US generics, where success attracts competition and margins evaporate quickly.

Geographic revenue distribution provides both diversification and complexity. North America remains the largest market, but contributions from Europe, emerging markets, and institutional business provide balance. This diversification helped cushion the blow when US pricing collapsed, but it also increases operational complexity and regulatory compliance costs.

The valuation picture is intriguing. Stock is trading at 2.91 times its book value, reflecting market recognition of intangible assets like regulatory approvals, customer relationships, and manufacturing expertise not fully captured on the balance sheet. Yet analyst estimates suggest the stock trades significantly below fair value, indicating either market skepticism about execution or an opportunity for patient investors.

Working capital management has improved significantly. Years of focus on inventory optimization, receivables collection, and payment term negotiations have freed up cash for debt reduction and growth investments. The cash conversion cycle has shortened, improving return on capital employed even as the business faces top-line pressures.

X. Playbook: Business & Investing Lessons

The Strides story offers a masterclass in emerging market entrepreneurship, but the lessons extend far beyond India's borders. Kumar's playbook—refined over three decades—provides insights for entrepreneurs, investors, and students of business strategy navigating complexity in global markets.

The Scarcity Hunter's Edge

Kumar's fundamental insight was counterintuitive: deliberately choose the hardest problems. While competitors fought in crowded markets for simple generics, Strides pursued products others wouldn't touch. Soft gels requiring specialized equipment and expertise. Controlled substances needing DEA licenses and special handling. Sterile injectables demanding massive capital investment and flawless quality systems.

This approach created multiple advantages. Limited competition meant better pricing power. High barriers to entry provided protection even after patents expired. Customers valued reliability in these difficult categories, creating stickier relationships. The strategy required patience—these businesses took years to build—but once established, they generated returns that justified the wait.

Inorganic Growth as Core Competency

Between 2005 and 2013, Strides completed over a dozen major acquisitions. But this wasn't empire building for its own sake. Each deal served specific strategic purposes: geographic expansion, capability acquisition, or regulatory approval access. Kumar developed an internal M&A capability that could identify, negotiate, and integrate acquisitions with remarkable efficiency.

The key was discipline about what not to buy. Kumar walked away from deals that didn't fit the scarcity thesis, even when bankers pushed for scale. He also understood that buying was only half the equation—integration determined success. Strides developed playbooks for merging quality systems, combining sales forces, and harmonizing IT platforms. This operational excellence in post-merger integration became as important as deal-making prowess.

The Art of Strategic Exit

The Agila sale revealed Kumar's most sophisticated skill: knowing when to sell. By 2012, injectable markets were attracting massive investment. New competitors were entering, the FDA was approving more facilities, and pricing power was eroding. Kumar saw the peak approaching and acted decisively.

But timing was only part of the story. Kumar had structured Agila as a separable entity years before the sale, maintaining distinct financials and operations. When buyers appeared, he could move quickly without untangling complex interdependencies. He also created competitive tension, engaging multiple bidders simultaneously. The result—$1.65 billion for a business generating $400 million in revenue—validated the strategy.

Managing Complexity Across Borders

Operating 15 facilities across six countries while serving 100+ markets creates staggering complexity. Different regulatory requirements, quality standards, tax regimes, and cultural norms all need navigation. Strides developed systems and processes that could handle this complexity without becoming bureaucratic.

The solution was selective centralization. Core functions like R&D and strategic planning remained centralized for efficiency. But local operations retained autonomy for market-specific decisions. Information systems connected the network, providing visibility without micromanagement. This balance between global coordination and local flexibility became a competitive advantage.

Capital Structure as Strategic Tool

Kumar's comfort with leverage distinguished him from many first-generation entrepreneurs. He understood that debt, properly used, could accelerate growth and enhance returns. But he also learned from near-disasters in 2006 when excessive leverage almost sank the company.

The evolution was toward sophisticated capital management. Different subsidiaries had different capital structures optimized for their specific needs. The company tapped multiple funding sources—bank debt, bonds, equity—to optimize cost and flexibility. Financial engineering became as important as pharmaceutical engineering.

Building for Institutional Investment

From early days, Kumar focused on attracting institutional capital. This meant investing in systems, governance, and transparency that sophisticated investors demanded. Independent directors, professional management, clear communication—all required investment but paid dividends in access to capital and valuation multiples.

The high foreign institutional ownership—among the highest in Indian pharma—validates this approach. International investors provide not just capital but credibility, market intelligence, and pressure for performance. Building a company that meets global institutional standards created options that wouldn't exist otherwise.

First-Generation Entrepreneurship Challenges

Without family business background or inherited wealth, Kumar faced unique challenges. No safety net meant each decision carried existential risk. No established relationships meant building networks from scratch. No precedent meant learning from mistakes rather than family wisdom.

But these constraints also created advantages. No legacy thinking meant freedom to pursue unconventional strategies. No family obligations meant decisions based purely on business logic. No inherited culture meant building one optimized for the chosen strategy. The very challenges of first-generation entrepreneurship became sources of strength.

The Strides playbook isn't universally applicable—it requires risk tolerance, patience, and operational excellence that not all possess. But for those willing to pursue scarcity, master complexity, and maintain discipline about when to build versus when to sell, it offers a proven path to value creation in global pharmaceutical markets.

XI. Analysis & Investment Case

The investment case for Strides Pharma Science presents a study in contrasts—compelling strategic positioning offset by execution risks, attractive valuation shadowed by governance concerns, growth potential tempered by market headwinds. Understanding these dynamics requires peeling back layers of complexity to reveal the core investment thesis.

The Bull Case: Scarcity Value at a Discount

The optimistic narrative starts with valuation. Multiple analysts suggest the stock trades significantly below intrinsic value, with some estimates indicating a 36% discount to fair value. For a company with established manufacturing capabilities, regulatory approvals, and global market presence, this discount seems excessive.

The earnings trajectory supports optimism. Analysts forecast earnings growth of 28% annually, driven by margin expansion rather than just revenue growth. This operating leverage story resonates—as complex generic launches gain traction and operational improvements flow through, profitability should expand disproportionately.

The strategic position as one of the world's largest soft gel manufacturers provides a defensive moat. This isn't a capability that new entrants can easily replicate. Years of manufacturing expertise, regulatory approvals, and customer relationships create barriers that protect against commoditization.

The US business, despite recent challenges, offers substantial upside. With infrastructure in place and a pipeline of complex products awaiting approval, even modest success could drive significant value creation. The $400 million revenue target by 2028 might seem ambitious, but it requires only a handful of successful launches given the high value of complex generics.

Management transition, paradoxically, might be positive. Kumar's move to non-executive chairman brings fresh operational leadership while retaining strategic guidance. New CEO Badree Komandur can focus on execution while Kumar provides vision and relationships. This combination of continuity and change could unlock value.

The Bear Case: Structural Headwinds and Execution Risk

Skeptics point to persistent challenges that have plagued Strides for years. The 10.6% five-year revenue CAGR in a growing pharmaceutical market suggests structural rather than cyclical issues. US pricing pressure shows no signs of abating, with new entrants, particularly from China, intensifying competition.

The pledged promoter shares—50.1% of their holding—raise governance concerns. While pledging might reflect personal financial decisions unrelated to company operations, it creates overhang risk. A sharp market correction could trigger margin calls, forcing stake sales at inopportune times.

Debt levels, while improving, remain elevated for a company facing revenue headwinds. Interest coverage has improved but hasn't reached comfortable levels. Any execution stumbles could quickly stress the balance sheet, limiting strategic flexibility.

The complexity of operations across multiple geographies and product categories creates execution risk. Each facility must maintain regulatory compliance—a single FDA warning letter can shut down production and destroy years of investment. This regulatory sword of Damocles hangs over all pharmaceutical manufacturers but seems particularly relevant given Strides' history of rapid expansion.

Competition continues intensifying across all segments. In soft gels, Chinese manufacturers are building capacity aggressively. In complex generics, big pharma companies are moving downstream to capture value. In emerging markets, local champions are strengthening. The competitive moat, while real, faces erosion.

The Balanced View: Optionality with Patience

The realistic assessment acknowledges both opportunity and risk. Strides isn't a momentum play—it requires patience and tolerance for volatility. But for investors with appropriate time horizons, the risk-reward appears favorable.

The key is optionality. Multiple paths could drive value creation: successful US launches, margin expansion from operational improvements, strategic partnerships or licensing deals, or another transformative transaction like Agila. Not all need to succeed for the investment to work—even partial success could drive substantial returns from current valuations.

The institutional ownership provides comfort. Sophisticated investors controlling 47% of shares suggests the story resonates with professional managers. The high foreign institutional holding indicates global investors see value despite the complexity.

The fundamental question for investors: Is this a value trap or a coiled spring? The answer likely depends on execution over the next 2-3 years. If management can deliver even modest US growth while maintaining margins and reducing debt, the current valuation appears compelling. If execution falters, the complexity and leverage could create a negative spiral.

For long-term fundamental investors, Strides offers an interesting proposition—exposure to growing pharmaceutical markets through a company with proven capabilities trading at a discount to replacement cost. The journey won't be smooth, but for those who can stomach volatility and have conviction in the scarcity thesis, the potential rewards justify the risks.

XII. Future Outlook & Strategic Priorities

The next chapter of the Strides story is being written against a backdrop of profound pharmaceutical industry transformation. Patent cliffs creating generic opportunities, emerging market healthcare expansion, and technological disruption all present both opportunities and threats. How Strides navigates these currents will determine whether it remains a mid-tier player or achieves the transformation Kumar has long envisioned.

The $400 Million US Ambition

Management's target of $400 million in US sales by 2028 requires nearly doubling current revenue run rates. This isn't impossible—a single successful complex generic launch can generate $50-100 million annually if competition is limited. With multiple products in the pipeline, probability suggests some will succeed.

The strategy focuses on the "white space"—products too complex for simple generic manufacturers but not valuable enough for originators to defend aggressively. Think controlled-release formulations of psychiatric drugs, hormone therapies requiring special handling, or combination products with complex delivery mechanisms. Each represents a puzzle that Strides' R&D and manufacturing capabilities are designed to solve.

The Chestnut Ridge facility acquired from Endo provides crucial infrastructure for controlled substances—a category with natural barriers to entry. DEA licenses, security requirements, and handling protocols limit competition. If Strides can successfully launch even a handful of controlled-release opioid alternatives or ADHD medications, the revenue impact could be transformative.

Debt-Free Ambitions and Capital Allocation

The journey toward a debt-free balance sheet represents more than financial engineering—it's about strategic flexibility. Without interest burdens and covenant restrictions, Strides could pursue opportunities more aggressively, whether acquisitions, R&D investments, or market expansion.

Cash flow improvements are already visible. Working capital optimization, better receivables management, and selective pruning of low-margin business have freed up resources. The question is deployment—will management return cash to shareholders, invest in growth, or maintain a fortress balance sheet for optionality?

The demerger discussions continue evolving. Following the Solara precedent, management has indicated willingness to separate businesses that don't fit the core strategy. This could unlock value by allowing focused management and appropriate capital structures for different business segments.

Emerging Market Dynamics

While the US grabs headlines, emerging markets offer quieter but potentially more sustainable growth. Africa, where Strides has built strong presence over decades, is experiencing healthcare expansion as governments increase spending and insurance coverage expands.

The institutional business serving WHO, UNICEF, and similar organizations provides ballast. These contracts offer lower margins but predictable demand and social impact that resonates with stakeholders. As global health initiatives expand, particularly post-COVID, this segment could surprise on the upside.

India itself presents opportunities. The government's push for healthcare access, insurance expansion, and quality generic medicines creates domestic growth potential. Strides' manufacturing capabilities and regulatory expertise position it well for government contracts and institutional sales.

Technology and Manufacturing Evolution

The future of pharmaceutical manufacturing is shifting toward continuous processing, AI-driven quality control, and personalized medicine. Strides must balance investing in new technologies while sweating existing assets.

Continuous manufacturing, where products flow through the production process without interruption, could dramatically reduce costs and improve quality. Early investments in this technology could provide competitive advantages as the industry transitions from batch processing.

Digital transformation extends beyond manufacturing. Supply chain visibility, predictive maintenance, and data analytics all offer efficiency improvements. The company that masters these technologies while maintaining regulatory compliance will have significant advantages.

Partnership and Licensing Opportunities

Rather than doing everything internally, Strides increasingly looks to partnerships for growth. Licensing deals for complex products, co-development agreements for difficult formulations, and distribution partnerships for new markets all provide capital-efficient expansion.

The soft gel expertise creates partnership opportunities with companies lacking this capability. Contract manufacturing for branded companies or other generic firms could provide steady revenue with limited risk. The key is selecting partners that value Strides' capabilities and will pay appropriately for them.

ESG and Sustainability Imperatives

Strides debuted with an outstanding ESG rating of 76/100 in S&P Global's CSA 2024, placed significantly ahead of peers in the first year of ESG evaluation. This isn't just about compliance—it's about access to capital, customer relationships, and employee engagement.

Sustainability in pharmaceutical manufacturing means reducing solvent use, minimizing waste, and improving energy efficiency. These initiatives often improve profitability while enhancing reputation. As ESG considerations increasingly influence investment decisions, strong performance here could improve valuations.

The Strategic Imperative

Looking ahead, Strides faces a clear strategic imperative: prove that the scarcity-hunting model still works in an increasingly competitive global pharmaceutical market. This requires disciplined execution, selective investment, and occasionally, the courage to walk away from opportunities that don't fit the strategy.

The pieces are in place—manufacturing capabilities, regulatory approvals, market presence, and improving financial position. What's needed now is execution that converts potential into performance. If management can deliver consistent results while maintaining strategic discipline, the next five years could see Strides finally achieve the transformation Kumar has pursued for three decades.

The path won't be linear—pharmaceutical markets rarely are. But for a company that has survived and thrived through multiple cycles, adapted to changing markets, and executed transformative transactions, the future offers more opportunity than threat. The question isn't whether Strides can succeed, but whether it can execute consistently enough to reward the patience of long-term shareholders who share Kumar's vision of value through scarcity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube