South Indian Bank: From Kerala's Scheduled Bank Pioneer to Digital Banking Transformation

I. Introduction & Episode Roadmap

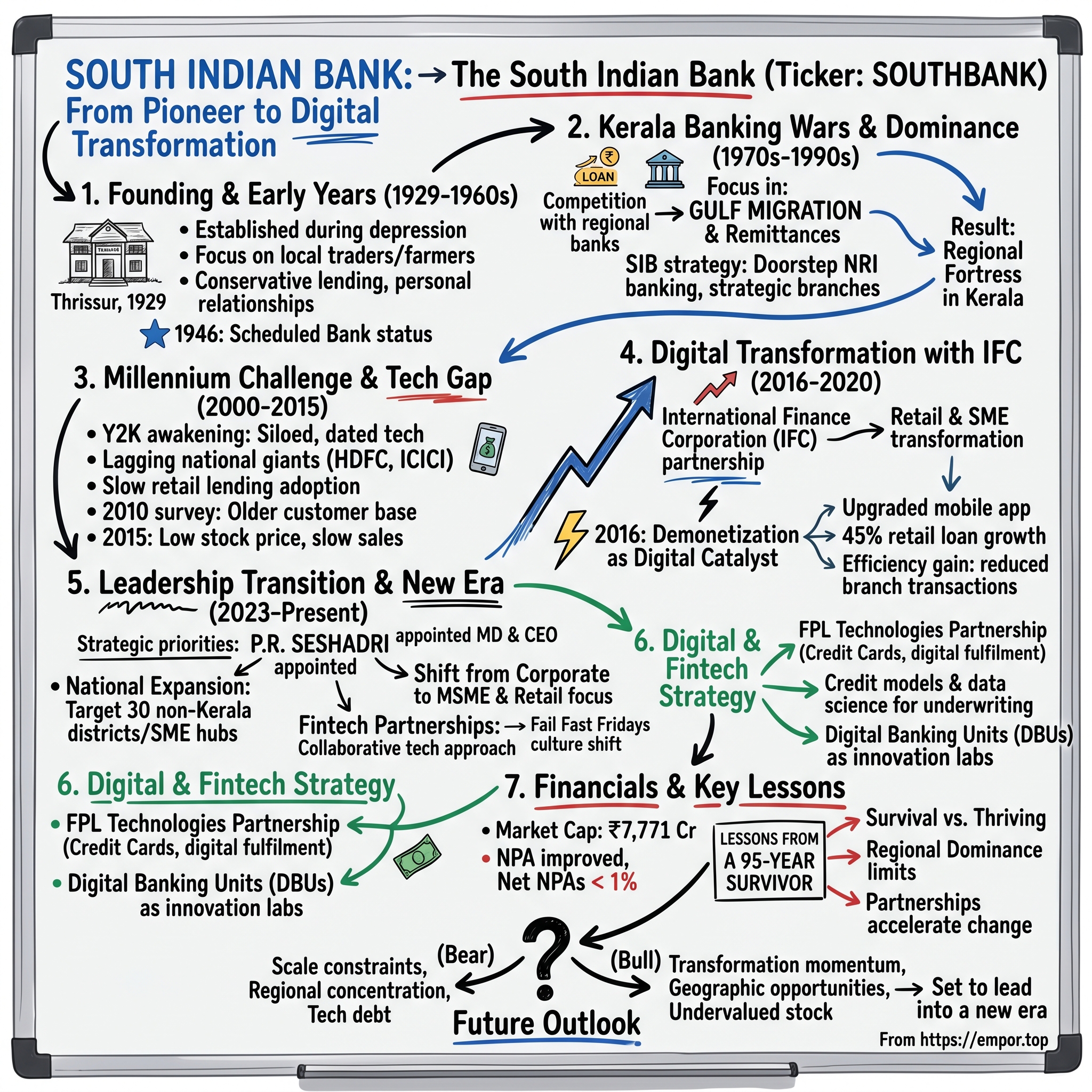

Picture this: It's 1929, the Great Depression is about to devastate the global economy, India is still under British rule, and in the temple town of Thrissur, Kerala, a group of local businessmen gather to establish what would become one of India's most enduring private banks. The South Indian Bank opened its doors at Round South, Thrissur, with ambitions that seemed almost quaint by today's standards—to serve the local trading community and provide safe banking to Kerala's agricultural economy.

Fast forward 95 years. The bank that started in a single building now operates 955 banking outlets and 1,290 ATMs across 26 states and 4 union territories. It has survived the Great Depression, World War II, Indian independence, multiple rounds of bank nationalization, the 1991 economic liberalization, the dot-com bust, the 2008 financial crisis, demonetization, and a global pandemic. While hundreds of its peers have vanished through mergers, acquisitions, or outright failure, South Indian Bank remains standing—scarred perhaps, but still fighting.

Here's the question that should fascinate any student of business history: How did a small Kerala bank not just survive but remain independent for nearly a century while better-capitalized, seemingly stronger institutions fell by the wayside? The answer isn't just about conservative banking or regional dominance. It's about a series of calculated pivots, near-death experiences, and the delicate balance between preserving heritage and embracing disruption. Today, with a market capitalization of ₹7,771 Crore, South Indian Bank sits at a fascinating inflection point. Under new leadership since October 2023, the bank is attempting its most ambitious transformation yet—breaking free from its Kerala fortress to become a true national player while simultaneously racing to build digital capabilities that took neo-banks a fraction of the time to develop.

This is a story of survival through conservatism, the price of that survival, and the audacious bet that a 95-year-old institution can reinvent itself without losing its soul. It's about understanding why some banks thrive while others merely survive, and what happens when a conservative regional player decides it's finally time to swing for the fences.

Our journey takes us from pre-independence India through the tumultuous decades of nationalization, the liberalization boom, the digital revolution, and into an uncertain future where traditional banks face existential questions about their relevance. Along the way, we'll uncover the strategic decisions, missed opportunities, and cultural DNA that shaped one of India's most enduring financial institutions.

II. Founding Story & Early Years (1929–1960s)

The year 1929 was perhaps the worst possible time to start a bank. As South Indian Bank opened its doors at Round South in Thrissur on January 29, the world was nine months away from the Wall Street crash that would trigger the Great Depression. In India, the independence movement was gaining momentum, civil disobedience campaigns were disrupting commerce, and the banking sector was a chaotic mess of unregulated institutions that appeared and disappeared with alarming frequency.

Yet for a group of Thrissur businessmen, mostly from the Syrian Christian community that dominated Kerala's trade networks, this chaos represented opportunity. The existing banking system, dominated by British banks and a handful of large Indian institutions, largely ignored small traders, farmers, and the emerging middle class of Kerala. Indigenous banks that did exist were often family-run affairs with questionable practices and even more questionable balance sheets.

South Indian Bank's founders had a different vision. They wanted to create an institution that combined the professionalism of British banks with the local knowledge and community trust of traditional Kerala financiers. The bank's early ledgers, still preserved in their Thrissur headquarters, reveal a fascinating pattern: alongside conventional business loans, there were advances for rubber plantations, loans secured by gold jewelry (a Kerala specialty that continues today), and financing for the spice trade that connected Kerala's hills to global markets.

The pre-independence period tested the young bank's resilience repeatedly. The 1930s saw multiple bank failures across India—between 1929 and 1939, over 200 banks collapsed. South Indian Bank survived by maintaining what would become its defining characteristic: extreme conservatism in lending coupled with deep community relationships. While other banks chased growth through aggressive lending, SIB's founders insisted on knowing every borrower personally, understanding their family background, and often requiring gold as collateral—a practice that seemed antiquated even then but proved prescient during economic downturns.

The Second World War brought unexpected opportunities. Kerala's strategic position on maritime trade routes and its production of crucial war materials like rubber and spices created a boom economy. South Indian Bank, with its established networks in these sectors, saw deposits surge. But the bank's leadership, led by its second chairman K.P. Hormis, made a crucial decision: instead of expanding rapidly, they used the windfall to strengthen capital reserves and establish new branches methodically, never straying far from their Kerala base.

The achievement that truly set South Indian Bank apart came on August 7, 1946—just one year before India's independence. The Reserve Bank of India included SIB in the second schedule, making it a scheduled bank. This wasn't just a regulatory milestone; it was a validation that transformed the bank's standing overnight. Scheduled bank status meant SIB could now borrow from the RBI, participate in clearing houses, and most importantly, present itself as a peer to much larger institutions. For a bank that was barely 17 years old and operated primarily in one state, this was remarkable.

The immediate post-independence years brought both opportunity and existential threat. The partition of India in 1947 triggered massive capital flight and banking crisis in many parts of the country. Kerala, relatively insulated from partition's direct impacts, became a haven for capital seeking stability. But the bigger threat was ideological. The new Indian government, influenced by socialist thinking, viewed private banks with suspicion. Nationalization rumors swirled constantly.

South Indian Bank's response was clever: they positioned themselves not as a private bank serving elite interests, but as a community institution supporting Kerala's agricultural economy and small businesses. They pioneered agricultural lending programs that predated government priority sector mandates by decades. When the Kerala government launched development programs, SIB was often the first private bank to participate.

By 1960, South Indian Bank had established a template that would serve it for decades: conservative lending, deep local roots, community trust, and just enough innovation to stay relevant without taking excessive risks. They had survived the Great Depression, World War II, independence, and the early threats of nationalization. The question now was whether this formula could scale beyond Kerala's borders.

III. The Kerala Banking Wars & Regional Dominance (1970s–1990s)

If you walked through any major Kerala town in the 1970s, you'd witness something unique in Indian banking: fierce competition between multiple private sector banks for every customer, from wealthy plantation owners to small shopkeepers. This was the era of the Kerala Banking Wars, and South Indian Bank was fighting on multiple fronts.

The landscape was crowded. Federal Bank, Catholic Syrian Bank, Dhanalakshmi Bank, and several smaller institutions all traced their roots to Kerala's Christian trading communities. Each had loyal customer bases, often divided along denominational lines (Syrian Catholics favored CSB, while other Christian communities might lean toward Federal or SIB). But the real battle wasn't for existing customers—it was for the massive opportunity that was about to reshape Kerala's economy: Gulf migration.

The 1973 oil crisis, paradoxically, became Kerala's goldmine. As petroleum prices quadrupled, Gulf countries launched massive infrastructure projects requiring millions of workers. Kerala, with its educated population and historical maritime connections, became the primary source of Indian labor. By 1980, remittances from Keralites working in the Gulf exceeded the state's entire budget. Every major Kerala bank understood that capturing these remittance flows meant survival; missing them meant irrelevance.

South Indian Bank's approach was methodical but aggressive. While Federal Bank rushed to open branches in every major town, SIB focused on strategic locations—not just where migrants came from, but where their families lived. The bank pioneered what they called "doorstep NRI banking." Bank officers would visit the homes of Gulf workers' families, helping elderly parents who couldn't navigate complex banking procedures access remittance funds. They established dedicated NRI branches with extended hours to accommodate international calling times.

The physical branch became SIB's fortress. By 1985, the bank operated over 200 branches, with some Kerala districts having an SIB branch every few kilometers. This might seem like overexpansion, but each branch served as a community hub. Branch managers knew every customer's family history, attended local festivals, and often mediated financial disputes informally. When a Gulf worker wanted to send money home for his daughter's wedding or to buy agricultural land, he didn't call a call center—he called his branch manager's home.

Competition intensified through the 1980s. Federal Bank, SIB's primary rival, pursued an aggressive growth strategy, expanding beyond Kerala into Mumbai and Delhi to capture NRI deposits at the source. Catholic Syrian Bank focused on technology, being among the first to introduce computerized banking. Smaller banks like Lord Krishna Bank (later acquired by Centurion Bank) tried to differentiate through higher interest rates.

South Indian Bank's response revealed both its strengths and limitations. Rather than chase Federal Bank to metros, SIB doubled down on Kerala and strategic locations in Tamil Nadu and Karnataka. They couldn't match CSB's technology investments, so they emphasized personal service. When competitors offered higher deposit rates, SIB sold stability and trust. "Your money is safer with us" became an unspoken motto, particularly powerful after several cooperative banks failed in the late 1980s.

The 1991 economic liberalization changed everything. Suddenly, new private sector banks like HDFC and ICICI could enter the market with massive capital, modern technology, and no legacy baggage. Many predicted the death of old private sector banks. Indeed, several Kerala banks didn't survive—Nedungadi Bank was acquired by Punjab National Bank in 2003, and numerous smaller institutions disappeared through mergers.

South Indian Bank survived, but at a cost. Their conservative approach meant they avoided the bad loans that plagued aggressive lenders, but it also meant slower growth. While HDFC Bank grew from nothing to national prominence in a decade, SIB remained largely confined to South India. The bank's loan book grew steadily but unspectacularly. They missed the retail lending boom of the late 1990s, staying focused on traditional products like gold loans and agricultural credit while new private banks pioneered credit cards and personal loans.

By 2000, South Indian Bank faced an existential question: Was survival enough? They had won the Kerala Banking Wars in the sense that they remained independent and profitable. But the battlefield had shifted. The competition was no longer other Kerala banks but national giants with technology platforms that made physical branches seem obsolete. The NRI remittance business, once SIB's goldmine, was being disrupted by specialized money transfer operators and online platforms.

IV. The Millennium Challenge: Technology & Scale (2000–2015)

The Y2K bug that never materialized became an unexpected catalyst for South Indian Bank's digital awakening. As 1999 drew to a close, the bank's technology team—all twelve of them—worked frantically to ensure their systems wouldn't collapse when the calendar flipped to 2000. The fire drill exposed an uncomfortable truth: SIB was running on technology that belonged in a museum.

While new private banks like HDFC and ICICI had built their operations on modern core banking systems from day one, South Indian Bank was still operating in silos. A customer with accounts in Thrissur and Kochi branches might as well have been banking with two different institutions. The bank's first attempt at computerization in the mid-1990s had resulted in a patchwork of incompatible systems—some branches used one software, others used different platforms, and many still relied primarily on physical ledgers.

The core banking transformation that began in 2001 was nothing short of traumatic. Branch managers who had run their fiefdoms for decades suddenly had to follow standardized procedures. Employees comfortable with pen-and-paper banking had to learn computers. The project, initially budgeted at ₹15 crores, eventually cost nearly ₹50 crores and took four years to fully implement. Several senior managers took early retirement rather than adapt.

But the real challenge wasn't technical—it was strategic. As South Indian Bank struggled with basic digitization, the market was racing ahead at breathtaking speed. ICICI Bank launched Internet banking in 1998 and had a million online customers by 2003. HDFC Bank's ATM network expanded to over 1,000 machines. These banks weren't just offering better technology; they were fundamentally reimagining banking.

The contrast was stark. A young professional in Bangalore could open an ICICI account online, get a credit card delivered to his door, and manage everything through Internet banking. The same customer at SIB would need to visit a branch, fill out paper forms, and wait days for basic services. The bank's customer base increasingly consisted of those who valued personal relationships over convenience—a shrinking demographic.

South Indian Bank's loan portfolio during this period reflected both its strengths and weaknesses. The bank engaged in providing a range of banking services including retail banking, corporate banking, and treasury operations through four segments. Their gold loan business, built on decades of expertise, remained robust. Agricultural lending, mandated by priority sector requirements, was profitable due to deep rural relationships. But they completely missed the retail lending boom. While HDFC Bank built a massive mortgage portfolio and ICICI dominated vehicle loans, SIB watched from the sidelines.

The 2008 financial crisis, ironically, validated SIB's conservatism briefly. While ICICI Bank's stock crashed over 70% due to concerns about derivatives exposure and aggressive lending, South Indian Bank's boring balance sheet suddenly looked attractive. Deposits actually grew as customers sought safety. Management pointed to this as vindication of their careful approach.

But the victory was pyrrhic. Yes, SIB had avoided the worst of the crisis, but they had also missed the best of the preceding boom. Between 2003 and 2008, while India's banking sector assets doubled, South Indian Bank grew at half that pace. More concerningly, they were losing relevance with younger customers. A 2010 internal survey revealed that the average age of an SIB customer was 47, compared to 34 for new private banks.

The mobile banking revolution of the early 2010s caught South Indian Bank completely flat-footed. While State Bank of India launched mobile banking in 2008 and ICICI had over a million mobile banking users by 2012, SIB's first serious mobile app didn't arrive until 2013—and it was barely functional. The app could check balances and recent transactions but couldn't transfer money or pay bills. Customer reviews were scathing.

Asset quality emerged as another challenge. The company delivered a poor sales growth of 3.93% over past five years, reflecting deeper structural issues. While the bank had avoided the aggressive corporate lending that created NPAs for many peers, their conservative approach meant they also missed relationships with quality borrowers who drove India's economic growth. The loan book was increasingly concentrated in traditional sectors with limited growth potential.

By 2015, South Indian Bank faced a stark reality. They were too small to compete with large private banks on scale, too traditional to match fintech startups on innovation, and too regionally concentrated to diversify risks effectively. The stock price, which had peaked at ₹140 in 2007, languished around ₹30. Board meetings grew increasingly tense as independent directors questioned whether the bank had a viable independent future.

The missed opportunities were particularly galling. Kerala's IT sector, centered in Technopark Thiruvananthapuram and Infopark Kochi, had grown dramatically, but SIB had minimal presence in technology sector lending. The state's tourism boom, medical tourism industry, and marine exports sector—all natural fits for a Kerala-based bank—were largely financed by competitors. Even in NRI banking, their historical strength, market share was eroding to specialized players and digital platforms.

V. Digital Transformation Partnership with IFC (2016–2020)

The meeting that would reshape South Indian Bank's destiny took place in a Mumbai hotel conference room in early 2016. Across the table from SIB's senior management sat representatives from the International Finance Corporation (IFC), the World Bank's private sector arm. The IFC team had studied dozens of traditional banks globally that had successfully transformed into digital-first institutions. Their message was blunt: "You have two years to fundamentally reimagine your bank, or you'll become irrelevant."

In 2016, IFC began a project with SIB to transform retail and SME businesses, with a transformation strategy to improve digital capabilities to drive customer engagement and mobilize deposits. This wasn't just about adding a few digital features—it was about fundamentally rewiring how the bank operated, thought, and competed.

The transformation began with a painful assessment. IFC's consultants spent three months shadowing employees, analyzing processes, and documenting customer journeys. Their findings were damning: A simple personal loan application took 7 days on average, involving 13 different handoffs. Account opening required 47 fields of data entry, many redundant. The bank's cost-to-income ratio was 61%, compared to 40% for efficient private banks. Most devastatingly, 70% of transactions still happened in branches, consuming enormous resources for routine activities.

But IFC also identified hidden strengths. South Indian Bank's field staff had incomparable knowledge of local markets. Their gold loan processes, refined over decades, were actually faster than many digital lenders. The bank's conservative culture had created robust risk management frameworks that just needed modern tools. The challenge was preserving these strengths while building new capabilities.

The transformation strategy was ambitious. IFC partnered with SIB to boost new accounts, increase existing customers' account usage, and grow the portfolio by leveraging technology and digital channels to target retail and SME customers. Rather than trying to compete with large banks across all segments, SIB would focus on specific niches where they could win: SME banking, gold loans, and NRI services, all delivered through digital channels.

Then came November 8, 2016. Prime Minister Modi's demonetization announcement invalidated 86% of India's currency overnight. For most traditional banks, it was a crisis. For South Indian Bank, deep in digital transformation, it became an unexpected catalyst. The bank had just launched its upgraded mobile app with UPI integration. As customers desperately sought digital payment options, SIB was ready. Mobile banking registrations increased 400% in two months. The crisis forced even conservative customers to adopt digital channels.

The cultural transformation proved harder than the technical one. Branch managers who had built careers on relationship banking suddenly had to promote digital channels that reduced foot traffic to their branches. The bank launched "Digital Champions"—young employees who coached both staff and customers on digital tools. Town halls featured branch managers sharing stories of how digital tools helped them serve customers better, not replace them.

The transformation strategy helped SIB improve efficiency and support growth by reducing the weight of transactions on branch network. By 2018, routine transactions in branches had dropped to 45%, freeing staff to focus on sales and advisory services. The average time for personal loan approval fell from 7 days to 48 hours. SME loan disbursements, previously taking weeks, could now happen in 72 hours for existing customers.

The SME focus proved particularly shrewd. While large banks chased corporate clients and fintechs targeted retail consumers, India's 63 million SMEs remained underserved. SIB developed specialized digital tools for SME banking: automated GST-based lending, supply chain financing platforms, and digital cash management solutions. They partnered with e-commerce platforms to offer working capital loans based on transaction history.

The numbers validated the strategy. Between 2016 and 2019, SIB's retail loan book grew 45%, faster than the industry average. Fee income from digital channels increased from ₹12 crores to ₹89 crores. Customer acquisition costs fell by 35%. The bank added 1.2 million new customers, with 60% acquiring them entirely through digital channels—unthinkable just three years earlier.

But the transformation wasn't without casualties. Nearly 200 branches were rationalized or converted to digital banking units. Over 1,000 employees took voluntary retirement, unable or unwilling to adapt. The bank's character changed—the paternalistic, relationship-first culture gave way to a more metrics-driven, efficiency-focused approach. Long-time customers complained about reduced personal attention.

The IFC partnership formally ended in 2020, just as COVID-19 struck. The pandemic became the ultimate test of SIB's digital transformation. Lockdowns made physical banking impossible, and the bank that had once required customers to visit branches for everything now had to serve them entirely through digital channels. The infrastructure built over four years—video KYC, digital lending platforms, API banking capabilities—suddenly became not just useful but essential.

Yet challenges remained. Despite dramatic improvement, South Indian Bank's digital capabilities still lagged leaders like HDFC and Kotak Mahindra. The cost-to-income ratio, though improved to 52%, remained high. Most critically, the transformation had been largely defensive—helping SIB catch up rather than leap ahead. The bank needed a new vision for the next phase of growth.

VI. Leadership Transition & New Era Under P.R. Seshadri (2023–Present)

The board meeting in early 2023 had the tension of a Shakespeare tragedy's final act. South Indian Bank's stock had underperformed peers for five consecutive years. Digital transformation, while successful, hadn't translated to market share gains. The board faced a critical decision: continue incremental improvements or bet on transformational leadership. They chose transformation.

P R Seshadri was named MD & CEO beginning October 1, 2023, with approximately 25 years banking expertise from Karur Vysya Bank and Citigroup. His appointment wasn't just a leadership change—it was a statement of intent. Seshadri had built his reputation transforming Karur Vysya Bank's retail franchise, growing its loan book 3x while maintaining superior asset quality. At Citigroup, he had overseen digital innovation initiatives across Asian markets.

Seshadri's first 100 days revealed a different leadership style. Unlike his predecessors who managed from headquarters, he spent weeks visiting branches, sitting with customers, shadowing relationship managers. In a town hall that became legendary within the bank, he declared: "We've been playing not to lose for too long. It's time to play to win."

His track record of scaling, optimising, growing, and transforming enterprises with ability to achieve long-term success emphasising digital operational frameworks immediately showed in his strategic choices. Instead of broad initiatives, he identified three focused bets: geographic expansion beyond Kerala, pivoting from corporate to retail and MSME lending, and building technology partnerships rather than everything in-house.

The geographic expansion strategy was surgical. Rather than opening branches randomly across India, Seshadri identified 30 high-growth districts where SIB had zero presence but strong SME ecosystems. Cities like Coimbatore, Surat, and Indore—manufacturing hubs underserved by large banks—became priority markets. Each new location wasn't just a branch but a digital-first banking hub designed to serve 500 SMEs within 18 months.

Looking to expand beyond Kerala, the bank began shifting focus to MSMEs and retail from current bias towards corporates. This wasn't just about changing lending mix—it required fundamental restructuring. The bank created specialized MSME units with dedicated credit teams trained in sector-specific lending. They hired relationship managers from successful regional banks who understood local business dynamics.

The technology strategy marked perhaps the biggest departure from tradition. Previous leadership had insisted on building capabilities internally, a slow and expensive process. Seshadri embraced partnerships. Within six months, SIB announced collaborations with five fintech companies covering everything from lending analytics to payment solutions. The message was clear: the bank would focus on banking while leveraging best-in-class technology from specialists.

Early results vindicated the approach. In Q4 FY2024, SIB reported its highest quarterly profit in five years. More importantly, the composition was changing—fee income grew 34% year-over-year, the CASA ratio improved to 31.9%, and fresh slippages declined. The stock market noticed, with shares appreciating 40% in Seshadri's first year.

But Seshadri's most significant contribution might be cultural. He introduced "Fail Fast Fridays"—sessions where teams presented failed experiments and lessons learned. The traditional blame culture began giving way to experimentation. Young employees, previously silenced by hierarchy, found their ideas reaching the CEO directly through digital suggestion platforms. The average age of branch managers dropped by 8 years as high performers received accelerated promotions.

The leadership team transformation was equally dramatic. Seven of twelve senior management positions saw new appointments, bringing expertise from HDFC Bank, Axis Bank, and fintech companies. The chief digital officer role, created for the first time, went to a former Paytm executive. The head of retail banking came from Bandhan Bank, bringing microfinance expertise. This injection of external talent created friction but also energy.

The bank is set to lead into an era of growth and innovation while respecting rich legacy and core principles. Seshadri's vision balanced ambition with pragmatism. The five-year plan targeted doubling the balance sheet while maintaining asset quality, expanding to 100 new cities while deepening Kerala presence, and achieving top-quartile digital metrics while preserving human touch in banking.

Yet challenges remained formidable. The banking sector's competitive intensity had only increased. Payment banks and small finance banks targeted SIB's traditional customer base. Large private banks used superior technology and capital to win market share. New-age fintechs unbundled banking services, cherry-picking profitable segments. Every strategic move required perfect execution in this unforgiving environment.

VII. Digital Banking & Fintech Strategy

The partnership announcement with FPL Technologies in March 2024 marked a watershed moment. SIB tied up with FPL Technologies for credit card relationships with entire fulfilment through mobile phones—no physical documentation, no branch visits, just a purely digital experience from application to activation. For a bank that once required customers to visit branches for everything, this represented a philosophical revolution.

The bank has been focusing on digital initiatives, looking at partnering with fintech aggregators to scale up, and has been investing in technology over the last few years. But unlike the scattershot approach of the past, the new strategy showed remarkable coherence. Each partnership addressed specific gaps: lending analytics with one partner, payment solutions with another, wealth management with a third. The bank became an orchestrator rather than trying to be everything.

The credit modeling transformation was particularly sophisticated. Using credit models and data science for underwriting, SIB developed different models for home loans, LAPs and personal loans. These weren't generic scoring systems but purpose-built algorithms that incorporated unique data points. The home loan model analyzed not just income and credit history but also employer stability, property micro-market trends, and even social media behavior patterns. The LAP (Loan Against Property) model used satellite imagery to verify property details and automated valuation models for instant pricing.

The results were dramatic. Loan approval times dropped from days to hours for standard cases. More importantly, the models identified good customers that traditional underwriting would reject—self-employed professionals with irregular income, small business owners with limited credit history, young professionals in emerging sectors. The bank's approval rates increased while NPAs actually declined, defying conventional banking wisdom.

The Digital Banking Units (DBUs) launched under government initiatives became SIB's laboratories for innovation. Unlike traditional branches designed for transactions, DBUs resembled tech startup offices—open spaces, digital walls displaying real-time analytics, video conferencing pods for remote advisory. Customers could experience virtual reality property tours for home loans, AI-powered financial planning, and blockchain-based trade finance—capabilities that seemed like science fiction just years earlier.

But the real innovation was in the partnership philosophy. Rather than viewing fintechs as competition, SIB positioned itself as the regulated backbone for innovative services. Fintech partners brought user experience and technology; SIB provided banking license, regulatory compliance, and capital. The bank's API platform, launched in 2024, allowed third-party developers to build services on SIB's infrastructure—turning the bank into a platform rather than just a service provider.

The payment space strategy was particularly nuanced. Rather than competing with PhonePe or Google Pay on UPI volumes (a losing battle), SIB focused on specialized payment solutions. They developed industry-specific payment platforms for Kerala's marine exports sector, specialized collection solutions for educational institutions, and integrated payment systems for hospital chains. Each solution addressed specific pain points that generic payment apps ignored.

The wealth management digital transformation surprised industry observers. Traditionally the preserve of relationship managers serving high-net-worth individuals, SIB democratized wealth services through robo-advisory platforms. A customer with ₹50,000 could access portfolio management previously available only to millionaires. The platform analyzed spending patterns, risk tolerance, and life goals to suggest personalized investment strategies, all delivered through intuitive mobile interfaces.

Yet the digital push created new challenges. Cybersecurity became paramount as digital transactions exploded. The bank invested heavily in AI-powered fraud detection, behavioral biometrics, and blockchain-based security systems. Every digital initiative required corresponding risk management enhancement. The technology budget, traditionally 3% of revenues, ballooned to 8%—comparable to pure-play digital banks.

Customer adoption remained uneven. While urban millennials embraced digital services enthusiastically, traditional customers—particularly senior citizens and rural segments—struggled with the transition. The bank launched "Digital Sakhi" programs where young customers taught elderly users, creating community-driven adoption. Branch staff were retrained as "digital ambassadors" rather than transaction processors.

The competitive response was swift. Large banks accelerated their own digital initiatives, while fintechs tried to poach SIB's technology talent. The bank had to triple technology salaries to retain key personnel, creating internal equity issues. The culture clash between traditional bankers and digital natives required constant management attention.

The partnership model also brought dependencies. When a key fintech partner faced regulatory issues, SIB's credit card launches were delayed by months. Integration challenges between multiple platforms created customer experience issues. The bank learned that while partnerships accelerated capability building, they also introduced new forms of risk that required careful management.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation still in progress. With a Market Cap of 7,771 Crore, Revenue of 9,461 Cr, and Profit of 1,331 Cr, South Indian Bank occupies a unique position—too large to be ignored, too small to dominate. But the granular metrics reveal more nuanced dynamics that explain both the bank's challenges and opportunities.

The key ratios paint a picture of stability with room for improvement: Capital Adequacy Ratio at 16.04%, Net Interest Margin at 3.28%, Gross NPA at 4.74%, Net NPA at 1.61%, and CASA Ratio at 31.9%. Each number tells its own story. The CAR of 16.04% provides a comfortable buffer above regulatory requirements, giving the bank firepower for growth without immediate capital raising needs. This strength becomes particularly relevant as the bank pursues aggressive expansion.

The Net Interest Margin of 3.28% sits in the sweet spot—high enough to generate profits but not so high as to suggest predatory pricing. Compare this to HDFC Bank's 3.4% or Kotak's 3.6%, and SIB's pricing seems competitive. But dig deeper, and you find the margin comes largely from high-yielding gold loans and SME lending rather than diversified portfolio strength.

Asset quality metrics reveal both progress and persistent challenges. The Gross NPA at 4.74% has improved from peaks above 6% but remains elevated compared to best-in-class peers like HDFC (1.3%) or Kotak (1.8%). The Net NPA at 1.61%, while manageable, suggests the bank maintains adequate provisions but hasn't fully resolved legacy stressed assets. This overhang from past corporate lending mistakes continues to constrain fresh credit growth.

The CASA Ratio at 31.9% represents a critical weakness. In an era where leading private banks maintain CASA above 45%, SIB's reliance on expensive term deposits pressures margins. Every 1% improvement in CASA could add 10 basis points to margins—meaningful in a competitive market. The bank's digital initiatives specifically target this metric, aiming to attract salary accounts and operating accounts that provide cheap, sticky funds.

Historical performance metrics are sobering: poor sales growth of 3.93% over the past five years and low return on equity of 13.4% over the last 3 years. These numbers explain why the stock has underperformed despite operational improvements. Investors see a bank that survived but didn't thrive during India's banking boom. The question is whether new leadership can change this trajectory.

Stock market performance tells its own story. Trading at a price-to-book ratio around 0.8x, the market values SIB below its accounting value—a clear vote of no confidence in current earnings power. Compare this to HDFC Bank at 3x book or Kotak at 4x, and the valuation gap becomes a chasm. But this also represents opportunity: even reaching 1.5x book value would double the stock price. Recent quarterly results provide glimpses of the transformation taking effect. South Indian Bank posted a net profit of Rs 322 crore for the quarter ending June 2025, reflecting a 10% increase compared to Rs 294 crore in the same period last year, despite a 4% fall in net interest income (NII), which decreased to Rs 832 crore from Rs 865 crore year-on-year. This ability to grow profits despite NII pressure demonstrates improving operational efficiency.

More encouragingly, gross non-performing assets (GNPAs) slightly reduced to 3.15% from 3.20% in the previous quarter, while net NPAs significantly decreased to 0.68% from 0.92%. This dramatic improvement in asset quality—net NPAs below 1%—removes a major overhang that had concerned investors for years.

The comparative analysis with peer banks reveals both gaps and opportunities. Against Kerala peers like Federal Bank (market cap ₹28,000 crore) and CSB Bank (₹3,800 crore), SIB holds middle ground. But against new-age banks like Bandhan (₹25,000 crore) or AU Small Finance Bank (₹24,000 crore), which started operations decades after SIB, the underperformance becomes stark. These banks achieved in 10 years what SIB couldn't in 95.

Yet the valuation gap also represents opportunity. If SIB can demonstrate consistent execution under new leadership, maintain asset quality improvements, and show market share gains in targeted segments, re-rating potential exists. A bank with improving metrics trading below book value in a growing economy presents asymmetric risk-reward for patient investors.

IX. Playbook: Lessons from a 95-Year Survivor

The South Indian Bank story offers a masterclass in institutional survival—and a cautionary tale about the cost of that survival. Every major Indian bank that started in the early 20th century faced similar existential moments. Most didn't make it. Understanding why SIB survived while others perished reveals timeless lessons about banking, business strategy, and organizational resilience.

Surviving vs. Thriving: The Conservation Paradox

SIB's conservative DNA, forged during the Great Depression and reinforced through multiple crises, became both its greatest strength and ultimate weakness. The bank's founders established a simple principle: never lend what you can't afford to lose. This meant missing the great credit booms but also avoiding the subsequent busts. While ICICI Bank wrote off thousands of crores in bad corporate loans post-2015, SIB's boring portfolio remained relatively clean.

But conservatism extracted a price. The bank's loan-to-deposit ratio rarely exceeded 75%, meaning 25% of deposits earned low treasury returns rather than higher lending yields. Risk-adjusted returns matter, but excessive risk aversion destroys value too. The lesson: conservation ensures survival but prevents dominance. In rapidly growing markets, playing not to lose means you've already lost.

Regional Dominance Strategy: Deep vs. Wide

SIB's Kerala fortress strategy worked brilliantly—until it didn't. By focusing intensely on one state, the bank built unmatched local knowledge. A branch manager in Thrissur knew three generations of every business family, understood local politics, and could assess credit risk through community intelligence that no algorithm could replicate. This deep, narrow focus created a moat that even HDFC Bank struggled to cross.

Yet geographic concentration became a trap. Kerala's economy, despite its strengths, grew slower than India's average. The state's politics often hostile to private capital, its industries largely traditional, and its best talent emigrated. SIB found itself perfectly positioned in a shrinking pond. The lesson: regional dominance provides stability but caps growth. Winners eventually must choose between being big fish in small ponds or competing in oceans.

Digital Transformation for Legacy Banks: The Innovator's Dilemma Incarnate

SIB's digital journey exemplifies Clayton Christensen's innovator's dilemma in banking. The bank's existing customers—older, relationship-oriented, branch-dependent—didn't initially want digital services. Investing in digital capabilities meant cannibalizing profitable branch-based business for uncertain digital returns. New private banks, unburdened by legacy, built digital-first operations from scratch.

The IFC partnership provided the solution: external catalyst forcing internal change. By framing digital transformation as survival rather than growth, IFC helped SIB overcome organizational inertia. The lesson: legacy organizations rarely self-disrupt successfully. External pressure—whether from consultants, investors, or crisis—often provides necessary momentum for fundamental change.

Managing Regulatory Changes Across Decades

SIB navigated Indian banking's regulatory maze with remarkable dexterity. From colonial-era banking regulations through socialist nationalization threats, liberalization, and modern prudential norms, the bank adapted continuously. They maintained higher capital ratios than required, implemented Basel norms ahead of schedule, and avoided regulatory censure that plagued aggressive peers.

This regulatory conservatism paid dividends during crisis. When RBI tightened norms post-2015, banks with aggressive practices faced restrictions. SIB's clean record allowed uninterrupted growth. The lesson: in highly regulated industries, compliance isn't a cost center but a competitive advantage. Regulatory capital—the trust and credibility with regulators—matters as much as financial capital.

Cultural Transformation in Traditional Organizations

Changing SIB's culture from relationship-banking to digital-first required deliberate, painful choices. The bank couldn't fire thousands of traditional bankers and hire digital natives—both practically and culturally impossible. Instead, they created parallel structures: digital teams operated like internal startups while traditional banking continued. Gradually, success stories from digital initiatives converted skeptics.

The "Digital Champions" program proved particularly effective. Rather than top-down mandates, peer influence drove adoption. When a 60-year-old branch manager in rural Kerala successfully used digital tools to serve customers better, it carried more weight than CEO speeches. The lesson: cultural transformation requires patience, multiple approaches, and visible wins that convert skeptics into evangelists.

Partnership Strategies with Fintechs and Global Organizations

SIB's evolution from viewing fintechs as threats to embracing them as partners reflects broader banking industry dynamics. Initially, the bank tried competing with fintechs directly—a losing proposition given resource constraints. The pivot to partnership leveraged SIB's banking license and regulatory expertise while accessing fintech innovation and agility.

The IFC partnership provided a different model: capability building through knowledge transfer. Rather than just capital or technology, IFC brought global best practices, methodologies, and networks. This combination of local knowledge and global expertise created capabilities neither party could achieve alone. The lesson: in technology-disrupted industries, strategic partnerships often trump build-or-buy decisions. The key lies in choosing partners whose capabilities complement rather than replicate yours.

X. Bear vs. Bull Case & Future Outlook

The Bear Case: Structural Headwinds and Competitive Realities

The pessimistic view on South Indian Bank starts with an uncomfortable truth: in banking, scale increasingly determines success. With assets of ₹1.17 lakh crore, SIB is one-fifteenth the size of HDFC Bank. This isn't just about bragging rights—scale drives everything from technology investments to talent acquisition to cost of funds. Every year SIB remains subscale, the gap widens.

Regional concentration in Kerala presents existential risk. The state's economy, while resilient, faces structural challenges: an aging population, limited industrial growth, and political environments often hostile to private capital. Kerala's educated youth continue emigrating, depleting SIB's natural customer pipeline. The Gulf remittance boom that fueled growth for decades is moderating as oil economies diversify away from foreign labor. Betting heavily on Kerala means betting against demographic and economic trends.

Competition from digital-first banks represents perhaps the gravest threat. A customer can open a Jupiter account, get a Federal Bank-backed card, and access sophisticated financial services without ever hearing "South Indian Bank." These neo-banks target exactly the young, urban customers SIB desperately needs. They offer superior user experience, innovative products, and venture capital-funded customer acquisition that SIB cannot match.

The technology debt accumulated over decades can't be wished away. While SIB has made progress, their core banking system remains a patchwork of solutions. True digital transformation would require investments that could consume multiple years of profits. Meanwhile, competitors leverage cloud-native architectures that cost fraction of legacy infrastructure. This technology gap compounds daily—by the time SIB implements today's innovations, competitors have moved to next-generation capabilities.

Legacy cost structures present another challenge. With over 950 branches and 9,000 employees, SIB carries fixed costs that digital banks avoid entirely. The average cost-to-income ratio of 52% compares poorly to digital banks operating below 35%. Every percentage point of inefficiency translates to lower returns, reduced investment capacity, and inability to price competitively.

The talent challenge grows acute. India's best technology and banking talent gravitates toward either high-paying multinationals or exciting startups. SIB offers neither global brand appeal nor startup equity upside. The bank's recent digital hires came at premium costs, creating internal equity issues. This talent disadvantage becomes self-reinforcing—without top talent, innovation lags; without innovation, attracting talent becomes harder.

The Bull Case: Hidden Assets and Transformation Potential

The optimistic view begins with valuation. Trading below book value, SIB offers rare opportunity to buy a functioning bank with 95-year history at liquidation prices. Even modest operational improvements could drive significant rerating. If the bank achieves ROE of 15% (below industry leaders but achievable), current valuations imply 100% upside.

The bank is indeed set to lead into an era of growth and innovation while respecting rich legacy and core principles. Under Seshadri's leadership, early indicators suggest transformation gaining momentum. Asset quality improvements, digital adoption metrics, and geographic expansion all trend positively. Leadership matters enormously in banking, and Seshadri brings proven transformation track record.

The untapped potential in national expansion presents massive opportunity. India needs multiple strong banks to serve its $5 trillion economy ambitions. SIB's conservative underwriting, strong capital position, and improving digital capabilities position it well for disciplined expansion. Success in just 10 new cities could double the bank's addressable market.

Digital transformation, while incomplete, has reached inflection point. The partnerships with fintechs provide capabilities that would take years to build internally. The bank's API platform could become significant revenue generator as embedded finance explodes. Having survived the painful part of transformation, SIB could reap benefits as digital adoption accelerates.

Strong capital adequacy at 16.04% provides runway for growth without dilution. Many peers require regular capital raising that dilutes returns. SIB can fund organic growth from internal accruals, allowing existing shareholders to capture full value from transformation. This capital strength also enables opportunistic acquisitions if right targets emerge.

The MSME lending focus aligns perfectly with India's economic priorities. Government schemes supporting MSME credit, combined with SIB's renewed focus on this segment, could drive sustainable growth. The bank's local knowledge and relationship banking heritage provide advantages in MSME lending that pure digital players cannot replicate.

Improving asset quality removes major overhang. With net NPAs below 1%, the bank has cleaned up legacy problems. This allows management to focus on growth rather than firefighting. Credit costs should remain low, supporting profitability even if competitive pressures compress margins.

The franchise value, while difficult to quantify, remains substantial. A 95-year-old bank doesn't survive without deep customer relationships, brand trust, and operational resilience. These intangible assets, properly leveraged through modern capabilities, could drive outperformance.

XI. Analysis & "If We Were CEOs"

Standing at the helm of South Indian Bank today would feel like captaining a sturdy ship that needs new engines while sailing through storms. The vessel is seaworthy—proven by 95 years of navigation—but competing against speedboats with jet engines. The strategic choices made in the next 24 months will determine whether SIB thrives independently, becomes an acquisition target, or slowly fades into irrelevance.

Strategic Priority #1: The Geographic Expansion Dilemma

The first CEO decision would be choosing between two expansion models. Option A: Identify 5 mega-cities (Mumbai, Delhi, Bangalore, Hyderabad, Chennai) and build substantial presence through 20-30 branches each, competing directly with large banks. Option B: Target 50 tier-2 cities where SIB could achieve local dominance, avoiding direct competition with giants.

The answer: Option B, but with a twist. Rather than physical branches, establish digital-first banking hubs in these cities. Each hub would have 3-5 relationship managers operating from co-working spaces, using technology for all transactions while providing human touch for complex needs. This model, costing one-tenth of traditional branches, allows rapid scaling while maintaining capital efficiency.

Strategic Priority #2: The M&A Question

With several small finance banks and struggling regional banks available, acquisition opportunities exist. The temptation would be acquiring a north or west India-focused bank to instantly achieve geographic diversification. But integration challenges, cultural mismatches, and regulatory approvals make this treacherous.

Instead, pursue "acqui-hiring"—acquiring entire teams from struggling institutions. When a competing bank downsizes, hire entire branches' staff with established customer relationships. This provides immediate market entry without integration nightmares. Target specific capabilities through team acquisition: a credit card team from a struggling fintech, a wealth management team from a downsizing foreign bank.

Strategic Priority #3: Technology Investment Architecture

The technology strategy would focus on becoming a "platform bank." Rather than building everything internally, create the best API platform in Indian banking. Allow fintechs, corporates, and developers to build services on SIB's infrastructure. Revenue would come from API calls, transaction fees, and revenue sharing rather than traditional interest margins.

Invest heavily in three areas: data analytics for credit decisioning, cybersecurity to protect the platform, and user experience design to ensure seamless integration. Everything else—payments, lending algorithms, wealth management tools—comes through partnerships. This approach turns technology from cost center to revenue generator.

Strategic Priority #4: Balancing Heritage with Innovation

The tension between 95-year heritage and digital innovation requires delicate handling. Create "SIB Heritage"—a premium service line celebrating the bank's history while delivering modern services. Long-standing customers get dedicated relationship managers, preferential pricing, and exclusive branch access. This preserves loyalty while freeing the main brand for aggressive digital positioning.

Launch "SIB Neo" as a digital-only subsidiary targeting millennials and Gen-Z. Operating under separate brand with startup culture, it competes directly with neobanks while leveraging parent bank's license and capital. This dual-brand strategy allows serving traditional customers while attacking new segments.

Strategic Priority #5: Building National Brand from Regional Base

Kerala remains SIB's fortress, providing stable profits and deep relationships. Rather than abandoning this strength, leverage it for national expansion. Position SIB as "Kerala's Gift to India"—emphasizing the state's reputation for education, healthcare, and quality services. Kerala nurses are trusted nationwide; why not Kerala bankers?

Create products that leverage Kerala's strengths: education loans for students nationwide attending Kerala's educational institutions, medical loans for health tourism to Kerala hospitals, trade finance for spices and marine exports. This builds national presence while maintaining regional advantage.

The Capital Allocation Framework

With limited resources, every rupee must generate maximum return. Allocate capital using a simple framework: 40% to digital transformation and technology, 30% to geographic expansion in targeted cities, 20% to strengthening Kerala franchise, and 10% reserve for opportunistic moves.

Measure every initiative against three criteria: does it improve cost-to-income ratio, does it attract customers under age 40, and does it differentiate from both large banks and fintechs? Initiatives failing these tests get killed quickly, freeing resources for winners.

The Cultural Revolution

Transform organizational culture through radical transparency. Publish internal metrics weekly—every employee sees branch-wise performance, digital adoption rates, customer satisfaction scores. Create internal prediction markets where employees bet on which initiatives will succeed. This gamification drives engagement while surfacing ground-truth about initiative viability.

Implement "reverse mentoring" where junior employees teach senior management about digital trends, social media, and changing customer preferences. Every executive committee member must spend one day monthly as customer service representative, experiencing front-line realities. This breaks hierarchical barriers while ensuring leadership stays connected to operational reality.

The next five years will determine whether South Indian Bank's second century surpasses its first. The pieces for transformation exist: adequate capital, improving asset quality, proven leadership, and burning platform creating urgency. Success requires executing multiple strategies simultaneously while maintaining operational stability—a high-wire act that few banks manage successfully.

XII. Recent News

The recent business updates paint a picture of steady momentum building under new leadership. South Indian Bank has reported an 11.94% year-on-year (YoY) increase in its gross advances for the quarter ended December 31, 2024. The figure stood at ₹86,965 crore, up from ₹77,686 crore in the corresponding period last year. This double-digit loan growth suggests the geographic expansion and MSME focus strategies are gaining traction.

Total deposits for the private lender grew by 6.28% YoY, reaching ₹1,05,378 crore compared to ₹99,155 crore a year earlier. This indicates a healthy increase in the bank's deposit base, aligning with its overall growth trajectory. While deposit growth lags loan growth, creating some asset-liability pressure, the quality of deposits appears to be improving.

The bank's Current Account and Savings Account (CASA) deposits rose by 4.13% YoY to ₹32,831 crore, up from ₹31,529 crore in Q3FY24. Though CASA growth remains modest, any improvement in this low-cost funding source directly impacts profitability.

The capital raising initiatives demonstrate proactive balance sheet management. South Indian Bank initiates ₹1,151.01 crore rights issue, opening today on March 6, 2024. The rights issue, priced at ₹22 per share, closes on March 20, 2024. This successful capital raise, completed before the current growth phase, provides ammunition for expansion without diluting returns.

Strategic partnerships continue expanding the bank's reach. Tata Motors on Monday said it has tied up with South Indian Bank to offer financing solutions to its commercial vehicle customers and dealerships. As part of the Memorandum of Understanding (MoU), South Indian Bank will offer financing solutions across the auto major's entire commercial vehicle portfolio. Such partnerships provide access to quality assets while leveraging partners' distribution networks.

The regulatory compliance focus yields dividends. South Indian Bank's FY 2024-25 Business Responsibility and Sustainability Report filed as per SEBI regulations demonstrates the bank's commitment to ESG principles, increasingly important for institutional investors and regulatory approvals.

Market sentiment shows cautious optimism. The stock's performance—gaining over 20% in the past year despite broader banking sector challenges—suggests investors recognize transformation potential while remaining wary of execution risks. Analyst recommendations lean toward "Buy" for long-term investors, though near-term volatility remains likely as transformation initiatives mature.

XIII. Links & Resources

Primary Sources: - South Indian Bank Annual Reports (2019-2024): southindianbank.com/investor-relations - RBI Statistical Database: dbie.rbi.org.in - BSE/NSE Filings: bseindia.com, nseindia.com - SEBI Corporate Filings: sebi.gov.in

Industry Reports: - IFC Digital Banking Transformation Studies: ifc.org/digital-finance - BCG Indian Banking Report 2024: bcg.com/industries/financial-institutions - McKinsey Global Banking Annual Review: mckinsey.com/industries/financial-services

Historical Banking Context: - "Banking in India: A Historical Perspective" - Reserve Bank of India Archives - "The Evolution of Private Sector Banking in Kerala" - Centre for Development Studies - "Indian Banking Sector: Challenges and Opportunities" - FICCI Reports

Digital Transformation Resources: - "Digital Banking in India: Challenges and Opportunities" - PwC India - "The Future of Banking: Digital Transformation Playbook" - Deloitte - "API Banking and Open Banking in India" - NPCI Documentation

Regulatory Framework: - RBI Master Circulars on Banking Operations - Basel III Implementation in India - RBI Guidelines - Priority Sector Lending Norms and Updates

Academic Research: - "Regional Banks and Economic Development" - Economic and Political Weekly - "Digital Transformation of Traditional Banks" - IIM Bangalore Research Papers - "NRI Banking and Kerala Economy" - Centre for Development Studies Working Papers

Investment Research: - Institutional Brokers' Reports (ICICI Securities, Motilal Oswal, Axis Capital) - Rating Agencies Reports (ICRA, CRISIL, CARE) - Proxy Advisory Firms Analysis (IiAS, SES)

This analysis represents an independent examination of South Indian Bank's business trajectory based on publicly available information. While extensive research has informed these insights, banking sector dynamics remain complex and rapidly evolving. The transformation story of South Indian Bank continues to unfold, offering valuable lessons about institutional resilience, strategic pivots, and the delicate balance between heritage and innovation in Indian banking.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube