Sheela Foam: India's Sleep Revolution

I. Cold Open & Episode Roadmap

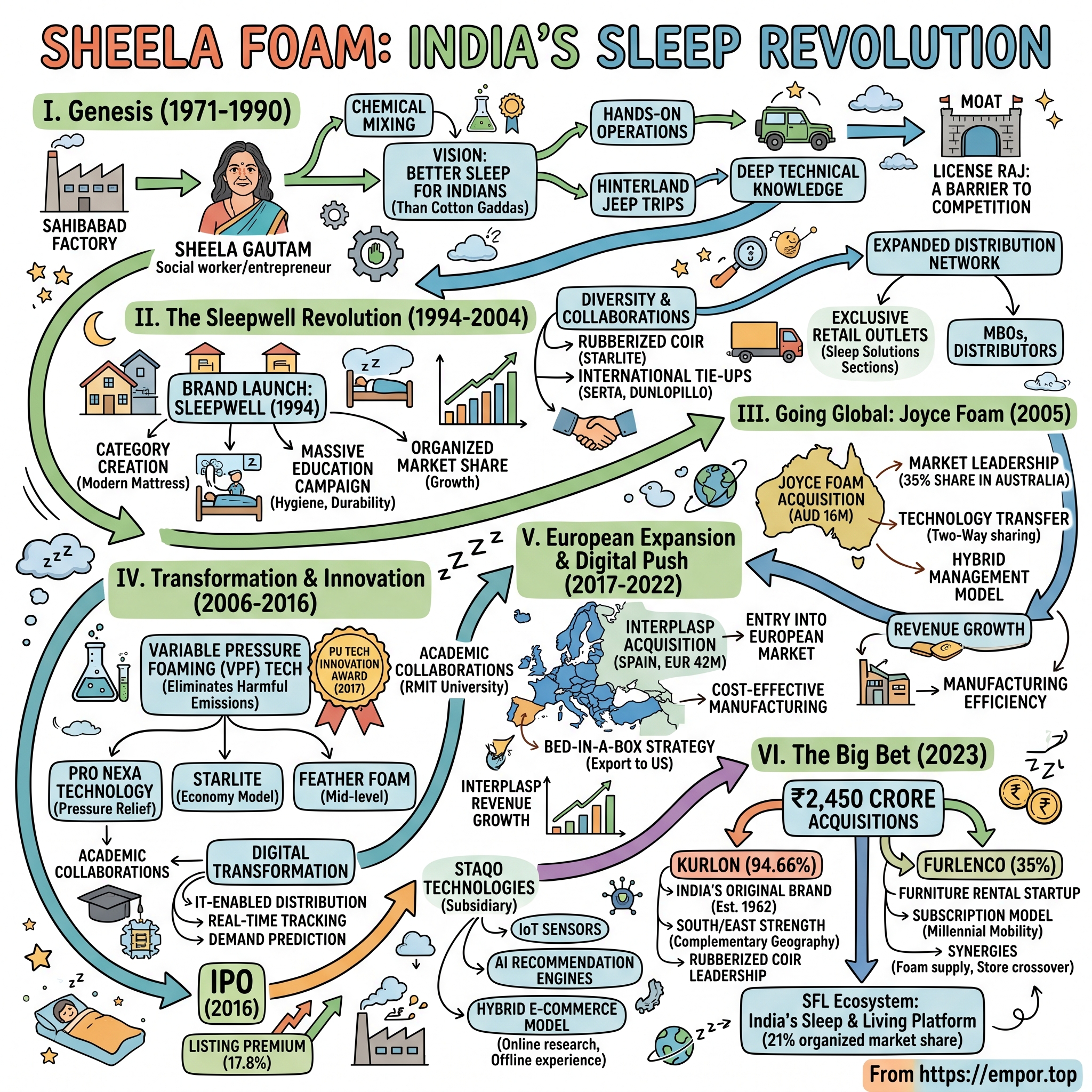

Picture this: It's 1971 in Sahibabad, a dusty industrial town on the outskirts of Delhi. While India grapples with the aftermath of the Bangladesh Liberation War and Indira Gandhi consolidates power, a social worker turned entrepreneur named Sheela Gautam is mixing chemicals in a small factory, convinced that Indians deserve to sleep better than on cotton mattresses that turn lumpy in monsoons and harbor dust mites year-round.

Fast forward five decades. That single foam plant has grown into a company with a 30% market share in India's mattress segment and a 40% market share in Australia. Sheela Foam operates across India, Australia, and Europe, with 22 manufacturing facilities in these regions. The company that started with industrial foam now commands a combined market share of around 21% in the modern mattress market in India after its recent acquisitions.

But here's the question that should intrigue any serious investor: How did a foam manufacturer started by a parliamentarian's daughter become the undisputed leader of India's organized mattress market? And perhaps more importantly, in an era where D2C brands are disrupting every consumer category, how has this 53-year-old company not just survived but thrived through strategic acquisitions worth over ₹2,400 crores in 2023 alone?

This is a story about three big themes. First, the power of category creation—how Sheela Foam didn't just make foam, they created India's modern sleep industry. Second, the art of patient geographic expansion—from Sahibabad to Sydney to Spain, each move calculated over decades. And third, the playbook for consolidating a fragmented market through vertical integration and strategic M&A.

What makes this particularly fascinating in the Indian consumer goods landscape is the timing. While everyone talks about India's consumption story, Sheela Foam has been quietly building the infrastructure for it since the License Raj era. They've navigated everything from the 1991 liberalization to the 2016 demonetization, from the rise of e-commerce to the COVID-19 pandemic. Each crisis became a catalyst for transformation.

II. Genesis: The Sheela Gautam Story & Early Years (1971–1990)

The rain was particularly heavy that monsoon of 1971 when Sheela Gautam established the company in Sahibabad, Uttar Pradesh, focusing initially on polyurethane foam production. But this wasn't your typical industrial startup story. Mrs. Sheela Gautam was a social worker and parliamentarian who envisioned an India that sleeps in comfort.

Think about the audacity of that vision in 1971 India. The country was still reeling from wars, facing foreign exchange crises, and most Indians slept on cotton mattresses that had to be beaten and sunned every few weeks. The organized mattress market didn't exist. Foam was something you might find in a car seat, not a bedroom.

She was 16 at the time of India's independence, and grew up watching and absorbing the lessons of integrity and service from her father, the respected freedom fighter Mohan Lal Gautam, known as the 'Patriot of Aligarh'. As a member of the Constituent Assembly which decided the constitution of India, he is among those who laid the foundation of the republic.

This background matters because it shaped how Sheela Gautam approached business. She rode the hinterland in her Jeep and took care of all operations in a hands-on way, setting the foundation for what it is today. The public service ethos inherited from her father was most visible in her yearning to serve the people. This wasn't just about making money—it was about democratizing comfort.

Sheela Foam was founded in 1971 by Rahul Gautam and his mother, Ms. Sheela Gautam, a 4-term Member of Parliament. Rahul, fresh from IIT Kanpur with a chemical engineering degree and later armed with a Master's from NYU, brought technical expertise to complement his mother's vision and social capital.

The early years were brutal. The License Raj meant you needed government permission for everything—expanding capacity, importing machinery, even changing your product mix. While Reliance was navigating textile quotas and Tata was dealing with steel allocations, Sheela Foam was trying to convince industrial buyers that polyurethane foam was superior to traditional materials.

The company started with basic industrial applications—foam for packaging, insulation, and automotive sectors. This was intentional. Industrial customers provided steady cash flow and didn't require brand building. But even here, Sheela Gautam's approach was different. She rode the hinterland in her Jeep and took care of all operations. Her high standards of integrity and governance served well. It led to a position of respect for the company and its leaders. This only goes to show how a solid foundation in ethics and public service can lead to growth and stability in business.

By the mid-1980s, a pattern emerged that would define Sheela Foam's strategy for decades: build trust in B2B markets first, understand the material science deeply, then move to consumer products. They weren't just foam suppliers; they were becoming foam experts. Every industrial application taught them something new about density, resilience, or durability that would later apply to mattresses.

The pre-liberalization era of the 1980s was particularly challenging. Import restrictions meant they couldn't easily access the latest foam technology from Europe or America. So they innovated with what they had. They experimented with different chemical formulations, modified second-hand equipment, and essentially reverse-engineered modern foam manufacturing in an environment where getting a phone connection took years.

But here's what's remarkable: while other companies saw the License Raj as a constraint, Sheela Foam saw it as a moat. The same regulations that made it hard for them to grow also made it nearly impossible for foreign competitors to enter. They had a decade to build relationships, understand Indian conditions (humidity, heat, dust), and create formulations specifically for the Indian market.

By 1990, as India stood on the brink of liberalization, Sheela Foam had quietly built three critical assets: deep technical knowledge of polyurethane chemistry, a network of industrial customers who trusted their quality, and most importantly, a second generation of leadership in Rahul Gautam who understood both the science and the business. They were ready for something bigger.

III. The Sleepwell Revolution: Creating a Brand (1994–2004)

The year was 1994. The Sensex had just crossed 4,000 for the first time. Cable television was bringing aspirational lifestyles into Indian homes. And in this environment of newfound optimism, Sheela Foam launched its flagship brand, Sleepwell, which became a major mattress brand in India.

But why 1994? The timing reveals strategic brilliance. Post-liberalization India was seeing the emergence of a middle class with disposable income. More importantly, urbanization was accelerating. People were moving from joint families in ancestral homes to nuclear families in apartments. And apartments meant furniture you bought, not inherited.

The gamble was enormous. Moving from B2B foam supplier to B2C branded mattresses meant competing with thousands of local manufacturers, investing in brand building, and creating distribution from scratch. Launched in 1994, Sleepwell is the leading brand of mattress and home comfort products that has held its ground amidst growing competition from online and offline brands and carries immense trust among consumers, retailers, and traders alike. It has a nationwide presence with a robust distribution network of exclusive retail outlets, multi-brand outlets and distributors.

Here's what most people miss about this transition: Sheela Foam didn't just launch a mattress brand. They created a category. In 1994, most Indians didn't know they needed a foam mattress. Cotton gadda was tradition. Your grandmother made them. They were part of dowries. Foam mattresses were seen as Western, expensive, unnecessary.

Established in 1994, Sleepwell has become one of India's most popular mattress brands. But popularity didn't come overnight. The education campaign was massive. They had to explain why foam was more hygienic (doesn't harbor dust mites), more durable (doesn't develop lumps), and more comfortable (provides uniform support). They positioned it not as replacing tradition but as evolution—the modern Indian family deserved modern comfort.

Between 1998 and 1999, the company introduced rubberized coir products Starlite and collaborated with Serta (USA), and Dunlopillo (UK), for mattress production. This was strategic product laddering. Starlite, with rubberized coir, was positioned as the entry point—more affordable than pure foam but superior to cotton. It was the gateway drug to the foam revolution.

The Serta and Dunlopillo collaborations were about technology transfer and credibility. These were global brands that brought manufacturing expertise and gave Sleepwell the halo of international quality. But unlike many Indian companies that became dependent on foreign partners, Sheela Foam maintained control and gradually absorbed the technology.

From 2001 to 2003, Sheela Foam established a polyurethane foam-producing plant in Greater Noida and expanded operations to Rajpura, Punjab, and Sikkim. This Greater Noida plant was particularly significant—it was designed to be India's largest PU foam facility. The scale economics were crucial. Larger production runs meant better cost per unit, which meant they could price competitively while maintaining margins.

The distribution challenge was perhaps the most complex. India's retail landscape in the late 1990s was fragmented beyond imagination. There were no big-box retailers. Each city had hundreds of small furniture shops, each with their own relationships and credit terms. They have pan India distribution network that consists of over 100 exclusive distributors, over 2,000 exclusive retail dealers and over 2,500 multi-brand outlets, as on March 31, 2016.

The genius was in the execution. Instead of trying to replace existing furniture retailers, Sheela Foam partnered with them. They provided training, marketing support, and crucially, credit terms that worked for small retailers. They created a category within furniture stores—the "sleep solutions" section.

Marketing strategy evolved from functional to emotional. Early ads focused on product features—density, warranty, technology. But by the early 2000s, Sleepwell advertising was about families, comfort, and care. The tagline wasn't about foam; it was about sleep. They weren't selling mattresses; they were selling better mornings.

We brought the concept of exclusive retail to the home comfort products sector in India with Sleepwell retail centres. Today, our store network has over 5500 exclusive outlets and a total of 20,000+ touchpoints across India. These exclusive outlets were game-changers. They allowed Sheela Foam to control the customer experience, showcase the full range, and most importantly, educate consumers hands-on about sleep health.

By 2004, a remarkable transformation had occurred. The company that had started as an industrial foam supplier was now synonymous with modern sleep in India. Sleepwell wasn't just a brand; it had become a category definition. When Indians thought foam mattress, they thought Sleepwell. The revolution was complete. But Rahul Gautam knew that to sustain leadership, they needed to look beyond India's borders.

IV. Going Global: The Joyce Foam Acquisition (2005)

The boardroom in Ghaziabad was tense in early 2005. The Indian mattress market was growing, but Rahul Gautam was proposing something radical: In 2005, Sheela Foam made its first global acquisition by purchasing Joyce Foam, an Australian polyurethane foam manufacturer. The price tag: AUD 16 million, excluding property and debt. For a company that had never made an international acquisition, this was betting the farm.

Joyce Foam was sold to India-based flexible PU foam manufacturer Sheela Foam Private Ltd. in 2005 for A$16 million (excluding property and debt). But this wasn't just about buying revenue. The company expanded its operations by acquiring the manufacturing businesses of PU Foam and polystyrene products from three Australian companies: Joyce Corporation Limited, Joyce Indpac Limited, and Marfoam Pty Limited in 2005.

Why Australia? The strategic rationale was multi-layered. First, Joyce, which supplies flexible PU foam to the bedding, furniture and automotive industries, became a wholly-owned Australian subsidiary of Indian flexible PU foam manufacturer, the Sheela Group, in 2005. Joyce then accounted for 35 percent of the Australian flexible PU market. This wasn't a fixer-upper; this was acquiring market leadership.

Second, technology. Sheela initially bought Joyce Foam eight years ago to acquire the division's advanced manufacturing technologies, and Joyce continues to share its technologies with the Indian parent company. In exchange, Sheela shares its new foam products, developed by its chemists. This two-way technology transfer would prove invaluable.

The integration challenges were immense. Australian labor costs were ten times higher than India. Safety and environmental regulations were stringent. Customer expectations around service and delivery were completely different. Many Indian companies had failed at international acquisitions precisely because they underestimated these operational differences.

Joyce Foam currently owns and operates 5 modern manufacturing facilities in 4 cities in Australia, namely Adelaide, Canberra, Melbourne, Perth, and Sydney. Managing facilities across an entire continent from India was a logistical nightmare. Time zones meant someone was always working at odd hours. Cultural differences in management styles caused initial friction.

But Sheela Foam did something unusual—they didn't impose Indian management. They retained the Australian team, learned from them, and gradually created a hybrid model. The Australian operations taught them about automation, quality systems, and worker safety that they would later implement in India.

Using VPF technology, Joyce Foam's products are manufactured in an enclosed, pressure-controlled environment, eliminating the need for blowing agents, for example, liquid CO2 and methylene chloride, to help the foam rise. The enclosed process also captures emissions. This Variable Pressure Foaming technology acquired through Joyce would later become central to Sheela Foam's environmental credentials globally.

The financial impact was immediate and positive. The financial performance of Joyce Foam has shown steady growth, with revenues recorded at INR 4,130 million in FY21, INR 4,295 million in FY22, and INR 4,379 million in FY23. More importantly, it provided natural hedging against rupee fluctuations and opened doors to other developed markets.

Joyce Foam is a leading manufacturer of flexible polyurethane foam with more than 35% market share in Australia. This market position gave Sheela Foam credibility in international markets that no amount of organic growth could have achieved. When you dominate Australia, a market known for high quality standards, doors open everywhere.

The knowledge transfer went beyond technology. Australian retail is sophisticated—dominated by chains, focused on inventory turns, demanding on compliance. Joyce Foam's relationships with retailers like Harvey Norman and Forty Winks taught Sheela Foam about modern retail management that would prove invaluable when Indian retail modernized.

In 2010, Joyce Foam consolidated its manufacturing operations into a single site in Moorebank in Sydney. Joyce will consolidate all of its foam manufacturing to a single site in Moorebank in Sydney. The company will invest the A$10 million from the NSW Government to expand its Moorebank base into national manufacturing headquarters. This consolidation improved efficiency dramatically and became a template for Sheela Foam's manufacturing strategy globally.

The Joyce acquisition also changed Sheela Foam's DNA. They were no longer an Indian company with international sales. They were becoming a multinational with operations across continents. The management team started thinking globally—sourcing chemicals at global scale, benchmarking against international competitors, and most crucially, seeing India not as their only market but as one market among many.

By 2010, five years after the acquisition, the transformation was complete. Joyce Foam wasn't just profitable; it had become the innovation center for the entire group. Technologies developed in Australia were being implemented in India. Relationships with global chemical suppliers negotiated through Joyce benefited Indian operations. The student had become the teacher, and vice versa. The foundation for further international expansion was set.

V. Transformation & Innovation Era (2006–2016)

The conference room at the Greater Noida facility hummed with nervous energy in 2015. Engineers from Canada, Australia, and India huddled around foam samples, testing what would become Sheela Foam's breakthrough innovation. After years of development, they were about to crack the code on Variable Pressure Foaming technology that would eliminate harmful emissions entirely.

This decade wasn't just about growth—it was about fundamental transformation. The company was simultaneously pursuing technology leadership, retail revolution, and preparing for public markets. Each initiative reinforced the others in ways that would only become clear later.

In 2017, the company received the PU Tech Innovation Award for its vertical variable pressure foaming technology. But the innovation journey had started much earlier with strategic partnerships. The joint ventures with Woodbridge (Canada) and AH Beards (Australia) weren't just about market access—they were technology acquisition plays disguised as partnerships.

Sheela Foam developed Variable Pressure Foaming (VPF) technology, a manufacturing process that eliminates harmful emissions. Think about the implications. In an era where environmental regulations were tightening globally, Sheela Foam had technology that gave them automatic compliance anywhere. This wasn't incremental improvement; this was category-defining innovation.

The retail revolution was equally dramatic. By 2010, the Indian retail landscape was transforming. Malls were proliferating, consumer financing was becoming available, and shopping was becoming experience-driven rather than purely transactional. Sheela Foam's response was the Sleepwell Worlds concept—experiential stores where customers could understand sleep science, test products, and get sleep consultations.

These weren't just stores; they were theaters of comfort. Customers could lie down on different mattresses, understand their sleep patterns, and get recommendations based on their specific needs. In a market where mattress buying had been a five-minute decision based on pressing your palm into foam, this was revolutionary.

The company also collaborated with RMIT University, Australia, to create Pro Nexa Technology, which improves pressure relief and body support compared to conventional memory foam. This academic collaboration was strategic—it gave their marketing claims scientific credibility and pushed their R&D capabilities to international standards.

The technology investments were paying off in unexpected ways. The automotive industry, struggling with weight reduction requirements for fuel efficiency, found Sheela Foam's lightweight, high-strength foams perfect for seating. The healthcare sector discovered their antimicrobial foams ideal for hospital bedding. Each new application deepened their material science expertise.

By 2015, the digital transformation was underway. While everyone talks about e-commerce, Sheela Foam was building something more fundamental—an IT-enabled distribution network that could track inventory in real-time across thousands of retail points, predict demand patterns, and optimize logistics. This wasn't sexy, but it was the infrastructure that would enable rapid scaling.

The IPO opens on November 29, 2016, and closes on December 1, 2016. The shares are proposed to be listed on BSE, NSE. The IPO preparation was meticulous. Sheela Foams promoter Polyflex Marketing Pvt Ltd. offloaded shares worth Rs 510 crore by way of an initial public offer (IPO) during the period from 29 November 2016 to 1 December 2016. The IPO was priced at Rs 730 per share. The stock was listed on the bourses on 9 December 2016.

The IPO timing was challenging—coming right after demonetization in November 2016. Sheela Foam got good subscription on the last day by QIB but not able to impress retail investors. The main concern for this IPO is the time they launch. The factors like RBI policy and Demonetization affected the subscription. Yet, Sheela Foam IPO listing is another superb performance in this market. It list at 17.8% premium at Rs.860 against its IPO price of Rs.730.

What the market recognized was that this wasn't just a mattress company going public. This was a technology-enabled, vertically integrated, multinational consumer goods company with leadership positions in multiple markets. The IPO wasn't an exit; it was graduation to a new league.

The innovation culture extended beyond products. They were innovating in business models—rental programs for corporate housing, subscription models for mattress upgrades, partnerships with real estate developers for bulk supplies. Each experiment taught them something about changing consumer behavior.

The company continually innovated its product offerings, introducing the economy model mattress 'Starlite' in 2017 and the mid-level mattress 'Feather Foam' in 2018. This portfolio segmentation was crucial. Starlite targeted rural markets and price-conscious consumers. Feather Foam went after the massive middle market. Sleepwell remained the premium brand. Three brands, three price points, one manufacturing backbone.

By 2016, as the company listed on the exchanges, the transformation was complete. The family-run foam manufacturer had become a professionally managed, technology-driven, publicly traded corporation. But Rahul Gautam knew the biggest transformations were still ahead. The world was going digital, consumer expectations were evolving rapidly, and competition was intensifying. The next phase would test everything they had built.

VI. European Expansion & Digital Push (2017–2022)

The WhatsApp message from the M&A advisor arrived at 2 AM India time in July 2019: "Interplasp is interested in talking. They're one of Europe's best foam manufacturers. Spanish company, but they serve all of Southern Europe and North Africa. Interested?"

Rahul Gautam was wide awake within seconds. Europe was the world's largest polyurethane foam market, and Sheela Foam had been looking for an entry point for years. Sheela Foam has received approval to acquire Interplasp S.L., Spain. The Board at its meeting held on July 26, 2019 approved the same. This acquisition will give the company a presence in Europe, the worlds largest polyurethane foam market, and a huge potential opportunity to grow.

Sheela Foam plans to buy Interplasp of Yecla, Spain for EUR 42m in cash. The price was steep, but the strategic value was clear. Interplasp, which was established in 1987, makes polyurethane foam for bedding, furniture and other applications in Spain and Portugal. The company has a manufacturing facility in Yecla, in Spain, with a capacity to produce 22,000 tons of polyurethane foam.

The Interplasp acquisition was different from Joyce. This wasn't about technology acquisition—it was about market access and strategic positioning. Recognized as one of the best European flexible polyurethane foam manufacturers, Interplasp is known for its strong technological base and innovation. It operates a modernized manufacturing facility in Yecla, Spain, which is one of the most cost-effective manufacturing locations in Europe. This enables the company to maintain a competitive edge and develop strong footprints in the region.

The timing was perfect. Interplasp is well-positioned to expand operations to meet the growing demand from Europe and the US. Recently, the company has started exporting to the US with the 'Bed-in-a-box' mattress strategy from its Spain plant, capitalizing on new opportunities as the US imposes trade restrictions on other countries. The US-China trade war had created an opening, and having a European manufacturing base meant avoiding tariffs.

The "bed-in-a-box" strategy deserves special attention. While Indian newspapers were writing about Casper and Purple disrupting the US mattress market, Sheela Foam was quietly building capabilities to compete in this space. Compressed mattresses that could be shipped directly to consumers required different foam formulations, packaging technology, and logistics capabilities. Interplasp had all three.

Then COVID-19 hit in March 2020, just months after the acquisition closed. In June 2020, Sleepwell partnered with the Indian government to donate 10,000 bedding units—including mattresses, pillows, and beds—for COVID-19 relief efforts. This CSR initiative was strategic—it positioned Sleepwell as a caring brand during crisis and got their products into COVID facilities where healthcare workers would experience their quality firsthand.

The pandemic accelerated digital adoption by a decade. Suddenly, consumers who had never bought furniture online were ordering mattresses through apps. Sheela Foam's response was swift and multi-pronged. They launched STAQO Technologies as a subsidiary focused on digital transformation. This wasn't just about e-commerce—it was about digitizing the entire value chain.

Sheela Foam invests in digital transformation through its subsidiary, STAQO Technologies. This subsidiary develops enterprise technologies, automation, and digital workflow optimization for manufacturing and retail operations. STAQO built systems for virtual showrooms, AR-based visualization (see how a mattress looks in your bedroom), and AI-driven recommendation engines.

The digital push extended to manufacturing. IoT sensors on production lines provided real-time quality data. Predictive maintenance reduced downtime. Digital twins of manufacturing processes allowed optimization without physical trials. The Spanish and Australian plants became testbeds for Industry 4.0 initiatives that would later scale to India.

Record date is 22 December 2022 for the purpose of ascertaining the eligibility of shareholders for issuance of Bonus shares in the ratio of 1 (One) equity share of Rs. 5/- each for every 1 (One) equity share of Rs.5/- each held by the Members. The bonus issue in December 2022 was perfectly timed. Stock markets were recovering from COVID lows, and the 1:1 bonus rewarded shareholders while making the stock more accessible to retail investors.

E-commerce strategy evolved from defense to offense. Initially, it was about protecting share from D2C startups. But Sheela Foam realized they had advantages—manufacturing scale, brand trust, and offline presence for trials. They launched online-exclusive SKUs, offered home trials, and created a hybrid model where customers could research online but experience offline.

The financial performance of Interplasp over recent years underscores its growth trajectory. Revenues have steadily increased from INR 1,032 million in FY20 to INR 3,954 million in FY23, with a revenue of INR 2,478 million recorded for the first nine months of FY24. This consistent revenue growth reflects the successful execution of strategic initiatives and the company's robust market presence in Europe.

The European operations were exceeding expectations despite COVID disruptions. But more importantly, they were opening new possibilities. European environmental regulations were pushing foam manufacturers toward sustainability. Interplasp's innovations in bio-based foams and recyclable products were creating IP that would have global applications.

By 2022, the digital and international expansions were converging. European customers could order customized mattresses online, manufactured in Spain using Australian technology and Indian cost management. Indian customers could buy European-designed furniture foam through apps, delivered within 48 hours. The company that had started with a single factory in Sahibabad was now a genuine global player with digital capabilities matching any startup.

But Rahul Gautam wasn't satisfied. The Indian mattress market was still 95% unorganized. Regional players dominated specific geographies. And a new generation of online-first competitors was emerging. What came next would be Sheela Foam's boldest move yet.

VII. The Big Bet: Kurlon & Furlenco Acquisitions (2023)

The board meeting on July 17, 2023, was unlike any other in Sheela Foam's history. On the table were two acquisitions that would fundamentally reshape the company: Sheela Foam Ltd on Monday said it would acquire 94.66% stake in rival Kurlon for Rs 2,150 crore, as it eyes a bigger share in India's mattress market, and it will buy 35% stake in House of Kieraya, the parent firm of Furlenco, which provides furniture rental services for homes.

The combined outlay of nearly ₹2,450 crores was massive—more than the company's entire revenue just five years earlier. The board room was divided. Some directors worried about integration risks. Others questioned the valuation. But Rahul Gautam saw something others didn't: the chance to consolidate India's fragmented mattress market once and for all.

Let's understand Kurlon first. This wasn't just another mattress company. Kurlon was India's original mattress brand, established in 1962, with a heritage that predated Sheela Foam by a decade. Kurlon has over 50 warehouses and 12 manufacturing facilities across five Indian states. Kurlon's sales rose 5.4% to Rs 809 crore in fiscal 2022.

The strategic rationale was compelling. The company is the leader in northern and western India whereas KEL has strengths in southern and eastern regions of India. This acquisition will help in extending a pan-India footprint. This geographic complementarity was rare. Most acquisitions involve overlapping territories and redundant assets. This was almost perfectly complementary.

The Kurlon deal gives Sheela Foam an undisputed leadership across major product categories with its flagship brand Sleepwell's strength in foam (consistent quality and innovation); and acquired brand Kurl-on's strength in rubberised coir; wherein both these companies are leaders in their respective product segments. Sheela Foam will now command a combined market share of around 21 per cent in the modern mattress market in India.

But Kurlon came with baggage. In FY2023, KEL has provided exit to private equity investor, Motilal Oswal Private Equity Investment Advisors through a group company, Kurlon Trading & Invest Management Private Limited (wholly owned subsidiary of Kurlon Limited). The group paid circa INR 325 crore for acquiring a 6.19% stake in KE which translated assigned valuation of INR 5250 crore. Sheela Foam was acquiring at less than half that valuation—a testament to their negotiation skills and timing.

The Furlenco acquisition was even more intriguing. Sheela Foam further said it would acquire a 35 per cent stake in House of Kieraya Pvt Ltd that runs online furniture business Furlenco, for Rs 300 crore, subject to customary working capital and other adjustments. This wasn't about mattresses—it was about the future of furniture.

House of Kieraya Private Limited ("Furlenco") is a Bengaluru-based startup founded by Mr. Ajith Mohan. The company offers easy and flexible access to designer furniture with options to change at periodic intervals. The company's product portfolio includes brand-new as well as refurbished furniture. In the age of millennial mobility and subscription everything, Furlenco's rental model was prescient.

The synergies were multifaceted. It will also help leverage the strong distribution network of Sheela Foam for Furlenco products and services. The investment would also create synergies by selling input products such as foam, etc., by Sheela Foam to manufacture Furlenco products. Sleepwell & Kurl-on exclusive stores may be made available with Furlenco furniture offerings.

The market reaction was swift and positive. Shares of Sheela Foam surged 15 per cent to Rs 1,363.55 on the BSE in Tuesday's intra-day trade after the company said it has acquired a controlling stake of 94.66 per cent in Kurlon Enterprises (KEL), maker of Kurl-on mattresses. Investors understood what critics missed: this wasn't just about adding revenue, it was about creating an ecosystem.

Integration began immediately. Unlike typical acquisitions where integration is an afterthought, Sheela Foam had a 100-day plan ready before the deal closed. Teams were identified, synergies mapped, and cultural integration programs designed. They retained Kurlon's management but embedded Sheela Foam executives in key positions.

The manufacturing synergies were immediate. Production efficiencies and cost savings - the Company and KEL have many complementary facilities which will help it to serve customers from lesser distance and improve both serving and reduce costs. The transaction also has manufacturing synergies. Plants could specialize, reducing changeover costs. Raw material procurement at combined scale delivered instant savings.

SFL has stated immediate target of taking Kurlon's revenue above INR 1000cr with 10%+ operating margins. This wasn't wishful thinking. By eliminating duplicate costs, optimizing production, and leveraging Sheela Foam's distribution, these targets were conservative.

The Furlenco stake was structured cleverly. Initially, SFL have equity stake of 35% and have an option of purchasing additional 9% stake at the same valuation to be exercised within 1 year. This gave them control without full acquisition risk, with upside if the model worked.

As stated by the company, out of total requirement of around Rs. 2,350 crores for both acquisitions, Rs. 800 crores will be funded through available cash with SFL and the rest would be funded through a combination of debt and equity. SFL will raise debt of circa INR 600 crore and remaining amount coming as equity portion. The financing structure was prudent—using internal cash to minimize dilution while keeping leverage manageable.

By year-end 2023, the integration was ahead of schedule. Combined sales teams were cross-selling products. Kurlon's strong presence in South India was opening doors for Sleepwell. Furlenco's digital capabilities were being leveraged across brands. The three companies weren't just coexisting; they were multiplying each other's strengths.

The boldest aspect wasn't the size of the deals but the vision they represented. Sheela Foam wasn't thinking like a mattress company anymore. They were building India's sleep and living solutions platform—from the mattress you sleep on to the furniture you sit on, from purchase to rental, from offline to online. The transformation from foam manufacturer to lifestyle company was complete.

VIII. Business Model & Competitive Advantages

Step into Sheela Foam's Greater Noida plant at 5 AM, and you'll understand their first competitive advantage immediately. The facility runs 24/7, with chemical tanks the size of buildings feeding into production lines that stretch for hundreds of meters. This is vertical integration at a scale that would make even the most ambitious competitor pause.

Sheela Foam Limited (SFL) is an Indian multinational company that manufactures and supplies polyurethane foam mattresses and related comfort products. Sheela Foam operates across India, Australia, and Europe, with 22 manufacturing facilities in these regions. But it's not just about the number of facilities—it's about what happens inside them.

The vertical integration starts with chemicals. While competitors buy foam blocks and cut them to size, Sheela Foam controls the entire chain from polyol and TDI (the basic chemicals) to the finished mattress in consumer homes. This means they control quality at molecular level, costs at every stage, and can innovate without depending on suppliers.

One of the subsidiaries Joyce Foam Ptv Ltd. in Australia holds a 40% market share in the Australian foam market, which caters to various industries including bedding, furniture, and medical applications. This isn't just international presence—it's technology arbitrage. Innovations in Australian medical foams improve Indian hospital mattresses. Spanish furniture foam technology enhances Indian automotive applications.

The multi-brand strategy is sophisticated portfolio management. Sleepwell commands premium pricing with 30-40% gross margins. The company continually innovated its product offerings, introducing the economy model mattress 'Starlite' in 2017 and the mid-level mattress 'Feather Foam' in 2018. Starlite operates at lower margins but higher volumes. Kurlon brings heritage and trust. Each brand targets different psychographics, not just demographics.

Distribution moat deserves special attention. We brought the concept of exclusive retail to the home comfort products sector in India with Sleepwell retail centres. Today, our store network has over 5500 exclusive outlets and a total of 20,000+ touchpoints across India. Twenty thousand touchpoints. Let that sink in. A new entrant would need decades and billions to replicate this.

But here's the hidden advantage: data from these touchpoints. Every sale, every customer complaint, every product return feeds into their system. They know which foam density works in Kerala's humidity, which firmness sells in Punjab, which price point moves in Tier-3 towns. This isn't just distribution; it's a nationwide sensing network.

Manufacturing scale creates brutal economics for competitors. Indian Manufacturing Capacity: 1,23,000 MTPA with a daily mattress production capacity of 20,000 units. Twenty thousand mattresses daily. The chemical procurement at this scale, the energy contracts, the logistics optimization—each creates cost advantages that compound.

Technology edge compounds over time. Variable Pressure Foaming (VPF) technology is introduced to Joyce. VPF isn't just about environmental compliance—it produces better foam with consistent cell structure, improving comfort and durability. Competitors using traditional methods literally cannot match the product quality regardless of price.

The R&D capability is underappreciated. The company also collaborated with RMIT University, Australia, to create Pro Nexa Technology, which improves pressure relief and body support compared to conventional memory foam. Academic collaborations, international technology transfers, and decades of proprietary knowledge create an innovation pipeline competitors cannot access.

Financial strength enables strategic patience. The company has delivered a poor sales growth of 10.1% over past five years. While analysts fixate on this "poor" growth, they miss the point. Sheela Foam sacrificed growth for profitability and strategic positioning. They could have grown faster by cutting prices or accepting lower margins. They chose not to.

The revenues of SHEELA FOAM stood at Rs 30,994 m in FY24, which was up 4.7% compared to Rs 29,589 m reported in FY23. SHEELA FOAM's revenue has grown from Rs 22,136 m in FY20 to Rs 30,994 m in FY24. Over the past 5 years, the revenue of SHEELA FOAM has grown at a CAGR of 8.8%. This steady growth masks the portfolio transformation happening underneath—premiumization, market share gains in profitable segments, and strategic exits from commoditized products.

Working capital management is a hidden strength. In a business where retailers demand credit and suppliers want advance payment, Sheela Foam's scale allows them to dictate terms. They get 60-90 day payment terms from chemical suppliers while collecting from large retailers in 30-45 days. This negative working capital cycle funds growth without external capital.

The institutional knowledge is irreplaceable. Fifty years of understanding how Indians sleep, what they'll pay for comfort, how their preferences change with income levels—this isn't in any database. It's in the collective experience of thousands of employees, the relationships with retailers, the trust with consumers.

Network effects are emerging. As Sleepwell becomes synonymous with quality sleep, hospitals specify Sleepwell for patient comfort. Hotels mention Sleepwell mattresses in their amenities. Real estate developers pre-install Sleepwell in premium projects. Each creates pull demand that reinforces the brand.

The integrated ecosystem post-acquisitions creates new moats. A customer buying a Furlenco furniture subscription gets exposed to Sleepwell. A Kurlon buyer in Chennai discovers Sleepwell's premium range. A Sleepwell customer upgrades their entire bedroom with Furlenco. Cross-selling opportunities multiply with each brand addition.

But perhaps the strongest competitive advantage is the most intangible: time. Every year that passes, their manufacturing gets more efficient, their distribution gets deeper, their brand gets stronger, and their data gets richer. Competitors can copy products, match prices, even poach talent. They cannot copy five decades of compounded advantages.

IX. Playbook: Lessons for Entrepreneurs & Investors

Picture two entrepreneurs in 2024: One raises $50 million to launch a D2C mattress brand with aggressive digital marketing. Another slowly builds relationships with furniture retailers while perfecting foam chemistry in a small factory. Conventional wisdom favors the first. Sheela Foam's history suggests betting on the second.

Lesson 1: Building Brands in Commoditized Categories

Foam is literally a commodity—sold by weight, undifferentiated, purely price-driven. Yet Sheela Foam built a brand that commands premium pricing. How? They didn't brand the product; they branded the benefit. Sleepwell isn't about foam; it's about sleep. This semantic shift changes everything—competition, pricing power, customer loyalty.

The execution required patience. For years, they educated consumers about sleep health, spine alignment, and hygiene. They didn't just run ads; they created sleep clinics, published research, and partnered with doctors. When you own the problem (poor sleep), you own the solution (better mattresses).

Lesson 2: The Power of Patient Capital

Sheela Foam was founded in 1971 by Rahul Gautam and his mother, Ms. Sheela Gautam, a 4-term Member of Parliament. The family control meant they could take 10-year bets. No quarterly earnings pressure, no activist investors, no forced exits. This patience enabled fundamental advantages.

Consider the Australian acquisition. It took five years to fully integrate, another five to maximize synergies. A private equity-owned competitor would have flipped the asset or stripped it for parts within three years. Patient capital allowed technology absorption, relationship building, and cultural integration that created lasting value.

Lesson 3: Geographic Expansion Through Strategic Acquisitions

Most Indian companies expand internationally by opening sales offices or finding distributors. Sheela Foam bought market leaders. Joyce Foam was sold to India-based flexible PU foam manufacturer Sheela Foam Private Ltd. in 2005 for A$16 million (excluding property and debt). They didn't enter Australia; they became Australian.

This strategy requires courage and capital but creates immediate scale. More importantly, it provides local knowledge, relationships, and credibility that organic expansion cannot match. The Kurlon acquisition follows the same playbook domestically—buy leadership in complementary geographies rather than fight for it.

Lesson 4: Managing Complexity Across B2B and B2C

Most companies struggle with either B2B or B2C. Sheela Foam mastered both simultaneously. The B2B business (automotive, healthcare, industrial foam) provides stable cash flows and technical knowledge. The B2C business (mattresses) provides brand value and pricing power. Each reinforces the other.

The key is organizational design. Separate teams with different KPIs, compensation structures, and cultures. But shared manufacturing, R&D, and procurement. This hybrid structure is hard to manage but creates competitive advantages neither pure B2B nor pure B2C players can match.

Lesson 5: Timing Market Transitions

Every major Sheela Foam move aligned with a macro transition. 1994 Sleepwell launch—post-liberalization consumer boom. 2005 Joyce acquisition—global integration of Indian companies. 2016 IPO—formalization of Indian economy. 2019 Interplasp—global supply chain restructuring. 2023 Kurlon—consolidation of fragmented markets.

This isn't luck; it's pattern recognition. They understood that transitions create opportunities for prepared players. While competitors react to change, Sheela Foam anticipates and positions. The lesson: study macro trends, but execute micro strategies.

Lesson 6: Vertical Integration as Competitive Advantage

In an era of asset-light models and outsourcing, Sheela Foam went the opposite direction. They integrated backward into chemicals and forward into retail. This seems capital-inefficient until you understand the control it provides—over quality, cost, innovation, and customer experience.

The integration must be selective. They don't manufacture TDI (the basic chemical)—that requires different scale and capabilities. They don't own retail real estate—that's capital-intensive with different skills. They integrate where it creates competitive advantage, outsource where it doesn't.

Lesson 7: Technology as an Enabler, Not the Strategy

Sheela Foam invested heavily in technology—VPF, digital transformation, e-commerce. But technology never became the strategy; it enabled the strategy. The strategy was market leadership in sleep solutions. Technology just made it possible to deliver better products more efficiently.

This distinction matters. Technology-first companies often build solutions looking for problems. Strategy-first companies identify problems and then deploy technology to solve them. Sheela Foam's digital initiatives succeeded because they solved real customer problems, not because they were digital.

Lesson 8: Building for the Long Arc

Every major decision at Sheela Foam seems to have a 10-year payoff horizon. The Joyce acquisition took a decade to fully pay off. The R&D investments in VPF technology took years to commercialize. The retail network took decades to build. This long-term thinking is their ultimate competitive advantage.

For entrepreneurs, the lesson is about choosing your capital structure and investors carefully. For investors, it's about identifying companies with this long-term orientation and having the patience to let compounding work. Quick wins are tempting, but lasting value takes time.

The Sheela Foam playbook isn't about any single brilliant move. It's about consistent execution over decades, strategic patience, and the courage to make big bets when opportunities arise. It's a playbook for building enduring value in an impatient world.

X. Analysis: Bear vs. Bull Case

Let's strip away the narrative and examine Sheela Foam with the cold calculus of capital allocation. Two investors sit across from each other, spreadsheets open, arguing the stock. Their debate illuminates the company's future.

The Bull Case: "This is India's Sleep Solution Platform at an Inflection Point"

"Look at the market structure," the bull begins. The company holds a 30% market share in India's mattress segment and a 40% market share in Australia. "Post-Kurlon, they have 21% of India's organized market. But here's what bears miss—the organized market is only 35% of total. As India formalizes, they capture disproportionate share."

The math is compelling. India's mattress market is ₹15,000 crores, growing at 12-15% annually. The organized segment is growing at 20%+, taking share from unorganized players who cannot handle GST compliance, quality standards, or modern retail requirements. Sheela Foam doesn't need to beat competitors; they just need to be present as the tide shifts.

"The acquisition track record is pristine," the bull continues. SFL has had a strong track record of acquisitions and also turning them around. Sheela Foam had acquired Joyce Foam in Australia with 5 manufacturing plants in 2003 and Comfort Technologies in Spain in 2019. Joyce is now the innovation center. Interplasp opened Europe and the US. Kurlon brings immediate synergies.

Revenues have steadily increased from INR 1,032 million in FY20 to INR 3,954 million in FY23. This consistent revenue growth reflects the successful execution of strategic initiatives and the company's robust market presence in Europe. The European operations are proof of execution capability.

Distribution is the moat. Today, our store network has over 5500 exclusive outlets and a total of 20,000+ touchpoints across India. "A D2C competitor needs to spend ₹500-1000 to acquire a customer online. Sheela Foam's CAC through retail is near zero. The economics are unarguable."

Technology leadership matters more than people realize. In 2017, the company received the PU Tech Innovation Award for its vertical variable pressure foaming technology. VPF technology isn't just environmental compliance—it's 15% better foam yield, 20% lower energy consumption, and product quality competitors cannot match.

"The balance sheet can support growth," the bull emphasizes. Despite recent acquisitions, debt-to-equity remains manageable. The business generates cash. Working capital is negative in good quarters. They can fund expansion internally while paying dividends.

The Bear Case: "This is a Slow-Growth, Capital-Intensive Business in a Fragmenting Market"

"Let's talk about that growth," the bear counters. The company has delivered a poor sales growth of 10.1% over past five years. "In a consumption boom, with GST formalizing markets, with e-commerce exploding—they managed 10% growth. That's not leadership; that's lagging."

The margins tell a worrying story. Operating profit margins witnessed a fall and down at 10.8% in FY24 as against 10.4% in FY23. "Raw materials are 60% of costs, tied to crude oil. They have zero pricing power with chemical suppliers and limited ability to pass costs to consumers. This is a margin squeeze waiting to happen."

"D2C disruption is real," the bear argues. Wakefit raised ₹370 crores at a ₹2,500 crore valuation. SleepyCat, Sunday Mattress, and a dozen others are stealing share. "Young consumers don't care about Sleepwell's heritage. They buy online, trust online reviews, want home trials. Sheela Foam is structurally disadvantaged."

Competition from unorganized players isn't disappearing. "GST didn't kill small players; it made them more nimble. They operate at 30% lower costs, don't invest in brands, and satisfy price-conscious consumers who are 70% of India. The formalization thesis is overplayed."

Finance costs increased by 225.7% YoY. "They're leveraging up just as interest rates peak. The Kurlon integration will take years. Furlenco is burning cash. They're juggling too many balls."

The bear's final point is strategic. "They're trying to be everything—foam manufacturer, mattress brand, furniture company, rental platform. Focus is lost. Complexity is increasing. Management bandwidth is stretched. This ends badly."

The Verdict: A Question of Time Horizons

Both cases have merit, but they operate on different timelines. The bear focuses on next quarter's margins, this year's growth, immediate competition. The bull sees a 10-year consolidation play, where scale and integration create insurmountable advantages.

The net profit of SHEELA FOAM stood at Rs 1,945 m in FY24, which was down -3.2% compared to Rs 2,008 m reported in FY23. This compares to a net profit of Rs 2,187 m in FY22 and a net profit of Rs 2,402 m in FY21. Over the past 5 years, SHEELA FOAM net profit has grown at a CAGR of 0.0%. The numbers support the bear's caution.

Yet, market leadership in a growing, formalizing market with high barriers to entry rarely trades at these valuations. The question isn't whether Sheela Foam is perfect—it isn't. The question is whether current prices adequately discount the risks while ignoring the optionality.

For fundamental investors, Sheela Foam presents a classic dilemma: a quality business at a reasonable price facing near-term headwinds but positioned for long-term dominance. Your view depends on whether you're buying a stock or buying a business.

XI. Epilogue & Future Outlook

Rahul Gautam stands in the new innovation center in Greater Noida, watching engineers test a mattress that adjusts firmness based on sleep patterns. It's 2024, and the company his mother started in 1971 is unrecognizable except for one thing: the relentless focus on how Indians sleep.

The future of sleep solutions in India is being written in three acts. Act One is premiumization. As Indians spend more on homes, cars, and experiences, they're ready to invest in sleep. The ₹50,000 mattress market, negligible five years ago, is exploding. Sheela Foam's premium positioning through Sleepwell and technology leadership positions them to capture disproportionate value.

Act Two is health and wellness. Sleep tracking, posture correction, temperature regulation—mattresses are becoming health devices. The company introduced the Sleepwell Tarang Mattress, designed as an affordable alternative to traditional cotton mattresses, and the Sleepwell Pro FitRest Mattress, which is recommended by the Indian Association of Physiotherapists for muscle recovery. The convergence of comfort and healthcare creates pricing power and differentiation.

Act Three is the home ecosystem. The Furlenco acquisition isn't about furniture rental—it's about owning the customer relationship for everything home comfort. From the bed you sleep on to the sofa you work from, from purchase to subscription, from physical to digital. The TAM expands from ₹15,000 crores (mattresses) to ₹100,000 crores (home furniture).

Sheela Foam has embarked on significant capacity expansion to capture growth opportunities in the economy mattress segment. This includes setting up new export-oriented greenfield plants in Madhya Pradesh and Gujarat, leveraging advanced technology from Australia and Spain. The key details of the expansion are: Total Capex: INR 350 crore for capacity expansion. Indian Manufacturing Capacity: 1,23,000 MTPA with a daily mattress production capacity of 20,000 units. This expansion isn't just about volume—it's about flexibility to serve every segment simultaneously.

Sustainability initiatives represent both risk mitigation and opportunity. Sheela Foam developed Variable Pressure Foaming (VPF) technology, a manufacturing process that eliminates harmful emissions. As environmental regulations tighten globally, their clean technology becomes a competitive advantage and potential licensing opportunity.

The digital transformation continues. STAQO Technologies is building capabilities in predictive analytics (which foam density will a customer prefer based on their demographics?), supply chain optimization (how to deliver 20,000 mattresses daily efficiently?), and customer experience (virtual reality showrooms, AI-powered sleep consultants).

International expansion has new vectors. The US market, accessed through Spain, represents a $15 billion opportunity. Africa, served from Europe and India, is virgin territory. The playbook—acquire local leaders, transfer technology, integrate operations—is proven and repeatable.

But challenges loom. Raw material volatility, tied to crude prices, remains unhedged. D2C competitors, funded by venture capital, will continue price aggression. Chinese manufacturers, post-COVID, are looking for new markets. The macro environment—interest rates, consumption patterns, real estate cycles—adds uncertainty.

What would success look like in 2030? Market leadership with 30%+ share in India's organized mattress market, now 60% of total market versus 35% today. Revenue of ₹10,000 crores across geographies. Operating margins stabilized at 15%+. A dividend yield that attracts institutional investors. And most importantly, when Indians think sleep, they think Sheela Foam brands.

The path isn't guaranteed. Integration risks are real. Competition is intensifying. Consumer preferences are evolving rapidly. But Sheela Foam has navigated every transition India has seen—from License Raj to liberalization, from physical retail to e-commerce, from unorganized to organized markets. Their ability to adapt, evolve, and eventually dominate has been proven over five decades.

For investors, Sheela Foam represents a bet on India's formalization, premiumization, and digitization—three irreversible trends. It's a bet that execution matters more than strategy, that distribution beats product, that patience defeats velocity. It's a bet that in the race to own India's sleep, the tortoise beats the hares.

As we close this deep dive, remember that great businesses are built over decades, not quarters. They compound advantages slowly, then suddenly. They seem boring until they're inevitable. Sheela Foam might not make headlines like the latest unicorn, but while others are dreaming of disruption, they're quietly ensuring India sleeps better. And in a nation of 1.4 billion people averaging 6.5 hours of sleep, that's a revolution worth investing in.

The story that began with Sheela Gautam mixing chemicals in Sahibabad continues with her son building a global comfort solutions company. But the real story isn't about foam or mattresses or even money. It's about recognizing that fundamental human needs—in this case, quality sleep—create enduring business opportunities for those patient enough to serve them properly.

The next chapter is being written now, in boardrooms from Ghaziabad to Sydney, in factories from Spain to Chennai, in homes from rural Bihar to urban Bangalore. Whether Sheela Foam becomes India's first truly global comfort brand or remains a solid regional player depends on execution over the next five years. But one thing is certain: the company that taught India to sleep on foam isn't done innovating yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube