Sanofi Consumer Healthcare India: The Demerger Story

I. Introduction & Episode Roadmap

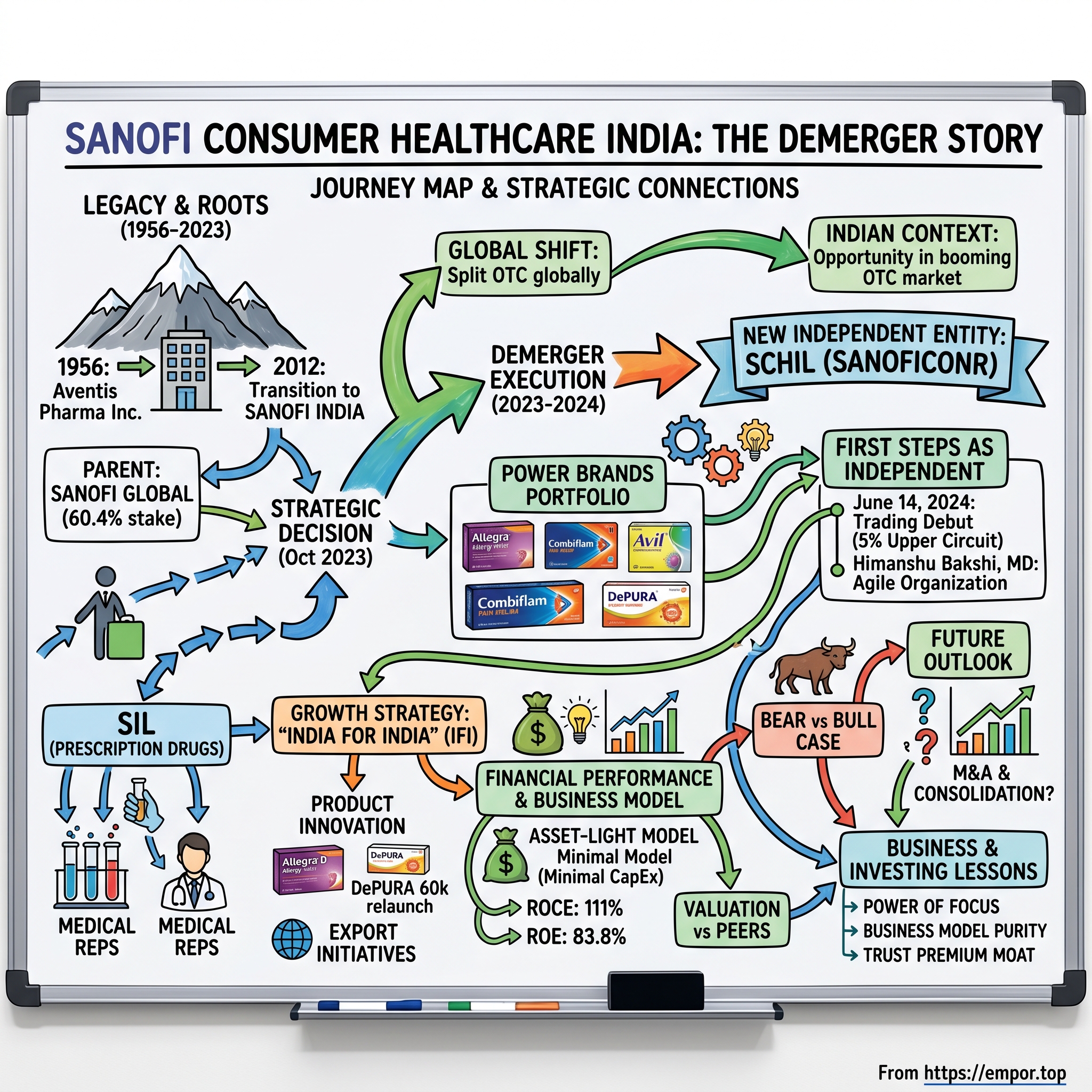

Picture this: June 14, 2024, the Bombay Stock Exchange. A new ticker symbol lights up the screens—SANOFICONR—and within minutes, the stock locks in a 5% upper circuit at ₹6,513.05. By day's end, it has surged 11% from its opening level. Within a month, it would zoom 62% to record highs. This wasn't a hot IPO or a tech unicorn debut. This was something far more unusual in Indian capital markets: a pharmaceutical giant's consumer healthcare division transformed overnight into one of India's most valuable standalone OTC companies through the alchemy of corporate restructuring.

The numbers tell a remarkable story: ₹11,679 Crore market capitalization, ₹724 Crore in revenue, ₹200 Crore in profit. But here's what makes it truly fascinating—this company was technically incorporated just a year earlier in 2023, yet it carries within it decades of consumer trust, iconic brands that generations of Indians have reached for in their medicine cabinets, and a business model so capital-efficient it generates a return on capital employed of 111%.

How does a division buried within a multinational pharmaceutical conglomerate suddenly emerge as a focused, high-margin consumer healthcare powerhouse? Why would Sanofi, the French pharmaceutical giant, choose to split its Indian operations—especially when the consumer healthcare business was delivering 28% of total turnover and growing at double-digit rates?

The answer lies in a global strategic shift, the unique dynamics of the Indian consumer healthcare market, and a textbook case of value creation through corporate unbundling. This is the story of how Allegra, Combiflam, and Avil—household names in Indian medicine cabinets—found their independence. It's a masterclass in demerger execution, a study in asset-light business models, and perhaps most importantly, a window into the future of consumer healthcare in the world's most populous nation.

Over the next few hours, we'll trace this journey from Sanofi India's roots as Aventis Pharma in 1956 to the dramatic demerger of 2024. We'll examine the strategic logic, dissect the execution, analyze the financials, and debate whether this newly independent entity can justify its lofty valuations. Along the way, we'll extract lessons about focused business models, the power of trusted brands, and the art of corporate restructuring in emerging markets.

II. The Parent Company Legacy & Global Context

The story begins not in 2023, but in May 1956, when a company called Aventis Pharma Limited was incorporated in India. This was barely a decade after independence, when Nehru's India was embarking on its industrial journey, and multinational pharmaceutical companies were establishing beachheads in what would become one of the world's largest drug markets. The company that would eventually become Sanofi India was among the pioneers, bringing Western pharmaceutical innovation to a nation grappling with public health challenges on an unprecedented scale.

The transformation from Aventis to Sanofi came on May 11, 2012, following the global merger waves that reshaped Big Pharma in the 2000s. By then, Sanofi India had evolved into one of the leading multinational companies in the Indian pharmaceutical market, with a portfolio spanning critical therapeutic areas: diabetes medications as India became the diabetes capital of the world, cardiovascular drugs for a population increasingly afflicted by lifestyle diseases, thrombosis treatments, central nervous system medications, and crucially for our story—antihistamines and consumer healthcare products.

The ownership structure tells its own story of colonial-era business structures meeting modern corporate governance. Sanofi Global and its 100% subsidiary Hoechst GmbH—a name redolent of German chemical industry heritage—together held 60.40% of Sanofi India. This wasn't just foreign ownership; it was a complex web of European pharmaceutical history, with French and German industrial legacies converging in Mumbai's Nariman Point. But what made Sanofi India particularly interesting in the 2010s was the evolution of its business mix. While the parent company globally remained focused on high-margin specialty pharmaceuticals and vaccines, the Indian subsidiary had quietly built a formidable consumer healthcare franchise alongside its prescription drug portfolio. Brands like Allegra for allergies, Combiflam for pain relief, and the venerable Avil—an antihistamine that had been a household name since the 1960s—generated predictable, cash-rich revenue streams that required minimal capital investment.

This dual nature would become central to our story when, in October 2023, Sanofi S.A. announced its intention to separate the Consumer Healthcare Business globally, with plans to create a publicly listed entity headquartered in France. The global rationale was clear: consumer healthcare needed "increased agility and flexibility to grow" and the ability to "address customers' needs across categories" as a standalone entity.

Think about the strategic logic from Paris's perspective. Sanofi's consumer brands globally included IcyHot, Allegra, Gold Bond, and generated sales of 5.2 billion euros in 2023, representing 11% of total revenue. Yet this business operated on fundamentally different dynamics than innovative pharmaceuticals—shorter product cycles, direct-to-consumer marketing, retail distribution, and competition from both pharmaceutical giants and FMCG companies. The separation would provide "greater management focus and resource allocation to the needs of the biopharma business", where the real value creation opportunities lay in the age of biologics and precision medicine.

For India, this global strategic shift would have profound implications. Following its parent's decision, the Indian entity would announce the demerger of its consumer healthcare business, creating what would become one of the most valuable pure-play consumer healthcare companies in the country virtually overnight.

The timing wasn't coincidental. The Indian pharmaceutical market was undergoing its own transformation. The country's growing middle class, increasing health awareness, and shift toward self-medication for common ailments had created a booming OTC market. Meanwhile, the prescription drug business faced pricing pressures, regulatory scrutiny, and the perpetual challenge of balancing innovation with affordability in a price-sensitive market. The stage was set for a dramatic restructuring that would unlock value hidden within a complex conglomerate structure.

III. The Strategic Demerger Decision

The boardroom at Sanofi House in Mumbai must have been charged with anticipation on May 10, 2023. The directors weren't just approving another routine corporate action—they were fundamentally reimagining the architecture of one of India's most established pharmaceutical companies. The Board of Directors approved a Scheme of Arrangement under Sections 230 to 232 of the Companies Act, 2013, to demerge the Consumer Healthcare Business from Sanofi India Limited into a newly created entity: Sanofi Consumer Healthcare India Limited.

The numbers alone justified serious consideration. For the year ended December 31, 2022, the consumer healthcare business generated turnover of approximately ₹728 crore, representing 28% of the company's total turnover. But raw revenue figures only told part of the story. Due to inherent features like being asset-light with limited trade restrictions, consumer healthcare businesses generate high margins and command better valuation and high dividend potential.

The strategic rationale went deeper than financial engineering. The demerger would enable "a different operating model for the consumer healthcare business, specific to and fit for the purpose for a fast-moving consumer healthcare company, which will lead to a greater ability to operate independently and positively shape the consumer healthcare environment". This wasn't corporate jargon—it reflected a fundamental truth about the different DNA required to succeed in consumer healthcare versus prescription pharmaceuticals.

Consider the operational differences. A prescription drug business revolves around medical representatives, doctor relationships, hospital formularies, and regulatory compliance for controlled substances. Success depends on clinical data, medical education, and navigating complex reimbursement landscapes. Consumer healthcare, by contrast, lives and dies by brand building, retail execution, digital marketing, and consumer trust. The skill sets, incentive structures, and corporate cultures required for each are almost antithetical.

The demerger would "facilitate pursuit of scale and independent growth plans and enable more focused management and stronger leverage of specific global resources within the Sanofi group". This was particularly relevant in India, where the consumer healthcare market was experiencing double-digit growth, driven by increasing health consciousness, rising disposable incomes, and a generational shift toward preventive healthcare.

The structure of the demerger was elegantly simple yet financially sophisticated. The consumer healthcare business included assets, liabilities and all other aspects pertaining to the consumer healthcare business including brands like Allegra, Combiflam, DePURA, and Avil. All intangibles related to the CHB division would get transferred to SCHIL—a crucial detail, as brand value represented the lion's share of the business's worth.

Interestingly, SIL's manufacturing facility in Goa would continue to remain part of the general medicines business, with SIL continuing to manufacture certain products for the consumer healthcare business under contract manufacturing arrangements. This arrangement revealed the pragmatic approach to the separation—maintaining operational efficiency while achieving strategic independence.

The shareholder treatment was designed to be seamless and equitable. Shareholders of SIL would receive 1 equity share of ₹10 each in SCHIL for every 1 equity share of ₹10 each in SIL, with the shareholding pattern of SCHIL mirror-imaging that of SIL as on the record date. Post-transaction, Sanofi S.A. through direct holdings and subsidiaries would maintain its 60.40% stake in both entities.

What made this demerger particularly interesting from a valuation perspective was the comparison to peers. Margins related to CHB of Sanofi were expected to be similar to those of Procter & Gamble Health Limited, one of India's most successful consumer healthcare companies. The significant part of the valuation would be attributable to the brands owned by the company—intangible assets that required minimal ongoing capital investment but generated substantial cash flows.

The global context provided additional urgency. Aligning with global pharma companies, Sanofi S.A. had announced separation of its Consumer Healthcare Business into a separate company, executing the separation in each country/region separately as per the optimum available method. India wasn't just following orders from Paris—it was seizing an opportunity to create a focused, nimble entity better suited to capture the explosive growth in Indian consumer healthcare.

The decision also reflected a broader trend in global pharmaceuticals. Companies from Johnson & Johnson to GSK had concluded that the synergies between prescription drugs and consumer products were largely illusory. Different customer bases, distribution channels, regulatory frameworks, and business models meant that housing both under one roof often led to suboptimal resource allocation and strategic confusion. The demerger would finally allow each business to optimize for its unique success factors.

IV. The Power Brands Portfolio

Walk into any Indian pharmacy, from the gleaming chains in metropolitan malls to the corner shops in tier-3 cities, and you'll encounter the brands that would form the backbone of Sanofi Consumer Healthcare India. These weren't just products; they were household names that had earned their place in Indian medicine cabinets through decades of trust and efficacy.

At the crown of this portfolio sat Allegra, the antihistamine that had become synonymous with allergy relief for millions of Indians. In a country where seasonal allergies, pollution-induced respiratory issues, and dust sensitivities affect vast swathes of the population, Allegra had positioned itself as the premium solution. The brand's performance spoke volumes: as of April 2023, Allegra had grown 22.2% in moving annual turnover, with 2022 MAT growing nearly 24% year-on-year. This wasn't just market share gain; it was category expansion, as more Indians moved from home remedies to scientifically proven OTC solutions.

Combiflam occupied a different but equally lucrative niche—pain management. In a nation where headaches from stress, body aches from long commutes, and general pain relief needs were ubiquitous, Combiflam had built a fortress of consumer loyalty. The combination of ibuprofen and paracetamol offered a one-two punch against pain that resonated with consumers seeking quick, effective relief. The brand's strength was such that even a temporary recall (later reversed with a relaunch of Combiflam Suspension) couldn't dent its market position.

Then there was Avil, a brand that carried the weight of history. Launched in the 1960s, Avil had been treating allergies and providing relief from insect bites for generations of Indians. In the corporate world, legacy brands often become liabilities—outdated, unfashionable, struggling to connect with younger consumers. But Avil had managed something remarkable: it maintained strong consumer trust while remaining relevant across demographic segments. Grandmothers recommended it to their grandchildren, creating a virtuous cycle of brand loyalty that marketing budgets alone could never buy.

DePURA represented the company's play in the rapidly growing vitamins and supplements category. As Indian consumers became more health-conscious and preventive healthcare gained traction, DePURA positioned itself at the intersection of pharmaceutical credibility and wellness aspiration. The brand would later see innovation with the relaunch of DePURA 60k, targeting vitamin D deficiency—a surprisingly common condition in sunny India due to lifestyle factors.

The portfolio was rounded out by brands like Festal for digestive issues, Baralgan for spasmodic pain, and Novalgin NU for fever and pain. Each occupied a specific therapeutic niche, together creating a comprehensive consumer healthcare offering that addressed the most common health concerns of Indian families.

What made this portfolio particularly valuable wasn't just the individual brand strength but the synergies in distribution and marketing. These products moved through the same channels—distributors, wholesalers, government institutions, hospitals, pharmacies, pharmacy chains, and increasingly, e-commerce platforms. A pharmacy stocking Allegra was likely to stock Combiflam; a consumer trusting Avil was predisposed to try DePURA. The portfolio effect created competitive moats that individual brands alone couldn't achieve.

The distribution strategy itself was a masterclass in market coverage. While premium brands often focused solely on modern trade and urban markets, Sanofi's consumer healthcare brands had achieved something more difficult: ubiquity with premium positioning. You could find Allegra in both Apollo Pharmacy and a small-town medical store, maintaining price discipline and brand equity across diverse retail environments.

E-commerce emergence added another growth vector. Online pharmacies and health platforms allowed direct-to-consumer engagement, data collection, and targeted marketing that traditional pharmaceutical distribution never permitted. The company could now track consumer behavior, understand purchase patterns, and respond with precision to market demands.

The brands also benefited from what marketers call the "halo effect" of pharmaceutical heritage. Unlike pure FMCG health products, these brands carried the credibility of Sanofi's pharmaceutical legacy. Consumers might not understand the science behind fexofenadine (Allegra's active ingredient), but they trusted the Sanofi name and the pharmaceutical pedigree it represented.

The portfolio strategy also revealed sophisticated market segmentation. While Allegra targeted urban, educated consumers willing to pay premiums for non-sedating antihistamines, Avil continued to serve price-conscious segments with a tried-and-tested solution. This multi-tier approach allowed the company to capture value across the economic spectrum without cannibalizing its premium offerings.

Innovation within established brands proved equally important. The launch of Allegra D in the allergy segment showed that even mature brands could find new growth vectors through line extensions and formulation improvements. Similarly, the reformulation and relaunch of products like DePURA 60k demonstrated responsiveness to evolving consumer needs and medical understanding.

Perhaps most importantly, these brands had achieved what every consumer company dreams of: they had become part of the Indian healthcare vernacular. "Take an Allegra" or "Try Combiflam" weren't just product recommendations; they had become shorthand for solving specific health problems. This linguistic embedding represented a competitive advantage that no amount of advertising spend could replicate.

V. The Demerger Mechanics & Execution

The execution of the demerger was a study in precision, navigating the labyrinthine Indian regulatory landscape while maintaining operational continuity and market confidence. Each step was choreographed to minimize disruption while maximizing value realization.

December 18, 2023, marked the first major milestone when shareholders overwhelmingly approved the demerger arrangement. The voting wasn't just a formality—it represented buy-in from thousands of retail and institutional investors who understood that the sum of the parts could exceed the whole. The approval came after months of investor education, roadshows, and detailed explanations of the strategic rationale.

The terms were straightforward in their equity: each member holding one equity share in Sanofi India as of the Record Date would be entitled to receive one equity share of Sanofi Consumer Healthcare India. This 1:1 ratio ensured no dilution, no complex calculations, no winners or losers—just a clean split that preserved everyone's proportional ownership in both entities.

The Record Date itself—June 13, 2024—would become etched in the memory of shareholders who suddenly found their portfolios expanded. One day they owned shares in a diversified pharmaceutical company; the next, they held stakes in two focused entities, each with distinct investment characteristics and growth trajectories.

But between shareholder approval and the record date lay the crucial regulatory gauntlet. The National Company Law Tribunal (NCLT) approval came on June 3, 2024, with an effective date of June 13, 2024. The NCLT process wasn't merely bureaucratic rubber-stamping. It involved detailed scrutiny of the scheme's fairness, protection of creditor interests, and compliance with numerous provisions of the Companies Act. The tribunal had to be satisfied that the demerger wouldn't prejudice any stakeholder—employees, creditors, minority shareholders, or the public interest.

The scheme officially became effective from June 1, 2024, with the consumer healthcare business demerged as a going concern. This "going concern" designation was crucial—it meant the business transferred with all its contracts, relationships, and operational momentum intact. Suppliers didn't need new agreements, customers didn't face disruption, and employees seamlessly transitioned to the new entity.

The operational continuity was remarkable. On May 31, 2024, consumer healthcare was a division within Sanofi India. On June 1, it was Sanofi Consumer Healthcare India Limited—a separate legal entity with its own board, management structure, and strategic autonomy. Yet for consumers buying Allegra or Combiflam, nothing changed. The products remained on shelves, quality standards were maintained, and the trusted brands continued their journey, now under a more focused corporate umbrella.

Post-demerger, Sanofi S.A. continued to own 60.4% stake in both entities, maintaining strategic control while allowing each business to chart its own course. This ownership structure provided stability—international shareholders knew the French parent remained committed—while enabling the operational flexibility that justified the split.

The logistics of the demerger revealed meticulous planning. Share certificates had to be issued, depositary receipts adjusted, and trading systems updated. The stock exchanges needed new ticker symbols, market makers required pricing models, and analysts scrambled to initiate coverage on the newly independent entity. Each technical detail, from ISIN number allocation to depositary participant instructions, was executed flawlessly.

The contract manufacturing arrangement with the Goa facility demonstrated pragmatic problem-solving. Rather than duplicating manufacturing infrastructure—a capital-intensive and time-consuming endeavor—the companies agreed to a supply arrangement that maintained efficiency while respecting corporate independence. This arrangement would ensure product availability while the new entity evaluated its long-term manufacturing strategy.

Employee transitions were handled with similar care. Key personnel in consumer healthcare moved to the new entity, maintaining institutional knowledge and relationships. Compensation structures were adjusted to reflect the new company's focus and growth potential. The cultural shift—from being part of a large pharmaceutical company to joining a nimble consumer healthcare specialist—required careful change management.

The tax implications were structured to be neutral for shareholders, avoiding the capital gains triggers that could have dampened enthusiasm for the demerger. This tax efficiency wasn't accidental—it required careful structuring and regulatory approvals to ensure shareholders weren't penalized for a corporate restructuring beyond their control.

Legal documentation ran into thousands of pages—scheme documents, court petitions, shareholder notices, creditor communications, and regulatory filings. Each document was scrutinized by lawyers, vetted by regulators, and ultimately formed the legal architecture supporting the new corporate structure.

The demerger also required separation of information systems, financial records, and intellectual property. Years of commingled data had to be cleanly divided, with each entity receiving the information relevant to its operations while maintaining data privacy and competitive confidentiality.

By the time June 14, 2024 arrived—the first trading day for the new entity—the execution had been so smooth that the market's enthusiastic response seemed almost anticlimactic. The stock's immediate surge validated not just the strategic logic but the flawless execution that made the value unlock possible.

VI. First Steps as Independent Entity

The morning of June 14, 2024, marked a defining moment in Indian capital markets. As trading opened, SANOFICONR didn't just debut—it exploded. The stock locked in a 5% upper circuit at ₹6,513.05, gained 11% from its opening level, and set the stage for a remarkable run that would see it zoom 62% within a month to record highs. This wasn't typical new listing volatility; it was the market's emphatic validation of focused business models over conglomerate structures.

The leadership team that would steer this newly independent ship brought serious credentials. Amit Jain assumed the role of chairman, bringing strategic oversight and board governance expertise. But the operational leadership fell to Himanshu Bakshi as Managing Director, whose vision would prove instrumental in defining the company's independent identity. Bakshi wasn't just inheriting a business—he was architecting a transformation.

"Our commitment to delivering high-quality, science-backed products remains unwavering," Bakshi would later articulate, but his vision went deeper. He spoke of being "driven by focused portfolio, research-led innovation, and agile organization"—corporate speak that actually meant something here. The agility part was crucial. Free from the bureaucracy of a global pharmaceutical giant, decisions that once took months now took weeks. Product launches that required multiple committee approvals could now move at market speed.

The ownership structure post-demerger revealed interesting dynamics. Opella Healthcare Participations B.V. emerged as the promoter, owning 60.4% of the company. This wasn't just a holding company—it represented Sanofi's global consumer healthcare architecture, providing strategic support while allowing operational independence. The promoter holding had increased 10.9% over the last quarter, a signal of confidence that sophisticated investors didn't miss.

The initial months of independence saw a flurry of activity that would have been impossible within the previous structure. The company commenced export operations, extending its reach toward international markets. This wasn't just about incremental revenue—it was about leveraging Indian manufacturing cost advantages and regulatory credibility to compete globally. The "Made in India" pharmaceutical story, which had already conquered generic drugs, was now extending to consumer healthcare.

Product innovation accelerated dramatically. The launch of Allegra D in the allergy segment showed the company could innovate within established franchises. The relaunch of DePURA 60k capitalized on growing awareness of vitamin D deficiency among urban Indians. Even the Combiflam Suspension relaunch, following an earlier recall, demonstrated the company's ability to address quality issues swiftly and return stronger.

The India for India (IFI) strategy emerged as the operational philosophy. This wasn't just marketing rhetoric but a fundamental recognition that Indian consumer healthcare needs differed from global templates. The strategy focused on "implementing go-to-market initiatives, enhancing operational efficiency" with emphasis on "all growth pillars." In practice, this meant products formulated for Indian conditions, price points calibrated for Indian wallets, and distribution strategies that acknowledged India's unique retail landscape.

Financial performance in the first quarters of independence vindicated the demerger thesis. Q2 2025 results showed revenue up 28% year-on-year to ₹220.9 crore, with profit after tax of ₹60.7 crore—up 21% quarter-on-quarter. These weren't just honeymoon period numbers; they reflected genuine operational improvements and market share gains enabled by focused execution.

The dividend policy signaled confidence and shareholder-friendly governance. An annual dividend of ₹55.00 per share, yielding 1.02%, might seem modest in absolute terms, but for a newly independent company investing in growth, it represented a balanced approach to capital allocation. The last ex-dividend date of April 17, 2025, would be closely watched as a indicator of sustainable shareholder returns.

Digital transformation, barely a priority in the previous structure, suddenly accelerated. E-commerce partnerships expanded, digital marketing budgets increased, and direct-to-consumer initiatives launched. The company could now move with the agility of a startup while leveraging the brand equity of decades.

The organizational culture shift was palpable. Employees who had been part of a large pharmaceutical company suddenly found themselves in a focused, entrepreneurial environment. Decision-making accelerated, innovation was rewarded, and market responsiveness became the norm rather than the exception. The company began attracting talent from FMCG companies and startups—professionals who wouldn't have considered a traditional pharmaceutical role but were excited by the consumer healthcare opportunity.

Stakeholder communications transformed as well. Investor calls became more frequent and detailed. Management was more accessible to analysts and media. The company began telling its story directly rather than being a footnote in global pharmaceutical earnings calls. This transparency and engagement created a virtuous cycle of market understanding and valuation support.

Supply chain optimization, freed from global procurement mandates, could now source locally where it made sense. This not only reduced costs but improved speed to market and supply chain resilience. The company could respond to local demand spikes—say, allergy medication during pollution peaks—with agility that the previous structure never permitted.

The regulatory strategy also evolved. As a focused consumer healthcare company, regulatory resources could concentrate on OTC-specific requirements rather than being spread across prescription and consumer portfolios. This specialization improved compliance efficiency and accelerated product approvals.

By the end of its first year of independence, Sanofi Consumer Healthcare India had proven that the demerger wasn't just financial engineering—it was strategic transformation that unlocked organizational potential previously constrained by structural complexity.

VII. Business Model & Financial Performance

The financial architecture of Sanofi Consumer Healthcare India reads like a private equity dream: asset-light operations generating returns on capital employed of 111% and return on equity of 83.8%. These aren't typos or accounting anomalies—they reflect the fundamental economics of branded consumer healthcare in India, where intellectual property and consumer trust generate cash flows that traditional manufacturing businesses can only fantasize about.

Start with the headline numbers: a market capitalization of ₹11,679 Crore supporting revenue of ₹724 Crore and profit of ₹200 Crore. The price-to-earnings ratio of 59.5 might trigger value investor vertigo, but context matters. This isn't a commodity business trading on cycles; it's a portfolio of annuity-like cash flows from products that Indian consumers have trusted for generations.

The book value of ₹112 per share seems almost quaint against a stock price in the thousands, reflecting the reality that traditional accounting struggles to capture intangible value. The brands, customer relationships, and distribution networks that constitute the company's true worth don't appear on balance sheets designed for industrial age businesses. The Q2 2025 performance validated the demerger thesis spectacularly. Revenue jumped 28% year-on-year to ₹220.9 crore, supported by export operations and product launches. Profit after tax for the quarter reached ₹60.7 crore, a 21% increase over Q1 2025. These weren't just post-demerger honeymoon numbers—they reflected genuine operational improvements enabled by focused execution.

The asset-light model deserves deeper examination. Unlike traditional pharmaceutical companies that require massive capital investments in R&D and manufacturing facilities, consumer healthcare operates on a different plane. The products are largely established, with proven safety profiles and well-understood manufacturing processes. The value creation happens not in laboratories but in brand building, distribution excellence, and consumer engagement.

Consider the working capital dynamics. Consumer healthcare products move faster than prescription drugs, with shorter shelf lives but quicker inventory turns. Cash conversion cycles compress, freeing up capital for marketing and distribution rather than being tied up in slow-moving inventory. The company doesn't need to maintain large safety stocks of raw materials or navigate complex active pharmaceutical ingredient supply chains.

The margin structure tells its own story. Due to inherent features like being asset-light with limited trade restrictions, consumer healthcare businesses generate high margins and command better valuation and high dividend. Without the burden of extensive R&D spending—which can consume 15-20% of revenue in innovative pharmaceutical companies—more drops to the bottom line.

The export initiative added another growth vector. The quarter marked the commencement of export operations, expanding the company's footprint internationally. This wasn't just opportunistic international sales but a strategic lever to amortize fixed costs across larger volumes while leveraging India's cost advantages and regulatory credibility in global markets.

Product innovation within established franchises proved remarkably capital-efficient. The company relaunched two previously recalled products—Depura 60k and Combiflam Suspension—and introduced a new offering, Allegra D, in the Allergy segment. These weren't moonshot R&D projects requiring hundreds of millions in investment but incremental innovations that extended brand franchises and addressed specific consumer needs.

The dividend policy reflected confidence in cash generation capabilities. An annual dividend of ₹55.00 per share might seem modest in yield terms at 1.02%, but for a newly independent entity with significant growth opportunities, it signaled balanced capital allocation. The company could fund growth, reward shareholders, and maintain financial flexibility—the trifecta of sound financial management.

Comparative valuation metrics reveal interesting dynamics. Trading at 45.2 times book value might seem excessive by traditional metrics, but consider the alternatives. Global consumer healthcare companies routinely trade at similar multiples, reflecting the value of brands, distribution networks, and predictable cash flows. In India's context, where trusted healthcare brands enjoy quasi-monopolistic positions in consumer minds, these valuations might actually prove conservative.

The financial resilience was tested early with product recalls, yet the company demonstrated its ability to navigate challenges. The successful relaunch of Combiflam Suspension and DePURA 60k showed that temporary setbacks didn't erode brand equity—consumers welcomed back trusted products once quality issues were resolved.

Management's commentary revealed strategic clarity. Himanshu Bakshi stated: "Our commitment to delivering high-quality, science-backed products continues to anchor our growth strategy, driven by a focused portfolio, research-led innovation, and an agile organization. The quarter reflects the outcomes of a focused approach".

The exceptional income of ₹66 million in Q2FY25 from reversal of excess demerger-related provisions might seem like a one-time benefit, but it reflected conservative provisioning during the demerger—management had prepared for complications that didn't materialize, a sign of prudent planning rather than aggressive accounting.

Looking at the capital structure, the company operated with minimal debt, reflecting the cash-generative nature of the business. This wasn't just financial conservatism but strategic positioning—in consumer healthcare, the ability to invest quickly in marketing campaigns, product launches, or distribution expansion often determines competitive success.

The tax efficiency post-demerger added another layer of value. As a focused entity with cleaner corporate structure, tax planning became more straightforward, optimizing the effective tax rate without the complications of transfer pricing between prescription and consumer divisions.

The scalability of the business model was perhaps most impressive. Revenue could grow significantly without proportional increases in fixed costs. The same brands, distribution networks, and organizational capabilities could support multiples of current revenue, creating operating leverage that would flow directly to bottom-line growth.

VIII. Product Innovation & Growth Strategy

Innovation in consumer healthcare doesn't follow the traditional pharmaceutical playbook of billion-dollar R&D programs and decade-long clinical trials. Instead, it's about understanding evolving consumer needs, leveraging existing molecular assets, and executing with speed and precision. Sanofi Consumer Healthcare India's post-demerger innovation strategy exemplified this focused approach.

The launch of Allegra D represented textbook brand extension strategy. Rather than cannibalizing the flagship Allegra franchise, Allegra D addressed a specific subset of allergy sufferers who needed decongestant relief alongside antihistamine benefits. This wasn't random product proliferation but targeted portfolio expansion based on consumer insights and unmet needs.

The relaunch of DePURA 60k deserves particular attention. Vitamin D deficiency had emerged as a silent epidemic in urban India—paradoxical in a sun-drenched country but explained by indoor lifestyles, pollution, and dietary habits. By reformulating DePURA with a higher, once-weekly dose, the company addressed both the medical need and the behavioral reality of supplement compliance. The '60k' wasn't just a number; it was a promise of convenience that resonated with time-pressed consumers.

The Combiflam Suspension relaunch following an earlier recall demonstrated resilience and quality commitment. Rather than abandoning a temporarily problematic product, the company fixed the issues, secured regulatory clearances, and returned to market stronger. This sent a powerful message: setbacks were learning opportunities, not permanent defeats.

International expansion emerged as a strategic pillar rather than an afterthought. The commencement of export operations expanded the company's footprint internationally. This wasn't just about incremental revenue but about leveraging Indian manufacturing cost advantages, regulatory harmonization with global standards, and the growing acceptance of Indian pharmaceutical products worldwide.

The "India for India" (IFI) strategy represented philosophical clarity about market focus. Rather than force-fitting global products into Indian markets or diluting focus with excessive internationalization, IFI meant developing products specifically for Indian health conditions, price points, and consumption patterns. This localization went beyond packaging—it influenced formulation, dosing, and even brand communication.

Management's vision, articulated by Himanshu Bakshi, emphasized being "driven by focused portfolio, research-led innovation, and agile organization." The agility part was crucial. Free from global corporate bureaucracy, product decisions that once took quarters now took weeks. Market feedback could be incorporated rapidly, competitive threats addressed swiftly, and opportunities seized before they evaporated.

The go-to-market initiatives under IFI focused on "all growth pillars"—existing brand growth, new product launches, geographic expansion, and channel diversification. Each pillar had dedicated resources and clear metrics, avoiding the diffusion of effort that plagued many diversified pharmaceutical companies.

Digital transformation accelerated dramatically post-demerger. E-commerce partnerships expanded beyond mere distribution to include exclusive launches, special packaging, and direct consumer engagement. The company could now experiment with D2C models, subscription services, and personalized health solutions—innovations impossible within a traditional pharmaceutical structure.

The innovation pipeline focused on adjacencies rather than moonshots. Instead of venturing into entirely new therapeutic areas, the company leveraged existing brand equity to address related health needs. An allergy brand could extend into respiratory wellness, a pain brand into sports recovery, a vitamin brand into immunity support. Each extension built on established trust while opening new revenue streams.

Regulatory strategy evolved to support innovation. Rather than viewing regulatory compliance as a cost center, the company positioned it as a competitive advantage. Faster approvals meant quicker market entry, quality certifications enabled premium pricing, and regulatory credibility facilitated international expansion.

The portfolio optimization continued post-demerger with strategic pruning. Not every legacy product deserved investment; some were maintained for completeness, others phased out to focus resources on growth drivers. This portfolio discipline—knowing what not to do—proved as important as innovation initiatives.

Partnerships and collaborations took new forms. Without the constraints of global pharmaceutical partnerships, the company could explore relationships with Indian FMCG companies, digital health startups, and retail chains. These partnerships brought new capabilities—digital marketing expertise, last-mile distribution, consumer insights—that traditional pharmaceutical relationships couldn't provide.

Manufacturing innovation, while maintaining the Goa facility relationship with the parent, focused on efficiency and flexibility rather than scale. Quick changeovers between products, smaller batch sizes for new launches, and quality systems that exceeded requirements became competitive advantages in a fast-moving market.

The R&D approach shifted from discovery to development. Instead of searching for new molecules, the focus turned to optimizing existing ones—better formulations, improved delivery systems, enhanced patient convenience. This pragmatic approach delivered faster returns with lower risk.

Consumer insight capabilities expanded dramatically. Post-demerger, the company could invest in sophisticated market research, social listening tools, and consumer panels. Understanding not just what consumers bought but why they bought it became central to innovation strategy.

The sustainability angle emerged as both responsibility and opportunity. Eco-friendly packaging, responsible sourcing, and carbon-neutral operations weren't just corporate social responsibility checkboxes—they resonated with increasingly conscious consumers and differentiated products in crowded categories.

Supply chain innovation focused on resilience and responsiveness. Multiple supplier relationships, local sourcing where possible, and inventory strategies that balanced efficiency with availability ensured products remained on shelves even during disruptions.

The talent strategy evolved to support innovation. The company began attracting professionals from FMCG companies, startups, and digital agencies—people who brought fresh perspectives and challenged pharmaceutical orthodoxies. This cultural transformation was perhaps the most important innovation of all.

IX. Playbook: Business & Investing Lessons

The Sanofi Consumer Healthcare India demerger offers a masterclass in value creation through corporate restructuring, but the lessons extend far beyond this single transaction. They speak to fundamental truths about business focus, capital efficiency, and the often-illusory nature of conglomerate synergies.

First, consider the power of focused business models versus diversified conglomerates. For decades, business schools taught the virtues of diversification—risk reduction, synergy capture, economies of scale. Yet the Sanofi demerger, like many before it, suggests the opposite. The demerger enabled "a different operating model for the consumer healthcare business, specific to and fit for the purpose for a fast-moving consumer healthcare company" and would "facilitate pursuit of scale and independent growth plans and enable more focused management".

The market's reaction—a 62% surge within a month of listing—wasn't irrational exuberance but recognition that focused companies often outperform diversified ones. Why? Because management attention is finite, capital allocation becomes clearer, and organizations can optimize for specific success factors rather than compromising across different business requirements.

The demerger illuminated the importance of business model purity. Prescription pharmaceuticals and consumer healthcare might both involve pills and potions, but their business models diverge fundamentally. One relies on R&D and doctor relationships; the other on brand building and consumer trust. Housing both under one roof often means neither receives optimal resource allocation or strategic focus.

Creating value through corporate restructuring doesn't require operational improvements or market growth—sometimes it's simply about recognizing that 1+1 equals less than 2 in corporate combinations. The same assets, same products, same people can be worth dramatically more in the right structure than the wrong one. This isn't financial engineering; it's strategic clarity.

The trust premium in consumer healthcare brands represents an underappreciated moat. Brands like Allegra and Combiflam weren't just products—they were promises backed by decades of consistent delivery. In healthcare, where the cost of a wrong choice can be severe, consumers pay premiums for certainty. This trust, once earned, creates pricing power and customer loyalty that new entrants struggle to overcome.

Timing matters enormously in corporate actions. The demerger coincided with several favorable trends: growing health consciousness in India, increasing self-medication acceptance, digital distribution proliferation, and global pharmaceutical companies recognizing the distinct nature of consumer healthcare. Executing the same demerger five years earlier or later might have yielded different results.

Asset-light businesses deserve premium valuations, but markets often take time to recognize this. The 111% return on capital employed wasn't an accounting anomaly but reflected the fundamental economics of brand-based businesses. When your primary assets are intangible—brands, relationships, trust—traditional book value metrics become almost meaningless.

The importance of operational continuity during restructuring cannot be overstated. The seamless transition from division to independent company, maintaining product availability and quality throughout, prevented competitor encroachment and preserved consumer confidence. Many restructurings fail not because the strategy is wrong but because execution falters.

Management quality and vision matter more in newly independent entities. Himanshu Bakshi's articulation of strategy, quick wins in product launches, and clear communication with stakeholders built confidence that this wasn't just a financial restructuring but a genuine business transformation.

The parent company's continued majority ownership (60.4%) provided stability while allowing operational independence—a Goldilocks structure that balanced entrepreneurial energy with corporate backing. Full spinoffs might offer more independence but less support; this hybrid model captured benefits of both.

Regulatory navigation capabilities represent hidden value in emerging markets. The company's ability to secure NCLT approval, manage the demerger process, and maintain compliance throughout demonstrated institutional capabilities that competitors couldn't easily replicate. In India's complex regulatory environment, this expertise constituted a competitive advantage.

The market's initial skepticism (or inability to value the demerged entity) created opportunity for astute investors. The 62% gain in the first month suggested the market needed time to understand and price the new entity appropriately. Corporate actions often create such valuation dislocations.

Brand portfolio management—knowing which brands to invest in, maintain, or discontinue—proved as important as innovation. Not every legacy brand deserved equal attention; strategic focus on high-potential brands like Allegra while maintaining cash cows like Avil optimized resource allocation.

The importance of distribution in consumer healthcare cannot be overstated. Products need to be available when consumers need them, where they shop, at prices they'll accept. The company's ability to maintain distribution through the demerger and quickly expand into e-commerce and exports demonstrated execution excellence.

Cultural transformation possibilities in newly independent entities often surprise. Freed from parent company constraints, organizations can evolve rapidly, attracting different talent and adopting new ways of working. The company's ability to hire from FMCG and digital sectors wouldn't have been possible within the pharmaceutical parent structure.

The dividend sustainability in asset-light businesses provides a margin of safety for investors. The ₹55 annual dividend might seem modest, but its sustainability even through restructuring and growth investments demonstrated the cash-generative nature of the business model.

For investors, the demerger highlighted the importance of looking beyond reported numbers to understand business quality. Traditional metrics suggested an expensive stock; understanding the business model revealed possible undervaluation despite high multiples.

The geographic focus paradox—sometimes global ambitions distract from local opportunities. The "India for India" strategy recognized that deep local focus could create more value than shallow global presence.

Finally, the demerger demonstrated that corporate restructuring isn't just financial engineering—it's about aligning structure with strategy, enabling focus, and unlocking human potential. The same assets in different configurations can create dramatically different outcomes.

X. Analysis & Bear vs. Bull Case

Bull Case: The Compounding Machine

The bull thesis for Sanofi Consumer Healthcare India rests on a confluence of powerful tailwinds that could drive sustained outperformance for years. Start with the staggering financial metrics: a return on capital employed of 111% and return on equity of 83.8%. These aren't temporary aberrations but structural advantages inherent to asset-light, brand-driven businesses.

The market opportunity appears vast and underpenetrated. India's per capita spending on OTC medications remains a fraction of developed markets, even adjusted for purchasing power. As income levels rise, health consciousness increases, and self-medication becomes more accepted, the addressable market expands geometrically, not linearly.

Brand strength provides the most defendable moat. Allegra's 24% year-on-year growth demonstrates pricing power and market share gains simultaneously—a rare combination suggesting the brand hasn't nearly reached saturation. These aren't commodities competing on price but trusted solutions to health problems, creating customer lifetime values that justify premium valuations.

Management execution since demerger has been exemplary. Quick product launches, successful relaunches of recalled products, export initiation, and strong financial performance demonstrate operational excellence. Himanshu Bakshi's vision of "research-led innovation and agile organization" isn't just rhetoric but reflected in results.

The asset-light model enables exceptional capital efficiency. Without massive manufacturing investments or R&D spending, incremental revenue drops disproportionately to the bottom line. Operating leverage means margin expansion as the business scales, creating a virtuous cycle of growth and profitability.

Distribution expansion into e-commerce and exports opens new growth vectors without cannibilizing existing channels. Digital distribution offers higher margins and direct consumer relationships, while exports leverage Indian cost advantages in global markets.

The promoter holding increase of 10.9% signals confidence from sophisticated insiders who understand the business better than anyone. When owners increase stakes in newly independent entities, it often presages sustained outperformance.

Regulatory tailwinds favor established players. As quality standards tighten and compliance costs rise, subscale competitors struggle while established companies with robust quality systems gain share. The company's pharmaceutical heritage provides regulatory credibility that pure FMCG players lack.

Portfolio optimization opportunities remain substantial. Many legacy brands haven't received focused attention for years; targeted investment could revitalize dormant franchises. The success with Allegra D and DePURA 60k suggests similar opportunities across the portfolio.

The valuation, while optically high at 59.5 times earnings, may actually be reasonable given the quality. Global consumer healthcare companies trade at similar multiples, and India's growth premium could justify even higher valuations. The 45.2 times book value reflects the inadequacy of book value in capturing intangible assets.

Bear Case: The Valuation Trap

The bear thesis begins with valuation vertigo. Trading at 45.2 times book value and 59.5 times earnings prices in perfection and beyond. Any disappointment—a product recall, regulatory action, competitive pressure—could trigger devastating multiple compression.

The dependency on a few key brands creates concentration risk. Allegra and Combiflam drive disproportionate value; issues with either could cripple the equity story. The product recalls, while successfully managed, demonstrate the perpetual quality risks in pharmaceutical manufacturing.

Competition intensifies from multiple directions. Global giants like P&G Health and GSK Consumer Healthcare bring international resources. Domestic players like Mankind and Cipla Health leverage local expertise and relationships. Digital-native brands target younger consumers with modern marketing. The competitive moat might be narrower than appears.

Regulatory risks lurk perpetually in healthcare. Price controls, quality issues, advertising restrictions, or changes in OTC classification could materially impact profitability. The Indian government's populist tendencies and focus on healthcare affordability create persistent overhangs.

The recent incorporation (2023) means limited operating history as an independent entity. The strong initial performance might reflect low-hanging fruit rather than sustainable advantages. Without long-term track records, investors are betting on potential rather than proven performance.

Market saturation in key categories looms. How much bigger can the antihistamine market grow? How many pain relief options do consumers need? Category maturity could constrain growth despite execution excellence.

The parent company overhang through 60.4% ownership creates governance concerns. Minority shareholders remain vulnerable to decisions favoring the parent. Transfer pricing, related-party transactions, and strategic decisions might not always align with minority interests.

Macro headwinds could disproportionately impact discretionary health spending. Economic slowdowns typically see consumers trading down to generics or delaying non-critical health purchases. The premium positioning makes the company vulnerable to consumption downturns.

Digital disruption threatens traditional distribution advantages. Telemedicine, online pharmacies, and D2C brands bypass traditional channels where established brands dominate. Younger consumers show less brand loyalty and more price consciousness.

The talent challenge in maintaining innovation momentum is real. Attracting and retaining top talent in Mumbai's competitive market, especially for a company transitioning from MNC subsidiary to independent entity, presents ongoing challenges.

The export strategy, while promising, faces execution risks. International markets have different regulatory requirements, competitive dynamics, and consumer preferences. Success in India doesn't guarantee international viability.

The Balanced View

The truth, as often, lies between extremes. Sanofi Consumer Healthcare India is neither a guaranteed compounder nor an overvalued trap but a high-quality business at a full price. The bull case strengths—brand power, asset-light model, execution capability—are real and sustainable. The bear case concerns—valuation, competition, regulatory risks—are equally valid and material.

For long-term investors, the key question isn't whether the business is good (it clearly is) but whether it's good enough to justify the price. The answer depends on one's assessment of India's consumer healthcare opportunity, management's execution capability, and the sustainability of competitive advantages.

The recent performance suggests the market sees more upside than downside, but markets can be wrong. The 62% surge post-listing might have pulled forward future returns, creating a period of consolidation ahead. Alternatively, it might be the beginning of a multi-year rerating as the market recognizes the value of focused consumer healthcare businesses.

Risk management becomes crucial at these valuations. Position sizing, diversification, and clear exit criteria matter more when investing in highly valued, concentrated businesses. The asymmetry—limited upside versus significant downside—demands careful portfolio construction.

XI. Epilogue & Future Outlook

As we conclude this deep dive into Sanofi Consumer Healthcare India's demerger journey, it's worth stepping back to consider what this transformation represents for Indian capital markets, the pharmaceutical industry, and the art of corporate restructuring itself.

Management's forward vision, articulated as remaining "steadfast in our purpose to make self-care simpler, more accessible and effective for consumers," might sound like standard corporate messaging, but it captures a profound shift in Indian healthcare consumption. The movement from doctor-dependent treatment to consumer-driven self-care represents not just a business opportunity but a societal transformation.

The Indian consumer healthcare landscape is evolving at unprecedented pace. Rising health consciousness, accelerated by the pandemic, has permanently altered consumer behavior. The stigma around self-medication is fading, replaced by informed self-care. Digital information accessibility means consumers research symptoms, compare products, and make educated choices. This informed consumer is both opportunity and challenge—more willing to pay for quality but also more demanding of value.

The potential for M&A and portfolio expansion looms large. As an independent entity with strong cash generation and a valuable currency in its highly-rated stock, Sanofi Consumer Healthcare India could become a consolidator. Acquiring regional brands, distressed assets from struggling competitors, or complementary portfolios from companies exiting consumer healthcare could accelerate growth beyond organic expansion.

Several key milestones deserve monitoring. The sustainability of current growth rates as the base grows larger. The success of international expansion beyond initial forays. The ability to launch truly innovative products rather than just line extensions. The maintenance of margins as competition intensifies. Each will test whether the demerger unlocked temporary or permanent value.

The lessons for other companies considering demergers are manifold. Structure matters—the right assets in the wrong configuration destroy value. Timing matters—market conditions, regulatory environment, and strategic clarity must align. Execution matters—the best strategy fails with poor implementation. Communication matters—stakeholders need to understand and believe in the vision.

Perhaps most importantly, this demerger challenges conventional wisdom about corporate structure in emerging markets. The assumption that companies need global parents for credibility, scale economies justify conglomeration, and diversification reduces risk all proved wrong here. Instead, focus, agility, and clarity created more value than size and scope.

Looking ahead, several scenarios could unfold. The company could continue its independent journey, compounding value through organic growth and operational excellence. It could become an acquisition target for global consumer healthcare giants seeking Indian exposure. It could itself become an acquirer, rolling up the fragmented Indian OTC market. Or it could expand internationally, leveraging Indian cost advantages to compete globally.

The regulatory environment will remain crucial. Government policies on healthcare pricing, OTC classification, and advertising will shape industry dynamics. The push for universal healthcare could expand or constrain OTC markets. Quality standards will likely continue tightening, favoring established players with robust systems.

Technological disruption presents both opportunity and threat. AI-driven health apps could recommend products, expanding the market, or replace products by suggesting lifestyle changes. Personalized medicine could create new categories or obsolete existing ones. The company's ability to navigate technological change will determine long-term success.

The competitive landscape will undoubtedly intensify. Global giants won't cede the Indian market without a fight. Domestic players will leverage local insights and relationships. New entrants will target niche segments with innovative models. Maintaining leadership will require constant innovation and execution excellence.

The sustainability imperative grows stronger. Consumers increasingly demand environmental responsibility alongside product efficacy. Sustainable packaging, ethical sourcing, and carbon neutrality will become competitive necessities, not optional extras. Companies that lead on sustainability could capture premium segments and consumer loyalty.

The human capital dimension deserves emphasis. As India's pharmaceutical talent pool deepens and consumer industry expertise grows, the company's ability to attract, develop, and retain top talent becomes crucial. Creating a culture that balances pharmaceutical rigor with consumer marketing creativity will determine innovation capacity.

For investors, Sanofi Consumer Healthcare India represents a clear choice. Those believing in India's consumption story, the power of focused business models, and management's execution capability will see opportunity despite high valuations. Those concerned about valuation risks, competitive threats, and regulatory uncertainties will await better entry points or avoid entirely.

The broader implications extend beyond this single company. If focused entities consistently outperform diversified conglomerates, more restructurings will follow. If consumer healthcare generates superior returns to prescription pharmaceuticals, capital will flow accordingly. If India demonstrates successful demergers create value, corporate India might undergo widespread restructuring.

In the end, the Sanofi Consumer Healthcare India story is still being written. The demerger was not a conclusion but a beginning—the first chapter of an independent journey that could lead anywhere. Whether it becomes a case study in value creation or a cautionary tale about excessive valuations remains to be determined.

What's certain is that the company has positioned itself at the intersection of powerful trends: India's growing health consciousness, the shift toward self-care, the premiumization of consumer products, and the digitization of healthcare. How successfully it navigates these trends while managing risks and competition will determine whether the market's initial enthusiasm proves prescient or premature.

For students of business, investors, and industry participants, Sanofi Consumer Healthcare India offers rich lessons about corporate strategy, value creation, and the evolving nature of healthcare consumption. The demerger demonstrated that sometimes the best path forward involves splitting apart, that focus can triumph over scale, and that recognizing distinct business models within conglomerates can unlock tremendous value.

As India continues its economic journey, stories like this—of corporate transformation, strategic clarity, and value creation—will multiply. The playbook written here will be studied, adapted, and improved upon. But for now, Sanofi Consumer Healthcare India stands as a testament to the power of focused strategy, excellent execution, and the courage to pursue independent paths when logic demands it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube