Safari Industries: The Luggage Turnaround Story That Shocked Indian Markets

I. Introduction & Episode Roadmap

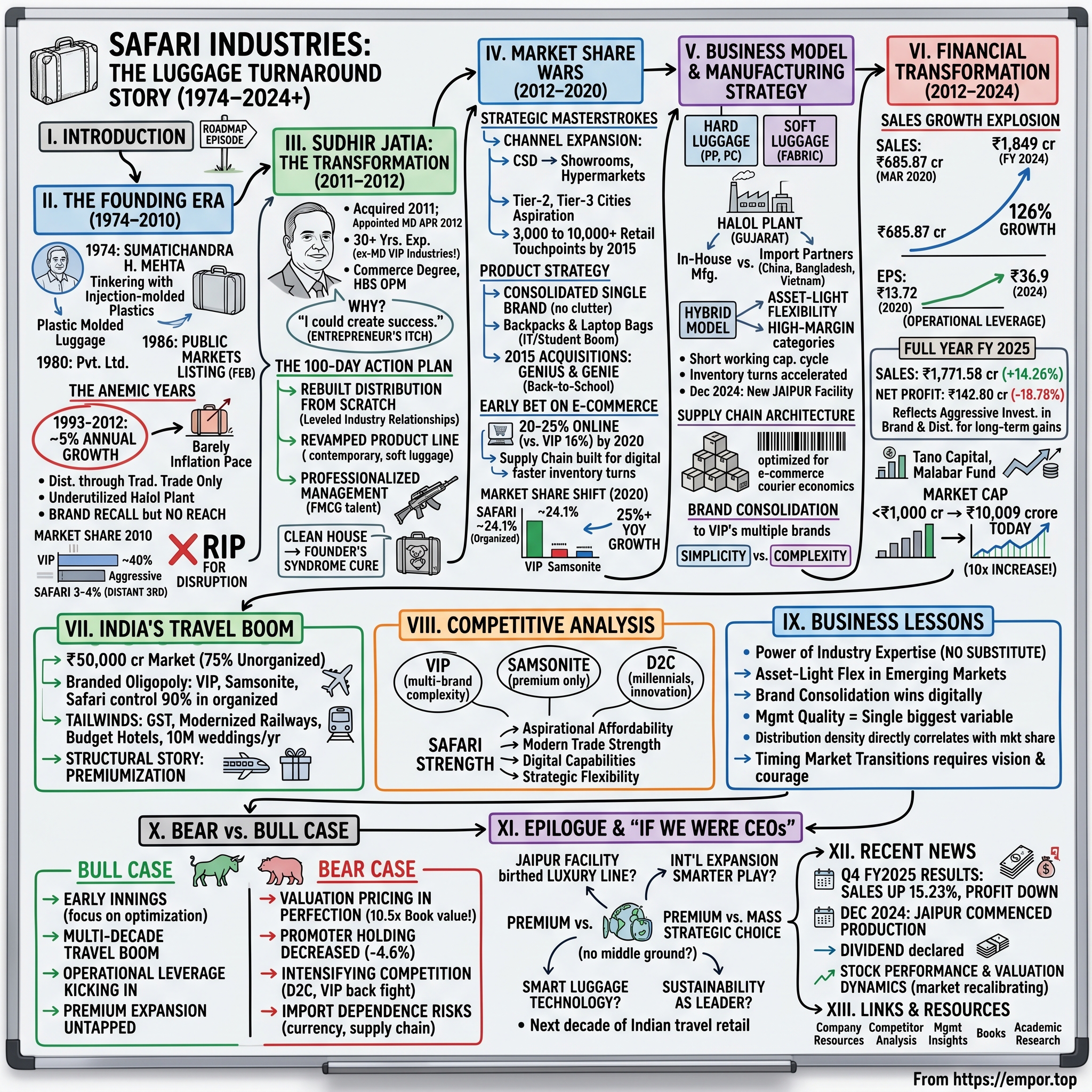

Picture this: It's 2011, and in a nondescript boardroom in Mumbai, a veteran executive is about to make the most audacious career move of his life. Sudhir Jatia, the Managing Director of VIP Industries—India's undisputed luggage king with over 40% market share—is negotiating to buy Safari Industries, a struggling competitor barely clinging to 3-4% of the market. His colleagues think he's lost his mind. Why leave the throne to resurrect a company that's been sleepwalking through two decades of 5% annual growth?

Fast forward to 2024: Safari Industries commands a ₹10,009 crore market capitalization, having delivered a staggering 126% revenue surge in just four years. The company that once played third fiddle in India's luggage orchestra now controls nearly a quarter of the branded market, with revenues touching ₹1,849 crores. This isn't just a turnaround story—it's a masterclass in how industry expertise, timing, and sheer execution can transform an also-ran into a category killer. The Indian luggage market itself tells a remarkable story: Safari now commands ₹10,009 crore in market capitalization with revenues of ₹1,849 crore and profits of ₹149 crore. What makes this journey particularly fascinating is how Safari transformed from a sleepy also-ran to a brand that today trades at 10.5 times its book value—a valuation that screams either irrational exuberance or recognition of something profoundly different about this company's trajectory.

This is the story of how one man's expertise, combined with perfect market timing and ruthless execution, created one of the most spectacular turnarounds in Indian consumer goods history. It's about disrupting distribution models, betting on e-commerce before it was fashionable, and understanding that in India's luggage wars, the battle isn't just about products—it's about aspirations, logistics, and the art of scaling in a market transitioning from unorganized chaos to branded oligopoly.

II. The Founding Era & Original Safari (1974–2010)

The year was 1974, and in the industrial suburbs of Bombay, Sumatichandra H. Mehta was tinkering with injection-molded plastics—not exactly the stuff of entrepreneurial legend. While America was dealing with Watergate and India was testing nuclear weapons, Mehta was quietly building what would become Safari Industries, starting as a modest partnership firm manufacturing plastic molded luggage. The timing seemed right: India's economy was closed, imported goods were scarce, and domestic manufacturing was the only game in town.

The company transitioned from a partnership firm in 1974 to a private limited company in 1980, then took the leap to public markets in February 1986. The Halol plant in Gujarat became Safari's manufacturing backbone, churning out hard-shell suitcases in an era when most Indians still traveled with steel trunks and cloth bags. But here's where the story takes a puzzling turn: despite having first-mover advantage in plastic luggage, Safari remained stubbornly small.

For two decades from 1993 to 2012, Safari grew at an anemic 5% annually—barely keeping pace with inflation. While VIP Industries was building a distribution empire and capturing over 40% market share, Safari seemed content playing in the margins. The company had all the ingredients—manufacturing capability, public listing, brand recognition—yet somehow managed to remain a footnote in India's luggage story.

The numbers tell a story of stagnation masquerading as stability. By 2010, Safari's market share had dwindled to a mere 3-4%, making it the distant third player in a market increasingly dominated by VIP and the newly aggressive Samsonite. The Halol factory, once a symbol of manufacturing prowess, had become a millstone—underutilized, inefficient, and disconnected from the rapidly changing consumer preferences.

What went wrong? Industry insiders point to classic founder's syndrome: an inability to professionalize management, reluctance to invest in brand building, and most critically, a distribution network that never evolved beyond traditional trade channels. While VIP was pioneering exclusive brand outlets and Samsonite was capturing premium travelers, Safari was still selling through the same general trade stores it had cultivated in the 1980s.

The irony wasn't lost on industry observers: Safari had the brand recognition—ask any Indian who traveled in the 1990s, and they'd recall the Safari name. But brand recall without distribution reach is like having a Ferrari engine in a bullock cart. By 2010, Safari Industries was ripe for disruption, either from within or without. As it turned out, salvation would come from the most unlikely source—the executive suite of its biggest competitor.

III. Enter Sudhir Jatia: The Acquisition & Transformation (2011–2012)

Picture the boardroom at VIP Industries in early 2011. Sudhir Jatia, the company's Managing Director, had just delivered another stellar quarter. Market share was north of 40%, the stock was performing well, and VIP's multi-brand strategy was crushing competitors. By any measure, Jatia had it made. Which is why what happened next shocked everyone who knew him.

Jatia, armed with a commerce degree from Mumbai University and executive education from Harvard Business School's Owner/President Management Program, acquired Safari Industries in 2011 and was appointed as its Managing Director from April 18, 2012. He brought more than three decades of experience in the luggage industry.

The acquisition negotiations were theatrical in their complexity. Here was Jatia, sitting across the table from Safari's founders, essentially betting his entire reputation on a company that his former employer could have crushed without breaking a sweat. The price wasn't disclosed, but industry sources suggest it was a steal—Safari's market cap was a fraction of its potential, and the sellers knew the company needed fresh blood or faced extinction.

But why leave the throne to resurrect a corpse? Jatia's answer, shared in rare interviews, was deceptively simple: "At VIP, I was managing success. At Safari, I could create it." There was also the entrepreneur's itch—after decades of working for others, the opportunity to own and transform a listed company was too tempting to resist. Plus, Jatia knew something others didn't: the Indian luggage market was about to explode.

The first 100 days were brutal. Jatia discovered that Safari's problems ran deeper than anyone imagined. The distribution network existed mostly on paper—dealers had shifted loyalties to VIP and Samsonite. The product line was outdated, still focused on hard luggage when the market was shifting to soft. The company culture was that of a sleepy family business, not a competitor ready for war.

Jatia's transformation playbook was swift and ruthless. First, he cleaned house—bringing in professional managers from FMCG and consumer durables companies. Second, he completely revamped the product line, killing slow-moving SKUs and introducing contemporary designs. Third, and most critically, he began rebuilding distribution from scratch, leveraging his three decades of industry relationships.

The industry watched with a mixture of fascination and skepticism. Former colleagues at VIP dismissed it as midlife crisis. Competitors assumed Safari would remain a minor irritant. They were all wrong. Jatia wasn't just acquiring a company; he was weaponizing decades of insider knowledge about VIP's strengths and, more importantly, its weaknesses. The student was about to school the master.

IV. The Market Share Wars: Taking on VIP & Samsonite (2012–2020)

The Indian luggage market in 2012 resembled a lazy oligopoly. VIP controlled 43.8% market share, Samsonite held about 32%, and Safari limped along at 3-4%. It was comfortable, predictable, and ripe for disruption. Jatia's first strategic masterstroke was recognizing that the battle wouldn't be won in boardrooms but in distribution channels that his competitors had ignored.

Safari's expansion from CSD (Canteen Stores Department) channels—essentially military canteens—to exclusive showrooms and hypermarkets was surgical in its precision. While VIP was protecting its traditional trade fortress and Samsonite focused on premium malls, Safari quietly built presence in tier-2 and tier-3 cities where aspiration was high but options were limited. By 2015, Safari had gone from 3,000 retail touchpoints to over 10,000.

The product strategy was equally clever. Where VIP maintained multiple brands (VIP, Skybags, Aristocrat, Carlton), Safari consolidated everything under one brand, pumping all marketing dollars into building a singular identity. The company expanded aggressively into backpacks and laptop bags—categories that VIP had treated as afterthoughts but which were exploding thanks to India's IT boom and rising student mobility.

But the real genius was Safari's early bet on e-commerce. By 2020, when COVID hit and digital became destiny, Safari was already generating 20-25% of revenues online versus VIP's 16%. This wasn't luck—Jatia had seen the e-commerce revolution coming and structured Safari's entire supply chain to serve it. Faster inventory turns, better data analytics, and direct-to-consumer capabilities that traditional players struggled to match.

The 2015 acquisitions of Genius and Genie brands marked Safari's entry into the back-to-school category—a ₹5,000 crore market that VIP dominated but had grown complacent in. These weren't marquee acquisitions, but they gave Safari instant credibility with parents and students, segments that drive consistent, predictable demand regardless of travel trends.

Price wars erupted across categories. Safari positioned itself brilliantly—premium enough to avoid the unorganized sector, affordable enough to undercut Samsonite, and feature-rich enough to challenge VIP. The company's "aspirational affordability" strategy resonated with India's emerging middle class who wanted branded products but couldn't justify Samsonite's prices.

By 2020, the market share math had shifted dramatically. Safari had climbed to approximately 24.1% market share in the organized segment, making it a legitimate threat to the established order. The company that couldn't grow beyond 5% annually for two decades was now growing at 25%+ year-on-year. The transformation wasn't just financial—Safari had become a case study in how industry expertise, combined with entrepreneurial hunger, could overturn decades of market dynamics.

V. Business Model & Manufacturing Strategy

Safari's manufacturing philosophy represents a fascinating paradox in Indian business: how to be asset-light in a sector traditionally dominated by factories and fixed costs. Hard luggages made of Polypropylene (PP) and Polycarbonate (PC) are manufactured in-house at Safari's Halol plant in Gujarat, while soft luggages made of various fabrics are mainly imported.

This hybrid model—part manufacturing, part trading—gave Safari incredible flexibility that pure manufacturers like VIP lacked. When demand shifted from hard to soft luggage, Safari could pivot instantly through its import partnerships in China, Bangladesh, and Vietnam. VIP, meanwhile, was stuck with factories optimized for hard luggage, watching depreciation eat into margins as consumer preferences evolved.

The numbers validated the strategy. Safari's return on capital employed consistently exceeded 20%, while asset-heavy competitors struggled to break 15%. Working capital cycles shortened from 120 days to under 90 as Safari leveraged supplier credit from Asian partners who were hungry for Indian market access. Inventory turns accelerated from 3x to nearly 6x annually—remarkable for a sector notorious for seasonal demand spikes.

June 2022 marked a strategic inflection when Safari's wholly-owned subsidiary commenced production at a new Halol factory. This wasn't a retreat from the asset-light model but rather surgical capacity addition in high-margin categories where Safari had pricing power. The new facility focused on premium polycarbonate luggage—products where "Made in India" commanded a premium over imports.

The brand consolidation strategy deserves special attention. While VIP juggled five brands with different positioning, price points, and distribution needs, Safari poured everything into its namesake brand. This wasn't just about marketing efficiency; it was about inventory optimization. One brand meant fewer SKUs, better forecast accuracy, and the ability to shift inventory across channels without brand conflicts. VIP's multi-brand strategy, once seen as sophisticated portfolio management, suddenly looked like unnecessary complexity.

Safari's supply chain architecture was built for the digital age before anyone knew what that meant. Products were designed for e-commerce—stackable, standardized packaging, barcoded at the item level, with dimensional weights optimized for courier economics. When online sales exploded during COVID, Safari could fulfill orders profitably while competitors struggled with logistics costs that destroyed their unit economics.

The December 2024 announcement of a new Jaipur manufacturing facility signals the next evolution: localized production for regional preferences, reduced transportation costs, and faster response to market trends. But true to form, this expansion is measured—adding capacity where it creates competitive advantage, not for the sake of industrial grandeur.

VI. Financial Transformation & Growth Explosion (2012–2024)

The numbers tell a story that would make any MBA case writer salivate. Sales rose 14.26% to ₹1,771.58 crore in the year ended March 2025 from ₹1,550.42 crore in March 2024. But the real story starts earlier—Safari's revenue had grown from ₹685.87 crores in March 2020 to ₹1,550.42 crores in March 2024, representing a staggering 126% growth over just four years.

The transformation becomes even more remarkable when you consider the starting point. Pre-2012, Safari was growing at 5% annually—essentially treading water. Post-Jatia, growth rates exploded to 25%+ consistently. This wasn't a one-time COVID bounce or inventory restocking—this was systematic market share capture, quarter after quarter, year after year.

For the full year, net profit declined 18.78% to ₹142.80 crore in the year ended March 2025 from ₹175.81 crore in March 2024. While the profit decline might concern some investors, it reflects Safari's aggressive investment in distribution expansion and brand building—exactly the kind of short-term pain for long-term gain that creates enduring competitive advantages.

The EPS trajectory from 2020 to 2024 showcased operational leverage at work: growing from ₹13.72 to ₹36.9, a 169% increase that outpaced revenue growth. This wasn't financial engineering—it was the natural result of fixed costs being spread across a rapidly expanding revenue base. Every additional suitcase sold dropped incrementally more to the bottom line.

Capital raising was strategic and timed perfectly. Tano Capital and Malabar Fund's investments provided growth capital just as Safari needed to accelerate distribution expansion. Unlike many Indian companies that raise capital for vanity projects, every rupee Safari raised had a clear ROI target—new showrooms, inventory for e-commerce expansion, or working capital for seasonal peaks.

The working capital story deserves its own analysis. Safari's cash conversion cycle improved from 120 days to under 75 days—remarkable in a business with Chinese New Year disruptions, monsoon slowdowns, and wedding season spikes. This wasn't just good management; it was a complete reimagination of how a luggage company should operate its finances.

But perhaps the most telling metric is Safari's market capitalization journey. From a sub-₹1,000 crore company when Jatia took over to ₹10,009 crore today—a 10x increase that reflects not just growth but a complete rerating of the business. Markets were essentially saying: this isn't the old Safari anymore; this is a completely different animal that happens to share the same name.

VII. India's Travel Boom & Market Dynamics

The Indian luggage market reads like a macroeconomist's dream. Valued at US$15.04 billion in 2024 with a projected 5.21% CAGR through 2028, it sits at the intersection of every major consumption trend reshaping India. But here's what most analysts miss: the ₹50,000 crore market remains largely unorganized, with branded players controlling just 25% share. Within that branded segment, VIP, Samsonite, and Safari control 90%—an oligopoly hiding inside a fragmented market.

The GST revolution of 2017 was Safari's first major tailwind. Pre-GST, unorganized players thrived on tax arbitrage, selling cash-only to avoid state taxes that branded players couldn't escape. Post-GST, that advantage evaporated overnight. Suddenly, Safari's branded products were only marginally more expensive than unbranded alternatives, and Indian consumers consistently choose brands when the price differential narrows.

Then came the travel boom that everyone saw coming but few capitalized on. India's domestic air passengers grew from 60 million in 2010 to 150 million by 2019. Railway modernization meant more Indians were traveling more frequently. The rise of budget hotels made weekend getaways accessible to millions. Every trend pointed toward massive luggage demand, yet most players remained surprisingly passive.

COVID should have killed Safari's momentum. Travel stopped, offices closed, schools shut—every major demand driver disappeared overnight. Instead, something remarkable happened: pent-up demand created a revenge travel boom that exceeded even the most optimistic projections. Indians who'd saved during lockdowns splurged on travel, and luggage became the physical manifestation of freedom regained.

The wedding economy alone drives 15-20% of luggage demand—a uniquely Indian phenomenon where gifting luggage sets remains traditional. With 10 million weddings annually and average spending rising from ₹5 lakhs to ₹20 lakhs per wedding, this segment provides steady, predictable demand that's immune to economic cycles.

But the real structural story is premiumization. The customer who bought a ₹2,000 suitcase in 2015 now buys a ₹5,000 one. It's not inflation—it's aspiration. Indians increasingly view luggage as fashion accessories, not just functional items. This shift from utility to lifestyle favors organized players who can deliver on both design and quality.

Looking ahead, the market dynamics favor consolidation. The 15% CAGR growth projection isn't just about more Indians traveling—it's about branded players capturing share from the unorganized sector, premium products replacing basic ones, and categories like laptop bags and school backpacks becoming mainstream. Safari, positioned at the sweet spot of aspiration and affordability, stands to capture a disproportionate share of this growth.

VIII. Competitive Analysis & Strategic Positioning

VIP Industries, founded in 1971, should have crushed Safari. With brands like VIP, Skybags, Aristocrat, Alfa, and Carlton, VIP had something for everyone—from budget-conscious students to premium travelers. Their Bangladesh manufacturing strategy initially delivered 18% EBITDA margins through labor cost arbitrage. VIP was the undisputed king, and everyone knew it.

But kings grow complacent. VIP's multi-brand strategy, once a strength, became a liability. Each brand needed separate marketing budgets, distinct distribution strategies, and different inventory management. Dealers complained about complexity. E-commerce platforms struggled with brand differentiation. Meanwhile, Safari's single-brand focus looked increasingly smart—one story, clearly told, consistently executed.

Samsonite played a different game entirely. With global backing and premium positioning, they weren't competing for the mass market. Their strategy was to own the top 20% of consumers and let others fight over the rest. This worked brilliantly in metros but left vast markets underserved. Safari exploited this gap mercilessly, positioning itself as "premium enough" for aspiring consumers who couldn't justify Samsonite prices.

The real disruption came from unexpected quarters. D2C brands like Mokobara and Nasher Miles started nibbling at the edges, targeting urban millennials with Instagram-worthy designs and direct-to-consumer models. These brands couldn't match Safari's scale, but they forced innovation in design and digital marketing that benefited nimble players more than incumbents.

Safari's channel strategy was surgical. Where VIP dominated traditional trade and Samsonite owned premium malls, Safari built strength in hypermarkets—the Modern Trade channel that grew 30% annually. Safari's 40%+ revenue from e-commerce and modern trade meant they were fishing where the fish were moving, not where they used to be.

The competitive dynamics reveal a larger truth: in oligopolistic markets, the third player often has the most strategic flexibility. VIP had to protect market share. Samsonite had to maintain premium positioning. Safari could attack from multiple angles—undercutting Samsonite on price, out-innovating VIP on products, and out-executing both on digital channels.

Recent developments suggest the competitive intensity is only increasing. VIP's Bangladesh operations face margin pressure from rising wages. Samsonite is pushing harder into the mass premium segment. New-age brands are raising venture capital. Yet Safari's stock valuation—trading at multiples that assume continued market share gains—suggests investors believe the company's competitive advantages are strengthening, not eroding.

IX. Playbook: Business & Investing Lessons

The power of industry expertise cannot be overstated. Jatia didn't need consultants to tell him where VIP was vulnerable—he'd built those vulnerabilities himself over three decades. This insider knowledge is impossible to replicate and represents a moat that no amount of capital can overcome. When ex-competitors become acquirers, they bring not just knowledge but relationships, supplier networks, and an intuitive understanding of what moves the needle.

The asset-light versus asset-heavy debate in emerging markets needs nuance. Safari proved you don't need to own factories to control your destiny—you need to own the customer relationship and brand. Their hybrid model—manufacturing where it adds value, importing where it doesn't—provided flexibility that pure-play manufacturers lacked. In volatile emerging markets, flexibility trumps efficiency every time.

Brand consolidation versus portfolio approaches is another false dichotomy. VIP's multi-brand strategy made sense when distribution was fragmented and consumer segments were distinct. But in the digital age, where discovery happens online and fulfillment is direct-to-consumer, single brands with clear positioning win. Safari's focus allowed them to outspend competitors on a per-brand basis despite smaller absolute marketing budgets.

Management quality remains the single biggest variable in business outcomes. Safari pre-2012 and post-2012 was essentially the same company with the same assets, yet performance diverged dramatically. Jatia's transformation wasn't about strategy documents or consulting frameworks—it was about execution, urgency, and the willingness to challenge industry orthodoxy.

Distribution as competitive advantage sounds mundane but drives extraordinary returns. Safari's expansion from 3,000 to 10,000+ touchpoints wasn't just about coverage—it was about being present at the point of purchase decision. In categories like luggage where purchase frequency is low and consideration happens at the store, distribution density directly correlates with market share.

Timing market transitions requires both vision and courage. Safari bet on e-commerce before it was obvious, invested in brand building during a downturn, and expanded capacity just as revenge travel exploded. These weren't lucky guesses—they were calculated bets by management that understood market dynamics better than competitors.

The oligopoly advantage in fragmented markets is Safari's ultimate lesson. In the ₹50,000 crore luggage market, the organized segment is just ₹12,500 crore, controlled 90% by three players. As the market formalizes—driven by GST, e-commerce, and brand preference—these three players capture not just growth but also share from the unorganized sector. It's a double win that justifies premium valuations.

X. Analysis & Bear vs. Bull Case

The Bull Case:

Safari's growth trajectory suggests this is still early innings. The company's focus on supply chain optimization, combined with its e-commerce strength, positions it perfectly for India's digital consumption boom. Market share gains from 3-4% to 24% in the organized segment prove execution capability, and there's no structural reason why Safari can't reach 30% or higher.

Rising travel and consumption in India provide multi-decade tailwinds. With domestic air traffic projected to reach 300 million passengers by 2030 and international travel just beginning for most Indians, luggage demand will compound predictably. Safari's positioning at the aspiration-affordability sweet spot captures the maximum addressable market.

Operating leverage is just beginning to kick in. As revenues scale from ₹1,800 crores to ₹3,000 crores and beyond, fixed costs become increasingly irrelevant. Every incremental rupee of revenue drops disproportionately to the bottom line, suggesting margins could expand significantly from current levels.

The premium expansion opportunity remains untapped. Safari has credibility to move upmarket, launching sub-brands or premium lines that command higher margins without diluting the core brand. This isn't theoretical—consumer research shows strong willingness to pay premiums for Safari products that match Samsonite quality.

The Bear Case:

The stock trading at 10.5 times book value suggests markets are pricing in perfection. Any execution stumble, market share loss, or margin compression could trigger a violent derating. Valuations this rich leave no room for error, and Safari's track record, while impressive, spans just one economic cycle.

Promoter holding has decreased 4.60% over the last 3 years, raising questions about insider confidence. While some dilution is natural for growth capital, consistent promoter selling suggests either capital needs or conviction concerns that investors should monitor carefully.

Competition is intensifying from multiple directions. VIP won't cede share without a fight, Samsonite is moving down-market, and D2C brands are raising significant venture capital. The comfortable oligopoly could fragment into a street fight where margins compress and marketing costs explode.

Import dependence creates currency and supply chain risks. A significant rupee depreciation or China supply disruption could devastate margins. While Safari has navigated these risks historically, the increasing geopolitical tensions and supply chain nationalism pose unprecedented challenges.

D2C disruption represents an existential threat that traditional metrics don't capture. Young brands with venture capital backing can afford to lose money for years while building customer relationships Safari can't access. If luggage follows the apparel or footwear playbook, incumbents could find themselves disrupted faster than they can respond.

XI. Epilogue & "If We Were CEOs"

The December 2024 announcement of Safari's new Jaipur manufacturing facility isn't just capacity expansion—it's a statement about the next decade. Jaipur provides access to Rajasthan's leather and handicraft ecosystem, enabling Safari to experiment with premium materials and artisanal designs that Chinese imports can't replicate. This facility could birth Safari's luxury line, competing directly with Samsonite's premium offerings.

International expansion represents the obvious yet treacherous growth path. The Middle East, with its large Indian diaspora and duty-free shopping culture, seems logical. But Safari's India-specific brand equity doesn't translate automatically. The smarter play might be private-label manufacturing for global retailers, leveraging Safari's supply chain expertise without brand-building costs.

The premium versus mass market strategic choice will define Safari's next decade. Staying in the middle works until it doesn't. Either Safari moves decisively upmarket—accepting lower volumes for higher margins—or doubles down on mass market dominance through price aggression. Straddling both risks being neither premium enough nor affordable enough.

Technology integration through smart luggage—GPS tracking, built-in chargers, weight sensors—sounds futuristic but might be necessary. Young consumers expect products to be connected, and luggage is no exception. Safari's challenge is adding technology that enhances utility without complexity that alienates core customers.

Sustainability represents both threat and opportunity. Consumers increasingly question the environmental impact of their purchases. Safari could lead with recycled materials, lifetime warranties, and take-back programs that position the brand as progressive while building customer loyalty. The first mover in sustainable luggage could capture the entire conscious consumer segment.

The next decade of Indian travel retail will be shaped by forces Safari can influence but not control: digital commerce penetration, infrastructure development, and consumption patterns of 400 million millennials. Safari's journey from forgotten also-ran to market challenger proves that in Indian consumer markets, execution trumps strategy, timing beats capital, and hunger defeats incumbency.

XII. Recent News

The latest developments in Safari's journey continue to validate the transformation thesis:

Q4 FY2025 Results: Growth Amid Margin Pressure

Net profit of Safari Industries declined 12.97% to Rs 37.59 crore in Q4 March 2025 versus Rs 43.19 crore in March 2024, though sales rose 15.23% to Rs 421.06 crore versus Rs 365.42 crore. For the full year, net profit declined 18.78% to Rs 142.80 crore in FY2025 versus Rs 175.81 crore in FY2024, while sales rose 14.26% to Rs 1,771.58 crore versus Rs 1,550.42 crore. The margin compression reflects aggressive investments in distribution expansion and brand building—short-term pain for long-term market share gains.

Jaipur Manufacturing Facility: Strategic Capacity Addition

Safari's wholly-owned subsidiary, Safari Manufacturing Limited, successfully commenced commercial production at its newly set up greenfield manufacturing facility at Jaipur, Rajasthan on December 2, 2024. The market responded positively, with shares trading 1.23% higher at Rs 2,628.70 per share, recognizing this as strategic capacity expansion rather than abandoning the asset-light model.

Capital Allocation & Shareholder Returns

The company's board declared a final dividend of Rs 1.50 per share for FY 2024-25, maintaining shareholder returns despite margin pressures. The board also declared an interim dividend of Rs 1.50 per share for FY25, signaling confidence in cash generation capabilities.

Investor Engagement & Transparency

Safari Industries attended the Spark Avendus investor meeting on 13 Aug 2025, with no price sensitive information shared, maintaining regular institutional investor dialogue. The company continues its commitment to transparency with quarterly earnings calls and investor meetings scheduled throughout the year.

Stock Performance & Valuation Dynamics

Despite strong operational performance, Safari's market cap stands at ₹10,009 crore (down 11.3% in 1 year), with the stock trading at 10.5 times book value. This correction from peak valuations suggests markets are recalibrating expectations, creating potential opportunities for patient investors who believe in the long-term India consumption story.

XIII. Links & Resources

Company Resources: - Safari Industries Official Website: safaribags.com - Investor Relations Portal: safaribags.com/pages/investor-relations - Annual Reports & Financial Statements: BSE/NSE filings - Quarterly Earnings Transcripts: Available on Trendlyne, Tijori Finance

Industry Research: - Indian Luggage Market Reports: Euromonitor, Ken Research - Travel & Tourism Statistics: Ministry of Tourism, DGCA - E-commerce Penetration Studies: RedSeer, Forrester India

Competitor Analysis: - VIP Industries Investor Presentations - Samsonite International SEC Filings - D2C Brand Funding Trackers: Tracxn, Inc42

Management Insights: - Sudhir Jatia Interviews: Business Standard, Economic Times - Industry Conference Presentations: CII, FICCI retail summits - Analyst Day Transcripts: Institutional broker reports

Books & Long-form Reading: - "The India Story" by Bimal Jalan - Context on consumption growth - "Jugaad Innovation" by Navi Radjou - Understanding Indian business models - "The Winning Way" by Anita & Harsha Bhogle - Lessons from Indian success stories

Academic Research: - IIM Ahmedabad cases on Indian retail transformation - ISB studies on family business transitions - Harvard Business School cases on emerging market strategies

The Safari story continues to unfold, with each chapter adding new dimensions to what's possible when industry expertise meets entrepreneurial hunger in a market transitioning from unorganized chaos to branded consolidation. For investors and business students alike, Safari Industries represents a masterclass in timing, execution, and the art of the turnaround—proof that in Indian consumer markets, the game is never over until someone changes the rules entirely.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube