Punjab & Sind Bank: The Story of India's Community Banking Pioneer

I. Introduction & Episode Roadmap

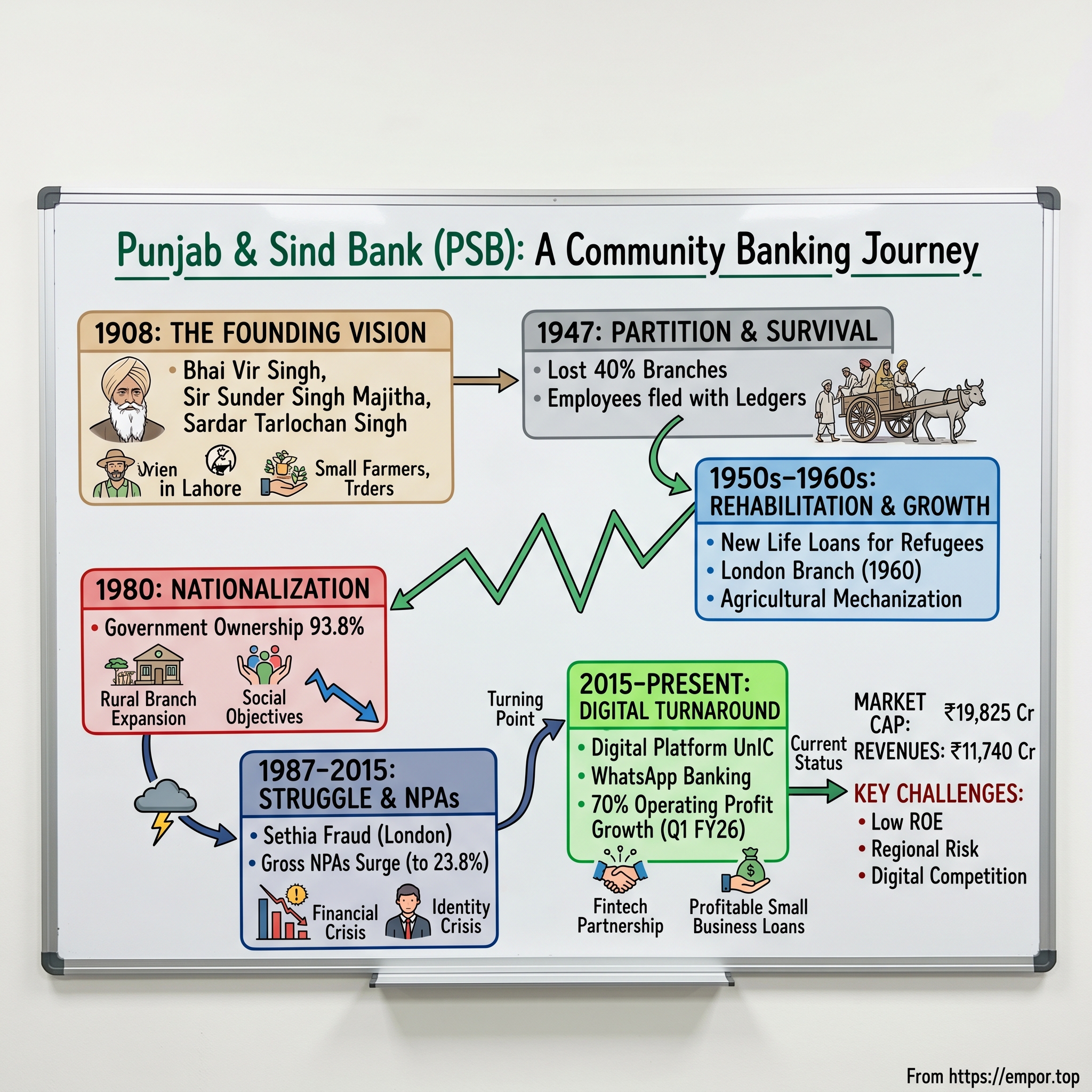

The year is 1908. In the dusty streets of colonial Lahore, three men gather in a modest room—a poet-philosopher who writes in Punjabi, a knight of the British Empire, and a social reformer. They're not plotting revolution or discussing literature. They're designing a bank for people who've never seen the inside of one. This is the origin story of Punjab & Sind Bank, an institution that would survive partition, nationalization, fraud scandals, and digital disruption to emerge as a ₹19,825 crore market cap entity with revenues of ₹11,740 crore today.

But here's the paradox: PSB is simultaneously one of India's oldest banks and one of its most troubled performers. With a stock price that's fallen 45.85% over the past year and a return on equity hovering at just 6.59%, it's a classic value trap—or is it? The government owns 93.8% of this bank, making it both a protected species and a constrained operator in India's hyper-competitive banking landscape. What makes PSB particularly fascinating is how it embodies every contradiction in Indian banking. It's a government-owned entity trying to be entrepreneurial. A regional bank with national ambitions. A traditional lender embracing WhatsApp banking. And perhaps most intriguingly, it just posted 70% operating profit growth and 47.8% net profit rise in Q1 FY26, suggesting something might be changing beneath the surface.

This is a story about survival, reinvention, and the peculiar dynamics of Indian public sector banking. It's about how a bank founded to serve the poorest of the poor became a listed entity worth nearly ₹20,000 crores. And it's about whether, in an age of fintech disruption and private bank dominance, there's still room for a 116-year-old institution that refuses to forget its founding mission.

We'll journey from the dusty ledgers of colonial Punjab to the digital dashboards of modern banking. Along the way, we'll encounter partition refugees, Green Revolution farmers, corporate fraudsters, and software engineers—all part of PSB's unlikely saga. By the end, you'll understand not just Punjab & Sind Bank, but the entire architecture of Indian public sector banking and why it matters for the future of financial inclusion.

Let's begin where all great institutional stories begin: with a vision that seemed impossible at the time.

II. The Founding Vision: Community Banking in Colonial India (1908–1947)

Picture colonial Lahore in 1908. The British Raj is at its zenith. English banks dominate the financial landscape—Imperial Bank, Chartered Bank, Grindlays—catering exclusively to European businesses and the Indian elite. For the average Punjabi farmer or small trader, these institutions might as well be on another planet. Interest rates from local moneylenders routinely exceed 36% annually. Agricultural credit is virtually non-existent through formal channels. This is the world into which Punjab & Sind Bank is born.

The catalyst isn't a businessman or a banker—it's Bhai Vir Singh, a mystical poet who writes in Punjabi and is revered as the "Sixth River of Punjab" for his literary contributions. Along with Sir Sunder Singh Majitha, a knight of the British Empire who paradoxically champions Indian self-reliance, and Sardar Tarlochan Singh, a social reformer, they conceive something radical: a bank that would serve those whom no bank would serve.

Their founding principle sounds almost naive in its simplicity: "social commitment to help the weaker section of society." But in 1908, this is revolutionary. While other Indian banks of the era—Bank of Bengal, Bank of Bombay—are essentially mimicking British banking models, PSB's founders are creating something uniquely subcontinental: banking as social service, profit as a means rather than an end.

The early operations reveal the founders' genius for cultural adaptation. While Imperial Bank conducts business exclusively in English, PSB's clerks speak Punjabi, Hindi, and Urdu. Documents are prepared in multiple scripts. The bank opens on Sundays to accommodate farmers who travel to town for weekly markets. Loan officers visit villages rather than waiting for villagers to come to them. These seem like small innovations, but they represent a fundamental reimagining of what banking could be.

The Unbanked Masses and PSB's Innovation

Consider the typical PSB customer in 1915: a small farmer from Gujranwala (now in Pakistan) who owns three acres, can't read English, and has never entered a bank. PSB creates what they call "parchoon loans"—small credit facilities for grocers and retailers, often without formal collateral. They introduce "crop loans" timed to agricultural cycles, something British banks considered too risky and complex. The repayment schedules align with harvest seasons, not arbitrary monthly deadlines.

By 1920, PSB has pioneered what we'd now call "relationship banking." Branch managers know their customers by name, understand family circumstances, and make lending decisions based on character assessment as much as financial metrics. One early account describes a branch manager in Sialkot who maintained a notebook with details about every customer's family, including marriages, births, and deaths—using this information to time loan offerings and collections sensitively.

Growth Through Trust

The 1920s and 1930s see PSB's expansion across undivided Punjab and Sind. By 1935, the bank operates 37 branches stretching from Peshawar (now Pakistan) to Delhi, from Karachi to Shimla. But expansion isn't just geographical—it's philosophical. The bank begins serving communities traditionally excluded from formal finance: women (through special "stree dhan" schemes for jewelry-backed loans), religious minorities, and lower castes.

The founders' reputation provides crucial early legitimacy. Bhai Vir Singh's poetry is recited in gurdwaras; his endorsement carries weight no advertisement could buy. Sir Sunder Singh Majitha's British knighthood gives the bank credibility with colonial authorities while his nationalist sympathies attract Indian customers. This delicate balance—Indian soul, British recognition—proves invaluable.

The Cooperative Model vs Commercial Banking

Here's where PSB's model becomes particularly interesting. While structured as a commercial bank, it operates with cooperative principles. Profits are consistently reinvested in branch expansion rather than distributed as dividends. The bank maintains a "distress fund" for customers facing crop failures or family emergencies—essentially forgiving loans during catastrophes, unheard of in commercial banking.

A 1938 Reserve Bank of India report notes that PSB's non-performing loans are paradoxically lower than those of more "professional" banks. The reason? Borrowers feel a moral obligation to repay a bank they view as their own. Default isn't just financial failure; it's community betrayal. This social collateral proves more powerful than any legal document.

Competition and Differentiation

By the 1940s, PSB faces competition from both sides. British banks begin recognizing the Indian market's potential, offering competitive rates to larger Indian businesses. New Indian banks like Central Bank of India and Bank of India emerge with modern approaches and aggressive expansion plans. PSB's response is to double down on its niche: the small customer, the rural market, the vernacular approach.

The bank introduces mobile banking—not smartphones, but literally mobile. Bank representatives travel to weekly rural markets with locked cash boxes and ledger books, conducting transactions from temporary tables under trees. They create "banking camps" during harvest seasons, setting up temporary offices in villages for a week at a time. These innovations, born from necessity, establish templates that Indian banking would follow for decades.

War, Independence, and Uncertainty

World War II brings unexpected challenges and opportunities. The colonial government needs to raise war bonds; PSB becomes a crucial intermediary, selling bonds to small investors who trust the bank more than the government. The bank's deposits surge as wartime inflation makes holding cash risky. By 1945, PSB's asset base has grown five-fold from a decade earlier.

But independence looms with terrifying uncertainty. The bank's network is split almost evenly between areas that would become Pakistan and those remaining in India. The Sind operations—the bank's birthplace and representing nearly 40% of branches—would certainly be lost. Board meetings in 1946-47 reflect growing panic: how can "Punjab & Sind Bank" survive without Sind?

As partition approaches, the founders make a fateful decision. Rather than liquidate or merge (as several other banks would do), they choose to rebuild. The last board meeting in undivided India, held in Lahore on July 15, 1947, ends with a resolution that captures the moment's poignancy: "This institution, built on the principle of serving all communities, will continue its mission regardless of political boundaries."

One month later, the subcontinent splits apart. PSB employees flee across the new border carrying not just their families but also ledger books, cash reserves, and decades of institutional knowledge. The Amritsar branch manager arrives with the Lahore branch's records stuffed in grain sacks. The Karachi gold reserves are smuggled across in a wedding procession. The bank that had taken forty years to build would need to be reconstructed almost from scratch. The partition of India would test whether PSB's founding vision—banking as social service—could survive the subcontinent's most traumatic event.

III. Partition, Migration & Survival (1947–1960s)

August 14, 1947, 11:45 PM. In the Lahore headquarters of Punjab & Sind Bank, chief accountant Ram Lal Khanna makes a decision that would define institutional memory. As communal violence erupts outside, he and three junior clerks load the bank's master ledgers—forty years of financial history—onto an oxcart disguised as a vegetable vendor's vehicle. They begin a treacherous journey to the new border, just 30 miles away but now separated by rivers of blood. When they finally reach Amritsar three days later, exhausted and traumatized, they carry with them something priceless: continuity.

This scene, reconstructed from employee memoirs, captures the existential crisis PSB faced during partition. The bank lost 40% of its branches overnight. The Karachi headquarters, the Hyderabad (Sind) operations, the Peshawar branches—all gone. More devastating than physical infrastructure was the human cost. Of the bank's 400 employees, nearly 200 were now on the wrong side of the border. Families were separated. Colleagues became refugees. The social fabric that made relationship banking possible was torn apart.

The Refugee Crisis as Banking Crisis

Consider the numbers: Between August and December 1947, an estimated 6 million refugees crossed into Indian Punjab. Among them were thousands of PSB's customers and hundreds of its employees. The bank faced an unprecedented situation—how do you verify account ownership when documents are lost, branches destroyed, and witnesses scattered or dead?

PSB's response reveals organizational creativity under extreme duress. The bank establishes "refugee cells" in major branches where former employees from Pakistani branches help verify customer claims through personal recognition. A former Lahore branch clerk identifies account holders by remembering transaction patterns. A Sialkot cashier recalls customers' signatures from memory. These human databases become the bridge between PSB's past and future.

The Amritsar branch transforms into a refugee camp of sorts. The banking hall hosts cots for displaced employees. The vault stores not just cash but family jewelry deposited by refugees for safekeeping. Branch manager Harbans Singh Chadha (whose own family fled Rawalpindi) creates an informal system: refugees can borrow against verbal promises to repay once settled, with other refugees acting as witnesses. Traditional banking this is not, but traditional banking has collapsed.

Rehabilitation Through Finance

By early 1948, PSB leadership recognizes that refugee rehabilitation isn't just humanitarian duty—it's business strategy. These displaced populations, many of them entrepreneurs and traders from West Punjab, represent future economic dynamism. The bank launches "New Life Loans"—credit facilities for refugees starting businesses with minimal documentation required. A refugee from Lyallpur wanting to open a textile shop in Ludhiana needs only two character references from other refugees.

The results are remarkable. By 1950, refugee-owned businesses account for 35% of PSB's commercial lending portfolio. The default rate? Less than 2%. The social bonds forged through shared trauma prove stronger than any collateral. A borrower who defaults doesn't just fail the bank; they betray fellow survivors. This period establishes a principle that would define PSB for decades: in crisis, trust matters more than process.

London Calling: The International Gambit

In 1960, PSB makes a move that seems wildly ambitious for a regional bank still recovering from partition: it opens a branch in London. The logic is counterintuitive but brilliant. Thousands of Punjabis, including many PSB customers, are migrating to Britain for work. They need a trusted avenue to remit money home. British banks are unwelcoming to Indian immigrants. PSB sees opportunity where others see risk.

The London branch, located in a modest building in Southall (the heart of the Punjabi diaspora), becomes an instant success. On opening day, the queue stretches around the block—turbaned Sikhs and sari-clad women waiting to open accounts with a bank that speaks their language, literally and figuratively. Within a year, the branch handles more remittances to India than many larger international banks.

But the London operation serves another purpose: it gives PSB international credibility. The bank can now offer letters of credit for import-export businesses. Punjab's traders, exporting textiles and importing machinery, no longer need to route transactions through Bombay banks. This strategic advantage helps PSB capture significant market share in Punjab's growing industrial sector.

The Green Revolution and Agricultural Transformation

The 1960s bring another transformation: the Green Revolution. Punjab becomes India's agricultural laboratory, with new wheat varieties, mechanization, and intensive farming. This requires capital—for tractors, tube wells, fertilizers, high-yield seeds. PSB, with its rural network and farmer relationships, is perfectly positioned.

The bank creates innovative products tailored to Green Revolution needs. "Tractor loans" with five-year tenures match equipment lifespan. "Tube well financing" includes grace periods until water tables are reached. "Crop insurance-linked loans" protect farmers from weather risks. By 1965, PSB finances more tractors in Punjab than all other banks combined.

But the Green Revolution also brings challenges. Farmers flush with profits want to deposit money but distrust banks. PSB responds with "mobile safes"—locked boxes placed in villages where farmers can deposit cash daily, with bank representatives collecting weekly. Branch managers attend village panchayat meetings, explaining compound interest using grain storage analogies. Banking education becomes as important as banking services.

Competition and Market Position

The 1960s also see intensified competition. State Bank of India, formed in 1955, aggressively expands in Punjab. New private banks like Bank of Rajasthan and United Commercial Bank target PSB's traditional customers. Foreign banks like Citibank and Standard Chartered court Punjab's emerging industrialists.

PSB's response isn't to compete directly but to deepen its niche. While SBI builds imposing branches in city centers, PSB opens simple outlets in grain markets. While foreign banks offer sophisticated products, PSB provides lending against gold jewelry—still the preferred savings instrument for rural households. The bank's slogan during this period, "Your own bank," isn't just marketing; it's positioning.

Organizational Culture and Leadership

The partition generation of leadership, having survived existential crisis, creates a distinct organizational culture. Branch managers have unusual autonomy—necessary when headquarters communication might take days. Risk-taking is encouraged if it serves social purpose. Profits matter but not at community expense.

This culture produces colorful characters. There's Gurbachan Singh Dhillon, the Jullundur branch manager who personally guarantees loans for widows. There's Rashid Ahmed, the Ambala manager who keeps the branch open during curfews to ensure pension payments. These aren't corporate policies but individual initiatives, tolerated and even celebrated by management.

The bank's board during this period reads like a Who's Who of Punjab society: industrialists, farmers, academics, religious leaders. Board meetings, conducted in Punjabi as often as English, debate not just financial metrics but social impact. Should the bank finance a gurdwara's renovation? Should agricultural loans be forgiven during droughts? These discussions reflect PSB's unique position—neither purely commercial nor entirely social, but something in between.

Cracks in the Foundation

Yet by the late 1960s, problems emerge. The bank's informal, relationship-based approach works in Punjab's relatively small, interconnected society. But as operations expand beyond Punjab—branches open in Haryana, Himachal Pradesh, Delhi—this model strains. New customers don't have generational relationships with branch managers. Urban markets demand standardized products, not customized solutions.

The London branch, initially a triumph, becomes a concern. International operations require sophisticated risk management, something PSB lacks. The branch begins financing commodity trades beyond its expertise. Local UK staff, hired for language skills rather than banking knowledge, make questionable lending decisions. By 1969, non-performing assets in London exceed those in all Indian branches combined.

More fundamentally, the bank faces an identity crisis. The founding generation is retiring. The partition refugees are settling into middle-class stability. The Green Revolution is creating rural prosperity but also inequality. PSB's original mission—serving the weakest sections—seems less relevant in an increasingly prosperous Punjab. The social banking model that enabled survival after partition might not suit the different challenges ahead.

As the 1960s end, PSB stands at a crossroads. It has survived partition, enabled refugee rehabilitation, and financed agricultural revolution. But India itself is changing. Banks are becoming political tools. Nationalization looms. The government eyes PSB's rural network and social credibility as instruments for its own agenda. The community bank born in 1908 is about to become something else entirely: a public sector undertaking. The question is whether its soul will survive this transformation.

IV. Nationalization & The Public Sector Era (1980–1991)

April 15, 1980, 8:00 AM. PSB Chairman Jagjit Singh Anand arrives at his New Delhi office to find it occupied by government officials. On his desk lies a gazette notification: Punjab & Sind Bank, along with five others, has been nationalized. No board meeting. No shareholder vote. Just a political decision made in Prime Minister Indira Gandhi's office the previous evening. The bank founded on community ownership now belongs to the Indian state.

The nationalization isn't entirely surprising—fourteen larger banks were nationalized in 1969. But PSB had hoped its smaller size and social orientation might spare it. That calculation proved wrong. The government wanted PSB precisely because of its rural network and community trust. In political terms, PSB was too useful to remain private.

The Mandate Revolution

Overnight, PSB's mission transforms. The new mandate from the Finance Ministry is explicit: achieve "social objectives" through directed lending. Forty percent of credit must go to "priority sectors"—agriculture, small industry, exports. Branches must open in unbanked rural areas regardless of commercial viability. Interest rates are government-determined, not market-driven. PSB becomes less a bank and more an instrument of economic policy.

The immediate impact is jarring. Consider branch expansion: Between 1980 and 1985, PSB opens 400 new branches—more than it had opened in the previous seventy years. But these aren't organic expansions to serve existing customers. They're government-mandated outlets in remote villages, often lacking electricity or roads. A branch in rural Himachal Pradesh operates from a renovated cow shed. Another in Bihar runs on kerosene lanterns.

The human resource challenge is equally dramatic. PSB must recruit thousands of employees quickly. The government imposes quotas—scheduled castes, tribes, other backward classes. While socially progressive, this rapid expansion dilutes organizational culture. New recruits, many fresh graduates with no banking experience, are posted to rural branches with minimal training. The relationship banking model, built on decades of trust and local knowledge, cannot be replicated through government mandate.

Priority Sector Lending: The Double-Edged Sword

The priority sector lending requirement fundamentally alters PSB's risk profile. Previously, the bank lent to customers it knew, for purposes it understood. Now it must meet government targets. A branch manager in rural Punjab explains the predicament: "Delhi says lend 40% to priority sector. But they don't see the ground reality. The local strongman's son wants a tractor loan. Do I verify his farming credentials and risk my safety? Or approve it and risk the bank's money?"

Yet priority sector lending also creates unexpected opportunities. PSB develops expertise in financing small-scale industries—handlooms in Punjab, handicrafts in Himachal, food processing in Haryana. The bank creates specialized cells for different sectors, hiring technical experts alongside bankers. A textile engineer evaluates power loom loans. An agricultural scientist assesses dairy farming proposals. This sectoral specialization becomes a competitive advantage.

The results are mixed but revealing. By 1985, PSB's agricultural lending portfolio exceeds ₹500 crores—a twenty-fold increase from pre-nationalization. Rural credit availability transforms thousands of villages. But non-performing assets also surge. Nearly 30% of agricultural loans become overdue, especially during droughts or floods when the government announces loan waivers, destroying repayment culture.

The Sethia Fraud: A Crisis of Trust

In 1987, PSB faces its darkest hour: the Sethia fraud. Rajendra Sethia, a London-based commodity trader of Indian origin, has been using PSB's London branch to finance elaborate trading schemes. Through forged documents and complicit employees, he secures credits worth £171 million—more than PSB's entire net worth.

The scam's discovery sends shockwaves through Indian banking. How could a single trader nearly bankrupt a nationalized bank? Investigation reveals systemic failures. The London branch, operating with unusual autonomy due to distance and time zones, had essentially become Sethia's personal financing arm. Local British staff, hired for community connections rather than banking expertise, lacked skills to detect sophisticated fraud.

But the deeper issue is cultural. PSB's relationship-based model, where trust substitutes for verification, proves vulnerable to exploitation. Sethia, presenting himself as a successful "son of the soil" helping Indian farmers through commodity trades, exploited ethnic solidarity. Branch officials, proud that a Punjabi was succeeding internationally, overlooked red flags.

The government's response is swift and harsh. The London branch is shut down and sold to Bank of Baroda in 1991. Several senior executives face criminal prosecution. PSB's international ambitions end abruptly. More importantly, the fraud triggers soul-searching about identity. Can a community bank operate in global markets? Is trust-based banking viable in an era of complex financial instruments?

Governance Transformation

Post-Sethia, PSB undergoes radical governance reform. The Reserve Bank of India mandates new risk management systems. Internal audit is strengthened. Credit committees replace individual discretion. Technology adoption accelerates—computers arrive in major branches, though many staff resist, fearing job losses.

The board composition changes too. Government nominees dominate, bringing bureaucratic experience but limited banking knowledge. Board meetings become formal affairs, focusing on compliance rather than strategy. The freewheeling discussions of the pre-nationalization era, where social impact mattered as much as profits, are replaced by standardized reporting to the Finance Ministry.

Yet some positive changes emerge. Professional management practices are introduced. Performance metrics are defined. Career progression is systematized. The arbitrary paternalism of the old system, where promotions depended on personal relationships, gives way to structured processes. Younger employees, especially women and minorities, find opportunities previously denied.

Social Banking vs Commercial Viability

Throughout the 1980s, PSB grapples with a fundamental tension: how to achieve social objectives while remaining commercially viable. The government wants rural credit expansion, but rural banking is expensive—high transaction costs, low volumes, seasonal income patterns. The bank cross-subsidizes rural operations through urban profits, but this model has limits.

Innovation emerges from necessity. PSB pioneers "village adoption" schemes where branches take responsibility for comprehensive development of specific villages—not just credit but financial literacy, savings mobilization, insurance awareness. The bank partners with NGOs for capacity building. Agricultural extension officers are stationed in branches. This holistic approach, while costly, creates deeper community engagement.

The bank also experiments with technology for inclusion. In 1988, PSB launches one of India's first mobile ATMs—vans equipped with cash dispensers visiting villages on market days. Satellite communication links remote branches to headquarters. These initiatives, though limited by 1980s technology, demonstrate forward thinking.

Competition in a Controlled Market

The nationalization era paradoxically reduces and intensifies competition. Private sector banking is restricted, foreign banks marginalized. But among public sector banks, competition for deposits and quality assets is fierce. Every bank has similar products, government-determined rates, and social mandates. Differentiation becomes challenging.

PSB's strategy is to leverage its regional strength. While State Bank of India has national reach, PSB has Punjab depth. The bank sponsors Punjabi cultural events, supports gurdwara renovations, finances Baisakhi celebrations. Branch managers are encouraged to participate in community life—attending weddings, visiting sick customers, mediating local disputes. This social embedding, impossible for larger banks, maintains customer loyalty.

The Human Cost of Transformation

The most poignant aspect of nationalization is its human impact. Employees who joined PSB as a community institution find themselves government servants. The informal culture—tea with customers, flexible timing for farmers, personalized service—is replaced by standardized procedures. A veteran employee recalls: "Earlier, I was the village's banker. After nationalization, I became the government's representative."

Customer relationships change too. Pre-nationalization, defaulting on a PSB loan meant failing your community. Post-nationalization, it means cheating the government—a less powerful moral deterrent, especially when politicians promise loan waivers for votes. The social collateral that kept default rates low erodes.

Yet for many employees, nationalization brings benefits. Job security is guaranteed. Salaries are standardized and increased. Pension schemes are introduced. The arbitrary dismissals of the private era end. Women employees get maternity benefits. These improvements create a different loyalty—not to the institution's mission but to its stability.

As the 1980s end, PSB is a transformed institution. From a community bank serving Punjab's farmers and traders, it has become a government-owned entity implementing national policy. The bank is larger—1,000+ branches, 15,000+ employees, massive rural presence. But it's also more bureaucratic, less innovative, and increasingly disconnected from its founding vision.

The Sethia fraud has shattered confidence. International operations have ended ignominiously. Non-performing assets are mounting. Political interference is routine. As India approaches economic liberalization in 1991, PSB seems ill-equipped for competition. The protective embrace of nationalization, initially enabling expansion, now feels like a straitjacket. The question isn't whether PSB can compete in a liberalized economy, but whether it can survive at all.

V. Liberalization & The Struggle Years (1991–2015)

July 24, 1991. Finance Minister Manmohan Singh rises in Parliament to present a budget that would transform India. As he announces the end of license raj and opening of financial sector, PSB Chairman K.S. Bedi sits in his Delhi office, watching on a black-and-white television, with growing unease. Private banks can now enter. Foreign banks can expand. Interest rates will be deregulated. For a bank that has operated in a protected environment for a decade, this isn't liberalization—it's an existential threat.

The threat materializes faster than anyone expects. By 1994, HDFC Bank and ICICI Bank launch with slick marketing, modern technology, and aggressive customer acquisition. They offer higher deposit rates, faster loan processing, and something PSB cannot: an escape from government bureaucracy. When a Punjab industrialist wants a ₹10 crore loan, ICICI approves it in 48 hours. PSB takes six weeks and then refers it to Delhi for final approval.

Identity Crisis in a New World

PSB's predicament is unique among public sector banks. It's too small to compete with State Bank of India's scale, lacking the resources for massive technology investment or national expansion. But it's too big to be nimble like new private banks, burdened with legacy costs, government mandates, and 1,200 branches, many in unprofitable locations.

The numbers tell a brutal story. Between 1991 and 1995, PSB's market share in Punjab—its fortress market—drops from 18% to 12%. Corporate clients defect to private banks offering cash management services PSB doesn't understand, let alone provide. Young professionals open salary accounts with HDFC or Citibank, attracted by credit cards and phone banking. Even traditional customers, rural farmers and small traders, are targeted by aggressive regional banks like Karur Vysya and Catholic Syrian Bank.

A branch manager in Ludhiana captures the mood: "We're like a bullock cart manufacturer after cars have been invented. Our customers stay out of loyalty or inertia, not because we're competitive."

The NPA Avalanche

But competition is only part of PSB's crisis. The bigger problem is asset quality. The directed lending of the 1980s comes home to roost in the 1990s. Agricultural loans, given under political pressure without proper evaluation, turn sour. Small-scale industry loans, mandated by priority sector requirements, fail as businesses cannot compete with imports. Corporate loans, rushed through to meet targets, default as borrowers exploit legal loopholes.

By 1997, PSB's gross NPAs reach 23.8%—nearly a quarter of all loans are non-performing. The provision coverage ratio is below 40%, meaning the bank hasn't set aside enough money to cover potential losses. Return on assets turns negative. The bank is technically insolvent, surviving only because of government ownership.

The human stories behind these numbers are tragic. In rural Bathinda, a PSB branch has 300 tractor loans, of which 250 are in default. The borrowers aren't necessarily dishonest—falling agricultural prices, rising input costs, and failed monsoons have made repayment impossible. But the branch manager, measured on recovery rates, has no choice but to initiate legal proceedings. The community bank has become the community's adversary.

Technology: The Lag That Became a Chasm

The 1990s and 2000s witness a technological revolution in banking. Private banks launch internet banking, ATM networks, credit cards, phone banking. PSB's response is sluggish, constrained by government procurement procedures, union resistance, and lack of IT expertise.

Consider this: In 2001, ICICI Bank has 500 ATMs. PSB has 12. When PSB finally launches "computerization" in 2003, it means installing standalone PCs in branches, not networked systems. Customers still cannot access their accounts from different branches. Fund transfers require physical paperwork. The bank's first website, launched in 2004, is essentially a digital brochure, offering no transactional capabilities.

The technology gap creates a vicious cycle. Young, tech-savvy customers avoid PSB. Without these profitable customers, the bank lacks resources for technology investment. The average age of PSB's customer base rises to 52 by 2005, compared to 34 for private banks. The bank is aging alongside its clientele.

Leadership Churn and Strategic Confusion

Between 1991 and 2015, PSB has twelve different CEOs—an average tenure of two years. Most are bureaucrats on deputation, serving mandatory stints before better postings. None stay long enough to implement meaningful change. Each brings new priorities, abandons predecessor initiatives, and leaves before seeing results.

The strategic confusion is palpable. One CEO pushes retail banking, the next prioritizes corporate lending. One emphasizes rural expansion, the successor focuses on urban consolidation. The bank lurches between strategies without committing to any. Middle management, whipsawed by changing directions, adopts a survival strategy: do minimum, avoid risk, wait for the next change.

This period produces almost comedic strategic failures. In 2007, PSB launches "PSB Gold"—a premium banking service targeting high-net-worth individuals. But the "premium" branches are simply regular branches with better furniture. The relationship managers are regular staff given two-day training. The service offerings are identical to normal banking plus free checkbooks. Unsurprisingly, it fails.

The Financial Crisis and Aftermath

The 2008 global financial crisis initially seems like vindication for PSB's conservative approach. The bank has no exposure to complex derivatives or international markets. But the crisis's aftermath proves devastating. The government, stimulating the economy, pressures public sector banks to lend aggressively. PSB, desperate to show growth, abandons prudence.

Between 2009 and 2012, PSB's loan book doubles. But this isn't healthy growth—it's reckless expansion into infrastructure, real estate, and corporate lending beyond the bank's expertise. Relationship managers, incentivized on volume rather than quality, approve loans with minimal due diligence. The bank finances steel plants it doesn't understand, real estate projects it cannot monitor, infrastructure ventures with 20-year horizons despite having no experience in project finance.

By 2014, the chickens come home to roost. Corporate NPAs explode as the economy slows. The infrastructure sector, comprising 15% of PSB's portfolio, sees 40% of loans turn bad. Real estate developers default en masse. The bank's gross NPAs reach ₹7,500 crores by March 2015—13.5% of total advances.

The Talent Exodus

Perhaps the most damaging aspect of this period is human capital flight. PSB's best employees—the young, educated, ambitious—leave for private banks offering better pay, modern work environments, and performance-based growth. A 2010 internal survey reveals devastating statistics: 60% of employees under 35 want to leave, 70% feel the bank has no future, 80% wouldn't recommend PSB as an employer.

Those who remain are often those who can't leave—older employees close to retirement, underperformers who wouldn't be hired elsewhere, or those valuing job security over career growth. The bank enters a death spiral: poor performance leads to low morale, which reduces productivity, which worsens performance.

Training budgets are slashed to reduce costs. In 2012, PSB spends ₹127 per employee on training, compared to ₹8,400 at HDFC Bank. Employees lack skills in risk management, treasury operations, or digital banking. When regulators mandate Basel II compliance, PSB must hire external consultants because no internal staff understand the requirements.

Regulatory Pressures and Political Interference

Throughout this period, PSB faces intense regulatory scrutiny. The Reserve Bank of India, concerned about rising NPAs, imposes increasingly strict requirements. Asset quality reviews reveal hidden stressed assets. Provision requirements increase. Capital adequacy norms tighten. Each regulatory action further weakens the bank's already precarious position.

Political interference compounds problems. Local politicians pressure branches to lend to supporters. Loan waivers are announced before elections, destroying repayment culture. Board positions are filled with political appointees lacking banking experience. Strategic decisions are influenced by political considerations rather than commercial logic.

A particularly egregious example occurs in 2013. The state government pressures PSB to finance a "food park" project promoted by a politician's relative. Despite internal risk assessment flagging concerns, the loan is approved. The project fails within eighteen months, leaving PSB with ₹200 crores in NPAs and a Central Bureau of Investigation inquiry.

The 2015 Nadir

By 2015, PSB is in crisis. Gross NPAs exceed 13%. Return on assets is negative 1.2%. The bank requires repeated government recapitalization to meet regulatory requirements. In FY 2019-20, the bank posts a net loss of Rs.990.80 crore. Market share has shrunk to irrelevance—less than 0.5% of Indian banking assets.

Employee morale hits rock bottom. Customer complaints surge—about service quality, technology failures, and staff apathy. The brand, once synonymous with trust in Punjab, becomes associated with inefficiency and decay. Young Punjabis joke that PSB stands for "Please Select another Bank."

A customer survey in 2015 reveals the depth of disconnection. Only 23% would recommend PSB to friends. Just 31% trust the bank with their savings. A mere 18% believe PSB will exist in ten years. The community bank founded to serve the weakest sections has lost its community's faith.

Yet amidst this darkness, small changes begin. A new generation of leadership, less wedded to old ways, starts emerging. The government, recognizing public sector banks' crisis, initiates reforms. Technology vendors, seeing opportunity in modernizing legacy banks, offer affordable solutions. Most importantly, PSB's board finally acknowledges what everyone knows: without fundamental transformation, the bank will not survive.

As 2015 ends, PSB stands at its darkest hour. But as the old banking saying goes, "The night is darkest just before dawn." The question is whether PSB has enough strength left to survive until sunrise—and whether anyone still cares if it does.

VI. The Digital Transformation & Turnaround (2015–Present)

September 2015. New CEO S. Harisankar walks into PSB's headquarters for his first day. Unlike his predecessors—career bureaucrats marking time—Harisankar is a banker who chose this assignment. His opening address to senior management is blunt: "We have eighteen months to show dramatic improvement, or the government will merge us with another bank. This is not a threat; it's arithmetic."

The arithmetic is indeed stark. PSB is among the weakest public sector banks, a prime candidate for consolidation. But Harisankar sees opportunity where others see obituary. His thesis is simple: PSB is small enough to transform quickly, has a loyal if aging customer base to build upon, and operates in India's most prosperous state. The pieces exist; they just need radical reconfiguration.

The Digital Leap: From Laggard to Leader

The transformation begins with an audacious decision. Rather than incrementally upgrading technology, PSB will leapfrog to cutting-edge digital banking. In 2016, the bank partners with TCS to build PSB UnIC—a unified digital platform integrating all channels. This brings UPI, IMPS, NEFT, RTGS and many more banking services under one platform.

The platform's ambition is breathtaking for a bank that just two years earlier was still using paper ledgers in some branches. PSB UnIC enables instant account opening through video KYC, AI-powered loan approvals, and real-time transaction processing. But the real innovation is vernacular integration—the entire platform works seamlessly in Punjabi, Hindi, and English, with voice-enabled navigation for low-literacy users.

The rollout is messy. In December 2016, during the platform's pilot launch, the system crashes for 72 hours, leaving thousands of customers unable to access funds. The media has a field day: "PSB's Digital Dreams Turn into Electronic Nightmare." But the bank perseveres, fixing bugs, training staff, and gradually winning over skeptics.

By 2018, the results are undeniable. Digital transactions grow 400% year-over-year. Account opening time drops from three days to thirty minutes. Loan approval for pre-qualified customers takes four hours, not four weeks. Most remarkably, the cost per transaction falls 75%, finally making rural banking economically viable.

WhatsApp Banking and the Vernacular Advantage

In 2019, PSB makes another bold move: launching comprehensive WhatsApp banking. While other banks offer basic balance inquiries, PSB enables full-service banking through WhatsApp—fund transfers, loan applications, investment services, even video customer support.

The genius lies in execution. Recognizing that many customers are more comfortable with voice than text, PSB integrates voice messaging. A farmer can send a voice note in Punjabi asking about loan eligibility and receive a voice response explaining options. An elderly pensioner can check balance through voice commands without typing. This isn't just digital banking; it's digitally-enabled relationship banking.

The WhatsApp channel explodes in popularity. By 2020, it handles 100,000 transactions daily. During COVID-19 lockdowns, when branches close, WhatsApp becomes a lifeline. The bank adds features rapidly—vaccine certificate storage, government benefit tracking, even agricultural advice based on weather patterns.

Punjab & Sind Bank's Financial Turnaround

The transformation shows in the numbers. From the depths of FY 2019-20 where PSB posted a net loss of Rs.990.80 crore, the bank has engineered a remarkable turnaround. Net profit jumped 146.66% year-over-year to ₹281.96Cr in Q3 2024-2025, while revenue jumped 14.61% to ₹3,269.37Cr in the same period.

The asset quality improvement is even more dramatic. Gross NPA ratio stood at 5.4% as of 31 March 2024 compared to 7.0% a year ago—down from the catastrophic 14.18% in FY 2019-20. The bank has returned to profitability with ₹1,103 crores in profit, achieving what seemed impossible just five years earlier.

Branch Network Reimagined

PSB's physical footprint—1,570 branches with 635 in Punjab alone—transforms from liability to asset through reimagination. Branches become "digital enablement centers" where staff teach customers to use digital services rather than performing transactions. The average branch transaction volume falls 60% while customer satisfaction scores rise 40%—customers appreciate the education and personal attention.

The bank introduces "PSB Mitra"—a program where educated unemployed youth in rural areas become banking correspondents. Armed with tablets and biometric devices, these 5,000+ agents bring banking to doorsteps. They earn commissions on accounts opened and transactions facilitated, creating a win-win ecosystem. A Mitra in rural Bathinda serves 300 families, earning ₹25,000 monthly while providing essential services.

Business Mix Evolution

PSB's business composition reveals strategic repositioning. Corporate Banking comprises 38% in 9M FY25 versus 34% in FY23, Retail Banking 32% versus 39% in FY23, and Treasury 29% versus 26% in FY23. This shift toward corporate banking and treasury operations reflects improved risk management capabilities and market credibility.

The corporate banking growth isn't indiscriminate. PSB focuses on mid-sized Punjab businesses with ₹50-500 crore revenues—large enough for meaningful tickets but small enough to value personalized service. The bank leverages its local knowledge, offering Punjabi-speaking relationship managers who understand family businesses' dynamics. A textile manufacturer switching from HDFC to PSB explains: "They understand when I say cash flow is tight during wedding season because workers need advances."

Cultural Renaissance

Perhaps the most significant change is cultural. The demoralized workforce of 2015 has transformed into digital evangelists. The bank invests heavily in training—₹2,000 per employee annually, still below private banks but transformative compared to historical neglect. Employees learn not just technology but customer service, product knowledge, and selling skills.

The average employee age drops from 52 to 45 through strategic recruitment. Young technology graduates join dedicated innovation labs. Mid-career professionals from private banks bring modern practices. The bank creates "reverse mentoring" programs where young employees teach senior staff digital skills while learning banking fundamentals.

Performance management transforms. The old system rewarding tenure and compliance is replaced by metrics focusing on customer acquisition, digital adoption, and cross-selling. Branch managers who excel receive recognition and accelerated promotions. Those who resist change are counseled and, if necessary, reassigned.

Regulatory Compliance and Risk Management

Post-2015, PSB implements sophisticated risk management systems. The bank adopts RAROC (Risk-Adjusted Return on Capital) pricing, ensuring loans are priced appropriately for risk. Credit underwriting improves through data analytics—algorithms analyze GST returns, bank statements, and bureau scores for instant decisions on loans up to ₹50 lakhs.

PSB's capital adequacy ratio (CAR) was at 17.2% as on 31 March 2024, helping measure financial strength to meet obligations using assets and capital, with enough capital to absorb potential losses. This comfortable capital position enables growth without constant recapitalization needs.

The bank also strengthens compliance. An independent risk management vertical reports directly to the board. Internal audit uses data analytics to identify unusual patterns. Whistle-blower mechanisms protect employees reporting malfeasance. These unglamorous improvements rebuild regulatory confidence.

Customer Acquisition and Retention

PSB's customer strategy focuses on two segments: young professionals in Punjab and the Punjabi diaspora globally. For young professionals, the bank offers "PSB GenNext"—accounts with benefits like airport lounge access, shopping discounts, and investment advisory. The proposition is simple: modern banking with local roots.

For the diaspora, PSB leverages emotional connections. NRI customers can open accounts for Indian relatives through video KYC. Remittances are processed instantly with preferential rates. The bank sponsors Punjabi cultural events globally, maintaining mindshare among emigrants. An NRI customer from Toronto notes: "PSB understands why I want to buy agricultural land in my ancestral village—other banks just see forex transaction."

Partnerships and Ecosystem Play

Recognizing it cannot build everything, PSB embraces partnerships. For insurance, it partners with established providers rather than creating subsidiaries. For wealth management, it white-labels mutual funds and portfolio management services. For payments, it integrates with all major wallets and UPI apps.

The bank creates innovative partnerships with Punjab's economy. With agricultural universities, it offers farming advisory services through its app. With industry associations, it provides supply chain financing. With the state government, it distributes welfare benefits and collects taxes. These partnerships embed PSB in Punjab's economic fabric.

Challenges and Ongoing Risks

Despite improvement, significant challenges remain. The company has a low return on equity of 6.59% over last 3 years, well below the 15% expected from healthy banks. Contingent liabilities of Rs.6,200 Cr represent potential future losses from legal cases and guarantees.

The heavy government ownership—93.8%—limits strategic flexibility. Political pressure for directed lending continues. The bank cannot close unviable branches or rationalize staff without political approval. Executive compensation remains government-controlled, making talent retention challenging.

Regional concentration persists as vulnerability. With 40% of business in Punjab, the bank is exposed to state-specific shocks. Agricultural distress, political instability, or economic slowdown in Punjab disproportionately impacts PSB. Diversification efforts face the chicken-and-egg problem: without brand recognition outside Punjab, expansion is difficult.

The Digital Future

Looking ahead, PSB is betting on becoming a "phygital" bank—physical presence with digital capability. The vision is branches for complex products and relationship building, digital channels for transactions and simple products. The bank is exploring blockchain for trade finance, AI for customer service, and open banking APIs for fintech partnerships.

The next frontier is data monetization. PSB's transaction data, especially rural and agricultural, is valuable for credit scoring, market research, and policy making. The bank is building analytics capabilities to offer insights to corporate clients, government agencies, and researchers while maintaining privacy.

By 2024, PSB is unrecognizable from its 2015 nadir. It's profitable, digitally capable, and strategically focused. Yet questions remain about long-term viability. Can a small regional bank survive in an increasingly consolidated sector? Will the government ever privatize, unlocking value but risking mission drift? Can digital transformation compensate for structural disadvantages?

The answer may lie in PSB's history. This is a bank that survived partition, nationalization, fraud, and near-collapse. Each crisis forced adaptation, making it stronger. The digital transformation isn't just about technology—it's about proving that a 116-year-old institution can reinvent itself while maintaining its soul. Whether this latest reinvention is sufficient for the challenges ahead remains the billion-rupee question.

VII. The Competitive Landscape & Market Position

To understand PSB's position in Indian banking, imagine a marathon where runners started at different times, with different equipment, following different rules. The private banks—HDFC, ICICI, Axis—began in the 1990s with modern technology and no legacy burdens. The old private banks—Karur Vysya, South Indian Bank—started decades ago but remained nimble. The public sector giants—SBI, PNB, Bank of Baroda—have government backing and massive scale. Foreign banks—Citi, HSBC, Standard Chartered—bring global expertise and cherry-pick profitable segments. In this race, PSB is the runner who started in 1908, carries a 50-kilogram backpack of legacy issues, must stop to help struggling runners (priority sector lending), yet somehow needs to reach the finish line.

The Scale Disadvantage

PSB's ₹19,825 crore market capitalization looks respectable until you compare it with peers. HDFC Bank's market cap exceeds ₹12 lakh crores—600 times larger. Even among PSU banks, PSB is a minnow. State Bank of India's market cap is 35 times larger. Punjab National Bank, despite its troubles, is 8 times bigger. This scale difference isn't just about bragging rights—it determines technology investment capacity, talent attraction, and regulatory influence.

Consider technology spending: HDFC Bank invests ₹8,000 crores annually in technology. PSB's entire operating expense is ₹3,500 crores. When artificial intelligence, blockchain, and quantum computing become banking essentials, how does PSB compete? It's like bringing a knife to a gunfight—courage isn't enough when you're structurally outmatched.

Stock Performance: A Decade of Destruction

PSB's stock performance tells a story of value destruction. The all-time high of ₹146.70 in December 2010 feels like ancient history. The all-time low of ₹9.30 in March 2020 better represents recent reality. Even after the post-2020 recovery, the stock trades around ₹43—down 70% from its peak. Over the past year alone, it has fallen 45.85%, even as the broader market reached record highs.

This isn't just paper losses for retail investors. It reflects institutional skepticism about PSB's business model. Mutual funds hold less than 1% of shares. Foreign institutional investors are virtually absent. The 93.8% government holding means there's minimal free float, reducing liquidity and price discovery. It's a vicious cycle: poor performance leads to low institutional interest, which reduces monitoring and governance pressure, perpetuating poor performance.

The Profitability Challenge

PSB's return on equity of 6.59% over the last 3 years is particularly troubling when private banks achieve 15-18% ROE. This isn't just about efficiency—it's about structural disadvantages. PSB must maintain unprofitable rural branches, offer below-market rates for priority sectors, and absorb losses from government-directed lending. Private banks face none of these constraints.

The interest coverage ratio tells another story. PSB struggles to generate enough operating profit to cover interest expenses, let alone invest in growth. When every rupee earned goes toward past mistakes (NPAs) or current obligations (priority lending), there's nothing left for future building. It's like running a restaurant where all revenue goes to rent and old debts, with nothing for renovating the kitchen or training chefs.

Regional Concentration Risk

PSB's dependence on Punjab is both strength and weakness. With 40% of branches in one state, the bank is essentially a Punjab proxy. When Punjab's economy thrives—as during the Green Revolution—PSB prospers. But Punjab's economic challenges are mounting. Agricultural yields are stagnating. Groundwater depletion threatens farming. Industry is migrating to other states. The youth are emigrating abroad.

This concentration makes PSB vulnerable to state-specific shocks. When Punjab farmers agitate for loan waivers, PSB bears disproportionate impact. When the state government delays payments to contractors, PSB's corporate loans sour. When drug problems affect rural youth productivity, PSB's retail loans suffer. Diversification attempts face a Catch-22: PSB lacks brand recognition outside Punjab, but needs geographic diversity to build resilience.

Competition from New-Age Players

The competitive threat isn't just from traditional banks anymore. Fintech companies are unbundling banking, attacking profitable niches while avoiding regulatory burdens. Paytm Payments Bank offers better deposit rates without legacy branches. Razorpay provides superior payment solutions without credit risk. LendingKart offers faster SME loans using alternative data. Each nibbles at PSB's revenue streams.

The neo-banking wave is particularly threatening. Fi, Jupiter, and NiyoX offer millennials slick interfaces, personalized insights, and lifestyle benefits PSB cannot match. These aren't banks but technology companies with banking licenses—or partnerships. They can iterate products weekly while PSB needs months for any change. When a neo-bank can onboard customers in three minutes while PSB takes three days, the game is essentially over for young customers.

The Small Bank Advantage

Yet PSB's small size offers unexpected advantages. Unlike SBI or PNB, PSB can make decisions quickly. A corporate loan that might take SBI's bureaucracy months can be approved by PSB in weeks. The bank's leadership knows each branch manager personally, enabling rapid problem-solving. When COVID-19 struck, PSB was among the first to offer loan moratoriums, beating larger banks by days.

The regional focus, while risky, creates deep expertise. PSB understands Punjab's kinnow orange trade better than any national bank. It knows which villages have water problems affecting crop loans. It recognizes family business dynamics in Ludhiana's textile industry. This granular knowledge enables better risk assessment than any algorithm.

PSB's community connection remains powerful. In rural Punjab, the PSB branch manager is still a respected figure, invited to weddings and consulted on financial matters. This social capital, built over a century, cannot be replicated by private banks or fintechs. When farmers need advice on crop insurance or traders want letters of credit, they trust PSB's guidance.

Competitive Positioning Strategy

PSB's competitive strategy is becoming clearer: don't compete everywhere, dominate somewhere. The bank is positioning itself as "Punjab's Own Bank"—the financial institution that understands and serves Punjab better than anyone. This isn't retreat but focus.

In corporate banking, PSB targets mid-sized Punjab businesses that are too small for large banks but too sophisticated for small banks. In retail banking, it focuses on mass affluent Punjabis who value relationships over rates. In agriculture, it leverages century-old expertise in crop cycles, water tables, and market dynamics. In NRI banking, it exploits emotional connections to homeland.

Partnerships Over Competition

Rather than competing head-on, PSB increasingly partners with potential competitors. With fintech companies, it provides banking infrastructure while they handle customer acquisition. With large banks, it participates in consortium lending, taking smaller shares but maintaining relationships. With foreign banks, it offers local expertise for international clients entering Punjab.

These partnerships acknowledge reality: PSB cannot win everything but can win something. By focusing on core strengths while partnering for weaknesses, the bank maintains relevance without overextension.

The Consolidation Question

The elephant in the room is consolidation. India has too many public sector banks for efficient oversight and capital allocation. The government has already merged several PSU banks. Will PSB be next? Its small size makes it an obvious target. Yet its unique regional identity and specialized expertise argue for independence.

The merger debate reflects broader questions about banking's future. Should India have a few large banks achieving global scale? Or many specialized banks serving niches? PSB's survival depends on this policy decision as much as operational performance. If consolidation comes, PSB might merge with Punjab National Bank, creating a Punjab-focused giant. If independence continues, PSB must prove that small, specialized banks have a role in India's financial system.

Market Positioning Metrics

By conventional metrics, PSB's market position is weak. Market share in total banking assets: 0.4%. Rank among Indian banks by assets: 21st. Share price performance: Bottom quartile. Analyst ratings: Mostly "Hold" or "Sell." These numbers suggest irrelevance.

But alternative metrics tell different stories. Market share in Punjab agricultural lending: 15%. Customer satisfaction in rural Punjab: 2nd highest. Cost per rural transaction: Lowest among PSU banks. These niche leadership positions matter for survival if not supremacy.

As one analyst notes: "PSB will never be HDFC Bank. But it doesn't need to be. It needs to be the best bank for its chosen segments in its chosen geography. On that metric, it's improving."

The competitive landscape reveals PSB's fundamental challenge: competing in a game where rules favor size, technology, and freedom from government control—none of which PSB possesses. Yet the bank's century-old roots, regional expertise, and community trust provide differentiation that pure-play digital competitors cannot replicate. The question isn't whether PSB can dominate Indian banking—it cannot. The question is whether there's sustainable space for a small, regional, relationship-focused bank in India's financial future. The answer will determine not just PSB's fate but the fate of specialized banking in India.

VIII. Playbook: Lessons from 116 Years of Banking

After traversing PSB's century-plus journey—from colonial-era community banking to digital transformation—what lessons emerge for investors, operators, and policymakers? PSB's story isn't just about one bank; it's a masterclass in institutional survival, adaptation, and the tensions between social mission and commercial viability. Here's the playbook distilled from 116 years of hard-won wisdom.

Lesson 1: Community Banking as Sustainable Competitive Advantage

PSB's original insight from 1908 remains valid: serving communities that mainstream finance ignores can be both profitable and sustainable. The bank's founders understood something modern financiers often forget—banking is fundamentally about trust, and trust is built through consistent community presence.

Consider PSB's survival through partition. When documentation was destroyed and legal systems collapsed, what remained? Relationships. The Amritsar branch manager who knew refugees from Lahore personally. The customers who repaid loans despite having no legal obligation. This social collateral proved more valuable than any physical collateral.

The lesson extends beyond crisis. PSB's lowest NPA periods coincided with strongest community engagement. When branch managers attended village panchayats, default rates dropped. When the bank sponsored local festivals, deposit mobilization increased. Community banking isn't charity—it's a business model based on information asymmetry reduction and social enforcement mechanisms.

Modern banks deploying AI for credit scoring might learn from PSB's relationship managers who knew that a farmer's loan repayment capacity depended on his daughter's wedding schedule. No algorithm captures this, but it materially affects credit risk. The playbook insight: In markets with information opacity and weak legal enforcement, relationship banking isn't outdated—it's essential.

Lesson 2: Surviving Multiple Crises Through Institutional Memory

PSB has survived existential crises that would destroy most institutions: partition's geographic disruption, nationalization's mission change, the Sethia fraud's reputational damage, liberalization's competitive onslaught, and the NPA crisis's financial stress. The survival mechanism? Institutional memory that transcends individual leaders.

Each crisis created organizational learning encoded in processes, culture, and collective memory. Partition taught the importance of documentation backup. The Sethia fraud instilled risk management discipline. The NPA crisis emphasized credit underwriting. These lessons, painfully learned, became organizational DNA.

The playbook teaches crisis management through institutional rather than individual response. When COVID-19 struck, PSB didn't need CEO genius—it had playbooks from previous crises. Branches knew how to operate with minimal staff (from partition experience). Risk teams knew how to handle mass defaults (from NPA crisis). Technology teams knew how to enable remote working (from digital transformation).

This institutional memory provides resilience that no startup can match. A fintech might be more innovative, but can it survive its first crisis? PSB has survived dozens. For investors, this suggests valuing institutional resilience alongside growth metrics.

Lesson 3: The Cost of Mission Drift

PSB's most challenging periods coincided with mission confusion. The bank thrived when clear about serving Punjab's underserved communities. It struggled when trying to be everything—a commercial bank, a development institution, a government policy tool, an international player.

The Sethia fraud exemplified mission drift costs. Why was a Punjab-focused community bank financing commodity trades in London? Because it had forgotten its core purpose in pursuit of prestige and profits. The massive NPAs of 2010-2015 reflected similar drift—a rural-focused bank suddenly financing infrastructure projects it didn't understand.

The playbook lesson is brutal: Organizations that forget their core purpose don't just underperform—they risk extinction. PSB's recent recovery coincided with renewed focus on its original mission, adapted for modern times. Digital transformation succeeded because it served the core mission of financial inclusion, not because digital was fashionable.

For operators, this means resisting temptation to chase every opportunity. For investors, it means skepticism when companies stray from core competencies. Mission drift isn't diversification—it's distraction.

Lesson 4: Government Ownership as Shield and Shackle

PSB's government ownership provided survival guarantee but imposed growth constraints. The shield aspect is obvious—no matter how badly PSB performed, the government wouldn't let it fail. This enabled risk-taking impossible for private entities. Would any private bank survive 25% NPAs? PSB did, multiple times.

But the shackle is equally real. Government ownership meant political interference, bureaucratic decision-making, and social obligations trumping commercial logic. PSB couldn't close unprofitable branches, couldn't pay market salaries, couldn't refuse politically-motivated loans. The bank became an instrument of state policy rather than an independent institution.

The playbook reveals a paradox: Government ownership enables survival but prevents excellence. PSB will never achieve HDFC Bank's efficiency under government ownership. But it might not exist without government support. For policymakers, this suggests rethinking public sector banking's role. Should PSU banks maximize profits or serve social objectives? Trying both ensures neither.

Lesson 5: Digital Transformation for Legacy Institutions

PSB's digital transformation offers lessons for legacy institutions worldwide. The bank didn't try to out-tech the fintechs. Instead, it digitized its core strength—relationship banking. WhatsApp banking in vernacular languages is innovation, but innovation that serves traditional customers rather than chasing new ones.

The transformation succeeded through pragmatic choices. Rather than building everything, PSB partnered. Rather than forcing digital on everyone, it offered choice. Rather than abandoning branches, it repurposed them. This isn't Silicon Valley disruption but something more valuable—evolution that preserves institutional strengths while addressing weaknesses.

The playbook for legacy institutions: Don't compete where you can't win. PSB will never match a neo-bank's user interface. But it can offer digital services with human fallback that pure-digital players cannot. The future isn't digital or physical—it's both, integrated intelligently.

Lesson 6: The Importance of Regional Identity

PSB's deep Punjab roots, seemingly a limitation, prove to be a differentiator. In an era of global banks and universal products, PSB's regional specificity provides competitive advantage. The bank understands Punjab's wedding loan needs, seasonal cash flows, and family business dynamics better than any algorithm.

This regional expertise enables risk assessment that standardized models miss. PSB knows that Ludhiana textile businesses need working capital in October for winter production. It understands that Jalandhar sports goods manufacturers face seasonal export cycles. This knowledge, accumulated over decades, cannot be replicated quickly.

The playbook suggests that in a globalizing world, local expertise becomes more, not less, valuable. Investors should value regional champions who dominate their geography over national players spread thin. Operators should resist homogenization temptation, preserving local adaptation that creates competitive moats.

Lesson 7: Risk Management in Agricultural and SME Lending

PSB's century of agricultural and SME lending provides risk management lessons unavailable from textbooks. The bank learned that agricultural risk isn't just about rainfall—it's about government procurement policies, input cost inflation, and social dynamics affecting repayment culture.

The playbook reveals that traditional risk metrics fail in these segments. A farmer's credit score might be poor, but his social standing ensures repayment. An SME's financials might look weak, but family wealth provides implicit guarantee. PSB developed heuristics that capture these realities: lending against gold jewelry (liquidatable, culturally significant), community guarantee mechanisms (peer pressure ensuring repayment), and seasonal adjustment (accepting irregular payments matching cash flows).

Modern lenders entering these segments often fail because they apply corporate lending frameworks to fundamentally different markets. PSB's experience suggests successful agricultural and SME lending requires patient capital, local presence, and social understanding that pure-data approaches miss.

Lesson 8: Building Trust Across Generations

Perhaps PSB's greatest achievement is maintaining trust across five generations of customers. The bank that served a customer's great-grandfather now serves his great-granddaughter. This multigenerational relationship transcends individual transactions, creating switching costs beyond economics.

Trust compounds across generations. A family that trusts PSB with savings trusts it with loans, then insurance, then investment advice. Children open accounts where parents bank. This organic growth, while slow, proves remarkably stable. Customer acquisition cost approaches zero when families self-perpetuate as clients.

The playbook teaches patience in trust-building. Modern banks spending fortunes on customer acquisition might learn from PSB's century-long approach. Trust isn't bought through advertising but earned through consistent presence, reliable service, and cultural alignment. Once built, it provides competitive advantage no technology can disrupt.

The Meta-Lesson: Institutional Purpose Beyond Profit

PSB's ultimate lesson transcends banking: Institutions serving purposes beyond profit can survive when pure profit-maximizers cannot. The bank's social mission—serving the underserved—provided resilience through crises that destroyed purely commercial entities.

This isn't corporate social responsibility grafted onto profit-seeking. It's purpose embedded in organizational DNA, guiding decisions when short-term profit conflicts with long-term mission. PSB survived partition because communities needed it to survive. It survived NPAs because the government couldn't let rural credit disappear. It's surviving digital disruption because someone must serve those whom technology leaves behind.

The playbook's final insight: In a world optimizing for efficiency, inefficiency serving social purpose might be the ultimate moat. PSB will never be India's most profitable bank. But it might be its most necessary bank. For investors seeking quick returns, PSB disappoints. For those valuing institutional permanence, it instructs.

These lessons from 116 years don't guarantee PSB's future success. But they provide a framework for understanding how institutions navigate the eternal tension between commercial viability and social purpose. In that navigation lies wisdom relevant far beyond banking.

IX. Analysis & Investment Case

Standing at PSB's crossroads in 2024, potential investors face a fascinating puzzle. Here's a bank trading at less than 0.5x book value, showing improving operational metrics, backed by government guarantee, yet shunned by markets. Is this the classic value trap—cheap for good reason? Or a contrarian opportunity where sentiment has diverged from fundamentals? Let's examine both sides with the rigor this decision demands.

The Bull Case: Deep Value with Catalysts

Valuation Discount to Intrinsic Value At ₹43 per share against a book value of approximately ₹90, PSB trades at a deeper discount than almost any listed bank globally. Even adjusting for hidden NPAs and generous provisioning assumptions, the discount seems excessive. If PSB merely reaches book value—not an aggressive target for a profitable bank—investors see 100%+ returns.

The government's 93.8% ownership provides an asymmetric risk-reward profile. Downside is limited because the government won't allow failure. Upside is substantial if operational improvements continue. It's like buying a call option where the strike price is protected by sovereign guarantee.

Operational Momentum Building The latest results show net profit jumping 146.66% year-over-year, suggesting turnaround momentum. Asset quality is improving with gross NPAs down from 14%+ to 5.4%. Digital adoption is accelerating with PSB UnIC platform gaining traction. These aren't cosmetic improvements but fundamental operational shifts.

The cost-to-income ratio, while still high at 68%, has declined from 75% two years ago. Operating leverage is kicking in—revenue growth exceeds cost growth. As digital transactions replace physical ones, this ratio should improve further, potentially reaching 55% within three years. Each percentage point improvement drops directly to bottom line.

Punjab's Economic Potential PSB is essentially a leveraged bet on Punjab's economy. The state's per capita income is 40% above national average. Agricultural productivity leads India. The entrepreneurial Punjabi diaspora provides remittance flows and investment capital. If Punjab's economy grows even moderately, PSB disproportionately benefits.

The state government's focus on industrial development—textile parks, sports manufacturing hubs, food processing clusters—creates credit demand PSB is uniquely positioned to capture. The upcoming Amritsar-Delhi-Kolkata industrial corridor passes through PSB's core markets. Infrastructure development typically drives 3-4x multiplier in credit growth.

Digitalization Payoff Pending PSB's technology investments haven't fully paid off. The PSB UnIC platform, WhatsApp banking, and video KYC are recent launches. As customers adopt these channels and the bank decommissions legacy systems, cost savings will be substantial. Industry benchmarks suggest digital transactions cost 90% less than physical ones.

The bank is also building data analytics capabilities that could transform risk assessment. With 116 years of customer data, PSB has information assets no fintech can match. Properly analyzed, this data enables better credit decisions, personalized product offerings, and risk-based pricing that could expand margins by 50-100 basis points.

Hidden Asset Value PSB owns real estate in prime locations across Punjab, carried at historical cost on books. The Amritsar main branch alone, in the city's commercial heart, could be worth ₹100+ crores. With 1,570 branches, many in now-valuable urban locations, the real estate value could exceed ₹5,000 crores—25% of market cap.

The bank's trust and pension management business, generating stable fee income, isn't properly valued. PSB manages pension schemes for several Punjab government departments. These sticky, fee-generating relationships provide annuity-like revenue streams worth significant multiples in private markets.

Regulatory Tailwinds Recent RBI regulations favor PSB's model. Priority sector lending requirements are increasing, benefiting banks with rural presence. The push for financial inclusion aligns with PSB's traditional strength. Restrictions on fintech lending remove predatory competition. These regulatory shifts level the playing field.

The Bear Case: Structural Challenges Persist

Profitability Remains Subpar Despite improvements, ROE at 6.59% over three years remains unacceptable. With cost of equity around 12%, PSB destroys value even while reporting profits. This isn't temporary—structural factors like priority sector lending, government interference, and high operating costs ensure permanently suppressed returns.

The net interest margin at 2.1% is among the lowest in Indian banking. While peers achieve 3.5-4%, PSB struggles because government ownership prevents risk-based pricing. Political pressure keeps lending rates low and deposit rates high, compressing margins structurally.

Contingent Liabilities: The Hidden Iceberg Contingent liabilities of Rs.6,200 crores represent potential bombs. These include guarantees to dubious borrowers, legal claims from past frauds, and disputed tax demands. If even 30% materialize, PSB needs another recapitalization.

The bank's disclosure on stressed assets remains opaque. How many restructured loans are genuinely recovering versus postponing inevitable default? Historical experience suggests 40-50% of restructured loans eventually fail. Current provisioning might prove inadequate.

Government Ownership: The Permanent Handicap With 93.8% government ownership, PSB cannot make independent decisions. Branch closures need political approval. Salary increases face bureaucratic delays. Strategic initiatives require ministry clearance. This governance handicap ensures permanent underperformance.