Prudent Corporate: India's Mutual Fund Distribution Powerhouse

I. Introduction & Episode Thesis

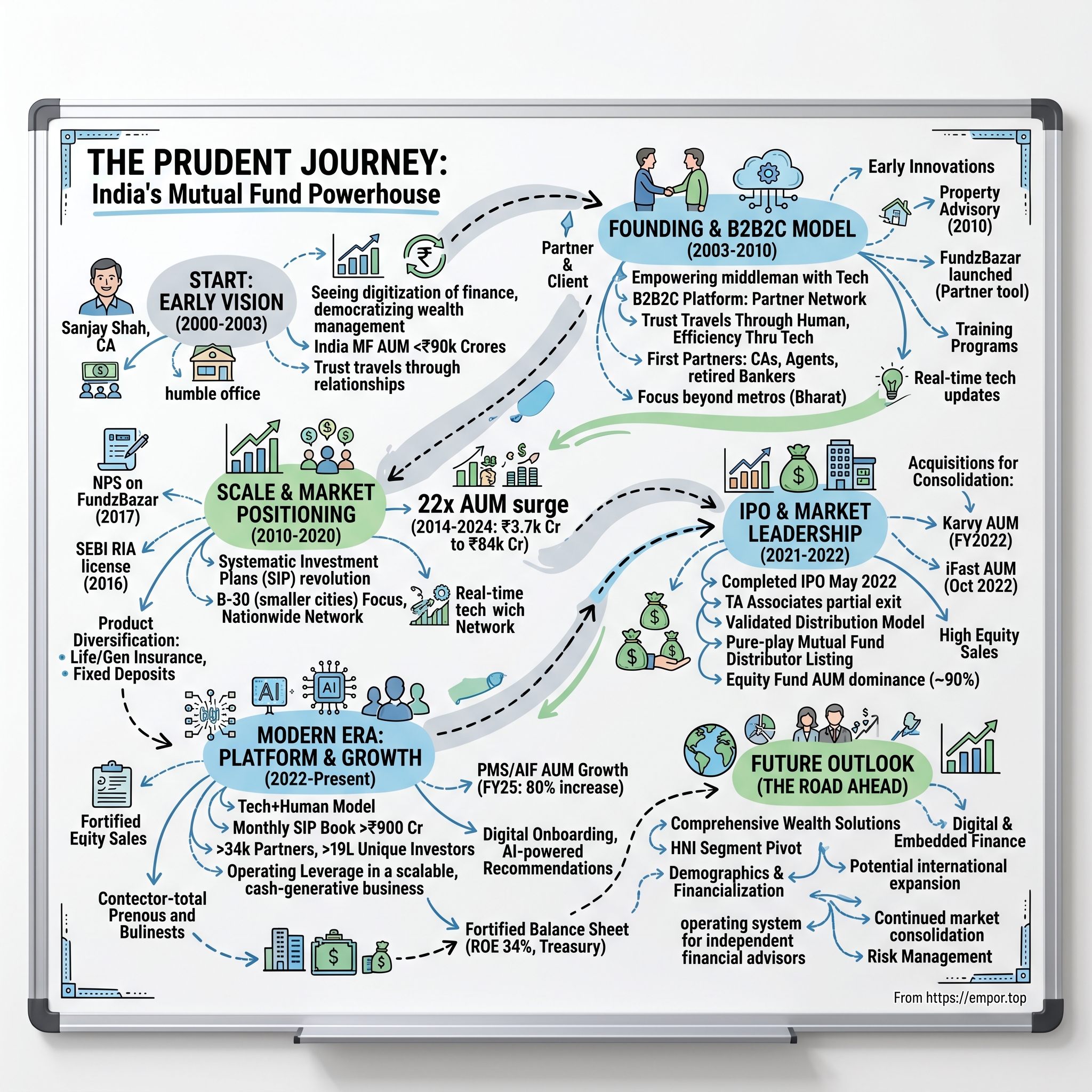

Picture this: It's 2000, and in a modest office in Ahmedabad, a chartered accountant named Sanjay Shah is staring at a computer screen showing UTI's mutual fund NAVs. The dot-com bubble is about to burst, India's mutual fund industry has barely ₹90,000 crores in AUM, and most Indians still keep their savings in gold, real estate, or fixed deposits. Shah sees something others don't—not just the digitization of finance, but the democratization of wealth management itself.

Fast forward to 2024: Prudent Corporate Advisory Services commands a market capitalization of ₹10,865 crores, with revenues touching ₹1,148 crores and profits of ₹203 crores. The company has become India's second-largest non-bank mutual fund distributor, managing assets that would have seemed fantastical in those early days. The question isn't just how they got here—it's how a company from Gujarat's business heartland cracked a code that eluded banks, brokerages, and tech platforms alike.

This is fundamentally a story about distribution, but not the kind you might expect. While Silicon Valley was obsessing over "cutting out the middleman," Prudent built an empire by empowering 34,000+ middlemen with technology. While fintech startups chased urban millennials, Prudent quietly captured Bharat—the real India beyond the metros. And while competitors fought over commission rates, Prudent created a platform business disguised as a distribution company.

The narrative arc we're about to explore touches on several profound themes: the financialization of Indian household savings (a $5 trillion opportunity), the power of B2B2C business models in emerging markets, and perhaps most importantly, why in the age of zero-commission brokers and direct mutual funds, a company built on distribution fees keeps growing at 40% annually. It's a case study in building moats where none should exist, creating network effects in traditional businesses, and riding secular trends with operational excellence.

What makes this particularly fascinating for investors is the paradox at its heart. Prudent operates in what should be a commoditized, margin-compressed business—mutual fund distribution. Yet it generates 18% net margins, throws off cash, requires minimal capital for growth, and has expanded its competitive advantages even as regulatory pressures mount. The company's trajectory offers lessons not just about Indian financial services, but about platform economics, trust-building at scale, and the enduring value of human relationships in digital commerce.

II. The Pre-History: India's Wealth Management Landscape (1990s-2000)

The year is 1999. The Kargil conflict has just ended. India's GDP is barely crossing $450 billion. In the bylanes of Gujarat's textile markets, businessmen still settle trades with hundis and post-dated cheques. The BSE Sensex hovers around 5,000, and Unit Trust of India holds a virtual monopoly over the country's mutual fund industry with its flagship US-64 scheme. Most Indians—if they save at all—park their money in gold jewelry, ancestral land, or the reassuring embrace of fixed deposits at 12% interest rates.

This was the canvas Sanjay Shah surveyed when he decided to leave his comfortable chartered accountancy practice to venture into financial distribution. His friends thought he'd lost his mind. Why leave a stable profession to sell mutual funds in a country where the household savings rate, though rising from 13% of GDP in 1970, was still heavily skewed toward physical assets? Where the average middle-class family viewed stock markets with the same suspicion they reserved for gambling dens?

To understand why 2000 represented such a pivotal moment, we need to rewind to India's financial markets in the 1990s—a decade that began with crisis and liberalization, witnessed the entry of private players, and ended with technological disruption that would reshape every industry it touched. UTI, established in 1963 at the initiative of the Government of India and Reserve Bank of India, had enjoyed its monopoly until 1987 when public sector mutual funds entered—SBI Mutual Fund in June 1987, followed by Canbank, Punjab National Bank, Indian Bank, Bank of India, and Bank of Baroda.

The real game-changer came in 1993. Kothari Pioneer (now merged with Franklin Templeton) became the first private sector mutual fund registered in July 1993, marking the beginning of a new era that gave Indian investors a wider choice of fund families. Foreign sponsors rushed in—Morgan Stanley, Templeton, Alliance Capital—bringing global best practices and aggressive marketing. By the end of 1993, the industry had grown to ₹47,004 crores in AUM, and by January 2003, it would reach ₹1,21,805 crores with 33 mutual funds operating.

But beneath these headline numbers lay a deeper structural problem. The distribution architecture was fundamentally broken. Banks sold their own funds, ignoring customer needs for unbiased advice. Independent financial advisors existed but lacked scale, technology, or training. Urban metros had wealth but limited trust in equity products after the Harshad Mehta scam of 1992. And tier-2 and tier-3 cities—where India's real savings pool resided—had virtually no access to professional wealth management.

The technology landscape of 2000 offered tantalizing possibilities. The Y2K scare had forced financial institutions to upgrade their systems. The internet, though nascent with less than 5 million users in India, promised to democratize information flow. Mobile phones were beginning their march beyond the elite. And critically, the National Stock Exchange's satellite-based trading network had proven that technology could overcome India's geographic vastness.

Shah saw what others missed: the convergence of three megatrends. First, India's savings rate was approaching its peak trajectory—it would rise from around 23% in the 1990s to 38% of GDP by 2008. Second, the demographic dividend was beginning—millions of young Indians entering the workforce needed investment avenues beyond traditional options. Third, regulatory reforms under SEBI were professionalizing the mutual fund industry, creating space for organized distribution.

The masterstroke wasn't choosing between technology or human distribution—it was recognizing that India needed both. While Mumbai's fintech entrepreneurs dreamed of replacing relationship managers with websites, Shah understood something fundamental about Indian financial behavior: trust travels through relationships, but efficiency travels through technology. The winning formula would be to arm trusted local advisors with world-class technology platforms.

Consider the market structure in 2000. UTI alone had 53 offices, 320 chief representatives, and managed 45 million accounts—more than any other mutual fund. But even this massive network couldn't reach India's 600,000 villages and thousands of small towns. The banks had branches but no incentive to sell competing products. The post office had reach but no financial sophistication. This distribution vacuum represented either an insurmountable challenge or an extraordinary opportunity, depending on your perspective.

Shah chose to see opportunity. His vision was audacious yet simple: create a technology-enabled platform that would allow anyone with financial acumen and local relationships to become a mutual fund distributor. Don't compete with the manufacturers (mutual funds) or try to displace existing channels (banks). Instead, create an entirely new channel—organized, scalable, and aligned with both investor and manufacturer interests.

The India of 2000 was particularly receptive to this model for cultural reasons often overlooked by pure-play technology companies. The concept of the trusted family advisor—whether the family doctor, lawyer, or chartered accountant—ran deep in Indian society. Financial decisions were rarely made in isolation; they required consultation, validation, and often, permission from multiple stakeholders. A web portal couldn't navigate these social complexities. But a local advisor, armed with technology and backed by a credible institution, could.

As Shah registered Prudent Corporate Advisory Services Limited in 2003, the mutual fund industry was about to witness its most dramatic transformation. In February 2003, following the repeal of the Unit Trust of India Act 1963, UTI was bifurcated into two separate entities—ending an era and creating space for new players to reimagine distribution. The stage was set for a company that would neither manufacture products nor own customer relationships in the traditional sense, but would instead become the vital connective tissue between India's savings and its capital markets.

III. The Founding Story: Sanjay Shah's Vision (2000-2003)

The story of Prudent's founding isn't just about Sanjay Shah starting a company—it's about a chartered accountant who saw the future of Indian finance while working with textile manufacturers in Ahmedabad's industrial corridors. A Chartered Accountant by qualification, Mr. Sanjay Shah is the Founder of the Prudent Group and Managing Director of Prudent Corporate Advisory Services Ltd. He previously worked with various Industries before laying foundation of Prudent in 2000.

Before Prudent, Shah had spent years advising Gujarat's thriving business community—textile barons, diamond merchants, pharmaceutical entrepreneurs. He watched them make fortunes in their core businesses, then struggle to deploy capital wisely. They'd buy more real estate, more gold, occasionally dabble in stocks during bull runs, and inevitably lose money when markets corrected. The irony wasn't lost on him: India's most successful businesspeople were often its worst investors.

He visualized the growth of Mutual fund and Financial Services sector through the power of technology at an early stage of his entrepreneurship journey. But visualization alone doesn't build businesses. Shah's genius lay in understanding three interconnected problems that existing players couldn't—or wouldn't—solve.

First was the trust deficit. The average Indian investor in 2000 had been burned multiple times—by the Harshad Mehta scam, by UTI's US-64 crisis that would soon unfold, by fly-by-night operators promising unrealistic returns. They needed advisors, but more importantly, they needed advisors backed by institutions with skin in the game.

Second was the knowledge gap. Mutual funds weren't like fixed deposits or gold—they required understanding of risk, asset allocation, market cycles. Banks had the trust but not the expertise or incentive to educate. Independent advisors had knowledge but lacked credibility. There was no scaled solution for financial literacy.

Third was the economics problem. Distributing mutual funds to retail investors, especially in smaller cities, was inherently unprofitable using traditional models. The ticket sizes were too small, the hand-holding requirements too high, the geographic spread too vast. This is why banks focused on their own products and why independent advisors remained subscale.

Shah's solution was elegant in its simplicity: don't try to own the customer relationship directly. Instead, enable thousands of local entrepreneurs to build their own distribution businesses, but provide them with everything they'd need—technology, training, products, compliance, and crucially, a brand that would open doors.

The early days were far from glamorous. Operating from a cramped office that colleagues would later remember for its modest size, Shah began building the infrastructure. The first challenge was technology. In 2000, most mutual fund transactions still happened on paper. NAVs were checked in newspapers. Applications were physically couriered. Shah invested heavily in creating a technology platform that could digitize these processes—not to eliminate human distributors but to make them exponentially more productive.

Vikaas Sachdeva expressed his admiration for Sanjay Shah's success, noting that Prudent Corporate Services had become larger than most Asset Management Companies (AMCs) in terms of Assets Under Management (AUM). He recalled Sanjay Shah's earlier days, remembering the cramped office space and how he managed operations from a small area. Sachdeva then asked Shah to share the origin of Prudent Corporate Services, including his thought process, vision, and focus when he started the company.

The second piece was the partner model. Rather than hiring salespeople, Shah invited local professionals—chartered accountants, insurance agents, retired bankers—to become "Prudent Partners." These weren't employees but independent entrepreneurs who would use Prudent's platform to build their own wealth management practices. The pitch was compelling: keep your independence, we'll handle the backend.

Incorporated in 2003, Prudent Corporate Advisory Services Limited began operations at precisely the moment when the mutual fund industry's old guard was crumbling. The UTI bifurcation created regulatory clarity. SEBI's strengthened regulations gave investors confidence. And the bull market of 2003-2007 was about to provide the perfect tailwind for a distribution-focused business.

But Shah's masterstroke was recognizing that distribution in India couldn't be purely transactional. In developed markets, investors might buy mutual funds online based on star ratings and past performance. In India, they needed someone to explain why systematic investment plans made sense, why equity allocation mattered, why staying invested during corrections was crucial. This advisory layer couldn't be automated—at least not in 2003.

The early partner acquisition strategy revealed Shah's deep understanding of Indian business culture. He didn't advertise in newspapers or hold mass recruitment drives. Instead, he identified respected professionals in each city—the CA who handled the local business community's taxes, the LIC agent who'd sold policies for decades, the retired bank manager who knew every family in town. One by one, he convinced them that financial distribution was the next evolution of their practices.

The training infrastructure Prudent built was unprecedented in Indian financial distribution. Partners weren't just given product brochures and commission structures. They underwent comprehensive education on financial planning, asset allocation, regulatory compliance. Many partners later credited Prudent's training for transforming them from product sellers to genuine financial advisors.

The technology platform, even in its early incarnation, was revolutionary for its time. Partners could check NAVs in real-time, submit applications electronically, track their clients' portfolios, generate reports—capabilities that seem basic today but were groundbreaking in 2003. This technology edge allowed a Prudent partner in a small town to offer the same service quality as a private banker in Mumbai.

By the end of 2003, Prudent had established proof of concept. The partner network was growing, the technology was working, and most importantly, assets were beginning to flow. But Shah knew this was just the beginning. The real test would come in scaling this model across India's vast geography while maintaining quality and compliance standards.

Looking back, colleagues would marvel at Shah's prescience in choosing 2000-2003 to build Prudent's foundation. He'd started during the dot-com bust when technology was cheap and talent was available. He'd incorporated just as the mutual fund industry was being restructured. And he'd built his distribution network just in time for India's greatest bull market. But those who knew him understood this wasn't luck—it was the methodical execution of a vision he'd been refining since his days advising Gujarat's industrialists about their investment mistakes.

IV. The Distribution Innovation: B2B2C Model (2003-2010)

The period from 2003 to 2010 would define Prudent's DNA forever. While competitors were debating whether to go digital or stay physical, Shah and his team were building something unprecedented in Indian financial services: a true B2B2C platform that made distribution partners the heroes of the story, not just commission agents.

FundzBazar is a leading online investment platform in India, simplifying the investment process for client and client management for our partners. But FundzBazar wasn't conceived as a direct-to-consumer play. It was designed from day one as a partner empowerment tool—a digital backbone that would allow independent distributors to compete with banks and large brokerages.

In 2006, the Company launched Partner Network. This wasn't just a distribution channel; it was a revolution in how financial products could be sold in India. The genius lay in recognizing that mutual fund distribution wasn't really about mutual funds—it was about trust, relationships, and solving financial anxieties. Technology could handle transactions, but only humans could handle emotions.

Company provide wealth management services to 19.28 lakhs unique retail investors through 33,308 MFDs on its business-to-business-to-consumer (B2B2C) platform and are spread across branches in 136 locations in 21 states in India, as on March 31, 2025. But in 2006, this massive network was just beginning. The early partners were pioneers—chartered accountants tired of just filing taxes, insurance agents seeking better products, retired bankers wanting to stay relevant.

The training infrastructure Prudent built was unlike anything in Indian financial distribution. Partners underwent 100+ hours of initial training covering not just products but behavioral finance, goal-based planning, and crucially, compliance. One early partner recalled: "I have attended so many training sessions in the last five years and that has surely helped me in my growth story."

The technology platform evolved rapidly. By 2007, partners could onboard clients digitally, track real-time NAVs, generate performance reports, and even conduct virtual meetings—capabilities that wouldn't become mainstream until the pandemic forced digital adoption. "Because of prudent's technology platform & support I am able to service my client quickly and professionally."

But the real innovation was in economics. Traditional distribution models treated advisors as either employees (high fixed costs) or pure commission agents (no loyalty). Prudent created a hybrid: partners remained independent entrepreneurs but received infrastructure, training, and brand support that made them feel part of something bigger. The company didn't just share commissions; it shared capabilities.

Owing to a large network of MFDs, it facilitate AMCs access to smaller cities, especially in the B-30 markets. This B-30 focus—cities beyond the top 30—became Prudent's moat. While competitors fought over Mumbai and Delhi's HNIs, Prudent partners were opening accounts in Jamnagar, Hubli, and Raipur. These weren't sexy markets, but they had savings, aspiration, and crucially, no competition.

The 2008 financial crisis tested the model severely. Markets crashed, investors panicked, redemptions spiked. Many distributors, especially bank-affiliated ones, simply stopped selling equity funds. But Prudent's partners, trained in market cycles and armed with educational materials, actually increased their client engagement. They conducted investor awareness sessions explaining why staying invested during downturns was crucial. This counter-cyclical behavior would become a hallmark of the Prudent model.

Founded by Sanjay Shah in 2000, Prudent Corporate started with humble beginnings in Ahmedabad. Today, it is among the top ten mutual fund distribution houses in India with assets under advisory of over Rs 22,000 crore and 14,600 channel partners. But the journey from startup to scale wasn't smooth. Technology failures, partner attrition, regulatory changes—each crisis forced evolution.

The platform capabilities expanded beyond transactions. Partners could now run financial planning simulations, create custom portfolios, even white-label reports with their own branding. "Prudent has one of the best systems, one of the best partner desks and one of the best IT teams to support. The array of products helps you grow as a good financial planner."

By 2010, the B2B2C model had proven its power. Partners weren't just selling mutual funds; they were building multi-generational relationships with families. A partner in Surat might manage the retirement planning of the parents, the SIPs of the children, and the insurance needs of the entire extended family. This depth of engagement created switching costs that no robo-advisor could overcome.

The numbers told the story. From virtually zero in 2003, Prudent had built an AUM of several thousand crores by 2010. More importantly, it had created a replicable, scalable model. Each new partner brought not just their existing relationships but also local market knowledge that no algorithm could capture. Each new city opened not through expensive branch setups but through empowered local entrepreneurs.

"Their online investment platform Fundzbazar.com helped me cut down all the limitations of demography in my business and I have clients all across India and abroad as well." "Me and my clients get lots of flexibility at one login on fundzbazar.com, I guess it is one of the best online platforms currently in india."

The platform architecture revealed sophisticated thinking about network effects. Every partner benefited from product additions, technology upgrades, and training programs developed for the entire network. But unlike traditional franchises, partners retained their independence and client ownership. This balance—standardization without commoditization—would prove crucial as the business scaled.

Looking back, the 2003-2010 period established three enduring competitive advantages. First, the partner network created distribution density that would take competitors decades to replicate. Second, the technology platform created switching costs—partners had invested time learning the system and wouldn't easily abandon it. Third, and most importantly, Prudent had cracked the trust equation in Indian financial services: global capabilities delivered through local relationships.

V. Growth Phase: Scaling and Market Positioning (2010-2020)

The decade from 2010 to 2020 would prove that Prudent wasn't just riding India's mutual fund wave—it was helping create it. Over the past five years, the company has expanded its Mutual Fund AUM by a CAGR of 28%. They have grown at a CAGR of 32.5% for AAUM and 34.4% for Commission respectively. But these numbers only tell part of the story.

The 2010s began with a crisis of confidence in Indian capital markets. The 2008 financial crisis had shaken investor faith, inflation was running high, and gold prices were soaring as Indians retreated to traditional safe havens. It was precisely the wrong time to be in financial distribution—which made it exactly the right time for contrarian expansion.

Associated with the group since 2005, Mr. Shirish Patel is currently the Chief Executive Officer of Prudent Corporate Advisory Services Ltd. As the CEO, his role entails the overall strategic direction, network building and operational responsibilities of the group. Under his leadership, the branch network expanded from five to 105 branches by the IPO date, reaching 124 branches spread over 21 states by 2024.

In 2010, the Company launched Property Advisory/Distribution services—a seemingly odd diversification that revealed strategic brilliance. Partners were already trusted advisors for all financial matters. When clients asked about real estate investments, partners had no answers. By adding property advisory, Prudent ensured partners remained the single point of contact for all wealth decisions.

The company grew faster among national distributors (amongst the top 10 mutual fund distributors) in terms of commission and AAUM with a CAGR of 34.4% and 32.5% respectively for the five year period ending Fiscal 2021. This growth wasn't just about adding partners or branches. It was about deepening engagement with existing clients and expanding wallet share.

The systematic investment plan (SIP) revolution transformed Prudent's business model between 2010-2020. SIPs converted one-time mutual fund purchases into recurring monthly investments, creating predictable cash flows and reducing market timing risks. Prudent partners were trained extensively on SIP benefits—how ₹5,000 monthly could become ₹1 crore over 20 years, how rupee cost averaging worked, how discipline trumped timing.

Geographic expansion followed a counterintuitive strategy. While competitors rushed to metros and tier-1 cities where wealth was concentrated, Prudent focused on B-30 markets—cities beyond the top 30. The company has built a nationwide network, servicing 16,356 PIN codes. These weren't glamorous markets, but they had three advantages: no competition, lower operating costs, and surprisingly sticky clients who valued personal relationships.

The technology platform underwent continuous evolution. In 2016, the Company obtained SEBI RIA licence to provide Investment Advisory services. In 2017, the Company launched NPS on Fundzbazar and Online paperless empanellment for Mutual Fund Distributors. Each addition wasn't just a feature—it was a capability that made partners more valuable to their clients.

The period saw interesting product expansions. The company obtained PFRDA Point of Presence license for NPS Distribution, received RERA Real Estate Agent License in Gujarat and Maharashtra, and even launched Fundzbot on Fundzbazar in 2018. These weren't random diversifications but systematic responses to partner and client needs.

The numbers from this period reveal explosive growth. Prudent Corporate Advisory Services has 1,067 employees strength, 35.05 lakhs live folios and 15.25 lakhs live SIPs as of December 31, 2021. Each folio represented a family's trust, each SIP a commitment to long-term wealth creation.

He highlighted that the company had set a target in the last two years to reach ₹1 lakh crore in AUM and ₹1,000 crore in SIP books by the end of the year. He explained that in 2014, Prudent's AUM was ₹3,700 crore, and by March 2024, it had surged to ₹84,000 crore, a 22-fold increase. He also shared that their equity book had grown from ₹2,000 crore in 2014 to ₹80,000 crore in 2024, a 40-fold rise.

The competitive landscape during 2010-2020 was evolving rapidly. Banks were pushing their own funds aggressively, often mis-selling to meet targets. Online platforms like Scripbox and FundsIndia were emerging, promising direct access without intermediaries. Robo-advisors claimed algorithms could replace human judgment. Yet Prudent's partner-centric model not only survived but thrived.

The key was understanding what technology could and couldn't do. Technology could process transactions, generate reports, and track performance. But it couldn't hold a client's hand during market crashes, couldn't convince a skeptical spouse about equity investing, couldn't navigate complex family dynamics around inheritance planning. Prudent partners did all this and more.

Training infrastructure became increasingly sophisticated. Partners weren't just taught products; they learned behavioral finance, tax planning, estate planning. The company invested heavily in certifications—encouraging partners to become Certified Financial Planners, NISM-certified advisors. This professionalization elevated the entire network's credibility.

Client acquisition strategies evolved from pure referrals to systematic processes. Partners learned to conduct financial planning workshops, leverage social media, create educational content. The company provided marketing materials, compliance support, and crucially, a brand that opened doors. "Prudent ka partner hai" (He's a Prudent partner) became a stamp of credibility in smaller cities.

The 2016 demonetization provided an unexpected catalyst. As cash-heavy Indians were forced into the banking system, Prudent partners were perfectly positioned to channel these flows into mutual funds. The government's push for financial inclusion, JAM trinity (Jan Dhan-Aadhaar-Mobile), and Digital India created tailwinds that Prudent rode expertly.

By 2020, Prudent had transformed from a regional distributor to a national platform. The partner network had grown to over 23,000, branches dotted the country's map, and the technology platform handled millions of transactions. But more importantly, Prudent had proven that distribution wasn't a commodity business—done right, it was a deep moat business with network effects, switching costs, and brand value.

Looking at the decade's achievements, what stands out isn't just the growth metrics but the resilience. Through the 2013 taper tantrum, 2016 demonetization, 2018 IL&FS crisis, and numerous market corrections, Prudent not only survived but gained market share. Each crisis proved the value of hand-holding, of local presence, of trusted advisors who could explain complexity in simple terms.

VI. The IPO Story & Public Market Entry (2021-2022)

The decision to go public in 2022 wasn't just about liquidity or prestige—it was a strategic inflection point that would test whether Prudent's model could withstand the scrutiny of public markets. The Company completed its IPO on the NSE and BSE in May 2022, but the story behind this listing reveals much about Indian capital markets, private equity dynamics, and the evolution of financial services businesses.

The timing seemed counterintuitive. Markets were jittery about rising interest rates, the Russia-Ukraine conflict had sparked inflation fears, and tech stocks globally were crashing from their pandemic highs. Yet Prudent chose this moment to test public appetite for an old-economy distribution business in new-economy clothing.

Wagner Ltd from TA Associates sold 82,81,340 shares worth Rs 527 cr in the IPO, and Shirish Patel sold 2,68,000 shares. This wasn't a capital-raising exercise—it was entirely an offer for sale, signaling confidence that the business didn't need fresh funds to grow. Wagner, a global investment firm, invested in Prudent Corporate Advisory Services in Fiscal 2019. Wagner is a member of TA Associates, a global investment fund.

The private equity backstory added credibility. TA Associates, with over 50 years of growth investing experience and $28 billion deployed since inception, had taken a minority stake in 2019. Their involvement wasn't just about capital—they brought governance standards, strategic thinking, and most importantly, validation that Prudent's model could scale globally.

"TA's investment is a critical milestone for Prudent as we embark on our next phase of growth and seek to deepen our presence across multiple states and untapped markets," Sanjay Shah had said at the time. Three years later, TA was partially monetizing, but crucially, retaining significant stake—a vote of confidence in future prospects.

The IPO roadshow revealed interesting investor concerns. How sustainable were distribution commissions in an age of direct plans? Could technology platforms disintermediate the partner network? What happened when the next bear market hit? Management's answers were instructive: they weren't selling mutual funds, they were selling trust, advice, and hand-holding—none of which could be commoditized.

As per the statement from BSE, Prudent Corporate Advisory Services allotted 25,30,651 equity shares at Rs 630 apiece and has raised Rs 159.43 cr from 24 anchor investors. The anchor book quality spoke volumes—it included marquee domestic mutual funds and insurance companies who understood the distribution business intimately.

The price band of Rs 595-630 per share valued the company at approximately Rs 2,600 crores at the upper end. For a business generating Rs 450 crores in revenue and Rs 100 crores in profit (FY21 numbers), this represented a premium valuation—around 26x earnings. The market was pricing in significant growth, but also the quality of the business model.

The opening date for this IPO was 10 May 2022, and the closing date was 12 May 2022. The issue was subscribed 1.22 times—modest by Indian IPO standards but respectable given market conditions. Retail investors bid for 0.76 times their portion, while qualified institutional buyers subscribed 1.79 times, suggesting institutional confidence exceeded retail enthusiasm.

The employee participation deserves mention. The company offered a discount of Rs 59 per share to eligible employees, with a reservation of shares worth up to Rs 6.50 crore. This wasn't tokenism—it was ensuring that the people who built the business could participate in its public market journey.

On the listing day, on the BSE, the opening value per share was Rs 660, at a premium of 4.7% over its issue price. While on the NSE, the listing price was Rs 650, 3.2% more than the issue price. The modest premium was actually positive—it suggested realistic pricing rather than frothy valuations that often lead to post-listing crashes.

The IPO prospectus revealed fascinating details about the business. Nearly 90% of the AUA of Prudent Corporate Advisory is in the form of equity fund AUM, which makes it a lot more attractive from a business standpoint. Equity funds generate higher commissions than debt funds, and the shift toward equity demonstrated both partner capability in selling complex products and client trust in accepting volatility.

Before the IPO, Wagner held 40% stake in the company, while Shirish Patel 3.15% stake. Post-IPO, the shareholding structure showed founder Sanjay Shah and family retaining majority control—crucial for maintaining strategic direction and culture. This wasn't a company being sold; it was a company accessing capital markets while keeping its soul intact.

The use of proceeds—or rather, the lack thereof—was telling. Since it was entirely an OFS, the company received no money. This signaled that organic growth could be funded through internal accruals—a testament to the cash-generative nature of the business. The IPO was about liquidity for early investors and currency for future acquisitions, not about funding operations.

"TA Associates will partially exit through the public issue as it will dilute about 20 per cent of its shareholding through the public issue, while Patel will divest 0.65 per cent stake in the company," Sanjay Shah, promoter and chairman, told media. The measured exit by TA suggested they saw significant upside remaining.

The strategic roadmap post-IPO was ambitious. "The company is planning to acquire new customers through existing mutual fund distributors. Further, it will expand the target customer base to HNIs and affluent segments," Shah explained. This wasn't just geographic expansion but moving up the value chain toward higher-margin clients.

The technology investments planned were substantial. "The company will continue to make investment in IT infrastructure to drive innovation and improve user interface. Also, it will strengthen data analytics capabilities in order to design new products." This signaled that despite being a distribution business, Prudent saw itself as a technology-enabled platform.

Market reaction post-listing was mixed initially. The stock traded sideways for months, as investors digested whether a traditional distribution business deserved a technology-like valuation. But as quarterly results showed consistent growth, market share gains, and successful execution of the acquisition strategy, sentiment shifted.

The IPO marked a watershed for several reasons. It was the first pure-play mutual fund distribution company to list in India, providing a template for others. It validated that distribution businesses could command premium valuations if they demonstrated platform characteristics. Most importantly, it gave Prudent currency for the aggressive expansion that would follow.

Looking back, the 2022 IPO timing was masterful. Prudent went public before the market rally of 2023-24 that would drive its AUM and stock price to record highs. Early public investors who understood the model would see multi-bagger returns. And the company gained the credibility and visibility that only public markets can provide.

VII. The Modern Era: Technology, Acquisitions & Market Leadership (2022-Present)

The post-IPO era has been transformative, with Prudent executing a playbook that would make Silicon Valley growth investors jealous—except this wasn't about burning cash for growth but deploying capital strategically while maintaining profitability. Acquisition of Mutual Fund AUM of Karvy Stock Broking Limited in an all-cash deal in FY2022 marked the beginning of an aggressive consolidation strategy.

The Karvy acquisition deserves detailed examination. As of July 2021, Karvy Stock Broking had 1.2 million folios and total asset under management (AUM) of Rs 9,261 crore. The acquisition was done through a competitive bidding process conducted by stock exchanges, with Prudent emerging as the highest bidder. This wasn't just about buying assets; it was about rescuing client relationships from a failed competitor and demonstrating that Prudent could be a consolidator in a fragmenting industry.

The timing was perfect. Karvy's troubles had created uncertainty among its mutual fund clients, who needed a stable home for their investments. Prudent didn't just transfer the assets; they deployed teams to hand-hold every client through the transition, turning a potentially negative situation into a trust-building exercise. The integration was seamless—a testament to Prudent's operational capabilities.

Acquisition of the Mutual Fund AUM of iFast Financial Pvt Ltd followed in October 2022. The Company acquired Mutual Fund Assets under Management (AUM) of iFAST Financial India Private Limited (iFAST) resulting this, the said AUM was transferred from iFAST ARN to the Company's ARN. This second acquisition within a year signaled that Prudent wasn't opportunistic but strategic about consolidation. Second largest non-bank mutual fund distributor in India and the only listed player in the market—this positioning wasn't achieved through organic growth alone. The modern era has been defined by aggressive execution, strategic pivots, and most importantly, the ability to capitalize on India's mutual fund boom while others hesitated.

40% revenue growth and 42% profit increase in FY25, with 90% of AUM from partner channel—these numbers tell a story of a business hitting its stride. In Q4 and FY '25, the company showcased impressive financial resilience, achieving a 40% revenue growth and a 42% profit increase, despite market volatility. The strategic pivot toward the partner channel, now comprising 90% of AUM, validated the B2B2C model at scale.

The SIP revolution has been Prudent's greatest tailwind. Systematic Investment Plan (SIP) book grew by 47% YoY in September to Rs 874 crore. Prudent's market share of SIP flows in the industry stood at 3.6% in September 2024. Monthly SIP Book (March 2025): INR 981 crore, up from INR 935 crore in December 2024. Each SIP represents not just recurring revenue but a long-term relationship that compounds in value.

The technology transformation post-IPO has been remarkable. Digital onboarding, AI-powered portfolio recommendations, automated compliance checks—capabilities that would have been science fiction in 2000 are now table stakes. Yet Prudent has managed to layer technology without losing the human touch that defines its model.

"Our Assets Under Management (AUM) surpassed Rs 1 lakh crore on July 26, 2024, about a year and a half ahead of schedule, largely due to marked to market movements," Sanjay Shah noted. "It took us nearly eighteen years to reach Rs 20,000 crore, but the last Rs 20,000 crore was added in just six months." This acceleration isn't just about market tailwinds—it's about operating leverage kicking in after decades of infrastructure building.

The geographic footprint continues expanding intelligently. 124 branches spread over 21 states might seem modest compared to banks, but each branch serves as a hub for hundreds of partners. The real distribution happens through 34,000+ partners reaching 19.28 lakh unique retail investors—a reach that would cost billions to replicate.

Product diversification has accelerated. PMS and AIF Average AUM Growth (FY25): 80% increase to INR 1,080 crore. Fixed Deposit Mobilization Growth (FY25): 43% higher than FY24. These aren't random additions but systematic responses to partner feedback about client needs. As clients' wealth grows, they need sophisticated products—and Prudent ensures partners can provide them.

The insurance vertical deserves special mention. The integration of insurance offerings has further bolstered performance, with significant increases in both life and general insurance premiums. Insurance isn't just another product—it's a gateway to deeper client relationships and higher lifetime value.

The numbers reveal operational excellence. Commission Payout Ratio (FY25): Increased by 300 basis points to 64.1%. This might seem concerning, but it reflects the strategic shift toward the partner channel and away from direct business. Partners generate higher gross margins even after their commission share.

Return on Equity (FY25): 34%. Treasury Book: Close to INR 500 crore. These metrics show a business generating exceptional returns while maintaining a fortress balance sheet. The cash generation funds both dividends and acquisitions without leveraging.

"Adoption to mutual funds is growing at an exponential pace. The unique mutual fund investor count for the industry surpassed the mark of 5 crores in the month of September," Shah observed. "Since the last three months, monthly addition of unique investors is at a run-rate above 10 lakhs." This isn't just industry growth—it's a structural shift in Indian savings behavior that Prudent is uniquely positioned to capture.

The competitive dynamics have evolved interestingly. While regulatory challenges in the P2P lending segment pose risks, diversification into PMS and AIF segments offers a buffer. Digital-only players have struggled to crack the advisory layer. Banks remain focused on their own products. And standalone advisors lack the scale to compete on technology or training.

Net Equity Sales (FY25): INR 12,606 crore, nearly double the previous year's INR 6,164 crore. This isn't just about market share—it's about deepening penetration in existing markets while expanding into new ones. Each partner is becoming more productive, each client is investing more, and the platform is handling exponentially more transactions without proportional cost increases.

The M&A pipeline remains active. Strong Cash Flow from Operations will give firepower for inorganic acquisitions going forward, management has indicated. The Karvy and iFast acquisitions proved Prudent can integrate assets successfully. Future targets likely include stressed regional distributors or specialized platforms in adjacent verticals.

Prudent expanded its distributor network by 56% in FY25, enhancing its market reach and distribution capabilities. But quantity isn't the only focus—quality matters more. New partners undergo extensive training, must meet minimum productivity standards, and are supported with technology and marketing resources that individual distributors could never afford.

Looking at the modern era holistically, Prudent has achieved something remarkable: it's become a platform company without abandoning its distribution roots. The technology enables scale, the partner network provides reach, the training creates differentiation, and the brand ties it all together. This isn't easily replicable—it took 24 years to build and would take competitors decades to match even with unlimited capital.

VIII. Business Model Deep Dive: Unit Economics & Moats

The beauty of Prudent's business model lies not in its complexity but in its elegant simplicity—yet this simplicity masks sophisticated unit economics and deep competitive moats that become apparent only upon careful examination. Offers Mutual Fund products, Life and General Insurance, Stock Broking, PMS, AIF, bonds, fixed deposits, and other financial products. But the product range is less interesting than how these products flow through the system.

At its core, Prudent operates on a commission-sharing model. When a client invests ₹1 lakh in an equity mutual fund through a Prudent partner, the fund house pays approximately 1% annually as trail commission. Prudent shares 50-70% of this with the partner, keeping 30-50% for platform, technology, training, and operations. On ₹1 lakh crore AUM, even a 0.3% net margin translates to ₹300 crores annually—recurring, predictable, and growing with markets.

Highly scalable, asset-light, and cash-generative business model—this description undersells the operational leverage. Adding the next ₹10,000 crores of AUM requires minimal incremental cost. The technology platform is built, the training infrastructure exists, the compliance framework operates. Each marginal rupee of AUM drops almost directly to the bottom line after partner payouts.

The partner economics reveal why the model works. A typical partner managing ₹10 crores of AUM might earn ₹5-7 lakhs annually in trail commissions. For a chartered accountant or insurance agent in a tier-2 city, this represents significant additional income with minimal additional effort. The partner doesn't need to build technology, manage compliance, or negotiate with fund houses—Prudent handles everything.

But here's where it gets interesting: the platform creates network effects that economists dream about. Each new partner makes the platform more valuable to fund houses (greater reach), which improves terms for all partners. Each new fund house makes the platform more valuable to partners (more products), which attracts more partners. Each new product category makes existing client relationships deeper, increasing switching costs.

The technology moat is underappreciated. FundzBazar isn't just a transaction platform—it's a complete practice management system. Partners can track every client interaction, automate compliance reporting, generate sophisticated analytics, even run their own marketing campaigns. Switching to another platform would mean learning new systems, migrating years of data, and potentially losing client history. The switching costs compound over time.

Consider the trust architecture Prudent has built. In financial services, trust isn't just important—it's everything. Prudent creates trust at three levels: institutional (the listed company with governance standards), local (the neighborhood partner you know), and technological (the platform that never fails). This three-layered trust is nearly impossible for pure-play digital platforms to replicate.

The regulatory moat deserves attention. Being a listed company with SEBI registration, stock broking license, insurance broking subsidiary, and various other licenses creates barriers that new entrants can't easily cross. Each license took years to obtain, requires ongoing compliance, and provides access to products that unlicensed players can't offer. The regulatory burden that might seem like a cost is actually a moat.

Geographic network effects operate differently than in typical platform businesses. In tier-2 and tier-3 cities, Prudent often has the only trained mutual fund distributors. This local monopoly creates pricing power—not in terms of charging clients more, but in negotiating better terms with fund houses desperate for distribution in these markets. The density in B-30 markets is a moat that metros-focused competitors can't replicate.

The data advantage compounds annually. With millions of transactions, Prudent knows which products sell in which markets, which partners are most productive, which client segments are most profitable. This data informs product development, partner recruitment, and geographic expansion. New entrants start with zero data in a business where patterns matter enormously.

Training as a moat sounds strange, but consider this: Prudent has trained 34,000+ partners over two decades. The curriculum, the trainers, the certification programs—all represent accumulated knowledge that can't be easily replicated. A new distributor joining Prudent gets access to this entire knowledge base. One joining a competitor starts from scratch.

The brand moat in financial services is peculiar. Prudent isn't a consumer brand like HDFC or ICICI. Instead, it's a B2B brand that enables B2C relationships. Fund houses trust Prudent to represent their products properly. Partners trust Prudent to handle operations honestly. This two-sided brand equity took decades to build and would take decades to replicate.

Capital efficiency reveals the model's elegance. Unlike banks that need capital for lending or insurers that need float for claims, Prudent needs minimal capital for growth. The business throws off cash that can be returned to shareholders or used for acquisitions. The return on incremental capital employed approaches infinity—a characteristic of the best platform businesses.

The unit economics improve with scale in non-obvious ways. Technology costs are largely fixed, so each additional crore of AUM reduces per-unit technology cost. Compliance costs spread across a larger base. Even training costs decrease per partner as batch sizes increase. This isn't just economies of scale—it's economies of scale with network effects.

Risk distribution is ingenious. Prudent doesn't take market risk (that's on investors), credit risk (that's on fund houses), or operational risk (distributed across partners). The main risk is regulatory, and even that's mitigated by diversification across products and geographies. This risk-light model allows for aggressive growth without corresponding risk accumulation.

The innovation cycle creates sustainable advantage. Every new feature on FundzBazar—whether AI-powered recommendations or automated tax harvesting—is immediately available to all 34,000 partners. This collective innovation is faster than any individual player could achieve. Partners contribute ideas, Prudent implements them, everyone benefits—a virtuous cycle of improvement.

Why haven't banks crushed them? Banks have distribution but lack focus—mutual funds are one product among hundreds. They have conflicts of interest—selling their own products versus best-for-client products. They have legacy technology that makes innovation slow. And crucially, they have cost structures that make serving smaller clients unprofitable. Prudent's focused, aligned, efficient model wins by design.

The platform versus product debate misses the point. Prudent is neither pure platform nor pure product—it's an ecosystem business. The platform enables distribution, distribution generates data, data improves the platform, and the cycle continues. This ecosystem has multiple reinforcing loops that strengthen over time.

Looking at valuation through this lens, the market's pricing makes sense. This isn't a traditional distribution business earning spreads—it's a platform business with network effects, near-zero marginal costs, and expanding moats. The 50+ P/E multiple reflects not current earnings but the optionality embedded in the model.

IX. Playbook: Lessons in Distribution & Platform Building

The Prudent playbook reads like a masterclass in building a platform business in a traditional industry, but the lessons extend far beyond financial services. Each strategic decision compounds over time, creating a system that's both resilient and scalable.

Building trust in financial services starts with understanding that trust isn't monolithic—it has components that can be systematically addressed. Prudent unbundled trust into competence (training and certification), reliability (technology and processes), and alignment (commission sharing and skin in the game). By addressing each component systematically, they built institutional trust that transcends individual relationships.

The first lesson: localize trust, centralize operations. While the partner provides the local relationship and trust, Prudent centralizes everything that benefits from scale—technology, compliance, training, negotiations with manufacturers. This division of labor is optimal: relationships remain high-touch and local while operations achieve economies of scale.

The power of feet-on-street + technology isn't about balance—it's about amplification. Technology doesn't replace the partner; it makes each partner 10x more productive. A partner with Prudent's platform can manage 500 clients effectively. Without it, maybe 50. This multiplication effect, not substitution, drives the model.

Consider partner recruitment strategy. Prudent doesn't advertise "Become a Mutual Fund Distributor!" in newspapers. Instead, they identify respected professionals in each micro-market—the CA who does everyone's taxes, the retired bank manager who knows every family, the insurance agent with deep relationships. These people already have trust; Prudent gives them products and platform.

Partner economics and incentive alignment go beyond commission sharing. Partners own their client relationships—if they leave Prudent, they take their clients. This ownership creates long-term thinking. Partners build multi-generational relationships knowing they're building their own businesses, not just generating commissions for Prudent. This alignment is rare in distribution businesses.

The training philosophy emphasizes education over sales. Partners learn modern portfolio theory, asset allocation, behavioral finance—concepts that elevate them from salespeople to advisors. This education-first approach creates differentiation in markets where most "advisors" are just product pushers. Clients notice the difference, partners feel the pride, and the business benefits from quality over quantity.

Geographic expansion strategy followed a counterintuitive pattern. Instead of covering all major cities first, Prudent went deep in Gujarat, then Rajasthan, then Maharashtra. This density-first approach created local network effects—partners could refer clients to each other, share best practices, even cover for each other during absences. Depth beat breadth.

The hub-and-spoke model for physical presence is clever. Each branch serves as a hub for 200-300 partners in surrounding areas. The branch provides training rooms, meeting facilities, and technical support. Partners don't need their own infrastructure but have access to professional facilities when needed. This shared infrastructure model reduces costs while maintaining professional standards.

Product expansion vs. focus trade-offs reveal sophisticated thinking. Prudent adds products that leverage existing relationships (insurance, loans) but avoids those requiring new capabilities (direct equity trading requiring research). Each product addition must pass three tests: Does it deepen client relationships? Can existing partners sell it? Does it leverage our platform? This disciplined expansion avoids the diversification disasters common in financial services.

The sequencing matters. Start with mutual funds (easy to understand, regulated, growing market), add insurance (natural cross-sell, higher ticket size), then complex products (PMS, AIF) only after partners have sophistication. This graduation path develops partner capabilities while expanding revenue streams.

Capital allocation: Organic vs. inorganic growth shows financial discipline rare in growth companies. Despite abundant growth opportunities, Prudent maintains a conservative balance sheet. Acquisitions are fully paid in cash. Dividends are paid regularly. This capital discipline signals confidence—we don't need leverage to grow, and we generate enough cash to both invest and return capital.

The acquisition integration playbook from Karvy and iFast reveals operational excellence. Don't just transfer assets—transfer trust. Deploy teams to meet every significant client, explain the transition, address concerns. Convert a potentially negative event (your distributor failed) into a positive one (you're now with a stronger platform). This human touch in integration explains why acquired assets stick rather than churn.

Technology investment philosophy balances innovation with reliability. Prudent isn't trying to build the most cutting-edge fintech app. They're building robust, reliable infrastructure that never fails. A partner explaining portfolio allocation to a nervous client can't afford system downtime. This reliability-first approach might seem conservative but builds trust that flashy features can't match.

The platform governance model deserves study. While Prudent controls the platform, partners have input through formal and informal channels. Regular partner meets, feedback systems, advisory councils—these create buy-in and ensure the platform evolves to meet actual needs rather than assumed ones. This participatory governance is rare in B2B2C models.

Marketing strategy reflects deep understanding of Indian financial behavior. Prudent doesn't advertise to consumers—they enable partners to market locally. Each partner receives marketing materials, but customized with their name and contact. This distributed marketing is more effective than centralized campaigns because financial decisions in India remain deeply personal and local.

The regulatory strategy is proactive, not reactive. Prudent often implements compliance requirements before they're mandatory. This forward-looking approach builds regulatory goodwill and avoids the disruptions that hit less-prepared competitors when rules change. In a highly regulated industry, being ahead of compliance is a competitive advantage.

Cultural elements underpin everything. The company culture emphasizes service over sales, relationships over transactions, long-term over short-term. This culture transmits to partners through training and daily interactions. When 34,000 partners share similar values and approaches, it creates a distributed culture that becomes a competitive advantage.

Risk management philosophy differs from typical financial services. Instead of trying to eliminate risk (impossible in markets), Prudent distributes it. Market risk stays with investors, operational risk is shared with partners, only platform risk is centralized. This risk distribution makes the overall system anti-fragile—problems in one area don't cascade system-wide.

The innovation approach is pragmatic. Instead of labs and innovation centers, Prudent innovates through rapid iteration based on partner feedback. A partner suggests a feature, it's tested with a small group, refined, then rolled out system-wide. This bottom-up innovation is faster and more relevant than top-down planning.

Looking at the complete playbook, several meta-lessons emerge. First, in businesses with network effects, the initial design matters enormously—Prudent's B2B2C structure created aligned incentives from day one. Second, trust and technology are complements, not substitutes—each amplifies the other. Third, in emerging markets, distribution is often more valuable than manufacturing—Prudent captured the valuable part of the value chain.

X. Analysis: Bull vs. Bear Case

The investment case for Prudent Corporate hinges on fundamental questions about India's financial future, the durability of distribution models, and the company's ability to navigate regulatory and technological disruption. Both bulls and bears have compelling arguments.

The Bull Case: India's Financialization Megatrend

India's financialization story is just beginning. Household financial savings are expected to grow from ₹31 trillion to ₹62 trillion over the next decade. With per capita income set to grow 10x in next twenty-five years, the addressable market expands not linearly but exponentially. As income crosses certain thresholds, savings rates increase and allocation to financial assets accelerates.

The SIP revolution provides unparalleled visibility. Monthly SIP flows industry-wide have grown from ₹3,000 crores to ₹25,000 crores in just five years. Prudent's SIP book growing at 47% annually creates an annuity-like revenue stream. Each SIP is a 10-20 year commitment, providing revenue visibility that few businesses enjoy. The behavioral shift from lump-sum to systematic investing reduces volatility and increases persistency.

Market share gains seem inevitable given structural advantages. As the only listed pure-play distributor, Prudent attracts the best partners. The technology platform continues improving faster than competitors can catch up. Geographic expansion into underpenetrated markets faces limited competition. The company's market share in SIP flows increasing from 3.0% to 3.6% despite intense competition validates the model's strength.

The platform characteristics justify premium valuations. Near-zero marginal costs mean incremental revenue flows almost entirely to bottom line. Network effects strengthen with scale—each new partner makes the platform more valuable. Switching costs compound over time as partners build their businesses on Prudent's infrastructure. These aren't features of traditional distribution businesses but of technology platforms.

Regulatory tailwinds support the organized sector. SEBI's push for transparency and compliance favors organized players over individual advisors. The shift from cash to digital payments makes informal advisory relationships harder to maintain. Tax regulations increasingly require proper documentation of financial transactions. Each regulatory tightening strengthens Prudent's position relative to unorganized competition.

The Bear Case: Direct Plan Threat and Structural Risks

SEBI mandated direct route in 2013, steady shift from Regular to Direct plans represents an existential threat. Direct plans offer 0.5-1% higher returns annually by eliminating distributor commissions. As investors become more sophisticated and cost-conscious, the shift to direct seems inevitable. Zerodha, Groww, and other platforms offer direct plans with superior digital experiences.

The demographic challenge is real. Younger investors comfortable with technology might skip advisors entirely. The success of robo-advisors globally suggests algorithm-driven investing could replace human advisors. If millennials and Gen-Z invest directly through apps, Prudent's addressable market shrinks dramatically.

Regulatory risks loom large. SEBI could cap distributor commissions further, mandating lower charges to protect investors. The shift from upfront to trail commissions already compressed margins. Future regulations might eliminate embedded commissions entirely, forcing fee-only models that Indian investors resist paying for.

Competition from banks and technology platforms intensifies. Banks have distribution reach and customer relationships. Technology platforms have user experience and cost advantages. If either figures out the advice layer—through AI or hybrid models—Prudent's moat erodes quickly.

Market volatility impacts the business model directly. Since revenue depends on AUM, market corrections immediately impact earnings. A 20% market correction means 20% revenue decline, with limited ability to cut costs proportionally. This operating leverage works both ways, amplifying downturns as much as upturns.

Myth vs Reality: Testing Common Narratives

"Direct plans will eliminate distributors"—Reality: Direct plan adoption has plateaued around 15-20% of flows. Most investors still need hand-holding, especially during market volatility. The advice gap can't be filled by algorithms alone, particularly in India where financial decisions involve multiple family members.

"Technology platforms will disrupt traditional distribution"—Reality: Pure technology players have struggled with customer acquisition costs and low lifetime values. The human touch matters more in India than in developed markets. Prudent's B2B2C model combines technology efficiency with human relationships.

"Regulatory changes will compress margins"—Reality: While regulations have evolved, they've generally favored organized players over individual advisors. Compliance requirements create barriers to entry. The shift to trail commissions actually improved business quality by aligning long-term incentives.

"Banks will leverage their distribution"—Reality: Banks have had decades to dominate mutual fund distribution but remain focused on their own products. Conflicts of interest, legacy systems, and organizational inertia prevent banks from being effective open-architecture distributors.

Valuation Framework and Peer Comparison

At 50+ times earnings, Prudent trades at premiums to traditional financial services but discounts to platform businesses. HDFC AMC trades at 35x, but faces manufacturing pressures. CAMS trades at 45x with similar platform characteristics but less growth. Global wealth managers trade at 20-30x but operate in mature markets.

The valuation makes sense if you believe: (1) India's mutual fund penetration increases from 15% to 30% of population, (2) Prudent maintains or gains market share, (3) Operating margins expand with scale, (4) The business model proves resilient through cycles. Each assumption is debatable but defensible.

Key Metrics to Watch

Partner productivity (AUM per partner) indicates platform value. Currently at ₹3 crores per partner, this could double with better tools and training. SIP market share trends reveal competitive position. Holding steady or gaining share validates the model. Non-mutual fund revenue growth shows diversification success. Insurance, PMS, and AIF growth reduces dependence on mutual fund commissions.

Cost-to-income ratio demonstrates operating leverage. Declining from 21% to 18.9% shows scale benefits kicking in. Further improvement to 15% seems achievable. Partner retention rates indicate platform stickiness. Low churn suggests high switching costs and partner satisfaction.

The bull case ultimately rests on India's demographic dividend and financial deepening. If India follows the path of other Asian economies, financial assets will grow from 15% to 30%+ of household wealth. Prudent, as the largest independent distributor, captures disproportionate value from this shift.

The bear case assumes technology disrupts traditional distribution faster than Prudent can adapt. If direct investing becomes mainstream and advisory services get automated, Prudent's model becomes obsolete. The question isn't if but when—and whether Prudent can evolve before disruption hits.

The realistic scenario likely falls between extremes. Some investors will go direct, but many still need advisors. Technology will augment human advisors rather than replace them. Regulations will evolve but won't eliminate distribution economics. In this scenario, Prudent's platform model and execution capabilities allow it to adapt and thrive.

XI. The Future: What's Next for Prudent

Per capita income set to grow 10x in next twenty-five years—this projection from government economists isn't just a number but a transformation that will reshape India's financial services landscape. For Prudent, this represents not just opportunity but necessity to evolve from a mutual fund distributor to a comprehensive wealth solutions platform.

The wealth management pivot for HNIs is already underway. Prudent's PMS and AIF AUM grew 80% to ₹1,080 crores in FY25, but this is just the beginning. As India creates millionaires at an unprecedented pace—adding 20,000+ annually—the demand for sophisticated financial products explodes. The same trust relationships that work for mutual funds become gateways to estate planning, tax optimization, and alternative investments.

The strategic logic is compelling. A partner managing ₹50 crores of mutual fund AUM likely has 5-10 clients with ₹1 crore+ portfolios. These clients need services beyond mutual funds—private equity access, structured products, offshore investing. By enabling partners to serve these needs, Prudent increases wallet share without adding new clients. The economics are attractive: PMS and AIF generate 2-3x the revenue per rupee of AUM compared to mutual funds.

Technology investments reveal ambitious plans. The company is building AI/ML capabilities not to replace partners but to make them superhuman. Imagine a partner in Rajkot having the analytical capabilities of a Goldman Sachs advisor—portfolio optimization algorithms, risk assessment tools, tax harvesting strategies. This democratization of sophisticated financial tools could redefine wealth management in India.

The data platform being built deserves attention. With millions of transactions and client data points, Prudent can identify patterns invisible to individual advisors. Which clients are likely to increase investments? Who might need insurance? What triggers redemptions? This predictive capability, delivered to partners as actionable insights, creates value that pure execution platforms can't match.

International opportunities exist but require careful consideration. The NRI market represents $600 billion in wealth seeking India exposure. Prudent partners already serve NRIs informally—formalizing this with proper licenses and platforms could unlock significant AUM. The Middle East, with its large Indian diaspora, seems the logical first international market.

But international expansion isn't just about NRIs. The Prudent model—empowering local distributors with technology and training—could work in other emerging markets. Southeast Asia, Africa, Latin America all have similar characteristics: growing middle class, underpenetrated financial markets, trust deficits in financial services. Prudent's playbook, properly adapted, could work globally.

The platform vs. product debate will intensify. Should Prudent remain a pure distributor or manufacture its own products? The temptation to launch a Prudent AMC exists—higher margins, more control, vertical integration. But this would create channel conflict with partner AMCs and compromise the open-architecture model. The likely path: strategic partnerships rather than outright manufacturing.

Digital transformation will accelerate but not in obvious ways. Instead of building a consumer-facing robo-advisor to compete with partners, Prudent will likely create a "robo-assistant" for partners. Automated portfolio rebalancing, tax optimization, report generation—capabilities that free partners to focus on relationship management rather than operational tasks.

The education imperative becomes more critical as products become complex. Prudent University, the company's training initiative, could evolve into a certified financial education platform. Imagine partners earning recognized certifications, clients attending financial literacy workshops, even schools teaching Prudent-designed financial curricula. Education as a moat is underappreciated but powerful.

Consolidation opportunities will multiply as the industry matures. Smaller distributors struggling with technology costs and regulatory compliance become acquisition targets. Regional players with strong relationships but weak infrastructure need platforms like Prudent. The company's strong balance sheet and proven integration capabilities position it as the natural consolidator.

The regulatory evolution toward fee-based advisory seems inevitable but distant. When it comes, Prudent's response won't be resistance but adaptation. Partners already provide significant value beyond product distribution—financial planning, tax advice, estate planning. Charging explicit fees for these services, while culturally challenging today, becomes possible as Indian investors mature.

ESG and sustainable investing represent an emerging opportunity. As Indian investors become conscious of environmental and social impacts, demand for ESG products will grow. Prudent could lead this transition, training partners on sustainable investing, partnering with ESG-focused fund houses, even creating India's first ESG-focused distribution platform.

The generational transition within partner networks needs managing. Many partners who joined in 2005-2010 are approaching retirement. Their children might not want to continue the business. Prudent needs succession planning support—helping partners transition clients to younger advisors, creating partnership structures, even facilitating practice sales. This succession challenge, handled well, becomes an opportunity to upgrade the partner network.

Embedded finance opportunities exist at the intersection of Prudent's capabilities. Imagine mutual fund investments integrated into e-commerce checkouts, insurance embedded in travel bookings, wealth management within banking apps. Prudent's APIs and distribution capabilities could power financial services for non-financial platforms.

The small-ticket investment revolution through technology could expand Prudent's addressable market dramatically. If technology can make serving ₹1,000 monthly SIP clients profitable, tens of millions of Indians become potential customers. This might require a different model—digital-first with human assistance only when needed—but the market size justifies experimentation.

Blockchain and tokenization will eventually impact fund distribution. Tokenized funds could trade 24/7, settle instantly, and fragment into smaller units. While this seems distant, Prudent needs to prepare. The company that distributed mutual funds on paper in 2000 and digitally in 2020 might distribute tokenized assets in 2030.

The China parallel offers both inspiration and caution. Ant Financial's evolution from payments to wealth management shows the possibilities. But regulatory crackdowns on technology platforms also warn against moving too fast. Prudent's balanced approach—innovation within regulatory frameworks—seems prudent indeed.

Climate finance and transition funding represent a multi-trillion dollar opportunity as India decarbonizes. Green bonds, renewable energy funds, carbon credits—new asset classes that need distribution. Prudent's partners, trained properly, could become conduits for climate finance reaching retail investors.

The ultimate vision seems clear: Prudent as the operating system for India's independent financial advisors. Every tool they need, every product they want to offer, every capability they require—all available through Prudent's platform. This platform vision, if executed, creates a business that's essentially infrastructure for India's financial services industry.

Looking ahead, the biggest risk isn't disruption or regulation but execution. Can Prudent maintain culture while scaling from 34,000 to 100,000 partners? Can technology platforms handle 10x transaction volumes? Can training quality be maintained as batch sizes explode? These operational challenges, mundane as they seem, will determine whether Prudent captures the opportunity ahead.

The next decade will test whether Prudent's model—human relationships augmented by technology—remains relevant as India digitizes. The bet is that financial decisions, involving life savings and family futures, will always require human judgment, empathy, and trust. Technology will evolve, regulations will change, competition will intensify, but the need for trusted financial advisors seems permanent. Prudent's job is to ensure its partners remain the best answer to that need.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube