Poly Medicure: From Faridabad Factory to Global MedTech Player

I. Introduction & Episode Roadmap

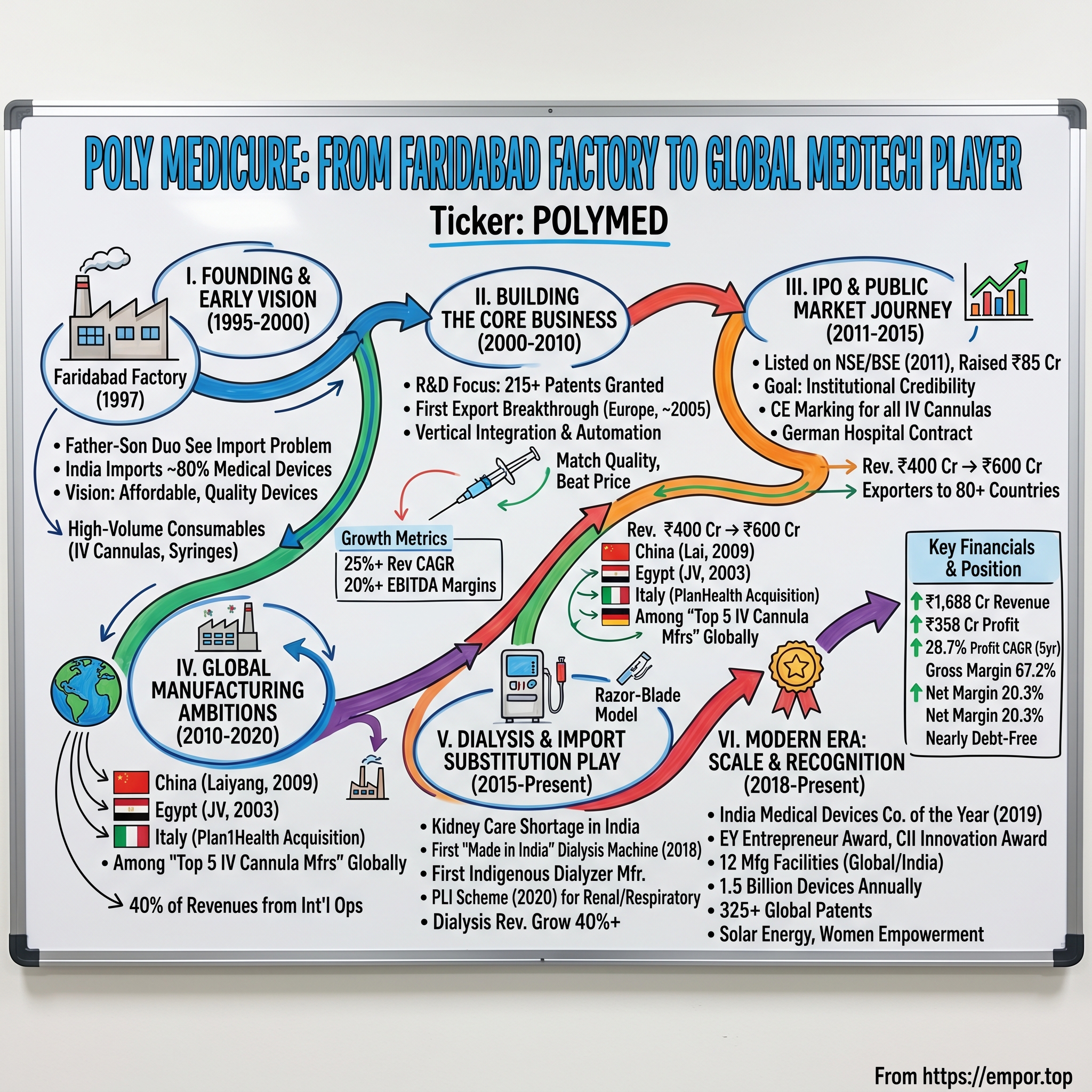

Picture this: A small factory floor in Faridabad, 1997. The air thick with the smell of polymer and sterilization chemicals. A father and son stand amid boxes of imported medical devices—IV cannulas, syringes, catheters—each stamped with foreign logos, each carrying a price tag that puts them beyond reach of most Indian hospitals. They're not doctors, but they see the problem clearly: India, with its billion-plus population, imports nearly 80% of its medical devices. Every IV drip, every blood collection tube, every surgical consumable—shipped from Europe, America, or China, marked up multiple times by the time it reaches a patient's bedside.

This is where our story begins. Not in a Silicon Valley garage or a Boston biotech lab, but in the industrial heartland of North India, where Poly Medicure would grow from that modest beginning to become a ₹19,482 crore market cap company manufacturing over 200 medical devices across 12 specialties. Today, they produce 1.5 billion devices annually, export to 125+ countries, and operate manufacturing facilities not just in India but in Egypt, China, and Italy. They've become India's first dialysis machine manufacturer, breaking a 100% import monopoly. They hold 325+ patents globally. And perhaps most remarkably, they've done it while remaining almost debt-free and maintaining a 28.7% profit CAGR over the past five years.

How does a company from Faridabad end up competing with Johnson & Johnson, Becton Dickinson, and Terumo? How do you convince German hospitals to buy IV cannulas made in India? And what does it take to build a global medical device champion from an emerging market?

This is a story about import substitution as industrial strategy, about the unglamorous but essential business of medical consumables, and about how emerging market companies can climb the value chain—from simple manufacturing to complex R&D, from local supplier to global player. It's about navigating the maze of FDA approvals, CE marks, and BIS certifications across multiple continents. And ultimately, it's about a bet that India's healthcare manufacturing could compete not just on cost, but on quality and innovation.

We'll trace Poly Medicure's journey through three distinct acts: the import substitution playbook of the early years, the global expansion ambitions of the 2010s, and the current push into high-value segments like dialysis equipment. Along the way, we'll examine the strategic decisions that shaped the company—why they went public in 2011, how they managed overseas manufacturing in politically complex markets, and why they chose to focus on consumables rather than flashier medical equipment.

The themes that emerge are particularly relevant for anyone thinking about emerging market companies: How frugal innovation can become competitive advantage. Why family businesses sometimes outperform professional management in certain contexts. And how companies from the periphery can move to the center of global supply chains.

II. The Founding Story & Early Vision (1995-2000)

The conference room at the Registrar of Companies office in Delhi, March 30, 1995. The paperwork for Poly Medicure Limited is being stamped and filed—another private limited company among thousands registered that year. But this wasn't a spontaneous startup. The founder had spent years watching India's healthcare system struggle with basic supplies. Every government tender for medical devices saw the same pattern: foreign suppliers, long lead times, prices that reflected multiple layers of distribution. The math was simple but devastating—a disposable IV cannula that cost $0.50 to manufacture in Europe would reach an Indian hospital at $2-3, putting even basic medical care beyond reach for millions. The real catalyst came in 1997 when operations truly began. The founder's son, Himanshu Baid, joined the company towards the end of 1995, bringing together their expertise in production, sales, and marketing. This wasn't a Silicon Valley story of college dropouts with a big idea—this was deliberate, methodical, almost conservative in its ambition. Start with products you understand. Build quality that matches imports. Price it at 30-40% less. Scale slowly but steadily.

The Faridabad factory that opened in 1997 was modest—a few thousand square feet, basic injection molding machines, manual assembly lines. But look closer and you'd see something important: clean rooms built to international standards, quality control processes that mirrored FDA guidelines, documentation systems that could eventually support global certifications. The vision from day one was providing affordable medical devices to society, but affordability without quality was a non-starter in medical devices. A contaminated IV cannula doesn't just lose you a customer—it can kill a patient.

The product choice was strategic. IV cannulas, syringes, blood collection tubes—these aren't glamorous. No one wins Nobel prizes for a better syringe. But they're used by the millions every single day in every hospital, clinic, and diagnostic center. They're essential, consumable, and at that time, almost entirely imported. The market was massive, fragmented, and ripe for disruption by anyone who could match quality at a better price point.

What made this particularly audacious was the competitive landscape. Becton Dickinson had been making syringes since 1906. Terumo, B. Braun, Smiths Medical—these weren't startups but century-old companies with deep R&D capabilities, global distribution networks, and relationships with every major hospital system in the world. For a company in Faridabad to say "we'll compete with them" required either remarkable naivety or exceptional confidence.

The early years were about proving a simple thesis: Indian manufacturing could meet international quality standards in medical devices. Each small victory—a successful batch, a hospital trial, an export order—built credibility. By 2000, Poly Medicure had established that it could consistently manufacture products that met not just Indian standards but could pass muster with European and American quality requirements.

But perhaps the most important decision in these early years was what not to do. They didn't chase the high-margin, high-tech segments—no MRI machines, no robotic surgery equipment, no implantables. They stayed focused on high-volume, essential consumables where manufacturing excellence and cost efficiency mattered more than cutting-edge R&D. It was unglamorous but profitable, essential but overlooked—exactly the kind of market where an emerging market challenger could build a beachhead.

III. Building the Core Business (2000-2010)

The 2000s opened with India's healthcare sector at an inflection point. Private hospitals were proliferating—Apollo, Fortis, Max—bringing world-class healthcare to Indian cities but still dependent on imported consumables. Meanwhile, the government's push for rural healthcare meant thousands of primary health centers needed basic medical supplies. Poly Medicure sat at the intersection of both opportunities, but capturing them required a transformation from small manufacturer to scaled enterprise. The decision to focus on R&D from early on set Poly Medicure apart from typical Indian manufacturing companies of that era. By the end of the decade, the company had successfully been granted 215+ product and process patents globally and had filed for grant of an additional 250+ patents. This wasn't about breakthrough innovation—most patents covered incremental improvements in needle safety mechanisms, valve designs, or manufacturing processes. But each patent represented a barrier to entry, a quality signal to global buyers, and most importantly, freedom to operate in export markets without IP concerns.

The export breakthrough came around 2005-2006. A European distributor, frustrated with long lead times from Chinese suppliers, agreed to trial Poly Medicure's IV cannulas. The order was small—just 50,000 units—but it represented validation. The products arrived on time, passed quality checks, and most crucially, were 35% cheaper than alternatives. Word spread through the tight-knit community of medical device distributors. By 2008, Poly Medicure was shipping to 50+ countries. They had become the highest exporter of consumable medical devices from India—a position they would hold for consecutive years.

The manufacturing philosophy that emerged during this period was distinctive: vertical integration wherever possible, automation where it made sense, but always with an eye on flexibility. They manufactured their own plastic components, assembled products in clean rooms, even set up their own gamma sterilization facility—unusual for a company of their size but essential for quality control and cost management. This integration would later prove crucial when supply chains were disrupted during global crises.

By 2010, Poly Medicure operated from multiple facilities across Faridabad, employed over 1,000 people, and had revenues approaching ₹300 crores. But perhaps more importantly, they had cracked the code on competing with global giants: match their quality, beat their prices, and most crucially, be more responsive to customer needs. A hospital in Nigeria needing a custom packaging size? Done. A distributor in Eastern Europe wanting private labeling? No problem. This flexibility—impossible for a Becton Dickinson or Terumo with their standardized global operations—became Poly Medicure's competitive moat.

The numbers tell the story of steady execution: revenue CAGR of 25%+ through the decade, EBITDA margins consistently above 20%, and critically, almost no debt. This wasn't venture-funded hypergrowth but bootstrap capitalism at its finest—profits reinvested into capacity, R&D funded from cash flows, expansion financed through operations. It set a template that would define the company's approach to capital allocation for decades to come.

As 2010 drew to a close, Himanshu Baid faced a critical decision. The company had proven it could compete globally while remaining private. But the next phase of growth—international manufacturing, higher-value products, deeper R&D—would require capital and credibility that only public markets could provide.

IV. The IPO & Public Market Journey (2011-2015)

December 7, 2011. The opening bell at the National Stock Exchange rings for Poly Medicure Limited. The stock lists at ₹117, a modest premium to its issue price of ₹115. No confetti, no champagne celebrations—just Himanshu Baid and his team watching screens as their company transitions from private enterprise to public entity. The IPO raised ₹85 crores, small by today's standards but transformational for a company that had grown entirely on internal accruals. Backed by steady growth, Mr. Baid made the company public in 2011. The decision wasn't driven by immediate capital needs—the company was generating healthy cash flows and had minimal debt. Instead, it was about institutional credibility. International customers, particularly in regulated markets like Europe and the US, preferred dealing with public companies with transparent financials and governance structures. The IPO wasn't just about raising money; it was about raising the company's profile.

The early public market years tested management's resolve. The stock languished between ₹100-150 for most of 2012-2013, well below comparable medical device companies globally. Analysts questioned why an Indian company could succeed where others had failed. The medical device sector in India was littered with companies that had tried to challenge imports and failed—either unable to match quality or unable to achieve scale. Quarterly earnings calls featured the same skeptical questions: How sustainable were the margins? Could they really compete with Chinese manufacturers on price while matching Western quality?

Himanshu Baid's response was consistent and methodical. Each quarter brought incremental progress—a new certification, an additional export market, a patent grant. The company used the IPO proceeds strategically, not for flashy acquisitions but for boring essentials: upgrading clean rooms to meet FDA standards, installing automated assembly lines to reduce contamination risk, expanding the R&D team to accelerate product development. By 2013, they had received CE marking for their entire IV cannula range, opening up the European market fully.

The real validation came from customers, not investors. A major German hospital chain, after extensive quality audits, signed a three-year contract for IV cannulas—the first time they'd sourced such critical supplies from an Indian company. An American medical distributor, impressed by Poly Medicure's ability to customize packaging for different state regulations, shifted their entire blood collection tube orders from a Chinese supplier. These weren't headline-grabbing deals, but they represented something more important: trust from the world's most demanding healthcare systems.

By 2015, the transformation was evident. Revenues had grown from ₹400 crores at IPO to over ₹600 crores. The company was exporting to 80+ countries. Most importantly, they had proven that an Indian medical device company could operate to global standards—not just in manufacturing but in governance, compliance, and innovation. The stock, which had been stuck around ₹120 for years, began its steady climb, crossing ₹300 by late 2015.

What's remarkable about this period is what Poly Medicure didn't do. They didn't chase hot trends—no pivots to digital health, no ventures into medical AI. They didn't make splashy acquisitions to boost growth. They didn't even significantly expand their product categories. Instead, they did the same things, just better and at larger scale. It was a masterclass in focused execution, proving that in medical devices, consistency and reliability matter more than innovation for innovation's sake.

The IPO years also saw a crucial organizational shift. The company professionalized operations while maintaining family control—a delicate balance many Indian companies struggle with. Professional managers were brought in for specialized functions, independent directors added genuine oversight, and systems were put in place that could scale beyond founder-dependency. Yet the Baid family maintained operational control and strategic direction, ensuring continuity of vision.

As 2015 ended, Poly Medicure stood at an inflection point. They had proven they could compete globally from an Indian base. But to truly challenge the medical device oligopoly, they needed to think beyond India. The next chapter would be about taking the fight to competitors' home turf—manufacturing in China, Egypt, and even Italy.

V. Global Manufacturing Ambitions (2010-2020)

The boardroom in Faridabad, 2010. Maps spread across the table—Egypt, China, Italy. Each marked with potential factory sites, distribution networks, regulatory requirements. The conventional wisdom said Indian companies should focus on the domestic market, maybe export from India. But Himanshu Baid saw a different path. To become a global medical device player, you couldn't just export from India. You needed to be local in global markets—understanding regulations, building relationships, responding quickly to customer needs. The decision to become the first Indian medical device company with overseas manufacturing wasn't about ambition; it was about survival in a globalized industry. China came first, through the wholly-owned subsidiary Poly Medicure (Laiyang) established in 2009. The logic was counterintuitive—why manufacture in China when Chinese companies were your biggest competitors? But Baid understood something crucial: to beat Chinese manufacturers, you needed to understand their ecosystem. The Laiyang facility wasn't just about production; it was about learning. This expansion offered a chance to enhance manufacturing capacity, delve into new product markets, and leverage R&D and other newer technologies. Chinese suppliers had mastered certain polymer processing techniques that could enhance product quality. Being local meant access to this knowledge, faster iteration, and most importantly, the ability to serve Asian markets with "Made in China" products when that mattered to buyers.

Egypt followed through a joint venture established in 2003, targeting the Middle East and Africa. The Cairo facility faced challenges Western companies wouldn't touch—currency volatility, political instability, infrastructure gaps. But these were markets Poly Medicure understood. They'd dealt with similar issues in India. The Egyptian operation became a gateway to 40+ African countries where European products were too expensive and Chinese products faced quality skepticism. An Indian company, manufacturing in Egypt, hit the sweet spot of acceptable quality at affordable prices.

The real coup came with Italy. Polymed acquired Plan1Health S.R.L., an Italy based manufacturing company which opened opportunities to enhance global customer base and helped the company gain access to new technologies in oncology and vascular access. Plan1 Health products adhere to the highest quality standards in Europe as they have ISO, CE, MDSAP and EU-MDR certifications. For a company from Faridabad to own a manufacturing facility in Italy—the heart of European medical device manufacturing—was audacious. But it solved a critical problem: European hospitals preferred "Made in EU" products for certain categories. The Italian facility gave Poly Medicure instant credibility and access to technologies in oncology and vascular access that would have taken years to develop independently.

Managing this global manufacturing network required a different organizational capability. You couldn't run a factory in Egypt the same way you ran one in Faridabad. Each location needed local management who understood regulations, labor practices, and customer preferences, but all had to maintain Poly Medicure's quality standards. The company developed what they called "glocal" management—global standards, local execution. Quality protocols were non-negotiable and standardized worldwide. But everything else—supplier relationships, workforce management, even product mix—was localized.

The numbers validated the strategy. By 2015, international operations contributed 40% of revenues. More importantly, they provided natural hedging against currency fluctuations and country-specific risks. When the Indian rupee weakened, export revenues provided cushion. When European demand softened, Asian markets compensated. The company had transformed from an Indian exporter to a truly global manufacturer.

But perhaps the most significant achievement was becoming among the 'Top 5 I.V. Cannula Manufacturers in the World'. This wasn't a self-proclaimed title but recognition from industry analysts. Five companies dominated 70% of the global IV cannula market—Becton Dickinson, B. Braun, Terumo, Smiths Medical, and now Poly Medicure. For an Indian company to break into this oligopoly was unprecedented.

The global expansion also drove innovation. Each market had unique requirements—the Chinese wanted ultra-thin wall cannulas for pediatric use, Middle Eastern markets needed products that could withstand extreme heat during transport, European customers demanded eco-friendly packaging. Meeting these diverse needs pushed Poly Medicure's R&D beyond what domestic market alone would have required. The patent portfolio expanded to 300+ grants, covering not just products but manufacturing processes, packaging innovations, and sterilization techniques.

As the decade closed, Poly Medicure had achieved what seemed impossible in 2010—becoming the first Indian medical devices company to have manufacturing facilities outside India. With 3 overseas manufacturing plants in Egypt (joint venture), China (wholly owned subsidiary) and Italy, Polymed exports medical devices to 125+ countries. They weren't just competing with global giants; they were beating them in specific markets and segments. The boy from Faridabad had taken on the world—and won.

VI. The Dialysis & Import Substitution Play (2015-Present)

The conference room at AIIMS Delhi, 2015. Government officials, nephrologists, and industry representatives gathered to discuss a crisis: India had 200,000 patients needing dialysis, but only 35,000 were getting treatment. The primary barrier wasn't medical expertise but equipment cost. Every dialysis machine was imported, mostly from Germany and Japan, costing ₹15-20 lakhs each. Every dialyzer (the artificial kidney used in each session) came from abroad at ₹800-1,500 per piece. For a country where 70% of healthcare spending was out-of-pocket, these prices meant death sentences for thousands. Himanshu Baid saw opportunity where others saw impossibility. Sensing the shortage of equitable and affordable access to kidney care in India and to reduce 100% import dependence on dialysis products, Polymed ventured into manufacturing dialysis equipment and other accessories used in the process. The technical challenges were immense. Dialysis machines involve complex fluid dynamics, precise filtration membranes, and electronic controls that must work flawlessly—a patient's life depends on every session. The dialyzer, often called the artificial kidney, requires hollow fiber membranes with pore sizes measured in nanometers. This wasn't IV cannula manufacturing; this was precision engineering.

The company's approach was methodical. First, they partnered with nephrologists to understand exact requirements. What frustrated doctors about imported machines? What features did Indian conditions require? The answers were revealing: machines that could handle voltage fluctuations common in tier-2 cities, dialyzers that could work with varying water quality, interfaces in local languages for technicians. These weren't innovations that would win design awards, but they addressed real problems.

The R&D investment was massive by Poly Medicure's standards—over ₹50 crores over three years. They set up a dedicated facility in Faridabad with clean rooms meeting ISO Class 7 standards. Engineers were recruited from companies like Wipro GE Healthcare. Most crucially, they brought in consultants who had worked with Fresenius and B. Braun—learning from competitors without copying.

The breakthrough came in 2018. The company manufactured India's first BIS Certified 'Made in India' dialysis machine and is the first Indigenous Dialyzer Manufacturer in India. The BIS (Bureau of Indian Standards) certification was crucial—it meant government hospitals could procure these machines. The first machine rolled out at ₹8 lakhs, less than half the cost of imports. The dialyzer was priced at ₹400-500, making treatment accessible to thousands more patients.

But the real accelerator came with the government's Production Linked Incentive (PLI) scheme in 2020. We have already applied for the PLI scheme. I feel, there is a lot of potential in renal space and respiratory care space in India. At present, around 90% of the renal products are imported in India and if the PLI scheme is approved then we will ramp-up our investment a lot. We will try to make India Atmanirbhar in the next 4-5 years under this sector. Poly Medicure applied for a PLI grant in 2020 and got approval for manufacturing a dialyser, dialysis machine, peritoneal dialysis kits, fistula, bloodline, haemodialysis catheter, and transducer protector.

The PLI scheme provided 5% incentive on incremental sales for five years—crucial support for a capital-intensive segment with long gestation periods. The Jaipur plant which falls under SEZ has been established to push for exports as there is a lot of potential in export in products like Catheter, while the Faridabad plant has been established especially for dialysis products. This wasn't just about serving Indian markets; Poly Medicure saw opportunity to export to other emerging markets facing similar challenges—Africa, Southeast Asia, Latin America.

The economics of the dialysis business were compelling. A dialysis center with 10 machines treating 4 patients per day each could generate ₹5-6 crores annual revenue. With Poly Medicure's machines and consumables, the capital investment dropped from ₹2 crores to ₹1 crore. Operating costs fell by 30-40%. Suddenly, dialysis centers became viable in tier-3 cities, not just metros. Private hospital chains like Apollo and Fortis, initially skeptical, began trials. When the machines performed reliably over thousands of cycles, orders followed.

The strategic implications went beyond immediate revenues. Dialysis created an ecosystem play—once a hospital installed Poly Medicure machines, they needed ongoing supplies of dialyzers, bloodlines, fistula needles, and other consumables. A single machine could generate ₹10-15 lakhs in annual consumable sales. It was the classic razor-and-blade model, but with life-saving implications.

The company acknowledges the Government of India's initiative to promote Make in India products and also thanks Government of India for reducing custom duty on parts /raw materials to make Dialyzer (artificial kidney) used in Dialysis treatment. This initiative will help in reduction of manufacturing cost for dialyzers (artificial kidney) and in turn reduce cost of Dialysis treatment to patients. These policy changes, combined with Poly Medicure's manufacturing capabilities, created a perfect storm for import substitution.

By 2023, the results were tangible. The dialysis segment contributed over ₹150 crores to revenues, growing at 40%+ annually. More importantly, Poly Medicure had proven they could compete in high-technology segments, not just commoditized consumables. They weren't just making syringes anymore; they were saving lives with complex medical equipment that even developed country manufacturers struggled to produce cost-effectively.

The dialysis success opened doors to other import substitution opportunities—ventilators post-COVID, cardiac stents, orthopedic implants. Each represented billions in imports, each an opportunity for an Indian manufacturer willing to invest in R&D and navigate regulatory complexities. For investors, it signaled a company transitioning from commodity medical devices to value-added products with higher margins and stronger competitive moats.

VII. Modern Era: Scale, Awards & Recognition (2018-Present)

The Vigyan Bhavan auditorium, New Delhi, 2019. The Minister of Chemicals and Fertilizers takes the stage to announce the "India Medical Devices Company of the Year" award. When Poly Medicure's name is called, it's more than corporate recognition—it's validation of a 25-year journey from a Faridabad startup to national champion. The government, which once saw medical devices as a sector to regulate, now celebrated it as strategic for India's healthcare sovereignty. The awards kept coming. 2024: Himanshu Baid wins EY Entrepreneur of the Year in Life Sciences & Healthcare. The CII "Top 50 Innovative Companies Award". Making it to Fortune's "The Next 500 Companies in India" list for three consecutive years. Each recognition built credibility, but more importantly, they reflected genuine transformation. With 12 manufacturing facilities in India and globally, Poly Medicure has an astounding manufacturing capacity of over 1.5 billion devices per year across multiple product segments.

The scale achieved by 2024 was staggering for a company that started with one small factory. 4000+ employees across 12 manufacturing facilities. 1.5 billion devices manufactured annually—enough to serve every hospital bed in India multiple times over. The facilities themselves had evolved—350+ molding machines, 1500+ molds and dies, 200+ automatic assembly machines, 100+ robots. Under his visionary leadership, Poly Medicure has strategically embraced automation to drive capacity expansion. This wasn't just about replacing labor with machines; it was about achieving consistency and quality at scale that manual processes could never deliver.

The automation strategy was particularly sophisticated. Unlike Western competitors who automated everything, Poly Medicure selective automated. High-precision operations like needle grinding and catheter tip forming—fully automated. But final assembly and quality inspection for complex products—still manual, leveraging India's skilled workforce advantage. This hybrid approach delivered Western quality at Indian costs, the holy grail of emerging market manufacturing.

Sustainability became a strategic differentiator, not just CSR checkbox. Poly Medicure produces 1,392MWh of solar energy and has implemented digital measures to reduce CO2 emissions. For European customers increasingly demanding carbon-neutral supply chains, this mattered. The Faridabad facility's rooftop solar installation wasn't just about electricity cost savings—though it saved ₹2 crores annually—it was about meeting global customer expectations. Water recycling systems, biodegradable packaging research, zero liquid discharge plants—each initiative small individually but collectively repositioning Poly Medicure as a responsible global supplier.

The patent portfolio expansion to 325+ grants globally represented another form of recognition—from competitors and regulators. These weren't breakthrough innovations but thousands of incremental improvements. A safety mechanism preventing needle stick injuries. A valve design reducing blood reflux. A packaging system maintaining sterility longer. Each patent a small moat, together forming a formidable barrier to competition. More importantly, they provided freedom to operate in litigious markets like the US where patent disputes could destroy businesses overnight.

The CSR initiatives, running across Faridabad, Jaipur, and Haridwar districts, went beyond typical corporate philanthropy. He is also committed to empowering women and the specially abled. The company employed over 1,000 women in assembly operations, provided skill training to 500+ disabled individuals, and supported 150+ students annually with scholarships. This wasn't just social responsibility—it was building a sustainable talent pipeline in communities where they operated.

Market recognition translated to financial performance. Stock price crossed ₹2,000 in 2024, up 20x from the IPO price. Market capitalization exceeded ₹19,000 crores, making it one of India's most valuable medical device companies. But perhaps more tellingly, institutional ownership increased from 5% in 2015 to over 35% by 2024. Sophisticated investors—mutual funds, insurance companies, foreign portfolio investors—were betting on Poly Medicure's future.

The recognition from the government was particularly significant. Being awarded "India Medical Devices Company of the Year" by Department of Pharmaceutical Ministry of Chemical & Fertilizer, Government of India wasn't just ceremonial. It meant preferential treatment in government tenders, support for export initiatives, and most importantly, validation for hospital customers still skeptical about Indian medical devices. When AIIMS Delhi, India's premier medical institution, chose Poly Medicure products for critical care units, it sent a signal across the healthcare system.

As we entered 2024, Poly Medicure had achieved what seemed impossible in 1997—becoming a globally recognized medical device manufacturer from India. They weren't just competing anymore; they were winning. Top 5 global IV cannula manufacturer. India's largest medical device exporter for 10 consecutive years. Manufacturing in four countries, selling in 125+. The boy from Faridabad hadn't just built a company; he'd built an institution.

VIII. Financial Performance & Market Position

The numbers tell a story of relentless execution. Current metrics: ₹1,688 Cr revenue, ₹358 Cr profit. Almost debt-free operations. 28.7% profit CAGR over 5 years. These aren't tech startup numbers with hockey stick growth and massive losses. This is old-school capitalism—make products, sell them for more than they cost, reinvest profits, repeat. But the simplicity masks sophisticated financial engineering and capital allocation that would make Warren Buffett proud. The latest Q1 FY26 results tell the operational story: Revenue from operations rose to ₹403.21 crore in Q1 FY26, a 4.8% increase from ₹384.78 crore in Q1 FY25, driven by sustained demand for its medical devices across key markets. But look deeper: Profit before tax surged 26.3% YoY to ₹122.94 crore from ₹97.28 crore, reflecting strong operational efficiency and cost management. Net profit climbed 25.8% to ₹93.08 crore from ₹74.03 crore. Profit growing faster than revenue—the holy grail of operating leverage.

The margin story is where Poly Medicure really shines. Poly Medicure's trailing twelve months (TTM) gross margin is 67.21%. For a manufacturing company, these are software-like margins. How? Vertical integration, automated production, and critically, product mix shifting toward higher-value items. An IV cannula might have 40% gross margin; a dialysis machine, 70%+. As the product mix evolves, so do the margins.

Poly Medicure's trailing twelve months (TTM) net profit margin is 20.27%. In an industry where global giants like Medtronic and Abbott operate at 15-18% net margins, this is remarkable. The secret: minimal sales and marketing expenses (selling to distributors, not end customers), low R&D costs relative to revenue (incremental innovation, not moonshots), and critically, almost zero debt servicing costs.

Speaking of debt, Poly Medicure's total debt-to-equity ratio is 6.52%—essentially debt-free. In a capital-intensive industry where competitors routinely carry debt-to-equity ratios of 50-100%, this provides enormous strategic flexibility. No interest payments eating into profits. No covenant restrictions limiting growth investments. No refinancing risks during downturns. Warren Buffett famously said, "When you combine ignorance and leverage, you get some pretty interesting results." Poly Medicure chose knowledge and no leverage—boring but beautiful.

The working capital management deserves attention. Working capital days have increased from 143 days to 305 days—concerning at first glance. But context matters. The company is extending credit to establish new distributor relationships in Latin America and Africa, strategic investments in market access. More importantly, with strong cash generation, they can afford this working capital expansion without stress.

Stock trading at 52.3 P/E, 7.04x book value—expensive by traditional metrics. But compare to global medical device peers: Edwards Lifesciences trades at 45x P/E, Intuitive Surgical at 65x, even mature players like Stryker at 30x. For a company growing at 20%+ with expanding margins and massive import substitution opportunity ahead, the valuation starts making sense.

Promoter Holding: 62.4%—skin in the game that aligns management with shareholders. The Baid family hasn't sold a single share since IPO, instead participating in every capital raise to maintain their stake. This isn't a company being dressed up for sale; it's a multi-generational enterprise being built.

The capital allocation framework is textbook efficient. First priority: organic growth capex, earning 30%+ returns. Second: strategic acquisitions like the Italian facility, bringing technology and market access. Third: modest dividends, signaling confidence without depleting growth capital. No buybacks, no financial engineering—just reinvestment in high-return opportunities.

Baid said that the company has already given guidance for overall growth to be around 20 per cent for the full financial year. Conservative guidance has been Poly Medicure's hallmark—underpromise, overdeliver. The street expects 18-22% revenue CAGR over the next three years, driven by dialysis expansion, new product launches, and geographic expansion.

The unit economics tell the real story. An IV cannula sells for ₹30-50, costs ₹15-20 to make, generates ₹15-30 gross profit. Multiply by 500 million units annually, and you have a ₹750-1,500 crore gross profit engine from just one product category. Layer on blood tubes, catheters, dialysis consumables—each with similar economics—and the profit generation becomes clear.

But perhaps most impressive is the return on invested capital (ROIC). With minimal debt and efficient operations, Poly Medicure's trailing twelve months (TTM) return on investment (ROI) is 15.99%. For every rupee invested, they generate 16 paise in returns—not spectacular by tech standards but exceptional for manufacturing. More importantly, incremental ROIC on new investments exceeds 25%, suggesting returns will improve as new capacity comes online.

IX. Playbook: Lessons for Emerging Market Companies

The Poly Medicure story offers a masterclass in how emerging market companies can compete globally without losing their souls or their shirts. The playbook isn't about disruption or blitzscaling—it's about patient execution, strategic focus, and turning perceived disadvantages into competitive advantages.

Import Substitution as Business Strategy: The genius wasn't identifying that India imported 80% of medical devices—everyone knew that. It was understanding which imports to target. Not the flashy, high-tech segments where R&D requirements would drain capital. Not commodities where Chinese manufacturers had unbeatable scale. But the middle ground—products complex enough to have barriers to entry but simple enough to manufacture with existing capabilities. IV cannulas, blood collection tubes, catheters—unsexy but essential.

The import substitution strategy also provided natural protection during growth phase. While building capabilities, Poly Medicure could rely on patriotic purchasing preferences, government support, and cost advantages in the domestic market. Only after achieving scale and quality did they venture into exports, reversing the typical emerging market trajectory of export first, domestic later.

Building Trust from the Periphery: How does a company from Faridabad convince a German hospital to buy life-critical medical devices? Not through marketing or salesmanship but through systematic trust building. Start with less critical products—bandages, syringes. Deliver flawlessly for years. Then gradually move up the value chain—IV cannulas, blood bags, dialysis consumables. By the time you're selling dialysis machines, you have a 20-year track record.

The quality strategy was particularly clever. Rather than claiming "as good as Western products," Poly Medicure pursued Western certifications—FDA, CE marking, ISO standards. When your products pass the same tests as Becton Dickinson's, quality debates become moot. The certifications cost millions but provided billions in credibility.

Patent Strategy for Emerging Markets: With our strong R&D initiatives, the Company have successfully been granted 215+ product and process patents globally and have also filed for grant of an additional 250+ patents. But these aren't breakthrough innovations. They're incremental improvements—a safer needle mechanism, a better seal design, an improved sterilization process. Each patent individually minor, collectively forming a defensive moat.

The patent strategy serves three purposes. First, freedom to operate in litigious markets. Second, signaling to customers about innovation capabilities. Third, and most importantly, preventing copycat competition from other emerging market players. Chinese competitors might match Poly Medicure's costs but can't copy their patented designs without legal risk.

Family Business Professionalization: The Baid family's approach to professionalization offers lessons for family businesses globally. Maintain family control of strategy and vision but hire professionals for specialized functions. The CFO, heads of R&D, manufacturing heads—all professionals with global experience. But key decisions—capital allocation, market entry, product strategy—remain with the family.

This hybrid model provides continuity (important for long-term supplier relationships) while bringing professional expertise. It also solves the succession challenge—the next generation can focus on strategic decisions while professionals handle operations.

Balancing Domestic and Export Growth: Revenue from the international market, which contributes approximately 70 per cent of the company's consolidated revenue. But this wasn't always the case. Early years focused on India, building scale and capabilities. Then gradual export expansion, starting with similar markets (Africa, Middle East) before tackling developed markets.

The balance provides resilience. When Indian healthcare spending slows, exports compensate. When global markets face headwinds, domestic demand provides stability. Currency movements become natural hedges rather than risks. No single market or customer becomes dominant enough to dictate terms.

ESG Integration Before It Was Cool: Poly Medicure produces 1,392MWh of solar energy and has implemented digital measures to reduce CO2 emissions. But this isn't greenwashing. For a company selling to European hospitals increasingly focused on supply chain sustainability, renewable energy and carbon reduction are competitive advantages.

The CSR initiatives—employing 1,000+ women, training disabled workers, supporting local education—create community goodwill essential for smooth operations. When you need to expand a factory or get regulatory approvals, community support matters. It's strategic CSR, not charity.

The "Make in India" Opportunity: Poly Medicure positioned perfectly for India's push toward medical device self-sufficiency. The PLI scheme, import duties on finished products but not raw materials, government procurement preferences—all policy tailwinds. But critically, they were ready when policies changed, having spent decades building capabilities.

The lesson: anticipate policy shifts and position accordingly. Governments worldwide are reconsidering healthcare supply chain dependencies post-COVID. Companies with domestic manufacturing capabilities in large markets will benefit. Poly Medicure's India focus, once seen as limiting, now looks prescient.

X. Analysis: Bull vs. Bear Case

Bull Case: The $50 Billion Opportunity

The numbers are staggering. India's medical device market, currently at $12 billion, expected to reach $50 billion by 2030. Even maintaining current market share would quadruple Poly Medicure's revenues. But the real opportunity is import substitution. At present, around 90% of the renal products are imported in India. Similar ratios exist for cardiac devices, orthopedic implants, diagnostic equipment. Each percentage point of import substitution represents hundreds of crores in revenue opportunity.

The competitive advantages compound over time. Manufacturing scale drives lower costs. Lower costs enable price competition. Market share gains provide more scale. It's a virtuous cycle that, once established, becomes difficult for competitors to break. Poly Medicure has reached escape velocity in several categories—IV cannulas, blood collection tubes—where they now have sustainable competitive advantages.

Emerging market demographics provide multi-decade tailwinds. Healthcare spending in India, China, Africa, and Latin America growing at 10-15% annually. These markets need affordable, reliable medical devices—exactly Poly Medicure's sweet spot. Western competitors find these markets difficult (price points too low) while Chinese competitors face quality skepticism. Poly Medicure sits perfectly in the middle.

The technology disruption in medical devices—AI, robotics, digital health—might seem threatening but could actually benefit Poly Medicure. These technologies will be applied first to high-value procedures in developed markets. The billions of basic procedures in emerging markets will still need traditional consumables for decades. Poly Medicure can focus on volume while others chase innovation.

Valuation remains reasonable despite recent gains. At 52x P/E, expensive versus historical averages but cheap versus global peers and growth potential. If Poly Medicure achieves its 2030 targets—₹5,000 crore revenue, 25% margins—the stock could triple from current levels. Not without risk, but asymmetric risk-reward for patient investors.

Bear Case: The Commodity Trap

The biggest risk is commoditization. IV cannulas, syringes, blood tubes—these aren't differentiated products. As Chinese manufacturers improve quality and Indian competitors scale up, margins could compress dramatically. We've seen this movie before in APIs, textiles, auto components—initial success followed by margin collapse as competition intensifies.

Regulatory risks loom large. By the end of FY26, the company is expecting to have around 10 to 12 products in the US, which would be approved by the FDA. But FDA approvals can be withdrawn, standards can change, recalls can destroy reputations overnight. Operating across 125 countries means navigating 125 different regulatory regimes—a single major recall or regulatory action could damage the entire business.

Currency and geopolitical risks are real and growing. However, this foreign push comes at a time when the device maker is seeing headwinds arising out of short-term demand uncertainties due to on-going geopolitical tensions and tariff issues. "We are monitoring the evolving situation closely. For now, our plans for the US market remain unchanged," Himanshu Baid, managing director of Poly Medicure, told Business Standard. Trade wars, currency volatility, sanctions—any could disrupt Poly Medicure's carefully constructed global supply chains.

The China dependence is concerning. Manufacturing in China, competing with Chinese companies, dependent on Chinese raw materials—this creates multiple vulnerabilities. If China decides to support domestic champions through subsidies or restrict raw material exports, Poly Medicure could face existential challenges.

Technology disruption remains a long-term threat. Yes, emerging markets will use traditional devices longer, but eventually, innovation reaches everywhere. Digital health, remote monitoring, AI-driven diagnostics—these could reduce demand for traditional consumables. Poly Medicure's R&D, while impressive for an Indian company, can't match the billions spent by Western giants.

Management succession is untested. Himanshu Baid has led the company brilliantly, but he's been CEO since inception. No succession plan is public. Family businesses often struggle with transitions. The next generation might lack the founder's vision or drive. Professional management might optimize for short-term profits over long-term building.

XI. The Future & Strategic Questions

The Poly Medicure boardroom, 2030. Himanshu Baid, now in his 60s, looks at a world map covered in pins—each representing a Poly Medicure facility or major customer. The company has achieved its ₹5,000 crore revenue target, operates 20 manufacturing facilities globally, and ranks among the top 10 medical device companies by volume. But the strategic questions have only gotten harder.

Can Poly Medicure Become a Global Top 10 Player?

By revenue, the top 10 medical device companies are giants—Medtronic ($30 billion), Johnson & Johnson ($25 billion), Abbott ($15 billion). Poly Medicure at ₹5,000 crores ($600 million) isn't even close. But by volume? By number of procedures supported? By lives touched? The metrics change the game. If you count every IV cannula, every blood tube, every dialysis session—Poly Medicure already ranks among global leaders in unit terms.

The path to top 10 requires a strategic choice: remain focused on high-volume consumables or expand into high-value equipment? The consumables focus has worked brilliantly, but growth might require entering surgical robotics, imaging equipment, or implantables—categories with different economics, capabilities, and risks.

M&A Opportunities and Capital Allocation

Poly Medicure reports no deviation in utilization of Rs 999.9998 crore QIP proceeds for June 2025 quarter. With nearly ₹1,000 crores raised in recent QIP and strong cash generation, Poly Medicure has firepower for acquisitions. But what to buy? Western companies with technology but struggling financially? Chinese competitors to eliminate competition? Downstream distributors to control market access?

The Italian acquisition provided a template—buy for technology and market access, not just capacity. But larger acquisitions bring integration challenges. Can Poly Medicure maintain its culture and cost structure while absorbing Western companies with different DNA?

Technology Disruption: Threat or Opportunity?

AI and robotics will transform medical devices, but how? Poly Medicure's approach—using automation for manufacturing efficiency rather than product innovation—has worked so far. But at some point, products themselves must evolve. Smart IV cannulas that monitor flow rates. Blood tubes with integrated diagnostics. Dialysis machines that adjust parameters automatically.

The company faces a classic innovator's dilemma. Invest heavily in unproven technologies that might cannibalize existing products? Or focus on current strengths and risk disruption? The answer likely lies in partnerships—collaborate with tech companies for innovation while maintaining manufacturing excellence.

The Next Frontier: High-Value Segments

Alongside dialysis, Poly Medicure will also focus on cardiology and oncology product lines. "However, scaling these up, especially to a global level, will take about two to three years. The idea is to first establish a strong presence in the Indian market, and then scale globally," he added. Cardiology and oncology represent massive opportunities but different challenges. Cardiac stents, cancer diagnostics, surgical implants—these require different R&D capabilities, regulatory pathways, and customer relationships.

The strategic question: build or buy these capabilities? Organic development takes time but maintains culture and cost structure. Acquisitions provide immediate capability but bring integration risks. The answer might be hybrid—acquire technology platforms but develop products internally.

Succession Planning and Next Generation Leadership

Every family business faces this challenge eventually. Himanshu Baid has built Poly Medicure from startup to global player, but what next? Does the next generation have the same hunger? Should professional management take over? How to maintain entrepreneurial culture while institutionalizing processes?

The best family businesses solve this through gradual transition. Next generation leaders work their way up, proving themselves at each level. Professional managers handle operations while family maintains strategic control. Board independence increases while family values persist. It's a delicate balance that determines whether companies survive generational transitions.

The Geopolitical Chess Game

Medical devices are becoming strategic assets. COVID showed the vulnerability of depending on imports for critical healthcare supplies. Governments worldwide are reconsidering supply chain dependencies. For Poly Medicure, this creates opportunities (import substitution support) and risks (protectionism in export markets).

The company must navigate carefully. Manufacturing in multiple countries provides options but increases complexity. Serving all markets while avoiding geopolitical crossfire requires diplomatic finesse. The decision to manufacture in China while competing with Chinese companies exemplifies these complexities.

Looking ahead, the biggest question might be identity. Is Poly Medicure an Indian company that exports? A global company from India? Or a truly multinational corporation? The answer determines everything from capital allocation to talent strategy to market positioning. As the company enters its fourth decade, these strategic questions will determine whether Poly Medicure becomes a footnote in India's industrial history or a global medical device champion that happens to have started in Faridabad.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube