Paramount Communications: The Cable Infrastructure Story of India

I. Introduction & Episode Framework

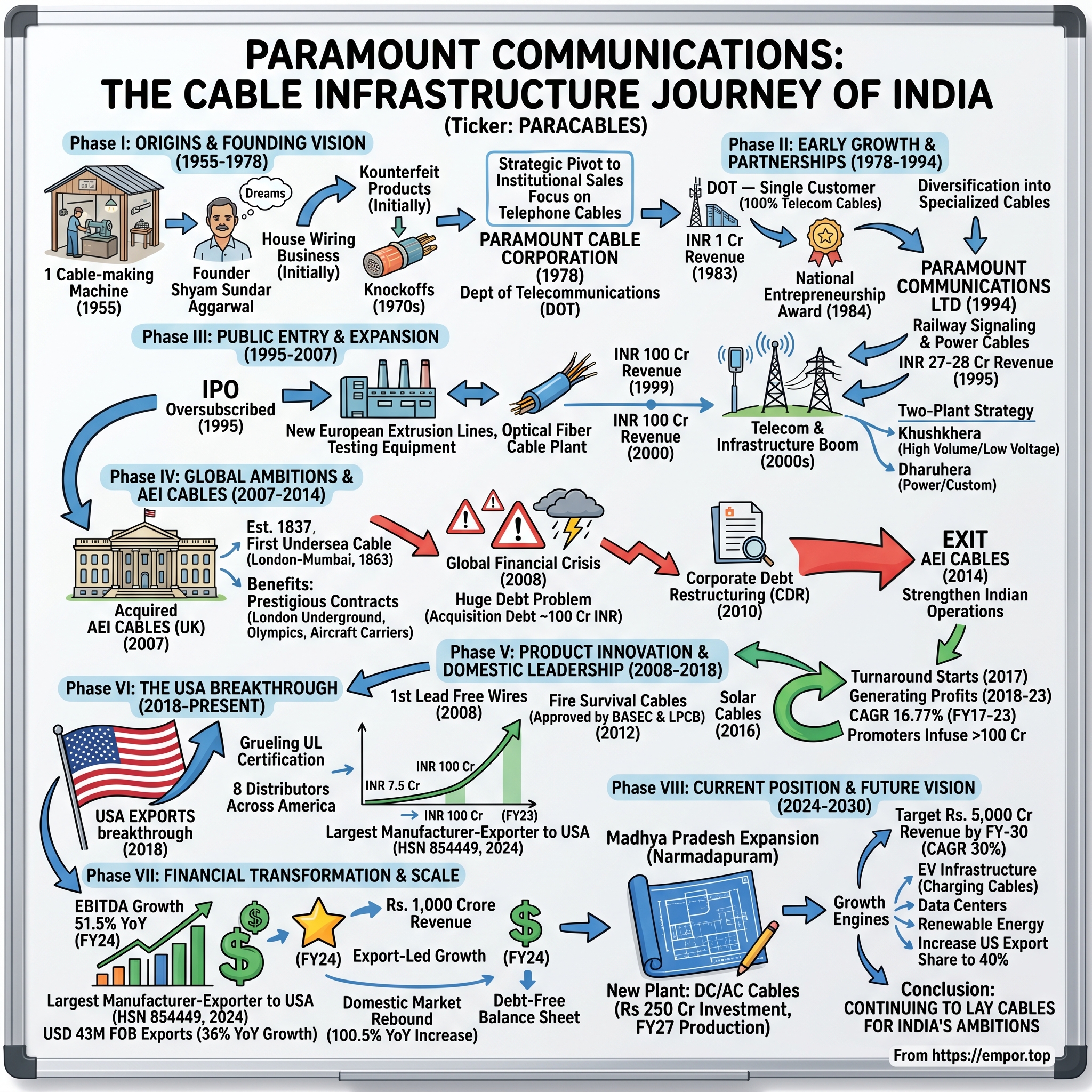

Picture a small workshop in 1955 Delhi—one cable-making machine humming away, a handful of workers carefully winding copper wire. The founder, Shyam Sundar Aggarwal, watches his modest operation with dreams far exceeding the cramped quarters. Fast forward to fiscal year 2024, and Paramount Communications crossed a landmark ₹1,000 crore revenue milestone, marking a growth of 34.4% year-over-year—a journey from that single machine to becoming India's cable infrastructure backbone.

Here's the remarkable hook: The company has led the industry in direct US exports, recording a remarkable USD 43 million in Free on-board (FOB) exports for the year, representing a 36% growth compared to USD 31 million in FOB exports in 2023. How did a family business battling counterfeit products in the 1970s transform into India's largest cable exporter to the USA?

Paramount Communications Ltd, part of the Paramount Cables Group, is one of India's leading wire & cable manufacturing company. With over six decades of operations, the group has built up a portfolio spanning a comprehensive range including HV & LV Power Cables, Optical Fiber Cables & other Telecom Cables, Railway Cables, Specialised Cables, Instrumentation & Data Cables, Fire Survival Cables etc.

This is a story of three pivotal transformations: the shift from consumer to institutional sales when faced with cheap knockoffs, the bold international acquisition that nearly broke the company, and the patient decade-long journey to crack the American market. It's about building capabilities before markets exist, strategic retreats when pride says push forward, and the unglamorous work of laying cables that power a nation's dreams.

II. Origins & Founding Vision (1955-1978)

The monsoon of 1955 brought more than rain to Delhi—it marked the birth of what would become a cable empire. In the year 1955, a small-scale cable manufacturing unit was set up as a family venture by Late Mr. Shyam Sunder Aggarwal, the founder chairman. Following its success, he established a new unit under the name of Paramount Cable Corporation in the year 1978 and started supplying telecom cables to the Department of Telecommunications.

The timing was both challenging and opportune. Post-independence India was building everything from scratch—power grids, telephone networks, railway systems. The License Raj meant navigating Byzantine bureaucracy, but it also meant protected markets for those who could deliver quality. Aggarwal's genius lay not in fighting the system but in becoming indispensable to it.

Founded in 1955 by the late Shri Shyam Sundar Aggarwal, Paramount Cables started as a house wiring business. However, the rise of counterfeit products in the late 1970s led to a strategic pivot towards institutional sales, focusing on telephone cables. This pivot would define Paramount's DNA—when cheap imitations flooded the consumer market, rather than race to the bottom, they moved upmarket to where quality certification mattered.

The workshop expanded slowly through the 1960s and early 1970s. Each new machine was a calculated bet, each new employee carefully chosen. Aggarwal built relationships patiently with government procurement officers, understanding that in the License Raj, trust was the ultimate currency. By 1978, he was ready for the big leap—incorporating as Paramount Cable Corporation and formally entering the government supply chain.

III. Early Growth & Government Partnerships (1978-1994)

The transformation from family workshop to serious industrial player began with a crucial government contract. By 1983, Paramount had reached INR 1 crore in revenue, supplying 100 percent of its telecom cables to the Department of Telecommunication (DOT). That's right—every rupee of revenue came from a single customer. In most business schools, this would be a case study in concentration risk. For Paramount, it was the foundation of an empire.

Diversification began with the manufacturing of specialized cables in the early 1980s. In the year 1984, it was the first company to be awarded the National Entrepreneurship Award by the President of India for Outstanding Achievement in the field of wire and cable manufacturing. The award wasn't just recognition—it was validation that a small Delhi company could compete with established industrial houses.

The 1980s saw Paramount methodically adding capabilities. Railway signaling cables came next, requiring different specifications and tolerances. Each new product line meant new certifications, new testing equipment, new quality processes. Over time, the company expanded into railway signalling cables and power cables, reaching INR 27-28 crore by 1995.

What distinguished Paramount wasn't technological breakthroughs—cable manufacturing isn't rocket science. It was execution discipline in an era when Indian manufacturing was synonymous with delays and quality issues. When the railways needed cables that could withstand vibration and weather extremes, Paramount delivered. When telecom needed cables with precise impedance characteristics, they invested in the testing equipment to guarantee it.

These humble beginnings with years of hard work, eventually transformed into Paramount Communications Limited and grew manifold to become one of the largest and most trusted names in the Indian cable manufacturing industry. The conversion to Paramount Communications Ltd in 1994 wasn't just a name change—it signaled ambitions beyond being a reliable government supplier.

IV. Public Market Entry & Rapid Expansion (1995-2000)

The liberalization of 1991 had unleashed animal spirits across Indian industry, but Paramount waited until 1995 to tap public markets. The timing was deliberate—they wanted a track record post-liberalization, proof they could compete without government protection. When the IPO finally came, it was oversubscribed, with investors betting on India's infrastructure boom.

The capital infusion transformed operations. New high-speed extrusion lines from Europe. Testing equipment that could verify cable performance to international standards. Most critically, working capital to bid for larger contracts. A successful IPO further fuelled growth, and by 2000, Paramount had set up an optical fiber cable plant, surpassing INR 100 crore in revenue.

The late 1990s brought the telecom revolution to India. Private operators were setting up networks, mobile telephony was taking off, and everyone needed cables—lots of them. Optical Fibre Cables plant operational in 1999, positioning Paramount at the cutting edge of the communications revolution.

But success brought challenges. Competition intensified as other manufacturers saw the opportunity. Chinese imports began appearing, often at prices below Paramount's raw material costs. The company's response was characteristic—instead of lobbying for protection, they moved further up the value chain, focusing on specialized cables where quality and certification barriers were higher.

Shifted the Delhi factory to spacious new facility at Khushkhera with substantial expansion and modernization in 2000, creating one of India's most modern cable manufacturing complexes. The Khushkhera facility wasn't just bigger—it was designed for flexibility, able to switch between product lines as demand shifted.

V. The Telecom & Infrastructure Boom (2000-2007)

The new millennium brought unprecedented infrastructure spending across India. Power sector reforms meant upgrading transmission networks. The telecom boom accelerated with falling tariffs and expanding coverage. Paramount was perfectly positioned—they had the certifications, the capacity, and crucially, the track record.

Diversified into production of 11 & 33 KV, medium voltage power cables in 2005, entering the lucrative power transmission market. These weren't your household wires—medium voltage cables required sophisticated insulation technology, precise manufacturing tolerances, and rigorous testing protocols.

The two-plant strategy emerged during this period. Khushkhera focused on high-volume telecom and low-voltage products, while Dharuhera in Haryana specialized in power cables and custom orders. This wasn't just operational efficiency—it was risk management. If one plant faced issues, the other could maintain critical supplies.

Building institutional credibility became paramount (pun intended). ISO certifications, vendor approvals from power utilities, registration with railway authorities—each certificate was a moat. When Reliance was building its pan-India telecom network, they needed suppliers who could deliver consistently across locations. When NTPC was upgrading power plants, they wanted vendors with proven reliability. Paramount had both.

The numbers tell the story of explosive growth. From ₹100 crore in 2000, revenues climbed steadily, driven by both volume and value. But the real achievement wasn't the topline—it was building an organization capable of handling complexity. By 2007, they were manufacturing dozens of cable types, managing hundreds of SKUs, serving customers from Kashmir to Kanyakumari.

VI. Global Ambitions: The AEI Cables Acquisition (2007-2014)

August 2007 should have been Paramount's finest hour. In August 2007, Paramount Communications Ltd. acquired AEI Cables Limited, the third-largest cable manufacturer in the UK, established in 1837. The British company wasn't just old—it was legendary. AEI Cables had manufactured and installed the first undersea telegraph cable connecting London to Mumbai in the year 1863.

The acquisition logic was compelling. AEI brought European technology, global customer relationships, and most importantly, credibility in developed markets. The acquisition gave us access to larger export markets, and soon, we secured prestigious projects, including the five-year exclusive cable contract for the London Underground, supplies for the London Olympics, and cables for the Queen Elizabeth aircraft carriers (QE1 & QE2).

But timing is everything in business, and Paramount's timing couldn't have been worse. Acquisition was done by raising debts of ~100 Crores INR while the company had a cash balance of only INR 6.3 Cr. The additional debt raised to fund the acquisition led to a huge debt problem post the global financial crisis.

The 2008 financial crisis hit like a tsunami. The 2008 global economic crisis resulted in a major slowdown, impacting the Indian and UK economies. Construction projects were cancelled, infrastructure spending froze, and suddenly Paramount was servicing acquisition debt while revenues collapsed on both sides of the Arabian Sea.

What followed was a seven-year battle for survival. In 2010, Paramount was forced to approach the banks for restructuring of its debt under the Corporate Debt Restructuring ('CDR') program and in 2016, The bankers exited from the CDR and the Company was taken over by Invent Asset Securitization & Reconstruction Pvt. Ltd.(ARC).

The UK operations, despite winning prestigious contracts, couldn't generate enough cash to service the debt. Management faced a brutal choice—keep bleeding cash to maintain global ambitions, or swallow pride and retreat. However, economic challenges following the 2008 financial crisis led Paramount to exit AEI Cables in 2014, allowing the company to refocus on strengthening its Indian operations.

The AEI exit was painful but necessary. It taught Paramount valuable lessons about international expansion, debt leverage, and the importance of timing. But it also gave them something invaluable—knowledge of global quality standards and customer expectations that would prove crucial a decade later.

VII. Product Innovation & Domestic Leadership (2008-2018)

While wrestling with debt, Paramount did something remarkable—they kept innovating. Lesser companies might have frozen R&D, but Paramount understood that standing still meant falling behind. Became a household name with the launch of the 1st Lead Free Wires for domestic wiring in India in 2008, addressing growing environmental concerns before regulations mandated it.

The fire survival cables launched in 2012 showcased technical sophistication. Started manufacturing Fire Survival cables. Most technologically advanced FS cable. Approved by BASEC & LPCB. These weren't just fire-resistant—they maintained circuit integrity even when engulfed in flames, critical for emergency systems in hospitals, airports, and high-rises.

Diversified into production of 11 & 33 KV, medium voltage power cables while simultaneously developing capabilities in specialized segments. Solar cables came in 2016, anticipating India's renewable energy push. Each product launch required months of development, testing, and certification—investments made while servicing crushing debt.

The turnaround began slowly. Turnaround starts in 2017 and the company starts generating profits between 2018-23 on the back of quality products and loyal clientele. Promoters infuse more than INR 100 Cr during this time. Revenue from Operations grew at a CAGR of 16.77% between FY17 and FY23, despite the lack of working capital support from banks.

This period demonstrated Paramount's resilience. While struggling with debt, they maintained quality, kept customer relationships intact, and continued investing in capabilities. When banks wouldn't provide working capital, they managed cash flows creatively. When competitors offered lower prices, Paramount sold reliability and certification.

VIII. The USA Breakthrough: New Export Chapter (2018-Present)

The American market represented Paramount's holy grail—massive, lucrative, but notoriously difficult to crack. Before 2018-19, Indian cables weren't being exported to the US. It took us years to develop products that met the strictest quality standards, but eventually, we gained acceptance.

The journey to UL certification was grueling. American standards weren't just different—they were philosophically distinct from Indian and British systems. Insulation compounds needed reformulation. Manufacturing processes required documentation at levels that seemed obsessive. Testing protocols made Indian standards look casual. Each failure meant starting over, each delay meant more investment.

But persistence paid off spectacularly. In the first two years, Paramount's US exports stood at INR 7.5 crore each year. By the third year, revenue surged to INR 100 crore, followed by INR 400 crore in the fourth year. The hockey stick growth reflected pent-up demand—American buyers wanted alternatives to Chinese suppliers, and Paramount offered quality at competitive prices.

The company has led the industry in direct US exports, recording a remarkable USD 43 million in Free on-board (FOB) exports for the year, representing a 36% growth compared to USD 31 million in FOB exports in 2023. Behind these numbers lies a sophisticated operation—eight distributors across America, inventory management across time zones, and quality consistency that satisfies American contractors.

With the US cable import market valued at USD 30 billion, Paramount faces stiff competition from countries like South Korea, Vietnam, Egypt, and Mexico, many of which export at zero duty. Despite this, Paramount is determined to expand its market share, currently exporting products worth approximately USD 65 million annually.

The US success isn't just about revenues—it's validation that an Indian manufacturer can meet the world's toughest standards. Each container shipped to Houston or Los Angeles carries not just cables, but proof that Indian manufacturing has come of age.

IX. Financial Transformation & Scale Achievement (2020-2024)

The pandemic could have derailed Paramount's recovery, but instead accelerated it. With supply chains disrupted globally, customers valued reliable suppliers over cheap ones. Paramount's two-plant strategy proved prescient—when lockdowns hit, they could maintain operations by careful management of workforce and inventory.

Growth in FY2023 was driven by entirely by exports (Rs 130 crore in FY2022 which increased to Rs 400 crore in FY2023; virtually all exports to US), while domestic revenues declined by 12% YoY. This export-led growth strategy wasn't without risks—currency fluctuations, customer concentration, geopolitical tensions—but it generated the cash flows needed for final debt resolution.

The financial transformation was remarkable. The company, which has two manufacturing facilities in Rajasthan and Haryana, it offers over 25 product types and 2,500 SKUs, said that its EBITDA (earnings before interest, taxes, depreciation, and amortization) grew 51.5 per cent y-o-y. In FY24, our EBITDA has increased to Rs. 972.6 million, showcasing a growth of 51.5 per cent growth as compared to Rs. 642.0 million in FY23. This growth, coupled with an EBITDA margin of 9.0 per cent, reflects the benefits of operating leverage and a sharp focus on cost control.

The crown jewel moment arrived in fiscal 2024. Wire and cable manufacturer Paramount Communications has informed exchanges that its revenue grew 34.4 per cent Year-on-Year (YoY) in the financial year 2024. This year, we reached a significant milestone by surpassing Rs.1,000 crore in revenue showing a growth of 34.4% y-o-y. From one machine to four-comma revenues—the journey was complete, yet just beginning.

Operating leverage became the secret weapon. With fixed costs spread across higher volumes, incremental revenues dropped straight to the bottom line. Revenue from domestic operations in FY24 amounted to Rs.7,944.8 million, showing a 100.5 per cent Y-o-Y increase from Rs.3,961.8 million in FY23. The domestic market, neglected during the export push, roared back as infrastructure spending accelerated.

X. Current Position & Future Vision (2024-2030)

Today's Paramount stands at an inflection point. Paramount Communications is the largest manufacturer-exporter of electric wires and cables under HSN code 854449 for 2024. The company achieved direct US exports of USD 43 million on an FOB basis for 2024, marking a 36% growth from 2023. But past success doesn't guarantee future growth—it merely provides the platform for bigger ambitions.

The Madhya Pradesh expansion represents the next chapter. Paramount Communications has acquired 31 acres of industrial land in Narmadapuram Industrial State, Madhya Pradesh for establishing its new cable manufacturing plant. Excluding the cost of land, this plant will come up with an investment of about Rs. 250 crore. The company will be manufacturing Direct Current (DC) and Alternating Current (AC) cables at this upcoming plant, which is expected to commence production by FY-27. The company is expected to achieve the first commercial production by December 2026.

The ambition is audacious but grounded in capability. Paramount targets to grow its topline at a Compound Annual Growth Rate (CAGR) of 30% over the next five years, targeting revenues exceeding Rs. 5,000 crore by FY-30. This isn't wild optimism—it's based on visible growth drivers: EV charging infrastructure, data center proliferation, renewable energy transmission, and export market penetration.

In CY 2024, the company's exports to the United States reached USD 43 million, marking an impressive 36% Year-over-Year (YoY) growth. The company targets to increase the share of US exports in its revenue to approximately 40% in the coming years. The American market, having validated Paramount's quality, now becomes the growth engine.

Electric vehicle infrastructure presents a generational opportunity. EV charging cables aren't just wires—they need to handle high current draws, resist weather, and maintain safety standards across thousands of charging cycles. Data centers need specialized cables for power and cooling systems. Solar farms require cables that survive decades of UV exposure. Each segment demands different capabilities that Paramount has methodically built.

XI. Playbook: Business & Strategic Lessons

Government relationships as moat: Paramount's six-decade relationship with government departments isn't easily replicable. They understand procurement cycles, specification requirements, and payment patterns. When a new competitor quotes lower prices, Paramount can point to decades of on-time delivery. In infrastructure, reliability trumps price.

Pivot strategy: When counterfeit house wires flooded the market in the 1970s, most manufacturers would have fought on price. Paramount's pivot to institutional sales was counterintuitive but brilliant. They chose customers who valued certification over cost, building capabilities that served them forty years later in American markets.

Patient capital allocation: The US market entry took years of preparation—product development, certification, relationship building—before generating meaningful revenue. Many companies would have given up after the first year of ₹7.5 crore sales. Paramount understood that some investments have J-curves measured in decades.

Manufacturing excellence: In cables, the product might be commodity but quality never is. A cable failure in a hospital, railway signal, or power grid has catastrophic consequences. Paramount's investment in testing equipment, quality processes, and certifications created trust that transcends price comparisons.

Portfolio approach: With 25+ product categories and 2500+ SKUs, Paramount can serve diverse customer needs while spreading risk. When telecom spending slows, power picks up. When domestic demand weakens, exports compensate. This portfolio approach provides resilience through cycles.

Export discipline: Rather than rushing into exports, Paramount built capabilities systematically. They understood that entering the US market prematurely would damage credibility irreparably. By waiting until they could consistently meet UL standards, they built a sustainable position rather than grabbing quick revenues.

Strategic retreat: Exiting AEI Cables after investing significant capital and management attention was painful but necessary. Many companies compound mistakes by throwing good money after bad. Paramount's willingness to retreat, restructure, and rebuild demonstrated rare management maturity.

XII. Bear vs Bull Case Analysis

Bear Case:

The commodity nature of cables means pricing pressure never disappears. Chinese manufacturers, despite tariffs, continue innovating in cost reduction. Vietnamese and Mexican producers enjoy preferential US market access. Paramount's margins depend on product mix and currency movements beyond their control.

Government dependence, while providing stability, carries risks. Payment delays from state electricity boards and railways can strain working capital. Policy changes, like preference for domestic manufacturers, could help or hurt depending on implementation. The institutional focus means limited brand value with end consumers.

The US concentration is concerning—The company targets to increase the share of US exports in its revenue to approximately 40% in the coming years. Any trade war escalation, tariff changes, or recession could disproportionately impact Paramount. Currency fluctuations add another layer of uncertainty to export-heavy operations.

Working capital requirements remain elevated. Cable manufacturing requires holding copper and aluminum inventory whose prices fluctuate daily. Customer payment terms, especially in exports, stretch cash cycles. Despite operational improvements, Paramount needs constant capital for growth.

Competition intensifies as the market grows. Every large infrastructure company sees the cable opportunity. Polycab dominates the domestic market with superior distribution. International players like Prysmian and Nexans have global scale advantages. New entrants with deep pockets could disrupt pricing.

Bull Case:

Paramount Communications is the largest manufacturer-exporter of electric wires and cables under HSN code 854449 for 2024. This leadership position in exports provides pricing power and customer stickiness. American customers, having qualified Paramount through rigorous processes, won't switch for marginal price differences.

India's infrastructure supercycle has barely begun. Power transmission needs massive upgrades for renewable integration. Railway electrification continues for decades. Smart cities, data centers, EV charging networks—each requires enormous cable quantities. Domestic demand alone could sustain 20%+ growth.

The debt-free balance sheet transforms possibilities. Without interest burdens, cash flows can fund expansion. Banking relationships, previously strained, now enable working capital support. The company can consider acquisitions or aggressive capacity expansion without existential risk.

Product premiumization drives margin expansion. Fire survival cables, solar cables, EV charging cables command higher margins than commodity power cables. As the mix shifts toward specialized products, profitability should expand despite competitive pressure on basic cables.

Export diversification beyond the US is beginning. European markets appreciate quality certifications. Middle Eastern infrastructure boom needs reliable suppliers. Australian renewable projects require solar cables. Each new geography reduces concentration risk while leveraging existing capabilities.

XIII. Epilogue: Infrastructure & Nation Building

From one machine to ₹1000+ crore revenues, Paramount's journey mirrors India's economic transformation. When Shyam Sundar Aggarwal started in 1955, India was importing basic industrial goods. Today, his company exports to the world's most demanding markets, embodying the shift from import substitution to global competitiveness.

The family business professionalized without losing its core values. The second generation, led by Sanjay and Sandeep Aggarwal, brought modern management while maintaining relationships built over decades. They survived near-bankruptcy, emerged stronger, and built an institution that outlasts individuals.

Paramount's cables power India's infrastructure story in ways both visible and hidden. The Mumbai local trains run on their railway signaling cables. Telecom towers connecting rural India use their optical fiber. Solar farms in Rajasthan transmit power through their specialized cables. They don't build monuments; they enable them.

The next generation of leadership faces different challenges—technology disruption, sustainability demands, global supply chain complexity. But they inherit something valuable: a culture of patient building, strategic flexibility, and the knowledge that sometimes the best businesses are the boring ones that simply work.

What the next decade holds depends partly on macroeconomics and geopolitics beyond Paramount's control. But if history guides, they'll adapt, invest ahead of demand, and continue laying the cables that carry India's ambitions. From that single machine in 1955 to targeting ₹5,000 crore by 2030—the journey continues, one cable at a time.

XIV. Outro & Resources

The Paramount story offers timeless lessons for entrepreneurs and investors. First, timing matters less than persistence—they entered the US market when everyone said Indian cables couldn't compete. Second, strategic retreats aren't failures—exiting AEI Cables saved the company. Third, boring businesses with high switching costs can generate extraordinary returns.

For investors studying infrastructure businesses in emerging markets, Paramount demonstrates that execution matters more than innovation in commodity products. Quality certifications, customer relationships, and manufacturing discipline create moats that pure technology companies might envy.

Building global competitiveness from India requires patience that quarterly earnings calls discourage. Paramount spent years developing US-compliant products before generating meaningful revenue. They invested in certifications when debt-servicing was painful. This long-term orientation, increasingly rare in public markets, drives sustainable competitive advantage.

The cable industry might seem unsexy compared to software or semiconductors, but it's essential infrastructure that compounds steadily. As India builds its next trillion dollars of infrastructure, companies like Paramount will lay the physical networks that everything else depends upon. Sometimes the best investments are hiding in plain sight, humming away like that first cable machine in 1955.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube