NMDC Steel: India's Bold Public Sector Steel Gambit

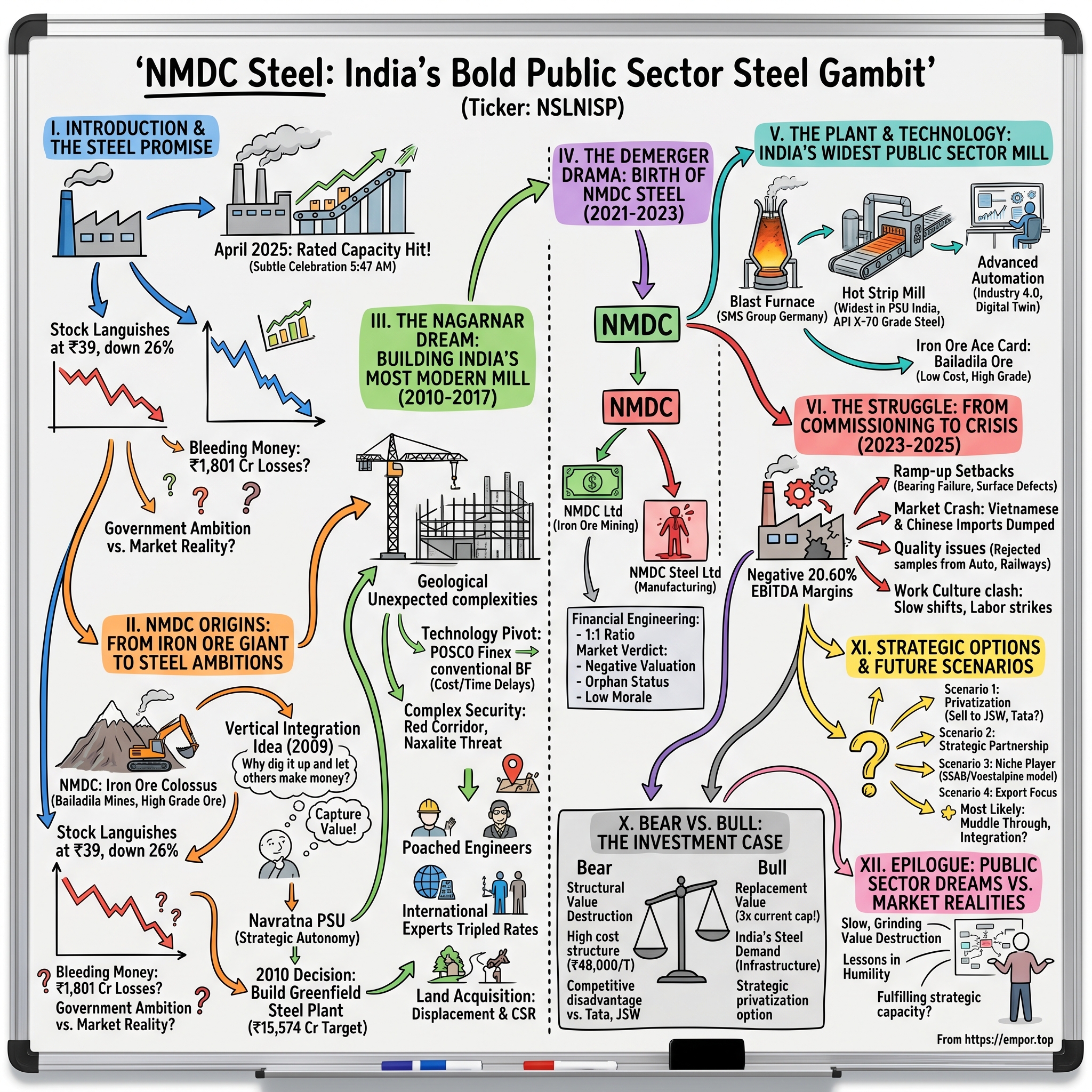

I. Introduction & The Steel Promise

The furnaces of Nagarnar hadn't cooled since April 26, 2025. That morning, at 5:47 AM, the control room erupted in subdued celebration—NMDC Steel's blast furnace had finally hit its rated capacity, producing 230,111 tonnes of hot metal that month. For the engineers who'd spent years nursing this ₹24,000 crore behemoth to life, it was vindication. For investors watching the stock languish at ₹39, down 26% from a year ago, it was too little, too late.

This is the story of NMDC Steel Limited—a government-owned enterprise that dared to build India's widest public sector steel mill in the heart of Chhattisgarh, only to discover that in the steel business, timing isn't just everything—it's the only thing.

Today, NMDC Steel stands as a curious paradox in India's capital markets. With a market capitalization of ₹12,332 crore and annual revenues touching ₹9,845 crore, it should be a mid-cap success story. Instead, it's bleeding money—₹1,801 crore in losses, with EBITDA margins at negative 20.60%. The company that was supposed to showcase India's public sector prowess in modern steelmaking has become a case study in what happens when government ambition collides with market reality.

The central question isn't whether NMDC Steel can make steel—it clearly can, with some of the most advanced technology in the country. The question is whether a government-owned greenfield steel plant, conceived during a commodity boom and born into a downturn, can survive in India's hyper-competitive steel market dominated by nimble private players like JSW and Tata Steel.

What makes this story particularly compelling is its timing. As India pushes toward becoming the world's third-largest economy, steel consumption is projected to double by 2030. The government's infrastructure spending has never been higher. The fundamentals scream opportunity. Yet NMDC Steel, with all its technological advantages and government backing, is struggling to stay afloat.

This isn't just another public sector undertaking story. It's a high-stakes experiment in industrial policy, a test of whether India can build world-class manufacturing capabilities through state intervention. The stakes extend beyond the ₹24,000 crore already invested—they touch on India's ability to achieve self-sufficiency in critical materials, the future of public sector enterprises, and the delicate balance between strategic autonomy and market efficiency.

Over the next several hours, we'll unpack how a company with captive iron ore mines, cutting-edge technology, and government backing ended up in this position. We'll explore the decisions—some bold, some questionable—that brought us here. And we'll examine what NMDC Steel's journey tells us about India's industrial ambitions in the 21st century.

II. NMDC Origins: From Iron Ore Giant to Steel Ambitions

The boardroom at NMDC's Hyderabad headquarters had seen many presentations, but the one in late 2009 was different. Chairman Rana Som stood before a map of India dotted with red markers—each representing a steel plant fed by NMDC's iron ore. "We dig it up, they make the money," he said, pointing to the value chain diagram. "Why shouldn't we capture that value ourselves?"

NMDC wasn't just any mining company. Since 1958, it had built itself into India's iron ore colossus, extracting 45 million tonnes annually from the red earth of Chhattisgarh and Karnataka. The Bailadila mines alone—carved into 14 deposits across the Dantewada district—held some of the world's highest-grade hematite ore, with iron content exceeding 65%. While private steel companies scrambled for raw materials during the 2000s commodity boom, NMDC sat on reserves that could last centuries.

The company's structure reflected India's mixed economy ideals. As a "Navratna" public sector undertaking—one of nine jewels in the government's crown—NMDC enjoyed operational autonomy while serving national interests. It had weathered Naxalite insurgencies in its mining areas, survived market cycles, and built infrastructure in some of India's most remote regions. By 2009, it was generating over ₹10,000 crore in annual revenue with EBITDA margins that private miners could only dream of.

But the global financial crisis of 2008 had exposed a painful truth. When steel demand collapsed, iron ore prices plummeted from $180 per tonne to below $60. NMDC's profits evaporated overnight. Meanwhile, integrated steel producers—those who owned both mines and mills—weathered the storm far better. They could absorb raw material volatility within their value chain.

The timing seemed perfect for vertical integration. India's steel consumption was growing at 8% annually, driven by massive infrastructure projects—highways, airports, metro systems. The Planning Commission projected demand would reach 200 million tonnes by 2020. Yet India remained a net steel importer, particularly of high-quality flat products used in automobiles and consumer durables.

Within NMDC, two camps emerged. The conservatives, mostly finance executives, argued the company should stick to what it knew—mining. Steel making was a different beast entirely, requiring massive capital, technical expertise NMDC didn't possess, and the ability to compete with established players who'd spent decades perfecting their operations. "We're profitable," they'd say. "Why risk it?"

The progressives, led by Som and backed by the Steel Ministry, saw a historic opportunity. They pointed to South Korea's POSCO, which had transformed from nothing into a global steel giant with government support. They cited China's state-owned steel companies, rapidly modernizing and dominating global markets. Why couldn't India do the same?

The government had its own calculations. The 2008 crisis had shown how vulnerable India was to global commodity cycles. Building domestic steel capacity wasn't just about business—it was about strategic autonomy. The Ministry of Steel's National Steel Policy explicitly called for raising production capacity to 300 million tonnes. NMDC, with its iron ore reserves and government backing, was the obvious candidate to lead this charge.

By early 2010, the die was cast. NMDC's board approved the construction of a 3 million tonne per annum integrated steel plant at Nagarnar, 16 kilometers from Jagdalpur in Chhattisgarh. The initial investment was pegged at ₹15,574 crore, with completion targeted for 2014. It would be India's first greenfield integrated steel plant built by a public sector company in over two decades.

The plan was audacious in its scope. Unlike incremental expansions that competitors pursued, NMDC would build everything from scratch—blast furnaces, steel melt shops, rolling mills, power plants, townships. The company would leapfrog older technologies, installing equipment that could produce automotive-grade steel from day one.

What NMDC's leadership didn't fully appreciate was that they weren't just entering the steel business—they were entering it at precisely the moment when global steel was about to face its greatest crisis since the Great Depression. Chinese overcapacity was building, about to flood global markets. Environmental regulations were tightening. And India's own steel industry was about to enter a phase of brutal consolidation.

But in 2010, optimism reigned. At the groundbreaking ceremony, attended by Chhattisgarh's Chief Minister and union ministers, Rana Som declared that NMDC Steel would be "India's most modern steel plant, a testament to public sector excellence." The crowd applauded. The earth movers began their work. And one of India's most expensive industrial experiments was underway.

III. The Nagarnar Dream: Building India's Most Modern Mill (2010-2017)

The first dynamite blast at Nagarnar echoed across the sal forests of Bastar on a humid June morning in 2010. Local villagers, gathered at a safe distance, watched as red earth erupted skyward—the beginning of what officials promised would transform one of India's most backward regions into an industrial powerhouse. Seven years later, those same villagers would still be watching, waiting for the transformation that seemed perpetually just around the corner.

The Nagarnar site sprawled across 1,980 hectares of undulating terrain, chosen for its proximity to NMDC's Bailadila iron ore mines just 100 kilometers away. On paper, it was perfect—abundant water from the Indravati river, rail connectivity to major ports, and most crucially, located in a state desperate for industrial development. Chhattisgarh's government had rolled out the red carpet, promising land, power, and political support.

But paper plans and ground realities diverged from day one. The first challenge came from beneath their feet. Soil tests revealed unexpected geological complexities—layers of hard rock where engineers expected soft earth, aquifers where foundations needed to go. The blast furnace foundation alone, originally budgeted at ₹50 crore, ballooned to ₹180 crore as engineers drove piles deeper and deeper to find stable ground.

The technology decisions would prove even more consequential. NMDC had initially chosen POSCO's FINEX technology, a cutting-edge process that could use iron ore fines directly without sintering—potentially saving hundreds of crores in processing costs. POSCO engineers arrived from South Korea, blueprints were drawn, and equipment orders placed. Then, in 2012, POSCO's own FINEX plant in Korea faced operational issues. Overnight, NMDC's technological leap looked like a potential disaster.

The pivot came at enormous cost—not just financial, but temporal. After 18 months of deliberation, NMDC switched to conventional blast furnace technology from Germany's SMS Group. Every blueprint had to be redrawn. Equipment orders were cancelled, penalties paid. The project, already behind schedule, lost another two years.

Project Director R.K. Goyal, a veteran of Steel Authority of India, would later describe those years as "building a plane while flying it." His team of 400 engineers, many poached from private steel companies with salary premiums, worked in temporary structures as monsoons turned the construction site into a muddy lake each year from June to September. "We'd make progress for eight months, then spend four months just preventing damage," one senior engineer recalled.

The human drama played out against a backdrop of India's most complex security situation. Nagarnar sat in the heart of the Red Corridor, where Maoist insurgents had waged a decades-long war against the state. In 2013, Naxalites attacked a convoy of Congress leaders just 50 kilometers away, killing 27 people. NMDC had to build not just a steel plant but a fortress—deploying over 600 paramilitary forces, constructing watchtowers, and coordinating daily with intelligence agencies.

The security concerns cascaded into construction delays. Equipment convoys could only move under armed escort. Specialized technicians from Europe refused to visit after reading news reports. One German engineer, arriving to commission the blast furnace, took one look at the armed guards and returned to Mumbai the same day. NMDC had to pay triple the normal rates to convince international experts to come to Nagarnar.

Local politics added another layer of complexity. The plant required displacing 635 families from seven villages. While NMDC offered compensation above market rates—₹5 lakh per acre when land was selling for ₹1 lakh—negotiations dragged on for years. Village leaders demanded jobs, contractors, and development projects. Some agreements were reached, and then reopened when leadership changed. The company spent ₹284 crore on rehabilitation and CSR activities, building schools and hospitals that often served more as negotiation chips than social investments.

By 2014, when the plant was originally supposed to be operational, only 30% of construction was complete. The budget had swollen from ₹15,574 crore to over ₹20,000 crore. The Steel Ministry, under pressure from the Prime Minister's Office about cost overruns in public sector projects, demanded explanations. NMDC's chairman was summoned to Delhi monthly, each time promising completion "within 18 months."

The technical challenges mounted as construction progressed. The blast furnace, with a capacity of 8,820 cubic meters per day, was among the largest in India. But size brought complexity—the refractory lining alone required 45,000 tonnes of specialized bricks, each placed by hand in precise patterns. When the first lining failed during hot trials in 2016, requiring complete replacement, project managers realized they were attempting something beyond NMDC's organizational DNA.

Management shuffles reflected the mounting pressure. Three project directors came and went between 2010 and 2017. Each brought new ideas, reversed previous decisions, and promised faster completion. The SMS Group's project manager, brought in from Germany to provide technical oversight, quit after 18 months, citing "irreconcilable differences in project execution philosophy."

Yet amid the chaos, something remarkable was taking shape. The steel melt shop, with its twin 150-tonne converters, incorporated technology that even private players hadn't adopted. The hot strip mill, capable of rolling steel to just 1.2mm thickness at 1650mm width—the widest in India's public sector—could produce automotive-grade steel that India was importing from Japan and South Korea.

The control systems, designed by Siemens, created a digital twin of the entire plant—every valve, sensor, and motor mapped in real-time. It was Industry 4.0 before the term became fashionable, a level of automation that would require fewer workers than plants a third its size. The water treatment facility could recycle 98% of industrial water, while the power plant would generate 300 MW, enough to run the plant and export to the grid.

By late 2017, as construction finally neared completion, NMDC had spent ₹23,000 crore—50% over the revised budget. The plant that was supposed to showcase public sector efficiency had become a symbol of everything critics said was wrong with government-run projects: delays, cost overruns, and endless bureaucracy.

But for those who'd spent seven years in Nagarnar's dust and heat, there was also pride. They'd built something unprecedented—a world-class steel facility in one of India's most challenging locations. Chief Engineer Mohanty, standing before the towering blast furnace as it underwent cold trials, told his team: "We may be late, but we've built it right."

The question was whether "right" would be good enough in a steel market that had fundamentally changed since that first dynamite blast in 2010.

IV. The Demerger Drama: Birth of NMDC Steel (2021-2023)

The PowerPoint slide lingered on the screen in NMDC's boardroom on July 15, 2021: "Strategic Demerger Proposal—Unlocking Value Through Focus." Chief Financial Officer Amitava Mukherjee clicked to the next slide, showing two entities where there was one—NMDC Limited (iron ore mining) and NMDC Steel Limited (steel manufacturing). Board members shifted in their seats. After eleven years and ₹23,000 crore, the steel plant that was supposed to crown NMDC's vertical integration strategy was being carved out.

The official narrative was elegant in its simplicity. Separating steel from mining would allow each business to focus on its core competencies. Investors could choose pure-play exposure. Management could optimize capital allocation. The stock market would properly value both entities. Behind closed doors, the reasoning was more brutal: the steel plant was hemorrhaging cash, and NMDC's mining shareholders were tired of subsidizing it.

The numbers told the story. While NMDC's mining operations generated EBITDA margins above 50%, the Nagarnar plant was burning through ₹200 crore monthly just to keep running. Fund managers who'd held NMDC for its dividend yield—often above 6%—watched payouts shrink as steel losses mounted. "We bought a mining company, not a steel experiment," one mutual fund manager told management during an investor call.

The demerger structure revealed careful financial engineering. NMDC Steel would receive ₹18,650 crore in assets—primarily the Nagarnar plant and associated infrastructure. Liabilities of ₹1,600 crore would transfer, mostly working capital loans. Critically, NMDC would provide a ₹4,000 crore loan to its offspring, ensuring the new entity wouldn't immediately face a liquidity crisis.

For every NMDC share held, investors would receive one share of NMDC Steel—a 1:1 ratio that seemed fair until you examined the implicit valuations. Analysts calculated that the market was valuing the steel business at negative ₹2,000 crore, essentially saying investors would pay to get rid of it. The government, holding 60.79% of NMDC, would maintain the same stake in both entities.

The regulatory approvals moved with unusual speed for a public sector undertaking. The National Company Law Tribunal fast-tracked hearings. SEBI granted exemptions from standard IPO requirements. The Ministry of Steel, which had championed the original steel project, now championed its separation. Everyone, it seemed, wanted this divorce finalized quickly.

October 28, 2022, marked the record date—shareholders on this day would receive NMDC Steel shares. Trading dynamics immediately revealed market sentiment. While NMDC shares held steady around ₹110, the when-issued NMDC Steel shares traded at ₹35, implying a combined value less than the original NMDC price. Arbitrageurs swooped in, buying NMDC shares and shorting the theoretical combined value, betting the sum of parts would be worth less than the whole.

The separate listing on February 15, 2023, was a subdued affair. No fanfare, no opening bell ceremony—just another stock added to the BSE and NSE listings. NMDC Steel opened at ₹37.50, slightly above the when-issued price but well below the ₹50 book value. Volume was thin—mostly institutional investors adjusting index portfolios and retail investors wondering what this new holding in their demat accounts was worth.

Management tried to paint an optimistic picture. CEO Amitava Ghosh, brought in from Steel Authority of India, spoke of "focus and agility" in investor calls. The company would benefit from dedicated management attention. Capital allocation would be optimized for steel operations. The technological superiority of Nagarnar would soon translate to market share.

But actions spoke louder than words. Key executives from NMDC chose to remain with the mining entity rather than move to NMDC Steel. The new company had to recruit fresh talent, often at premium salaries, to fill critical positions. The headquarters in Hyderabad felt empty—many floors unused, a skeleton crew managing a ₹24,000 crore asset.

The governance structure revealed the challenges of government ownership without the cushion of profitable operations. Board meetings stretched for hours as independent directors questioned every capital expenditure. The Ministry of Steel nominated bureaucrats with limited steel industry experience. Procurement decisions required multiple approvals, slowing response to market conditions.

Investment bankers who'd pitched the demerger painted it as a "value unlock" story. In reality, it was triage—separating the healthy from the sick, hoping both might survive independently. The market's verdict was swift and harsh. Within six months of listing, NMDC Steel was trading at ₹29.75, a 40% discount to book value. No research analysts initiated coverage—why waste time on a structurally challenged, government-owned steel company in an oversupplied market?

The employees at Nagarnar felt the shift most acutely. Under NMDC, they were part of a profitable Navratna company with job security and prestige. Under NMDC Steel, they worked for a loss-making entity with an uncertain future. Morale plummeted. Engineers who'd spent years commissioning the plant started sending out resumes. The company had to introduce retention bonuses just to prevent mass exodus.

Yet the demerger also brought unexpected clarity. For the first time, NMDC Steel's true economics were visible. No longer could losses be buried in consolidated statements. Every tonne of steel produced, every rupee lost, was now scrutinized. The government couldn't ignore the bleeding—it was happening in plain sight, in a listed entity with minority shareholders.

The birth of NMDC Steel through this demerger wasn't a celebration—it was an acknowledgment that the original vision had failed. The vertical integration dream was dead. What remained was a standalone steel company, technologically advanced but commercially challenged, trying to find its place in one of the world's most competitive steel markets.

V. The Plant & Technology: India's Widest Public Sector Mill

At 4:30 AM, the control room at Nagarnar resembles a NASA mission control—banks of monitors displaying real-time data from 14,000 sensors, operators in hard hats adjusting parameters with surgical precision. The blast furnace temperature reads 2,100°C, hot enough to vaporize rock. Every eight hours, like clockwork, 400 tonnes of molten iron cascades into torpedo ladles, beginning its journey to become steel sheets thinner than a credit card.

This ₹24,000 crore facility isn't just another steel plant—it's an engineering marvel that most industry veterans didn't believe a public sector company could build. The hot strip mill, the crown jewel of Nagarnar, can roll steel sheets to 1650mm width—wider than any other public sector mill in India. When automotive manufacturers need steel for car doors that won't dent or railway wagons that can carry 30% more load, they traditionally imported from Japan. Now, theoretically, they could source from Chhattisgarh.

The technological choices at Nagarnar reflected ambitions that went beyond mere steelmaking. The blast furnace, designed by Germany's SMS Group, incorporated a bell-less top charging system that could segregate different grades of iron ore in the furnace itself—a feature that even ArcelorMittal's Hazira plant didn't have. The pulverized coal injection system could reduce coke consumption by 40%, a critical advantage when coking coal costs ₹25,000 per tonne.

But technology alone doesn't make steel competitive—raw material access does. Here, NMDC Steel held an ace card. The Bailadila iron ore mines, just 100 kilometers away, could deliver 7 million tonnes annually of 65% Fe grade ore—among the world's best. While competitors paid ₹5,000 per tonne for similar grade ore, NMDC Steel's transfer pricing from its former parent meant costs closer to ₹3,000. In the steel business, where raw materials constitute 60% of costs, this should have been an insurmountable advantage.

The product portfolio revealed strategic thinking about market positioning. Rather than compete in commodity construction steel where JSW and Tata dominated, Nagarnar focused on specialized grades. API X-70 grade steel for oil pipelines that could withstand 70 kilograms per square millimeter of pressure. Dual-phase steel for automotive chassis that was 30% stronger but 20% lighter than conventional steel. High-strength low-alloy (HSLA) grades for LPG cylinders that met the most stringent safety standards.

The steel melt shop, with its twin 150-tonne LD converters, could produce 40 different grades of steel by adjusting chemistry in real-time. Sensors measured carbon content every 30 seconds, automatically adjusting oxygen flow to achieve precise specifications. The ladle furnace could fine-tune temperature to within 2°C, critical for achieving uniform mechanical properties. When operating at full capacity, this shop could produce one heat every 40 minutes—3.6 million tonnes annually of liquid steel.

The rolling mill complex stretched for nearly a kilometer—a symphony of synchronized machinery that transformed red-hot slabs into finished sheets. The roughing mill, with its 5,000-tonne pressing force, could reduce a 250mm thick slab to 30mm in a single pass. The finishing mill's seven stands, each computer-controlled to micron precision, could roll steel at 90 kilometers per hour while maintaining thickness tolerance of ±0.01mm.

Quality control bordered on obsessive. Seventeen different testing stations checked steel properties—tensile strength, elongation, hardness, grain structure. X-ray machines scanned for internal defects. Laser systems measured flatness to prevent the waviness that plagued domestic steel in automotive applications. The laboratory, equipped with ₹50 crore worth of German and Japanese testing equipment, could certify steel to international standards that Indian labs typically couldn't match.

The environmental systems reflected modern sustainability mandates—and added substantial costs. The ₹2,000 crore sinter plant included electromagnetic precipitators that captured 99.9% of particulate emissions. The water treatment facility, designed to achieve zero liquid discharge, could process 40,000 cubic meters daily. The coke oven's by-product plant converted toxic benzene and toluene into saleable chemicals rather than flaring them.

Power generation showcased industrial symbiosis at its best. Three generators captured waste heat from coke ovens, blast furnaces, and LD converters, producing 300 MW of electricity—enough to run the plant with surplus for the grid. When Chhattisgarh faced power shortages in summer 2024, NMDC Steel exported 50 MW to the state grid, earning ₹20 crore in additional revenue.

The automation level approached Industry 4.0 standards before the term became fashionable. The Manufacturing Execution System (MES) tracked every slab from casting to shipping, maintaining genealogy of heat chemistry, rolling parameters, and quality results. Predictive maintenance algorithms analyzed vibration patterns to forecast equipment failures weeks in advance. The digital twin—a virtual replica of the entire plant—allowed engineers to simulate production changes before implementing them.

Yet for all its technological sophistication, utilization told a different story. The blast furnace, designed to produce 9,000 tonnes daily, averaged 6,500 tonnes. The hot strip mill, capable of rolling 300 coils per day, produced 180. The finishing lines, equipped for value-added coating and galvanizing, often sat idle for want of orders.

The mismatch between capability and utilization revealed a fundamental challenge. Nagarnar was built for a market that didn't yet exist—or rather, for a market that NMDC Steel couldn't access. Automotive companies had long-term contracts with established suppliers. Infrastructure projects specified grades that didn't require Nagarnar's sophistication. Export markets, where quality premiums existed, were 1,000 kilometers away through some of India's worst transport infrastructure.

The recent development of Deposit 4 added another dimension to the raw material story. This new mining block, with 7 million tonnes annual capacity, was configured specifically for Nagarnar's 5 million tonne requirement. The slurry pipeline project, when completed, would transport iron ore as liquid suspension, cutting transportation costs by 40%. But these advantages would only matter if the plant could sell what it produced.

Standing in the hot strip mill, watching orange-hot steel transform into mirror-finish sheets, it's impossible not to admire the engineering achievement. This is world-class technology, implemented successfully in one of India's most challenging locations. The tragedy isn't that NMDC Steel built the wrong plant—it's that they built the right plant at the wrong time, in the wrong place, for a market that wasn't ready to pay for what it could produce.

VI. The Struggle: From Commissioning to Crisis (2023-2025)

The furnace roared to life on a scorching April morning in 2023, sending a pillar of flame into the Chhattisgarh sky. NMDC Steel's first commercial heat was tapped—2,450°C of molten steel that would become coils destined for an LPG cylinder manufacturer in Gujarat. CEO Amitava Ghosh, watching from the control room, allowed himself a moment of satisfaction. After thirteen years and ₹24,000 crore, Nagarnar was finally making steel for customers. Within six months, he would be explaining to the board why the company was losing ₹200 crore every month.

The ramp-up trajectory that looked smooth on paper turned into a staircase of setbacks. Month one: 50,000 tonnes production, 40% capacity utilization. Month two: 45,000 tonnes—a bearing failure in the roughing mill caused five days of downtime. Month three: 60,000 tonnes, but 30% was downgraded to secondary quality due to surface defects. The learning curve that management projected would take six months stretched to eighteen.

The financial hemorrhaging was spectacular in its consistency. Q1 FY24: ₹420 crore loss. Q2: ₹380 crore loss. Q3: ₹440 crore loss. Q4: ₹561 crore loss. In three years of operation, NMDC Steel accumulated losses of ₹1,801 crore—roughly ₹50 lakh for every day the plant operated. The stock price traced a similar trajectory, sliding from the IPO levels of ₹37 to touch ₹29.75 in March 2023.

The EBITDA margins told the story more starkly: negative 20.60%. For every tonne of steel sold, NMDC Steel lost ₹4,000 at the operational level—before even accounting for interest and depreciation. The interest burden alone—₹400 crore annually on borrowings of ₹4,500 crore—meant the company needed to generate ₹1 crore in cash daily just to service debt.

Return on equity painted the complete picture: negative 8.26% over three years. Shareholders who'd received NMDC Steel shares in the demerger watched their wealth evaporate. The government's 60.8% stake, worth ₹7,500 crore at demerger, had shrunk to ₹4,800 crore. No dividends were declared—how could they be when the company was burning cash to stay alive?

The market timing couldn't have been worse. Global steel prices, which had spiked to $900 per tonne during COVID supply disruptions, crashed to $450 as Chinese exports flooded markets. Domestic prices followed, with hot-rolled coils dropping from ₹65,000 per tonne to ₹42,000. NMDC Steel, having based its business plan on ₹55,000 per tonne realizations, found itself selling below production cost from day one.

Competition from established players proved more brutal than anticipated. When NMDC Steel approached Maruti Suzuki with automotive-grade samples, they discovered Tata Steel had exclusive supply agreements locked until 2027. JSW's relationship managers had been visiting auto component manufacturers for decades; NMDC Steel's newly hired sales team was still learning customer names. The price discount needed to break these relationships—often 8-10%—eliminated any margin.

The import tsunami added another layer of pain. Vietnamese steel, subsidized and dumped, arrived at Indian ports at ₹38,000 per tonne. Chinese stainless steel, rebadged through Indonesia to avoid duties, undercut domestic prices by 15%. NMDC Steel's sophisticated products competed not against quality but against price—and in commodity markets, price always wins.

Operational metrics revealed deeper problems. The blast furnace, designed for 90% utilization, achieved barely 65%. The sintering plant, critical for preparing iron ore, faced repeated breakdowns—its European components required specialized maintenance that local contractors couldn't provide. The coke ovens, operating below optimal temperature to save costs, produced inferior coke that reduced furnace efficiency.

Quality issues plagued customer acquisition. Early shipments to pipe manufacturers were rejected for inconsistent tensile strength. An order for railway wagons was cancelled when surface defects appeared after galvanizing. Each rejection meant not just lost revenue but damaged reputation in an industry where trust takes years to build.

The employee productivity numbers were embarrassing. With 2,640 employees producing 2 million tonnes annually, NMDC Steel's productivity was 757 tonnes per employee—half that of Tata Steel. The public sector work culture, with its emphasis on process over output, clashed with the demanding rhythm of continuous production. Shifts that should change in 30 minutes took 90, reducing effective production time by 10%.

Labor issues compounded operational challenges. The union, emboldened by government ownership, demanded wage parity with profitable SAIL plants. A tool-down strike in December 2023 lasted four days, causing ₹40 crore in losses. Contract workers, comprising 60% of the workforce, turned over every six months, taking their learned skills with them.

Working capital management became a daily crisis. Customers demanded 60-90 day credit terms while raw material suppliers wanted advance payment. The cash conversion cycle stretched to 120 days, requiring ₹1,200 crore in working capital financing. Banks, seeing mounting losses, tightened terms—interest rates rose from 8% to 11%, adding ₹36 crore to annual costs.

The leadership churn reflected the crisis. Three CFOs in two years. Two marketing heads in eighteen months. The board, dominated by government nominees with limited steel experience, took months to approve critical decisions. A ₹200 crore automation upgrade, identified as essential in January 2024, received approval only in September.

Market sentiment turned from skepticism to abandonment. No analyst covered the stock—why waste time on a structural value destroyer? Institutional investors, holding 8.6% at demerger, had reduced stakes to 3.2%. Retail investors, initially enthusiastic about a "government steel company," discovered that government ownership guaranteed neither profits nor stock appreciation.

The April 2025 milestone—achieving rated capacity—should have been cause for celebration. The plant produced 230,111 tonnes that month, 8.5% growth from March. The liquid nitrogen facility began supplying medical oxygen to Chhattisgarh hospitals. For a brief moment, it seemed the corner had been turned.

But the underlying economics remained brutal. Even at full capacity, NMDC Steel's cost structure—₹48,000 per tonne all-in cost versus ₹42,000 market price—meant losing money on every tonne sold. The sophisticated technology that was supposed to be an advantage had become a burden, requiring expensive maintenance and specialized skills the company struggled to retain.

Standing at the precipice of its third year of losses, NMDC Steel faced an existential question: Could operational improvements and market recovery overcome structural disadvantages, or was this a business model that simply didn't work? The answer would determine whether the ₹24,000 crore invested in Nagarnar was an expensive lesson or the foundation for an eventual turnaround.

VII. The Market Reality: Stock Performance & Investor Sentiment

The WhatsApp message pinged across trading floors at 9:14 AM on February 15, 2024: "NMDC Steel touching 73.70—new high!" Portfolio managers who'd written off the stock scrambled to their screens. In a market where Tata Steel traded at 8x EBITDA, here was NMDC Steel—bleeding money, government-owned, operationally challenged—suddenly surging 40% in three weeks. By March, those same managers would watch it crash back to ₹45, another reminder that in Indian markets, narrative often trumps fundamentals.

The stock's journey from listing to present reads like a cardiac monitor during a heart attack—violent spikes followed by deeper troughs. The initial listing at ₹37.50 in February 2023 had established a floor, or so investors thought. Then came the first quarterly results: ₹420 crore loss. The stock slumped to ₹29.75 by March 2023, a 40% discount to book value that suggested the market valued the ₹24,000 crore plant at roughly ₹14,000 crore.

The absence of analyst coverage created an information vacuum that amplified volatility. While Tata Steel had 34 analysts tracking every production update, NMDC Steel operated in darkness. No initiation reports, no target prices, no earnings estimates. Fund managers relied on management commentary and quarterly results—often discovering surprises that moved the stock 10% in a day.

The February 2024 surge to ₹73.70 illustrated the power of narrative in an information-poor environment. Chinese steel production cuts, announced in January, had sparked dreams of a global price recovery. A single bulk order from Indian Railways for wagon-grade steel—₹200 crore, insignificant in the grand scheme—was interpreted as validation of NMDC Steel's quality. Retail investors, seeing the stock double from its lows, piled in through social media tips and YouTube channels.

The crash was equally narrative-driven. When Q4 FY24 results showed losses widening to ₹561 crore despite higher production, the story flipped overnight. The operational leverage that was supposed to drive profitability at higher utilization hadn't materialized. The stock gave back all its gains in six weeks, settling into a ₹35-45 trading range that persists today.

Government ownership—60.8% by the Ministry of Steel—created unique dynamics. Unlike private promoters who might buy shares to support prices, the government remained passive. No buybacks were announced despite the stock trading below book value. No strategic investors were courted. The free float of 39.2% was dominated by index funds required to hold the stock and retail investors hoping for a turnaround.

The one-year performance tells the story starkly: down 26.36% while the Nifty gained 18%. Every rally fizzled as sellers emerged—employees exercising stock options, pre-demerger NMDC shareholders finally capitulating, traders who'd learned that NMDC Steel rallies were selling opportunities.

Retail participation remained puzzlingly high—over 2.8 lakh individual shareholders held 18.4% of equity. The attraction seemed partly aspirational (a government steel company must eventually succeed), partly mathematical (trading at 0.6x book value seemed cheap), and partly hope that the government wouldn't let a showcase project fail completely.

The institutional exodus was more telling. Mutual funds that held 4.2% at demerger had reduced holdings to 1.3%. Foreign institutional investors, initially curious about India's newest steel capacity, held just 0.8%. The smart money had voted with its feet—this wasn't a turnaround story worth waiting for.

Trading volumes revealed the stock's orphan status. Average daily volume of ₹15 crore meant large orders moved prices disproportionately. Market makers quoted wide spreads—often ₹0.50 between bid and ask on a ₹40 stock. The options market was non-existent; no derivatives meant no hedging, no speculation, no price discovery beyond daily spot trading.

Corporate actions—or their absence—spoke volumes. No dividends, obviously. No bonus shares or splits to improve liquidity. The annual general meetings were sparse affairs, with a handful of retail shareholders questioning management while government nominees remained silent. The investor presentations, updated quarterly, recycled the same optimistic projections that had been wrong for three years.

The comparison with peers was brutal. JSW Steel traded at 1.8x book value; NMDC Steel at 0.6x. Tata Steel commanded EV/tonne of capacity at $400; NMDC Steel at $150. The market was saying that NMDC Steel's modern plant was worth less than half of older, less efficient private sector capacity.

The ESG angle, which should have been a positive, barely registered. Despite superior environmental controls and lower emissions than peers, no ESG funds showed interest. The governance issues—government ownership, board composition, operational control—overshadowed any environmental advantages.

Recent price action suggests resignation rather than anticipation. The stock trades in a narrow ₹38-42 band, volume has dried up to ₹8-10 crore daily, and volatility has compressed. It's as if the market has decided NMDC Steel will neither dramatically succeed nor completely fail—it will simply persist as a value-destroying government enterprise.

The few brave souls still recommending the stock point to replacement value—building Nagarnar today would cost ₹35,000 crore. But replacement value only matters if someone would actually want to replace it. In a market oversupplied with steel capacity, with better-located plants available for acquisition, why would anyone recreate Nagarnar?

The stock price, hovering around ₹39 as of late 2024, has become less a reflection of business fundamentals and more a measure of hope versus resignation. Every operational improvement sparks a brief rally; every disappointing quarter confirms the bears. Without analyst coverage to provide benchmarks or institutional interest to provide stability, NMDC Steel stock drifts—a ₹5,000 crore market cap company that the market has essentially decided to ignore.

VIII. Operational Milestones & Recent Developments

The morning shift on April 26, 2025, began like any other at Nagarnar—except for the countdown timer displayed on every monitor. At 10:47 AM, when the blast furnace production crossed 8,000 tonnes for the day, putting monthly production on track for design capacity, the control room erupted. Engineers who'd spent five years nursing this temperamental giant finally had their vindication. The plant that critics said would never run properly had just achieved what its designers promised back in 2010.

The April 2025 production figures—230,111 tonnes of hot metal, an 8.5% jump from March—represented more than just numbers. Each percentage point of improvement had required solving dozens of micro-problems. The sinter plant's inconsistent output, fixed by recalibrating feeders. The blast furnace's irregular temperature profile, resolved by adjusting burden distribution. The rolling mill's surface defects, eliminated by replacing worn work rolls more frequently.

But the most unexpected development came from an adjacent facility. The air separation unit, built to supply oxygen for steelmaking, had excess capacity for producing liquid nitrogen and medical-grade oxygen. When Chhattisgarh faced an oxygen shortage during a dengue outbreak in April 2025, NMDC Steel's oxygen plant became a lifeline. The company began supplying 20 tonnes daily to government hospitals—a small revenue stream but enormous reputational value.

The workforce of 2,640 employees as of August 2025 told its own story of evolution. The initial team, heavy with transferred NMDC mining personnel, had given way to steel specialists poached from private plants. The average age dropped from 48 to 38. Engineers from IITs and NITs, initially skeptical of joining a struggling PSU, were attracted by the chance to work with cutting-edge technology and solve complex problems.

Training had become almost obsessive. Every operator spent three months in simulation before touching actual equipment. The company partnered with Germany's SMS Group to create a technical university within the plant, where workers studied metallurgy, automation, and safety. The accident rate—initially alarming at 12 per million man-hours—had dropped to 3, better than many established plants.

The CSR initiatives, mandated by law but executed with unusual vigor, had transformed Nagarnar's relationship with surrounding villages. The company had built 12 schools, serving 3,000 students who previously traveled 20 kilometers for education. The 100-bed hospital, initially meant for employees, had become the region's primary healthcare facility. The skill development center trained 500 youth annually in welding, electrical work, and mechanical maintenance—creating a pool of contractors who supported plant operations.

The infrastructure developments around the plant were equally significant. The railway siding, completed in 2024, could handle 10 rakes daily, eliminating the truck bottleneck that had constrained early production. The 220 kV power transmission line provided reliable electricity to 40 surrounding villages for the first time. The four-lane highway to Jagdalpur, partially funded by NMDC Steel, cut transportation time to the state capital by half.

The slurry pipeline project, though delayed, promised to revolutionize raw material economics. When completed in 2026, iron ore would flow as slurry from Bailadila mines directly to Nagarnar, cutting transportation costs from ₹800 per tonne to ₹300. The 267-kilometer pipeline, crossing forests and rivers, required environmental clearances that took three years to obtain.

The pellet plant proposal, with 6 million tonne capacity, would allow NMDC Steel to process lower-grade ore that currently went to waste. The board had approved ₹4,000 crore investment, though funding remained uncertain given ongoing losses. If built, it would reduce raw material costs by 15% and improve blast furnace efficiency by 10%.

Digital initiatives, launched in early 2025, were showing unexpected promise. The AI-based production optimization system, developed with IIT Kharagpur, could predict quality defects three hours before they occurred, allowing operators to adjust parameters preemptively. The blockchain-based supply chain system provided customers real-time tracking from production to delivery, addressing complaints about shipment delays.

The talent retention programs, critical given the 30% attrition in technical roles, had evolved from standard HR practices to innovative partnerships. The company sponsored employees for executive education at IIMs, created an innovation fund where engineers could prototype improvements, and offered shadow equity that would vest if the company achieved profitability.

Safety improvements went beyond statistics. The plant hadn't had a fatal accident in 18 months—remarkable for a facility handling molten metal at 2,000°C. Every near-miss was investigated as thoroughly as an actual accident. Workers could stop production for safety concerns without repercussion. The safety culture, initially resisted as "unnecessary bureaucracy," had become a source of pride.

Environmental milestones were being achieved despite financial constraints. The plant's water consumption—2.8 cubic meters per tonne of steel—was among the lowest in India. The green belt, covering 33% of plant area with 200,000 trees, had created a microclimate that reduced ambient temperature by 2°C. The solar power project, though scaled back from 100 MW to 20 MW due to funding constraints, would commence generation by December 2025.

Customer relationships were slowly improving. The rejection rate had dropped from 8% to 2%. Repeat orders, non-existent in the first year, now constituted 40% of sales. The company had secured long-term contracts with three oil companies for pipeline-grade steel, providing ₹500 crore in assured annual revenue.

Recent operational initiatives focused on cost reduction rather than capacity expansion. The alternate fuel injection system, using plastic waste and biomass, would reduce coke consumption by 20%. The waste heat recovery project, adding 30 MW of power generation, would make the plant energy-positive. Every percentage point improvement in yield—currently at 92%—saved ₹50 crore annually.

Yet for all these improvements, the fundamental challenge remained. The plant was getting better at making steel, but not necessarily better at making money. The gap between operational excellence and financial performance highlighted a truth the industry had known for decades: in commodity businesses, location and timing matter more than technology and efficiency.

IX. Playbook: Lessons from a Public Sector Steel Venture

The consultant from McKinsey stood before NMDC's board in 2010, presenting slide after slide of hockey-stick growth projections. "Steel demand will double by 2020," he proclaimed, pointing to China's trajectory. "First-mover advantage in modern capacity will create lasting competitive moats." Fourteen years and ₹24,000 crore later, those slides serve as a masterclass in how smart people make catastrophic capital allocation decisions.

The first lesson from NMDC Steel's journey is the most painful: in commodity businesses, timing isn't just important—it's everything. The decision to build Nagarnar during the 2009-2010 commodity supercycle seemed logical when steel prices exceeded $800 per tonne and India was importing 10 million tonnes annually. By the time production began in 2023, Chinese overcapacity had crashed global prices to $450, and India had become a net exporter. The seven-year construction period had transformed a strategic opportunity into a structural disadvantage.

The public sector execution challenges were predictable yet somehow unexpected. Government-owned enterprises operate under constraints private companies don't face—every purchase order scrutinized for corruption, every hire subject to reservation quotas, every decision potentially questioned by the Comptroller and Auditor General. What takes JSW three months takes a PSU nine months. In industries where speed determines survival, this handicap proves fatal.

Consider the technology selection debacle. NMDC spent two years evaluating POSCO's FINEX technology, another year negotiating contracts, then abandoned it entirely when technical issues emerged. A private player would have decided in six months and pivoted in three. The cost wasn't just the ₹500 crore in wasted preparatory work—it was the opportunity cost of entering production three years late.

The vertical integration thesis that seemed so compelling—iron ore miner becomes steelmaker—ignored operational realities. Mining and steelmaking require fundamentally different capabilities. Mining is about geology, logistics, and government relations. Steelmaking is about chemistry, customer relationships, and rapid response to market changes. NMDC's DNA, built over 60 years of mining, couldn't transform overnight into a steel company's genetic code.

The location decision revealed another blind spot. Nagarnar's proximity to iron ore seemed like an advantage worth the infrastructure challenges. But steel plants need more than raw materials—they need proximity to customers, skilled workers, and logistics networks. Tata Steel's Jamshedpur plant, despite being 400 kilometers from its mines, generates better returns because it's closer to auto manufacturers, ports, and engineering talent.

Capital allocation during construction showed how government ownership distorts decision-making. When costs overran by ₹8,000 crore, a private company would have stopped, reassessed, possibly abandoned the project. But PSUs face different incentives—admitting failure means parliamentary questions, CBI investigations, and career destruction for bureaucrats. So money keeps flowing into projects that should be terminated, creating assets that destroy value from day one.

The stakeholder management complexity in PSUs deserves its own business school case. NMDC Steel had to satisfy the Steel Ministry (wanting production targets met), Finance Ministry (demanding returns on investment), local politicians (seeking employment and contracts), unions (demanding wages comparable to profitable plants), environmental groups (opposing expansion), and shareholders (wanting dividends). These competing demands created paralysis—every decision optimized for political acceptability rather than business logic.

The market entry strategy—or lack thereof—highlighted how PSUs misunderstand competition. NMDC Steel assumed that superior technology would automatically win customers. They didn't appreciate that Tata Steel's relationship managers had been visiting automotive companies for decades, that JSW's supply chain could deliver within 24 hours, that imported steel would always provide a price ceiling. In commodity markets, customer relationships and logistics matter more than product quality.

The financing structure revealed government's flawed approach to industrial projects. Instead of equity funding that could absorb losses during ramp-up, NMDC Steel carried ₹4,500 crore in debt from day one. Interest payments of ₹400 crore annually meant the company needed to generate positive EBITDA immediately—impossible for any greenfield project. Private players like JSW fund new plants with equity, converting to debt only after operations stabilize.

The human capital challenge went beyond hiring. PSU culture—emphasizing process over output, seniority over merit, job security over performance—clashed with steel manufacturing's demands. When a blast furnace campaign extends from 15 to 20 years based on operator skill, you can't afford to promote based on years of service. Yet changing organizational culture proved harder than building a ₹24,000 crore plant.

The technology paradox deserves special attention. NMDC Steel's plant is genuinely world-class—automation, environmental controls, and product capability match global standards. But in commodity markets, being 10% better doesn't matter if you're 20% more expensive. The sophisticated technology that was supposed to be an advantage became a burden, requiring expensive maintenance and specialized skills while producing steel that customers wouldn't pay premiums for.

The government's role as shareholder created unique dysfunction. Unlike private promoters who might inject capital during downturns, the government couldn't be seen favoring one PSU over others. Unlike financial investors who might push for restructuring, the government prioritized employment over efficiency. The result: a shareholder that neither supported nor disciplined, leaving management in perpetual limbo.

The lesson about commodity cycles bears repeating: they're longer, deeper, and more violent than any spreadsheet projects. The consultants who predicted Indian steel demand doubling by 2020 weren't wrong about direction—just about timing and magnitude. Demand did grow, but so did supply. Prices didn't rise; they collapsed. The cycle that was supposed to turn in 2-3 years has lasted a decade.

For industrial policy, NMDC Steel offers sobering lessons. Governments dream of creating national champions through large capital investments. But industrial competitiveness comes from ecosystems, not individual plants. South Korea's POSCO succeeded because the entire economy was mobilized around export-oriented industrialization. India's PSU steel plants struggle because they're islands of government ownership in an ocean of private competition.

The ultimate lesson might be about acknowledging reality versus maintaining face. Three years into operations, it's clear NMDC Steel's current model isn't working. A private company would restructure, sell, or shut down. But PSUs operate in a political economy where admitting failure is worse than perpetual losses. So the plant continues operating, destroying value daily, because the alternative—acknowledging that ₹24,000 crore was wasted—is politically unthinkable.

X. Bear vs. Bull: The Investment Case

The elevator pitch for shorting NMDC Steel writes itself: a loss-making, government-owned steel company with negative EBITDA margins, competing in an oversupplied commodity market against more efficient private players, located far from customers, burning cash while trading at 0.6x book value—which still seems expensive given value destruction. Yet three institutional investors quietly accumulated 2% of equity in Q2 2025. Were they seeing something others missed, or simply catching a falling knife?

The Bear Case: Structural Value Destruction

The numbers are brutally clear. Three years of operations: ₹1,801 crore in cumulative losses. EBITDA margin: negative 20.60%. Return on equity: negative 8.26%. Cash burn: ₹200 crore monthly. At current loss rates, shareholder equity of ₹14,800 crore would be completely eroded in seven years. This isn't a turnaround story—it's a countdown to insolvency.

The commodity cycle headwinds show no signs of abating. China, producing 1 billion tonnes annually (half of global output), has 200 million tonnes of excess capacity. Every time steel prices recover above $500, Chinese exports flood markets. India's domestic capacity of 150 million tonnes serves demand of 120 million tonnes. This structural oversupply will persist until massive capacity shutdowns occur—and inefficient plants close first.

The competitive position remains untenable. Tata Steel's Jamshedpur plant, depreciated over decades, has cash costs of ₹35,000 per tonne. JSW's Dolvi plant, located near Mumbai port, can import coking coal at 20% lower landed cost. NMDC Steel, with its modern but remote plant, has structural costs of ₹48,000 per tonne. No amount of operational improvement can overcome a 35% cost disadvantage in a commodity business.

Execution track record suggests problems run deeper than market conditions. The April 2025 achievement of rated capacity came five years late. The rejection rate, though improved, remains double the industry average. The employee productivity—757 tonnes per person—is half that of private peers. If management couldn't execute during construction, when government attention was highest, why expect improvement during operations?

The debt burden becomes unsustainable as losses mount. Current debt of ₹4,500 crore carries ₹400 crore annual interest. The company needs another ₹4,000 crore for the pellet plant and slurry pipeline. With negative cash flows, this funding must come from additional borrowing. At 10% interest rates, debt service would exceed ₹800 crore annually—impossible to service even if operations break even.

Government ownership ensures perpetual disadvantage. Procurement decisions take months. Salary structures can't compete for talent. Board appointments prioritize bureaucratic experience over industry knowledge. The government can't inject capital without parliamentary approval, can't sell without political backlash, can't restructure without union opposition. It's the worst of all worlds—a commercial entity with non-commercial constraints.

The Bull Case: Hidden Value and Optionality

The replacement value argument remains compelling. Building Nagarnar today would cost ₹35,000 crore—triple the current market capitalization. The land alone—1,980 hectares in mineral-rich Chhattisgarh—would cost ₹2,000 crore. The environmental clearances, taking seven years to obtain today, are invaluable. At 0.6x book value, the market prices NMDC Steel as if the assets are worth 40% of construction cost.

The technological superiority isn't fully monetized. The 1650mm width capability—unique in India's public sector—becomes valuable as automotive demand shifts to SUVs requiring wider steel. The API-grade certification opens oil and gas markets growing at 15% annually. The dual-phase steel capability positions for electric vehicle lightweighting. When—not if—India's quality requirements increase, NMDC Steel is already there.

India's long-term steel demand story remains intact. Per capita consumption at 75 kg compares to global average of 230 kg and China's 650 kg. To reach even the global average by 2040, India needs 350 million tonnes capacity. The infrastructure pipeline—₹100 trillion over 15 years—requires domestic steel. Import substitution alone—India still imports 15 million tonnes of specialized grades—represents a ₹30,000 crore opportunity.

The iron ore advantage is permanent and widening. While competitors pay market prices, NMDC Steel sources from captive mines at extraction cost. As high-grade ore becomes scarcer—India's reserves declining from 65% to 62% Fe average—this advantage magnifies. The Deposit 4 development adds 30 years of assured supply when competitors struggle to secure 3-year contracts.

Government backing, while constraining, prevents bankruptcy. Unlike private players that might shut unprofitable plants, the government will support NMDC Steel through cycles. Additional funding, while slow, remains available. Strategic importance—steel for defense, railways, infrastructure—ensures continued operation. In downturns, this stability has value.

Recent operational improvements suggest turnaround potential. Production rising 8.5% monthly. Rejection rates falling from 8% to 2%. Customer relationships strengthening with 40% repeat orders. The slurry pipeline and pellet plant, once operational, would cut costs by ₹5,000 per tonne. At industry-average margins, the company would generate ₹1,500 crore EBITDA.

The privatization option provides asymmetric upside. The government's privatization agenda, though stalled, will eventually resume. Strategic sale to Tata or JSW would immediately unlock value—they could optimize operations, reduce costs 30%, and integrate with existing networks. Even minority stake sale to strategic investors would rerate the stock. At 1x book value—still cheap for operational steel assets—the stock would double.

Market timing might finally align. Steel cycles average 7-10 years. The current downturn, beginning in 2021, is entering its fourth year. China's domestic stimulus, decarbonization driving closures, and India's infrastructure spending could tighten markets by 2026. When cycles turn, operational leverage is enormous—a 10% price increase would swing NMDC Steel from ₹500 crore loss to ₹1,000 crore profit.

The Verdict

The bear case rests on current reality—persistent losses, structural disadvantages, and government ownership constraints. The bull case requires faith in future changes—market recovery, operational improvements, and potential privatization. For fundamental investors, the question becomes: Is the optionality worth the carry cost of ongoing losses?

The answer depends on time horizon and risk tolerance. For investors needing returns within 2-3 years, NMDC Steel is uninvestable. The losses will continue, the stock will drift, and opportunity cost will mount. For those with 5-7 year horizons, willing to bet on India's infrastructure story and potential restructuring, the risk-reward at 0.6x book value might be attractive.

But perhaps the real lesson is that some assets are neither good investments nor good shorts—they're simply dead money. NMDC Steel might be one of them, perpetually cheap for good reasons, never quite failing enough to force change, limping along as a monument to misallocated capital and misplaced ambition.

XI. Strategic Options & Future Scenarios

The boardroom at NMDC Steel's Hyderabad headquarters has a tradition—every strategic planning session begins with the same slide: "Status Quo Is Not An Option." After three years of losses, with shareholders growing restless and the government's patience wearing thin, that statement has evolved from corporate motivational speak to existential reality. The company faces five distinct paths forward, each with radically different implications for stakeholders.

Scenario 1: The Privatization Path

The whispers started in the steel ministry corridors in early 2025—NMDC Steel might be the test case for privatizing loss-making PSUs. The logic was compelling: private management could cut costs by 30%, optimize product mix, and leverage existing customer relationships. Tata Steel and JSW had both expressed informal interest, though at valuations that would mean massive losses for the government.

A strategic sale would likely value NMDC Steel at ₹8,000-10,000 crore—below book value but above current market capitalization. The buyer would get modern assets at distressed prices, captive iron ore access, and elimination of a competitor. The synergies are obvious: JSW could integrate Nagarnar with its Dolvi-Vijaynagar corridor, saving ₹1,000 crore annually in logistics. Tata could leverage its automotive relationships to finally utilize NMDC Steel's sophisticated products.

The obstacles are equally obvious. Unions would strike—3,000 direct employees and 10,000 indirect jobs at stake. Chhattisgarh's government, regardless of party, would oppose losing the state's largest industrial investment. The precedent—admitting a ₹24,000 crore government project failed—would haunt every future PSU investment.

Scenario 2: Strategic Partnership Model

The middle path involves maintaining majority government ownership while bringing in strategic partners for specific functions. ArcelorMittal could take 26% equity and manage operations. A Japanese trading house like Mitsubishi could handle marketing and exports. Technology partners could optimize specific processes for revenue share.

This model has precedents—SAIL's joint ventures with international steel companies generated better returns than standalone operations. The government retains control, unions accept gradual change, and operational efficiency improves. NMDC Steel could focus on specialized grades where technology matters, leaving commodity grades to volume players.

The execution complexity would be enormous. Multiple partners mean multiple agreements, conflicting interests, and diluted accountability. The government's 51% stake would still mean bureaucratic decision-making for major investments. Partners might cherry-pick profitable segments, leaving NMDC Steel with unviable operations.

Scenario 3: The Niche Player Strategy

Instead of competing across all products, NMDC Steel could focus exclusively on high-margin, specialized grades where its technology provides genuine advantage. API-grade pipes for oil exploration, defense-grade steel for naval vessels, ultra-high-strength steel for space applications. The volumes would be lower but margins higher.

This requires dramatic restructuring. The blast furnace, designed for 3 million tonnes, would run at 30% capacity—economically unviable. The workforce would need reskilling from volume production to precision manufacturing. Marketing would shift from price competition to technical collaboration with customers.

The precedent exists in global markets. Sweden's SSAB, with similar high costs, focuses on specialty steels with 20% EBITDA margins. Austria's Voestalpine abandoned commodity grades entirely. But these transformations took decades and required patient capital that public markets rarely provide.

Scenario 4: The Export Orientation

With domestic markets oversupplied, NMDC Steel could pivot to exports, leveraging India's steel cost advantage versus developed markets. The Middle East, consuming 50 million tonnes annually but producing only 20 million, offers opportunities. Africa's infrastructure boom requires 30 million tonnes of imports. Even 10% market share would fully utilize Nagarnar's capacity.

The challenges multiply with distance. Nagarnar sits 1,000 kilometers from the nearest port. Transportation would add $50 per tonne, eroding cost advantages. Export markets demand consistent quality, reliable delivery, and long-term relationships—all areas where NMDC Steel has struggled. Currency fluctuations add another layer of risk to an already volatile business.

Scenario 5: The Technology Licensing Play

The most radical option: abandon steel production entirely and become a technology services company. The digital twin technology, developed at great cost, could be licensed to other steel plants. The environmental systems, achieving near-zero emissions, have value as countries impose carbon taxes. The automation expertise could be packaged as consulting services.

This would mean writing off most of the ₹24,000 crore investment—politically suicidal for any government. The technology, while sophisticated, isn't unique globally. And transforming a manufacturing company into a services firm would require capabilities NMDC Steel has never demonstrated.

The Most Likely Path: Muddle Through

Political economy suggests the most probable scenario: continue operating with periodic government support, hoping for market recovery. Small improvements—5% cost reduction here, 10% productivity gain there—while avoiding hard decisions. The government might inject equity during election years, provide interest subsidies during downturns, and mandate purchases by other PSUs.

This path leads to value erosion—not dramatic enough to force action, not successful enough to generate returns. NMDC Steel becomes a zombie company, technically alive but economically dead. Shareholders suffer slow dilution, employees face uncertain futures, and taxpayers bear hidden costs.

The Integration Option

One scenario gaining traction in government circles: merge NMDC Steel back with NMDC Limited, reversing the demerger. The mining profits could absorb steel losses, providing breathing room for turnaround. The integrated entity could optimize transfer pricing, share overhead costs, and present a cleaner story to investors.

The accounting would be complex—minority shareholders in both entities would need protection. The market would likely punish NMDC Limited's stock for reabsorbing a loss-making subsidiary. But it would solve the immediate crisis of NMDC Steel's standalone unviability.

Time Horizons and Trigger Points

Each scenario has different triggers. Privatization requires political will, likely after an election. Strategic partnerships need market recovery to attract partners. Niche strategy demands board courage to shrink before growing. Export orientation needs infrastructure investment. Technology licensing requires admitting defeat in manufacturing.

The timeline matters. Every month of losses reduces options. If accumulated losses exceed net worth—possible within four years at current rates—the company becomes technically insolvent, forcing government action. Credit rating downgrades could trigger debt covenants, accelerating the crisis.

The most honest assessment: NMDC Steel has 18-24 months to show dramatic improvement before political pressure forces dramatic action. Whether that action is privatization, restructuring, or government bailout depends on factors beyond management control—election outcomes, global steel cycles, and India's broader economic trajectory.

XII. Epilogue: Public Sector Dreams vs. Market Realities

The last shift change at Nagarnar happens at 10 PM, when the day workers hand over to night crew. In the darkness, the plant glows like a small city—blast furnaces burning orange, rolling mills lit fluorescent white, the endless movement of molten metal through vessels and ladles. From a distance, you can't tell if this ₹24,000 crore investment is profitable or bleeding money. Steel gets made, products get shipped, the machinery of production continues its relentless rhythm. But the market has already rendered its verdict.

NMDC Steel's story is ultimately about the gap between industrial policy dreams and market economy realities. When government officials stood at Nagarnar's groundbreaking in 2010, they saw more than just a steel plant. They saw energy security, import substitution, regional development, and national pride. They saw India taking its place among modern industrial nations. What they didn't see—or chose to ignore—were the invisible hands of global competition, commodity cycles, and technological disruption that would determine the project's fate.

The broader lesson extends beyond one failed investment. Across India, similar monuments to misplaced ambition dot the landscape—fertilizer plants that never reached capacity, airports that handle ten flights daily, ports that survive on government cargo. Each began with compelling PowerPoints about strategic importance and market opportunity. Each ended as a lesson in why governments make poor venture capitalists.

The cost isn't just the ₹24,000 crore invested in Nagarnar. It's the opportunity cost of capital that could have built hospitals, schools, or infrastructure with clear social returns. It's the human capital of talented engineers spending careers optimizing a structurally unviable business. It's the market distortion of subsidized capacity competing with efficient private investment.

Yet dismissing NMDC Steel as pure failure misses nuance. The plant does produce steel that India needs. It does employ thousands in one of India's poorest regions. It has created capabilities—technological, managerial, operational—that didn't exist before. In a parallel universe where China didn't flood markets with excess capacity, where Indian infrastructure spending doubled as projected, where commodity cycles aligned differently, Nagarnar might be profitable.

This counterfactual matters because India will face similar decisions again. Should the government invest in semiconductor fabrication? Green hydrogen production? Battery manufacturing? Each carries the same promise of strategic autonomy and industrial advancement. Each faces the same risks of execution delays, market timing, and global competition.

The comparison with successful state-led industrialization is instructive. South Korea's POSCO, China's Baosteel, and Japan's earlier Nippon Steel all began as government projects. But they emerged in protected markets, with patient capital, export focus, and most critically, the ability to shut unsuccessful ventures without political backlash. India's democratic constraints—parliamentary questions, judicial interventions, electoral cycles—make such ruthless efficiency impossible.

What success would actually look like for NMDC Steel remains unclear. Breaking even? Impossible with current cost structures. Generating returns above cost of capital? Unlikely even with perfect execution. Perhaps success means simply existing—maintaining India's steel capacity for strategic purposes, providing employment in backward regions, and developing capabilities for future cycles.

The human dimension deserves recognition. Thousands of engineers, operators, and managers have dedicated prime years to making Nagarnar work. They've solved technical problems, improved processes, and achieved operational milestones despite overwhelming structural challenges. Their efforts, while financially unrewarded, have created knowledge and experience that will outlast NMDC Steel's corporate existence.

For investors, NMDC Steel offers a masterclass in value destruction. Every classical valuation metric—DCF, replacement cost, earnings multiple—fails when a business has negative and declining cash flows. The stock price of ₹39 might seem cheap at 0.6x book value, but book value assumes assets can generate returns. When they can't, even one rupee might be overvalued.

The governance lessons are equally stark. Independent directors, however qualified, couldn't overcome government ownership constraints. Audit committees couldn't prevent value destruction when the business model itself was flawed. Minority shareholders discovered that government control means political priorities supersede economic returns.

Looking forward, NMDC Steel faces an existential reckoning. The government must decide whether strategic autonomy in steel production is worth perpetual losses. If yes, it should fund the company properly and abandon profit expectations. If no, it should exit quickly, accepting losses rather than compounding them. The current middle ground—expecting commercial returns from a structurally disadvantaged business—satisfies no one.

The global context adds urgency. As countries pursue net-zero emissions, steel production must transform from blast furnaces to hydrogen-based processes. This technological shift requires massive new investment that NMDC Steel cannot fund from operations. The company risks being stranded with obsolete assets just as it finally optimizes them.

Perhaps the ultimate lesson is about humility. Markets are complex adaptive systems that humble the smartest planners and best intentions. The consultants who projected demand, the engineers who designed plants, and the bureaucrats who approved investments weren't stupid or corrupt—they were just wrong about the future. In commodity businesses, being wrong about timing is indistinguishable from being wrong about everything.

NMDC Steel will likely continue operating for years, perhaps decades. Government ownership ensures survival if not success. The plant will produce steel, employ workers, and consume capital. Politicians will inaugurate expansions, unions will negotiate wages, and shareholders will hope for turnarounds that never arrive.

But the real verdict has already been delivered. In choosing to build Nagarnar, India bet that government industrial planning could create globally competitive manufacturing. The market has responded with brutal clarity: in the 21st century economy, competitive advantage comes from innovation, efficiency, and adaptation—qualities that government ownership systematically destroys.

The furnaces at Nagarnar will keep burning, the steel will keep rolling, and the losses will keep mounting. It's not a tragedy—tragedies require fallen heroes and moral lessons. It's simply what happens when public sector dreams meet market realities: slow, grinding, inevitable value destruction that everyone sees but no one can stop.

The story of NMDC Steel isn't over, but its ending is already written in the accumulated losses, mounting debt, and relentless competition. The only question is how long it takes to reach the inevitable conclusion, and how much more capital will be destroyed along the way.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube