Niva Bupa Health Insurance: India's Healthcare Revolution

I. Introduction & Episode Roadmap

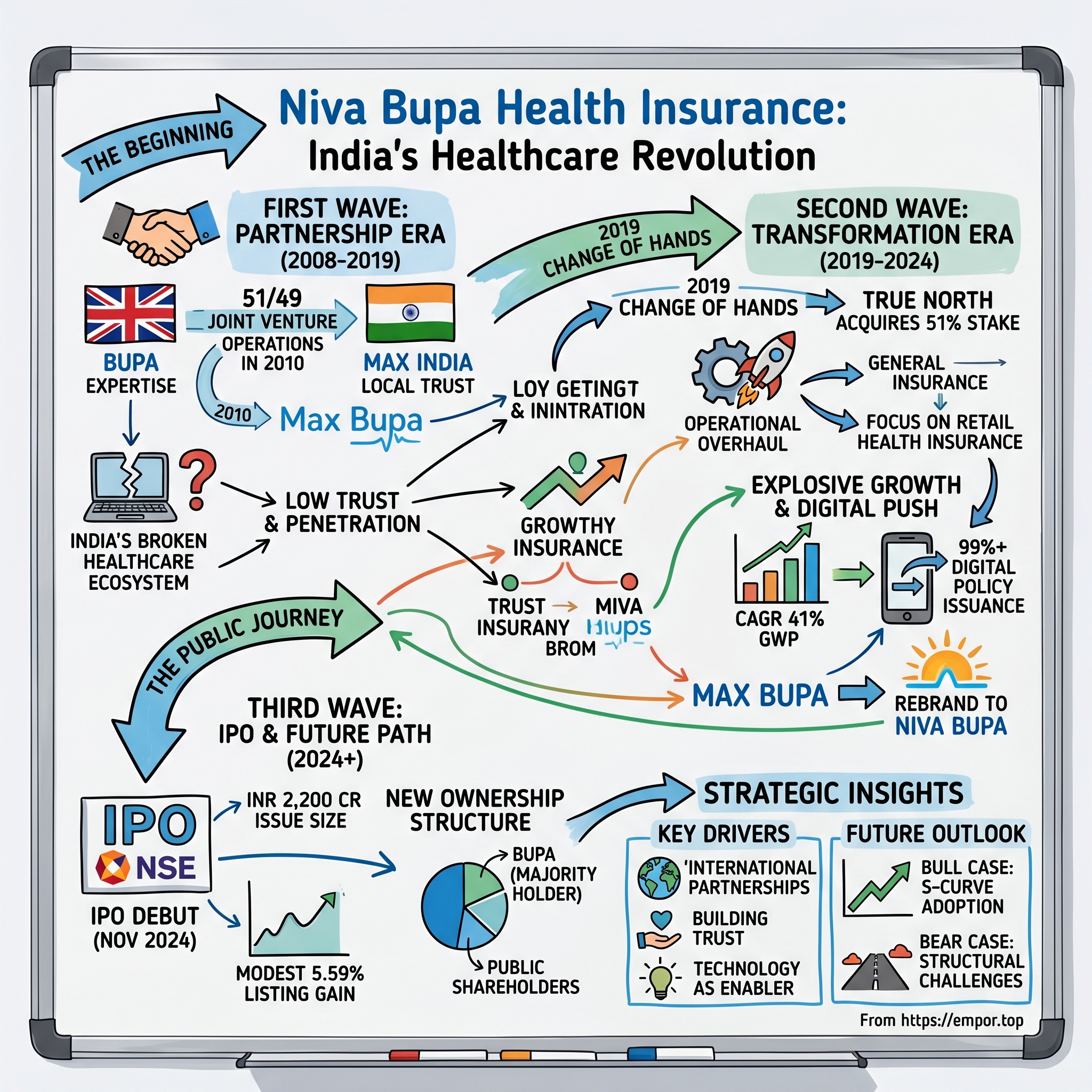

The trading floor at the National Stock Exchange erupted in applause at 9:15 AM on November 14, 2024. After years of private ownership and strategic maneuvers, Niva Bupa Health Insurance Company Limited had successfully completed an Initial Public Offering (IPO) on the National Stock Exchange of India (NSE), with a total issue size of INR 2,200 crore (c.£200 million) representing c16% of Niva Bupa's share capital. The shares opened at ₹78.14, delivering a 5.59% listing gain over the issue price of ₹74—a modest but respectable debut in a market increasingly scrutinizing healthcare valuations.

But this wasn't just another insurance IPO. This was the culmination of a 16-year journey that began with a British healthcare giant's bet on India's nascent health insurance market, weathered ownership changes, regulatory upheavals, and a global pandemic, to emerge as the 3rd largest and the 2nd fastest growing standalone health insurer (SAHI) in India based on overall health gross direct premium income (GDPI) of Rs 5,494.43 crore in FY24.

The question that frames our exploration today: How did a joint venture startup in 2008, entering a market where health insurance penetration rate in India was just 0.35%, transform into a public company serving millions while the entire Indian health insurance industry remained fundamentally underpenetrated?

This is a story of international partnerships meeting local execution, of patient capital confronting short-term pressures, and of technology disrupting traditional distribution—all set against the backdrop of India's healthcare awakening. We'll trace Niva Bupa's evolution from its origins as Max Bupa through multiple ownership transitions, examine how it navigated India's complex regulatory landscape, and understand what its journey reveals about building financial services businesses in emerging markets.

Along the way, we'll uncover the strategic decisions that mattered: Why Bupa chose India in 2008. How True North's entry in 2019 changed everything. What the 2024 IPO really means for India's insurance landscape. And perhaps most importantly—whether this story is just beginning or approaching its climax.

II. The India Healthcare Opportunity & Context

Picture India in the early 2000s: a nation of over a billion people where visiting a doctor meant either queuing for hours at overcrowded government hospitals or paying cash at private clinics. Health insurance was a foreign concept to most Indians—something companies provided to white-collar employees, not a product individuals purchased. Out-of-pocket expenses accounted for over 70% of healthcare spending. A single medical emergency could wipe out a family's savings, pushing millions into poverty each year.

Into this landscape stepped the Insurance Regulatory and Development Authority of India (IRDAI), constituted in April 2000 following the recommendations of the Malhotra Committee. The regulator's formation marked a watershed moment: The IRDA opened up the market in August 2000 with an invitation for registration applications; foreign companies were allowed ownership up to 26 percent. For the first time, private players could enter India's insurance market, previously monopolized by government-owned companies.

The standalone health insurance license, introduced in the mid-2000s, created an entirely new category. Unlike general insurers who treated health as one product among many, these specialized players would focus exclusively on health coverage. The opportunity was staggering: a massive, underserved population, rising incomes, increasing lifestyle diseases, and growing awareness of healthcare costs.

Enter Bupa—the British healthcare services expert that had been quietly studying emerging markets. Bupa was a founding shareholder when the business (then known as Max Bupa) was first established in India in 2008. But why India? And why partner with Max?

Established in 1947, the Bupa Group is an international healthcare organisation serving over 50 million customers globally as of December 31, 2023. Unlike typical insurers, Bupa operated without shareholders—it was essentially a provident association reinvesting profits into healthcare. This long-term orientation made it uniquely suited for India's nascent market where profits would take years to materialize.

The Max Group, led by Analjit Singh, brought local credibility and distribution knowledge. Max had already built a successful life insurance venture with New York Life. They understood Indian consumers, regulatory nuances, and critically, how to build trust in a market scarred by decades of poor insurance experiences.

Niva Bupa Health Insurance was founded in 2008 as a joint venture between Max India and Bupa and started operations in 2010. The timing seemed perfect: India's GDP was growing at 8-9% annually, the middle class was expanding, and corporate India was increasingly offering health benefits. The reality would prove far more challenging.

The competitive landscape in 2010 was dominated by four public sector giants—New India Assurance, Oriental Insurance, National Insurance, and United India Insurance—who controlled over 60% of the health insurance market. These behemoths had vast distribution networks, government backing, and decades-old relationships. New private entrants like Star Health, Apollo Munich (later HDFC ERGO), and Religare were all racing to establish themselves.

What nobody fully appreciated was how broken India's health insurance ecosystem truly was. Hospitals routinely overcharged insured patients. Claims processing took weeks. Policy documents were incomprehensible. Fraud was rampant. Trust was non-existent. The entire value chain needed rebuilding—and that would take more than capital and good intentions.

III. The Founding Story: Max & Bupa Partnership (2008–2019)

The first meeting between Max India executives and Bupa's international team in 2007 was a study in contrasts. The British delegation arrived with thick binders of actuarial models, global best practices, and risk management frameworks developed over six decades. The Indian team came armed with stories—of families selling jewelry to pay for surgeries, of fake medical bills, of insurance agents who disappeared after selling policies.

Analjit Singh, Max Group's chairman, had a vision that went beyond mere profitability. He saw health insurance as essential infrastructure for India's development, much like roads or power plants. His pitch to Bupa was simple: "You bring the expertise, we'll teach you India."

The joint venture agreement signed in 2008 gave Max India 51% and Bupa 49%, respecting India's foreign ownership limits. But the real negotiations were cultural. Bupa's representatives were stunned by Indian pricing expectations—premiums that wouldn't cover a basic health checkup in London were supposed to insure entire families for a year. Max's team struggled to explain why Bupa's sophisticated underwriting models, which worked perfectly in developed markets, would fail in India where medical records were handwritten and often fabricated.

The early product development was a fascinating exercise in adaptation. Bupa's global templates assumed things that didn't exist in India: standardized treatment protocols, electronic health records, established referral systems. The first product, launched in 2010, was essentially rebuilt from scratch. It covered hospitalization (because that's what Indians associated with insurance), included family coverage (because individual policies wouldn't sell), and critically, offered cashless treatment at network hospitals—a feature that would become Niva Bupa's differentiator.

In Jun 2011, it integrated with Insurance Regulatory and Development Authority's Integrated Grievance Management System in real-time, which made the company the first health insurance company in India to have such a system. This wasn't just compliance—it was a statement of intent. While competitors viewed regulatory requirements as burdens, Max Bupa saw them as opportunities to build trust.

Building distribution in those early years was grueling. India's insurance was sold, not bought. This meant feet on the street, relationships with banks, and most challenging, educating a sales force accustomed to selling life insurance (where commissions were higher and sales simpler) to understand health products.

The Bangalore expansion in 2012 revealed the market's complexity. What worked in Delhi failed in Karnataka. Hospital networks had to be rebuilt, pricing recalibrated, even marketing messages adjusted for local sensibilities. The company was essentially building multiple regional businesses under one brand.

By 2015, the struggle years were taking their toll. Losses mounted as claims ratios exceeded 100% in some quarters. The Indian health insurance industry was in a price war, with companies undercutting each other to gain market share. Max Bupa was burning cash, and neither parent seemed willing to invest substantially more.

The breakthrough came from an unexpected source: technology. While competitors focused on traditional distribution, Max Bupa quietly built digital capabilities. Online policy issuance, digital claims processing, app-based services—investments that seemed premature in 2015 would prove prescient by 2019.

The real test came in 2018 when Max India decided to exit. The company had burned through hundreds of crores with no clear path to profitability. But Bupa, seeing the long-term potential, stayed. The search for a new partner would lead to the next chapter of transformation.

IV. The True North Transformation (2019–2024)

February 2019 marked a turning point that few outside India's private equity circles fully grasped. Max India's entire 51 per cent stake was acquired by Fettle Tone LLP, an affiliate of private equity firm True North for ₹1,010 crore. True North wasn't just another financial investor—they were operators who had previously transformed businesses across India's financial services landscape.

The Monday morning after the deal closed, True North's operating partners walked into Max Bupa's Gurgaon headquarters with a simple message: "Forget everything you know about health insurance in India. We're going to rebuild this from first principles."

The transformation began with a fundamental insight: Max Bupa had been trying to be everything to everyone. True North's playbook was different—focus ruthlessly on retail health insurance where margins were better and customer relationships deeper. Corporate group insurance, despite its scale, became secondary.

The numbers tell the story of explosive growth: Premium crossed ₹4,000 crore by 2022, up from ₹1,000 crore in 2019. But raw growth wasn't the achievement—it was profitable growth in an industry notorious for losing money while scaling.

The digital transformation under True North wasn't just about apps and websites. It was about reimagining every customer touchpoint. The company built what they called a "digital nervous system"—real-time tracking of every policy application, claim, complaint, and query. Machine learning models began predicting which customers would likely file claims, enabling proactive engagement. The call center, traditionally a cost center, became a profit center through intelligent cross-selling.

Then came the rebrand—from Max Bupa to Niva Bupa. "Niva" is a popular Hindi/Sanskrit word and also means SUN – which is a symbol of hope, positivity, energy and above all life itself. This wasn't mere cosmetics. It signaled independence from the Max legacy and aligned with Bupa's global brand while maintaining local relevance.

The distribution revolution was perhaps most dramatic. The company built a 410-person telemarketing team using machine learning lead scoring, product recommendations, and real-time CRM. But they also recognized that India remained a relationship market. The key was marrying high-tech with high-touch—using technology to empower human agents, not replace them.

From FY 2022 to FY 2024, overall GWP grew at CAGR of 41.27%, retail health increased by 33.41%. For FY24, it had 99.95% of its new policies applied for digitally, 81.27% of the claims submitted digitally, 85.39% of renewals completed without human intervention, and 95.50% of the number of payments received made digitally through its website and mobile app.

The product innovation during this period was remarkable. Instead of copying competitors, Niva Bupa introduced features others considered impossible in India: unlimited restoration of sum insured, coverage for mental illness, global coverage options. Each innovation was carefully calibrated—generous enough to attract customers, prudent enough to maintain profitability.

The True North years also saw geographical expansion done right. Rather than planting flags everywhere, the company methodically built presence in high-potential markets. The firm has 210 physical branches across 22 states and 4 union territories in India. Each new geography was treated as a mini-launch, with local partnerships, customized products, and dedicated service infrastructure.

By 2023, the transformation was complete. What True North had acquired as a struggling joint venture was now a profitable, technology-enabled health insurer ready for its next phase. The question was: what would that next phase be?

V. The Bupa Majority Stake & IPO Journey (2023–2024)

September 2023 brought news that sent ripples through India's insurance industry: Bupa's joint venture partner, True North, agreed to sell a significant part of its stake in Niva Bupa. This transaction has now received regulatory approval which means that Bupa's shareholding has increased by around 20% to approximately 63%.

This wasn't just a stake sale—it was a validation of India's health insurance opportunity by one of the world's most sophisticated healthcare companies. The transaction valued Niva Bupa at over ₹10,000 crore, a 10x multiple from True North's entry just four years earlier.

Inside Bupa's London headquarters, the India investment had become a board-level priority. The move comes as India's insurance industry is experiencing strong growth amidst increasing awareness and demand for health insurance. The pandemic had accelerated India's health insurance adoption by perhaps five years. Digital distribution was finally working. The regulatory environment was supportive. The stars were aligning.

In January 2024, Bupa reaffirmed its commitment to India's growing market with its continued investment in India and became the majority shareholder in Niva Bupa. This was one of the largest transactions in Indian insurance since the FDI limit in the insurance sector has been raised to 74 percent according to the 2021 union budget.

The IPO preparation began immediately. Morgan Stanley and Kotak Mahindra Capital led a process that would test whether public markets were ready to value an Indian health insurer appropriately. The challenge was positioning: Niva Bupa was profitable but with a low return on equity of 6.41% over last 3 years. It was growing rapidly but in a highly competitive market.

The roadshow in October 2024 was revealing. International investors asked about medical inflation, claims ratios, and regulatory risks. Indian institutions focused on distribution strength and market share gains. Everyone wanted to know: was this Star Health 2.0, or something different?

Niva Bupa has announced that it has already raised Rs 990 crore from anchor investors in a bidding concluded on November 6, 2024. The anchor book included marquee names—a vote of confidence in the story. But it was retail investors who would determine the IPO's success.

Niva Bupa Health Insurance IPO bidding started from November 7, 2024 and ended on November 11, 2024. The shares got listed on BSE, NSE on November 14, 2024. The subscription was modest—just 1.17 times—reflecting market caution about insurance valuations.

The listing day was anticlimactic by Indian IPO standards. No doubling of price, no media frenzy. Just a steady debut at ₹78.14, a 5.59% premium to the issue price. But for Bupa's leadership, this was perfect. They weren't looking for speculators but long-term investors who understood the business.

Bupa will remain a majority shareholder following the IPO. This was crucial—it signaled continued commitment while providing liquidity and growth capital. The IPO proceeds would augment its capital base to maintain and strengthen solvency levels, enabling further expansion without diluting returns.

The post-IPO structure was elegant: Bupa held 56%, True North (through Fettle Tone) retained a stake, and public shareholders owned about 16%. It balanced control, alignment, and market validation—a structure that would become a template for similar transactions.

VI. Business Model & Operations Deep Dive

Understanding Niva Bupa requires peeling back layers of operational complexity that most investors never see. At its core, this is a business of probability and trust, wrapped in technology and delivered through relationships.

The company had 14.73 million active lives insured as of March 31, 2024. But these aren't just numbers—each represents a family's health security, a claims probability, a renewal opportunity. The business model monetizes the gap between premiums collected and claims paid, but the real value creation happens in between.

Start with product architecture. Unlike general insurance where a car is a car, health insurance must account for infinite human variation. A 35-year-old software engineer in Bangalore has different health risks than a 35-year-old farmer in Bihar. Niva Bupa's actuarial models incorporate over 200 variables, from pin code-level disease prevalence to occupation-specific accident rates.

The retail versus group split reveals strategic choices. The company strategically focuses on the retail health market and its GWP from retail health market accounted for 68.47% of overall GWP for Fiscal 2024. Retail customers are stickier, more profitable, and provide direct relationships. Group insurance, sold to corporates, offers scale but commoditized pricing and annual churn.

Distribution is where rubber meets road. The 410-person telemarketing team using machine learning lead scoring sounds impressive, but the real innovation is micro-segmentation. The AI doesn't just score leads—it predicts which product, at what price point, communicated in which language, is most likely to convert. A lead from Chennai gets a different call script than one from Chandigarh.

The digital infrastructure deserves special attention. 95.50% of the number of payments received made digitally through its website and mobile app. This isn't just convenience—it's cost reduction. Every digital transaction saves ₹50-100 in processing costs. Multiply that by millions of transactions, and it's a competitive advantage.

Hospital network management is perhaps the most underappreciated capability. Niva Bupa doesn't just sign up hospitals—it actively manages them. Automated claim audits flag unusual billing patterns. Preferred providers get faster payments in exchange for better rates. The network becomes a moat—customers choose insurers based on hospital coverage.

The claims process reveals operational philosophy. Traditional insurers make claiming difficult, hoping friction reduces payouts. Niva Bupa took the opposite approach: 10,000+ network hospitals across India, that facilitate cashless claim processing in less than 30 minutes. The bet is that smooth claims create customer evangelists who drive organic growth.

Technology integration goes beyond customer-facing apps. The core insurance platform runs on cloud infrastructure, enabling real-time pricing updates, instant policy modifications, and dynamic risk assessment. APIs connect with hospitals, diagnostic centers, pharmacies, creating an ecosystem, not just a product.

The workforce strategy is distinctive. While competitors outsource extensively, Niva Bupa maintains in-house expertise in critical areas: actuarial, claims assessment, technology. The logic is simple—these capabilities are competitive advantages, not costs to minimize.

Unit economics tell the real story. Average premium per retail policy: ₹15,000-20,000. Claims ratio: 65-70%. Operating expenses: 25-30%. That leaves 5-10% for profit—razor-thin margins that require massive scale. Hence the obsession with growth, efficiency, and retention.

VII. Financial Performance & Metrics

The numbers tell a story of transformation, but you need to read between the lines to understand what really happened. Market cap of ₹14,960 crore, Revenue ₹5,621 crore, Profit ₹141 crore—these headlines mask dramatic underlying changes.

Start with growth trajectory. The 40.1% profit growth CAGR over the last 5 years sounds impressive until you realize it's from a near-zero base. More revealing is the premium growth: from ₹1,000 crore in 2019 to ₹5,494 crore in FY24. That's not organic growth—it's a business model transformation.

The profitability evolution is instructive. Niva Bupa has successfully transitioned from a net loss of INR 196.53 crore in FY 2022 to a net profit of INR 81.85 crore in FY 2024. This wasn't cost-cutting—revenues grew throughout. It was about claims management, risk selection, and operational leverage finally kicking in.

On a fully consolidated basis at HY 2024, Niva Bupa contributed £220m in revenues and a £45m underlying loss, resulting from acquisition cost strain on short term new business and renewals. The loss seems concerning until you understand insurance accounting—new business is expensive upfront but profitable over time. The strain indicates growth investment, not operational problems.

The return on equity question haunts the valuation. Company has a low return on equity of 6.41% over last 3 years. In isolation, this looks terrible. But context matters: health insurance is capital-intensive, regulatory solvency requirements lock up capital, and the business was transitioning from startup to scale. ROE should improve as premium-to-capital ratios optimize.

Cash flow dynamics reveal the business model's beauty and challenge. Premiums arrive upfront, claims pay out over time. This creates float—money to invest while waiting for claims. But medical inflation means future claims cost more than modeled. It's a race between investment returns and medical cost escalation.

Expense ratios show operational leverage emerging. Management expenses as a percentage of GWP to 39.29% in FY24, 41.14% in FY23, from 42.46% in FY22. Every percentage point improvement drops straight to the bottom line. At ₹5,000 crore premium, 1% equals ₹50 crore—material in a thin-margin business.

Solvency ratios indicate financial strength. Insurance regulators mandate minimum capital relative to risks underwritten. Niva Bupa maintains buffers above requirements, enabling growth without constant capital raises. The IPO proceeds strengthen this further, providing dry powder for expansion.

Comparing with peers provides perspective. Star Health, the largest standalone health insurer, trades at significantly higher multiples despite similar growth rates. ICICI Lombard and HDFC ERGO, as diversified general insurers, command premium valuations. Niva Bupa's discount reflects its smaller scale and shorter public track record.

Geographic revenue concentration shows opportunity and risk. Metro cities contribute disproportionately to premiums, but growth is faster in Tier 2/3 cities. The expansion strategy must balance profitable urban markets with higher-growth but lower-margin emerging markets.

Investment income contributes increasingly to profitability. As the premium base grows, so does investible float. In a rising rate environment, this becomes a meaningful earnings driver. The investment portfolio remains conservative—government securities and high-rated corporate bonds—prioritizing safety over returns.

VIII. The India Health Insurance Market Dynamics

To understand Niva Bupa's position, you must first grasp the almost incomprehensible scale of India's health insurance opportunity. The Indian health insurance industry is set to grow at a compound annual growth rate (CAGR) of 12.8% from ₹1.3 trillion (US$15.1 billion) in 2024 to ₹2.0 trillion ($23.8 billion) in 2028. Yet, this growth comes from a tiny base.

The penetration statistics are staggering in their implications. Insurance penetration fell to 3.7 per cent in the 2023-24 financial year. India's insurance penetration remains significantly lower than the global average of 7 per cent. More specifically for health insurance, health insurance penetration rate in India (0.35%), which was lower as compared to other regional markets such as Taiwan (1.8%), Australia (0.93%), China (0.78%), and Hong Kong (0.67%) in 2023.

Think about what 0.35% penetration means: for every 1,000 Indians, only 3-4 have private health insurance they purchased themselves. The rest rely on employer coverage, government schemes, or more commonly, pray they don't get sick.

Niva Bupa has an overall market share of 5.1% in India's health insurance market. This positions it as the third-largest standalone health insurer, behind Star Health (market leader with ~30% share) and Care Health. But market share in a nascent market is less important than capability to capture growth.

The regulatory environment has become increasingly supportive. Effective from April 1, 2024, the Insurance Regulatory and Development Authority of India (IRDAI) removed the age cap of 65 years to buy health insurance policies. This opens up the senior citizen segment—historically underserved due to high medical risks but increasingly important as India ages and life expectancy increases.

Additionally, insurers are now prohibited from refusing to issue policies to individuals with severe medical conditions like cancer, heart or renal failure, and AIDS. While this seems consumer-friendly, it creates adverse selection risks that sophisticated insurers must price carefully.

Competition analysis reveals three distinct categories. First, standalone health insurers like Star Health, Care (formerly Religare), and Niva Bupa who focus exclusively on health. Second, large general insurers like ICICI Lombard, HDFC ERGO, and Bajaj Allianz who offer health among other products. Third, new-age insurtechs like Digit and Acko attacking with digital-first models.

Each competitor type has advantages. Standalone insurers have focus and expertise. General insurers have distribution and capital. Insurtechs have technology and agility. Niva Bupa's strategy is to combine standalone focus with Bupa's global expertise and True North's operational excellence.

Distribution wars intensify as everyone chases the same customers. Bancassurance partnerships command astronomical fees. Digital aggregators like PolicyBazaar extract massive commissions. Direct-to-consumer acquisition costs spiral higher. The winner won't be who spends most, but who converts and retains best.

The Ayushman Bharat effect is complex. The government's ambitious health coverage scheme for poor families theoretically reduces the private insurance market. In practice, it creates health awareness, builds hospital infrastructure, and establishes insurance habits that graduate to private coverage as incomes rise.

Medical inflation remains the existential challenge. Medical inflation climbed to 14% in 2024 and now outpaces general inflation. If medical costs rise faster than premiums can be increased, the entire business model breaks. This requires sophisticated provider management, fraud detection, and preventive care programs.

The pandemic's impact extends beyond temporary growth spurts. The Indian health insurance industry has witnessed impressive growth since the onset of the Covid-19 pandemic. In 2023, it grew by 17.8%. COVID created permanent behavior change: health insurance moved from nice-to-have to must-have for millions of middle-class families.

Technology disruption accelerates. Insurers are leveraging AI/ML for personalized underwriting, fraud detection, and enhanced customer service, improving operational efficiency. But technology is becoming table stakes—everyone has apps, AI, and APIs. Competitive advantage comes from using technology to enable uniquely better experiences or economics.

IX. Playbook: Key Lessons & Strategic Insights

After sixteen years, multiple ownership changes, and an IPO, what can we extract from Niva Bupa's journey that applies beyond Indian insurance? The lessons are surprisingly universal for anyone building in emerging markets.

The Power of International Partnerships in Emerging Markets

Bupa's involvement wasn't just capital—it was credibility. In markets where trust is scarce, a globally recognized partner provides instant validation. But the partnership must be structured for alignment. Bupa's provident association structure, without demanding shareholders seeking quick returns, enabled patient capital deployment. The lesson: when entering emerging markets, your partner's incentive timeframe matters more than their balance sheet size.

Building Trust in Low-Trust Categories

Insurance in India suffers from decades of mis-selling, claim rejections, and opacity. Niva Bupa's early investment in becoming the first health insurance company in India to integrate with IRDAI's Integrated Grievance Management System in real-time wasn't about compliance—it was trust-building through transparency. Every customer-friendly feature, from 30-minute cashless approvals to digital claims tracking, chips away at category distrust. The playbook: in low-trust categories, over-invest in trust-building even at the expense of short-term economics.

Technology as Enabler vs Differentiator

Everyone talks about digital transformation, but Niva Bupa's approach was nuanced. Technology enabled operational efficiency—digital policies, automated underwriting, AI-driven claims. But differentiation came from using technology to enhance human capabilities, not replace them. The 410-person tele-calling team armed with machine learning is more powerful than either alone. The insight: in emerging markets, pure digital plays often fail because customers still need human reassurance for complex products.

The Importance of Patient Capital

From 2008 to 2019, Max Bupa burned cash with no clear path to profitability. Most investors would have exited. But insurance is a long-gestation business where customer acquisition costs are front-loaded while lifetime value accrues over years. True North's entry with operational expertise and growth capital at exactly the right moment unlocked value. The lesson: business model timing and capital structure must align.

Distribution is King in India

Despite all the digital hype, India remains a relationship-driven market. Niva Bupa's multi-channel approach—digital direct, telemarketing, agents, bancassurance—recognizes that different customer segments have different buying preferences. The affluent might research online but buy through their relationship manager. The middle class might prefer telemarketing with vernacular support. The playbook: don't bet everything on one distribution channel, no matter how modern it seems.

Balancing Growth with Profitability

The transition from loss-making growth to profitable growth is treacherous. Cut marketing too early, and growth stalls. Grow too aggressively, and unit economics never recover. Niva Bupa's 2019-2024 phase under True North shows the balance: aggressive growth in chosen segments (retail health) while maintaining pricing discipline. The framework: grow aggressively where unit economics are proven, experiment cautiously elsewhere.

Local Expertise + Global Best Practices

Neither pure localization nor pure globalization works. Bupa's global risk models needed Indian adaptation. Indian distribution needed global technology enablement. The synthesis—globally proven concepts adapted for local context—created competitive advantage. The meta-lesson: in emerging markets, competitive advantage comes from synthesis, not replication.

X. Bear vs Bull Case & Future Outlook

Bull Case: The Decade of Health Insurance

The optimists see Niva Bupa at the beginning of a massive S-curve. Start with the macro: India's GDP per capita crossing $3,000, the sweet spot where insurance adoption accelerates globally. The India health insurance market size in terms of Gross Written Premium (GWP), was estimated at USD 15.06 billion in 2024 and is projected to grow at a CAGR of 20.9% from 2025 to 2030. If Niva Bupa maintains market share, that's a 3x revenue opportunity.

The regulatory tailwinds are unprecedented. Age caps removed, waiting periods reduced, standardized products mandated—IRDAI is actively promoting insurance adoption. The regulator's vision of "Insurance for All by 2047" might be ambitious, but directionally, it ensures continued support.

With the backing of Bupa Group, Niva Bupa has grown to become the third-largest standalone health insurer in India in the retail segment with over 14.99m people insured. This customer base is an asset that compounds—renewals are cheaper than new acquisition, cross-selling becomes easier, and network effects kick in.

The digital-first approach positions perfectly for India's demographic shift. With 600 million Indians under 25, digital-native customers will dominate future growth. Niva Bupa's technology investments, made when others focused on traditional channels, provide first-mover advantage.

Bupa's continued majority ownership provides strategic flexibility. Need growth capital? Parent has deep pockets. Need global expertise? Bupa operates in 190 countries. Need patience during turbulent periods? Bupa's structure enables long-term thinking.

The bear case worries are solvable. Low ROE improves with scale. Competition is actually positive—it grows the category. Medical inflation forces innovation in care delivery. The bull case sees problems as opportunities for differentiation.

Bear Case: Structural Challenges Persist

The skeptics point to stubborn realities. Low return on equity of 6.41% isn't just transitional—it might be structural in a regulated, capital-intensive business. If ROE remains below cost of capital, value destruction is mathematical.

Competition intensifies from every direction. Star Health has scale advantages. HDFC ERGO has bancassurance distribution. New entrants like Acko have no legacy costs. Price wars seem inevitable as everyone chases growth. In commoditized insurance, lowest price wins, destroying industry economics.

Regulatory risks loom large. IRDAI's consumer-friendly mandates—covering pre-existing conditions, removing age caps, standardizing products—help adoption but hurt profitability. Price controls, already existing in motor insurance, could extend to health. One adverse regulation could wreck the business model.

Medical inflation represents an existential threat. At 14% annually, medical costs double every five years. But competitive pressure limits premium increases. The scissors effect—costs rising faster than revenues—eventually cuts margins to nothing.

Customer acquisition costs spiral higher as competition intensifies. Digital channels seem efficient until everyone bids for the same keywords. Bancassurance partners extract increasing fees. Traditional agents demand higher commissions. The CAC/LTV equation deteriorates.

The bear case sees India's health insurance as structurally challenged: necessary but unprofitable, growing but value-destructive, promising but perpetually disappointing.

The Realistic Path Forward

Reality likely lies between extremes. Niva Bupa will probably grow revenues at 20-25% annually, in line with industry growth. Profitability will improve gradually as operational leverage kicks in, but ROE might plateau around 12-15%—decent but not spectacular.

The key variables to watch: market share (can they maintain 5% in a growing market?), combined ratio (can they keep claims + expenses below 95%?), and distribution costs (can technology really reduce acquisition costs?).

Strategic options abound. Geographic expansion into underserved markets. Product innovation in outpatient and preventive care. Vertical integration into hospital chains or diagnostics. Partnership with global reinsurers for complex risks. Each path has different risk-return profiles.

The IPO provides currency for acquisitions. Consolidation seems inevitable in Indian insurance—too many subscale players chasing the same opportunity. Niva Bupa could be acquirer or acquired, depending on execution over the next 24 months.

XI. Recent News

The post-IPO period has been eventful. The stock has found its level around ₹74-78, suggesting the market agrees with the IPO pricing. Trading volumes remain modest—this isn't a momentum stock but an institutional holding.

Management has been conservative in guidance, projecting 20-25% premium growth for FY25. This suggests focus on profitability over growth-at-any-cost. The claims ratio guidance of 65-70% indicates confidence in underwriting despite competitive pressure.

Recent product launches show continued innovation. A new cancer-specific product addresses India's rising cancer incidence. Mental health coverage, still rare in India, positions for younger customers. Outpatient coverage experiments with subscription models.

Partnership announcements reveal distribution strategy. A tie-up with a leading fintech for embedded insurance. Collaboration with diagnostic chains for preventive health packages. These aren't just distribution deals but ecosystem plays.

Regulatory developments remain supportive. IRDAI's push for standardized health products helps comparison shopping but also commoditization. The proposed health claims exchange would revolutionize claims processing. The insurance-for-all vision drives category growth.

Competitive moves warrant attention. Star Health's aggressive digital push. HDFC ERGO's bancassurance dominance. New entrants like Acko's billions in funding. The market is heating up, making execution more critical than strategy.

XII. Links & Resources

For those wanting to dig deeper into Niva Bupa and India's health insurance landscape, primary sources provide the richest insights:

- Annual Reports and Investor Presentations: Available on Niva Bupa's investor relations website, these provide detailed financials, strategy updates, and management commentary

- IRDAI Annual Reports: The regulator publishes comprehensive industry statistics, regulatory changes, and market analysis

- Bupa Group Global Reports: Understanding the parent's global strategy helps contextualize India investments

- True North Portfolio Insights: The PE firm's approach to operational transformation applies beyond Niva Bupa

Industry research worth studying: - McKinsey's India Insurance Reports: Regular publications on market opportunity and strategic imperatives - Swiss Re Sigma Studies: Global reinsurer's perspective on emerging market insurance - CRISIL and ICRA Ratings Reports: Credit rating agencies provide independent analysis of financial strength

For broader context on Indian healthcare and financial services: - "The Bill of the Century" by Steven Brill: While US-focused, illuminates healthcare economics universally - "Banker to the Poor" by Muhammad Yunus: Microfinance lessons apply to insurance inclusion - "The Fortune at the Bottom of the Pyramid" by C.K. Prahalad: Framework for emerging market opportunities

Technology and insurtech resources: - CB Insights Insurtech Reports: Global trends eventually reach India - Reinsurance News: Understanding reinsurance helps appreciate primary insurance economics - The Digital Insurer: Case studies of digital transformation in insurance

The Niva Bupa story is still being written. Whether it becomes India's healthcare infrastructure or another subscale player will depend on execution, market evolution, and perhaps a bit of luck. What's certain is that India's 1.4 billion people need health insurance, and someone will capture that opportunity. The question is whether Niva Bupa's combination of global expertise, local knowledge, and patient capital proves to be the winning formula.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube