Max Financial Services: India's Life Insurance Powerhouse

I. Introduction & Episode Framing

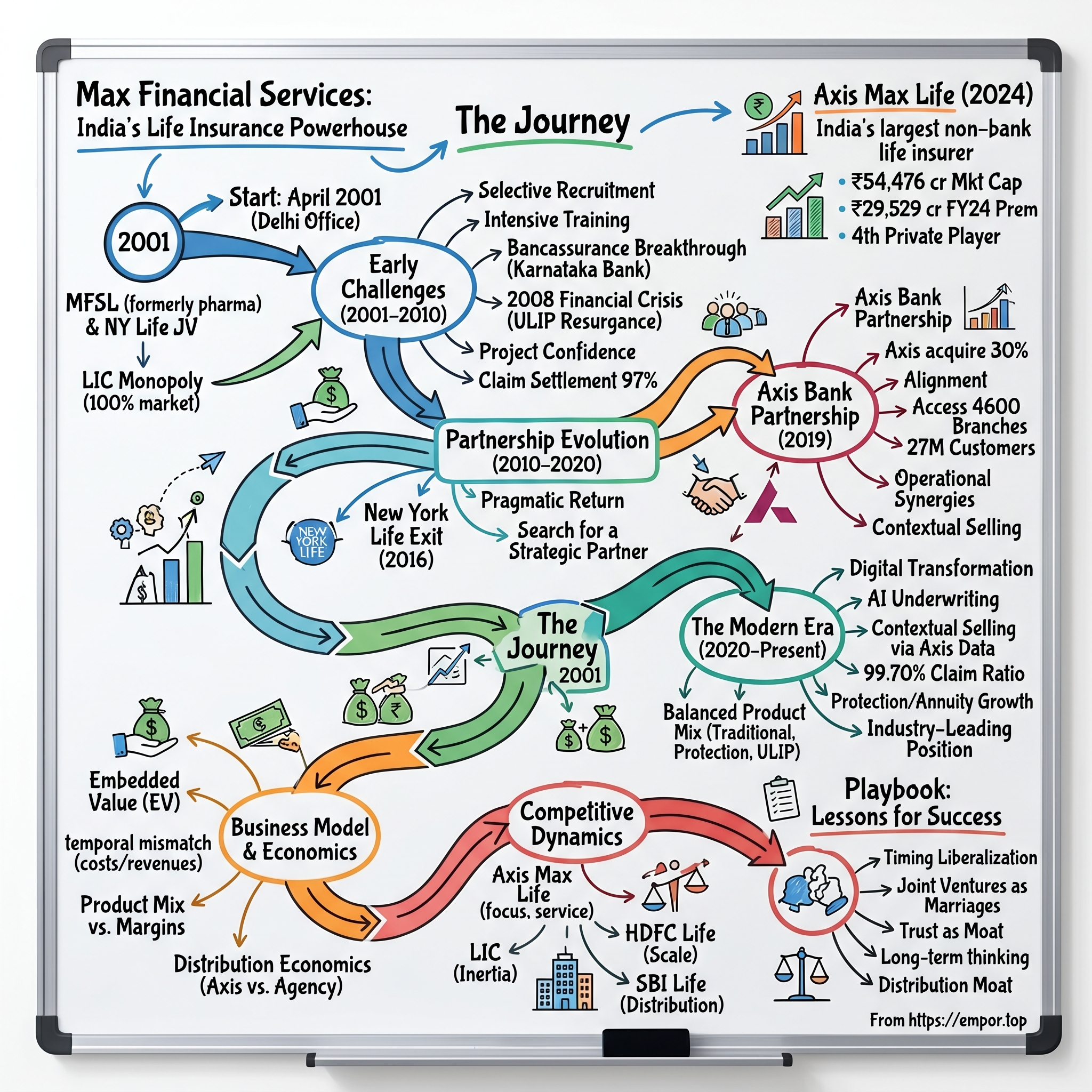

Picture this: It's April 2001, and in a modest office in Delhi, a team of former pharmaceutical executives is about to sell their first life insurance policy in a market that has been monopolized by the government for 44 years. The Life Insurance Corporation of India controls 100% of the market. Foreign insurers have been barred since 1956. And here comes Max Life—a joint venture between a diversified Indian conglomerate and New York Life—attempting the impossible.

Fast forward to 2024: Max Financial Services Limited (MFSL) owns 81.83% of what is now Axis Max Life Insurance, India's largest non-bank life insurer and the fourth-largest private life insurance company. With a market capitalization of ₹54,476 crores and gross written premiums of ₹29,529 crores in FY2023-24, MFSL has built one of India's most valuable insurance franchises. The company that started selling policies door-to-door now processes claims with a 99.70% payout ratio—among the best in the industry.

But here's the question that makes this story fascinating: How does a pharmaceutical intermediates manufacturer pivot to build one of India's most dominant life insurance franchises? How do you compete against a government monopoly that has a 44-year head start? And perhaps most intriguingly, how do you convince Indian families—traditionally skeptical of private financial services—to trust you with their life savings?

This is a story about liberalization arbitrage—being perfectly positioned when regulations change. It's about mastering the art of joint ventures in a country where foreign ownership is restricted but foreign expertise is desperately needed. And fundamentally, it's about betting on India's demographic dividend before the term even existed—recognizing that a young, growing, increasingly prosperous population would need financial protection products at scale.

What makes MFSL particularly instructive for students of business is how it navigated three distinct challenges simultaneously: building in heavily regulated markets where rules can change overnight, managing complex international partnerships where cultural differences run deep, and creating long-term value in an industry where payoffs take decades to materialize. The company's journey from zero to nearly 10% private market share offers a masterclass in patient capital deployment, strategic partnership selection, and the unglamorous but essential work of building trust in financial services.

As we'll see, the Max story isn't just about insurance—it's about understanding how value gets created when demographic shifts, regulatory changes, and entrepreneurial vision converge. It's about why boring businesses selling complicated products can generate extraordinary returns. And it's about how, sometimes, the best opportunities come from markets everyone else thinks are too hard, too regulated, or too dominated by incumbents to bother attacking.

II. The Analjit Singh Origin Story & Max Group Genesis

The conference room at Ranbaxy headquarters in 1985 was thick with tension. Analjit Singh, barely 31 years old, had just inherited control of the pharmaceutical empire his father Bhai Mohan Singh had built from scratch. But unlike a typical succession story, this wasn't a smooth handover—his father had died suddenly, leaving behind a complex web of family holdings, ambitious expansion plans, and crucially, two sons who would eventually take the business in completely different directions.

Analjit Singh wasn't supposed to be a businessman. Born in 1954 into one of India's pioneering pharmaceutical families, he had the bearing of an intellectual—soft-spoken, contemplative, more interested in architecture and design than balance sheets and production schedules. His father, Bhai Mohan Singh, had founded Ranbaxy in 1961, transforming it from a small distributor into one of India's first multinational pharmaceutical companies. The expectation was that both sons—Analjit and his brother Parvinder—would jointly carry forward the legacy.

But visions diverge. By 1985, it became clear the brothers had fundamentally different philosophies about business. Parvinder wanted to double down on pharmaceuticals, to make Ranbaxy a global generic drugs powerhouse. Analjit saw opportunity in diversification—in building a conglomerate that could capture value across India's liberalizing economy. The solution was surgical: split the empire. Parvinder kept Ranbaxy. Analjit took a smaller piece and the freedom to build something entirely his own.

What Analjit inherited was modest: a single FDA-approved facility in Okhla, Delhi, producing penicillin drug intermediates. Revenue was negligible compared to Ranbaxy. Industry observers whispered that he'd gotten the worse end of the deal. But Analjit saw it differently. He named his new company Max India—"Max" suggesting maximum potential, maximum service, maximum life. From day one, the philosophy was clear: this wouldn't just be another pharmaceutical company. It would be, as he would later articulate, in the "business of life."

The early Max India was a study in pragmatic diversification. While the Okhla facility churned out pharmaceutical intermediates for export, Analjit was already scanning the horizon for opportunities. He entered telecom equipment manufacturing, clinical research, healthcare delivery. Each move seemed disconnected, but there was a thread: businesses that served India's emerging middle class, that required high service standards, that could scale with the country's growth.

By the early 1990s, Max Group had become a legitimate conglomerate, though still far from a household name. The pharmaceutical business was generating steady cash flows. The telecom venture was riding the wave of India's communication revolution. But Analjit was restless. He could see that India was at an inflection point. The 1991 economic reforms had begun dismantling the License Raj. Foreign investment was trickling in. Industries that had been government monopolies for decades were opening up.

It was during a trip to the United States in 1994 that the vision crystallized. Analjit spent time studying American financial services companies, particularly life insurers. He was struck by a simple observation: in developed markets, life insurance wasn't just about death benefits—it was the primary savings and investment vehicle for middle-class families. In India, Life Insurance Corporation (LIC) held a monopoly, but its products were archaic, its service notorious for bureaucracy. If—when—the sector opened up, the opportunity would be massive.

The preparation was meticulous. Even though insurance liberalization was still years away, Analjit began recruiting talent with financial services experience. He studied global insurance models, particularly the agency-driven distribution systems of Asia. He built relationships with potential foreign partners, knowing that when the sector opened, international expertise would be crucial.

What set Analjit apart wasn't just his vision—it was his philosophy of business. In 2011, the Indian government would award him the Padma Bhushan, one of the country's highest civilian honors, not for building a large company, but for his approach to building it. Max Group became known for its obsession with service excellence. Employee training programs borrowed from hospitality companies. Customer service metrics were tracked with the precision of a Swiss watch manufacturer.

The "business of life" wasn't just a tagline—it became an organizing principle. Every Max venture, whether in healthcare, insurance, or later in senior living, was evaluated through this lens: Does it improve quality of life? Can we deliver it with excellence? Will it matter 20 years from now? This long-term orientation would prove crucial when entering life insurance—a business where policies sold today might not generate profits for a decade.

By the late 1990s, Max Group was ready. The conglomerate had cash flows, credibility, and crucially, a leader who understood that the biggest opportunities often come from the most regulated, most difficult markets. While others saw insurance liberalization as a regulatory headache, Analjit saw it as the chance to build something generational. The boy who had inherited a single pharmaceutical facility was about to bet everything on selling life insurance to a country that didn't yet know it needed it.

III. The Insurance Liberalization Opportunity (1991–2000)

The year was 1999, and inside the wood-paneled offices of the Insurance Regulatory and Development Authority in Hyderabad, history was being written one clause at a time. After months of parliamentary debates, street protests by LIC unions, and intense lobbying by global insurers, India was finally ready to end one of the world's last great financial monopolies. For Analjit Singh, waiting in Delhi with a team that had been preparing for this moment for five years, every regulatory announcement was scrutinized like a battlefield dispatch.

To understand the magnitude of this opportunity, you need to grasp the absurdity of India's insurance market in the 1990s. Since 1956, when Jawaharlal Nehru's government nationalized the sector, Life Insurance Corporation had been the only legal provider of life insurance to 900 million Indians. LIC's monopoly was so complete that the word "insurance" and "LIC" had become synonymous in the Indian lexicon. Policies were sold like government schemes, claims took months to process, and customer service was an oxymoron.

The 1991 economic reforms had liberalized manufacturing, banking, and telecom, but insurance remained untouchable—too politically sensitive, too entrenched with vested interests. LIC employed over 100,000 people, had agents in every village, and more importantly, was a captive source of funds for government borrowing. Opening insurance wasn't just an economic decision; it was political dynamite.

But demographics have a way of forcing change. India's middle class was exploding—from 50 million in 1990 to a projected 200 million by 2000. These families had savings, aspirations, and crucially, no faith in LIC's antiquated products. They wanted unit-linked plans that could beat inflation, term insurance that actually paid claims, and service that didn't require bribes or connections. The pressure was building.

The Malhotra Committee report of 1994 was the first crack in the dam. It recommended allowing private players, permitting foreign partnerships, and establishing an independent regulator. But it would take another five years of political maneuvering before the Insurance Regulatory and Development Authority (IRDA) Act was finally passed in 1999. The rules were carefully crafted to balance competing interests: private companies could enter, but foreign partners were capped at 26% ownership. Companies needed ₹100 crores in capital—enough to ensure serious players only.

For Max, the foreign partnership requirement wasn't a constraint—it was the strategy. Analjit had spent years courting potential partners, and his approach was tellingly different from competitors. While others chased the biggest names—Allianz, Prudential, AIG—Max focused on cultural fit. The question wasn't who had the most assets under management, but who understood the peculiarities of selling insurance in a developing market.

The courtship with New York Life began in 1998, a full year before regulations were finalized. New York Life wasn't the largest U.S. insurer, but it had something unique: it was a mutual company, owned by policyholders rather than shareholders. This structure meant they thought in decades, not quarters—perfectly aligned with Max's philosophy. They had experience in emerging markets, having operated in Argentina and Taiwan. Most importantly, they understood that India wouldn't be a copy-paste job of Western models.

The negotiations were intricate. Beyond the 26% equity stake mandated by regulation, the partnership agreement covered technology transfer, training protocols, product development, and crucially, an option for Max to increase its stake over time. New York Life would bring actuarial expertise, risk management systems, and global best practices. Max would provide local knowledge, regulatory relationships, and the entrepreneurial hunger to challenge a monopoly.

As 2000 dawned, the chess pieces were in place. IRDA had received 42 applications for life insurance licenses—everyone from industrial houses like Birla and Tata to banks like HDFC and ICICI wanted in. But Max had advantages. They had spent five years preparing, recruiting executives from LIC who understood the market's intricacies. They had identified their first 100 branch locations. They had even begun training agents, technically for "financial services," ready to pivot to insurance the moment licenses were granted.

The license came through in November 2000—Max New York Life Insurance Company Limited was among the first private life insurers approved by IRDA. The authorized capital was ₹250 crores, with New York Life taking its maximum allowed 26% stake. But more than capital, what mattered was timing. Being in the first wave meant Max could cherry-pick talent, secure prime real estate for branches, and most importantly, shape customer perceptions of what private insurance could be.

The challenge ahead was staggering. LIC had 2,048 branches, over a million agents, and 100% market share. Max Life started with zero policies, zero customers, and a brand nobody had heard of. But they had something LIC didn't: the ability to innovate without bureaucracy, to serve without legacy systems, and to build a business for India's future rather than its past.

On the eve of launching operations, Analjit Singh held an all-hands meeting at Max headquarters. His message was simple but powerful: "We're not just selling insurance. We're selling trust in a country where private companies have never been trusted with life savings. Every policy we sell, every claim we pay, we're not just building a business—we're changing how India thinks about financial security."

The liberalization window was open. The partnership was sealed. The regulations were clear. Now came the hard part: convincing Indians to buy life insurance from a company that wasn't LIC. As 2001 began, Max Life was ready to find out if five years of preparation had been enough.

IV. Building Max Life: The Early Years (2001–2010)

The first Max Life Insurance policy was sold on April 15, 2001, in a small apartment in South Delhi. The customer was a 35-year-old software engineer named Rajesh Mehta, the product was a traditional endowment plan for ₹5 lakhs, and the agent who sold it had defected from LIC just three weeks earlier. As CEO Analjit Singh personally called to congratulate both customer and agent, nobody in that room could have imagined that this single policy would cascade into a ₹29,000 crore premium business.

Starting from absolute zero in a monopoly market requires a special kind of delusion—or vision. Max Life's first office in Gurgaon was a study in contrasts: state-of-the-art computers running New York Life's actuarial software sat next to empty desks waiting for agents who hadn't been hired yet. The company had regulatory approval to sell insurance but no customers who knew they existed. They had world-class products but no way to distribute them. They had ambitious targets—₹100 crores in first-year premium—but no playbook for achieving them.

The fundamental question was distribution. LIC's million-plus agent army had been built over 45 years, with agents often inheriting the "business" from their fathers. These weren't just salespeople; they were trusted advisors embedded in communities, present at weddings and funerals, part of the social fabric. How do you compete with that?

Max's answer was to not compete directly but to reimagine the agent model entirely. Instead of recruiting anyone who could fog a mirror (LIC's approach), Max introduced something radical: selective recruitment with intensive training. The first batch of 100 agents underwent six weeks of training—not just on products, but on financial planning, need analysis, and consultative selling. They were given laptops (revolutionary in 2001 India), professional marketing materials, and most importantly, higher commissions than LIC offered.

But the real innovation was in product design. While LIC's products were one-size-fits-all endowment plans with opaque returns, Max Life introduced segmentation. Young professionals got unit-linked plans that offered market participation. Families got term insurance with premiums 70% lower than LIC's whole life policies. High-net-worth individuals got wealth management solutions. Each product came with something LIC couldn't offer: transparency. Customers could actually understand what they were buying.

The early growth was explosive but fraught. By December 2001, Max Life had sold 10,000 policies—remarkable for eight months of operation. But each sale was a battle. Customers would ask, "What happens if your company disappears?" Agents had to explain IRDA regulations, solvency requirements, and the New York Life partnership. Many potential customers would listen politely, then buy from LIC anyway—the gravitational pull of the incumbent was massive.

The 2003 breakthrough came from an unexpected source: bancassurance. Max partnered with Karnataka Bank, a regional lender with 400 branches. While tiny compared to State Bank of India, Karnataka Bank's customers were exactly Max's target market: urban, educated, and underserved by LIC. The bank's endorsement provided instant credibility. Suddenly, Max Life policies were being sold alongside fixed deposits and mutual funds. First-year premiums jumped from ₹50 crores in 2002 to ₹200 crores in 2003.

Then came the real test: the 2008 financial crisis. For a seven-year-old insurance company with significant unit-linked products, this was an existential threat. Markets crashed 60%. Customers who had bought ULIPs expecting 15% returns saw their fund values decimated. Surrender requests flooded in. New business dried up overnight. At LIC, with its traditional products and government backing, it was business as usual. At Max Life, it was crisis mode.

The response defined the company's character. Instead of hiding behind fine print, Max Life launched "Project Confidence"—agents personally visited every ULIP customer to explain market cycles, the power of rupee-cost averaging, and why surrendering would lock in losses. They introduced "premium holidays"—allowing customers to pause payments without losing coverage. Most remarkably, they launched guaranteed return products in the midst of market chaos, betting their own balance sheet that they could navigate the volatility.

The strategy worked. While competitors saw surrender rates spike above 20%, Max Life kept theirs below 12%. More importantly, when markets recovered in 2009, customers remembered who had stood by them. The company that had entered the crisis with ₹2,000 crores in new business premium emerged with credibility that money couldn't buy.

By 2010, the numbers told a remarkable story. Max Life had grown from zero to ₹5,633 crores in new business premium. Market share among private players had reached 7.8%. The company had 1.8 million customers, 35,000 agents, and 419 offices across 140 cities. But the most important metric wasn't in any annual report: claim settlement ratio had reached 97%, compared to the industry average of 89%. In a business built on trust, Max Life was keeping its promises.

The first decade had proven that a private company could successfully challenge LIC's monopoly. But it had also revealed uncomfortable truths. Customer acquisition costs were higher than projected—it took ₹3,000 in expenses to generate ₹1,000 in new premium. The agency model, while successful, was expensive and difficult to scale. Banking partnerships were powerful but came with their own demands for revenue sharing.

As 2010 ended, Max Life faced a strategic inflection point. They had built a viable business, but profitability remained elusive. New York Life was happy with progress but wanted faster returns. Competitors like HDFC Life and ICICI Prudential were leveraging their banking parents for massive distribution advantages. The easy growth of a virgin market was over. The next decade would require a different playbook—one that would eventually lead to the most important partnership in the company's history.

V. The Partnership Evolution: From New York Life to Axis Bank

The boardroom at Max Towers in November 2019 was electric with tension. After months of negotiations, regulatory approvals, and strategic deliberations, Analjit Singh was about to sign the deal that would fundamentally reshape Max Financial Services. Axis Bank, India's third-largest private sector bank, would acquire 30% of Max Life Insurance, creating a new 70:30 joint venture. As the ink dried on the agreement, it marked not just a transaction but a strategic masterstroke—transforming Max Life from an independent player fighting for distribution into a bancassurance powerhouse with access to 4,600 branches and 27 million customers.

To understand why this partnership shift was inevitable, we need to examine the New York Life years with clear eyes. From 2000 to 2016, New York Life had been the perfect launch partner. Their actuarial expertise helped Max Life price products competitively while maintaining solvency. Their training programs created one of India's most professional agency forces. Their patient capital—they didn't take a single rupee in dividends for 15 years—allowed Max Life to reinvest everything into growth.

But cracks were emerging. Indian insurance regulations capped foreign ownership at 26% (later raised to 49%), meaning New York Life's influence was limited despite their expertise. More problematically, they had no distribution network in India to leverage. While competitors like HDFC Life could tap into HDFC Bank's customer base, Max Life had to build every distribution relationship from scratch. The math was becoming uncomfortable: customer acquisition costs were rising, bancassurance partnerships demanded ever-higher revenue shares, and profitability targets kept getting pushed out.

The 2016 decision by New York Life to exit wasn't acrimonious—it was pragmatic. They had earned solid returns on their investment, helped build a valuable franchise, but recognized that the next phase of growth required capabilities they couldn't provide from 8,000 miles away. The sale of their 26% stake to Mitsui Sumitomo Insurance for ₹2,731 crores validated the value creation but also started a clock ticking. Max needed a strategic partner, not just a financial investor.

Enter Axis Bank, which in 2019 was facing its own strategic imperatives. Under CEO Amitabh Chaudhry, the bank was looking to reduce its dependence on corporate lending and build a retail franchise. Insurance distribution was incredibly profitable for banks—generating fee income without consuming capital—but Axis's existing partnership with LIC was underperforming. Max Life, with its product sophistication and service quality, offered a chance to capture the premium end of the market.

The courtship was complex. It wasn't just about Axis buying a stake; it was about creating operational synergies that had eluded many bancassurance partnerships. The deal structure was ingenious: Axis would acquire 30% of Max Life through a combination of cash (₹1,600 crores) and share swap (12% of Max Financial shares). This created alignment—both companies were now shareholders in each other, making success mutually beneficial.

But the real innovation was in the operating agreement. Unlike typical bancassurance deals where the bank simply sells insurance for commission, Axis and Max Life created deep integration. Axis relationship managers would be trained by Max Life. Products would be co-created based on Axis's customer data. Technology platforms would be unified. Most importantly, Axis committed to making Max Life its primary insurance partner, gradually phasing out other relationships.

The impact was immediate and dramatic. In the first year of partnership (FY2020), Max Life's new business premium from the Axis channel grew 47% to ₹1,890 crores. By FY2024, Axis Bank contributed 54% of Max Life's total new business premium. The cost efficiencies were even more impressive—customer acquisition costs dropped 30% as warm leads from Axis required less convincing than cold calls.

The partnership evolution reached its logical conclusion in December 2024 with the rebranding from Max Life to Axis Max Life Insurance. This wasn't just a cosmetic change—it represented full strategic alignment. The Axis brand, trusted by millions of Indians for banking, now extended its halo to life insurance. For customers, the message was clear: your bank and your insurer were now seamlessly integrated.

The current structure—80% Max Financial, 20% Axis Bank—might seem like Max retained control, but the reality is more nuanced. Axis's distribution power gives it influence far beyond its equity stake. Board decisions require consensus. Product strategies must align with Axis's customer segments. It's less a majority-minority relationship and more a strategic marriage where both parties need each other to succeed.

What makes this partnership particularly powerful is the complementary capabilities. Max brings four decades of insurance expertise, sophisticated product design, and a proven agency network. Axis brings distribution reach, customer data, and most crucially, trust at the point of sale. When an Axis relationship manager recommends Axis Max Life insurance, it carries weight that no standalone insurer could match.

The financial impact has been transformative. Max Life's market share among private insurers rose from 8.9% in FY2019 to 9.9% in FY2024. Embedded value—the actuarial measure of an insurer's worth—grew from ₹10,500 crores to ₹18,200 crores. Most importantly, the path to profitability became clear. With distribution costs controlled and premium growth accelerating, Max Life posted its highest-ever profit of ₹334 crores in FY2024.

Looking back, the partnership evolution from New York Life to Axis Bank illustrates a fundamental truth about Indian financial services: in a market where trust is scarce and distribution is expensive, strategic partnerships aren't just helpful—they're essential. Max Life spent its first decade proving it could build a quality insurance business. With Axis Bank, it's spending its current decade proving it can build a profitable one. The transition from startup partner to scale partner, from foreign expertise to local distribution, shows the maturity not just of Max Life, but of the Indian insurance market itself.

VI. The Rebranding & Modern Era (2020–Present)

The December 2024 rebranding ceremony at Mumbai's Jio Convention Center was meticulously choreographed. As the curtain lifted to reveal the new "Axis Max Life Insurance" logo, Amitabh Chaudhry and Analjit Singh stood together, representing not just two companies but the convergence of banking and insurance in India. The media coverage focused on the visual identity change, but insiders knew this was about something deeper: completing a transformation from insurgent challenger to establishment powerhouse.

The timing of the rebrand was no accident. By 2024, the Indian life insurance market had fundamentally shifted. Digital adoption, accelerated by COVID-19, had changed how policies were sold. Customers no longer needed agents to explain products—they researched online, compared options, and increasingly, bought directly through apps. The traditional agency model that had built Max Life was becoming just one channel among many.

The numbers from FY2023-24 tell the story of a company at scale: ₹29,529 crores in gross written premium, making Axis Max Life India's fourth-largest private life insurer. The 9.9% market share among private players represented nearly one in ten policies sold outside of LIC. With 1.2 million policies issued during the year and ₹2.8 lakh crores of sum assured, the company was protecting more Indian families than ever before.

But raw size doesn't capture the strategic transformation. The product portfolio evolution has been remarkable. While traditional products still form the backbone—₹9,800 crores in FY24—the growth is coming from protection and annuity products. Term insurance premiums grew 42% year-over-year as middle-class Indians finally understood the difference between investment and insurance. The guaranteed lifetime income products, virtually non-existent a decade ago, now contribute ₹3,200 crores annually as India grapples with an aging population without social security.

The digital transformation runs deeper than mobile apps and online purchases. Axis Max Life has deployed artificial intelligence for underwriting, reducing policy issuance time from days to hours for standard cases. Machine learning algorithms analyze claims patterns to detect fraud while ensuring legitimate claims are fast-tracked. The company's "Smart Assist" platform uses natural language processing to handle customer queries, resolving 73% without human intervention.

Yet technology is just an enabler. The real transformation is in customer-centricity, best exemplified by the industry-leading 99.70% claim settlement ratio in FY24. This number—which means only 3 in 1,000 claims are rejected—wasn't achieved through loose underwriting but through better upfront disclosure, clearer documentation, and most importantly, a cultural shift from finding reasons to reject claims to finding ways to pay them.

The Axis Bank integration has created unexpected synergies. Using Axis's customer data, Max Life can now identify life events—marriages, births, home purchases—and proactively offer relevant protection. A customer taking an Axis home loan receives a term insurance quote that exactly covers the loan amount. Parents opening child savings accounts see education plans tailored to projected college costs. This contextual selling has improved conversion rates from 2% to 8% for targeted campaigns.

The agency force, once thought to be obsolete, has been reimagined for the digital age. The 95,000 agents aren't just salespeople—they're financial advisors equipped with tablets running proprietary software that can generate personalized financial plans in real-time. The "Max Life Partner" app provides them with leads, training modules, and commission tracking. Average agent productivity has increased 67% since 2020, even as the total number has remained flat.

COVID-19, despite its tragic human cost, accelerated insurance awareness in India. Max Life's new business premium grew through the pandemic—₹7,800 crores in FY21, ₹9,200 crores in FY22—as families confronted mortality and financial vulnerability. The company's quick pivot to video medical examinations, digital documentation, and contactless selling proved that insurance could be sold without physical interaction.

The competitive landscape has intensified but also clarified. HDFC Life remains the largest private player, leveraging India's biggest private bank. ICICI Prudential focuses on the affluent segment. SBI Life dominates rural markets through State Bank's unmatched reach. Axis Max Life has carved out its position: urban and semi-urban middle class, balanced product mix, superior service. It's not trying to be everything to everyone—it's being the best at serving India's growing middle class.

Environmental, Social, and Governance (ESG) considerations, once afterthoughts, are now central to strategy. Max Life's investment portfolio of ₹1.2 lakh crores increasingly factors in sustainability criteria. The company has committed to carbon neutrality by 2030. More importantly, financial inclusion initiatives—micro-insurance products, vernacular language support, simplified products for first-time buyers—are expanding the market rather than just competing for existing customers.

The senior leadership transition has been smooth but significant. Prashant Tripathy, who took over as CEO in 2019, brought fresh perspective from his HDFC Life experience. The leadership team now blends Max veterans who understand the culture with industry experts who bring best practices. Analjit Singh, now 70, remains Chairman but has empowered the next generation to drive operational decisions.

As 2025 begins, Axis Max Life stands at an interesting juncture. The rebranding is complete, the Axis partnership is delivering results, and digital capabilities are mature. But challenges remain: regulatory changes on commission structures could pressure margins, new-age insurtech startups are cherry-picking profitable segments, and LIC's digital transformation threatens to make the giant more agile.

The modern era isn't just about being bigger—it's about being better. The company that started by selling one policy in a Delhi apartment now processes 3,000 policies daily. The insurer that struggled to explain why private insurance was trustworthy now has millions trusting it with their family's future. The transformation from Max Life to Axis Max Life isn't just a rebranding—it's recognition that in Indian financial services, you're only as strong as your ecosystem. And right now, that ecosystem is perfectly aligned for the next phase of growth.

VII. The Business Model & Unit Economics

Understanding life insurance economics requires abandoning conventional business thinking. When Axis Max Life sells a 20-year term insurance policy today for ₹15,000 annual premium, it won't know if that sale was profitable until 2045. The agent commission is paid immediately, the medical examination costs are borne upfront, but the claims—if any—could come two decades later. This temporal mismatch between costs and revenues makes life insurance perhaps the most complex business model to analyze, yet also one of the most valuable when executed correctly.

The concept of Embedded Value (EV) is where the magic—and confusion—begins. As of March 2024, Axis Max Life's embedded value stood at ₹18,200 crores, despite the company's book value being just ₹7,800 crores. This gap represents the present value of future profits from existing policies, discounted back at risk-adjusted rates. Think of it this way: every policy sold adds to a pool of future cash flows that are almost contractually guaranteed, barring mass mortality events. The ₹10,400 crore difference between EV and book value is wealth already created but not yet recognized by accounting standards.

The product mix drives everything in life insurance economics, and Axis Max Life's portfolio evolution tells a strategic story. Traditional products—endowment and money-back plans—contribute 33% of new business premium but generate 45% of embedded value due to their high margins. These products are expensive for customers (lower returns than mutual funds) but profitable for insurers because of the investment spread and surrender penalties.

Protection products—term and health insurance—are the opposite dynamic. They represent just 18% of premium but are strategically crucial. A 35-year-old buying ₹1 crore term coverage pays perhaps ₹12,000 annually. If claims are well-underwritten and mortality follows expected patterns, these products generate 30-40% margins. But one unexpected claim cluster—say, a pandemic—can wipe out years of profits. It's high-wire actuarial risk management.

Unit-Linked Insurance Plans (ULIPs), contributing 27% of premium, are the most transparent but least profitable. Customers bear investment risk, the company just charges management fees of 1.35% annually. During bull markets, ULIPs sell themselves. During crashes, they become reputation destroyers. Axis Max Life has strategically de-emphasized ULIPs from 45% of mix in 2018 to current levels, focusing on predictable products.

The newest category—annuity and pension products at 22% of mix—represents the future. As India ages without social security, guaranteed lifetime income products are seeing explosive growth. These are capital-intensive (the insurer guarantees payments for life) but generate steady fee income and benefit from mortality credits when annuitants die earlier than expected.

Distribution economics determine profitability more than any other factor. The agency channel, despite digital disruption, still contributes 41% of new business. But here's the catch: agent commissions for traditional products can be 35% of first-year premium, 7.5% in year two, and 5% thereafter. A productive agent selling ₹50 lakhs of annual premium earns ₹17.5 lakhs in first-year commissions alone. The math only works if persistency—policies staying active—exceeds 85% by year five.

The Axis Bank channel, now contributing 54% of new business, has transformed unit economics. Bank commissions are lower (15-20% of premium) and customer quality is higher (pre-verified income, existing relationships). The cost per policy sold through Axis is ₹8,000 versus ₹12,000 through agencies. More importantly, Axis-sourced policies have 13-month persistency of 89% versus 83% for agency channel—those six percentage points translate to hundreds of crores in retained value.

The digital direct channel, though just 5% of business, offers the best economics—near-zero distribution costs, educated customers who understand products, and surprisingly high persistency. But it's limited to simple products like term insurance. Nobody buys complex traditional products online without advice, creating a natural ceiling for digital penetration.

Capital intensity remains life insurance's biggest challenge. Solvency regulations require maintaining 150% of risk-adjusted capital—meaning for every ₹100 of new business, ₹30-40 of capital must be held initially. This capital gets released over time as policies mature, but the upfront requirement makes growth expensive. Axis Max Life's solvency ratio of 189% represents ₹3,400 crores of excess capital that could theoretically be distributed but is maintained for growth and regulatory comfort.

The investment side of the balance sheet is where patient capital generates returns. With ₹1.2 lakh crores of assets under management, even 50 basis points of extra return translates to ₹600 crores annually. The portfolio is boringly conservative—65% in government securities, 20% in AAA corporate bonds, 15% in equities—but that's the point. Insurance companies are in the business of certainty, not speculation.

Understanding the J-curve of profitability is crucial. A cohort of policies sold in year one typically shows losses until year seven, breaks even by year ten, and generates the bulk of lifetime profits in years 10-20. This is why life insurance is a 20-year business, not a 5-year one. Quarterly earnings are meaningless; what matters is the vintage performance of policy cohorts over decades.

For Max Financial Services as the holding company, the economics are simpler but no less attractive. Owning 81.83% of an embedded value of ₹18,200 crores implies ₹14,900 crores of value, against a market cap of ₹54,476 crores. The 3.7x EV multiple reflects market confidence in future growth, the Axis partnership, and management execution. Dividend policy remains conservative—₹50 crores in FY24—as retained earnings fund growth capital needs.

The beauty of life insurance economics is its predictability once scale is achieved. Unlike banking where one bad loan can destroy years of profits, or manufacturing where technology can obsolete products overnight, life insurance is governed by the law of large numbers. Mortality is predictable, persistency improves with scale, and investment returns compound over time. It's boring, capital-intensive, and requires decades of patience. Which is exactly why, when done right, it creates enormous value. The ₹18,200 crore embedded value isn't just a number—it's twenty years of promises made to customers, slowly but surely converting into shareholder wealth.

VIII. Competitive Dynamics & Market Position

The Indian life insurance market in 2024 is a fascinating study in contrasts. On one side stands LIC, the former monopolist, still commanding 61% market share despite two decades of private competition—a behemoth with 1.3 million agents and policies in every village from Kashmir to Kanyakumari. On the other side, 23 private insurers fight for the remaining 39%, each trying to carve out defensible positions. In this landscape, Axis Max Life's 9.9% share of the private market makes it the fourth-largest private player—significant, but the real story is how that position was achieved and defended.

Understanding competitive positioning requires recognizing that Indian life insurance isn't one market but several. There's the rural mass market where LIC remains dominant, selling simple endowment products through agents embedded in communities for generations. There's the urban affluent segment where HDFC Life leverages its parent's premium banking relationships. There's the digital-native segment where term insurance aggregators and insurtech startups compete on price. Axis Max Life has deliberately chosen the urban and semi-urban middle class—large enough to matter, sophisticated enough to value service over just price.

HDFC Life, the market leader among private players with 15.8% share, represents the most direct competition. The parallels are striking: both have powerful bank parents, similar product mixes, overlapping target segments. But dig deeper and differences emerge. HDFC Life's solo bancassurance model means complete dependence on HDFC Bank, while Axis Max Life maintains its agency network as a hedge. HDFC Life's aggressive growth has come with higher costs—their expense ratio of 18.2% compares to Axis Max Life's 14.8%. In the race for scale, profitability got sacrificed.

ICICI Prudential Life, with 13.2% private market share, took a different path—premiumization. Their average ticket size of ₹87,000 is 40% higher than Axis Max Life's ₹62,000. They've consciously ceded the mass market to focus on high-net-worth individuals and corporate solutions. It's a profitable strategy but naturally limits growth. Their return on embedded value of 18% exceeds Axis Max Life's 14%, but absolute value creation is lower due to the smaller base.

SBI Life presents an interesting contrast—massive distribution through State Bank of India's 22,000 branches, but chronic underperformance in product innovation and service. Their claim settlement ratio of 94.5% significantly lags Axis Max Life's 99.7%. Despite having the country's largest bank as parent, their market share has stagnated around 12% of private players. Distribution without execution has limits.

But the most instructive comparison is with LIC itself. Despite losing market share every year since privatization—from 100% in 2000 to 61% today—LIC remains the only insurer most Indians trust implicitly. Their new business premium of ₹2.1 lakh crores dwarfs the entire private sector combined. Yet their product mix tells a story of inertia: 91% traditional products in an era when customers want market participation, term protection, and retirement solutions. Their expense ratio of 8.9% seems efficient until you realize it's subsidized by legacy policies generating pure profit.

The foreign partnership dynamics add another competitive layer. While Axis Max Life has essentially become an Indian company with Axis Bank's partnership, competitors maintain significant foreign shareholdings. HDFC Life has Standard Life Aberdeen at 21%, ICICI Prudential has Prudential Corporation at 22%, SBI Life has BNP Paribas Cardif at 26%. These partnerships bring global expertise but also create friction—foreign partners want dividends and exits, Indian promoters want reinvestment and growth.

Regulatory dynamics increasingly shape competition. IRDA's push for protection products favors players like Axis Max Life with strong underwriting capabilities. New rules on commission structures hurt players dependent on high-cost distribution. Solvency requirements favor well-capitalized incumbents over aggressive new entrants. The regulatory moat is real and growing.

The bancassurance advantage deserves special attention. Banks contribute 54% of Axis Max Life's new business, compared to 35% for the industry. This isn't just about having a bank partner—it's about integration depth. When Axis Bank's relationship managers are trained by Axis Max Life, when products are designed for specific customer segments, when technology platforms are unified, it creates a competitive advantage that's nearly impossible to replicate.

New threats are emerging from unexpected quarters. Insurtech startups like Acko and Digit, while focused on general insurance now, have ambitions in life insurance. Their digital-first models, venture capital backing, and freedom from legacy systems pose long-term threats. More immediately, platforms like PolicyBazaar have commoditized term insurance, driving prices down 30% in five years. Axis Max Life's response—focusing on complex products that need advice—works today but may not forever.

The competitive responses are telling. LIC finally launched a digital transformation, spending ₹1,500 crores on technology upgrades. HDFC Life is expanding beyond HDFC Bank, partnering with cooperative banks and NBFCs. ICICI Prudential is building a direct-to-consumer digital stack. Everyone recognizes that past advantages—distribution, brand, foreign expertise—won't be sufficient for future success.

What makes Axis Max Life's position defensible? First, the Axis Bank relationship is exclusive and deepening—the rebranding cements a partnership competitors can't poach. Second, the balanced channel mix provides resilience—if bancassurance regulations change, the agency network provides backup. Third, the service excellence creates switching costs—customers with good claim experiences become advocates.

Market share, however, only tells part of the story. Value market share—percentage of industry embedded value—paints a different picture. Here, Axis Max Life punches above its weight, with 11.2% of private sector embedded value despite 9.9% premium share. This reflects better product mix, superior persistency, and operational efficiency—the factors that ultimately determine winner from also-rans in insurance.

Looking ahead, the basis of competition is shifting from distribution to data, from products to experiences, from growth to profitability. In this evolving landscape, Axis Max Life's position—not the largest but among the most profitable, not the fastest-growing but the most sustainable—might prove to be exactly right. Sometimes in business, being fourth place in a race where most competitors are running in the wrong direction is exactly where you want to be.

IX. Playbook: Lessons in Building Financial Services

The Max Financial story, stripped of its specifics, reveals a replicable playbook for building financial services businesses in emerging markets. These aren't theoretical frameworks but battle-tested strategies that turned a pharmaceutical intermediates manufacturer into one of India's most valuable insurance franchises. Each lesson carries scars from mistakes and insights from victories.

Timing Regulatory Liberalization is perhaps the most underappreciated skill in emerging markets. Analjit Singh didn't wait for insurance privatization to be announced—he began preparing five years before regulations changed. This meant recruiting talent when there was no business to run, studying global models when there was no market to enter, building relationships with regulators who didn't yet regulate anything. The lesson: regulatory change is telegraphed years in advance through committee reports, political speeches, and demographic pressures. Winners position themselves before the starting gun fires.

Consider the counter-factual: companies that entered insurance in 2005, after the market was proven, paid 3x more for talent, 5x more for real estate, and faced entrenched competitors. Being early isn't just about first-mover advantage—it's about shaping the rules, influencing regulations, and defining customer expectations before categories solidify.

The Art of Joint Ventures in India requires understanding that partnerships here aren't contracts—they're marriages. The New York Life partnership worked because they understood they were minority shareholders in equity but equal partners in operations. The Axis Bank partnership works because both sides need each other—Max needs distribution, Axis needs product expertise. Failed insurance JVs (and there are many) typically broke because foreign partners tried to impose global templates or Indian partners treated foreigners as mere technology vendors.

The unwritten rules: Foreign partners must accept that India isn't a copy-paste market; strategies that work in developed markets often fail here. Indian partners must acknowledge that global expertise, while needing localization, brings genuine value. Both must align on time horizons—insurance is a 20-year business, but most JVs are structured with 5-year exit clauses. The structural misalignment dooms many partnerships from day one.

Building Trust in Financial Services isn't about advertising spends or celebrity endorsements—it's about boring consistency. Max Life's 99.7% claim settlement ratio wasn't achieved through one initiative but thousands of small decisions: simplifying claim forms, training call center staff in empathy, creating dedicated claim settlement officers, publishing settlement data transparently. Trust compounds slowly but destroys instantly.

The insight here is that financial services trust is built through crisis, not calm. Max Life's response to the 2008 financial crisis—visiting customers personally, offering premium holidays, honoring claims despite market chaos—created more brand value than decades of advertising could. Every financial services company will face its crisis moment. How you respond defines whether you're building a business or a brand.

Long-term Thinking in Short-term Markets might be the hardest lesson. Indian capital markets reward quarterly performance, but insurance value creation happens over decades. Max Financial's stock has underperformed in multiple quarters when new business growth slowed, even as embedded value compounded. The discipline to ignore market mood swings while building long-term value requires unusual stakeholder alignment.

The practical application: structure your capital table for patience. Max Financial's concentrated ownership—promoters still own 23%—provides stability. Choose investors who understand the business model. Communicate in embedded value, not just accounting profits. Most importantly, ensure management incentives align with long-term value creation, not short-term stock prices.

Managing Stakeholder Complexity in financial services makes other industries look simple. Axis Max Life manages relationships with: IRDA (regulator), Axis Bank (partner and shareholder), 95,000 agents (who technically aren't employees), millions of customers (whose claims might come decades later), investors (wanting returns now), and employees (building careers in a slow-growth industry). Each stakeholder has different, often conflicting, interests.

The framework that works: radical transparency with all stakeholders about trade-offs. When Axis Max Life reduced ULIP commissions, they explained to agents why it was necessary for long-term survival. When growth slowed to improve profitability, they walked investors through the math. When claims were rejected, they published detailed reasons. Stakeholder management isn't about keeping everyone happy—it's about everyone understanding why decisions are made.

Distribution as the Ultimate Moat seems obvious but is persistently underestimated. Products in insurance are largely commoditized—everyone offers term insurance, endowment plans, ULIPs. Technology can be bought or built. Brands can be created. But distribution—real, embedded, trust-based distribution—takes decades to build and is nearly impossible to replicate.

Axis Max Life's multi-channel strategy wasn't accident but architecture. The agency channel provides reach, bancassurance provides efficiency, digital provides cost advantages. More importantly, each channel serves different customer segments with different products. The lesson: don't optimize for one perfect channel but build a portfolio of distribution assets that hedge against regulatory and market changes.

Why Culture Matters in Financial Services sounds like corporate platitude but is existential reality. Insurance is ultimately about promises—promises that might be tested 20 years after they're made. The employee processing a claim in 2044 for a policy sold in 2024 needs to honor commitments made by people who've long left the company. This requires culture, not just processes.

Max's "In the Business of Life" isn't just tagline but organizing principle. It influences hiring (preference for service-oriented backgrounds), training (mandatory customer service rotations), and decision-making (customer impact weighted equally with financial impact). Culture in financial services isn't about free lunches and casual Fridays—it's about embedding values that outlast individuals.

The meta-lesson from these lessons: building financial services in emerging markets requires a different mental model from Silicon Valley-style disruption. It's not about moving fast and breaking things but moving deliberately and building trust. It's not about winner-take-all dynamics but stable oligopolies with room for multiple winners. It's not about exits and liquidity events but compounding value over generations.

For entrepreneurs and operators studying Max Financial's playbook, the message is clear: the biggest opportunities in emerging markets lie in the most regulated, most complex, most patience-testing sectors. These markets reward those who prepare before opportunities become obvious, partner with humility, build trust through consistency, and think in decades while executing in quarters. It's not easy. That's precisely why it's valuable.

X. Bear vs Bull Case & Valuation Analysis

The investment debate around Max Financial Services crystallizes into a fundamental question: Is this a mature insurance company trading at fair value, or a growth composite with decades of compounding ahead? At ₹54,476 crores market capitalization against ₹14,900 crores of attributable embedded value (81.83% of ₹18,200 crores), the market assigns a 3.7x multiple—rich by global standards where insurers trade at 1-2x EV, but perhaps cheap for India's under-penetrated market. Let's examine both sides with the rigor this valuation gap demands.

The Bull Case rests on five structural pillars that could drive sustained compounding over the next decade.

First, the demographics are undeniable. India's insurable population—those aged 25-55 with household incomes above ₹5 lakhs annually—will grow from 200 million today to 400 million by 2035. This isn't speculation but mathematical certainty based on current age cohorts and GDP growth. More importantly, this demographic shift coincides with declining family support systems. The joint family that once provided financial security is fragmenting into nuclear units that need insurance protection.

Second, penetration remains astoundingly low. Life insurance penetration at 3.2% of GDP compares to 7.8% in China, 9.2% in South Korea, and 11% in Taiwan at similar development stages. Even reaching China's level implies a tripling of the market. Within this expansion, private insurers are taking disproportionate share—from 15% in 2010 to 39% today, heading toward 60% by 2030 if trends persist. Axis Max Life, as the fourth-largest private player with demonstrated execution, should capture its fair share of this growth.

Third, the Axis Bank synergy is just beginning. Of Axis Bank's 27 million customers, only 2.1 million have Axis Max Life policies—less than 8% penetration. Best-in-class bancassurance achieves 25-30% penetration over time. The revenue potential from deepening existing relationships dwarfs the need for new customer acquisition. Every 1% increase in Axis Bank customer penetration adds ₹300 crores to annual premium.

Fourth, the business model is inflecting toward profitability. After years of investment, the cost ratios are declining, persistency is improving, and the back-book is generating substantial renewal premiums. Operating leverage is kicking in—expenses growing at 8% annually while premiums grow at 18%. The embedded value return of 14% should expand to 18-20% as the business matures, similar to established Asian insurers.

Fifth, execution track record inspires confidence. Management has consistently delivered on strategic promises: the Axis partnership integration exceeded targets, the product mix shift toward protection improved margins, the digital transformation maintained competitiveness. This isn't a turnaround story requiring faith in change—it's a proven operator in execution mode.

The Bear Case presents equally compelling concerns that challenge the growth narrative.

Regulatory risk looms largest. IRDA's proposed changes to commission structures could reduce agent compensation by 30-40%, devastating distribution economics. Regulations mandating higher rural penetration or social sector obligations could force unprofitable growth. Most concerning, discussions about reducing tax benefits for insurance premiums would eliminate a key purchase driver for retail customers. Regulatory changes aren't possibilities but certainties—the only question is magnitude and timing.

Competition is intensifying from unexpected directions. LIC's digital transformation, backed by unlimited government support, could reclaim lost market share. New-age insurtechs, unencumbered by legacy costs, are cherry-picking profitable term insurance segments. Most threateningly, global tech giants are eyeing Indian financial services—imagine competing against Google or Amazon with their data advantages and customer relationships.

Interest rate sensitivity presents near-term challenges. Rising rates, while good for new business, create mark-to-market losses on existing bond portfolios. More problematically, guaranteed return products sold during low-rate periods could become loss-making if rates stay elevated. The duration mismatch inherent in life insurance—short-term liabilities funded by long-term assets—creates vulnerability to rate volatility that equity investors often underestimate.

The growth versus profitability trade-off remains unresolved. Bulls celebrate 18% premium growth, but bears note that acquisition costs remain stubbornly high. The promise of operating leverage assumes rational competition, but history shows insurance players periodically engage in destructive price wars for market share. The current benign competitive environment, with everyone focusing on profitability, could quickly deteriorate if growth slows.

Succession and key-person risks deserve consideration. Analjit Singh, at 70, has built extraordinary businesses but hasn't clearly communicated succession plans. The Axis partnership, while strong today, depends on personal relationships that new leadership might not maintain. Insurance is a relationship business where management changes can trigger partner nervousness and talent exodus.

Valuation Analysis requires understanding what the market is pricing in. At 3.7x embedded value, investors expect either: (a) 15% annual EV growth for the next decade, or (b) significant multiple expansion as the business matures, or (c) both. This seems aggressive but not impossible.

Comparing to global benchmarks provides perspective. AIA trades at 2.2x EV with 8% growth, Prudential at 1.1x with 5% growth, Ping An at 1.5x with 12% growth. The Max Financial premium implies either Indian exceptionalism or eventual disappointment. Bulls argue India's 20-year growth runway justifies higher multiples. Bears contend that regulatory risks and competitive intensity offset growth advantages.

The sum-of-parts analysis offers another lens. The life insurance stake at 3x EV implies ₹45,000 crores. Max Healthcare (held separately) adds ₹8,000 crores. Other investments contribute ₹2,000 crores. Total value of ₹55,000 crores roughly matches current market cap, suggesting little margin of safety at current prices.

What the Market is Missing might be the optionality embedded in the platform. A potential IPO of Axis Max Life could crystallize value—comparable insurers list at 4-5x EV in India. The health insurance opportunity remains untapped despite clear synergies. International expansion, particularly to similar markets like Bangladesh or Sri Lanka, could provide growth beyond India.

The ultimate question for investors isn't whether Max Financial is good business—it clearly is—but whether it's a good investment at current prices. The bull case requires belief in India's structural story, management execution, and regulatory stability. The bear case simply requires acknowledgment that things rarely go as planned in financial services. At 3.7x embedded value, the market is voting with the bulls, but not overwhelmingly. The next decade will determine who was right.

XI. Power & Counter-Positioning Analysis

In the framework of business strategy, true competitive advantages—what Hamilton Helmer calls "Powers"—are rarer than most investors believe. For Max Financial Services, identifying which advantages are sustainable versus temporary determines whether the current valuation multiple is justified or excessive. Let's examine each potential source of power with the skepticism this analysis demands.

Scale Economies represent Max's most tangible power, though it's weaker than initially appears. With ₹1.2 lakh crores of assets under management, fixed costs get spread across a large base—technology investments, regulatory compliance, actuarial teams cost roughly the same whether managing ₹50,000 crores or ₹150,000 crores. The operating expense ratio declining from 22% in 2010 to 14.8% in 2024 demonstrates this leverage.

But scale in insurance isn't like scale in software. Claims costs are variable, not fixed. Distribution costs actually increase with scale as you chase marginal customers. Most critically, India's insurance market is still subscale by global standards—even LIC would be considered mid-sized internationally. The scale advantages Max enjoys versus smaller private players exist but aren't insurmountable. A new entrant with sufficient capital could reach minimum efficient scale within a decade.

Switching Costs provide more durable advantage, though they're often overestimated in insurance. A customer with an existing traditional policy faces surrender charges of 30-50% if they switch in early years. The paperwork burden of changing insurers—medical examinations, documentation, waiting periods—creates friction. Most powerfully, the psychological switching cost is enormous: life insurance is sold on fear and trust, and once that trust is established, customers rarely reconsider.

Yet switching costs are asymmetric. They're high for traditional products but negligible for term insurance. They matter for existing customers but not new ones. Most concerning, regulatory pressure to improve portability could erode these advantages. IRDA's proposals for policy portability, similar to health insurance, would eliminate much of this power. The switching costs that exist today are more regulatory artifact than business fundamental.

Brand Power in financial services is peculiar—it's less about preference and more about trust. The Axis Max Life brand, especially post-rebrand, carries the halo of Axis Bank's credibility. For risk-averse middle-class Indians, buying insurance from "their bank's insurance company" provides comfort that no amount of advertising could create.

But brand in insurance is fragile and narrow. It's fragile because one mis-handled claim can destroy decades of reputation building. It's narrow because brand drives consideration, not purchase—customers still buy based on product features and price. The proliferation of comparison platforms like PolicyBazaar commoditizes brand value for simple products. Brand matters most where it matters least (complex products that need explanation) and matters least where it matters most (simple products with high volumes).

Counter-Positioning Against LIC represents Max's most interesting strategic power. By explicitly not trying to be LIC—not serving rural markets, not offering social sector products, not maintaining massive branch networks—Max can optimize for profitable urban segments. This isn't weakness but strategic focus.

LIC's cost structure, built for universal service, can't compete in urban markets where customers value service over presence. Their 590,000 employees and 2,048 branches are assets for rural penetration but liabilities for urban efficiency. Max's 9,500 employees serving similar premium volumes demonstrates the advantage of counter-positioning.

The risk is that LIC could create a subsidiary optimized for urban markets, negating this advantage. But organizational antibodies make this unlikely—unions would resist, politicians would object, and culture would clash. Counter-positioning works precisely because incumbents can't respond without destroying their existing model.

Network Effects in Distribution exist but are weaker than in true network businesses. Each additional Axis Max Life agent makes the agency force marginally more attractive to join—better training programs, stronger brand recognition, more referral opportunities. The 95,000-agent network creates density advantages in urban markets that smaller competitors can't match.

But insurance distribution isn't winner-take-all. Agents often work with multiple insurers. Customers don't benefit from other customers using the same insurer. The network effects that exist are linear, not exponential. They provide advantage but not dominance.

Process Power in Underwriting and Claims might be Max's most underappreciated advantage. Two decades of mortality data, claims patterns, and fraud detection create proprietary insights that new entrants can't replicate. The ability to price risk 5% better than competitors compounds over time into enormous advantages.

Consider their 99.7% claim settlement ratio—this isn't largesse but precision. They've learned to identify fraudulent claims (the 0.3%) while paying legitimate ones quickly. This creates a virtuous cycle: better claim experience attracts better customers who file fewer fraudulent claims, enabling even better ratios.

But process power in insurance faces constant erosion. Reinsurers share data across companies. Regulatory requirements for standard products reduce differentiation. Most concerning, artificial intelligence democratizes underwriting expertise. The process advantages that took decades to build might be replicated by machines in years.

The Axis Bank Relationship as Strategic Asset transcends typical bancassurance arrangements. This isn't just distribution but deep operational integration. Shared customer data enables precise risk assessment. Co-located employees reduce coordination costs. Aligned incentives ensure sustainable partnership.

The power here is relationship-specific advantage—no other insurer can access Axis Bank's distribution, and Axis Bank can't easily switch insurers without massive disruption. The rebranding to Axis Max Life makes this irreversible from both sides. It's the corporate equivalent of marriage, with all the commitment that implies.

Yet dependence creates vulnerability. If Axis Bank faces challenges—regulatory action, competitive pressure, management change—Max Life suffers collaterally. The exclusive relationship that provides advantage also concentrates risk. Diversification through the agency channel provides some hedge but doesn't eliminate the exposure.

Synthesizing Power Analysis, Max Financial possesses multiple advantages but no single overwhelming power. Scale provides cost advantages but not dominance. Brand creates trust but not pricing power. Counter-positioning enables focus but not monopoly. The Axis relationship provides distribution but creates dependence.

This combination of moderate powers might actually be optimal. Businesses with one overwhelming advantage often become complacent. Those with no advantages obviously fail. Max's portfolio of reinforcing but not dominant advantages creates resilience—if regulation erodes switching costs, brand and scale remain. If competition intensifies in urban markets, the Axis relationship provides defense.

For investors, this power analysis suggests Max Financial is a high-quality business but not an exceptional one. It should earn returns above cost of capital but not extraordinary profits. It can defend market share but not dominate the industry. The current valuation at 3.7x embedded value prices in more power than actually exists. Unless new sources of advantage emerge—regulatory changes that favor incumbents, technology breakthroughs in underwriting, or unexpected consolidation—the business quality supports a good investment, not a great one.

XII. Looking Forward: The Next Decade

The boardroom at Max Towers in December 2034 will look vastly different from today. Analjit Singh, if still present, will be 80. The executives managing the company will likely be digital natives who've never sold insurance face-to-face. The customers they serve will be Gen Z Indians who research insurance on social media, buy through apps, and expect claims to be settled in hours, not days. The question isn't whether Max Financial will exist—insurance companies rarely disappear—but whether it will thrive or merely survive in this transformed landscape.

India's Insurance Penetration Opportunity remains the north star for any forward-looking analysis. Even conservative projections suggest life insurance penetration reaching 5% of GDP by 2035, up from 3.2% today. With GDP expected to double from $3.7 trillion to $7.5 trillion, the market size expands from ₹8 lakh crores to ₹30 lakh crores. Private insurers, taking 60% share by then, would control ₹18 lakh crores—a 5x expansion from today.

But penetration isn't destiny. Japan's insurance penetration has declined from 9% to 6% over the past decade despite an aging population. China's growth has slowed dramatically after reaching 4% penetration. The assumption that India will follow the Asian insurance playbook ignores cultural differences—Indians save through real estate and gold, not financial products. The joint family system, though weakening, still provides informal insurance. Penetration will grow, but perhaps to 4%, not 7%, and over 15 years, not 10.

Digital Transformation and Insurtech Disruption will fundamentally reshape distribution economics. By 2034, the 95,000-agent army that built Max Life might be as anachronistic as door-to-door encyclopedia salesmen. Already, 40% of term insurance is sold online. As millennials become the primary insurance buyers, digital-first becomes digital-only for simple products.

The transformation goes beyond distribution. Artificial intelligence will automate underwriting for 80% of cases. Blockchain-based smart contracts will enable instant claim settlement. Parametric insurance—automatic payouts triggered by events like hospitalization or job loss—will eliminate claims processing entirely for certain products. The operational advantages that established players enjoy will evaporate.

Yet digital transformation in insurance faces unique barriers. Complex products still need human explanation. Regulatory requirements for physical documentation remain. Most fundamentally, insurance is sold, not bought—even digital natives need nudging to buy adequate coverage. The future likely holds hybrid models: AI-powered agents, video-based advice, gamified education. Max's challenge is building these capabilities while maintaining current operations.

Health Insurance Adjacencies represent the most obvious expansion opportunity. The health insurance market, at ₹90,000 crores and growing 15% annually, is where life insurance was in 2005—underpenetrated, dominated by public sector players, ripe for innovation. The synergies with life insurance are obvious: shared distribution, customer data, operational infrastructure.

But Max has watched this opportunity for a decade without acting decisively. The reasons are telling: health insurance is operationally intensive (claims happen annually, not at death), fraud-prone (hospitals and customers often collude), and regulatory-heavy (price controls, coverage mandates). The skills that make Max successful in life insurance—patient capital, long-term thinking, relationship focus—don't necessarily translate to health insurance's transactional nature.

The likely path is partnership or acquisition rather than organic entry. Acquiring a mid-sized health insurer would provide instant scale and expertise. Partnering with Axis Bank's health insurance offerings could create bundled products. But execution risk is high—many life insurers have stumbled trying to crack health insurance.

The Potential IPO of Max Life could be the defining event of the next decade. With embedded value approaching ₹30,000 crores by 2030, a listing at 4x EV would value Axis Max Life at ₹120,000 crores. Max Financial's 70% stake (assuming Axis increases to 30%) would be worth ₹84,000 crores—a 50% premium to today's entire market cap.

But IPO dreams often disappoint. Regulatory approval requires demonstrated profitability—achievable but not guaranteed. Market conditions must align—insurance IPOs have narrow windows. Most critically, Axis Bank must agree, and their incentives might differ. They benefit from keeping Max Life captive for exclusive distribution. An IPO creates pressure for Max Life to diversify distribution, potentially undermining Axis's strategic advantage.

Succession Planning and Leadership Transition looms as the most delicate challenge. Analjit Singh has built extraordinary businesses but hasn't clearly groomed successors. His children work in the business but haven't demonstrated independent leadership. Professional managers run operations but lack the founder's vision and relationships.

The insurance industry is littered with companies that stumbled during succession. Founder-entrepreneurs build through force of personality and intuition. Professional managers optimize through process and analysis. The transition often loses the entrepreneurial spark while gaining operational discipline. For Max, maintaining cultural DNA while professionalizing management will determine whether the next decade builds on or squanders the last two.

What Success Looks Like in 2035 requires imagining a fundamentally different company. Successful execution would see Max Financial controlling 15% of private market share, up from 9.9% today. Embedded value would exceed ₹50,000 crores. The business would be sustainably profitable with return on embedded value above 20%. Distribution would be 60% digital, 30% bancassurance, 10% agency. Health insurance would contribute 20% of value. Most importantly, the company would have successfully navigated leadership transition while maintaining service excellence.

But success might look different than growth. Perhaps Max Financial in 2035 is smaller but more profitable, having ceded market share while improving margins. Perhaps it's merged with another insurer, creating India's first true insurance powerhouse. Perhaps it's expanded internationally, building presence in similar markets. The path to value creation isn't always through size.

The certainties for the next decade are few but important. India will have 1.5 billion people, most still underinsured. Technology will reshape but not eliminate insurance distribution. Regulations will tighten, not loosen. Competition will intensify from both traditional players and new entrants. Within these parameters, Max Financial must navigate between growth and profitability, innovation and stability, independence and partnership.

The company that enters 2035 will be dramatically different from today's Max Financial. Whether it's better or just different, stronger or just bigger, more valuable or just more complex, depends on decisions being made today in boardrooms and regulatory offices, in technology labs and agency meetings. The next decade's story is being written now. Based on the last two decades, Max Financial has earned the right to optimism, tempered by the reality that in financial services, the future rarely unfolds as planned.

XIII. Key Takeaways & Lessons

After examining Max Financial Services from every angle—its history, strategy, economics, and prospects—what emerges aren't just insights about one company but broader lessons about value creation in emerging markets. These takeaways challenge conventional wisdom about how businesses should be built and valued.

Why Boring Businesses Can Create Extraordinary Value might be the most counterintuitive lesson. In an era celebrating disruption, Max Financial built enormous value by selling a product—life insurance—that hasn't fundamentally changed in centuries. No network effects, no software margins, no viral growth. Just the patient accumulation of customers who pay premiums for decades.

The numbers tell the story: ₹500 crores invested in 2000 is worth ₹54,000 crores today—a 100x return that would make any venture capitalist envious. This wasn't achieved through multiple expansion or financial engineering but through compound growth in a boring industry. The lesson: extraordinary returns often come from ordinary businesses executed extraordinarily well.

The Importance of Regulatory Relationships cannot be overstated in emerging markets. Max's success wasn't just about navigating regulations but shaping them. By engaging constructively with IRDA, proposing sensible frameworks, and demonstrating good behavior, Max influenced rules that advantaged responsible incumbents over reckless entrants.