NHPC: India's Hydropower Colossus

I. Cold Open & Episode Roadmap

Picture this: Deep in the Himalayas, at 2,800 meters above sea level, engineers blast through granite mountains in -20°C temperatures. They're building what will become the Uri-I hydroelectric project—a 480 MW powerhouse that will light up Kashmir. The year is 1989, and this is NHPC at work, quietly constructing the backbone of India's renewable energy infrastructure, one massive concrete dam at a time.

Today, NHPC Limited commands a ₹82,148 crore market capitalization, operates 7,233 MW of power generation capacity, and holds the crown as India's largest hydropower company. It's a Navaratna enterprise—one of only 16 central public sector enterprises granted this prestigious status by the Indian government. Yet despite these accolades, the company's five-year sales growth languishes at a mere 0.73%. Its stock has delivered underwhelming returns compared to the broader market. The disconnect is jarring.

Here's the question that matters: How did a government PSU created during India's socialist era become the country's hydropower monopoly? And more importantly, why is this monopoly struggling to grow in an era when India desperately needs clean energy?

The NHPC story is really three stories intertwined. First, it's a tale of nation-building—how a newly independent India sought energy security through ambitious infrastructure projects. Second, it's a case study in the complexities of operating in India's federal structure, where every dam requires negotiating with states, tribes, environmentalists, and local communities. Third, it's a financial puzzle—a company with 41.8% net profit margins that somehow delivers single-digit returns on equity.

Over the next few hours, we'll journey from NHPC's founding in 1975 through the oil crisis, trace its evolution from a government department to a listed company, examine its ambitious failures like the still-incomplete Subansiri project, and evaluate whether this hydropower giant can reinvent itself for India's renewable future. We'll explore why building dams in the Himalayas is as much about geology as it is about politics, why the company's best projects are also its most controversial, and what the rise of solar power means for a business model built on 50-year asset lives.

This isn't just NHPC's story—it's the story of how India builds infrastructure, manages natural resources, and balances development with democracy. It's about the tensions between Delhi's energy ambitions and the ground realities in remote valleys where these projects take shape.

So what for investors: NHPC represents a unique paradox in Indian markets—a government-backed monopoly with pristine profit margins trading at modest valuations. Understanding why requires looking beyond the numbers to the structural challenges of hydropower development in a democratic, federal, and environmentally conscious India.

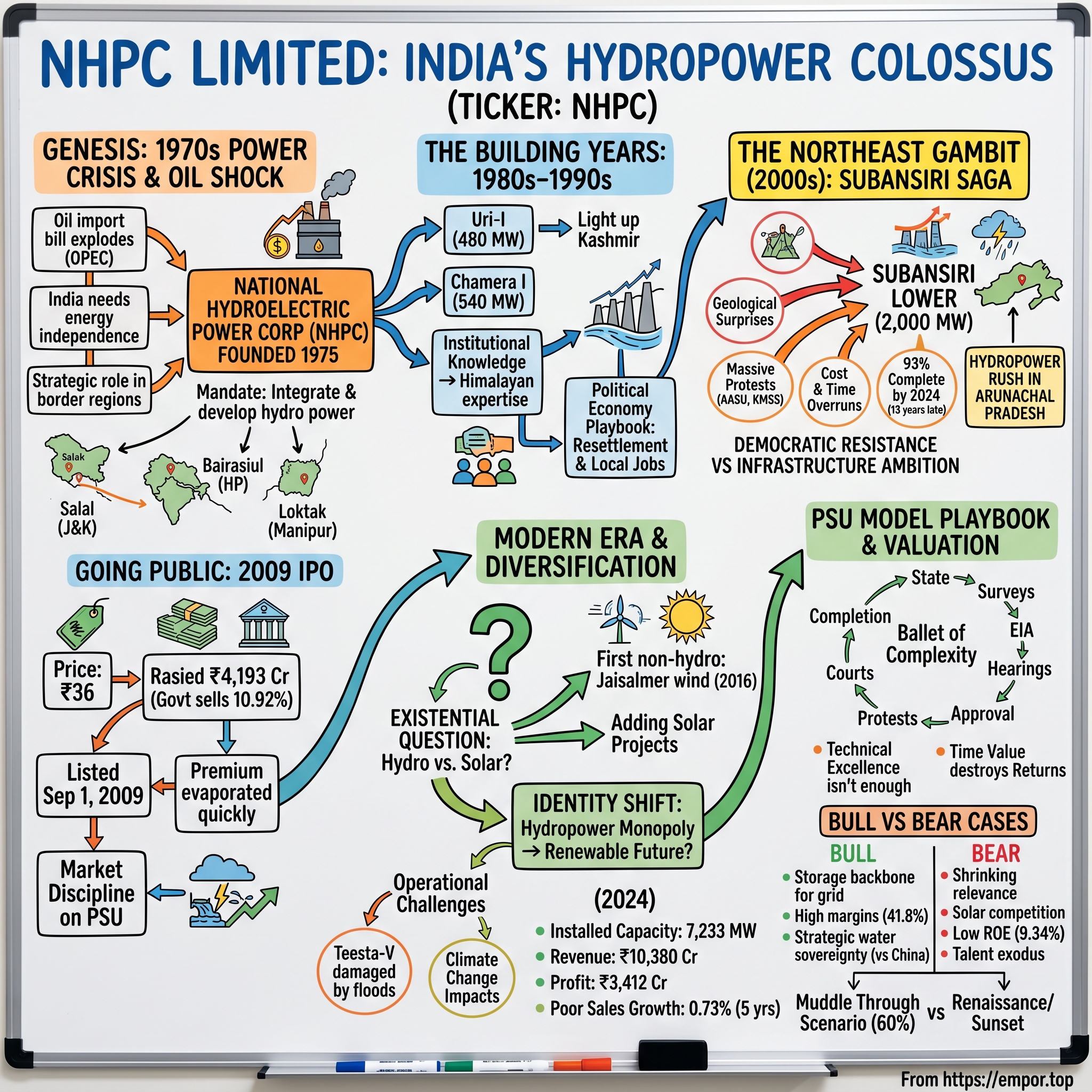

II. Genesis: India's Power Crisis & The Birth of NHPC (1970s)

The lights went out across Delhi in January 1975. Not for an hour or two—but for days. Factories shut down, water pumps stopped working, and the capital of the world's largest democracy sat in darkness. This wasn't unusual. Power cuts were so routine that middle-class families planned their lives around load-shedding schedules. Industrial production crawled. The energy crisis wasn't just an inconvenience; it was strangling India's economic aspirations.

Then came the oil shock. When OPEC quadrupled crude prices in 1973-74, India's import bill exploded. The country was spending precious foreign exchange—already scarce—on fuel it couldn't afford. Prime Minister Indira Gandhi's government faced a stark reality: India needed energy independence, and it needed it fast.

Enter the Himalayas—8,600 kilometers of mountains holding an estimated 148,700 MW of hydroelectric potential. While thermal power plants required imported coal or oil, these mountains offered something radical: free fuel in the form of glacier-fed rivers. The Sutlej, Beas, Chenab, and Brahmaputra carried enough kinetic energy to power the entire nation. The problem? Nobody knew how to harness it at scale.

On November 7, 1975, while Emergency rule gripped the nation, the government quietly incorporated National Hydroelectric Power Corporation Limited. The mandate was ambitious: "to plan, promote and organize integrated and efficient development of hydroelectric power in all aspects." Translation: build dams, lots of them, wherever water flowed down a mountain.

NHPC didn't start from scratch. It inherited three stalled projects from the Central Hydroelectric Projects Control Board—Salal Stage-I in Jammu & Kashmir (345 MW), Bairasiul in Himachal Pradesh (180 MW), and Loktak in Manipur (105 MW). These weren't random selections. Salal sat on the Chenab river, controlling water that Pakistan also claimed under the Indus Water Treaty. Loktak would bring electricity to the insurgency-prone Northeast. Bairasiul would tap the Ravi river's potential. Each project carried strategic significance beyond mere megawatts.

The Baira Suil project became NHPC's first real test. Located in Himachal Pradesh's Chamba district, it required building a 47-meter-high dam in a seismically active zone, diverting the Baira river through a 5.3-kilometer tunnel, and constructing an underground powerhouse—all using 1970s technology. The project would take 11 years to complete, coming online only in 1981. But it proved something crucial: Indian engineers could build complex hydroelectric infrastructure in the Himalayas.

The government's vision extended beyond engineering. Hydropower offered a unique economic model—massive upfront capital investment, but near-zero operating costs thereafter. Once built, a dam could generate electricity for 50-100 years with minimal fuel costs. For a foreign-exchange-starved economy, this was compelling. Every megawatt of hydro meant less oil imported, less coal burned, less currency spent.

But there was a deeper strategic calculus at play. The Himalayas formed India's northern border with China and Pakistan. Building infrastructure in these remote regions wasn't just about electricity—it was about establishing presence, creating roads, bringing development to border areas. NHPC's projects would double as instruments of national integration.

By 1980, NHPC had clarity on its role: it would be the government's vehicle for tapping Himalayan hydropower. The company began surveying rivers, studying geological formations, and identifying sites. Engineers trained in the Soviet Union and Norway brought back expertise in cold-climate construction. The organization started building something more valuable than dams—institutional knowledge of how to execute projects in the world's most challenging terrain. The government's hydropower ambitions weren't theoretical. By the end of the 1970s, NHPC had assembled teams, acquired Soviet-era equipment, and started breaking ground. The company commissioned Baira Siul in 1981, Loktak in 1983, and Salal-I in 1987, establishing its credentials as India's premier hydropower developer.

Myth vs Reality Box:

Myth: NHPC was created as just another inefficient PSU.

Reality: The company was founded with specific strategic objectives—energy security post-oil crisis and infrastructure development in border regions. Its early projects weren't random; each carried geopolitical significance.

So what for investors: NHPC's genesis reveals a structural advantage that persists today—government backing for projects deemed strategically important. This means access to capital, regulatory clearances, and political support that private players can't match. However, it also means accepting lower returns in exchange for executing national priorities.

III. The Building Years: Scaling State Capacity (1980s-1990s)

The boardroom at NHPC's Delhi headquarters erupted in debate in early 1986. The question on the table: Should a government department transform into a public limited company? The old guard worried about losing bureaucratic protection. The reformers saw opportunity—access to capital markets, operational flexibility, faster decision-making. By year's end, the reformers won. NHPC became a public limited company, signaling ambitions beyond being just another government department.

This transformation coincided with NHPC taking on its most ambitious projects yet. Chamera I Power Station (540 MW) in Himachal Pradesh would be commissioned in 1994, but its construction through the late 1980s pushed NHPC's engineering capabilities to new limits. The project required building a 133-meter-high concrete gravity dam in a seismically active zone, creating a 33-kilometer reservoir, and installing three 180 MW Francis turbines—technology that India had never deployed at this scale.

The Uri-I project in Kashmir presented different challenges. Beyond the technical complexity of building at high altitude, NHPC had to navigate the region's security situation. Construction camps needed military protection. Supply lines crossed territory where militants operated. Engineers wore bulletproof vests to site inspections. Yet the project's strategic importance—providing power to Kashmir and demonstrating Indian control over the region—meant failure wasn't an option. When Uri-I's 480 MW capacity came online in 1997, it represented more than just electricity generation; it was a statement of India's ability to build infrastructure anywhere within its borders.

Teesta V Power Station (510 MW) in Sikkim, commissioned in 2007-08, showcased NHPC's evolving sophistication. The project featured a 96.45-meter-high concrete dam and an underground powerhouse carved into the mountain—a design that minimized environmental impact while maximizing generation efficiency. The 17.5-kilometer headrace tunnel, one of India's longest at the time, demonstrated NHPC's mastery of tunnel-boring technology.

But the real transformation during these decades wasn't visible in concrete and steel. NHPC built something more valuable: institutional knowledge. The company developed protocols for working in extreme altitudes where oxygen levels dropped by 40%. It created logistics systems to transport 200-ton turbines through mountain roads designed for pack animals. It learned to manage projects where the nearest medical facility might be 200 kilometers away.

The financial model evolved too. NHPC pioneered the "70:30" financing structure—70% debt, 30% equity—that became standard for Indian infrastructure projects. The company negotiated power purchase agreements with state electricity boards, creating predictable revenue streams that banks could lend against. It developed relationships with multilateral agencies like the World Bank and Asian Development Bank, accessing not just capital but global best practices.

Consider the organizational culture that emerged. NHPC engineers spent years at remote project sites, living in prefabricated colonies, their children attending makeshift schools. A unique esprit de corps developed—part engineering excellence, part frontier spirit. The company's training center in Faridabad became a finishing school for hydropower professionals, with engineers from other countries coming to learn high-altitude construction techniques.

The political economy of dam building revealed itself during this period. Every project required negotiating with multiple stakeholders: the central government (which owned NHPC), state governments (which controlled land and water rights), local communities (who faced displacement), and environmental groups (increasingly vocal through the 1990s). NHPC developed a playbook: generous compensation packages for displaced families, jobs for local youth, infrastructure development in project areas. The Chamera project, for instance, transformed the economy of Chamba district, with NHPC building roads, schools, and hospitals that served communities beyond just project-affected families. By the late 1990s, NHPC had completed projects totaling over 2,500 MW. Uri-I's construction started in 1989 and was commissioned in 1997 with 480 MW capacity, Chamera I (540 MW) was commissioned in 1994, and multiple smaller projects came online. The company had proven it could execute complex infrastructure in India's most challenging terrain.

So what for investors: The 1980s-1990s established NHPC's core competitive advantages that persist today—engineering expertise in Himalayan construction, relationships with multilateral lenders, and a political economy playbook for managing stakeholder complexity. These capabilities create high barriers to entry but also explain why project execution remains slow and capital-intensive.

IV. The Northeast Gambit: Subansiri & The Dam Rush (2000s)

The helicopter descended through monsoon clouds over the Brahmaputra valley in August 2003. Inside sat NHPC's survey team, maps spread across their laps, marking what would become India's most ambitious—and controversial—hydropower project. Below them, where the Subansiri river met the Brahmaputra at the Assam-Arunachal Pradesh border, lay the site for a 2,000 MW power station. It would be India's largest hydroelectric project, a symbol of the nation's renewable energy ambitions. Within a decade, it would also become a cautionary tale about the limits of top-down infrastructure development in a democracy.

The early 2000s marked a turning point in India's energy thinking. The BJP-led NDA government, riding high on the "India Shining" narrative, pushed aggressively for non-carbon fuel sources. Climate change entered mainstream policy discourse. Coal plants faced environmental opposition. Nuclear power remained controversial post-Chernobyl. Hydropower, suddenly, looked like the answer—clean, renewable, and leveraging India's Himalayan advantage.

Arunachal Pradesh became ground zero for this hydropower rush. The state government, eager for revenue and development, signed an astonishing 153 Memorandums of Understanding by 2009 for projects totaling 43,000 MW—more than Spain's entire installed capacity. NHPC led the charge with Subansiri Lower, but private players like Reliance, Jaiprakash, and GMR rushed in, each claiming their piece of Himalayan rivers.

Subansiri Lower was designed to be India's biggest electricity supplier at 2,000 MW. The numbers were staggering: a 116-meter-high concrete gravity dam creating a reservoir submerging 3,436 hectares, eight 250 MW Francis turbine generators, and an underground powerhouse carved into solid rock. The original cost estimate of ₹6,600 crores seemed reasonable for a project of this scale.

Then reality hit. First came the geological surprises. The rock formations weren't as stable as surveys suggested. Landslides during construction destroyed access roads. The underground powerhouse location had to be shifted when engineers discovered a fault line. Each surprise added years and billions to the project cost.

But the real crisis emerged from an unexpected quarter—civil society. In 2011, a coalition of student organizations, environmental groups, and local communities launched protests that would reshape India's approach to dam building. The All Assam Students' Union (AASU) mobilized thousands, blocking roads to the construction site. The Krishak Mukti Sangram Samiti (KMSS) organized sit-ins that lasted months. Their concerns weren't frivolous: they pointed to inadequate downstream impact studies, seismic risks in a Zone V earthquake area, and the potential for catastrophic dam failure.

The protests turned violent. NHPC's offices were ransacked. Engineers received death threats. Supply trucks were burned. By December 2011, NHPC made an unprecedented decision—it suspended construction indefinitely. For a Navratna PSU to halt its flagship project due to public protests was unheard of. The site, where ₹5,000 crores had already been spent, turned into a ghost town. Massive turbines sat rusting. The half-built dam stood as a monument to India's infrastructure ambitions meeting democratic resistance.

The Subansiri crisis revealed fundamental flaws in India's hydropower development model. Environmental Impact Assessments were treated as formalities rather than genuine studies. Public consultations happened after projects were approved, not before. The cumulative impact of multiple dams on a single river basin was never assessed. Most critically, the development model ignored that rivers don't respect state boundaries—a dam in Arunachal Pradesh affects farmers in Assam, but Assam had no say in Arunachal's hydropower decisions.

NHPC found itself caught between multiple power centers. The central government, which owned the company, wanted projects completed. State governments wanted revenue and development. Local communities wanted protection from flooding and displacement. Environmental groups wanted rivers preserved. The courts wanted procedures followed. No amount of engineering expertise could navigate these political rapids.

The financial implications were severe. By 2015, Subansiri's cost had ballooned to over ₹20,000 crores. The project's IRR, once projected at 15%, fell into single digits. NHPC's stock price reflected investor concerns about the company's ability to execute projects. The broader hydropower sector froze—banks became reluctant to lend, private developers abandoned projects, and the 43,000 MW Arunachal dream shrank to a few thousand megawatts of actual capacity. The protests were led by groups like KMSS, AASU and AJYCP. The construction cost went up by about ₹1,200 crore owing to forced suspension of work since December 2011, with NHPC having already spent about ₹6,600 crore. By January 2020, the cost of the mega project had escalated to around Rs 20,000 crore from the initial worth of Rs 6,285 crore.

Yet even as Subansiri languished, NHPC slowly worked through the political and legal maze. Construction resumed in October 2019 after clearance from the National Green Tribunal. By 2024, the project was 93% complete, with power generation expected to begin in March 2025—13 years behind schedule and at triple the original cost.

Myth vs Reality Box:

Myth: Environmental protesters killed India's hydropower dreams.

Reality: The protests exposed fundamental flaws in project planning—inadequate environmental assessments, minimal public consultation, and ignoring downstream impacts. The real failure was treating mega-infrastructure as a technical rather than socio-political challenge.

So what for investors: The Subansiri saga reveals NHPC's greatest vulnerability—execution risk in democratic India. While the company eventually completes projects, the time and cost overruns destroy returns. The 43,000 MW Arunachal dream becoming a few thousand MW of reality shows the gap between policy ambitions and ground realities.

V. Going Public: The 2009 IPO Story

The trading floor at the Bombay Stock Exchange buzzed with unusual energy on September 1, 2009. NHPC's shares were about to start trading—the first major PSU IPO since the global financial crisis. The government had priced the issue at ₹36 per share, raising ₹4,193 crores by selling a 10.92% stake. Within minutes of opening, the stock jumped to ₹42, a 17% premium. Investment bankers celebrated. The government declared victory. But behind this apparent success lay a more complex story about why a profitable monopoly needed public markets at all.

The decision to list NHPC wasn't driven by the company's capital needs—it had healthy cash flows and government backing for project financing. Instead, the IPO was part of a broader governance reform agenda. The UPA government believed that public listing would impose market discipline on PSUs, forcing transparency, improving efficiency, and creating shareholder accountability. For NHPC specifically, access to capital markets would reduce dependence on budgetary support at a time when the government faced fiscal constraints.

The IPO roadshow revealed fascinating dynamics. Institutional investors loved NHPC's fundamentals—monopolistic position, 40%+ operating margins, massive growth pipeline. But they worried about execution risk, remembering Tehri and Narmada controversies. Retail investors, attracted by the government's credibility and the discount offered to them, oversubscribed their portion 2.7 times. The employee portion saw 5.5 times subscription, reflecting internal confidence.

The prospectus made for interesting reading. NHPC disclosed 24 operational projects with 5,175 MW capacity, 13 projects under construction totaling 5,322 MW, and a pipeline of future projects exceeding 10,000 MW. The company reported revenues of ₹4,425 crores and net profit of ₹2,115 crores for FY2009—a 48% net margin that would make any private company envious. Yet buried in the risk factors were hints of challenges ahead: "land acquisition delays," "geological surprises," "rehabilitation issues," "environmental clearances."

Post-listing, NHPC faced a new reality. Quarterly earnings calls meant explaining why projects were delayed. Stock price movements reflected market sentiment about government policies. Analysts questioned capital allocation decisions. The company had to balance its role as a government instrument for energy security with its duty to minority shareholders seeking returns.

The market's initial enthusiasm waned as reality set in. By 2010, NHPC's stock had fallen below the IPO price as Subansiri delays became apparent. Investors discovered that owning a piece of India's hydropower monopoly meant accepting the constraints of democratic decision-making, environmental activism, and geological uncertainty. The stock would remain range-bound for years, reflecting this tension between monopolistic advantages and execution challenges.

The IPO did bring some benefits. NHPC improved its project monitoring systems, introduced enterprise resource planning, and enhanced disclosure standards. Independent directors brought fresh perspectives to board discussions. The company became more conscious of return on equity, even if it couldn't always optimize for it given its PSU mandate.

But fundamental tensions remained unresolved. How should a listed PSU balance commercial objectives with national priorities? Should it maximize profits or ensure energy security? Can it reject unviable projects assigned by the government? These questions would define NHPC's journey as a public company. The market data confirms the IPO details: priced at ₹36 per share, with shares listed on BSE and NSE on September 1, 2009. The stock opened at ₹39 on BSE, reaching a high of ₹39.75 before closing at ₹36.70 on the first day—a modest premium that quickly evaporated.

So what for investors: NHPC's IPO marked a transition from pure PSU to quasi-public company, but fundamental tensions remain unresolved. The company trades at modest valuations (current P/E around 24x) despite monopolistic advantages, reflecting market skepticism about execution capabilities and return on equity. For investors, NHPC represents a bet on India's energy transition, but one constrained by democratic processes and PSU limitations.

VI. The Dibang Dream & Environmental Battles

The helicopter carrying Prime Minister Manmohan Singh descended through clouds into the remote Dibang Valley in January 2008. Below, where the Dibang river cuts through pristine forests home to the Idu Mishmi tribe, India planned to build the world's tallest concrete gravity dam—288 meters high, dwarfing even China's Three Gorges Dam in height. As Singh laid the foundation stone, he declared this would be India's answer to climate change, a 3,000 MW carbon-free power source. Sixteen years later, not a single cubic meter of concrete has been poured. The Dibang project has become India's most expensive monument to the gap between infrastructure ambitions and environmental democracy.

The Dibang Multipurpose Project represented everything ambitious about India's hydropower dreams. The dam would create a reservoir submerging 5,056 hectares of biodiversity hotspot forest. It would generate 11,223 million units of electricity annually. The initial cost estimate of ₹15,886 crores seemed reasonable for a project that would be India's largest hydroelectric installation. NHPC mobilized its best engineers, confident that their experience from Uri and Chamera would ensure smooth execution.

But Dibang was different. This wasn't just challenging terrain—it was one of the world's biodiversity hotspots, home to 159 species of butterflies, 680 species of birds, and countless endemic plants. The Idu Mishmi people, numbering barely 12,000, considered the Dibang valley sacred. Their creation myths spoke of emerging from these forests. Their shamans communicated with spirits that resided in specific trees marked for submergence.

The first public hearing in 2008 turned into a confrontation. Idu Mishmi elders spoke of losing not just land but their cosmology. Environmental scientists presented data showing the area harbored the last viable populations of the Mishmi takin and the Blyth's tragopan. NHPC's officials, armed with compensation packages and development promises, found themselves in debates about epistemology—whose knowledge counted, whose values mattered.

The environmental clearance process became a bureaucratic odyssey. The Forest Advisory Committee rejected the proposal in 2013, citing the loss of 2,00,000 trees. NHPC responded by reducing the dam height to 278 meters, shrinking the submergence area. The Wildlife Board flagged concerns about endemic species. NHPC commissioned more studies. The Expert Appraisal Committee demanded cumulative impact assessments. NHPC hired international consultants.

Each iteration revealed deeper contradictions. The project's very purpose kept shifting—flood control, power generation, water storage—depending on which approval was needed. Cost estimates ballooned as design changes accumulated. By 2014, the estimated cost had doubled to over ₹30,000 crores. The promised commissioning date moved from 2016 to 2020, then became indefinite.

The tragedy of Dibang wasn't just delay—it was what the delay revealed about India's development model. NHPC had followed every procedure, obtained every clearance, yet couldn't build. The Idu Mishmi had used every democratic tool—petitions, protests, legal challenges—yet couldn't definitively stop a project that threatened their existence. The environment ministry was caught between development imperatives and conservation mandates, issuing clearances then withdrawing them.

In 2019, a breakthrough seemed imminent when the Forest Advisory Committee finally recommended clearance. But it came with 29 conditions, including maintaining minimum environmental flows, real-time monitoring, and compensatory afforestation of 10,000 hectares. Each condition added complexity and cost. NHPC's internal estimates suggested the project's IRR had fallen below 5%, making it commercially unviable even with government support.

The Dibang story intersected with larger geopolitical anxieties. China's dam-building spree on the Brahmaputra's upper reaches created pressure to establish "prior use" rights through Indian projects. Military strategists argued that infrastructure in Arunachal Pradesh was essential for border security. Climate negotiators pointed to hydropower as proof of India's renewable energy commitment. Yet on the ground, nothing moved. The data confirms the dam specifications and controversy. If constructed, it will be India's largest dam and the world's tallest concrete gravity dam, standing 288 metres (945 ft) tall. The foundation stone for the dam was laid on 31 January 2008 by Prime Minister Manmohan Singh. Construction on the project, however, has yet to begin. The total cost of the project at November 2007 price level was estimated at 15886.39 crores.

By 2024, the Dibang project exists in a strange limbo. It has all clearances but no construction. NHPC continues to maintain a project office, conduct studies, and negotiate compensation. The Idu Mishmi continue their lives, knowing the dam could start any day. The forests remain uncut, the river flows free, but the threat of submergence hangs over the valley like monsoon clouds.

Myth vs Reality Box:

Myth: Environmental clearances killed the Dibang project.

Reality: The project has all necessary clearances. What's missing is economic viability—with costs exceeding ₹30,000 crores and low IRRs, even NHPC struggles to justify construction. The environmental battles bought time, but economics may deliver the final verdict.

So what for investors: Dibang exemplifies NHPC's capital allocation challenges. The company has sunk costs into projects that may never generate returns, while opportunity costs mount. For investors, it's a reminder that NHPC's project pipeline shouldn't be valued at face value—execution probability must be heavily discounted.

VII. Modern Era: Diversification & Financial Performance (2010s-Present)

The conference room at NHPC's Faridabad headquarters hummed with tension in March 2015. On the screen: solar power tariffs had just hit ₹4.63 per unit in Madhya Pradesh. Around the table: NHPC's senior management stared at their latest hydro project economics—₹5.50 per unit, best case. The writing wasn't just on the wall; it was in neon lights. After four decades as India's hydropower champion, NHPC faced an existential question: What happens to a hydropower monopoly when hydro stops being competitive?

The transformation began quietly. In 2016, NHPC commissioned its first non-hydro project—a 50 MW wind farm in Jaisalmer, Rajasthan. By 2024, the company had added solar projects in multiple states, reaching 262 MW of renewable capacity beyond hydro. The diversification seemed logical—leverage existing transmission infrastructure, utilize vacant land near projects, maintain the renewable energy mandate. But it also represented a profound identity shift for an organization built around the unique challenges of Himalayan dam construction.

Today's numbers tell a sobering story: Market cap of ₹82,148 crores, revenue of ₹10,380 crores, profit of ₹3,412 crores. The margins remain impressive—41.8% net profit margin in FY24 would make most companies envious. But dig deeper and cracks appear. The company has delivered a poor sales growth of 0.73% over past five years. Company has a low return on equity of 9.34% over last 3 years.

The operational challenges have been relentless. In October 2023, a glacial lake outburst flood destroyed NHPC's crown jewel—the 510 MW Teesta-V project in Sikkim. The powerhouse was buried under debris, transforming a cash-generating asset into a write-off overnight. Climate change, ironically, was destroying the very infrastructure meant to combat it. The Himachal Pradesh floods of 2023 damaged multiple projects. Natural disasters that were once-in-a-century events became annual occurrences.

Competition emerged from unexpected quarters. Solar power, once dismissed as expensive and unreliable, achieved grid parity and then kept falling. By 2024, solar-plus-storage costs undercut new hydro projects. State governments, once eager for hydropower development, now preferred faster-to-build solar parks. Private developers, who couldn't match NHPC in dam construction, could easily outcompete in solar execution.

NHPC's response revealed both strengths and limitations. The company leveraged its engineering expertise to enter pumped storage—using excess grid power to pump water uphill, then releasing it during peak demand. Projects like the 1,000 MW Tehri PSP showed promise. But execution remained slow. While private solar developers commissioned projects in 18 months, NHPC's pumped storage projects faced familiar delays—land acquisition, environmental clearances, geological surprises.

The financial engineering became increasingly complex. As of Q3 FY25, the company has an installed capacity of 7,233 MW, including hydro and renewables. It is one of India's largest hydropower producers, with 6,971 MW of hydropower (~15% of the country's total). But capacity didn't translate to growth. Regulated tariffs meant limited pricing power. New projects required massive capital with uncertain returns. The debt-to-equity ratio of 0.8 looked healthy but masked the reality that major expansion would require significant leveraging.

Government support remained strong but complicated. The 2019 decision to classify large hydro as renewable energy opened access to new financing. The push for 500 GW of renewable capacity by 2030 included hydro targets. But political capital for large dams had evaporated. No politician wanted to be associated with displacement and protests. The easier path was ribbon-cutting at solar parks.

The international dimension added complexity. Chinese companies dominated solar manufacturing and were increasingly competitive in international hydro projects. In Nepal and Bhutan, where NHPC once had exclusive relationships, Chinese firms offered better terms. The strategic imperative—maintaining influence in Himalayan water resources—clashed with commercial realities.

NHPC's workforce, 7,000 strong and averaging 45 years old, embodied both institutional knowledge and inertia. Engineers trained in concrete pouring and tunnel boring couldn't easily transition to solar panel installation. The company culture, forged in remote construction sites over decades, struggled with the fast-paced, modular world of renewable energy. The financial data confirms the challenges: NHPC reported a 10% drop in FY24 revenue, down to INR 8,405 crores, primarily due to severe floods causing a 12% decline in power generation. Net profit margins during the year grew from 40.2% in FY23 to 41.8% in FY24, but absolute profits declined.

The 9,314 MW under construction represents hope and burden in equal measure. Projects like Subansiri (2,000 MW), Dibang (3,000 MW), and various joint ventures could transform NHPC's capacity. But each carries execution risks that markets have learned to price in. The company trades at a P/E of around 24x, reasonable for a utility but disappointing for a growth story.

So what for investors: NHPC in the 2020s faces an identity crisis—too slow for renewable energy markets, too controversial for mega-hydro projects. The impressive margins mask stagnant growth and poor capital allocation. Unless the company can dramatically improve execution speed or pivot successfully to pumped storage, it risks becoming a value trap—profitable but shrinking in relevance.

VIII. Playbook: The PSU Model in Power

Step into NHPC's war room during project planning, and you'll witness a ballet of complexity that would make Silicon Valley's "move fast and break things" crowd weep. Here's how India's hydropower monopoly actually makes decisions: First, a state government identifies a river. Then NHPC conducts surveys for 2-3 years. Environmental consultants spend another year on impact assessments. Public hearings happen (or don't, triggering delays). Multiple ministries review. Cabinet approves. Land acquisition begins. Local protests emerge. Courts intervene. Design changes. Cost escalates. A decade passes. Sometimes, concrete gets poured.

This isn't inefficiency—it's the price of building infrastructure in the world's largest democracy. NHPC's playbook, refined over five decades, reveals fundamental truths about how India develops and why it struggles to develop faster.

The Economics: Patient Capital, Uncertain Returns

Hydropower economics are beautifully simple in theory, maddeningly complex in practice. The model: invest ₹5,000-10,000 crores upfront, generate nearly free electricity for 50 years. A 600 MW project might cost ₹6,000 crores to build but generate ₹500 crores in annual revenue at ₹3 per unit—an apparent 8% return before maintenance.

But the devil lurks in the details. Construction takes 8-10 years (optimistically), during which you're paying interest on borrowed capital with no revenue. Geological surprises can double costs overnight. Once operational, you're selling into a regulated market where tariffs are set by commissions balancing consumer interests against your returns. Your 8% return becomes 6%, then 4% as delays mount.

NHPC's solution? The 70:30 debt-equity model, where 70% comes from loans at 8-10% interest, 30% from government equity expecting modest returns. This leverage boosts equity returns when projects work but creates massive losses when they don't. Subansiri's ₹20,000 crore cost against an original budget of ₹6,285 crores shows what happens when the model breaks.

Managing Stakeholder Complexity: The Art of Democratic Infrastructure

Every NHPC project navigates a maze of stakeholders with conflicting interests. The central government wants energy security and GDP growth. State governments want revenue and development but not displacement protests before elections. Local communities want jobs and compensation but not cultural disruption. Environmentalists want rivers protected. Courts want procedures followed. Banks want returns. Each can delay or derail projects.

NHPC's approach evolved from ignoring stakeholders (1970s-1980s) to managing them (1990s-2000s) to attempting genuine engagement (2010s-present). The standard package now includes: 12% free power to host states, 1% of project cost for local area development, jobs for project-affected families, and extensive CSR programs. Yet as Dibang shows, even generous packages can't overcome fundamental opposition.

The real innovation isn't technical—it's procedural. NHPC maintains teams of anthropologists who study local communities. Lawyers who navigate Forest Rights Acts. Liaison officers who drink tea with village headmen. Environmental specialists who count butterflies. This soft infrastructure, invisible in annual reports, determines project success more than engineering excellence.

Regulatory Navigation: Dancing with Multiple Masters

NHPC operates in one of the world's most complex regulatory environments. The Central Electricity Authority approves technical designs. The Ministry of Environment clears ecological impacts. The Ministry of Tribal Affairs protects indigenous rights. State pollution boards issue no-objection certificates. The Central Water Commission manages river flows. Each has veto power.

The company's response resembles a careful dance. Environmental Impact Assessments run to thousands of pages, anticipating every objection. Public hearings are choreographed events where supporters are bused in to counter protesters. When regulations change mid-project—as they frequently do—NHPC absorbs costs and adapts rather than abandoning investments.

Consider the 2019 reclassification of large hydro as renewable energy. NHPC lobbied for this for years, understanding that "renewable" status unlocks financing, regulatory fast-tracks, and purchase obligations. When it finally happened, the company was ready with a pipeline of projects to leverage the change.

Capital Allocation in a PSU: Commercial Logic vs. National Priority

As a listed PSU, NHPC faces an impossible balance. Markets want IRRs above 15%. The government wants strategic projects regardless of returns. The board, with independent directors, has fiduciary duties to all shareholders. The result is capital allocation by committee, where nobody is truly accountable for outcomes.

Take Subansiri—commercially unviable at current costs but strategically important for Northeast development. A private company would walk away. NHPC continues, hoping for government support or tariff revision. The Dibang project sits in limbo, too important to cancel, too expensive to build. Meanwhile, profitable operational plants subsidize these adventures.

The company's dividend policy reflects this tension. With 40%+ margins, NHPC could return massive cash to shareholders. Instead, it maintains modest payouts, preserving capital for projects that may never generate returns. The market prices in this capital destruction, explaining why NHPC trades at discounts despite monopolistic positions.

Trade-offs of the PSU Model: Stability vs. Dynamism

NHPC embodies both the strengths and weaknesses of India's PSU model. Strengths: patient capital for long-gestation projects, ability to pursue strategic objectives, stability of employment and operations, access to government support during crises. Weaknesses: slow decision-making, political interference, limited accountability, inability to exit unviable projects.

The model worked when India needed basic infrastructure and private capital was scarce. Today, with abundant private capital and urgent climate deadlines, its limitations are glaring. NHPC takes a decade to build what Chinese companies construct in three years. Solar developers commission projects while NHPC conducts surveys.

Yet the PSU model offers something private companies can't: legitimacy to operate in sensitive border areas, tribal regions, and ecological hotspots. No private company could have sustained Subansiri through a decade of protests. No private board would approve Dibang knowing its economics. These projects happen (or don't) because NHPC exists in the liminal space between state and market.

Lessons from the Journey

NHPC's playbook teaches hard truths about infrastructure development in democratic societies:

-

Technical excellence isn't enough. NHPC's engineers can build anything, but building requires social license that engineering can't provide.

-

Time value destroys returns. Every year of delay doesn't just add costs; it fundamentally changes project economics as alternatives become cheaper.

-

Stakeholder management is risk management. The community that wasn't consulted becomes the protest that stops construction.

-

Regulatory complexity creates defensive organizations. NHPC optimizes for compliance, not innovation, because one regulatory violation can destroy decades of work.

-

PSUs can't escape political economy. Every project carries political baggage that private companies can avoid but PSUs must bear.

So what for investors: Understanding NHPC's playbook explains both its resilience and limitations. The company will survive—government support ensures that. It will complete projects—eventually. It will generate cash—those 40% margins are real. But it won't generate returns commensurate with risks, won't match market expectations for growth, and won't escape the fundamental contradictions of being a commercial entity with uncommercial obligations. Price accordingly.

IX. Bear vs. Bull Case & Valuation

Picture two investors debating NHPC over coffee in Mumbai's Nariman Point. The bear, a hedge fund analyst, pulls up a chart showing NHPC's stock meandering sideways for five years. The bull, a pension fund manager, counters with NHPC's 40% profit margins. Both are right. Both are missing something. The NHPC investment case isn't about choosing sides—it's about understanding which future you're betting on.

The Bear Case: A Melting Ice Cube in Rising Temperatures

The bear case starts with a simple observation: The company has delivered a poor sales growth of 0.73% over past five years. Company has a low return on equity of 9.34% over last 3 years. In a country growing at 6-7% annually, NHPC is essentially shrinking in real terms.

The core problem is structural. Hydropower's economics are deteriorating against alternatives. Solar-plus-battery costs have fallen 90% in a decade. A 1,000 MW solar park can be built in 18 months for ₹4,000 crores. NHPC's projects take 10+ years and cost ₹10,000+ crores per 1,000 MW. By the time NHPC commissions a project, solar costs have halved again. It's like bringing a sword to a drone fight.

Environmental and social opposition is intensifying, not abating. Every new project faces scrutiny that didn't exist in the 1980s. The Idu Mishmi's resistance to Dibang isn't unique—it's the template. Young, educated tribal populations use social media, international NGOs, and courts effectively. The era of building dams by fiat has ended.

Climate change, paradoxically, threatens hydropower most. Glacial lake outburst floods, like the one that destroyed Teesta-V, will increase. Erratic monsoons mean feast-or-famine water availability. Extreme weather damages infrastructure designed for historical patterns. NHPC's assets are stranded not by regulation but by nature itself.

The talent exodus is accelerating. NHPC's best engineers see better opportunities in renewable energy companies offering stock options and international exposure. The average employee age of 45+ means retirement waves without adequate replacement. Institutional knowledge, painstakingly built over decades, walks out the door daily.

Government support is weakening. The 2019 renewable status for large hydro was likely the last major policy win. Political capital for large dams has evaporated. State governments prefer distributed solar that doesn't displace voters. Even strategic border infrastructure arguments carry less weight when satellites and drones provide surveillance.

The financial metrics are damning. P/E of 24x for a company growing at 0.73% annually makes no sense. The dividend yield of 2-3% doesn't compensate for opportunity costs. The 9.34% ROE in an era of 10% risk-free rates means value destruction. Markets are slowly recognizing this reality.

The Bull Case: The Renewable Grid's Essential Backbone

The bull case begins with energy physics: renewable grids need storage, and pumped hydro remains the cheapest large-scale storage solution. NHPC's existing dams can be retrofitted for pumped storage at fraction of new-build costs. The 10,000 MW pumped storage pipeline could generate ₹15,000 crores in annual revenue at peak-power premiums.

India's power demand will double by 2035. Even with aggressive solar deployment, the grid needs firm capacity for when sun doesn't shine and wind doesn't blow. Hydropower provides instant ramp-up capability that no other source matches. NHPC's 7,000 MW can stabilize a grid with 500,000 MW of intermittent renewables.

The margins tell a story of moat-protected returns. Net profit margins during the year grew from 40.2% in FY23 to 41.8% in FY24. These aren't competitive margins—they're monopoly margins. Once built, hydro projects are cash machines. Baira Siul, commissioned in 1981, still generates ₹100 crores annually with minimal maintenance.

Government backing isn't weakening—it's evolving. The ₹15,000 crore National Infrastructure Pipeline allocation for hydropower, green bonds for renewable projects, and diplomatic pressure for border infrastructure ensure continued support. NHPC's Navratna status provides operational autonomy while maintaining sovereign backing.

The strategic value is irreplaceable. As tensions with China escalate, controlling Himalayan water resources becomes existential. Every NHPC dam is dual-use infrastructure—power generation in peacetime, water weapon during conflict. No private entity can fulfill this role. The government will ensure NHPC's survival and success regardless of commercial logic.

Climate adaptation favors hydropower. While extreme events damage infrastructure, they also increase water availability. Glacial melt, while tragic environmentally, boosts generation for decades. Flood control benefits from dams will be increasingly valued. NHPC's expertise in high-altitude construction becomes more valuable as climate impacts intensify.

The replacement value is astronomical. Building NHPC's 7,000 MW portfolio today would cost ₹200,000+ crores. The market cap of ₹82,000 crores represents a 60% discount to replacement value. Even accounting for operational challenges, this gap is too wide.

Valuation: Between Dreams and Reality

Traditional valuation models struggle with NHPC. DCF analysis depends on project completion timelines nobody can predict. Comparable analysis fails because no true comparables exist—NTPC operates thermal plants, Power Grid transmits rather than generates, private hydro companies are subscale.

Let's attempt a sum-of-parts approach:

Operational assets (7,233 MW): At ₹8 crores per MW (market transactions for operational hydro), worth ₹58,000 crores.

Under-construction projects (9,314 MW): Heavily discounted for execution risk, at ₹3 crores per MW, worth ₹28,000 crores.

Pipeline projects: Given uncertainty, valued at option value only, perhaps ₹5,000 crores.

Total value: ₹91,000 crores against market cap of ₹82,000 crores, suggesting 11% upside.

But this misses the real question: what's the value of optionality on India's energy transition? If pumped storage becomes critical for grid stability, NHPC's sites could be worth multiples of current valuations. If border tensions escalate, strategic value trumps financial metrics. If climate impacts accelerate, flood control benefits alone might justify investments.

Conversely, if solar-plus-battery achieves another 50% cost reduction, if environmental movements gain more power, if talented engineers continue exodus, NHPC could become India's Kodak—a former monopoly made irrelevant by technological change.

The Verdict: A Value Trap or Deep Value?

NHPC represents a peculiar investment proposition: a monopoly that can't grow, a renewable company threatened by renewables, a strategic asset with uncertain strategy. The bear case is compelling tactically—why own a 0.73% grower in a 7% growth economy? The bull case is compelling strategically—who else will build India's water infrastructure?

For growth investors, NHPC is uninvestable. The company won't deliver the 15%+ returns that India's market offers elsewhere. For value investors, it's intriguing but requires patience measured in decades, not quarters. For ESG investors, it's a paradox—renewable energy that destroys ecosystems.

The institutional imperative matters. Pension funds seeking 20-year stable cash flows might find NHPC attractive despite growth limitations. Index funds must own it regardless. Government-related entities will support it for non-financial reasons. Retail investors chasing momentum will be disappointed.

So what for investors: NHPC is priced for modest disappointment but not disaster or delight. At ₹80-90, markets expect continued muddling—some projects completed, some delayed indefinitely, margins maintained, growth absent. Any surprise—successful pumped storage pivot, major project cancellations, government privatization—would trigger rerating. Without surprises, expect continued sideways movement with dividend yields barely beating inflation. For most investors, there are better uses of capital. For those who believe India's water infrastructure is fundamentally undervalued, NHPC offers a flawed but unique exposure. Choose accordingly.

X. Epilogue: The Future of Indian Hydropower

Stand at the Subansiri dam site today, and you'll see India's infrastructure paradox in concrete and steel. The 116-meter wall is complete, turbines are installed, but protests and politics keep the generators silent. It's a ₹20,000 crore monument to the gap between ambition and execution, between what India needs and what its democracy can deliver. As we look toward 2030 and beyond, NHPC's future—and India's hydropower sector—hangs in the balance between compelling necessity and complex reality.

Climate change isn't waiting for India to resolve its infrastructure debates. The Himalayas are warming twice as fast as the global average. Glaciers that feed India's rivers are retreating 10-20 meters annually. By 2050, the Ganges could see 50% reduced flows in dry seasons, 30% increased flows during monsoons. This volatility makes hydropower both more essential (for flood control) and more vulnerable (to extreme weather events).

The China factor looms larger than any domestic consideration. Beijing has built or planned 11 dams on the Brahmaputra, including a 60,000 MW mega-project at the Great Bend that would dwarf anything in India's pipeline. Each Chinese dam affects water availability downstream, creating strategic vulnerability that transcends commercial calculations. NHPC's projects, whatever their economics, become instruments of water sovereignty.

The numbers are stark: 9,314 MW under construction across Subansiri (2,000 MW), Dibang (3,000 MW), and smaller projects in Himachal Pradesh, Uttarakhand, and Kashmir. If completed by 2030—a heroic assumption—they would add 40% to NHPC's capacity. But at current execution rates, 2040 seems more realistic, by which time India's power demand will have doubled, and solar-plus-storage costs will have halved again.

Can NHPC reinvent itself for the renewable age? The company is attempting three pivots simultaneously. First, positioning hydropower as the grid stability solution for intermittent renewables. Second, developing pumped storage projects that use excess solar to pump water uphill, generating during peak demand. Third, expanding into floating solar on its reservoirs, leveraging existing transmission infrastructure.

Each pivot faces obstacles. Grid stability services require market mechanisms that don't yet exist in India's regulated power markets. Pumped storage projects face the same land acquisition and environmental challenges as traditional hydro. Floating solar remains experimental at scale, with questions about impact on reservoir ecology and evaporation rates.

The institutional evolution is equally uncertain. Proposals to split NHPC into separate development and operations entities, to privatize profitable plants while keeping strategic projects under government control, to merge with other power PSUs for scale—all remain in perpetual discussion. Meanwhile, organizational arteriosclerosis advances as experienced engineers retire without adequate succession planning.

Yet dismissing NHPC would be premature. The company has survived and adapted for five decades, outlasting multiple political regimes, economic crises, and technological disruptions. Its deep engineering capabilities, relationships across mountain communities, and understanding of Himalayan geology can't be replicated quickly. If India gets serious about water security—and climate change ensures it must—NHPC's expertise becomes invaluable.

The investment implications depend on timeframe and perspective. Over 1-3 years, expect continued stagnation—projects delayed, growth absent, stock sideways. Over 5-10 years, strategic value might assert itself as water scarcity intensifies and grid stability becomes critical. Over 20+ years, NHPC's dams will still be generating power when today's solar panels need replacement.

Three Scenarios for 2035:

Scenario 1: The Muddle Through (60% probability) NHPC completes 5,000 MW of the 9,314 MW pipeline. Pumped storage provides modest growth. Stock delivers 6-8% annual returns including dividends. The company remains a strategic asset performing tactical operations, neither thriving nor dying.

Scenario 2: The Renaissance (25% probability) Water crisis and grid instability force policy transformation. Pumped storage becomes mandatory, tariffs reflect true value, and NHPC's expertise commands premium. Stock re-rates to 15x earnings on visible growth. Returns exceed 15% annually.

Scenario 3: The Sunset (15% probability) Technological breakthrough makes large hydro obsolete. Environmental movements gain veto power. NHPC becomes stranded asset manager of declining portfolio. Stock trades at liquidation value.

Final Reflections on India's Infrastructure Model

NHPC's story is really India's story—a democracy trying to build infrastructure, a developing nation balancing growth with equity, a civilization managing ancient rivers with modern technology. The tensions are irreducible: development versus environment, national versus local, present needs versus future impacts.

The PSU model that created NHPC may be outdated, but the need it addresses isn't. Someone must build infrastructure with 50-year paybacks in 5-year electoral cycles. Someone must balance competing stakeholder claims in a noisy democracy. Someone must pursue strategic objectives that markets won't finance.

Whether that someone should be NHPC, or whether new models must emerge, remains open. What's certain is that India's water-energy nexus will only grow more critical. The Himalayas will keep melting, monsoons will keep intensifying, and 1.4 billion people will need electricity and flood protection.

For investors, NHPC represents a bet on institutional adaptation—can a 1975-vintage PSU evolve for 2025 challenges? For India, it represents something larger—can democratic societies build infrastructure at the pace climate change demands? The answer will shape not just NHPC's stock price but India's development trajectory.

As you contemplate NHPC's investment case, remember that you're not just evaluating a company but a country's capacity to manage its most precious resource—water—in an era when water becomes more precious daily. The dams NHPC builds, or fails to build, will determine whether India's rivers remain sources of prosperity or become instruments of catastrophe.

The next decade will be decisive. Either NHPC transforms into a modern water-and-energy solutions company, or it becomes a cautionary tale about institutional inertia in times of rapid change. For investors willing to bet on India's ability to reform and adapt, NHPC offers asymmetric upside. For those skeptical of PSU transformation, better opportunities exist elsewhere.

The Subansiri dam will eventually generate power—democracy is slow, not permanently paralyzed. The question is whether it will matter by then, whether NHPC will have evolved beyond dam-building, whether India will have found better answers to its water-energy challenges. These questions don't have answers yet, which is precisely what makes NHPC fascinating and frustrating in equal measure.

So what for investors: NHPC embodies the infrastructure investor's eternal dilemma—assets that society needs aren't always assets that generate returns. The company will muddle through because it must, but muddling through isn't an investment thesis. Unless you believe in strategic revaluation (water crisis forcing policy change) or operational transformation (pumped storage succeeding at scale), NHPC remains a dividend play with option value on India's infrastructure future. In a market offering multiple 15%+ return opportunities, that's a tough sell. But in a world running short of water and stability, it might be exactly what portfolios need. The choice, like democracy itself, is messy, uncertain, and ultimately yours to make.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube