Citigroup: The Rise, Fall, and Resurrection of a Financial Empire

I. Introduction and Episode Roadmap

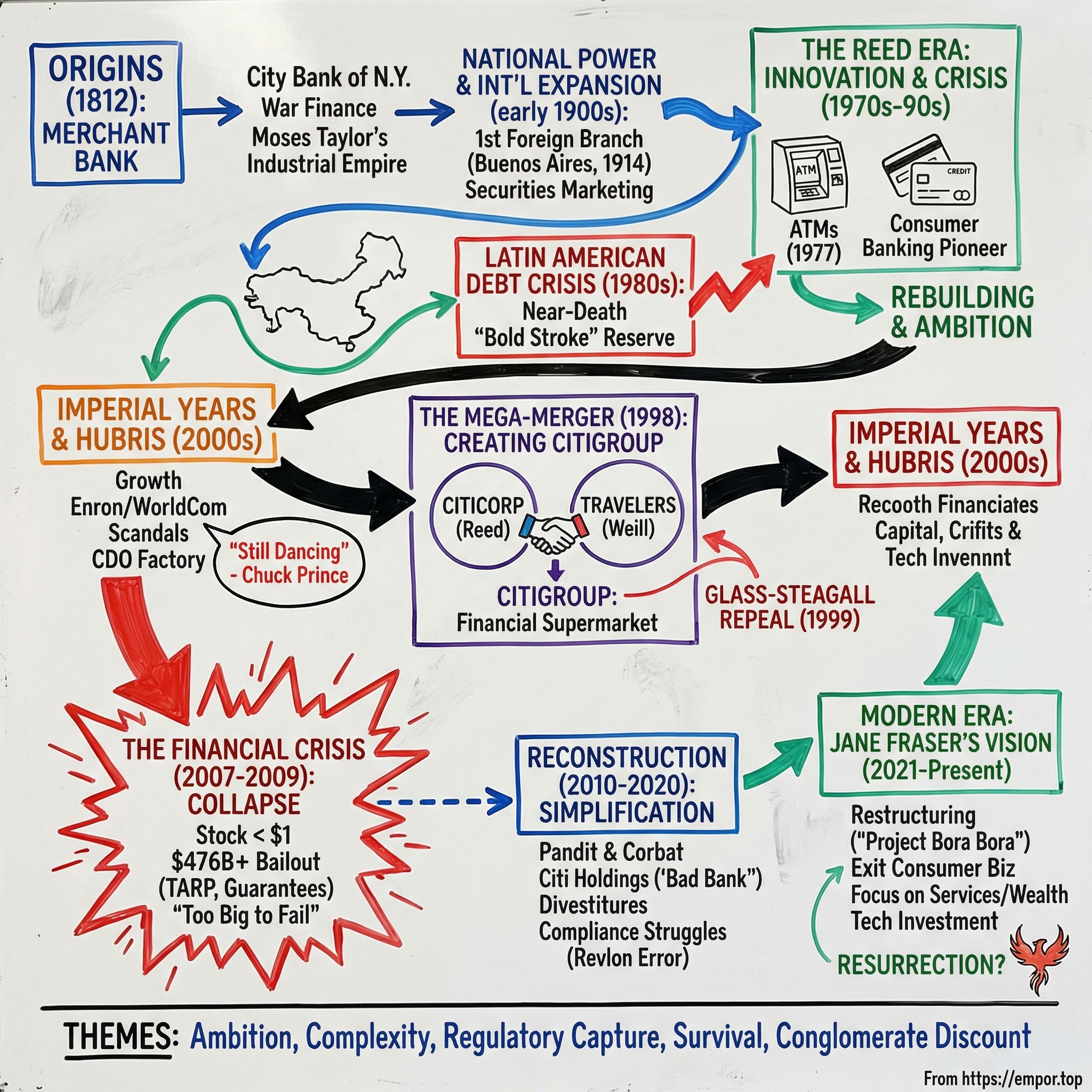

Picture a single institution that has financed wars, survived panics, pioneered consumer banking technology, helped repeal one of America's most important financial laws, nearly collapsed in the worst crisis since the Great Depression, received the largest government bailout in history, and is now in the middle of the most ambitious corporate restructuring in modern banking. That institution is Citigroup.

Founded in 1812 as the City Bank of New York, Citigroup today operates in over 160 countries, employs roughly 227,000 people, and manages trillions of dollars in assets. It is, by any measure, one of the most complex financial organizations ever constructed. And yet for all its scale, Citigroup has spent most of the last two decades trading at or below the value of its own assets, a humbling verdict from the market that this sprawling empire has never quite figured out how to be worth more than the sum of its parts.

The story of Citigroup is not just a banking story. It is the story of American capitalism itself: of ambition unchecked by prudence, of innovation deployed without adequate safeguards, of regulatory frameworks built, dismantled, and rebuilt. It is the story of men and women who believed that bigger was better, that complexity could be managed, and that the rules of gravity somehow did not apply to institutions deemed too important to fail.

How did a nineteenth-century New York merchant bank become too big to fail? And can it now become small enough to succeed?

This deep dive follows the arc from merchant banking origins through empire building to near-death experience and, finally, to the ongoing effort under CEO Jane Fraser to turn what was once the world's most unwieldy financial conglomerate into something leaner, simpler, and actually profitable enough to justify its existence. Along the way, the key themes keep recurring: ambition, complexity, regulatory capture, and survival. The question, even now, remains whether Citigroup can finally break the cycle.

II. Origins: From Merchant Bank to National Power (1812–1960s)

On the morning of September 14, 1812, in a modest office at 52 Wall Street, a new bank opened its doors in lower Manhattan. The United States had declared war on Great Britain just three months earlier. New York's financial community was reeling from Congress's refusal, the previous year, to renew the charter of the First Bank of the United States. Into this vacuum stepped a group of New York merchants who saw both a civic need and a business opportunity.

The City Bank of New York was chartered by the State of New York on June 16, 1812, with two million dollars in authorized capital. Its first president was Colonel Samuel Osgood, one of the most distinguished public servants of the early republic. Osgood had served as a colonel in the Revolutionary War, sat in the Continental Congress, and held the distinction of being the nation's first Postmaster General under the Constitution. His home at 1 Cherry Street in lower Manhattan had served as George Washington's first presidential mansion. But Osgood would not live to see what his bank would become. He died less than a year after the bank's founding, on August 12, 1813.

In its earliest years, City Bank served as a conservative merchant bank, making collateralized loans and accepting deposits from New York's trading houses. The bank's founding capital of two million dollars came primarily from local merchant subscriptions, with ownership concentrated among New York's trading houses. It financed war bonds for the War of 1812, a fortuitous timing given that the war had been declared just days before the bank's charter was granted. Over the next several decades, it survived the periodic financial panics that swept through the young republic, building a reputation for conservative management and reliable liquidity.

But the bank's first true transformation came under a figure who would turn it into something altogether more powerful and personal.

Moses Taylor was born in 1806, the son of a close associate of John Jacob Astor. At fifteen, he began working at a shipping firm. When the Panic of 1837 devastated New York's banking system, Astor maneuvered Taylor onto City Bank's board. By 1856, Taylor was president, a position he held until his death twenty-six years later. Under Taylor, City Bank became something unusual in American finance: a personal banking empire disguised as a commercial institution.

Taylor's method was elegant and ruthless. Every company in his vast industrial network, from railroads to coal mines to import firms, was required to keep its principal account with City Bank. This gave Taylor real-time visibility into the financial health of every enterprise he touched. He was not just a banker; he was an intelligence operation unto himself.

When the Panic of 1857 brought the Delaware, Lackawanna and Western Railroad to the brink of bankruptcy, Taylor scooped up shares at five dollars apiece. Within seven years, those shares were worth two hundred and forty dollars, a return of nearly five thousand percent. At his death in 1882, Taylor's estate was valued at seventy million dollars, making him one of the wealthiest Americans of the nineteenth century. The Pyne family, descendants of Taylor through his daughter Albertina, continued the banking dynasty for generations afterward.

The bank's next great leap came under James Stillman, who took the presidency in the 1890s and transformed City Bank from a personal vehicle into a truly national institution. In 1865, the bank had converted to a national charter, becoming the National City Bank of New York. Under Stillman, it grew through acquisition, purchasing the Third National Bank of New York in 1897 and becoming America's largest bank by 1900 with one hundred and fifty million dollars in assets. Stillman also hired Frank Vanderlip, a former Assistant Secretary of the Treasury, who would push the bank onto the world stage.

Because U.S. national banks were legally prohibited from operating overseas, National City Bank worked through the International Banking Corporation, a separately chartered entity that opened offices in London, Shanghai, and Calcutta between 1901 and 1902. When the Federal Reserve Act of 1913 finally allowed national banks to establish foreign branches, Vanderlip moved immediately. In October 1914, National City Bank opened its first international branch in Buenos Aires, the first foreign branch of any nationally chartered American bank. It was almost immediately profitable, thanks to the foreign exchange business created by World War I's disruption of European banking.

From 1914 to 1916, Vanderlip established branches around the world and created the American International Corporation, a foreign investment trust. The DNA of international ambition, the belief that a New York bank could and should operate everywhere, was established here. It would define the institution for the next century, for better and for worse.

The early twentieth century brought yet another chapter. Under Charles Mitchell in the 1920s, National City Bank became one of the first American banks to aggressively market securities to retail investors, selling bonds to ordinary Americans in what was, for the era, a revolutionary innovation in financial distribution. When the stock market crashed in 1929 and the Great Depression followed, it emerged that many of these securities had been of dubious quality. Mitchell was indicted for tax evasion and became a public symbol of Wall Street excess. The bank survived the Depression, but the episode led directly to the Glass-Steagall Act of 1933, which separated commercial banking from securities dealing. It was a law that would shape American finance for sixty-six years and would one day be repealed at the direct behest of City Bank's corporate descendants.

Through the mid-twentieth century, the bank continued to grow, expanding its international footprint under leaders like James Perkins and Howard Sheperd. By the 1960s, it was one of the largest and most international banks in the world, with a presence in dozens of countries and a reputation for innovation that attracted the brightest young talent on Wall Street.

In 1974, the holding company was renamed Citicorp, and in 1976 the banking business took the name Citibank. By that point, the institution that had started with Colonel Osgood and two million dollars in capital had already survived the Civil War, the panics of 1857, 1873, 1893, and 1907, two World Wars, and the Great Depression. What it had not yet survived was the ambition of its own leaders. That was about to change.

III. The John Reed Era: Innovation and Near-Death (1970s–1998)

John Shepard Reed grew up not in the boardrooms of New York but on the streets of Buenos Aires. His father worked for Armour and Company, the meatpacking giant, and the family lived in Argentina from the time Reed was five until he was seventeen. He returned to the United States for college, earning an undergraduate degree through a combined program between Washington and Jefferson College and MIT, followed by a master's in management from MIT's Sloan School. After two years in the Army, Reed joined Citibank in 1965 as a twenty-six-year-old analyst.

His first major assignment was prophetic. The bank's president handed him a report on the future of the financial industry and asked him to figure out what computers might mean for banking. Reed took a year to study the question, returned to MIT to consult with faculty, and visited equipment manufacturers. He concluded that online, interactive systems, similar to the airline reservation systems then being developed, would transform the business. This was not a popular view in 1966.

Reed spent the next decade building Citibank's consumer banking operation from near-scratch. In the late 1970s, he made a bet that would define the modern banking experience. The first automated teller machine appeared at a Citibank branch in Queens in 1977. By the end of that year, there were two at every branch in New York, one as backup, ensuring customers could access their money twenty-four hours a day, seven days a week. The investment cost hundreds of millions of dollars, and Citibank's consumer banking division lost money for years before the strategy paid off. Most bankers thought Reed was insane. Customers were accustomed to human tellers; why would they trust a machine with their money?

But Reed understood something his peers missed. Banking was not about relationships with tellers. It was about access to money. And a machine that never slept, never took a lunch break, and never had a bad day was a better delivery system than any human could be. The ATM network became the foundation of Citibank's consumer franchise. During the blizzard of 1978, when New York's bank branches were shuttered for days, Citibank's ATMs kept working. Usage surged, and consumer resistance to the machines evaporated almost overnight. Reed later described it as the moment he knew the bet would pay off.

Reed also built what would become the largest credit card operation in the world. Working with colleague Dave Phillips, he launched a massive direct mail campaign using credit scoring and credit checks to acquire customers nationwide. Within eighteen months, Citibank had built the biggest direct mail credit card operation in the country. By the 1980s, Citibank was the largest issuer of credit and charge cards in the world. In September 1984, at age forty-five, Reed was named Chairman and CEO of Citicorp.

Reed's approach to technology was not just operational; it was philosophical. He believed that banking was fundamentally an information business, and that the institution that could process information fastest and most efficiently would win. This insight, seemingly obvious in retrospect, was radical in the 1970s. Most bankers still thought of their business as being about relationships and judgment. Reed thought it was about systems and data. He was decades ahead of his time, and his investments in technology infrastructure would give Citibank a competitive advantage that lasted well into the 1990s.

Then the developing world nearly destroyed him.

Throughout the 1970s, Citicorp and other major American banks had aggressively lent to Latin American governments, recycling petrodollars from oil-producing nations into sovereign loans. Latin American debt to commercial banks quadrupled from seventy-five billion dollars in 1975 to more than three hundred and fifteen billion by 1983, representing half the region's GDP. It was the financial equivalent of a ticking bomb, and no institution was more exposed than Citicorp.

In August 1982, Mexico declared it could no longer service its foreign debt, triggering a cascade of similar declarations across the region. The crisis dragged on for years, with banks engaging in what the industry euphemistically called "extend and pretend," rolling over loans rather than acknowledging they would never be repaid in full. Regulators, terrified that acknowledging the true scale of losses would render the entire banking system technically insolvent, actually weakened regulatory standards for large banks exposed to developing-country debt.

In May 1987, nearly five years into the crisis, Reed made a dramatic move. Citicorp announced it was establishing a three-point-three-billion-dollar loan loss reserve, representing more than thirty percent of its total exposure to developing countries. It was the first major acknowledgment by a top American bank that these loans would never be fully repaid. Fortune magazine put Reed on its cover under the headline "John Reed's Bold Stroke." Other major banks were forced to follow suit almost immediately. The Brady Plan of 1989 eventually provided a framework for resolution, with private lenders forgiving sixty-one billion dollars in loans. Citicorp survived, but just barely.

And then, almost immediately, it nearly died again.

In the late 1980s, Citicorp had underwritten billions in commercial real estate loans and leveraged buyout financing. When the American economy slammed into recession in 1990, those loans went bad. The bank's stock sank to just over nine dollars per share, and there was widespread concern that Citibank might actually fail. An August 1991 article in Financial World ran under the headline "Too Big to Fail," a phrase that would follow the institution for the next three decades.

The rescue came from an unlikely source. In late 1990, Saudi Prince Alwaleed bin Talal quietly purchased 4.9 percent of Citicorp's shares for two hundred and seven million dollars. In January 1991, he agreed to invest an additional five hundred and ninety million dollars in convertible securities. His total investment of nearly eight hundred million dollars, combined with a second capital raise of six hundred million from institutional investors, gave Citicorp the roughly 1.4 billion dollars it needed to survive. Alwaleed's thesis was simple: the bank was too big to fail, and its global brand made it a compelling investment. He was spectacularly right.

Reed spent the mid-1990s rebuilding. He cut costs aggressively, recapitalized the balance sheet, and expanded globally. By the late 1990s, Citicorp was once again one of the most profitable banks in America. Reed had survived two near-death experiences and was dreaming bigger than ever. He wanted to build the ultimate universal bank, combining commercial banking, investment banking, insurance, and consumer finance under a single roof. The only problem was that American law made that dream illegal.

He needed a partner with the same ambition and zero patience for legal obstacles. He found one in Sandy Weill.

IV. The Sandy Weill Saga: Empire Builder (1960s–1998)

Sandy Weill's story begins about as far from Wall Street's gilded corridors as you can get while still being in New York. Born on March 16, 1933, in Brooklyn to Polish Jewish immigrants, Weill was the first in his family to earn a college degree, graduating from Cornell University in 1955. After graduation, he took a job as a runner at Bear Stearns, essentially a messenger carrying documents between offices, earning thirty-five dollars a week. He worked his way up to stockbroker, and by 1960, at twenty-seven, he was ready to build something of his own.

Weill co-founded Carter, Berlind, Potoma and Weill, a small brokerage firm, in 1960. Over the next two decades, he did something no one else on Wall Street had the patience or stomach for: he built a major securities firm through serial acquisition. More than fifteen deals over twenty years, each one adding capabilities, clients, and scale.

The firm's name kept changing as it absorbed competitors, a running joke on the Street that each new acquisition brought a new name. It became CBWL-Hayden Stone in 1970, Hayden Stone in 1972, Shearson Hammill in 1974 after a merger, and finally Shearson Loeb Rhoades in 1979. By the early 1980s, it was the country's second-largest brokerage. Weill had built it deal by deal, often targeting distressed or undermanaged firms where his cost-cutting abilities could unlock immediate profit improvement.

Weill's management philosophy was brutally simple: cut costs, motivate employees, cross-sell everything, and maintain absolute control. He was famous for personally reviewing expense reports, for knowing the profitability of individual branches, and for an operational intensity that bordered on the obsessive. He was not a strategist in the grand sense. He was an operator, perhaps the best operator Wall Street has ever produced.

In 1981, Weill sold Shearson Loeb Rhoades to American Express for approximately nine hundred and fifteen million dollars in stock. The deal made him wealthy but unhappy. He was named president of American Express in 1983, but the job was hollow. The real power belonged to CEO James Robinson III, and Weill knew he would never get the top seat. In August 1985, at fifty-two, he resigned. Robinson immediately replaced him with Louis V. Gerstner Jr., who would later go on to famously turn around IBM. For Weill, it was a humiliation.

What followed was one of the great comeback stories in American business history. Weill spent a year in the wilderness, depressed and directionless. Friends described him pacing his apartment, unable to sit still. He was a builder without a building, an empire-maker without an empire. His wife Joan reportedly told him he needed to find something to do before he drove everyone around him crazy.

After a failed bid to become CEO of Bank of America, where he was nominated and vetted by the board only to be rejected at the final stage, Weill found his vehicle in an unlikely place: a struggling subsidiary of Control Data Corporation in Minneapolis called Commercial Credit Company, based in Baltimore. In September 1986, Weill negotiated a deal to spin off Commercial Credit. Control Data sold eighty-two percent to the public at twenty dollars and fifty cents per share, while Weill and other executives bought ten percent. Weill personally invested seven million dollars. The subsidiary had been aimlessly diversified into money-losing ventures in Israeli leasing and Latin American loans. Under Weill's leadership, the new management cut non-core businesses and tripled operating profits within a year.

From this tiny base in Baltimore, far from the power centers of Wall Street, Weill began rebuilding his empire with the methodical precision of a chess grandmaster. Each move was designed to add scale, diversify revenue, and position the company for the next, larger deal.

In 1988, he merged Commercial Credit with the larger but struggling Primerica, acquiring securities firm Smith Barney in the process. In 1993, he reacquired his old Shearson brokerage from American Express for 1.2 billion dollars, a deeply satisfying full-circle moment. That same year, he completed a four-billion-dollar stock deal to take over Travelers Corporation, renaming the entire enterprise Travelers Group.

Then, in September 1997, Weill made the move that would set the stage for everything that followed. He acquired Salomon Inc., the parent of the legendary Salomon Brothers, for over nine billion dollars in stock, merging it with Smith Barney to create Salomon Smith Barney. In a single stroke, Weill had added world-class investment banking and trading capabilities to his insurance, brokerage, and consumer finance operation. Travelers Group was now a full-spectrum financial powerhouse.

But Weill wanted more. He wanted it all: commercial banking, investment banking, insurance, consumer finance, global reach. He wanted to build the biggest financial institution the world had ever seen. There was just one problem. American law, specifically the Glass-Steagall Act of 1933, made it illegal to combine commercial banking with securities and insurance businesses. The law had stood for sixty-five years, erected in the aftermath of the Great Depression specifically to prevent the kind of institution Weill wanted to create.

Most people would have seen Glass-Steagall as an insurmountable obstacle. Weill saw it as a starting point for negotiation.

V. The Mega-Merger: Creating Citigroup (1998–2000)

One spring evening in 1998, John Reed sat down to dinner with Sandy Weill at Travelers Group's conference center in Armonk, a quiet hamlet in Westchester County, New York. Both men were in their early sixties. Both had spent their careers building financial empires. And both believed that the future of finance belonged to whoever could combine every financial service, commercial banking, investment banking, insurance, consumer credit, into a single institution.

The subject of their conversation was a merger that would create the largest financial services company on Earth.

What happened next was remarkable even by Wall Street standards. Reed and Weill put the merger together in just five weeks, without investment bankers. No Goldman Sachs advisory team. No Morgan Stanley fairness opinions. Two CEOs and their respective teams, working out the terms over breakfasts and dinners. They agreed on fifty-fifty ownership between Citicorp and Travelers shareholders, an eighteen-member board of directors, and a new name that combined both legacies: Citigroup.

On April 6, 1998, they announced what was then the biggest merger in history. The deal was valued at roughly seventy-six billion dollars, though the combined entity's market capitalization approached one hundred and forty billion, depending on the valuation methodology. The new company would marry Citicorp's global commercial banking franchise, with operations in over one hundred countries, to Travelers' insurance, brokerage, and consumer finance operations.

The market reaction was euphoric. Both stocks surged. Analysts tripped over themselves to praise the vision. The Dow Jones Industrial Average rose two hundred points. The prevailing view was that the financial supermarket had arrived and that any institution not pursuing a similar strategy was destined for irrelevance.

There was just one rather significant problem. The merger was flatly illegal.

The Glass-Steagall Act of 1933 and the Bank Holding Company Act prohibited exactly this kind of combination of commercial banking, securities, and insurance businesses under one corporate roof. Reed and Weill were betting, explicitly and publicly, that they could force a change in the law before a two-year regulatory forbearance expired. It was an audacious gambit: announce a merger that violates existing law, then spend the next two years lobbying to change the law.

The lobbying campaign was massive. During the 1997-1998 congressional session, banks, securities firms, and insurance companies contributed more than eighty-five million dollars in campaign donations to both parties. The Citicorp-Travelers merger made the issue impossible for Congress to ignore. Here was the largest financial merger in history, openly operating in violation of existing law, daring regulators and legislators to either shut it down or get out of the way.

The political dynamics were fascinating. Treasury Secretary Robert Rubin, a former Goldman Sachs co-chairman, was broadly supportive of financial modernization. Federal Reserve Chairman Alan Greenspan had long advocated for removing Glass-Steagall restrictions. The banking industry framed the issue as one of American competitiveness: European and Japanese banks could already offer the full range of financial services, and American banks needed the same flexibility to compete globally. Critics, including a small but vocal group of consumer advocates and congressional Democrats, warned that combining commercial banking with speculative trading would create institutions too large and too risky to manage.

They were outvoted decisively. The Gramm-Leach-Bliley Act, officially titled the Financial Services Modernization Act of 1999, was introduced by Senator Phil Gramm of Texas in the Senate and Representatives Jim Leach and Thomas Bliley in the House. The final vote was overwhelming: ninety to eight in the Senate, three hundred and sixty-two to fifty-seven in the House. President Bill Clinton signed it into law on November 12, 1999, formally repealing the barriers that had separated commercial banking from securities and insurance for sixty-six years. Rubin, notably, left the Treasury in July 1999 and joined Citigroup's board in October, a revolving door that would draw significant criticism in the years that followed.

But the merger had a structural flaw that no amount of lobbying could fix: the co-CEO arrangement.

Reed was the cerebral technologist, the MIT-trained systems thinker who had pioneered ATMs and credit cards. Weill was the Brooklyn-born dealmaker, the former Wall Street messenger who had built and rebuilt financial empires through sheer operational intensity. Their management styles, their visions for the company, and their fundamental beliefs about what Citigroup should become were incompatible. Reed saw the future in technology and global consumer banking. Weill saw it in acquisitions, cost-cutting, and cross-selling.

The power struggle was swift and brutal. Reed was effectively sidelined when Weill was given responsibility for most of Citigroup's operating divisions, while Reed was put in charge of the company's Internet strategy, a prestigious-sounding but operationally meaningless assignment. The board battle lasted eight hours. A key vote in Weill's favor was allegedly delivered by board member Mike Armstrong, CEO of AT&T, which Salomon Smith Barney analyst Jack Grubman had recently upgraded to a buy rating, some suspected at Weill's request.

Reed's departure was announced in a February 28, 2000, press release. He formally retired on April 18, 2000, leaving Sandy Weill as the sole Chairman and CEO of the world's largest financial services company. In subsequent years, Reed would express deep regret about the merger, acknowledging that Citigroup had become too large and complex to manage effectively. The financial supermarket model that both men had believed in was about to be tested by reality.

The question was whether anyone could actually run an institution this vast, this complex, and this sprawling. The answer, it turned out, was no. But before the market would render its verdict, Citigroup would enjoy a brief but intoxicating period of imperial glory, the illusion of omnipotence that comes with being the biggest player in the biggest game.

VI. The Imperial Years: Growth and Hubris (2000–2007)

With Reed gone, Sandy Weill ran Citigroup the way he had always run things: through deals, cost discipline, and force of personality. The early 2000s were Citigroup's imperial years, a period of aggressive global expansion and deepening market dominance. The financial supermarket was open for business, offering everything from savings accounts to mortgage-backed securities, from life insurance to emerging market debt, all under the same corporate umbrella.

But the empire had cracks, and they appeared almost immediately.

The first major scandal involved Enron. Citigroup had assisted the energy company in disguising billions of dollars in debt through complex structured transactions known as prepays. In these arrangements, Enron was paid upfront to deliver commodities at a later date, but the economic substance was that of a loan. Citigroup structured prepay contracts with Enron totaling 3.8 billion dollars. In one scheme, Enron transferred assets to a sham joint-venture called Fishtail, which used a two-hundred-million-dollar loan from Citigroup, guaranteed by Enron, to buy them back. The effect was to allow Enron to report loan proceeds as operating cash flow, deceiving investors about its true financial condition.

Then came WorldCom. Citigroup's subsidiary Salomon Smith Barney was deeply entangled through analyst Jack Grubman, who had relentlessly promoted WorldCom stock even as the company was engaging in what would become the largest accounting fraud in American history, estimated at eleven billion dollars. Grubman went so far as to script what CEO Bernie Ebbers said on analyst conference calls. Citigroup also lent sixty-three million dollars to Ebbers personally and allocated lucrative IPO shares to him, a practice known as spinning.

The Grubman story had a lurid subplot that captured the absurdity of the era. Grubman wanted to get his twin children into the exclusive 92nd Street Y preschool in Manhattan. In a memo titled "AT&T and the 92nd Street Y," he reminded Weill of productive meetings with AT&T executives while noting the "ridiculous but necessary process of preschool applications in Manhattan." Weill proposed a one-million-dollar donation to the school if Grubman's children were admitted. The school was receptive, and Grubman became more receptive to AT&T's business model, upgrading the stock from neutral to buy. The entire episode was a microcosm of the conflicts of interest that permeated Wall Street in the early 2000s.

The penalties were staggering. Citigroup paid two billion dollars to settle claims from Enron investors and 2.65 billion dollars to settle the WorldCom investor lawsuit. Grubman was fined fifteen million dollars and permanently banned from the securities industry. Citigroup paid an additional four hundred million dollars to regulators over analyst conflicts of interest.

Beyond the financial penalties, the scandals revealed something deeply troubling about Citigroup's culture. The institution had become so large, so decentralized, and so focused on revenue generation that ethical guardrails had eroded across multiple business lines simultaneously. It was not a case of one rogue employee or one bad department. It was systemic. And it would only get worse.

In October 2003, Weill stepped down as CEO, though he remained chairman. His successor was Chuck Prince, a lawyer by training who had served as Weill's personal counsel and consigliere for decades. Prince was an unusual choice for the top job at the world's largest financial institution. He was not a banker. He was not a trader. He was a lawyer who had risen through the ranks by solving Sandy Weill's problems. The market viewed his appointment with skepticism, and Prince knew it.

What Prince inherited was a machine that had been optimized for growth at any cost. Citigroup's structured products operation was churning out collateralized debt obligations and mortgage-backed securities at an extraordinary pace. To understand what went wrong, it helps to understand what a CDO actually is. Think of it as a financial factory: a bank takes thousands of individual mortgages, bundles them together, and then slices the bundle into layers, like floors of a building. The top floor gets paid first and is therefore safest; the bottom floor absorbs losses first and is riskiest. Rating agencies blessed the top floors with triple-A ratings, the same grade as U.S. Treasury bonds, which allowed pension funds and insurance companies to buy them. The problem was that the underlying mortgages were increasingly being made to borrowers who could not afford them, the so-called subprime loans. When home prices stopped rising and borrowers defaulted, the entire structure collapsed from the bottom up.

Citigroup was not just manufacturing these products for sale to outside investors. It was holding enormous quantities on its own balance sheet and in off-balance-sheet vehicles called structured investment vehicles, or SIVs. Risk management was decentralized, underfunded, and increasingly ignored.

Then, on July 9, 2007, Prince gave an interview to the Financial Times in Japan that would become the single most infamous utterance of the financial crisis era. Asked about the booming leveraged lending market and whether the credit cycle was nearing a turn, Prince said: "When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

He went on to add that the depth of the pools of liquidity was so much larger than it used to be that a disruptive event would need to be much more disruptive than it used to be. It was a statement that acknowledged the risk, acknowledged the absurdity, and then declared that competitive pressures made it impossible to stop. It was the sound of a CEO admitting that his institution was riding a wave he could not control.

Less than four months later, on November 4, 2007, Prince resigned after Citigroup disclosed massive losses on CDOs and mortgage-backed securities. He received a thirty-eight-million-dollar departure package. The music had stopped, and Citigroup was about to discover just how bad things really were.

VII. The Financial Crisis: Too Big to Fail (2007–2009)

The unraveling happened with a speed that stunned even the pessimists. On January 15, 2008, Citigroup announced fourth-quarter write-downs of 17.4 billion dollars on subprime-related exposures and a net loss of 9.83 billion dollars for the quarter. Full-year 2007 subprime losses reached 18.3 billion dollars pretax. In December 2007, the bank had already taken fifty-nine billion dollars in assets from its structured investment vehicles onto its balance sheet.

The new CEO, Vikram Pandit, had arrived in December 2007 under unusual circumstances. Pandit had spent two decades at Morgan Stanley, rising to president of the institutional securities business, before leaving in 2005 after being passed over for the top job. In 2006, he co-founded a hedge fund called Old Lane. In 2007, Citigroup purchased Old Lane for eight hundred million dollars, bringing Pandit into the firm. The fund was subsequently shut down, making the acquisition price one of the more dubious deals of the era. Pandit personally received one hundred and sixty-five million dollars from the sale. He was then named CEO of Citigroup just as the worst financial crisis since the Great Depression was accelerating.

Pandit inherited a balance sheet that was essentially a weapon of self-destruction. Cumulative CDO and subprime write-downs reached 46.8 billion dollars by November 2008. Among American firms, only Merrill Lynch reported comparable losses. But Merrill could be acquired by Bank of America. Citigroup was too large, too complex, and too interconnected to be absorbed by anyone. It could only be saved by the government.

The stock price collapse was breathtaking in both speed and scale. In 2006, Citigroup's market capitalization had been approximately two hundred and fifty billion dollars, making it the most valuable financial institution on the planet. The stock had traded above fifty-five dollars per share. By November 12, 2008, it hit single digits for the first time since 1996. During the week of November 17 through 21, one of the most harrowing weeks in financial history, the stock lost sixty percent of its value. Customers began withdrawing deposits. Counterparties started pulling credit lines. The interbank lending market, where banks lend to each other overnight, essentially froze. Market capitalization fell to 20.5 billion dollars, a loss of eighty-seven percent for the year. By March 2009, shares traded at ninety-nine cents.

Think about that number for a moment. Citigroup, the institution that had been America's largest bank for much of the twentieth century, the bank that had pioneered international banking, ATMs, and credit cards, the company that Sandy Weill and John Reed had merged into the world's largest financial conglomerate, was trading for less than a dollar a share. The entire company was worth less than what Prince Alwaleed had invested in it during the 1991 crisis.

The government rescue came in waves, each one larger and more desperate than the last.

On October 28, 2008, the Treasury used twenty-five billion dollars from the Troubled Asset Relief Program to buy preferred shares of Citigroup. It was the same amount given to JPMorgan and Bank of America, and the intention was to signal confidence. But for Citigroup, it was not enough.

After the stock collapsed further in November, a second emergency rescue was announced on November 23: an additional twenty billion dollars in TARP capital, plus a government guarantee limiting losses on three hundred and six billion dollars in risky loans and securities. Under the guarantee, Citigroup would absorb the first twenty-nine billion in losses plus ten percent of remaining losses; the government would backstop the rest. According to the Congressional Oversight Panel, Citigroup received a grand total of 476.2 billion dollars in cash and guarantees, an almost incomprehensible sum that exceeded the GDP of most countries.

Pandit managed the crisis with a combination of public contrition and structural overhaul. In November 2008, he announced plans to cut fifty-two thousand jobs, one in seven employees, the most dramatic layoff in American banking history. He declared his salary should be one dollar per year with no bonus until the company returned to profitability, a gesture that resonated with the public even if it did little to change the economics.

In January 2009, he announced the creation of two separate operating units: Citicorp, the good bank containing core businesses, and Citi Holdings, the bad bank containing toxic assets and non-core operations to be divested. The concept was simple but important: by separating the healthy businesses from the toxic ones, investors and regulators could track the runoff of bad assets separately from the performance of the core franchise. It was an acknowledgment that the financial supermarket had failed and that the only path forward was to start taking it apart.

On February 27, 2009, the Treasury converted twenty-five billion dollars of its preferred stock into Citigroup common stock, giving the U.S. government approximately 33.6 percent ownership of Citigroup. The United States government was now the single largest shareholder of one of America's most storied financial institutions.

The recovery, when it came, was slow but ultimately profitable for taxpayers. At the end of 2009, Citigroup raised 20.5 billion dollars in public equity to repay the twenty billion in preferred securities, and the asset guarantee was canceled. Through 2010, the Treasury sold its common shares at an average price of $4.14 per share. In May 2011, Citigroup executed a one-for-ten reverse stock split to bring its share price from roughly four dollars to approximately forty dollars. By the time all was said and done, the Treasury had received more than 58.4 billion dollars in total repayments and income on its forty-five-billion-dollar investment, a net profit for taxpayers of approximately 13.4 billion dollars.

The government made money. Citigroup survived. But the damage to the institution's reputation, its culture, and its competitive position would take far longer to repair than any balance sheet.

The financial crisis exposed the fundamental flaw in the Citigroup model. The institution that Sandy Weill had built was designed for growth, not resilience. Its complexity, which had once been marketed as a competitive advantage, had turned it into a machine that nobody fully understood, not its management, not its board, not its regulators, and certainly not its shareholders. The question now was whether the wreckage could be reassembled into something that actually worked.

VIII. The Reconstruction: Simplification and Survival (2010–2020)

Vikram Pandit's tenure ended abruptly on October 16, 2012. While officially characterized as a resignation, reports indicated that Pandit was forced out by the board after eroding investor confidence and damaging the company's relationships with regulators. His replacement was Michael Corbat, a lifelong Citigroup employee who had spent the previous three years running the single hardest job in American banking: CEO of Citi Holdings, the toxic-asset dumping ground.

Corbat was born in Bristol, Connecticut, graduated from Harvard in 1983 where he played offensive guard on the football team, and joined Salomon Brothers in fixed-income sales immediately after college. He had spent his entire career at Citigroup or its predecessors, which gave him both deep institutional knowledge and a clear-eyed view of just how broken the organization was.

At Citi Holdings, Corbat had overseen the divestiture of more than forty businesses and more than five hundred billion dollars in assets. The experience shaped his philosophy as CEO. His mantra for Citigroup was four words: simpler, smaller, safer, stronger. It was, by design, the opposite of everything Sandy Weill had stood for.

The Corbat era was defined by subtraction rather than addition. Over his nine-year tenure, he divested more than seventy non-core businesses and reduced total assets from roughly 1.9 trillion to about 1.8 trillion dollars. He sold Smith Barney to Morgan Stanley, completing a transaction that had begun under Pandit. He unwound consumer banking operations in countries where Citigroup lacked the scale to compete. He sold Citi's stake in the Mexican toll road operator and exited dozens of other peripheral investments. In April 2016, Citigroup announced the elimination of Citi Holdings entirely, as the bad bank had been wound down to a negligible size. The financial supermarket was being dismantled, aisle by aisle.

But simplification proved to be a much harder task than anyone anticipated. Citigroup's technology infrastructure was a geological record of decades of acquisitions: hundreds of systems, many of them incompatible, layered on top of each other like sedimentary rock. A single customer transaction might pass through a dozen different legacy platforms, each originally built for a different acquired company, each with its own data formats and processing rules.

Risk management was decentralized and inconsistent. Different business units measured risk differently, reported it differently, and aggregated it differently. Data governance was so poor that the bank often could not tell regulators basic things about its own operations with any confidence. When regulators asked simple questions like "how much do you have in total exposure to a particular counterparty?", the answer sometimes took weeks to assemble because the data lived in so many different systems.

In October 2020, both the Office of the Comptroller of the Currency and the Federal Reserve issued consent orders over deficiencies in Citigroup's risk management, data governance, and internal controls. The consent orders were triggered in part by the most embarrassing operational failure in modern banking history.

On August 11, 2020, while processing a routine 7.8-million-dollar interest payment on Revlon's 2016 loan, a Citibank employee accidentally wired 894 million dollars to Revlon's lenders, the full outstanding principal, three years early. The error was a consequence of an antiquated software system that required manual workarounds for routine transactions. Several lenders refused to return the money, leading to a legal battle that went all the way to the Second Circuit Court of Appeals before being resolved in Citigroup's favor in September 2022. The case became a landmark in banking operations and prompted industry-wide reviews of wire transfer controls.

The consent orders, the wire error, and persistent struggles with compliance and technology investment made it clear that Corbat's simplification, while necessary, had not gone far enough. The bank was still too complex, its returns were still inadequate, and its operational infrastructure was still unreliable. When Corbat announced his retirement in September 2020, effective February 2021, the question was whether his successor could do what he had not: fundamentally transform Citigroup from the inside out.

Throughout this decade, Citigroup's competitive position deteriorated relative to its peers. JPMorgan Chase, under Jamie Dimon, had emerged from the financial crisis as the undisputed winner among American banks, gaining market share in virtually every business line. Bank of America, which had gone through its own crisis and restructuring, executed its recovery more quickly and more cleanly. Goldman Sachs and Morgan Stanley thrived as pure-play investment banks before expanding selectively into wealth management. Citigroup, stuck in the middle, was too diversified to compete with the specialists and too poorly integrated to compete with JPMorgan's scale and execution.

Throughout the Corbat years, Citigroup was also plagued by a series of scandals that kept regulators on high alert. The bank paid substantial fines related to foreign exchange rate manipulation, where traders in its London dealing room had colluded with competitors to rig benchmark currency rates. It faced penalties related to anti-money-laundering failures in its Mexican operations, where the Banamex unit had been used to launder drug proceeds. And it repeatedly failed Federal Reserve stress tests, which are the annual health checks designed to determine whether large banks have enough capital to survive a severe recession. Failing a stress test was not just embarrassing; it meant the bank could not return capital to shareholders through dividends or buybacks, creating a vicious cycle of depressed stock price and frustrated investors.

For investors, the decade delivered a stark verdict. While JPMorgan's stock roughly quadrupled from its crisis lows, Citigroup barely managed to double. The bank's return on equity consistently lagged its cost of capital, meaning that for most of the 2010s, Citigroup was actually destroying shareholder value on an economic basis. The market reflected this by pricing the stock at a persistent discount to tangible book value, a signal that investors believed the company was worth more dead, broken into pieces, than alive as a going concern.

IX. Modern Citigroup: Jane Fraser's New Vision (2021–Present)

On March 1, 2021, Jane Fraser became Citigroup's Chief Executive Officer and the first woman to lead a major U.S. bank. Born in St Andrews, Scotland, Fraser studied economics at Cambridge and earned her MBA at Harvard Business School. She spent a decade at McKinsey, where she specialized in financial services, before joining Citigroup in 2004. Over the next seventeen years, she ran the Latin American division, led the strategy and mergers function, served as CEO of Citigroup's global consumer banking business, and, critically, oversaw the bank's mortgage business in the years after the financial crisis. She knew where the bodies were buried, quite literally, having managed the wind-down of some of the crisis-era portfolios. She also understood, from her McKinsey training, that Citigroup's problems were not primarily about talent or strategy but about organizational structure and operational execution.

Fraser's strategy was radical by Citigroup's standards: stop trying to be everything to everyone. In April 2021, she announced Citigroup would exit retail banking in thirteen markets across Asia and Europe, a stunning reversal for a bank that had defined itself by its global consumer footprint for over a century. The exits included major markets like South Korea, Australia, India (consumer), and China (consumer). The message was clear: Citigroup could no longer afford to maintain a subscale consumer banking presence in dozens of countries while its core institutional business was underinvested.

In late 2023 and early 2024, Fraser launched "Project Bora Bora," the most sweeping organizational restructuring in the company's modern history. The old two-division structure was demolished and replaced with five core business units: Services, Markets, Banking, U.S. Personal Banking, and Wealth, each reporting directly to the CEO. Five layers of management were eliminated. Bureaucracy was compressed. The goal was to create clear accountability where none had existed before.

The human cost was significant. Citigroup targeted approximately twenty thousand job cuts by the end of 2026, roughly eight to ten percent of the workforce. When the Banamex divestiture is included, total headcount is expected to fall from roughly 240,000 to around 180,000. In January 2026, a thousand positions were eliminated in a single week, with additional layoffs of managing directors and senior employees planned for March. The cost savings target is up to 2.5 billion dollars annually.

Inside the bank, the restructuring was often painful and chaotic. Employees described being uncertain of their roles for months at a time. Some found themselves reporting to new managers in entirely different business units. Others were asked to reapply for their own jobs. But Fraser was unapologetic about the disruption, arguing that the old organizational structure was the single biggest obstacle to Citigroup's performance.

Fraser also brought in outside talent to rebuild key businesses. Andy Sieg, former president of Merrill Lynch Wealth Management, joined as Head of Wealth in September 2023. Viswas Raghavan, previously JPMorgan's head of global investment banking, was hired as Head of Banking in early 2024. Both hires signaled Fraser's intent to compete at the highest level in businesses where Citigroup had historically underperformed.

The results have been mixed but increasingly encouraging. Full-year 2025 revenue reached 85.2 billion dollars, the highest since 2010. Adjusted net income was 16.1 billion, up twenty-seven percent year-over-year. All five business segments achieved record revenues and positive operating leverage for the first time.

Investment banking fees surged, with M&A advisory climbing eighty-four percent in the fourth quarter, lifting Citigroup to fourth place in global M&A advisory rankings. The hiring of Raghavan from JPMorgan was clearly paying dividends, as the banking unit began winning mandates it would not have competed for under the old structure. The wealth management business, under Sieg, grew revenues twenty percent year-over-year with investment assets reaching 587 billion dollars. For the first time in years, Citigroup was gaining market share rather than losing it in businesses that matter.

The Treasury and Trade Solutions business, Citigroup's crown jewel, continued to gain market share, with cross-border transaction values rising five percent and USD clearing volume up eight percent. This is the business that gives Citigroup its unique competitive moat: the ability to move money across borders for the world's largest corporations and financial institutions. To understand why this matters, think of TTS as the plumbing of global commerce. When a multinational corporation needs to pay suppliers in thirty countries, collect revenue in twenty currencies, and manage its cash positions across time zones, there are very few banks with the infrastructure to handle that at scale. No other bank matches Citigroup's geographic reach in transaction banking, and this is the franchise Fraser is building around.

The technology investment is enormous but necessary. Citigroup allocated 11.8 billion dollars to technology in 2024, plus an additional 2.9 billion for transformation initiatives. Fraser and her CFO have been unusually direct about the role of artificial intelligence in the company's future, stating publicly that AI will drive continued headcount reductions as the bank automates routine processes and improves productivity. This is not just cost-cutting rhetoric; it reflects a genuine strategic bet that technology can solve the operational challenges that have plagued Citigroup for decades.

On the regulatory front, there has been measured progress. In July 2024, the OCC fined Citigroup 136 million dollars for failing to make sufficient progress on the 2020 consent order's requirements. But by December 2025, the OCC removed that amendment, signaling that Citigroup had made adequate progress. The original 2020 consent orders from both the OCC and the Federal Reserve remain in place, however, and full resolution is likely years away.

The Banamex divestiture, the exit from Citigroup's enormous Mexican consumer banking operation, has been complex but is progressing. In September 2025, Citigroup sold a twenty-five percent stake to Fernando Chico Pardo for approximately 2.3 billion dollars. In early 2026, an additional twenty-four percent stake was sold to a consortium including General Atlantic, Blackstone, Qatar Investment Authority, and others for roughly 2.5 billion dollars. An IPO on the Mexican Stock Exchange is expected sometime in 2026. The Russia exit was completed in February 2026 with the sale of AO Citibank to Renaissance Capital, freeing up approximately four billion dollars in capital.

In a widely reported internal memo dated January 14, 2026, Fraser wrote: "We are not graded on effort. We are judged on our results. And I expect to see the last vestiges of old, bad habits fall away, and a more disciplined, more confident, winning Citi fully emerge in 2026." It was both a rallying cry and a warning. The transformation is underway, but it is not complete, and Fraser knows that the market will not give Citigroup credit until the results are sustained over multiple years.

As of early 2026, the stock trades around one hundred and sixteen dollars per share, with a market capitalization of roughly 198 billion dollars. The stock rallied forty-seven percent in 2025, reflecting growing confidence in the transformation. But the price-to-book ratio remains below one, meaning the market still values Citigroup at less than the liquidation value of its assets. Closing that valuation gap is the central investment thesis for the stock, and it depends entirely on whether Fraser can deliver on the promised return on tangible common equity target of ten to eleven percent in 2026 and beyond.

X. Playbook: Business and Investing Lessons

The Citigroup story is a masterclass in what happens when ambition outpaces the ability to execute. Every business school case about conglomerate failure, regulatory arbitrage, and risk management breakdown can be found in this single institution's history. Here are the lessons that matter most.

The conglomerate discount is real, and in financial services, it is devastating. Sandy Weill's vision of a financial supermarket assumed that combining commercial banking, investment banking, insurance, and consumer finance under one roof would create cross-selling synergies and economies of scale.

In theory, a Citibank customer could have a checking account, a mortgage, an investment portfolio, and a life insurance policy, all serviced by the same institution. The pitch was compelling: one relationship, one statement, one institution that understood every aspect of your financial life. In practice, the cultures were incompatible, the technology systems did not talk to each other, and the regulatory requirements of each business created enormous compliance overhead.

The "synergies" that justified the merger never materialized in any meaningful way. Consumers did not want to buy insurance from their bank. Investment bankers did not want to share client relationships with retail brokers. The cross-selling dream was precisely that: a dream. The market's response was to apply a permanent discount to Citigroup's stock price, essentially telling management that the company was worth less together than it would be as separate pieces.

Regulatory arbitrage, the practice of structuring transactions to exploit gaps between what the law permits and what regulators enforce, is a strategy with an expiration date. Citigroup was built on a bet that Glass-Steagall would be repealed, and the bet paid off. But the repeal created an institution that was too complex for any management team to oversee and too interconnected for any regulatory framework to monitor. When the crisis came, the very complexity that had been Citigroup's competitive advantage became its near-fatal vulnerability. The lesson is that regulatory arbitrage creates fragile institutions. They perform well in good times and catastrophically in bad ones.

The too-big-to-fail problem creates moral hazard that is almost impossible to eliminate. Citigroup was bailed out not because the government wanted to reward failure but because the consequences of letting it fail were judged to be worse than the consequences of saving it.

But the bailout sent a signal to every large financial institution: take risks aggressively, because if you are big enough, the government will catch you when you fall. This is the classic heads-I-win, tails-taxpayers-lose dynamic that pervades systemically important financial institutions. The Dodd-Frank Act of 2010, the consent orders, stress tests, and living will requirements that followed the crisis were all attempts to address this problem, but Citigroup's ongoing struggles with compliance suggest that the problem has not been fully solved. The institution that was once too big to fail proved that it was also too big to fix quickly.

Cultural integration in mega-mergers is not a human resources problem. It is a strategic problem. The clash between Citicorp's relationship bankers and Travelers' deal-oriented traders was never resolved because it was never truly addressed. Management treated culture as a soft issue that would work itself out over time. It did not. The cultural fault lines that emerged during the co-CEO period persisted for decades, manifesting in inconsistent risk management, decentralized decision-making, and an inability to enforce common standards across the organization.

Perhaps the most important lesson is about management succession. Weill chose Prince, his personal lawyer, as CEO, not because Prince was the best banker available but because Prince was loyal and controllable. Prince chose inaction when action was required, continuing to build subprime exposure even as he acknowledged the risks. The board chose Pandit, an outsider who arrived via an eight-hundred-million-dollar hedge fund acquisition, as crisis CEO.

Each succession decision was made for reasons that had little to do with what the institution actually needed. Weill wanted a successor who would not challenge his legacy. The board wanted a crisis manager with fresh eyes. In neither case was the question "who is the best person to run this institution for the next decade?" The result was a leadership vacuum during the most critical periods in the company's history. It was not until Fraser's appointment that the board finally chose a leader with deep institutional knowledge, a clear strategic vision, and the mandate to make fundamental changes.

The risk management lesson is particularly important. Citigroup's risk management was not just underfunded; it was structurally subordinated to the revenue-generating businesses. Risk officers who raised concerns were marginalized or overruled. The compensation structure rewarded short-term revenue generation and penalized caution. When risk management is treated as a cost center rather than a critical business function, the result is predictable: risks accumulate until they become catastrophic. JPMorgan, by contrast, invested heavily in risk management under Jamie Dimon and emerged from the crisis in a position of strength. The difference was not luck; it was organizational design.

For founders and executives in any industry, the lesson is sobering: ambition without operational capability is a recipe for catastrophe. Building an empire is exciting. Running one is hard. And no amount of dealmaking brilliance can substitute for the unglamorous work of integrating systems, managing risk, and building a culture that can sustain itself across business cycles.

XI. Analysis: Bear vs. Bull Case

The Bear Case

The pessimistic thesis on Citigroup starts with a simple but damning observation: this is a serial underperformer. Consider the long-term numbers. An investor who bought Citigroup stock in January 2000, at the height of the financial supermarket excitement, and held through February 2026 would still be deeply underwater on an inflation-adjusted basis, even after the 2025 rally. Over that same period, JPMorgan delivered returns that made it one of the best-performing large-cap stocks in America. The reasons for Citigroup's underperformance are structural, not cyclical.

The regulatory overhang is real and shows no signs of lifting. The original 2020 consent orders from both the OCC and the Federal Reserve remain in force. Full remediation of the data governance, risk management, and internal control deficiencies that triggered these orders is a multi-year, multi-billion-dollar project with no guaranteed timeline. Each new regulatory setback, and there have been several, reinforces the narrative that Citigroup cannot operate at the level of competence required of a systemically important institution.

Operational complexity remains the company's fundamental problem. Despite a decade of simplification under Corbat and now Fraser, Citigroup still operates one of the most complex technology and operational infrastructures in global banking. The 894-million-dollar Revlon wire error was not an isolated incident. It was a symptom of systemic issues that persist across the organization. Until Citigroup's technology infrastructure is modernized and its risk management processes are standardized, the bank remains vulnerable to operational failures that erode both capital and credibility.

Return on equity has consistently been below the cost of capital, meaning that on an economic basis, Citigroup has been destroying shareholder value for most of the past fifteen years. The 2026 target of ten to eleven percent return on tangible common equity is an improvement but may still fall short of what is needed to trade at a meaningful premium to tangible book value. For context, JPMorgan consistently delivers returns on tangible equity north of twenty percent.

Geopolitical exposure adds another layer of risk. Citigroup's extensive presence in emerging markets and its role as the world's preeminent cross-border banking institution mean that it is uniquely exposed to sanctions risk, currency volatility, political instability, and the operational complexity of navigating dozens of regulatory regimes simultaneously. The Russia exit, which cost approximately 1.2 billion dollars pretax, illustrated how quickly geopolitical risk can crystallize into real losses. In a world of increasing geopolitical fragmentation, the very global reach that makes Citigroup unique also makes it uniquely vulnerable.

The Bull Case

The optimistic thesis begins with valuation. As of early 2026, Citigroup trades at roughly 1.25 times tangible book value and below one times book value. This is a dramatic discount to peers: JPMorgan trades at over 2.5 times tangible book, and Bank of America at over 1.6 times. The discount implies that the market expects Citigroup to continue underearning its cost of capital indefinitely. If Fraser's transformation succeeds in closing even a portion of that gap, the stock repricing potential is enormous.

The transformation is showing real results. Full-year 2025 revenue was the highest since 2010. All five business segments delivered positive operating leverage. Investment banking fees surged. The wealth management business is growing rapidly under Andy Sieg. And the removal of the OCC's 2024 consent order amendment signals genuine regulatory progress. The trajectory is clearly improving.

Citigroup's transaction banking franchise, Treasury and Trade Solutions, is genuinely unique. No other bank matches Citigroup's ability to move money across borders in over 160 countries. This franchise benefits from powerful network effects: the more countries Citigroup operates in, the more valuable its network becomes to multinational corporate clients. It is a business with high barriers to entry and sticky client relationships, precisely the kind of franchise that Hamilton Helmer would classify as a network economy power.

Competitive Positioning and Strategic Analysis

Through the lens of Porter's Five Forces, Citigroup occupies an interesting position. The threat of new entrants in global transaction banking is low because of the massive regulatory, capital, and infrastructure requirements. Fintech companies have disrupted domestic payments but have struggled to replicate the cross-border capabilities that require physical presence in dozens of regulatory jurisdictions. Building what Citigroup has in transaction banking from scratch would take decades and billions in investment, a barrier that protects the existing franchise. Supplier power is moderate, as the bank depends on technology vendors and human capital that are increasingly scarce and expensive. Buyer power is moderate to high, as large corporate clients can and do spread their business across multiple banks, though switching costs in transaction banking are high because of the integration work required. Rivalry among existing competitors is intense, particularly with JPMorgan aggressively investing to compete in every market where Citigroup operates. HSBC and Standard Chartered compete directly in cross-border banking in Asia and the Middle East, though neither matches Citigroup's breadth across the Americas. The substitution threat from blockchain-based cross-border payment systems and digital currencies remains theoretical but bears watching over the longer term.

The capital return story is compelling if the transformation succeeds. Citigroup generated thirteen billion dollars in share buybacks in 2025 alone, out of a twenty-billion-dollar authorization. With the capital released from the Russia exit and the upcoming Banamex IPO, the bank will have significant additional capacity for buybacks and dividends. For a stock trading near book value, aggressive capital return at these levels is highly accretive to remaining shareholders.

The emerging markets growth potential should not be overlooked. While Citigroup is exiting subscale consumer operations in many countries, it is doubling down on institutional banking in the fastest-growing economies in the world. As global trade flows shift toward Asia, Africa, and Latin America, Citigroup's existing infrastructure in these regions becomes increasingly valuable.

Using Hamilton Helmer's Seven Powers framework, Citigroup's primary source of competitive advantage is its network economy in transaction banking. The value of the Citigroup network to any single client increases as the network expands to more countries and serves more counterparties. This is a genuine and durable competitive moat. The bank also benefits from scale economies in technology and operations, though these have historically been offset by the costs of complexity. Citigroup has weak or no power in several of the other Helmer categories, notably brand power (damaged by the crisis and ongoing scandals), counter-positioning (it is not offering a fundamentally different model from peers), and process power (its operational infrastructure is a weakness, not a strength).

Key Performance Indicators

For investors tracking Citigroup's ongoing performance, two metrics matter most. First, return on tangible common equity, which measures the bank's ability to generate profits relative to the equity capital deployed. This is the single most important number for any bank, and it is the metric that will determine whether Citigroup can close its valuation discount to peers. Fraser's near-term target is ten to eleven percent, but the long-term aspiration needs to be in the low-to-mid teens to justify a price-to-tangible-book above 1.5 times. Second, the efficiency ratio, which measures operating expenses as a percentage of revenue. Citigroup's 2026 target of approximately sixty percent is an improvement from historical levels, but JPMorgan consistently operates in the mid-fifties. Sustained improvement in this ratio will signal that the restructuring is generating real operating leverage rather than just one-time cost savings.

XII. Epilogue: What Might Have Been

What if Glass-Steagall had never been repealed? The question is more than academic. Without the Gramm-Leach-Bliley Act, the Citicorp-Travelers merger would have been unwound within two years. Citicorp would have continued as a global commercial bank. Travelers would have remained a diversified insurance and brokerage company. There would have been no Citigroup, no financial supermarket, and no institution large enough and complex enough to require 476 billion dollars in government support to survive.

Would the financial crisis still have happened? Almost certainly, yes. The underlying causes, excessive leverage, underpriced risk, and inadequate regulation, were not unique to Citigroup. Lehman Brothers, Bear Stearns, and AIG all collapsed or nearly collapsed without having merged with commercial banks. But the crisis might have been less severe, and the government response might have been less costly, if the largest institutions had been smaller and less interconnected.

The creation of Citigroup was both a symptom of the deregulatory zeitgeist of the 1990s and an accelerant of the risks that ultimately produced the crisis. The institution became a case study in why the original authors of Glass-Steagall had separated commercial and investment banking in the first place: because the combination creates institutions that are simultaneously too important to let fail and too complex to manage safely.

What if Reed had won the power struggle? Reed's vision for Citigroup was technology-driven and consumer-focused. He wanted to build a digital bank before anyone was using that phrase. It is impossible to know whether his vision would have worked, but it is worth noting that the businesses Reed championed, consumer banking, credit cards, and global payments, are precisely the businesses that have proven most durable and valuable.

The businesses Weill championed, investment banking, trading, and insurance, are the ones that produced the scandals, the losses, and the regulatory headaches. Ironically, Citigroup eventually divested insurance (selling Travelers to MetLife and spinning off Primerica) and sold its brokerage (Smith Barney to Morgan Stanley), essentially undoing the very acquisitions that Weill had fought so hard to assemble. Reed's departure did not just change who ran Citigroup. It changed what Citigroup became, and what it eventually had to undo.

What if Citigroup had been allowed to fail in 2008? The government's decision to bail out Citigroup was based on the judgment that its failure would have cascading consequences across the global financial system. Given Citigroup's role in cross-border payments, its presence in over one hundred countries, and its interconnections with thousands of financial counterparties, that judgment was almost certainly correct. A Citigroup bankruptcy would have been Lehman Brothers on a global scale, with consequences that are difficult to fully imagine.

The ongoing debate about whether Citigroup should be broken up persists. Prominent voices, including former Citigroup CEO John Reed himself, have argued that institutions of this size and complexity are inherently unmanageable. In a 2013 interview, Reed said plainly: "I'm sorry. I don't think it's possible to regulate such a large institution effectively." The bank's persistent discount to tangible book value is the market's way of saying that the institution in its current form is not worth what its parts would be worth separately. Fraser's strategy is, in effect, an attempt to prove the market wrong by simplifying the organization, improving returns, and demonstrating that a focused global institutional bank can deliver value that exceeds the sum of its parts.

Whether she succeeds remains the central question of the Citigroup story. The bank has been trying to transform itself for a quarter century, through four CEOs and two existential crises. Each time, the ambition has been there. The question has always been about execution.

Citigroup's story is, in the end, a story about the tension between ambition and capability, between what an institution wants to be and what it can actually become. It is a story about the seductive power of complexity and the brutal cost of getting it wrong. It is a story about an institution that has been too big to fail and, paradoxically, too big to succeed. The challenge for Jane Fraser and her team is to prove that these two conditions are not permanent, that an institution with Citigroup's history and global reach can be disciplined enough to deliver returns that justify its existence without taking the kinds of risks that have brought it to the brink of destruction twice in the last thirty-five years.

The next few years will determine whether Citigroup's story ends as a cautionary tale about the limits of financial ambition or as a comeback story for the ages. Either way, it remains one of the most consequential stories in the history of American capitalism.

XIII. Recent News

Citigroup's most recent earnings, reported on January 14, 2026, showed strong momentum. Fourth-quarter adjusted revenue reached 21 billion dollars, beating consensus by roughly three hundred million, while adjusted earnings per share of $1.81 exceeded estimates by fourteen cents. Investment banking was the standout, with M&A advisory fees surging eighty-four percent year-over-year and the banking unit's total revenue climbing seventy-eight percent to 2.2 billion dollars.

The Russia exit reached a significant milestone. Putin approved the sale of AO Citibank to Renaissance Capital in November 2025, and the transaction was completed in February 2026. While the exit resulted in approximately 1.2 billion dollars in pretax losses recorded in the fourth quarter of 2025, it freed up four billion dollars in risk-weighted capital, strengthening Citigroup's capital position for buybacks and investment.

The Banamex divestiture continues to progress toward an anticipated IPO on the Mexican Stock Exchange in 2026. After selling a twenty-five percent stake in September 2025 and an additional twenty-four percent stake in early 2026 to a consortium of global investors including General Atlantic, Blackstone, and the Qatar Investment Authority, Citigroup is approaching the final phase of what has been one of the most complex divestitures in banking history. Banamex, which Citigroup originally acquired in 2001 for approximately twelve billion dollars, represents both the crown jewel of Mexico's banking sector and a persistent source of operational complexity for Citigroup. The IPO will mark the end of a twenty-five-year chapter in Citigroup's relationship with Mexico.

On the leadership front, CFO Mark Mason announced plans to step down in March 2026, transitioning to the role of Executive Vice Chair and Senior Executive Advisor to the CEO. Gonzalo Luchetti, who previously led the U.S. Personal Banking division, will succeed him as CFO. The transition comes at a critical moment, as Citigroup enters 2026 with guidance calling for NII growth of five to six percent, an efficiency ratio target of approximately sixty percent, and a return on tangible common equity target of ten to eleven percent.

The fourth quarter of 2025 also saw Citigroup book approximately three billion dollars in restructuring charges and other one-time items, including losses related to the Russia exit, Argentina currency devaluation impacts, and severance costs from ongoing layoffs. While these charges depressed reported earnings, the market largely looked through them, focusing instead on the trajectory of the underlying businesses.

The regulatory picture improved modestly in December 2025 when the OCC removed its July 2024 amendment to the consent order, acknowledging Citigroup's progress on risk management and data governance remediation. However, the original 2020 consent orders from both the OCC and the Federal Reserve remain in place.

Citigroup's stock rose approximately forty-seven percent in 2025, its strongest annual performance in years, reflecting growing investor confidence in Fraser's transformation. The bank authorized a twenty-billion-dollar share repurchase program and raised its quarterly dividend to sixty cents per share in the third quarter of 2025. As of late February 2026, the stock trades around one hundred and sixteen dollars per share, with a market capitalization of roughly 198 billion dollars.

XIV. Links and References

Books: - Tearing Down the Walls: How Sandy Weill Fought His Way to the Top of the Financial World and Then Nearly Lost It All by Monica Langley (2003) - The House of Citigroup by Harold van B. Cleveland and Thomas F. Huertas (1985) - Too Big to Fail by Andrew Ross Sorkin (2009) - Thirteen Bankers: The Wall Street Takeover and the Next Financial Meltdown by Simon Johnson and James Kwak (2010)

Key Regulatory and Government Sources: - Congressional Oversight Panel: "Extraordinary Financial Assistance Provided to Citigroup, Inc." (2011) - TARP Investment Tracker: ProPublica Bailout Database - Federal Reserve History: "Latin American Debt Crisis of the 1980s" and "Financial Services Modernization Act of 1999" - SEC Enforcement Actions re: Enron and WorldCom settlements

Long-Form Journalism: - "Citi's Relentless Quest for Growth" -- The Washington Post (November 2008) - "John Reed's Bold Stroke" -- Fortune (June 1987) - "Birth of ATMs: John Reed Describes a Banking Transformation" -- MIT Alumni Association - "The Titanic of Wall Street: The Citigroup Merger 20 Years Later" -- Marketplace (April 2018)